Embed Size (px)

Citation preview

November 28, 2008 GIPSA 1

JOINT MEETING OF ALL CHECK-OFF QUALIFIED UNIONS /

ASSOCIATIONS OF GIPSA COs.

EXPLORATORY TALKS ON PROPOSED WAGE REVISION

W.E.F. 01.08.2007Friday, November 28, 2008

New Delhi

November 28, 2008 GIPSA 2

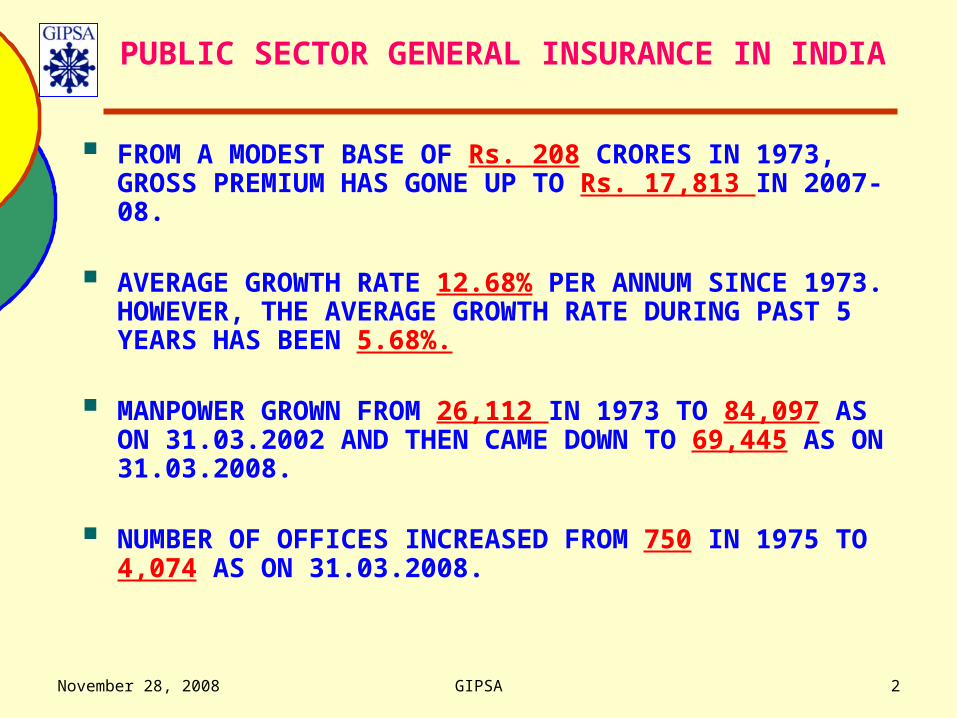

PUBLIC SECTOR GENERAL INSURANCE IN INDIA

FROM A MODEST BASE OF Rs. 208 CRORES IN 1973, GROSS PREMIUM HAS GONE UP TO Rs. 17,813 IN 2007-08.

AVERAGE GROWTH RATE 12.68% PER ANNUM SINCE 1973. HOWEVER, THE AVERAGE GROWTH RATE DURING PAST 5 YEARS HAS BEEN 5.68%.

MANPOWER GROWN FROM 26,112 IN 1973 TO 84,097 AS ON 31.03.2002 AND THEN CAME DOWN TO 69,445 AS ON 31.03.2008.

NUMBER OF OFFICES INCREASED FROM 750 IN 1975 TO 4,074 AS ON 31.03.2008.

November 28, 2008 GIPSA 3

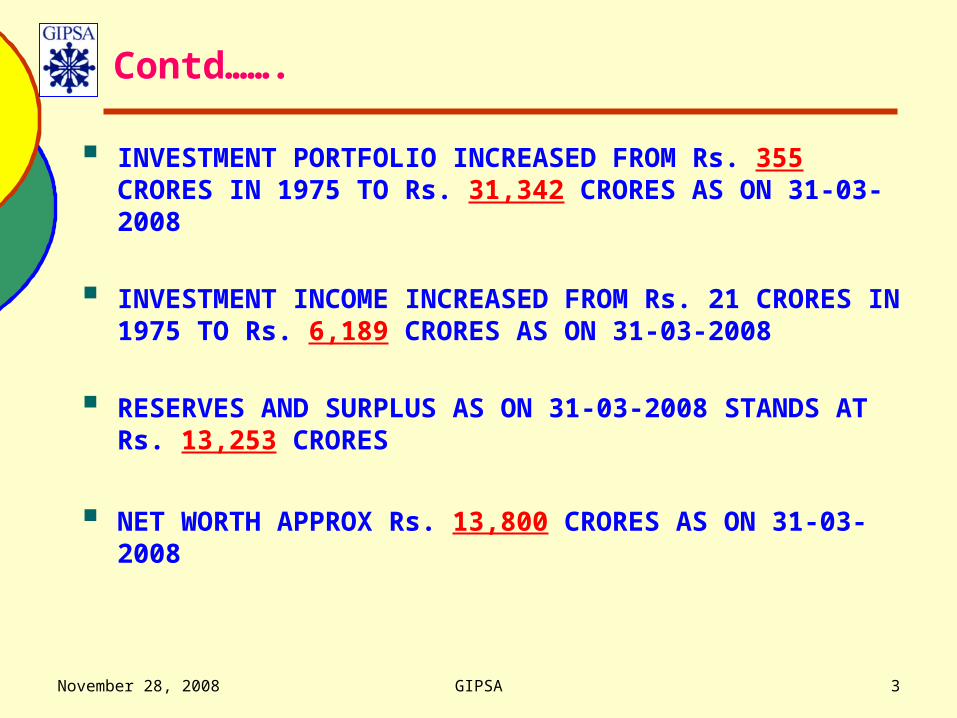

Contd…….

INVESTMENT PORTFOLIO INCREASED FROM Rs. 355 CRORES IN 1975 TO Rs. 31,342 CRORES AS ON 31-03-2008

INVESTMENT INCOME INCREASED FROM Rs. 21 CRORES IN 1975 TO Rs. 6,189 CRORES AS ON 31-03-2008

RESERVES AND SURPLUS AS ON 31-03-2008 STANDS AT Rs. 13,253 CRORES

NET WORTH APPROX Rs. 13,800 CRORES AS ON 31-03-2008

November 28, 2008 GIPSA 4

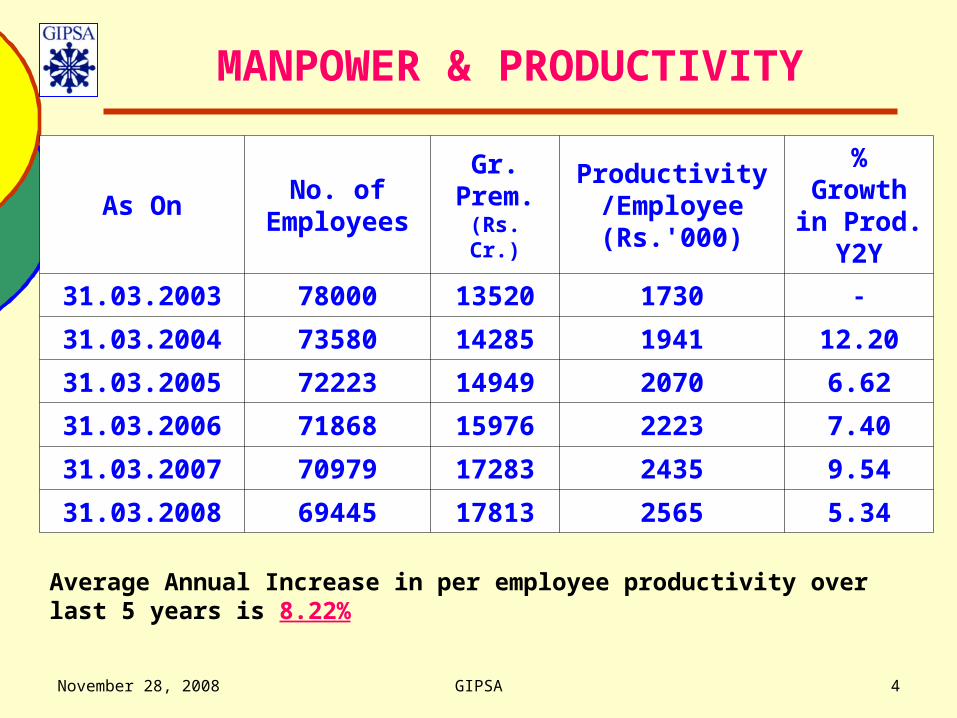

MANPOWER & PRODUCTIVITY

As OnNo. of

Employees

Gr. Prem. (Rs. Cr.)

Productivity/Employee (Rs.'000)

%Growth in Prod.

