Embed Size (px)

Citation preview

OCCAS IONAL PAPER SER IESNO. 42 / DECEMBER 2005

THE NEW BASEL CAPITAL FRAMEWORK AND ITS IMPLEMENTATION IN THE EUROPEAN UNION

by Frank Dierick,Fatima Pires,Martin Scheicherand Kai Gereon Spitzer

In 2005 all ECB publications will feature

a motif taken from the

€50 banknote.

OCCAS IONAL PAPER S ER I E SNO. 42 / DECEMBER 2005

This paper can be downloaded without charge from the ECB’s website (http://www.ecb.int) or from the Social Science Research Network

electronic library at http://ssrn.com/abstract_id=807416.

THE NEW BASEL CAPITAL FRAMEWORK AND ITS IMPLEMENTATION IN

THE EUROPEAN UNION *

by Frank Dierick 1,Fatima Pires 1,

Martin Scheicher 2

and Kai Gereon Spitzer 3

* The authors are grateful for research assistance by Sara Testi and comments by Mauro Grande, Panagiotis Strouzas and ananonymous referee. The views expressed in this paper are those of the authors and do not necessarily reflect those of the

ECB, the Eurosystem or the Deutsche Bundesbank.1 Directorate Financial Stability and Supervision of the ECB

2 Directorate General Research of the ECB3 Banking and Financial Supervision Department of the Deutsche Bundesbank

© European Central Bank, 2005

AddressKaiserstrasse 2960311 Frankfurt am MainGermany

Postal addressPostfach 16 03 1960066 Frankfurt am MainGermany

Telephone+49 69 1344 0

Websitehttp://www.ecb.int

Fax+49 69 1344 6000

Telex411 144 ecb d

All rights reserved. Any reproduction,publication and reprint in the form of adifferent publication, whether printedor produced electronically, in whole orin part, is permitted only with theexplicit written authorisation of theECB or the author(s).

The views expressed in this paper donot necessarily reflect those of theEuropean Central Bank.

ISSN 1607-1484 (print)ISSN 1725-6534 (online)

3ECB

Occasional Paper No. 40December 2005

C O N T E N T SABBREVIATIONS 4

ABSTRACT 5

EXECUTIVE SUMMARY 6

INTRODUCTION 7

PART 1 – OVERVIEW OF THE NEW FRAMEWORK 8

1 DEVELOPMENT 8

2 STRUCTURE 9

2.1 General overview 9

2.2 Pillar I – Minimum capitalrequirements 11

2.3 Pillar II – Supervisory reviewprocess 18

2.4 Pillar III – Market discipline 19

3 THE NEW FRAMEWORK IN THE EU 20

3.1 Legal and institutional setting 20

3.2 Specific features of EUimplementation 23

PART II – ISSUES OF SPECIFIC RELEVANCEIN THE EU CONTEXT 29

4 PROCYCLICALITY 29

4.1 Definition 29

4.2 Empirical evidence 29

4.3 Mitigating measures 31

4.4 Monitoring in the EU 31

5 HOME-HOST ISSUES AND THECONSOLIDATING SUPERVISOR 32

5.1 International and Europeancontext 32

5.2 Powers and responsibilitiesof the consolidating supervisor 33

5.3 Assessment of the consolidatingsupervisor 36

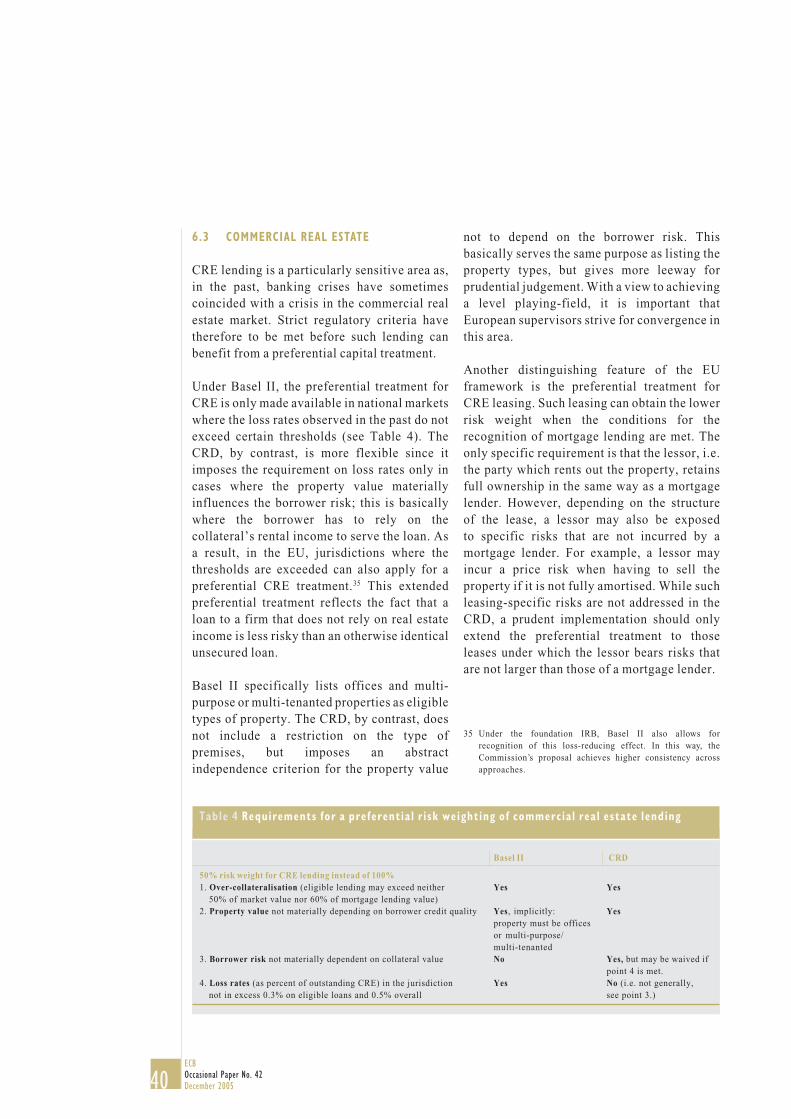

6 REAL ESTATE LENDING 37

6.1 Overview 37

6.2 Residential real estate 38

6.3 Commercial real estate 40

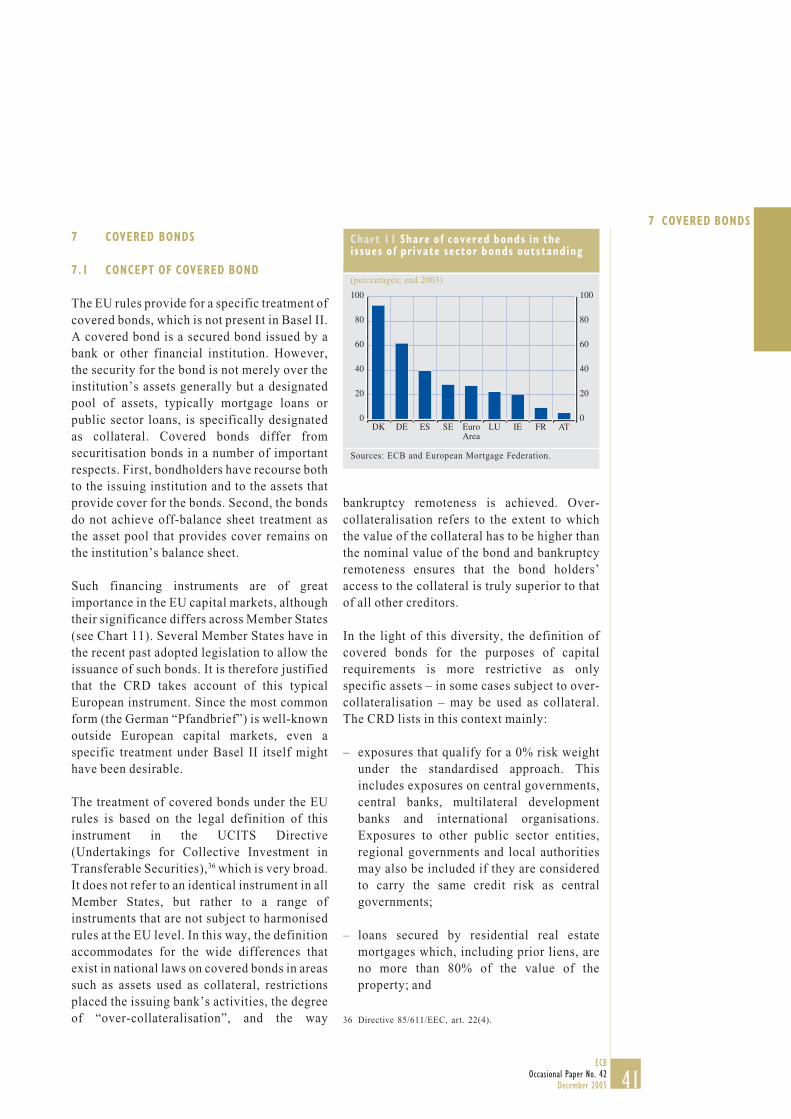

7 COVERED BONDS 41

7.1 Concept of covered bond 41

7.2 Capital treatment 42

CONCLUDING REMARKS 43

GLOSSARY 45

REFERENCES 48

LIST OF OCCASIONAL PAPERS 52

4ECBOccasional Paper No. 42December 2005

ABBREVIATIONS

AIG Accord Implementation GroupAMA advanced measurement approachesASRF asymptotic single risk factorBCBS Basel Committee on Banking SupervisionCAD Capital Adequacy Directive (93/6/EEC)CBD Codified Banking Directive (2000/12/EC)CEBS Committee of European Banking SupervisorsCP consultative paperCRD Capital Requirements DirectiveCRE commercial real estateEAD exposure at defaultECAI external credit assessment institutionECB European Central BankEFR European Financial Services Round TableEU European UnionFSAP Financial Services Action PlanIRB internal ratings-basedLGD loss given defaultM effective maturityMiFID Markets in Financial Instruments Directive (2004/39/EC)PD probability of defaultQIS quantitative impact studyRRE residential real estateSMEs small and medium-sized enterprisesS&P Standard & Poor’sUCITS Undertakings for Collective Investment in Transferable Securities

5ECB

Occasional Paper No. 42December 2005

ABSTRACT

ABSTRACT

Following the adoption by the BaselCommittee of new capital rules for banks, aprocess is now taking place in the EU totranspose the rules into Community law and,ultimately, into national legislation. This papergives an overview of the main issues that relateto the EU implementation, mainly from theperspectives of financial stability and financialintegration. Although the EU rules are to alarge extent based on the texts of the BaselCommittee, modifications have beenintroduced to account for the specific legal andinstitutional setting, as well as for somefeatures of the European financial system.The paper gives an overview of thesemodifications and deals in greater detail with anumber of selected topics: the monitoring ofprocyclicality, the role of the consolidatingsupervisor and the treatment of real estatelending and covered bonds. The paperconcludes with an outlook for the future.

