Embed Size (px)

DESCRIPTION

Nonprofit Industry Studies 2006

Citation preview

Nonprofits 2006One Fabric, Different Threads

2

Study Objectives

Raise awareness of the industry and its place in Hawaii’s economy

Create a “landscape map” So organizations can “see where they fit and

who their neighbors are”

Initiate discussions with different stakeholders

Refine the capacity building efforts of HCF

3

Sources of Information

2006 & 2001 Hawaii Community Foundation State of the Industry surveys

GuideStar/National Center for Charitable Statistics

Focus groups & interviews with Executive Directors

Secondary sources

State of the Nonprofit Industry

5

The nonprofit industry plays a significant role in Hawaii’s economy…

Hawaii California United States

Expenses per Capita $3,018 $5,824 $2,438

Total Expenses $4 billion $84 billion $687 billion

Percentage of GD/SP 7.6% 6.3% 6.9%

Sources: Expenses - GuideStar 990 data

Hawaii Gross State Product - US Dept of Commerce (2004)

California & US GDP - SPEN Bay Area Nonprofit report

California & US expenses per capita - SPEN Bay Area Nonprofit report

Hawaii population - DBEDT data book

6

Also a major player in Hawaii’s workforce

The sector employs about 48,000 people about 8% of the state’s workforce

Approximately $1.45 billion dollars in wages about 7% of all wages paid in the state

Source: 1997 & 2002 economic census, as well as bea.gov (Bureau for Economic Analysis) since census doesn’t include government and military jobs

7

Increase in number of nonprofits

4,081

5,188

1,5742,076

0

1,000

2,000

3,000

4,000

5,000

6,000

2000 2001 2002 2003 2004 2005

Total Registered Filed Tax Return (revenues greater than $25,000)