Y2Y

31.03.2003 78000 13520 1730 -

31.03.2004 73580 14285 1941 12.20

31.03.2005 72223 14949 2070 6.62

31.03.2006 71868 15976 2223 7.40

31.03.2007 70979 17283 2435 9.54

31.03.2008 69445 17813 2565 5.34

Average Annual Increase in per employee productivity over last 5 years is 8.22%

November 28, 2008 GIPSA 5

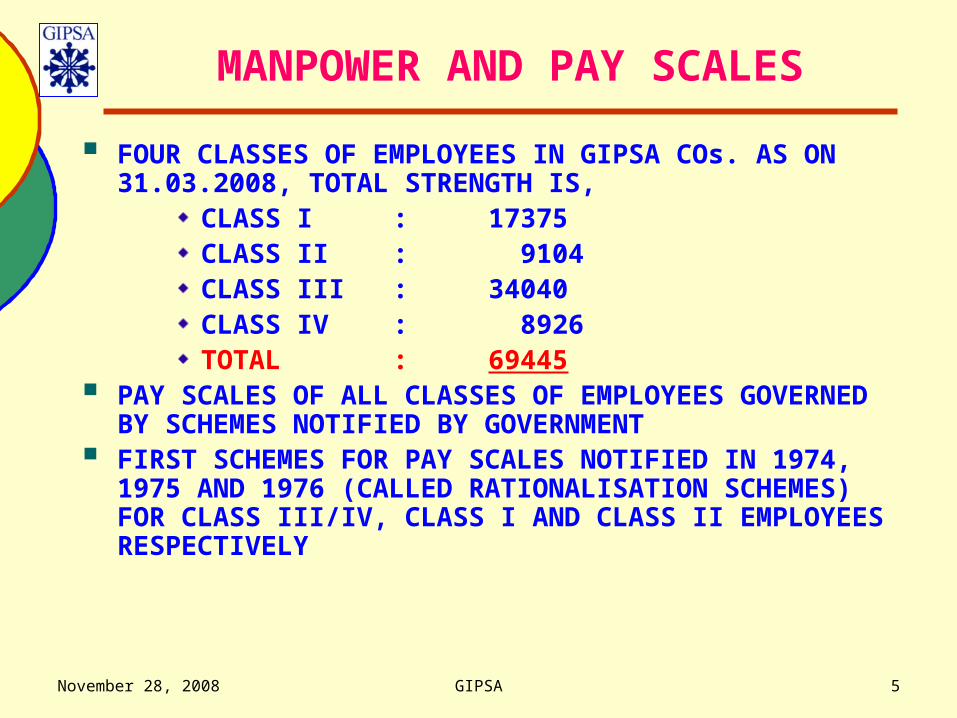

MANPOWER AND PAY SCALES

FOUR CLASSES OF EMPLOYEES IN GIPSA COs. AS ON 31.03.2008, TOTAL STRENGTH IS,

CLASS I : 17375CLASS II : 9104CLASS III : 34040CLASS IV : 8926TOTAL : 69445

PAY SCALES OF ALL CLASSES OF EMPLOYEES GOVERNED BY SCHEMES NOTIFIED BY GOVERNMENT

FIRST SCHEMES FOR PAY SCALES NOTIFIED IN 1974, 1975 AND 1976 (CALLED RATIONALISATION SCHEMES) FOR CLASS III/IV, CLASS I AND CLASS II EMPLOYEES RESPECTIVELY

November 28, 2008 GIPSA 6

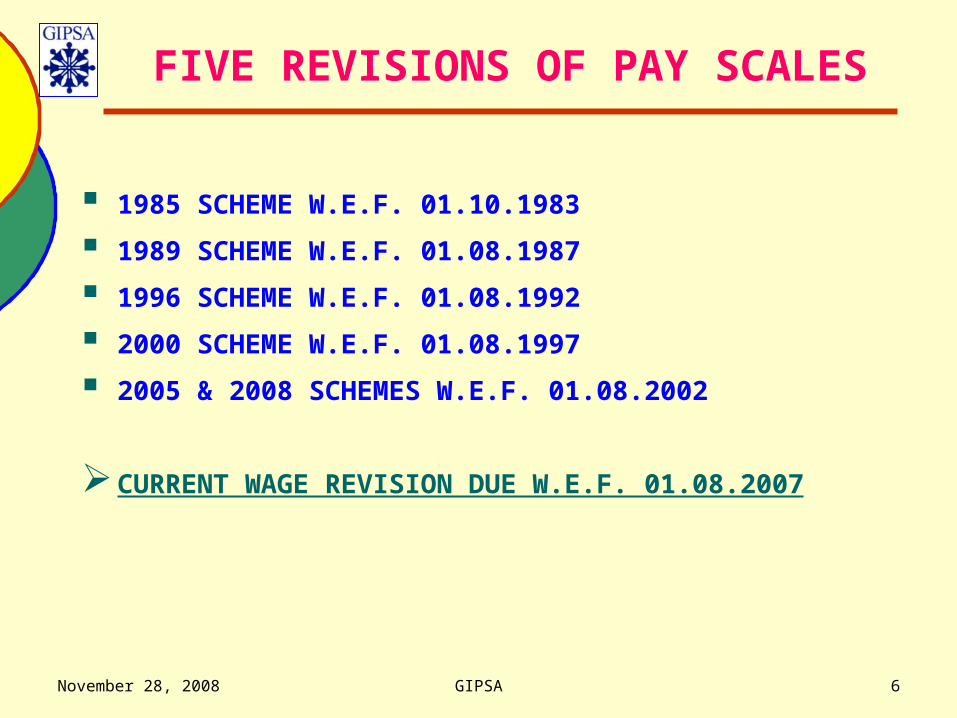

FIVE REVISIONS OF PAY SCALES

1985 SCHEME W.E.F. 01.10.1983

1989 SCHEME W.E.F. 01.08.1987

1996 SCHEME W.E.F. 01.08.1992

2000 SCHEME W.E.F. 01.08.1997

2005 & 2008 SCHEMES W.E.F. 01.08.2002

CURRENT WAGE REVISION DUE W.E.F. 01.08.2007

November 28, 2008 GIPSA 7

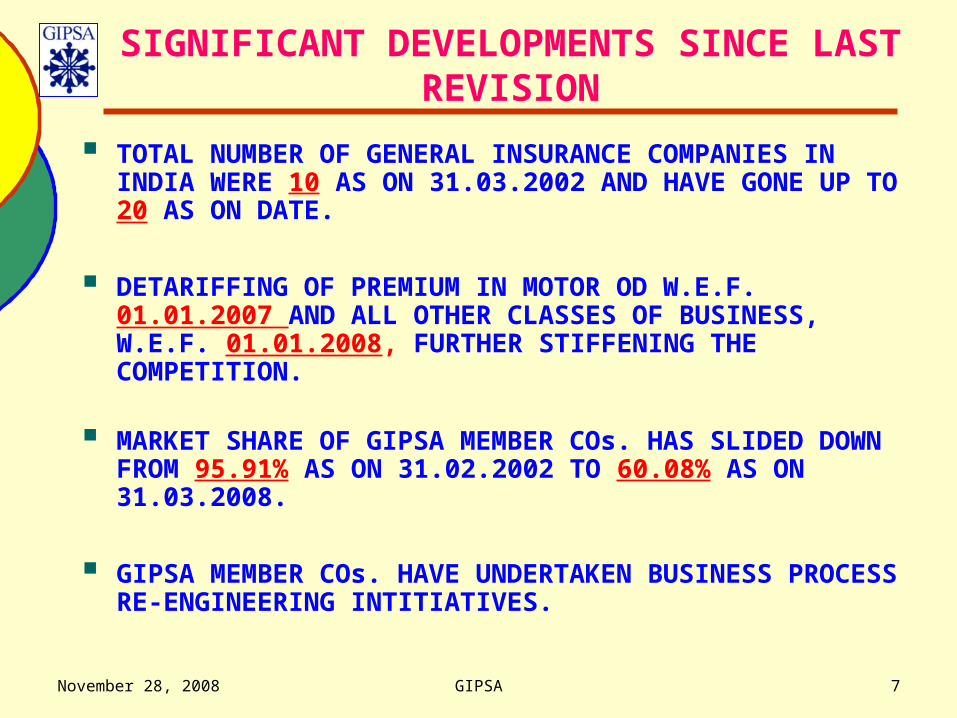

SIGNIFICANT DEVELOPMENTS SINCE LAST REVISION

TOTAL NUMBER OF GENERAL INSURANCE COMPANIES IN INDIA WERE 10 AS ON 31.03.2002 AND HAVE GONE UP TO 20 AS ON DATE.

DETARIFFING OF PREMIUM IN MOTOR OD W.E.F. 01.01.2007 AND ALL OTHER CLASSES OF BUSINESS, W.E.F. 01.01.2008, FURTHER STIFFENING THE COMPETITION.

MARKET SHARE OF GIPSA MEMBER COs. HAS SLIDED DOWN FROM 95.91% AS ON 31.02.2002 TO 60.08% AS ON 31.03.2008.

GIPSA MEMBER COs. HAVE UNDERTAKEN BUSINESS PROCESS RE-ENGINEERING INTITIATIVES.

November 28, 2008 GIPSA 8

MARKET SHARE

AS ON PUBLIC PRIVATE

31.03.2002 95.91 4.09

31.03.2003 90.35 9.65

31.03.2004 85.52 14.48

31.03.2005 79.93 20.07

31.03.2006 73.66 26.34

31.03.2007 65.28 34.72

31.03.2008 60.08 39.92

Sept-08 (Flash Figures) 58.25 41.75

November 28, 2008 GIPSA 9

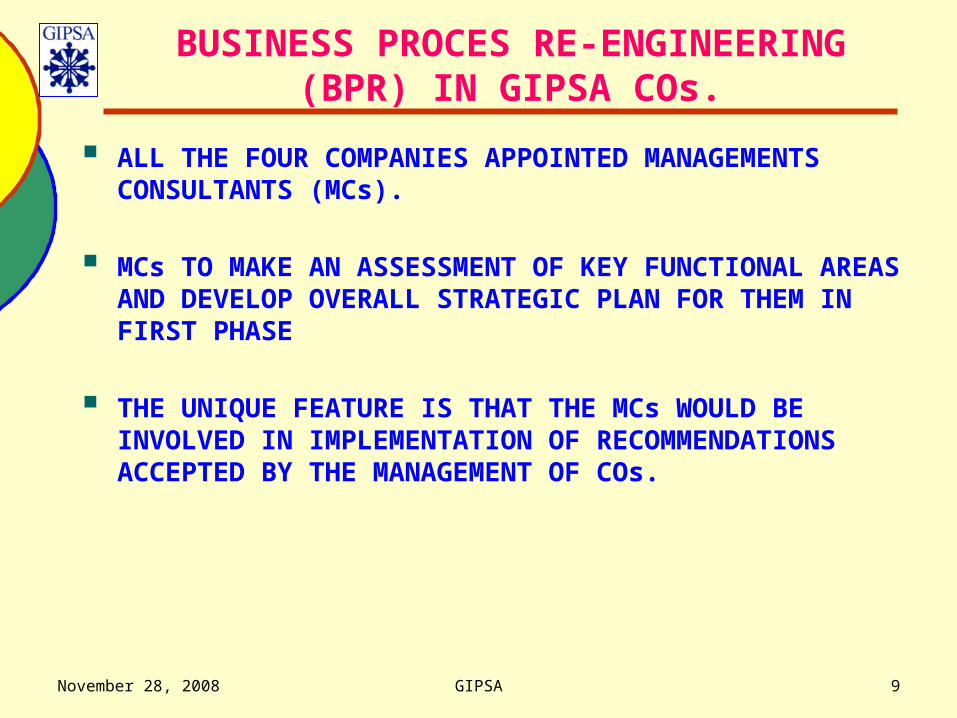

BUSINESS PROCES RE-ENGINEERING (BPR) IN GIPSA COs.

