Embed Size (px)

Citation preview

Norwegian Air Shuttle ASAQ1 2016 Presentation 21 April 2016

Highlights Q1 2016

Launched new routes to/from Paris and the USA (LAX, NYC and FLL) and a short haul base in Rome, Italy

Norwegian Reward reached 4 million members

Tentative approval of NAI by the US Department of Transportation (DoT)

Added five new 737-800 aircraft and one 787-9 Dreamliner to the fleet

Clean EBITDA improved by NOK 400 million

2

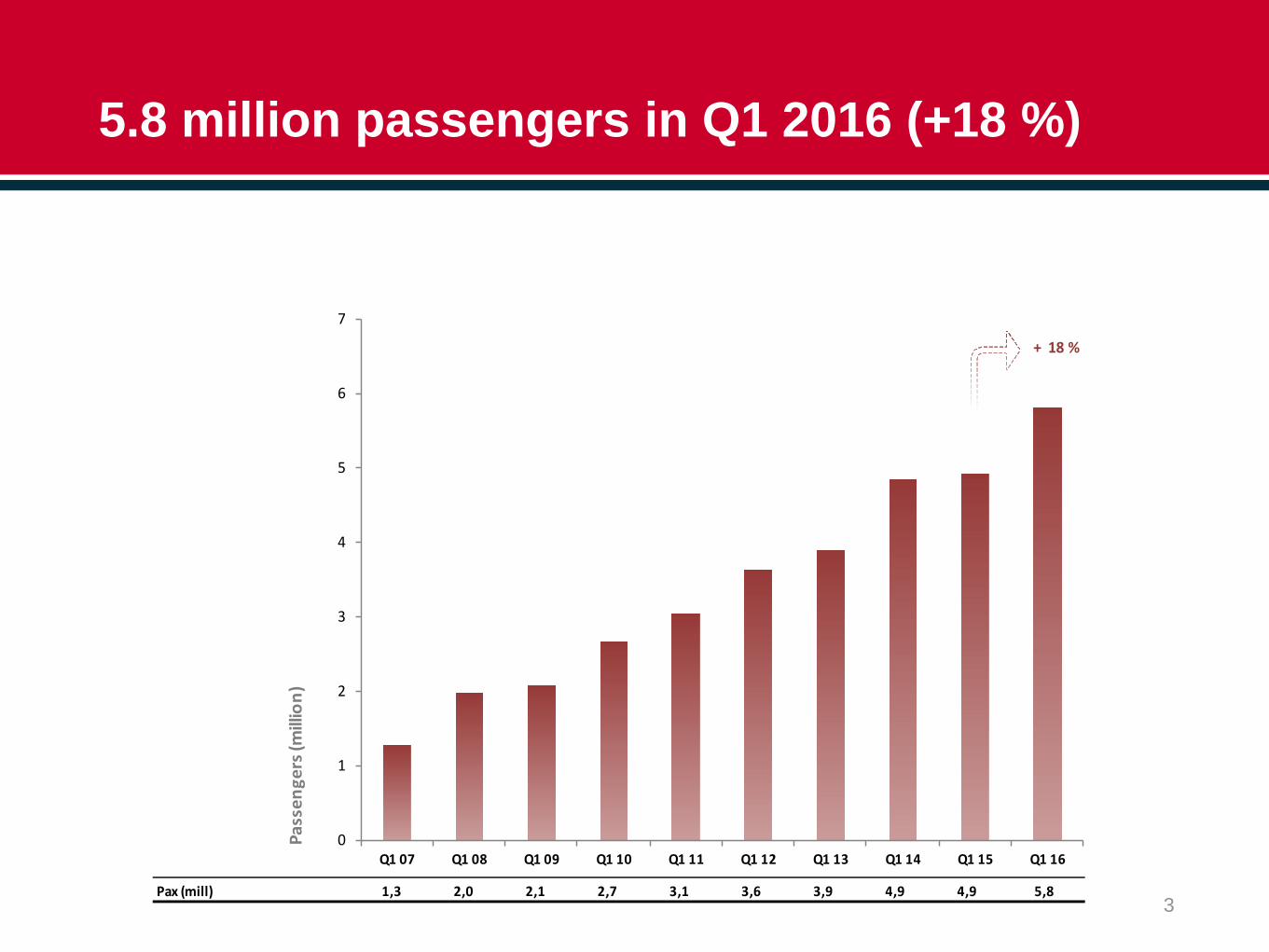

5.8 million passengers in Q1 2016 (+18 %)

3Pax (mill) 1,3 2,0 2,1 2,7 3,1 3,6 3,9 4,9 4,9 5,8

0

1

2

3

4

5

6

7

Q1 07 Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14 Q1 15 Q1 16

Pass

enge

rs (m

illio

n)

+ 18 %

Q1 load factor up to 85 % (+2 p.p.)

4

ASK 1 342 2 183 2 674 3 507 4 498 5 266 6 378 9 421 10 056 11 803

Load Factor 74,8 % 77,2 % 74,8 % 75,1 % 74,3 % 77,2 % 76,1 % 77,3 % 83,0 % 85,1 %

74,8 %77,2 %

74,8 % 75,1 % 74,3 %77,2 % 76,1 % 77,3 %

83,0 %85,1 %

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

11 000

12 000

13 000

14 000

15 000

16 000

17 000

18 000

Q1 07 Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14 Q1 15 Q1 16

Load

Fact

or

Avai

labl

e Se

at K

M (A

SK)

ASK Load Factor Load+2 p.p.

