Embed Size (px)

Citation preview

The business of banking essentially involves intermediation-acceptance of deposits and channeling these deposits in to lending activities. Since the deposits received from the depositors have to be repaid to them by the bank, they are known as banks’ ‘Liabilities’ and as the loan given to the borrowers are to be received back from them, they are termed as banks’ ‘Assets’ so assets are banks’ loans and advances1 . In the traditional banking business of lending financed by deposits from customers, Commercial Banks are faced with the risk of default by the borrower in the payment of either principal or interest. This risk in banking parlance is termed as ‘Credit Risk’ and accounts where payment of interest and /or repayment of principal is not forthcoming are treated as Non-Performing Assets2 , as per the Reserve Bank of India, an asset, including a leased asset, becomes non-Performing when it ceases to generate income for the bank. Existence of Non-Performing Asset is an integral part of banking and every bank has some Non-Performing Assets in its advance portfolio. However, the high level of NPA is a cause of worry to any financial institution.

IMPLICATIONS OF NPAs For an Economy : Developing of sound and healthy financial institutions, especially banks, is an essential condition for maintaining over all stability of the financial system of the country. The high level of NPAs in banks and financial institutions has been a matter of grave concern to the public as bank credit is the catalyst to the economic growth of the country and any bottleneck in the smooth flow of credit, one cause for which is the mounting NPAs, is bound to create adverse repercussions on the economy. When the loans taken are not repaid, much of the funds go out of financial system and the cycle of lending- repaying-borrowing is broken. The banks have also to repay their depositors and others from whom the money had been borrowed. If the borrowers do not pay, the banks have to borrow additional funds to repay the depositors and creditors. This leads to a situation where banks are reluctant to lend fresh funds to new projects or the on-going projects thus choking the system. Once the credit to various sectors of the economy slows down, the economy is badly hurt. There is slow down in GDP growth and industrial output and fall in the profit margins of the corporate which resultantly cause depression in the market.

For Banking: The most important business implication of the NPAs is that it leads to credit risk management assuming priority over other aspects of bank’s functioning. The bank’s whole machinery would thus be pre-occupied with

recovery procedures rather than concentrating on expanding business. A bank with a high level of NPAs would be forced to incur carrying costs on non-income yielding assets. Other consequences would be reduction in interest income, high level of provisioning (as banks are required to keep aside a portion of their operating profit as provisions, as NPAs increases banks have to increase the amount kept aside as provisions which will reduce their net profits) stress on profitability and capital adequacy, gradual decline in ability to meet steady increase in cost, increased pressure on Net Interest Margin (NIM) thereby reducing competitiveness, steady erosion of capital resources and increased difficulty in augmenting capital resources. NPAs generate a vicious cycle of affects on the sustainability and growth of the banking system, and if not managed properly could lead to bank failure.

FACTORS RESPONSIBLE FOR NPAs The following factors confronting the borrowers are responsible for incidence of NPAs in the banks:- (i) Diversion of funds for expansion/modernization/setting up new projects/helping promoting sister concerns. (ii) Time/cost overrun while implementing projects. (iii) External factors like raw-material shortage, raw-material/Input price escalation, power shortage, industrial recession, excess capacity, natural calamities like floods, accident etc. 3 (iv) Business failure like product failing to capture market, inefficient management, strike/strained labour relations, wrong technology, technical problem, product obsolescence, etc. (v) Failure, non-payment/over dues in other countries, recession in other countries, externalization problems, adverse exchange rate, etc. (vi) Government policies like excise, import duty changes, deregulation, pollution control orders, etc. (vii) Wilful default, siphoning of funds, fraud, misappropriation, promoters/management disputes etc. Besides above, factors such as deficiencies on the part of the banks viz. deficiencies in credit appraisal, monitoring and follow-up; delay in release of limits; delay in settlement of payments/subsidies by Government bodies, etc. are also attributed for the incidence of NPAs3 . Indian Banking and NPA regulations: until mid eighties, management of NPAs was left to the banks and the auditors. In 1985, the first ever system of classification of assets for the Indian banking system was introduced on the recommendations of A. Ghosh Committee on Final Accounts. This system, called the ‘Health Code System’ (HCS) involved classification of bank advances into eight categories ranging from 1 (satisfactory) to 8 (bad and doubtful debt)4 . In

1991, the Narasimhan Committee on the financial system felt that the classification of assets according to the HCS was not in accordance with international standards and suggested that for the purpose of provision, banks should classify their advances into four broad groups, viz. (i) standard assets; (ii) substandard assets; (iii) doubtful assets; (iv) loss assets. Following this, prudential norms relating to income recognition, asset classification and provisioning were introduced in 1992 in a phased manner. In 1998, the Narasimhan Committee on Banking Sector Reforms recommended a further tightening of prudential standards in order to strengthen the prevailing norms and bring them on par with evolving 3 India, Lok Sabha (14th), Estimates Committee (2004-05), Sixth Report, presented on 25.4.2005,international best practices5 . With the introduction of 90-days norms for classification of NPAs in 2001, the NPA guidelines were brought as par with international standards6 . The NPAs can broadly be classified into (i) Gross NPAs, (ii) Net NPAs. Gross NPAs are the sum total of all loan assets that are classified as NPAs as per RBI guidelines as on balance sheet date. It reflects the quality of loans made by banks. (Gross NPAs Ratio = Gross NPAs/Gross Advances). Net NPAs are those type of NPAs in which the banks deduct the provisions regarding NPAs. It shows the actual burden of banks (Net NPAs = Gross NPAs-Provision/Gross Advances-Provisions).

.NPA IN INDIAN BANKING SYSTEM:

NPA surfaced suddenly in the Indian banking scenario, around the Eighties, in the midst of turbulent structural changes overtaking the international banking institutions ,and when the global financial markets were undergoing sweeping changes. In fact after it had emerged the problem of NPA kept hidden and gradually swelling unnoticed and unperceived, in the maze of defective accounting standards that still continued with Indian Banks up to the Nineties and opaque Balance sheets.

In a dynamic world, it is true that new ideas and new concepts that emerge through such changes caused by social evolution bring beneficial effects, but only after levying a heavy initial toll. existing set-up leads to an immediate disorder and unsettled conditions. People are not accustomed to the new models. These new formations take time to configure, and work smoothly. The old is cast away and the new is found difficult to adjust. Marginal and sub-marginal operators are swept

away by these convulsions. Banks being sensitive institutions entrenched deeply in traditional beliefs and conventions were unable to adjust themselves to the changes. They suffered easy victims to this upheaval in the initial phase.

Consequently banks underwent this transition-syndrome and languished under distress and banking crises surfaced in quick succession one following the other in many countries. But when the banking industry in the global sphere came out of this metamorphosis to re-adjust to the new order, they emerged revitalized and as more vibrant and robust units. Deregulation in developed capitalist countries particularly in Europe, witnessed a remarkable innovative growth in the banking industry, whether measured in terms of deposit growth, credit growth, growth intermediation instruments as well as in network.

During all these years the Indian Banking, whose environment was insulated from the global context and was denominated by State controls of directed credit delivery, regulated interest rates, and investment structure did not participate in this vibrant banking revolution. Suffering the dearth of innovative spirit and choking under undue regimentation, Indian banking was lacking objective and prudential systems of business leading from early stagnation to eventual degeneration and reduced or negative profitability. Continued political interference, the absence of competition and total lack of scientific decision-making, led to consequences just the opposite of what was happening in the western countries. Imperfect accounting standards and opaque balance sheets served as tools for hiding the shortcomings and failing to reveal the progressive deterioration and structural weakness of the country banking institutions to public view .This enabled the nationalized banks to continue to flourish in a deceptive manifestation and false glitter, though stray symptoms of the brewing ailment were discern able here and there.

