Embed Size (px)

Citation preview

© 2014 Platts, McGraw Hill Financial. All rights reserved.

Natural Gas Market Update 2015 LDC/SCC ConferenceFredericksburg, VA

Chris Foster

October 7, 2015

Restrictions on Use: You may use the prices, indexes, assessments and other related information (collectively, “Data”) in this presentation only for your personal use. You may not publish, reproduce, distribute, retransmit, resell, create any derivative work from and/or otherwise provide access to Data or any portion thereof to any person (either within or outside your company including, but not limited to, via or as part of any internal electronic system or Internet site), firm or entity. Disclaimer: Platts, its affiliates and all of their third-party licensors disclaim any and all representations and warranties, express or implied, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use as to the data, or the results obtained by its use or as to the performance thereof. Limitation of Liability: In no event whatsoever shall Platts, its affiliates or their third-party licensors be liable for any indirect, special, incidental, punitive or consequential damages, including but not limited to loss of profits, trading losses, or lost time or goodwill, even if they have been advised of the possibility of such damages, whether in contract, tort, strict liability or otherwise. The Data is provided on an “as is” basis and your use of the Data is at your own risk. Copyright © 2013 by Platts, McGraw Hill Financial, Inc. All rights reserved. No portion of this publication may be photocopied, reproduced, retransmitted, put into a computer system or otherwise redistributed without prior authorization from Platts. Platts is a trademark of McGraw Hill Financial.

Today’s Agenda

US Supply Outlook Impact of Collapse in the Btu Gap Producer Efficiency Gains Financial Stress in the Oil Patch Canadian Imports

Northeast Focus Outlook for Northeast Production Pipeline Infrastructure Projects Demand Growth in VA/Southeast VA Pricing Outlook

US Demand Outlook Power Burn Industrial Mex Exports LNG Exports

Bullish or Bearish: Final Conclusions 2

US Supply Outlook

Tightening Btu Gap

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$/M

MB

tu E

qu

ival

en

t

WTI Brent Mont Belvieu - NonTET HH CAPP

Tightening Value Gap: Why It Matters for Natural Gas Markets

Reduced Supply Growth- Diminishing NGL/crude value uplift with associated gas.- Fewer $ from US banks/international players to fund producer

drilling activities. Reduced Demand Growth

- US exports (refined products, condensate, NGLs, poly-olefins, LNG/Mexico).

- Lessened incentive for fuel oil conversions/GTLs/nat. gas vehicles, ships, rail.

- Reduced US manufacturing cost advantage and slower industrial growth.

- More difficult price environment for Canadian oil sands: supply (production) and demand (nat. gas/power/C5+).

5

Bullish or Bearish: Which one grows faster/further going forward?

0%

10%

20%

30%

40%

50%

60%

70%

80%

IRRs: July 2014 vs. Sep 2015July'14 Sep' 15

Lower Crude/NGL Prices: Lower Returns

Source: BENTEK

6

August 2015 Price Assumptions: Gas = 12 month forward average curve for each regional pricing point (range $1.78 - $2.93/Mcf)Oil = 12 month forward average WTI +/- differential (range $37.14 - $52.57/barrel)NGLs = weighted average $/barrel, 12-mo forward average Mt. Belvieu prices (range $16.97 - $22.30/barrel)

Producers Quickly Respond to $60/bbl

7

0

500

1000

1500

2000

2500

$0

$20

$40

$60

$80

$100

$120

# o

f ac

tive

rig

s

WTI

($

/bb

l)

Rig Activity v. US Oil Prices

WTI Active Rigs

Source: Bentek, Platts, RigData ,data as of August 7, 2015

Huge Well Backlog Aiding Growth

8Source: : Rig Data May15; OH DNR Feb’15; PA DEP Mar’15

NE PA Dry

Well Inventory

(1,425 wells)

~2,500 Wells in Inventory

19 Bcf/d of ‘Trapped’

Production

Wet Marcellus/Utica

Well Inventory

(1,059 wells)

Producers continue to focus on core acreage to grow production

65%

70%

75%

80%

85%

90%

0

50

100

150

200

250

300

350

400

450

% C

ore

# W

ells

Percentage of Wells Drilled in Core

EF Total Core Total % Core

Source: Bentek, Rig Data, data as of May 2015 Core Counties Include: De Witt, Dimmit, Gonzales, Karnes, La Salle, McMullen and Webb

Remaining rigs drill faster and produce more

Source: RigData, Bentek

0

5

10

15

20

25

30

35

40

45

50

0

100

200

300

400

500

600

700

Anadarko Bakken DJ Eagle Ford Permian

# o

f d

ays

to d

rill

IP R

ate

s (b

/d)

