Embed Size (px)

Citation preview

ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES ARE IN THE DISCLOSURE APPENDIX. FOR OTHER

IMPORTANT DISCLOSURES, PLEASE REFER TO https://firesearchdisclosure.credit-suisse.com.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

November Manufacturing PMI Roundup

Welcome, but Somewhat Puzzling Strength

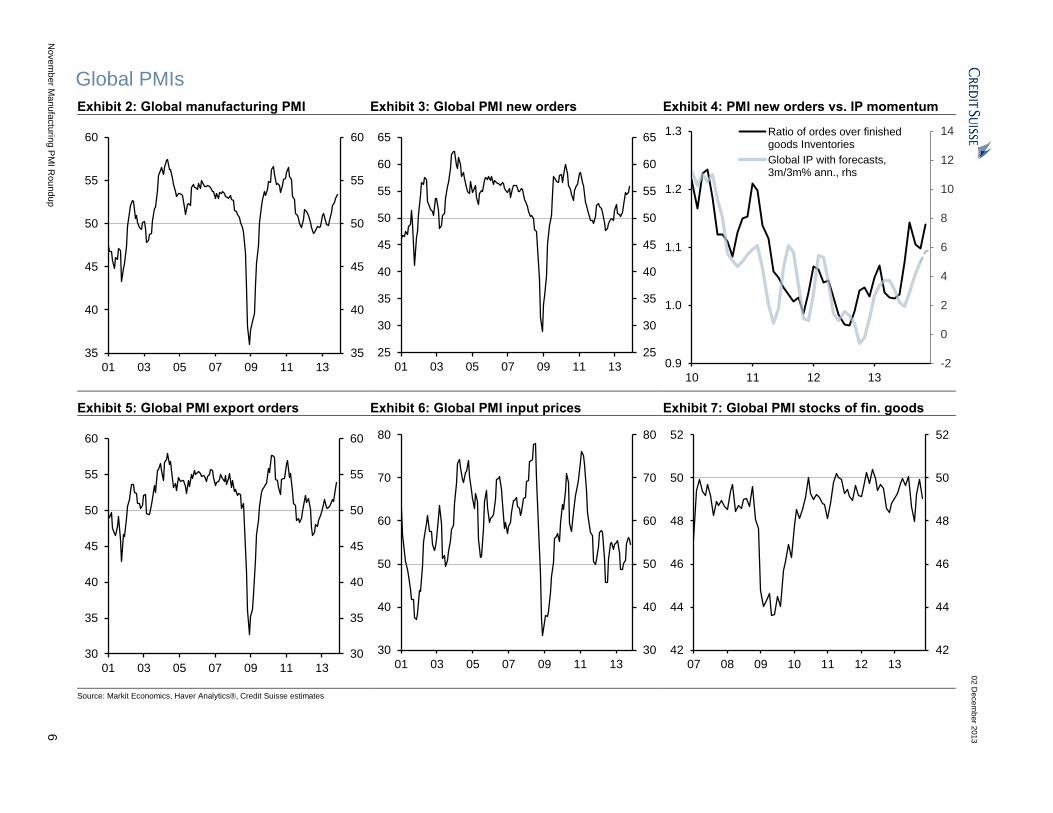

The global manufacturing PMI increased further for the sixth consecutive

month in November to 53.4 from 53.01. The index reached its highest level

since May 2011 and is running above its long-term average of 51.5. This is

consistent with our view that the pace of global industrial activity is running

above trend.

The monthly advance was mainly driven by developed markets – especially the

US and Japan – but emerging markets have also contributed positively to the

monthly rise. This is encouraging, but one of the puzzles inasmuch as global

trade has been lackluster over the last two years.

The new orders component of the survey confirmed the rebound observed in

October, while the stocks of finished goods fell on the month. Such a mix is

generally indicative of a positive production outlook in the short term. We

would note, though, that our latest CS Basic Materials Index (CSBMI) (Cruising

Along) is pointing to a softening in industrial activity in the coming months. This

is another puzzle.

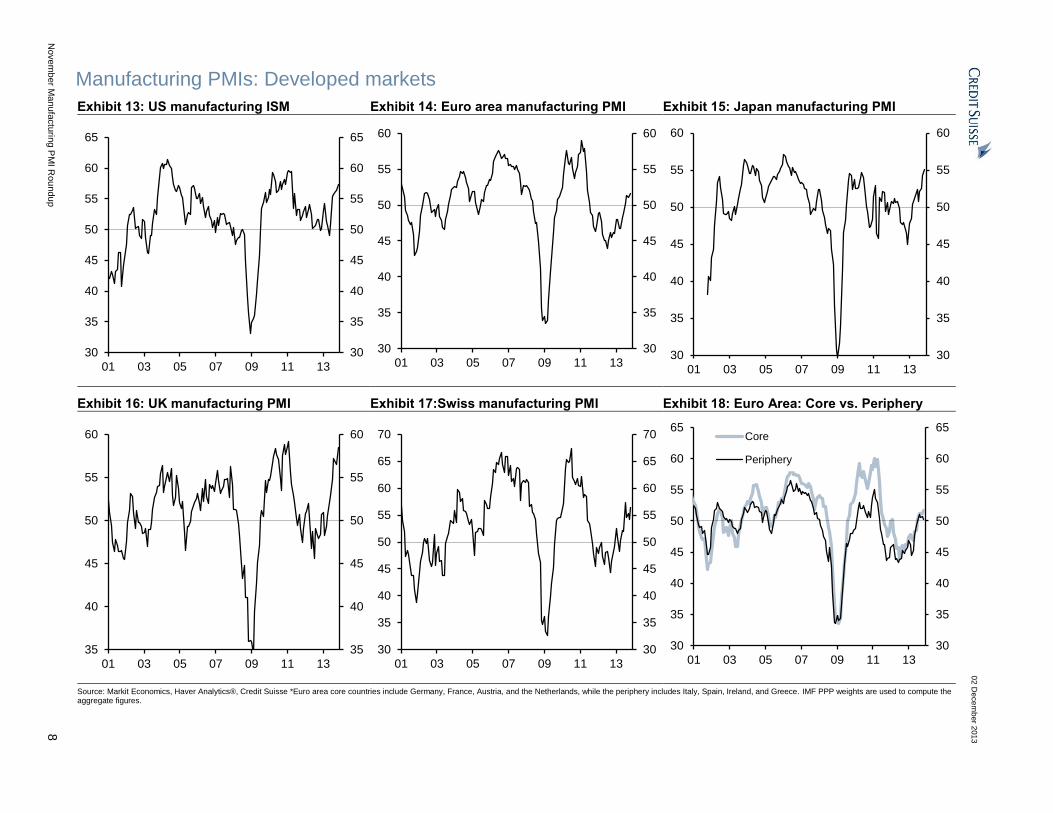

In the US, November ISM manufacturing registered its sixth consecutive

increase, rising 0.9 points to 57.3, the highest level since April 2011. New

orders, the leading indicator, rose a robust 3.0 points to 63.6, recording a notable

fourth consecutive print above 60. The new orders-inventory spread widened to

13.1 after narrowing over the previous two months. This may suggest the recent

strong inventory gains in both hard data and the survey data have not resulted in

an “oversupply” condition. Consistent with that story, the ISM customer inventory

index declined on the month, to a subdued level of 45.0. Additionally, stronger

foreign demand was manifest in the report. New Export Orders notched another

impressive increase; the November index printed at 59.5, among the better levels

of the current expansion. Foreign demand appears to be a key driver behind the

firmer readings in overall new orders.