The government hastily introduced the first phase of reforms in the financial and banking sectors after the economic crisis of 1991. This was an effort to quickly resurrect the health of the banking system and bridge the gap between Indian and global banking development. Indian Banking, in particular PSB’s suddenly woke up to the realities of the situation and to face the burden of the surfeit of their woes. Simultaneously major revolutionary transitions were taking place in other

sectors of the economy on account the ongoing economic reforms intended towards freeing the Indian economy from government controls and linking it to market driven forces for a quick integration with the global economy. Import restrictions were gradually freed. Tariffs were brought down and quantitative controls were removed. The Indian market was opened for free competition to the global players. The new economic policy in turn revolutionalized the environment of the Indian industry and business and put them to similar problems of new mixture Of opportunities and challenges. As a result we witness today a scenario of banking, trade and industry in India, all undergoing the convulsions of total reformation battling to kick off the decadence of the past and to gain a new strength and vigor for effective links with the global economy. Many are still languishing unable to get released from the old set-up, while a few progressive corporate are making a niche for themselves in the global context. During this decade the reforms have covered almost every segment of the financial sector. In particular, it is the banking sector, which experienced major reforms. The reforms have taken the Indian banking sector far away from the days of nationalization. Increase in the number of banks due to the entry of new private and foreign banks; increase in the transparency of the banks balance sheets through the introduction of prudential norms and norms of disclosure; increase in the role of the market forces due to the deregulated interest rates, together with rapid computerization and application of the benefits of information technology to banking operations have all significantly affected the operational environment of the Indian banking sector.

In the background of these complex changes when the problem of NPA was belatedly recognized for the first time at its peak velocity during 1992-93, there was resultant chaos and confusion. As the problem in large magnitude erupted suddenly banks were unable to analyze and make a realistic or complete assessment of the sur mounting situation. It was not realized that the root of the problem of NPA was centered else wherein multiple layers, as much outside the banking system, more particularly in the transient economy of the country, as within. Banking is not a compartmentalized and isolated sector delinked from the rest of the economy. As has happened elsewhere in the world, a distressed national economy shifts a part of its negative results to the banking industry. In short, banks are made ultimately to finance the losses incurred by constituent industries and businesses. The unprepared ness and structural weakness of our banking system to

act to the emerging scenario and de-risk itself to the challenges thrown by the new order, trying to switch over to globalization were only aggravating the crisis. Partial perceptions and hasty judgments led to a policy of ad-hoc-ism, which characterized the approach of the authorities during the last two-decades towards finding solutions to banking ailments and dismantling recovery impediments. Continuous concern was expressed. Repeated correctional efforts were executed, but positive results were evading. The problem was defying a solution.

The threat of NPA was being surveyed and summarized by RBI and Government of India from a remote perception looking at a birds-eye-view on the banking industry as a whole delinked from the rest of the economy. RBI looks at the banking industry average on a macro basis, consolidating and tabulating the data submitted by different institutions. It has collected extensive statistics about NPA in different financial sectors like commercial banks, financial institutions, urban cooperatives, NBFC etc. But still it is a distant view of one outside the system and not the felt view of a suffering participant. Individual banks inherit different cultures and they finance diverse sectors of the economy that do not possess identical attributes. There are distinct diversities as among the 29 public sector banks themselves, between different geographical regions and between different types of customers using bank credit. There are three weak nationalized banks that have been identified. But there are also correspondingly two better performing banks like Corporation and OBC. There are also banks that have successfully contained NPA and brought it to single digit like Syndicate (Gross NPA 7.87%) and Andhra (Gross NPA 6.13%). The scenario is not so simple to be generalized for the industry as a whole to prescribe a readymade package of a common solution for all banks and for all times. Similarly NPA concerns of individual Banks summarized as a whole and expressed as an average for the entire bank cannot convey a dependable picture. It is being statistically stated that bank X or Y has 12% gross NPA. But if we look down further within that Bank there are a few pockets possessing bulk segments of NPA ranging 50% to 70% gross , which should consequently convey that there should also be several other segments with 3 to 5% or even NIL % NPA, averaging the banks whole performance to 12%. Much criticism is made about the obligation of Nationalized Banks to extend priority sector advances. But banks have neither fared better in non-prioritysector.

The comparative performance under priority and non-priority is only a difference of degree and not that of kind.

The assessment of the mix-of contributing factors includes:

1. human factors (those pertaining to the bankers and the credit customers),

2. environmental imbalances in the economy on account of wholesale changes and also

3. Inherited problems of Indian banking and industry.

Variable skill, efficiency and level integrity prevailing in different branches and indifferent banks accounts for the sweeping disparities between inter-bank and intra-bank performance. We may add that while the core or base-level NPA in the industry is due to common contributory causes, the inter-se variations are on account of the structural and operational disparities. The heavy concentrated prevalence of NPA is definitely due to human factors contributing to the same.

No bank appears to have conducted studies involving a cross-section of its operating field staff, including the audit and inspection functionaries for a candid and comprehensive introspection based on a survey of the variables of NPA burden under different categories of sectoral credit, different regions and in individual Branches categorized as with high, medium and low incidence of NPA. We do not hear the voice of the operating personnel in these banks candidly expressed and explaining their failures. Ex-bankers, i.e. the professional bankers who have retired from service, but possess a depth of inside knowledge do not out-pour candidly their views. After three decades of nationalized banking, we must have some hundreds of retired Bank executives in the country, who can boldly and independently, but objectively voice their views. Everyone is satisfied in blaming the others. Bank executives hold willful defaulters responsible for all the plague. Industry and business blames the government policies.

Important fact-revealing information for each NPA account is the gap period between the date, when the advance was originally made and the date of its becoming NPA. If the gap is long, it is the case of a sunset industry. Things were

all right earlier, but economic variance in trade cycles or market sentiments have created the NPA. Credit customers who are in NPA today, but for years were earlier rated as good performers and creditworthy clients ranging within the top 50 or 100. Significant part of the NPA is on account of clout banking or willfully given bad loans. Infant mortality in credit is solely on account of human factors and absence of human integrity.

Credit to different sectors given by the PSB’s in fact represents different products. Advance to weaker sections below Rs.25000/- represents the actual social banking. NPA in this sector forms 8 TO 10% of the gross amount. Advance to agriculture, SSI and big industries each calls for different strategies in terms of credit assessment, credit delivery, project implementation, and post advance supervision. NPA in different sector is not caused by the same resultant factors. programmed by a sector-wise strategy involving a role of the actively engaged participants who can tell where the boot pinches in each case. Business and industry has equal responsibility to accept accountability for containment of NPA. Many of the present defaulters were once trusted and valued customers of the banks. Why have they become unreliable now, or have they?

The credit portfolio of a nationalized bank also includes a number of low-risk and risk-free segments, which cannot create NPA. Small personal loans against banks own deposits and other tangible and easily marketable securities pledged to the bank and held in its custody are of this category. Such small loans are universally given in almost all the branches and hence the aggregate constitutes a significant figure. Then there is food credit given to FCI for food procurement and similar credits given to major public Utilities and Public Sector Undertakings of the Central Government. It is only the residual fragments of Bank credit that are exposed to credit failures and reasons for NPA can be ascertained by scrutinizing this segment.

