Embed Size (px)

Citation preview

-FILE ALBERTA STOCK EXCHANGE

NOTICE TO MEMBERS

No. 95-04

March 8, 1995

FORMER APPROVED PERSON DISCIPLINED

Following a contested hearing and penalty submissions, a panel of the Hearing

Committee of The 2dberta Stock Exchange (the "Exchange") imposed penalties upon

Brian Michael Meyer for violations of sections 16.01(1), 16.07(1) and 21.14(1) of the

General By-law of the Exchange (the "By-law") as follows:

1. A suspension from acting in the capacity of an Approved Person for a periodof three (3) years;

2. A fine in the sum of $30,000 plus investigation and hearing costs of

$16,413.52, totalling $46,413.52;

3. Strict supervision for a period of one (1) year following reregistration;

4. Close supervision for a further period of one (1) year following the initialperiod of strict supervision; and

5. Successful completion of the Canadian Securities Course, The Conduct &

Practices Handbook for Securities Industry Professionals and Canadian

Options Course examinations prior to reregistration.

Section 16.01(1) of the By-law requires every Approved Person to learn the essential

facts relative to every customer and every order or account accepted, to ensure thatthe acceptance of any order is within the bounds of good business practice, and to

ensure that recommendations made for any account are appropriate for the client and

in keeping with his investment objectives.

Section 16.07(1) of the By-law prohibits an Approved Person from accepting

authorization for a discretionary account. Section 16.07(1) also prohibits the exercise

of discretionary power with respect to a client's account unless the client has given

prior written authorization and the account has been accepted in writing by a Partneror Director designated pursuant to the By-law.

Section 21.14(1) of the By-law prescribes penalties whic, may be/mposed by theExchange.

1_ Stock Exchange Tower. 21st Floor, 300 Fifth Avenue S.W., Calgary, Alberta T2P 3C4Telephone: (403) 974-7400 Fax: (403) 237-0450

ANOTICE TO MEMBERS

-2-

While an Approved Person, Mr. Meyer conducted trading activity m the accounts ofthree clients which was unsuitable for such clients. By so doing, Mr. Meyer failed touse due diligence to ensure that recommendations made for the accounts of thoseclients were appropriate for the said clients and in keeping with their investmentobjectives, contrary to section 16.01(1) of the By-law.

While an Approved Person, Mr. Meyer placed numerous trades in the accounts ofseven clients without their prior knowledge, authorization or approval, contrary tosection 16.07(1) of the By-law.

Factors considered by the Hearing Panel in its ruling included Mr. Meyer's apparentlack of remorse or contrition for his conduct in relation to these matters.

At the time of the infractions, Mr. Meyer was employed as a RegisteredRepresentative with the Red Deer office of Richardson Greenshields of Canada!,im_ted. No fault has been attributed to the member firm.

Copies of the Reasons for Decision of the Hearing Panel of the Exchange are availableon request.

Mr. Meyer has filed a Notice of Appeal. The appeal is scheduled to be heard onThursday, March 30, 1995 before the Board of Governors.

BY ORDER OF THE BOARD OF GOVERNORS

Jill A. Browne

Legal Counsel & Exchange Secretary (Acting)

IN THE MATTER OFTHE ALBERTA STOCK EXCHANGE ACT, S.A. 1974, C. 79

AND IN TIlE MATTER OF THE GENERAL BY-LAWOF THE ALBERTA STOCK EXCHANGE

AND IN THE MATTER OFBRIAN MICHAEL MEYER

NOTICE OF HEARING AND PARTICULARS

TAKE NOTICE that a heating will be held before a panel of the Hearing Committee ofThe Alberta Stock Exchange (the "Exchange") pursuant to section 21.14 of the General By-lawof the Exchange (the "By-law") on March 14, 15, and 16, 1994 commencing at 9:00 in the

'_ forenoon or so soon thereafter as this matter may be heard, at the offices of the Exchange, 2100,300 Fifth Avenue, S.W., Calgary, Alberta, to consider whether Brian Michael Meyer (the

"Respondent") has contravened sections 16.01, 16.07, and 21.14(1)(b) of the By-law and section54(1) of the Alberta Securities Act, S.A. 1981, c. S-6.1 and to consider the imposition of suchpenalties or remedies, if any, against the Respondent as may be considered appropriate.

AND FURTI/F__ TAKE NOTICE that a summary of the facts alleged and intended to

be relied upon by the Exchange and the conclusions drawn therefrom are as follows:

1. Respondent has been an Approved Person as that term is defined in the By-law from April19, 1989 to March 26, 1993. During this period, the Respondent was employed as aRegistered Representative with Richardson Greenshields of Canada Limited ("Richardson")in Red Deer, Alberta.

2. The Respondent was discharged by Richardson on March 26, 1993. The UniformTermination Notice filed with the Exchange in relation to such termination of employmentindicates that the Respondent was dismissed for, among other reasons, discretionary andunsuitable trading.

3. At all times material hereto, the Respondent was the Registered Representative responsiblefor the following accounts:

-2-

ClientName(s) AccountNo. DateOpened

Anderson, Donald Barry 56-7531-2 Aug 20/90Anderson, Vicki 56-0419-5 Dec 02/88Anderson, Vicki 56-0461-0 Jan 08/90Evans, William 56-7520-L Mar 30/89Hilgartner, Ralph & Mary 56-0521-0 Jan 30/91Lacey, Gordon & Norma 56-0543-9 Nov 13/89McMullen Farms Ltd. 56-0543-0 Oct 03/91

McMullen, Floyd & Ruth 56-0528-5 May 07/91Riffenstein, Randy 56-7538-3 Mar 30/92

4. The Respondent opened a self directed RRSP account for Donald Barry Anderson onAugust 20, 1990. Pursuant to instructions received from Mr. Anderson, the Respondentpurchased 900 shares of Telus Corp. on October 10, 1990.

5. On December 18, 1990, the Respondent sold 900 shares of Telus Corp. and purchased1,000 shares of Corona Corp. A for Mr. Anderson's account without his prior knowledge,authorization or approval.

S"

_" 6. On March 5, 1991, the Respondent purchased 2,500 shares of Circa TelecommunicationsInc. for Mr. Anderson's account without his prior knowledge, authorization or approval.

7. Mr. Anderson became aware of the transactions referenced in paragraphs 5 and 6 hereofthrough a third party, Donna Carson.

8. The transactions referenced in paragraphs 5 and 6 above generated gross commissions tothe Respondent in the sum of $441.00.

9. On December 8, 1989, the Respondent became the Registered Representative for theaccount of Vicki Anderson (account no. 56-0419-5). The new client account form

("NCAF") for this account indicates a net worth of $200,000, annual income of $20,000,and investment objectives of 50 % security and 50 % income.

10. On January 8, 1990, the Respondent opened a margin account for Mrs. Anderson (accountno. 56-0461-0) for the purposes of conducting hedge spread transactions and completeda NCAF, listing investment objectives as 25 % security, 25 % growth, 25 % income and25 % risk.

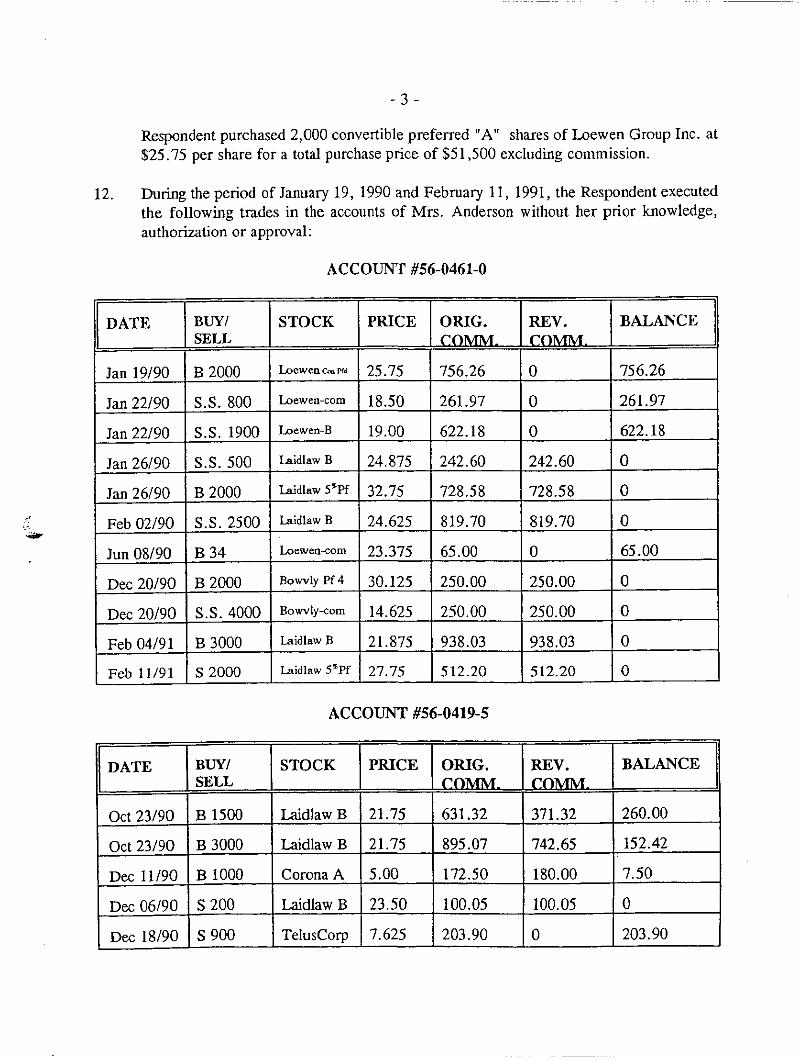

I 1. On or about January 8, 1990, Mrs. Anderson agreed to enter the stock market via a singlepurchase of Loewen Group Inc. shares and instructed the Respondent to limit her exposureto the sum of $2,000. On January 19, 1990, contrary to Mrs. Anderson's instructions, the

-3-

Respondent purchased 2,000 convertible preferred "A" shares of Loewen Group Inc. at$25.75 per share for a total purchase price of $51,500 excluding commission.

12. During the period of January 19, 1990 and February 1I, 1991, the Respondent executedthe following trades in the accounts of Mrs. Anderson without her prior knowledge,authorization or approval:

ACCOUNT #56-0461-0

DATE BUY/ STOCK PRICE ORIG. REV. BALANCESELL COMM. COMM,

Jan 19/90 B 2000 I,oewenc,,._, 25.75 756.26 0 756.26

Jan 22/90 S.S. 800 Loewen-com 18.50 261.97 0 261.97

Jan 22/90 S.S. 1900 Loewen-B 19.00 622.18 0 622.18

Jan 26/90 S.S. 500 LaidlawB 24.875 242.60 242.60 0

/an 26/90 B 2000 Laidlaw5_Pf 32.75 728.58 728.58 0

:)! Feb 02/90 S.S. 2500 LaidlawB 24.625 819.70 819.70 0

Jun 08/90 B 34 Loewen-com 23.375 65.00 0 65.00

Dec 20/90 B 2000 13owvlyPf4 30.125 250.00 250.00 0

Dec 20/90 S.S. 4000 Bowvly-com 14.625 250.00 250.00 0

Feb 04/91 B 3000 LaidlawB 21.875 938.03 938.03 0

Feb 11/91 S 2000 Laidlaw5rPf 27.75 512.20 512.20 0

ACCOUNT #56-0419-5

DATE BUY/ STOCK PRICE ORIG. REV. BALANCESELL COMM. COMM.

