Embed Size (px)

Citation preview

Best low-cost airline in Europe 2013-2015 World’s best Long Haul low-cost airline 2015

Norwegian Air Shuttle ASA Q2 2015 Presentation

Photo: Bo Mathiesen

Europe’s best low-cost airline 2013,2014 & 2015

• New routes launched

– domestic Spain

– London-Boston

– Caribbean (Puerto Rico + winter routes)

• SkyTrax awards 2015

– Best Low-Cost airline in Europe (3 years in a row)

– World’s best Long Haul Low-Cost airline

• Three new aircraft to the fleet in Q2

– 2 new 737-800’s (four new in first half)

– 1 new 787-8 Dreamliner (to a fleet of eight)

• Strong progress for long-haul

• EBT improved to NOK 456 million from a

loss of NOK 137 million last year

Q2 2015 Highlights

2

Europe’s best low-cost airline 2013,2014 & 2015

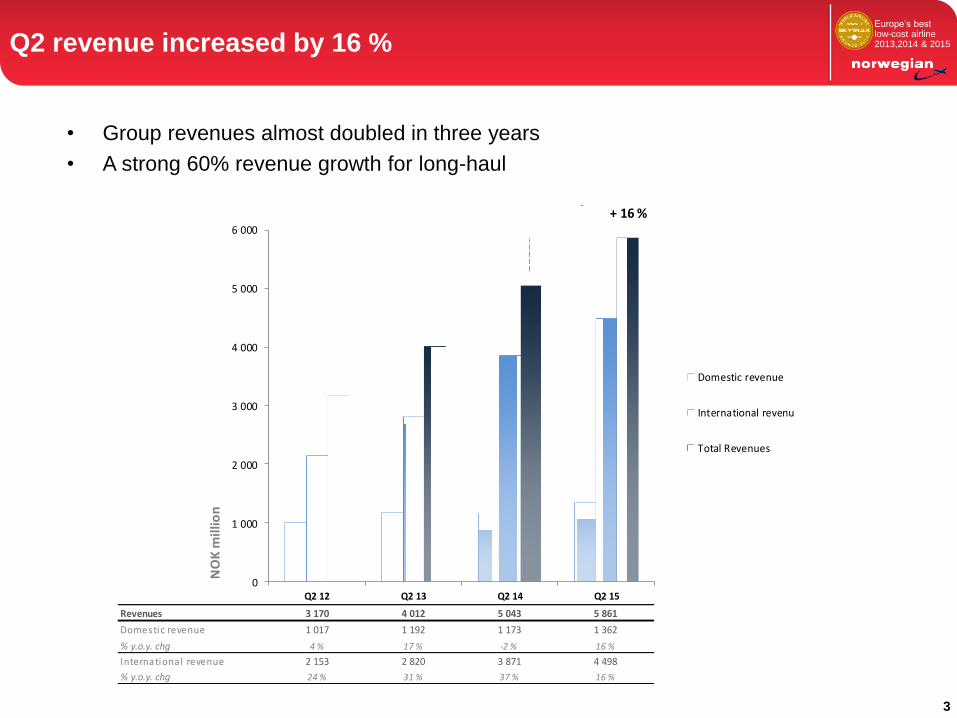

• Group revenues almost doubled in three years

• A strong 60% revenue growth for long-haul

Q2 revenue increased by 16 %

Revenues 3 170 4 012 5 043 5 861

Domestic revenue 1 017 1 192 1 173 1 362

% y.o.y. chg 4 % 17 % -2 % 16 %

International revenue 2 153 2 820 3 871 4 498

% y.o.y. chg 24 % 31 % 37 % 16 %

0

1 000

2 000

3 000

4 000

5 000

6 000

Q2 12 Q2 13 Q2 14 Q2 15

NO

K m

illi

on

Domestic revenue

International revenue

Total Revenues

+ 16 %

3

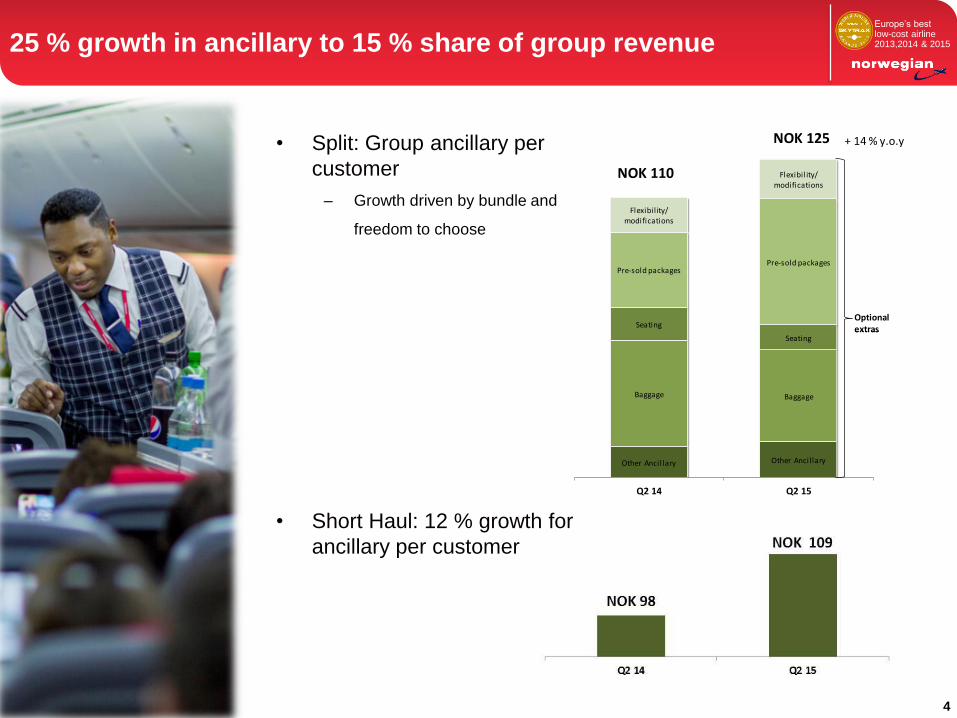

Europe’s best low-cost airline 2013,2014 & 2015 25 % growth in ancillary to 15 % share of group revenue

