Embed Size (px)

DESCRIPTION

nomura

Citation preview

Connecting Markets East & West

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Any authors named on this report are research

analysts unless otherwise indicated.

Equity Research

Quantitative Equity Strategy

October 2014

Quantitative Strategy

Inigo Fraser Jenkins – NIplc Alla Harmsworth – NIplc Paul Danis – NIplc Mark Diver – NIplc +44 20 7102 4658 +44 20 7102 2219 +44 20 7102 3406 +44 20 7102 2987 [email protected] [email protected] [email protected] [email protected]

Gerard Alix Guerrini – NIplc Rohit Thombre Robertas Stancikas – NIplc +44 20 7102 8153 +91 22 305 32561 +44 20 7102 3127 [email protected] [email protected] [email protected] Quantitative Solutions Industry Specialists

Ethan Brodie – NSI Bhavik Shah – NIplc Sarah McCarthy – NIplc Norman Pfeifer – NIplc +1 212 667 1076 +44 20 7103 9988 +44 20 7103 9988 +44 20 7103 9988 [email protected] [email protected] [email protected] [email protected]

Rupal Agarwal +91 22 6723 5436 [email protected]

Market outlook

Are earnings growing in Europe?

Global quant equity portfolio:

Tactical factor allocation: Buy growth over income as rates rise

Strategic quant trades

Long horizon concentrated strategies

Sector allocation and current trade ideas

Fund-management strategy

Is passive the new active?

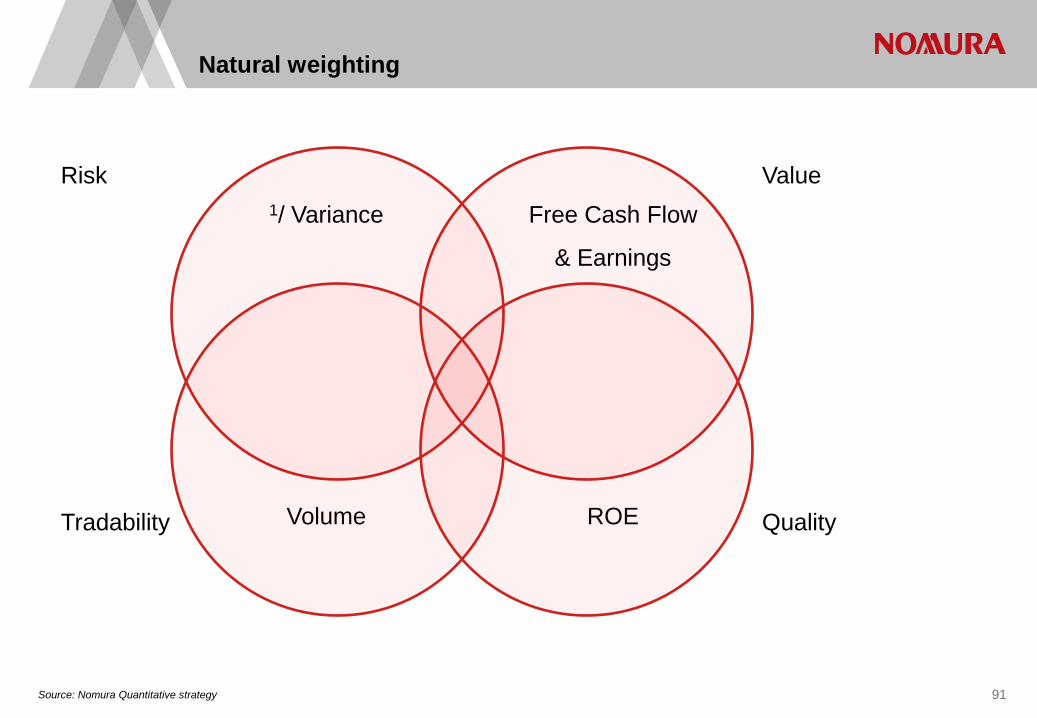

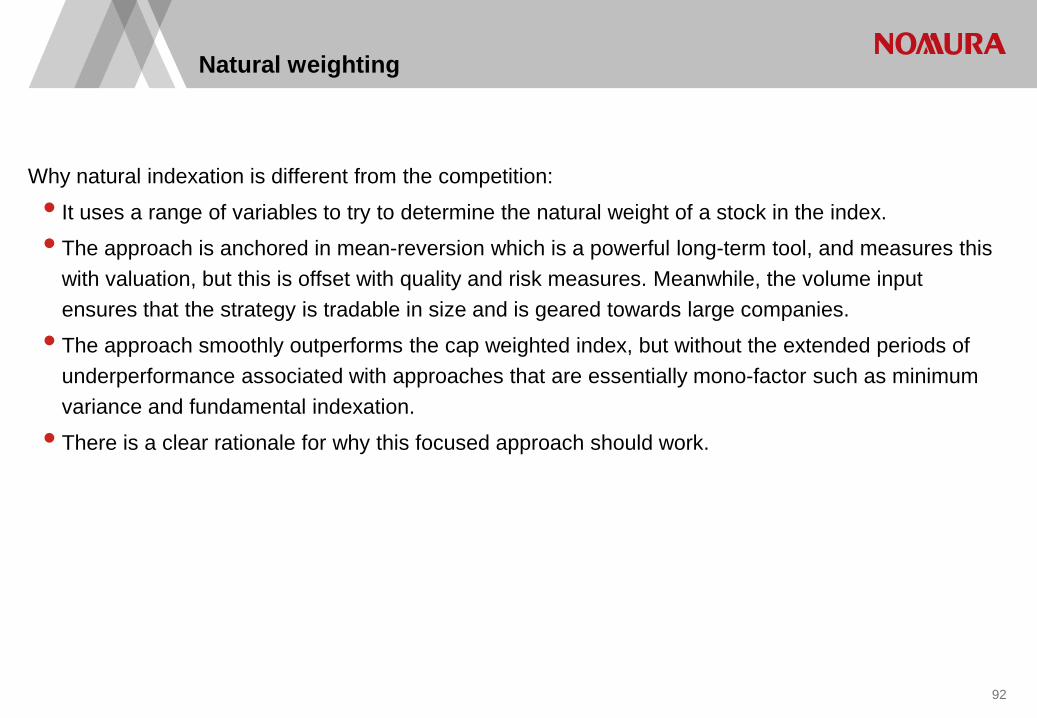

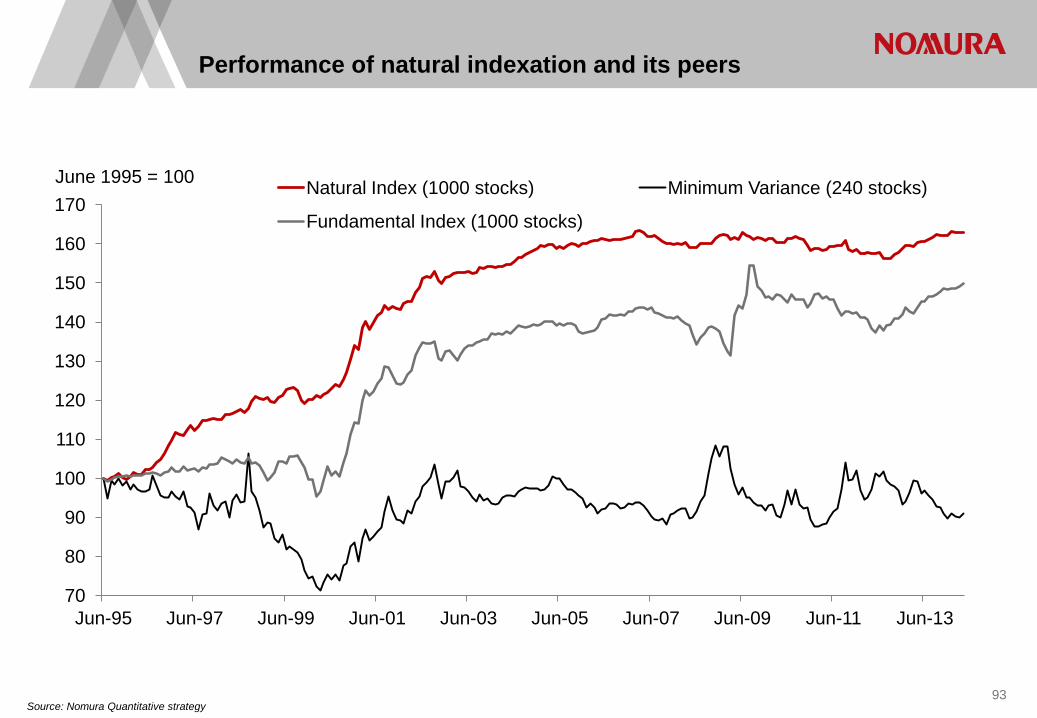

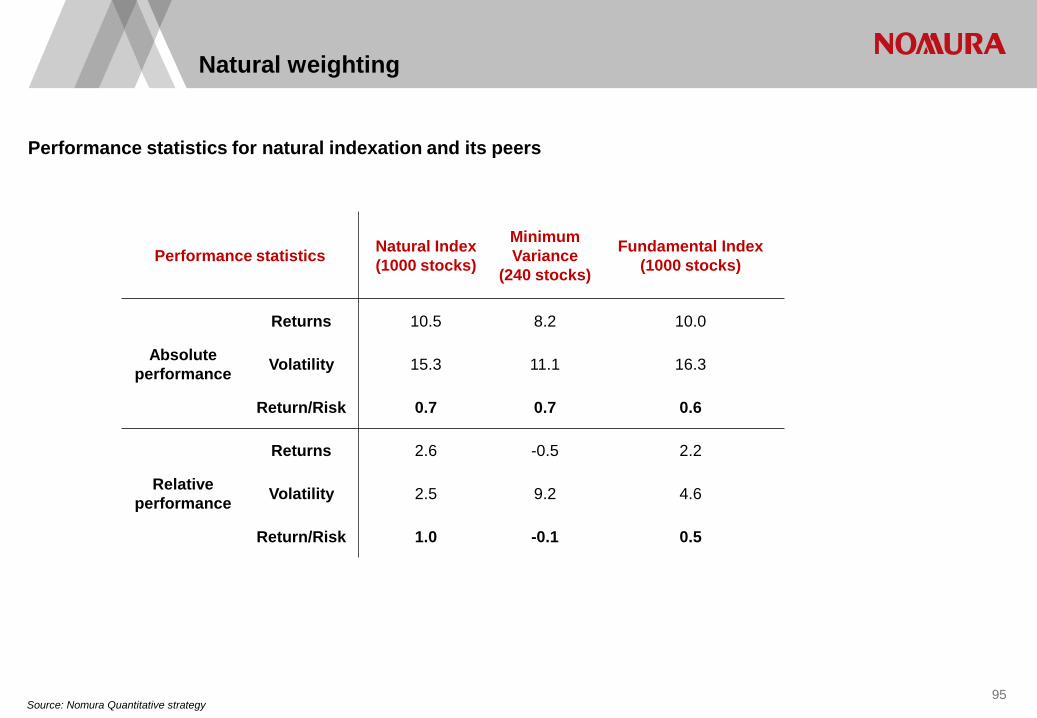

Natural weighting

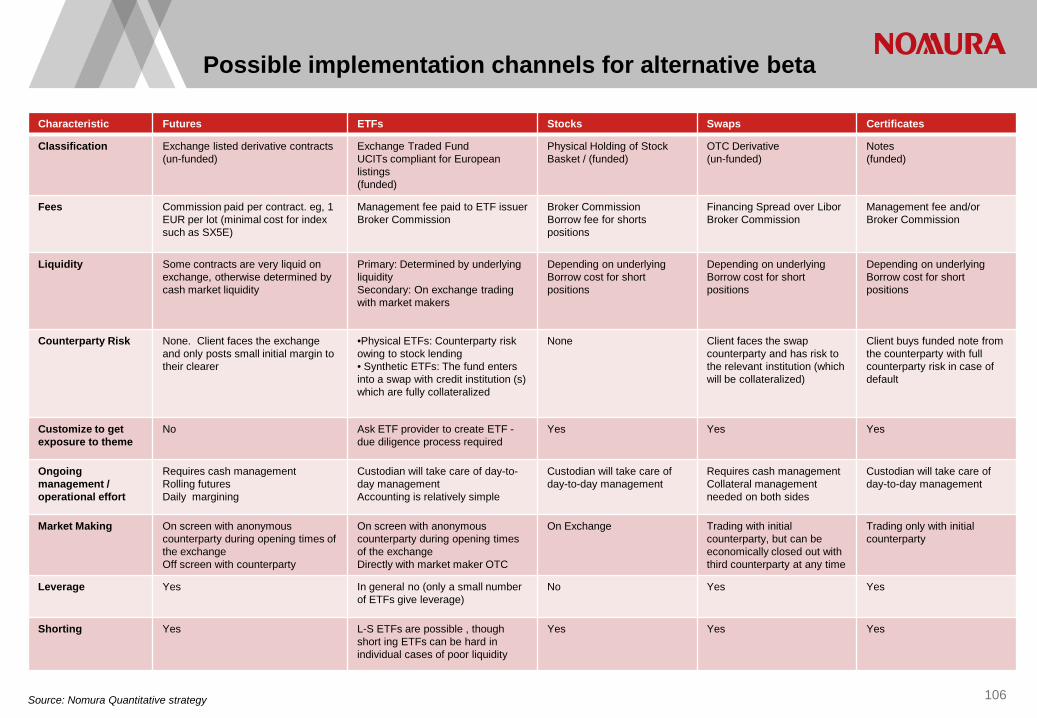

Cross-asset alternative beta/risk premia investing

EM country selection

Website, recommended strategy portfolio

Introduction

1

Market outlook

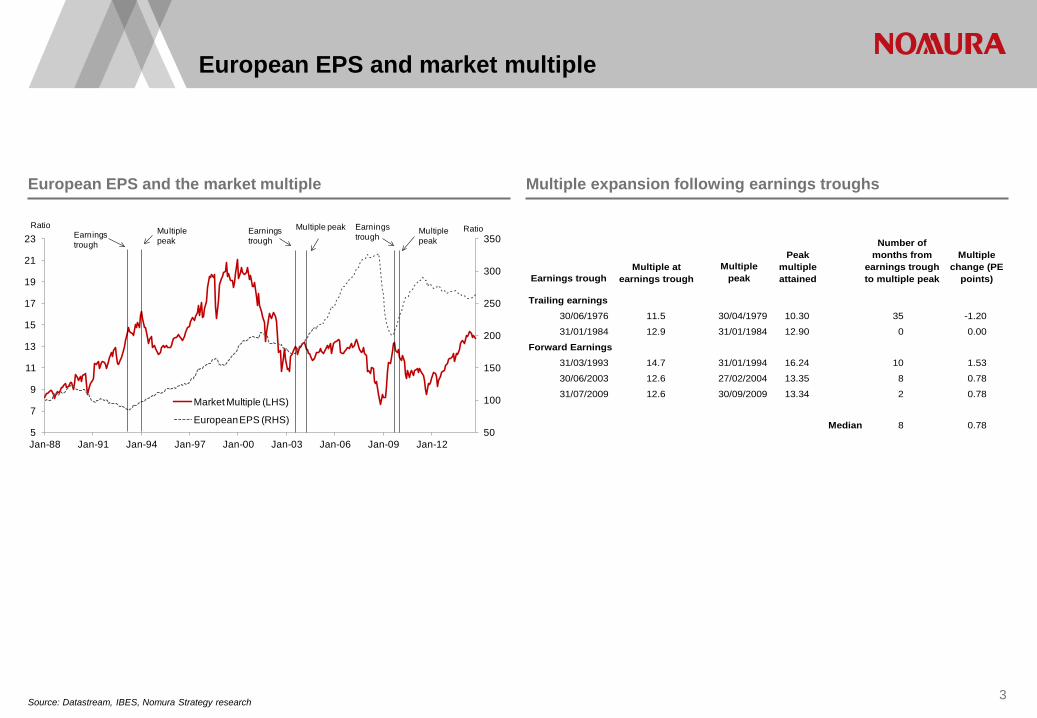

European EPS and market multiple

Source: Datastream, IBES, Nomura Strategy research 3

European EPS and the market multiple Multiple expansion following earnings troughs

Earnings troughMultiple

peak

Trailing earnings30/06/1976 11.5 30/04/1979 10.30 35 -1.20

31/01/1984 12.9 31/01/1984 12.90 0 0.00

Forward Earnings31/03/1993 14.7 31/01/1994 16.24 10 1.53

30/06/2003 12.6 27/02/2004 13.35 8 0.78

31/07/2009 12.6 30/09/2009 13.34 2 0.78

Median 8 0.78

Peak multiple attained

Multiple change (PE

points)Multiple at

earnings trough

Number of months from

earnings trough to multiple peak

50

100

150

200

250

300

350

5

7

9

11

13

15

17

19

21

23

Jan-88 Jan-91 Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Jan-09 Jan-12

RatioRatio

Market Multiple (LHS)

European EPS (RHS)

Multiple peakMultiple peak

Multiple peak

Earnings trough

Earnings trough

Earnings trough

Source: Nomura Strategy research, Shiller database 4

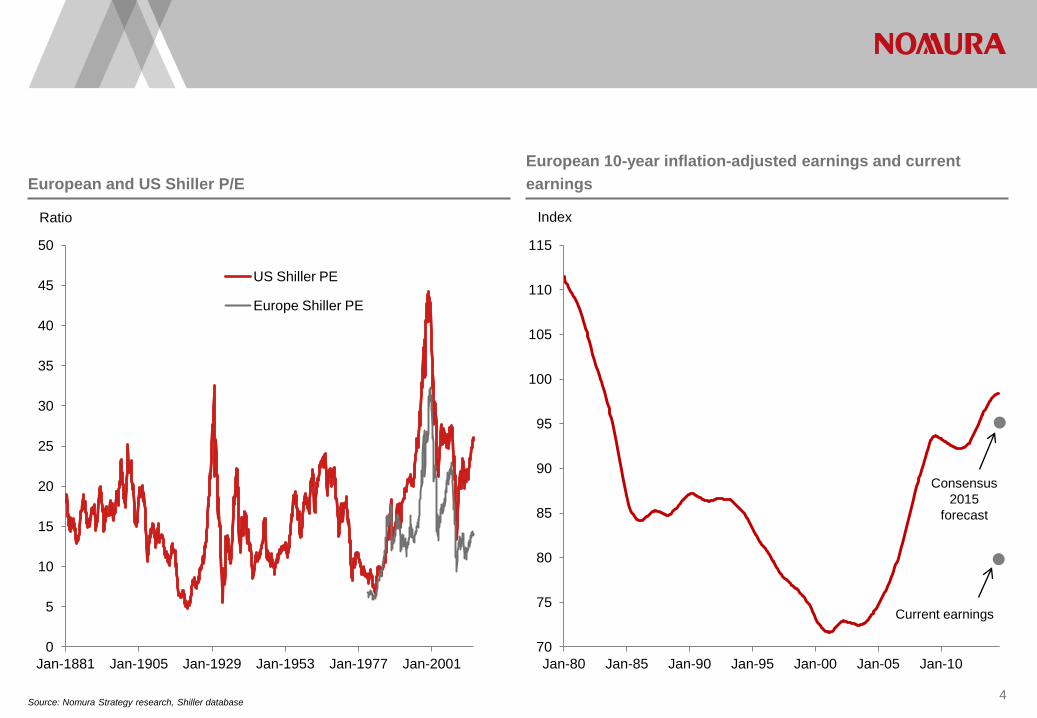

European and US Shiller P/E European 10-year inflation-adjusted earnings and current earnings

0

5

10

15

20

25

30

35

40

45

50

Jan-1881 Jan-1905 Jan-1929 Jan-1953 Jan-1977 Jan-2001

Ratio

US Shiller PE

Europe Shiller PE

70

75

80

85

90

95

100

105

110

115

Jan-80 Jan-85 Jan-90 Jan-95 Jan-00 Jan-05 Jan-10

Index

Current earnings

Consensus 2015

forecast

5

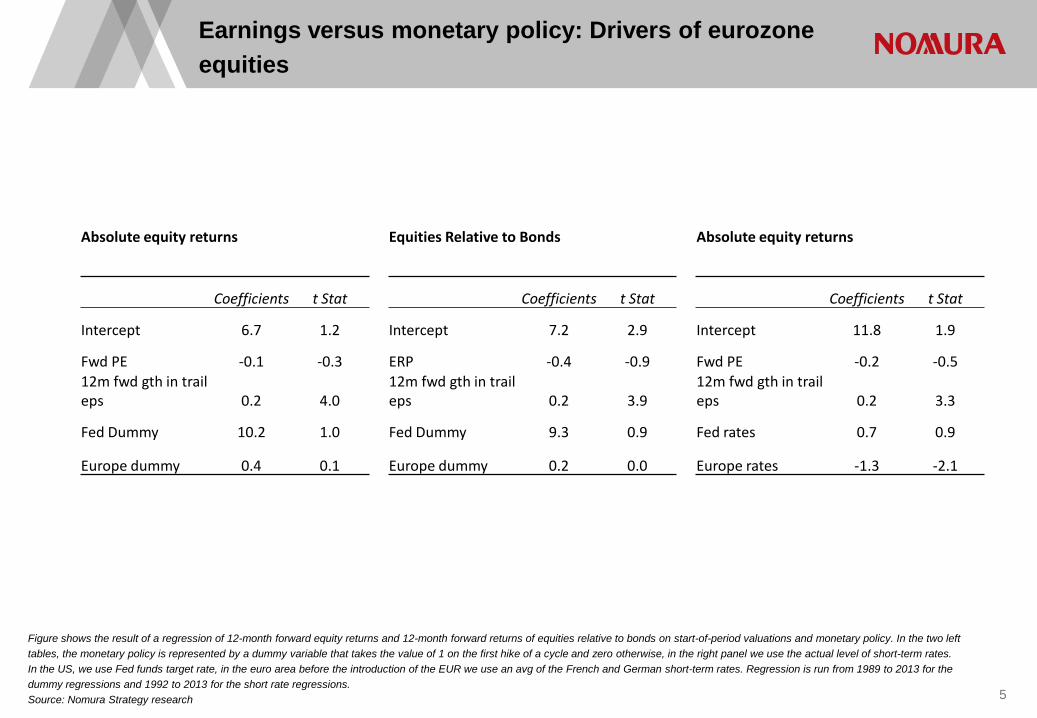

Figure shows the result of a regression of 12-month forward equity returns and 12-month forward returns of equities relative to bonds on start-of-period valuations and monetary policy. In the two left tables, the monetary policy is represented by a dummy variable that takes the value of 1 on the first hike of a cycle and zero otherwise, in the right panel we use the actual level of short-term rates. In the US, we use Fed funds target rate, in the euro area before the introduction of the EUR we use an avg of the French and German short-term rates. Regression is run from 1989 to 2013 for the dummy regressions and 1992 to 2013 for the short rate regressions. Source: Nomura Strategy research

Earnings versus monetary policy: Drivers of eurozone equities

Absolute equity returns Equities Relative to Bonds Absolute equity returns

Coefficients t Stat Coefficients t Stat Coefficients t Stat

Intercept 6.7 1.2 Intercept 7.2 2.9 Intercept 11.8 1.9

Fwd PE -0.1 -0.3 ERP -0.4 -0.9 Fwd PE -0.2 -0.5 12m fwd gth in trail eps 0.2 4.0

12m fwd gth in trail eps 0.2 3.9

12m fwd gth in trail eps 0.2 3.3

Fed Dummy 10.2 1.0 Fed Dummy 9.3 0.9 Fed rates 0.7 0.9

Europe dummy 0.4 0.1 Europe dummy 0.2 0.0 Europe rates -1.3 -2.1

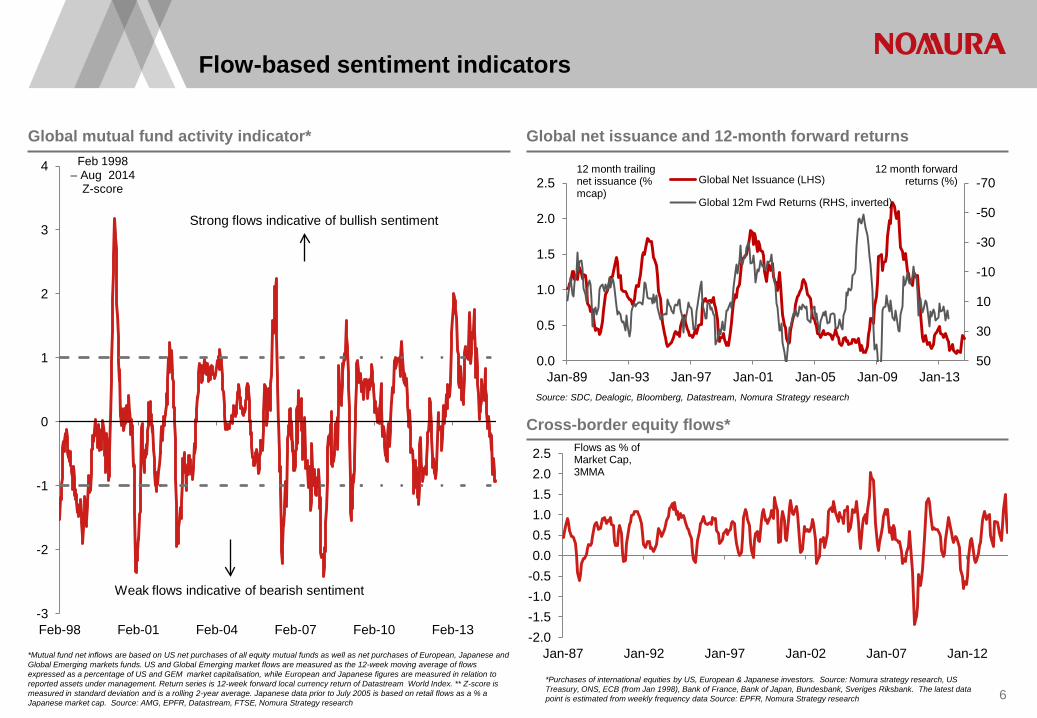

Flow-based sentiment indicators

*Mutual fund net inflows are based on US net purchases of all equity mutual funds as well as net purchases of European, Japanese and Global Emerging markets funds. US and Global Emerging market flows are measured as the 12-week moving average of flows expressed as a percentage of US and GEM market capitalisation, while European and Japanese figures are measured in relation to reported assets under management. Return series is 12-week forward local currency return of Datastream World Index. ** Z-score is measured in standard deviation and is a rolling 2-year average. Japanese data prior to July 2005 is based on retail flows as a % a Japanese market cap. Source: AMG, EPFR, Datastream, FTSE, Nomura Strategy research

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5

Jan-87 Jan-92 Jan-97 Jan-02 Jan-07 Jan-12

Flows as % of Market Cap, 3MMA

-3

-2

-1

0

1

2

3

4

Feb-98 Feb-01 Feb-04 Feb-07 Feb-10 Feb-13

Feb 1998 – Aug 2014

Z-score

6

Global mutual fund activity indicator* Global net issuance and 12-month forward returns

Cross-border equity flows*

Strong flows indicative of bullish sentiment

Weak flows indicative of bearish sentiment

*Purchases of international equities by US, European & Japanese investors. Source: Nomura strategy research, US Treasury, ONS, ECB (from Jan 1998), Bank of France, Bank of Japan, Bundesbank, Sveriges Riksbank. The latest data point is estimated from weekly frequency data Source: EPFR, Nomura Strategy research

-70

-50

-30

-10

10

30

50 0.0

0.5

1.0

1.5

2.0

2.5

Jan-89 Jan-93 Jan-97 Jan-01 Jan-05 Jan-09 Jan-13

12 month forward returns (%)

12 month trailing net issuance (% mcap)

Global Net Issuance (LHS)

Global 12m Fwd Returns (RHS, inverted)

Source: SDC, Dealogic, Bloomberg, Datastream, Nomura Strategy research

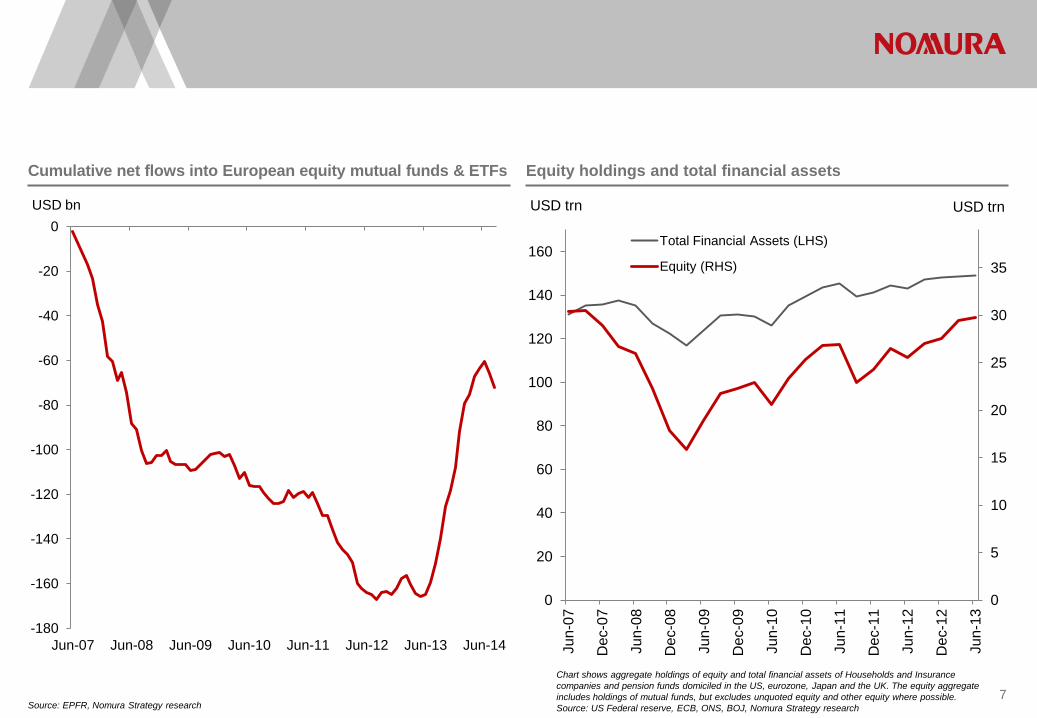

Chart shows aggregate holdings of equity and total financial assets of Households and Insurance companies and pension funds domiciled in the US, eurozone, Japan and the UK. The equity aggregate includes holdings of mutual funds, but excludes unquoted equity and other equity where possible. Source: US Federal reserve, ECB, ONS, BOJ, Nomura Strategy research

Cumulative net flows into European equity mutual funds & ETFs Equity holdings and total financial assets

0

5

10

15

20

25

30

35

0

20

40

60

80

100

120

140

160

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

USD trn USD trn

Total Financial Assets (LHS)

Equity (RHS)