Source: National Center for Charitable Statistics

27% increase

32% increase

8

Increase primarily in # of organizations with revenues less than $100,000

More than $5 million

7%

$100,000 - 499,999

26%

$500,000-999,999

9%

$1-5 million13%

Less than $100,000

45%

Source: National Center for Charitable Statistics

Less than $100,000

50%$500,000-999,999

7%

$1-5 million13%

More than $5 million

6%

$100,000 - 499,999

24%

2000 2005

Organizations filing a tax return, broken out by revenue levels

9

The mix within the industry has stayed roughly the same

Arts, Culture, and

Humanities16% Education

16%

Health9%

Environment and Animals

6%

Human Services

30%

International, Foreign Affairs

2%

Unknown7%Public,

Societal Benefit

10%

Religion Related

4%

Source: National Center for Charitable Statistics

10

Revenue increases…

$4,174,730,624

$2,249,241,123

$0

$500,000,000

$1,000,000,000

$1,500,000,000

$2,000,000,000

$2,500,000,000

$3,000,000,000

$3,500,000,000

$4,000,000,000

$4,500,000,000

$5,000,000,000

2000 2001 2002 2003 2004 2005 -projected

Total Rev Rev w/out largest

Source: National Center for Charitable Statistics

5% increase

32% increase

11

Increase in revenue has been mostly in Program Services and Contracts

16%

7%

34%

20%

4%

60%

15%

43%

0%

10%

20%

30%

40%

50%

60%

70%

Contributions,Gifts, & Grants

InvestmentIncome

ProgramServices and

Contracts

Dues, NetSales, & Other

Income

20012004

Source: National Center for Charitable Statistics

12

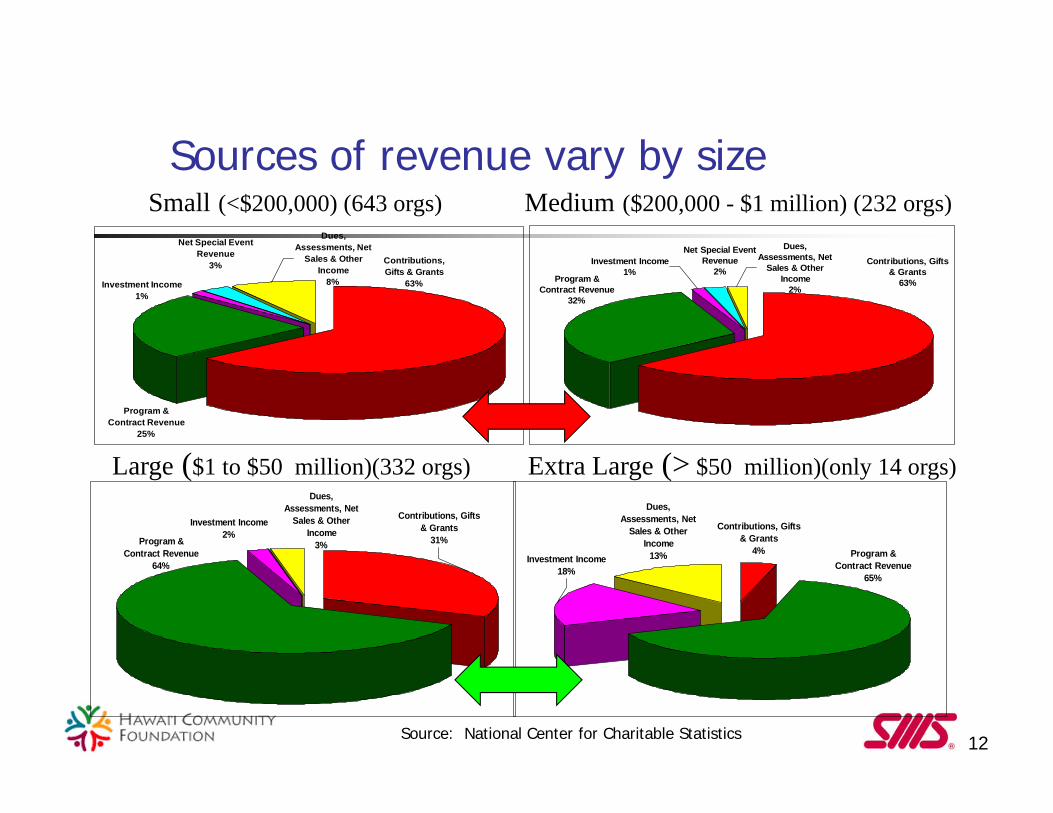

Sources of revenue vary by size

Program & Contract Revenue

25%

Dues, Assessments, Net

Sales & Other Income

8%

Contributions, Gifts & Grants

63%Investment Income1%

Net Special Event Revenue

3%

Contributions, Gifts & Grants

4%Investment Income

18%

Dues, Assessments, Net

Sales & Other Income

13% Program & Contract Revenue

65%

Net Special Event Revenue

2%Investment Income

1%Program &

Contract Revenue32%

Contributions, Gifts & Grants

63%

Dues, Assessments, Net

Sales & Other Income

2%

Program & Contract Revenue

64%

Dues, Assessments, Net

Sales & Other Income

3%

Investment Income2%

Contributions, Gifts & Grants

31%

Small (<$200,000) (643 orgs) Medium ($200,000 - $1 million) (232 orgs)

Large ($1 to $50 million)(332 orgs) Extra Large (> $50 million)(only 14 orgs)

Source: National Center for Charitable Statistics

13

Sources of revenue continues to vary significantly by sector

Dues, Net Sales, & Other Income *

16%

Program Services and Contracts

28%Investment Income

2%Net Special Events

Income2%

Contributions, Gifts, & Grants

52%

Dues, Net Sales, & Other Income *

6%

Net Special Events Income

1%

Investment Income1%

Contributions, Gifts, & Grants

47%Program Services

and Contracts45%

Program Services and Contracts

30%

Investment Income12%

Contributions, Gifts, & Grants

17%

Dues, Net Sales, & Other Income *

41%

Program Services and Contracts

85%

Investment Income1%

Dues, Net Sales, & Other Income *

6%

Contributions, Gifts, & Grants

8%

Arts & Humanities (284 orgs) Education (274 orgs)

Health (223 orgs) Human Services (428 orgs)

Source: National Center for Charitable Statistics

14

Sources of revenue (continued)