IP Rates and Drill Times by Basin (2010 v. 2014)

2010 IP 2014 IP 2010 Drill Time 2014 Drill Time

10

Producers realizing an average of 15% reduction in drilling costs

11

*Data sample comprised of 20+ Producers

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

Williston Permian Marcellus Eagle Ford DJ

$ m

illio

n/w

ell

Average Well Cost by Basin (2014 v. 2015)

2014 Average Q1 2015 Average

Source: Bentek, producer presentations

↓15%↓19%

↓9% ↓16%

↓14%

154%

63%

22%/69%

Utica Dry$2.99

Haynesville$3.07

MarcellusDry

Source: BENTEK

Arkoma-Wood

$3.65

$2.11

Green River

$3.68

Dry Gas Play

Half-cycle Natural Gas Break-Evens

$4.66

$3.35Barnett

Fayetteville

$4.35 Piceance

$2.07

$4.22Montney

Duvernay

August 2015 Price Assumptions: Gas = 12 month forward average curve for each regional pricing point (range $1.78 - $2.93/Mcf)Oil = 12 month forward average WTI +/- differential (range $37.14 - $52.57/barrel)NGLs = weighted average $/barrel, 12-mo forward average Mt. Belvieu prices (range $16.97 - $22.30/barrel)

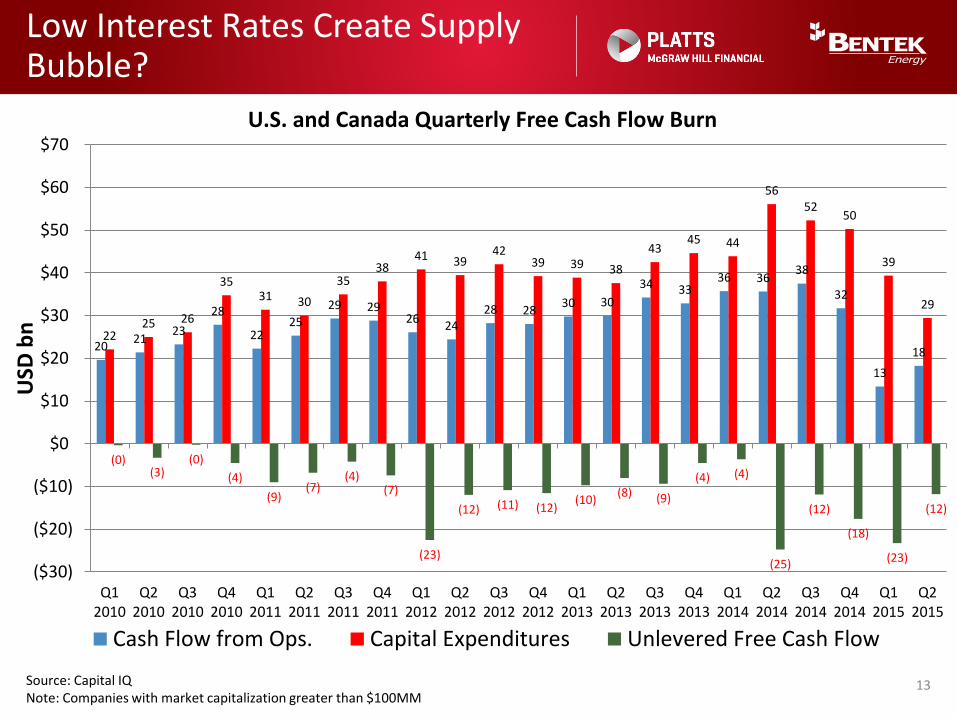

Low Interest Rates Create Supply Bubble?

13Source: Capital IQNote: Companies with market capitalization greater than $100MM

2021

23

28

2225

29 2926

2428 28

30 30

34 3336 36

38

32

13

1822

25 26

35 31 30

35 38

41 39 42

39 39 38

43 45 44

56 52

50

39

29

(0)(3)

(0)

(4)

(9)(7)

(4)(7)

(23)

(12) (11) (12)(10)

(8) (9)

(4) (4)

(25)

(12)

(18)

(23)

(12)

($30)

($20)

($10)