17 % growth in capacity (ASK)

21 % growth in traffic (RPK)

Average flying distance increased by 4 %

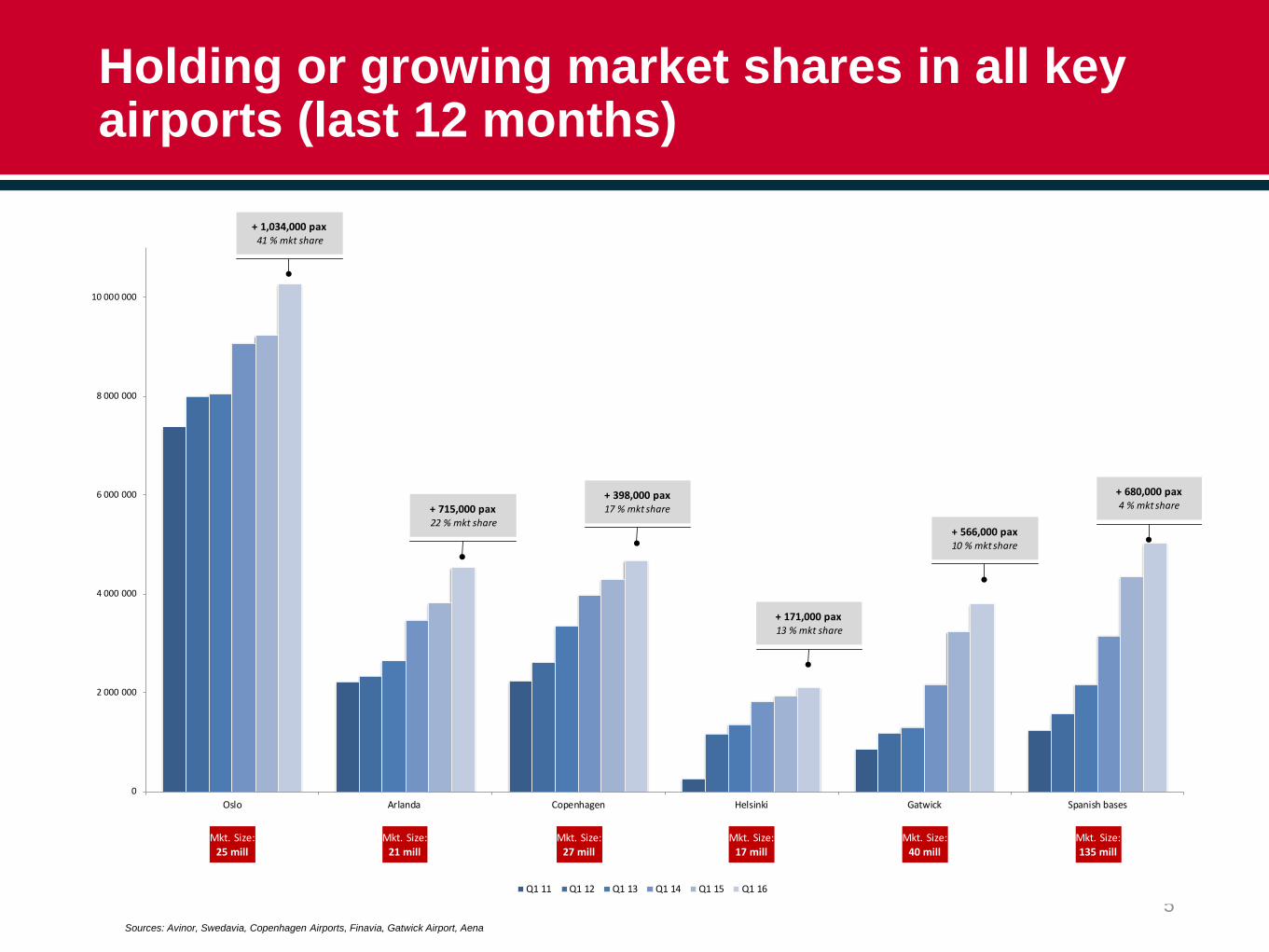

Holding or growing market shares in all key airports (last 12 months)