A conspicuous gap has opened up between the ISM and hard data on US

industrial production and durable goods. The puzzle isn’t readily explained, but

we would note ISM has had a stronger relationship with global measures

of activity than US measures of activity in recent years. This may be part of

the story. Recent ISM strength may be more indicative of a global rebound than

a specific US rebound.

The euro area PMI has continued to hover around a level consistent with

sluggish growth for the fourth consecutive month. After a compelling

improvement observed last Spring, current dynamics are consistent with our

view that the pace of the recovery should be modest. Despite certain

normalization in economic conditions, a number of negative factors appear to be

keeping the Eurozone’s growth prospects constrained in coming months. In

details, the November manufacturing PMI increased slightly to 51.6 from 51.3,

the highest level reached since June 2011. The output component rose a touch

1 Please refer to the Technical Note on page 4 on the methodology used in constructing our global manufacturing PMIs.

Research Analysts

Neal Soss

+1 212 325 3335

Axel Lang

+44 20 7883 3738

Isaac Lebwohl

+1 212 538 1906

Natig Mustafayev

+44 20 7888 1065

02 December 2013

Economics Research

http://www.credit-suisse.com/researchandanalytics

02 December 2013

November Manufacturing PMI Roundup 2

to 53.1 from 52.9 and the new orders index was also up, to 52.3 from 51.9, mainly thanks

to a robust export market. On the other hand, the stock of finished goods has crept up

marginally higher while employment remains stuck at unsatisfactory levels.

At the country level, divergent dynamics are reappearing after several months of

synchronized improvement. In Germany, the index increased by one point to 52.7, its

highest level since June 2011. The output and new orders components, respectively, rose

to a healthy 54.9 and 54.5 (from 53.6 and 52.5) while inventories increased at a more

moderate pace. The French index fell to 48.4 from 49.1. The cyclical weakness of that

economy was again apparent in the PMI report, which has remained below the 50-line

since July 2011. The details of the survey were unpromising: new orders declined to 46.8

from 48.3, output fell to 48.0 from 49.0, and inventories rose slightly at 47.1 from 46.6.

Similarly, the Spanish PMI returned below the 50-line, falling by 2.5 points to 48.6, its

lowest level since May. Domestic new orders (-4.7 points) were the main drag this month

as Spain’s export market appears resilient at 53.7. Output consequently corrected

significantly by almost 3 points to 48.8. On the other hand, the Italian index showed signs

of resilience, increasing to 51.4 after 50.7 in October. The improvement was mainly due to

the employment index, which rose above 50 for the first time since May 2011. New orders

remained unchanged but new export orders rose solidly to a high 57.2, suggesting some

weakness stemming from domestic demand. Finally, the Greek PMI increased to 49.2

from 47.3, its highest level since August 2009, indicating that economic conditions are

stabilizing across all the sectors of the economy.

In the UK, the November PMI was solid, reaching 58.4, its highest level since February

2011. In addition, the new orders component was the highest since July 1994. The

employment index was also very strong, and new orders minus stocks of finished goods

(which we use as a cyclical indicator) was at levels indicating a solid expansion.

Japan’s PMI advanced further in November to 55.1 from 54.2, reaching the highest

level since July 2006. The move in the forward-looking new orders index was similarly

encouraging: new orders rose 1.7 points to 58.4, also a multiyear high. New export orders

were stronger in November, while the stock of finished goods fell slightly on the month.

Separately, industrial production rose just 0.5% mom in October after a 1.3% mom gain in

September. There seems relatively limited room for a major acceleration in the production

recovery in the winter. A fading-out of the boost from the yen’s depreciation, and a sign of

a local peak in Q4 hinted by the global leading indicator of the production cycle (CSBMI),

do not augur well for strong production increases in Japan in the coming months.

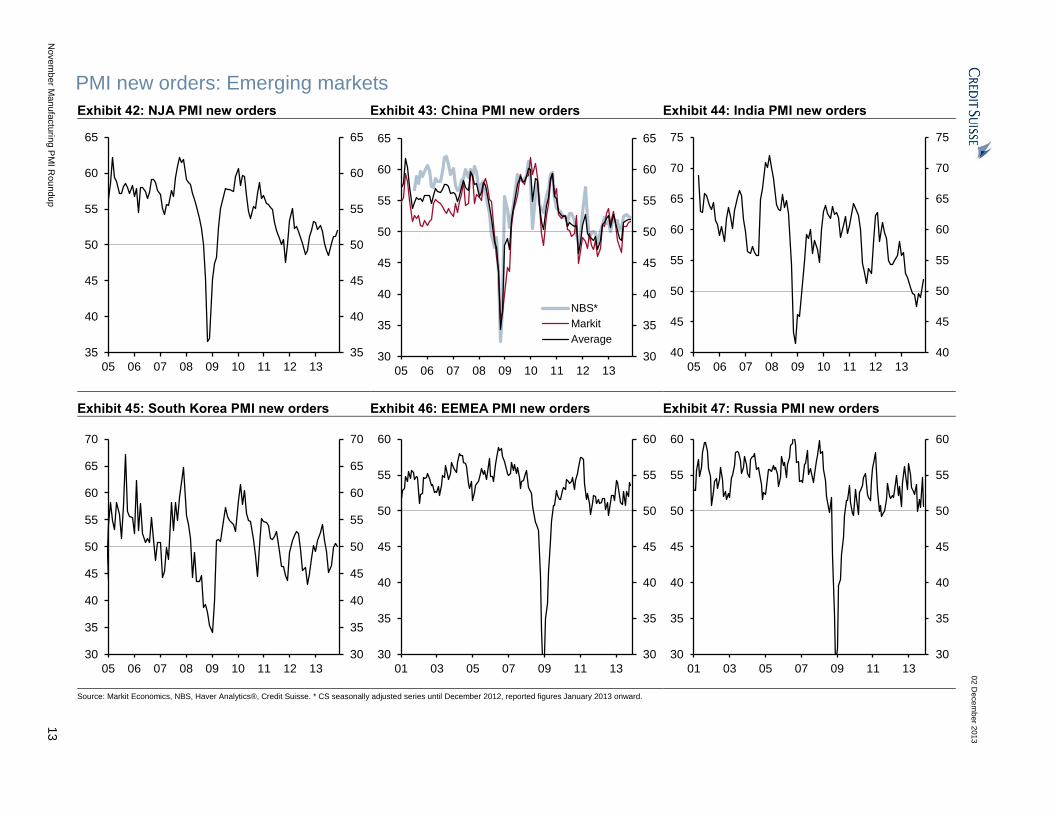

EM’s aggregate PMI increased further for the fourth consecutive month to an eight-

month high of 51.2 in November from 51.0 in October, driven by the pick-up in the

NJA and EEMEA (excluding Russia) regions. This result is in line with our VAR analysis

published in the report Pulse of Global Industry: Tentative Signs of a 4Q Peak in IP

Momentum (page 23) as the emerging markets have been benefiting from the pick-up in

economic activity in developed markets since 3Q 2013. It is worth highlighting that in

November, the manufacturing PMI declined only in Brazil and Russia, and remained

broadly unchanged in China.