ALL THE FOUR COMPANIES APPOINTED MANAGEMENTS CONSULTANTS (MCs).

MCs TO MAKE AN ASSESSMENT OF KEY FUNCTIONAL AREAS AND DEVELOP OVERALL STRATEGIC PLAN FOR THEM IN FIRST PHASE

THE UNIQUE FEATURE IS THAT THE MCs WOULD BE INVOLVED IN IMPLEMENTATION OF RECOMMENDATIONS ACCEPTED BY THE MANAGEMENT OF COs.

November 28, 2008 GIPSA 10

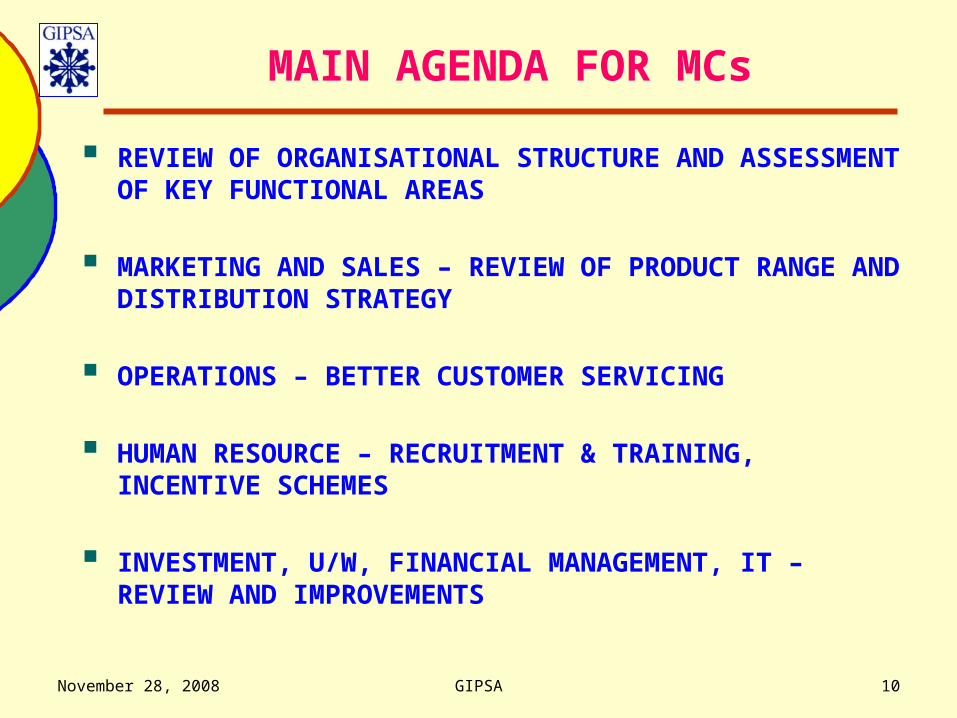

MAIN AGENDA FOR MCs

REVIEW OF ORGANISATIONAL STRUCTURE AND ASSESSMENT OF KEY FUNCTIONAL AREAS

MARKETING AND SALES – REVIEW OF PRODUCT RANGE AND DISTRIBUTION STRATEGY

OPERATIONS – BETTER CUSTOMER SERVICING

HUMAN RESOURCE – RECRUITMENT & TRAINING, INCENTIVE SCHEMES

INVESTMENT, U/W, FINANCIAL MANAGEMENT, IT – REVIEW AND IMPROVEMENTS

November 28, 2008 GIPSA 11

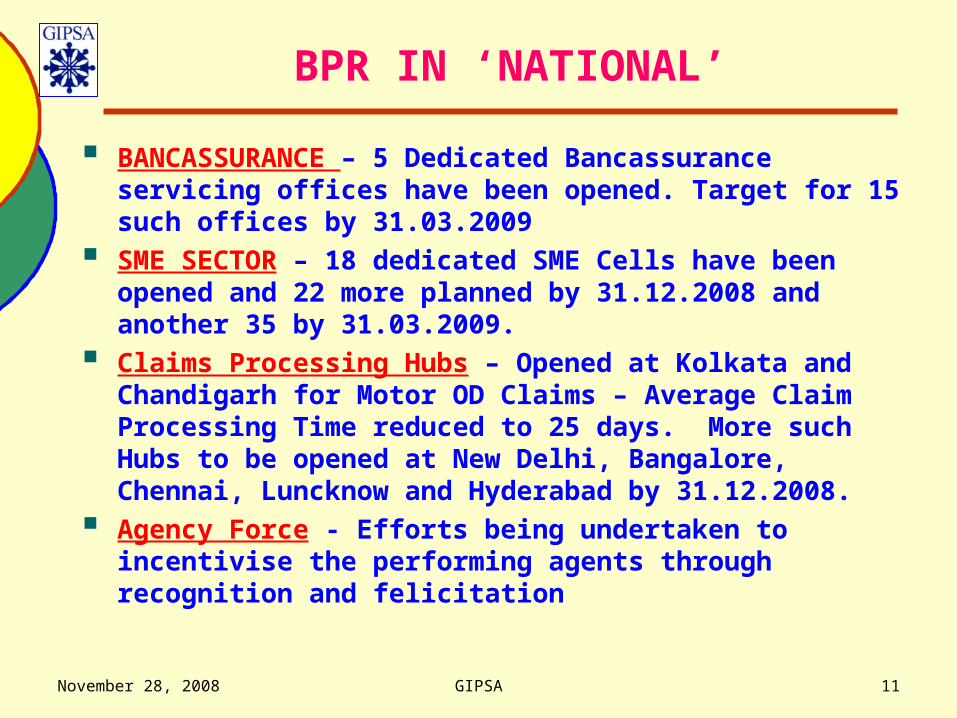

BPR IN ‘NATIONAL’

BANCASSURANCE – 5 Dedicated Bancassurance servicing offices have been opened. Target for 15 such offices by 31.03.2009

SME SECTOR – 18 dedicated SME Cells have been opened and 22 more planned by 31.12.2008 and another 35 by 31.03.2009.

Claims Processing Hubs – Opened at Kolkata and Chandigarh for Motor OD Claims – Average Claim Processing Time reduced to 25 days. More such Hubs to be opened at New Delhi, Bangalore, Chennai, Luncknow and Hyderabad by 31.12.2008.

Agency Force - Efforts being undertaken to incentivise the performing agents through recognition and felicitation

November 28, 2008 GIPSA 12

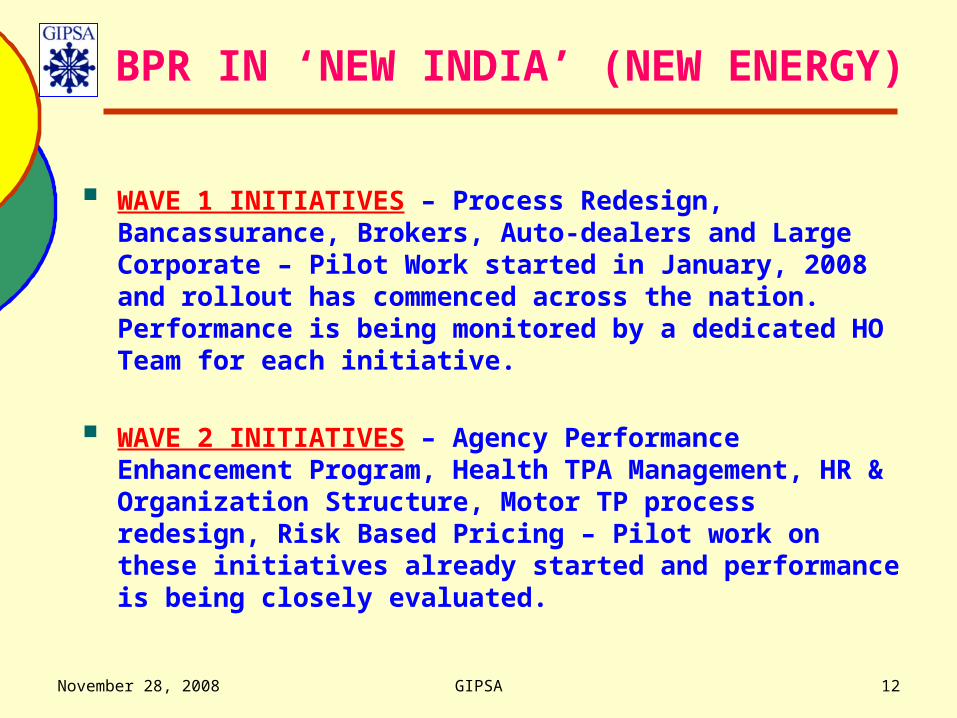

BPR IN ‘NEW INDIA’ (NEW ENERGY)

WAVE 1 INITIATIVES – Process Redesign, Bancassurance, Brokers, Auto-dealers and Large Corporate – Pilot Work started in January, 2008 and rollout has commenced across the nation. Performance is being monitored by a dedicated HO Team for each initiative.

