Embed Size (px)

Citation preview

Exam NVQ/SVQ Level 4 in Accounting Preparing Personal Taxation Computations (PTC) 2003 Standards

Diploma in Accounting (Diploma Pathway) Preparing Personal Taxation Computations (PTC) 2003 Standards

Friday 22 June 2007 (morning) Time allowed - 3 hours plus 15 minutes’ reading time Please complete the following information in BLOCK CAPITALS: Student member number Desk number Venue code Date Venue name Important: This exam paper is in two sections. You should try to complete all tasks in both sections. We recommend that you use the 15 minutes’ reading time to study the exam paper fully and carefully so that you understand what to do for each task. However, you may begin to write your answers within the reading time, if you wish. We strongly recommend that you use a pen rather than a pencil. You may not use programmable calculators or dictionaries in the exam. Do NOT open this paper until instructed to do so by the Supervisor.

PTC

2

Note: You may use this page for your workings.

3

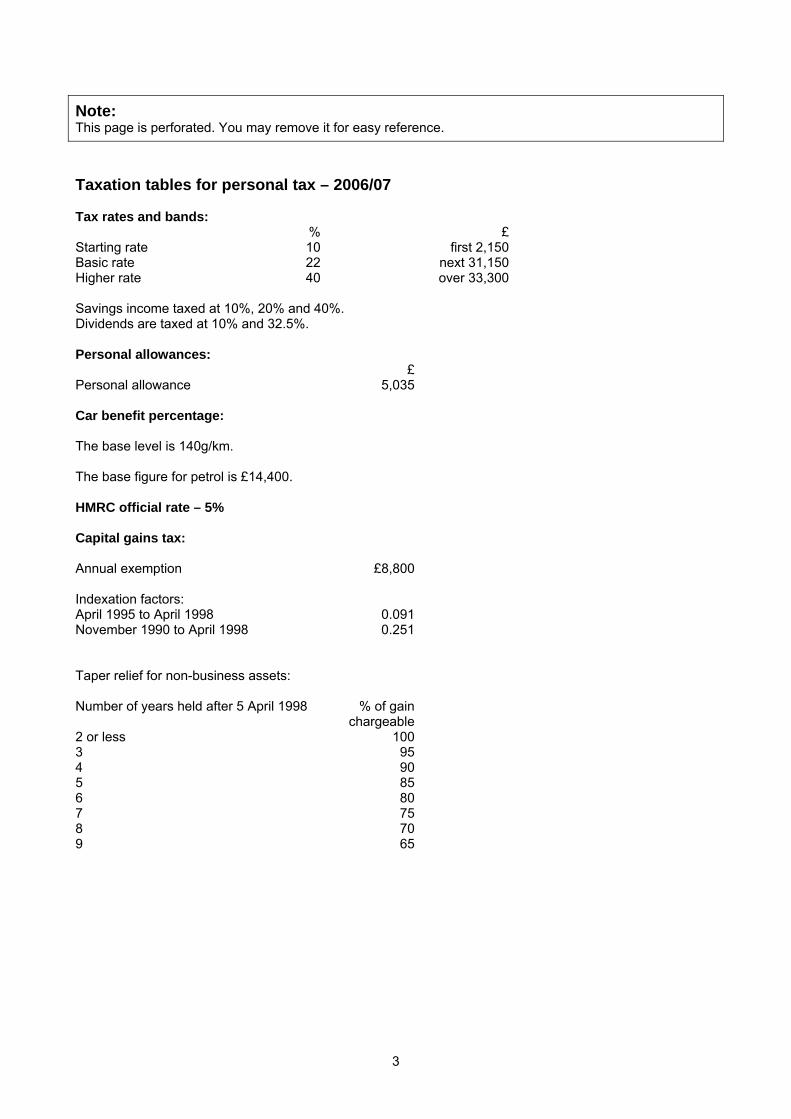

Note: This page is perforated. You may remove it for easy reference. Taxation tables for personal tax – 2006/07 Tax rates and bands: % £ Starting rate 10 first 2,150 Basic rate 22 next 31,150 Higher rate 40 over 33,300 Savings income taxed at 10%, 20% and 40%. Dividends are taxed at 10% and 32.5%. Personal allowances: £ Personal allowance 5,035 Car benefit percentage: The base level is 140g/km. The base figure for petrol is £14,400. HMRC official rate – 5% Capital gains tax: Annual exemption £8,800 Indexation factors: April 1995 to April 1998 0.091 November 1990 to April 1998 0.251 Taper relief for non-business assets: Number of years held after 5 April 1998 % of gain chargeable 2 or less 100 3 95 4 90 5 85 6 80 7 75 8 70 9 65

