Embed Size (px)

Citation preview

PAGE 2 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

Canadian-based NCSGCrane & Heavy Haul Corp.announced that its U.S. subsid-iary, NCSG Crane & HeavyHaul Services, Inc., boughtGreat Falls-based H&H CraneService Inc.

H&H CraneService’s parentcompany wasfounded in GreatFalls in 1987 byTom Harant.

“H&H has aproud 27 yearhistory of pro-viding fully-operated andmaintainedcrane and liftingsolutions to itsmany customers

in the Great Falls region andwe are thrilled to be partneringwith Tom Harant and the restof the H&H team going for-ward” said Ted Redmond,president of NCSG. “We willcontinue to provide crane ser-vices to the Great Falls marketand plan to grow our crane andheavy haul fleet in this marketto meet the needs of currentcustomers and the proposedprojects in the region.”

As a part of the transaction,Harant has taken an ownershipinterest in NCSG, and intendsto work closely with NCSG togrow the crane and heavy haulservices business in the GreatFalls region. “I will continue torun the business and NCSG/H&H Crane will enhance thecurrent services with addition-al equipment from NCSG’scrane and heavy haul opera-tions,” said Harant. “With ac-cess to NCSG’s team of 700employees and fleet of over 290cranes, 235 lines of hydraulicplatform trailers, 300 conven-tional trailers and specializedrigging services such as jackand slide and hydraulic gan-tries, NCSG/H&H Crane will beable to take on larger projectsand maintenance jobs and meeteven more of our customers'rigging, lifting and heavy haulneeds.”

Employee buys share ofauto body business

1st Avenue Auto Body Gen-eral Manager Billy Rostenbought a share of the business.Rosten has worked for 1st Ave-nue Body for eight years andhas worked in the industry for17 years as a painter, in auto

body repair, frame repair andas a manager and estimator. Heis I-CAR Platinum ASE certi-fied.

“I wanted to invest in thebusiness because of the qualityof work 1st Avenue Body isknown for,” said Rosten. “Ihave seen the business growand the repeat customers wehave is something you justdon’t see anywhere else.”

1st Avenue offers a full lineof auto body repair, includingcollision repair, mechanical,frame straightening, and state-of-the-art automobile painting.Additional services includespray in-bed liners, windshieldreplacement, paint protectionfilm and complete auto detail-ing.

The business is located at706 1st Ave. S. The phone num-ber is 453-3368.

SBA announces fiscalyear-end loan guaranteeresults for Montana

The Montana District Officeof the U.S. Small Business Ad-ministration released its fiscalyear-end loan figures for 2014.

During Fiscal Year 2014,SBA guaranteed 307 loans total-ing $104.68 million, whichhelped create and retain 2,621jobs. Of these loans, 287 for$84,462,100 were made throughSBA’s 7(a) Guaranty Loan Pro-gram, which provides short orlong term financing for smallbusiness start-up or expansionneeds. Twenty loans totaling$20.22 million were madethrough SBA’s 504 CertifiedDevelopment Company pro-gram, which provides long

term fixed-rate financing forland, buildings and equipment.

Of the 307 loans, 57 loanstotaling $10.5 million weremade to women-owned busi-nesses, 17 loans totaling $6.6million were made to veterans,and 18 loans totaling $6.8 mil-lion were made to minoritybusiness owners.

“Montana is well-known forbeing one of the best places inthe country to start a smallbusiness,” said Wayne Gardel-la, the SBA District Directorfor Montana. “Out of the 307loans that were guaranteed bythe SBA, 36 percent were tostart up businesses and 112 newbusinesses received$24,643,800 in SBA guaranteedfunding.”

Cascade County had 15 SBAloans last year, totaling $1.19million.

New salon opens in GreatFalls

Designer Salon opened at219 5th St. S. Suite C.

Bev Ball, Mary Brandvold,Lisa Maxwell, Jude Silver, andKi Wine have over 175 yearscombined experience.

Designer Salon offers hairservices, facial waxing, man-icures, pedicures, and artificialnails.

Call all 750-4141.

New consulting businessopens

Comprehensive ProfessionalResources provides profession-al services to assist organiza-tions achieve goals by provid-ing cost-effective solutions tosupplement limited resources.

“The premise of our busi-ness is to keep overhead lowfor all types of businesses.Instead of hiring personnel on apart- or full-time basis, CPRcan plan and manage projectsor prepare grants as needsarise,” said Sally Newhall, apartner in the new business.

CPR offers a full menu ofservices including grant prep-aration, development strate-gies, human resource manage-ment, event planning, fiscalassessments, board develop-ment, retail operations manage-ment and business plan devel-opment. For businesses withemployees on leave, CPR willalso provide temporary exec-utive fill-in services. The mem-bers of CPR bring a wide array

of experience to their new com-pany, with significant successin their previous positions.

The company’s membersinclude Donna Camp, SusanJohnson, Sally Newhall andNancy Zadick. They metthrough their most recent em-ployment at the C.M. Russell

Museum and other earlier col-laborations.

Visit the website at cprcon-sultingmt.com, call Susan John-son at 406-788-2933 or send anemail to [email protected] for addi-tional information or to sched-ule an appointment.

New ownership for local crane company

JO DEEBLACKTribuneBusinessEditor

COURTESY PHOTO

Designer Salon recently opened inGreat Falls. The stylists are, backrow, left, Jude Silver, Ki Wine andMary Brandvold. In the front row,last to right, are Lisa Maxwell andBev Ball. Young Professional

Profile

Meet the Great Falls Tribune’snewest journalist. / Page 3

My Office

Optometrist Anthony Turk and hiswife Shelley build Complete EyeCare on the former National Laun-dry site. / Page 4

Market Mojo

Be consistent when telling yourbusiness’ story. / Page 4

Staying Power

Great Falls Paper and Supply inbusiness for 101 years. / Page 6-7

One Year Later

The Celtic Cowboy Pub and Restau-rant. / Page 8-9

Affordable Care Act

Businesses prepare for new re-quirements. / Page 10 - 16

People Talk

Sharpen your listening skills./ Page 17

Your Money

What is the market? / Page 18

Great Falls Business

GREAT FALLS BUSINESS IS A PUBLI-CATION OF THE GREAT FALLSTRIBUNE

What’s inside

Complete Eye Care is locatedat 1012 1st Ave. N.

TRIBUNE FILE PHOTO

The Celtic Cowboy Pub andRestaurant is housed in oneof oldest buildings in GreatFalls.

GETTY IMAGES/ISTOCKPHOTO

Businesses plan for new ACArequirements.

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 3

Andrea Fisher-Nitschke

Age: 29

Hometown: St. Louis, Mis-souri (just down the river!)

Family: Husband, Jason anddaughter, Logan, 13 months.

What I do at work: I am thecops and courts reporter atthe Great Falls Tribune. I covercourt proceedings, crime andother news involving theGreat Falls Police Department.

How long I’ve workedthere: I have almost twoweeks in. I am a newbie at theTribune, but I have four yearsof previous experience atboth TV stations in Great Falls.

My favorite thing aboutmy job: My co-workers. Nooffense to any of my old newscohorts, but this newsroom isthe best! I also love this newchallenge of covering thenews of the area in a differentway for this medium that isnew to me. I’m having somuch fun already.

What I do in my free time:My husband and I have some“must-watch” TV that wecatch up on when the babygoes to sleep. I also love

taking walks, shopping andcrafting.

Why I live and work inGreat Falls: We moved backto Great Falls after three yearsaway because we want toraise our little girl here. Wewere both presented withfantastic career opportunities,too. I’ve already reconnectedwith many work sources, andit feels great to receive such awarm reception upon ourreturn.

My favorite thing aboutGreat Falls: The appreciationyou gain for the simple, im-portant things in life. Thistown has a wonderful familyfeel and I think it will only getbetter as various groups have

made it their mission to im-prove this city.

Random/interesting/unique fact about myself: Iwon multiple ribbons (twoblue!) for scrapbook pages ofmy destination wedding atthe Montana State Fair in2011.

Twitter or Facebook:@GFTrib_Andrea on Twitter

Young Professional ProfileSEEKING YOUNGPROFESSIONALS

Profiles include the followingquestions: Name; age; home-town; family; what I do atwork; where I work; my favor-ite thing about my job; what Ido in my free time; why I liveand work in my town; myfavorite thing about my town;random/interesting/uniquefact about myself; and Twitteror Facebook. We also need aphoto, a head-and-shouldersshot, attached as a jpeg.Please include a phone num-ber.

To submit a profile, contactRoxy Perez at the Chamber ofCommerce at [email protected].

FILE PHOTO

Andrea Nitschke

As manufacturerscontinue to roll out newsmartphones, luring cus-tomers to ditch their oldphones, data securityexperts warn that im-properly disposed phonescan be mined for personaldata by hackers in theU.S. and abroad.

“People have moreinformation on their cell-phones than they do athome,” once you havesomebody’s cellphone youhave someone’s entirelife,” said Nick Akerman,partner and data securityexpert at Dorsey &Whitney.

The EnvironmentalProtection Agency re-ports more than 416,000cellphones are disposed

of every day and almost40 percent of cellphoneusers fail to take anysecurity measures, suchas erasing their data be-fore disposing of it, ac-cording to ConsumerRe-ports.Org.

“Most people forget towipe their cellphonesbefore they get rid ofthem,” stated Dan Guido,Co-Founder and CEO ofTrail of Bits, an informa-tion security companythat specializes in securi-ty defense. “You shouldalways set your phone tofactory settings beforegiving it away.”