Key words: banks, Basel II, capitalrequirements, financial regulation, financialstability, financial supervision, risk management.

JEL classification: G21, G28

6ECBOccasional Paper No. 42December 2005

EXECUTIVE SUMMARY

In June 2004, the Basel Committee on BankingSupervision published its new capital rules forbanks (“Basel II”). Recently, the EuropeanParliament and the Council approvedlegislation transposing these rules intoCommunity law and this legislation will,in turn, be transposed into national law.The European Central Bank (ECB) has aninterest in these developments because of theirpossible implications for financial supervision,financial stability and financial integration. Aswell as providing a non-technical overview ofthe main elements of the new framework, thispaper focuses on issues related to the EuropeanUnion (EU) implementation. The paper isstructured in two parts. Part I gives an overviewof Basel II and the main issues that are relevantfor its implementation in the EU. Against thisgeneral setting, Part II deals in greater detailwith a number of selected topics that areparticularly important for the EU: themonitoring of procyclicality, the role of theconsolidating supervisor and the treatment ofreal estate lending and covered bonds.

Basel II is based on three mutually reinforcingpillars: minimum capital requirements (PillarI), the supervisory review process (Pillar II)and market discipline (Pillar III). A maininnovation is that a set of increasinglysophisticated approaches is now available tobanks to calculate their minimum capitalrequirements. Although the simplest method tocalculate capital for credit risk is based onassessments by rating agencies, under the mostadvanced approaches, banks are allowed to usetheir own estimated risk parameters. Moreover,for the first time, banks are required to holdcapital for operational risk.

While the EU rules are to a very large extentsimilar to those developed by the BaselCommittee, they are not an exact copy. First,the legal and institutional setting is different.The EU rules are legislative in nature andbinding in all Member States. Moreover, therecently established Committee of European

Banking Supervisors (CEBS) will play a majorrole in developing supervisory guidance toimplement the new rules. Second, the specificstructure of the European financial system,such as the role of the Single Market, justifiescertain deviations.

The EU rules diverge from Basel II in theirscope of application and the range ofapproaches that will be available to institutionsto calculate their capital requirements. Theyalso change the supervisory responsibilitiesby giving a larger role to the consolidatingsupervisor and by requiring supervisorydisclosure. In the Single Market there isa greater need for cooperation betweensupervisors. Some specific features of the EUeconomy and financial system need to beaddressed as well. This includes venturecapital, real estate lending and covered bonds.In addition, the EU rules provide for specificarrangements concerning the issue ofprocyclicality. Empirical evidence indicatesthat capital rules can indeed exacerbate theeconomic cycle. However, in the developmentof the new rules various changes were madeto accommodate these concerns. A studyperformed under the auspices of the EuropeanCommission confirmed that procyclicalityshould no longer be a major problem, althoughit should be kept under review. To that end, theEU rules provide for a monitoring arrangementthat also involves the ECB.

In more detail, the EU rules provide for anenhanced role of the consolidating supervisor,in particular, through the process of approval ofadvanced methods to calculate capitalrequirements on a group-wide basis. Althoughthis extended role does not go as far as somelarge financial groups would like, it willsimplify the interaction between the bankinggroup and its supervisors as well as between thevarious supervisors. It is also likely to bebeneficial for financial stability andintegration, although it raises compleximplementation issues that will need to befollowed up closely.

7ECB

Occasional Paper No. 42December 2005

INTRODUCTION

Real estate lending is another important areagiven its significance in bank lending and thatbanking crises have often coincided with crisesin the real estate market. In the treatment of realestate lending, the EU rules seem to achievegreater consistency than Basel II, although thisleads to a somewhat less conservativetreatment of commercial real estate lending.From a financial stability perspective,however, it is important that this more lenienttreatment does not apply to the more risky realestate, the income of which is used for debtservicing. Some of the rules offer further scopefor supervisory convergence, which would bebeneficial for the integration of real estatelending in Europe.

Covered bonds receive a specific treatmentunder the EU rules that is not present in BaselII. These financing instruments, with the“Pfandbrief” as its best-known exponent, areimportant for EU capital markets. Thispreferential treatment, reflecting the additionalsecurity inherent in these bonds, is fullyconsistent with the principles underlying BaselII. It also seems that most of the existingcovered bonds in the EU would qualify for thispreferential treatment.

This paper concludes by listing some keychallenges for the capital rules, first, as regardstheir EU implementation and, second, in along run perspective. In the longer term, thedefinition of regulatory capital and itsinteraction with the new accounting rules willhave to be addressed. Other areas which maywarrant further study relate to the blurring ofthe border between credit risk and market risk,and the possible use of full credit portfoliomodels by banks to calculate their capitalrequirements.

INTRODUCTION

In June 2004, the Basel Committee on BankingSupervision (BCBS) published its newsolvency rules for banks1, the New CapitalFramework (“Basel II”).2 A parallel process

has taken place in the EU to transpose theinternationally agreed capital standards intoCommunity law. Member States will also haveto transpose the EU rules into nationallegislation in due course.

The ECB has an interest in these new rulesbecause of its responsibilities in the areas offinancial supervision and financial stability.3

The New Framework may also affect theEurosystem credit operations through its rulesfor ratings assigned to financial assets used ascollateral for such operations.4 In addition, theproposed EU rules provide for arrangements tomonitor the macro-economic impact of theNew Framework, which includes a specific rolefor the ECB. Finally, the implementation of thenew solvency rules may have implications forfinancial integration, a Community objectivethat is supported by the ECB. The ECB wasactively involved in the discussions on the newrules through its participation in the BCBS andEuropean fora, and via its policy advice.5

This paper aims to give an overview of the mainissues related to the implementation of the NewFramework in the EU, especially from theperspectives of financial stability and financialintegration. Although the proposed EU rulesare to a large extent similar to the onesdeveloped by the Basel Committee, they are notan exact copy of them. First, the legal andinstitutional setting is different. The EUframework is legislative in nature and thereforebinding in all Member States. Moreover,account has to be taken of the new regulatoryand supervisory set-up in the EU as a result ofthe extension of the “Lamfalussy framework”to the banking sector. Second, the specificfeatures of the European financial system, suchas the role of the Single Market, justify somedeviations.

1 In this paper, the term “bank” is used as a synonym for“credit institution”.

2 Basel Committee on Banking Supervision (2004a).3 Art. 105(5) of the Treaty establishing the European

Community.4 See in this respect ECB (2005a).5 See in particular ECB (2005b).

8ECBOccasional Paper No. 42December 2005

This paper is structured in two main parts. Thefirst one deals with the Basel Framework andits implementation in the EU and the second oneaddresses certain topics that are particularlyimportant in the EU context. In Part I, Section 1briefly recalls the main steps that were taken infinalising the Basel II Framework and Section2 provides an overview of its main elements. InSection 3, the EU implementation of Basel II isdiscussed in general terms. It starts by recallingthe specific legal and institutional setting in theEU and then turns to the main differencesbetween the Basel and the EU rules.

Part II builds on this general analysis andsingles out a number of areas, which are ofparticular relevance for the EU, andinvestigates them in greater detail. Section 4tackles the issue of procyclicality, i.e. theconcern that the new capital rules mayexacerbate economic cycles. It reviews theempirical evidence, the different measures tomitigate such effects and the specificmonitoring arrangement provided for under theEU rules. Implementation issues in a cross-border context are analysed in Section 5. Here,the EU rules diverge from Basel by enhancingthe role of the authority responsible forsupervision on a consolidated basis. Section 6compares the EU and Basel rules in theirtreatment of real estate collateral, both forresidential and commercial real estate lending.The treatment of covered bonds, a financinginstrument that is particularly popular in theEU, is dealt with in Section 7. The paperconcludes by giving a future outlook as Basel IIand its implementation in the EU represent veryimportant steps in a longer term process, butnot its end.

PART 1 – OVERVIEW OF THE NEW FRAMEWORK

1 DEVELOPMENT

With its New Framework for capitalrequirements, the BCBS aims to alleviate someof the drawbacks of the current regime datingback to 1988 (“Basel I”).6 First, the current

Basel I rules offer a simplified and rigidquantification of credit risk, that are not in linewith best practices applied by banks in theirrisk management. Basel II significantly refinesthe framework’s risk sensitivity by requiringhigher levels of capital for high-risk borrowers.By aligning required capital more closely to abank’s own risk estimates, the New Frameworknarrows the gap between regulatory capital andeconomic capital (requirements).7 It thereforeencourages banks to improve their riskassessment methods. Furthermore, theincreasing use of risk mitigation andsecuritisation has created the need to treat themmore extensively. Another drawback of thecurrent framework stems from its unintendedincentives for capital arbitrage throughtechniques such as securitisation. In addition,the current framework lacks rules for propermarket disclosure and therefore does notsupport market discipline. Finally, it offers noguidance for the supervisory review of banks’risk management practices.