Oct 23/90 B 1500 Laidlaw B 21.75 631.32 371.32 260.00

Oct 23/90 B 3000 Laidlaw B 21.75 895.07 742.65 152.42

Dec 11/90 B 1000 Corona A 5.00 172.50 180.00 7.50

Dec 06/90 S 200 Laidlaw B 23.50 100.05 100.05 0

Dec 18/90 S 900 TelusCorp 7.625 203.90 0 203.90

-4-

13. The transactions referenced in paragraph 12 above generated gross commissions to theRespondent in the sum of $2,314.23 (original commission $7,449.36 - reversedcommission $5,135.13).

14. During the period of January 19, 1990 and February 11, 1991, the Respondent effectednumerous transactions in Mrs. Anderson's accounts which were unsuitable and contraryto the investment objectives and personal information referenced in the new clientdocumentation for her accounts.

15. On November 13, 1989, the Respondent opened an account for Gordon and Nonna Lacey

(account no. 56-0453-9). The NCAF for this account was not completed and excludedinformation regarding the clients' investment objectives, net worth, and investment

knowledge.

16. During the period of May 3, 1991 and February 17, 1993, the Respondent executed thefollowing trades in the account of Mr. and Mrs. Lacey without their prior knowledge,authorization, or approval:

ACCOUNT #56-0543-9

L

_ DATE BUY/ STOCK PRICE COMMISSIONs ,r,t,

May 03/91 B 700 Laidlaw CI B 14.25 272.36

May 17/91 B 400 TD Bank 2.25 Pfd 25.325 211.74

Jul 12/91 B 400 Bank of Montreal 35.50 254.14

Sep 06/91 B 200 Royal Bank 7.625% 25.00 187.50

NOV07/91 S 400 Bank of Montreal 38.75 267.89

Jan 16/92 B 1000 Rogers Com. Unit 15.10 453.00

Jan 24/92 S 200 Royal Bank 7.625% 28.00 110.39

Feb 04/92 B 1000 Provigo Inc. Rpts. 25.00 1093.75

Feb 28/92 B 4000 Veto Resource Ltd 0.81 121.64

May 14/92 B 4000 Santa Fe Engy Grp 0.90 134.60

May 15/92 S 4000 Santa Fe Engy Grp 1.16 172.04

May 26/92 B 3000 Santa Fe Engy Grp 1.48 160.13

May 26/92 B 1000 Santa Fe Engy Grp 14.00 53.38

-5-

Jul 21/92 S 1000 Rogers Com. CI B 14.00 375.54

Jul 23/92 S 4000 European Tech Intl 2.16 302.93

Jul 30/92 B 1500 Nova Scotia Pwr 10.00 290.62

Aug 05/92 B 7000 Trio Gold Corp. 0,87 220.31

Aug 14/92 S 1500 Nova Scotia Pwr 10.75 449.08

Sept 09/92 B 1000 Bombardier CI B 14.125 378.22

Sept 11/92 B 3000 European Tech Intl 2.10 227.12

Sept 25/92 B 9000 Veto Resource Ltd 0.57 192.12

Oct 02/92 B 5000 Noranda Inst Rpts. 50.00 375.00

Jan 15/93 B 600 Cdn Pacific Ltd. 16.75 256.30

Jan 15/93 S 3000 European Tech Intl 2.15 231.98

Jan 15/93 S 500 Petro Canada 7.87 129.50

Jan 22/93 S 200 Univa Pfd Ser 1 28.25 108.80

"_ Jan 26/93 B 800 CIBC Ser 13 Pfd 25.00 750.00

Feb 09/93 S 800 Univa Pfd Ser 1 23.25 311.87

Feb 17/93 S 5000 Noranda Inst l_pts. 58.10 127.12

Feb 17/93 B 200 Royal Bank 7"l° Pfd 25.00 187.50

17. The transactions referenced in paragraph 16 above generated gross commissions to theRespondent in the sum of $8,406.57.

18. The transactions referenced in paragraph 14 hereof were unsuitable for Mr. and Mrs.Lacey.

19. In or around May, 1993, the Respondent gave Mr. Lacey investment advice in relation tothe shares of Brookfield Capital Corp. without being properly registered to do so.

20. On or about January 22, 1991, the Respondent opened a commodities trading account forRalph and Mary I-tilgartner (account no. 56-0521-0). Mr. and Mrs. Hilgartner specifiedthat they wished only to conduct commodities trading in barley, canola, wheat and oatsand a Commodities Hedging Agreement was signed specifying those particularcommodities.

-6-

21. During the period of October 24, 1991 to January 29, 1992 the Respondent executed thefollowing commodities trades in the account of Mr. and Mrs. Hilgartner without theirprior knowledge, authorization or approval:

ACCOUNT #56-0521-0

DATE BUY/ SECURITY PRICE COMMISSIONS_t,t,

oct 24/91 S 1 Dec 91 Unleaded Gas 63.65

Nov 19/91 B 1 Dec 91 Unleaded Gas 63.00 65.00

Nov 19/91 S 1 Dec 91 HeatOil 2 64.90

Oct 24/91 B 1 Dec 91 I-IeatOil 2 69.15 65.00

Nov 22/91 S 1 Jan 92 Unleaded Gas 60.00

Nov 19/91 I] 1 Jan 92 Unleaded Gas 61.35 65.00

Nov 19/91 S 1 Jan 92 HeatOil 2 65.85

Nov 22/91 B 1 Jan 92 Heat0il 2 63.35 65.00

Nov 13/91 S 1 Feb 92 Unleaded Gas 61.75

Jan 03/92 B 1 Feb 92 Unleaded Gas 56.30 90.00

Jan 08/92 S 1 Feb 92 HeatOil 2 49.50

Nov 13/91 B 1 Feb 92 I-IeatOil 2 66.45 90.00

Dec 20/91 S 1 Apr 92 HeatOil 2 52.65

Jan 09/92 B 1 Apr 92 HeatOil 2 51.20 90.00

Jan 09/92 S 1 Jul 92 Unleaded Gas 56.80

Jan 13/92 S 1 Jul 92 Unleaded Gas 59.30

Jan 16/92 B 2 Jul 92 Unleaded Gas 60.20 180.00

Jan 29/92 S 2 Apr 92 Unleaded Gas 59.70

Dec 20/91 B 1 Apr 92 Unleaded Gas 59.00

Jan 13/92 B 1 Apr 92 Unleaded Gas 59.60 155.00

r Jan 16/92 S 2 May 92 Unleaded Gas 60.60

Jan 29/92 B 2 May 92 Unleaded Gas 60.50 180.00

-7-

22. The transactions referenced in paragraph 21 above generated gross commissions to the

Respondent in the sum of $1,045.00.

23. The trades referenced in paragraph 18 hereof were not in keeping with the instructions ofMr. and Mrs. Hilgartner for trading in specified grains as evidenced by the NCAF andCommodities Trading Agreement for the account.

24. On or about April 30, 1989, the Respondent became the Registered Representativeresponsible for the account of William Evans. The Respondent completed a NCAF for theaccount, listing investment objectives of 25 % security, 25 % income, 25 % growth, and25% risk. Instructions on the account were given at all material times by Anne Evans, thewife of William Evans, as Mr. Evans suffers from Alzheimer's Disease.

25. The Respondent failed to obtain written authorization permitting Mrs. Evans to giveinstructions for the account of Mr. Evans.

26. During the period of October 16, 1990 and March 19, 1993, the Respondent executed thefollowing trades in the account of Mr. Evans without the prior knowledge, authorizationor approval of either William or Anne Evans.

!_ ACCOUNT #56-7520-L

DATE BUY/ STOCK PRICE COMMISSION$1_',1,1,

Oct 16/90 B 400 TD Bank 15.875 161.51

Oct 24/90 13600 Corona Corp 5.50 110.40

Dec 13/90 S 900 Telus Corp 7.625 203.90

Jan 18191 13500 Bank Nova Scotia 12.25 178.73

Feb 12/91 S 400 TD Bank 19.00 185.79

Feb 26/91 S 500 Bank Nova Scotia 15.00 208.00

Mar 05/91 B 500 Laidlaw CI B 19.25 229.17

Mar 06191 B 300 Bombardier Cl B 16.625 136.85

May 29191 S 300 Bombardier C1B 20.50 148.07

July 03/91 B 250 Petro Canada 13.00 162.50

Dec 14/91 S 650 Telus Corp 5.75 133.701

Mar 19/93 S 800 Inprv Pipe 14.875 319.25

Mar 19/93 B 8000 Trio Gold Corp 0.84 236.84

-8-

' 27. The transactions referenced in paragraph 26 above generated gross commissions to theRespondent in the sum of $2,414.71.

28. Mrs. Evans contacted the Respondent regarding the trades referenced in paragraph 26hereof on numerous occasions, both by telephone and in person, and requested theRespondent to cease trading in her account. Notwithstanding such requests, theRespondent continued to conduct transactions in the account of Mr. Evans without theprior knowledge, authorization or approval of the clients.

29. The transactions referenced in paragraph 26 hereof were not in keeping with the statedinvestment objectives for the account of Mr. Evans and were therefore unsuitable.

30. On or about March 30, 1992, the Respondent opened a self directed RRSP account forRandy Riffenstein (account no. 56-7538-3) and transferred the account from the AlbertaTreasury Branch to Richardson. The Respondent completed a NCAF for the accountindicating investment objectives of 25 % security, 25 % income, 25% growth and 25 % risk.The Respondent completed the investment objectives on the NCAF without consulting Mr.Riffenstein.

31. On or about April 15, 1993, the Respondent purchased 2,500 shares of Veto Resourceswithout the prior knowledge, authorization or approval of Mr. Riffenstein.

32. On or about October 3, 1991, the Respondent opened a commodities trading account forMcMuUen Farms Ltd. (account no. 56-0543-0) following discussions with Floyd and RuthMcMullen. The Respondent completed a NCAF for the account indicating investmentobjectives of 99 % risk and a Commodity Account Supplement indicating investmentobjectives of 100% risk.

33. On or about October 30, 1991 the Respondent became the Approved Person responsiblefor a Joint Cash US/Canadian account for Floyd and/or Ruth McMuUen (account no. 56-0528-5). The Respondent completed a NCAF for the account indicating investmentobjectives of 50% risk and 50% growth.

34. On or about November 8, 1991, Mr. and Mrs. McMullen transferred the sum of $150,000into their cash account (account no. 56-0528-5) at Richardson with instructions to theRespondent to invest such funds into low risk treasury bills or money market securities.

