Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

Non‐Profit Cost Allocation Plan StrategiesMastering the State's Tax Reform and Planning for Flow‐Through Income, Tax Credits and Other Issues

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, JULY 26, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Hydeh Ghaffari Senior Partner Ghaffari Zaragoza Oakland CalifHydeh Ghaffari, Senior Partner, Ghaffari Zaragoza, Oakland, Calif.

Colette Kamps, Senior Manager, Henry & Horne, Scottsdale, Ariz.

Jean Gilbert, Outsourcing Senior Manager, Raffa, P.C., Washington, D.C.

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Attendees must stay on the line for at least 100 minutes in order to qualify for a full 2 credits of CPE. Attendance is monitored as required by NASBA.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

N P fit C t All ti Pl Non‐Profit Cost Allocation Plan Strategies Seminar

July 26, 2011

Colette Kamps, Henry & [email protected]

Hydeh Ghaffari, Ghaffari [email protected]

Jean Gilbert, Raffa, P.C. [email protected]

Today’s Program

Tying Together Three Frameworks[Hydeh Ghaffari]

Slide 7 – Slide 15

Definitions Of Relevant Concepts[Colette Kamps]

Slide 16 – Slide 26

GAAP/Tax Differences And Federal Awards[Hydeh Ghaffari]

Slide 27 – Slide 36

Determining An Allocation Methodology[Jean Gilbert]

Slide 37 – Slide 47

TYING TOGETHER THREEHydeh Ghaffari, Ghaffari Zaragoza

TYING TOGETHER THREE FRAMEWORKS

Allocating Costs: Information Availability

• Financial statements

• Audited financial statements open to public inspection in some statesso e states

• Made available to funding sources by management

• Increasingly posted on NFPs’ websites

• Tax returns

• Form 990 is open for public inspectionForm 990 is open for public inspection

• Posted at Guidestar

8

Allocating Costs: Importance

• Measure of stewardship

• Increasing public scrutiny• Increasing public scrutiny

• Watchdog groups

• Donors

• Advisors

• Faulty bookkeeping• Faulty bookkeeping

• Intentional misrepresentation

9

Allocating Costs: Uses

• Informed decision-making

• Externally

― Governmental funding sourcesGovernmental funding sources

― Private funding sources

― Watchdog groups (rating)

• Internally

― Cost of program activity or a project within the activity

Full recovery of costs― Full recovery of costs

― Whether to respond to an RFP

― Self-evaluation

10

Allocating Costs: Framework

• Cost assignment

• Cost directly benefits the final cost objective • Cost directly benefits the final cost objective.

• Cost allocation

• Cost benefits two or more final cost objectives, to a degree.

― Cost allocation basisCost allocation basis

― Cost allocation methods

11

Allocating Costs: Framework (Cont.)• GAAP

• ASC 958-720-45• AICPA A&A Guide, Chap. 13• Required at entity level

― Program activities― Administration (management and general)― Fundraising― Membership

• Internal Revenue Service• Part IX: Statement of Functional Expenses

― Program services ― Management and general― Fundraising

R i d f 501( )(3) d 501( )(4) i ti d t i t t• Required for 501(c)(3) and 501(c)(4) organizations and certain trusts

12

Allocating Costs: Cost Assignment• Activities (GAAP) ( )

• Program activities (not a funding source)

― Provider trainings

Respite services― Respite services

― Daycare services

• Administration (management and general)

― Overall administration of the organization (governance, marketing, strategic decision-making, financing, etc.)

― Obtaining and responding to RFP related to exchange transactions

• Fundraising

― Solicitation of contributions

• Membership development (Not donor development)

13

Allocating Costs: Cost Allocation

• Cost benefiting one or more activities as defined in the previous slide

• Facility-related costs

― Operations (copier, rent, postage, etc.)( )

― Cost of people maintaining the facility

• Joint activities

― Cost of an activity with a fundraising component― Cost of an activity with a fundraising component

• Cost benefiting several projects within an activity

• Provider training

h• Training the trainers

• Cost benefiting various population served within an activity

• E.g., residents of Alameda County

• People affected by HIV virus

14

Allocating Costs: Definition• Final cost objectiveFinal cost objective

• A project, or

• A program activity, or

• Certain population, or

• An award, or

• Another direct activity of an entity for which costs can be • Another direct activity of an entity for which costs can be accumulated

• Direct cost

• Cost that can be assigned directly to a final cost objective

• Shared

• Cost for which a cost allocation method and basis should Cost for which a cost allocation method and basis should be used

15

DEFINITIONS OF RELEVANTColette Kamps, Henry & Horne

DEFINITIONS OF RELEVANT CONCEPTS

Allocating Costs:What situations require cost allocations?