WAVE 2 INITIATIVES – Agency Performance Enhancement Program, Health TPA Management, HR & Organization Structure, Motor TP process redesign, Risk Based Pricing – Pilot work on these initiatives already started and performance is being closely evaluated.

November 28, 2008 GIPSA 13

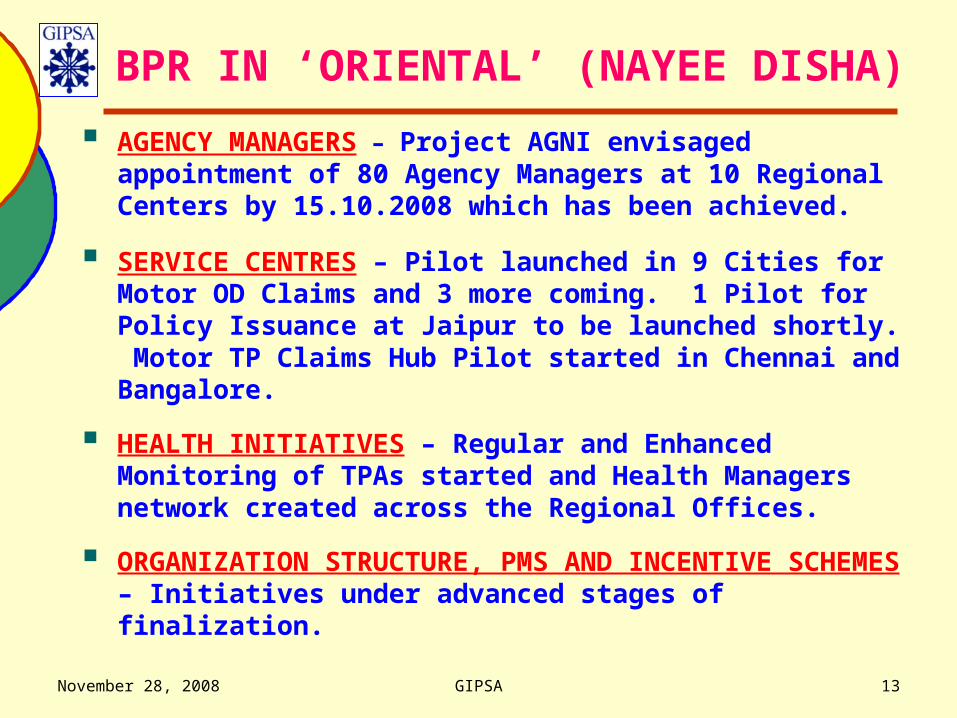

BPR IN ‘ORIENTAL’ (NAYEE DISHA)

AGENCY MANAGERS – Project AGNI envisaged appointment of 80 Agency Managers at 10 Regional Centers by 15.10.2008 which has been achieved.

SERVICE CENTRES – Pilot launched in 9 Cities for Motor OD Claims and 3 more coming. 1 Pilot for Policy Issuance at Jaipur to be launched shortly. Motor TP Claims Hub Pilot started in Chennai and Bangalore.

HEALTH INITIATIVES – Regular and Enhanced Monitoring of TPAs started and Health Managers network created across the Regional Offices.

ORGANIZATION STRUCTURE, PMS AND INCENTIVE SCHEMES – Initiatives under advanced stages of finalization.

November 28, 2008 GIPSA 14

BPR IN ‘UNITED INDIA’ (UNISURGE)

As on 15.10.2008, have opened 7 Bancassurance Offices against 6 planned, 9 Tie-ups with Motor Dealers against target of 8, implemented Agency Managers concept in 96 Offices (9 ROs) and opened 3 Large Corporate & Broker Cells.

In Motor, 2 ‘filing ready’ products have been developed.

Design and Plan for Service Hub finalized with identification of location and personnel.

PMS and Incentive Schemes for Employees under final stages of discussion.

November 28, 2008 GIPSA 15

BPR – HR - COMMON IN ALL COs.

Management Consultants in each Company took extensive studies in the area of Manpower Planning.

Reforms in Promotional Processes undertaken by GIPSA to address the contemporary requirements in the changed business scenario.

New Promotion Policies evolved for Class I Officers and Class III/IV Employees. Promotion Policy for Development Officers amended to the requisite extent.

November 28, 2008 GIPSA 16

Contd…….

Companies have initiated Promotion Exercises for Promotions From Class IV to III, within Class III, From Class III to Class I, From Class II to I and within Class I (Scale I, II, III & IV)

All these Promotion Exercises scheduled to be completed by 15.12.2008.

Transfer and Mobility Policy now in vogue in all cadres to provide requisite flexibility in deployment to serve Organizational Requirements and career development of Employees.

PMS and Incentive Schemes for Employees under final stages of evolution.

November 28, 2008 GIPSA 17

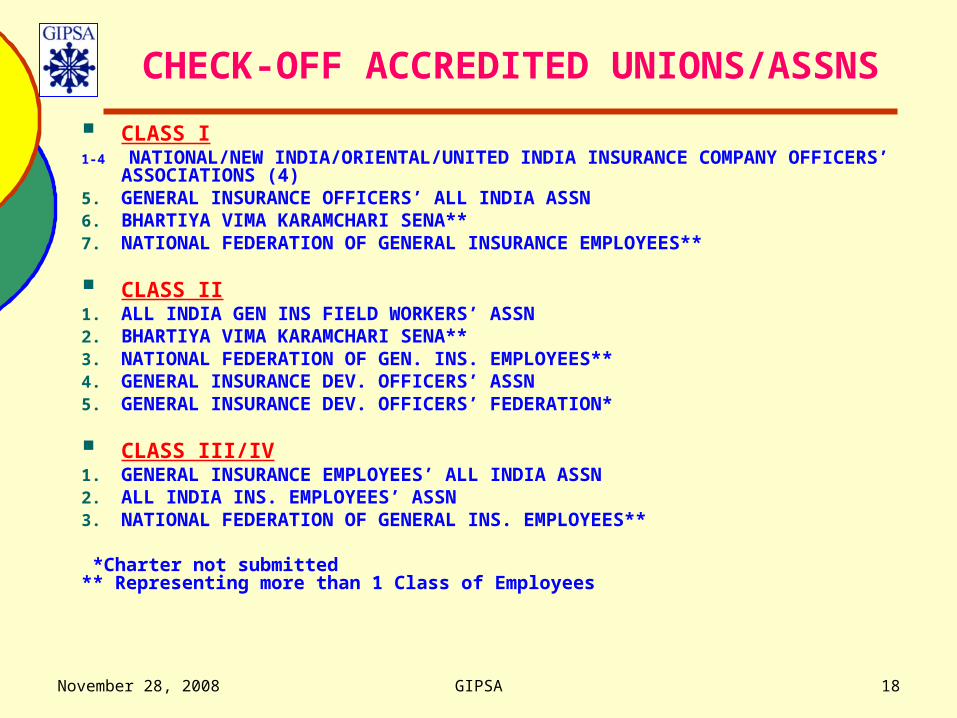

PROCESS AND FACTORS OF WAGE REVISION

12 CHECK-OFF QUALIFIED UNIONS / ASSOCIATIONS OF EMPLOYEES IN MEMBER COMPANIES.

2 OF THESE UNIONS REPRESENT MORE THAN ONE CLASS OF EMPLOYEES

ALL CHECK-OFF QUALIFIED UNIONS/ASSOCIATIONS (EXCEPT ONE FROM DEVELOPMENT OFFICERS) HAVE SUBMITTED THEIR CHARTER OF DEMANDS.

November 28, 2008 GIPSA 18

CHECK-OFF ACCREDITED UNIONS/ASSNS

CLASS I1-4 NATIONAL/NEW INDIA/ORIENTAL/UNITED INDIA INSURANCE COMPANY

OFFICERS’ ASSOCIATIONS (4)5. GENERAL INSURANCE OFFICERS’ ALL INDIA ASSN6. BHARTIYA VIMA KARAMCHARI SENA**7. NATIONAL FEDERATION OF GENERAL INSURANCE EMPLOYEES**

CLASS II1. ALL INDIA GEN INS FIELD WORKERS’ ASSN2. BHARTIYA VIMA KARAMCHARI SENA**3. NATIONAL FEDERATION OF GEN. INS. EMPLOYEES**4. GENERAL INSURANCE DEV. OFFICERS’ ASSN5. GENERAL INSURANCE DEV. OFFICERS’ FEDERATION*

CLASS III/IV1. GENERAL INSURANCE EMPLOYEES’ ALL INDIA ASSN2. ALL INDIA INS. EMPLOYEES’ ASSN3. NATIONAL FEDERATION OF GENERAL INS. EMPLOYEES**