5

0

2 000 000

4 000 000

6 000 000

8 000 000

10 000 000

Oslo Arlanda Copenhagen Helsinki Gatwick Spanish bases

Q1 11 Q1 12 Q1 13 Q1 14 Q1 15 Q1 16

+ 1,034,000 pax 41 % mkt share

+ 715,000 pax22 % mkt share

+ 398,000 pax17 % mkt share

+ 171,000 pax13 % mkt share

+ 566,000 pax10 % mkt share

+ 680,000 pax4 % mkt share

Mkt. Size:25 mill

Mkt. Size:21 mill

Mkt. Size:135 mill

Mkt. Size:40 mill

Mkt. Size:17 mill

Mkt. Size:27 mill

Sources: Avinor, Swedavia, Copenhagen Airports, Finavia, Gatwick Airport, Aena

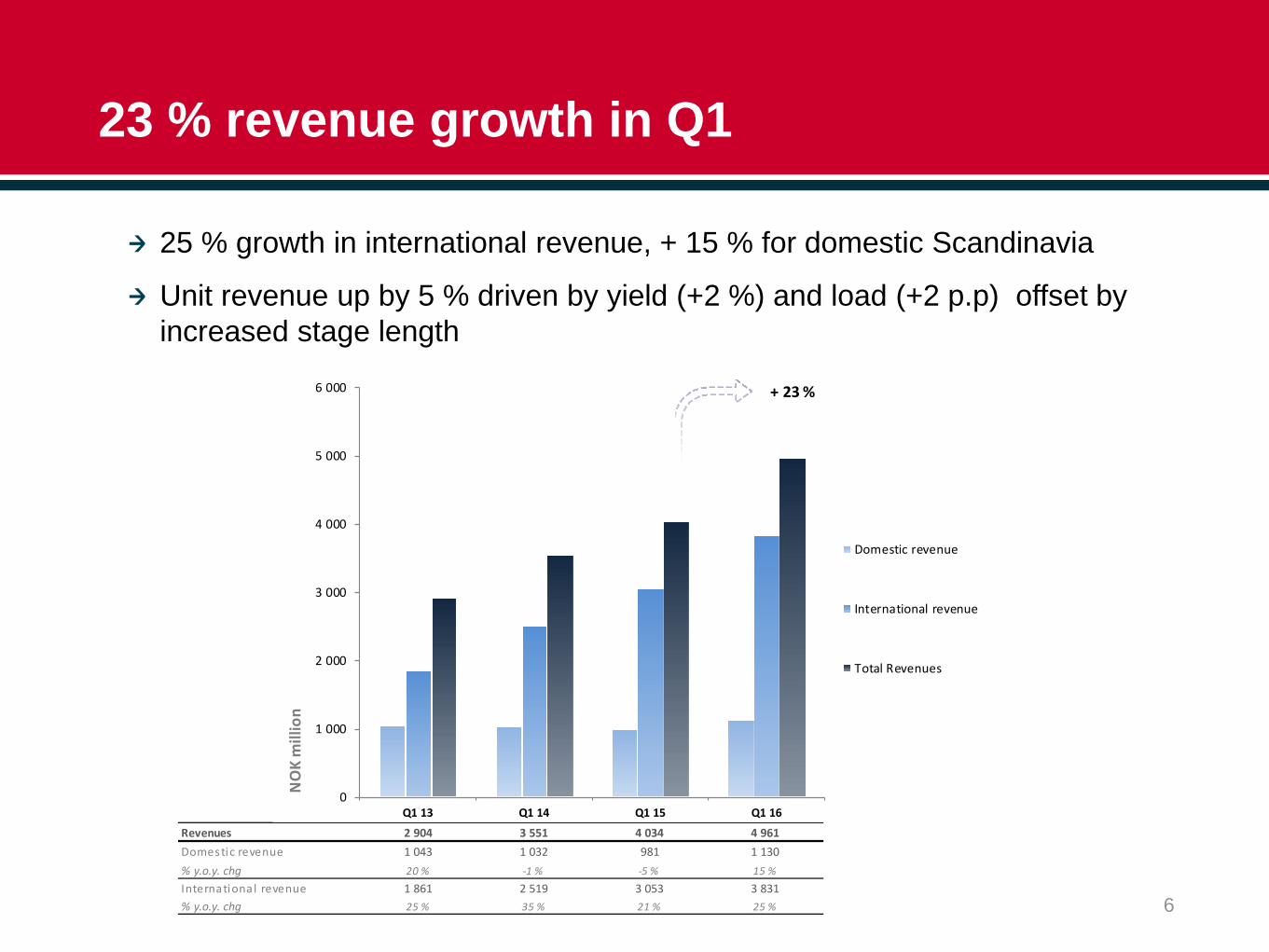

23 % revenue growth in Q1

6

Revenues 2 904 3 551 4 034 4 961Domestic revenue 1 043 1 032 981 1 130% y.o.y. chg 20 % -1 % -5 % 15 %International revenue 1 861 2 519 3 053 3 831% y.o.y. chg 25 % 35 % 21 % 25 %

0

1 000

2 000

3 000

4 000

5 000

6 000

Q1 13 Q1 14 Q1 15 Q1 16

NO

K m

illio

n

Domestic revenue

International revenue

Total Revenues

+ 23 %

25 % growth in international revenue, + 15 % for domestic Scandinavia

Unit revenue up by 5 % driven by yield (+2 %) and load (+2 p.p) offset by increased stage length

19 % growth in ancillary revenue in Q1

7

16 % share of Group revenue

1 % growth per passenger

Other Ancillary Other Ancillary

BaggageBaggage

SeatingSeating

Pre-sold packages(bundle)

Pre-sold packages (bundle)

Flexibility/ modifications

Flexibility/ modifications

Q1 15 Q1 16

NOK 138

Optional extras

NOK 136

Growing share of revenue in USD, GBP and Euro Norway now reduced to 35 % of group passengersOver 40% of passengers booking from outside Scandinavia

Strongest growth in USA and Spain

8

0% 10% 20% 30% 40% 50% 60%

Finland

Denmark

Italy

Norway

UK

Sweden

France

Hungary

Spain

USA

Norway

SwedenSpain

Denmark

UK

Finland

USAGermany

Poland

FranceItaly

Hungary Other

New corporate contracts boosting sales

Revenue from corporate agreements Q1:• Norway up by 22 % y-o-y• Sweden up by 17 % y-o-y

Corporate contracts signed in Q1 2016:Forsvaret (Norwegian army) • Four year contract from February for 17,000 employees

(Norwegian only)

NAV (Norwegian Labour and Welfare Administration) • Two year contract + option to extend 2 x 1 year, for 19,000

employees (Norwegian only)

HINAS (Norwegian health care system)• Three year contract from April, 13 domestic routes for

employees and patients

9

ChangeRetail 65 %Consultants 38 %Construction 24 %Health Care 18 %IT/Telecom 13 %Bank/Finace 13 %Public sector 10 %Industrials 9 %Media -2 %Oil/Offshore -4 %

Reported earnings: lower fuel offset by currency

10

Q1 13 Q1 14 Q1 15 Q1 16 Q1 13 Q1 14 Q1 15 Q1 16EBITDAR margin 15 % -6 % 2 % 1 % EBT margin -6 % -23 % -19 % -20 %