Source: EPFR, Nomura Strategy research 7

-180

-160

-140

-120

-100

-80

-60

-40

-20

0

Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14

USD bn

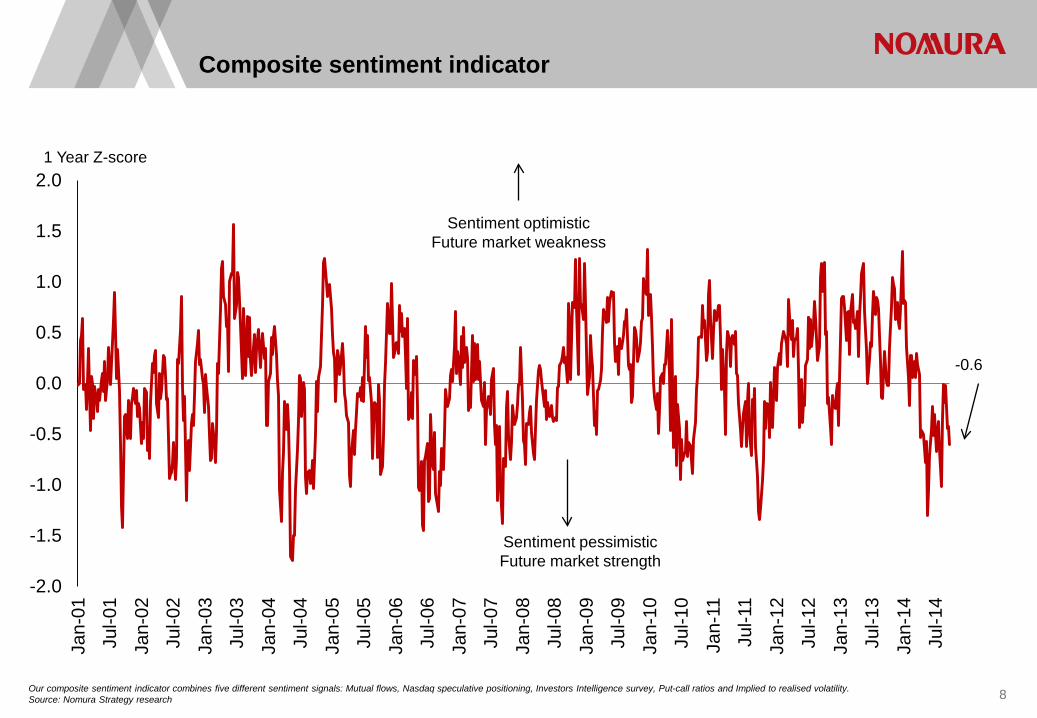

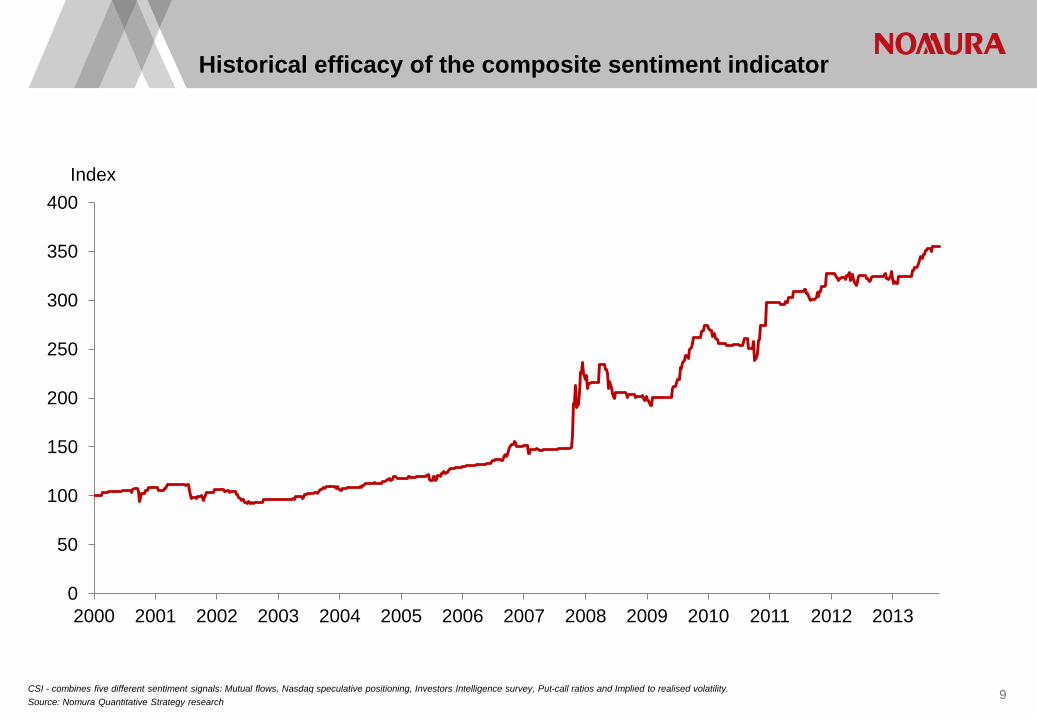

Composite sentiment indicator

Our composite sentiment indicator combines five different sentiment signals: Mutual flows, Nasdaq speculative positioning, Investors Intelligence survey, Put-call ratios and Implied to realised volatility. Source: Nomura Strategy research

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

1 Year Z-score

-0.6

Sentiment optimistic Future market weakness

Sentiment pessimistic Future market strength

8

CSI - combines five different sentiment signals: Mutual flows, Nasdaq speculative positioning, Investors Intelligence survey, Put-call ratios and Implied to realised volatility. Source: Nomura Quantitative Strategy research

Historical efficacy of the composite sentiment indicator

9

0

50

100

150

200

250

300

350

400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Index

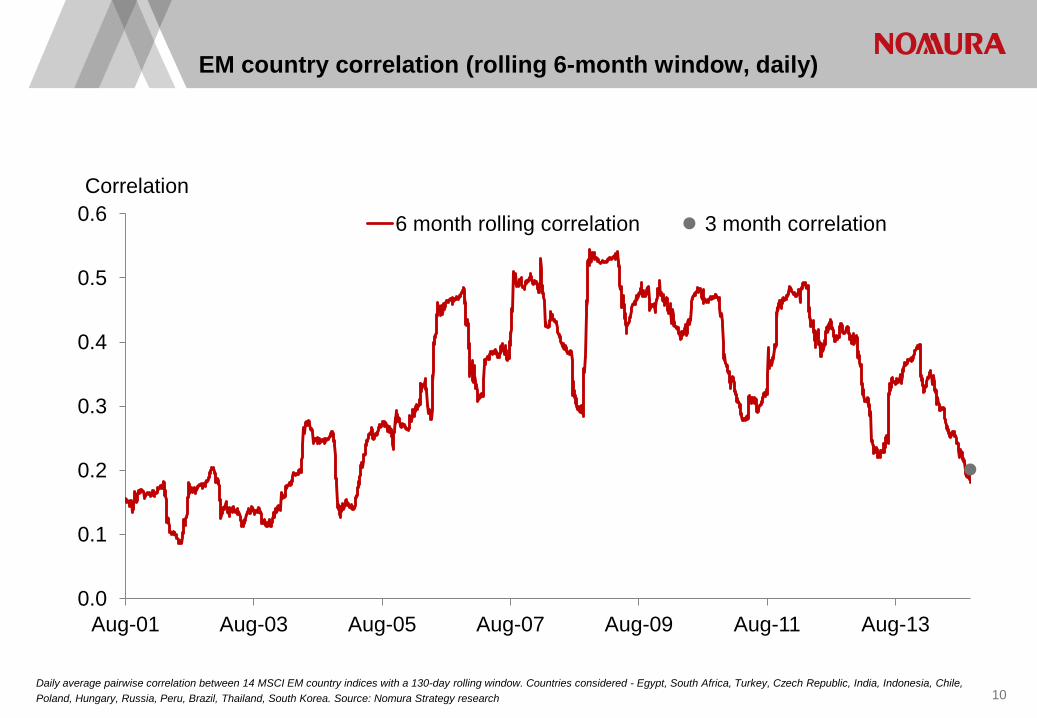

Daily average pairwise correlation between 14 MSCI EM country indices with a 130-day rolling window. Countries considered - Egypt, South Africa, Turkey, Czech Republic, India, Indonesia, Chile, Poland, Hungary, Russia, Peru, Brazil, Thailand, South Korea. Source: Nomura Strategy research

EM country correlation (rolling 6-month window, daily)

10

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Aug-01 Aug-03 Aug-05 Aug-07 Aug-09 Aug-11 Aug-13

Correlation

6 month rolling correlation 3 month correlation

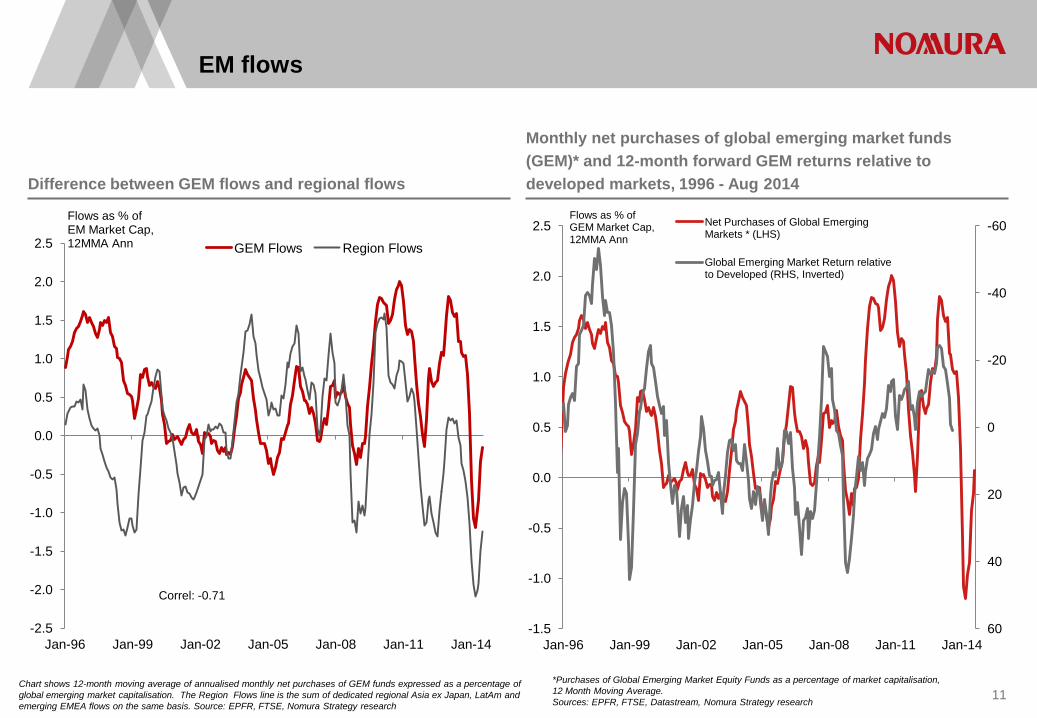

EM flows

Chart shows 12-month moving average of annualised monthly net purchases of GEM funds expressed as a percentage of global emerging market capitalisation. The Region Flows line is the sum of dedicated regional Asia ex Japan, LatAm and emerging EMEA flows on the same basis. Source: EPFR, FTSE, Nomura Strategy research

11

Difference between GEM flows and regional flows

Monthly net purchases of global emerging market funds (GEM)* and 12-month forward GEM returns relative to developed markets, 1996 - Aug 2014

*Purchases of Global Emerging Market Equity Funds as a percentage of market capitalisation, 12 Month Moving Average. Sources: EPFR, FTSE, Datastream, Nomura Strategy research

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Flows as % of EM Market Cap, 12MMA Ann GEM Flows Region Flows

Correl: -0.71

-60

-40

-20

0

20

40

60 -1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Flows as % of GEM Market Cap, 12MMA Ann

Net Purchases of Global Emerging Markets * (LHS)

Global Emerging Market Return relative to Developed (RHS, Inverted)

12 Source: Nomura Quantitative strategy

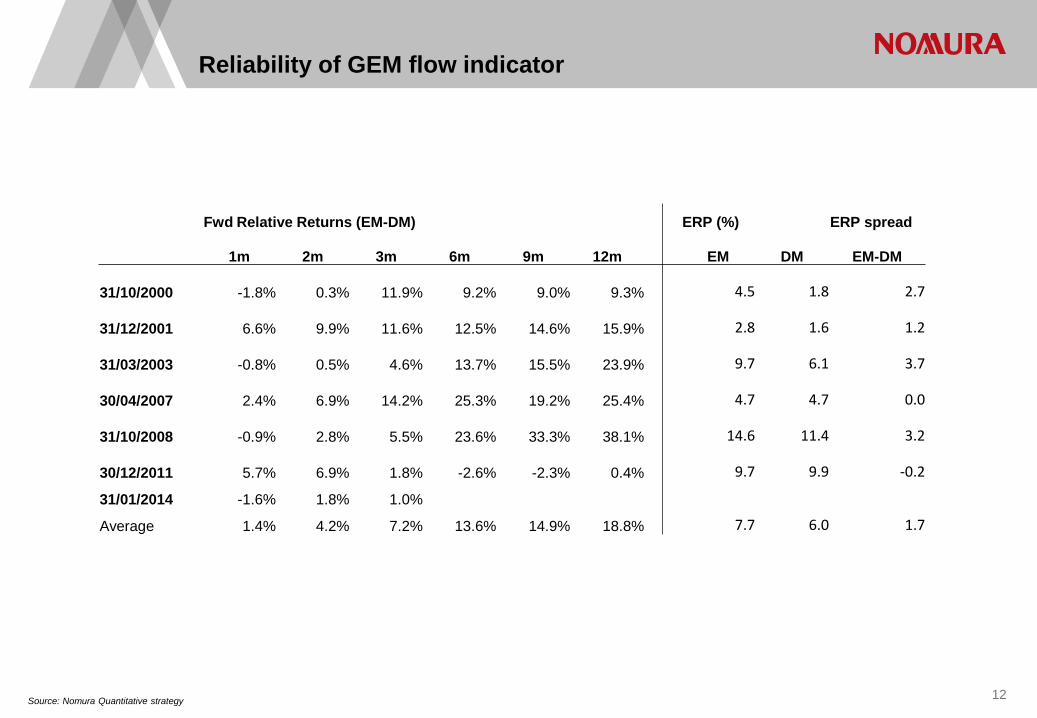

Reliability of GEM flow indicator

Fwd Relative Returns (EM-DM) ERP (%) ERP spread

1m 2m 3m 6m 9m 12m EM DM EM-DM

31/10/2000 -1.8% 0.3% 11.9% 9.2% 9.0% 9.3% 4.5 1.8 2.7

31/12/2001 6.6% 9.9% 11.6% 12.5% 14.6% 15.9% 2.8 1.6 1.2

31/03/2003 -0.8% 0.5% 4.6% 13.7% 15.5% 23.9% 9.7 6.1 3.7

30/04/2007 2.4% 6.9% 14.2% 25.3% 19.2% 25.4% 4.7 4.7 0.0

31/10/2008 -0.9% 2.8% 5.5% 23.6% 33.3% 38.1% 14.6 11.4 3.2

30/12/2011 5.7% 6.9% 1.8% -2.6% -2.3% 0.4% 9.7 9.9 -0.2

31/01/2014 -1.6% 1.8% 1.0%

Average 1.4% 4.2% 7.2% 13.6% 14.9% 18.8% 7.7 6.0 1.7

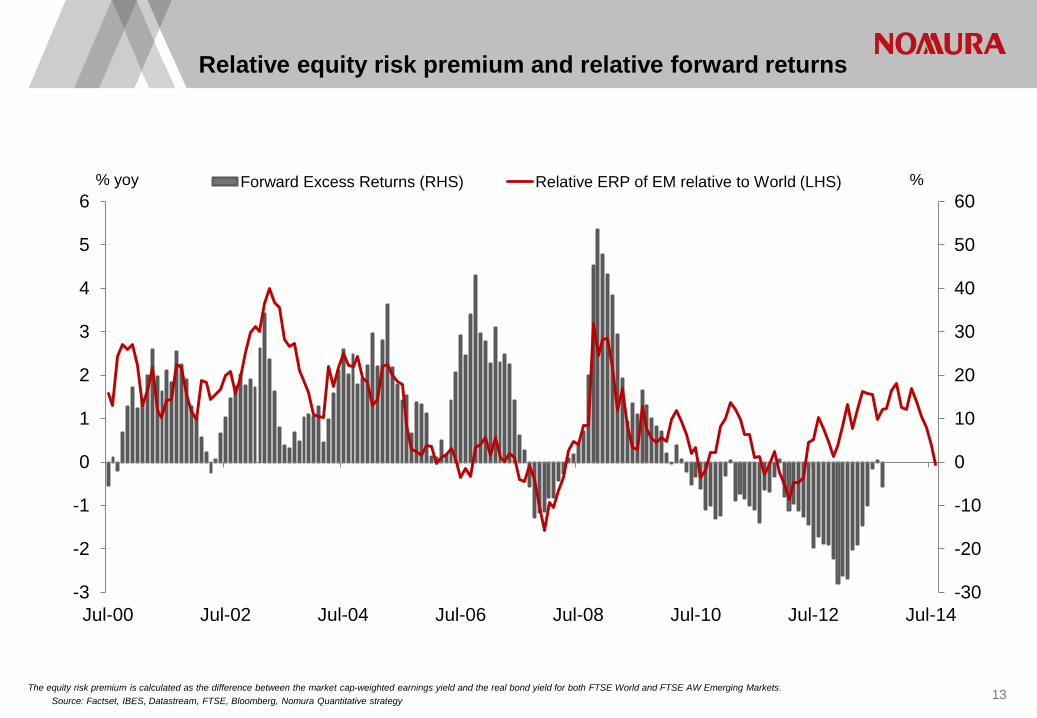

13 The equity risk premium is calculated as the difference between the market cap-weighted earnings yield and the real bond yield for both FTSE World and FTSE AW Emerging Markets. Source: Factset, IBES, Datastream, FTSE, Bloomberg, Nomura Quantitative strategy

Relative equity risk premium and relative forward returns

-30

-20

-10

0

10

20

30

40

50

60

-3

-2

-1

0

1

2

3

4

5

6

Jul-00 Jul-02 Jul-04 Jul-06 Jul-08 Jul-10 Jul-12 Jul-14

% % yoy Forward Excess Returns (RHS) Relative ERP of EM relative to World (LHS)

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Correlation coefficient

Weekly average of absolute pairwise-correlations between returns of different asset classes over a 90-day rolling window. Asset classes considered - FTSE World Index (proxy for developed equities), FTSE EM Index (proxy for EM equities), dollar spot, gold spot, US govt. 10y bond, commodity index, credit spread indices (investment grade and high yield). Source: Nomura Quantitative strategy

14

Multi-asset correlation (90 day) Index volatility - Factor volatility (Global)

Chart shows 75 day rolling realised volatility of the FTSE World index less the average 75-day rolling volatility of Value, Growth, Momentum, Risk and Quality for a global universe. Note that the underlying factor indices are long-short $-neutral. Source: Nomura Quantitative strategy

-4

-3

-2

-1

0

1

2

3

4

5

6

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

%

Are earnings growing in Europe?

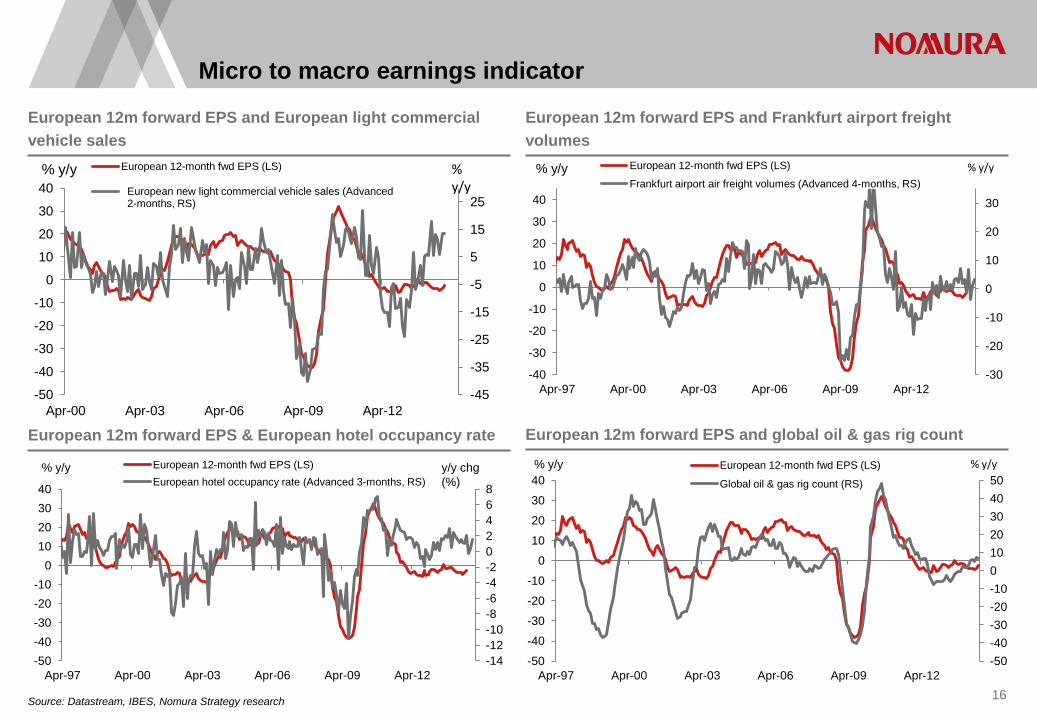

Source: Datastream, IBES, Nomura Strategy research 16

European 12m forward EPS and European light commercial vehicle sales

European 12m forward EPS and Frankfurt airport freight volumes

European 12m forward EPS & European hotel occupancy rate European 12m forward EPS and global oil & gas rig count

Micro to macro earnings indicator

-30

-20

-10

0

10

20

30

-40

-30

-20

-10

0

10

20

30

40

Apr-97 Apr-00 Apr-03 Apr-06 Apr-09 Apr-12

European 12-month fwd EPS (LS)

Frankfurt airport air freight volumes (Advanced 4-months, RS) % y/y % y/y

-14 -12 -10 -8 -6 -4 -2 0 2 4 6 8

-50 -40 -30 -20 -10

0 10 20 30 40

Apr-97 Apr-00 Apr-03 Apr-06 Apr-09 Apr-12

European 12-month fwd EPS (LS) European hotel occupancy rate (Advanced 3-months, RS)

% y/y y/y chg (%)

-50 -40 -30 -20 -10 0 10 20 30 40 50

-50

-40

-30

-20

-10

0

10

20

30

40

Apr-97 Apr-00 Apr-03 Apr-06 Apr-09 Apr-12

European 12-month fwd EPS (LS)

Global oil & gas rig count (RS)

% y/y % y/y

-45

-35

-25

-15

-5

5

15

25

-50

-40

-30

-20

-10

0

10

20

30

40

Apr-00 Apr-03 Apr-06 Apr-09 Apr-12

European 12-month fwd EPS (LS)

European new light commercial vehicle sales (Advanced 2-months, RS)

% y/y % y/y

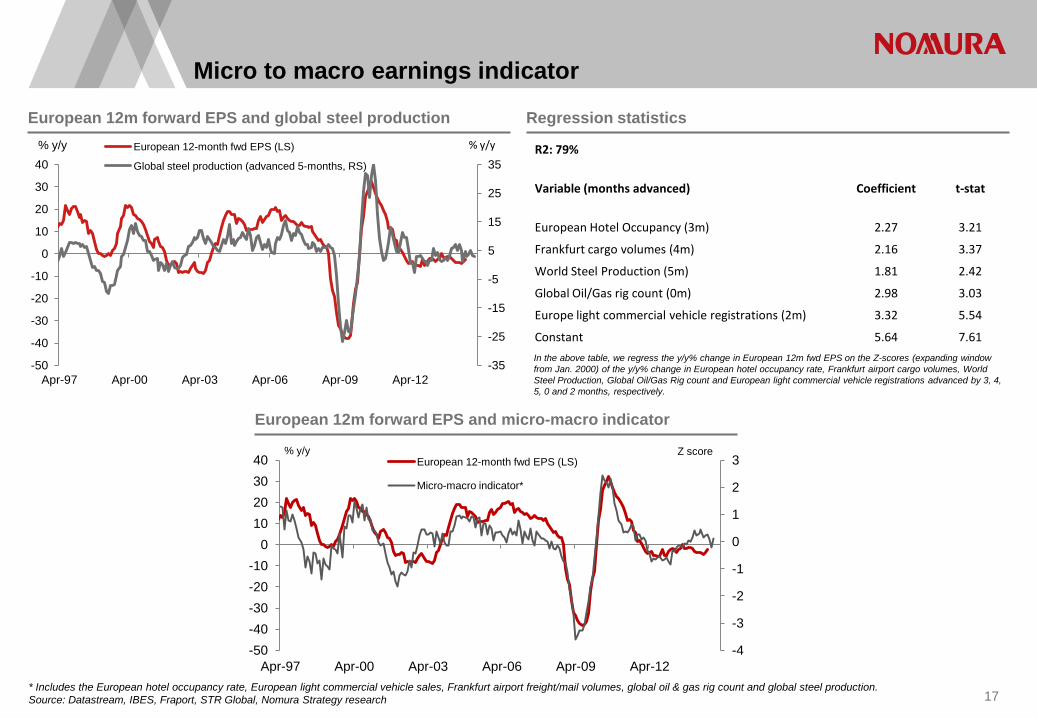

* Includes the European hotel occupancy rate, European light commercial vehicle sales, Frankfurt airport freight/mail volumes, global oil & gas rig count and global steel production. Source: Datastream, IBES, Fraport, STR Global, Nomura Strategy research

European 12m forward EPS and global steel production Regression statistics

R2: 79%

Variable (months advanced) Coefficient t-stat

European Hotel Occupancy (3m) 2.27 3.21

Frankfurt cargo volumes (4m) 2.16 3.37

World Steel Production (5m) 1.81 2.42

Global Oil/Gas rig count (0m) 2.98 3.03

Europe light commercial vehicle registrations (2m) 3.32 5.54

Constant 5.64 7.61 In the above table, we regress the y/y% change in European 12m fwd EPS on the Z-scores (expanding window from Jan. 2000) of the y/y% change in European hotel occupancy rate, Frankfurt airport cargo volumes, World Steel Production, Global Oil/Gas Rig count and European light commercial vehicle registrations advanced by 3, 4, 5, 0 and 2 months, respectively.

European 12m forward EPS and micro-macro indicator

17

Micro to macro earnings indicator

-4

-3

-2

-1

0

1

2

3

-50 -40 -30 -20 -10

0 10 20 30 40

Apr-97 Apr-00 Apr-03 Apr-06 Apr-09 Apr-12

Z score % y/y European 12-month fwd EPS (LS)

Micro-macro indicator*

-35

-25

-15

-5

5

15

25

35

-50

-40

-30

-20

-10

0

10

20

30

40

Apr-97 Apr-00 Apr-03 Apr-06 Apr-09 Apr-12

European 12-month fwd EPS (LS)

Global steel production (advanced 5-months, RS)

% y/y % y/y

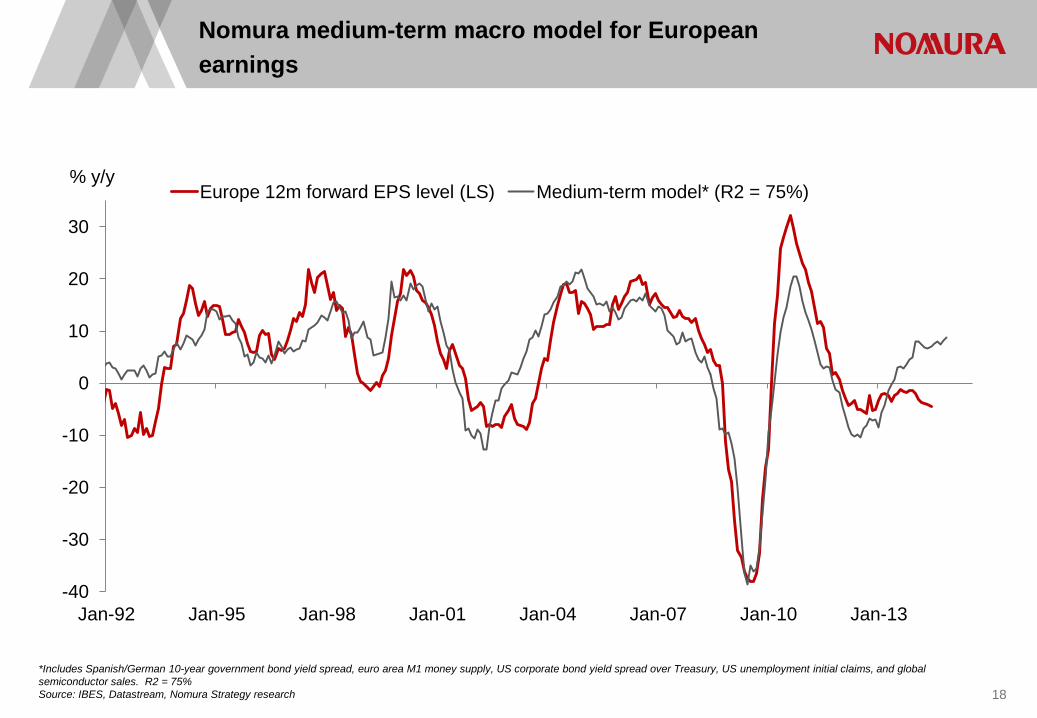

Nomura medium-term macro model for European earnings

18

*Includes Spanish/German 10-year government bond yield spread, euro area M1 money supply, US corporate bond yield spread over Treasury, US unemployment initial claims, and global semiconductor sales. R2 = 75% Source: IBES, Datastream, Nomura Strategy research

-40

-30

-20

-10

0

10

20

30

Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10 Jan-13

% y/y Europe 12m forward EPS level (LS) Medium-term model* (R2 = 75%)

19

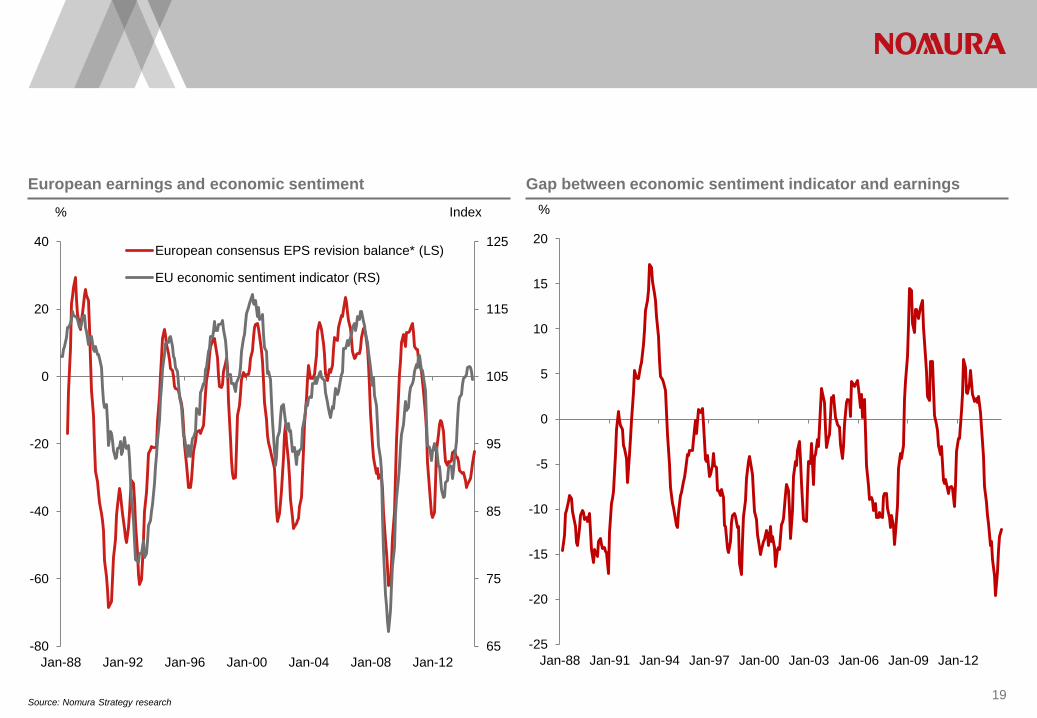

European earnings and economic sentiment Gap between economic sentiment indicator and earnings