• Natural vs. functional

• Accounting standards• Require nonprofits to report expenses by functional

l fclassification• Voluntary health and welfare organizations are required to

present a Statement of Functional ExpensesV l t h lth d lf i ti F d f― Voluntary health and welfare organization: Formed for the purpose of performing voluntary services for various segments of society; organized for the benefit of the public. It concentrates efforts in attempt to solve healthpublic. It concentrates efforts in attempt to solve health and welfare problems.

17

Allocating Costs:Definitions and descriptions

• Program expenses

• Supporting services expenses

• Management and general expenses

F d i i • Fundraising expenses

18

Allocating Costs:Definitions and descriptions (Cont.)

• Program expenses: Expenses related to activities carried out to fulfill the mission; include both direct and indirect expenses

b f l l f l d b• Reporting by functional classification includes reporting by major program and supporting expenses• Need to determine the organization’s major programs

R i j d t d k l d f th i ti• Requires judgment and knowledge of the organization

19

Allocating Costs:Definitions and descriptions (Cont.)

• Considerations in determining major programs

• Report as a separate program if revenues or expenses are• Report as a separate program if revenues or expenses are > 10%

• Separately report programs making up (in total) at least 75% f t t l75% of total program expenses

• Is discrete program financial info available?

• Does management separately evaluate?g p y

• Form 990 requires disclosure/description of three largest programs

M th 10 b l d t il d• More than 10 may become overly detailed

20

Allocating Costs:Definitions and descriptions (Cont.)

• Supporting services expenses

• Management and general

• Fundraising

M b hi d l• Membership development

21

Allocating Costs:Definitions and descriptions (Cont.)

• Management and general expenses

• Relate to the overall direction of the organization• Relate to the overall direction of the organization

• Although indispensible to the organization, they are not identifiable with a specific program and are not a fundraising activity.

• Include oversight, business management, record keeping, budgeting, financing

22

Allocating Costs:Definitions and descriptions (Cont.)

• Common types of management/general expenses• Relating to board and committee meetings• Providing executive direction and organization planning

(salary of executive director)• Accounting, auditing, budgeting, financial reporting

d l (h )• Procuring and retaining personnel (human resources)• Office services (receptionist, mail distribution, filing duties)• Preparing the annual report• Disseminating information to the public about the

organization’s use of donated funds• Costs of advertising for ticket sales or admissions of a

performing arts organization museum zoo or similarperforming arts organization, museum, zoo, or similar organization

23

Allocating Costs:Definitions and descriptions (Cont.)

• Further consideration of advertising expenses

• Is the purpose of the advertising primarily to generate• Is the purpose of the advertising primarily to generate revenue from services/admissions, or is it primarily to promote the organization and its services?

• Is the related fee charged de minimis compared with the actual fair market value?

• Does the related fee help to increase the effectiveness of the organization’s programs?the organization s programs?

24

Allocating Costs:Definitions and descriptions (Cont.)

• Fundraising expenses: Costs related to activities that involve inducing potential donors to contribute assets (cash and non-cash), services or time

• Common types• Conducting of fund-raising campaigns

Conducting special events• Conducting special events• Maintaining donor lists• Preparing/distributing fund-raising materials

R iti l t ( if t i d)• Recruiting volunteers (even if revenue not recognized)• Conducting solicitations• Professional fund-raiser (do not net with revenue)

O h i i i i l i li i i ib i• Other activities involving soliciting contributions

25

Allocating Costs (Cont.)

Problems with fundraising costs/ratios• Problems with fundraising costs/ratios

• Allocations are often subjective, not objective.

• Some contributions do not requiring ongoing fund raising q g g g gexpenses (bequests, ongoing foundation support)

• Highly dependent on nature of the organization

• The ratio can be affected by temporary events (stage of a • The ratio can be affected by temporary events (stage of a capital campaign, the economy)