In China, the official NBS PMI remained unchanged at 51.4 in November, while

Markit/HSBC PMI edged slightly lower. The official NBS PMI remained flat in November

at a 19-month high of 51.4 after increasing for four consecutive months from its recent

trough in June. Meanwhile, the Markit/HSBC PMI declined only marginally by 0.1 index-

points from a seven-month peak of 50.9 in October. According to our economists, both

indices confirm that the Chinese economy sustained its growth momentum in November

and the ongoing trend can be characterized as one of a weak expansion without a further

upward momentum (see China: NBS PMI showed sustained growth stabilisation).

The authors of this report wish to

acknowledge the contribution made

by Pawel Chmielniak, an employee

of CRISIL Global Research and

Analytics, a business division of

CRISIL Limited, a third-party

provider of research services to

Credit Suisse, in preparing the EM

section of this report.

02 December 2013

November Manufacturing PMI Roundup 3

In the rest of the NJA region, the manufacturing PMI improved in all countries of the

region with India recording the most notable increase in November. India’s

manufacturing PMI rebounded in recent months from a 54-month low of 48.5 in August to

an eight-month high of 51.3 in November. The sharp pick-up was mainly driven by output

and forward-looking new orders components, however, we should note that PMI still

remained relatively weak compared to an average of 53.0 in 1Q 2013. In Korea, the

manufacturing PMI increased slightly for the fourth consecutive month to 50.4 in

November from 50.2 in October, however, we note that new export orders declined

sharply from a 31-month high of 53.7 in October to 51.9 in November. Taiwan’s

manufacturing PMI remained elevated and picked up slightly from 53.0 to a 20-month high

of 53.4 in November, driven mainly by current output and new orders components.

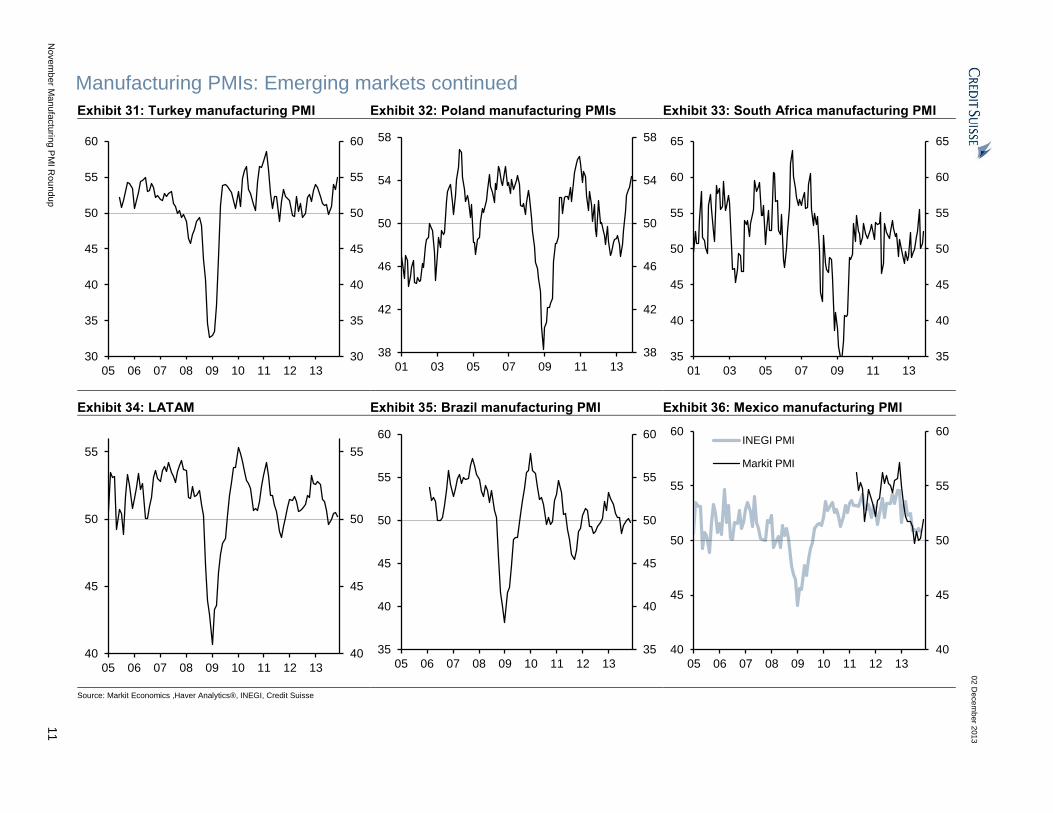

In Latin America, Brazil’s manufacturing PMI declined slightly from 50.2 in October to

49.7 in November. We note that 2H 2013 PMI readings in Brazil have been weaker

compared to 1H 2013. In Mexico, the manufacturing PMI improved significantly from 50.2

in October to an eight-month high of 51.9 in November, confirming that Mexico’s economy

has been recovering in recent months. Mexico’s November PMI by INEGI will be released

on 4 December.

The EEMEA region’s manufacturing PMI declined modestly to 52.0 in November

from a 30-month high of 52.4 in October, led by a sharp decline in Russia’s PMI

despite the pick-up in the rest of the region. The manufacturing PMI improved

modestly in CE3 countries and significantly in Turkey and South Africa. The forward-

looking PMI new orders index, however, was down by 0.5 points to 53.5 in November,

suggesting a more subdued pace of expansion in the coming months.

In Russia, the manufacturing PMI declined significantly from an eight-month high of 51.8,

back to 49.4 in November. The decrease was driven by broad-based deceleration of

almost all PMI components. This outturn confirms very weak economic activity in the

manufacturing sector despite stable oil prices, revival in economic activity among trading

partners and a weaker Rouble. Turkey’s manufacturing PMI improved to a 32-month high

of 55.0 in November from 53.3 in October, driven mainly by current output, new orders and

new export orders components. In South Africa, the Kagiso manufacturing PMI increased

from 50.7 in October to 52.4 in November, driven by acceleration in all PMI components.

In CE3 countries, the most notable pick-up was recorded in Hungary, as the manufacturing

PMI rebounded from a three-month low of 51.1 in October to 52.6 in November. Meanwhile,

Czech and Polish PMIs continued increasing and reached multi-year highs in November. In

Poland, the manufacturing PMI increased for the seventh consecutive month from 53.4 in

October to 54.4 in November, the highest reading since April 2011. We note the elevated

readings for both current output and new orders in Poland, as they increased to 56.9 and

57.2, respectively. The Czech Republic’s manufacturing PMI picked up to a 30-month high

of 55.4 in November from 54.5 a month earlier. The increase was driven by output, new

orders and new export orders components. We maintain our view that the pickup in

manufacturing activity in CE3 countries is driven by a rebound in Germany, which is likely to

continue in the coming months, as Germany’s Ifo expectations indicator picked up sharply in

November after moderating modestly in October.