Source: Nomura Strategy research

-25

-20

-15

-10

-5

0

5

10

15

20

Jan-88 Jan-91 Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Jan-09 Jan-12

%

65

75

85

95

105

115

125

-80

-60

-40

-20

0

20

40

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12

European consensus EPS revision balance* (LS)

EU economic sentiment indicator (RS)

% Index

Source: Nomura Strategy research 20

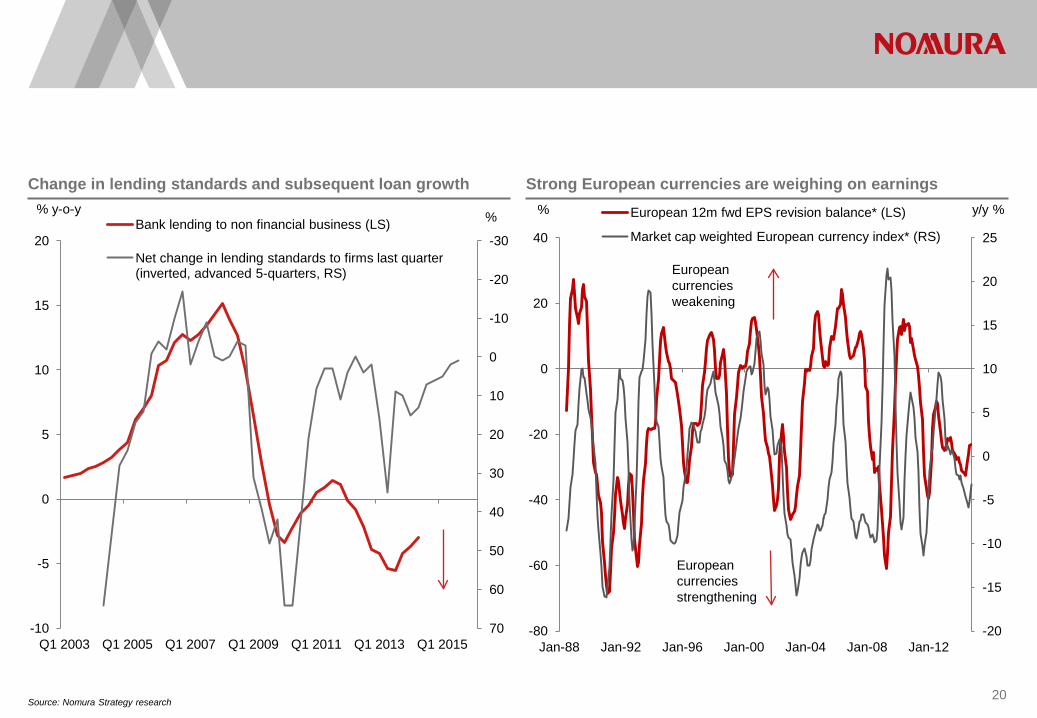

Change in lending standards and subsequent loan growth Strong European currencies are weighing on earnings

-30

-20

-10

0

10

20

30

40

50

60

70 -10

-5

0

5

10

15

20

Q1 2003 Q1 2005 Q1 2007 Q1 2009 Q1 2011 Q1 2013 Q1 2015

% % y-o-y Bank lending to non financial business (LS)

Net change in lending standards to firms last quarter (inverted, advanced 5-quarters, RS)

-20

-15

-10

-5

0

5

10

15

20

25

-80

-60

-40

-20

0

20

40

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12

y/y % % European 12m fwd EPS revision balance* (LS)

Market cap weighted European currency index* (RS)

European currencies strengthening

European currencies weakening

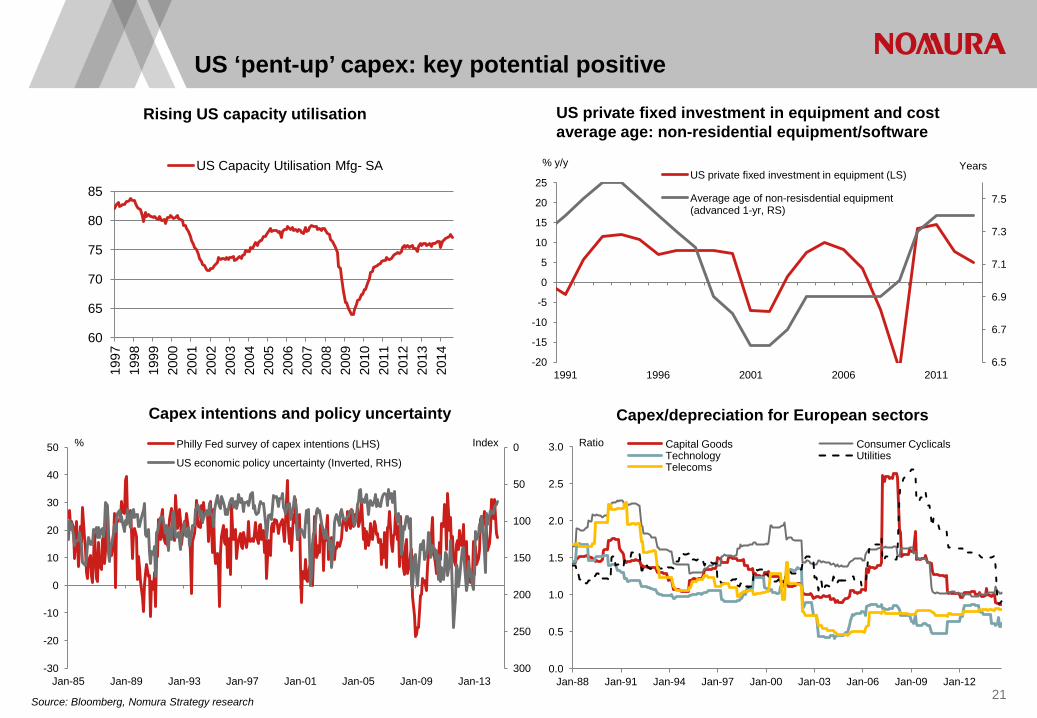

US ‘pent-up’ capex: key potential positive

Source: Bloomberg, Nomura Strategy research

Rising US capacity utilisation US private fixed investment in equipment and cost average age: non-residential equipment/software

21

6.5

6.7

6.9

7.1

7.3

7.5

-20

-15

-10

-5

0

5

10

15

20

25

1991 1996 2001 2006 2011

US private fixed investment in equipment (LS)

Average age of non-resisdential equipment (advanced 1-yr, RS)

Years % y/y

0

50

100

150

200

250

300 -30

-20

-10

0

10

20

30

40

50

Jan-85 Jan-89 Jan-93 Jan-97 Jan-01 Jan-05 Jan-09 Jan-13

Index % Philly Fed survey of capex intentions (LHS)

US economic policy uncertainty (Inverted, RHS)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-88 Jan-91 Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Jan-09 Jan-12

Ratio Capital Goods Consumer Cyclicals Technology Utilities Telecoms

Capex/depreciation for European sectors Capex intentions and policy uncertainty

60

65

70

75

80

85

1997

19

98

1999

20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

US Capacity Utilisation Mfg- SA

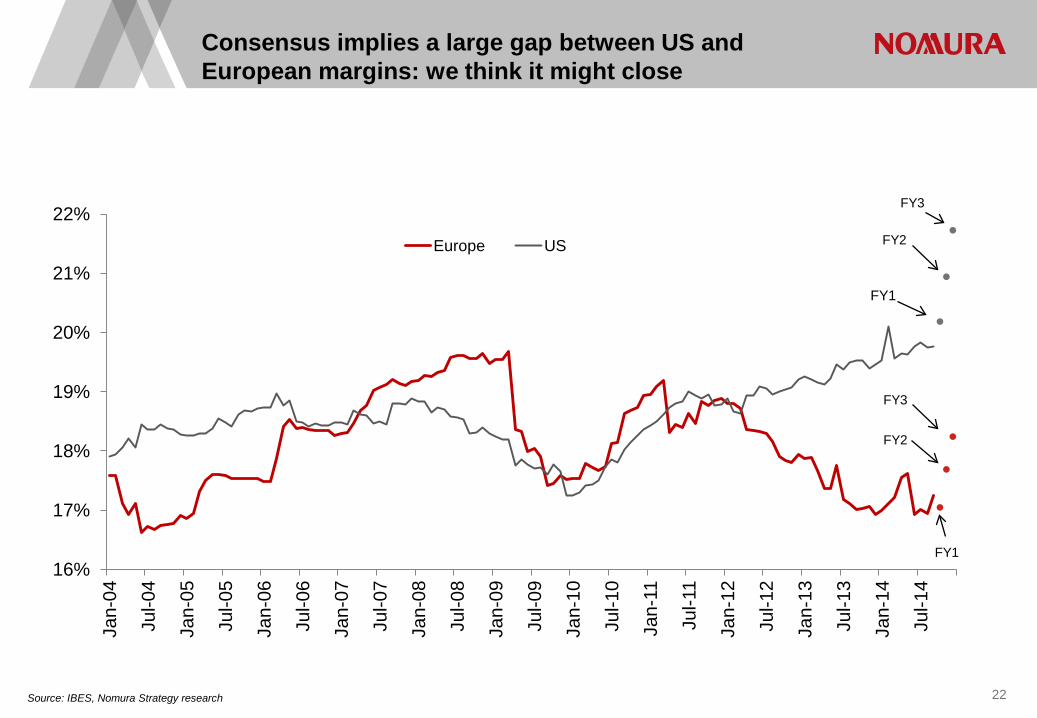

Consensus implies a large gap between US and European margins: we think it might close

22

16%

17%

18%

19%

20%

21%

22%

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Europe US FY2

FY3

FY1

FY2

FY3

FY1

Source: IBES, Nomura Strategy research

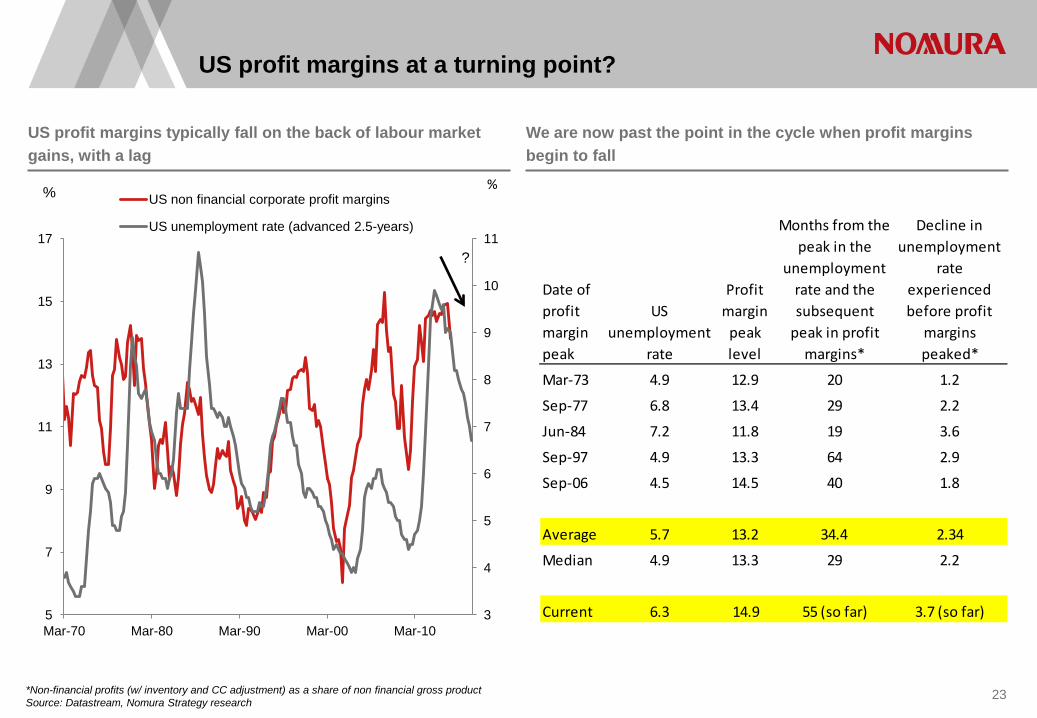

US profit margins at a turning point?

US profit margins typically fall on the back of labour market gains, with a lag

We are now past the point in the cycle when profit margins begin to fall

*Non-financial profits (w/ inventory and CC adjustment) as a share of non financial gross product Source: Datastream, Nomura Strategy research

23

3

4

5

6

7

8

9

10

11

5

7

9

11

13

15

17

Mar-70 Mar-80 Mar-90 Mar-00 Mar-10

US non financial corporate profit margins

US unemployment rate (advanced 2.5-years)

?

% %

Date of profit margin peak

US unemployment

rate

Profit margin

peak level

Months from the peak in the

unemployment rate and the subsequent

peak in profit margins*

Decline in unemployment

rate experienced before profit

margins peaked*

Mar-73 4.9 12.9 20 1.2

Sep-77 6.8 13.4 29 2.2

Jun-84 7.2 11.8 19 3.6

Sep-97 4.9 13.3 64 2.9

Sep-06 4.5 14.5 40 1.8

Average 5.7 13.2 34.4 2.34

Median 4.9 13.3 29 2.2

Current 6.3 14.9 55 (so far) 3.7 (so far)

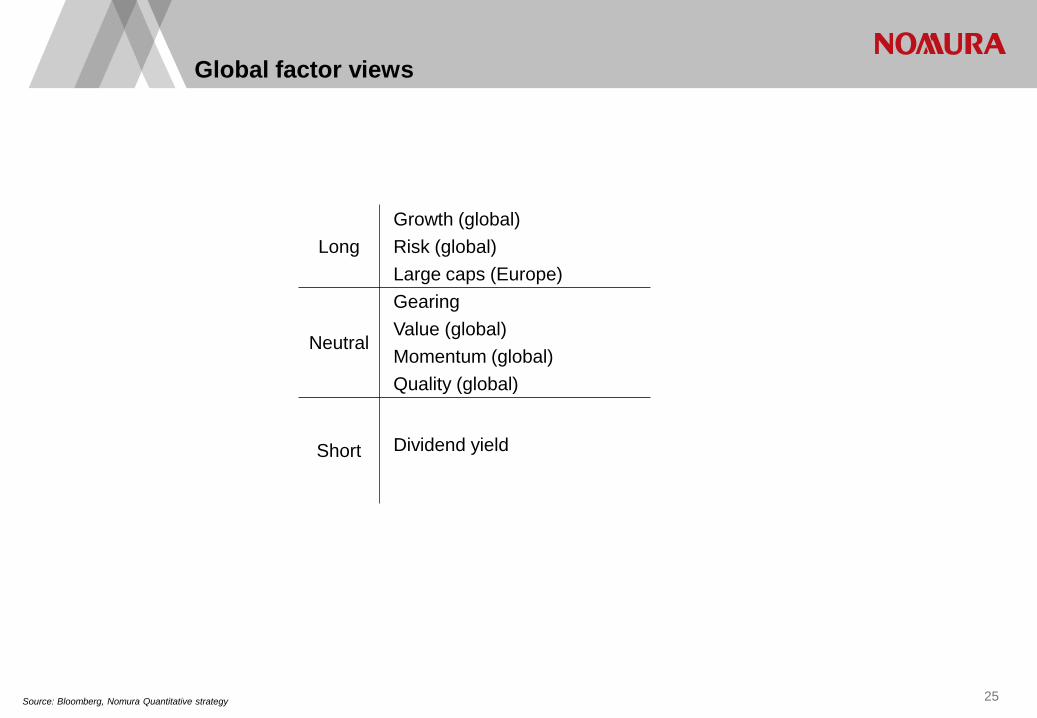

Factor allocation and global quant equity portfolio

Global factor views

Source: Bloomberg, Nomura Quantitative strategy 25

Long Growth (global) Risk (global) Large caps (Europe)

Neutral

Gearing Value (global) Momentum (global) Quality (global)

Short

Dividend yield

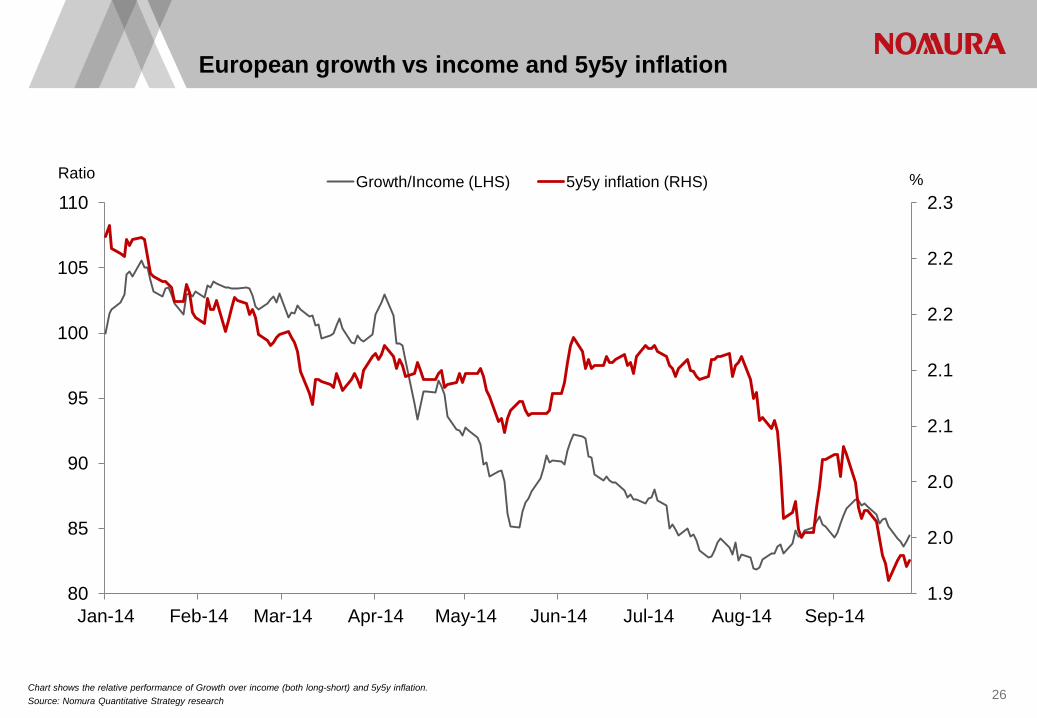

Chart shows the relative performance of Growth over income (both long-short) and 5y5y inflation. Source: Nomura Quantitative Strategy research

European growth vs income and 5y5y inflation

1.9

2.0

2.0

2.1

2.1

2.2

2.2

2.3

80

85

90

95

100

105

110

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

% Ratio Growth/Income (LHS) 5y5y inflation (RHS)

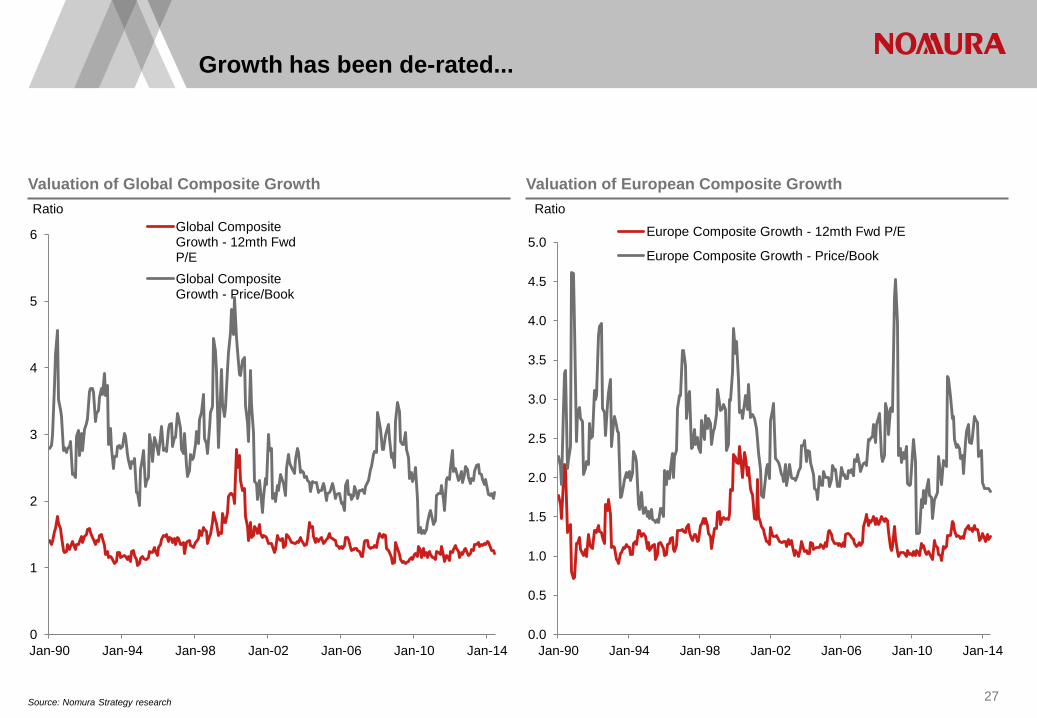

26

Growth has been de-rated...

Source: Nomura Strategy research

Valuation of Global Composite Growth Valuation of European Composite Growth

0

1

2

3

4

5

6

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

Ratio Global Composite Growth - 12mth Fwd P/E Global Composite Growth - Price/Book

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

Ratio

Europe Composite Growth - 12mth Fwd P/E

Europe Composite Growth - Price/Book

27

28

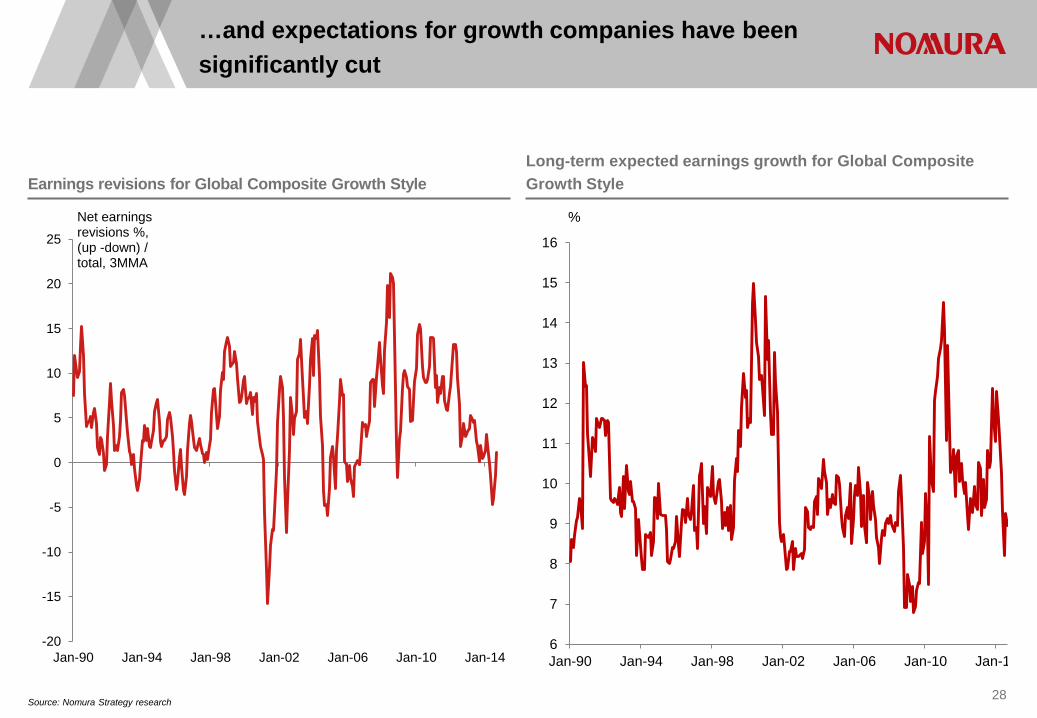

Earnings revisions for Global Composite Growth Style Long-term expected earnings growth for Global Composite Growth Style

6

7

8

9

10

11

12

13

14

15

16

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-1

%

Source: Nomura Strategy research

…and expectations for growth companies have been significantly cut

-20

-15

-10

-5

0

5

10

15

20

25

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

Net earnings revisions %, (up -down) / total, 3MMA

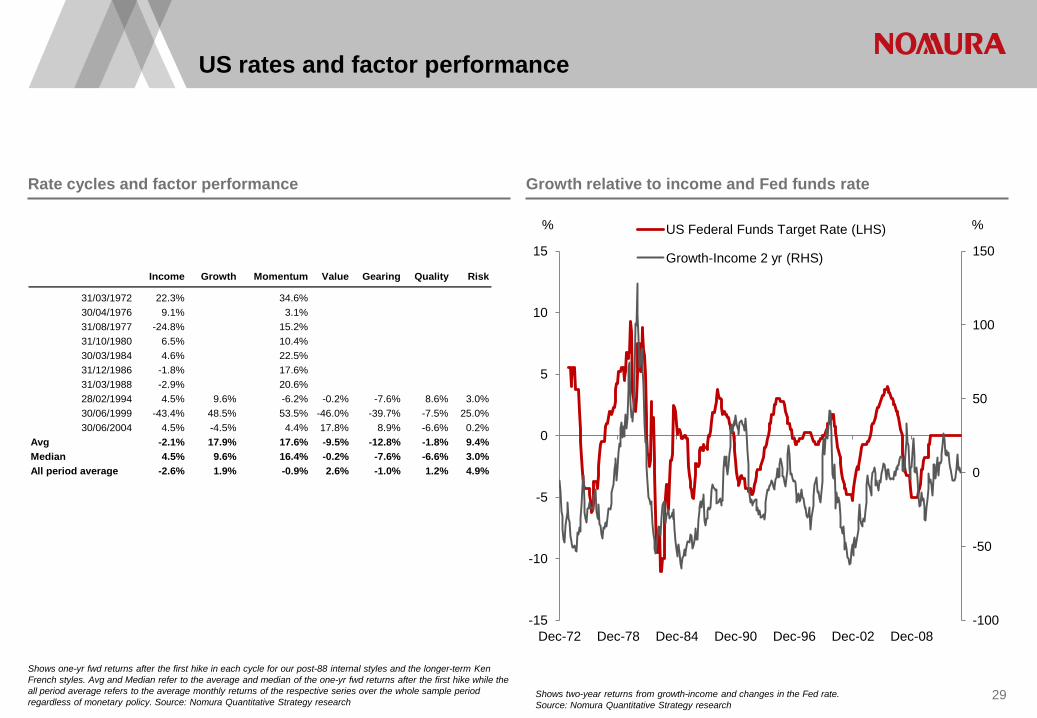

US rates and factor performance

Shows one-yr fwd returns after the first hike in each cycle for our post-88 internal styles and the longer-term Ken French styles. Avg and Median refer to the average and median of the one-yr fwd returns after the first hike while the all period average refers to the average monthly returns of the respective series over the whole sample period regardless of monetary policy. Source: Nomura Quantitative Strategy research 29

Rate cycles and factor performance Growth relative to income and Fed funds rate

Income Growth Momentum Value Gearing Quality Risk

31/03/1972 22.3% 34.6%30/04/1976 9.1% 3.1%31/08/1977 -24.8% 15.2%31/10/1980 6.5% 10.4%30/03/1984 4.6% 22.5%31/12/1986 -1.8% 17.6%31/03/1988 -2.9% 20.6%28/02/1994 4.5% 9.6% -6.2% -0.2% -7.6% 8.6% 3.0%30/06/1999 -43.4% 48.5% 53.5% -46.0% -39.7% -7.5% 25.0%30/06/2004 4.5% -4.5% 4.4% 17.8% 8.9% -6.6% 0.2%

Avg -2.1% 17.9% 17.6% -9.5% -12.8% -1.8% 9.4%Median 4.5% 9.6% 16.4% -0.2% -7.6% -6.6% 3.0%All period average -2.6% 1.9% -0.9% 2.6% -1.0% 1.2% 4.9%

-100

-50

0

50

100

150

-15

-10

-5

0

5

10

15

Dec-72 Dec-78 Dec-84 Dec-90 Dec-96 Dec-02 Dec-08

% % US Federal Funds Target Rate (LHS)

Growth-Income 2 yr (RHS)

Shows two-year returns from growth-income and changes in the Fed rate. Source: Nomura Quantitative Strategy research

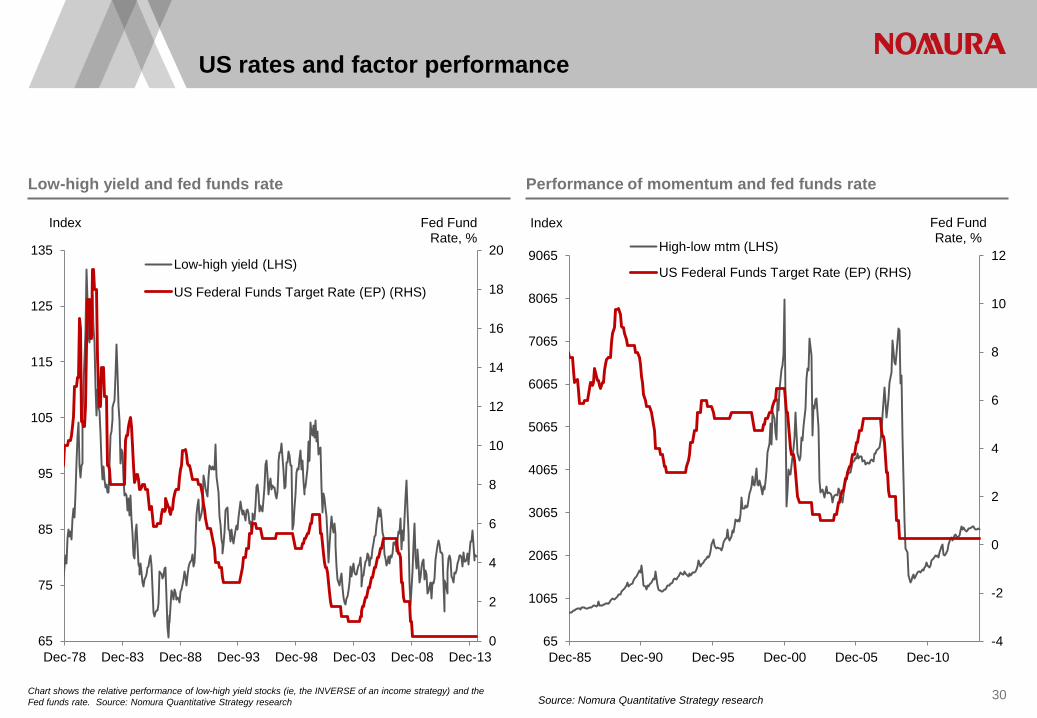

US rates and factor performance

Chart shows the relative performance of low-high yield stocks (ie, the INVERSE of an income strategy) and the Fed funds rate. Source: Nomura Quantitative Strategy research 30

