Embed Size (px)

Citation preview

North Deal Team Timeswww.pwc.blogs.com/northMay 2012

Lead articles

2 North Deal Team Times May 2012

Keeping the deal on the railsContinued uncertainty and volatility in the economy suggests that it may be a difficult time to sell a business. However, here in the North, we are seeing deals being completed and attractive multiples being achieved where a well planned sale process is employed.

Jonathan Cooper0161 245 2313 [email protected]

Valuation multiples can be particularly attractive in two scenarios:1. Where trade buyers are willing to pay

a strategic price now, for synergies and market access. To access this potential generally requires a proactive, confidential and planned process of market testing by sellers, especially to unlock overseas interest.

2. The business has a strong growth profile that enables financial investors to pay a compelling multiple, even with conservative gearing. There is still a wall of private equity funds needing investment, but a lack of debt and quality investment opportunities.

Whether you are responding to an unsolicited approach or you are considering commencing a sales process, one piece of advice remains – the more you plan and prepare for exit, the greater the value – so start planning early. Below we highlight some of the key pitfalls to avoid in a sales process:• Businesses are increasingly being

approached off-market, which can result in shareholders and management being caught off-guard. Without consultation with experienced corporate finance advisors, value may be eroded by the incorrect presentation of information, lack of negotiation strategy and a poorly run process.

• Competitive sales processes which are not tailored appropriately for the audience, specifically when the likely buyers are overseas trade players. Some buyers, particularly in emerging markets, are unwilling to participate in auction processes until they have had the opportunity and time to understand the asset on offer.

• Deals can often reach a stalemate if black holes are identified during due diligence, in particular: defined benefit pension liabilities; ongoing legal disputes; environmental liabilities; vacant properties; and tax exposures. In carve out situations, there can often be a lack of clarity over what is included or excluded in the business being disposed of and this can erode buyer confidence, particularly later in a process if they perceive they are getting less than they based their offer on.

• Vendors may set unrealistic timetables, which they often cannot meet due to a lack of resources to prepare the information required by potential buyers. This then results in an iterative process in order for interested parties to receive sufficient insight into the business – and can often end in buyers becoming frustrated and walking away.

• Current trading results falling below forecast, resulting in a deterioration in confidence from interested parties.

• Lack of clear understanding and explanation as to why the business has performed above or below the market in recent periods.

PwC’s North Deal Team includes a range of dedicated “deal doers”, including specialists in corporate finance, vendor assistance and vendor due diligence. Please contact a member of the team should you wish to discuss how we can support you in planning and getting the maximum value for your deal.

Andy Parker0161 245 [email protected]

3 North Deal Team Times May 2012

The RGF supports projects and programmes that push private sector investment creating economic growth and sustainable employment. The North has been awarded the largest number of projects so far in rounds 1 and 2.

PwC in the North are supporting organisations in one of two ways: either assisting companies to put together their application to the RGF, or by performing due diligence services on the applicant organisations and their projects (which is a requirement of the process). We are currently working with companies across a range of industries, including automotive, engineering, renewable energy and the public sector.

From our experience, we believe that there are a number of key areas that organisations should consider before making their application, including:• understanding all eligibility criteria,

including the fact that the minimum bid threshold of £1m still applies (however, joint bids are possible);

• ensuring that supporting business plans are credible, strong and robust;

• consideration of how the application will demonstrate job creation and/or job safeguarding; and

• whether the application is compliant with the various state aid rules.

Nigel Ward, Partner at PwC, said “The RGF is a key part of delivering growth to the region, and should be considered by all organisations who are planning significant capital expenditure and development projects. The application process requires thought upfront, as we have seen a number of applications that have required re-work between the application being accepted and the subsequent due diligence process.”

Kevin Barnard, Director at PwC added, “Our significant knowledge and expertise throughout the firm allows us to find the right specialists to offer a tailored package to applicant organisations, whether it is advising on putting together a bid or performing the required due diligence. From our experience of recent projects, early consultation with advisors is crucial to help compile a robust and credible bid which is compliant with all relevant regulations.”

Syedul Hussain, Director at PwC added “A recent example of this has been our support to Bentley Motors who have secured a £4.7m grant from the RGF towards training new workers and engine research and development. We were able to quickly assemble the right team with the appropriate industry and grant knowledge to efficiently and effectively undertake the required due diligence.”