Overall, November PMI reports are consistent with our expectation of a continued

rebound in global IP growth toward the end of this year. However, we expect global IP

growth to plateau in Q1 2014 following the strong pick-up in H2 2013. This is further

confirmed by our Basic Material Indicator (CSBMI), which reached a local peak in

September. The CSBMI generally leads IP growth dynamics by about two months. Our

current expectation is for the IP to slow toward its trend growth rate by next spring before

picking up again in the summer (see our November 25 report Pulse of Global Industry:

Cruising Along).

02 December 2013

November Manufacturing PMI Roundup 4

Technical Note

We report global aggregates based on our own calculation. The main differences between

the calculation of our global aggregates and those reported by Markit Economics include

the following:

1) We use the US ISM Manufacturing Index and the average of the China official NBS

(Credit Suisse adjusted) and the HSBC/Markit PMI surveys in our calculation, while

Markit Economics includes the US Markit PMI and China HSBC/Markit surveys.

The US ISM has more than a 55-year track record, while the Markit PMI data dates only

from May 2007. We may need a bit more time to assess the reliability of Markit PMIs. At this

stage, it seems sensible to include ISM in computing aggregate global and regional PMIs.

The China NBS PMI headline, new orders, and export orders indices retain residual

seasonality. We seasonally adjust the NSA PMIs using the PBoC’s bespoke X12

package until December 2012. Since January 2013, the NBS survey sample size has

increased significantly from 820 to 3,000, which raises the question of how comparable

the new readings are with the historical data before the change. For this reason, we

have not seasonally adjusted the NSA NBS PMIs after the sample increase, but use

the reported figures directly. In addition, the NBS PMI is focused more on large

companies and SOEs, but the Markit survey is more focused on small- and medium-

sized companies and private businesses. By using the average of these two surveys,

our approach should provide a proxy in capturing the bigger picture.

2) Rolling IMF PPP weights are used to compute our regional and global figures, while

fixed GDP shares in 2010 are used in calculating Markit’s global aggregates. We think

PPP weights are more appropriate for computing aggregate manufacturing PMI. For

example, China industrial production in dollar terms accounted for about 18% of global

industrial production in 2011. Fixed GDP shares in 2010 give China about a 7.9%

weight, while rolling PPP weights assign a 14% weight to China.

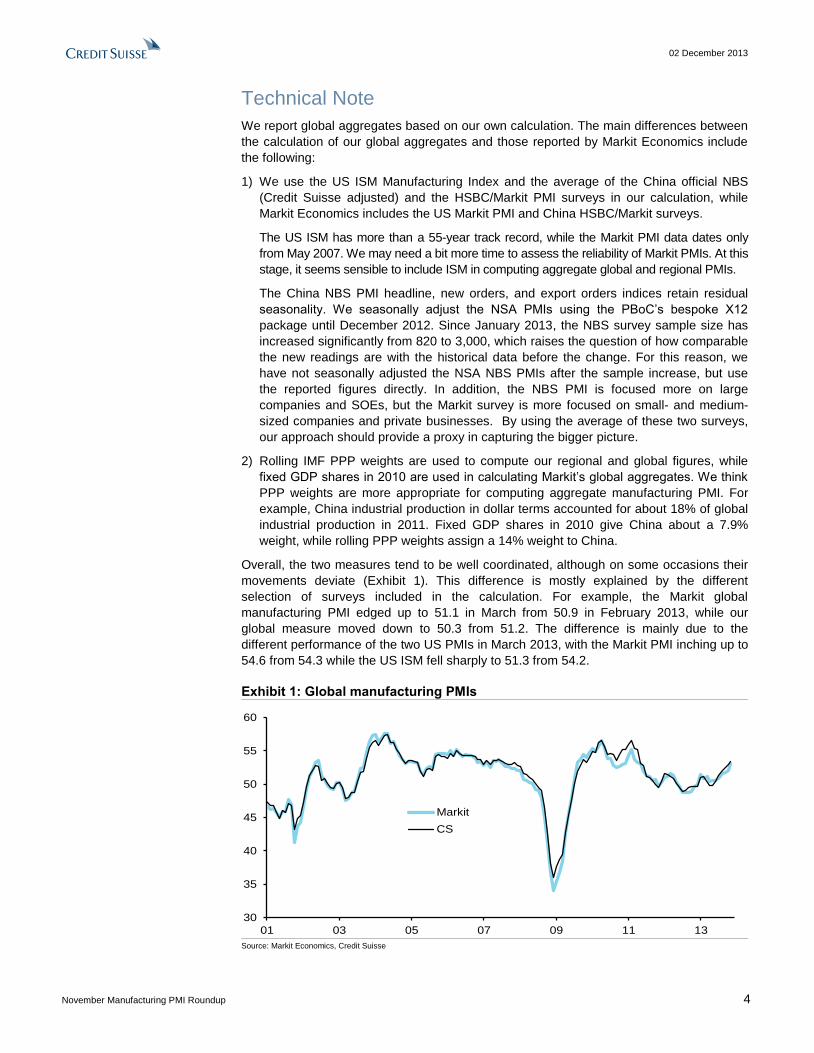

Overall, the two measures tend to be well coordinated, although on some occasions their

movements deviate (Exhibit 1). This difference is mostly explained by the different

selection of surveys included in the calculation. For example, the Markit global

manufacturing PMI edged up to 51.1 in March from 50.9 in February 2013, while our

global measure moved down to 50.3 from 51.2. The difference is mainly due to the

different performance of the two US PMIs in March 2013, with the Markit PMI inching up to

54.6 from 54.3 while the US ISM fell sharply to 51.3 from 54.2.

Exhibit 1: Global manufacturing PMIs

30

35

40

45

50

55

60

01 03 05 07 09 11 13

Markit

CS

Source: Markit Economics, Credit Suisse

02 December 2013

November Manufacturing PMI Roundup 5

Table of Contents

Technical Note 4

Global PMIs 6

DM/EM PMIs 7

Manufacturing PMIs: Developed markets 8

Manufacturing PMIs: Developed markets continued 9

Manufacturing PMIs: Emerging markets 10

Manufacturing PMIs: Emerging markets continued 11

PMI new orders: Developed markets 12

PMI new orders: Emerging markets 13

PMI new orders: Emerging markets continued 14

PMI export orders: Developed markets 15

PMI export orders: Emerging markets 16

PMI export orders: Emerging markets continued 17

PMI inventories: Developed markets 18

PMI inventories: Emerging markets 19

PMI inventories: Emerging markets continued 20

PMI input prices: Developed markets 21

PMI input prices: Emerging markets 22

PMI input prices: Emerging markets continued 23

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

6

Global PMIs

Exhibit 2: Global manufacturing PMI Exhibit 3: Global PMI new orders Exhibit 4: PMI new orders vs. IP momentum

35

40

45

50

55

60

35

40

45

50

55

60

01 03 05 07 09 11 13

25

30

35

40

45

50

55

60

65

25

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

-2

0

2

4

6

8

10

12

14

0.9

1.0

1.1

1.2

1.3

10 11 12 13

Ratio of ordes over finishedgoods Inventories

Global IP with forecasts,3m/3m% ann., rhs

Exhibit 5: Global PMI export orders Exhibit 6: Global PMI input prices Exhibit 7: Global PMI stocks of fin. goods