$0

$10

$20

$30

$40

$50

$60

$70

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

USD

bn

U.S. and Canada Quarterly Free Cash Flow Burn

Cash Flow from Ops. Capital Expenditures Unlevered Free Cash Flow

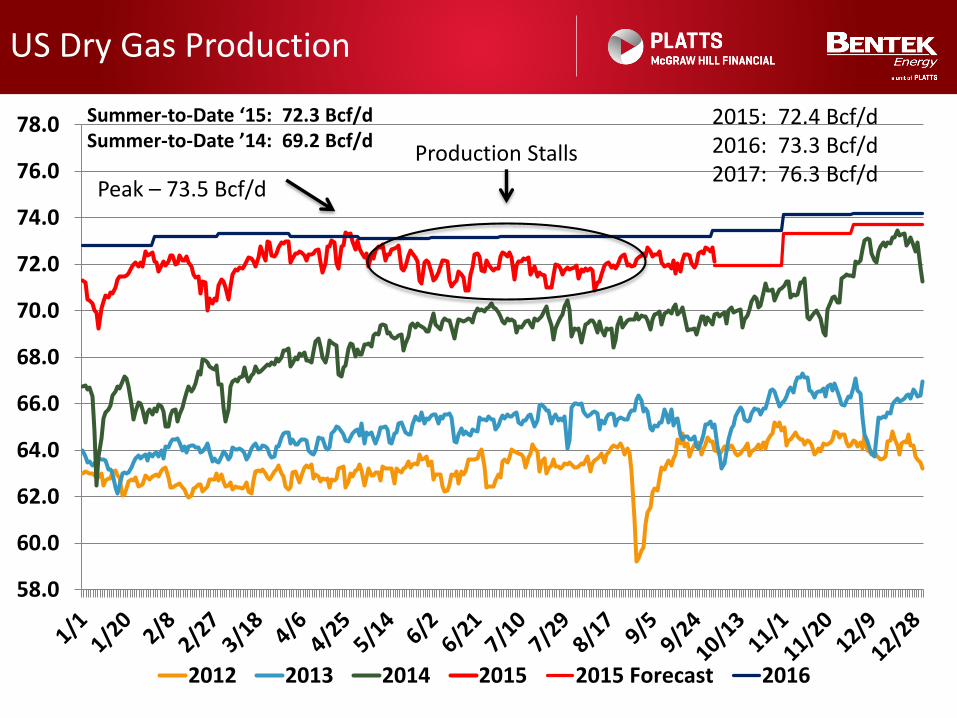

US Dry Gas Production

58.0

60.0

62.0

64.0

66.0

68.0

70.0

72.0

74.0

76.0

78.0

2012 2013 2014 2015 2015 Forecast 2016

Summer-to-Date ‘15: 72.3 Bcf/d Summer-to-Date ’14: 69.2 Bcf/d

Peak – 73.5 Bcf/d

Production Stalls

2015: 72.4 Bcf/d2016: 73.3 Bcf/d2017: 76.3 Bcf/d

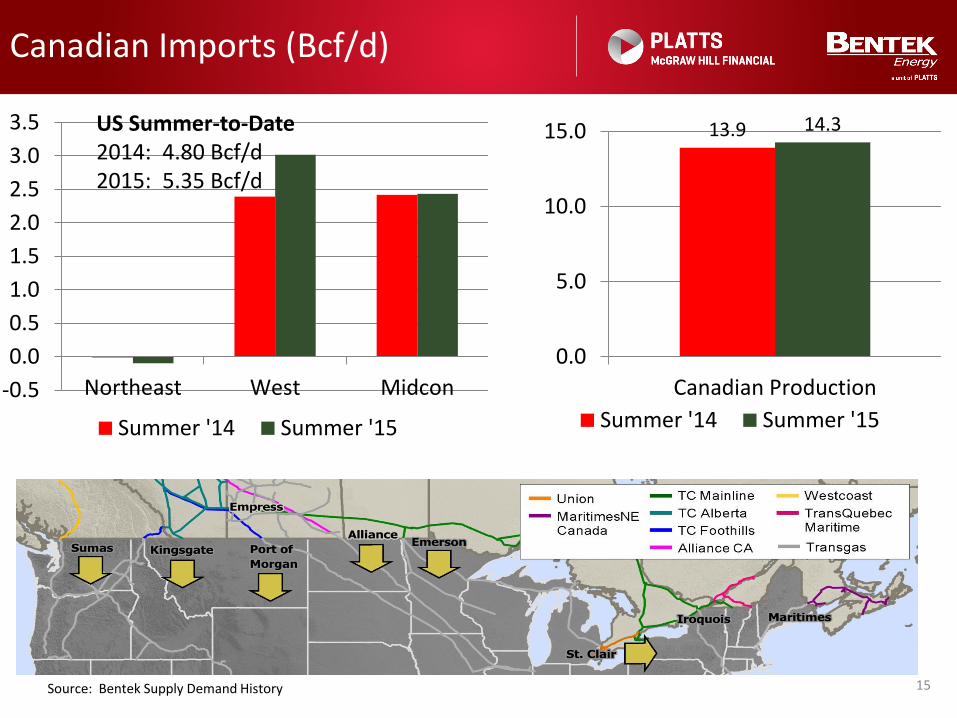

Canadian Imports (Bcf/d)