Contact Kevin or Syedul if you are interested in applying for a grant, or wish to discuss likely due diligence requirements.

Kevin Barnard0191 269 4445 [email protected]

Syedul Hussain0161 247 4076 [email protected]

Round 3 of the Regional Growth Fund set to drive further growth in the region Round 3 of the Regional Growth Fund (“RGF”) opened for bids on 23 February with the aim of delivering a further £1bn into the economy to encourage local enterprise, growth and job creation across a range of sectors. PwC has supported a number of organisations across the North in the first 2 rounds and there is already a significant level of interest in the third round, which closes on 13 June.

4 North Deal Team Times May 2012

Due to a combination of market conditions, we are now finding that when people are exit planning we are retained increasingly early in the process to assist the business in preparation for sale and to raise the right appetite from trade buyers.

One particularly active area at present is the technology sector. Overall, technology deal volumes declined 10% over the course of 2011, but 2011 volumes were still 19% higher than those in the 2009 trough. Total deal value remains far healthier, and for 2011 was approximately 90% higher than in 2009. As highlighted above, some of these technology deals represent “mega-deals”, which are typically driven by structural changes across the technology market, such as the increasing trend towards mobile and tablet technology.

Trade buyers continue to have a strong appetite for strategic deals, both in the context of mega-deals and the middle market. Large established players in the technology sectors, including the likes of IBM and Microsoft, are facing relatively low organic growth prospects in their more mature, established markets. These companies are making acquisitions to gain exposure to a combination of high growth markets (e.g. smartphones), high growth regions (e.g. South America), and to increase their existing software and service based revenues.

Despite tough debt market conditions, many private equity buyers have significant capital to be deployed, and are attracted to the underlying market fundamentals and attractive business models in the technology sector. Technology companies are critical within private equity portfolios, as they often have a secure customer base and long term recurring cash flows, making them resilient in a downturn. However, we have seen a polarisation of private equity in the technology market, despite this attractiveness. Many that recently entered the sector have left, whilst those houses experienced in the sector have continued to invest in emerging longer-term trends. For example, Lyceum Capital made three acquisitions in 2011 (Clearswift, a security software company; Adapt, an IT services provider; and Access, a provider of business application software).

A further factor underpinning M&A activity in the technology sector is that, in general,

valuations do not appear excessive. For more established listed businesses the valuation multiple gap between the technology sector and the overall market is minimal and can, typically, be explained by the higher forecast growth. Where strategic premiums are being paid, these are often linked to an informed view of the quantum and timing of revenue and cost synergies as well as the longer term market opportunity.

A clear trend has been the increased value placed on intellectual property, with patent acquisition being the driver behind a number of deals, particularly in the area of mobility.

Looking ahead to the coming year, whilst the macroeconomic outlook remains volatile, both private equity and corporate buyers retain their appetite for M&A in the technology sector and have the necessary cash to conclude deals. The prospect of long term structural change in an industry which offers visibility of revenues and where valuations can be supported, will continue to offer buyers compelling reasons to pursue acquisitions despite the challenging market.

Structural changes, and visibility over revenues, continue to entice buyers in the technology marketIn addition to the mid-market M&A activity seen locally, the wider deals market has also seen some mega-deal activity, including the acquisition of Skype by Microsoft, Autonomy by HP and the acquisition of McAfee by Intel.

Stuart Warriner0113 289 [email protected]

5 North Deal Team Times May 2012

Christine Adshead0161 245 [email protected]

Merger creates one of the UK’s largest debt recovery law firmsThe North Deal Team has provided financial due diligence support to Yorkshire based Drydens on their merger with Fairfax.

With a combined workforce of circa 300 and turnover of approximately £15m the combined firm will trade under the brand of drydensfairfax solicitors. Bradford based Drydens and Leeds based Fairfax were both part of national law firms before separating to become specialist debt collection and debt litigation practices. Both firms have a long history of acting for some of the country’s largest financial institutions as well as key Government departments.

PwC performed financial due diligence on Fairfax, to a focussed scope of work – this ensured costs were kept low and Drydens’ specific areas of concern were addressed. During the project, we worked closely with both parties to ensure that Fairfax’s confidentiality concerns were managed, whilst still enabling Drydens to make a well informed decision on the transaction. PwC also performed tax structuring work in connection with the transaction.