Work on the New Framework started after 1996when the Capital Accord underwent a majoramendment to introduce capital requirements formarket risk.8 At the current juncture, fullimplementation of the Basel II Framework isexpected for the end of 2007. The whole process,therefore, from the initiation of discussions tothe moment when the most advanced calculationmethods will become available, will havestretched out over more than a decade.

Box 1 lists the key development stages andthe next steps in the implementation. Thedevelopment process was characterised by anintensive dialogue with the banking industry,reflected in the various consultation paperspublished by the BCBS. The Basel Committeealso carried out several quantitative impact

6 Basel Committee on Banking Supervision (1988). Basel I isalso called the “Basel Capital Accord”.

7 Regulatory capital is capital that is eligible to meetregulatory capital requirements; economic capital is capitalheld by the bank internally as a result of its own riskassessment. Technical terms are explained in the glossary atthe end of the paper.

8 Basel Committee on Banking Supervision (1996).

9ECB

Occasional Paper No. 42December 2005

2 STRUCTURE

Box 1

CHRONOLOGY OF THE BASEL PROCESS

June 1999 First Consultation Paper (CP1)July 2000 Quantitative Impact Study 1(QIS1)January 2001 Second Consultation Paper (CP2)April 2001 Quantitative Impact Study 2 (QIS2)November 2001 Quantitative Impact Study 2.5 (QIS2.5)October 2002 Quantitative Impact Study 3 (QIS3)April 2003 Third Consultation Paper (CP3)2004/2005 Quantitative Impact Studies 4 and 5 (QIS4/5)January 2004 “Madrid compromise”June 2004 Publication of the “New Framework” documentApril 2005 Consultation on the trading book review and double defaultJuly 2005 Publication of the trading book review and double defaultSpring 2006 Scheduled recalibration of the New FrameworkEnd 2006 Scheduled G10 implementation of simpler methodsEnd 2007 Scheduled G10 implementation of advanced methods

studies to gauge the impact of the new rules onbanks’ solvency positions and further refine therules.

Basel II has been designed as an evolutionaryframework, so updates will be made over timeto keep pace with ongoing developments in thefinancial industry. Prior to the implementationof the new rules, the Framework may undergo aquantitative adjustment (“recalibration”) onthe basis of the results of the most recent impactstudies. In addition, some technical changeswere introduced after June 2004 to address the“double default” issue and to bring thetreatment of trading activities more in line withthe New Framework.9 In the longer term, theBCBS intends to address a number of otherareas which are discussed in greater detail inthe last section dealing with the future outlook.

2 STRUCTURE

2.1 GENERAL OVERVIEW

An overview of the New Framework and itsmain components is shown in Chart 1. The darkboxes, which will be discussed in greater detail

below, refer to the components that have beenintroduced or to which there are major changesas a result of the new rules; the bright boxesrefer to the components that have remainedunchanged. Whereas Basel I only coveredminimum capital requirements, the Basel IIFramework now rests on three complementarypillars, namely minimum capital requirements(Pillar I), the supervisory review process(Pillar II) and market discipline (Pillar III). Inorder to effectively support financial stability,the Framework requires a smooth interactionbetween all three pillars.

As regards Pillar I, the minimum solvency ratioof 8% remains unchanged. This ratio expressesthe relationship between the bank’s regulatoryown funds (capital) and its “risk-weightedassets”, a measure of the risks it incurs. Risk-weighted assets are asset values multiplied by afactor (risk weight) that is a proxy of the (credit)risk related to these assets. For operational riskand market risk, the two other risk categories

9 Basel Committee on Banking Supervision (2005b). “Doubledefault” refers to the fact that the risk of both a borrower anda guarantor defaulting on the same obligation may besubstantially lower than the risk of only one of the partiesdefaulting; this feature is not suff iciently recognised in theJune 2004 Framework.

10ECBOccasional Paper No. 42December 2005

Chart 1 Overview of the New Framework

covered by the Framework, the risk-weightedassets that enter into the capital ratio are derivedfrom the directly calculated capital requirementsby multiplying them by 12.5 (the reciprocal ofthe minimum ratio of 8%). In addition, thedefinition of regulatory capital (the numerator ofthe capital ratio) was basically unaffected.

Pillar I, however, provides a fundamental updateof the Basel I methodology for the calculation ofrisk weighed assets, the denominator of thecapital ratio. First, operational risk is introducedas a new risk category for which the bank has tohold regulatory capital. This risk categorycomprises losses resulting from inadequate orfailed internal processes, people or systems, orfrom external events.

Second, a range of increasingly sophisticatedand risk-sensitive options are now available fordetermining banks’ capital requirements, bothfor credit risk and operational risk. In this way,

the option can be chosen that best suits the bank’sspecific features. Moreover, incentives are inplace for banks to adopt the more sophisticatedapproaches and thus improve their riskmanagement capabilities over time.10 In the areaof credit risk, two methods are available, namelythe standardised approach and the internalratings-based (IRB) approach. The former tiesrisk weights to ratings provided by recognisedrating agencies. The latter uses banks’ ownestimates of certain risk factors; depending onthe risk factors they are allowed to estimate, adistinction is made between a “foundation” andan “advanced” approach. The new rules for creditrisk also cover a detailed treatment ofsecuritisation and credit risk mitigation. Finally,in the area of operational risk, a bank can

10 For example the QIS3 results for the EU showed thatinstitutions adopting the standardised approach would facean increase in capital requirements of 2%, while thoseadopting the foundation IRB and the advanced IRBapproaches would see a decline of 7% and 9% respectively.See European Commission (2003a).

Source: ECB.

Pillar IMinimum

capitalrequirements

Pillar IISupervisory

review process

Pillar IIIMarket

discipline

BASEL II FRAMEWORK

Risk-weighted

assets

Operationalrisk

Standardisedapproach

Own funds

Market risk Core capital Supplementarycapital

Credit risk

Internalratings-based

approach

Standardisedapproach

FoundationIRB

AdvancedIRB

Advancedmeasurement

approach

Standardisedapproach

Internalmodels

approach

Basic indicatorapproach

11ECB

Occasional Paper No. 42December 2005

2 STRUCTURE

calculate its capital requirements on the basis ofits gross income (basic indicator approach andstandardised approach) or by using its ownmodel (advanced measurement approach). Asregards market risk, the New Framework leavesthe existing approaches basically unchanged.

2.2 PILLAR I – MINIMUM CAPITALREQUIREMENTS

2.2.1 CAPITAL REQUIREMENTS FOR CREDITRISK

(a) Standardised approachThe standardised approach is closest to thepresent capital rules. Exposures are classifiedinto a set of standardised asset classes (seeChart 2) and a risk weight is applied to eachclass, reflecting the relative degree of creditrisk. As under Basel I, off-balance sheetexposures are for capital purposes transformedinto “assets” through the application of “creditconversion factors”. The main changescompared to Basel I relate to the use of externalcredit ratings as the basis for determining therisk weights and the greater differentiation inthe possible risk weights.

Chart 2 Asset c lasses in the standardised approach

To give an example, risk weights for corporateexposures are now connected with their creditratings as indicated in Table 1 (for illustrativepurposes, ratings by Standard & Poor’s or S&Pare used).

Compared to Basel I, where all corporateexposures are weighted at 100%, there is now aconsiderable differentiation in the risk weights.The weight for investment-grade firms hasdeclined considerably (e.g. to 20 % for AAA),whereas in the non-investment grade segment, arisk weight of 150% applies to firms rated below“BB-”. Furthermore, unrated firms now obtainthe same risk weight as that formerly obtained byall corporates under Basel I.

For claims on banks, the former distinctionbetween institutions from OECD (20% riskweight) and non-OECD countries (100%) is nolonger applied. Instead, two options areavailable to national supervisors. Under thefirst option, the risk weights for banks arederived from the ratings of the country in whichthe bank is incorporated. Under the secondoption, the risk weights are determined on thebasis of the bank’s own rating.

Rating AAA to AA- A+ to A- BBB+ to BB- Below BB- Unrated

Risk weight 20 50 100 150 100

Table 1 Risk weights for corporate exposures under the standardised approach

(percentages)

Corporate exposures

Bank exposures

Sovereignexposures

Retail exposures

Commercialreal estate exposures

Other assetsResidentialproperty

exposures

Asset classes in the standardised approach

Source: ECB.

12ECBOccasional Paper No. 42December 2005

Retail exposures (75% instead of 100%) andmortgage loans (35% instead of 50%) aretreated more advantageously than underBasel I. Exposures to small businesses mayunder certain conditions also benefit from thepreferred retail treatment.

The rating agencies, or external creditassessment institutions (ECAIs) as they arereferred to in the New Framework, must obtainrecognition from the banking supervisor beforetheir ratings can be used by banks fordetermining risk weights. To get suchrecognition, an ECAI must satisfy each of thefollowing six criteria:

1. Objectivity of the rating or credit riskassessment methodology.

2. Independence. The ECAI must be free frompolitical or economic pressures, whichcould influence the analysis.

3. International access/transparency. TheECAI should offer its services to bothdomestic and foreign firms at similar terms.

4. Disclosure of material information.Includes the rating methodology, thedefinition of default, the time horizon, themeaning of each rating, the actual defaultrates experienced in each assessmentcategory and the transition matrix.11

5. Sufficient resources for offering creditassessments of high quality.

6. Credibility of the credit assessments.

(b) Internal ratings-based approach

Theoretical foundationThe internal ratings-based (IRB) approach tocredit risk is one of the most innovativeelements of the New Framework because itallows banks themselves to determine certainkey elements in the calculation of their capitalrequirements. Hence, the risk weights – andthus the capital charges – are determined

through a combination of quantitative inputsprovided either by banks or supervisoryauthorities, and risk weight functions specifiedby the BCBS. The new methodology isdesigned to be suitable for implementation bybanks of different size, business structure andrisk profile. Due to this characteristic, astandardised approach to modelling credit riskacross all types of banks is used for supervisorypurposes for the first time.