4

• Split: Group ancillary per

customer

– Growth driven by bundle and

freedom to choose

• Short Haul: 12 % growth for

ancillary per customer

Other Ancillary Other Ancillary

Baggage Baggage

Seating

Seating

Pre-sold packagesPre-sold packages

Flexibility/ modifications

Flexibility/ modifications

Q2 14 Q2 15

Optional extras

NOK 125

Optional extras

+ 14 % y.o.y

NOK 110

Europe’s best low-cost airline 2013,2014 & 2015 EBT improved by NOK 593 million on higher load

Q2 12 Q2 13 Q2 14 Q2 15 Q2 12 Q2 13 Q2 14 Q2 15

EBITDAR margin 21 % 22 % 11 % 22 % EBT margin 4 % 7 % -3 % 8 %

680

878

563

1 285

-150

50

250

450

650

850

1 050

1 250

1 450

NO

K m

illio

n

125

277

-137

456

-150

50

250

450

650

850

1 050

1 250

1 450

NO

K m

illio

n

EBT development Q2 EBITDAR development Q2

5

(NOK million) Q2 15 Q2 14 Change

EBITDAR 1 285 563 722

EBITDA 765 94

EBIT 520 -85

Pre-tax profit (EBT) 456 -137 593

Net profit 325 129

Europe’s best low-cost airline 2013,2014 & 2015

• USD/NOK has strengthened by 29 % y.o.y

• Spot fuel price down by 39 % (-20 % in NOK)

• Saved NOK 572 million on lower fuel cost (-18 % per ASK)

– NOK 826 million reduction due to lower spot price

– NOK 42 million saved on lower fuel consumption due to new aircraft

– NOK 296 million negative impact of currency (USD/NOK)

• Other opex: NOK 311 million negative impact from currency

– Related to leasing, maintenance, airport charges, handling, etc.

• One-offs included in EBT

– NOK 84 million extra cost related to engine maintenance

– NOK 10 million Wetlease

– NOK 100 million gain on hedging

Tailwind from fuel offset by currency

6

Europe’s best low-cost airline 2013,2014 & 2015

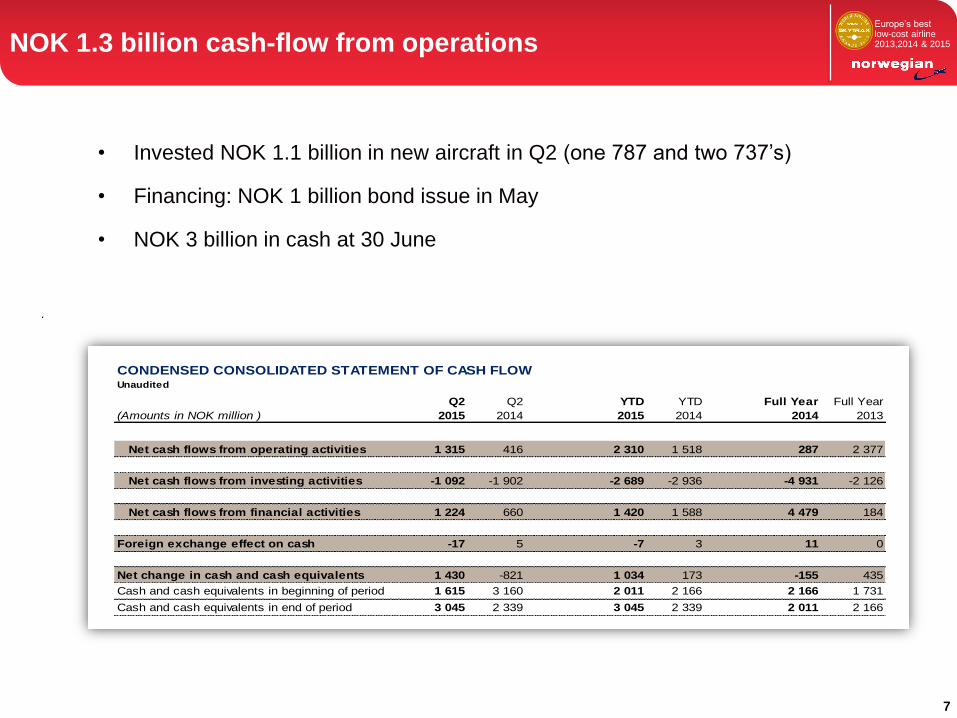

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWUnaudited

Q2 Q2 YTD YTD Full Year Full Year

(Amounts in NOK million ) 2015 2014 2015 2014 2014 2013

Net cash flows from operating activities 1 315 416 2 310 1 518 287 2 377

Net cash flows from investing activities -1 092 -1 902 -2 689 -2 936 -4 931 -2 126

Net cash flows from financial activities 1 224 660 1 420 1 588 4 479 184

Foreign exchange effect on cash -17 5 -7 3 11 0

Net change in cash and cash equivalents 1 430 -821 1 034 173 -155 435

Cash and cash equivalents in beginning of period 1 615 3 160 2 011 2 166 2 166 1 731

Cash and cash equivalents in end of period 3 045 2 339 3 045 2 339 2 011 2 166

NOK 1.3 billion cash-flow from operations

7

• Invested NOK 1.1 billion in new aircraft in Q2 (one 787 and two 737’s)

• Financing: NOK 1 billion bond issue in May

• NOK 3 billion in cash at 30 June

Europe’s best low-cost airline 2013,2014 & 2015 Balance sheet boost by currency and new aircraft