Low-high yield and fed funds rate Performance of momentum and fed funds rate

0

2

4

6

8

10

12

14

16

18

20

65

75

85

95

105

115

125

135

Dec-78 Dec-83 Dec-88 Dec-93 Dec-98 Dec-03 Dec-08 Dec-13

Fed Fund Rate, %

Index

Low-high yield (LHS)

US Federal Funds Target Rate (EP) (RHS)

-4

-2

0

2

4

6

8

10

12

65

1065

2065

3065

4065

5065

6065

7065

8065

9065

Dec-85 Dec-90 Dec-95 Dec-00 Dec-05 Dec-10

Fed Fund Rate, %

Index

High-low mtm (LHS)

US Federal Funds Target Rate (EP) (RHS)

Source: Nomura Quantitative Strategy research

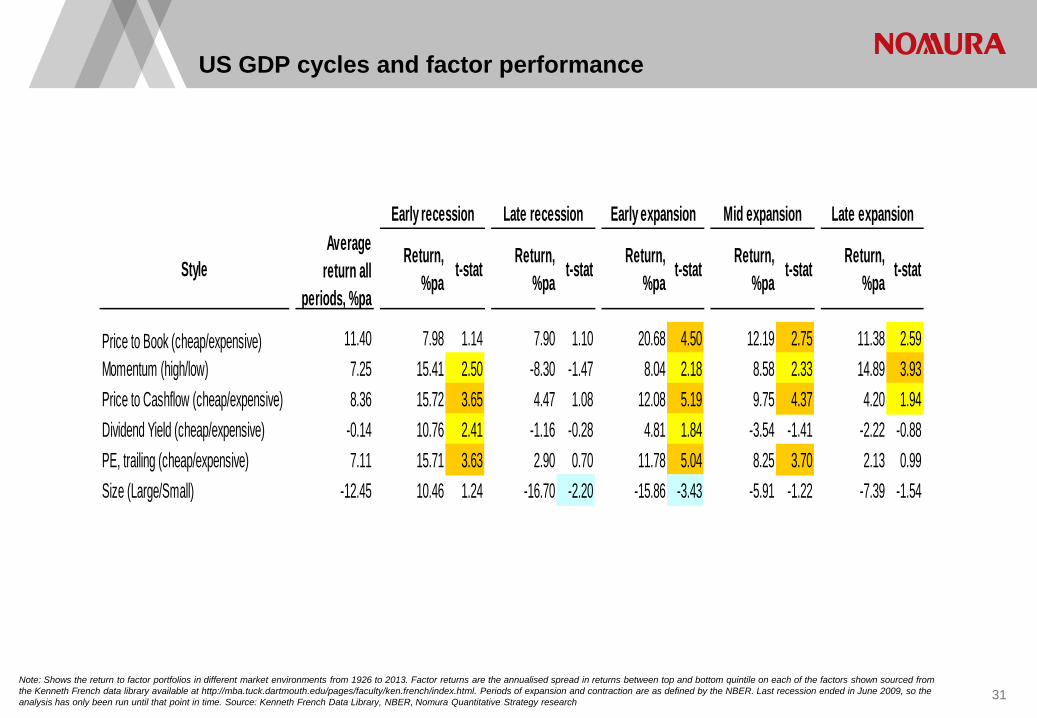

US GDP cycles and factor performance

31 Note: Shows the return to factor portfolios in different market environments from 1926 to 2013. Factor returns are the annualised spread in returns between top and bottom quintile on each of the factors shown sourced from the Kenneth French data library available at http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/index.html. Periods of expansion and contraction are as defined by the NBER. Last recession ended in June 2009, so the analysis has only been run until that point in time. Source: Kenneth French Data Library, NBER, Nomura Quantitative Strategy research

StyleAverage

return all periods, %pa

Return, %pa t-stat Return,

%pa t-stat Return, %pa t-stat Return,

%pa t-stat Return, %pa t-stat

Price to Book (cheap/expensive) 11.40 7.98 1.14 7.90 1.10 20.68 4.50 12.19 2.75 11.38 2.59Momentum (high/low) 7.25 15.41 2.50 -8.30 -1.47 8.04 2.18 8.58 2.33 14.89 3.93Price to Cashflow (cheap/expensive) 8.36 15.72 3.65 4.47 1.08 12.08 5.19 9.75 4.37 4.20 1.94Dividend Yield (cheap/expensive) -0.14 10.76 2.41 -1.16 -0.28 4.81 1.84 -3.54 -1.41 -2.22 -0.88PE, trailing (cheap/expensive) 7.11 15.71 3.63 2.90 0.70 11.78 5.04 8.25 3.70 2.13 0.99Size (Large/Small) -12.45 10.46 1.24 -16.70 -2.20 -15.86 -3.43 -5.91 -1.22 -7.39 -1.54

Early recession Late recession Early expansion Mid expansion Late expansion

32

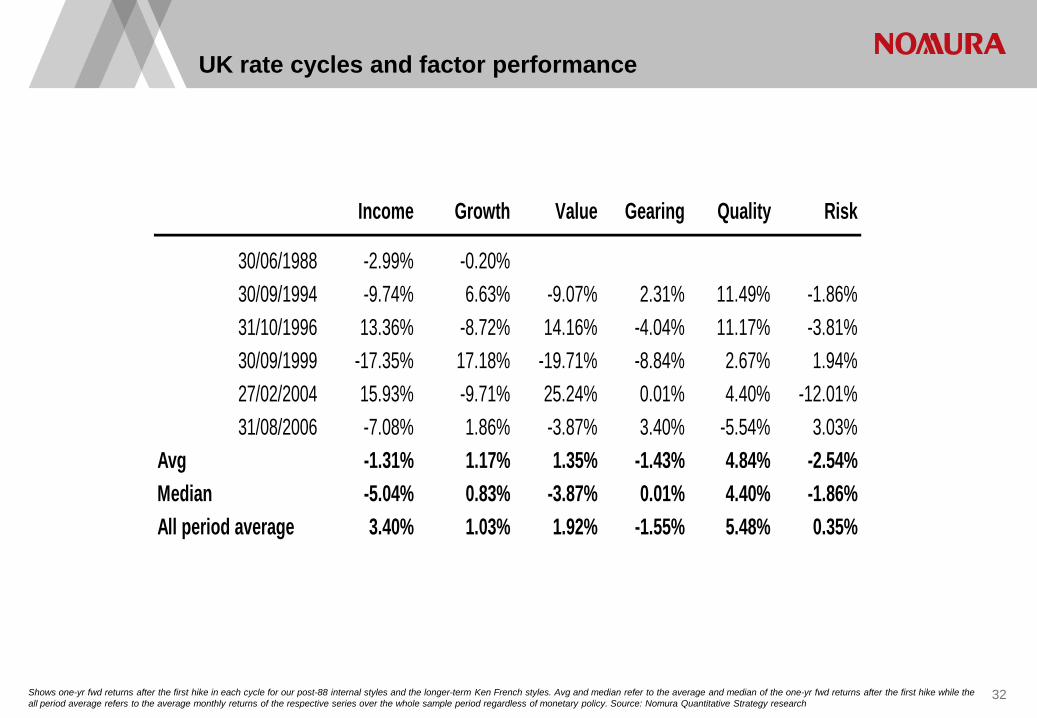

UK rate cycles and factor performance

Income Growth Value Gearing Quality Risk

30/06/1988 -2.99% -0.20%30/09/1994 -9.74% 6.63% -9.07% 2.31% 11.49% -1.86%31/10/1996 13.36% -8.72% 14.16% -4.04% 11.17% -3.81%30/09/1999 -17.35% 17.18% -19.71% -8.84% 2.67% 1.94%27/02/2004 15.93% -9.71% 25.24% 0.01% 4.40% -12.01%31/08/2006 -7.08% 1.86% -3.87% 3.40% -5.54% 3.03%

Avg -1.31% 1.17% 1.35% -1.43% 4.84% -2.54%Median -5.04% 0.83% -3.87% 0.01% 4.40% -1.86%All period average 3.40% 1.03% 1.92% -1.55% 5.48% 0.35%

Shows one-yr fwd returns after the first hike in each cycle for our post-88 internal styles and the longer-term Ken French styles. Avg and median refer to the average and median of the one-yr fwd returns after the first hike while the all period average refers to the average monthly returns of the respective series over the whole sample period regardless of monetary policy. Source: Nomura Quantitative Strategy research

33 Source: Nomura Quantitative Strategy research

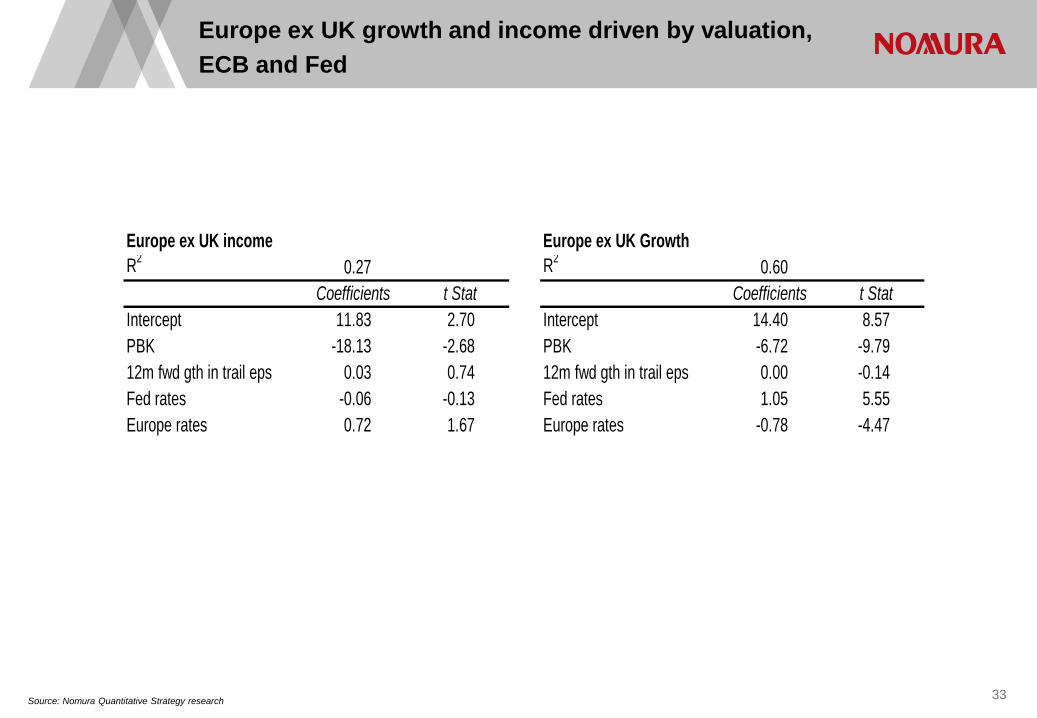

Europe ex UK growth and income driven by valuation, ECB and Fed

Europe ex UK income Europe ex UK GrowthR2 0.27 R2 0.60

Intercept 11.83 2.70 Intercept 14.40 8.57PBK -18.13 -2.68 PBK -6.72 -9.7912m fwd gth in trail eps 0.03 0.74 12m fwd gth in trail eps 0.00 -0.14Fed rates -0.06 -0.13 Fed rates 1.05 5.55Europe rates 0.72 1.67 Europe rates -0.78 -4.47

Coefficients Coefficientst Stat t Stat

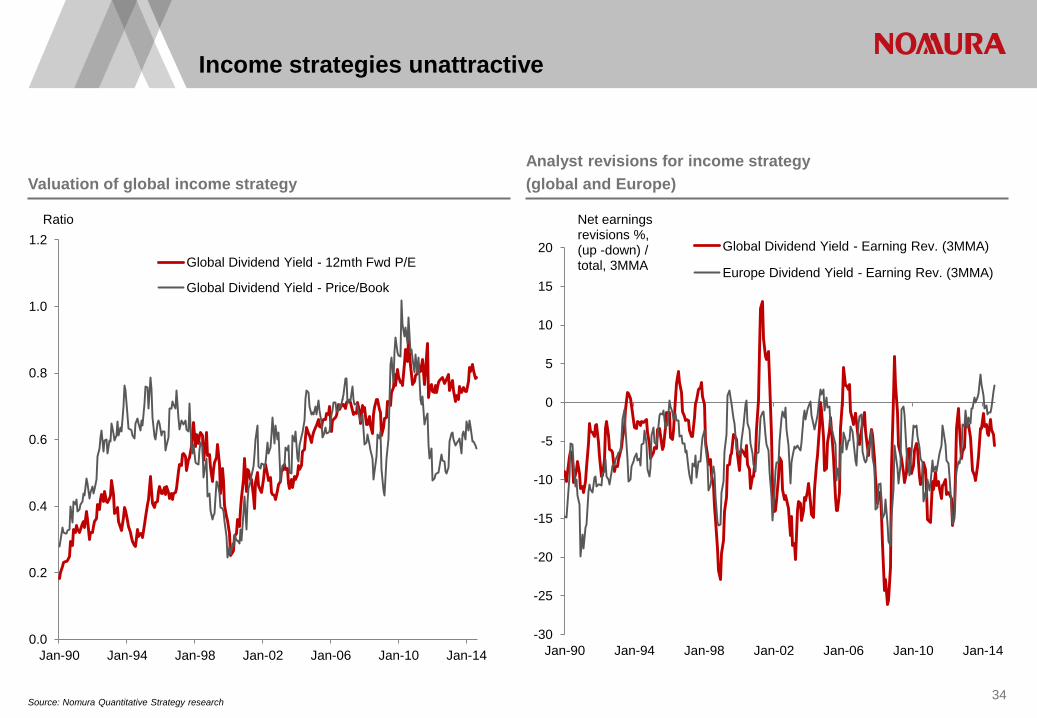

Income strategies unattractive

Source: Nomura Quantitative Strategy research 34

Valuation of global income strategy Analyst revisions for income strategy (global and Europe)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

Ratio

Global Dividend Yield - 12mth Fwd P/E

Global Dividend Yield - Price/Book

-30

-25

-20

-15

-10

-5

0

5

10

15

20

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

Net earnings revisions %, (up -down) / total, 3MMA

Global Dividend Yield - Earning Rev. (3MMA)

Europe Dividend Yield - Earning Rev. (3MMA)

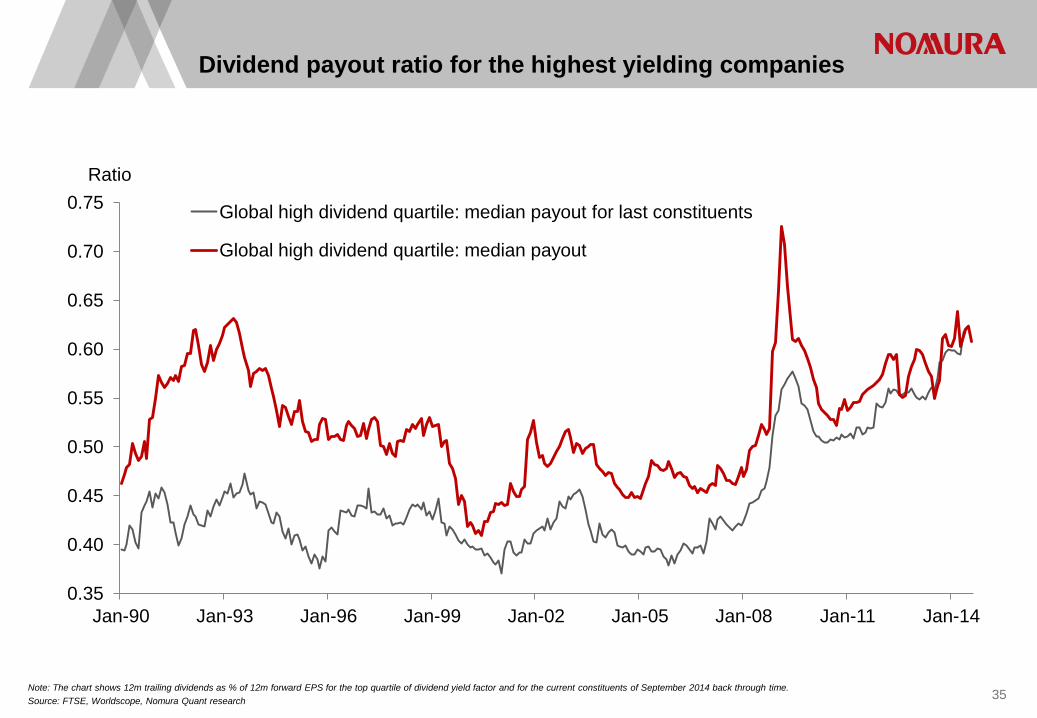

35 Note: The chart shows 12m trailing dividends as % of 12m forward EPS for the top quartile of dividend yield factor and for the current constituents of September 2014 back through time. Source: FTSE, Worldscope, Nomura Quant research

Dividend payout ratio for the highest yielding companies

0.35

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Ratio

Global high dividend quartile: median payout for last constituents

Global high dividend quartile: median payout

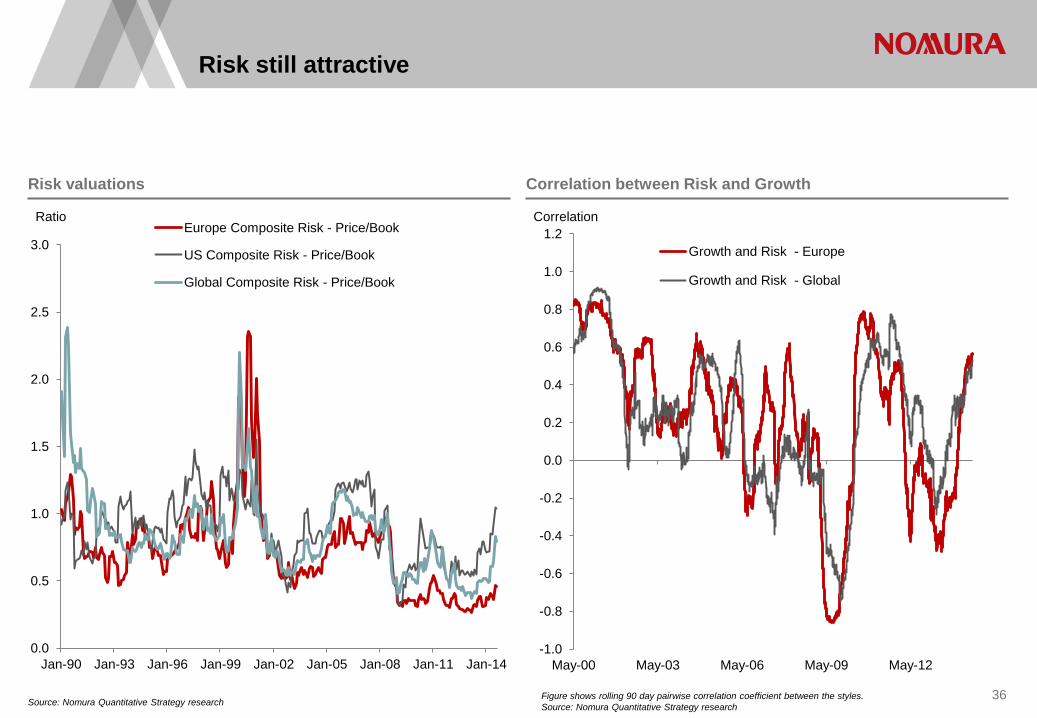

Source: Nomura Quantitative Strategy research 36

Risk valuations Correlation between Risk and Growth

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Ratio Europe Composite Risk - Price/Book

US Composite Risk - Price/Book

Global Composite Risk - Price/Book

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

May-00 May-03 May-06 May-09 May-12

Correlation

Growth and Risk - Europe

Growth and Risk - Global

Figure shows rolling 90 day pairwise correlation coefficient between the styles. Source: Nomura Quantitative Strategy research

Risk still attractive

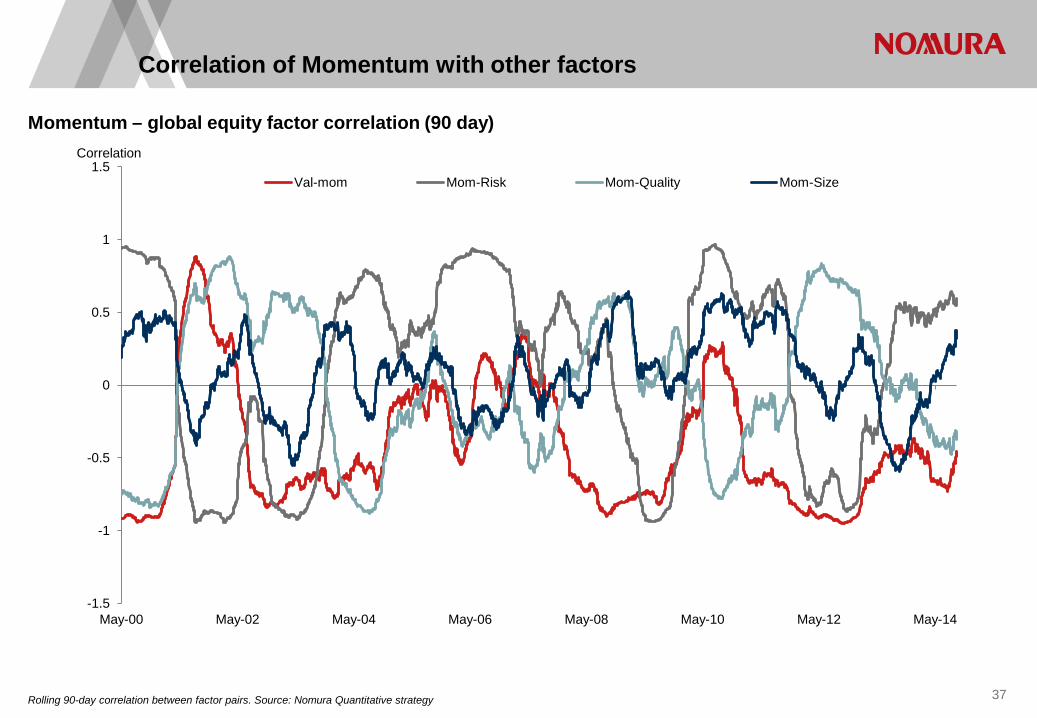

37 Rolling 90-day correlation between factor pairs. Source: Nomura Quantitative strategy

Correlation of Momentum with other factors

Momentum – global equity factor correlation (90 day)

-1.5

-1

-0.5

0

0.5

1

1.5

May-00 May-02 May-04 May-06 May-08 May-10 May-12 May-14

Correlation

Val-mom Mom-Risk Mom-Quality Mom-Size

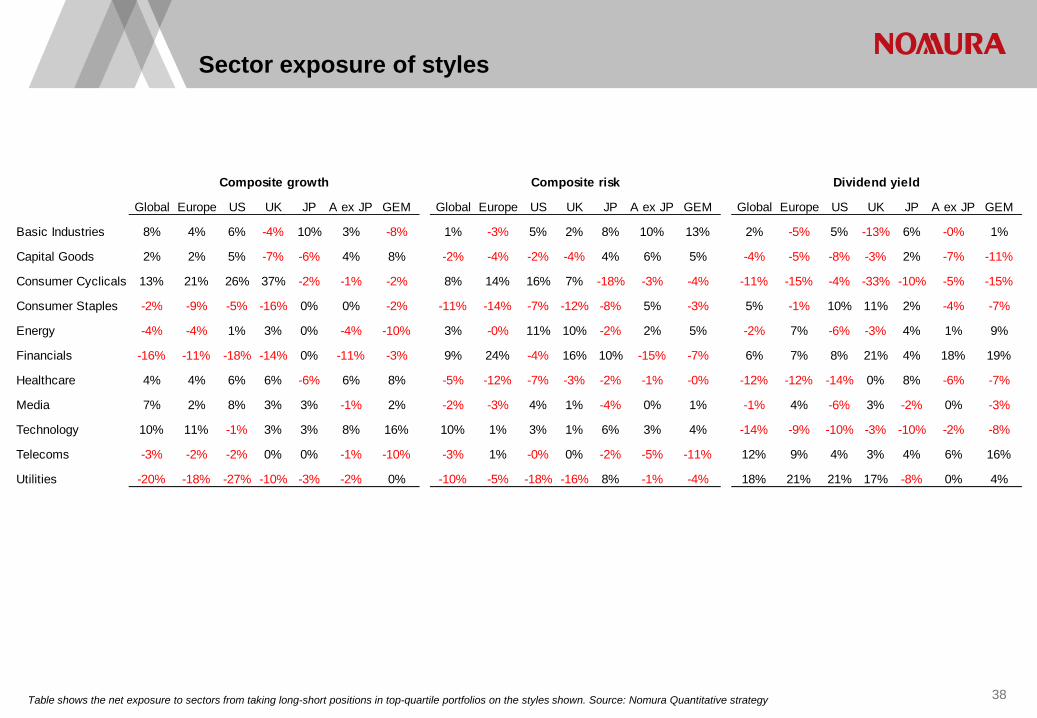

Table shows the net exposure to sectors from taking long-short positions in top-quartile portfolios on the styles shown. Source: Nomura Quantitative strategy

Sector exposure of styles

38

Global Europe US UK JP A ex JP GEM Global Europe US UK JP A ex JP GEM Global Europe US UK JP A ex JP GEM

Basic Industries 8% 4% 6% -4% 10% 3% -8% 1% -3% 5% 2% 8% 10% 13% 2% -5% 5% -13% 6% -0% 1%

Capital Goods 2% 2% 5% -7% -6% 4% 8% -2% -4% -2% -4% 4% 6% 5% -4% -5% -8% -3% 2% -7% -11%

Consumer Cyclicals 13% 21% 26% 37% -2% -1% -2% 8% 14% 16% 7% -18% -3% -4% -11% -15% -4% -33% -10% -5% -15%

Consumer Staples -2% -9% -5% -16% 0% 0% -2% -11% -14% -7% -12% -8% 5% -3% 5% -1% 10% 11% 2% -4% -7%

Energy -4% -4% 1% 3% 0% -4% -10% 3% -0% 11% 10% -2% 2% 5% -2% 7% -6% -3% 4% 1% 9%

Financials -16% -11% -18% -14% 0% -11% -3% 9% 24% -4% 16% 10% -15% -7% 6% 7% 8% 21% 4% 18% 19%

Healthcare 4% 4% 6% 6% -6% 6% 8% -5% -12% -7% -3% -2% -1% -0% -12% -12% -14% 0% 8% -6% -7%

Media 7% 2% 8% 3% 3% -1% 2% -2% -3% 4% 1% -4% 0% 1% -1% 4% -6% 3% -2% 0% -3%

Technology 10% 11% -1% 3% 3% 8% 16% 10% 1% 3% 1% 6% 3% 4% -14% -9% -10% -3% -10% -2% -8%

Telecoms -3% -2% -2% 0% 0% -1% -10% -3% 1% -0% 0% -2% -5% -11% 12% 9% 4% 3% 4% 6% 16%

Utilities -20% -18% -27% -10% -3% -2% 0% -10% -5% -18% -16% 8% -1% -4% 18% 21% 21% 17% -8% 0% 4%

Composite growth Composite risk Dividend yield

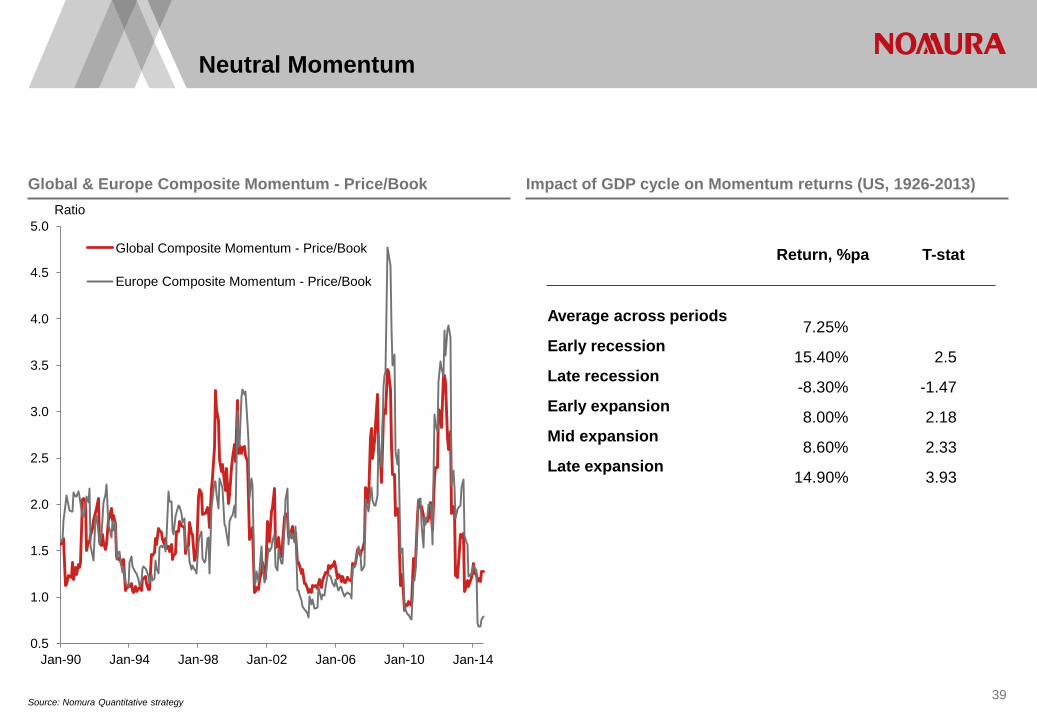

Neutral Momentum

Source: Nomura Quantitative strategy 39

Global & Europe Composite Momentum - Price/Book Impact of GDP cycle on Momentum returns (US, 1926-2013)