Secondly NPA is not a dilemma facing exclusively the Bankers. It is in fact an all pervasive national scourge swaying the entire Indian economy. NPA is a sore throat of the Indian economy as a whole. The banks are only the ultimate victims, where life cycle of the virus is terminated.

Now, how does the Government suffer? What about the recurring loss of revenue by way of taxes, excise to the government on account of closure of several lakhs of erstwhile vibrant industrial units and inefficient usage of costly industrial infrastructure erected with considerable investment by the nation? As per statistics collected three years back there are over two and half million small industrial units representing over 90percent of the total number of industrial units. A majority of the industrial work force finds employment here and the sectors contribution to industrial output is substantial and is estimated at over 35 percent while its share of exports is also valued to be around 40percent. Out of the 2.5 million, about 10% of the small industries are reported to be sick involving a bank credit outstanding around Rs.5000 to 6000 Crores, at that period. be even more now. These closed units represent some thousands of displaced workers Previously enjoying gainful employment. Each closed unit whether large, medium or small occupies costly developed industrial land. Several items of machinery form security for the NPA accounts should either be lying idle or junking out. In other words, large value of land, machinery and money are locked up in industrial sickness. These are the assets created that have turned unproductive and these represent the real physical NPA, which indirectly are reflected in the financial statements of nationalized banks, as the ultimate financiers of these assets. In the final analysis it represents instability in industry.NPA represents the owes of the credit recipients, in turn transferred and parked with the banks.

Recognizing NPA as a sore throat of the Indian economy, the field level participants should first address themselves to find the solution. Why not representatives of industries and commerce and that of the Indian Banks Association come together and candidly analyze and find an everlasting solution heralding the real spirit of deregulation and decentralization of management in banking sector, and accepting self-discipline and self-reliance? What are the deficiencies in credit delivery that leads to its misuse, abuse or loss? How to check

misuse and abuse at source? How to deal with erring Corporate? In short, the functional staff of the Bank along with the representatives of business and industry has to accept a candid introspection and arrive at a code of discipline in any final solution. And preventive action to be successful should start from the credit-recipient level and then extend to the bankers. RBI and Government of India can positively facilitate the process by providing enabling measures. Do not try to set right industry and banks, but help industry and banks to set right themselves. The new tool of deregulated approach has to be accepted in solving NPA.

REASONS FOR THE EXISTENCE OF HUGE LEVEL OF NPA’S IN THE INDIAN BANKING SYSTEM (IBS): The origin of the problem of burgeoning NPA’s lies in the quality of managing credit risk by the banks concerned. What is needed is having adequate preventive measures in place namely, fixing pre-sanctioning appraisal responsibility and having an effective post-disbursement supervision. Banks concerned should continuously monitor loans to identify accounts that have potential to become non-performing. To start with, performance in terms of profitability is a benchmark for any business enterprise including the banking industry. However, increasing NPA’s have a direct impact on banks profitability as legally banks are not allowed to book income on such accounts and at the same time banks are forced to make provision on such assets as per the Reserve Bank of India (RBI) guidelines. Also, with increasing deposits made by the public in the banking system, the banking industry cannot afford defaults by borrowers since NPA’s affects the repayment capacity of banks. Further, Reserve Bank of India (RBI) successfully creates excess liquidity in the system through various rate cuts and banks fail to utilize this benefit to its advantage due to the fear of burgeoning non-performing assets.

Some of the other reasons were:

• After the nationalization of banks sector wise allocation of credit disbursements became compulsory.

• Banks were compelled to give credit to even those sectors, which were not considered to be very profitable, keeping in mind the federal policy.

• People in the agricultural sector were hardly interested in returning the loans as they were confident that the loans with the interest would be written off by the successive governments.

• The small scale industries also availed credit even though they were not sure of performing to the extent of returning the loans.

• Banks were also not in the position to press enough securities to cover the loans in calls of timings.

• Even if the assets were provided they proved to be substandard assets as the values that could be realized were very low.

• Free distribution done during “loan mails” (congress regime) also contributed to the heavy increase in NPA’s.

• The slackness in effort by the bank authorities to collect or recover loan advances in time also contributes to the increase in NPA’s

. • Lack of accountability of the officers, who sanctioned the loans led to a caste whole approach by the officers recovering the loans.

• Loans sanctioned to under servicing candidates due to pressure from the ministers and other politicians also led to the non recovery of debts.

• Poor credit appraisal system, lack of vision while sanctioning credit limits.

• Lack of proper monitoring.

• Reckless advances to achieve the budgetary targets.

• Lack of sincere corporate culture, inadequate legal provisions on foreclosure and bankruptcy.

• Change in economic policies/environment.

• Lack of co-ordination between banks.

Some of the internal factors of the organization leading to NPA’s are:

• Division of funds for expansion, diversification, modernization, undertaking new projects and for helping associate concerns, this is coupled with recessionary trends and failure to tap funds in the capital and debt markets.

• Business failure( product, marketing etc.,),inefficient management, strained labor relations, inappropriate technology, technical problems, product obsolescence etc.,

• Recession , shortage of input, power shortage, price escalation, accidents, natural calamities, besides externalization problem in other countries leading to non payment of overdue.

• Time/cost overrun during the project implementation stage.

• Government policies like changes in the excise duties, pollution control orders.

• Willful default, siphoning off of funds, fraud, misappropriation, promoters/directors disputes etc.,

• Deficiencies on the part of the banks like delay in release of limits and delay in release of payments/subsidies by the government.

OPERATIONAL DEFINITION

NPA : An asset is classified as a non performing assets (NPA) if dues in the form of principal and interest are not paid by the borrower for a period of 90 days .

Standard Assets: Such an asset is not a non-performing asset. In other words, it carries not more than normal risk attached to the business.

Sub-standard Assets: It is classified as non-performing asset for a period not exceeding18 months .

Doubtful Assets: Asset that has remained NPA for a period exceeding 18 months is a doubtful asset.

Loss Assets: Here loss is identified by the banks concerned or by internal auditors or by external auditors or by Reserve Bank India (RBI) inspection

Cash Reserve Ratio (CRR): It is the reserve which the banks have to maintain with itself in the form of cash reserves or by way of current account with the Reserve Bank of India(RBI), computed as a certain percentage of its demand and time

liabilities. The objectives to ensure the safety and liquidity of the deposits with the banks.

Statutory Liquidity Ratio (SLR): It is the one which every banking company shall maintain in India in the form of cash, gold or unencumbered approved securities, an amount which shall not, at the close of business on any day be less than such percentage of the total of its demand and time liabilities in India as on the last Friday of the second preceding fortnight, as the Reserve Bank of India (RBI) may specify from time to time.

RBI GUIDELINES ON INCOME RECOGNITION (INTEREST INCOME ON NPA’s)

Income Recognition: Income from Non Performing Assets should not recognize on accrual basis but should be booked as income only when it is actually received. Therefore interest should not be charged and taken into income account till the account become standard asset.

♦ Interest charged to be stopped

♦ Provision to be made

Over Due: Any amount due to the Bank under any credit facility is

“Over due” if it is not paid on the due date fixed by the Bank.

Out of Order: An account should be treated as “out of order”

♦ If the outstanding balance remains continuously in excess of the sanctioned limit/ drawing power.

♦ In cases where the outstanding balance in the principal operating account is less than the sanctioned limit/ drawing power, but there are no credits continuously for 90 days as on the date of Bank’s Balance Sheet or Where are credits are not enough to cover the interest debited during the same period.

A Non Performing Asset shall be an advance where:

Term Loan: Interest and/ or installment of principal remain “over due” for a period of more than 90 days.

Cash Credit/ Over Draft: If the account remains out of order for a period more than90 days.