4

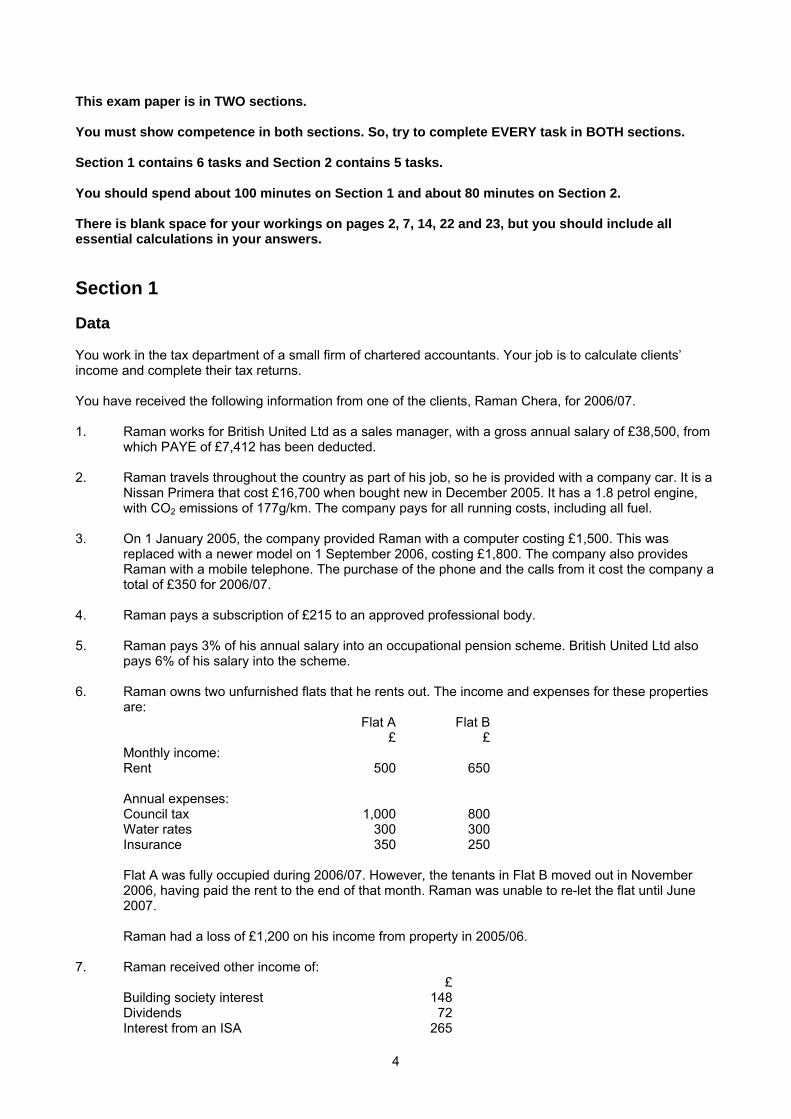

This exam paper is in TWO sections. You must show competence in both sections. So, try to complete EVERY task in BOTH sections. Section 1 contains 6 tasks and Section 2 contains 5 tasks. You should spend about 100 minutes on Section 1 and about 80 minutes on Section 2. There is blank space for your workings on pages 2, 7, 14, 22 and 23, but you should include all essential calculations in your answers. Section 1 Data You work in the tax department of a small firm of chartered accountants. Your job is to calculate clients’ income and complete their tax returns. You have received the following information from one of the clients, Raman Chera, for 2006/07. 1. Raman works for British United Ltd as a sales manager, with a gross annual salary of £38,500, from

which PAYE of £7,412 has been deducted. 2. Raman travels throughout the country as part of his job, so he is provided with a company car. It is a

Nissan Primera that cost £16,700 when bought new in December 2005. It has a 1.8 petrol engine, with CO2 emissions of 177g/km. The company pays for all running costs, including all fuel.