6 North Deal Team Times May 2012

Simon Viner0161 247 [email protected]

A budget for businessThe UK continues on its journey to become one of the most competitive corporate tax environments in the G20 and compared to many others European territories, is looking to emphasise a stable tax regime in which to do deals.

George Osborne unashamedly stated that this was a budget for business, and the extra 1ppt cut in corporation tax, reducing the headline rate to 24% from 1 April 2012 falling by 1ppt in the next two years to 22% in 2014, clearly demonstrated this commitment. Contrast this with measures taken by our European competitors who are raising headline rates, restricting loss utilisation and limiting interest deductibility.

In addition to corporate rate reductions, the Coalition has taken other steps to make the UK more competitive from a tax perspective. These include plans to introduce a new 10% patent box regime; an above-the-line and potentially EBITDA enhancing R&D tax credit; relaxing the anti-avoidance rules dealing with the taxation of profits of overseas subsidiaries; as well as confirming that there are no new restrictions on interest deductibility. Over and above these measures, the video gaming, animation and high-end television industries are in line to receive further corporation tax incentives.

However, one issue to watch is the review of the taxation of interest income and the deduction of withholding tax. The UK, unlike many of our European competitors, still deducts withholding tax on interest and any review that increases the administration burden to UK companies would be most unwelcome.

From a personal tax perspective, the 5p reduction in the income tax top rate from 6 April 2013 is the headline grabber. Another reason to be cheerful is the doubling of the maximum value of tax efficient Enterprise Management Incentive (“EMI”) share options that can be granted to an employee from £120,000 to an unprecedented £250,000. In addition, there are proposals that Entrepreneur’s Relief (which allows the first £10m of individual’s capital gains to be taxed at 10%) should apply to EMI shares. These measures will be effective once EU state aid approval has been granted later in the year.

Finally, it should be noted that businesses next year will face increased challenges and costs arising from their role as unpaid tax collectors with the introduction of the pensions auto-enrolment regime and the provision of real time information to HMRC.

7 North Deal Team Times May 2012

Paul Mankin0191 269 [email protected]

Sale of Attends Europe to Domtar Corporation for €180m PwC Corporate Finance was delighted to act as lead adviser to Rutland Partners (“Rutland”) on its sale of Attends Healthcare Limited (“Attends Europe”) to Domtar Corporation (“Domtar”), a U.S. domiciled, North American manufacturer, marketer and distributor of fiber-based products with annual revenues of $5.6bn. Following exchange of contracts at the end of January, the transaction completed on 29 February 2012 for an enterprise value of €180m.

Attends Europe is a leading provider of branded and private label adult incontinence products across Northern and Western Europe. Products are manufactured in Aneby, Sweden and supplied through a mix of reimbursement, retail and contract channels. Attends Europe’s head office is based in Newcastle.

3i Group plc acquired Attends from Proctor and Gamble in 2002 and subsequently decided to split the business: Attends Europe was acquired by Rutland for €93.5m in 2007 and Attends US was acquired by KPS Capital Partners. PwC Corporate Finance advised Rutland when it made its original investment to acquire Attends Europe in 2007. Rutland has since invested over €25m in capital expenditure to support management’s business plan as they sought to develop the product portfolio to better address growth areas of the market, whilst also implementing a strategy of cost reduction.

Since 2007, Attends Europe has grown sales to a current run rate in excess of €140 million and EBITDA by 45% to a current run rate of approximately €23 million. Domtar’s purchase price represents approximately eight times run rate earnings and generates a cash multiple of 3.3 times Rutland’s original investment. Domtar are retaining the existing management led by James Steele (Chief Executive) and aim to double earnings over the next five years from strong growth in the incontinence market.

Following the deal, PwC received the following feedback from Nick Morrill, Managing Partner at Rutland:

In September 2011 Domtar announced the acquisition of Attends US from KPS Capital Partners for $315m as part of its strategic aim to grow its revenues and offset the long-term decline in paper demand. With the successful acquisition of Attends Europe, Domtar have now consolidated the Attends brand on both sides of the Atlantic. Along with corporate finance advice, PwC also provided tax, SPA and pensions advice on the deal.

“Just a massive thank you for all your help and support….it’s a fantastic result for Rutland and your contribution has been hugely valuable throughout.”