John Shegerian, CEOof Electronic RecyclersInternational, argueswithout proper handlingof electronic disposaleveryone is at risk. “Com-panies and governments

are throwing their rep-utations in the trash.When they dispose oftheir devices it’s beinghandled inappropriately,therefore making theman easy target for databreach.”

The fastest growingissue for EPA is e-waste,the agency’s websiteclaims, and with little tono monitoring, it’s theconsumer’s responsibilityto secure their informa-tion.

“What you need to dobefore you hand off yourold cellphone is wipe offall your personal data,”said Kevin Haley, direc-tor of Product Manage-ment for Symantec Secu-rity Response. “Improperuse of disposing yourcellphone is a risk and it’sreal.”

Smartphone disposal posessecurity risks, experts warnBy Charmaine Crutchfield

USA TODAY

Cascade 4.5% 3.5% 41,047 41,000Yellowstone 3.0% 4.0% 83,980 85,285Missoula 4.5% 3.5% 60,689 61,957Flathead 6.3% 4.8% 44,394 45,109Gallatin 3.6% 2.8% 53,755 55,895Lewis & Clark 4.0% 3.2% 34,454 35,060Silver Bow 4.8% 4.0% 17,675 17,569Montana 5.6% 4.6% 513,345 520,368

CountySept. 2013

LABOR FORCE

Sept. 2013 Sept. 2014

PERCENT UNEMPLOYED

Sources: Department of Labor & Industry, Research and analysis Bureau; Montana Aeronautics Division; Constructionmonitor.com

Sept.

2014

2014

to date

2013

to date

Sept.

2013

Cascade $2.9 $9.60 $57.90 $101.48Yellowstone $29.00 $48.76 $418.36 $295.12Missoula $12.46 $9.71 $108.43 $92.90Lewis & Clark $18.49 $9.75 $108.20 $91.61Gallatin $34.32 $50.63 $257.60 $369.77Flathead $27.00 $25.03 $195.35 $203.44

Value in millions of dollars(Residential and commcercial)

Sept. 2014

City

Great Falls 14,499 14,615 139,772 147,090 Billings 33,629 35,859 290,101 317,031 Missoula 25,787 31,246 228,012 254,311 Bozeman 39,326 43,367 354,557 382,187Helena 8,876 8,301 73,417 73,772Kalispell 19,967 23,175 161,650 184,461Statewide* 147,211 162,219 1,285,811 1,404,806

Oct.

2014

Oct.

2013

2013

to date

2014

to date

*Statewide total includes smaller airports not listed

MONTANA EMPLOYMENT REPORT

BUILDING PERMITS IN THE STATE’S TOP COUNTIES

AIRLINE BOARDINGS IN MONTANA’S TOP CITIES

V I T A L S I G N S

THE AFFORDABLE

CARE ACT

GFTRIBUNE.COM

REACHING MONTANA DECISION-MAKERS

NOVEMBER 2014

ONE YEAR

LATER

The Celtic Cowboy Pub & Restaurant

STAYING

POWER

Great Falls Paper & Supply in business 101 years

MY OFFICE

Complete Eye Care: Anthony and Shelley Turk build new clinic

BUSINESSES STRUGGLE TO

ANTICIPATE IMPACT OF NEXT

PHASE OF OBAMACARE

PAGE 4 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

When construction workerswere building at 1012 1st Ave.N., everyone was curious.

“People wanted to knowwhat was being built and wewere trying so hard to keep itquiet,” said Shelley Turk. Peo-ple would stop and ask the crewwhat was going up in the oldNational Laundry site, someeven called banks to try to findout details.

The suspense is over nowthat Dr. Anthony Turk’s officebuilding is finished. CompleteEye Care opened on Sept. 2 andwhat was once an empty lot andthe former site of NationalLaundry, now holds an attrac-tive eye clinic and landscapedparking.

Anthony and Shelley Turkbought the lot years ago andwere waiting for the right timeof Anthony to leave his work asan optometrist with Shopko andopen the couple’s own office.The Turks own five city lots onthe block, four in the front andone in the alley.

“Because we have five lots,it gave us the space to have thebuilding we wanted and ade-quate parking,” Shelley said.She added that they have roomfor another business on theirproperty as well.

Anthony Turk made thedecision to open his own clinicbecause he wanted to be inbusiness fully for himself and

provide the full care he felt hispatients needed, Shelley Turksaid.

Anthony Turk, an optome-trist, has been providing eyecare in the community for 14years.

Now that he owns his ownbuilding, he and wife, Shelleyhave been adapting to the extrawork that brings.

“There is so much we didn’tdo before. Now we have tothink about landscaping, snowremoval, lawn care, things wehave to take care of ourselvesthat add extra hours to thework week,” Shelley said. “Butit’s ours and we’re going to doit. We’re privileged to do it. It’sa blessing.”

In thinking about the archi-

tecture of his office there wasone important thing to Turk. Hewanted it to be functional. Shel-ley was more interested in thevisual so she sat down with thearchitect and the constructioncompany and picked out thedetails: bricks, counter tops,paint.

“I had never done that be-fore. It was a huge undertaking

and still, his response was,‘Whatever you decide, dear.’”

Shelley said the space pulledtogether beautifully. The wait-ing room is large and open withnatural light provided by themany windows and the wallsare covered with frame boardsso people can browse for glass-es.

The building contains roomsfor pre-screening, specialtytesting and contact trainingalong with a lab space and astaff room with kitchen. Antho-ny Turk decided to make theexam rooms bigger so patientswouldn’t feel cramped, espe-cially if they brought a familymember with them. Also, with abigger room he wouldn’t needto use a refraction mirror sys-tem when testing eye sight.

“For years, eye doctors’offices were small andcramped. We went back to full-sized exam rooms and the of-fice space is roomy.” Shelleysaid.

The extra space has im-proved Anthony Turk’s timemanagement. He sees plenty ofeye emergencies and now canhave several exam rooms goingat one time and can see morepatients because he has theappropriate space.

“Now we can make every-one’s care very individualized,we can meet everybody’sneeds. The building is nice butit’s mainly a place to be caredfor,” Shelley said.

Complete Eye Care, built to doctor’s orders

TRIBUNE PHOTO/LARRY BECKNER

Optometrist Anthony Turk opened Complete Eye Care at 1012 1st Ave. N., a new office built on the former NationalLaundry site.

By Jenny KunkaFor Great Falls Business

Today’s marketing landscapeallows consumers to truly inter-act with brands in more ways

than ever before.Not only is itcritical to a mar-keter’s successto have a strongbrand image butalso to be consis-tent and authen-tic across all thedifferent plat-forms availabletoday. In order tomaintain this

consistency, it is important tohave a well-defined brand.

So, how do we define brand-ing? Branding is the process of

establishing and continuing tomanage an organization’s rep-utation. It is the relationshipbetween the consumer and aproduct or service. A brand isnot a logo, tagline, colorscheme or fonts – instead theseare elements that support thebrand. A brand is emotion,thoughts and feelings; it is whatyour customer thinks and feelsabout your business. A strongbrand is authentic, memorableand must be consistent acrossall touch points and platforms.

The first step in being stra-tegic and consistent in commu-nicating your brand is to devel-op brand guidelines. Identifyyour core attributes, compet-

itive advantages and strengths.Know your audience and deter-mine the authentic voice youwill use when communicatingwith them. What is your story?What is your brand personal-ity? What does your brand envi-ronment look like? These areall questions that need to beanswered when developingyour brand direction.

Also included in your brandguidelines will be graphic stan-dards to ensure visual consis-tencies when communicatingyour brand. Whether you arereaching your audience with aFacebook post or a tri-fold bro-chure, your voice and visualrepresentations of your brand

need to be consistent. Graphicstandards will define fontstyles, colors, logo treatments,etc. that should always be fol-lowed when communicatingacross multiple platforms.

Another necessity to astrong and consistent brand isto be authentic. Determineyour brand personality andalways ensure you are consis-tently communicating this per-sonality whether you are writ-ing a 140 word blog post or 140character tweet. Be real. Begenuine. Consumers want torelate brands with real people.Humanize your brand as muchas possible.

All the various platforms in

today’s marketing world maybe overwhelming to some. Butif you know and understandyour target audience, have astrong, authentic and consis-tent brand voice, then theseplatforms provide multipleopportunities to effectivelyconnect and start meaningfulconversations with your audi-ence.

Jennifer Fritz is senior accountmanager at The Wendt Agency, anadvertising and public relationsagency located in Great Falls.Follow Wendt atthewendtagency.com, on Facebookat facebook.com/wallywendt andTwitter@WendtAds.

Be consistent when telling your business’ story

JENNIFERFRITZMarket Mojo

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 5

MINNEAPOLIS — After a health insur-ance company laid him off in 2012, JohnColumbus spent the next 20 monthsanswering as many questions aboutgaps in his résumé as about his years ofemployment.

Then a friend steered him to U.S.Bank, which was piloting a White Houseinitiative for hiring the long-term un-employed. “There are some companiesthat ask you for any involuntary termi-nation,” Columbus said. “Those compa-nies never call back. U.S. Bank looked atme as a whole person with 30 years ofexperience.”

If Columbus, 53, embodies the woesof Americans out of work for more thansix months, the Obama administrationhopes a new hiring drill at Minneapolis-based U.S. Bank helps the nation ad-dress an ugly legacy of the Great Reces-sion.