3. On 1 January 2005, the company provided Raman with a computer costing £1,500. This was

replaced with a newer model on 1 September 2006, costing £1,800. The company also provides Raman with a mobile telephone. The purchase of the phone and the calls from it cost the company a total of £350 for 2006/07.

4. Raman pays a subscription of £215 to an approved professional body. 5. Raman pays 3% of his annual salary into an occupational pension scheme. British United Ltd also

pays 6% of his salary into the scheme. 6. Raman owns two unfurnished flats that he rents out. The income and expenses for these properties

are: Flat A Flat B £ £ Monthly income: Rent 500 650 Annual expenses: Council tax 1,000 800 Water rates 300 300 Insurance 350 250 Flat A was fully occupied during 2006/07. However, the tenants in Flat B moved out in November

2006, having paid the rent to the end of that month. Raman was unable to re-let the flat until June 2007.

Raman had a loss of £1,200 on his income from property in 2005/06. 7. Raman received other income of: £ Building society interest 148 Dividends 72 Interest from an ISA 265

5

Task 1.1 Calculate the total assessable benefits in kind for 2006/07. If a benefit is not assessable, you need to state why.

6

Task 1.2 Calculate the assessable income from property for 2006/07.

7

Note: You may use this page for your workings.

8

Task 1.3 Prepare a computation of taxable income for 2006/07, clearly showing the distinction between the different types of income.

9

Task 1.4 Calculate the net income tax payable for 2006/07.