8

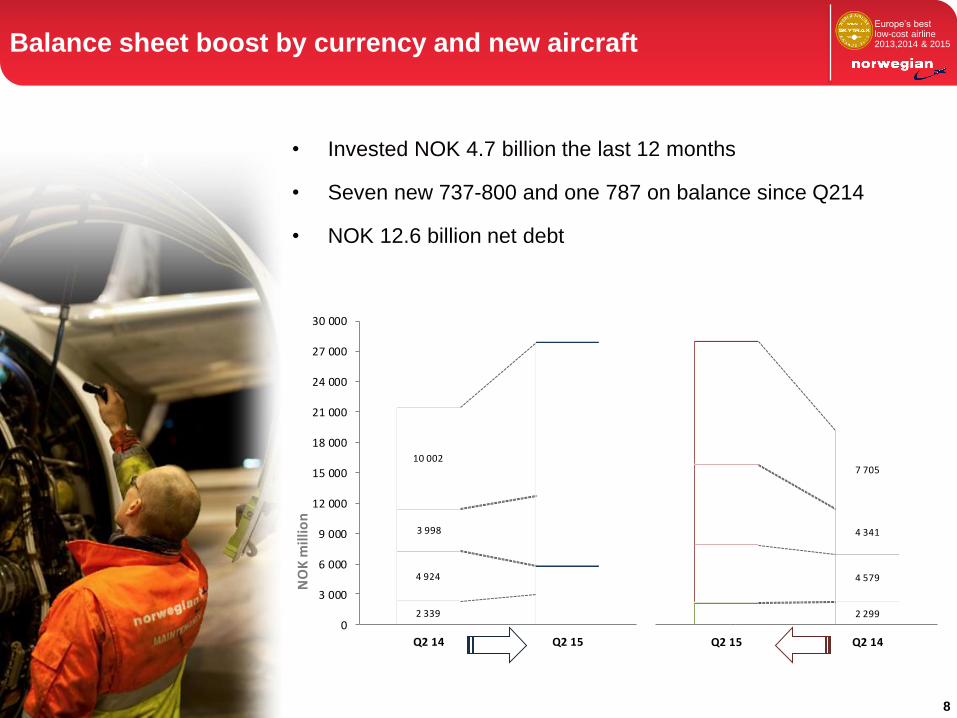

• Invested NOK 4.7 billion the last 12 months

• Seven new 737-800 and one 787 on balance since Q214

• NOK 12.6 billion net debt

2 339Cash3 045

4 924 Receivables2 801

3 998

Aircraft PDP / other assets

6 783

10 002

Aircraft15 140

0

3 000

6 000

9 000

12 000

15 000

18 000

21 000

24 000

27 000

30 000

Q2 14 Q2 15

NO

K m

illi

on

Equity2 163

2 299

Pre-sold tickets5 605

4 579

Otherliabilities

7 910

4 341

Aircraft Financing

12 092

7 705

Q2 15 Q2 14

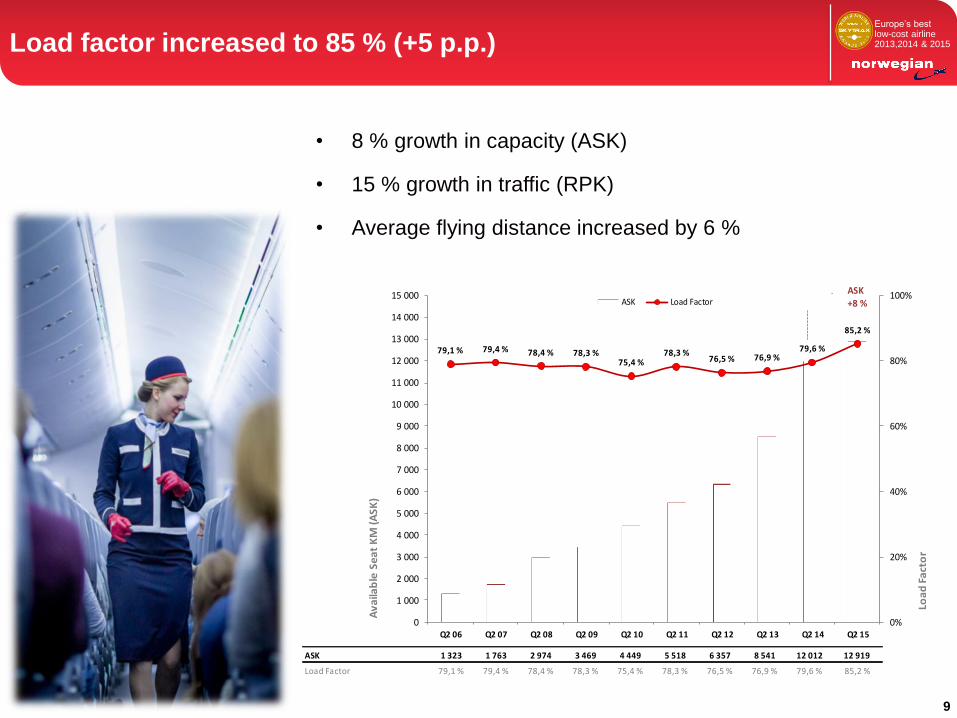

Europe’s best low-cost airline 2013,2014 & 2015 Load factor increased to 85 % (+5 p.p.)

• 8 % growth in capacity (ASK)

• 15 % growth in traffic (RPK)

• Average flying distance increased by 6 %

ASK 1 323 1 763 2 974 3 469 4 449 5 518 6 357 8 541 12 012 12 919

Load Factor 79,1 % 79,4 % 78,4 % 78,3 % 75,4 % 78,3 % 76,5 % 76,9 % 79,6 % 85,2 %

79,1 % 79,4 % 78,4 % 78,3 %75,4 %

78,3 %76,5 % 76,9 %

79,6 %

85,2 %

0%

20%

40%

60%

80%

100%

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

11 000

12 000

13 000

14 000

15 000

Q2 06 Q2 07 Q2 08 Q2 09 Q2 10 Q2 11 Q2 12 Q2 13 Q2 14 Q2 15

Loa

d F

act

or

Av

aila

ble

Se

at

KM

(A

SK

)