Some recent research shows thatbusinesses would rather hire peoplewith no experience than experiencedworkers who have been out of work fora long time. Using recommendationsfrom a handbook drafted by DeloitteConsulting and the Rockefeller Founda-tion, U.S. Bank is searching for ways togive a fairer shake to those job seekers.The handbook “increases knowledge ofconscious or unconscious bias” againstthe unemployed, explained U.S. Bankhuman resources chief Jennie Carlson.

This consciousness-raising has yield-ed new employees like Columbus, whoseextended jobless status and age oftenleft him drowning on the bottom of theapplicant pool. The bank’s work drewthe praise of a senior White House offi-cial.

“U.S. Bank has taken an active lead-ership role in this initiative, includingpartnering with peer companies to en-gage other Twin Cities employers toembrace these practices,” Byron Au-guste, deputy director of the NationalEconomic Council, told the Star Tribunein an email.

Whether programs like the one U.S.Bank piloted can work nationally “de-pends on whether employers are doingthis (discrimination) unintentionally orwhether they believe it produces a bet-ter pool of workers,” said Joe Ritter, aprofessor of applied economics at theUniversity of Minnesota.

There has been progress. The ranksof the long-term unemployed haveshrunk by 900,000 since the WhiteHouse hiring initiative kicked off inJanuary. But that is not yet enough toaddress the drag of long-term unem-

ployment on the economy. In mid-2009,people out of work more than 27 weeksaccounted for over 40 percent of thenation’s total unemployed. Last month,more than five years into economicrecovery, the long-term unemployedstill represented almost one-third of thecountry’s jobless. Today, roughly 3 mil-lion Americans have been out of workmore than 27 weeks.

Even in Minnesota, which consistent-ly boasts employment rates a couple ofpercentage points higher than the na-tional average, the long-term unem-ployed struggle to find work. A decadeago, the percentage of Minnesota’s un-employed who had been out of workmore than 27 weeks was in the teens.Since 2010, it has been in the low 30s orhigh 20s.

Rather than write these people offusing impersonal screening processes,U.S. Bank implemented ideas to in-crease personal contact and focused onmatching skills with job openings, re-gardless of an applicant’s employmentstatus. The company signed an employ-ment pledge with the White House inJanuary 2014 with 300 other U.S. compa-nies, including Richfield, Minn.-basedBest Buy. Then, U.S. Bank was picked asone of several pilot sites for tweakingpersonnel policies.

The company still talks to would-beemployees about prior layoffs. Butthere is a conscious effort by recruitersand applicants not to let layoffs dom-inate the discussion.

“The employer handbook reminds usto look at all of a person’s story,” Carlsonsaid.

U.S. Bank now partners with non-profits and government agencies toidentify specific long-term unemployedindividuals who might make good em-ployees, Carlson said. The bank alsosteers experienced applicants who failto get hired on their first try to otheropenings.

In mid-October, Carlson met withofficials at the White House to discussways to broadly distribute handbooks tothe long-term unemployed and the busi-nesses that might hire them. She alsotalked about how companies that pilotedthe new hiring model can help integrateit into America’s business culture.

A few weeks ago, U.S. Bank joinedprivate businesses, including TargetCorp. and Wells Fargo Bank, at the TwinCities Long-Term Unemployment Initia-tive kickoff. The meeting aimed to con-nect private companies with Minnesotanonprofit groups and state and localagencies that can serve as pipelines to

Bank fighting biasagainst unemployed

By Jim SpencerStar Tribune (Minneapolis) (MCT)

See UNEMPLOYED, Page 16

Phone: 406-454-1311

Toll Free: 800-735-7003•Full service & overhaul

•Medium & heavy duty trucks

•Diesel powered motorcoaches & RVs

•Air-conditioning service

Our total truck

care keeps you

on the road

2121 Vaughn Rd Great Falls, MT • www.istatetruck.comSales, Parts &

Service Dealer:Authorized Parts & Service center for:

MT-0000341688

State of the Art Conference CenterBook your next Conference, Wedding, or Special Event at

the Hilton Garden Inn • Full Service Restaurant & Bar

MT-0000341710

2301 14th St. SW406-453-2675

www.greatfalls.hamptoninn.com

2520 14th St. SW406-452-1000www.greatfalls.hgi.com

Full Service Restaurant,Bar & Evening Room Service

Located next to the Great Falls Market Place

PAGE 6 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

Great Falls Paper and Sup-ply has been a fixture in down-town Great Falls for 101 years.James Flaherty came to GreatFalls more than 100 years agoand started the general supplystore. It sold products in bulk tosmall general stores in areacommunities such as Sand Cou-lee as well as local businessesin Great Falls, such as Eklundsand Kaufmans.

Soon James’ two brothers,Louis and Frank, joined himand they all had sons whohelped with the the business. Intime, the business was ownedby Mike’s father, James Jr andhis cousin Frank Jr. Mike’sfather bought out Frank Jr. andthen Mike joined his father inbusiness. Later, Mike boughtout his father.

“I sit in my grandpa’s oldoffice, my dad’s old office andnow my office,” Flaherty said.

Staying in business for morethan 100 years means knowingwhat to change in order to meetthe needs of the time. And itmeans knowing what to keepthe same.

“Because we’ve been inbusiness for 101 years, we’vehad to systematically changethe way we do business. Buggywhips don’t sell now, but in 1913they did. Sweeping compoundfor cleaning up warehousefloors sold in 1913 and it hassold steadily throughout theentire history of our company,”said Mike Flaherty, the thirdgeneration of Flaherty’s to ownthe business.

Being located on MachineryRow, 600 2nd St. S., was impor-tant 101 years ago because therailroad tracks ran close to thebuilding. Products came on therailway since there was nointerstate system at the time,Flaherty said. Even as a juniorhigh school student, Flahertyunloaded rail cars into the busi-ness warehouse.

Although the railroad tracksare now gone, the business stillsits in the same location andstill uses a large warehouse tostore products before sendingthem out to hundreds of busi-nesses in the area and somesurrounding states. The origi-

nal building burned down in1936. The wooden structure wasfilled with paper and was atotal loss in less than an hour.The family rebuilt, however,right on top of the cinders,creating a new brick space thathad a conference room, offices,plus plenty of warehouse floorfor their products.

Great Falls Paper and Sup-ply used to sell hosiery, print-ing paper, buggy whips andafter WWII they sold appli-ances as well. Then, the marketchanged. Big retailers grabbedthe market on appliances. Also,many of the mom and popstores that Mike’s grandfatherhad supplied began to close. Asa result, Great Falls Paper andSupply had to adapt.

“You find new things to sell.

My dad was the first one tobring cut paper to town, paperalready cut to size andwrapped. We were the firstones to bring plastic garbagebags to Montana. You have toevolve in time, to meet theneed,” Flaherty said.

Flaherty said the bulk of hissales today are paper products,a wide variety of paper towelsand toilet paper which he sellsto businesses along with retailpackaging. He also sells foodservice products such as takeout containers, deli cups andproduce bags along with bulkcleaning supplies.

“You start looking at themarket. You evolve in time,listening to your customer basewho is asking you to look atnew ideas.”

Even though the paper prod-ucts are the business’ breadand butter, Flaherty isn’t afraidto market new items.

“I look for something differ-ent, something my competitorsdon’t have that differentiatesme from them. We all haveservice and quality, so whatmakes me different? That iswhere some of us tend tochange. I’m forced to evolve allthe time and to do that, youneed to be up on what is goingon. Learning all the time.”

Although the business hasbeen adaptable, they havestayed loyal to their longtimecustomers. They are alwayslooking for new customers aswell, the little niches that wanta quality distributor for thelong term.

Flaherty said when they wona family business award yearsago, they were asked the ques-tion, “What are your businessvalues and what are your per-sonal values.” The answer,Flaherty said, was that personalvalues become business values.

“I was raised to be honest. Ihave to be able to deliver. Ican’t promise the moon and thestars; I need to be honest andforthcoming with customersbecause that is how we go downthe road together. We want tobe realistic, upfront and trans-parent about what we can pro-vide and when.

“We all talk about customerservice, quality and pricing,”Flaherty said, “But I reallythink the longevity of our busi-ness is the family business

Great Falls Paper and Supply

TRIBUNE PHOTO/LARRY BECKNER

Mike Flaherty poses in the warehouse of Great Falls Paper and Supply, the business has been in his family for 101 years.

Celebrating 101years in business

By Jenny KunkaFor Great Falls Business

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 7

Silver Wolf Enterprises

*Water Heaters *Heating/Cooling *Ice Machines *Commercial Coffee Equipment *Food Service Equipment *Bottle Water Cooler *Floor Care

268-8080900 12th St North • Great Falls

Hours: 8-4 • Monday - FridaySilverwolfenterprises.com • [email protected]

See Our Full Line of QUALITY BRANDS

You Can Trust.

All Water Heater Products In Stock

Tank Style Water Heaters

Residential & Commercial

Water Distillers

™

MT-0000341619

New Product

water softeners

staybridgesuites.com/greatfallsmt

Staybridge Suites Great Falls 201 3rd St. NW ▪ Great Falls, MT

Reservations: 406.761.4903

or 800.238.8000

Ex tended S tay Rates ▪ Bus iness Cente r ▪ Comp l imentary Laundry Room ▪ Fu l l K i t chens ▪ F ree Wi re less Anywhere ▪ S tud io , One and Two Bedroom Su i tes ▪ Comp l imentary Ho t B reak fas t Bu f f e t ▪ Pe t F r iend ly ▪ F i tness Room ▪ The Soc ia l Even ing Recep t ions ▪ The Pan t ry Conven ience S to re ▪ IHG Rewards ▪ Comp l imenta ry A i rpo r t Shut t le

Where you can work and unwind

your own way.