The IRB approach is closely linked to keyresults of academic work on credit riskmodelling.12 Its theoretical basis is theasymptotic single risk factor (ASRF) model ofcredit risk. Here, the likelihood of a borrowerbeing unable to repay his debt is derived fromthe distance between the value of its assets andthe nominal amount of his debt. The value ofthe firm’s assets is modelled as a variablewhich changes over time, in part as a result ofthe impact of random shocks. Default occurswhen a borrower’s assets are too low to coverits debt. The corresponding measure of creditrisk within a certain time frame (commonly setat one year, also in Basel II) is the probabilityof default (PD).

The ASRF characteristic of the model impliesthat it does not take into account borrower-specific idiosyncratic risks, i.e. risks that canbe diversified away in the lending bank’s loanportfolio. Instead, the model measures themarginal risk contribution of an exposure thatit would add to an already well diversifiedportfolio. In this respect the IRB approachdiffers from models that some banks applyinternally which measure a loan’s riskcontribution to a bank’s actual portfolio,inclusive of a potential additionaldiversification effect achieved by adding anexposure to this specific borrower (“credit riskportfolio model”). The IRB approach thereforecontains a deliberate simplification compared

11 The transition matrix provides a distribution of the likelychanges in a borrower’s credit quality (expressed by itsrating) over a certain time period, usually f ixed at one year.

12 Details on the theoretical background are given in BaselCommittee on Banking (2005a) and Gordy (2003).

13ECB

Occasional Paper No. 42December 2005

2 STRUCTURE

with the most advanced techniques currentlyapplied. This simplification allows for a modelthat is standardised and can be applieduniformly to banks of different sizes andportfolio compositions. It also avoids theparticular uncertainties connected with theestimation of correlations between the risks ofindividual borrowers.

Under the IRB approach, the requiredminimum capital is based on the probabilitydistribution of losses due to the default risk in aportfolio of loans or other financialinstruments. The horizon of the risk assessmentis set at one year. The IRB model furtherassumes a 99.9% confidence level. This meansthat once in a thousand years, the actual loss isexpected to exceed the model’s estimate.

Designed to address unexpected lossesAs a result of the agreement reached by theBCBS in January 2004 with the “Madridcompromise”, the IRB capital requirementsnow cover only unexpected losses whereaspreviously they were designed to cover bothexpected and unexpected losses. Unexpectedlosses are losses that occur above expectedlevels and this at a certain confidence level(99.9%). Although capital requirements are

designed to cover unexpected losses, bankshave to cover their expected losses on anongoing basis, e.g. through pricing, provisionsand write-offs.

In the IRB framework, banks have to comparethe stock of provisions they have made to coverloan losses with the expected losses based onthe IRB parameters. Any shortfall should bededucted equally from core capital andsupplementary capital13 and any excess will beeligible for inclusion in supplementary capitalsubject to a cap. The cap depends on the risk-weighted assets and is currently set at 0.6%.

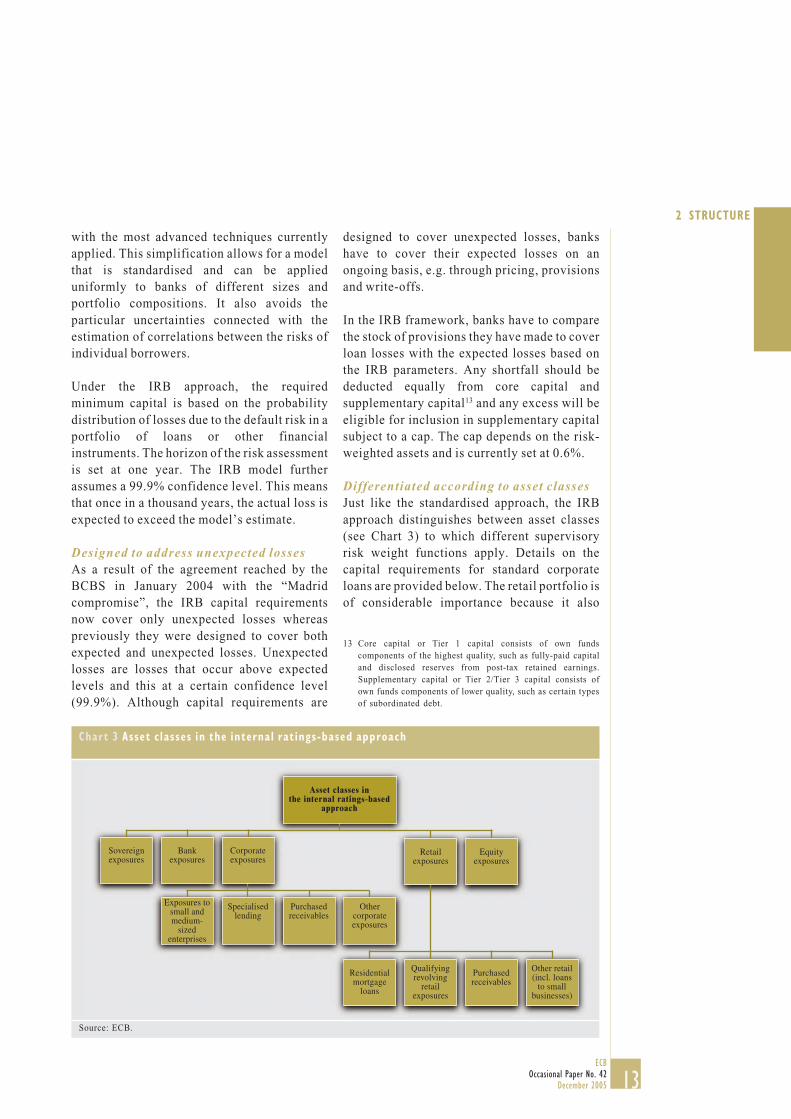

Differentiated according to asset classesJust like the standardised approach, the IRBapproach distinguishes between asset classes(see Chart 3) to which different supervisoryrisk weight functions apply. Details on thecapital requirements for standard corporateloans are provided below. The retail portfolio isof considerable importance because it also

Chart 3 Asset c lasses in the internal rat ings-based approach

13 Core capital or Tier 1 capital consists of own fundscomponents of the highest quality, such as fully-paid capitaland disclosed reserves from post-tax retained earnings.Supplementary capital or Tier 2/Tier 3 capital consists ofown funds components of lower quality, such as certain typesof subordinated debt.

Source: ECB.

Asset classes in the internal ratings-based

approach

Retail exposures

Equity exposures

Bank exposures

Sovereignexposures

Specialisedlending

Exposures tosmall andmedium-

sized enterprises

Residentialmortgage

loans

Qualifyingrevolving

retail exposures

Purchasedreceivables

Other retail(incl. loans

to small businesses)

Purchasedreceivables

Othercorporate exposures

Corporate exposures

14ECBOccasional Paper No. 42December 2005

Chart 4 Basic structure of the internal rat ings-based approach

applies to a sizeable fraction of lending to smallfirms. Subject to certain conditions, the NewFramework permits aggregate exposures to asingle firm of up to €1 million to be treatedunder the IRB approach as retail exposures,which is advantageous compared to thetreatment of other corporate lending. Evenloans to other small and medium-sizedenterprises (SMEs) that do not qualify as“retail” can benefit from a preferentialtreatment based on an adjustment relative to thefirm’s size under the standard corporatetreatment. This reduction applies when thefirm’s total sales are between €5 million and€50 million and its impact declines inproportion to the sales. Economically, the firmsize adjustment can be justified by the fact thatdefault probabilities for smaller firms areobserved to be less correlated with the overallstate of the economy so that they contributerelatively less risk to a well diversified loanportfolio.

Calculation methodThe calculation of capital requirements for aloan’s default risk under Basel II requires four

input parameters to the supervisory risk weightfunctions (see Chart 4):

1. Probability of default (PD): Estimate of thelikelihood of the borrower defaulting on hisobligations within one year.

2. Loss given default (LGD): Loss on theexposure following the borrower’s default,commonly expressed as a percentage of thedebt’s original nominal value.

3. Exposure at default (EAD): Nominal valueof the borrower’s outstanding debt.

4. Effective maturity of the loan (M).

A “foundation” and an “advanced” version ofthe IRB approach is available, the difference inthe two approaches being in the input variablesfor which the bank can use its own estimates.Both approaches rely on banks’ PD estimates,but banks’ internal estimates of LGD, EAD andM can only be applied in the advanced IRBapproach.

LGD

PD 1)

EAD

M

Risk weightSupervisory

risk weight function

Source: ECB.1) To be estimated by the bank under the foundation variant; for the other risk factors, a value f ixed by the BCBS has to be used. Forthe advanced variant, all four risk factors have to be estimated by the bank. In principle, both the foundation and the advanced IRBapproaches are available for all asset classes, the exception being the retail class, where only the advanced version is available.

15ECB

Occasional Paper No. 42December 2005

2 STRUCTURE

The resulting risk weights are plotted in Chart 5with the PDs shown on the horizontal axis. Asdesigned by the BCBS, the capital charge forretail portfolios is significantly below thecharge for corporate loans. This difference is ofconsiderable importance as it indicates that alarge number of small borrowers, includingsmall commercial undertakings, will benefitfrom a more favourable capital treatment thanlarger corporate borrowers.

A particular aim of the BCBS is to preserveoverall capital neutrality compared to thecurrent capital requirements, i.e. the capitalrequired from an average bank should not differmarkedly under the current Accord and BaselII. To this end, the BCBS had introduced intothe IRB formula a multiplier which is currentlyset at 1.06 (not reflected in Chart 5). This valueis based on the studies that the BCBS hasperformed so far on the overall impact of thenew requirements. With future assessments ofthe quantitative impact of the new capital rules,the issue of capital neutrality may have to be re-addressed. This multiplier provides then for asimple way to adjust the overall level of capitalrequired from IRB banks.