Dues, Net Sales, & Other Income *

10%

Contributions, Gifts, & Grants

71%

Net Special Events Income

1%

Investment Income3%

Program Services and Contracts

15%

Program Services and Contracts

18% Investment Income3%

Contributions, Gifts, & Grants

51%

Dues, Net Sales, & Other Income *

28%

et Special Events Income

1%

Investment Income8%

Program Services and Contracts

12%

Dues, Net Sales, & Other Income *

2% Contributions, Gifts, & Grants

77%

Dues, Net Sales, & Other Income *

1%

Program Services and Contracts

9%Net Special Events

Income1%

Investment Income1%

Contributions, Gifts, & Grants

88%

Environment & Animals (79) Public & Societal Benefit (150)

International (36) Religion Related (56)

Source: National Center for Charitable Statistics

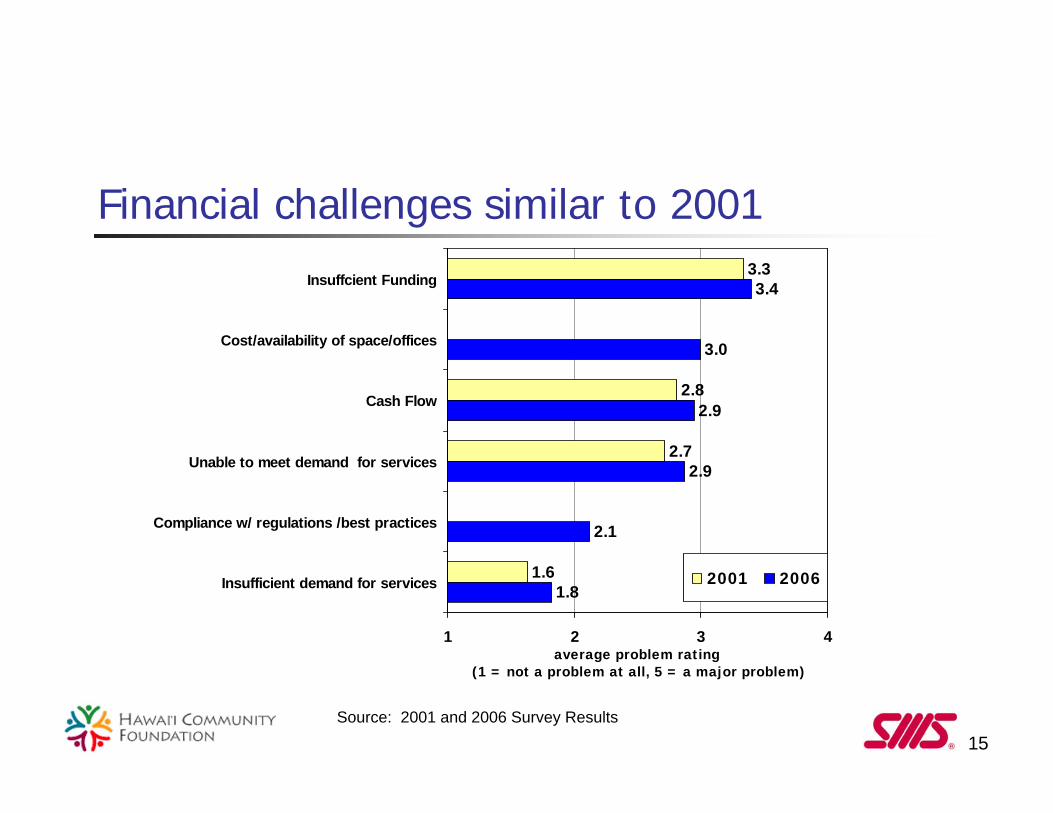

15

Financial challenges similar to 20013.3

2.8

2.7

1.6

3.4

3.0

2.9

2.9

2.1

1.8

1 2 3 4

Insuffcient Funding

Cost/availability of space/offices

Cash Flow

Unable to meet demand for services

Compliance w/ regulations /best practices

Insufficient demand for services

average problem rating (1 = not a problem at all, 5 = a major problem)

2001 2006

Source: 2001 and 2006 Survey Results

16

Attracting effective board members and quality staff are still the largest human resource issues

2.6

2.4

1.9

2.9

2.8

2.7

2.7

2.4

2.2

1 2 3

Attracting effective board members

Difficulty attracting quality staff

Providing staff development

Difficulty attracting/retaining volunteers

Supportive, rewarding corporate culture

High staff turnover

average problem rating (1 = not a problem at all, 5 = a major problem)