35. During the period of November 8, 1991 to January 31, 1992 a number of purchases oftreasury bills and a purchase of 650 shares of Telus Corp. were made by the Respondentfor the accounts of MeMullen Farms Ltd. and Mr. and Mrs. McMuUen (hereinafter calledthe "McMullen Accounts") in accordance with the clients' instructions. Shortly thereafter,

the Respondent executed the following transactions without the prior knowledge,authorization or approval of Mr. and Mrs. McMuUen:

-9-

ACCOUNT #56-0543-0

DATE BUY/ STOCK PRICE COMM/SSIONSSELL

Feb 06/92 B 2000 Rogers Communications Units 15.00 450.00

Mar 13/92 B 5000 Veto Resources Ltd. 0.80 149.00

July 2/92 B 2500 Veto Resources Ltd. 0.61 60.00

July 28/92 S 2000 Rogers Communications Class B 18.00 710.00

Sept 03/92 B 3000 Trio Gold 0.83 94.00

Sept 11/92 B 5000 European Tech International 2.02 350.00

Sept 16/92 B 2000 Bombardier Class B 14.125 714.00

Oct 15/92 B 5000 Trio Gold 0.80 149.00

Oct 15/92 B 500 Veto Resources Ltd. 0.58 103.00

Oct 15/92 B 9500 Veto Resources Ltd. 0.59 103.00

_:_ Jan 22/93 S 5000 European Tech International 2.30 395.00

Feb 16/93 S 1000 Rogers Communications Wts 2.35 90.00

ACCOUNT #56-0528-5

DATE BUY/ STOCK PRICE COMMISSIONSSELL

Nov 05/91 B 1500 CIBC Ser 11 8.85 Pfd 25.00 562.50

Dec 10/91 B 1000 National Bank 8% Pfd 25.00 562.50

Jan 31/92 S 1500 CIBC Ser 11 8.85 Pfd 27.00 728.00

Jan 31/92 B 4500 Veto Resources Ltd 0.81 136.00

Feb 04/92 S 1000 National Bank 8% Pfd 24.875 490.00

Feb 25/92 B 1000 Provigo Inc. Receipts 25.00 562.50

Jun 02/92 B 7000 Santa Fe Energy Group 1.45 351.00

Jul 30/92 S 7000 European Tech. International 2.10 400.72

- 10-

Aug 06/92 B 4000 Trio Gold Corp. 0.89 325.00

Aug 12/92 B 6000 Trio Gold Corp. 0.87 325.00

Oct 19/92 B 4000 Noranda Instalment Receipts 50.00 300.00

Nov 26/92 B 2000 Discovery West Corp. 4.95 343.00

Jan 21/93 S 696 Cdn 88 Energy CI A 1.20 60.00

Feb 01/93 S 2000 Discovery West Corp. 5.875 384.00

Feb 01/93 S 800 Univa 1st Pfd Ser 1 23.00 380.00

Feb 01/93 S 200 Univa 1st Pfd Ser 1 23.25 95.00

Feb 02/93 S 4000 Noranda Instalment Receipts 51.44 850.00

i Feb 08/93 S 1500 Trio Gold Corp. 0.80 411.80

U.S. ACCOUNT

DATE BUY/ STOCK PRICE COMMISSIONS_-._ SELL

Feb 04/92 B 1000 Bank of Montreal 6.75 (US) 25.00 562.50

Oct 08/92 S 1000 Bank of Montreal 6.75 (US) 25.625 446.00

Feb 08/93 S 200 IBM 52.25 192.00

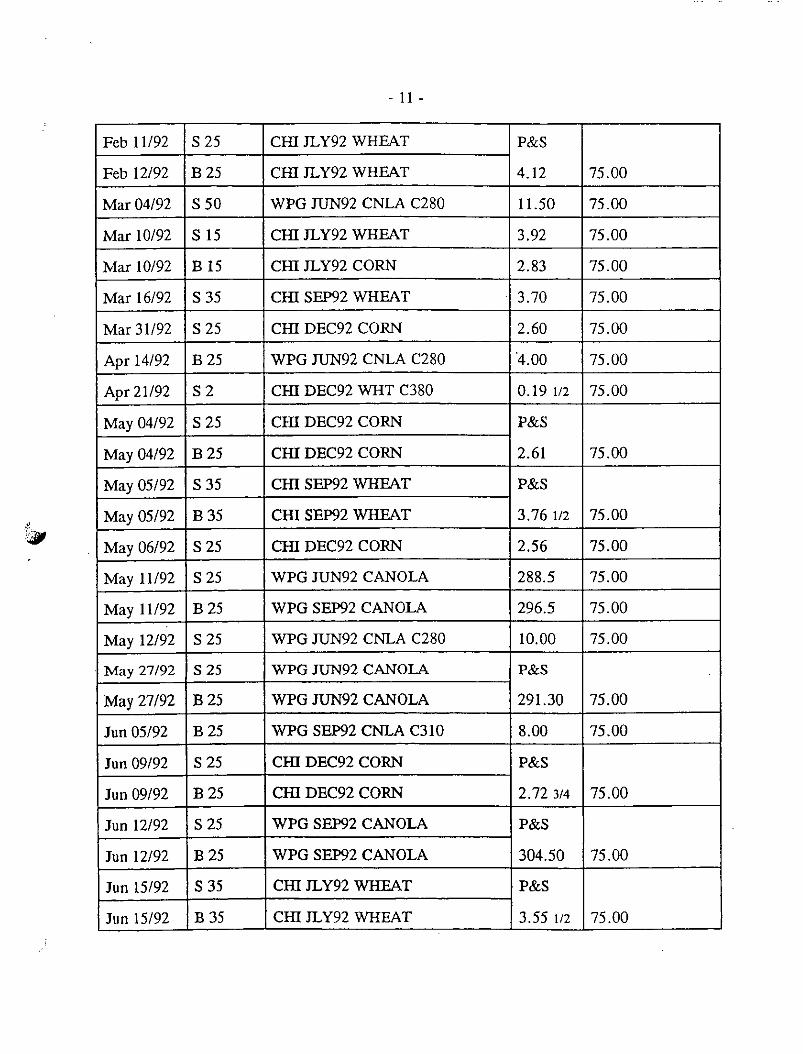

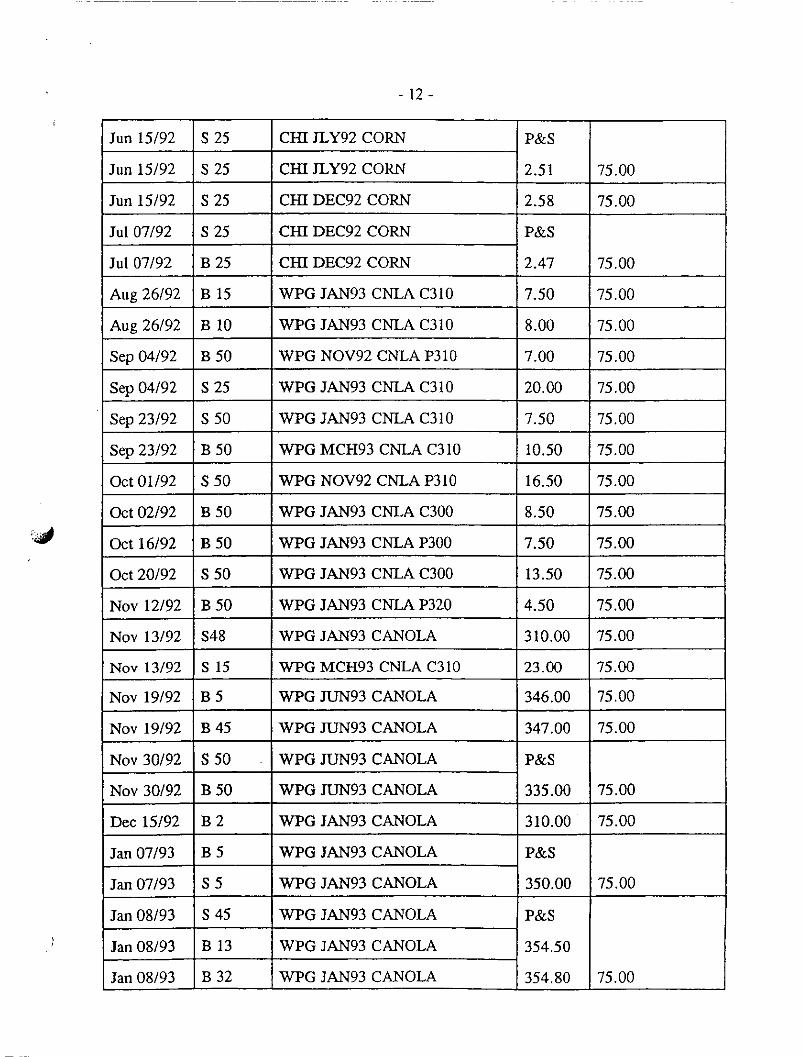

ACCOUNT #56-0543-0

DATE BUY/ COMMODITY PRICE COMMISSIONSSELL

Jan 24/92 B 15 WPG SF]x)2 CNLA C300 6.00 75.00

Jan 20/92 : B 10 CI-II JLY92 CORN 2.72 75.00

Jan 22/92 _B 15 CI-H JLY92 WHEAT 3.80 75.00

Feb 07/92 B 10 CI-II JLY92 WHEAT 4.10 75.00

Feb 10/92 B 10 CI--IIJLY92 WHEAT 4.20 75.00

Feb 11/92 B 10 CHI JLY92 WHEAT 4.04 1/2 75.00

-11-

Feb 11/92 S 25 CHI JLY92 WHEAT P&S

Feb 12/92 B 25 CHI JLY92 WHEAT 4.12 75.00

Mar 04/92 S 50 WPG JUN92 CNLA C280 I 1.50 75.00

Mar 10/92 S 15 CHI JLY92 WHEAT 3.92 75.00

Mar 10/92 B 15 CHI JLY92 CORN 2.83 75.00

Mar 16/92 S 35 CHI SEP92 WHEAT 3.70 75.00

Mar 31/92 S 25 CHI DEC92 CORN 2.60 75.00

Apr 14/92 B 25 WPG JUN92 CNLA C280 '4.00 75.00

Apr 21/92 S 2 CHI DEC92 WIlT C380 0.19 1/2 75.00

May 04/92 S 25 CHI DEC92 CORN P&S

May 04/92 B 25 CHI DEC92 CORN 2.61 75.00

May 05/92 S 35 CHI SEP92 WHEAT P&S

May 05/92 B 35 CHI SEtO2 WHEAT 3.76 1/2 75.00

May 06/92 S 25 CHI DEC92 CORN 2.56 75.00

May 11/92 S 25 WPG JUN92 CANOLA 288.5 75.00

May 11/92 B 25 WPG SEI_2 CANOLA 296.5 75.00

May 12/92 S 25 WPG JUN92 CNLA C280 10.00 75.00

May 27/92 S 25 W'PG JUN92 CANOLA P&S

May 27/92 B 25 WPG JUN92 CANOLA 291.30 75.00

Jun 05/92 B 25 WPG SEtO2 CNLA C310 8.00 75.00

Jun 09/92 S 25 CI-I/DEC92 CORN P&S

Jun 09/92 B 25 CI-II DEC92 CORN 2.72 3/4 75.00

Jun 12/92 i S 25 WPG SEtO2 CANOLA P&S

Jun 12/92 1325 WPG SEtO2 CANOLA 304.50 75.00

Jun 15/92 S 35 CI-_ JLY92 WHEAT P&S

Jun 15/92 B 35 CHI JLY92 WHEAT 3.55 1/2 75.00

-12-

Jun 15/92 S 25 CHI JL¥92 CORN P&S

Jun 15/92 S 25 CHI JLY92 CORN 2.51 75.00

Jun 15/92 S 25 CHI DEC92 CORN 2.58 75.00

Jul 07/92 S 25 CHI DEC92 CORN P&S

Jul 07/92 B 25 CHI DEC92 CORN 2.47 75.00

Aug 26/92 B 15 WPG JAN93 CNLA C310 7.50 75.00

Aug 26/92 B 10 WPG JAN93 CNLA C310 8.00 75.00

Sep 04/92 B 50 WPG NOV92 CNLA P310 7.00 75.00

Sep 04/92 S 25 WPG JAN93 CNLA C310 20.00 75.00

Sep 23/92 S 50 WPG JAN93 CNLA C310 7.50 75.00

Sep 23/92 B 50 WPG MCH93 CNLA C310 10.50 75.00

Oct 01/92 S 50 WPG NOV92 CNLA P310 16.50 75.00

Oct 02/92 B 50 WPG JAN93 CNLA C300 8.50 75.00

_-_ Oct 16/92 B 50 WPG JAN93 CNLA P300 7.50 75.00

Oct 20/92 S 50 WPG JAN93 CNLA C300 13.50 75.00

Nov 12/92 B 50 WPG JAN93 CNLA P320 4.50 75.00

Nov 13/92 $48 WPG JAN93 CANOLA 310.00 75.00

Nov 13/92 S 15 WPG MCH93 CNLA C310 23.00 75.00

Nov 19/92 B 5 WPG JUN93 CANOLA 346.00 75.00

Nov 19/92 B 45 WPG JUN93 CANOLA 347.00 75.00

Nov 30/92 S 50 WPG JIYN93 CANOLA P&S

Nov 30/92 B 50 WPG JUN93 CANOLA 335.00 75.00

Dec 15/92 B 2 WPG JAN93 CANOLA 310.00 75.00

Jan 07/93 B 5 WPG JAN93 CANOLA P&S

Jan 07/93 S 5 WPG JAN93 CANOLA 350.00 75.00

Jan 08/93 S 45 WPG JAN93 CANOLA P&S

i Jan 08/93 B 13 WPG JAN93 CANOLA 354.50

Jan 08/93 B 32 WPG JAN93 CANOLA 354.80 75.00

-13-

Feb 05/93 S 35 WPG MCH93 CANOLA 328.80

Feb 05/93 S 15 WPG MCH93 CANOLA 328.80

Feb 05/93 S 20 WPG MCH93 CANOLA 328.80 75.00

36. The transactions referenced in paragraph 35 above generated gross commissions to theRespondent in the sum of $15,434.52

37. During the period of November 5, 1991 to February 16, 1993 the Respondent effectednumerous transactions in the McMullen Accounts which were unsuitable.