438

-215

69 63

-300

-200

-100

0

100

200

300

400

500

NO

K m

illio

n

-160

-813 -776

-992

-1 300

-1 050

-800

-550

-300

-50

200

NO

K m

illio

n

EBT development Q1EBITDAR development Q1

(NOK million) Q1 15 Q1 16 Change

Revenue 4 034 4 961

EBITDAR 69 63 -6

EBITDA -502 -606 -104

Pre-tax profit (EBT) -776 -992 -216

Net profit -538 -800

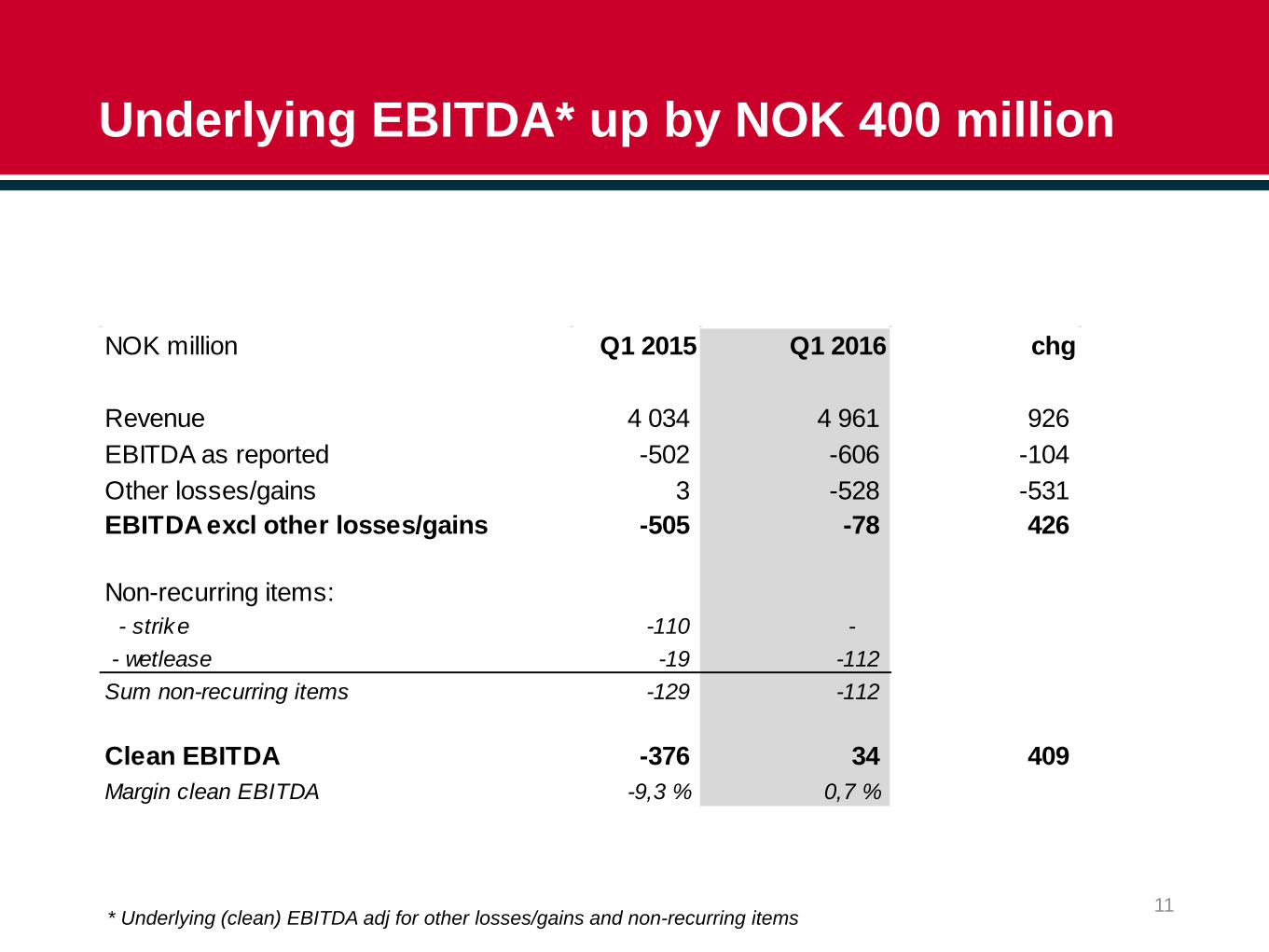

Underlying EBITDA* up by NOK 400 million

11* Underlying (clean) EBITDA adj for other losses/gains and non-recurring items

NOK million Q1 2015 Q1 2016 chg

Revenue 4 034 4 961 926 EBITDA as reported -502 -606 -104 Other losses/gains 3 -528 -531 EBITDA excl other losses/gains -505 -78 426

Non-recurring items: - strike -110 - - wetlease -19 -112 Sum non-recurring items -129 -112

Clean EBITDA -376 34 409 Margin clean EBITDA -9,3 % 0,7 %

Unit cost cut by 5 %

CASK ex fuel +1 % to NOK 0.35 on currency

12

0,44

0,46 0,450,40

0,37 0,360,33 0,32

0,35 0,35

0,11

0,16

0.15

0,11 0,12 0,15

0,13 0,14

0,10 0,07

0,00

0,05

0,10

0,15

0,20

0,25

0,30

0,35

0,40

0,45

0,50

0,55

Q1 07 Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14 Q1 15 Q1 16

Ope

ratin

g co

st E

BITD

A le

vel p

er A

SK (C

ASK)

CASK excl fuel

Fuel share of CASK

Other losses / (gains) is not included in the CASK concept as it primarily contains hedge gains/losses offset under financial items* as well as other non-operational income and/or cost items such as gains on the sale of spare part inventory and unrealized foreign currency effects on receivables/payables and (hedges of operational expenses).*Norwegian hedges USD/NOK to counter foreign currency risk exposure on USD denominated borrowings translated to the prevailing currency rate at each balance sheet date. Hedge gains and losses are according to IFRS recognized under operating expenses (other losses/ (gains) while foreign currency gains and losses from translation of USD denominated borrowings are recognized under financial items.