26

GAAP/TAX DIFFERENCES AND Hydeh Ghaffari, Ghaffari Zaragoza

FEDERAL AWARDS

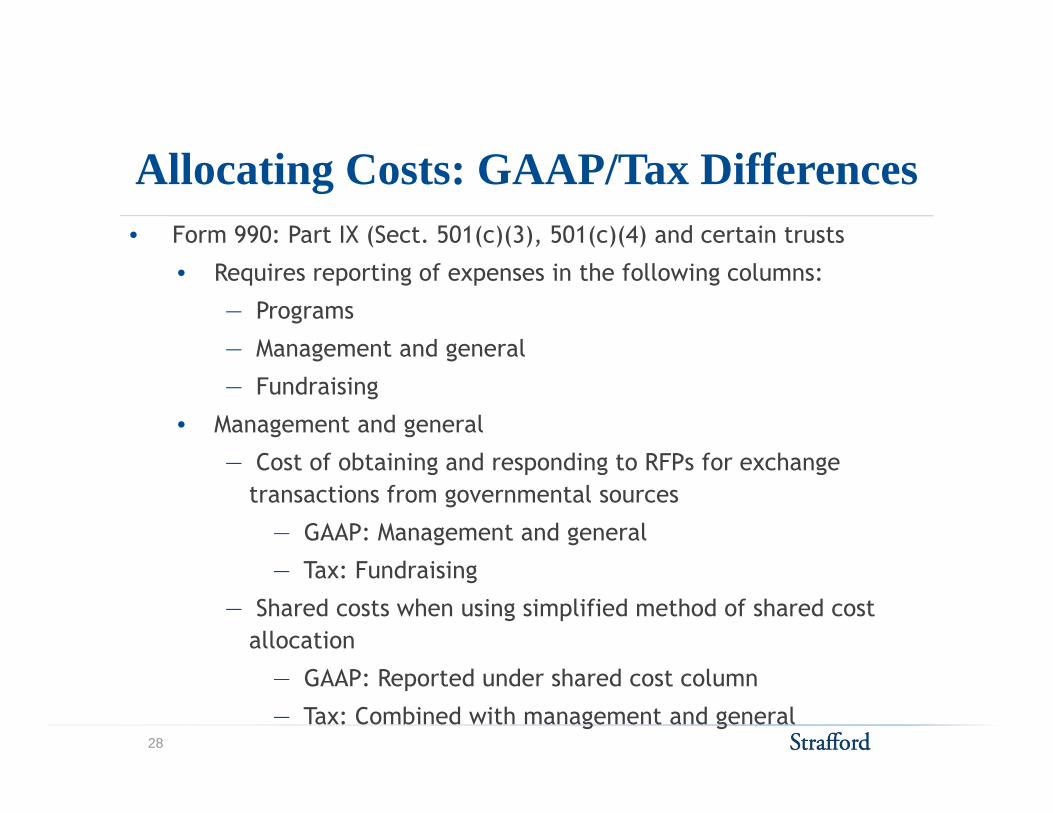

Allocating Costs: GAAP/Tax Differences• Form 990: Part IX (Sect. 501(c)(3), 501(c)(4) and certain trusts

• Requires reporting of expenses in the following columns:

― Programs

― Management and generalManagement and general

― Fundraising

• Management and general

Cost of obtaining and responding to RFPs for exchange ― Cost of obtaining and responding to RFPs for exchange transactions from governmental sources

― GAAP: Management and general

― Tax: Fundraising

― Shared costs when using simplified method of shared cost allocation

― GAAP: Reported under shared cost column

― Tax: Combined with management and general 28

Allocating Costs: GAAP/Tax Differences (Cont.)