MT-0000341663

values. The value of beinghonest and fair.”

This sense of workingwith others for the longhaul may be part of whathas kept the businessviable for 101 years.

“We support our localmerchants. We really,really believe in buyinglocally. We’re all in it

together and to make itwork we have to be acommunity,” Flahertysaid.

“I grew up with a dif-ferent set of family val-ues so we ate dinner inplaces that bought fromus and we bought grocer-ies from the stores thatbought from us. We’ve

been a Chamber memberfor 101 years. We don’tjust take the money, wegive it back. It’s the coregroup of this businesscommunity that made ourtown grow and that is ourjob. We’re all in this to-gether and, at the end ofthe day, how do you makeit work for everybody?”

TRIBUNE FILE PHOTO/PETER JOHNSON

Great Falls Paper and Supply Co., 600 2nd. St. S., has been in Great Falls 101 years.

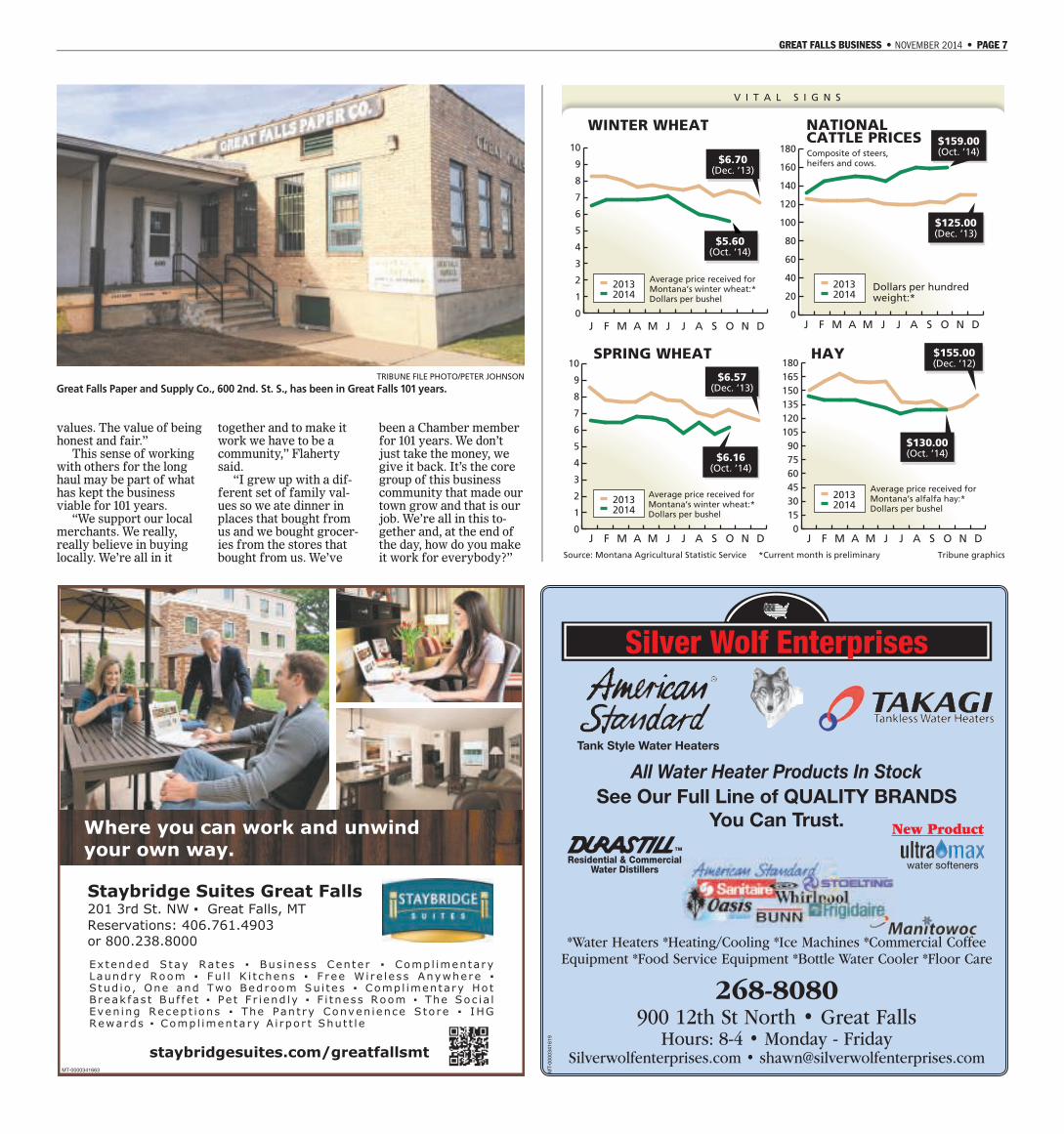

Source: Montana Agricultural Statistic Service *Current month is preliminary Tribune graphics

Average price received for Montana’s winter wheat:* Dollars per bushel

$6.70 (Dec. ’13)

20142013 Dollars per hundred

weight:*

$125.00 (Dec. ’13)

Composite of steers, heifers and cows.

$155.00 (Dec. ’12)

$130.00 (Oct. ’14)

Average price received for Montana’s winter wheat:* Dollars per bushel

$6.16 (Oct. ’14)

20142013

20142013

20142013

0

20

40

60

80

100

120

140

160

180

0

1

2

3

4

5

6

7

8

9

10

J F M A M J J A S O N D J F M A M J J A S O N D

0

1

2

3

4

5

6

7

8

9

10

0

15

30

45

60

75

90

105

120

135

150

165

180

J F M A M J J A S O N D J F M A M J J A S O N D

Average price received for Montana’s alfalfa hay:* Dollars per bushel

V I T A L S I G N S

WINTER WHEAT NATIONALCATTLE PRICES $159.00

(Oct. ’14)

HAYSPRING WHEAT

$6.57 (Dec. ’13)

$5.60 (Oct. ’14)

PAGE 8 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

Wayne Thares and his busi-ness partner, Channing Harteli-us opened The Celtic Cowboy ayear ago, an Irish pub and res-taurant, a $3.5 million project

in the remodeled Arvon Blockat 114 to 118 1st Ave. S.

The building was originally alivery stable, built in 1890.

The pub concept was devel-oped by The Irish Pub Co., aDublin-based company origi-nally established by Guinness.

The company developedmore than 400 Irish pubs in theU.S., but The Celtic Cowboy istheir first in Montana, Tharessaid.

The Arvon Block was amongfive buildings downtown evalu-ated in feasibility studies paid

for in part by a $21,500 Mon-tana Preservation Office grant,part of the Preserve Americaprogram.

City-County Historic Preser-vation Officer Ellen Sievertapproached Thares and hiswife, Sandy, for input about the

boutique hotel idea for thebuilding.

"One thing lead to another,"Thares said. "I did some re-search and found The Irish PubCo."

The name of the pub, TheCeltic Cowboy, is the nickname

TRIBUNE PHOTO/LARRY BECKNER

Brianna Grantier pours a beer from a tap at The Celtic Cowboy, a pub and restaurant that opened a year ago.

TRIBUNE PHOTO/LARRY BECKNER

The Celtic Cowboy opened their doors a year ago in the ArvonBlock of 1st Avenue South.

One Year Later: Celtic CowboyBy Jenny KunkaFor Great Falls Business

We Sell Maison Blanche Paint

We OB er Chalk-Based Painting Classeswww.provincialtreasures.com

• Color Consultation• Faux Finishing• Custom Painted Furniture• Murals • Staging• Licensed & Insured• Home Decor

Rebekah Mather

Certi5 ed Surface Designer

MT-0000341618

Provincial Treasures

WeWe S Selell l MaMaisison B Blalanchehe P Paiaint PaintncWeWeW l l Ml is

wwwww.w.prprovovinininincicicicialalalaltrtrtreaeasusureres.s.cocommres.commcocoeaeaww w.w.ppw.provinininccc

406.868.6070 • 1427 3rd Ave N • Great Falls, MT

Business Meetings • Receptions Baby Showers • All Occasions

SENIOR LIVING

(406) 761-6661 | 20 3rd Street North, Great Falls MT

MT-0000341709

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 9

of the original owner ofthe building, RobertVaughn. Originally fromWales, Vaughn made hisfortune in ranching in theSun River Valley. Hemoved to Great Falls withhis 16-month-old daugh-ter, Arvonia, after hiswife died.

"He became friendswith Paris Gibson andbecame interested indevelopment," Tharessaid. "The livery stablewas the most modern atthe time in the Northwest.There was a ramp for thestables, which were in thebasement. The main floorwas the saddlery and theshowroom on the mainfloor and a hotel on theupper floors.

"It was either theGreat Falls Tribune or theGreat Falls Leader thatcalled Vaughn 'The CelticCowboy,'" Thares said.

Thares and his part-ners in the building, Har-telius, Peter Jennings andMac Smith continue towork on the rest of thebuilding to complete theplan they had envisionedfrom the start: a pub,wine snug and boutiquehotel.

“The building was theimpetus for the businessand not the other wayaround. We’re thrilledwith the space. Everydaythe personality comesout,” Thares said.

Great Falls Business:How long did you planbefore committing tothe business?