Fuel share of opex reduced to 15 % (23% in Q115)

7 % negative impact of currency

Fuel hedging: • 50 % of 2016• 27 % of 2017

13

0,00

0,02

0,04

0,06

0,08

0,10

0,12

0,14

0,16

Q1 11 Q1 12 Q1 13 Q1 14 Q1 15 Q1 16

12 mths rolling 12 mths rolling 12 mths rolling 12 mths rolling 12 mths rolling 12 mths rolling

Personnel

Other

Technical

Airport/ATC

Leasing

Depreciation

Sales & Distribution

Handling

Fuel

Fuel15 %

Personnel16 %

Airport & ATC12 %

Handling10 %

Leasing12 %

Technical7 %

Gen. and adm. exp.

5 %

Other Flight ops. exp.

4 %

Depr.4 %

Sales/ distrib.

2 %

NOK 1 bn higher cash-flow from operations

14

Invested NOK 1.7 bn in new B737-800 aircraft

NOK 3.2 billion in cash at the end of Q1

Q1 Q1NOK million 2015 2016 Change

Profit before tax -777 -992 -215Depreciation 220 288 68Air traffic settlement liabilities 2 497 2 954 457Change working capital -945 -243 702Net cash flows from operating activities 996 2 007 1 012Net cash flows from investing activities -1 597 -1 666 -69Net cash flows from financial activities 196 375 179Foreign exchange effect on cash 10 20 10Net change in cash and cash equivalents -396 736 1 132Cash and cash equivalents, end of period 1 615 3 190 1 574

Net debt reduced by NOK 1 bn in the quarter

15

Added five new 737-800 on balance + PDP’s

NOK 16 bn net debt (reduced from NOK 17bn at the end of 2015)

Equity ratio of 6 % (11 % incl. market value of Bank Norwegian)

1 615Cash3 190

2 998

Receivables3 180

5 134 Other assets

2 139

4 103 Aircraft PDP 5 939

12 512

Aircraft18 536

0

3 000

6 000

9 000

12 000

15 000

18 000

21 000

24 000

27 000

30 000

33 000

Q1 15 Q1 16

NO

K m

illio

n

Equity1 986 1 876

Pre-sold tickets6 969 5 462

Otherliabilities

4 9314 311

PDP and bonds6 104

4 684

Aircraft Financing

12 994

10 028

Q1 16 Q1 15

Aircraft financing on track

Expected capex (all aircraft incl. PDP)USD 1.1 bn for 2016 (unchanged)USD 2 bn for 2017USD 2 bn for 2018

PDP financingPDP financing with backstop lease B 737 800 (in 1H 2016)PDP Financing for 50 A320 Neo’s in placeNegotiating PDP financing for Boeing deliveries