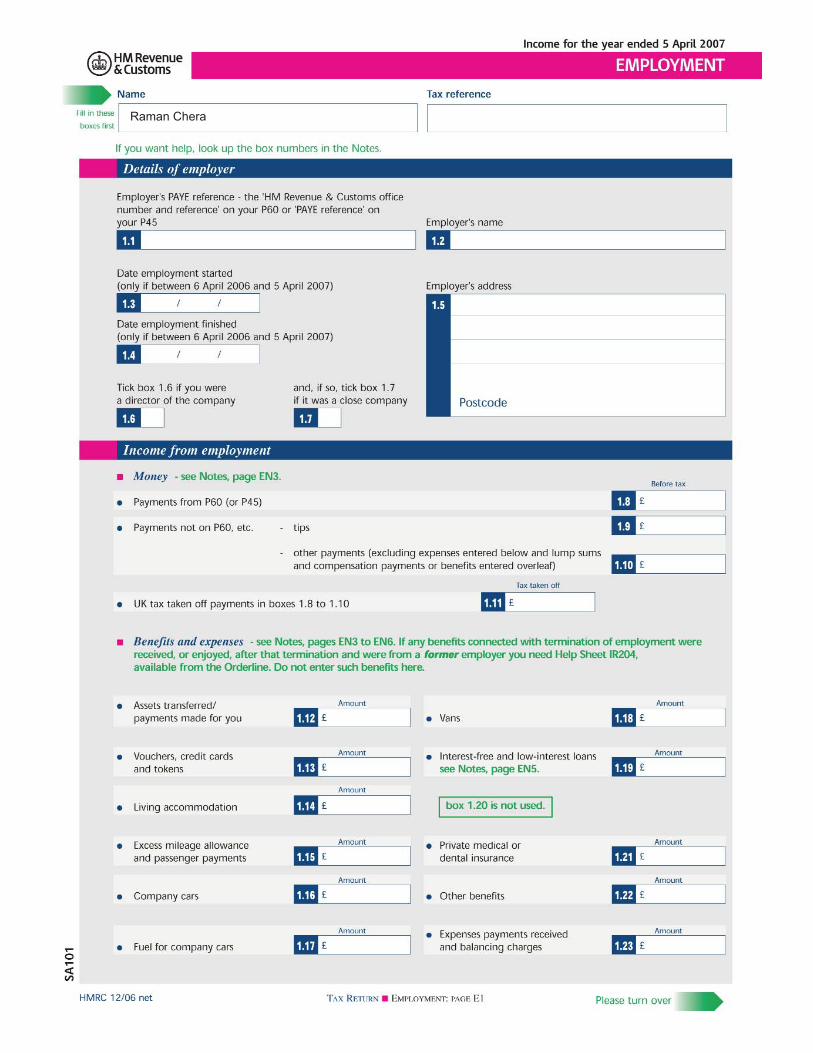

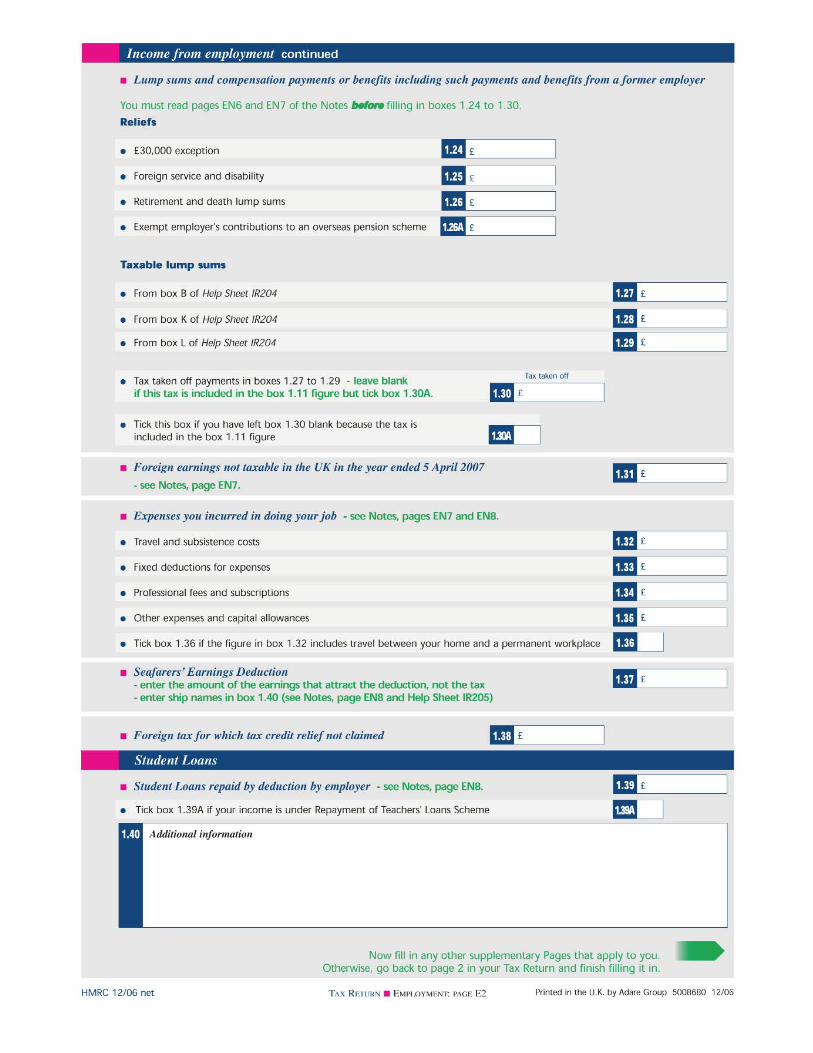

Task 1.5 Using the information you have been given, complete the tax return for Raman’s income from employment for 2006/07. The form you need is on pages 10 and 11.