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

30

40

50

60

70

80

30

40

50

60

70

80

01 03 05 07 09 11 13

42

44

46

48

50

52

42

44

46

48

50

52

07 08 09 10 11 12 13

Source: Markit Economics, Haver Analytics®, Credit Suisse estimates

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

7

DM/EM PMIs

Exhibit 8: DM/EM Manufacturing PMIs Exhibit 9: DM/EM PMI new orders Exhibit 10: DM/EM PMI export orders

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

EM DM

25

30

35

40

45

50

55

60

65

25

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

EM DM

30

35

40

45

50

55

60

65

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

EM DM

Exhibit 11: DM/EM PMI input prices Exhibit 12: DM/EM PMI stocks of fin. goods

25

30

35

40

45

50

55

60

65

70

75

80

85

25

30

35

40

45

50

55

60

65

70

75

80

85

01 03 05 07 09 11 13

EM DM

40

42

44

46

48

50

52

54

40

42

44

46

48

50

52

54

06 07 08 09 10 11 12 13 14

EM DM

Source: Markit Economics, NBS, CLIC, Haver Analytics®, INEGI, Credit Suisse * DM includes Australia, Canada, Denmark, Euro Area, Japan, New Zealand, Switzerland, the UK, and the US. EM includes China (CS SA PMI), India, Singapore, Korea, Taiwan, Czech Republic, Hungary, Poland, Russia, South Africa, Turkey, Mexico (INEGI PMI), and Brazil. IMF PPP weights are used to compute regional aggregate figures.

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

8

Manufacturing PMIs: Developed markets

Exhibit 13: US manufacturing ISM Exhibit 14: Euro area manufacturing PMI Exhibit 15: Japan manufacturing PMI

30

35

40

45

50

55

60

65

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

Exhibit 16: UK manufacturing PMI Exhibit 17:Swiss manufacturing PMI Exhibit 18: Euro Area: Core vs. Periphery

35

40

45

50

55

60

35

40

45

50

55

60

01 03 05 07 09 11 13

30

35

40

45

50

55

60

65

70

30

35

40

45

50

55

60

65

70

01 03 05 07 09 11 13

30

35

40

45

50

55

60

65

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

Core

Periphery

Source: Markit Economics, Haver Analytics®, Credit Suisse *Euro area core countries include Germany, France, Austria, and the Netherlands, while the periphery includes Italy, Spain, Ireland, and Greece. IMF PPP weights are used to compute the aggregate figures.

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

9

Manufacturing PMIs: Developed markets continued Exhibit 19: Germany manufacturing PMI Exhibit 20: France manufacturing PMI Exhibit 21: Italy manufacturing PMI

30

35

40

45

50

55

60

65

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

Exhibit 22: Spain manufacturing PMI Exhibit 23: Ireland manufacturing PMI Exhibit 24: Greece manufacturing PMI

25

30

35

40

45

50

55

60

25

30

35

40

45

50

55

60

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

35

40

45

50

55

60

35

40

45

50

55

60

01 03 05 07 09 11 13

Source: Markit Economics, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

10

Manufacturing PMIs: Emerging markets

Exhibit 25: NJA manufacturing PMI Exhibit 26: China manufacturing PMIs Exhibit 27: India manufacturing PMI

40

45

50

55

60

40

45

50

55

60

05 06 07 08 09 10 11 12 13

35

40

45

50

55

60

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

NBS*

Markit

Average

44

46

48

50

52

54

56

58

60

62

44

46

48

50

52

54

56

58

60

62

05 06 07 08 09 10 11 12 13

Exhibit 28: South Korea manufacturing PMI Exhibit 29: EEMEA manufacturing PMI Exhibit 30: Russia manufacturing PMI

38

42

46

50

54

58

62

38

42

46

50

54

58

62

05 06 07 08 09 10 11 12 13

35

40

45

50

55

60

35

40

45

50

55

60

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

Source: Markit Economics, NBS, Haver Analytics®, Credit Suisse . * CS seasonally adjusted series until December 2012, reported figures January 2013 onward.

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

11

Manufacturing PMIs: Emerging markets continued

Exhibit 31: Turkey manufacturing PMI Exhibit 32: Poland manufacturing PMIs Exhibit 33: South Africa manufacturing PMI

30

35

40

45

50

55

60

30

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

38

42

46

50

54

58

38

42

46

50

54

58

01 03 05 07 09 11 13

35

40

45

50

55

60

65

35

40

45

50

55

60

65

01 03 05 07 09 11 13

Exhibit 34: LATAM Exhibit 35: Brazil manufacturing PMI Exhibit 36: Mexico manufacturing PMI

40

45

50

55

40

45

50

55

05 06 07 08 09 10 11 12 13

35

40

45

50

55

60

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

40

45

50

55

60

40

45

50

55

60

05 06 07 08 09 10 11 12 13

INEGI PMI

Markit PMI

Source: Markit Economics ,Haver Analytics®, INEGI, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

12

PMI new orders: Developed markets

Exhibit 37: US ISM new orders Exhibit 38: Euro area PMI new orders Exhibit 39: Japan PMI new orders

20

30

40

50

60

70

20

30

40

50

60

70

01 03 05 07 09 11 13

25

30

35

40

45

50

55

60

65

25

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

15

20

25

30

35

40

45

50

55

60

65

15

20

25

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

Exhibit 40: Germany PMI new orders Exhibit 41: UK PMI new orders

20

30

40

50

60

20

30

40

50

60

01 03 05 07 09 11 13

30

35

40

45

50

55

60

65

30

35

40

45

50

55

60

65

01 03 05 07 09 11 13

Source: Markit Economics, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

13

PMI new orders: Emerging markets

Exhibit 42: NJA PMI new orders Exhibit 43: China PMI new orders Exhibit 44: India PMI new orders

35

40

45

50

55

60

65

35

40

45

50

55

60

65

05 06 07 08 09 10 11 12 13

30

35

40

45

50

55

60

65

30

35

40

45

50

55

60

65

05 06 07 08 09 10 11 12 13

NBS*

Markit

Average

40

45

50

55

60

65

70

75

40

45

50

55

60

65

70

75

05 06 07 08 09 10 11 12 13

Exhibit 45: South Korea PMI new orders Exhibit 46: EEMEA PMI new orders Exhibit 47: Russia PMI new orders

30

35

40

45

50

55

60

65

70

30

35

40

45

50

55

60

65

70

05 06 07 08 09 10 11 12 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

Source: Markit Economics, NBS, Haver Analytics®, Credit Suisse. * CS seasonally adjusted series until December 2012, reported figures January 2013 onward.