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

Ratio

Global Composite Momentum - Price/Book

Europe Composite Momentum - Price/Book

Return, %pa T-stat Average across periods

7.25% Early recession

15.40% 2.5 Late recession

-8.30% -1.47 Early expansion

8.00% 2.18 Mid expansion

8.60% 2.33 Late expansion

14.90% 3.93

40 Source: Nomura Quantitative strategy

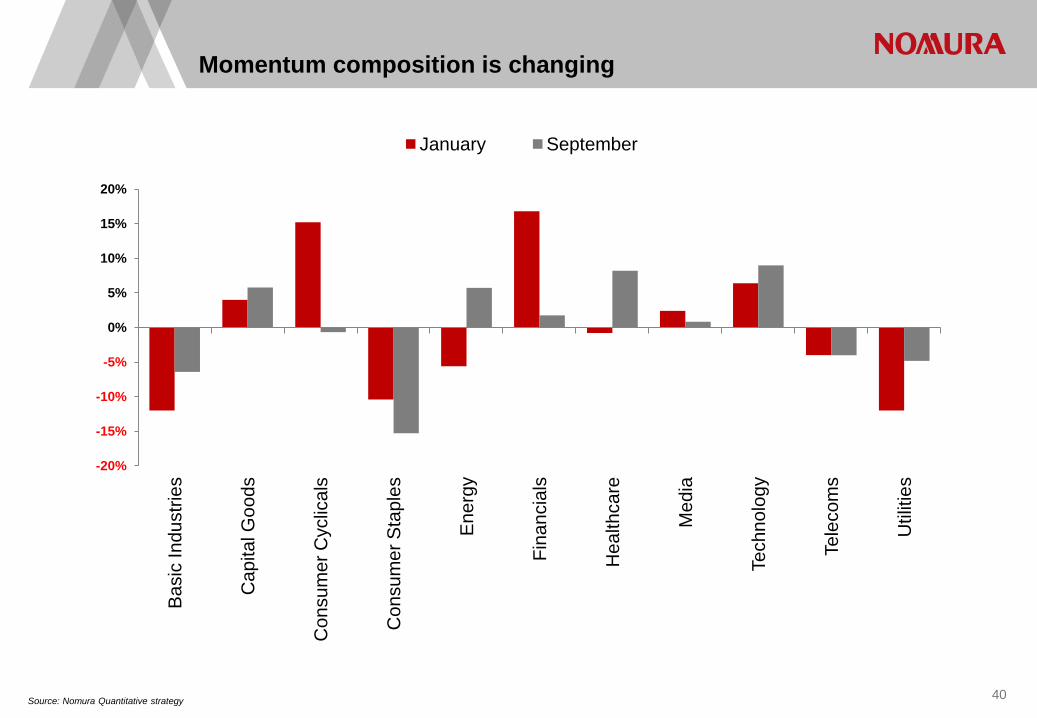

Momentum composition is changing

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20% B

asic

Indu

strie

s

Cap

ital G

oods

Con

sum

er C

yclic

als

Con

sum

er S

tapl

es

Ene

rgy

Fina

ncia

ls

Hea

lthca

re

Med

ia

Tech

nolo

gy

Tele

com

s

Util

ities

January September

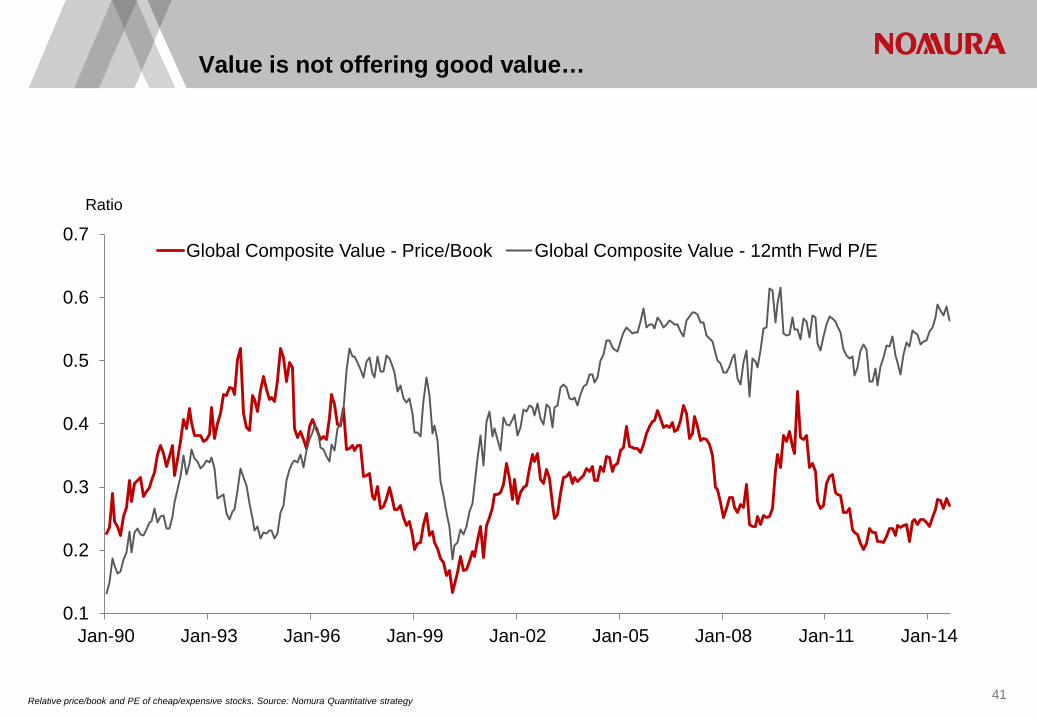

41 Relative price/book and PE of cheap/expensive stocks. Source: Nomura Quantitative strategy

Value is not offering good value…

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Ratio

Global Composite Value - Price/Book Global Composite Value - 12mth Fwd P/E

42 Source: Nomura Quantitative strategy

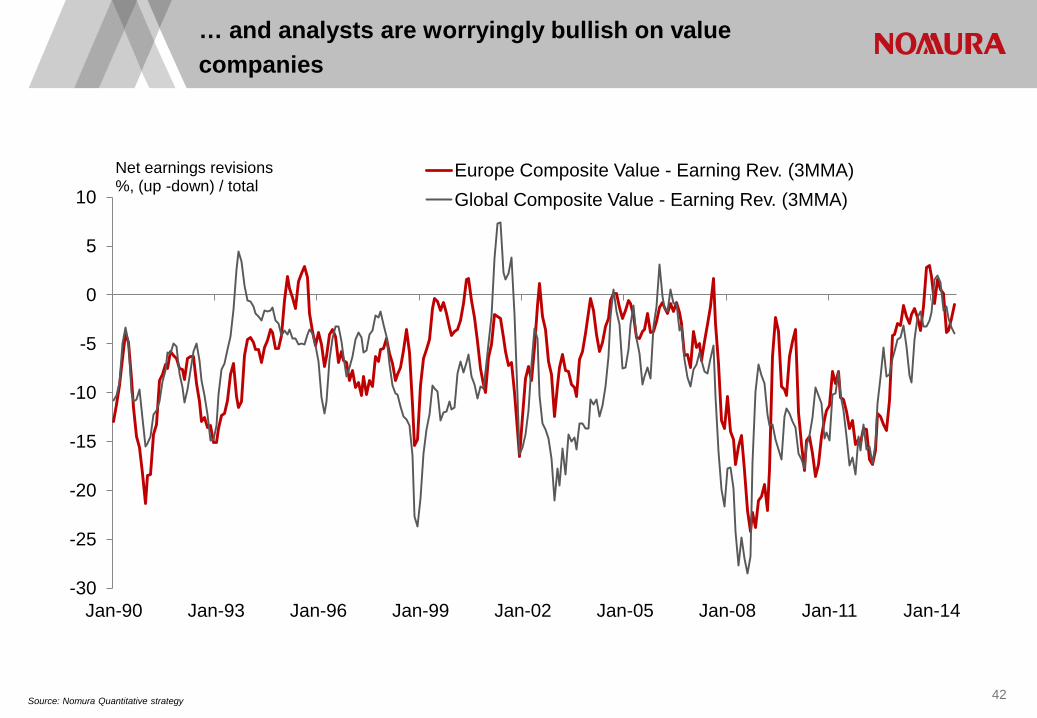

… and analysts are worryingly bullish on value companies

-30

-25

-20

-15

-10

-5

0

5

10

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Net earnings revisions %, (up -down) / total

Europe Composite Value - Earning Rev. (3MMA) Global Composite Value - Earning Rev. (3MMA)

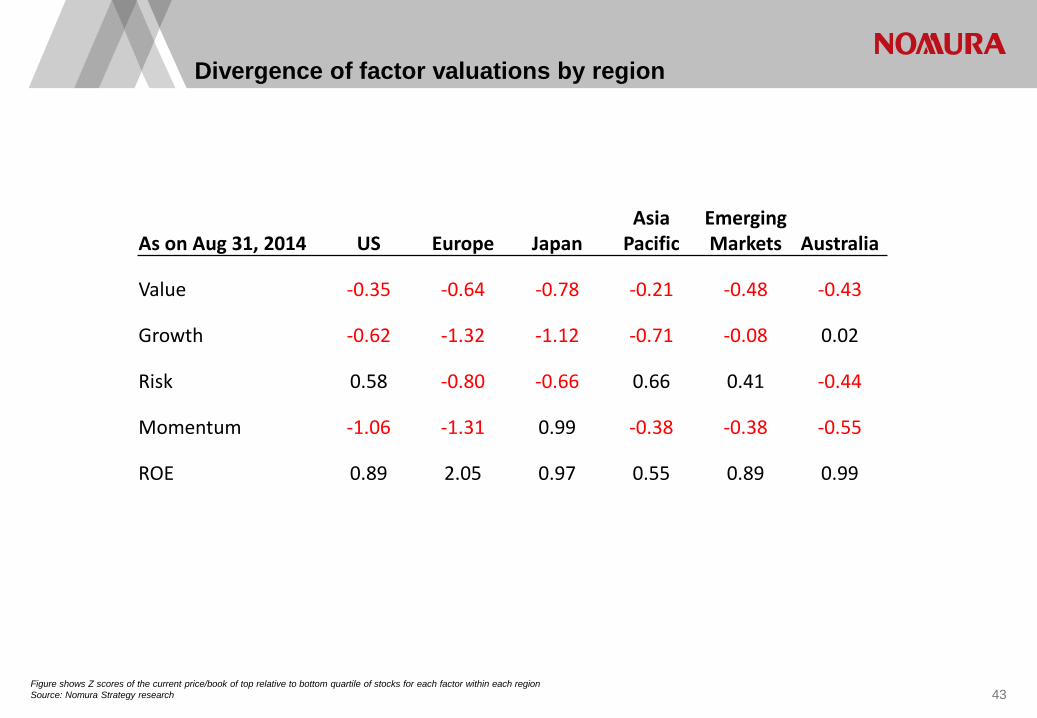

Divergence of factor valuations by region

Figure shows Z scores of the current price/book of top relative to bottom quartile of stocks for each factor within each region Source: Nomura Strategy research 43

As on Aug 31, 2014 US Europe Japan Asia

Pacific Emerging Markets Australia

Value -0.35 -0.64 -0.78 -0.21 -0.48 -0.43

Growth -0.62 -1.32 -1.12 -0.71 -0.08 0.02

Risk 0.58 -0.80 -0.66 0.66 0.41 -0.44

Momentum -1.06 -1.31 0.99 -0.38 -0.38 -0.55

ROE 0.89 2.05 0.97 0.55 0.89 0.99

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-90 Jan-94 Jan-98 Jan-02 Jan-06 Jan-10 Jan-14

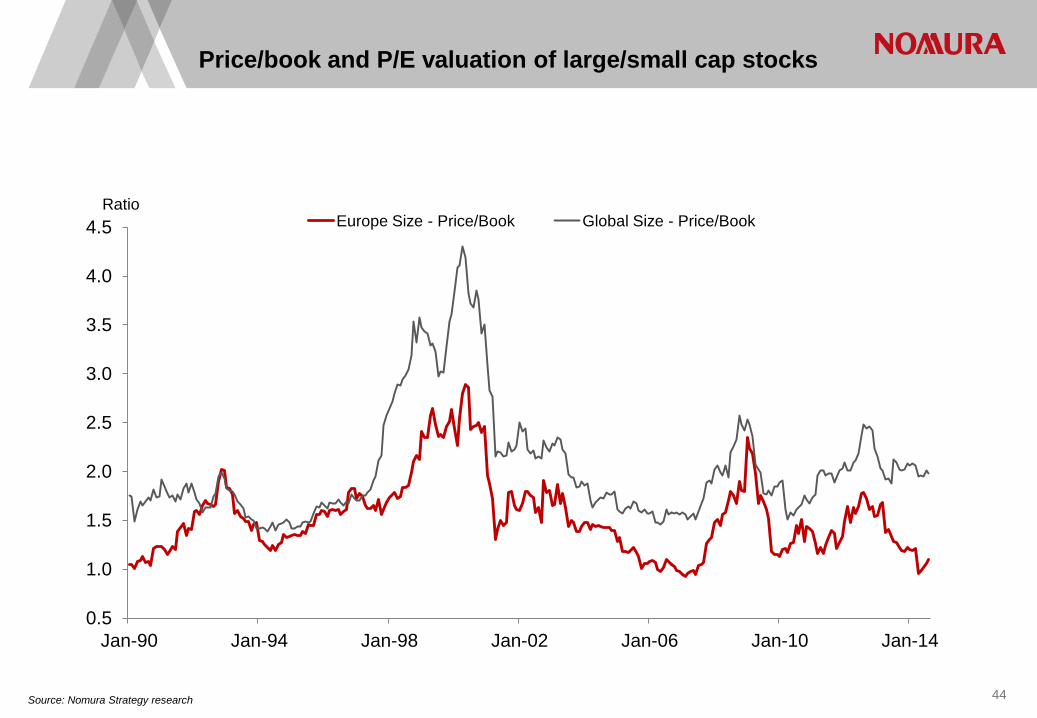

Ratio Europe Size - Price/Book Global Size - Price/Book

44 Source: Nomura Strategy research

Price/book and P/E valuation of large/small cap stocks

Source: Bloomberg

Real time factor performance for all regions

45

Source: Nomura Quantitative strategy 46

Stable dividend strategy

•There is a ‘hunt for yield’, but simply buying passive equities is not an optimal way to do that and buying the highest yielding equities looks outright unattractive. •Instead we prefer to buy the next tranche of stocks down in terms of yield level, where the dividend is well covered and an analysis of historical dividend policy implies that dividends are likely to grow or be stable. •Purely systematic.

Aim

Methodology

The stocks are ranked on the following five criteria on an equal-weighted composite basis. •Trailing last reported Dividend Yield. •Dividend Growth (Compounded Annual Growth Rate over the past five years), but with a ‘knockout clause’ that the stock gets excluded if in any given year that growth is negative. •Last reported FCF dividend cover. •Standard deviation of the annual dividend growth rate over the past five years. •The five-year Z score of the Fwd P/E. We then create a combined rank and select the stocks that are in the top quartile based on this combination of criteria. The investment universe is the top 500 stocks from the FTSE World and the FTSE Japan for our Japanese version.

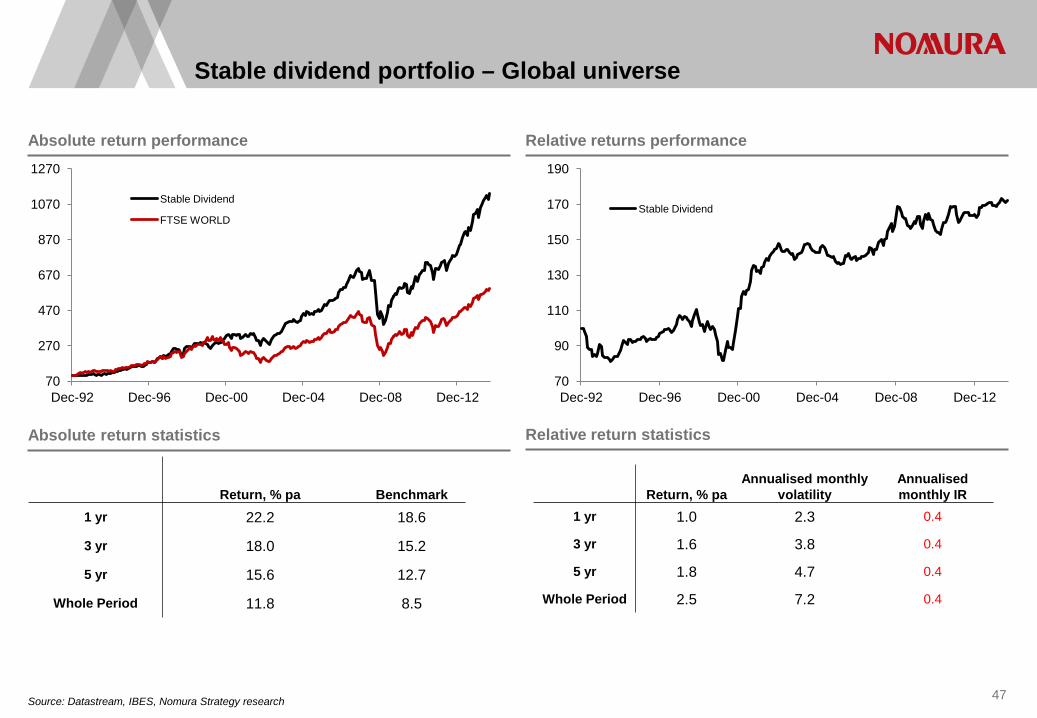

Source: Datastream, IBES, Nomura Strategy research 47

Absolute return performance Relative returns performance

Absolute return statistics Relative return statistics

Stable dividend portfolio – Global universe

Return, % pa Benchmark 1 yr 22.2 18.6

3 yr 18.0 15.2

5 yr 15.6 12.7

Whole Period 11.8 8.5

Return, % pa Annualised monthly

volatility Annualised monthly IR

1 yr 1.0 2.3 0.4

3 yr 1.6 3.8 0.4

5 yr 1.8 4.7 0.4

Whole Period 2.5 7.2 0.4

70

270

470

670

870

1070

1270

Dec-92 Dec-96 Dec-00 Dec-04 Dec-08 Dec-12

Stable Dividend

FTSE WORLD

70

90

110

130

150

170

190

Dec-92 Dec-96 Dec-00 Dec-04 Dec-08 Dec-12

Stable Dividend

Source: Nomura Quantitative strategy 48

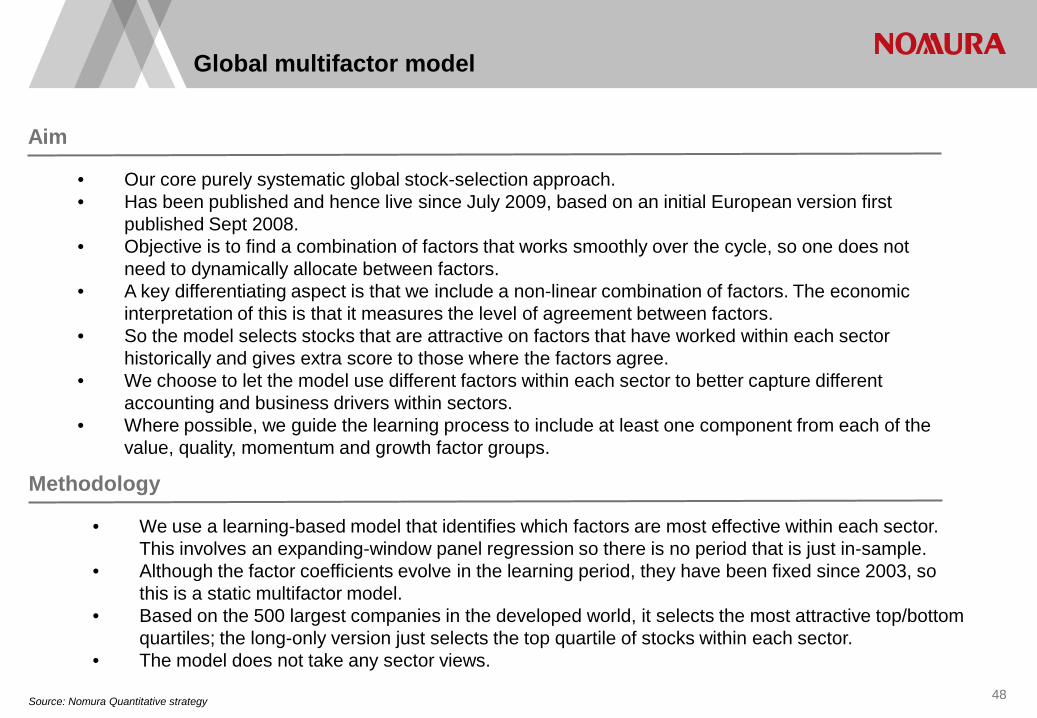

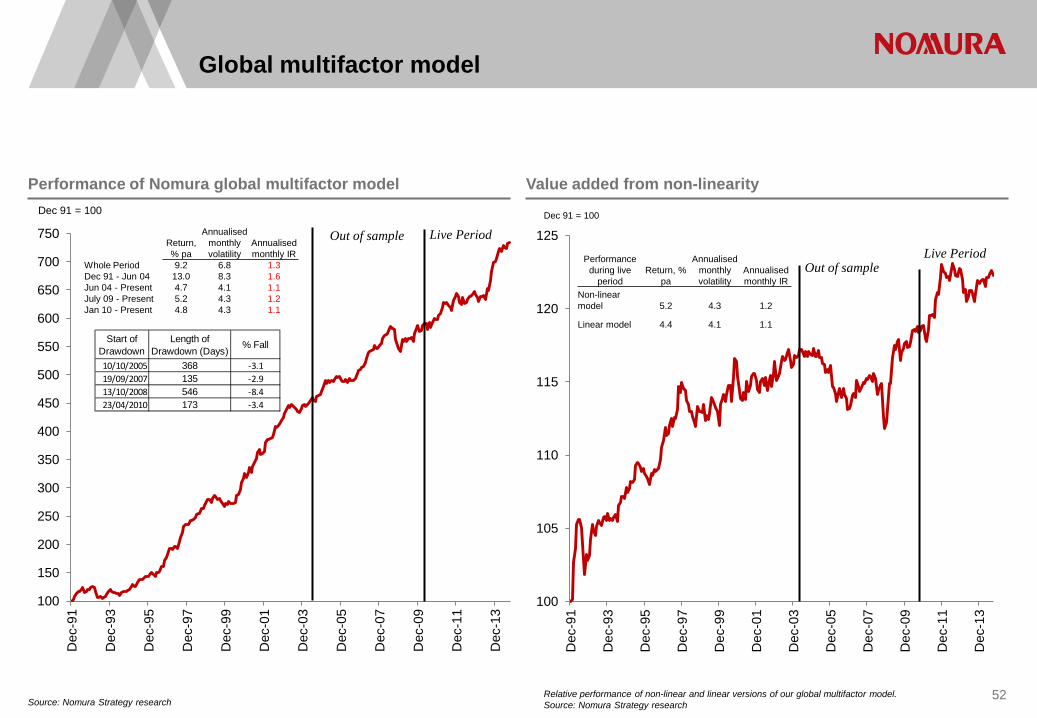

Global multifactor model

• Our core purely systematic global stock-selection approach. • Has been published and hence live since July 2009, based on an initial European version first

published Sept 2008. • Objective is to find a combination of factors that works smoothly over the cycle, so one does not

need to dynamically allocate between factors. • A key differentiating aspect is that we include a non-linear combination of factors. The economic

interpretation of this is that it measures the level of agreement between factors. • So the model selects stocks that are attractive on factors that have worked within each sector

historically and gives extra score to those where the factors agree. • We choose to let the model use different factors within each sector to better capture different

accounting and business drivers within sectors. • Where possible, we guide the learning process to include at least one component from each of the

value, quality, momentum and growth factor groups.

Aim

Methodology

• We use a learning-based model that identifies which factors are most effective within each sector. This involves an expanding-window panel regression so there is no period that is just in-sample.

• Although the factor coefficients evolve in the learning period, they have been fixed since 2003, so this is a static multifactor model.

• Based on the 500 largest companies in the developed world, it selects the most attractive top/bottom quartiles; the long-only version just selects the top quartile of stocks within each sector.

• The model does not take any sector views.

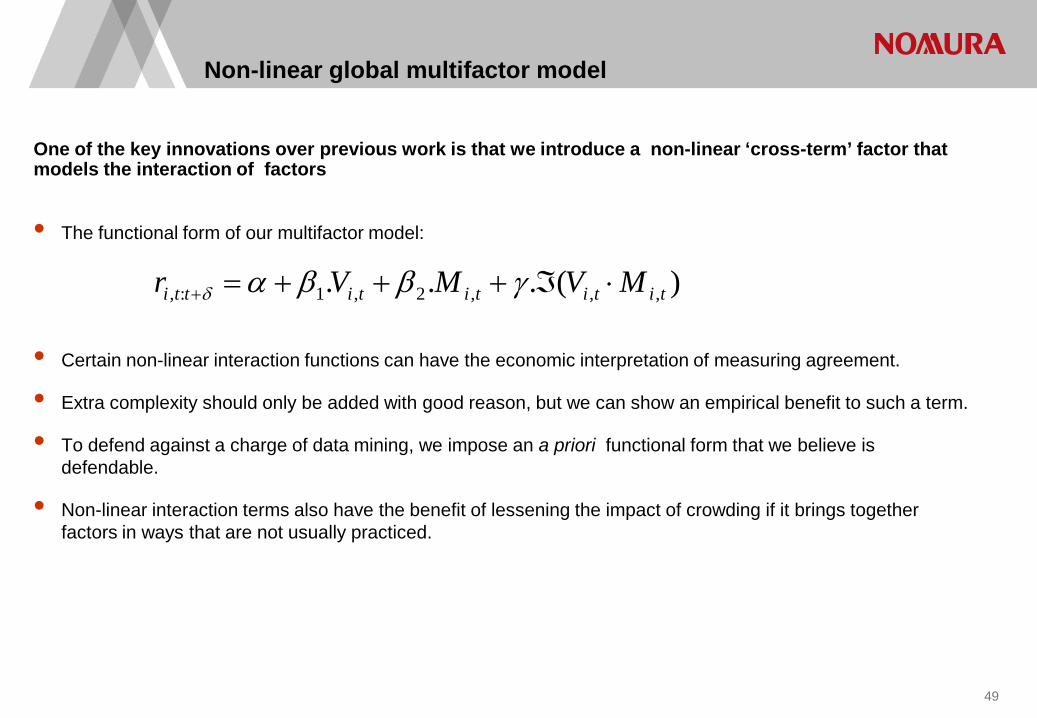

One of the key innovations over previous work is that we introduce a non-linear ‘cross-term’ factor that models the interaction of factors

• The functional form of our multifactor model:

• Certain non-linear interaction functions can have the economic interpretation of measuring agreement.

• Extra complexity should only be added with good reason, but we can show an empirical benefit to such a term.

• To defend against a charge of data mining, we impose an a priori functional form that we believe is defendable.

• Non-linear interaction terms also have the benefit of lessening the impact of crowding if it brings together factors in ways that are not usually practiced.

Non-linear global multifactor model

)(... ,,,2,1:, tititititti MVMVr ⋅ℑ+++=+ γββαδ

49

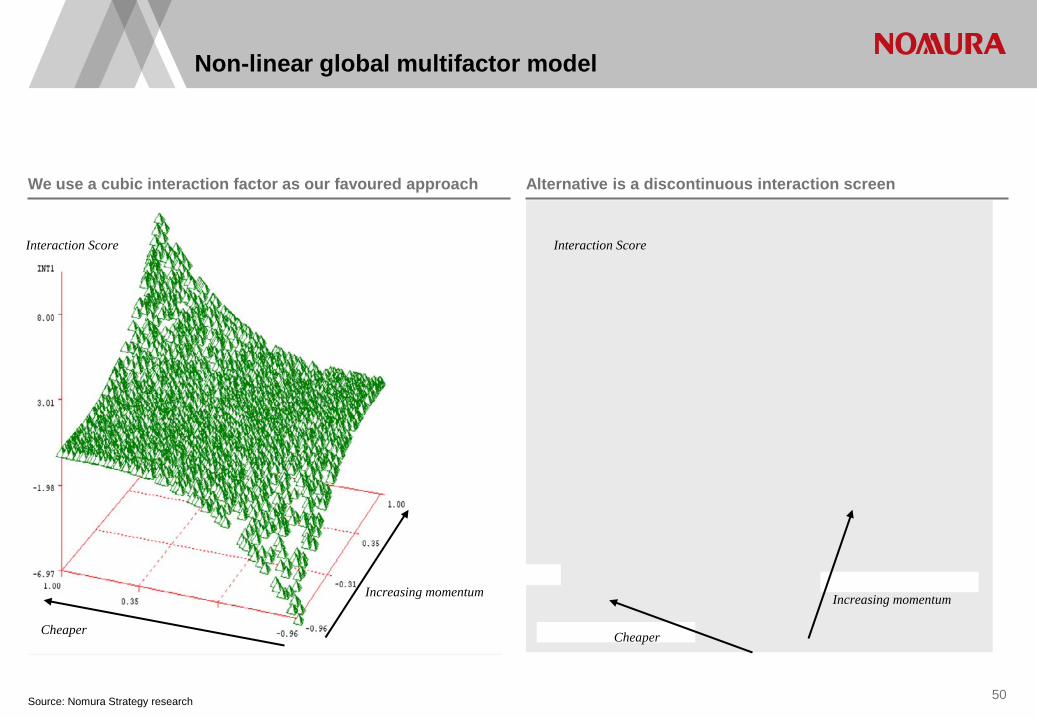

Source: Nomura Strategy research

We use a cubic interaction factor as our favoured approach Alternative is a discontinuous interaction screen

Increasing momentum

Cheaper

Increasing momentum

Cheaper

Interaction Score Interaction Score

50

Non-linear global multifactor model

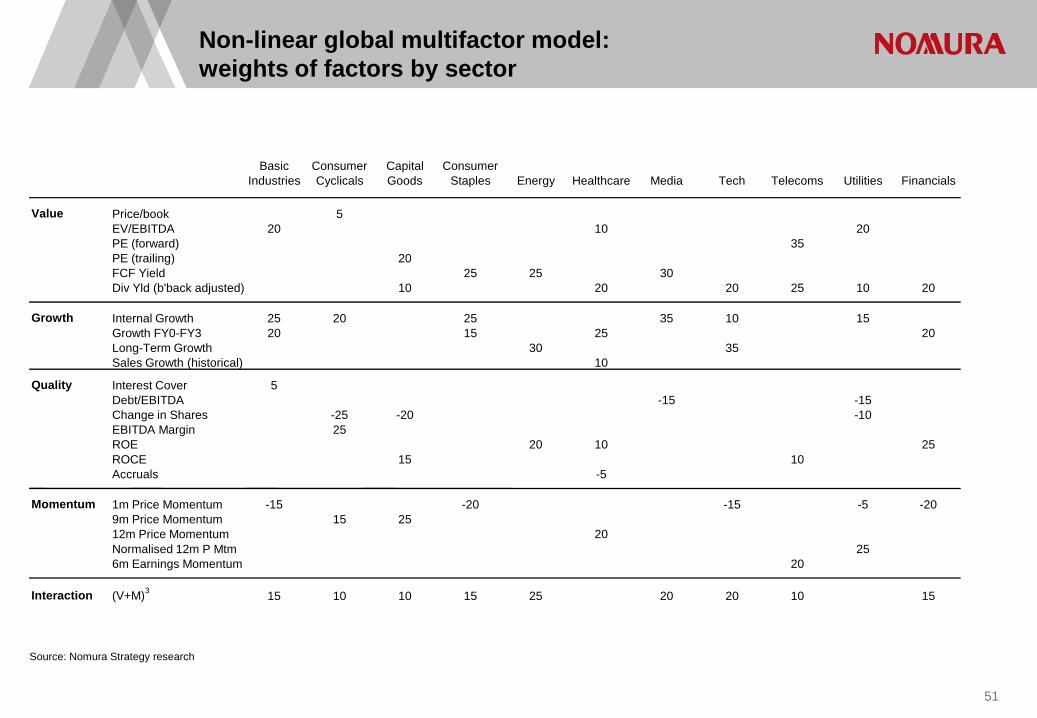

Non-linear global multifactor model: weights of factors by sector

Source: Nomura Strategy research

Basic Industries

Consumer Cyclicals

Capital Goods

Consumer Staples Energy Healthcare Media Tech Telecoms Utilities Financials

Value Price/book 5 EV/EBITDA 20 10 20 PE (forward) 35 PE (trailing) 20 FCF Yield 25 25 30 Div Yld (b'back adjusted) 10 20 20 25 10 20