ASK Load FactorASK +8 %

9

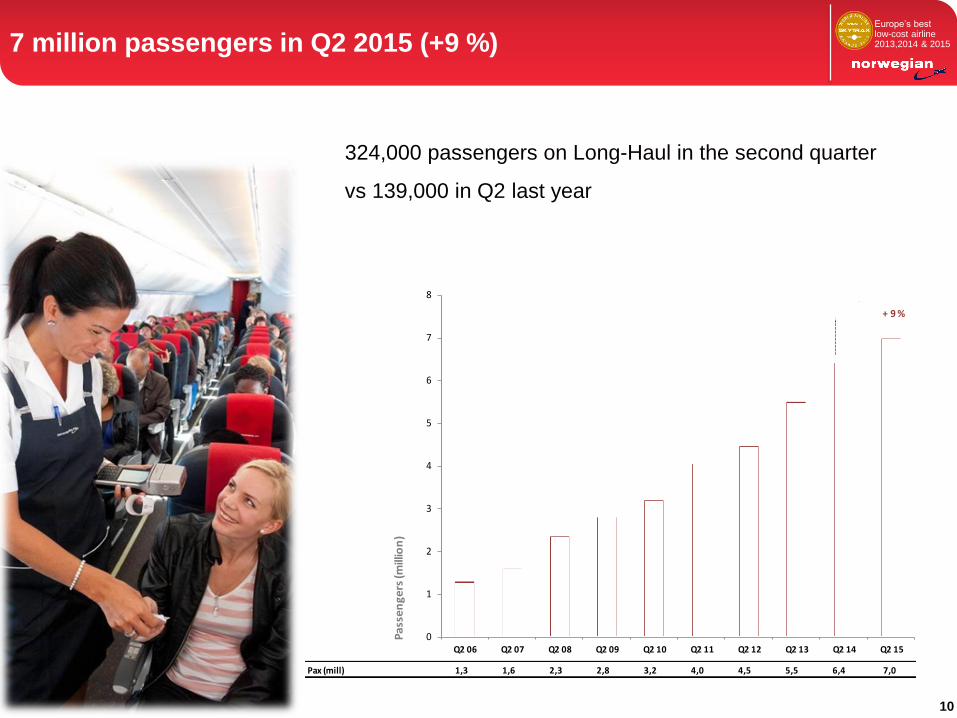

Europe’s best low-cost airline 2013,2014 & 2015 7 million passengers in Q2 2015 (+9 %)

324,000 passengers on Long-Haul in the second quarter

vs 139,000 in Q2 last year

Pax (mill) 1,3 1,6 2,3 2,8 3,2 4,0 4,5 5,5 6,4 7,0

0

1

2

3

4

5

6

7

8

Q2 06 Q2 07 Q2 08 Q2 09 Q2 10 Q2 11 Q2 12 Q2 13 Q2 14 Q2 15

Pa

sse

ng

ers

(mill

ion

)

+ 9 %

10

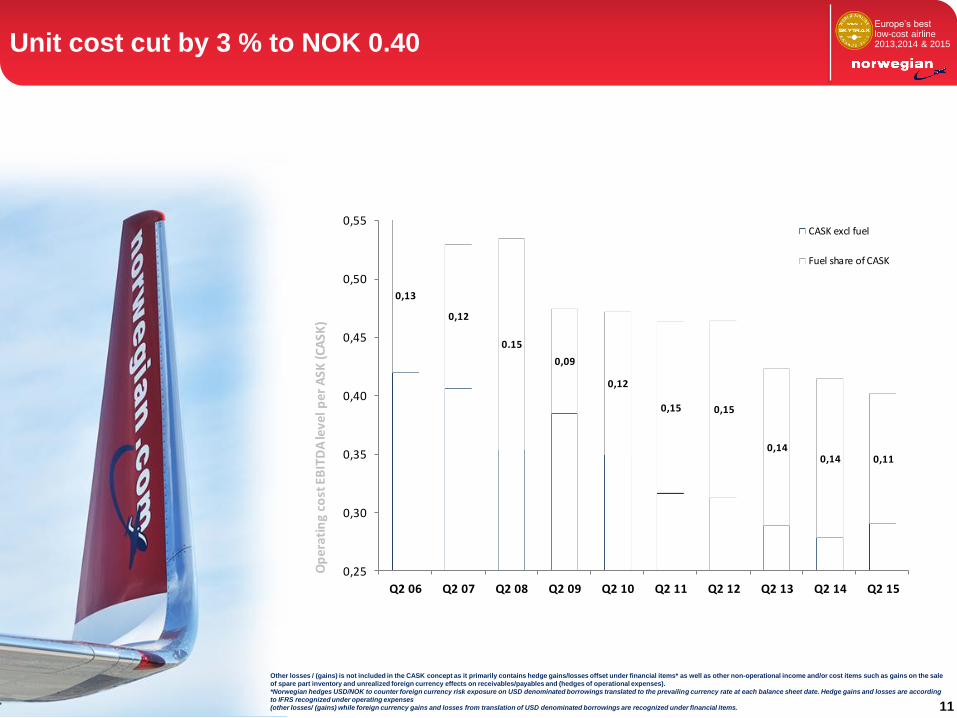

Europe’s best low-cost airline 2013,2014 & 2015 Unit cost cut by 3 % to NOK 0.40

Other losses / (gains) is not included in the CASK concept as it primarily contains hedge gains/losses offset under financial items* as well as other non-operational income and/or cost items such as gains on the sale

of spare part inventory and unrealized foreign currency effects on receivables/payables and (hedges of operational expenses).

*Norwegian hedges USD/NOK to counter foreign currency risk exposure on USD denominated borrowings translated to the prevailing currency rate at each balance sheet date. Hedge gains and losses are according

to IFRS recognized under operating expenses

(other losses/ (gains) while foreign currency gains and losses from translation of USD denominated borrowings are recognized under financial items.

11

0,42

0,41

0,35

0,38

0,35

0,32 0,31

0,290,28

0,29

0,13

0,12

0.15

0,09

0,12

0,15 0,15

0,14 0,14 0,11

0,25

0,30

0,35

0,40

0,45

0,50

0,55

Q2 06 Q2 07 Q2 08 Q2 09 Q2 10 Q2 11 Q2 12 Q2 13 Q2 14 Q2 15

Op

era

tin

g co

st E

BIT

DA

leve

l pe

r A

SK (

CA

SK)