Practical implementationThe use of the IRB approach is subject to anexplicit supervisory approval, which dependson meeting certain minimum requirementsfrom the outset and on an ongoing basis. Theserequirements are aimed at the IRB systemproviding an adequate assessment of the bank’sexposures, a meaningful differentiation of riskand a reasonably good estimate of risk. Forexample, a qualifying IRB system is required tohave two separate dimensions, the risk ofborrower default and transaction-specificfactors (e.g. collateral, seniority, producttype). The IRB approach must also beconsistent with the internal use by the bank ofthe estimates it produces (“use test”).

In the practical implementation of the IRBsystem, validation (the assessment of thesoundness of the different system elements)will be important. In this context, the Accord

Implementation Group (AIG) of the BCBShas outlined a number of principles.14 First,validation is interpreted as an assessment of thepredictive ability of a bank’s risk estimates andthe use of ratings in the credit process. Inaddition, the bank has primary responsibilityfor validation. Furthermore, validation of theIRB approaches should encompass bothquantitative and qualitative elements. Finally,validation processes and outcomes should besubject to an independent review.

(c) Asset securitisationSecuritisation is one of the most rapidlygrowing activities of major banks. Banksincreasingly apply it to pools of loans on theirbalance sheets. In parallel, other creditinstruments such as corporate bonds areincreasingly used as underlying assets forsecuritisation transactions. With the explicittreatment of securitisation, Basel II providesfor an internationally harmonised standard forthe supervisory treatment of such transactions.At the same time, by making the capitalrequirements depend on the risk in the

14 Basel Committee on Banking Supervision (2005c).

Chart 5 IRB r isk weights across asset c lasses

(percentages)

Source: ECB.Note: Standard assumptions about the risk factors other thanPD, are made. Risk weights are calibrated to cover onlyunexpected losses, which have to be met via capitalrequirements.

Probability of default

020406080

100120140160180200220

020406080100120140160180200220

0 1 2 3 4 5 6 7 8 9 10

Risk weight

corporate, sovereign and banks exposuresexposure to small and medium size entitiesretail exposure: residential mortgage loansretail exposure: revolving creditsother retail exposures

16ECBOccasional Paper No. 42December 2005

securitisation positions, Basel II aims atreducing the scope for capital arbitrage, a keydrawback of the current framework andapparently an important securitisation driver.

Pillar I contains detailed rules for thesupervisory treatment of securitisation, whichcover the two roles a bank can play in asecuritisation transaction, namely as originatorand investor. In the first case, the banksecuritises its own assets; in the second case, itbuys and holds tranches of securitisations.Basel II deals with traditional transactions,e.g. the sale of loans through asset backedsecurities, as well as synthetic securitisations,such as the transfer of credit risk through creditderivatives without selling the loans.

Just as for credit risk, a number of approachesof different complexity are introduced to dealwith the wide variety in instruments and degreeof sophistication of the bank. Also here, astandardised and an IRB approach areavailable. The structure of the standardisedapproach for securitisation exposures is similarto the standardised approach for credit risk,although tranches that carry a higher risk or areunrated are dealt with more conservatively(higher risk weight or capital deduction).

Banks which were given supervisory approvalto use the IRB approach for the type ofunderlying exposures securitised must alsoapply the IRB methodology to securitisation.However, instead of a foundation andadvanced approach, there are now threeways of calculating capital requirements:the (external) ratings-based approach, thesupervisory formula approach and the internalassessment approach. The first is similar to thestandardised approach, although a greater riskdifferentiation is provided for. The next twoapproaches apply to unrated exposures, andthe third only to the specific case ofexposures resulting from ABCP (asset backedcommercial paper) programmes.

(d) Credit risk mitigationCompared with the current Capital Accord, theNew Framework contains a wider range ofcredit risk mitigation techniques that mayreceive recognition in the form of lower capitalrequirements, subject to prudent eligibilitystandards. For credit risk mitigation in the formof guarantees and credit derivatives, theborrower’s risk weight is replaced by thatof the protection provider. This “substitutionapproach” was recently modified by the BCBSto take account of the pair-wise correlation ofthe borrower and protection provider’s defaultprobabilities.15

For collateralised exposures, the Frameworkcomprises a range of methodologies that are ofdifferent degrees of sophistication. In general,the more sophisticated the methodology andthe more stringent the application conditions,the wider the range of eligible collateral.Compared to Basel I, the range of eligiblecollateral has also been expanded.

Banks using the standardised approach canapply the “simple method” for financialcollateral under which the risk weight of theborrower is replaced by the risk weight thatwould apply to the collateral if it were theexposure. Under both the standardised and thefoundation IRB approaches, there is also a“comprehensive method” for financialcollateral that foresees that the exposureamount under the standardised approach, or thesupervisory LGD under the foundation IRB, isreduced to reflect the adjusted value of thecollateral. In adjusting the collateral value,banks have to take account of the volatility ofits market value. A specific feature of thefoundation IRB is the presence of a supervisorymethod for the recognition of certain physicalcollateral.

For banks using the advanced IRB, the range ofadmissible collateral is unbounded as long asthe bank can demonstrate that it has goodestimates for the collateral value in the

15 Basel Committee on Banking Supervision (2005b).

17ECB

Occasional Paper No. 42December 2005

2 STRUCTURE

situation when the borrower has defaulted.While under the standardised approach there isin principle no recognition of physicalcollateral, real estate collateral is an exception.Also under the foundation IRB approach, thereare particular conditions that need to beobserved for this kind of collateral, asdiscussed in greater detail in Section 6.

2.2.2 CAPITAL REQUIREMENTS FOROPERATIONAL RISK

Operational risk has so far not been subject tocapital requirements. However, this does notimply that adding this new component toregulatory capital leads for an average bank tohigher overall requirements. Rather, theadditional requirement for operational riskcorresponds on average to lower capitalrequirements for credit risk compared with thecurrent rules so that the BCBS goal of capitalneutrality can on balance be reached. Foroperational risk, three options of differentlevels of sophistication are introduced.

The two most simple options are based on anindicator, namely gross income, which servesas a rough proxy for the size and the degree ofrisk of the operations. For this purpose, grossincome is defined as the sum of net interestincome and net non-interest income. Fees paidto outsourcing providers are not deducted fromthe income because it was considered thatoutsourcing is not a perfect mitigant foroperational risk and should therefore not leadto lower capital requirements. Gross income isalso adjusted for a number of items that areconsidered irregular and is in additionsmoothed by using a three-year average,excluding negative annual figures. Thisindicator, multiplied with a supervisory factor,delivers the capital requirement.

Under the basic indicator approach, thesupervisory factor (called “alpha”) is appliedto the total gross income. Under thestandardised approach, the gross income issplit out over eight different business lines,namely corporate finance, trading and sales,retail banking, commercial banking, payment

and settlement, agency services, assetmanagement, and retail brokerage. To eachbusiness line a different supervisory factor(called “beta”) is applied, reflecting therelative risk of the business line according tothe BCBS’ expert judgment. The average betaequals the alpha so that clear incentives toadopt the standardised rather than the basicindicator approach are only present for thosebanks that derive most of their gross incomefrom business lines with low betas, such asretail banking. Banks that want to use thestandardised approach have to implement a riskmanagement for operational risk that conformsto a number of qualitative minimumrequirements; such requirements are notmandatory for banks using the basic indicatorapproach.

In contrast to the case of the IRB as the mostadvanced approach for credit risk, the BCBSdoes not resort to a single modelling techniquefor operational risk. Rather, the most advancedoption for determining regulatory capital foroperational risk consists of a class ofapproaches referred to as the advancedmeasurement approaches (AMA). Under theAMA, the regulatory capital requirement iscalculated on the basis of banks’ internaloperational risk measurement systems. Thesehave to take account not only of actual internaland external loss data, but also of scenarioanalyses and factors relating to the banks’business environment and internal controls.Furthermore, the model has to achieve astatistical soundness standard comparable tothat of the IRB approach, where capital chargesare based upon a one-year time horizon and a99.9% confidence level, as described above.Subject to compliance with these modelproperties, banks are free to develop their ownapproach. This freedom is explained by the factthat, until now, no reliable candidate for astandard operational risk model has beenidentified.

In addition to the soundness standards for themodel itself, banks that request approval fromtheir supervisors for their AMA have to comply

18ECBOccasional Paper No. 42December 2005

with minimum requirements on theiroperational risk management that are moredemanding than for the standardised approach.By taking into account banks’ businessenvironment and internal controls, banks underthe AMA are in principle able to mitigate theiroperational risk capital charge by improvingtheir operational risk management, for instanceby introducing enhanced controls into thebusiness process. However, many openmethodological questions still remain withrespect to how this can be done in a sound andpractical manner. Banks are also allowed torecognise insurance as a risk mitigant for up to20% of their AMA capital requirements; thecondition is that their insurance contracts andproviders meet certain eligibility standards.

In the context of operational risk capitalrequirements, the study by De Fontnouvelle etal. (2004) is of considerable importance. Usingloss data from a number of internationallyactive banks, the authors find that loss data byevent types are quite similar acrossinstitutions. They also show that their resultsare consistent with economic capital numbersdisclosed by some large banks, and with theresults of studies modelling losses usingpublicly available “external” loss data.

2.3 PILLAR II – SUPERVISORY REVIEWPROCESS

Under Pillar II, banks assess their capitaladequacy on the basis of own internal riskmanagement methodology and supervisorsanalyse whether a specific bank’s capitaladequacy assessment is in line with its overallrisk profile and business strategies. Aconsistent application of supervisory practicesacross countries is of great importance to avoidany undue compliance burden and to ensure alevel playing-field. This is particularly true ifbanks belonging to the same group aim to makeuse of group-wide risk management but facedifferent expectations from their respectivenational supervisory authorities. Convergenceand cooperation in supervisory practices mayconstitute a way to alleviate this concern. The

extended role for the authority that exercisesconsolidated supervision, as provided for in theproposed EU rules, deserves particularattention in this regard (see Section 5).