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

14

PMI new orders: Emerging markets continued

Exhibit 48: Turkey PMI new orders Exhibit 49: Poland PMI new orders Exhibit 50: South Africa PMI new orders

20

30

40

50

60

20

30

40

50

60

05 06 07 08 09 10 11 12 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

30

40

50

60

70

30

40

50

60

70

01 03 05 07 09 11 13

Exhibit 51: LATAM PMI new orders Exhibit 52: Brazil PMI new orders Exhibit 53: Mexico new orders

35

40

45

50

55

60

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

42

46

50

54

58

62

42

46

50

54

58

62

05 06 07 08 09 10 11 12 13

INEGI PMI

Markit PMI

Source: Markit Economics, NBS, CLIC, INEGI, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

15

PMI export orders: Developed markets

Exhibit 54: US ISM export orders Exhibit 55: Euro area PMI export orders Exhibit 56: Japan PMI export orders

35

40

45

50

55

60

65

35

40

45

50

55

60

65

01 03 05 07 09 11 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

20

30

40

50

60

20

30

40

50

60

01 03 05 07 09 11 13

Exhibit 57: Germany PMI export orders Exhibit 58: UK PMI export orders

20

30

40

50

60

20

30

40

50

60

01 03 05 07 09 11 13

35

40

45

50

55

60

35

40

45

50

55

60

01 03 05 07 09 11 13

Source: Markit Economics, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

16

PMI export orders: Emerging markets

Exhibit 59: NJA PMI export orders Exhibit 60: China PMI export orders Exhibit 61: India PMI export orders

35

40

45

50

55

60

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

25

30

35

40

45

50

55

60

25

30

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

NBS*

Markit

Average

40

45

50

55

60

40

45

50

55

60

05 06 07 08 09 10 11 12 13

Exhibit 62: South Korea PMI export orders Exhibit 63: EEMEA PMI export orders Exhibit 64: Russia PMI export orders

40

45

50

55

60

40

45

50

55

60

05 06 07 08 09 10 11 12 13

30

35

40

45

50

55

30

35

40

45

50

55

01 03 05 07 09 11 13

25

30

35

40

45

50

55

25

30

35

40

45

50

55

01 03 05 07 09 11 13

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

17

PMI export orders: Emerging markets continued

Exhibit 65: Turkey PMI export orders Exhibit 66: Poland PMI export orders Exhibit 67: Brazil PMI export orders

30

35

40

45

50

55

60

30

35

40

45

50

55

60

05 06 07 08 09 10 11 12 13

30

35

40

45

50

55

60

30

35

40

45

50

55

60

01 03 05 07 09 11 13

30

35

40

45

50

55

30

35

40

45

50

55

05 06 07 08 09 10 11 12 13

.Source: Markit Economics, NBS, CLIC, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

18

PMI inventories: Developed markets

Exhibit 68: US Markit stocks of finished goods Exhibit 69: Euro area PMI stocks of fin. goods Exhibit 70: Japan PMI stocks of fin. goods

30

35

40

45

50

55

30

35

40

45

50

55

07 08 09 10 11 12 13

40

42

44

46

48

50

52

40

42

44

46

48

50

52

01 03 05 07 09 11 13

44

46

48

50

52

54

56

44

46

48

50

52

54

56

01 03 05 07 09 11 13

Exhibit 71: Germany PMI stocks of fin. goods Exhibit 72: UK PMI stocks of fin. goods Exhibit 73: Swiss PMI stocks of fin. goods

36

38

40

42

44

46

48

50

52

54

36

38

40

42

44

46

48

50

52

54

01 03 05 07 09 11 13

38

40

42

44

46

48

50

52

54

38

40

42

44

46

48

50

52

54

01 03 05 07 09 11 13

38

42

46

50

54

58

38

42

46

50

54

58

01 03 05 07 09 11 13

Source: Markit Economics, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

19

PMI inventories: Emerging markets

Exhibit 74: NJA PMI stocks of fin. goods Exhibit 75: China PMI stocks of fin. goods Exhibit 76: India PMI stocks of fin. goods

44

46

48

50

52

44

46

48

50

52

05 06 07 08 09 10 11 12 13

42

44

46

48

50

52

54

42

44

46

48

50

52

54

05 06 07 08 09 10 11 12 13

NBS PMI

Markit PMI

44

46

48

50

52

54

44

46

48

50

52

54

05 06 07 08 09 10 11 12 13

Exhibit 77: South Korea PMI stk. of fin. goods Exhibit 78: EEMEA stk. fin. goods Exhibit 79: Russia PMI stocks of fin. goods

38

42

46

50

54

58

38

42

46

50

54

58

05 06 07 08 09 10 11 12 13

42

44

46

48

50

52

42

44

46

48

50

52

01 03 05 07 09 11 13

42

44

46

48

50

52

54

42

44

46

48

50

52

54

01 03 05 07 09 11 13

.Source: Markit Economics, NBS, CLIC, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

20

PMI inventories: Emerging markets continued

Exhibit 80: Turkey PMI stocks of fin. goods Exhibit 81: Poland PMI stocks of fin. goods Exhibit 82: South Africa PMI stk. of purchases

40

42

44

46

48

50

52

54

40

42

44

46

48

50

52

54

05 06 07 08 09 10 11 12 13

40

42

44

46

48

50

52

40

42

44

46

48

50

52

01 03 05 07 09 11 13

30

40

50

60

70

30

40

50

60

70

01 03 05 07 09 11 13

Exhibit 83: LATAM PMI stk. of fin. goods Exhibit 84: Brazil stocks of fin. goods Exhibit 85: Mexico PMI stocks of fin. goods

46

48

50

52

46

48

50

52

05 06 07 08 09 10 11 12 13

44

46

48

50

52

44

46

48

50

52

05 06 07 08 09 10 11 12 13

40

45

50

55

60

44

46

48

50

52

54

56

05 06 07 08 09 10 11 12 13

INEG PMI

Markit PMI

Source: Markit Economics, NBS, CLIC, INEGI, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

21

PMI input prices: Developed markets

Exhibit 86: US ISM input prices Exhibit 87: Euro area PMI input prices Exhibit 88: Japan PMI input prices

30

35

40

45

50

55

60

65

10

20

30

40

50

60

70

80

90

01 03 05 07 09 11 13

20

30

40

50

60

70

80

20

30

40

50

60

70

80

01 03 05 07 09 11 13

30

35

40

45

50

55

60

65

70

75

80

30

35

40

45

50

55

60

65

70

75

80

01 03 05 07 09 11 13

Exhibit 89: Germany PMI input prices Exhibit 90: UK PMI input prices Exhibit 91: Swiss PMI input prices

20

30

40

50

60

70

80

90

20

30

40

50

60

70

80

90

01 03 05 07 09 11 13

30

40

50

60

70

80

30

40

50

60

70

80

01 03 05 07 09 11 13

40

42

44

46

48

50

52

54

56

58

20

30

40

50

60

70

80

01 03 05 07 09 11 13

Source: Markit Economics, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

22

PMI input prices: Emerging markets

Exhibit 92: NJA PMI input prices Exhibit 93: China PMI input prices Exhibit 94: India PMI input prices

30

40

50

60

70

80

30

40

50

60

70

80

05 06 07 08 09 10 11 12 13

10

20

30

40

50

60

70

80

90

10

20

30

40

50

60

70

80

90

05 06 07 08 09 10 11 12 13

NBS PMI

Markit PMI

40

45

50

55

60

65

70

40

45

50

55

60

65

70

05 06 07 08 09 10 11 12 13

Exhibit 95: South Korea PMI input prices Exhibit 96: EEMEA PMI input prices Exhibit 97: Russia PMI input prices