8 North Deal Team Times May 2012

Andy Parker0161 245 [email protected]

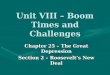

PE portfolio companies maintain their focus on growth In April 2012, PwC released its latest annual survey of PE portfolio companies. We held in depth, face-to-face interviews with 77 companies across different sectors, of all different sizes, with a range of different PE backers, from all around the UK.

In last year’s survey, our analysis highlighted a shift in emphasis from the cost cutting measures necessary to ensure survival towards a strategic focus on growth, following better than expected performance during the downturn. Growth now remains the number one strategic objective.

Attracting and incentivising high calibre people is also high on the agenda of PE backed companies and evidence of a “skills gap” appears to be developing. Nearly 4 in 5 companies increased average pay in the year, with 86% of companies paying bonuses. However, there was a significant drop in the number of managers who felt incentivised, down from 69% to 51%.

This lack of incentivisation for managers may be driven by expectations around exits, where expected timing has slipped by an average of 18 months compared with plans when the original investment was made. PwC has helped a number of teams rebalance their incentives to take account of a changing economic environment.

There has also been some reduction in expectations of the multiple which will be achieved on exit. In addition, there is an increasing focus on trade buyers as the expected exit route – this is something we are seeing in our business, with international buyers leading the way.

PE backed companies recognise the challenge to secure new financing as term loans reach maturity. There is a wall of refinancings due over the next two to three years (a combination of short term financings since the start of the global financial crisis and seven and eight year loans created in the boom years before it) and management teams are right to seek advice about how to secure this funding well in advance.

Growth

Improving cash flow management

Reducing costs and seeking efficiencies

Improving margins

Broadening service offering or intro new products

Staff development, retention and motivation

4.6

4.6

3.5

3.4

3.6

3.6

3.6

3.6

3.6

3.7

3.8

Top 6 areas of strategic focus

Answers for 2012Answers to same questions in 2011

Mean importance score (1=low, 5=high)

Nigel Ward0113 288 2277 [email protected]

9 North Deal Team Times May 2012

Trevor Milne0161 247 [email protected]

Ambassador employs approximately 100 people and operates out of its Winsford, Cheshire base as well as a number of regional UK sites. The business distributes a wide range of protective packaging products, including the Jiffy bag range.

This acquisition by Antalis cements its leadership in the distribution of paper and communications support materials (print & office paper, visual communication & packaging products). Antalis is the largest European group in the distribution of communications support materials, with more than 230,000 customers and operations in 44 countries spanning 5 continents and a group turnover in excess of €2.8 billion.

This transaction is yet another example of the increasingly cross-border M&A market that we referenced in our September 2011 issue of Deal Team Times.

We worked closely with Antalis to ensure that our work not only focussed on those matters important to value but also on a successful transition of the business. Jonathan Cooper led the engagement for PwC with support from Trevor Milne (financial due diligence) and Jeff Nye who worked closely with Antalis’ in-house counsel in negotiation of the sale and purchase agreement.

Commenting upon the transaction, Hervé Poncin, Chief Operating Officer of Antalis said: “We are pleased to have secured the acquisition of Ambassador, which significantly strengthens our position in a fragmented packaging distribution market that is currently growing at 5% per year. PwC have supported us with a number of our transactions globally, and it was comforting to be able to call upon the skills of their Manchester team for this latest acquisition.”

Antalis acquires Ambassador PackagingOur Transaction Services team provided support to Antalis on its acquisition of Ambassador Packaging in January 2012.

10 North Deal Team Times May 2012

Getting value: supporting growthRebecca Clayton, from our Valuation practice, outlines her thoughts on how to better understand and deliver value in the current environment.

Rebecca Clayton0161 245 [email protected]

Businesses and investors alike are facing a number of well documented challenges in the current environment. Yet growth is still possible; but it is all about making smarter investment decisions.

Investors and stakeholders are looking for investments with intrinsic strength, valuable intellectual property and businesses that have demonstrated resilience.

Historically, investment decisions made for the wrong reason or the wrong price can damage not only the company’s reputation but also the individuals involved. So if you have growth aspirations, the key appraisal stages for a potential investment need robust challenge to help develop an effective decision making framework, identify the key risks and track delivery.

For example, nothing is more important than getting the price right, especially at a time when markets remain volatile. In our view, price remains flexible throughout the deal process. Determining the price to be paid should factor in the following:• An assessment of the value of the target

on a standalone basis. This includes understanding the current strategy, identifying key value drivers and benchmarking these against historic and market performance. Our experience demonstrates that to gain investment approval market multiples should not be selected without questioning their reasonableness in the context of market circumstances.