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Northeast West Midcon

Summer '14 Summer '15

15Source: Bentek Supply Demand History

US Summer-to-Date2014: 4.80 Bcf/d2015: 5.35 Bcf/d

13.9 14.3

0.0

5.0

10.0

15.0

Canadian Production

Summer '14 Summer '15

Northeast Focus

Northeast Production Driving US Production Growth

0%

5%

10%

15%

20%

25%

30%

0

10

20

30

40

50

60

70

80

Bcf

/d

Production

Rest of US Northeast % of Northeast

(5)

-

5

10

15

2011 2012 2013 2014 2015

Bcf

/d

Northeast Net flows

17

Northeast Stagnates Too

18

-

1

2

3

4

5

6

7

8

9

10

Bcf

/d

App OH NE PA Dry

NE PA Dry Production Peaks Last Winter at

9 Bcf/dNortheast producers

choke more than 1 Bcf/d of gas due to low prices

Another winter ramp in store??

Transco Leidy Line Maintenance

Northeast Capacity Additions

Project Name Est. ISD Capacity Status

REX Zone 3 East-to-West 7/1/2015 1,200 Operating

TETCO Uniontown to Gas City Expansion 8/1/2015 425 Operating

TETCO OPEN Ohio Pipeline Energy Network Project 9/15/2015 550 Partial Service

TCO East Side Expansion Project 9/1/2015 312 Under Construction

Transco Virginia Southside Expansion 9/1/2015 270 Operating

ANR Sulphur Springs Expansion (Formerly Glen Karn) 11/1/2015 133 Under Construction

NFG Northern Access 2015 Expansion 11/1/2015 140 Under Construction

NFG Tuscarora Lateral 11/1/2015 69 Under Construction

TGP Niagara Expansion 11/1/2015 158 Under Construction

TGP Broad Run Flexibility Project 11/1/2015 590 Under Construction

NFG Line N West Side Expansion and Modernization 11/1/2015 175 Under Construction

Transco Leidy Southeast Expansion 12/1/2015 525 Under Construction

Total 4,547 19

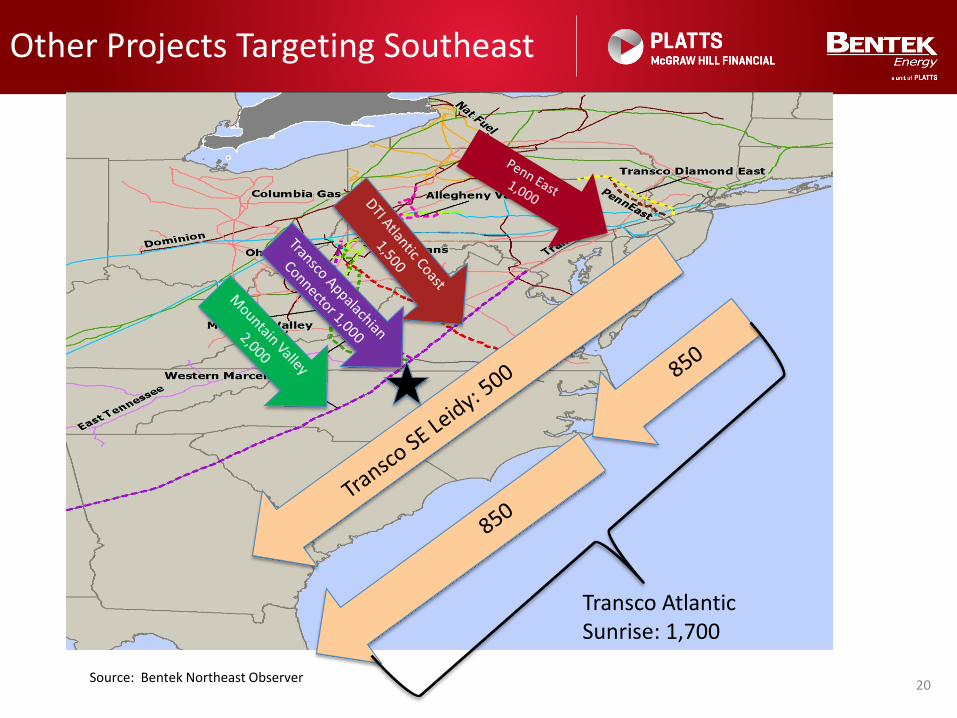

Other Projects Targeting Southeast

20Source: Bentek Northeast Observer

Transco Atlantic Sunrise: 1,700

Southeast Demand (Bcf/d)

21

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2009 2010 2011 2012 2013 2014 2015