CASK excl fuel

Fuel share of CASK

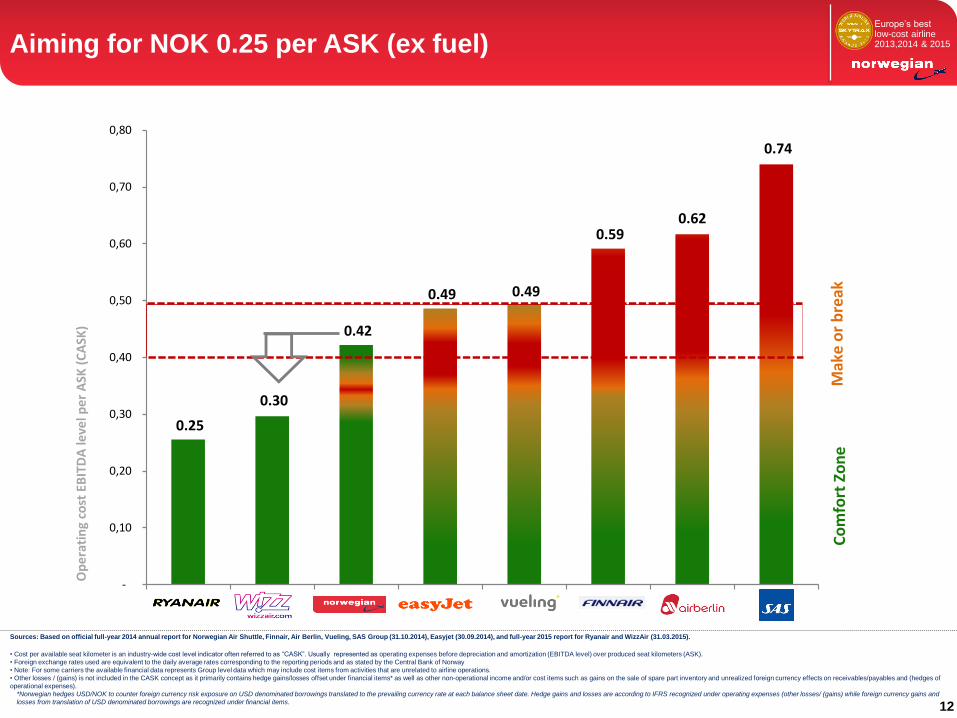

Europe’s best low-cost airline 2013,2014 & 2015 Aiming for NOK 0.25 per ASK (ex fuel)

• Cost per available seat kilometer is an industry-wide cost level indicator often referred to as “CASK”. Usually represented as operating expenses before depreciation and amortization (EBITDA level) over produced seat kilometers (ASK).

• Foreign exchange rates used are equivalent to the daily average rates corresponding to the reporting periods and as stated by the Central Bank of Norway

• Note: For some carriers the available financial data represents Group level data which may include cost items from activities that are unrelated to airline operations.

• Other losses / (gains) is not included in the CASK concept as it primarily contains hedge gains/losses offset under financial items* as well as other non-operational income and/or cost items such as gains on the sale of spare part inventory and unrealized foreign currency effects on receivables/payables and (hedges of

operational expenses).

*Norwegian hedges USD/NOK to counter foreign currency risk exposure on USD denominated borrowings translated to the prevailing currency rate at each balance sheet date. Hedge gains and losses are according to IFRS recognized under operating expenses (other losses/ (gains) while foreign currency gains and

losses from translation of USD denominated borrowings are recognized under financial items.

Sources: Based on official full-year 2014 annual report for Norwegian Air Shuttle, Finnair, Air Berlin, Vueling, SAS Group (31.10.2014), Easyjet (30.09.2014), and full-year 2015 report for Ryanair and WizzAir (31.03.2015).

12

0.25

0.30

0.42

0.49 0.49

0.59 0.62

0.74

-

0,10

0,20

0,30

0,40

0,50

0,60

0,70

0,80

Op

era

tin

g co

st E

BIT

DA

leve

l pe

r A

SK (

CA

SK)