Growth Internal Growth 25 20 25 35 10 15 Growth FY0-FY3 20 15 25 20 Long-Term Growth 30 35 Sales Growth (historical) 10

Quality Interest Cover 5 Debt/EBITDA -15 -15 Change in Shares -25 -20 -10 EBITDA Margin 25 ROE 20 10 25 ROCE 15 10 Accruals -5

Momentum 1m Price Momentum -15 -20 -15 -5 -20 9m Price Momentum 15 25 12m Price Momentum 20 Normalised 12m P Mtm 25 6m Earnings Momentum 20

Interaction (V+M) 3 15 10 10 15 25 20 20 10 15

51

Global multifactor model

Source: Nomura Strategy research 52

Performance of Nomura global multifactor model Value added from non-linearity

100

150

200

250

300

350

400

450

500

550

600

650

700

750

Dec

-91

Dec

-93

Dec

-95

Dec

-97

Dec

-99

Dec

-01

Dec

-03

Dec

-05

Dec

-07

Dec

-09

Dec

-11

Dec

-13

Dec 91 = 100

Out of sample Live Period

Start of Drawdown

Length of Drawdown (Days)

% Fall

10/10/2005 368 -3.119/09/2007 135 -2.913/10/2008 546 -8.423/04/2010 173 -3.4

Return, % pa

Annualised monthly volatility

Annualised monthly IR

Whole Period 9.2 6.8 1.3 Dec 91 - Jun 04 13.0 8.3 1.6 Jun 04 - Present 4.7 4.1 1.1 July 09 - Present 5.2 4.3 1.2 Jan 10 - Present 4.8 4.3 1.1

100

105

110

115

120

125

Dec

-91

Dec

-93

Dec

-95

Dec

-97

Dec

-99

Dec

-01

Dec

-03

Dec

-05

Dec

-07

Dec

-09

Dec

-11

Dec

-13

Out of sample

Dec 91 = 100

Live Period Performance during live

period Return, %

pa

Annualised monthly volatility

Annualised monthly IR

Non-linear model 5.2 4.3 1.2

Linear model 4.4 4.1 1.1

Relative performance of non-linear and linear versions of our global multifactor model. Source: Nomura Strategy research

Source: Datastream, IBES, Nomura Strategy research 53

Absolute return performance (out of sample period) Relative returns performance (out of sample period)

Absolute return statistics Relative return statistics

Global multifactor (long-only version)

70.0

120.0

170.0

220.0

270.0

320.0

Jun-04 Jun-07 Jun-10 Jun-13

GMF Long only Sector Weighted

FTSE WORLD

90 95

100 105 110 115 120 125 130 135 140

Jun-04 Jun-07 Jun-10 Jun-13

GMF Long only Sector Weighted

Return, % pa Benchmark 1 yr 30.1 18.6

3 yr 19.4 15.2

5 yr 16.0 12.7

Out of sample Period 11.5 8.0

Return, % pa Annualised monthly

volatility Annualised monthly IR

1 yr 7.7 2.3 3.3

3 yr 3.3 3.4 1.0

5 yr 2.8 3.1 0.9 Out of sample

Period 3.2 3.2 1.0

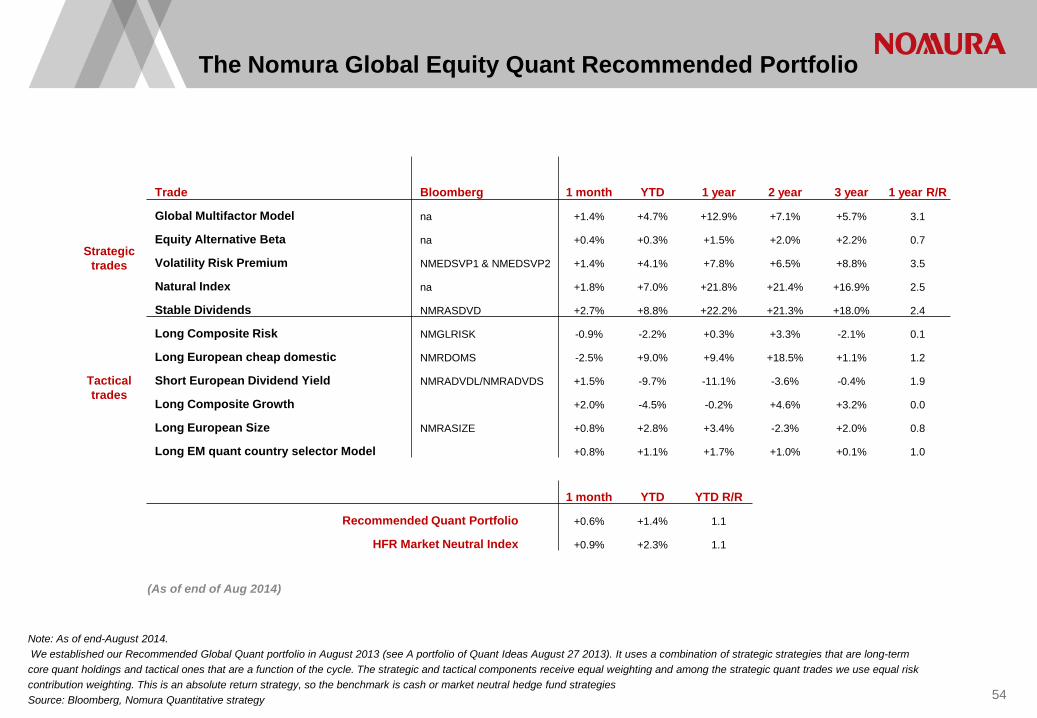

The Nomura Global Equity Quant Recommended Portfolio

Note: As of end-August 2014. We established our Recommended Global Quant portfolio in August 2013 (see A portfolio of Quant Ideas August 27 2013). It uses a combination of strategic strategies that are long-term core quant holdings and tactical ones that are a function of the cycle. The strategic and tactical components receive equal weighting and among the strategic quant trades we use equal risk contribution weighting. This is an absolute return strategy, so the benchmark is cash or market neutral hedge fund strategies Source: Bloomberg, Nomura Quantitative strategy 54

Trade Bloomberg 1 month YTD 1 year 2 year 3 year 1 year R/R

Strategic trades

Global Multifactor Model na +1.4% +4.7% +12.9% +7.1% +5.7% 3.1

Equity Alternative Beta na +0.4% +0.3% +1.5% +2.0% +2.2% 0.7

Volatility Risk Premium NMEDSVP1 & NMEDSVP2 +1.4% +4.1% +7.8% +6.5% +8.8% 3.5

Natural Index na +1.8% +7.0% +21.8% +21.4% +16.9% 2.5

Stable Dividends NMRASDVD +2.7% +8.8% +22.2% +21.3% +18.0% 2.4

Tactical trades

Long Composite Risk NMGLRISK -0.9% -2.2% +0.3% +3.3% -2.1% 0.1

Long European cheap domestic NMRDOMS -2.5% +9.0% +9.4% +18.5% +1.1% 1.2

Short European Dividend Yield NMRADVDL/NMRADVDS +1.5% -9.7% -11.1% -3.6% -0.4% 1.9

Long Composite Growth +2.0% -4.5% -0.2% +4.6% +3.2% 0.0

Long European Size NMRASIZE +0.8% +2.8% +3.4% -2.3% +2.0% 0.8

Long EM quant country selector Model +0.8% +1.1% +1.7% +1.0% +0.1% 1.0

1 month YTD YTD R/R

Recommended Quant Portfolio +0.6% +1.4% 1.1

HFR Market Neutral Index +0.9% +2.3% 1.1

(As of end of Aug 2014)

Long horizon concentrated strategies: a global recommended quant stock portfolio

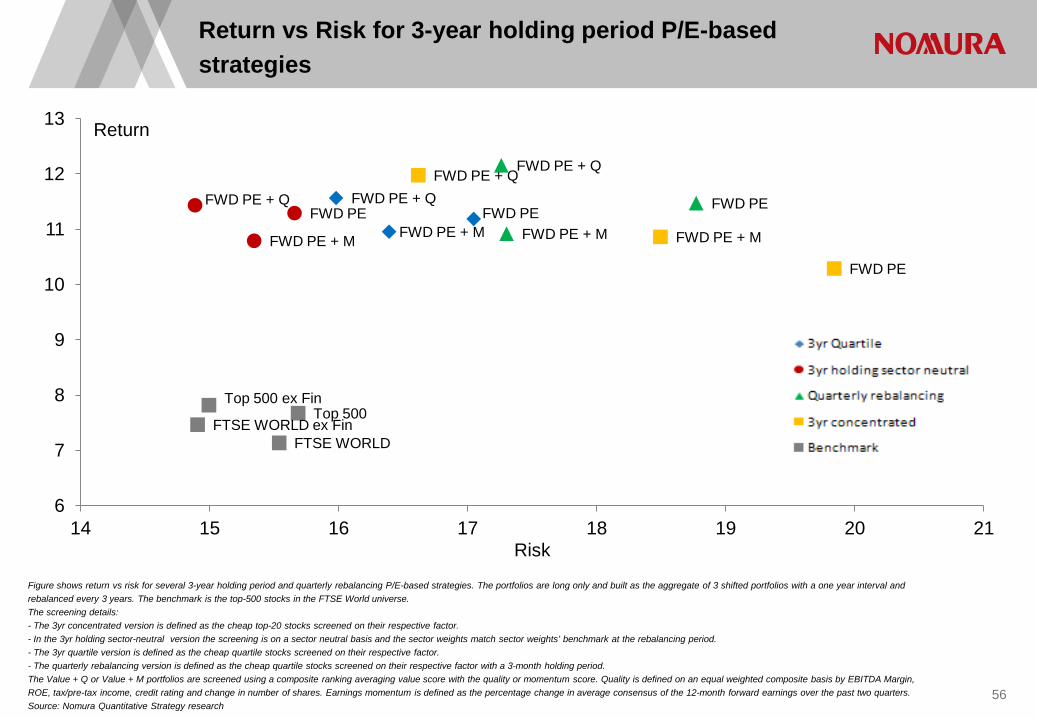

Figure shows return vs risk for several 3-year holding period and quarterly rebalancing P/E-based strategies. The portfolios are long only and built as the aggregate of 3 shifted portfolios with a one year interval and rebalanced every 3 years. The benchmark is the top-500 stocks in the FTSE World universe. The screening details: - The 3yr concentrated version is defined as the cheap top-20 stocks screened on their respective factor. - In the 3yr holding sector-neutral version the screening is on a sector neutral basis and the sector weights match sector weights’ benchmark at the rebalancing period. - The 3yr quartile version is defined as the cheap quartile stocks screened on their respective factor. - The quarterly rebalancing version is defined as the cheap quartile stocks screened on their respective factor with a 3-month holding period. The Value + Q or Value + M portfolios are screened using a composite ranking averaging value score with the quality or momentum score. Quality is defined on an equal weighted composite basis by EBITDA Margin, ROE, tax/pre-tax income, credit rating and change in number of shares. Earnings momentum is defined as the percentage change in average consensus of the 12-month forward earnings over the past two quarters. Source: Nomura Quantitative Strategy research

Return vs Risk for 3-year holding period P/E-based strategies

56

FWD PE FWD PE + Q

FWD PE + M FWD PE

FWD PE + Q

FWD PE + M

FWD PE

FWD PE + Q

FWD PE + M

FWD PE

FWD PE + Q

FWD PE + M

FTSE WORLD FTSE WORLD ex Fin

Top 500 Top 500 ex Fin

6

7

8

9

10

11

12

13

14 15 16 17 18 19 20 21

Return

Risk

Source: Nomura Quantitative strategy 57

Global Recommended Portfolio

•This is a blend of bottom-up systematic stock selection with top-down strategy views on regions and sectors. •The systematic stock selection uses our long-horizon quant stock selection model. •Note that the portfolio has always been a blend of quant and discretionary, but the long-horizon quant stock selection model has only been used since we published it in 2013.

•Portfolio has been run since 1997.

Aim

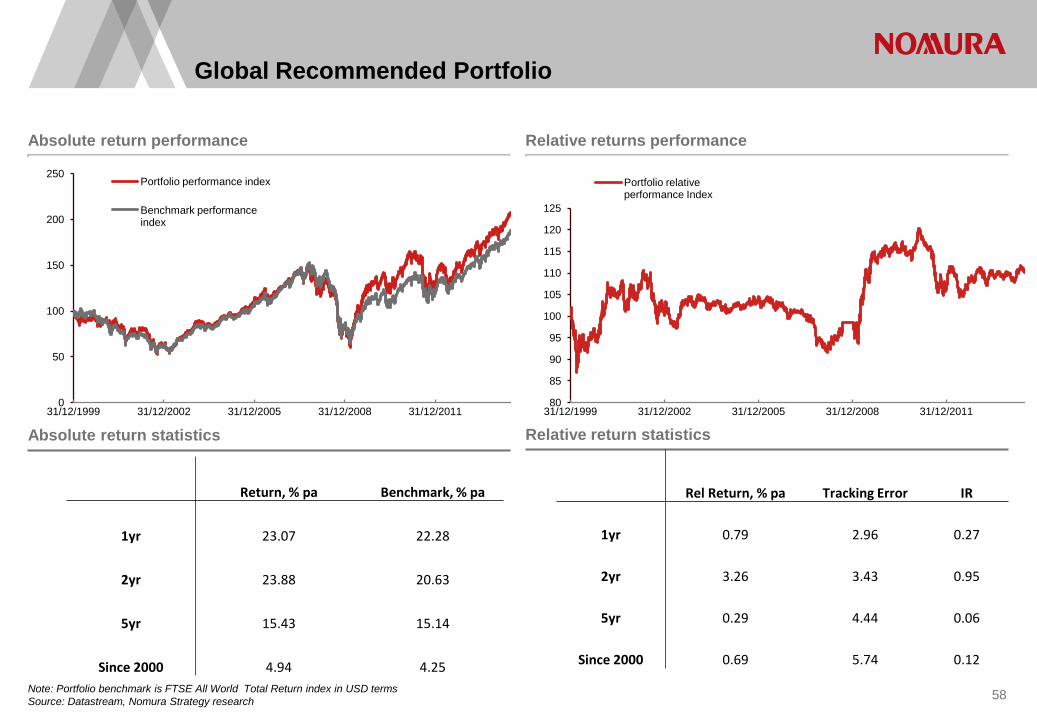

Note: Portfolio benchmark is FTSE All World Total Return index in USD terms Source: Datastream, Nomura Strategy research 58

Absolute return performance Relative returns performance

Absolute return statistics Relative return statistics

Global Recommended Portfolio

0

50

100

150

200

250

31/12/1999 31/12/2002 31/12/2005 31/12/2008 31/12/2011

Portfolio performance index

Benchmark performance index

80

85

90

95

100

105

110

115

120

125

31/12/1999 31/12/2002 31/12/2005 31/12/2008 31/12/2011

Portfolio relative performance Index

Return, % pa Benchmark, % pa

1yr 23.07 22.28

2yr 23.88 20.63

5yr 15.43 15.14

Since 2000 4.94 4.25

Rel Return, % pa Tracking Error IR

1yr 0.79 2.96 0.27

2yr 3.26 3.43 0.95

5yr 0.29 4.44 0.06

Since 2000 0.69 5.74 0.12

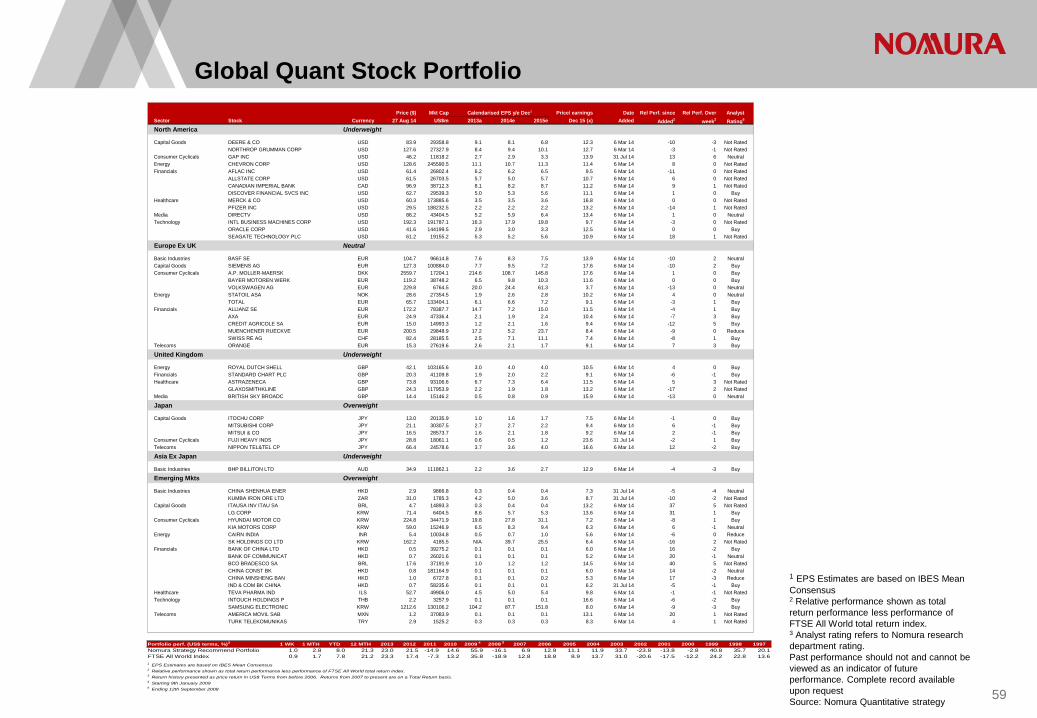

Global Quant Stock Portfolio

59

1 EPS Estimates are based on IBES Mean Consensus 2 Relative performance shown as total return performance less performance of FTSE All World total return index. 3 Analyst rating refers to Nomura research department rating. Past performance should not and cannot be viewed as an indicator of future performance. Complete record available upon request Source: Nomura Quantitative strategy

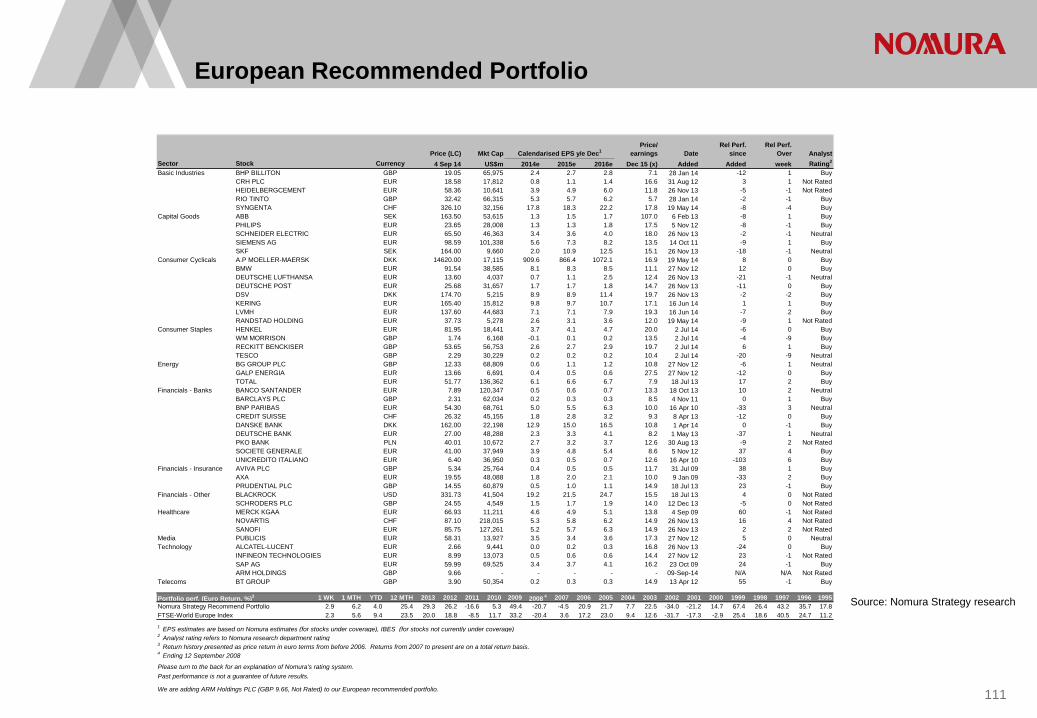

Price ($) Mkt Cap Calendarised EPS y/e Dec1 Price/ earnings Date Rel Perf. since Rel Perf. Over AnalystSector Stock Currency 27 Aug 14 US$m 2013a 2014e 2015e Dec 15 (x) Added Added2 week2 Rating6

North America Underweight

Capital Goods DEERE & CO USD 83.9 29358.8 9.1 8.1 6.8 12.3 6 Mar 14 -10 -3 Not RatedNORTHROP GRUMMAN CORP USD 127.6 27327.9 8.4 9.4 10.1 12.7 6 Mar 14 -3 -1 Not Rated

Consumer Cyclicals GAP INC USD 46.2 11818.2 2.7 2.9 3.3 13.9 31 Jul 14 13 6 NeutralEnergy CHEVRON CORP USD 128.6 245590.5 11.1 10.7 11.3 11.4 6 Mar 14 8 0 Not RatedFinancials AFLAC INC USD 61.4 26802.4 6.2 6.2 6.5 9.5 6 Mar 14 -11 0 Not Rated

ALLSTATE CORP USD 61.5 26703.5 5.7 5.0 5.7 10.7 6 Mar 14 6 0 Not RatedCANADIAN IMPERIAL BANK CAD 96.9 38712.3 8.1 8.2 8.7 11.2 6 Mar 14 9 1 Not RatedDISCOVER FINANCIAL SVCS INC USD 62.7 29539.3 5.0 5.3 5.6 11.1 6 Mar 14 1 0 Buy

Healthcare MERCK & CO USD 60.3 173885.6 3.5 3.5 3.6 16.8 6 Mar 14 0 0 Not RatedPFIZER INC USD 29.5 188232.5 2.2 2.2 2.2 13.2 6 Mar 14 -14 1 Not Rated

Media DIRECTV USD 86.2 43404.5 5.2 5.9 6.4 13.4 6 Mar 14 1 0 NeutralTechnology INTL BUSINESS MACHINES CORP USD 192.3 191787.1 16.3 17.9 19.8 9.7 6 Mar 14 -3 0 Not Rated

ORACLE CORP USD 41.6 144199.5 2.9 3.0 3.3 12.5 6 Mar 14 0 0 BuySEAGATE TECHNOLOGY PLC USD 61.2 19155.2 5.3 5.2 5.6 10.9 6 Mar 14 18 1 Not Rated

Europe Ex UK Neutral

Basic Industries BASF SE EUR 104.7 96614.8 7.6 8.3 7.5 13.9 6 Mar 14 -10 2 NeutralCapital Goods SIEMENS AG EUR 127.3 100884.0 7.7 9.5 7.2 17.6 6 Mar 14 -10 2 BuyConsumer Cyclicals A.P. MOLLER-MAERSK DKK 2559.7 17204.1 214.6 108.7 145.8 17.6 6 Mar 14 1 0 Buy

BAYER MOTOREN WERK EUR 119.2 38748.2 6.5 9.8 10.3 11.6 6 Mar 14 0 0 BuyVOLKSWAGEN AG EUR 229.8 6764.5 20.0 24.4 61.3 3.7 6 Mar 14 -13 0 Neutral

Energy STATOIL ASA NOK 28.6 27354.5 1.9 2.6 2.8 10.2 6 Mar 14 4 0 NeutralTOTAL EUR 65.7 133404.1 6.1 6.6 7.2 9.1 6 Mar 14 -3 1 Buy

Financials ALLIANZ SE EUR 172.2 78387.7 14.7 7.2 15.0 11.5 6 Mar 14 -4 1 BuyAXA EUR 24.9 47336.4 2.1 1.9 2.4 10.4 6 Mar 14 -7 3 BuyCREDIT AGRICOLE SA EUR 15.0 14993.3 1.2 2.1 1.6 9.4 6 Mar 14 -12 5 BuyMUENCHENER RUECKVE EUR 200.5 29848.9 17.2 5.2 23.7 8.4 6 Mar 14 -9 0 ReduceSWISS RE AG CHF 82.4 28185.5 2.5 7.1 11.1 7.4 6 Mar 14 -8 1 Buy

Telecoms ORANGE EUR 15.3 27619.6 2.6 2.1 1.7 9.1 6 Mar 14 7 3 Buy

United Kingdom Underweight

Energy ROYAL DUTCH SHELL GBP 42.1 103165.6 3.0 4.0 4.0 10.5 6 Mar 14 4 0 BuyFinancials STANDARD CHART PLC GBP 20.3 41109.8 1.9 2.0 2.2 9.1 6 Mar 14 -6 -1 BuyHealthcare ASTRAZENECA GBP 73.8 93106.6 6.7 7.3 6.4 11.5 6 Mar 14 5 3 Not Rated

GLAXOSMITHKLINE GBP 24.3 117953.9 2.2 1.9 1.8 13.2 6 Mar 14 -17 2 Not RatedMedia BRITISH SKY BROADC GBP 14.4 15146.2 0.5 0.8 0.9 15.9 6 Mar 14 -13 0 Neutral

Japan Overweight

Capital Goods ITOCHU CORP JPY 13.0 20135.9 1.0 1.6 1.7 7.5 6 Mar 14 -1 0 BuyMITSUBISHI CORP JPY 21.1 30307.5 2.7 2.7 2.2 9.4 6 Mar 14 6 -1 BuyMITSUI & CO JPY 16.5 28573.7 1.6 2.1 1.8 9.2 6 Mar 14 2 -1 Buy

Consumer Cyclicals FUJI HEAVY INDS JPY 28.8 18061.1 0.6 0.5 1.2 23.6 31 Jul 14 -2 1 BuyTelecoms NIPPON TEL&TEL CP JPY 66.4 24578.6 3.7 3.6 4.0 16.6 6 Mar 14 12 -2 Buy

Asia Ex Japan Underweight

Basic Industries BHP BILLITON LTD AUD 34.9 111862.1 2.2 3.6 2.7 12.9 6 Mar 14 -4 -3 Buy

Emerging Mkts Overweight

Basic Industries CHINA SHENHUA ENER HKD 2.9 9866.8 0.3 0.4 0.4 7.3 31 Jul 14 -5 -4 NeutralKUMBA IRON ORE LTD ZAR 31.0 1785.3 4.2 5.0 3.6 8.7 31 Jul 14 -10 -2 Not Rated

Capital Goods ITAUSA INV ITAU SA BRL 4.7 14893.3 0.3 0.4 0.4 13.2 6 Mar 14 37 5 Not RatedLG CORP KRW 71.4 6404.5 8.6 5.7 5.3 13.6 6 Mar 14 31 1 Buy

Consumer Cyclicals HYUNDAI MOTOR CO KRW 224.8 34471.9 19.8 27.8 31.1 7.2 6 Mar 14 -8 1 BuyKIA MOTORS CORP KRW 59.0 15246.9 6.5 8.3 9.4 6.3 6 Mar 14 6 -1 Neutral

Energy CAIRN INDIA INR 5.4 10034.8 0.5 0.7 1.0 5.6 6 Mar 14 -6 0 ReduceSK HOLDINGS CO LTD KRW 162.2 4185.5 N/A 39.7 25.5 6.4 6 Mar 14 -16 2 Not Rated

Financials BANK OF CHINA LTD HKD 0.5 39275.2 0.1 0.1 0.1 6.0 6 Mar 14 16 -2 BuyBANK OF COMMUNICAT HKD 0.7 26021.6 0.1 0.1 0.1 5.2 6 Mar 14 20 -1 NeutralBCO BRADESCO SA BRL 17.6 37191.9 1.0 1.2 1.2 14.5 6 Mar 14 40 5 Not RatedCHINA CONST BK HKD 0.8 181164.9 0.1 0.1 0.1 6.0 6 Mar 14 14 -2 NeutralCHINA MINSHENG BAN HKD 1.0 6727.8 0.1 0.1 0.2 5.3 6 Mar 14 17 -3 ReduceIND & COM BK CHINA HKD 0.7 58235.6 0.1 0.1 0.1 6.2 31 Jul 14 -5 -1 Buy

Healthcare TEVA PHARMA IND ILS 52.7 49906.0 4.5 5.0 5.4 9.8 6 Mar 14 -1 -1 Not RatedTechnology INTOUCH HOLDINGS P THB 2.2 3257.9 0.1 0.1 0.1 16.6 6 Mar 14 -6 -2 Buy

SAMSUNG ELECTRONIC KRW 1212.6 130106.2 104.2 87.7 151.8 8.0 6 Mar 14 -9 -3 BuyTelecoms AMERICA MOVIL SAB MXN 1.2 37083.9 0.1 0.1 0.1 13.1 6 Mar 14 20 1 Not Rated

TURK TELEKOMUNIKAS TRY 2.9 1525.2 0.3 0.3 0.3 8.3 6 Mar 14 4 1 Not Rated

Portfolio perf. (US$ terms, %)3 1 WK 1 MTH YTD 12 MTH 2013 2012 2011 2010 2009 4 2008 5 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997Nomura Strategy Recommend Portfolio 1.0 2.8 8.0 21.3 23.0 21.5 -14.9 14.6 55.9 -16.1 6.9 12.9 11.1 11.9 33.7 -23.8 -13.8 -2.8 40.8 35.7 20.1FTSE All World Index 0.9 1.7 7.8 21.2 23.3 17.4 -7.3 13.2 35.8 -18.9 12.8 18.8 8.9 13.7 31.0 -20.6 -17.5 -12.2 24.2 22.8 13.61 EPS Estimates are based on IBES Mean Consensus

3 Return history presented as price return in US$ Terms from before 2006. Returns from 2007 to present are on a Total Return basis.