NC SC VA

Source: Bentek Pipeline Flow Data

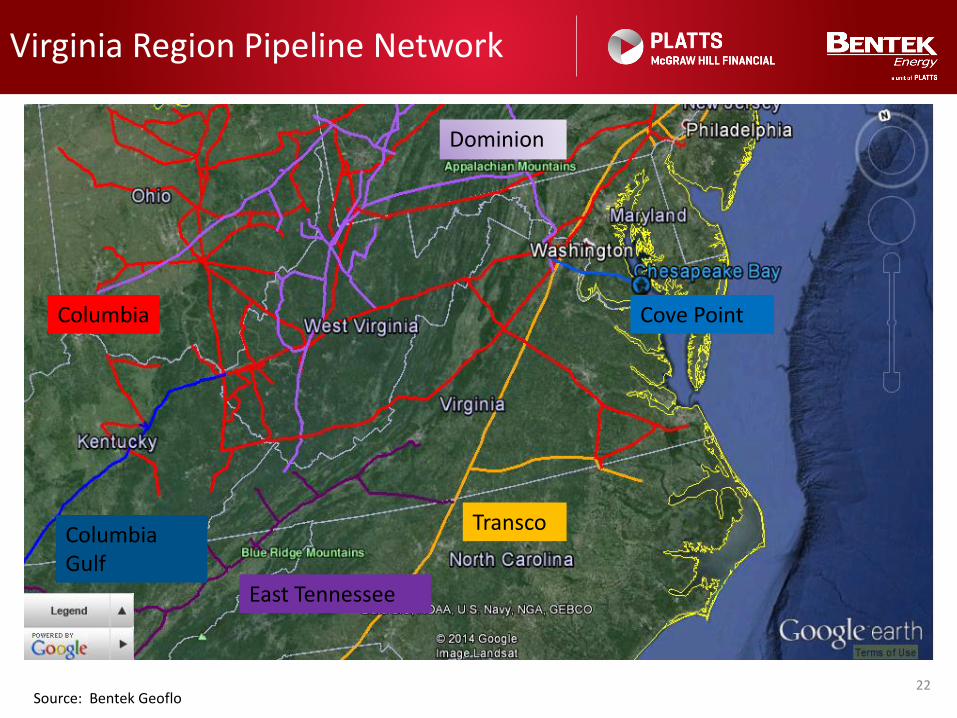

Virginia Region Pipeline Network

22Source: Bentek Geoflo

Transco

Cove Point

East Tennessee

Dominion

Columbia Gulf

Columbia

VA Deliveries by Pipeline (Bcf/d)

0.0

0.5

1.0

1.5

2.0

2.5

Columbia Gas Transco Dominion Cove Point East Tennessee

Bentek Pipeline Flow Data 23

Columbia Gas: 38%Transco: 28%Dominion: 26%Cove Point: 6%East Tenn: 2%

VA Demand Sector (Bcf/d)