Thares: We hadworked on the plans forabout 18 months prior toopening. We actuallyworked on the plans forabout 13 months prior tostarting construction

Great Falls Business:Did you write a businessplan?

Thares: Absolutely.The banks require that.An extensive businessplan for the pub, the winesnug and the hotel.

Great Falls Business:In planning to open thistype of business, didyou have a mentor?

Thares: We did a lot ofresearch online. Guinnessdoes a very good job oflining up future pub own-ers with consultants. Wetalked to a lot of theirconsultants. Also, I’ve

worked at the hotel/res-taurant business for along time.

Great Falls Business:What’s the best advicesomeone else gave youabout going into thepub business?

Thares: The best ad-vice was to keep it au-thentic. If you are goingto do an Irish pub, makesure it looks like you’re inIreland. So we spent agreat deal of money mak-ing sure that the bar wasauthentic, that the atmos-phere and that everythingabout it was as authenticas we could make it.

Great Falls Business:What advice would yougive someone elsethinking about openinga similar business?

Thares: I would say doyour research, make yourbusiness plans and yourforecasts and then adjustthem as needed. But real-ly follow your plan. Wewere about 3 months lateopening the pub, we arenow a year late openingthe basement and we’ll betwo years late openingthe hotel. We’ve had toadjust our business planand our projections everytime we have a setbackbut you just have to real-ize that those setbacksare going to occur and notget frustrated with them.

You need to adjust so thatit works. Do it efficientlybut not cheaply.

Great Falls Business:What would you haveliked to do over in thefirst year in business?

Thares: I think beingmore realistic on time-lines and understandingthat the process takeslonger. We had a lot ofexpectations that justdidn’t happen.

Great Falls Business:How many hours a weekdo you put in at TheCeltic Cowboy?

Thares: I probably put40-50 hours a week at thepub. I have other busi-nesses that I have to payattention to as well. Butwe’ve hired a phenomenalstaff that have done agreat job. I have full trustin them so I don’t have tobe there twenty-fourseven.

Great Falls Business:What is the best thingabout owning this typeof business?

Thares: The most grat-ifying things are the com-ments from out-of-townguests who come in andare blown away. They say,“We never expected aplace like this in GreatFalls, Montana, this isDenver quality, this isSeattle quality.” That isthe most gratifying thing

for us. That we took thetime to make sure we didit right.

Great Falls Business:What is the hardest

thing about owning thistype of business?

Thares: Regulations.All of the things it takesto open any business. It’s

amazing, all the thingsyou don’t think aboutuntil it comes time toopen.

Great Falls Business:What plans do you havefor the future of TheCeltic Cowboy?

Thares: On Oct. 31stwe opened our basement,which will be known asthe Darkhorse Hall andDarkhorse Wine Snug. Itwill have a wine bar andprivate wine lockers andmeeting and banquetspace. The DarkhorseHall opened with a Hal-loween costume partywith a guest DJ. We’llstart the Darkhorse WineClub, a subscription-based monthly wine clubas part of the wine snugthe first part of January.We’ll sell subscriptionsduring the holidays forthat. It will offer privateaccess to the wine roomand a private wine locker.Our plans are to open thehotel in March prior tothe art auction.

TRIBUNE PHOTO/LARRY BECKNER

Wayne Thares, one of the owners of Celtic Cowboy, stands inthe Darkhorse Hall and Wine Snug.

TRIBUNE PHOTO/LARRY BECKNER

The Celtic Cowboy opened their doors a year ago in the ArvonBlock of 1st Ave. S.

PAGE 10 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

What’s now called Taylor’sFamily Auto Group, the compa-ny that started as a car dealer-ship in Fort Benton and todayemploys just under 100 thereand in Great Falls, has not seenmany changes since the Afford-able Care Act went into effectJan. 1.

But “we have providedhealth insurance for manyyears,” said Bamma Taylor,controller. “Since Day One” in1980.

Today, the company that’s anumbrella for Jim Taylor Motorsin Fort Benton, and Taylor’sAutoMax, Taylor’s ACR, Tay-lor’s ServiceMax and Taylor’sTransportation in Great Fallshas “not changed what we pro-vide. The only thing that’s hap-pened is that the cost had goneup some before (ACA) wentinto effect. And then ACA exac-erbated rising costs.”

Starting Jan. 1, 2015, though,employers the size of Taylor’sapparently will be required totrack and file a detailed reporton what coverage they provide(see sidebar).

Taylor said one of the bigfrustrations began a year ago,in the run up to ACA takingeffect. “We never received oneword of information from thegovernment about what wasgoing to happen, what the ex-pectations were on what to do,when to do it and how to do it,”she said of her family’s busi-ness. Information only camefrom Taylor’s third-part provid-ers.

Asked if she was preparedfor the new reporting require-ment, she said “we’ve alwaysbeen above the standard. …Why should I have to give theminformation if I’m in compli-ance. It’s onerous. … I feel likeI work for the government.”

Gary Sears, general man-ager of the Best Western PlusHeritage Inn, said “we’re in await-and-see-type attitude, not

knowing what’s coming downthe pike. It certainly wouldimpact us,” he said of the 181-employee hotel, Great Falls’biggest.

The Heritage does not di-rectly provide health coverageto all employees, but he saidmany workers are able to pur-chase through the hotel’s insur-ance agent with a cost reduc-tion. However they often endup with high-deductible, cata-strophic coverage.

Taylor’s Family Auto Grouphas raised deductibles on itspolicies because family policieswere getting so expensive em-ployees couldn’t afford to buythem, Bamma Taylor said. Thecompany now deposits $60 permonth into employees’ health-reimbursement accounts “tohelp with their deductibles.”

That money can be used topay for claims before the de-ductible is met. “It’s one thingI’ve done to re mediate the costto the employee. Obviously thepolicy is a little cheaper” withthe higher deductible, althoughTaylor is expecting a 7 percentto 8 percent increase in premi-ums when renewal comes up inDecember.

Dwight Holman, presidentof Holman Aviation Co. willface a different change, al-though, because of its size, the24-employee flight-servicescompany is exempt from man-dates requiring insurance orreporting.

With general changes in the

health-insurance marketbrought about by ACA, he said,his policy offerings shifted toage-based pricing. He expectsincreases to be “enormous. …Some employees have gone up30 percent to 40 percent.”

He said because HolmanAviation’s last renewal camebefore ACA went into effect,“we only had to comply whenwe renewed.”

Coverage will be redesignedand it will be more expensivefor his older workers, Holmansaid. “They will take a reallybig hit.”

Kim Gillan, Department ofHealth & Human Services Re-gion 8 director, said “smallbusinesses are the backbone ofMontana’s economy. Before theAffordable Care Act, smallbusinesses paid 18 percentmore in premiums for the samebenefits as their larger compet-itors due to lack of purchasingpower. In Montana, small busi-nesses enrolled through thenew SHOP marketplace arefinding quality affordable cov-erage. In 2015 Montana smallgroup rates will raise an aver-age of 1.12 percent, well belowpast yearly trends.”

In addition “many smallemployers qualify for a taxcredit,” Gillan said from thefederal agency’s regional officein Denver. “That can cut theirpremiums as much as 50 per-cent.”

Gillan, a former Billingslegislator and director of a

workforce training program atMontana State University, said“the ACA is working to providea healthy workforce that willsupport a healthy economy.”

Taylor said “I don’t knowwhat’s going to happen. Thecost of health care has gone up,availability has gone down andemployees are confused.” Shesaid in some cases, employeescan find cheaper policies fortheir dependents on the HealthInsurance Marketplace.

“It has not been fun,” Taylorsaid. For the last two or threeyears, and everything that’sbeen “pushed through, we nev-er changed (coverage), evenduring the downturn of 2008.

We’re going to take care of ouremployees.”

She said the health caresituation is complicated foremployees too and, recently,there’s “frustration trying toget in to see doctors. They’reoverwhelmed. … Unless youhave a previous relationship,”with a doctor, and many em-ployees haven’t, “now they’relooking for relationship withphysicians and it’s difficult.”

Overall, Taylor said, “I’m nota huge fan. We provided insur-ance for 34 years. Nobodymade us do this. It’s a decisionwe made long ago, we cared forour employees and they’re avital part of our business.”

Employers unsure about ACA

GETTY IMAGES/ISTOCKPHOTO

Affordable Care Act requirements for businesses begin Jan. 1.

TRIBUNE PHOTO/RION SANDERS

Bamma Taylor, controller for Taylor's Auto Max, talks with Cheryl Haynes onin the Taylor's Auto Max business office. The business must file newpaperwork with the federal government beginning Jan. 1, part of ACArequirements for businesses with more than 50 employees.

Businessrequirementsbegin Jan. 1

By Marc StergionisTribune Staff Writer

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 11

PAGE 12 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 13

PAGE 14 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 15

2015 ACA SPECIFICS

Employer Shared Responsibility provisionsBeginning in 2015, employers with 100 or more full-time or full-timeequivalent employees who do not offer affordable health insurancethat provides minimum value to their full-time employees (and depen-dents) may be required to pay an assessment if at least one of theirfull-time employees is certified to receive a Premium Tax Credit in theindividual Health Insurance Marketplace. Under these rules, a full-timeemployee is one who is employed an average of at least 30 hours perweek.The assessment, called an Employer Shared Responsibility payment, iscalculated different ways and is either $2,000 or $3,000 per employeeper year depending on the circumstance. Businesses are not requiredto make a payment on the first 30 full-time equivalent employees.There are tax advantages to offering health coverage to employees,but Shared Responsibility payments are not tax deductible.For employers with 50-99 full time/full-time equivalent employees,these rules will not apply until 2016 provided employers of this sizemeet certain certification requirements.Information reporting on health coverage by employersBeginning in 2015, the Affordable Care Act provides for informationreporting by employers with 50 or more full-time or full-time equiv-alent employees regarding the health coverage they offer to theirfull-time employees. New information reporting by issuers, self-in-suring employers, and other parties that provide health coverage alsotake effect in 2015. The first of these reports must be filed in 2016.