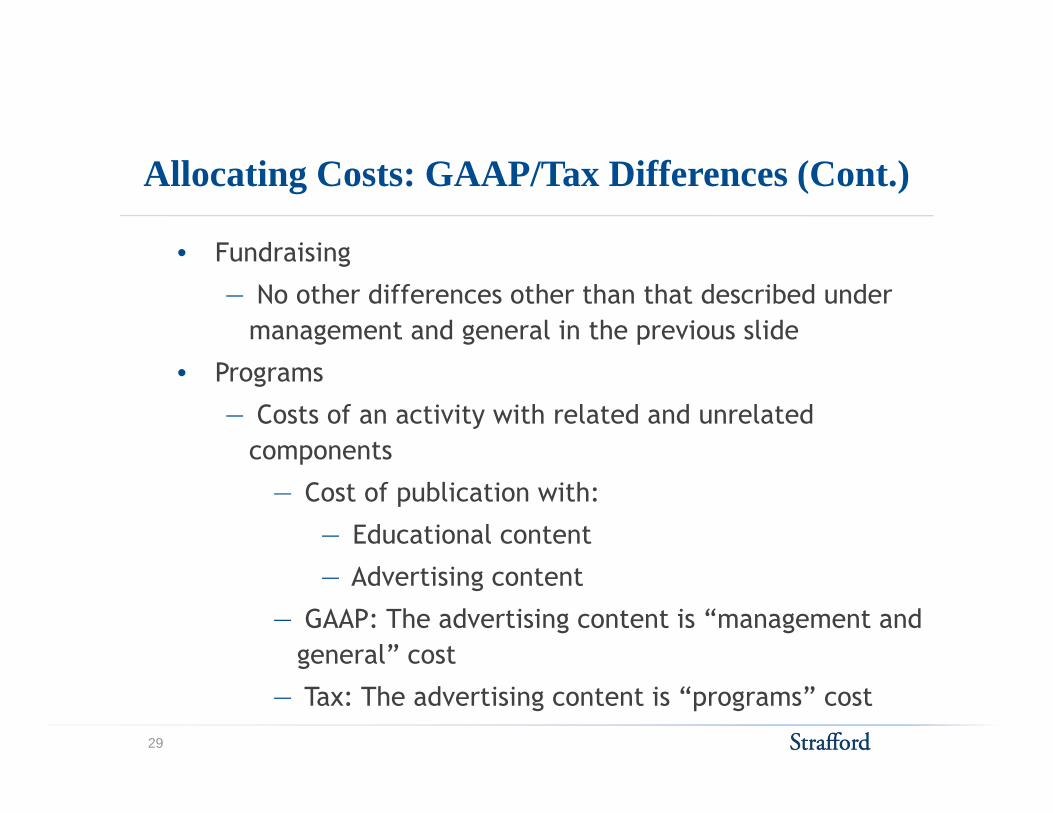

• Fundraising• Fundraising

― No other differences other than that described under management and general in the previous slide

• Programs

― Costs of an activity with related and unrelated componentscomponents

― Cost of publication with:

― Educational content

― Advertising content

― GAAP: The advertising content is “management and general” costgeneral cost

― Tax: The advertising content is “programs” cost

29

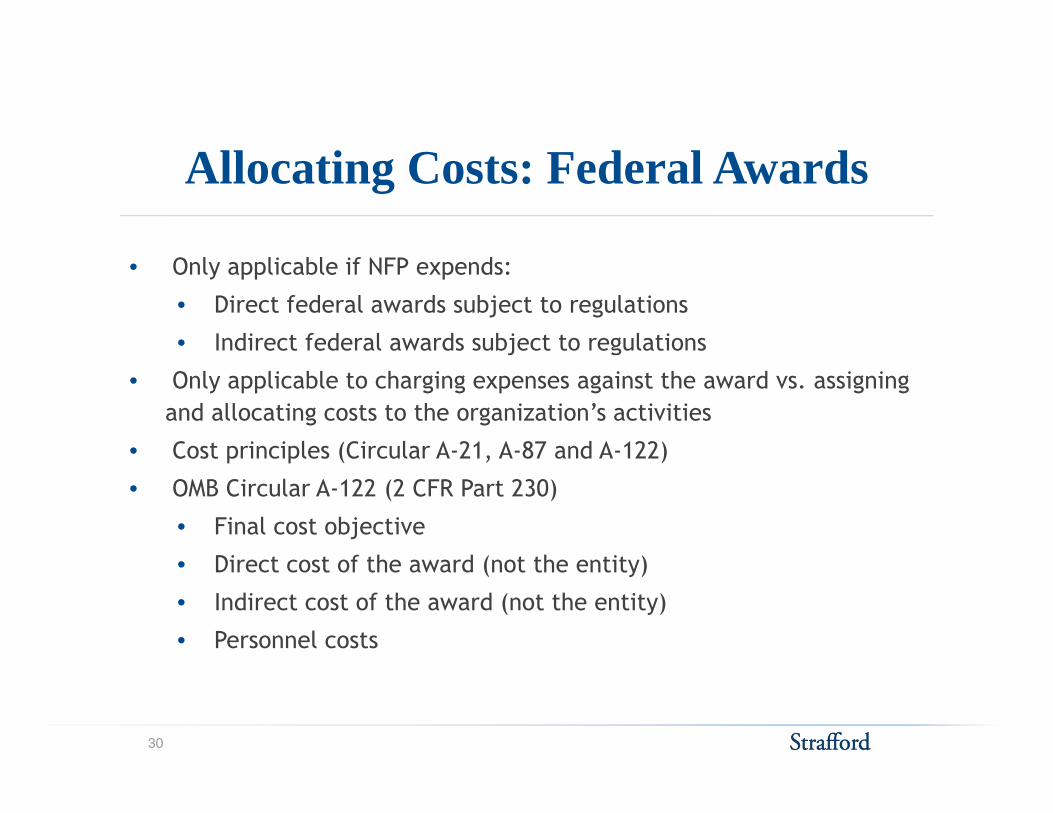

Allocating Costs: Federal Awards

• Only applicable if NFP expends:

• Direct federal awards subject to regulations

• Indirect federal awards subject to regulations

• Only applicable to charging expenses against the award vs. assigning and allocating costs to the organization’s activities

• Cost principles (Circular A-21, A-87 and A-122)Cost principles (Circular A 21, A 87 and A 122)

• OMB Circular A-122 (2 CFR Part 230)

• Final cost objective

Direct cost of the award (not the entity)• Direct cost of the award (not the entity)

• Indirect cost of the award (not the entity)

• Personnel costs

30

Allocating Costs: Federal Awards (Cont.)• Final cost objective

• An award, OR

― Providing training to foster parents residing in Alameda County

• A project, OR

― Providing training to foster parents

• A service, OR

― Providing training (Foster parents, adoptive parents, respite care providers, etc.)

• Other direct activity of an entity

― An employee should be clear about the effort spent in the cost objectiveobjective

― I worked 20% of my time providing training to foster parents

― I worked 20% on the project funded by Department of Health and Human Servicesand Human Services

31

Allocating Costs: Federal Awards (Cont.)

• Direct cost of the award• Direct cost of the final cost objective• Cost that can be directly identified with the cost objective

Payment to trainers providing the training ― Payment to trainers providing the training ― Material used during the training― Cost of facilities used for the training

• Indirect cost of the award• At cost objective level

― Cost that benefits two or more cost objectives― Salary of director of training (oversees all various types of

training)― Supplies cost (when supplies are used by all different types of

trainings)• At entity levelAt entity level

― Cost of organizational facilities (i.e. shared costs)― Management and general costs of the organization

32

Allocating Costs: Federal Awards (Cont.)

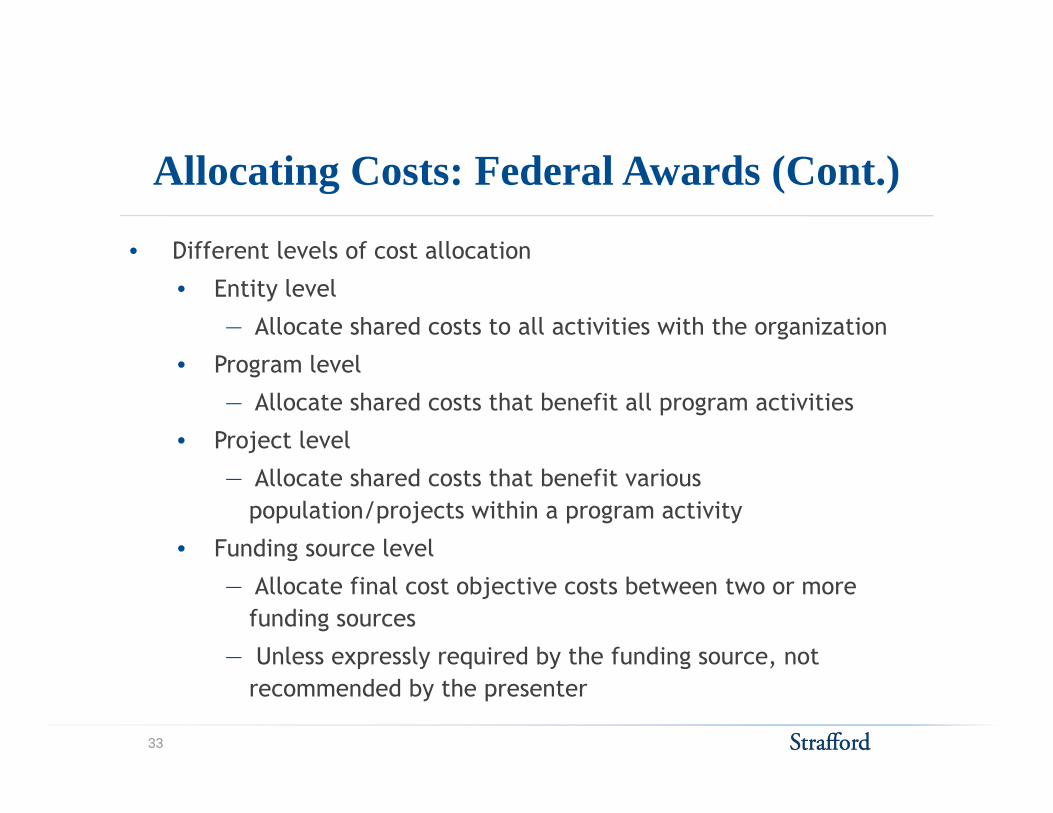

• Different levels of cost allocation• Different levels of cost allocation

• Entity level

― Allocate shared costs to all activities with the organization

P l l• Program level

― Allocate shared costs that benefit all program activities

• Project level

― Allocate shared costs that benefit various population/projects within a program activity