2001 2006

Source: 2001 and 2006 Survey Results. Turnover is significantly higher in 2006

17

Use of technology has increased significantly in the past five years

Source: 2001 and 2006 Survey Results. Significant increase in use of all technology

72%

54%

38%

33%

31%

12%

96%

83%

77%

60%

60%

23%

21%

0% 25% 50% 75% 100%

Easy access to the Internet

Computerized accounting system

Operational Web site

Computerized database ofcontributors

Database systems

Offer online giving

MIS/Computer technician 2001 2006

18

Increase in formal planning

Source: 2001 and 2006 Survey Results; Significant difference between 2001 and 2006 in all areas except fundraising

32%

26%

40%

36%

56%

40%

45%

45%

52%

69%

0% 25% 50% 75% 100%

Marketing, Outreach

Operating agreements w ith othernonprofits

Fundraising

Measurement of organizational progress

Strategic planning

2001 2006

19

Three emerging themes for consideration

Diverse revenue mix of sectors create different challenges and pressures

Depending on who you are, growth may not be the answer

The competition for talent is heating up

20

Diverse revenue mix of sectors create different challenges and pressures

Dues, Net Sales, & Other Income *

16%

Program Services and Contracts

28%Investment Income

2%Net Special Events

Income2%

Contributions, Gifts, & Grants

52%

Dues, Net Sales, & Other Income *

6%

Net Special Events Income

1%

Investment Income1%

Contributions, Gifts, & Grants

47%

Program Services and Contracts

45%

Program Services and Contracts

30%

Investment Income12%

Contributions, Gifts, & Grants

17%

Dues, Net Sales, & Other Income *

41%

Program Services and Contracts

85%

Investment Income1%

Dues, Net Sales, & Other Income *

6%

Contributions, Gifts, & Grants

8%

Arts & Humanities Education

Health Human Services

Source: National Center for Charitable Statistics

21

Revenue mix (continued)

Dues, Net Sales, & Other Income *

10%

Contributions, Gifts, & Grants

71%

Net Special Events Income

1%

Investment Income3%

Program Services and Contracts

15%

Program Services and Contracts

18% Investment Income3%

Contributions, Gifts, & Grants

51%

Dues, Net Sales, & Other Income *

28%

Net Special Events Income

1%

Investment Income8%

Program Services and Contracts

12%

Dues, Net Sales, & Other Income *

2% Contributions, Gifts, & Grants

77%

Dues, Net Sales, & Other Income *

1%

Program Services and Contracts

9%Net Special Events

Income1%

Investment Income1%

Contributions, Gifts, & Grants

88%

Environment & Animals Public & Societal Benefit

International Religion Related

Source: National Center for Charitable Statistics

22

Sources of revenue

16%

7%

34%

20%

4%

60%

15%

43%

0%

10%

20%

30%

40%

50%

60%

70%

Contributions,Gifts, & Grants

InvestmentIncome

ProgramServices and

Contracts

Dues, NetSales, & Other

Income

20012004

Source: National Center for Charitable Statistics

23

State contracts for Health & Human Services have increased 18% between 2004 and 2006

$0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

$800,000,000

$900,000,000

2004 2005 2006

State contracts & Federal contracts issued through the State Est. Non-profit contracts

Source: State of Hawaii Office of Procurement Website

Note: Not all State Contracts for Health & Human Services go to non-profits therefore SMS estimated that 80% of all contracts makes up the non-profit contracts line

24

From 2001-2004, revenue grew faster than the number of organizations except for small organizations

32%

47%

12%

30%

16%

26%

0% 20% 40% 60%

Large ($1M - $100M)

Medium ($250,000 to $1M)

Small (Less than$250,000)

% change in revenue

% change in # orgs

Source: National Center for Charitable Statistics

25

Revenue challenges and opportunities

The numbers game Many more nonprofits, largely small Growth in contributions not keeping pace Affect certain sectors more than others

Implications Increase/diversify revenue segments Find creative means to contain expenses Are we reaching a carrying capacity issue?