Long-term financingCommercial financing of 6 B 737 800 Ex-Im and ECAEETC

16

Top modern fleet with an average age of 3.6 years

17

8 58 11 1320

22 2323 22

115 5

2

2 55 5

55 5

5

7 16 21

2325 29

2927 23 19

28

1013

13

1313

13

2

7 15 23

30 41 5168

85

6

4

12

2

55

9

14

1

23

3

7

8 11 1322

3240

46

5762

68

85

9599

120

156

0

20

40

60

80

100

120

140

160

2003year-end

2004year-end

2005year-end

2006year-end

2007year-end

2008year-end

2009year-end

2010year-end

2011year-end

2012year-end

2013year-end

2014year-end

2015year-end

2016year-end

2017year-end

B788/B789 Owned

B788/B789 Leased

A320neo owned

B737 MAX 8 owned

B738 owned

B738 S&LB

B738 leased

B733 owned

B733 leased

M80 leased

Re-deliveries 737-800-744 seats

2016:Deliveries 737-800

+3,162 seatsDeliveries 787-9

+1376 seats

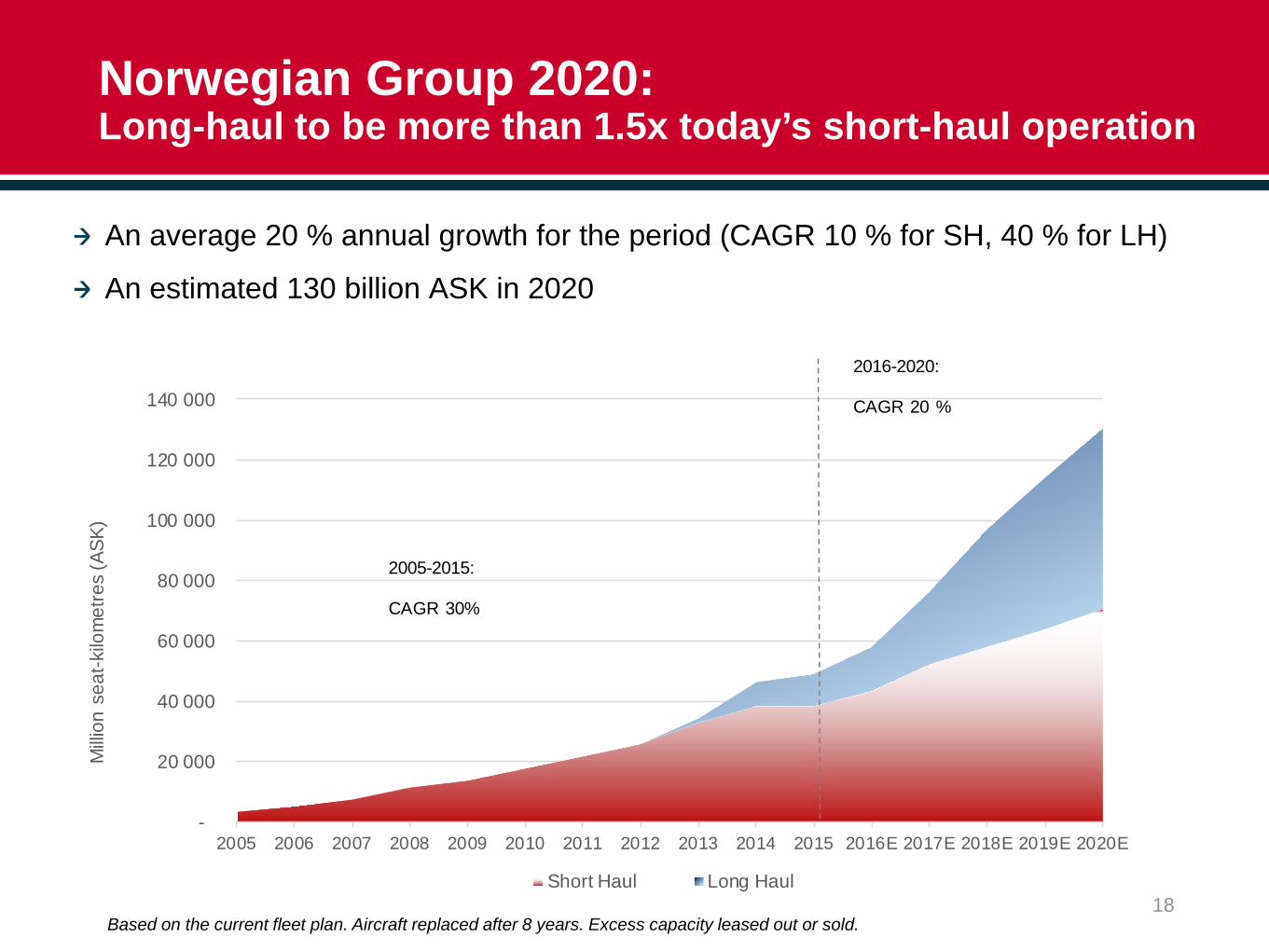

Norwegian Group 2020: Long-haul to be more than 1.5x today’s short-haul operation

An average 20 % annual growth for the period (CAGR 10 % for SH, 40 % for LH)

An estimated 130 billion ASK in 2020

18

-

20 000

40 000

60 000

80 000

100 000

120 000

140 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Milli

on s

eat-k

ilom

etre

s (A

SK)

Short Haul Long Haul

2016-2020:

CAGR 20 %

2005-2015:

CAGR 30%

Based on the current fleet plan. Aircraft replaced after 8 years. Excess capacity leased out or sold.