0.0

0.5

1.0

1.5

2.0

2.5

LDCs/ResCom/Ind Power

Bentek Pipeline Flow Data 24

LDC/Ind/Rescom: 56%Power: 44%

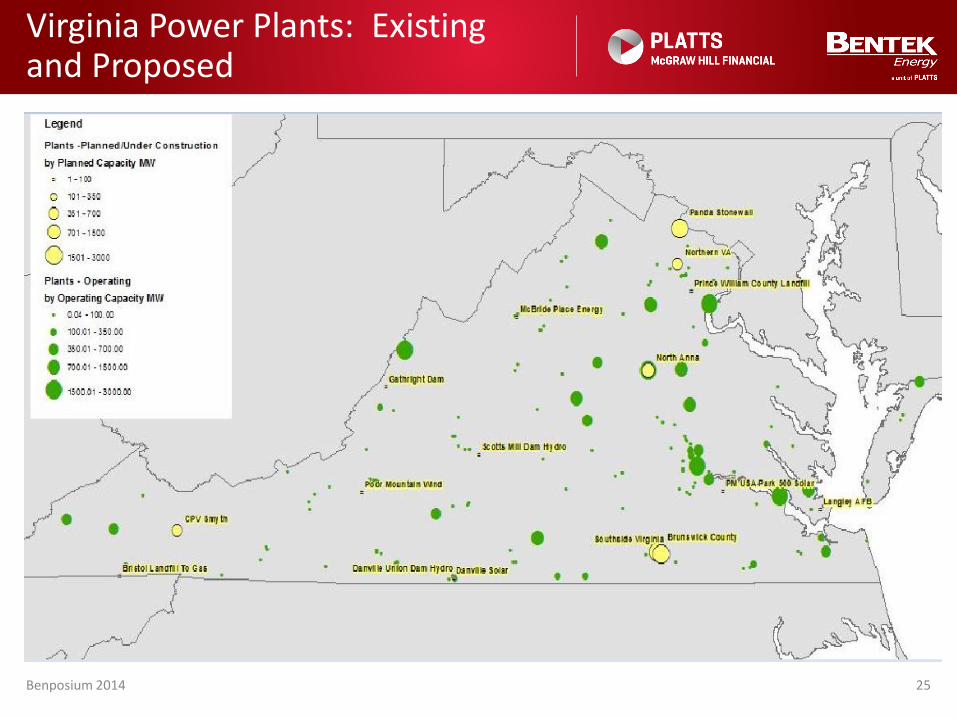

Virginia Power Plants: Existing and Proposed

25Benposium 2014

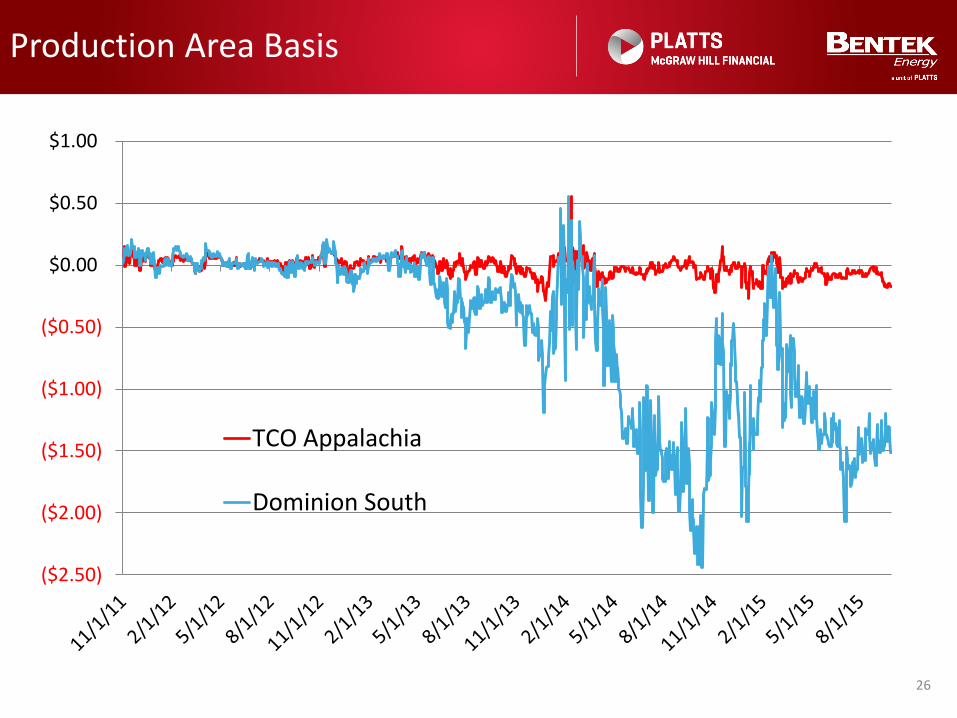

Production Area Basis

26

($2.50)

($2.00)

($1.50)

($1.00)

($0.50)

$0.00

$0.50

$1.00

TCO Appalachia

Dominion South

Production Area Basis

27Source: Bentek Northeast Observer

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

DTI Receipts

DTI Production DTI Interconnect

0

1,000

2,000

3,000

4,000

5,000

6,000TCO Receipts

TCO Production TCO Interconnect

Dom Receipts grow 2.5 Bcf/d since Jan. 2013

TCO Receipts Flat Since Jan 2013

Transco: Bad Deal for Consumers?

28

($2.50)

($2.00)

($1.50)

($1.00)