Bills: Overdue for a period of more than 90 days.

Other accounts: Any amount to be received remains overdue for a period of more than90 days.

Short duration crops: If the installment of principal or interest there on remains overdue for two crop seasons.

Long duration crops: If installment of principal or interest there on remains overdue for One Crop season.

An account would be classified as NPA only if the interest charged during any quarter is not serviced fully within 90 days from the end of the quarter.

ASSET CLASSIFICATION

Standard Assets: Is one which does not disclose any problem and which does not carry more than normal risks attached to the business.

Substandard Assets: Which has remained NPA for a period of less than or equal to 12 months.

Doubtful Assets: If it has remained NPA for a period exceeding 12 months

.Loss Assets: A loss asset is one where loss has been identified by the bank.

RBI GUIDELINES ON PROVISIONING REQUIREMENT OF BANK ADVANCES:

Loss Assets: 100% of the outstanding amount.

Doubtful Assets: 100% of unsecured portion.

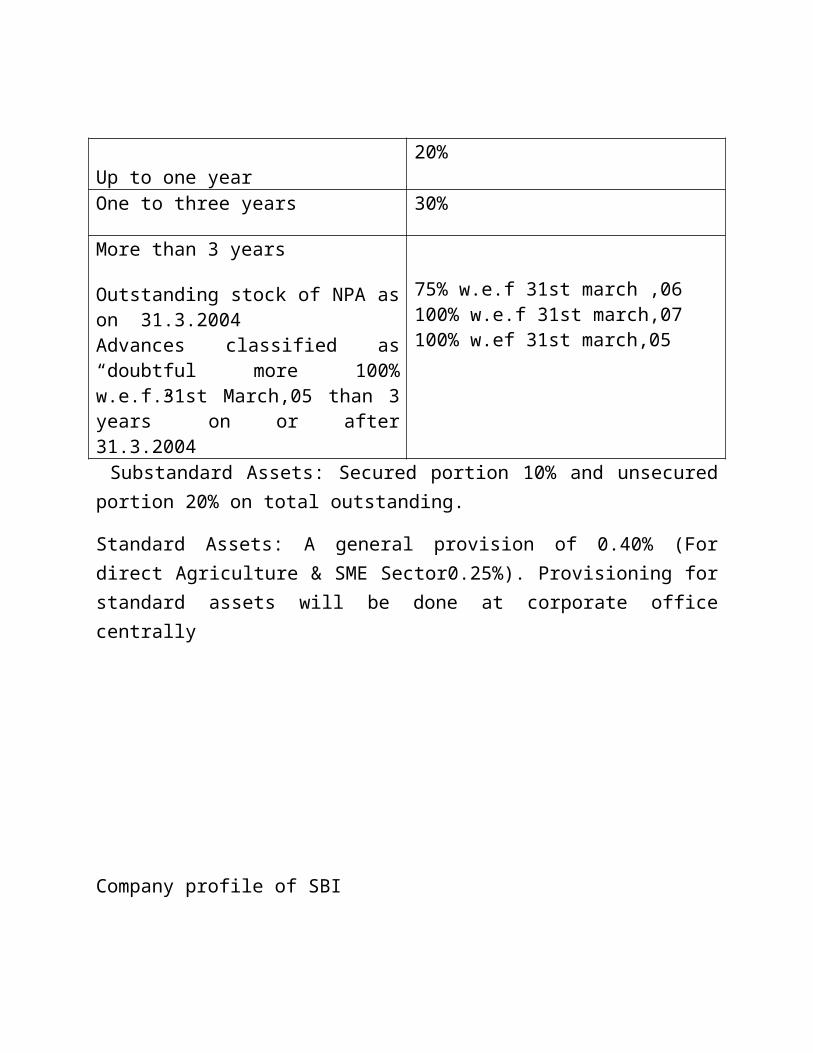

Secured portion

Up to one year 20%

One to three years 30%

More than 3 years

Outstanding stock of NPA as on 31.3.2004Advances classified as “doubtful more 100% w.e.f.31st March,05 than 3 years” on or after 31.3.2004

75% w.e.f 31st march ,06100% w.e.f 31st march,07100% w.ef 31st march,05

Substandard Assets: Secured portion 10% and unsecured portion 20% on total outstanding.

Standard Assets: A general provision of 0.40% (For direct Agriculture & SME Sector0.25%). Provisioning for standard assets will be done at corporate office centrally

Company profile of SBI

The evolution of State Bank of India can be traced back to the first decade of the 19th century. It began with the establishment of the Bank of Calcutta in Calcutta, on 2 June 1806. The bank was redesigned as the Bank of Bengal, three years later, on 2 January 1809. It was the first ever joint-stock bank of the British India, established under the sponsorship of the Government of Bengal. Subsequently, the Bank of Bombay (established on 15 April 1840) and the Bank of Madras(established on 1 July 1843) followed the Bank of Bengal. These three banks dominated the modern banking scenario in India, until when they were amalgamated to form the Imperial Bank of India, on 27 January 1921.

An important turning point in the history of State Bank of India is the launch of the first Five Year Plan of independent India, in 1951. The Plan aimed at serving the Indian economy in general and the rural sector of the country, in particular. Until the Plan, the commercial banks of the country, including the Imperial Bank of India, confined their services to the urban sector. Moreover, they were not equipped to respond to the growing needs of the economic revival taking shape in the rural areas of the country. Therefore, in order to serve the economy as a whole and rural sector in particular, the All India Rural Credit Survey Committee recommended the formation of a state-partnered and state-sponsored bank.

The All India Rural Credit Survey Committee proposed the take over of the Imperial Bank of India, and integrating with it, the former state-owned or state-associate banks. Subsequently, an Act was passed in the Parliament of India in May 1955. As a result, the State Bank of India (SBI)was established on 1 July 1955. This resulted in making the State Bank of India more powerful, because as much as a quarter of the resources of the Indian banking system were controlled directly by the State. Later on, the State Bank of India (Subsidiary Banks) Act was passed in1959. The Act enabled the State Bank of India to make the eight former State-associated banks as its subsidiaries.

The State Bank of India emerged as a pacesetter, with its operations carried out by the 480offices comprising branches, sub offices and three Local Head Offices, inherited from the Imperial Bank. Instead of serving as mere repositories of the

community savings and lending to creditworthy parties, the State Bank of India catered to the needs of the customers, by banking purposefully. The bank served the heterogeneous financial needs of the planned economic development.

Branches

The corporate center of SBI is located in Mumbai. In order to cater to different functions, t here are several other establishments in and outside Mumbai, apart from the corporate center. The bank boasts of having as many as 14 local head offices and 57 Zonal Offices, located at major cities throughout India. It is recorded that SBI has about 10000 branches, well networked to cater to its customers throughout India.