Co

mfo

rt Z

on

eM

ake

or

bre

ak

Europe’s best low-cost airline 2013,2014 & 2015

8 58 11 1320

2223

23 22

115 5

2

2 5

5 5

5

5 5

5

7 16 21

23

2529

29

2720

16

2

810

13

13

13

1313

2

7 1523

30 4151 68

83

5

4

12

2

55

9

12

1

23

3

3

811 13

22

32

4046

5762

68

85

9599

117

144

0

20

40

60

80

100

120

140

2003year-end

2004year-end

2005year-end

2006year-end

2007year-end

2008year-end

2009year-end

2010year-end

2011year-end

2012year-end

2013year-end

2014year-end

2015year-end

2016year-end

2017year-end

B788 Owned

B788/B789 Leased

A320neo

B737 MAX 8

B738 owned

B738 S&LB

B738 leased

B733 owned

B733 leased

M80 leased

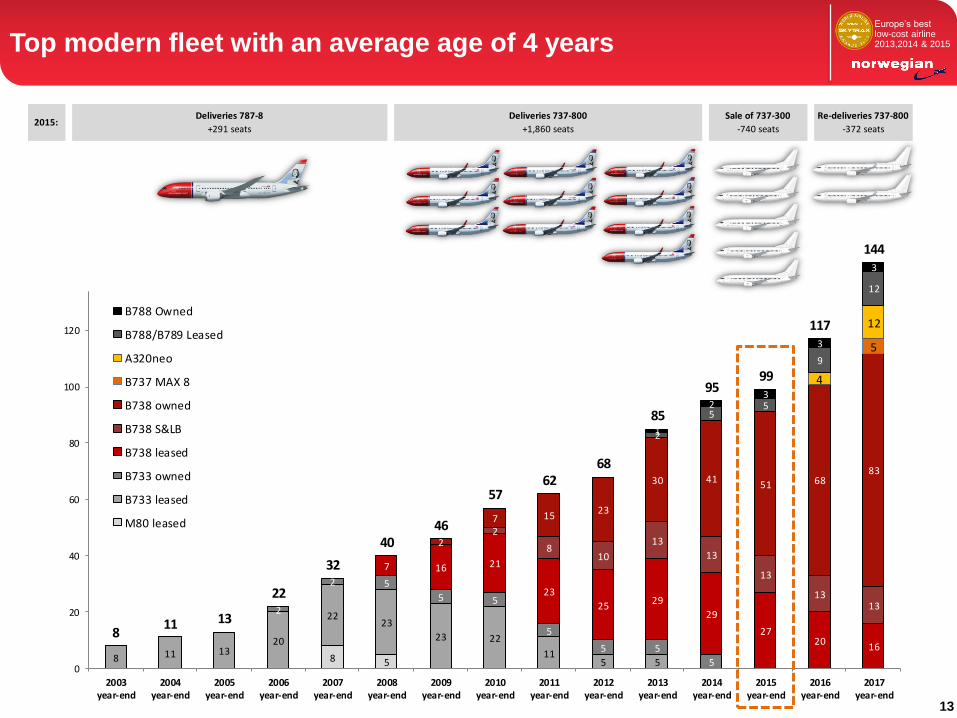

Top modern fleet with an average age of 4 years

13

2015:Sale of 737-300

-740 seats

Re-deliveries 737-800

-372 seats

Deliveries 737-800

+1,860 seats

Deliveries 787-8

+291 seats

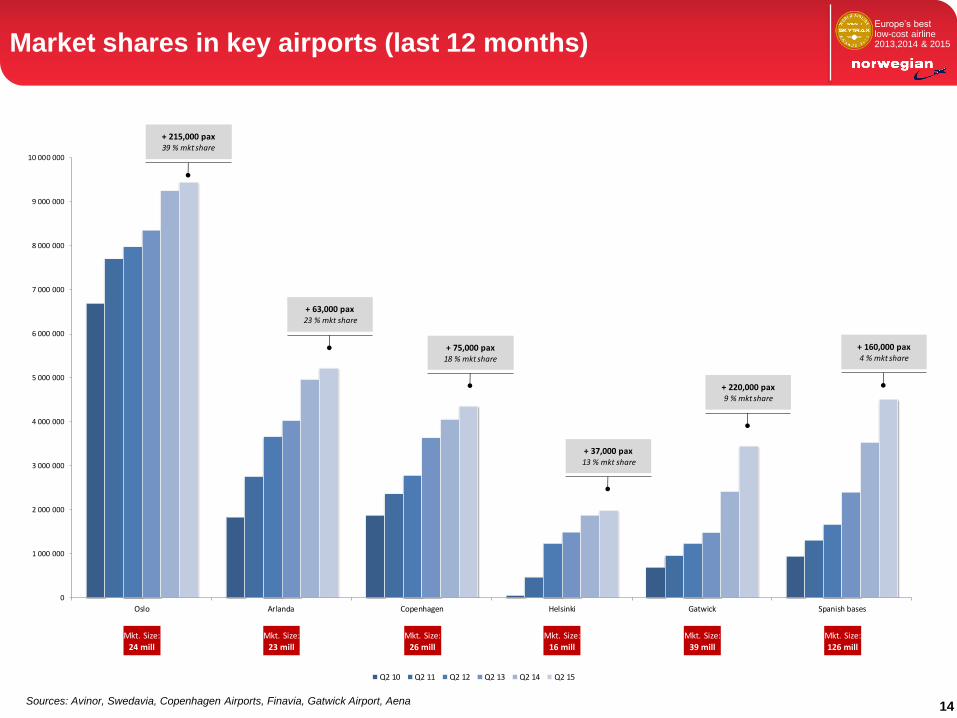

Europe’s best low-cost airline 2013,2014 & 2015 Market shares in key airports (last 12 months)

14

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

9 000 000

10 000 000

Oslo Arlanda Copenhagen Helsinki Gatwick Spanish bases

Q2 10 Q2 11 Q2 12 Q2 13 Q2 14 Q2 15

+ 215,000 pax 39 % mkt share

+ 63,000 pax23 % mkt share

+ 75,000 pax18 % mkt share

+ 37,000 pax13 % mkt share

+ 220,000 pax9 % mkt share

+ 160,000 pax4 % mkt share

Mkt. Size:24 mill

Mkt. Size:23 mill

Mkt. Size:126 mill

Mkt. Size:39 mill

Mkt. Size:16 mill

Mkt. Size:26 mill

Sources: Avinor, Swedavia, Copenhagen Airports, Finavia, Gatwick Airport, Aena

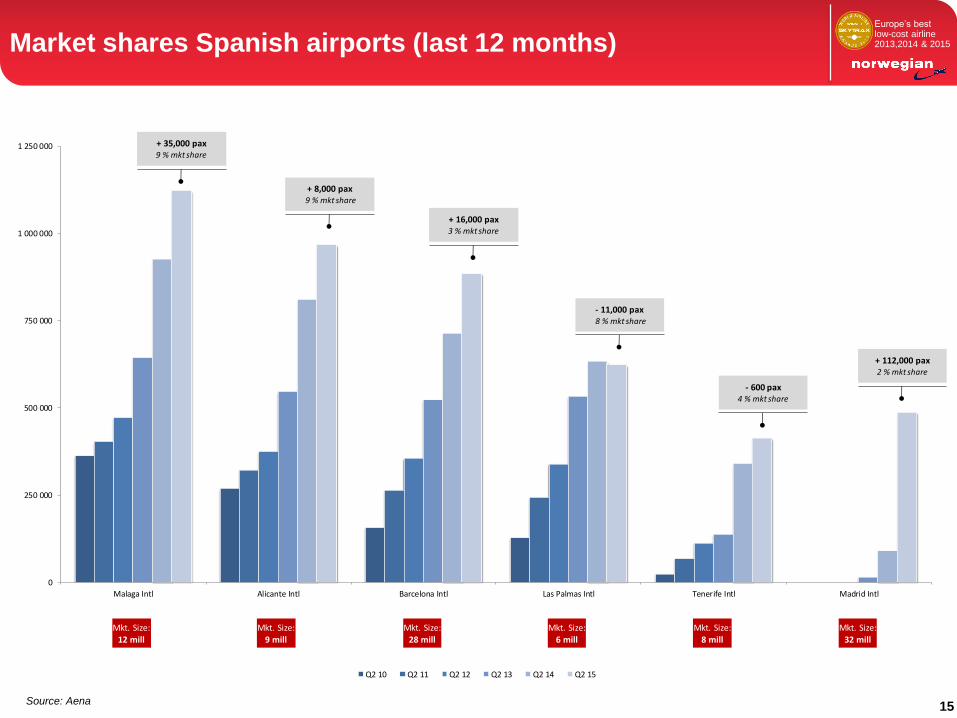

Europe’s best low-cost airline 2013,2014 & 2015 Market shares Spanish airports (last 12 months)

15

0

250 000

500 000

750 000

1 000 000

1 250 000

Malaga Intl Alicante Intl Barcelona Intl Las Palmas Intl Tenerife Intl Madrid Intl

Q2 10 Q2 11 Q2 12 Q2 13 Q2 14 Q2 15

+ 35,000 pax 9 % mkt share

+ 8,000 pax9 % mkt share

+ 16,000 pax3 % mkt share

- 11,000 pax8 % mkt share

- 600 pax4 % mkt share

+ 112,000 pax2 % mkt share

Mkt. Size:

12 mill

Mkt. Size:

9 mill

Mkt. Size:

32 mill

Mkt. Size:

8 mill

Mkt. Size:

6 mill

Mkt. Size:

28 mill

Source: Aena

Europe’s best low-cost airline 2013,2014 & 2015

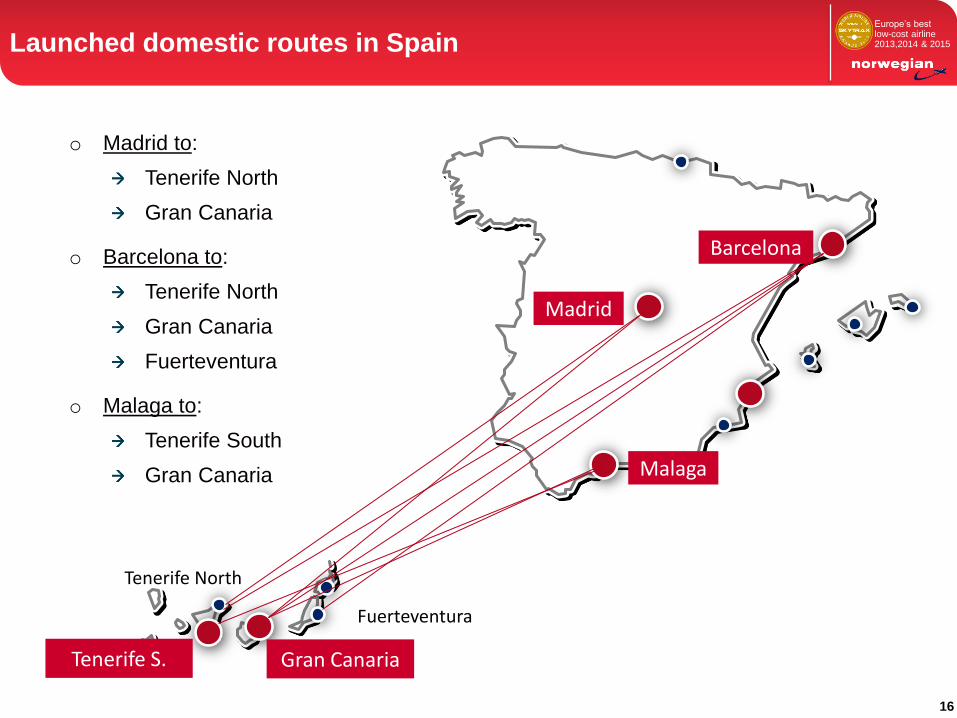

Madrid

Barcelona

Malaga

Fuerteventura

Gran Canaria Tenerife S.

Tenerife North

o Madrid to:

Tenerife North

Gran Canaria

o Barcelona to:

Tenerife North

Gran Canaria

Fuerteventura

o Malaga to:

Tenerife South

Gran Canaria

16

Launched domestic routes in Spain

Europe’s best low-cost airline 2013,2014 & 2015 New routes to North America and the Caribbean

17

Europe’s best low-cost airline 2013,2014 & 2015

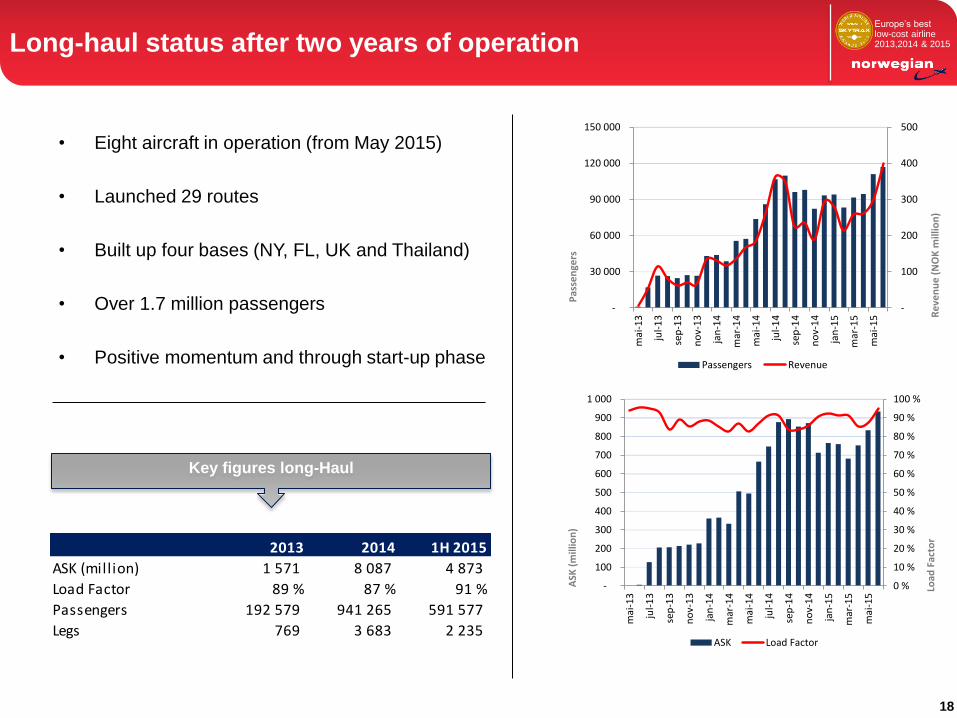

• Eight aircraft in operation (from May 2015)

• Launched 29 routes

• Built up four bases (NY, FL, UK and Thailand)

• Over 1.7 million passengers

• Positive momentum and through start-up phase

Long-haul status after two years of operation

Key figures long-Haul

-

100

200

300

400

500

-

30 000

60 000

90 000

120 000

150 000

mai

-13

jul-

13

sep

-13

no

v-1

3

jan

-14

mar

-14

mai

-14

jul-

14

sep

-14

no

v-1

4

jan

-15

mar

-15

mai

-15 R

eve

nu

e (

NO

K m

illio

n)

Pas

sen

gers

Passengers Revenue

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

-

100

200

300

400

500

600

700

800

900

1 000

mai

-13

jul-

13

sep

-13

no

v-1

3

jan

-14

mar

-14

mai

-14

jul-

14

sep

-14

no

v-1

4

jan

-15

mar

-15

mai

-15

Load

Fac

tor

ASK

(m

illio

n)