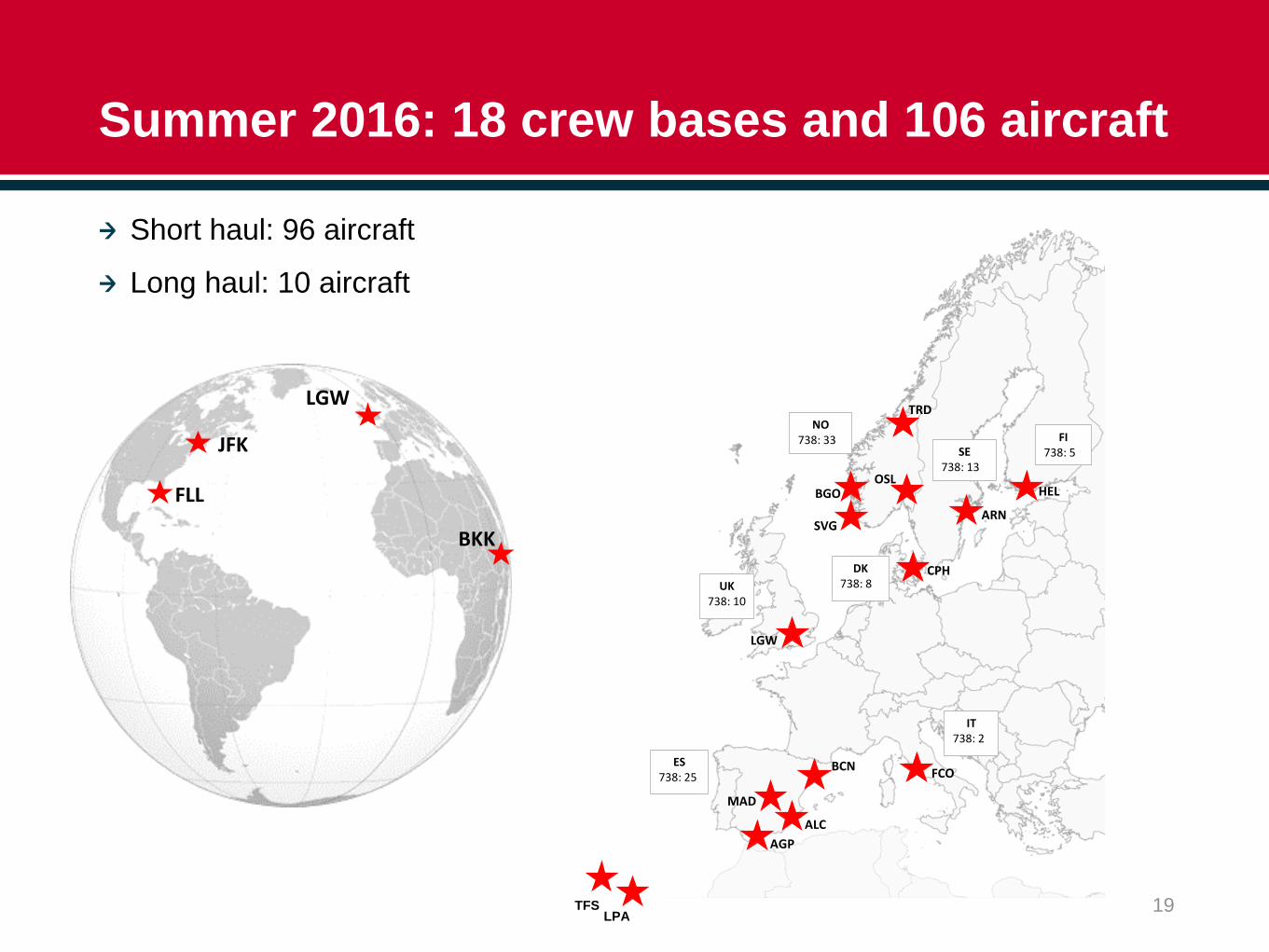

Summer 2016: 18 crew bases and 106 aircraft

19

BGO

BCN

OSLHEL

ARN

LGW

ALCAGP

MAD

CPH

TRD

SVG

UK738: 10

ES738: 25

NO738: 33

SE738: 13

FI738: 5

DK738: 8

FCO

IT738: 2

LGW

BKK

JFK

FLL

Short haul: 96 aircraft

Long haul: 10 aircraft

LPATFS

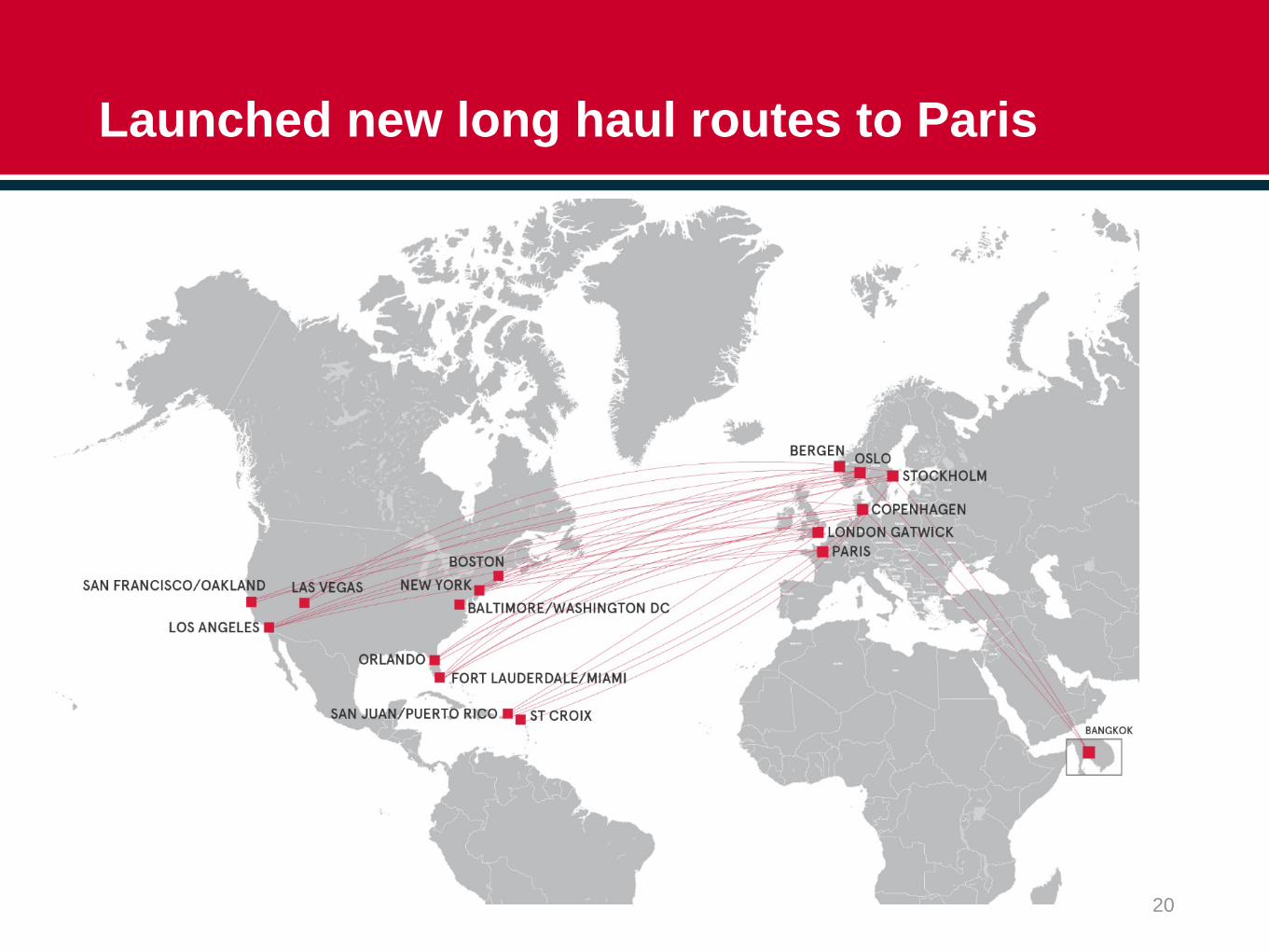

Launched new long haul routes to Paris

20

Outlook for 2016

Markets and business Soft macro and passenger tax to be introduced in Norway, strong competition in DenmarkStable in other key marketsPositive momentum for long-haulGroup bookings ahead of last year, capacity adjusted