Raman Chera

12

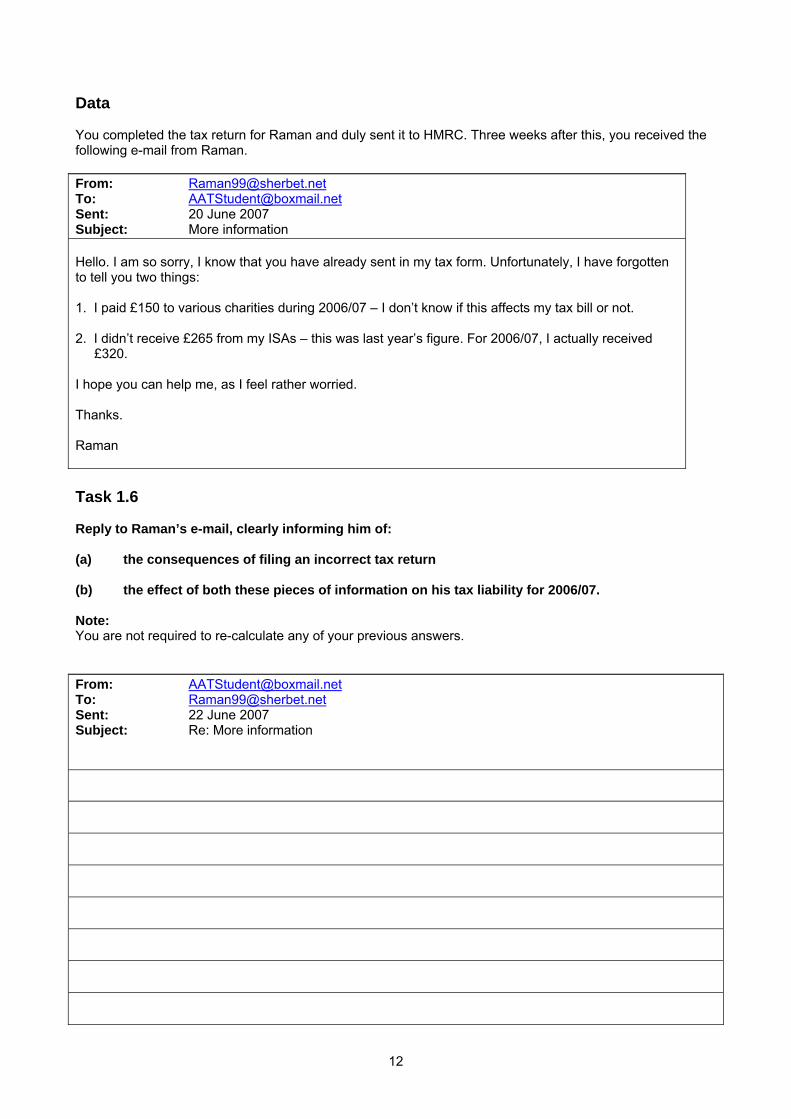

Data You completed the tax return for Raman and duly sent it to HMRC. Three weeks after this, you received the following e-mail from Raman. From: [email protected] To: [email protected] Sent: 20 June 2007 Subject: More information Hello. I am so sorry, I know that you have already sent in my tax form. Unfortunately, I have forgotten to tell you two things: 1. I paid £150 to various charities during 2006/07 – I don’t know if this affects my tax bill or not. 2. I didn’t receive £265 from my ISAs – this was last year’s figure. For 2006/07, I actually received

£320. I hope you can help me, as I feel rather worried. Thanks. Raman Task 1.6 Reply to Raman’s e-mail, clearly informing him of: (a) the consequences of filing an incorrect tax return (b) the effect of both these pieces of information on his tax liability for 2006/07. Note: You are not required to re-calculate any of your previous answers. From: [email protected] To: [email protected] Sent: 22 June 2007 Subject: Re: More information

13

This page is for the continuation of your e-mail. You may not need all of it.

14

Note: You may use this page for your workings.