Under the supervisory review process, thequestion will also be addressed whether thebank should hold additional capital againstrisks that are not, or not fully, covered in PillarI, and this may involve supervisory actionwhen this is indeed the case. An active role forsupervisory authorities will give banksincentives to continuously improve their riskmanagement models and systems. Relative tothe present situation, Pillar II requiressupervisors to apply considerably morediscretion in their assessment of capitaladequacy in individual banks.

The supervisory review process relies on fourprinciples:

1. Banks should have a process for assessingtheir overall capital adequacy in relation totheir risk profile and a strategy formaintaining capital levels.

2. Supervisors should review and evaluatebanks’ internal capital adequacyassessments and strategies, as well as theirability to monitor and ensure compliancewith regulatory capital ratios. If they are notsatisfied with the result of this process,supervisors should take appropriate action.

3. Supervisors should expect banks to operateabove the minimum regulatory capital ratiosand should have the ability to require banks tohold capital in excess of the minimum.

4. Supervisors should seek to intervene at anearly stage to prevent capital from fallingbelow the minimum levels required tosupport the risk characteristics of a bank andshould require rapid remedial action ifcapital is not maintained or restored.

The BCBS has outlined some important issuesto which both banks and supervisors should

19ECB

Occasional Paper No. 42December 2005

2 STRUCTURE

devote attention in the supervisory reviewprocess. These issues also include riskcategories which are not directly addressedunder Pillar I, such as interest rate risk in thebanking book16 and credit concentration risk.

Interest rate risk in the banking book has beengiven specific attention because it is seen byregulators as a material risk in the bankingsystem. Although the market risk amendmentof 1996 introduced interest rate risk as aseparate category, it was aimed at theexposures in the trading book. Hence, the 1996modification focused on the risk of lossesarising from, for example, bond portfolios orother categories of fixed-income instrumentsheld for trading. The BCBS acknowledged thisgap in the treatment of losses coming fromsharp interest rate changes. While it did not adda separate capital requirement, wording hasbeen included under Pillar II that requiressupervisors to identify those banks as outliersthat would experience a loss amounting to morethan 20% of their capital from a simulatedstandardised interest rate shock. Supervisoryauthorities must take measures to address thesituation of such outlier banks.

As regards the treatment of creditconcentration risk, there are twocomplementary motivations. First, severalbanking crises have been clearly linked tomaterial risk concentrations in bank portfolios.Second, the ASRF model, which is the basis forthe IRB approach, relies on two assumptionsabout a significant diversification in bankportfolios. First, the ASRF assumes that noborrower accounts for more than a very smallshare of total portfolio exposure. Second, itassumes that banks are well diversified acrossgeographical areas and industrial sectorswithin a large economy. Both assumptions maybe valid for the majority of exposures of someof the larger banks, but in the EU, the IRBapproach is likely to also be applied to smallerbanks, where concentration of exposure toindividual borrowers or certain sectors may bemore substantial. In this context, it should berecalled that the rules on large exposures in the

Codified Banking Directive (2000/12/EC)already serve to limit single-nameconcentration risk. Theoretical analysis hasshown that a ratings-based approach to settingcapital requirements needs the twoaforementioned assumptions, at leastimplicitly. Therefore, the concentrationproblem cannot be addressed merely bymodifications to the IRB risk-weights. Hence,under Pillar II, supervisors will analysepotential risk concentrations and may alsopotentially develop appropriate Pillar II capitalbuffers against such risk concentrations.

2.4 PILLAR III – MARKET DISCIPLINE

Under Pillar III, banks will be required topublish information focused on the keyparameters of their business profile, riskexposure and risk management. Suchdisclosures are seen as a precondition for theeffective working of market discipline onbanks. For banking groups, the requirementsapply to the top consolidated level of thebanking group.

Both qualitative and quantitative informationmust be disclosed. Hence, disclosure isrequired on the structure and adequacy ofcapital, and should therefore include details onthe core capital. It is envisaged that credit,market and operational risk are addressedseparately. For the disclosure of credit risk, it isalso planned to publish data on the portfoliostructure, the major types of credit exposure,the geographical and sectoral distribution andimpaired loans. In addition, information oncredit risk mitigation techniques and assetsecuritisation has to be provided. Banks will berequired to outline some details on their use ofIRB approaches, which represent a majorcomponent of the New Framework. Regardingmarket risk, banks have to summarise the key

16 The banking book is the bank portfolio which consists off inancial instruments that are not held for trading. Thetrading book is the bank portfolio that consists of f inancialinstruments that are held for short-term trading purposes, i.e.they are held intentionally for short-term resale and/or withthe intent of benef iting from short-term price movements orto lock in arbitrage prof its.

20ECBOccasional Paper No. 42December 2005

details of their internal models whereapplicable and to describe their use of stresstesting and back testing. Disclosurerequirements further cover the management ofand the compliance with requirements onoperational risk. Finally, the New Frameworkrequires that information on equity holdingsand interest rate risk in the banking book to bepublished.

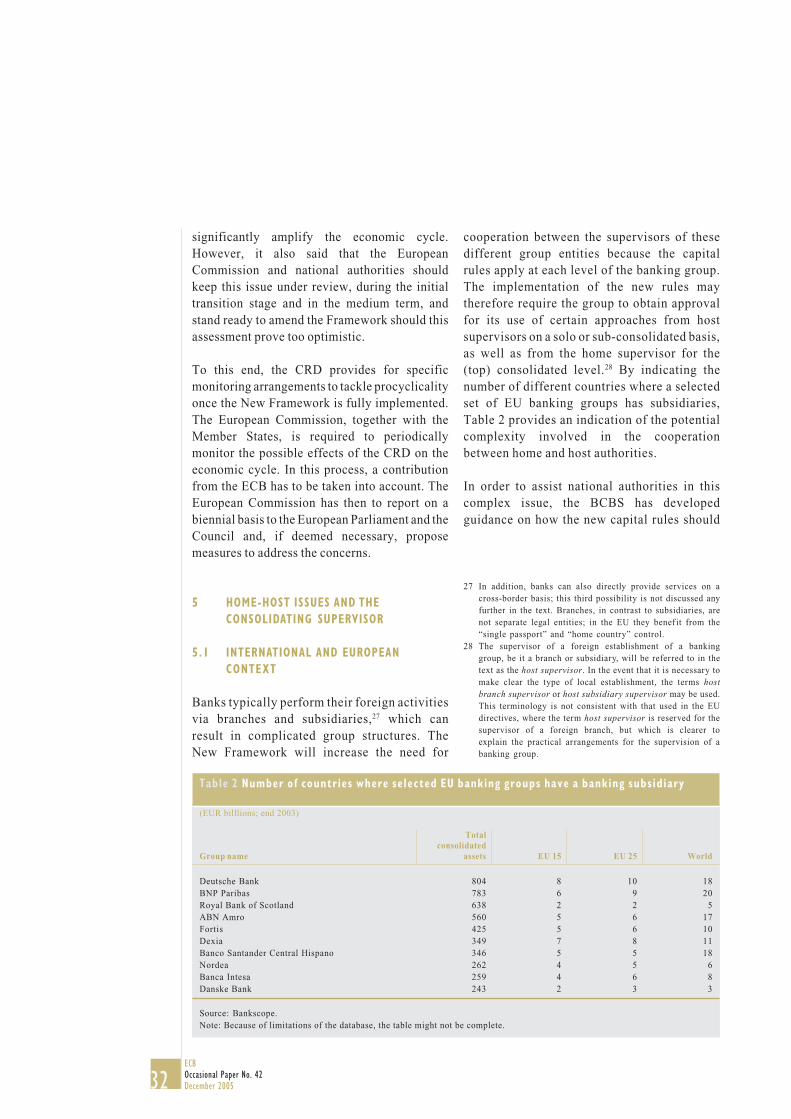

3 THE NEW FRAMEWORK IN THE EU

3.1 LEGAL AND INSTITUTIONAL SETTING

One month after the BCBS published itsdocument on the New Framework, theEuropean Commission released its ownproposals on new capital requirements forbanks and investment firms in the EU.17 Theproposals reflected to a large extent Basel II,but were at the same time tailored to thespecific features of the EU market. TheCommission’s initiative is part of the widerFinancial Services Action Plan (FSAP)launched in 1999. The FSAP outlined a numberof policy objectives and measures to improvethe Single Market for financial services. One ofits objectives was to ensure financial stabilityby keeping pace with state-of-the-artprudential rules and supervision, in particularin the area of banks’ solvency requirements.The Single Market is an important factor thatexplains why in some cases the proposed EUrules go further than the Basel rules.

Thereafter, the Commission’s proposals havebeen subject to scrutiny by the EuropeanParliament and the Council and to tripartitenegotiations with the Commission. Thesenegotiations resulted in a package of almost600 amendments, subject to which both theParliament and Council approved the proposalsin September and October 2005. In this way,they cleared the way for the new capitalrequirements to enter into force in the EU asscheduled by the BCBS.

Although there are a large number ofamendments, they leave the content and thrustof the Commission’s proposals intact. Theamendments introduce the trading book reviewand double default treatment as released by theBCBS in July 2005, reduce the number ofnational discretions, make some minortechnical corrections and take account ofseveral specific concerns relating to MemberStates’ national markets. Finally, theamendments also provide a preliminarysolution to the long debated issue ofinstitutional balance in the “comitology”procedure as part of the Lamfalussy approach,which is discussed in more detail below.

An important distinguishing feature of theimplementation of the Basel rules in theEuropean Union is the legal nature of thecapital adequacy framework. While the BaselII Framework takes the form of an accord oragreement amongst national bankingsupervisors represented in the BCBS – thusimplementation remains in principle voluntary– in the EU, the framework is legislative andbinding in all EU Member States. The Basel IIFramework will be transposed into EUlegislation by means of the CapitalRequirements Directive (CRD). Technically,this has been done via a recasting of theexisting Codified Banking Directive or CBD(2000/12/EC) and the Capital AdequacyDirective or CAD (93/6/EEC). The re-castingtechnique, established by the interinstitutionalagreement 2002/C77/01 of 28 November 2002,allows the incorporation in current legislativetexts of both amended and unchangedprovisions.