ATM Services

SBI provides easy access to money to its customers through more than 8500 ATMs in India. The Bank also facilitates the free transaction of money at the ATMs of State Bank Group, which includes the ATMs of State Bank of India as well as the Associate Banks – State Bank of Bikaner & Jaipur , State Bank of Hyderabad, State Bank of Indore, etc. You may also transact money through SBI Commercial and International Bank Ltd by using the State Bank ATM-cum-Debit (Cash Plus) card. State Bank Group includes a network of eight banking subsidiaries and several non-banking subsidiaries. Through the establishments, it offers various services including merchant banking services, fund management, factoring services, primary dealership in government securities ,credit cards and insurance

The eight banking subsidiaries are:

• State Bank of Bikaner and Jaipur (SBBJ)

• State Bank of Hyderabad (SBH)

• State Bank of India (SBI)

• State Bank of Indore (SBIR)

• State Bank of Mysore (SBM)

• State Bank of Patiala (SBP)

• State Bank of Saurashtra (SBS)

• State Bank of Travancore (SBT)

Products And Services

Personal Banking

• SBI Term Deposits SBI Loan For Pensioners

• SBI Recurring Deposits Loan Against Mortgage Of Property

• SBI Housing Loan Against Shares & Debentures

• SBI Car Loan Rent Plus Scheme

• SBI Educational Loan Medi-Plus Scheme Other Services

• Agriculture/Rural Banking

• NRI Services

• ATM Services

• Demat Services

• Corporate Banking

• Internet Banking 16

• Mobile Banking

• International Banking

• Safe Deposit Locker

• E-Pay

NPA MANAGEMENT IDENTIFICATION OF POTENTIAL NPA / STRESSED ASSETS

1. Reckoning of NPA : A NPA account to be identified based on its status / position of the accounts erosion in security as on the date of balance sheet of the bank. Nevertheless, the date of a NPA account would be the actual date on which the slippage occurred. If an account is regularized before the balance sheet date by repayment of overdue amount through genuine sources (not by sanctioning of additional facilities or transfer of funds between accounts), the account need not be treated as NPA.

It has, however, to be ensured that in the account remains in order subsequently and a solitary or few credits made in the account on or before the balance sheet date which extinguishes the overdue amount of interest or installment of principal is not reckoned as the sole criterion for treating the asset as standards one.

2. Identification and monitoring of potential NPA / stressed assets:

Indention of potential NPA account as its incipient stage of sickness and initiating immediate corrective measures is the most important step for preventing an asset from becoming NPA. The guidelines issued by Credit Monitoring Cell (CMC) CAD, HO should be followed in this regard.

3.Constitution pf NPA Prevention Cell at the ROs.

It has been decided to constitute a NPA Prevention cell at the ROs to monitor the Standard-B accounts and to ensure the prevention of their slippage to NPA. The cell headed by Regional Manager would comprise Regional Manager, Dy. Regional Manager and Credit Officer. It will conduct its meeting every fortnight.

ITS FUNCTION WILL BE AS UNDER:

To examine the information received from branches relating to Standard ‘B’ (based on 60 days norms), NPA accounts and identify the accounts for restructuring. The entire process should be completed within a time frame of 30 days.

To review the performance of the existing restructured accounts including BIFR and CDR cases.

The cell will send information on fortnightly basis to CMC, CAD Head Office.

Regional Manager to cell for the explanation from the Branch Managers whose performance in recovery is far from satisfactory.

3. Review and reporting of potential NPA / Stressed assets Following steps be taken for review and reporting of potential NPA / Stressed Assets:

Step-1: Analysis of reason of deterioration of health, signs of sickness, problem character of the Ac.

Step-2: Close interaction with the borrower, visit to the unit, close and frequent monitoring of the account, drawing the attention of the borrower to the irregularity / deterioration in he asset quality / signs of weakness in the account.

Step-3: Advice the borrower to correct the irregularity immediately in a time bound manner and obtain his categorical assurance.

Step-4: Corrective measures for prevention of slippages:

Review the account and consider sanction of need based working capital limits on merits, if the present limits are inadequate.

Identify Stressed Assets accounts and consider restructuring / realignment / re-schedulement on merits.

Early warning signal, if any, to be watched and addressed to.

Verification of (i) the documents for its correctness, enforceability, (ii) correctness of ROD (iii) insurance covers (iv) value/marketability of prime/collateral security eye.

Verification of existence of primary / collateral security of the borrower. Step-5: Report to the next higher authority, the details on the above aspects and suggesting specific corrective measures in time. Step-6: Implement the corrective action and report to higher authority.

5.Maintaining the Assets Quality :

Post sanction monitoring, supervision, and follow up Following measures should be put in place.(i) Terms and condition of the sanction: Terms and condition of sanction

have to be strictly complied with (ii) Verification: Verification of end use of the funds, stocks and assets

by Bank officials or through duly appointed concurrent auditors as per norms for effective monitoring of the accounts.

(iii) Legal Formalities: Formalities like obtaining / execution of documents / search certificates, registration of charges, timely revival of the documents, completion of equitable mortgage formalities etc. as per norms are the most important steps.

(iv) Stock Statements: Branches should obtain stock statements at monthly intervals regularly. As per RBI guidelines, the outstanding in the A/C based on the drawing powers calculated from stock statements older than 3 months would be deemed as irregular and if such irregular drawings are permitted for 90 days continuously, the A/C will be NPA.

6.Stock audit: Stock audit is to be conducted every year in every NPA account with outstanding limit of Rs 1 crore and above. However, wherever current assets are depleted or unit is closed, the stipulation may be exempted. 6. Management of NPA: The RMs personally verify and ensure that all accounts, especially high value advances are properly classified into standard, Sub-std. Doubtful or loss categories strictly as per prudential norms. It will be their responsibility to finalize and eliminate delay or postponed of identification of NPA. In case of doubts due to

any reason, RMs may seek guidance from HO and settle the matter within one month from the date on which the account would have been classified as NPA as per norms. It may be noted that if RBI observes any divergences in asset classification, especially in high value accounts due to willful non-compliance of RBI guidelines by any official responsible for classification then RBI may initiate deterrent action including imposition of monetary penalty.

7. Appropriation of recovery in NPAs:

a) Non decreed accounts: In case of NPA accounts in all categories i.e. Sub standard, Doubtful and Loss appropriated first against outstanding in the account and the surplus available, if any, is to be taken to interest / income. The same norm will be applicable to the compromised accounts also.

b) Decreed accounts: In case of decreed accounts where there is no compromise settlement amount recovered should be appropriated as per the decretal terms. However, if there is no specific term as regards appropriation of recovery in the decrial terms, the recovery should be appropriated first towards Principal and the balance towards interest.

(c) Appropriation of ECGC claim amount in NPA Accounts: As per the existing procedure, Bank is expected to keep the claim amount received from the ECGC in a separate memorandum account and pursue recovery efforts against the concerned Exporter borrower for the full amount of dues inclusive of the claim amount settled

Effects of NPA upon banks

A strong banking sector is important for flourishing economy. The failure of the banking sector may have an adverse impact on other sectors. Non-performing assets are one of the major concerns for banks in India. The only problem that hampers the possible financial performance of the public sector banks is the increasing results of the Non- performing Assets. The Non-performing Assets impacts drastically to the working of the banks. The efficiency of a bank is not always reflected only by the size of its balance sheet but by the level of return on its assets. NPAs do not generate interest income for the banks, but the same time banks are required to make provisions for such NPAs from their current profits.

1.They erode current profits through provisioning requirements. They result in reduced interest income.

2. They require higher provisioning requirements affecting profits and accretion to capital.

3. They limit recycling of funds, set in assets-liability mismatches, etc.

4. Adverse impact on Capital Adequacy Ratio.

5.ROE and ROA goes down because NPAs do not earn.

6.Bank’s rating gets affected.

7.Bank’s cost of raising funds goes up.

8. RBI’s approval required for declaration of dividend if Net NPA ratio is above 3%. Bad effect on Goodwill.

9.Bad effect on equity value.

The RBI has also develop many schemes and tools to reduce the NPA assets by introducing internal checks and control scheme, relationship mangers as stated by RBI who have complete knowledge of the borrowers, credit rating system , and early warning system and so on. The RBI has also tried to improve the securitization Act and SRFAESI Act and other acts related to the pattern of the borrowings.