*Charter not submitted** Representing more than 1 Class of Employees

November 28, 2008 GIPSA 19

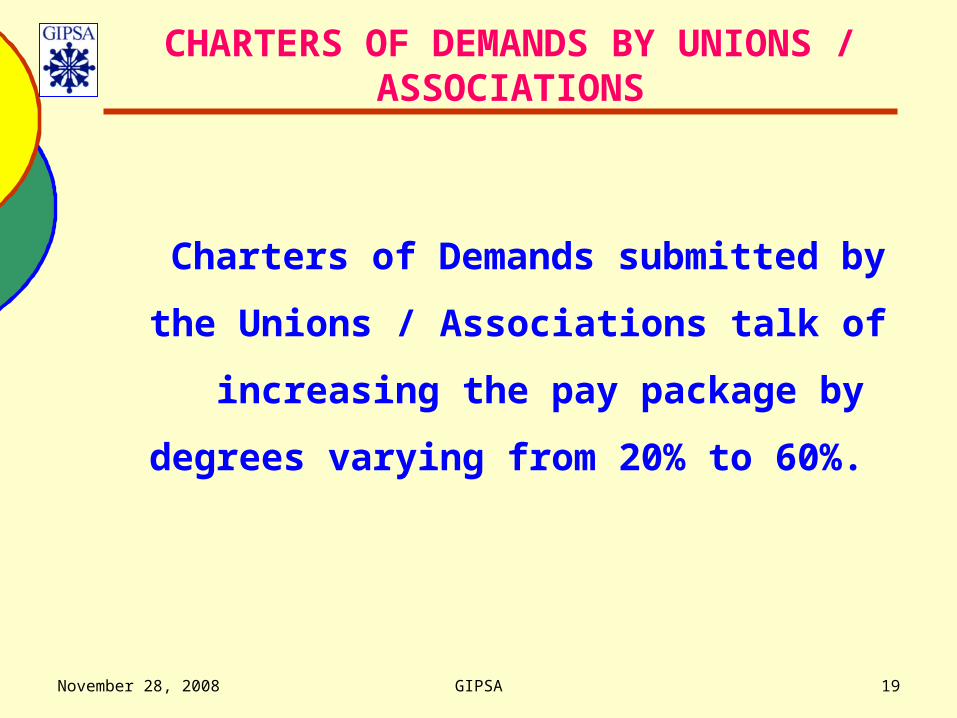

CHARTERS OF DEMANDS BY UNIONS / ASSOCIATIONS

Charters of Demands submitted by

the Unions / Associations talk of

increasing the pay package by

degrees varying from 20% to 60%.

November 28, 2008 GIPSA 20

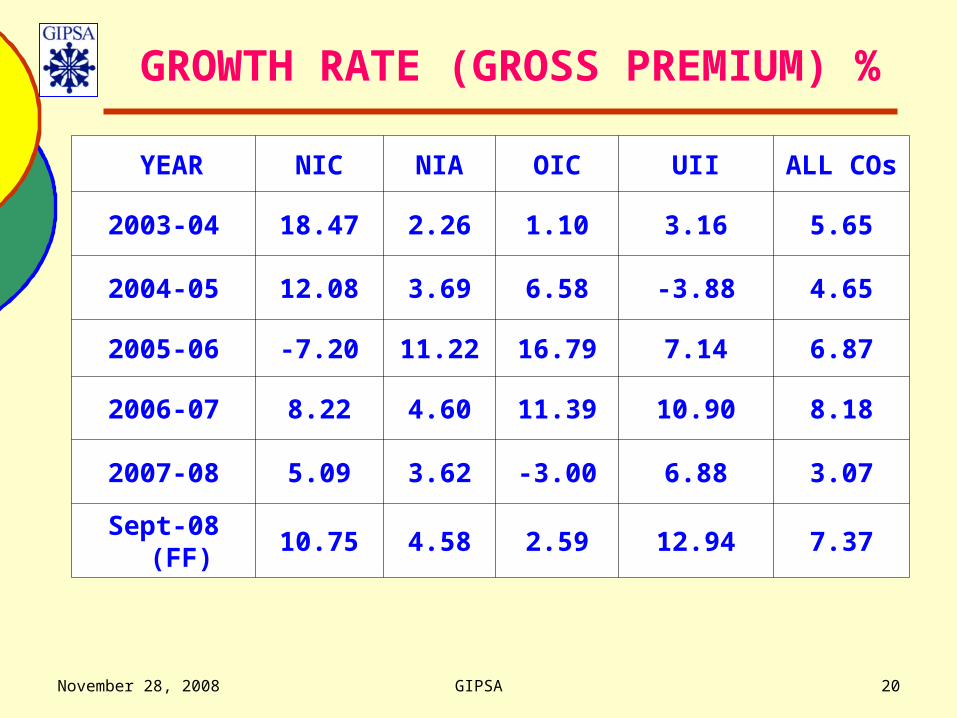

GROWTH RATE (GROSS PREMIUM) %

YEAR NIC NIA OIC UII ALL COs

2003-04 18.47 2.26 1.10 3.16 5.65

2004-05 12.08 3.69 6.58 -3.88 4.65

2005-06 -7.20 11.22 16.79 7.14 6.87

2006-07 8.22 4.60 11.39 10.90 8.18

2007-08 5.09 3.62 -3.00 6.88 3.07

Sept-08 (FF) 10.75 4.58 2.59 12.94 7.37

November 28, 2008 GIPSA 21

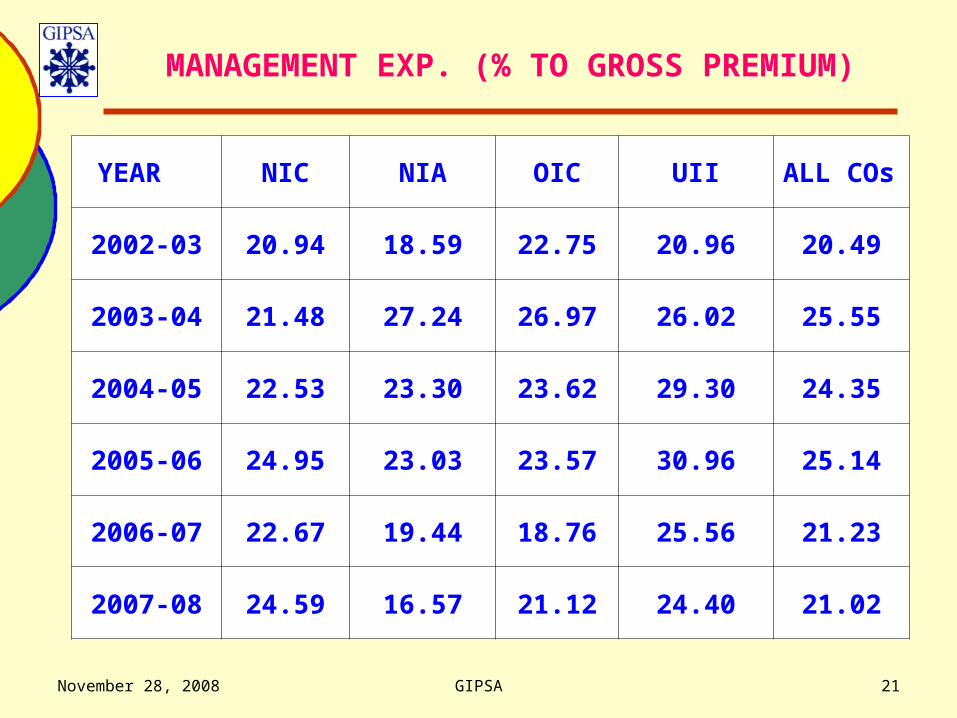

MANAGEMENT EXP. (% TO GROSS PREMIUM)

YEAR NIC NIA OIC UII ALL COs

2002-03 20.94 18.59 22.75 20.96 20.49

2003-04 21.48 27.24 26.97 26.02 25.55

2004-05 22.53 23.30 23.62 29.30 24.35

2005-06 24.95 23.03 23.57 30.96 25.14

2006-07 22.67 19.44 18.76 25.56 21.23

2007-08 24.59 16.57 21.12 24.40 21.02

November 28, 2008 GIPSA 22

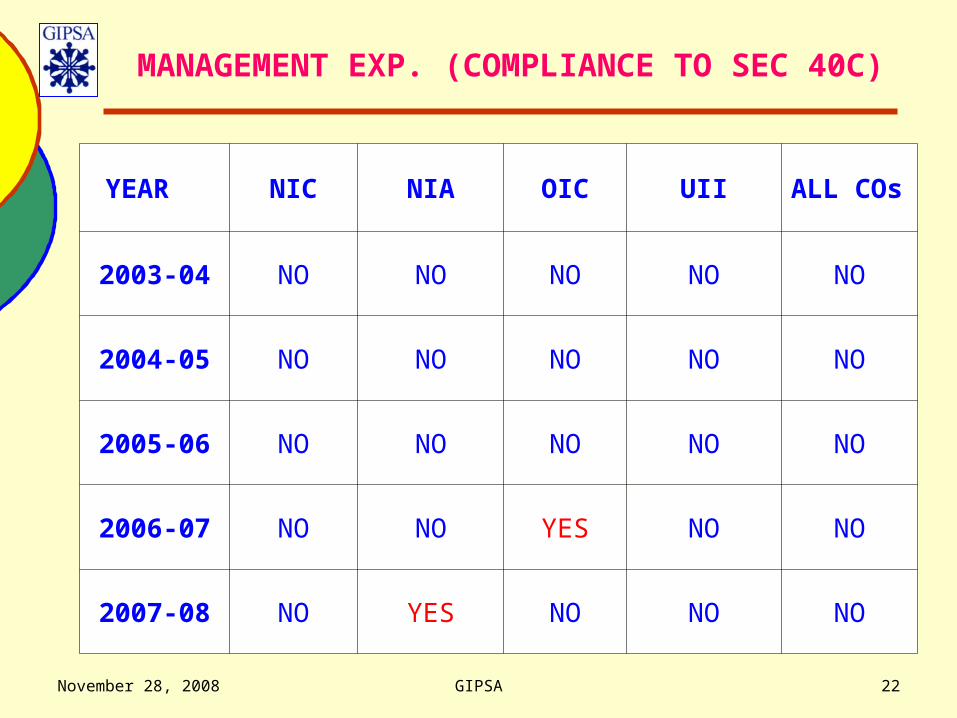

MANAGEMENT EXP. (COMPLIANCE TO SEC 40C)