2 Relative performance shown as total return performance less performance of FTSE All World total return index.

4 Starting 9th January 20095 Ending 12th September 2008

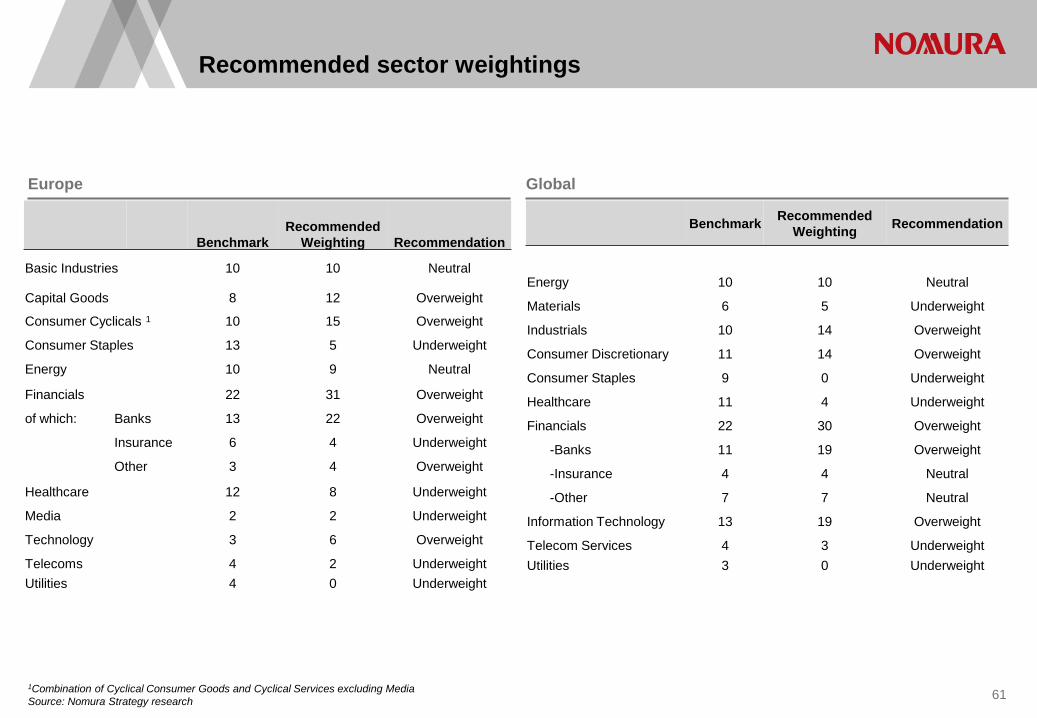

Sector allocation

Recommended sector weightings

1Combination of Cyclical Consumer Goods and Cyclical Services excluding Media Source: Nomura Strategy research

Europe Global

61

Benchmark Recommended

Weighting Recommendation

Energy 10 10 Neutral

Materials 6 5 Underweight

Industrials 10 14 Overweight

Consumer Discretionary 11 14 Overweight

Consumer Staples 9 0 Underweight

Healthcare 11 4 Underweight

Financials 22 30 Overweight

-Banks 11 19 Overweight

-Insurance 4 4 Neutral

-Other 7 7 Neutral

Information Technology 13 19 Overweight

Telecom Services 4 3 Underweight Utilities 3 0 Underweight

Benchmark Recommended

Weighting Recommendation

Basic Industries 10 10 Neutral

Capital Goods 8 12 Overweight

Consumer Cyclicals 1 10 15 Overweight

Consumer Staples 13 5 Underweight

Energy 10 9 Neutral

Financials 22 31 Overweight

of which: Banks 13 22 Overweight

Insurance 6 4 Underweight

Other 3 4 Overweight

Healthcare 12 8 Underweight

Media 2 2 Underweight

Technology 3 6 Overweight

Telecoms 4 2 Underweight Utilities 4 0 Underweight

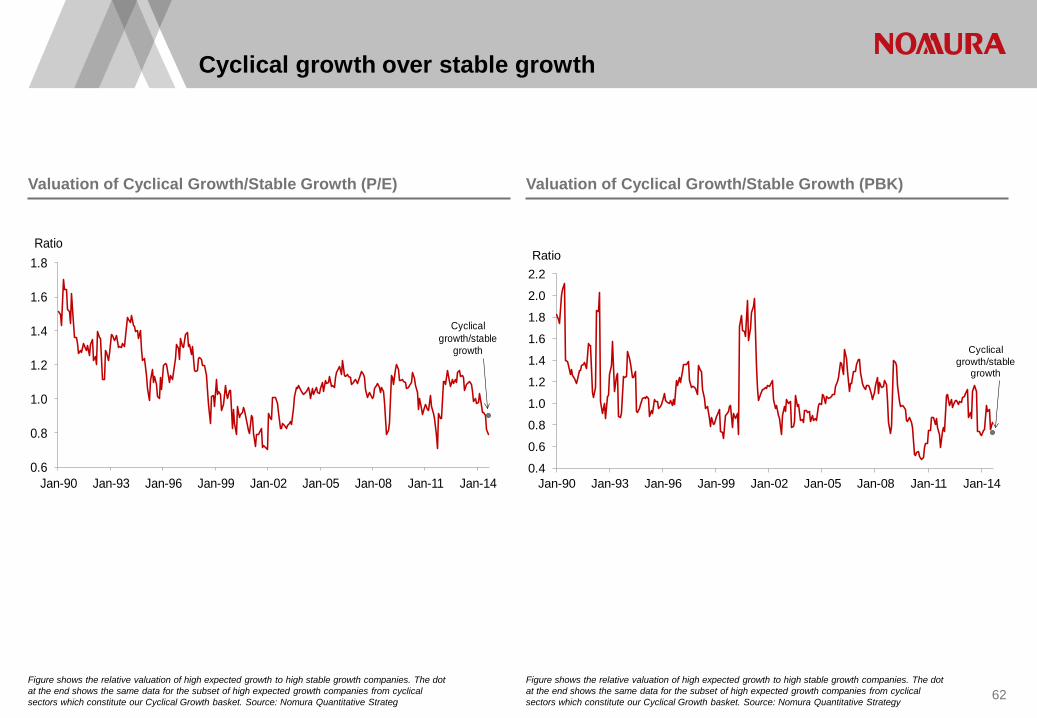

Cyclical growth over stable growth

Figure shows the relative valuation of high expected growth to high stable growth companies. The dot at the end shows the same data for the subset of high expected growth companies from cyclical sectors which constitute our Cyclical Growth basket. Source: Nomura Quantitative Strateg 62

Valuation of Cyclical Growth/Stable Growth (P/E) Valuation of Cyclical Growth/Stable Growth (PBK)

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Ratio

Cyclical growth/stable

growth

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-11 Jan-14

Ratio

Cyclical growth/stable

growth

Figure shows the relative valuation of high expected growth to high stable growth companies. The dot at the end shows the same data for the subset of high expected growth companies from cyclical sectors which constitute our Cyclical Growth basket. Source: Nomura Quantitative Strategy

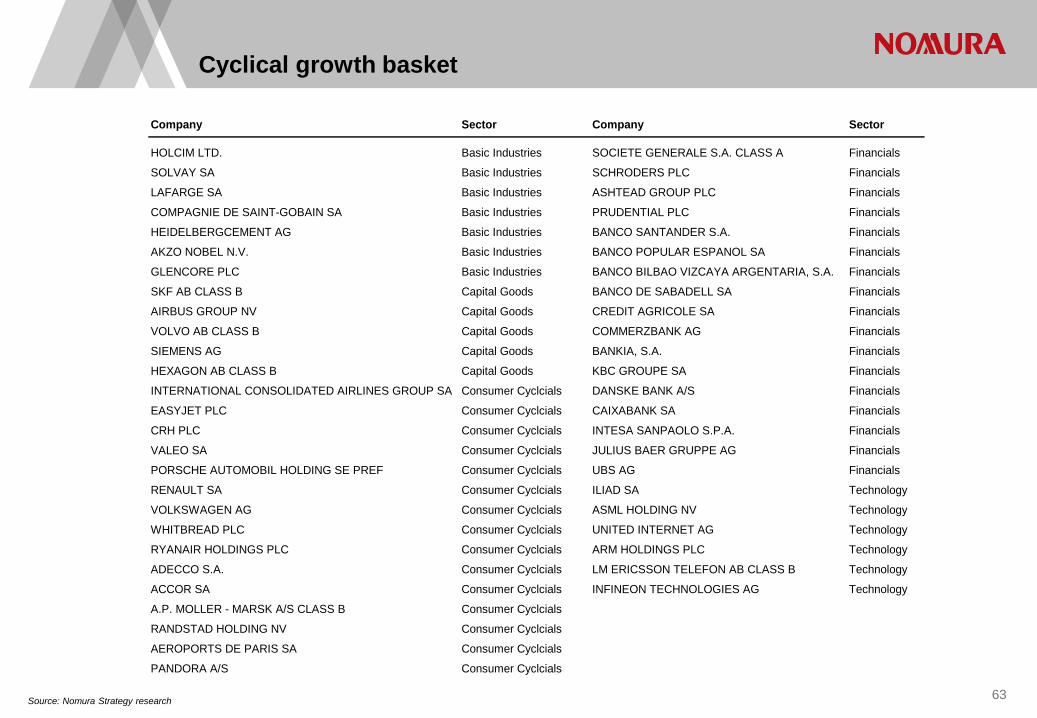

63 Source: Nomura Strategy research

Cyclical growth basket

Company Sector Company Sector

HOLCIM LTD. Basic Industries SOCIETE GENERALE S.A. CLASS A Financials

SOLVAY SA Basic Industries SCHRODERS PLC Financials

LAFARGE SA Basic Industries ASHTEAD GROUP PLC Financials

COMPAGNIE DE SAINT-GOBAIN SA Basic Industries PRUDENTIAL PLC Financials

HEIDELBERGCEMENT AG Basic Industries BANCO SANTANDER S.A. Financials

AKZO NOBEL N.V. Basic Industries BANCO POPULAR ESPANOL SA Financials

GLENCORE PLC Basic Industries BANCO BILBAO VIZCAYA ARGENTARIA, S.A. Financials

SKF AB CLASS B Capital Goods BANCO DE SABADELL SA Financials

AIRBUS GROUP NV Capital Goods CREDIT AGRICOLE SA Financials

VOLVO AB CLASS B Capital Goods COMMERZBANK AG Financials

SIEMENS AG Capital Goods BANKIA, S.A. Financials

HEXAGON AB CLASS B Capital Goods KBC GROUPE SA Financials

INTERNATIONAL CONSOLIDATED AIRLINES GROUP SA Consumer Cyclcials DANSKE BANK A/S Financials

EASYJET PLC Consumer Cyclcials CAIXABANK SA Financials

CRH PLC Consumer Cyclcials INTESA SANPAOLO S.P.A. Financials

VALEO SA Consumer Cyclcials JULIUS BAER GRUPPE AG Financials

PORSCHE AUTOMOBIL HOLDING SE PREF Consumer Cyclcials UBS AG Financials

RENAULT SA Consumer Cyclcials ILIAD SA Technology

VOLKSWAGEN AG Consumer Cyclcials ASML HOLDING NV Technology

WHITBREAD PLC Consumer Cyclcials UNITED INTERNET AG Technology

RYANAIR HOLDINGS PLC Consumer Cyclcials ARM HOLDINGS PLC Technology

ADECCO S.A. Consumer Cyclcials LM ERICSSON TELEFON AB CLASS B Technology

ACCOR SA Consumer Cyclcials INFINEON TECHNOLOGIES AG Technology

A.P. MOLLER - MARSK A/S CLASS B Consumer Cyclcials

RANDSTAD HOLDING NV Consumer Cyclcials

AEROPORTS DE PARIS SA Consumer Cyclcials

PANDORA A/S Consumer Cyclcials

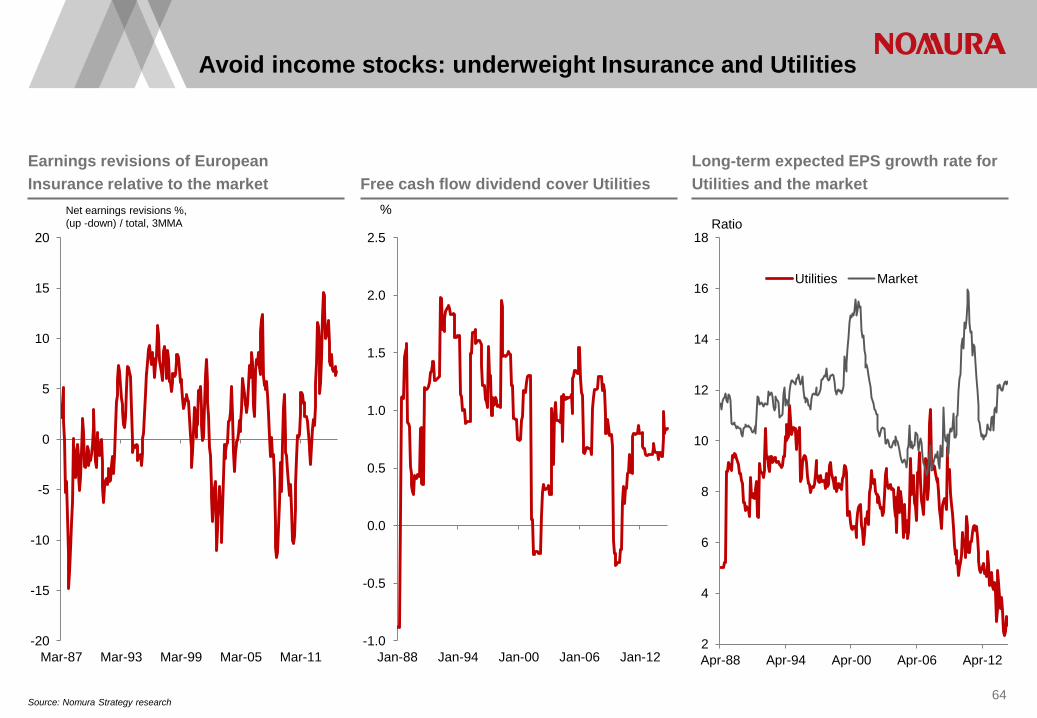

Avoid income stocks: underweight Insurance and Utilities

Source: Nomura Strategy research 64

Earnings revisions of European Insurance relative to the market Free cash flow dividend cover Utilities

Long-term expected EPS growth rate for Utilities and the market

2

4

6

8

10

12

14

16

18

Apr-88 Apr-94 Apr-00 Apr-06 Apr-12

Ratio

Utilities Market

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan-88 Jan-94 Jan-00 Jan-06 Jan-12

%

-20

-15

-10

-5

0

5

10

15

20

Mar-87 Mar-93 Mar-99 Mar-05 Mar-11

Net earnings revisions %, (up -down) / total, 3MMA

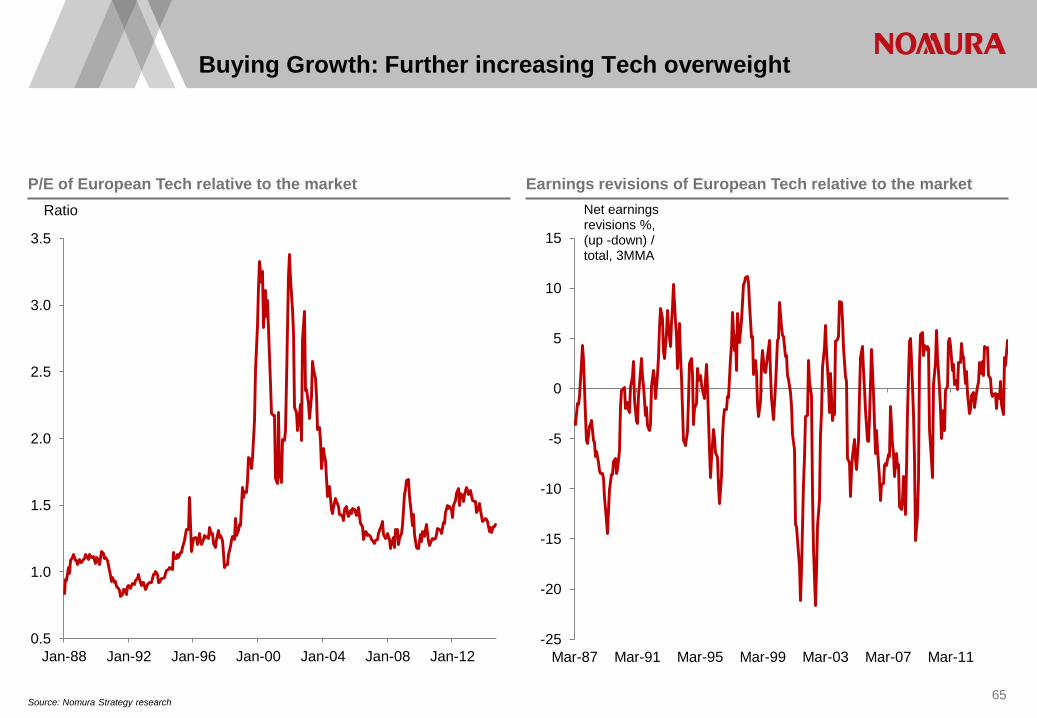

Buying Growth: Further increasing Tech overweight

65

P/E of European Tech relative to the market Earnings revisions of European Tech relative to the market

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12

Ratio

-25

-20

-15

-10

-5

0

5

10

15

Mar-87 Mar-91 Mar-95 Mar-99 Mar-03 Mar-07 Mar-11

Net earnings revisions %, (up -down) / total, 3MMA

Source: Nomura Strategy research

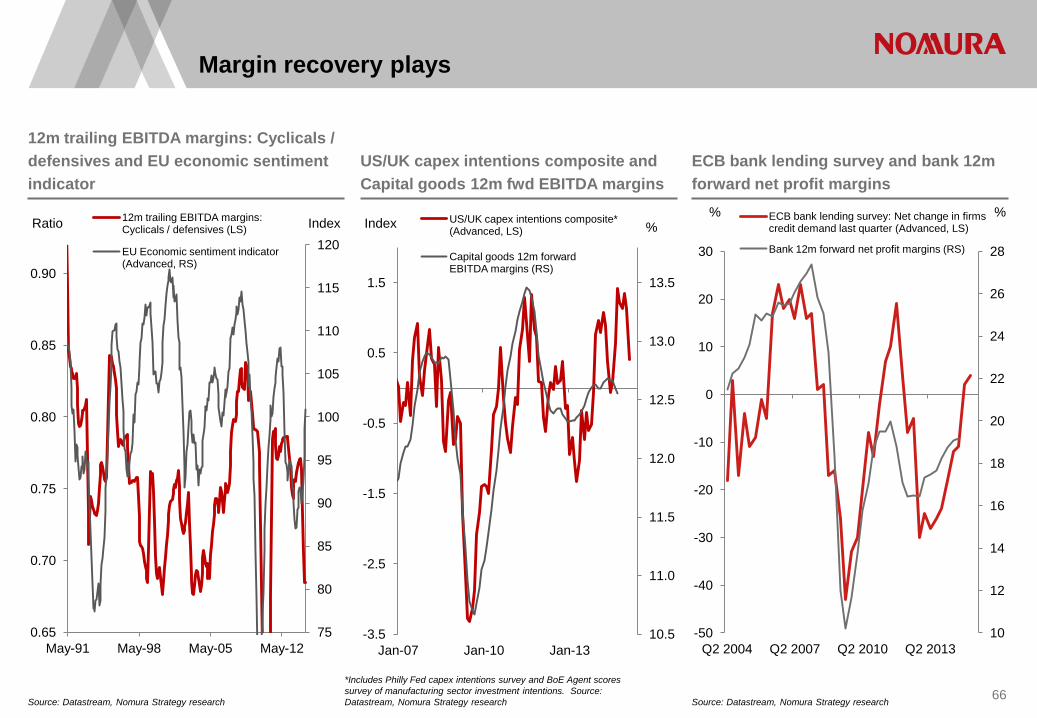

Margin recovery plays

Source: Datastream, Nomura Strategy research 66

12m trailing EBITDA margins: Cyclicals / defensives and EU economic sentiment indicator

US/UK capex intentions composite and Capital goods 12m fwd EBITDA margins

ECB bank lending survey and bank 12m forward net profit margins

75

80

85

90

95

100

105

110

115

120

0.65

0.70

0.75

0.80

0.85

0.90

May-91 May-98 May-05 May-12

Index Ratio 12m trailing EBITDA margins: Cyclicals / defensives (LS)

EU Economic sentiment indicator (Advanced, RS)

10.5

11.0

11.5

12.0

12.5

13.0

13.5

-3.5

-2.5

-1.5

-0.5

0.5

1.5

Jan-07 Jan-10 Jan-13

% Index US/UK capex intentions composite* (Advanced, LS)

Capital goods 12m forward EBITDA margins (RS)

*Includes Philly Fed capex intentions survey and BoE Agent scores survey of manufacturing sector investment intentions. Source: Datastream, Nomura Strategy research

10

12

14

16

18

20

22

24

26

28

-50

-40

-30

-20

-10

0

10

20

30

Q2 2004 Q2 2007 Q2 2010 Q2 2013

ECB bank lending survey: Net change in firms credit demand last quarter (Advanced, LS)

Bank 12m forward net profit margins (RS)

% %

Source: Datastream, Nomura Strategy research

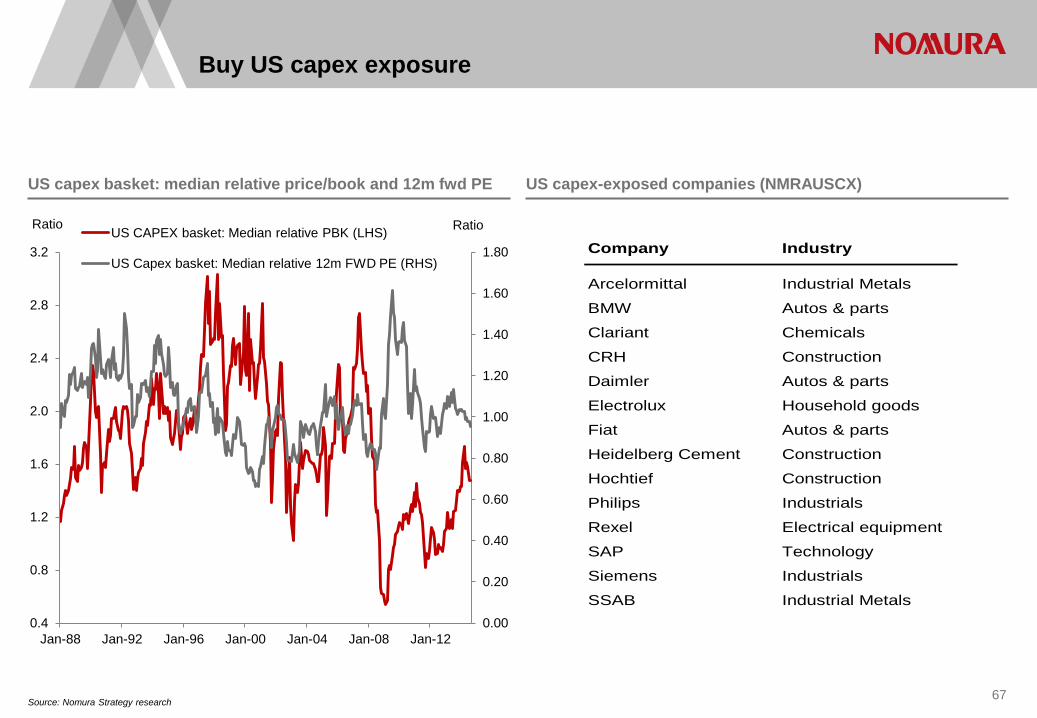

Buy US capex exposure

Source: Nomura Strategy research 67

US capex basket: median relative price/book and 12m fwd PE US capex-exposed companies (NMRAUSCX)

Company Industry

Arcelormittal Industrial Metals

BMW Autos & parts

Clariant Chemicals

CRH Construction

Daimler Autos & parts

Electrolux Household goods

Fiat Autos & parts

Heidelberg Cement Construction

Hochtief Construction

Philips Industrials

Rexel Electrical equipment

SAP Technology

Siemens Industrials

SSAB Industrial Metals 0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

0.4

0.8

1.2

1.6

2.0

2.4

2.8

3.2

Jan-88 Jan-92 Jan-96 Jan-00 Jan-04 Jan-08 Jan-12

Ratio Ratio US CAPEX basket: Median relative PBK (LHS)

US Capex basket: Median relative 12m FWD PE (RHS)

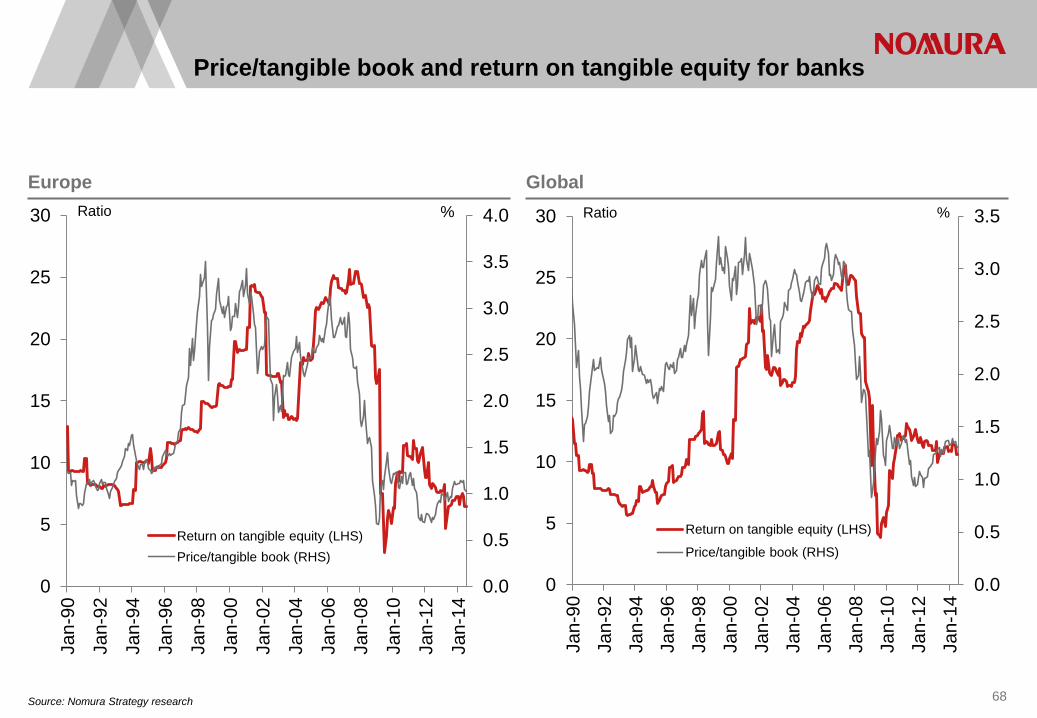

Price/tangible book and return on tangible equity for banks

Source: Nomura Strategy research 68

Europe Global

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

5

10

15

20

25

30

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

Jan-

06

Jan-

08

Jan-

10

Jan-

12

Jan-

14

% Ratio

Return on tangible equity (LHS) Price/tangible book (RHS)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0

5

10

15

20

25

30

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

Jan-

06

Jan-

08

Jan-

10

Jan-

12

Jan-

14

% Ratio

Return on tangible equity (LHS)

Price/tangible book (RHS)

Fund management strategy and minimum variance

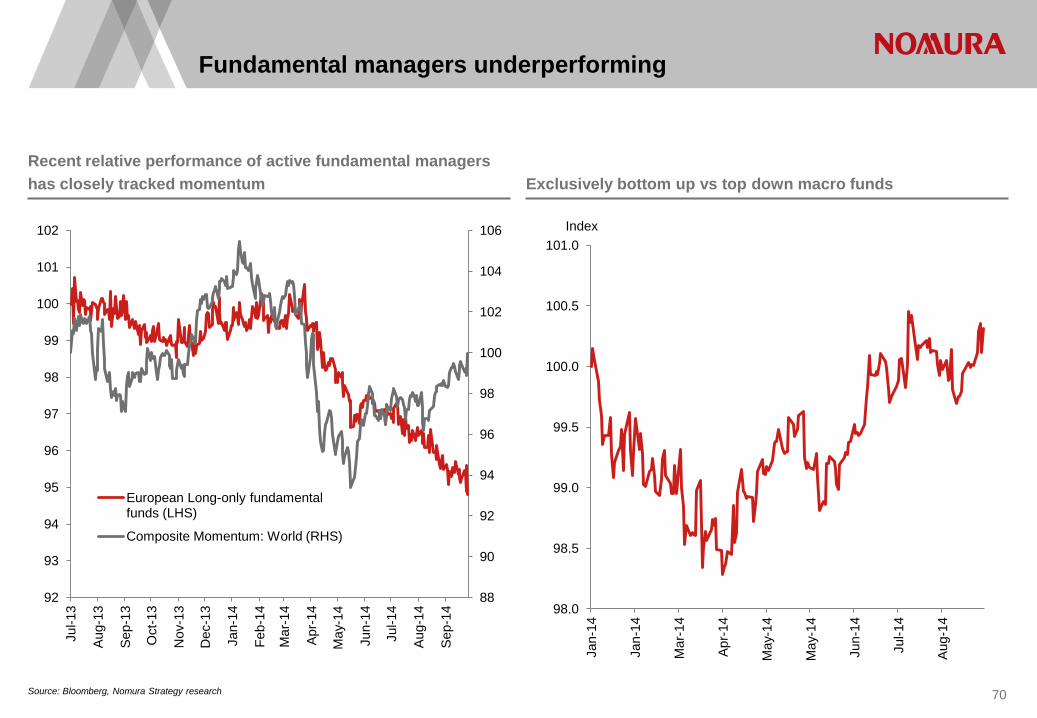

Fundamental managers underperforming

Source: Bloomberg, Nomura Strategy research

70

Recent relative performance of active fundamental managers has closely tracked momentum Exclusively bottom up vs top down macro funds

98.0

98.5

99.0

99.5

100.0

100.5

101.0

Jan-

14

Jan-

14

Mar

-14

Apr-

14

May

-14

May

-14

Jun-

14

Jul-1

4

Aug-

14

Index

88

90

92

94

96

98

100

102

104

106

92

93

94

95

96

97

98

99

100

101

102

Jul-1

3

Aug-

13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr-

14

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

European Long-only fundamental funds (LHS)

Composite Momentum: World (RHS)

Source: Nomura Quantitative strategy

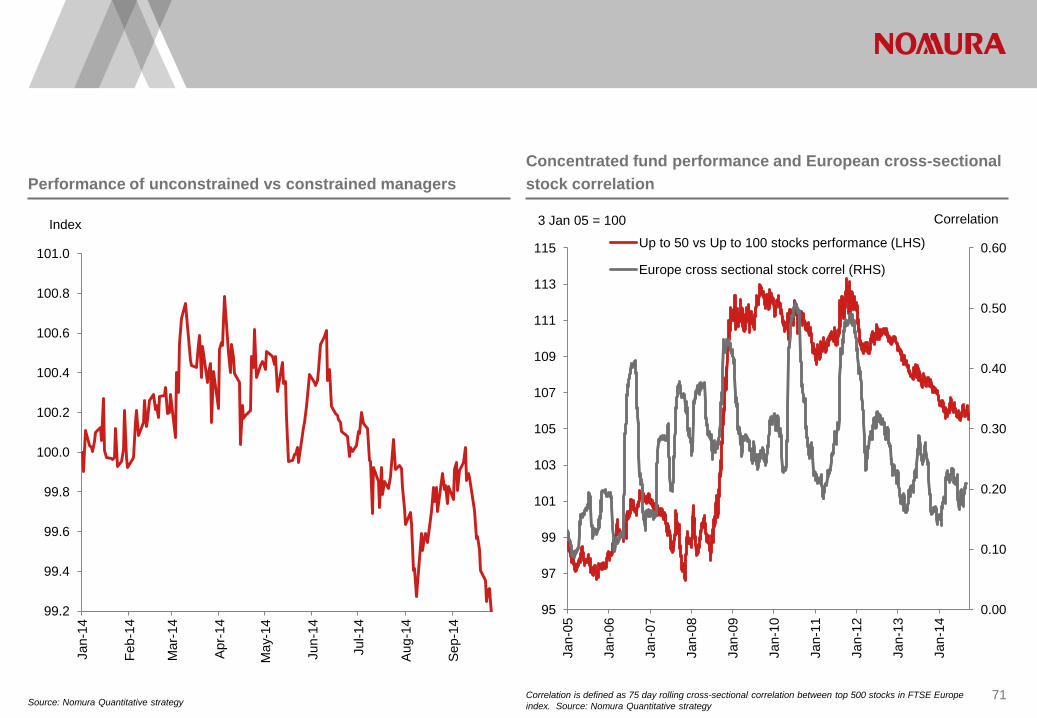

Performance of unconstrained vs constrained managers Concentrated fund performance and European cross-sectional stock correlation