An estimated production growth (ASK) of 18 % (unchanged)Short-haul + 12 %, Long-haul + 40 %Increasing distance driven by mix (long-haul)

Unit cost in the area of NOK 0.37 (unchanged)Assumptions: Fuel price of USD 350 per metric ton, USD/NOK 8.25, EUR/NOK 9.00 Based on the current route portfolio and planned production

25 aircraft scheduled for delivery in 2016 Seventeen direct buy B737-800 (returning four leased 737-800)Four leased B787-9 DreamlinersFour direct buy A320Neo (to be leased out)

21

Summary

Won several corporate agreements as businesses want to reduce travel expenses

NAI has received tentative approval from DoT

Bookings ahead of last year

Financing on-track

Unchanged guidance for 2016 on production and unit cost

Bank Norwegian to be listed on OSE

22

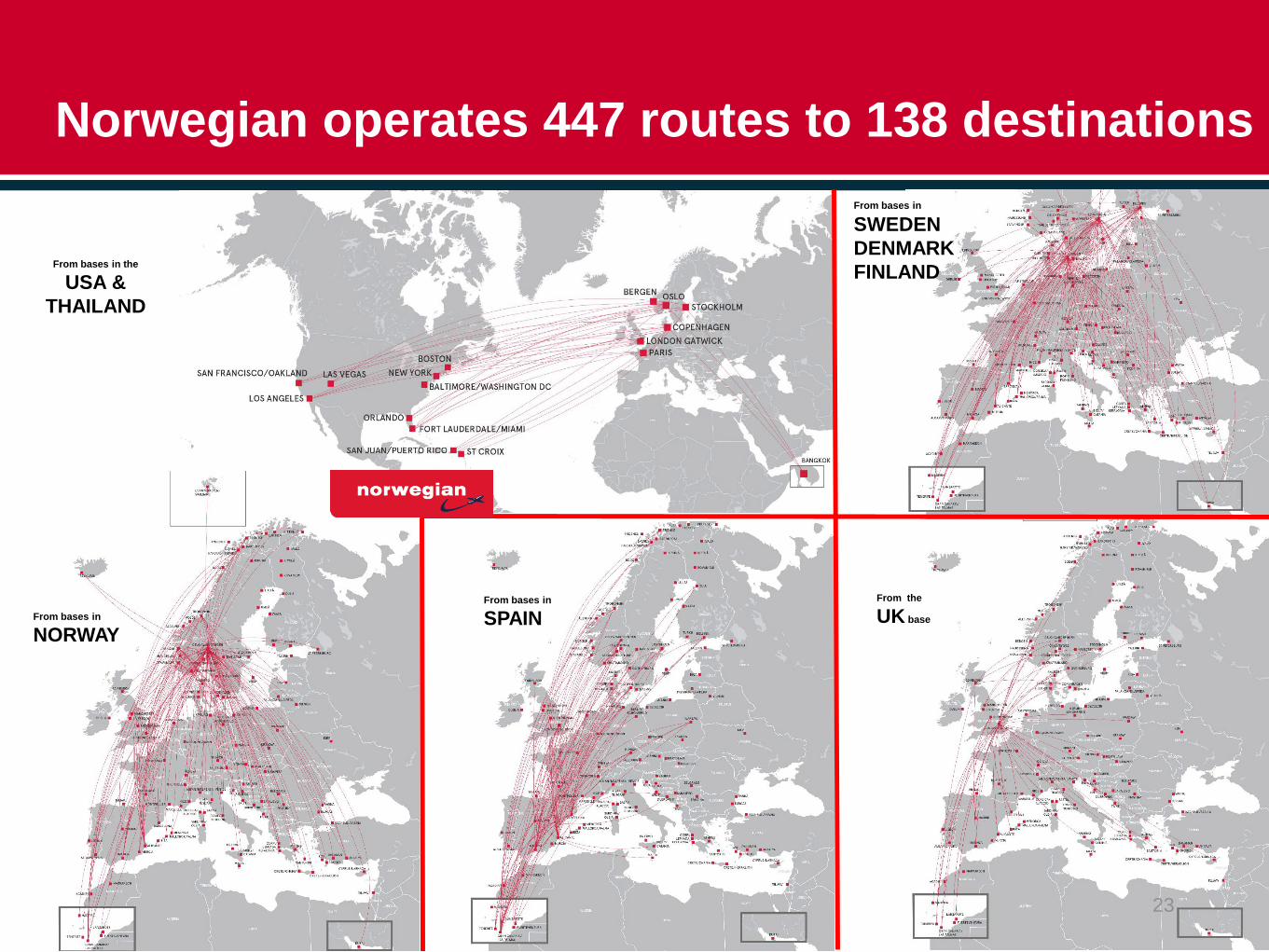

Norwegian operates 447 routes to 138 destinations

23

From bases in

SWEDEN DENMARK FINLAND

From the

UK base

From bases in

SPAIN

From bases in the

USA & THAILAND

From bases in

NORWAY

![$ EDUCATIONAL FACILITIES REVENUE [AND REVENUE REFUNDING… · EDUCATIONAL FACILITIES REVENUE [AND REVENUE REFUNDING] ... Educational Facilities Revenue [and Revenue ... Aeronautical](https://img.pdfslide.net/doc/110x75/5b16e1207f8b9a686d8e7aa7/-educational-facilities-revenue-and-revenue-refunding-educational-facilities.jpg)