40

45

50

55

60

65

70

40

45

50

55

60

65

70

05 06 07 08 09 10 11 12 13

40

45

50

55

60

65

70

75

80

40

45

50

55

60

65

70

75

80

01 03 05 07 09 11 13

40

45

50

55

60

65

70

75

80

40

45

50

55

60

65

70

75

80

01 03 05 07 09 11 13

Source: Markit Economics, NBS, CLIC, Haver Analytics®, Credit Suisse

02

De

ce

mb

er 2

01

3

Nove

mb

er M

anufa

ctu

ring P

MI R

ou

ndu

p

23

PMI input prices: Emerging markets continued

Exhibit 98: Turkey PMI input prices Exhibit 99: Poland PMI input prices Exhibit 100: Brazil PMI input prices

40

50

60

70

80

90

40

50

60

70

80

90

05 06 07 08 09 10 11 12 13

40

45

50

55

60

65

70

75

80

40

45

50

55

60

65

70

75

80

01 03 05 07 09 11 13

40

45

50

55

60

65

70

75

40

45

50

55

60

65

70

75

05 06 07 08 09 10 11 12 13

Source: Thomson Reuters DataStream, Haver Analytics®, Credit Suisse

European Economics team: Coverage of regions, institutions, themes and countries

HEAD OF EUROPEAN ECONOMICS Neville Hill

REGION THEME COUNTRY

Euro area Cyclical outlook Austria Greece Spain

[email protected] [email protected] [email protected] [email protected] [email protected]

+44 20 7888 1334 +44 20 7888 1334 +44 20 7888 1383 +44 20 7888 6827 +44 20 7888 6827

[email protected] [email protected] [email protected]

Northern euro area +44 20 7883 4192 Belgium +44 20 7888 7536 +44 20 7888 1383

[email protected] [email protected]

+44 20 7888 1383 Inflation +44 20 7883 3738 Ireland Sweden

[email protected] [email protected] [email protected]

Southern euro area +44 20 7883 4192 Cyprus +44 20 7883 7360 +44 20 7883 4192

[email protected] [email protected] [email protected] [email protected]

+44 20 7888 6827 +44 20 7888 1334 +44 20 7888 7536 +44 20 7888 1334 Switzerland

Scandinavia Fiscal policy Denmark Italy +44 20 7883 4192

[email protected] [email protected] [email protected] [email protected]

+44 20 7883 4192 +44 20 7888 6827 +44 20 7883 4192 +44 20 7883 4192 UK

[email protected] [email protected]

INSTITUTION Monetary policy Finland +44 20 7888 6827 +44 20 7888 1334

[email protected] [email protected] [email protected]

European Central Bank +44 20 7888 1383 +44 20 7883 4192 Netherlands +44 20 7883 7360

[email protected] [email protected] [email protected]

+44 20 7888 1383 +44 20 7888 1334 France +44 20 7888 1383

European Commission/EFSF/ESM "The periphery" +44 20 7888 6827 Norway

[email protected] [email protected] [email protected] [email protected]

+44 20 7888 6827 +44 20 7883 3738 +33 1 7039 0103 +44 20 7883 4192

Bank of England +44 20 7888 6827 Germany Portugal

[email protected] [email protected] [email protected]

+44 20 7888 1334 +44 20 7888 1383 +44 20 7883 3738

GLOBAL FIXED INCOME AND ECONOMIC RESEARCH

Dr. Neal Soss, Managing Director Chief Economist and Global Head of Economic Research

+1 212 325 3335 [email protected]

Eric Miller, Managing Director Global Head of Fixed Income and Economic Research

+1 212 538 6480 [email protected]

US ECONOMICS

Dr. Neal Soss, Managing Director

Head of US Economics

+1 212 325 3335

Jay Feldman, Director

+1 212 325 7634

Dana Saporta, Director

+1 212 538 3163

dana.saporta@credit-

suisse.com

Isaac Lebwohl, Associate

+1 212 538 1906

isaac.lebwohl@credit-

suisse.com

LATIN AMERICA ECONOMICS AND STRATEGY

Alonso Cervera, Managing Director

Head of Non-Brazil Latam Economics

+52 55 5283 3845

Mexico, Chile

Casey Reckman, Vice President

+1 212 325 5570

Argentina, Venezuela

Daniel Chodos, Vice President

+1 212 325 7708

Latam Strategy

Juan Lorenzo Maldonado, Associate

+1 212 325 4245

Colombia, Peru

Di Fu, Analyst

+1 212 538 4125

Nilson Teixeira, Managing Director

Head of Brazil Economics

+55 11 3701 6288

Daniel Lavarda, Vice President

+55 11 3701 6352

Brazil

Iana Ferrao, Associate

+55 11 3701 6345

Brazil

Leonardo Fonseca, Associate

+55 11 3701 6348

Brazil

Paulo Coutinho, Associate

+55 11 3701-6353

Brazil

EURO AREA AND UK ECONOMICS

Neville Hill, Managing Director

Head of European Economics

+44 20 7888 1334

Christel Aranda-Hassel, Director

+44 20 7888 1383

Giovanni Zanni, Director

+44 20 7888 6827

Violante di Canossa, Vice President

+44 20 7883 4192

Axel Lang, Associate

+44 20 7883 3738

Steven Bryce, Analyst

+44 20 7883 7360

Mirco Bulega, Analyst

+44 20 7883 9315

EASTERN EUROPE, MIDDLE EAST & AFRICA ECONOMICS AND STRATEGY

Berna Bayazitoglu, Managing Director

Head of EEMEA Economics

+44 20 7883 3431

Turkey

Sergei Voloboev, Director

+44 20 7888 3694

Russia, Ukraine, Kazakhstan

Carlos Teixeira, Director

+27 11 012 8054

South Africa

Gergely Hudecz, Vice President

+33 1 7039 0103

Czech Republic, Hungary, Poland

Alexey Pogorelov, Vice President

+7 495 967 8772

Russia, Ukraine, Kazakhstan

Shahzad Hasan, Vice President

+44 20 7883 1184

EEMEA Strategy

Natig Mustafayev, Associate

+44 20 7888 1065

EM and EEMEA cross-country analysis

Nimrod Mevorach, Associate

+44 20 7888 1257

EEMEA Strategy, Israel

JAPAN ECONOMICS AND STRATEGY

Hiromichi Shirakawa, Managing Director

+81 3 4550 7117

Takashi Shiono, Associate

+81 3 4550 7189

Tomohiro Miyasaka, Director

+81 3 4550 7171

NON-JAPAN ASIA ECONOMICS

Dong Tao. Managing Director

Head of NJA Economics

+852 2101 7469

China

Robert Prior-Wandesforde, Director

+65 6212 3707

Regional, India, Indonesia, Australia

Christiaan Tuntono, Vice President

+852 2101 7409

Hong Kong, Korea, Taiwan

Santitarn Sathirathai, Vice President

+65 6212 5675

Regional, Malaysia, Thailand

Michael Wan, Analyst

+65 6212 3418

Singapore, Philippines

Weishen Deng, Analyst

+852 2101 7162

China

..