YEAR NIC NIA OIC UII ALL COs

2003-04 NO NO NO NO NO

2004-05 NO NO NO NO NO

2005-06 NO NO NO NO NO

2006-07 NO NO YES NO NO

2007-08 NO YES NO NO NO

November 28, 2008 GIPSA 23

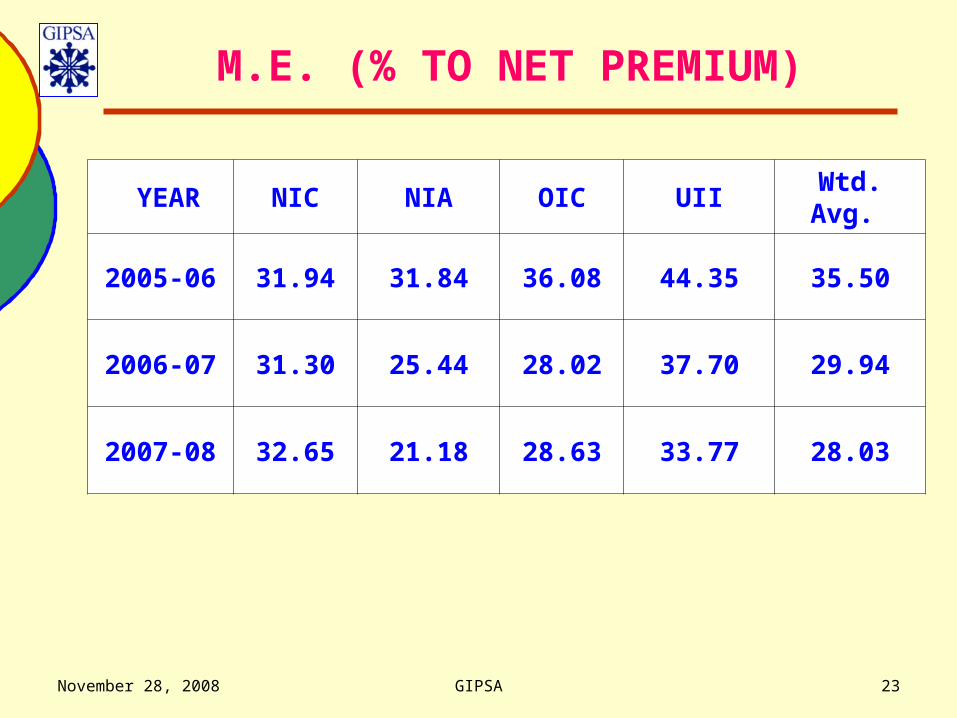

M.E. (% TO NET PREMIUM)

YEAR NIC NIA OIC UII Wtd. Avg.

2005-06 31.94 31.84 36.08 44.35 35.50

2006-07 31.30 25.44 28.02 37.70 29.94

2007-08 32.65 21.18 28.63 33.77 28.03

November 28, 2008 GIPSA 24

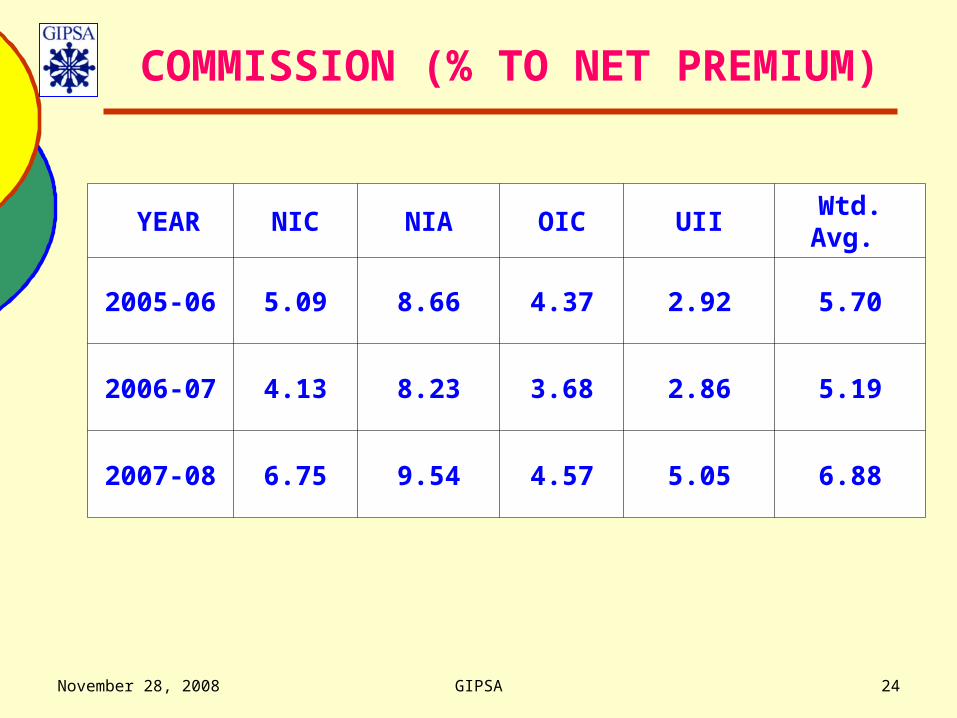

COMMISSION (% TO NET PREMIUM)

YEAR NIC NIA OIC UII Wtd. Avg.

2005-06 5.09 8.66 4.37 2.92 5.70

2006-07 4.13 8.23 3.68 2.86 5.19

2007-08 6.75 9.54 4.57 5.05 6.88

November 28, 2008 GIPSA 25

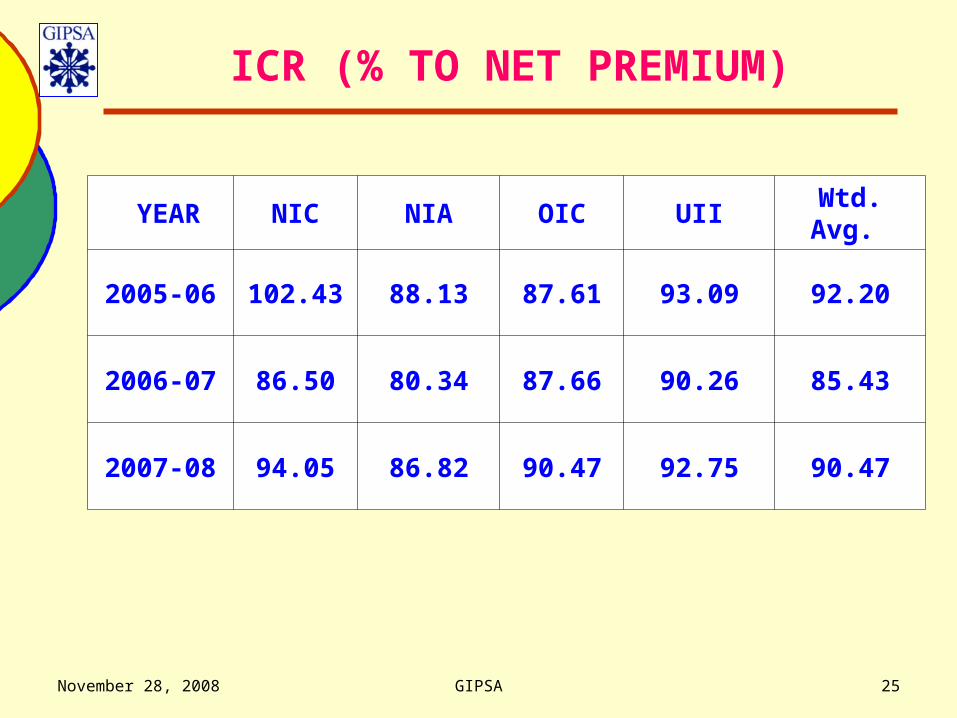

ICR (% TO NET PREMIUM)

YEAR NIC NIA OIC UII Wtd. Avg.

2005-06 102.43 88.13 87.61 93.09 92.20

2006-07 86.50 80.34 87.66 90.26 85.43

2007-08 94.05 86.82 90.47 92.75 90.47

November 28, 2008 GIPSA 26

COMBINED RATIO* (% TO NET PREMIUM)

YEAR NIC NIA OIC UII Wtd. Avg.

2005-06 139.46 128.63 128.06 140.36 123.41

2006-07 121.93 114.01 119.36 130.81 120.55

2007-08 133.45 120.00 123.67 131.58 126.24

*INCLUDES NET INCURRED CLAIMS, M.E. & COMM.

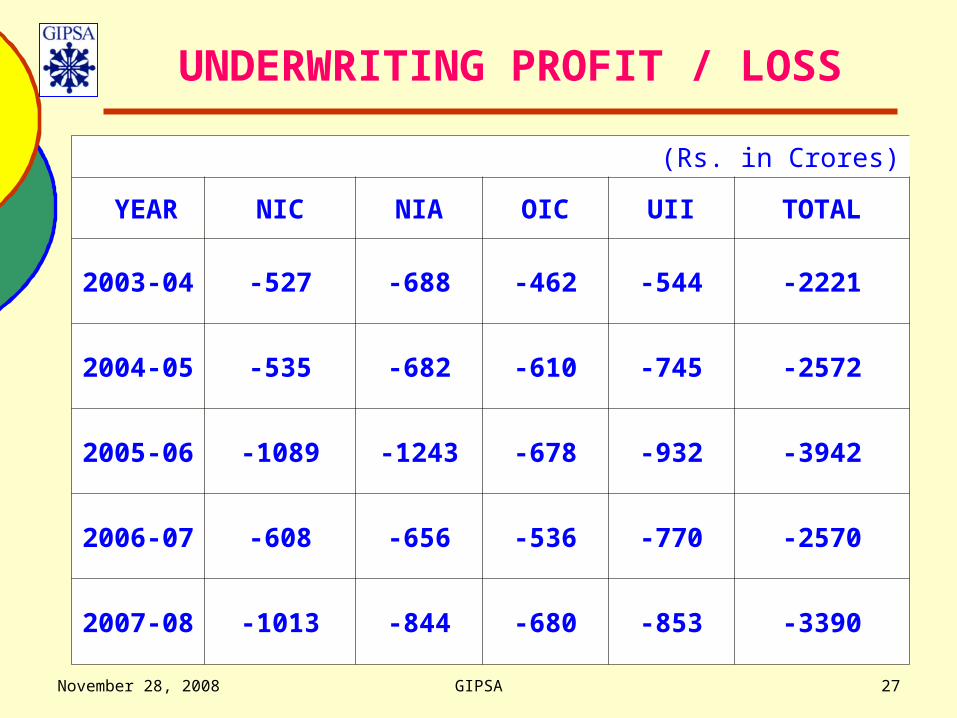

November 28, 2008 GIPSA 27

UNDERWRITING PROFIT / LOSS

(Rs. in Crores)

YEAR NIC NIA OIC UII TOTAL

2003-04 -527 -688 -462 -544 -2221

2004-05 -535 -682 -610 -745 -2572

2005-06 -1089 -1243 -678 -932 -3942

2006-07 -608 -656 -536 -770 -2570

2007-08 -1013 -844 -680 -853 -3390

November 28, 2008 GIPSA 28

ESTIMATED WAGE BILL AS ON 31.07.2007*

(Rs. Crores)

NIC NIA OIC UII ALL Cos.