($0.50)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

Transco Z5 Transco Zn6 NY Transco Zn6 xNY

NE PA Dry Production Constrained Until 2017-18

0

2

4

6

8

10

12

14

16

18

20

Bcf

/d

NE PA Dry Production vs Pipeline Capacity

NE PA and Central Dry Pipeline Takeaway Pipeline Takeaway High Case

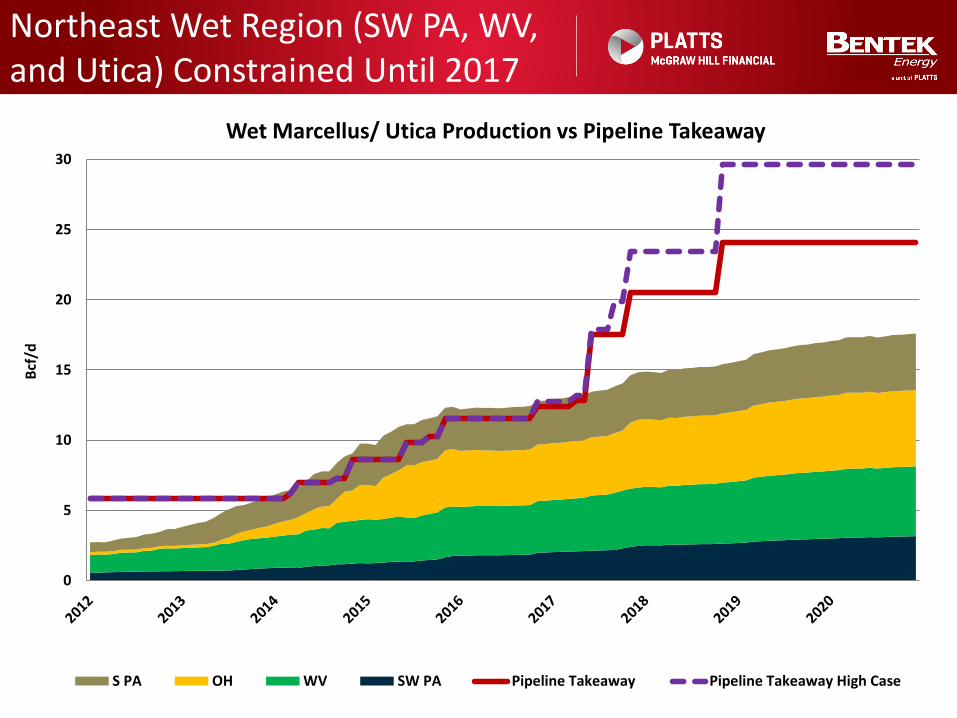

Northeast Wet Region (SW PA, WV, and Utica) Constrained Until 2017

0

5

10

15

20

25

30

Bcf

/d

Wet Marcellus/ Utica Production vs Pipeline Takeaway

S PA OH WV SW PA Pipeline Takeaway Pipeline Takeaway High Case

US Demand Outlook

Power Burn Testing 2012 Levels

10

15

20

25

30

35

40

45

1-Apr 1-May 1-Jun 1-Jul 1-Aug 1-Sep 1-Oct

Bcf

/d

5 yr range 2012 2014 2015 forecast

32

Power Burn Season to date:Versus 2014: +4.3 Bcf/d Versus 2012: -0.4 Bcf/d

Future Northeast Power Burn Driven by Changes in Generation Fleet

33

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MW

Gas New Builds

Non-NE New Gas Plants NE New Gas Plants

Source: Bentek’s NA Power Plant Databank

Increased Efficiencies and Renewables Offsetting Growth in Power Burn

34Source: Bentek Supply Demand History

US Industrial Demand (Bcf/d)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Northeast Southeast Texas Midcon West