• Funding source levelg

― Allocate final cost objective costs between two or more funding sources

― Unless expressly required by the funding source, not Unless expressly required by the funding source, not recommended by the presenter

33

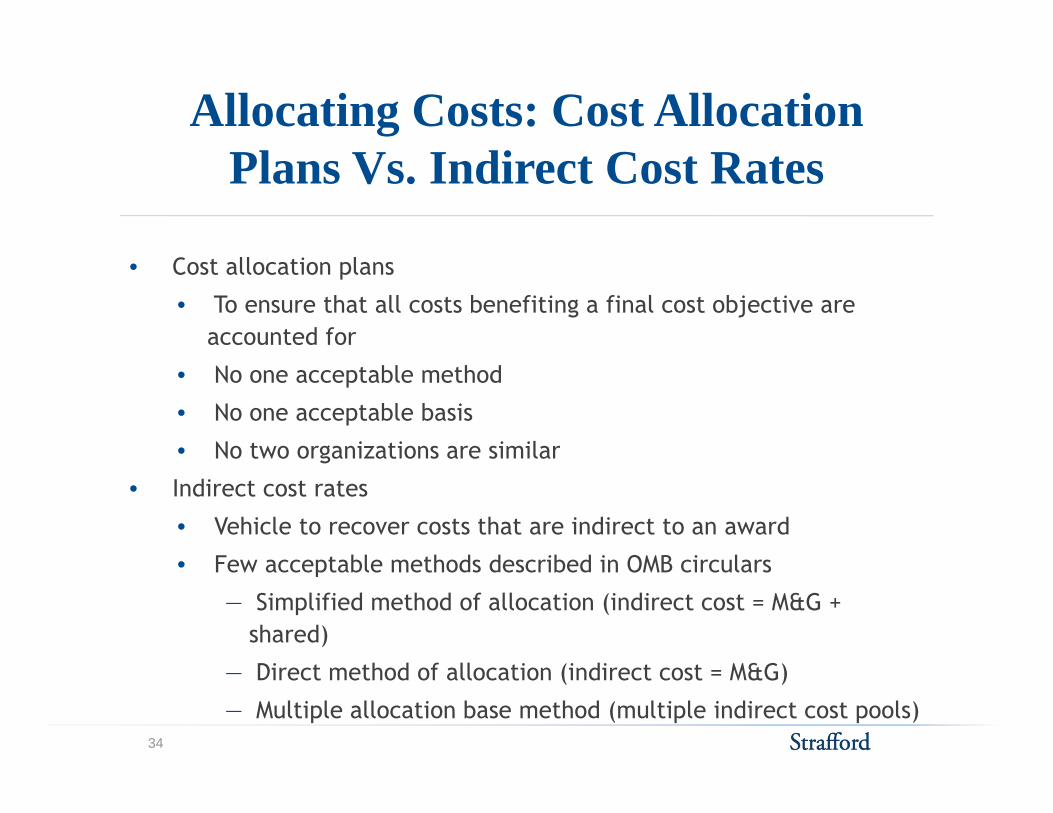

Allocating Costs: Cost AllocationPlans Vs. Indirect Cost Rates

• Cost allocation plans

• To ensure that all costs benefiting a final cost objective are accounted for

• No one acceptable method

• No one acceptable basis

• No two organizations are similarNo two organizations are similar

• Indirect cost rates

• Vehicle to recover costs that are indirect to an award

Few acceptable methods described in OMB circulars• Few acceptable methods described in OMB circulars

― Simplified method of allocation (indirect cost = M&G + shared)

Di h d f ll i (i di &G)― Direct method of allocation (indirect cost = M&G)

― Multiple allocation base method (multiple indirect cost pools)34

Allocating Costs: Cost AllocationPlans Vs. Indirect Cost Rates (Cont.)