38. Mr. and Mrs. McMullen attempted to contact the Respondent by telephone on numerousoccasions to object to the unauthorized transactions referenced in paragraph 35 hereof.Numerous meetings were also held with the Respondent regarding the said transactions,following which the Respondent continued to conduct transactions in the McMullenAccounts without the prior knowledge, authorization or approval of the clients.

39. In or around November, 1992, Mr. and Mrs. McMullen contacted the Respondent toinstruct him that no further trades were to be conducted in the McMuUen Accounts.

_ Notwithstanding such instructions, the Respondent continued to conduct unauthorizedtransactions in the McMullen Accounts during the months of December, 1992, January and

February, 1993.

40. In or around March, 1991 the Respondent met with Mr. William Brown and Mr. DonMilligan of Richardson in relation to the complaint of Vicki Anderson. At that time, theRespondent was advised that he is required to obtain the prior permission from clients withrespect to each and every trade conducted.

41. The Exchange submits that the foregoing conduct constitutes violations of sections16.01(1), 16.07(1) and 21.14(1) of the By-law, and section 54(1) of the Alberta SecuritiesAct, which state in part:

Section 16.01 - Supervision of Accounts

(1) Every member shaU use due diligence:

(a) to learn the essential facts relative to every customer and every order oraccount accepted;

(b) to ensure that the acceptance of any order for any account is within thebounds of good business practice; and

l

- 14-

(c) to ensure that recommendations made for any account are appropriate forthe client and in keeping with his investment objectives.

Section 16.07 - Discretionary and Managed Accounts

(1) Discretionary Accounts - No registered representative or other employee (otherthan a director or partner) of a member shall be permitted to accept authorizationfor a discretionary account from a customer of a member. No member shallexercise any discretionary power with respect to a client's account unless suchclient has given prior written authorization and the account has been accepted inwriting by the partner or director designated pursuant to section 16.01. Everydiscretionary order must be identified as discretionary at the time of entry.

Section 21.14 - Powers and Remedies

(1) Where a person under the jurisdiction of the Exchange has:

(a) contravened any Exchange Requirement; or

(b) engaged in conduct, business or affairs that is unbecoming, inconsistentwith just and equitable principles of trade or detrimental to the interestsof the Exchange or the public; or

(c) is not in compliance with any Exchange requirement,

the Board or a committee of the Board may impose any one or more of thepenalties or remedies described in subsection (2) against the person.

Section 54 - Registration

(1) No person or company shall

(a) trade in a security unless the person or company is registered with theChief of Securities Administration as

(i) a dealer,

(ii) a salesman, or

(iii) a partner or officer of a registered dealer that acts on behalf ofthe dealer,

J

- 15-

(b) act as an underwriter unless the person or company is registered with theChief of Securities Administration as an underwriter, or

(c) act as an adviser unless the person or company is registered with theChief of Securities Administration as

(i) an adviser, or

(ii) a partner or officer of a registered adviser that acts on behalf ofthe adviser.

AND FURTHER TAKE NOTICE that the hearing will be held in accordance with theprovisions of Part XXI of the By-law.

AND FURTHER TAKE NOTICE that the Respondent is entitled to be present at thehearing and to be represented by counsel or an agent, to call and examine witnesses, to presentarguments and submissions, and to conduct cross-examinations of witnesses at the heatingreasonably required for a full and fair disclosure of the facts in relation to which such witnesses

_J have given evidence.

AND FURTttT, R TAKE NOTICE that the Respondent has ten (10) days from the dateof service of this Notice of Hearing and Particulars to serve upon the Exchange a Reply signedby the Respondent or an individual authorized by the Respondent that specifically denies, with asummary of the supporting facts and arguments, any and all of the allegations of fact andconclusions drawn therefrom as contained in the Notice of Hearing and Particulars.

AND FURTHER TAKE NOTICE that the panel of the Hearing Committee of theExchange as convened may accept as having been proven any facts alleged or conclusions drawntherefrom by the Exchange in the Notice of Hearing and Particulars which are not specificallydenied, with a summary of supporting facts and arguments in the Reply.

AND FURTNER TAKE NOTICE that if the Respondent does not serve a Reply or attendat the hearing as aforesaid, the panel of the Hearing Committee of the Exchange may proceed witha hearing in this matter at the time and place specified in the Notice of Hearing and Particularswithout further notice to the Respondent and in his absence may accept the facts as alleged or theconclusions drawn by the Exchange in the Notice of Hearing and Particulars as having beenproven by the Exchange and may impose penalties pursuant to the By-law in relation thereto.

-16-

AND FURTItlgR TAKE NOTICE that the Exchange will seek all costs of and incidental

to the hearing in this matter against the Respondent.

DATED at the City of Calgary, ) THE AI3_ERTA STOCK EXCHANGE

in the Province of Alberta, )) Per:

this _r_U, day of February, 1994. ) Patricia M. Johnston) Legal Counsel & Exchange Secretary

• 1 ORIGINALL

IN THE MATTER OF

THE ALBERTA STOCK EXCHANGE ACT, S.A. 1994, C.79

AND IN THE MATTER oF

THE GENERAL BY-LAW OF THE ALBERTA STOCK EXCHANGE

AND IN THE MATTER OFBRIAN MICHAEL MEYER

PROCEEDINGS AT APPEAL HEARING

March 30th A.D. 1995

Calgary, Alberta

BOARD:

J. Burns, Esq., ChairmanMs. J. McLaws, Panel MemberMr. J. Wells, Panel Member

Mr. T. Cummings, Panel Member

Ms. L. Smyth Alberta Stock Exchange

............................................................

APPEARANCES:

J. Browne, Ms., For the Alberta Stock Exchange

Doug B. Todd, Esq. For Brian Michael Meyer.

***AMICUS REPORTING GROUP***

MR. CHAIRMAN: We would like to give you the

verbal finding of the panel.

We concur with the finding of the Hearing

Panel, but we have determined after a review of all factors,

that the penalty should be suspension of two years, which

have been served; rewrite all three exams; supervision, one

year of strict, one year of close; the fine $20,000, costs

of $5,000 for an aggregate of $25,000.

That's our finding.

MR. WELLS: So, you'll be sending that out

to all of us in written form?

MR. CHAIRMAN: I'll do a one-liner and get

you --

...... MS. BROWNE: The mechanics, we'll get it

and circulate it to you.

MR. CHAIRMAN: We, as a panel, would like to

thank counsel for both sides and all participants. Thank

you.

............................................................

PROCEEDINGS ADJOURNED

............................................................

***AMICUS REPORTING GROUP***

Certificate of Transcript

I, the undersigned, hereby certify that the foregoing pages

_I to 3 are a true and faithful transcript of the proceedings

taken down by me in shorthand and transcribed from my

shorthand notes to the best of my skill and ability.

Dated at the City of Calgary, Province of Alberta, this 2nd

day of April, A.D. 1995.

/Shaayna Vance, Ms., CSR(A)

Court Reporter

/4 CAT - Printed April 2, 1995

SV

***AMICUS REPORTING GROUP***

D

The Alberta Stock Exchanee ActSA 1974 C-79

In the Matter of

The Alberta Stock Exchange

and

Brian Michael Meyer

PENALTY HI_ARING DECISION

The Hearing Committee of The Alberta Stock Exchange consisting of:

Edward R.R. Carruthers, Q.C., Chairman

J. Bruce Kennedy, Member

Kev'm P. Bannister, Member

Appearances: Patricia M. Iohnston for The Alberta Stock ExchangeDouglas B. Todd for Brian Michael Meyer

Heard: In Calgary on December 5, 1994

DECISION

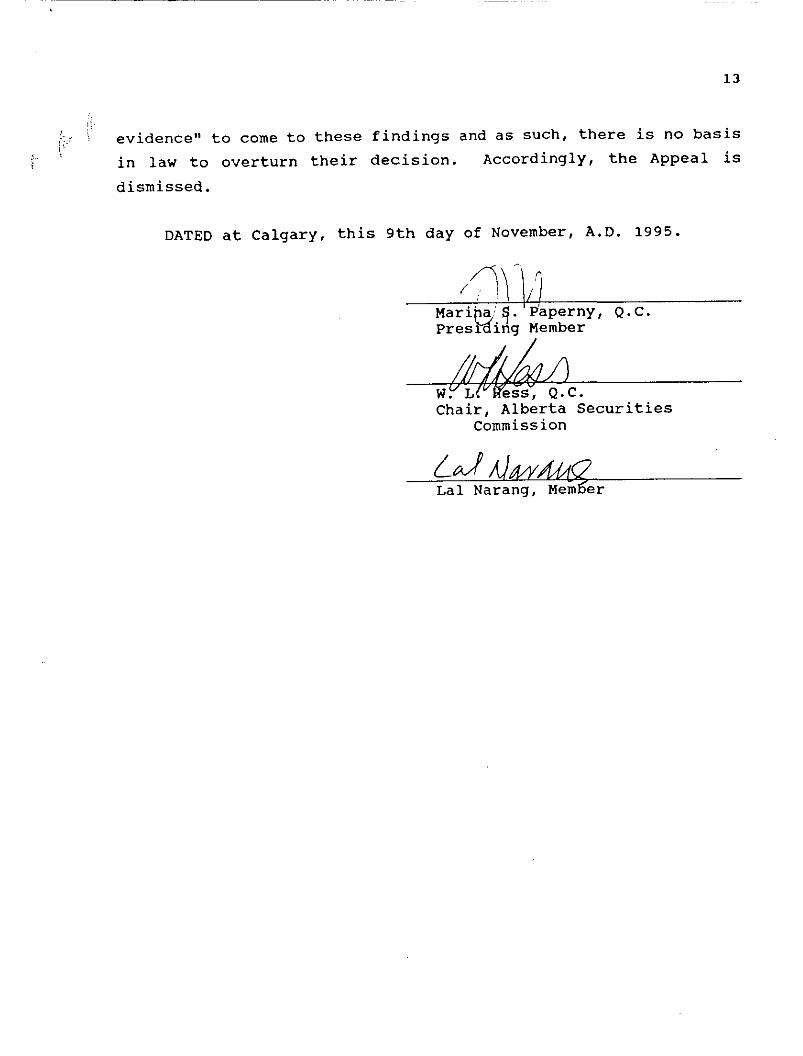

._ We have determined that we are going to give Mr. Meyer an opportunity to re-enter thebusiness, but not easily. We are troubled by the apparent lack of remorse or contritionevidenced by Mr. Meyer, and this has made our decision extremely difficult.