641.41 774.26 560.89 720.85 2697.41

*Extrapolated on the basis of expenses as on 31st March, 2007 & 2008

November 28, 2008 GIPSA 29

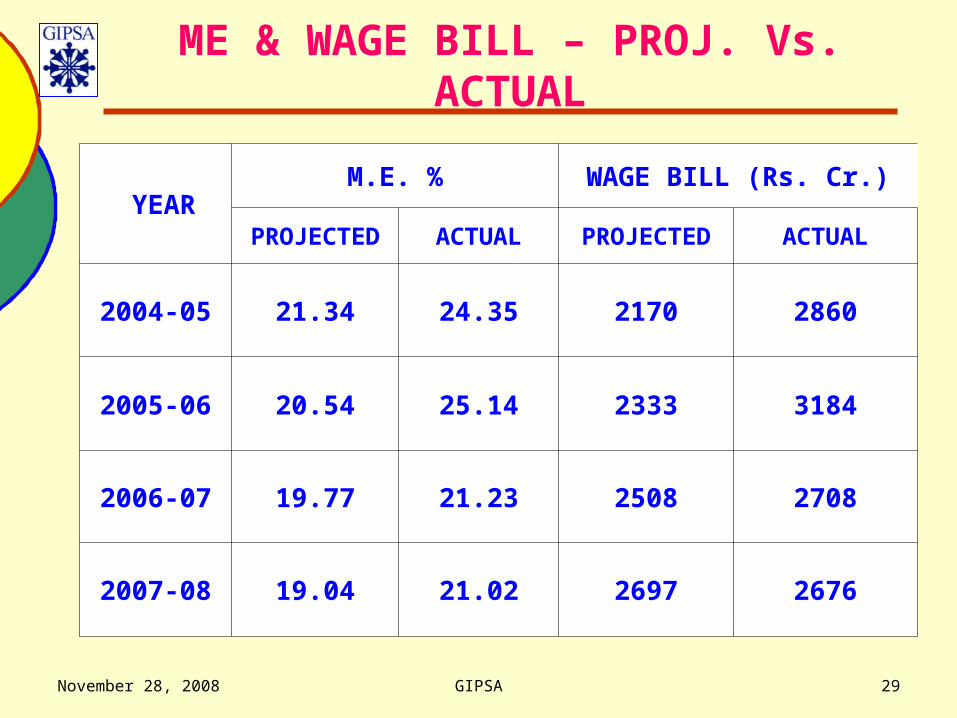

ME & WAGE BILL – PROJ. Vs. ACTUAL

YEARM.E. % WAGE BILL (Rs. Cr.)

PROJECTED ACTUAL PROJECTED ACTUAL

2004-05 21.34 24.35 2170 2860

2005-06 20.54 25.14 2333 3184

2006-07 19.77 21.23 2508 2708

2007-08 19.04 21.02 2697 2676

November 28, 2008 GIPSA 30

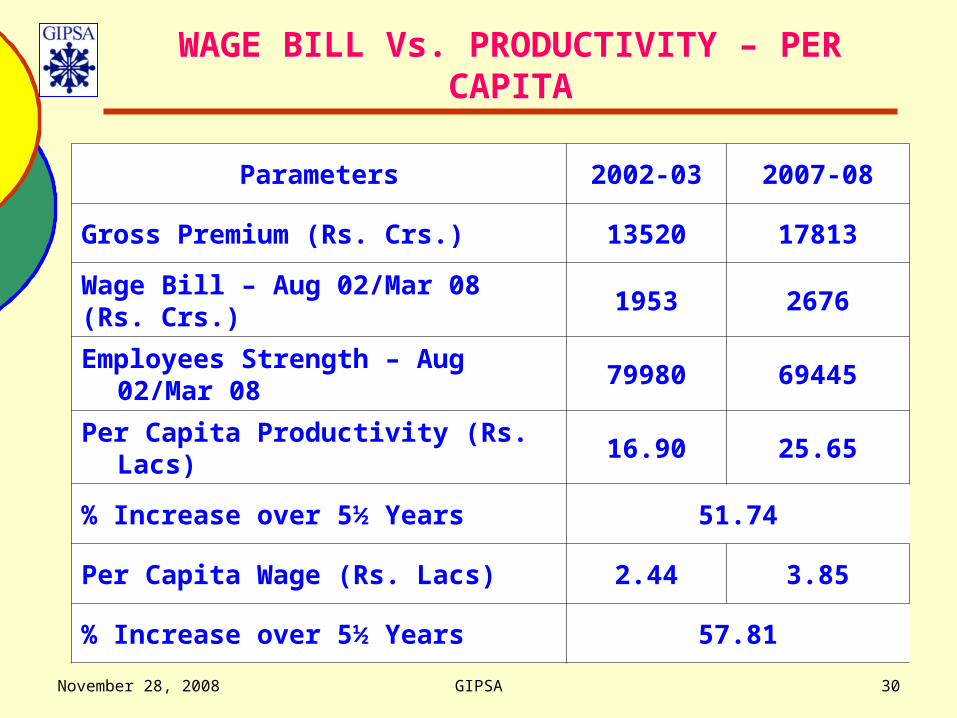

WAGE BILL Vs. PRODUCTIVITY – PER CAPITA

Parameters 2002-03 2007-08

Gross Premium (Rs. Crs.) 13520 17813

Wage Bill – Aug 02/Mar 08 (Rs. Crs.) 1953 2676

Employees Strength – Aug 02/Mar 08 79980 69445

Per Capita Productivity (Rs. Lacs) 16.90 25.65

% Increase over 5½ Years 51.74

Per Capita Wage (Rs. Lacs) 2.44 3.85

% Increase over 5½ Years 57.81

November 28, 2008 GIPSA 31

CUSTOMER SERVICE INDICES (%)

NIC NIA OIC UII

Suit Claim Ratio

Avg. - last 3 yrs 25.40 28.23 25.99 24.89

Actual 2007-08 27.09 27.00 23.87 29.50

Target 2008-09 35.00 35.00 35.00 35.00

Non Suit Claim Ratio

Avg. - last 3 yrs 81.96 89.90 86.95 85.53

Actual 2007-08 83.85 90.00 88.67 87.60

Target 2008-09 90.00 95.00 90.00 90.00

Grievance Redressal

Avg. - last 3 yrs 87.48 82.33 90.91 73.21

Actual 2007-08 83.29 83.00 96.16 81.04

Target 2008-09 88.00 90.00 95.00 85.00

November 28, 2008 GIPSA 32

CHALLENGES AHEAD

EXTERNAL CHALLENGES

INTERNAL CHALLENGES

November 28, 2008 GIPSA 33

EXTERNAL CHALLENGES

Intense Competition on more profitable lines of Business.

Premium rates to remain under pressure in De-tariffed regime.

Business acquisition cost continue to rise.

Re-insurance cost also continue to rise due to reduction in ceding commission by Treaty Re-insurers to compensate for lower rates in de-tariffed regime.

November 28, 2008 GIPSA 34

Contd………

Shadow of global recession looming large on Indian Industry and Economy

Capital Markets meltdown reduces reliance on investment portfolio for net profit

Changing customer profile and increasing customer expectations

New emerging risks and need for continuous innovations

November 28, 2008 GIPSA 35

INTERNAL CHALLENGES

Statutory limits on ME Ratios – Sec. 40 C

Every rise in Wage Bill demands corresponding rise in productivity

Rigidity in pay package impedes retention of talent - need for flexi pay / differential pay package

Skill gap in the manpower flowing from fast changing technologies

November 28, 2008 GIPSA 36

Contd…………..

Adverse age profile of manpower – climate of inertia and rigidity

Imbalances in deployment of manpower – continued pockets of surplus / deficit despite structured TMP – widen TMP or more flexible TMP?

Continuous losses in Motor TP, Health etc. – Loss Management and Minimization

Attitudinal issues of manpower at various levels – commitment vs. alienation

November 28, 2008 GIPSA 37

GAP BETWEEN “HAVE” & “WANT TO HAVE” - 1

(Rs. in Crores)

ACTUAL PROJECTIONS

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Gross Prem ↑ @ 5.68% p.a.