Another significant element is the regulatoryand supervisory setting that is now in placein the EU as a result of the “Lamfalussy”approach (see Box 2). This approach wasinitially applied to the securities sector18 but

17 European Commission Services (2004).18 The Lamfalussy approach was set out by the Committee of

Wise Men on the Regulation of European Securities Markets,chaired by Baron Alexandre Lamfalussy, in its “FinalReport” dated 15 February 2001.

21ECB

Occasional Paper No. 42December 2005

3 THE NEWFRAMEWORK

IN THE EUwas later extended to all financial sectors,including banking. It was introduced with theaim of improving the speed and flexibility of

the rulemaking process, so that regulation canbetter keep up with developments in financialmarkets.

Box 2

THE LAMFALUSSY APPROACH

Level 1

Proposal for Community legislation advanced by the European Commission and adopted underthe co-decision procedure by the Council and the European Parliament. The legislation takesthe form of directives or regulations. It should be limited to framework principles and definethe powers for the Commission to implement the necessary technical rules.

Level 2

The European Commission enacts legislation containing the technical details for theframework principles approved at Level 1. This requires the intervention of a regulatorycommittee under the “comitology procedure”1. These regulatory committees are chaired by theCommission and composed of high-level representatives from Member States. The ECB hasobserver status in the banking, securities and financial conglomerates committees.

The “Level 2” regulatory committeesBanking European Banking Committee (EBC)Securities and investment funds European Securities Committee (ESC)Insurance and pension funds European Insurance and Occupational Pensions

Committee (EIOPC)Financial conglomerates European Financial Conglomerates Committee (EFCC)

Level 3

Level 3 committees are entrusted with the task of facilitating the day-to-day implementation ofCommunity law with the goal of converging both supervisory practices and the application ofCommunity legislation, and enhancing supervisory cooperation. Guidelines, interpretativerecommendations, common standards or best practices may be issued, but these are not legallybinding and implementation remains voluntary. Level 3 committees also assist theCommission in drafting the more technical provisions of the legislation enacted at Level 2. Thesupervisory committees are composed of high-level representatives from the competentnational supervisory authorities.

The “Level 3” supervisory committeesBanking Committee of European Banking Supervisors (CEBS)Securities and investment funds Committee of European Securities Regulators (CESR)Insurance and pension funds Committee of European Insurance and Occupational

Pensions Supervisors (CEIOPS)Financial conglomerates At present, there is no Level 3 committee

1 The procedure whereby the Commission is assisted by a Committee comprising representatives from Member States in theadoption of implementing measures for Community legislation. Council Decision 1999/468/EC of 28 June 1999 laying down theprocedures for the exercise of implementing powers conferred on the Commission specif ies the types of comitology proceduresgoverning the adoption of implementing measures.

22ECBOccasional Paper No. 42December 2005

Level 4

The European Commission is responsible for ensuring that Member States’ national lawcomplies with Community law and, if needed, to take enforcement action. Legal action againstMember States can be taken before the European Court of Justice. Strengthening enforcementis underpinned by enhanced cooperation between Member States, the regulatory bodies and theprivate sector.

The increased flexibility of the legislativeprocess envisaged by the Lamfalussy approachis reflected in the CRD transposing thecapital requirements into EU law. Whereasamendments to the main principles still have tobe made via co-decision, amendments to themore technical provisions can be introducedvia the more flexible and faster “comitology”procedure. However, the CRD is not apure “Lamfalussy directive” as it combinesboth framework principles and technicalimplementation rules in the same legalinstrument.

The issue of “comitology” and the institutionalbalance between Parliament, Commission andCouncil was long debated given that the currentprocedure does not grant the Parliament theright to “call back” the “comitology” powers ofthe Commission, although such a right wasintended to be introduced as part of theConstitutional Treaty. A last minutecompromise between Commission, Counciland Parliament as part of the above-mentionedamendments means that the current comitologysystem – which provides no formal “call-back”right for Parliament – can be used to implementand update the Directives for a maximum oftwo years or until 1 April 2008 at the latest.After this period, aforementioned powerscan be renewed only with the agreement of thethree institutions. This timeframe should allowfor reflection on a possible recalibration asscheduled by the BCBS for Spring 2006.

The implementation of the New Frameworkrepresented in principle a “window ofopportunity” to structure the new rules alongthe lines of what had been introduced for thesecurities sector. This would have entailed a

clear distinction between framework principles(Level 1 acts) and technical implementationrules (Level 2 acts), with the adoption ofregulations for the latter, wheneverappropriate. In general, recourse to regulationswould reinforce convergent implementationacross the EU, given that they are directlyapplicable in all Member States, as opposed todirectives, which need to be transposed intonational law. This in turn would facilitatecompliance by cross-border groups andcontribute to promoting a level playing-fieldand further integration. This opportunity wasnot exploited and hence, the current legalframework should be viewed as a first step in alonger term process where the ultimate goalwould be to arrive at a uniform and directlyapplicable set of European rules for financialinstitutions.

Regulatory convergence and a consistentimplementation of rules across Member Statesare important to ensure a level playing-field inthe Single Market. However, the CRD stillincludes several national discretions, meaningthat the scope for potential divergent nationalimplementation is considerable. In addition, theuse of terms that are not clearly defined providesnational authorities with considerable leeway,which may also result in significantly differentinterpretations. In this respect, the work by theLevel 3 banking committee – the CEBS – iscrucial. The CEBS has given priority to theidentification and reduction of national options.The progress achieved thus far by the CEBS isreflected in the final CRD text and must beacknowledged, while the pursuit of more workin this field should be strongly encouraged. Asthe EU financial systems become increasinglymore integrated, some of the remaining national

23ECB

Occasional Paper No. 42December 2005

3 THE NEWFRAMEWORK

IN THE EUdiscretions may become obsolete over time,necessitating further revisions.

Furthermore, in its work on supervisoryconvergence regarding the new capital rules,the CEBS is focusing on a number of importantareas.19 Foremost is the development of acommon reporting framework for the newsolvency ratio, which is especially importantfor cross-border banking groups that arepresently confronted with a variety of nationalreporting schemes. The CEBS is also workingon guidance for the supervisory reviewprocess, which comprises the bank’s internalcapital adequacy process and the supervisoryreview and evaluation process. As regards thestandardised approach, a common approach isunderway for the recognition of external creditassessment institutions (ECAIs), as well as fordeveloping the criteria to transform (“map”)ratings into risk weights. For the advancedcalculation methods, a common approach tovalidation principles is being defined. Anotherimportant task is to foster cooperation betweenhome and host authorities. Finally, the CRDnot only provides for disclosure by banks butalso by supervisors, for which the CEBS isestablishing a common framework.

3.2 SPECIFIC FEATURES OF EUIMPLEMENTATION

The implementation of the new capital rules inEurope will not fully mirror the Basel IIFramework; rather the EU rules have beenadapted in order to reflect the specific SingleMarket context, which encompasses suchfeatures as the single banking licence, homecountry control and minimum harmonisation ofprudential requirements. The main specificitiesof the European setting that have been taken intoaccount when developing the EU rules arepresented below.

(a) Scope of applicationOne of the main diverging aspects concernsthe scope of application of the rules. Just likeBasel I, the Basel II Framework is envisagedto apply only to internationally active banks. The

European implementation of the capitalrequirements, by contrast, will in principle applyto all banks and investment firms,20 independentof their size or the geographical scope of theiractivity. Financial institutions dealing in thesame activity or providing similar services willtherefore be subject to the same capitalrequirements, thus ensuring a level playing-fieldwithin the EU. In this respect, it should berecalled that following the CAD, banks andinvestment firms in the EU are already subject tothe same capital rules. This similar treatment isrooted in the fact that the CBD allows theuniversal banking model, i.e. the combination ofbanking and securities activities in the samelegal entity or within the same financial group.

Another difference in the scope of applicationis the level at which the new rules apply. TheBasel II rules apply to internationally activebanks at every layer of the banking group ona (sub)consolidated basis. No general explicitcapital requirements are formulated forindividual banks, but when an entity of thegroup itself qualifies as an internationallyactive bank, the Basel II capital requirementsmust also be met by this entity. The EU rules,by contrast, apply in principle both on aconsolidated and an individual (solo) basis.However, subject to certain conditions, theCRD contains the possibility to waive the solorequirements on (only) domestic subsidiaries.The conditions for this waiver are aimed atensuring that the parent guarantees thecommitments of the subsidiary that has beenexempted from the solo capital requirements.

(b) Range of available approachesThe full spectrum of approaches for thecalculation of capital requirements asenvisaged by the Basel II Framework, from thesimple methods to those based on internal

19 This is reflected in the different Consultation Papers (CP)released by the CEBS. See in particular the CP3 (supervisoryreview process), CP4 (solvency reporting framework), CP5(supervisory disclosure), CP7 (recognition of ECAIs), CP9(supervisory cooperation) and CP10 (validation of advancedcalculation methods).

20 Investment firms are f irms authorised under the Markets inFinancial Instruments Directive (MiFID), 2004/39/EC.

24ECBOccasional Paper No. 42December 2005

models, will be available in the EU. Theapplication of the New Framework in the EU toall banks and investment firms, irrespective oftheir level of complexity or sophistication,indeed requires the full spectrum of approachesto be available to all institutions. In thiscontext, it should be noted that, in the US, theapplication of Basel II will only encompass themost advanced methods (see Box 3).

The comprehensive scope of application in theEU was also the basis for the development ofrules on “permanent partial use”. In the contextof credit risk, partial use refers to thepossibility of using the simpler standardisedapproach for certain exposure classes, whileapplying the more sophisticated IRBapproaches for the remaining classes. UnderBasel II, a bank using the IRB for any exposuremay only permanently apply the standardisedapproach for so-called non-material exposureclasses and business lines. All other exposureshave to be treated under the IRB within a timeframe agreed with the respective supervisorupfront (“roll out” plan). This rule aims to limitthe potential for “cherry-picking” betweenapproaches with different risk sensitivities.