— Small Business Administration

INSURANCE, TAX CREDITS FOR SMALLEMPLOYERS

The Small Business Health Options Program (SHOP) Marketplace isopen to employers with 50 or fewer full-time-equivalent employees.Employers with fewer than 25 employees may qualify for tax credits ifthey buy insurance through SHOP. Businesses may qualify for employerhealth care tax credits if they have fewer than 25 full-time-equivalentemployees making an average of about $50,000 a year or less.

To qualify for the Small Business Health Care Tax Credit, businessesmust pay at least 50 percent of their full-time employees' premiumcosts. Businesses don’t need to offer coverage to part-time employeesor to dependents.

The tax credit is worth up to 50 percent of an employer’s contributiontoward employees' premium costs (up to 35 percent for tax-exemptemployers).

The tax credit is highest for companies with fewer than 10 employeeswho are paid an average of $25,000 or less. The smaller the business,the bigger the credit.

—healthcare.gov

MT-0000341616

Pam Hansen Alfred, Agent2817 10th Avenue SouthGreat Falls, MT 59405

Bus: 406-453-6010

If you’re about to retire or

change jobs, you may have

some decisions to make about

your retirement plan money.

Good thing there’s someone

who knows you and is ready

to help.

Like a good neighbor,

State Farm is there.®

CALL ME TODAY.

Talk tous about a401(k) rollover.

State Farm Mutual Automobile Insurance Company, Bloomington, ILwww.pamalfred.com 623 1st Avenue N.W. • Phone 454-3612

Black Velvet 1/2 gal

Was 2070 Now 1970

Pinnacle Whipped Vodka 1/2 gal

Was 2170 Now 2070

Bacardi Rum 1/2 gal

Was 2725 Now 2525

MT-0000341695

Noble’sWestsideLiquor

Small businesses face somenew requirements to complywith Affordable Care Act reg-ulations starting Jan. 1, butthere will be some govern-ment infrastructure enablingthem to fulfill the require-ments.

This weekend the federally-facilitated Small BusinessHealth Options (SHOP) Mar-ketplace on HealthCare.govlaunched a host of new onlinefeatures for small employerswith up to 50 employees thatwill allow them to shop for,select, and offer employeeshigh quality health and dentalcoverage, and allow employ-ees to enroll — all online, fed-eral officials said. There arealso a host of online tools tohelp small employers makeinformed decisions.

The online SHOP Market-place will allow small employ-ers to find a SHOP-registeredagent or broker in their areaand, if they choose, to autho-rize that agent and broker toassist in managing their SHOPaccount online.

“Offering employees healthcoverage through SHOP alsoallows eligible employers toqualify for the Small BusinessHealth Care Tax Credit, worthup to 50 percent of the employ-er’s premium contributions,”officials said.

Under regulations in placenow, “employers with fewer

than 50 full-time-equivalentemployees are not required tooffer health insurance,” offi-cials said, “and there’s no pen-alty if they choose not to. Thisprovision is not changing.”

For 2015 and after, busi-nesses employing at least acertain number of employees(generally 50 full-time em-ployees or a combination offull-time and part-time em-ployees that is equivalent to 50full-time employees) will besubject to the ACA’s EmployerShared Responsibility provi-sions.

Under the ACA a full-timeemployee is an individualemployed on average at least30 hours of service per week.An employer that meets the 50full-time employee thresholdis referred to as an applicablelarge employer.

Under Employer SharedResponsibility, “if these em-ployers do not offer affordablehealth coverage that providesa minimum level of coverage

to their full-time employees,and their dependents, the em-ployer may be subject to anEmployer Shared Responsibil-ity payment if at least one ofits full-time employees re-ceives a premium tax creditfor purchasing individualcoverage” on the Health Insur-ance Marketplace Market-place, officials said.

But officials said “undertransition-relief rules employ-ers with fewer than 100 full-time employees, includingfull-time equivalents, in 2014,aren’t subject to EmployerShared Responsibility pay-ments during 2015.”

Beginning in 2015, thehealth care law requires newinformation reporting by:

» Employers with 50 ormore full-time (or full-timeequivalent) employees.

» Health insurance issuers.» Self-insuring employers

of any size.» Other parties that provide

health coverage.

Programs help withnext phase of ACA

DompierHolmanGillan

By Marc StergionisTribune Staff Writer

PAGE 16 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

Thousands of small busi-nesses around the U.S. areracing to renew their healthinsurance policies Dec. 1 tobeat large premium increasestheir brokers say will hit themJan. 1 when the AffordableCare Act takes full effect.

Some health insurance bro-kers also say 2014 may be thelast year many of the compa-nies even offer health insur-ance.

Insurance brokers fromseveral states told USA TODAYthat 60 percent to 80 percent oftheir small-business clients —those with 50 employees orfewer — are renewing theirpolicies early to skirt the law.Companies with more than 50employees aren’t allowed toadjust their renewal dates.

Many companies are stillwaiting to hear what ratesthey’ll be facing in 2014, asstate insurance commissionersare backlogged with tasks re-lated to ACA compliance.

The National Federation ofIndependent Business esti-mates 42 percent of the at least7 million small businesses with50 or fewer employees offerhealth insurance. Early thismonth the group released asurvey in which 64 percent of921 small-business owners andoperators reported they paymore for insurance premiumsper employee in 2013 than theydid in 2012.

The Department of Healthand Human Services says thesituation is better than it has

been in the past. “Since theAffordable Care Act becamelaw, health care costs havebeen slowing and premiums areincreasing by the lowest ratesin years,” HHS spokeswomanJoanne Peters says. “The law ismaking it easier for businessesto offer coverage, just like itdid in Massachusetts whenemployer coverage increasedafter reform passed.”

Beginning this summer,insurance companies warnedbrokers and businesses thatrates could rise dramaticallybecause of the ACA, and someof these agents say they areseeing increases of 30 percentto even 100 percent in premi-ums, especially for businessesthat have young workforces.That’s because companies willno longer be able to chargeolder people more than threetimes they do younger ones.

Moving up renewal dates,which could affect millions ofworkers, will save these em-ployees money on their premi-ums, but critics warn it alsomeans they won’t benefit fromsome of the ACA’s provisions.Among the changes that takeeffect Jan.1: fully paid preven-tive care doctor visits, limits onout-of-pocket expenses andmandatory dental coverage forchildren.

“The consumer protectionsare in there for a good reason,”says Wendell Potter, a formerspokesman for Cigna insur-ance, now an author and indus-try watchdog. “The value of thepolicies that will be mandatoryafter (Jan. 1) will be much bet-ter.”

Plans offered by small busi-nesses, Potter says, “often haveskimpy coverage or very, veryhigh deductibles. That’s whymany of them are less expen-sive.”

In Chicago, health insurancebroker Allen Wishner, an ACAsupporter, says most of hisclients’ plans already had themost important benefits re-quired in the new law, so hedoesn’t think the delay putstheir employees at a disad-vantage.

Wishner says 72 percent ofhis 1,600 small-business clientsthat have responded to insur-ers’ early renewal offers decid-ed to go with Dec. 1 renewals.He expects that trend to con-tinue when his other 1,000 cli-ents make their decisions.

What’s happening in someareas:

» In Louisville, Ky., brokerMatt Schwartz says about 60percent of his small-businessclients are renewing Dec. 1. Heestimates the new insurancerating rules will increasehealthy younger companies’group rates anywhere from 30percent to 100 percent. Hisearly-renewal clients hope atleast to delay that for up to 11months, he says. After that,“clearly, some of these smallbusinesses will drop their in-surance,” he says. .

» In Hampstead, N.H., TomHarte says it would benefitabout half of his approximately200 small-business clients torenew on Dec. 1. It was an easydecision for one company thatwas facing a 3% premium in-crease in December vs. a 20

percent one in January. “I’m100 percent confident somehealthy young groups’ premi-ums in other states are dou-bling,” he says.

» In Americus, Ga., brokerRuss Childers says he has justreceived the rates for his small-business clients, and many ofthem are significantly higher— unless the company employsa lot of older workers. His ad-vice to clients: “When in doubt,early renew. Then they canswitch to something else later.”But he says he’s not doing it forthe insurance companies. “Wesell what our clients need.”

» In Sacramento, brokerLaurie Rood says about 80% ofher small-business clients —ranging from law firms to pestcontrol companies — moved toa Dec. 1 renewal date. Roodsays companies are unhappythey have to “purchase addi-tional benefits they didn’tneed.”

» In Scotts Hill, Tenn., J.Darlene Tucker says most ofher small-business clients kepttheir 2014 renewal dates, oftenbecause it’s too hectic at theend of the year to have to dealwith insurance.

All businesses with 50 ormore employees have to pro-vide health insurance begin-ning on Jan. 1, 2015. NFIB saidits study showed 13 percent ofbusinesses plan to cut the hoursof part-time workers next year.However, it noted no more thanhalf of those cuts are related tothe ACA. Rood says many res-taurateurs in her area reducedtheir employees’ hours so theywould be considered part-time

and not eligible for insurance,but all the state and federalwebsite problems means thoseworkers can’t get online toenroll yet.