We are of the view that a registered representative has a fiduciary responsibility vis-a-vis hisclients and his firm, and that his conduct must be characterized by the highest regard for the

investment objectives of his client. It is our view that Mr. Meyer has exhibited asregard for the wishes of his clients and for their investment objectives, even afterd his responsibilities brought home to him at the time that the Vickie Anderson

complaint was dealt with internally by his firm. On the other hand, we are cognizant of the factthat there is not evidence of theft or fraud or manipulation of accounts and that the offencesconsist of discretionary or unauthorized transactions and unsuitable transactions.

If Mr. Meyer should choose to return to the business, he must rewrite all of the examinationswhich are required, being the Canadian Securities exam, the Conduct and Practices Handbookfor Securities Industry Professionals exam, and the options exam.

In addition, he must have a substantial period of close supervision in which his activities aresupervised following his re-entry.

Finally, we assess a fine which should be substantial in order to bring home to Mr. Meyer theseriousness with which this panel regards the obligations of a broker and his disregard of them,

. . the protection of the public, which is part of our mandate, and the importance to the industryand the public that the markets be seen to be fair and well regulated.

In the result, our decision is that Mr. Meyer shall stand suspended for three years from the dateof his termination; that he rewrite the three examinations, namely the Canadian Securities exam,the Conduct and Practices Handbook for Securities Industries Professionals exam, and the OptionExam; that following his re-entry into the business, he have a period of one year of strictsupervision followed by one year of close supervision; that he be assessed a fine of $30,000;and that he pay the costs of the investigation and hearing in an amount to be determined betweenthe Exchange and Mr. Todd on the basis of what the Exchange has indicated in the Exchange'ssubmission.

DATED at Calgary, Alberta and effective the 5th day of December, 1994.

./ Edward R.R. _;/arruthers, Q.C., Chairman

Kevin P. Bannister, Member

J. Bruce Kennedy, Member (__............/

[The Alberta Stock Exchange Act

SA 1974 C-79

In the Matter of

The Alberta Stock Exchange

and

Brian Michael Meyer

REASONS FOR DECISION

lBefore the Hearing Committee of The Alberta Stock Exchange consisting of:

Edward R.R. Carruthers, Q.C., Chairman

J. Bruce Kennedy, Member

Kevin P. Bannister, Member

Appearances: Patricia M. Johnston for The Alberta Stock ExchangeDouglas B. Todd for Brian Michael Meyer

IHeard: In Calgary on March 14, 15, 16 and 17th, 1994.

[

.......

BACKGROUND

_. By Notice of Hearing and Particulars (the "Notice") dated February 5, 1994, The Alberta Stock

Exchange (the "Exchange") convened a Hearing to consider whether Brian Michael Meyer

(hereafter referred to as "Mr. Meyer" or the "Respondent") had contravened sections 16.01,

-16.07 and 21.14(1)(b) of the By-law of the Exchange (the "By-Law") and section 54(1) of the

Alberta Securities Act, S.A. 1981 Chapter S-6.1 (the "Act").

The Notice alleged unsuitable trading, contrary to section 16.01 of the By-Law with respect to

accounts belonging to:

Vicky Anderson;

Gordon and Norma Lacey;

WilliamEvans;and" McMullen Farms Ltd. and Floyd and Ruth McMullen.

[The Notice also alleged that the Respondent traded in certain accounts without receiving the

prior authorization of the customer contrary to section 16.07 of the By-Law with respect to the

following persons:

Donald Barry Anderson;

Vicky Anderson;

Gordon and Norma Lacey;

Ralph and Mary Hilgartner;

William Evans;

i RandyReiffenstein;and

McMullen Farms Ltd. and Floyd and Ruth McMullen.

I:

1" 2 "

Mr. Meyer presents as a bright, intelligent person. He was born in 1949 and farmed in the

Hanna district from 1970 to 1988. In November of 1988 he joined Richardson Greenshields of

Canada Limited ("Richardson Greenshields") in Red Deer as a trainee. He completed the

Canadian Securities Course and became registered in April, 1989. He quickly distinguishedr

himself as a personable and productive salesperson and earned compliments for his production.

He became an integral member of the Red Deer office of Richardson Greenshields and appearedto be well liked. The Richardson Greenshields office was comprised of five or six salesmen in

1990 but salespeople left and their accounts were divided amongst the remaining brokers such

that Mr. Meyer got progressively more accounts and busier both as a result of his own accounts

and through acquisition of accounts of departing salesmen.

The resident manager of the office, Mr. John Scow, left Richardson Greenshields in March of

1991 and a new manager was not appointed until August of 1992. During this time the level

of supervision in the Red Deer office of Richardson Greenshields was significantly diminished

in that the supervisor was visiting the office on a weeny basis from Calgary.

[Mr. Meyer was the subject of a complaint in April 1991 with respect to the Vicky Anderson

l account which was ultimately dealt with by the firm in the Fall of 1991. He was reprimanded

at that time.

A new manager, David Noble, was appointed to the Red Deer office in August of 1992. He

immediately became aware of complaints in the handling of certain accounts by Mr. Meyer and

received further complaints as a result of investigations which he then undertook. Mr. Meyer

was terminated by Richardson Greenshields in March of 1993 and a uniform termination notice

was filed. As a result of the contents of that notice, the Exchange commenced an investigation

relative to the conduct of Mr. Meyer during the period noted in the termination notice which

i resulted in the issuance of the Notice.

I The complaints involved seven different customers of Mr. Meyer and a number of accounts.

We propose to deal with each charge and each witness separately but prior to dealing with that

should comment on the standard of proof that we will apply to the evidence.

- 3 -

Counsel for Mr: Meyer brought to our attention the decision of the Hearing Committee of the

Exchange in the case of Deborah Ann Windle. We have adopted the evidentiary standard

articulated in Windle in these proceedings and we quote from the reasons for the decision of that

panel:

"It is also useful to comment at the outset on the burden of proof that we appliedto the evidence in making our findings. This was not a criminal proceeding, and

therefore we were not held to the criminal standard of 'proof beyond a reasonable

doubt'. Counsel for both parties acknowledged, however that in light of the

seriousness of the charges and the adverse impact that they might have on Mrs.

Windle's ability to earn a livelihood in the securities industry, something more

than the civil standard of 'proof on the balance of probabilities' was required.

Some legal decisions were cited to us in support of the contention that the

standard of proof that we should apply was 'clear and convincing proof based on

cogent evidence.' As both counsel were in agreement on this point, this is the

_ standardthat we applied.

E Counsel for Mr. Meyer also made the following observation:

"I must confess that I looked around to see what I could find that was binding on

you, and there is precious little. There is really nothing that is binding on this

type of a hearing, except, perhaps to do justice in this case."

This is a statement with which we agree. The panel is constituted under the By-Law with two

persons knowledgable in the industry and an independent Chairman. The panel is not obliged

to follow the strict rules of evidence and is entitled to utilize its knowledge of the industry in

I attempting to do justice and to ensure that persons who carry on securities or related activitiesunder the jurisdiction of the Exchange discharge their obligations to their customers and do not

breach the By-Law.

As indicated, the charges against Mr. Meyer fall under two categories, unsuitable trades and

discretionary trades.

I

• The By-law prOvisions related to suitability are contained in sub-section I of section 16.01 of

the By-Law which provides as follows:

(1) Every member shall use due diligence:F

(a) to learn the essential facts relative to every customer and every order oraccount accepted;

(b) to ensure that the acceptance of any order for any account is within the

bounds of good business practice; and

(c) to ensure that recommendations made for any account are appropriate for

the client and in keeping with his investment objectives.

In short, this section requires that the person taking the order from a customer must ensure that

[ the order is within the stated client objectives as contained in the new account application form

and, in any event, is suitable to the customer given the customer's net worth, investment

experience, ability to withstand risk and trading history.

The other allegations relate to discretionary trading. The requirements are contained within

section 16.07(1) of the By-Law which states as follows:

"Discretionary Accounts - No registered representative or other employee (other

than a director or partner) of a member shall be permitted to accept authorization

for a discretionary account from a customer of a member. No member shall

exercise any discretionary power with respect to a client's account unless such

client has given prior written authorization and the account has been accepted inwriting by the partner or director designated pursuant to section 16.01. Every

[. discretionary order must be identified as discretionary at the time of entry."

In short, this section requires that each order must be approved by the customer prior to entry

of the order and that only certain designated persons may accept authorization from a customer

1-- 5 -

to trade in a customer's account without that prior approval. There is no issue here that Mr.

Meyer was not capable of accepting those instructions and had not received that approval.

The Exchange called witnesses in addition to the customers and Mr. Meyer called witnesses in

his defense. Before dealing with the evidence of the customers we will deal with the evidence

of the non-customer witnesses.

DAYED NOBLE

Mr. Noble became manager of the Red Deer Branch on August 1, 1992. This was his first

management position. He was given a very clear mandate from head office when he assumed

the position to clean up the margin situation and the compliance problems which had previously

existed at that Branch. These margin problems were not necessarily isolated to Mr. Meyer

although Mr. Noble was of the understanding as he undertook his responsibilities that Mr.

Meyer's accounts were where the primary margin problem existed.

[He met immediate resistance from Mr. Meyer in that there appeared to him to be some

resentment on the part of Mr. Meyer that, in Mr. Noble's words, "this young buck comes in

from Edmonton and not only does he come in and it's his first management position he was

carrying a big stick in terms of not allowing any kind of margin problems to continue". Mr.

Noble noted that the personnel in the office appeared to get on well with each other. He

characterized the office as a "tight team". Mr. Noble was very strict as to what the margin had

to be and in his words "I don't think they were used to that kind of surveillance."

The Branch had not had a resident manager since the previous manager, Mr. Scory, had left at

the end of March, 1991. In the intervening period Mr. Meyer had assumed the day to day

management other than those matters which required a signature.

Upon taking office Mr. Noble received a number of complaints from Mr. Meyer's customers

which he reported to head office as he had been instructed to do. The investigation of these

complaints was undertaken by Mr. William Brown. Ultimately, Mr. Noble was instructed by

head office to advise Mr. Meyer of his termination.

- 6 -

LEONA MARSHALL AND SHERRY BOLANGER

Ms. Bolanger and Ms. Marshall were staff members in the office during the time Mr. Meyer

was employed and were called by Mr. Meyer. Each gave evidence which indicated that thet-Richardson Greenshields office in Red Deer was a very busy office having been reduced in size

[_ from six brokers to two with Mr. Meyer and one other broker trying to handle all the clients.After Mr. Scory left Mr. Meyer took on most of the day to day manager responsibilities with

Mr. Milligan or Mr. Stoll coming down from Calgary one day a week, usually for a couple of

hours to sign the applications and any other matters which needed a signature.

In addition to Ms. Bolanger and Ms. Marshall, Mr. Meyer called John Scory and Edward

Beckingsale.

Mr. Beckingsale gave evidence that he had been a customer of Mr. Meyer but that he had not

made a complaint. This corresponds with Mr. Noble's evidence that Mr. Beckingsale had

contacted him with respect to a trading loss but had not ever filed a letter. There are no

allegations with respect to Mr. Beckingsale's account in the Notice.