Summer '14 Summer '15

35Source: Bentek Supply Demand History

US Summer-to-Date2014: 19.42 Bcf/d2015: 19.07 Bcf/d

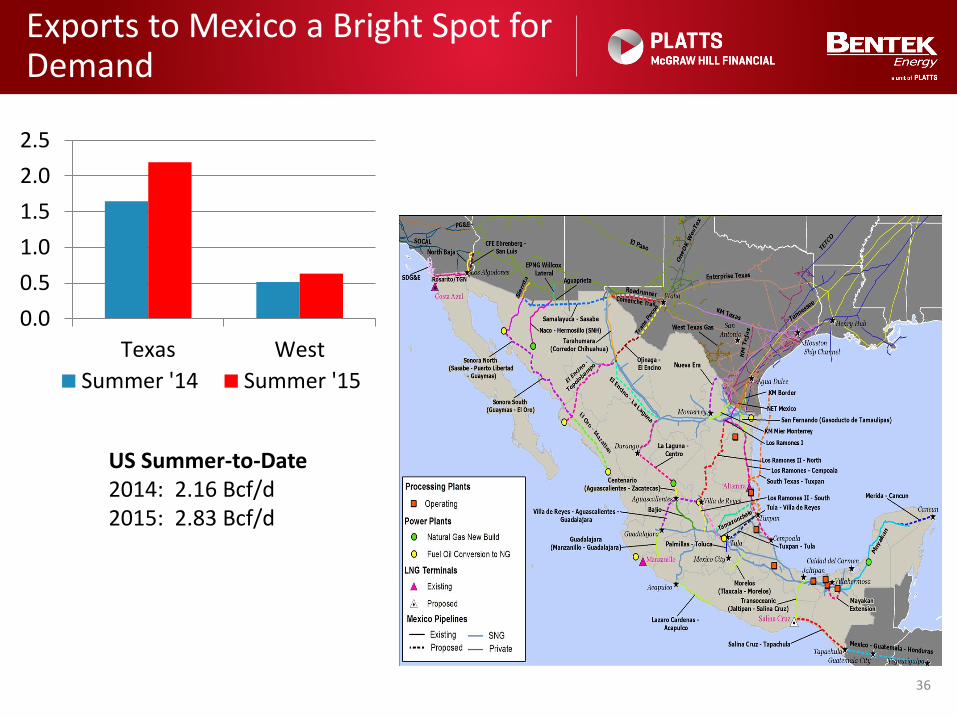

Exports to Mexico a Bright Spot for Demand

36

0.0

0.5

1.0

1.5

2.0

2.5

Texas West

Summer '14 Summer '15

US Summer-to-Date2014: 2.16 Bcf/d2015: 2.83 Bcf/d

47 Bcf/d of proposed capacity…

• BENTEK expects 10.1 Bcf/d to get built

LNG Exports could reach 6 Bcf/d in 2020

Benposium 201537

East Coast Export Terminals:Cove Point – 1 Bcf/d

Gulf Coast Liquefaction Capacity:Sabine Pass T1-5 3.5– Bcf/d

Freeport LNG T1-3 – 2.1 Bcf/d Cameron T1-3 – 2.1 Bcf/d

Corpus Christi T1-2 – 1.4 Bcf/d

Bentek LNG Exports Forecast

02468

1012

Bcf

/d

Base US LNG Capacity

Sabine Pass T12 Sabine Pass T2 Sabine Pass T3

Sabine Pass T4 Sabine Pass T5 Freeport LNG T1

Freeport LNG T2 Freeport LNG T3 Cameron LNG T1

Cameron LNG T2 Cameron LNG T3 Cove Point T1

Corpus Christi T1 Corpus Christi T2

Source: Bentek

Global LNG Prices Also Signal Lack Of Demand

$0

$5

$10

$15

$20

$25

$M

MB

tu

Henry Hub JKM NBP

38

FUKUSHIMA

Storage Outlook

39Source: Bentek CellCAST

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Bcf

US Natural Gas Inventories

Five Year Range US Inventory History US Inventory Forecast

Markets eliminate inefficiencies/move to the mean.

Economic growth moves to more normal levels.

Environmental issues continue to plague coal and

nuclear making natural gas the clear fuel of choice.

US best place to invest in incremental supplies and

is the marginal cost supplier.

Prices move to variable cost spreads Natural gas moves to variable transport differentials

LNG/crude/LPG prices reflect variable shipping rates

Conclusion: Btu Gap moves to reflect variable spreads

The Btu Gap: Where Does It Go From Here?

40

Conclusion: Bearish Short Term/Bullish Long Term

• US Demand Growth Accelerating. Gains Critical Mass in 2017 – Power Burn demand will increase due to

economics/environmental concerns, but conservation, efficiencies and renewables offset.

– Industrial renaissance tempered, but material.– Mexican exports on the rise.– LNG exports expectations reduced, but still significant.

• Increased Production is Needed to Meet Growing Demand– Higher prices needed to allow producers to earn a return.– Higher prices needed for banks to loan money.– Producer efficiency gains will continue, but movement away

from core areas and higher service company costs will offset these gains to some degree.

• Northeast will continue to fuel production growth and pipeline expansions. Northeast basis strengthens as capacity constraints alleviated. Weaker basis values move southward.

Benposium 2014 41

Thank You!

BENTEK is an energy market analytics company focused on the natural gas, oil, and liquids markets and related energy sectors.

Chris [email protected]

Contract Chris at 212/904-6915 or contact any Bentek Analyst at 303/988-1320

DISCLAIMER. THIS REPORT IS FURNISHED ON AN “AS IS”BASIS. BENTEK DOES NOT WARRANT THE ACCURACY OR CORRECTNESS OF THE REPORT OR THE INFORMATION CONTAINED THEREIN. BENTEK MAKES NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE USE OF ANY INFORMATION CONTAINED IN THIS REPORT IN CONNECTION WITH TRADING OF COMMODITIES, EQUITIES, FUTURES, OPTIONS OR ANY OTHER USE. BENTEK MAKES NO EXPRESS OR IMPLIED WARRANTIES AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANT- ABILITY OR FITNESS FOR A PARTICULAR PURPOSE.RELEASE AND LIMITATION OF LIABILITY: IN NO EVENT SHALL BENTEK BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL, INCIDENTAL, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFIT) ARISING OUT OF OR RELATED TO THE ACCURACY OR CORRECTNESS OF THIS REPORT OR THE INFORMATION CONTAINED THEREIN,WHETHER BASED ON WARRANTY, CONTRACT, TORT OR ANY OTHER LEGAL THEORY.