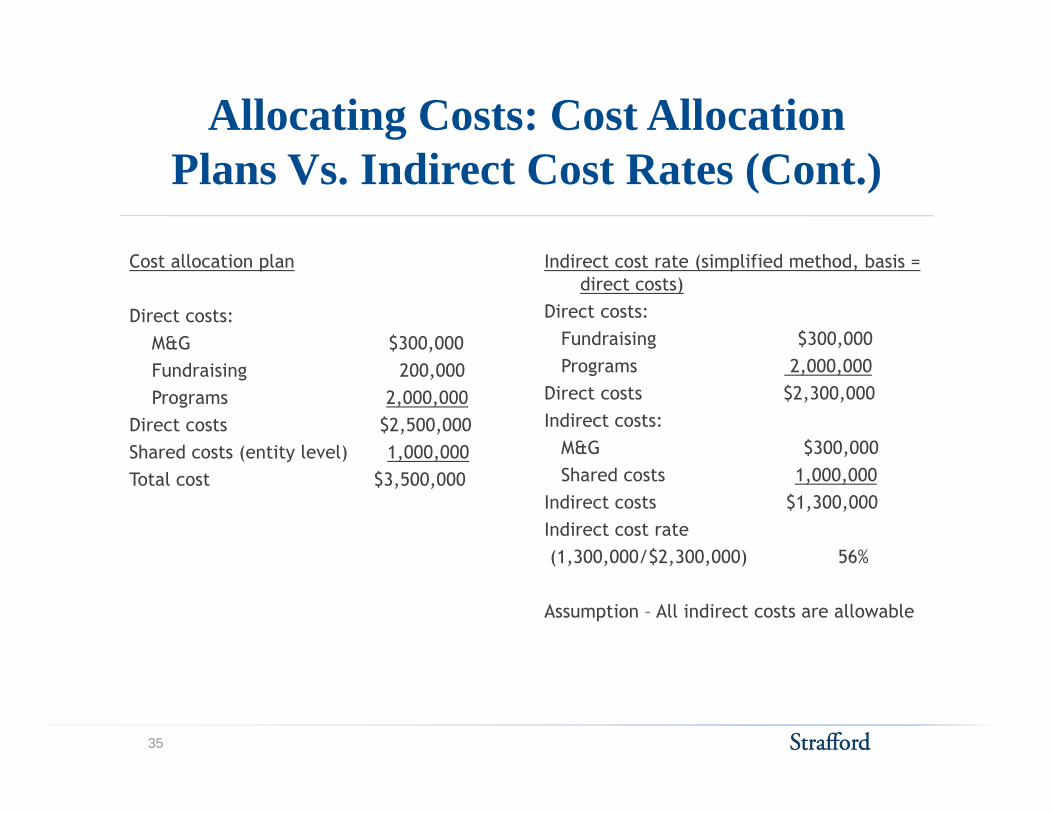

Cost allocation plan

Direct costs:M&G $300,000

Indirect cost rate (simplified method, basis = direct costs)

Direct costs:Fundraising $300,000

Fundraising 200,000Programs 2,000,000

Direct costs $2,500,000Shared costs (entity level) 1,000,000

Programs 2,000,000Direct costs $2,300,000Indirect costs:

M&G $300,000Shared costs (entity level) 1,000,000Total cost $3,500,000 Shared costs 1,000,000

Indirect costs $1,300,000Indirect cost rate (1,300,000/$2,300,000) 56%(1,300,000/$2,300,000) 56%

Assumption – All indirect costs are allowable

35

Allocating Costs: Federal Awards (Cont.)