[JOHN SCORY

John Scory was the manager of the Richardson Greensbields office in Red Deer from November

i, 1986 until March 31, 1991. He had hired Brian Meyer. He gave evidence to the effect that

Mr. Meyer, having a farming background, was able to relate well with the rural clients and

quickly developed a substantial customer base amongst the farmers and ranchers of the area.

Mr. Scory characterized Mr. Meyer as an "eager beaver" in that he was in the office early and

left late. He was well liked by the other staff. He did not recall any complaints against Mr.

I Meyer while he was manager of the office.

Much of Mr. Scory's evidence related to technical aspects of hedge spreads and the relative risk

related thereto. Having previously determined that, in our view, hedge spreads are not

necessarily an unsuitable investment or an inappropriate strategy, much of Mr. Scory's evidence

was not relevant to the charges against Mr. Meyer.

[_ = 7 -

_. MR. W.M.R. BROWN

Mr. Brown was cailed by the Exchange. He is a director and counsel for Richardson

Greenshields, responsible for compliance. He discussed each of the customer complaints and[

the resolution of them by Richardson Greenshields. As indicated in the course of the hearing,

we are of the view that the actions taken by Richardson Greenshields in dealing with itscustomers have little bearing on whether or not the Exchange has made out its case as contained

in the Notice.

Mr. Brown did, however, make some observations which are worth noting in these Reasons.

Mr. Brown's first contact with Mr. Meyer came in 1991 as a result of the complaint made by

Mrs. Victoria Anderson. At that time there had been a meeting with Mrs. Anderson, Mr.

Meyer and Mr. Brown. Following resolution of that complaint Mr. Brown says he discussed

in depth with Mr. Meyer the basic concepts of suitability and the obligations of an RR to his

'. customer. Mr. Brown testified that he was frustrated at Meyer'sMr. attitude in that Mr. Meyer

did not appear to be listening and because of that attitude Mr. Brown advised Mr. Meyer that

his recommendation would be that Mr. Meyer be terminated. On this basis he was finallyable

to get through to Mr. Meyer as to the seriousness of the issues and Mr. Brown left the meeting

feeling that Mr. Meyer did understand what was suitable and what the obligations of an RR

were. There appears to have been an attempt, following the resolution of the Anderson

complaint, to supervise Mr. Meyer more carefully but there was still no supervisor in the Red

Deer office. This combined with changes in Richardson Greenshields sales management

structure appeared to result in the continuation of the lack of supervision in Red Deer.

Mr. Brown offered his view and impressions with respect to the customers from whom

complaints had been received. We have not had regard to these observations in these Reasonssince we had the opportunity to hear evidence from each of these persons ourselves. Therefore,

1[ we have not given Mr. Brown's comments great weight in these Reasons.

- 8 -

BRIAN MEYER

The final witness on behalf of Mr. Meyer was himself. Mr. Meyer gave evidence for almost

a full day and dealt with each of the customer accounts. Mr. Meyer stated emphatically that he[had his orders confirmed by each of the customers but as he continued to testify he spoke in

generalities, theorizing about actions "he would have taken" rather than stating positively thathe did take certain actions. Certain patterns emerged with Mr. Meyer which leads us to believe

that he had general discussions with clients about stocks and strategies and would keep a list of

clients who had indicated, in a general way, an interest in certain strategies, such as hedge

spreads and the purchase of new preferred share issues of banks. When the opportunity arose

he would simply execute the transactions without confirming with the clients that that is what

they wished to do. This behaviour seemed to get progressively more exaggerated through 1991.

A picture emerges of a young headstrong broker thrust into a situation after being registered ordy

two years where the office diminished in size and the "book" was split among the remaining

brokers, coupled with inadequate supervision. Mr. Meyer was essentialIy able to run things his

i own way from the time Mr. Story left until the time /Cir. Noble arrived. This appears to be

confirmed by the memo from Mr. Bill Lewis of July 11, 1991 wherein Mr. Lewis, in defense

of Mr. Meyer, states "Brian is a hardworking, strong-minded IA who in his particular branch

environment received very little coaching and counselling and compliance training." "He was

not properly supervised ...".

This, however, does not excuse any conduct of Mr. Meyer. He should have been well aware

of his obligations to his customers and had had those obligations specifically brought home to

him by Mr. Brown and Mr. Lewis in the Fall of 1991. The evidence of Mr. Brown is that this

was brought home very forcefully at the time that the Vicky Anderson complaint was dealt with.

Mr. Meyer appears to have continued, however, to flaunt the requirements as detailed in the

Notice.

We will now proceed to review the evidence of the customers in respect of whose accounts the

complaints were made.

F- 9 -

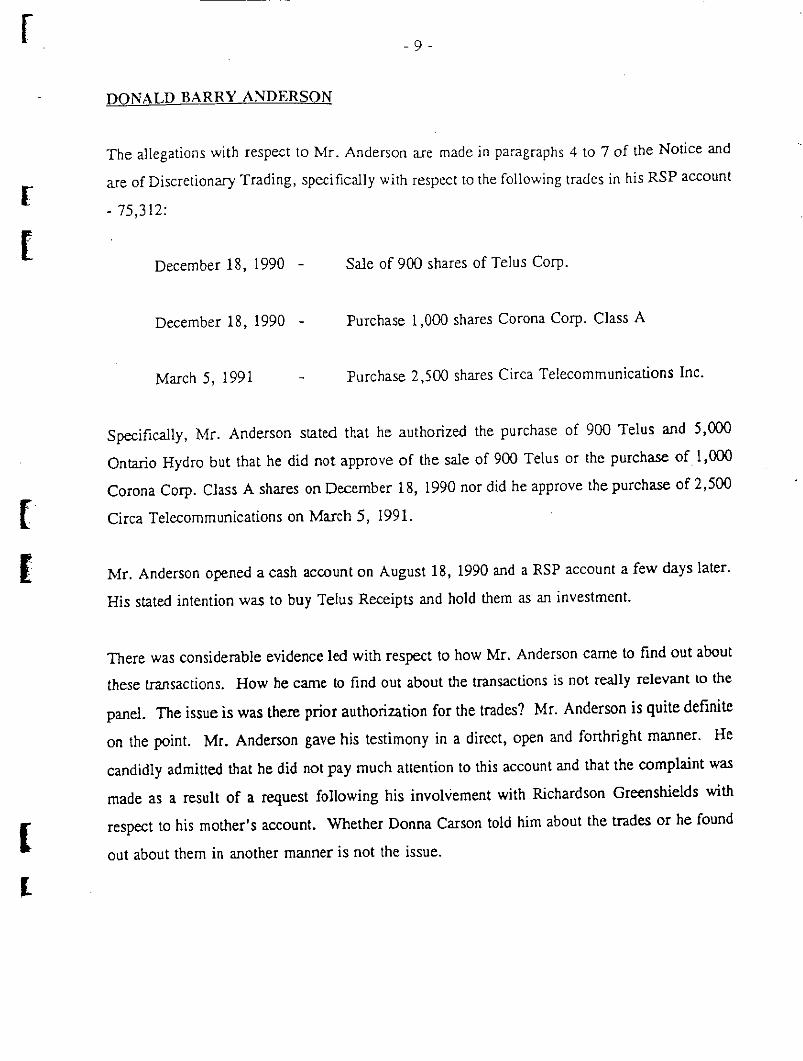

DONALD BARRY ANDERSON

The allegations with respect to Mr. Anderson are made in paragraphs 4 to 7 of the Notice and

1- are of Discretionary Trading, specifically with respect to the following trades in his RSP account- 75,312:

[December 18, 1990 Sale of 900 shares of Telus Corp.

December 18, 1990 Purchase 1,000 shares Corona Corp. Class A

March 5, 1991 Purchase 2,500 shares Circa Telecommunications Inc.

Specifically, Mr. Anderson stated that he authorized the purchase of 900 Telus and 5,000

Ontario Hydro but that he did not approve of the sale of 900 Telus or the purchase of 1,000

Corona Corp. Class A shares on December 18, 1990 nor did be approve the purchase of 2,500

Circa Telecommunications on March 5, 1991.

Mr. Anderson opened a cash account on August 18, 1990 and a RSP account a few days later.

His stated intention was to buy Telus Receipts and hold them as an investment.

There was considerable evidence led with respect to how Mr. Anderson came to fred out about

these transactions. How he came to find out about the transactions is not really relevant to the

panel The issue is was there prior authorization for the trades? Mr. Anderson is quite definite

on the point. Mr. Anderson gave his testimony in a direct, open and forthright manner. He

candidly admitted that he did not pay much attention to this account and that the complaint was

made as a result of a request following his invol',_ement with Richardson Greenshields with

I respect to his mother's account. Whether Donna Carson told him about the trades or he foundout about them in another manner is not the issue.

I-

-10-

In Mr. Meyer's evidence he sated:

"In this specific case, I clearly remember Mr. Anderson coming to the office on

his own wish late in the afternoon, and I'm assuming it was the day beforebecause we wouldn't have done the transaction the same day because of the

timing. Mr. Anderson and I visited in a little lounge, and he made reference tothat yesterday, and had a beer or whatever and discussed the sale of Telus; and

to be consistent with his mother's purchase of Corona and all the other clients

that we talked about that had moved into Corona, Mr. Anderson was in

agreement with the principal concept of taking his investment at Telus,

transferring it into the purchase of Corona..."

It will be noticed, however, that both Mr. Anderson and Vicky Anderson sold Telus and bought

Corona on the same day, namely December 18, 1990. If Mr. Anderson approved the purchase

to be consistent with his mother's purchase, it would have had to been after the fact since, by

' Mr. Meyer's own evidence, the discussion, if it was held, was held after the market had closed.

In addressing the conversation in the lounge there is a discrepancy as to when it was held. Mr.

Meyer said it was some time after the first order when they were discussing the sale of Telus

and purchase of Corona. In his cross-examination Mr. Anderson indicated that they had a beer

after their initial meeting, when he had opened the account, that is the Fall of 1990 when

Mr. Anderson instructed Mr. Meyer to buy the Telus receipts.

Mr. Meyer did not even remember Mr. Anderson's name, referring to him as David Anderson

in his Reply. In our view, Mr. Meyer's recollection of the meeting does not accord with the

other evidence and therefore we prefer the evidence of Mr. Anderson and find that Mr. Meyer

did, in fact, sell the Telus stock, acquire the Corona stock and thereafter acquired the Circa

Telecommunications stock without the prior authorization of Mr. Anderson contrary to section16.01(1) of the By-Law.