• A discounted cash flow approach should be based on objectively reviewed forecasts with a focus on long term trends. We believe that there may be a move to more ‘probabilistic’ valuation approaches using sensitivity analysis on key value drivers to address uncertainty. Identifying and understanding the potential impact of risks and upsides adds credibility to in-house analysis and rigour to pricing negotiations.

• An understanding of the value of intellectual property owned by a target can help communicate the rationale for a deal to key decision makers and potential stakeholders. In addition, for those purchasers who account under IFRS, understanding the impact of acquired intangible assets on future earnings can not only influence the investment decision but can also prevent nasty surprises post completion.

• Quantifying synergies helps assess the value of a target to a purchaser and generates an understanding of the incremental P&L and cash flow impact. This again helps communicate the rationale for a deal and can also be extremely beneficial during negotiations.

• The combination of due diligence and valuation advice ensures that due diligence is focussed on those areas that go to value and enables the price to be adjusted to reflect any findings.

• Purchasers may also benefit from obtaining an independent and objective “Fairness Opinion” together with a summary of the key value drivers that the Board should monitor during post deal integration.

In summaryTo maximise growth and hence value for shareholders, management need to critically and robustly understand the benefits and risks of all potential investments.

Our Deal Team can work with you and bring together experts who can deliver actionable insights ranging from helping clients select the right acquisition target, the right price to pay through to advising why previous investments have failed to deliver. The result is a better return for your business.

11 North Deal Team Times May 2012

PwC provided corporate finance advice and also financial, commercial and tax due diligence on the £24 million MBO of Brand Addition from UK listed 4imprint. The deal was backed by H.I.G. Europe. Brand Addition is a market leader in the provision of promotional products to large corporates across Europe for use in their corporate marketing and consumer promotion campaigns. The business provides a full outsource service including product design, ethical sourcing, stock holding/management, international logistics and web creation/hosting. Customers include numerous Global Fortune 500 companies. The company employs 260 people across 5 offices in the UK, Germany and China.

PwC Corporate Finance acted as advisor to management, after building a deep relationship with the team over the last few years, which ensured that we knew their objectives and ambitions as part of this transaction. This trusted relationship was important in helping to deliver a great deal for all involved. Chris Lee, CEO of Brand Addition, said “We are very pleased to have completed the MBO of Brand Addition with H.I.G. Europe. With their backing, we will be in a strong position to take advantage of this growth market, which is worth more than £3 billion across Europe.” He went on to say “PwC cared about the outcomes for us. Knowing that getting it right for us mattered, and had a powerful effect.”

A separate PwC Transaction Services team led by Nigel Ward provided financial, commercial and tax due diligence services on the deal. Nigel’s team were initially engaged by 4imprint to do vendor due diligence and subsequently did top-up work for H.I.G..

Andi Tomkinson from our Corporate Finance team commented “This was a fantastic North West deal that we are proud to be involved in. Chris and the team have an excellent partner in H.I.G.. Together, I’m sure, they will enjoy future success.”

Andi Tomkinson0161 245 [email protected]

Nigel Ward0113 288 [email protected]

Brand Addition MBOThe Deal Team advises on the MBO of Brand Addition

12 North Deal Team Times May 2012

North Deal Team contacts

M&A Tax

Simon Viner0161 247 4257 [email protected]

Gordon Singer0113 288 [email protected]

Financial Decisions and Analysis

Dan Stott0113 289 4670 [email protected]

Jeff Nye07775 [email protected]

SPA Advisory

Debra Halcrow0113 288 2137 [email protected]

Ian Logan0113 288 2050 [email protected]

Valuations

Transaction Services

Christine Adshead0161 245 2529 [email protected]

Mark Webster0191 269 4011 [email protected]

Jonathan Cooper0161 245 2313 [email protected]

Nigel Ward0113 288 2277 [email protected]

Corporate Finance

Stuart Warriner0113 289 [email protected]

Paul Mankin0191 269 [email protected]

Andy Parker0161 245 2388 [email protected]

To unsubscribe from this mailing, please email [email protected] with “Unsubscribe North DTT” in the subject line.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2012 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom), which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

Design Services 27586 (05/12).