The federal and state healthinsurance marketplaces will allhave a Small Business HealthOptions Program, or SHOP, thatwill allow small business own-ers to make side-by-side com-parisons of plans. Enrollment inSHOP is year round and cov-erage could start Jan 1. Work-ers in small businesses thatdon’t offer coverage will havebetter options for insuranceand consumer protections and acompetitive individual market-place, HHS says.

As for whether small busi-nesses will continue to offerinsurance, Wishner says, “any-thing could happen in a year.”Nervous about all the un-knowns about their newly in-sured customers, many in-surers “have been raising ratespretty steadily over last fouryears.” And he says he’s had totell companies in previousyears that they were facing30%-50% premium increasesand “employers pay it.”

Childers says his clients,which range from a collegefoundation to a timber farmerand sprinkler company, arehoping to continue offeringinsurance after next year, evenwith rate increases.

“Most haven’t made a deci-sion yet because they don’tknow what it’s going to costnext year,” he says. “Most ofthem think they will be able tooffer something, but as costs goup it becomes harder.”

The race to renew health plans earlyBy Jayne O’Donnell

USA TODAY

promising applicants that usualscreening processes mightexclude.

Ritter, the economics profes-sor, likened employer discrimi-nation against the long-termunemployed to racial profiling.

“To me, it seems possiblethat many employers don’tknow they are doing it,” hesaid. “If that’s true, it could belike dealing with racial profil-

ing. Training and awarenesshelp.”

Letting the long-term un-employed languish costs theeconomy in lost productivityand tax revenue and increasedspending on government wel-fare programs. But gettingthem back into the workforcemeans valuing what they offer.

“The idea,” Carlson said, “isto begin with a warm relation-ship instead of a cold one. …The most important piece isremoving barriers.”

Columbus knows all aboutbarriers. He has been laid off

four times in his IT career.With each succeeding layoff,the difficulty finding workincreased.

He went back to college in2008 to complete a degree pro-gram. It didn’t seem to matter.Because of his job history andincreasing age, the pickingsstayed slim or got slimmer.Once he’d been out of work fora certain period, it was as if hewas tainted.

“They grill you,” he said.“’Why can’t you find a job?’”

Or at least keep one.He applied for 70 different

jobs at the health insurancecompany where he used towork before he found someonein the organization willing tohire him.

“And there were probably200 to 250 applications at othercompanies” that didn’t pan out,he said.

The U.S. Bank job was noslam dunk either, despite thecompany’s new focus on help-ing the long-term unemployed.Columbus worked with severalof the bank’s recruiters. Hemade it to the final selectionprocess for posts as a project

manager and an audit servicesmanager, but lost out on both.

Close to running out of mon-ey to pay his bills, he appliedfor something else. The recruit-er working with him pointedhim away from that job to an-other one in risk managementauditing. It turned out to be aperfect fit for his skill set.

“It was not three strikes andyou’re out,” Columbus said ofhis new employer’s approach.

It can’t be, explained Carl-son, if the idea is to get peopleback to work who haven’t had ajob for a long time.

UnemployedContinued from Page 5

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 17

“You didn’t hear a word Isaid, did you.”

“I’m sorry, can you repeatthat?”

“Are you listening?” Sound familiar? We have all

been guilty ofnot listening.Listening is oneof those skillsthat, if done well,increases oureffectiveness ateverything we doyet is not oftenpracticed withany consciousintent.

What doesconscious intent

really mean when thinkingabout listening? First of all it isabout thinking – thinking aboutlistening. In order for any of usto really listen with the rightintent and attention, we mustconsciously make a decision tostop and focus on the otherperson. What is fascinatingabout our minds and our hear-ing is that when we are trulyfocused on listening to anotherperson we literally tune outmost of the noise around us. Wejust don’t hear it. You can besitting in a noisy coffee shopand not hear all the conversa-tions or noises around you ifyou are focused on what is infront of you; another person,your laptop, or your cell phone.

The challenge today is thereare too many distractions thatmake it hard to focus on anyone thing. Our world is full ofreadily available information.Much of it appears to be use-less yet we often sort through itto find something of value. AsJanet Marturano says, whowrote the recent book, “Findingthe Space to Lead” “The weight

of messages leaves us too littletime simply to reflect on whatthey really mean.” We are over-whelmed and often don’t evenrealize it.

People consume their timescouring the Internet, readingendless emails, and scrollingthrough Facebook . Some wouldargue that our ability to payattention for any length of timehas decreased over the lastfifteen years.

In 1977, Herbert Simon, aNobel-winning economist hadthis to say about attention – “Inan information rich world, whatinformation consumes is theattention of its recipients.Hence a wealth of informationcreates a poverty of attention. “And, that was before the In-ternet, email, cell phones and

Facebook! When our attentionis drawn in different directions,seemingly simultaneously, arewe really focused on anything?The term being used today isContinuous Partial Attention.With all of the external stimu-lus we try to be attentive to alot of things and can’t be fullyfocused on any one thing.

Back to the not so simpleconcept of listening. There aredifferent types of listening thatwe all do. The highest level isthe type of listening where wetruly want to understand theother person’s perspective,regardless of whether we agreeor disagree. The reality is thatwe can’t listen at this level allthe time. But, those times whenwe do need to listen at thislevel, do we? It means being

able to tune out the rest of theworld and truly be there foranother person. That takesconscious effort on our part.

Here are five different lev-els of listening. The first twoare really not listening butthink about those times whenyou have not listened in theseways and why.

» I don’t listen because Idon’t like you or your idea.

» I don’t listen because I amindifferent to what you have tosay.

» I do listen, but with theintent to counter what you sayand then make my point.

» I listen for commonground between what you thinkand what I think.

» I listen to see your point ofview completely and accurate-

ly. In lots of conversations with

others we listen at level three.We listen for what we disagreewith and when the person takesa breathe we jump in to countertheir point.

True, level five listening issimple to understand yet hardto practice. It means stoppingourselves and really listeningfor understanding. When weconsciously practice listeningand pay attention in the mo-ment we become more effec-tive in our relationships withothers. People want to be heardand understood.

So, try this seemingly simpleexercise. Try to listen to oneperson for at least one minutewithout talking and just noticehow you feel and how othersrespond. You may notice that itis hard for you not to speak.You may notice that your mindtends to wander and it is hardto stay focused on what theperson is saying. You may no-tice that it is relatively easy todo. Whatever your experiencejust be in the moment and payattention to the act of listening.You might be surprised by whatyou see!

Listening is a skill and onewe should be interested in fur-ther developing. We live in aworld of sound bytes and con-stant distraction. To stop andreally pay attention can be achallenge, however, not listen-ing when we should might belimiting our success in everyaspect of our lives.

Mark Willmarth workspart-time as the training and

development director for the city ofGreat Falls. With his wife, Mary, he

operates Vision West Inc., aconsulting business. Contact him

Are you flexing your listening skills?

MARKWILLMARTHPeople Talk

Listening isa skill andone weshould beinterestedin furtherdeveloping.We live in aworld ofsoundbytes andconstantdistraction. GETTY

IMAGES

Member SIPCMT-0000341665

Struggling for Investment income? Let’s talk.

Jordan L. HustedFinancial Advisor501 1st Ave SouthGreat Falls, MT 59401406-727-1111 [email protected]

Follow us on Facebookfor Market Updates and Insightsfacebook.com/EJAdvisorJHusted

AUTO CAREPROFESSIONAL AUTO &LIGHT TRUCK REPAIRS

24 Hour Towing

761-1342

Computer Diagnostics - Tune Ups

Cooling Systems - Air Conditioning

Quick Lube - Brakes

www.carlsautocare-gf.com2300 10th Avenue South

Great Falls, MTMT-0000341711

Auto Care

Center

PAGE 18 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

MONTANA REFINING, LLC

MT-0000341690

Expanding and Fueling Our

Future

MT-0000341712

Making InsuranceSimple for You

- Insurance

• Life

• Property

• Auto

- Business Investments

• Education Planning

• Retirement Funding

• Estate Strategies

• Annuities

• Mutual Funds

I am committed to helping you prepare for the

future & protect what matters most

Randy Bogden201 Smelter Ave NW, Great Falls, 59404

453-5255 | www.RandyBogden.com

Randy Bogden

Every day, when I walk in the doorfrom work, my 8-year-old says, “Dad,was the market up or down today?” Idon’t think he cares that much about themarket results, as much as he has deter-

mined that it is often agood barometer of mymood.

What is “the market?”When most investorsrefer to the market, theyare referring to the stockmarket, and most in-vestors use an index or aselection of stocks tomeasure the results of thestock market. Most com-monly, U.S. investors useone of two indexes: the

Dow Jones Industrial Average (Dow), orthe Standard & Poor’s 500 (S&P 500).While they are both similar in terms ofhow they measure market results, theyare quite different in how they are cal-culated.

Let’s start with the oldest and prob-ably best-known index, the Dow. TheDow was invented by Charles Dow in1896, and is comprised of 30 of the larg-est companies in the U.S. across a rangeof industries (except transport and util-ities). The criteria to be chosen for theDow are somewhat vague; all are verylarge companies and leaders in theirrespective industries. The editors of theWall Street Journal (owned by DowJones & Co.) pick the stocks that com-prise the index. The component compa-nies of the Dow don’t change very oftenas it takes a significant change in thecompany (acquisition, merger, or sig-nificant downsizing) for it to be re-moved from the index.