26

Revenue challenges and opportunities

Revenue growth fueled by government Program services and contracts and grants Mostly affecting the H/HS sectors

Implications Efficiency/economies of scale important Changing mandates and short contracts make

focused mission more difficult Infrastructure investment required

27

Depending on who you are, growth may not be the answer

Many organizations feel compelled to grow—Why? Increase services and programs Strengthen financial condition Increase capacity by hiring staff Growth is an indicator of success

28

Different Organizational Characteristics

Small Organizations Narrow mission ED – hands on Few or no paid

employees Revenues more

reliant on donations Outcomes easy to

measure, but no funding to support

Large Organizations Broader mission, some

drift EDs more managerial Paid ED/Staff Revenues more reliant

on program services & contracts

Outcomes more difficult to measure, but required for funding

29

While most older organizations are large, there are still many long-lived small orgs

6%

10%

30%

54%

5%

21%

41%

33%

20%

18%

49%

12%

0% 10% 20% 30% 40% 50% 60%

Pre 1950s

1950-1969

1970-1989

1990-2006

Yea

r O

rg E

stab

lishe

d in

Haw

aii

Large ($1M - $49.9M)Medium ($200K - $999,999)

Small (under $200K)

Source: 2006 Survey Results

30

Small orgs have better indicators of financial wellness than medium size orgs

0% 10% 20% 30% 40% 50% 60%

Low

Medium

High

Fina

ncia

l Wel

lnes

s Le

vel

Large ($1M - $50M)

Medium ($200K-$1M)

Small (under $200K)

Source: GuideStar and 2006 Survey results. Significant difference (p=0.000)

31

Sources of revenue vary by size

Program & Contract Revenue

25%

Dues, Assessments, Net

Sales & Other Income

8%

Contributions, Gifts & Grants

63%Investment Income1%

Net Special Event Revenue

3%

Net Special Event Revenue

2%Investment Income

1%Program &

Contract Revenue32%

Contributions, Gifts & Grants

63%

Dues, Assessments, Net

Sales & Other Income

2%

Program & Contract Revenue

64%

Dues, Assessments, Net

Sales & Other Income

3%

Investment Income2%

Contributions, Gifts & Grants

31%

Small (<$200,000) (643) Medium ($200,000 - $1 million) (232)

Large ($1 to $50 million)(332)

Source: National Center for Charitable Statistics

32

Challenges of growth

Depending on the revenue source to fuel growth, it can stress organizational capacity, mission, systems, financial health, culture

Implications Be clear about benefits/outcomes Clear plan for investments and changes Think before you grow

33

The competition for talent is heating up 2.6

2.4

1.9

2.9

2.8

2.7

2.7

2.4

2.2

1 2 3

Attracting effective board members

Difficulty attracting quality staff

Providing staff development

Difficulty attracting/retaining volunteers

Supportive, rewarding corporate culture

High staff turnover

average problem rating (1 = not a problem at all, 5 = a major problem)

2001 2006

Source: 2001 and 2006 Survey Results. Turnover is significantly higher in 2006

34

Half of all nonprofit EDs are 55 years or older

0%

1%

13%

36%

38%

12%

0% 10% 20% 30% 40%

18-24

25-34

35-44

45-54

55-64

65 or older

Source: 2006 Survey Results

35

42% of Executive Directors expect to leave by the end of 2010

How long do you plan on staying in your current position?

7%

16%

19%

35%

24%

0% 10% 20% 30% 40%

Less than one year

1-2 years

3-5 years

More than 5 years

Don't know

Source: 2006 Survey Results

36

44% of organizations find it hard to attract effective board members

Level of concern with attracting effective board members

28%

11%

17%

30%

14%

0% 10% 20% 30% 40%

Not a problem at all

2

3

4

A major problem

Source: 2006 Survey Results

37

Number of board members: 13 Number of vacancies: 2-3 About half have term limits Length of term limits: 3-4 yrs Most current board members have

served for 3-6 years

Source: 2006 Survey Results

The law of averages for boards

38

Implications in the competition for talent

Retention as important as recruitment Finding ways to increase tenure of

leadership (staff and board)

New leadership will come from two sources Younger, civic-minded individuals Baby boomers

Mahalo!

Presentation available at: www.hawaiicommunityfoundation.org