ASK Load Factor

18

2013 2014 1H 2015

ASK (million) 1 571 8 087 4 873

Load Factor 89 % 87 % 91 %

Passengers 192 579 941 265 591 577

Legs 769 3 683 2 235

Europe’s best low-cost airline 2013,2014 & 2015

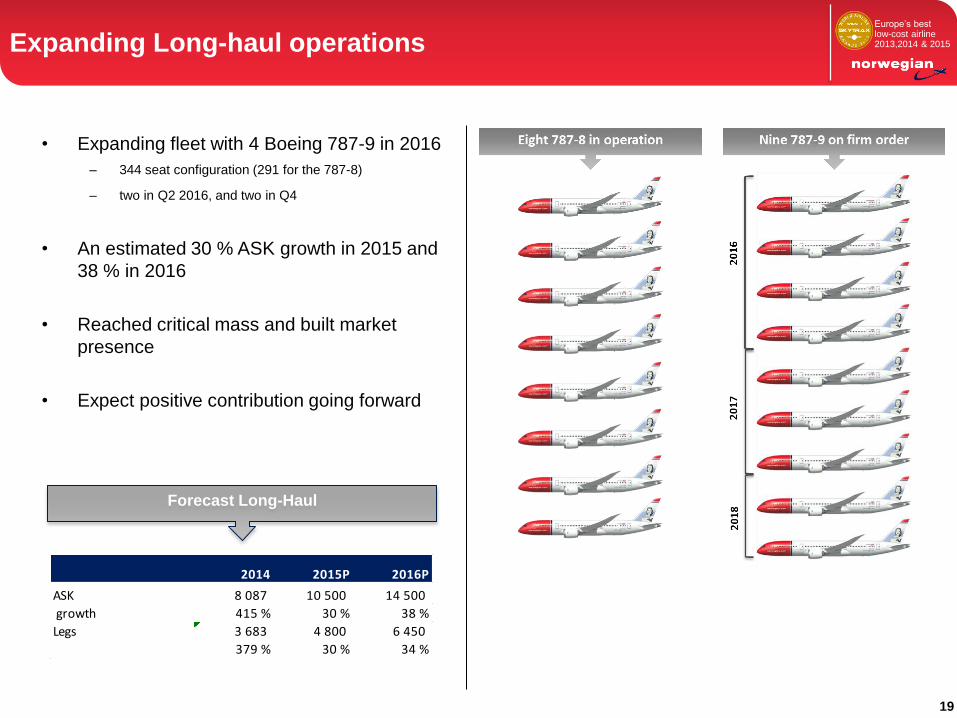

• Expanding fleet with 4 Boeing 787-9 in 2016

– 344 seat configuration (291 for the 787-8)

– two in Q2 2016, and two in Q4

• An estimated 30 % ASK growth in 2015 and

38 % in 2016

• Reached critical mass and built market

presence

• Expect positive contribution going forward

Expanding Long-haul operations

Forecast Long-Haul

2014 2015P 2016P

ASK 8 087 10 500 14 500

growth 415 % 30 % 38 %

Legs 3 683 4 800 6 450

379 % 30 % 34 %

19

Europe’s best low-cost airline 2013,2014 & 2015

• Business environment

– Bookings for Q3 2015 ahead of last year (capacity adjusted)

– Stable market in the Nordic region

– Good load and improving yield for long-haul

• The company expects a production growth (ASK) of 5 % (unchanged)

– Increasing utilization and distance driven by long-haul

– Continuous optimization of the route portfolio

• Unit cost target in the range of NOK 0.39 to 0.40 (unchanged)

– Fuel price assumption: USD 575 per MT

– Currency assumptions: USD/NOK 7.5 and EUR/NOK 8.5

– Including impact of pilot-strike

– Based on the current planned route portfolio and mix

• Investments and capex

– Aircraft deliveries:

• 2015: 11 new aircraft; 10 B737 and one B787-8 (returning 7 older aircraft)

• 2016: 25 aircraft; 17 B737, 4 A320Neo, 4 leased B787-9 (returning 7 leased 737, lease out 4 Neo’s)

– Expected capex mainly related to PDP and aircraft deliveries for FY 2015 and

2016 of NOK 5.5bn and 8.4bn, respectively

Expectations for 2015 (Group)

20

Europe’s best low-cost airline 2013,2014 & 2015

• Awarded Europe’s Best Low-Cost Carrier

2015 and Global Best Low-Cost Long-

Haul Carrier 2015 by SkyTrax

• Bookings for Q3 2015 ahead of last year

• An estimated NOK 2 billion lower fuel

cost for 2015

• Expect positive contribution from Long-

Haul going forward

• Aiming for further unit cost reductions

• Successful placing of NOK 1 billion bond

Summary

21

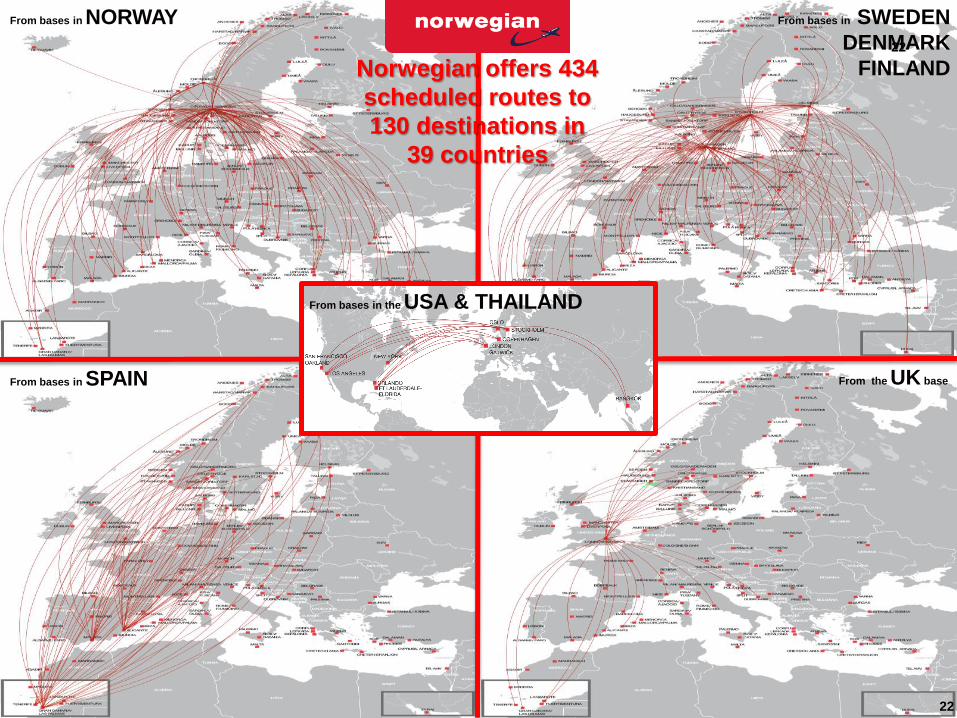

From bases in NORWAY From bases in SWEDEN

DENMARK

FINLAND

From the UK base From bases in SPAIN

From bases in the USA & THAILAND

Norwegian offers 434

scheduled routes to

130 destinations in

39 countries

22

22