[

[-11-

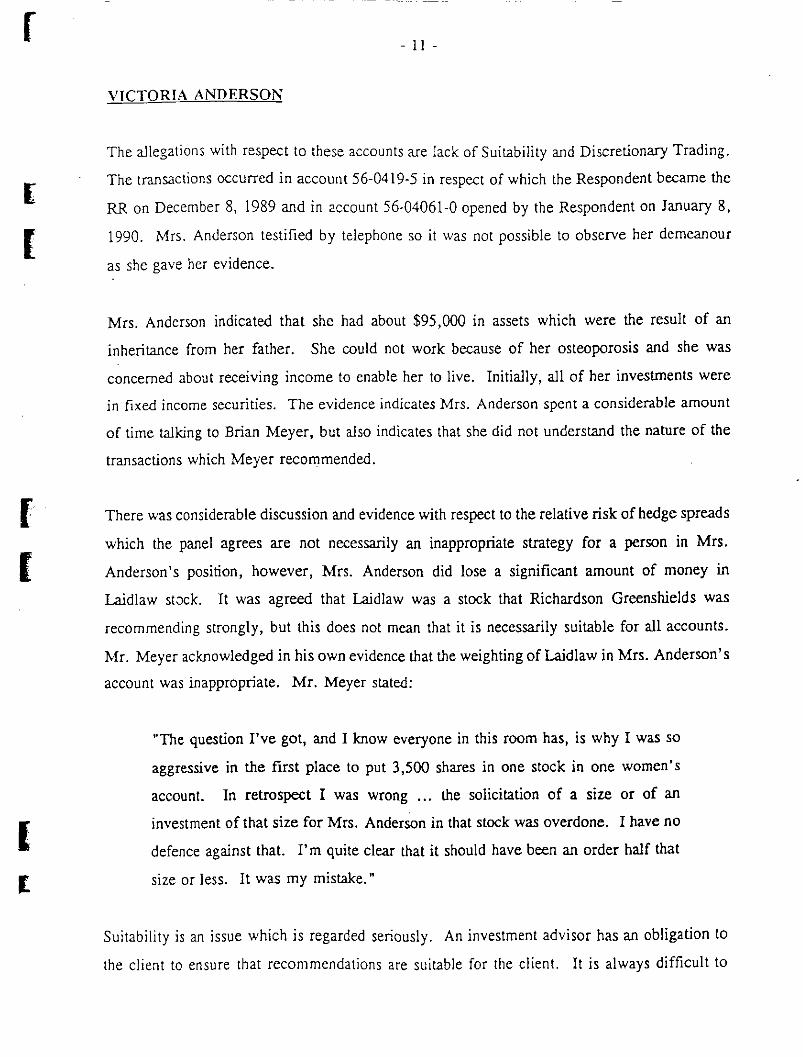

VICTORIA ANDERSON

The allegations with respect to these accounts are lack of Suitability and Discretionary Trading.

The transactions occurred in account 56-0419-5 in respect of which the Respondent became the[RR on December 8, 1989 and in account 56-04061-0 opened by the Respondent on January 8,

1990. Mrs. Anderson testified by telephone so it was not possible to observe her demeanouras she gave her evidence.

Mrs. Anderson indicated that she had about $95,000 in assets which were the result of an

inheritance from her father. She could not work because of her osteoporosis and she was

concerned about receiving income to enable her to live. Initially, all of her investments were

in fixed income securities. The evidence indicates Mrs. Anderson spent a considerable amount

of time talking to Brian Meyer, but also indicates that she did not understand the nature of the

transactions which Meyer recommended.

( There was considerable discussion and evidence with respect to the relative risk of hedge spreads

which the panel agrees are not necessarily an inappropriate strategy for a person in Mrs.

Anderson's position, however, Mrs. Anderson did lose a significant amount of money in

Laidlaw stock. It was agreed that Laidlaw was a stock that Richardson Greenshields was

recommending strongly, but this does not mean that it is necessarily suitable for all accounts.

Mr. Meyer acknowledged in his own evidence that the weighting of Laidlaw in Mrs. Anderson's

account was inappropriate. Mr. Meyer stated:

"The question I've got, and I know everyone in this room has, is why I was so

aggressive in the first place to put 3,500 shares in one stock in one women's

account. In retrospect I was wrong ... the solicitation of a size or of an

investment of that size for Mrs. Anderson in that stock was overdone. I have no

defence against that. I'm quite clear that it should have been an order half that

I[ sizeor less. It was my mistake."

Suitability is an issue which is regarded seriously. An investment advisor has an obligation to

the client to ensure that recommendations are suitable for the client. It is always difficult to

-12-

balance the needs of the client against the needs of the RR and that is an aa-ea which always

causes difficulty. The RR does not get paid unless the client trades and yet the trades must be

appropriate or suitable given the client. The RR can never substitute his or her judgment for

the informed decision of the client. We are concerned that Mr. Meyer crossed this boundary[

as evidenced by his statement:

["The upside potential was so great that we did not have a concern about the size

of the order number, not at that time we didn't."

Mrs. Anderson was quite clearly not capable of making an informed decision. She did not

understand her account, notwithstanding the significant amount of time Mr. Meyer spent with

her trying to explain the entries and her positions. In fact, from Mrs. Anderson's testimony Mr.

Meyer appeared to mislead her as to the true nature of the amount of her account and the

amount of the debits in the account and as to the disposition of one of the maturing bond

coupons which was paid against the debit.

Mr. Meyer's testimony does not stand up with respect to Mrs. Anderson. Mr. Meyer indicated

that Mrs. Anderson fully understood hedge spreads and, in fact, liked them so broughtmuch she

her sister in to open an account. Mrs. Anderson stated, "/-.fr. Meyer didn't buy me any stock

until the end of January so therefore I couldn't possibly have told her (her sister) anything about

a hedge spread or whatever or the stock market because I wasn't even involved in it at the time

she opened her account."

The account statements submitted appear to corroborate this in that Mrs. Chillibeck's accounts

were opened January 17 and 25 in 1990 and the first spread transaction which was put on in

Mrs. Anderson's account was January 26 and 29. It, therefore, appears unlikely that Mrs.

i Anderson would have discussed the hedge spreads with her sister.

1[ In our view, Mr. Meyer appears to have substituted his judgment for the judgment of hiscustomer in the case of the Laidlaw purchase which resulted in a loss disproportionate to the size

of the portfolio. This is a serious offence and we find him guilty.

f -13-

Further, Mrs. Anderson clearly stated that her Telus shares were sold without her consent and

Corona shares were purchased without her consent. Mr. Meyer said only that taking a profit

on Telus and buying Corona was something "that I had taken to many, many, many clients."

He did not cogently refute Mrs. Anderson's clear statement that she had not authorized thisl-

purchase but rather spoke in a general way that this strategy had been taken to many clients.

The evidence of Donna Carson, an accountant consulted by Mrs. Anderson, tends to corroborate

that Mrs. Anderson did not understand what was being done in her account but has no weight

in terms of whether specific instructions were given.

In the result, we are not satisfied that Mrs. Anderson gave prior instructions to Mr. Meyer with

respect to the impugned share transactions in her account and we find, therefore, that Mr. Meyer

is guilty of trading without authority in the sale of Telus and the purchase of Corona.

GORDON AND NORMA LACEY

[The allegations with respect to Mr. and Mrs. Lacey are that Mr. Meyer executed trades without

their prior knowledge, authorization or approval and that certain of the transactions were

unsuitable for Mr. and Mrs. Lacey.

Mr. Lacey gave evidence. He is a sincere but unsophisticated man with a self deprecating sense

of humour. He was very vague on details, but was very aware that he had lost money. His

memory is not good and he got very confused both in his direct testimony and in cross-

examination. We also found Mr. Lacey suggestible on details and frankly had great difficulty

in understanding what he was saying.

He opened an account with Mr. Meyer at the end of November, 1989 and transferred hisaccount at Mutual Life into it. This account represented the life savings of Mr. & Mrs. Lacey

[ of over $I00,000. He was looking for safety and income.

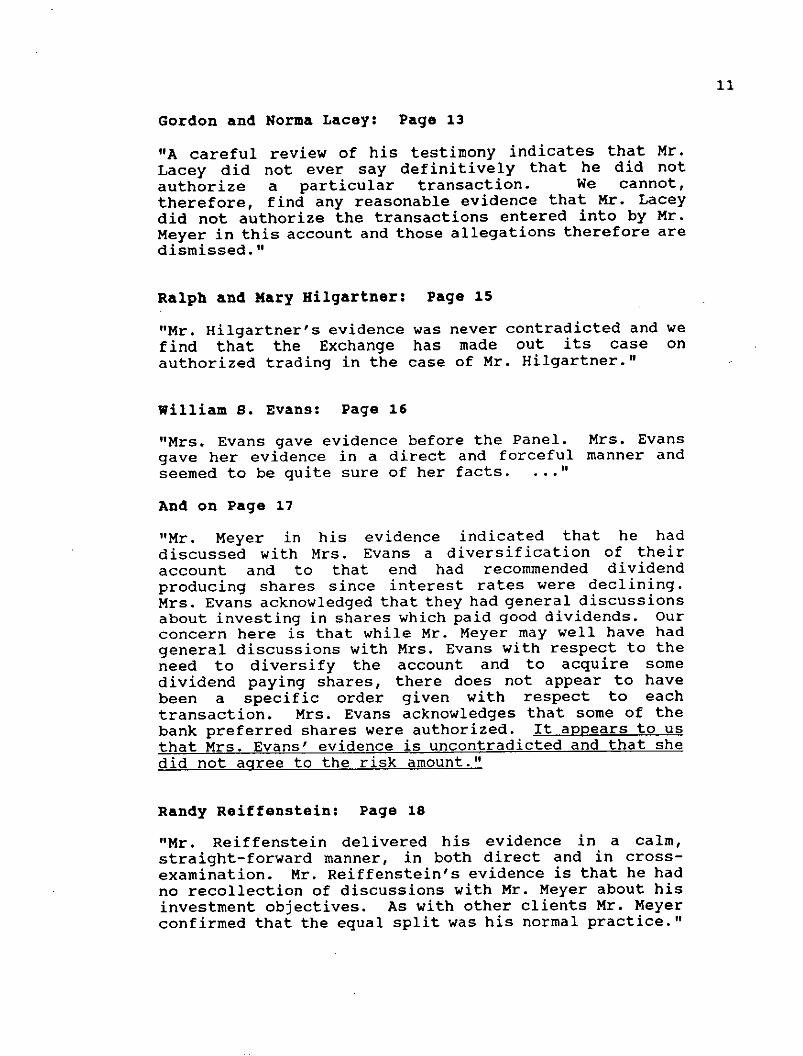

A careful review of his testimony indicates that Mr. Lacey did not ever say definitively that he

did not authorize a particular transaction. We cannot, therefore, find on any reasonable evidence

-14-

that Mr. Lacey did not authorize the transactions entered into by Mr. Meyer in this account and

those allegations therefore are dismissed.

It is also alleged that the transactions were unsuitable and with this we have less problem. Mr.

Meyer's evidence was that Mr. Lacey continually wanted to "lean to the side of safety" and that

he used this expression on a regular basis. This is consistent with his statement that the MutualLife accounts represented a lifetime of savings. On that basis, therefore, it is our view that the

trades in Veto, Santa Fe and Trio Gold were all inappropriate for an estate where an individual

had expressed the objective of safety and income. All three of these companies were junior

speculative issues with uncertain prospects and which were years away from producing dividend

income. We are therefore of the view that the Exchange has made out its case with respect to

suitability in the case of Mr. and Mrs. Lacey.

RALPH AND MARY HILGARTNER

Ralph Hilgartner gave evidence in person. Mr. Hilgartner is a 51 year oldfarmer from

Camrose. He and his wife operate a mixed farm and met Mr. Meyer after a seminar which Mr.

Meyer presented to a grain growers' club of which Mr. Hilgartner was a member. The account

was opened lanuary 21, 1991 in order to trade in commodities to help stabilize the market prices

he was receiving for his grain. This was Mr. Hilgartner's first experience with a broker and

he freely admitted that he was not sophisticated.

When questioned about his objectives shown in the NCAF as 25% to each category of security,

income, growth and risk he said Mr. Meyer told him "that's the way he normally starts them".

He trusted Mr. Meyer and had gone to Richardson Greenshields because Nwe thought they were

a reputable company and that we should be safe with them". Mr. Hilgartner gave short direct

I answers and seem to have a grasp of the details and what he wanted. His evidence was clear,cogent and uncontradicted on cross-examination.