Though RBI has taken number of measures to reduce the level of the Non performing Assets the result is not up to expectations. To improve NPAs each bank should be motivated to introduce their own precautionary steps. Before lending the banks must evaluate the feasible financial and operational prospective results of the borrowing companies or customer. They must evaluate the borrowing companies by keeping in considerations the overall impacts of all the factors that influence the business. NPAs reflect the performance of banks. A high level of NPAs suggests high probability of a large number of credit defaults that affect the profitability and net-worth of banks and also erodes the value of the asset. The NPA growth involves the necessity of provisions, which reduces the overall profits and shareholders’ value.

Causes for an Account becoming NPA

Those Attributable to Borrower

a) Failure to bring in Required capital

b) Too ambitious project

c) Longer gestation period

d) Unwanted Expenses

e) Over trading

f) Imbalances of inventories

g) Lack of proper planning

h) Dependence on single customers

I) Lack of expertise

j) Improper working Capital Mgmt.

k) Mismanagement

l) Diversion of Funds

m) Poor Quality Management

n) Heavy borrowings

o) Poor Credit Collection

p) Lack of Quality Control Causes Attributable to Banks a) Wrong selection of borrower b) Poor Credit appraisal c) Unhelpful in supervision d) Tough stand on issues e) Too inflexible attitude f) Systems overloaded g) Non inspection of Units h) Lack of motivation i) Delay in sanction j) Lack of trained staff k) Lack of delegation of work l) Sudden credit squeeze by banks m) Lack of commitment to recovery n) Lack of technical, personnel & zeal to work. 33

Other Causes a) Lack of Infrastructure b) Fast changing technology c) Un helpful attitude of Government d) Changes in consumer preferences e) Increase in material cost f) Government policies g) Credit policies h) Taxation laws I) Civil commotion j) Political hostility k) Sluggish legal system l) Changes related to Banking amendment Act 34.

Early symptoms by which one can recognize a performing asset turning in to Non-performing asset Four categories of early symptoms

:Financial: Non-payment of the very first installment in case of term loan. Bouncing of cheque due to insufficient balance in the accounts. Irregularity in installment Irregularity of operations in the accounts. Unpaid overdue bills. Declining Current Ratio Payment which does not cover the interest and principal amount of that installment While monitoring the accounts it is found that partial amount is diverted to sister concern or parent company.

Operational and Physical: If information is received that the borrower has either initiated the process of winding up or are not doing the business. Overdue receivables. Stock statement not submitted on time. External non-controllable factor like natural calamities in the city where borrower conduct his business. Frequent changes in plan Nonpayment of wages 35

Attitudinal Changes: Use for personal comfort, stocks and shares by borrower Avoidance of contact with bank Problem between partnersOthers: Changes in Government policies Death of borrower Competition in the market 36

38. SALE OF NPA TO OTHER BANKSA NPA is eligible for sale to other banks only if it has remained a NPA for at least twoyears in the books of the selling bankThe NPA must be held by the purchasing bank at least for a period of 15 months before itis sold to other banks but not to bank, which originally sold the NPA.The NPA may be classified as standard in the books of the purchasing bank for a periodof 90 days from date of purchase and thereafter it would depend on the record of recoverywith reference to cash flows estimated while purchasing.The bank may purchase/ sell NPA only on without recourse basis.If the sale is conducted below the net book value, the short fall should be debited to P&Laccount and if it is higher, the excess provision will be utilized to meet the loss onaccount of sale of other NPA. 37

39. Preventive Measurement forNPANPA Management Practices inIndiaMeasures Initiated by RBI forReduction of NPAsInternational Practices on NPAManagementDifficulties with NPAs 38

40. Preventive Measurement for NPAEarly Recognition of the Problem: Invariably, by the time banks start their efforts to get involved ina revival process, it’s too late to retrieve the situation- both in terms of rehabilitation ofthe project and recovery of bank’s dues. Identification of weakness in the very beginningthat is : When the account starts showing first signs of weakness regardless of the factthat it may not have become NPA, is imperative. Assessment of the potential of revivalmay be done on the basis of a techno-economic viability study. Restructuring should beattempted where, after an objective assessment of the promoter’s intention, banks areconvinced of a turnaround within a scheduled timeframe. In respect of totally unviableunits as decided by the bank, it is better to facilitate winding up/ selling of the unit earlier,so as to recover whatever is possible through legal means before the security positionbecomes worse.Identifying Borrowers with Genuine Intent: Identifying borrowers with genuine intent from those who arenon- serious with no commitment or stake in revival is a challenge confronting bankers.Here the role of frontline officials at the branch level is paramount as they are the oneswho has intelligent inputs with regard to promoters’ sincerity, and capability to achieveturnaround. Based on this objective assessment, banks should decide as quickly aspossible whether it would be worthwhile to commit additional finance. In this regard banks may consider

having “Special Investigation”of all financial transaction or business transaction, books of account in order to ascertain 39

41. real factors that contributed to sickness of the borrower. Banks may have penal of technical experts with proven expertise and track record of preparing techno-economic study of the project of the borrowers. Borrowers having genuine problems due to temporary mismatch in fund flow or sudden requirement of additional fund may be entertained at branch level, and for this purpose a special limit to such type of cases should be decided. This will obviate the need to route the additional funding through the controlling offices in deserving cases, and help avert many accounts slipping into NPA category. Timeliness and Adequacy of response: Longer the delay in response, grater the injury to the account andthe asset. Time is a crucial element in any restructuring or rehabilitation activity. The responsedecided on the basis of techno-economic study and promoter’s commitment, has to be adequatein terms of extend of additional funding and relaxations etc. under the restructuring exercise. Thepackage of assistance may be flexible and bank may look at the exit option. Focus on Cash Flows: While financing, at the time of restructuring the banks may not beguided by the conventional fund flow analysis only, which could yield a potentially misleadingpicture. Appraisal for fresh credit requirements may be done by analyzing funds flow inconjunction with the Cash Flow rather than only on the basis of Funds Flow. Management Effectiveness: The general perception among borrower is that it is lack of financethat leads to sickness and NPAs. But this may not be the case all the time. Management 40

42. effectiveness in tackling adverse business conditions is a very important aspect that affects aborrowing unit’s fortunes. A bank may commit additional finance to an align unit only afterbasic viability of the enterprise also in the context of quality of management is examined andconfirmed. Where the default is due to deeper malady, viability study or investigative auditshould be done – it will be useful to have consultant appointed as early as possible to examinethis aspect. A proper techno- economic viability study must thus become the basis on which anyfuture action can be considered. Multiple Financing: A. During the exercise for assessment of viability and restructuring, a Pragmatic and unified approach by all the lending banks/ FIs as also sharing of all relevant information on the borrower would go a long way toward overall success of rehabilitation exercise, given the

probability of success/failure. B. In some default cases, where the unit is still working, the bank should make sure that it captures the cash flows (there is a tendency on part of the borrowers to switch bankers once they default, for fear of getting their cash flows forfeited), and ensure that such cash flows are used for working capital purposes. Toward this end, there should be regular flow of information among consortium members. A bank, which is not part of the consortium, may not be allowed to offer credit facilities to such defaulting clients. Current account facilities may also be denied at non-consortium banks to such clients and violation may attract penal action. The Credit Information Bureau of India Ltd. (CIBIL) may be very useful for meaningful information exchange on defaulting borrowers once the setup becomes fully operational. C. In a forum of lenders, the priority of each lender will be different. While one set of lenders may be willing to wait for a longer time to recover its dues, another lender may have a much shorter timeframe in mind. So it is possible that the letter categories of lenders may be willing to exit, even a t a cost – by a discounted settlement of the exposure. Therefore, any plan for restructuring/rehabilitation may take this aspect into account. 41