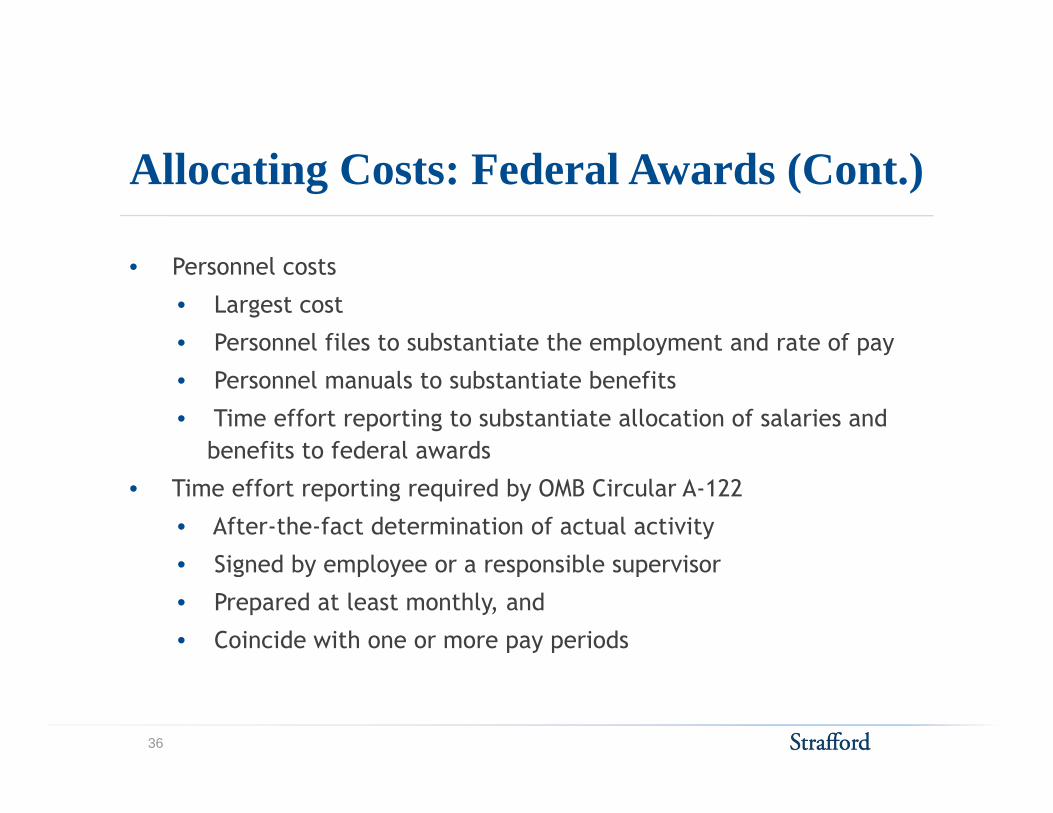

• Personnel costs

• Largest cost

• Personnel files to substantiate the employment and rate of pay

• Personnel manuals to substantiate benefits

• Time effort reporting to substantiate allocation of salaries and benefits to federal awardsbenefits to federal awards

• Time effort reporting required by OMB Circular A-122

• After-the-fact determination of actual activity

Signed by employee or a responsible supervisor• Signed by employee or a responsible supervisor

• Prepared at least monthly, and

• Coincide with one or more pay periods

36

DETERMINING AN Jean Gilbert, Raffa, P.C.

ALLOCATION METHODOLOGYMETHODOLOGY

Allocating Costs: Identify Goals

• The reason we allocate costs is to determine the true cost of • The reason we allocate costs is to determine the true cost of any activity.

• Function

• Program

• Project

38

Allocating Costs: Basic Definitions

• Understand the difference between direct and indirect costs• Understand the difference between direct and indirect costs

• Direct costs: Costs that are unique and exclusive to the activity

• Indirect costs: Costs that are shared resources used by the entire organization

39

Allocating Costs: Basic Definitions (Cont.)

• Indirect cost pool: This is a grouping of indirect costs that • Indirect cost pool: This is a grouping of indirect costs that must be allocated.

• Cost driver: The criterion upon which a cost pool is allocated

40

Allocating Costs: Drivers

• When a driver is identified it should be:• When a driver is identified, it should be:

• Reasonable

• Logical

• Defensible

41

Allocating Costs: Drivers (Cont.)

• Reasonable

• Common element to all activities• Common element to all activities

• Usually the highest expense

― Examples: Headcount, square footage, $ value of time, total direct expenses

42

Allocating Costs: Drivers (Cont.)

• Logical

• It is direct and proportional• It is direct and proportional.

• It is based on the efforts and costs of the activity itself, not the outcome.

― Example: Payroll based on effort expended on activity

43

Allocating Costs: Drivers (Cont.)

• Defensible

• The results are fair and consistent• The results are fair and consistent.

• The results can be duplicated.

• The methodology is documented.

― Example: The auditor can take your methodology and duplicate the resultsduplicate the results.

44

Allocating Costs: Drivers (Cont.)

• Examples of drivers

• IT costs for HQ and regional offices for a national • IT costs for HQ and regional offices for a national organization

― Number of employees per location

― Square footage used per location

― Payroll costs per location

45

Allocating Costs: Where To Allocate

Program services allocations: The cost pool is 100% allocated to all program services. (OMB)

Reciprocal allocations: The cost pool is allocated only to the extent that the driver allows costs to be allocated from the pool (GAAP)from the pool. (GAAP)

46

Allocating Costs: Best Practices

Use the same driver for multiple line items, in order to keep your analysis as simple as possible.

Be consistent. Use the same driver and allocation methodology every year. If you have a good reason to change drivers then recalculate the prior year for change drivers, then recalculate the prior year for comparability.

47

![Cost allocation joint cost [compatibility mode]](https://img.pdfslide.net/doc/110x75/54448861b1af9f740a8b49b9/cost-allocation-joint-cost-compatibility-mode.jpg)