For small EU banks, it may be particularly hard,or even impossible, to roll out the IRB approach

to certain exposure classes where they havea very limited number of counterparties.Nevertheless, the exposure to thesecounterparties may still be material in relation tothe bank’s overall exposures. For this reason,there is the possibility for exposures to banks,investment firms, sovereigns and certain otherpublic sector bodies to qualify for a permanentpartial use. Such exposures could then remain onthe standardised approach, independent of theirmateriality, while the bank otherwise uses theIRB approach.

The broad application in the EU of the capitalrequirements framework to institutions thatrange from very sophisticated internationallyactive banks to less complex investment firms,together with the potentially burdensomeoverall impact of the new rules on certaininvestment firms, requires that the prudentialstandards be adapted. Therefore, investmentfirms falling within certain categories may beexempted by the competent authorities fromcalculating capital requirements foroperational risk. Where this exemption is used,the currently used “expenditure-based” capitalcharge, that is otherwise abolished, will beretained. Under this approach, investmentfirms are required to hold minimum capital inrelation to their overhead costs.

Box 3

IMPLEMENTATION OF BASEL II IN THE US AND ITS IMPLICATIONS FOR EU BANKS

The US authorities decided to confine the spectrum of approaches available in the Basel IIFramework.1 Large internationally active banks (consolidated assets over USD 250 billion andforeign exposure of at least USD 10 billion), including subsidiaries of foreign banks, will berequired to use only the advanced methodologies to calculate capital requirements. Thesemethods include the advanced IRB approach for credit risk and the AMA for operational risk.Approximately ten banks fall into this category. In addition, other banks that meet therequirements for the use of the advanced approaches will be allowed to opt into Basel II. Thiswill be the case for approximately another ten banks. Overall, the banks which are expectedto apply Basel II are those that are active in cross-border banking. They account forapproximately 99% of the foreign assets held by the top fifty US banking organisations and forabout two-thirds of the assets of US banks. The remaining banks (approximately 6,500) in the

1 Federal Reserve Board et al. (2003).

25ECB

Occasional Paper No. 42December 2005

3 THE NEWFRAMEWORK

IN THE EUUS and subsidiaries of foreign banks that donot meet the criteria to adopt Basel II willremain under the current Basel I rules.2

The implementation of Basel II in the US mayhave implications for EU banks operating in theUS, especially those with a significant presence(see chart for some examples). These banksmay be required to operate under rules thatdiffer from those applying to the rest of thebanking group, in particular the parentcompany in the respective home country. Thiscan be costly and inefficient and potentiallyraises negative competitive effects forEuropean banks. A US subsidiary of a foreignbank has to comply with US rules, which willentail the need for these subsidiaries to eithermeet the prerequisites in order to apply theadvanced approaches of Basel II or to remain under the current Basel I based rules. Hence,subsidiaries which would have targeted the foundation IRB will continue to apply the Basel Irules, irrespective of whether or not the rest of the banking group applies these approaches on aconsolidated basis.

The US authorities have publicly conveyed that they would be prepared to explore thepossibility of allowing foreign subsidiaries to use conservative estimates for a transitionperiod.3 However, further work to develop concrete proposals still needs to be pursued. In thiscontext, the work of the BCBS’ Accord Implementation Group (AIG) in maintaining a levelplaying-field across countries and in achieving an acceptable level of consistency in theimplementation of Basel II is of the utmost importance.

More recently, the results of the fourth quantitative impact study (QIS4) have shown a muchhigher than expected capital reduction (of around 15% on aggregate and by more than 26% inmore than half of the participating banks) vis-à-vis the current level of the 26 large US financialinstitutions replying to the QIS4, and also a very wide dispersion across banks (ranging from adecrease of 47% to an increase of 56%).4

These results have prompted the US authorities to delay the scheduled publication of the Notice ofProposed Rulemaking (NPR). They now plan to make the US Basel II proposal available in thefirst quarter of 2006 and to introduce additional prudential safeguards to address the concernsresulting from the QIS4. In particular, a one-year delay in the implementation will be proposed.Further, the capital floors tied to the current Basel I rules will extend to 2011, after which they willbe reconsidered on an institution-by-institution basis.5 Given the significant implications that thedecisions by the US authorities may have in maintaining a level playing-field internationally, thisis an issue that will have to be closely monitored in the EU.

2 These rules will be revised somewhat and made more risk-sensitive. This regime is sometimes called “Basel IA”.3 Ferguson (2003).4 Schmidt Bies (2005) and Powell (2005).5 Federal Reserve Board et al. (2005).

European banking groups with a s igni f icantpresence in the US

(US assets as % of total assets)

Source: ECB calculations on the basis of the 2004 annualreports of the respective banking groups.Note: Figures refer to North America for ABN Amro, BNPParibas, Deutsche Bank and HSBC; f igures refer to loans/commitments for ABN Amro and BNP Paribas.

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

HSBC ABNAmro

DeutscheBank

Royal Bank ofScotland

BarclaysBank

BNPParibas

26ECBOccasional Paper No. 42December 2005

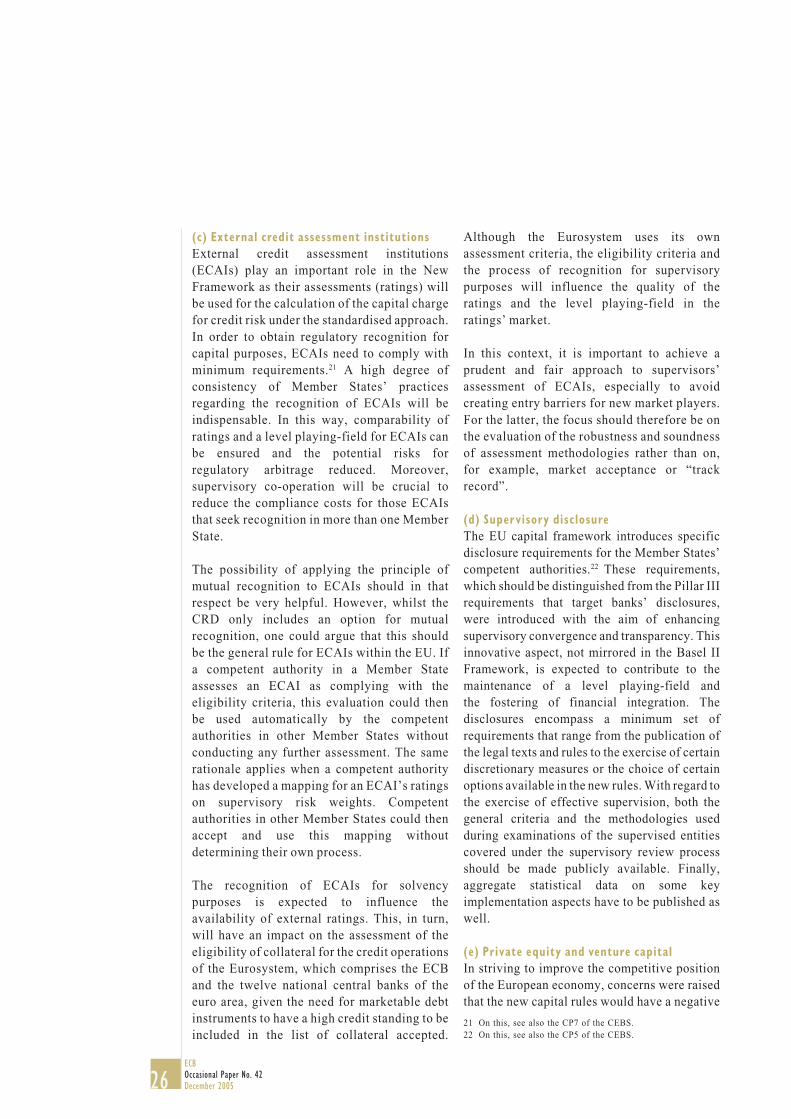

(c) External credit assessment institutionsExternal credit assessment institutions(ECAIs) play an important role in the NewFramework as their assessments (ratings) willbe used for the calculation of the capital chargefor credit risk under the standardised approach.In order to obtain regulatory recognition forcapital purposes, ECAIs need to comply withminimum requirements.21 A high degree ofconsistency of Member States’ practicesregarding the recognition of ECAIs will beindispensable. In this way, comparability ofratings and a level playing-field for ECAIs canbe ensured and the potential risks forregulatory arbitrage reduced. Moreover,supervisory co-operation will be crucial toreduce the compliance costs for those ECAIsthat seek recognition in more than one MemberState.

The possibility of applying the principle ofmutual recognition to ECAIs should in thatrespect be very helpful. However, whilst theCRD only includes an option for mutualrecognition, one could argue that this shouldbe the general rule for ECAIs within the EU. Ifa competent authority in a Member Stateassesses an ECAI as complying with theeligibility criteria, this evaluation could thenbe used automatically by the competentauthorities in other Member States withoutconducting any further assessment. The samerationale applies when a competent authorityhas developed a mapping for an ECAI’s ratingson supervisory risk weights. Competentauthorities in other Member States could thenaccept and use this mapping withoutdetermining their own process.

The recognition of ECAIs for solvencypurposes is expected to influence theavailability of external ratings. This, in turn,will have an impact on the assessment of theeligibility of collateral for the credit operationsof the Eurosystem, which comprises the ECBand the twelve national central banks of theeuro area, given the need for marketable debtinstruments to have a high credit standing to beincluded in the list of collateral accepted.

Although the Eurosystem uses its ownassessment criteria, the eligibility criteria andthe process of recognition for supervisorypurposes will influence the quality of theratings and the level playing-field in theratings’ market.

In this context, it is important to achieve aprudent and fair approach to supervisors’assessment of ECAIs, especially to avoidcreating entry barriers for new market players.For the latter, the focus should therefore be onthe evaluation of the robustness and soundnessof assessment methodologies rather than on,for example, market acceptance or “trackrecord”.