43. D. Corporate Debt Restructuring mechanism has been institutionalized in 2001 to provide a timely and transparent system for restructuring of the corporate debt of Rs. 20 crore and above with the banks and FIs on a voluntary basis and outside the legal framework. Under this system, banks may greatly benefit in terms of restructuring of large standard accounts (potential NPAs) and viable sub-standard accounts with consortium/multiple banking arrangements. 42

44. NPA MANAGEMENT PRACTICES IN INDIA Formation of the Credit Information Bureau (India) Limited (CIBIL) Release of Willful Defaulter’s List. RBI also releases a list of borrowers with aggregate outstanding of Rs.1 crore and above against whom banks have filed suits for recovery of their funds Reporting of Frauds to RBI Norms of Lender’s Liability – framing of Fair Practices Code with regard to lender’s liability to be followed by banks, which indirectly prevents accounts turning into NPAs on account of bank’s own failure Risk assessment and Risk management RBI has advised banks to examine all cases of willful default of Rs.1 crore and above and file suits in such cases. Board of Directors are required to review NPA accounts of Rs.1 crore and above with special reference to fixing of staff accountability. Reporting quick mortality cases Special mention accounts for

early identification of bad debts. Loans and advances overdue for less than one and two quarters would come under this category. However, these accounts do not need provisioningNPA MANAGEMENT – RESOLUTION Compromise Settlement Schemes Restructuring / Reschedulement Lok Adalat Corporate Debt Restructuring Cell Debt Recovery Tribunal (DRT) Proceedings under the Code of Civil Procedure Board for Industrial & Financial Reconstruction (BIFR)/ AAIFR National Company Law Tribunal (NCLT) Sale of NPA to other banks Sale of NPA to ARC/ SC under Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act 2002 (SRFAESI) Liquidation 43

45. MEASURES INITIATED BY RBI AND GOVERNMENT OF INDIA FOR REDUCTION OF NPAs Compromise settlement schemes : The RBI / Government of India have been constantly goading the banks to take steps for arresting the incidence of fresh NPAs and have also been creating legal and regulatory environment to facilitate the recovery of existing NPAs of banks. More significant of them, I would like to recapitulate at this stage. The broad framework for compromise or negotiated settlement of NPAs advised by RBI in July 1995 continues to be in place. Banks are free to design and implement their own policies for recovery and write-off incorporating compromise and negotiated settlements with the approval of their Boards, particularly for old and unresolved cases falling under the NPA category. The policy framework suggested by RBI provides for setting up of an independent Settlement Advisory Committees headed by a retired Judge of the High Court to scrutinize and recommend compromise proposals. Specific guidelines were issued in May 1999 to public sector banks for onetime non-discretionary and non-discriminatory settlement of NPAs of small sector. The scheme was operative up to September 30, 2000. [Public sector banks recovered Rs. 668 crore through compromise settlement under this scheme.] Guidelines were modified in July 2000 for recovery of the stock of NPAs of Rs. 5 crore and less as on 31 March 1997. [The above guidelines which were valid up to June 30, 2001 helped the public sector banks to recover Rs. 2600 crore by September 2001] An OTS Scheme covering advances of Rs.25000 and below continues to be in operation and guidelines in pursuance to the budget announcement of the Hon’ble Finance Minister providing for OTS for advances up to Rs.50,000 in respect of NPAs of small/marginal farmers are being drawn up. 44

46. Negotiating for compromise settlements;The first crucial step towards meaningful NPA management is to accept that recoveries are onesown responsibility. To keep the Banks operating cycle going smoothly, it is essential that thisrealization of ones duties be transformed into deeds by resorting to various methods of recovery.Of the various methods available for NPA Management, Compromise Settlements are the mostattractive, if handled in a professional manner.Advantagesi) Saves money, time and manpowerBanks are mainly concerned with recovery of dues, to the maximum possible extent, at minimumexpense. By entering into compromise settlements, the objective is achieved. Also, a lot ofexecutive time is saved because most of the usual problems / delays associated with court actionare avoided.ii) Projects a helpful image of the BankA well-concluded compromise settlement, which results in a ‘WIN-WIN’ for the Bank as well asthe borrower, is a strong positive propaganda for the Bank. The impression generated is that theBank is capable not only of sympathy, but also empathy.iii) Expedites recycling of fundsCompromise settlements aim at quick recovery. Recovery means funds becoming available forrecycling and, additional interest generation.iv) Cleanses Balance SheetWith the NPA level going down, and the additional funds becoming available for recycling asfresh advances, the asset quality of the Bank is bound to go up. Improved asset quality signifieshigher profits by reduced provisions and increased interest income. With additions to thereserves, the capital position also improves, improving the Capital Adequacy position.Besides the above, compromise offers the best option when, i. The documents are defective and cannot be rectified, ii. security is not enforceable, iii. forced sale is extremely difficult, or would result only in realizing a paltry amount and iv. The borrowers become untraceable and recovery can be only though guarantors.Disadvantages i. Compromise involves loss, since full recovery is not possible. In fact, full recovery is not even envisaged, but sacrifice is. ii. It may be viewed as a reward for default, especially if chronic default cases are settled by negotiations. 45

47. iii. It may have a demonstrative effect, and so may vitiate the culture of repayment iv. There is also the possibility of misuse or, even, malafides, since assessment of situation is highly subjective. Practical aspects of compromise settlements Every compromise proposal needs to be looked at individually, evaluated strictly on merits, and negotiated properly for maximization of benefit to

the Bank. Hence, a straight jacket approach is not possible, neither is it desirable, to give strict guidelines for compromise settlements. Restructuring and RehabilitationA. Banks are free to design and implement their own policies for restructuring/ rehabilitation of the NPA accountsB. Reschedulement of payment of interest and principal after considering the Debt service coverage ratio, contribution of the promoter and availability of security Lok Adalats Lok Adalat institutions help banks to settle disputes involving accounts in “doubtful” and “loss” category, with outstanding balance of Rs.5 lakh for compromise settlement under Lok Adalats. Debt Recovery Tribunals have now been empowered to organize Lok Adalats to decide on cases of NPAs of Rs.10 lakhs and above. The public sector banks had recovered Rs.40.38 crore as on September 30, 2001, through the forum of Lok Adalat. The progress through this channel is expected to pick up in the coming years particularly looking at the recent initiatives taken by some of the public sector banks and DRTs in Mumbai. Some of features are Small NPAs up to Rs.20 Lacs Speedy Recovery Veil of Authority Soft Defaulters Less expensive Easier way to resolve 46

48. Debt Recovery Tribunals The Recovery of Debts due to Banks and Financial Institutions(amendment) Act, passed in March 2000 has helped in strengthening the functioningof DRTs. Provisions for placement of more than one Recovery Officer, power toattach defendant’s property/assets before judgment, penal provisions for disobedienceof Tribunal’s order or for breach of any terms of the order and appointment ofreceiver with powers of realization, management, protection and preservation ofproperty are expected to provide necessary teeth to the DRTs and speed up therecovery of NPAs in the times to come. Though there are 22 DRTs set up at major centers in the country withAppellate Tribunals located in five centers viz. Allahabad, Mumbai, Delhi, Calcuttaand Chennai, they could decide only 9814 cases for Rs.6264.71 crore pertaining topublic sector banks since inception of DRT mechanism and till September 30,2001.The amount recovered in respect of these cases amounted to only Rs.1864.30crore. Looking at the huge task on hand with as many as 33049 casesinvolving Rs.42988.84 crore pending before them as on September 30, 2001, I wouldlike the banks to institute appropriate documentation system and render all possibleassistance to the DRTs for speeding up decisions and recovery of some of the wellcollateralized NPAs involving large amounts. I may add that familiarizationprogrammes have been offered in NIBM at

periodical intervals to the presidingofficers of DRTs in understanding the complexities of documentation and operationalfeatures and other legalities applicable of Indian banking system. RBI on its part hassuggested to the Government to consider enactment of appropriate penal provisionsagainst obstruction by borrowers in possession of attached properties by DRTreceivers, and notify borrowers who default to honour the decrees passed againstthem. 47