Disclosure Appendix

Analyst Certification The analysts identified in this report each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report. References in this report to Credit Suisse include all of the subsidiaries and affiliates of Credit Suisse operating under its investment banking division. For more information on our structure, please use the following link: https://www.credit-suisse.com/who_we_are/en/This report may contain material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse AG or its affiliates ("CS") to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates. The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients of this report as its customers by virtue of their receiving this report. The investments and services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. CS does not advise on the tax consequences of investments and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. Information and opinions presented in this report have been obtained or derived from sources believed by CS to be reliable, but CS makes no representation as to their accuracy or completeness. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in this report. Those communications reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other communications are brought to the attention of any recipient of this report. CS may, to the extent permitted by law, participate or invest in financing transactions with the issuer(s) of the securities referred to in this report, perform services for or solicit business from such issuers, and/or have a position or holding, or other material interest, or effect transactions, in such securities or options thereon, or other investments related thereto. In addition, it may make markets in the securities mentioned in the material presented in this report. CS may have, within the last three years, served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned in this report or may be providing, or have provided within the previous 12 months, significant advice or investment services in relation to the investment concerned or a related investment. Additional information is, subject to duties of confidentiality, available on request. Some investments referred to in this report will be offered solely by a single entity and in the case of some investments solely by CS, or an associate of CS or CS may be the only market maker in such investments. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR's, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS's own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS's website shall be at your own risk. This report is issued and distributed in Europe (except Switzerland) by Credit Suisse Securities (Europe) Limited, One Cabot Square, London E14 4QJ, England, which is authorised by the Prudential Regulation Authority ("PRA") and regulated by the Financial Conduct Authority ("FCA") and the PRA. This report is being distributed in Germany by Credit Suisse Securities (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienstleistungsaufsicht ("BaFin"). This report is being distributed in the United States and Canada by Credit Suisse Securities (USA) LLC; in Switzerland by Credit Suisse AG; in Brazil by Banco de Investimentos Credit Suisse (Brasil) S.A or its affiliates; in Mexico by Banco Credit Suisse (México), S.A. (transactions related to the securities mentioned in this report will only be effected in compliance with applicable regulation); in Japan by Credit Suisse Securities (Japan) Limited, Financial Instruments Firm, Director-General of Kanto Local Finance Bureau (Kinsho) No. 66, a member of Japan Securities Dealers Association, The Financial Futures Association of Japan, Japan Investment Advisers Association, Type II Financial Instruments Firms Association; elsewhere in Asia/ Pacific by whichever of the following is the appropriately authorised entity in the relevant jurisdiction: Credit Suisse (Hong Kong) Limited, Credit Suisse Equities (Australia) Limited, Credit Suisse Securities (Thailand) Limited, having registered address at 990 Abdulrahim Place, 27 Floor, Unit 2701, Rama IV Road, Silom, Bangrak, Bangkok 10500, Thailand, Tel. +66 2614 6000, Credit Suisse Securities (Malaysia) Sdn Bhd, Credit Suisse AG, Singapore Branch, Credit Suisse Securities (India) Private Limited regulated by the Securities and Exchange Board of India (registration Nos. INB230970637; INF230970637; INB010970631; INF010970631), having registered address at 9th Floor, Ceejay House, Dr.A.B. Road, Worli, Mumbai - 18, India, T- +91-22 6777 3777, Credit Suisse Securities (Europe) Limited, Seoul Branch, Credit Suisse AG, Taipei Securities Branch, PT Credit Suisse Securities Indonesia, Credit Suisse Securities (Philippines ) Inc., and elsewhere in the world by the relevant authorised affiliate of the above. Research on Taiwanese securities produced by Credit Suisse AG, Taipei Securities Branch has been prepared by a registered Senior Business Person. Research provided to residents of Malaysia is authorised by the Head of Research for Credit Suisse Securities (Malaysia) Sdn Bhd, to whom they should direct any queries on +603 2723 2020. This report has been prepared and issued for distribution in Singapore to institutional investors, accredited investors and expert investors (each as defined under the Financial Advisers Regulations) only, and is also distributed by Credit Suisse AG, Singapore branch to overseas investors (as defined under the Financial Advisers Regulations). By virtue of your status as an institutional investor, accredited investor, expert investor or overseas investor, Credit Suisse AG, Singapore branch is exempted from complying with certain compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the "FAA"), the Financial Advisers Regulations and the relevant Notices and Guidelines issued thereunder, in respect of any financial advisory service which Credit Suisse AG, Singapore branch may provide to you. This research may not conform to Canadian disclosure requirements. In jurisdictions where CS is not already registered or licensed to trade in securities, transactions will only be effected in accordance with applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade be made in accordance with applicable exemptions from registration or licensing requirements. Non-U.S. customers wishing to effect a transaction should contact a CS entity in their local jurisdiction unless governing law permits otherwise. U.S. customers wishing to effect a transaction should do so only by contacting a representative at Credit Suisse Securities (USA) LLC in the U.S. Please note that this research was originally prepared and issued by CS for distribution to their market professional and institutional investor customers. Recipients who are not market professional or institutional investor customers of CS should seek the advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. This research may relate to investments or services of a person outside of the UK or to other matters which are not authorised by the PRA and regulated by the FCA and the PRA or in respect of which the protections of the PRA and FCA for private customers and/or the UK compensation scheme may not be available, and further details as to where this may be the case are available upon request in respect of this report. CS may provide various services to US municipal entities or obligated persons ("municipalities"), including suggesting individual transactions or trades and entering into such transactions. Any services CS provides to municipalities are not viewed as "advice" within the meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. CS is providing any such services and related information solely on an arm's length basis and not as an advisor or fiduciary to the municipality. In connection with the provision of the any such services, there is no agreement, direct or indirect, between any municipality (including the officials, management, employees or agents thereof) and CS for CS to provide advice to the municipality. Municipalities should consult with their financial, accounting and legal advisors regarding any such services provided by CS. In addition, CS is not acting for direct or indirect compensation to solicit the municipality on behalf of an unaffiliated broker, dealer, municipal securities dealer, municipal advisor, or investment adviser for the purpose of obtaining or retaining an engagement by the municipality for or in connection with Municipal Financial Products, the issuance of municipal securities, or of an investment adviser to provide investment advisory services to or on behalf of the municipality. If this report is being distributed by a financial institution other than Credit Suisse AG, or its affiliates, that financial institution is solely responsible for distribution. Clients of that institution should contact that institution to effect a transaction in the securities mentioned in this report or require further information. This report does not constitute investment advice by Credit Suisse to the clients of the distributing financial institution, and neither Credit Suisse AG, its affiliates, and their respective officers, directors and employees accept any liability whatsoever for any direct or consequential loss arising from their use of this report or its content. Principal is not guaranteed. Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that. Copyright © 2013 CREDIT SUISSE AG and/or its affiliates. All rights reserved.

Investment principal on bonds can be eroded depending on sale price or market price. In addition, there are bonds on which investment principal can be eroded due to changes in redemption amounts. Care is required when investing in such instruments. When you purchase non-listed Japanese fixed income securities (Japanese government bonds, Japanese municipal bonds, Japanese government guaranteed bonds, Japanese corporate bonds) from CS as a seller, you will be requested to pay the purchase price only.

![Rebound of us_supplier_industry_final[1]](https://img.pdfslide.net/doc/110x75/5410260d7bef0a3e088b8281/rebound-of-ussupplierindustryfinal1.jpg)