17813 18825 19894 21024 22218 23480

M. Exp (w/o WR) ↑ @ 9.1% p.a.

3744 4085 4456 4862 5304 5787

ME % 21.02 21.70 22.40 23.13 23.87 24.65

Addition to ME with 5% WR w.e.f. 01.08.2007

93 153 167 182 199 217

Total ME 3837 4238 4624 5044 5503 6004

ME (% to GP) 21.54 22.51 23.24 23.99 24.77 25.57

For 19.50% ME, Required Gross Prem. (@11.5 GR) - 21733 23710 25868 28222 30790

Premium Gap - -2908 -3816 -4844 -6004 -7310

November 28, 2008 GIPSA 38

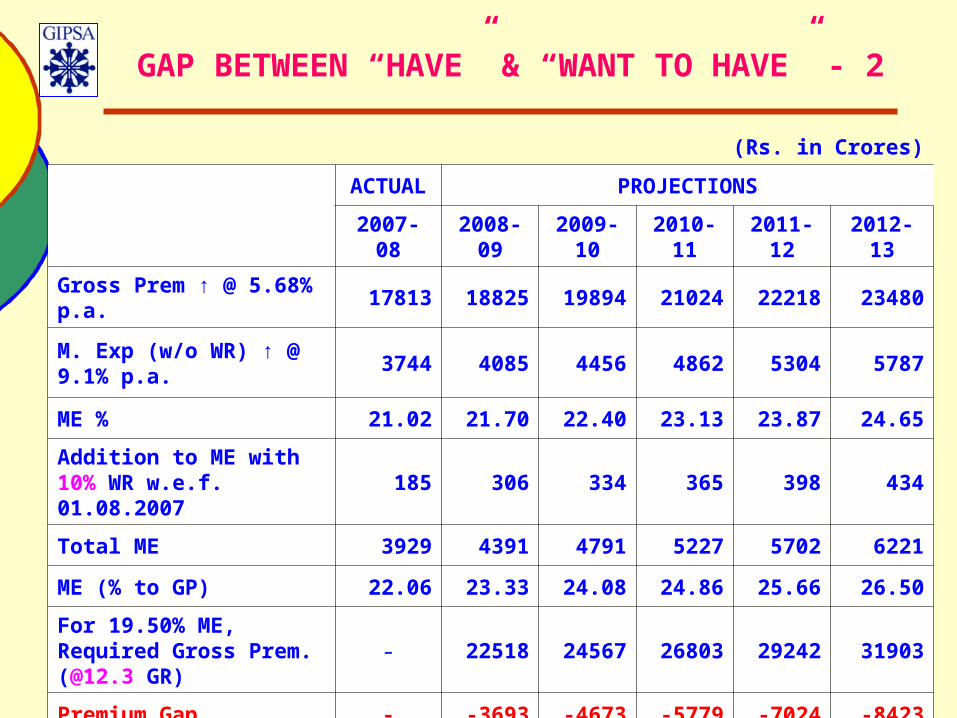

GAP BETWEEN “HAVE” & “WANT TO HAVE” - 2

(Rs. in Crores)

ACTUAL PROJECTIONS

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Gross Prem ↑ @ 5.68% p.a.

17813 18825 19894 21024 22218 23480

M. Exp (w/o WR) ↑ @ 9.1% p.a.

3744 4085 4456 4862 5304 5787

ME % 21.02 21.70 22.40 23.13 23.87 24.65

Addition to ME with 10% WR w.e.f. 01.08.2007

185 306 334 365 398 434

Total ME 3929 4391 4791 5227 5702 6221

ME (% to GP) 22.06 23.33 24.08 24.86 25.66 26.50

For 19.50% ME, Required Gross Prem. (@12.3 GR) - 22518 24567 26803 29242 31903

Premium Gap - -3693 -4673 -5779 -7024 -8423

November 28, 2008 GIPSA 39

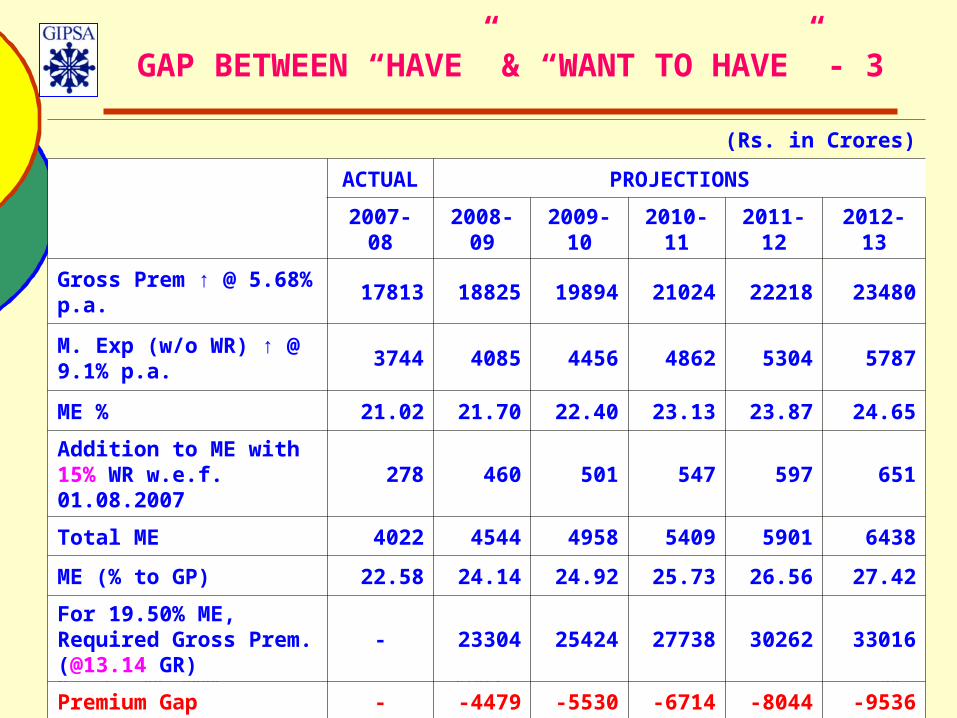

GAP BETWEEN “HAVE” & “WANT TO HAVE” - 3

(Rs. in Crores)

ACTUAL PROJECTIONS

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Gross Prem ↑ @ 5.68% p.a.

17813 18825 19894 21024 22218 23480

M. Exp (w/o WR) ↑ @ 9.1% p.a.

3744 4085 4456 4862 5304 5787

ME % 21.02 21.70 22.40 23.13 23.87 24.65

Addition to ME with 15% WR w.e.f. 01.08.2007

278 460 501 547 597 651

Total ME 4022 4544 4958 5409 5901 6438

ME (% to GP) 22.58 24.14 24.92 25.73 26.56 27.42

For 19.50% ME, Required Gross Prem. (@13.14 GR)

- 23304 25424 27738 30262 33016

Premium Gap - -4479 -5530 -6714 -8044 -9536

November 28, 2008 GIPSA 40

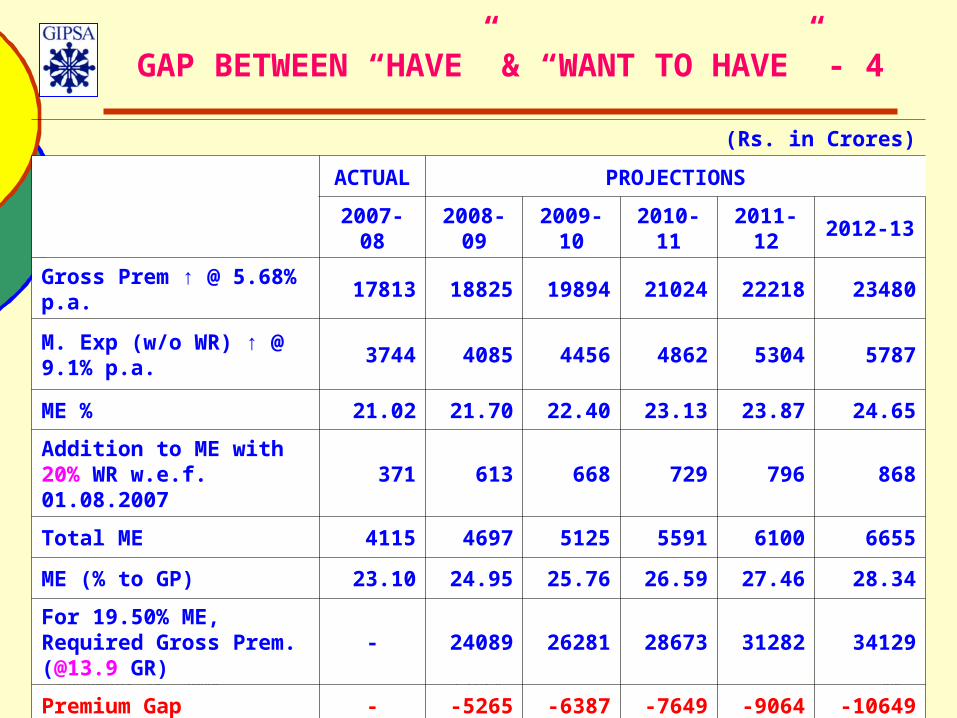

GAP BETWEEN “HAVE” & “WANT TO HAVE” - 4

(Rs. in Crores)

ACTUAL PROJECTIONS

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Gross Prem ↑ @ 5.68% p.a.

17813 18825 19894 21024 22218 23480

M. Exp (w/o WR) ↑ @ 9.1% p.a.

3744 4085 4456 4862 5304 5787

ME % 21.02 21.70 22.40 23.13 23.87 24.65

Addition to ME with 20% WR w.e.f. 01.08.2007

371 613 668 729 796 868

Total ME 4115 4697 5125 5591 6100 6655

ME (% to GP) 23.10 24.95 25.76 26.59 27.46 28.34

For 19.50% ME, Required Gross Prem. (@13.9 GR)

- 24089 26281 28673 31282 34129

Premium Gap - -5265 -6387 -7649 -9064 -10649

November 28, 2008 GIPSA 41

HOPES

BPR initiatives expected to boost up productivity and rationalize expenses besides improving Customer Care.

Active co-operation from Employees and their Unions / Associations required to supplement these efforts.

An Organizational Agenda common to the Management and the Unions / Associations required for coordinated efforts and synergy.

Let us evolve such an Agenda.