49. Circulation of information on defaulters The RBI has put in place a system for periodical circulation of details of willful defaults of borrowers of banks and financial institutions. This serves as a caution list while considering requests for new or additional credit limits from defaulting borrowing units and also from the directors /proprietors / partners of these entities. RBI also publishes a list of borrowers (with outstanding aggregating Rs. 1 crore and above) against whom suits have been filed by banks and FIs for recovery of their funds, as on 31st March every year. It is our experience that these measures had not contributed to any perceptible recoveries from the defaulting entities. However, they serve as negative basket of steps shutting off fresh loans to these defaulters. I strongly believe that a real breakthrough can come only if there is a change in the repayment psyche of the Indian borrowers. Recovery action against large NPAs After a review of pendency in regard to NPAs by the Hon’ble Finance Minister, RBI had advised the public sector banks to examine all cases of willful default of Rs 1 crore and above and file suits in such cases, and file criminal cases in regard to willful defaults. Board of Directors are required to review NPA accounts of Rs.1 crore and above with special reference to fixing of staff accountability.On their part RBI and the Government are contemplating several supporting measures Asset Reconstruction Company: An Asset Reconstruction Company with an authorized capital of Rs.2000 crore and initial paid up capital Rs.1400 crore is to be set up as a trust for undertaking activities relating to asset reconstruction. It would negotiate with banks and financial institutions for acquiring distressed assets and develop markets for such assets. Government of India proposes to go in for legal reforms to facilitate the functioning of ARC mechanism 48

50. Legal Reforms The Honorable Finance Minister in his recent budget speech has alreadyannounced the proposal for a comprehensive legislation on asset foreclosure andSecuritization. Since enacted by way of Ordinance in June 2002 and passed byParliament as an Act in December 2002.Corporate Debt

Restructuring (CDR) Corporate Debt Restructuring mechanism has been institutionalized in2001 to provide a timely and transparent system for restructuring of the corporatedebts of Rs.20 crore and above with the banks and financial institutions. The CDRprocess would also enable viable corporate entities to restructure their dues outsidethe existing legal framework and reduce the incidence of fresh NPAs. The CDRstructure has been headquartered in IDBI, Mumbai and a Standing Forum and CoreGroup for administering the mechanism had already been put in place. Theexperiment however has not taken off at the desired pace though more than sixmonths have lapsed since introduction. As announced by the Hon’ble FinanceMinister in the Union Budget 2002-03, RBI has set up a high level Group under theChairmanship of Shri. Vepa Kamesam, Deputy Governor, RBI to review theimplementation procedures of CDR mechanism and to make it more effective. TheGroup will review the operation of the CDR Scheme, identify the operationaldifficulties, if any, in the smooth implementation of the scheme and suggest measuresto make the operation of the scheme more efficient.Credit Information Bureau Institutionalization of information sharing arrangements through thenewly formed Credit Information Bureau of India Ltd. (CIBIL) is under way. RBI isconsidering the recommendations of the S.R.Iyer Group (Chairman of CIBIL) tooperationalise the scheme of information dissemination on defaults to the financial 49

51. system. The main recommendations of the Group include dissemination of information relating to suit-filed accounts regardless of the amount claimed in the suit or amount of credit granted by a credit institution as also such irregular accounts where the borrower has given consent for disclosure. This, I hope, would prevent those who take advantage of lack of system of information sharing amongst lending institutions to borrow large amounts against same assets and property, which had in no small measure contributed to the incremental NPAs of banks. Proposed guidelines on willful defaults/diversion of funds RBI is examining the recommendation of Kohli Group on willful defaulters. It is working out a proper definition covering such classes of defaulters so that credit denials to this group of borrowers can be made effective and criminal prosecution can be made demonstrative against willful defaulters. Corporate Governance A Consultative Group under the chairmanship of Dr. A.S. Ganguly was set up by the Reserve Bank to review the supervisory role of Boards of banks and financial institutions

and to obtain feedback on the functioning of the Boards vis-à-vis compliance, transparency, disclosures, audit committees etc. and make recommendations for making the role of Board of Directors more effective with a view to minimizing risks and over-exposure. The Group is finalizing its recommendations shortly and may come out with guidelines for effective control and supervision by bank board’s over credit management and NPA prevention measures.[Dr. Bimal Jalan, Governor, RBI, in a speech titled "Banking and Finance in the NewMillennium." delivered at 22nd Bank Economists Conference, New Delhi, 5th February,2001] 50

52. INTERNATIONAL PRACTICES ON NPA MANAGEMENT Subsequent to the Asian currency crisis which severely crippled the financial system in most Inaddition to the above, some of the more recent and aggressive steps to resolve NPAs have beentaken by Taiwan. Taiwanese financial institutions have been encouraged to merge (though withlimited success) and form bank based AMCs through the recent introduction of FinancialHolding Company Act and Financial Institution Asian countries, the magnitude of NPAs inAsian financial institutions was brought to light. Driven by the need to proactively tackle thesoaring NPA levels the respective Governments embarked upon a program of substantial reform.This involved setting up processes for early identification and resolution of NPAs. The tablebelow provides a cross country comparison of approaches used for NPA resolution. MergersAct. Alongside the Ministry of Finance has followed a carrot and stick policy of specifying therequired NPA ratios for banks (5% by end 2003), while also providing flexibility in modes ofNPA asset resolution and a conducive regulatory and tax environment. Deferred loss write-offprovisions have been instituted to provide breathing space for lenders to absorb NPA write-offs.While it is too early to comment on’ he success of the NPA resolution process in Taiwan, theearly signs are encouraging. Detailed below are the some key NPA management approachesadopted by banks in South East Asian countries.1. Credit Risk MitigationAs part of the overall credit function of the bank, early recognition of loans showing signs ofdistress is a key component. Credit risk management focuses on assessing credit risk andmatching it with capital or provisions to cover expected losses from default.2. Early Warning SystemsLoan monitoring is a continuous process and Early Warning Systems are in place for staff tocontinuously be alert for warning signs.3. Asset Management CompaniesTo resolve NPA problems and help restore the health and confidence of the financial

sector, thecountries in South East Asia have used one broad uniform approach, i.e. they set up specializedAsset Management Companies (AMCs) to tackle NPAs and put in place Debt Restructuringmechanism to bring creditors and debtors together, often working along with independentadvisors. This broad approach was locally adapted and used with a varying degree of efficacyacross the region. For example, while in some countries a centralized government sponsoredAMC model has been used, in others a more decentralized approach has been used involving thecreation of several "bank-based" AMCs. Further different countries have allowed/used differentapproaches (in-house restructuring versus NPA Sale) to resolve their NPAs. Additionally, theefficacy of bankruptcy and foreclosure laws has varied in various countries. A number of factorsinfluenced the successful resolution of NPAs through sale to AMCs and some of these keyfactors are discussed below 51