[The commodities trading form tendered in evidence indicated that his initial order was for 20

contracts of barley, 30 contracts of canola, 20 contracts of wheat and 30 contracts of oats. He

specified clearly that he only wished to trade in grain because "that's all I grow". Initially, Mr.

-15-

Meyer traded in grain commodities in accordance with Mr. Hilgartner's instructions. However,

in the Fall of 1991 things started to change. Mr. Hilgarmer alleges that there were unauthorized

trades commencing October 21, 1991 to January 29, 1992. The Notice contains a list of

statements of transactions of which a number are hedging agreements in heating oil. Mr.

Hilgartner's evidence was that when he got the statement showing the heating oil contract he

called Mr. Meyer who responded something to the effect that he decided he should move himinto that "cause there's some money to be made there." And he said "Well I guess I have to

trust you" and left it. Mr. Hilgartner's evidence is that he attempted to contact Mr. Meyer on

a number of occasions subsequent to that but was not able to connect with him. He left

messages but the calls were not returned. In the end there was a $7,000 debit in the accounts.

The Hilgartners ultimately wrote a complaint letter dated December 7, 1992 advising that they

did not want to have any further association with Mr. Meyer.

: Mr. Hilgartner was specifically referred to Item 2(d) in the Reply wherein Mr. Meyer sates,

"Ralph Hilgartner always gave the approval for each transaction. Brian Meyer believes that he

" solicited the Gas and Heating Oil Spreads and that each order was placed after discussing them

with Ralph Hilgartner and securing his approval. Brian Meyer denies that the five (5) spreads

E entered over fifteen (15) months were without Mr. Hilgartner prior knowledge, authorization,

or approval."

Mr. Hilgartner's response was "that's false". On cross-examination Mr. Hilgarmer made it

clear that the trading they wanted to do was only related to grain and that he had not given his

approval for the non-grain transactions.

Mr. Meyer's testimony with respect to Mr. Hilgartner is interesting indeed. It appears to us that

Mr. Meyer would discuss a concept with an investor or a group of investors such as the group

i to whom he gave a seminar. On the basis of these conceptual discussions he would generate alist of clients who were interested in the concept. He seemed to treat those like open orders,

notwithstanding that no open order was ever submitted. Similar to the transactions on preferredshares, he would simply enter the orders when the price approached the target, but does not

appear to have reconfirmed the orders. It would appear therefore, in the Hilgartner case that,

while Mr. Hilgartner might have had a discussion about heating oil futures with Mr. Meyer, he

-16-

did not specifically instruct Mr. Meyer to enter into transactions with respect to heating oil

futures. For example, Mr. Meyer stated "he (Mr. HiIgartner) may not have understood the

spread in its entirety. I will never make that allegation, but he knew the general concept of a

[ spread".

Mr. Hilgartner's evidence was never contradicted and we find that the Exchange has made outits case of unauthorized trading in the case of Mr. Hilgartner.

WILLIAM S. EVANS

Mr. Evans opened an account with Richardson Greenshields in November of 1988. Mr. Meyer

assumed responsibility for the account in April of 1989 when he became registered. Mr. Evans

deposited the proceeds of a life insurance policy settlement which became payable when he

became disabled. His wife, Anna Evans, who was Mr. Meyer's first cousin, effectively made

the decisions on the account although she and Mr. Evans jointly discussed the account with Mr.

Meyer.

There was no Power of Attorney on the account and Mr. Meyer simply accepted the instructions

of Mrs. Evans who was usually with her husband when they saw Mr. Meyer. We could not

come to a decision whether this was appropriate or not since there was insufficient evidence as

to the degree of incapacity of Mr. Evans at the time the account was opened and at the time the

material instructions were given. There is simply insufficient evidence to make that

determination.

Mrs. Evans gave evidence before the panel. Mrs. Evans gave her evidence in a direct and

forceful manner and seemed to be quite sure of her facts. She said she was focused on the

account because "when your husband's sick and disabled you're pretty clear on what you'regoing to live on for your retirement". The account opened was a no fee R.R.S.P. The initial

[ investments were fixed income securities such as Alberta Capital Bonds and other provincial or

provincially guaranteed instruments.

-17-

bits. Evans is not a sophisticated investor but did state that she wanted to avoid risk. She does

not appear to have been aware that an unauthorized purchase could be reversed out of her

account without commissions. She appeared to believe that once a stock had been purchased

there was no recourse and she did not want to incur the commission incurred in trading it out

by selling it. For example, when asked by counsel for the Exchange "did you object to the

placement of this investment in your account'?." she responded "No. I wasn't happy about it butno, I was already invested in, (sic) It was -- he already bought the shares, so okay, we hope for

the best."

She stated emphatically that she asked Mr. Meyer to stop trading in her account without

authorization on January 28, 1992 without success. The unauthorized purchases continued

including Veto and Interprovincial Pipe. She stated that by March of 1993 after an unauthorized

purchase of Trio Gold shares she had made her mind up to move the account somewhere else

when she was advised that Mr. Meyer had been terminated by Richardson Greenshields. She

did not contradict herself on cross-examination.

[Mrs. Evans acknowledged that she spoke with Mr. Meyer on a number of occasions, both on

the telephone and at his office and also indicated that they spoke at family gatherings. There

was inconsistency in the evidence about when the order was placed for certain Telus shares.

Mr. Meyer in his direct evidence pointed out that it would have been virtually impossible for

Mrs. Evans to have asked him to buy Telus since the issue came to the market at 2:30 Friday

afternoon and had to be sold by Monday. Whether this order was solicited or unsolicited is

irrelevant since Mrs. Evans acknowledged that it was an authorized purchase.

Mr. Meyer in his evidence indicated that he had discussed with Mrs. Evans some diversification

of their account and to that end had recommended dividend producing shares since interest rates

I were declining. Mrs. Evans acknowledged that they had had general discussions about investingin shares which paid good dividends. Our concern here is that while Mr. Meyer may well have

bad general discussions with Mrs. Evans with respect to the need to diversify the account and

to acquire some dividend paying shares, there does not appear to have been a specific order

given with respect to each transaction. Mrs. Evans acknowledges that some of the bank

preferred shares were authorized. It appears to us that Mrs. Evans' evidence is uncontradicted

-18-

and that she did not agree to the risk amounts. The allocation of 25 % risk on the NCAF appear

to be purely arbitrary and, as indicated above appears to have been the "standard procedure" for

Mr. Meyer. There was clearly no room for risk in this portfolio and that allocation should not

have been made on the NCAF. To try and justify the placement of Veto Resources and Triot;Gold into the account on the basis of that allocation therefore does not stand. Looking at the

client having regard to the age, investment knowledge, need for income and assets available,there is no place in this portfolio for a speculative security.

We find therefore that there are unauthorized transactions, specifically Veto and Trio Gold and

that neither of these securities were suitable for the Evans' account.

RANDY REIFFENSTEIN

Mr. Reiffenstein had met Mr. Meyer when Mr. Meyer was doing a television program at the

television station in Red Deer where Mr. Reiffenstein worked. The evidence indicated they

_. spent a lot of time talking about general things including investments, advertising and the like.

After Mr. Reiffenstein had left Red Deer he contacted Mr. Meyer and opened a self-directed

R.R.S.P. account and a joint cash account. The new account forms for both the R.R.S.P. and

the cash account indicated an equal 25% split among each of security, income, growth and risk.

Mr. Reiffenstein delivered his evidence in a calm, straight forward manner, in both direc/: and

in cross-examination. Mr. Reiffenstein's evidence is that he had no recollection of discussions

with Mr. Meyer about his investment objectives. As with other clients Mr. Meyer confirmed

that the equal split was his normal practice.

In his direct testimony Mr. Reiffenstein indicated that he had told Mr. Meyer that he had

previously been bankrupt and had previously had a bad experience in the stock market and thattherefore he was very cautious. His evidence was that it was tough to save the money and that

he didn't wantto lose it.

Mr. Reiffenstein is an unsophisticated investor. In his direct examination he confirmed his

statements in paragraph eight of his affidavit that he received a confirmation slip with respect

-19-

to the execution of an order to purchase 2,500 shares of Veto Resources at $.78 and that he did

not give prior approval for that transaction. The first time he was aware of the transaction was

when he received the confirmation slip. His response to a question about when he first heard

about Veto was "Absolutely. First time I heard about Veto Resources was when I got the firstE

statement in April of 92". He stated that he tried to contact Mr. Meyer "right off the bat" but

did not get a response back. He tried to contact him several times without success. Hisevidence was uncontradicted on cross-examination.

Mr. Meyer in his direct evidence, pointed out that all of the account documentation had been

done on the same day, March 30, 1992. That he had arranged for a cheque for $1,000.00 to

be issued to Mr. Reiffenstein against delivery of the Telus shares and had received an order to

sell them. He had made application for the transfer of the R.R.S.P. amount from the Treasury

Branch to the RSP account. Subsequent to receipt of that money he had made a single purchase

of Veto on the basis that it was a small amount of money. He said Mr. Reiffenstein had

indicated to him that he was not happy with the interest amounts and it was a simple purchase.

'" Mr. Meyer did not say with certainty that he did contact Mr. Reiffenstein, only that:

"In that 15-day period I would have contacted him and said, okay, our discussions

previously were to look at a junior stock because we're not looking at fixed

income or you would have stayed where you were. Now that the funds are here,

let's go with this. One simple purchase two years ago."

That part we believe, the rest of Mr. Meyer's testimony we do not believe. Mr. Meyer stated,

"We had a very small amount of cash. We had a very clear cut situation here that he

was not in 1992 satisfied with the return of the bank on income investments. The GIC

l rate, if it may have been 7 or 8 or 9 percent was one of his motives for moving from theTreasury Branch into a self-administered account.

[It makes no sense to me to receive $2,200.00 in an R.R.S.P. account from an institution

where he had an interest bearing vehicle and come to me with $2,200.00 and stay in an

interest bearing investment."

-20-

This statement fits with the lack of concern for the client's desires evidenced by Mr. Meyer.

Mr. Reiffenstein did not mention in his evidence anything at all about rates. He talked about

safety. He had had a bad experience, he didn't want to repeat it. If Mr. Meyer had a small

amount of money he could have put it in a mutual fund. But it seems to us that Mr. Meyer's17

attitude is summed up in the preceding quote. In other words Mr. Meyer was substituting his

judgment for the judgment of the client. By way of peripheral evidence we note that in hishandwritten response found at Tab 33, Mr. Meyer attributes the trading price of Veto as beilag

"what really promoted this ridiculous complaint". We do not believe that asking to be put into

something safe and being put into a junior stock without your knowledge constitutes a ridiculous

complaint. Mr. Meyer said he wasn't going to split it up and did one simple transaction and

bought Veto. In other words he met his own needs and did not meet the client's needs. We

find therefore contravention of section 16.07 of the By-Law has been proved.

McMULLEN FARMS, FLOYD AND RUTH MeMULLEN

The allegations with respect to the McMullen accounts arise out of activities in the McMullen

Farms Limited, account 56-0543-0 and the joint account 56-0528-5. The allegations conslitute

unauthorized trading and unsuitable transactions.

Floyd McMullen operates a mixed farm growing grains and raising livestock near Innisfail.

He testified that he opened an account because he had sold some CanNa and he wanted to "buy

it back'. In other words he had sold and delivered the Canola to an elevator but was concerned

that perhaps the price would go up and wanted to protect that price by buying a canola future.

He opened his account in October of 1991 with a new account application form indicating his

objectives to be 99% risk. The supplementary account agreement showed 100% risk. Mr.