Correlation is defined as 75 day rolling cross-sectional correlation between top 500 stocks in FTSE Europe index. Source: Nomura Quantitative strategy

71

99.2

99.4

99.6

99.8

100.0

100.2

100.4

100.6

100.8

101.0

Jan-

14

Feb-

14

Mar

-14

Apr-

14

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Index

0.00

0.10

0.20

0.30

0.40

0.50

0.60

95

97

99

101

103

105

107

109

111

113

115

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Correlation 3 Jan 05 = 100

Up to 50 vs Up to 100 stocks performance (LHS)

Europe cross sectional stock correl (RHS)

72 Source: Nomura Quantitative Strategy research

Asset share of fundamental managers with more than or fewer than 100 stocks

0.0

0.5

1.0

1.5

2.0

2.5

0

5

10

15

20

25

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

% %

Up to 100 >100

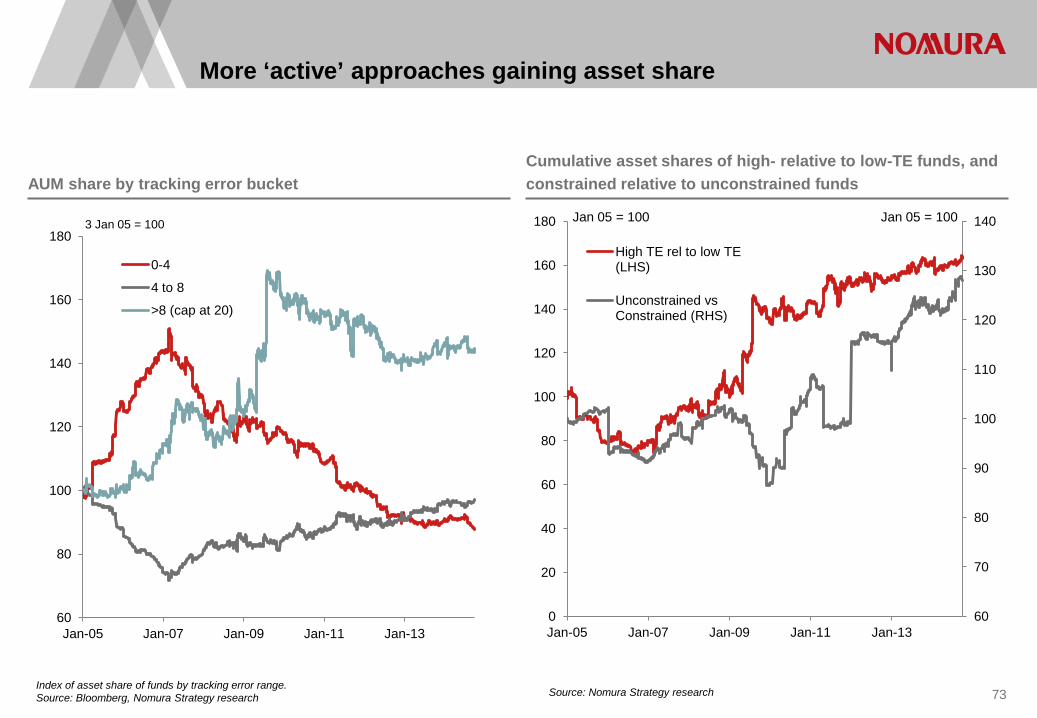

More ‘active’ approaches gaining asset share

Index of asset share of funds by tracking error range. Source: Bloomberg, Nomura Strategy research

AUM share by tracking error bucket Cumulative asset shares of high- relative to low-TE funds, and constrained relative to unconstrained funds

Source: Nomura Strategy research 73

60

80

100

120

140

160

180

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

3 Jan 05 = 100

0-4

4 to 8

>8 (cap at 20)

60

70

80

90

100

110

120

130

140

0

20

40

60

80

100

120

140

160

180

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

Jan 05 = 100 Jan 05 = 100

High TE rel to low TE (LHS)

Unconstrained vs Constrained (RHS)

-1500

-1000

-500

0

500

1000

1500

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

USDbn

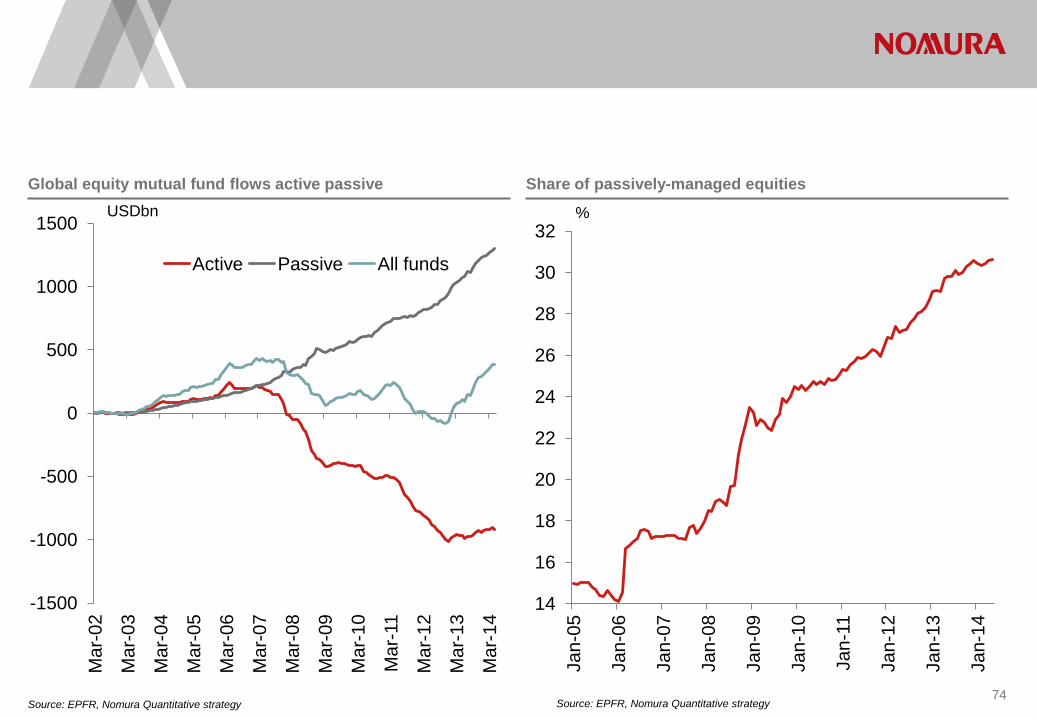

Active Passive All funds

Source: EPFR, Nomura Quantitative strategy 74

Global equity mutual fund flows active passive Share of passively-managed equities

Source: EPFR, Nomura Quantitative strategy

14

16

18

20

22

24

26

28

30

32

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

%

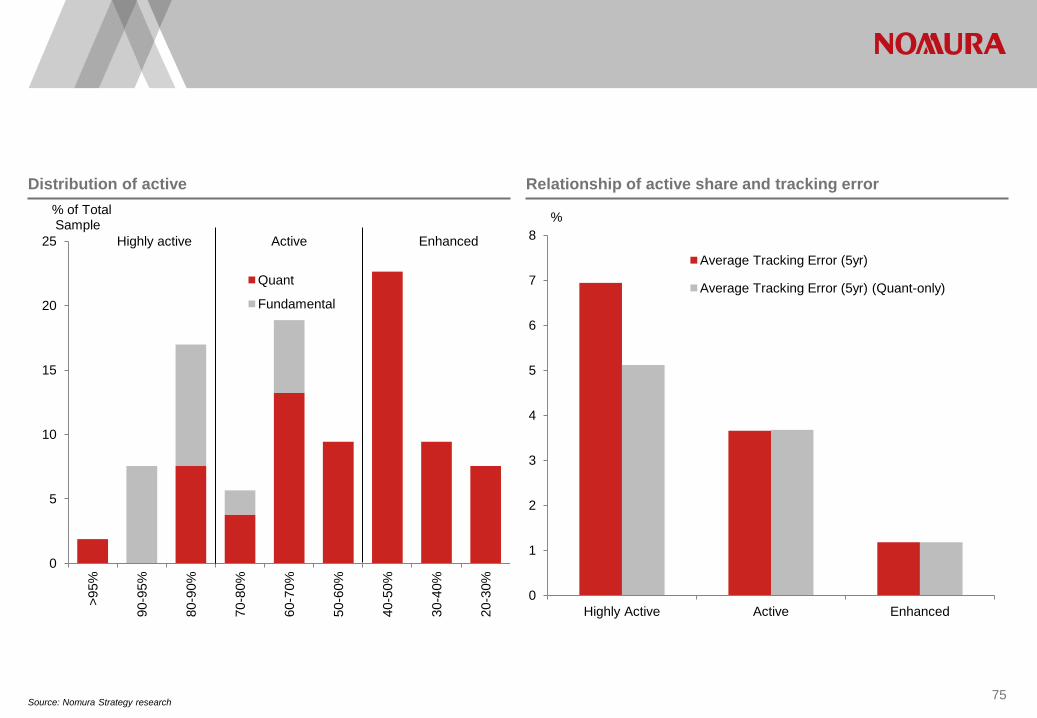

Source: Nomura Strategy research 75

Distribution of active Relationship of active share and tracking error

0

5

10

15

20

25

>95%

90-9

5%

80-9

0%

70-8

0%

60-7

0%

50-6

0%

40-5

0%

30-4

0%

20-3

0%

% of Total Sample

Quant

Fundamental

Enhanced Active Highly active

0

1

2

3

4

5

6

7

8

Highly Active Active Enhanced

%

Average Tracking Error (5yr)

Average Tracking Error (5yr) (Quant-only)

Active share

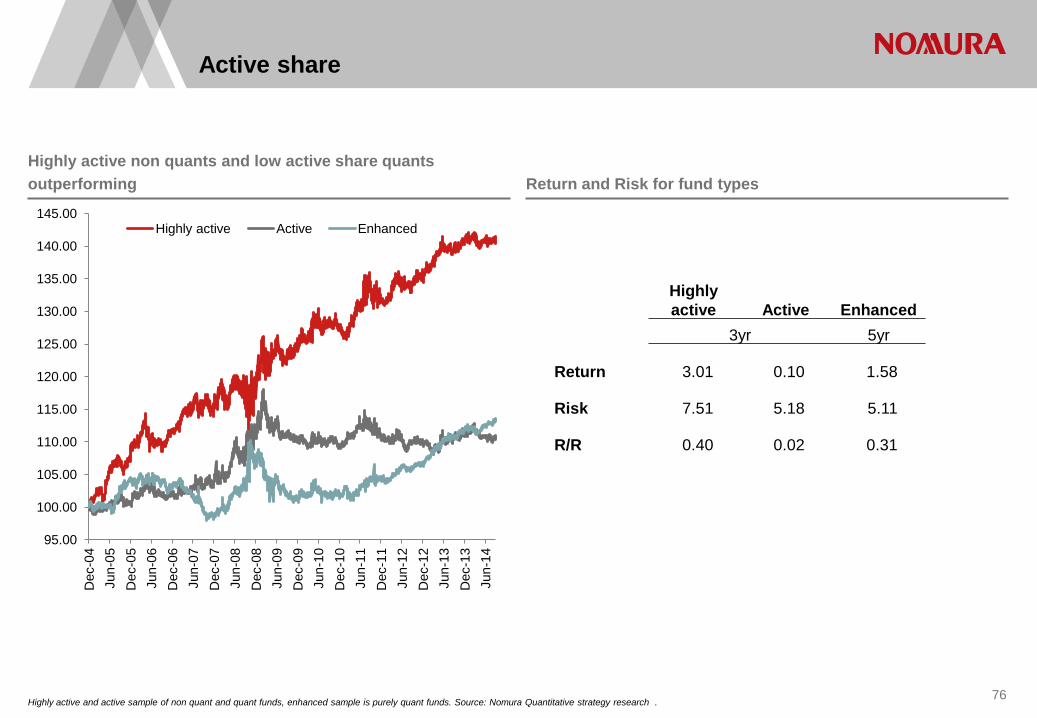

Highly active and active sample of non quant and quant funds, enhanced sample is purely quant funds. Source: Nomura Quantitative strategy research . 76

Highly active non quants and low active share quants outperforming Return and Risk for fund types

Highly active Active Enhanced

3yr 5yr

Return 3.01 0.10 1.58

Risk 7.51 5.18 5.11

R/R 0.40 0.02 0.31

95.00

100.00

105.00

110.00

115.00

120.00

125.00

130.00

135.00

140.00

145.00

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Jun-

14

Highly active Active Enhanced

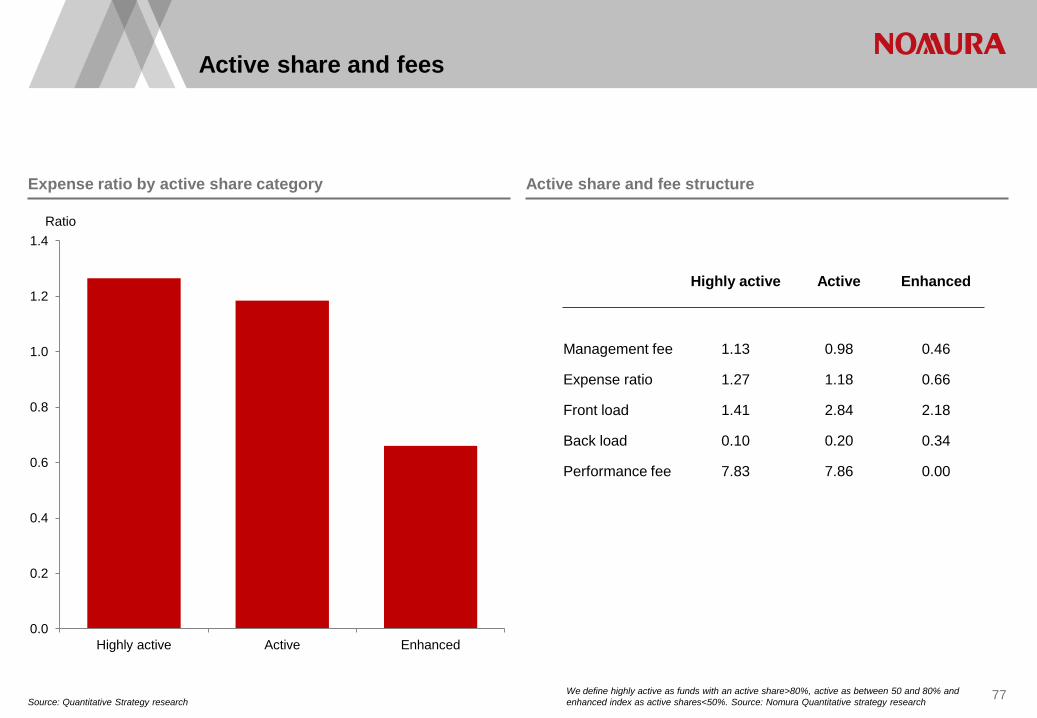

Active share and fees

Source: Quantitative Strategy research 77

Expense ratio by active share category Active share and fee structure

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Highly active Active Enhanced

Ratio

Highly active Active Enhanced

Management fee 1.13 0.98 0.46

Expense ratio 1.27 1.18 0.66

Front load 1.41 2.84 2.18

Back load 0.10 0.20 0.34

Performance fee 7.83 7.86 0.00

We define highly active as funds with an active share>80%, active as between 50 and 80% and enhanced index as active shares<50%. Source: Nomura Quantitative strategy research

78

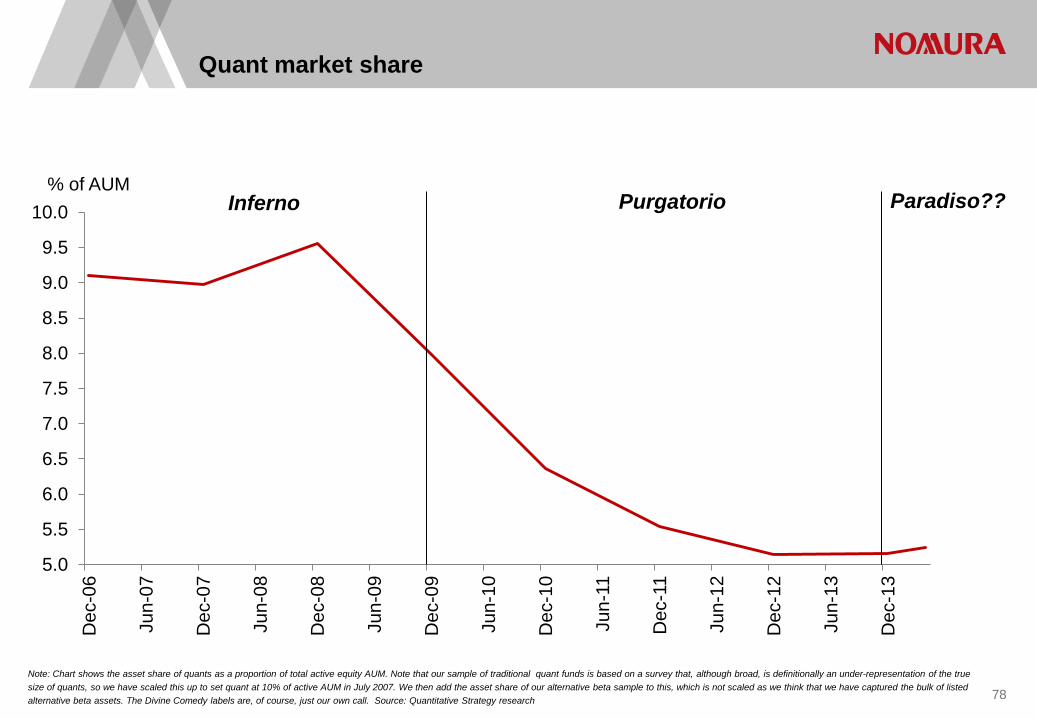

Note: Chart shows the asset share of quants as a proportion of total active equity AUM. Note that our sample of traditional quant funds is based on a survey that, although broad, is definitionally an under-representation of the true size of quants, so we have scaled this up to set quant at 10% of active AUM in July 2007. We then add the asset share of our alternative beta sample to this, which is not scaled as we think that we have captured the bulk of listed alternative beta assets. The Divine Comedy labels are, of course, just our own call. Source: Quantitative Strategy research

Quant market share

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

% of AUM Inferno

Purgatorio Paradiso??

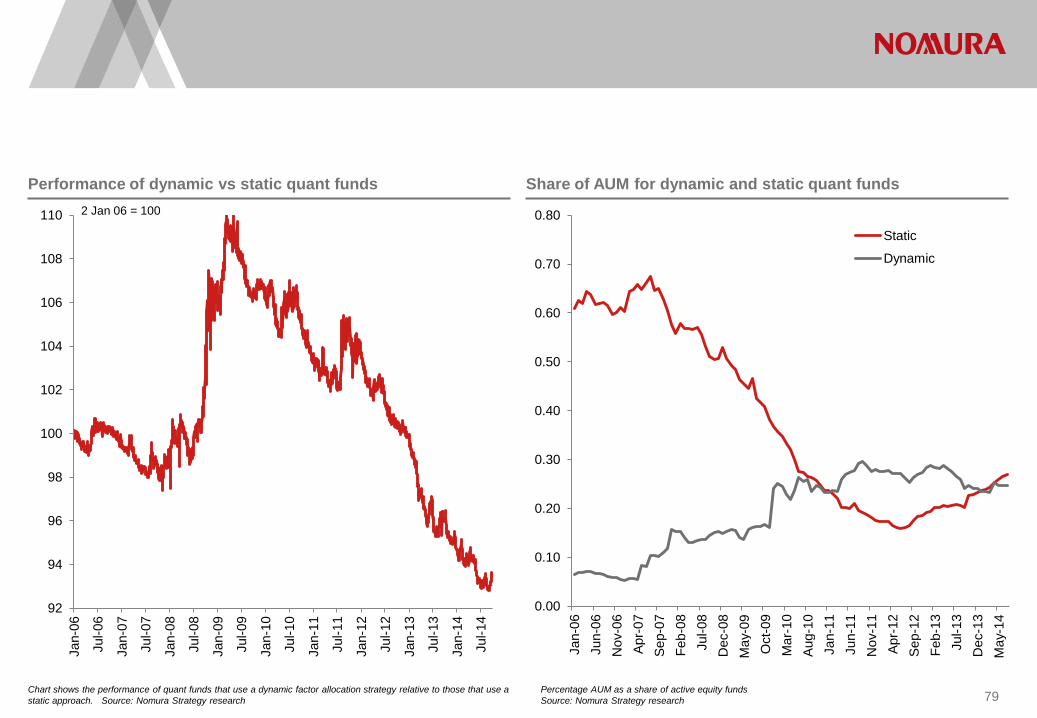

Chart shows the performance of quant funds that use a dynamic factor allocation strategy relative to those that use a static approach. Source: Nomura Strategy research

Performance of dynamic vs static quant funds Share of AUM for dynamic and static quant funds

79 Percentage AUM as a share of active equity funds Source: Nomura Strategy research

92

94

96

98

100

102

104

106

108

110

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

2 Jan 06 = 100

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Jan-

06

Jun-

06

Nov

-06

Apr-

07

Sep-

07

Feb-

08

Jul-0

8 D

ec-0

8 M

ay-0

9 O

ct-0

9 M

ar-1

0 Au

g-10

Ja

n-11

Ju

n-11

N

ov-1

1 Ap

r-12

Se

p-12

Fe

b-13

Ju

l-13

Dec

-13

May

-14

Static

Dynamic

Performance of funds with and without discretion

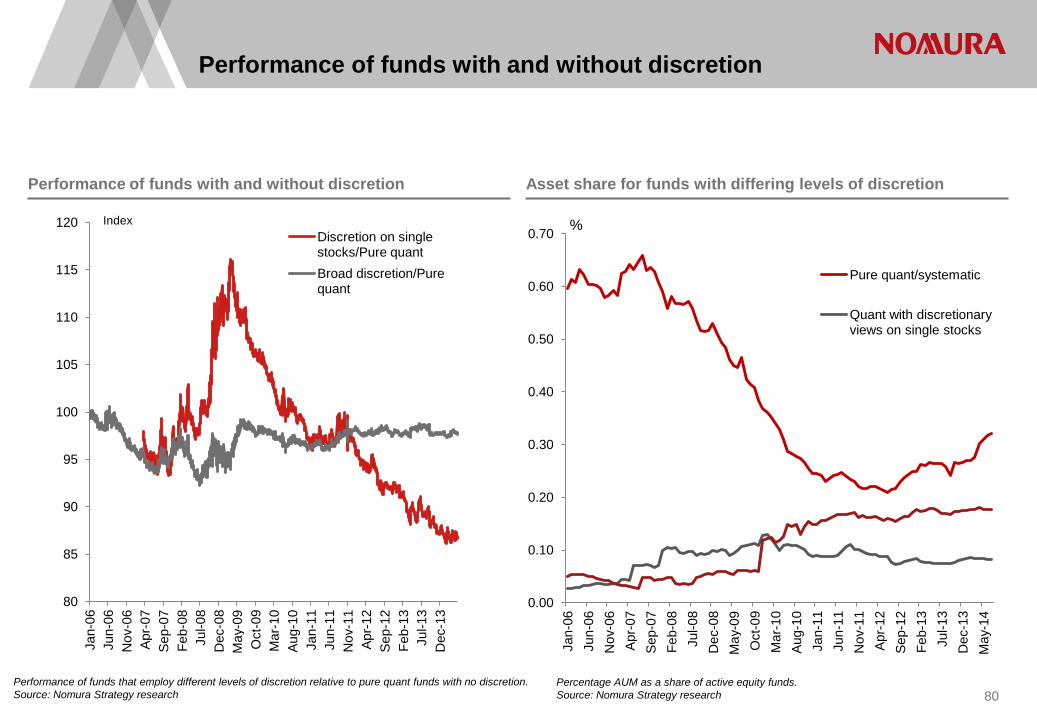

Performance of funds that employ different levels of discretion relative to pure quant funds with no discretion. Source: Nomura Strategy research

Performance of funds with and without discretion Asset share for funds with differing levels of discretion

80 Percentage AUM as a share of active equity funds. Source: Nomura Strategy research

80

85

90

95

100

105

110

115

120

Jan-

06

Jun-

06

Nov

-06

Apr-

07

Sep-

07

Feb-

08

Jul-0

8 D

ec-0

8 M

ay-0

9 O

ct-0

9 M

ar-1

0 Au

g-10

Ja

n-11

Ju

n-11

N

ov-1

1 Ap

r-12

Se

p-12

Fe

b-13

Ju

l-13

Dec

-13

Discretion on single stocks/Pure quant Broad discretion/Pure quant

Index

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Jan-

06

Jun-

06

Nov

-06

Apr-

07

Sep-

07

Feb-

08

Jul-0

8 D

ec-0

8 M

ay-0

9 O

ct-0

9 M

ar-1

0 Au

g-10

Ja

n-11

Ju

n-11

N

ov-1

1 Ap

r-12

Se

p-12

Fe

b-13

Ju

l-13

Dec

-13

May

-14

Pure quant/systematic

Quant with discretionary views on single stocks

%

Source: Quantitative Strategy research 81

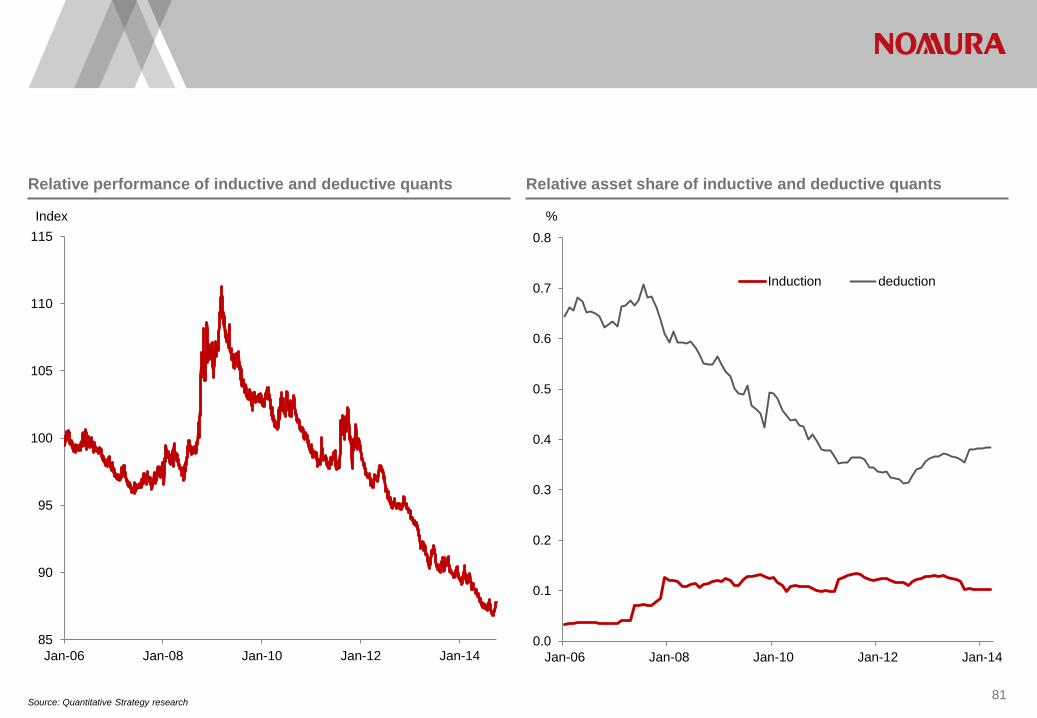

Relative performance of inductive and deductive quants Relative asset share of inductive and deductive quants

85

90

95

100

105

110

115

Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

Index

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Jan-06 Jan-08 Jan-10 Jan-12 Jan-14

%

Induction deduction

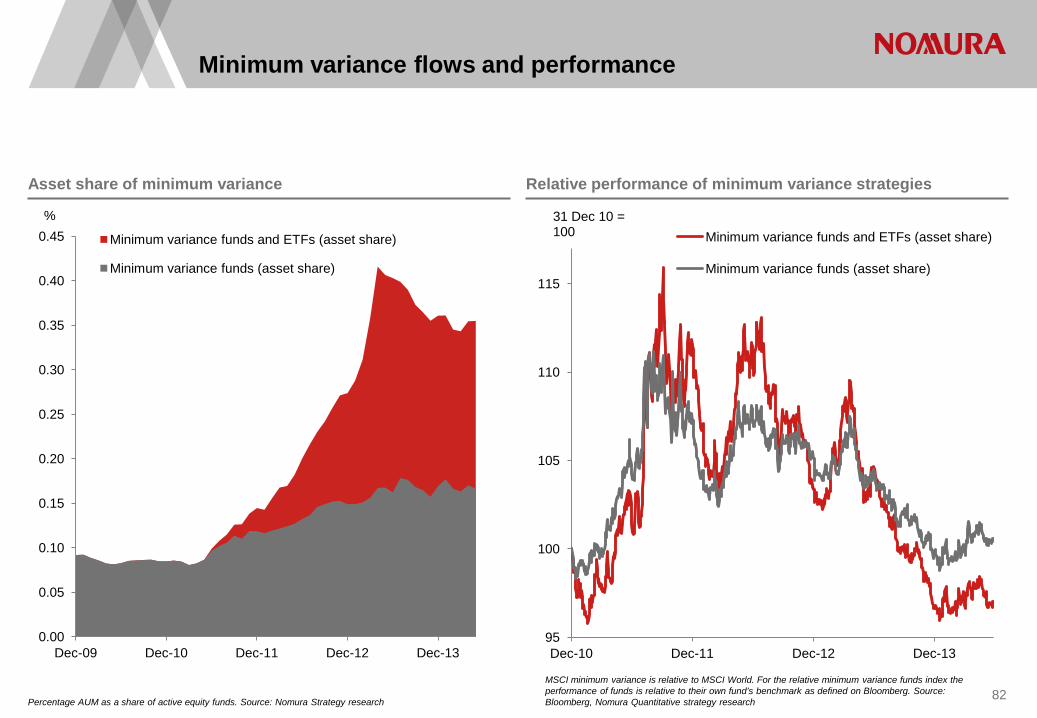

Minimum variance flows and performance

Percentage AUM as a share of active equity funds. Source: Nomura Strategy research 82

Asset share of minimum variance Relative performance of minimum variance strategies

MSCI minimum variance is relative to MSCI World. For the relative minimum variance funds index the performance of funds is relative to their own fund’s benchmark as defined on Bloomberg. Source: Bloomberg, Nomura Quantitative strategy research

95

100

105

110

115

Dec-10 Dec-11 Dec-12 Dec-13

31 Dec 10 = 100 Minimum variance funds and ETFs (asset share)

Minimum variance funds (asset share)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

%

Minimum variance funds and ETFs (asset share)

Minimum variance funds (asset share)

Minimum variance: the volatility advantage and valuations

Volatility of the MSCI low volatility index less volatility of the MSCI World index, rolling 30-day periods. Source: Datastream, Bloomberg, Nomura Strategy research 83