The S&P 500 was originally createdin 1957 and is comprised of the marketcapitalization of 500 large companieslisted on the New York Stock Exchangeor Nasdaq. It is widely considered oneof the best representations of the U.S.stock market because of its breadth ofcompanies. The S&P 500 was developedand continues to be maintained by S&PDow Jones Indices, a joint ventureowned by McGraw Hill Financial. Thecomponents of the S&P 500 are alsochosen by a committee, which assessesthe merits of a candidate company usingcriteria such as market capitalization,liquidity, financial viability, and lengthof time publicly traded. The committeethen selects companies representativeof the industries in the U.S. economy.

The major difference between thesetwo indexes is that the Dow includes aprice-weighted average of 30 stocks,while the S&P 500 is a market value-weighted index of 500 stocks. A price-weighted average (like the Dow) is cal-culated by adding the share prices of allof the stocks in the index and then divid-ing by the number of stocks. So, of the30 stocks in the Dow, the highest priced

stocks (companies like Visa, GoldmanSachs, and IBM) will have the greatestimpact on the price movement of theoverall index.

A market value-weighted index (likethe S&P 500) is calculated by adding themarket capitalizations (the total value ofthe outstanding shares of the company)of all the stocks and dividing by thenumber of stocks. So, for the S&P 500,companies with the largest market capi-talization (companies like Apple, ExxonMobil, and Microsoft) will have thegreatest impact on the price movementof the overall index.

While neither index perfectly repre-

sents the entire movement of stocks inthe U.S. stock market, because the S&P500 includes 500 companies and isweighted by size (rather than price), it isgenerally accepted as a more accuratemeasure of the overall market. By un-derstanding these nuances between

each index, investors can better un-derstand how each measures overallstock market performance.

Brad Thurber, is a vice president,financial consultant with D.A. Davidson &

Co.

BRADTHUBERYour Money

What is the market?

GETTY IMAGES/AMANA IMAGES RF

Most commonly, U.S. investors use one of two indexes: the Dow Jones Industrial Average (Dow),or the Standard & Poor’s 500 (S&P 500).

GETTY IMAGES/INGRAM PUBLISHING

When most investors refer to the market, theyare referring to the stock market.

GREAT FALLS BUSINESS ● NOVEMBER 2014 ● PAGE 19

IN TOWN5 PM-7 PM

MT-0000341676

COME IN TO A FAMILY FRIENDLY ATMOSPHERE!›› FULL MENU SERVED 8 AM-10 PM›› BREAKFAST, LUNCH & DINNER›› ALL SPORTS PACKAGES›› 13 108’’ PROJECTOR TVS›› 52 FLATSCREENS

IIIIIIINNNNNNN TTTTTOOOOOOWWWWWWWWNNNNNNNNNNNN5 PM-7 PM

BINGOEVERY THURSDAYSTARTING AT 6:30 PM

BEST

1101 N.W. BYPASS, GREAT FALLS, MT111111000111 NN.WWW. BBBYYYPPPAAASSSSSS, GGGGRRRREEAAATT FFFAAALLLLSSS, MMMTTT

SATURDAY & SUNDAY

8:00 AM - NOON

If there’s one thing I’ve learned fromwriting about whether the minimumwage should be raised, it’s that writingabout whether the minimum wageshould be raised is a tricky business.

There are passionate voices on bothsides of the debate, and those voices areoften backed up by research that sup-ports their points of view.

There’s no question the Americanpublic supports a minimum wage in-crease. In the midterm elections, fourstates — Alaska, Nebraska, South Dako-ta and Arkansas — voted to raise theminimum wage. Voters in San Franciscofavored a minimum wage boost up to$15 an hour.

Some opposed to a wage increaseargued that voters sent mixed mes-sages, because they also elected a num-ber of Republican lawmakers who op-pose changing the minimum wage. Idisagree with that analysis. None of thecandidates ran strictly on opposition to aminimum wage increase, and therewere so many other factors at play inthe election that you can’t claim theGOP wave was an indication that publicopinion on this issue has shifted.

It hasn’t. People want to see the mini-mum wage raised.

If the election taught us anything it’sthat states and cities aren’t going to waitaround for lawmakers in Washington,D.C., to act.

“It’s clear that states and cities aregoing to have to lead the way for restor-ing the minimum wage to a more mean-ingful level,” said Paul Sonn, generalcounsel for the National EmploymentLaw Project. “We’re seeing it already.More than half the states have stoppedwaiting for Washington and raised theirminimum wage above the federal level.And now some larger cities are raisingtheir wages higher than the state level.The question now is how long is it goingto take before Washington is pressuredto act.”

While I very much like the idea ofpeople making more money, I havetrepidations about just raising the mini-mum wage without also implementingpolicies that will help people earn morein the long run.

Opponents of an increase describethe minimum wage as a “blunt instru-ment” for addressing the needs of lowerincome people. They believe a betterapproach is to bolster the educationsystem and offer more job prepared-ness programs while possibly tweakingthe Earned Income Tax Credit, a federalwage subsidy for low-income people, tomore directly benefit those who need

financial help.“We’ve got to get into teaching people

how to fish,” said Allen Sanderson, asenior lecturer in the University ofChicago’s Department of Economics. “Inthe high-tech world that we live in,somebody who’s unskilled, their eco-nomic life is basically over. They’revirtually unemployable. So one has tofind out how to fix that. Even if it takes10 years, it’s going to be much, muchbetter in the long run.”

In the end, I agreed that just raisingthe minimum wage is not the best idea.It’s a Band-Aid over a bullet wound. Theincome gap and the struggles low-wageworkers face need to be addressed in acomprehensive manner, so why notmake a moderate increase in the mini-mum wage while putting programs inplace that give people a fighting chanceto move up into higher paying jobs.

Sounds good, right? The problem is, Istill don’t hear politicians who opposeraising the minimum wage talking aboutlogical alternatives that will help low-income workers.

Sanderson agreed: “Politicians have avery short time horizon. In some ways,they just don’t give a rip about some-thing that happens 10 years out, theycare about something that’s two yearsout.”

Sonn, with the National EmploymentLaw Project, agrees that comprehensivechange is needed, but believes a wageboost should come first because it’s “areadily achievable first step.”

“We need to tackle and modernize ourjob training system, but that’s notenough,” Sonn said. “We need revampedjob training and K-12 education and acollege system that better fits our econ-omy. But it’s clear none of that is ade-quate to raise income levels for peopleon the bottom .”

This all makes me sigh rather loudly.The smart thing for us to do is attack

this problem from different directions— a moderate wage increase; bettereducation; smarter job training; taxcredits that target those who need itmost. But it’s clear the political will isn’tthere, and even though politicians pridethemselves on being communicators,they’ve done a lousy job explaining theneed to look at more than just the per-hour money.

Unless wage increase opponents gettheir acts together — swiftly — it’s clearstates and cities will take action and theminimum wage will go up.

I’m not saying that’s a bad thing. Iwant people to make more money, and Idon’t presently see another option on thetable.

I just think we could do better. Andwe’re not.

Solving the minimumwage issue? Not yet

By Rex HuppkeChicago Tribune (MCT)

PAGE 20 ● NOVEMBER 2014 ● GREAT FALLS BUSINESS

Unless you’re downsizing, movingdoesn’t usually lead to saving money.After all, between hiring movers, rent-ing a moving truck, furnishing the newspace and making back-and-forth trips(not to mention potentially having tobreak your lease), moving is usuallysomething people have to do, not some-thing they choose to do to save money.

But if you’re moving locally, or evenout of state for work or other reasons,there are some ways you can save mon-ey if you plan ahead.

Whether it’s picking a cheaper zipcode or renegotiating some of your bills,a move doesn’t have to incur costs. Hereare several ways you can save moneywith a new address.

COMMUTE

When moving to a new city, or relo-cating to a new part of town, take intoaccount your commute.

Driving 40 miles versus 5 of coursemakes a different, but what about tak-ing the highway versus side streets?

I recently relocated locally and endedup moving farther away from work.However, because my commute nowentails 9 miles of highway driving ver-sus 3 miles on congested side streets,my car’s use of fuel has become about 15percent more efficient. I’m going anextra 40 miles per tank, which is reduc-ing my monthly gas costs by about onetank, or $55 dollars. It helps too that myhighway commute is against traffic,whereas my side street commute waswith it.

A CHANGE OF ADDRESS COMESWITH DEALS

In my recent move, I also made themistake of purchasing everything formy new apartment before changing myaddress. More than $300 was racked upon the basics, from cleaning supplies totrash cans and additional kitchenware.

Once I changed my address online Ireceived a packet in the mail with a

dozen coupons to Home Depot, PotteryBarn and Target, among others. I madesure to go back to each store with myreceipts to get the discount after thefact, but if I’d waited to change my ad-dress for much longer I could have lostout on my opportunity to save as muchas 20 percent on my purchases.

According to the U.S. Census Bureau,nearly 12 percent of Americans movedbetween 2012 and 2013. Of the roughly36 million who did, more than 23 millionmoved within the same county, nearly 7million moved within the same state andnearly 5 million moved out of state.Those who move across state linesmight find it cheaper to buy some itemsnew rather than move everything theyhave.

YOU CAN RENEGOTIATE YOURLEASE

If you’re not looking to move but arefaced with a rent increase at the end ofyour lease, you could save money byopting to move rather than pay more