15

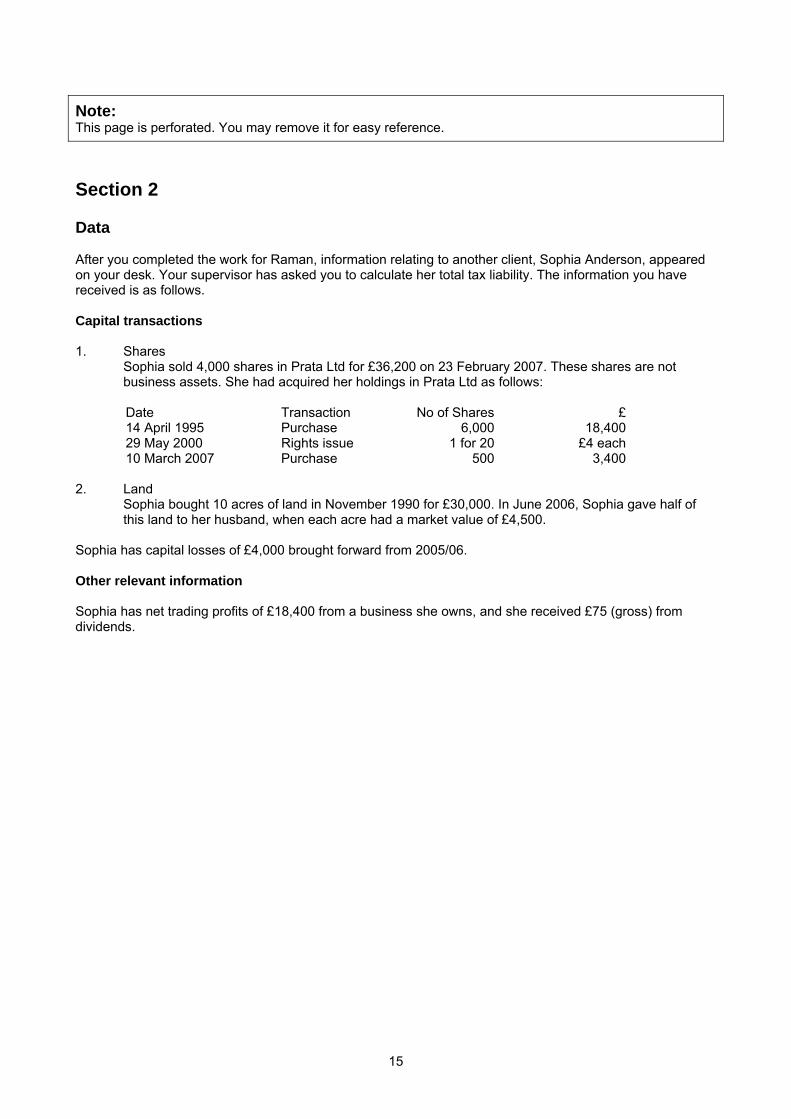

Note: This page is perforated. You may remove it for easy reference. Section 2 Data After you completed the work for Raman, information relating to another client, Sophia Anderson, appeared on your desk. Your supervisor has asked you to calculate her total tax liability. The information you have received is as follows. Capital transactions 1. Shares

Sophia sold 4,000 shares in Prata Ltd for £36,200 on 23 February 2007. These shares are not business assets. She had acquired her holdings in Prata Ltd as follows:

Date Transaction No of Shares £ 14 April 1995 Purchase 6,000 18,400 29 May 2000 Rights issue 1 for 20 £4 each 10 March 2007 Purchase 500 3,400 2. Land

Sophia bought 10 acres of land in November 1990 for £30,000. In June 2006, Sophia gave half of this land to her husband, when each acre had a market value of £4,500.

Sophia has capital losses of £4,000 brought forward from 2005/06. Other relevant information Sophia has net trading profits of £18,400 from a business she owns, and she received £75 (gross) from dividends.

16

Note: This page is intentionally blank. You should not use it for workings.

17

Task 2.1 Calculate the chargeable gain or loss, if any, made on the disposal of the shares in Prata Ltd, before taper relief. State the balance of shares to be carried forward for future disposal.

18

Task 2.2 Calculate the chargeable gain or loss, if any, made on the disposal of the land, before taper relief.

Task 2.3 Calculate the net taxable gains for the year 2006/07.

19

Task 2.4 Calculate for 2006/07: (a) the total income tax liability

(b) the total capital gains tax liability. State the date on which this tax liability is due.

20

Data You have received the following e-mail from Sophia. From: [email protected] To: [email protected] Sent: 20 June 2007 Subject: Advice Hi, I am hoping you can help me with some advice. I want to raise some money so that I can buy a timeshare in Portugal. I need about £7,500, and I have three assets that I think I can sell that would raise approximately this amount of money. The first one is a vintage car that I inherited from my father. I have no idea what he paid for it, but I think he bought it about 1950. I believe that it has a market value of £8,000. The second one is a painting that I bought in 1985 for £500. It turns out to be by a famous artist, and has a market value of £10,000. However, I really like this painting and would prefer not to sell it. The third asset I have is another painting that I bought in 1988 for £1,800. It should be worth about £5,800. Before I decide which one to sell to raise the money, I would like to understand the taxation implications of each sale. This is because I have already used up my annual capital gains tax exemption for 2007/08. Your advice and help in this matter would be greatly appreciated. Regards Sophia Task 2.5 Reply to Sophia’s e-mail informing her of the capital gains tax implications of each item. Note: Assume all tax rates in 2007/08 are the same as for 2006/07, and that Sophia is a basic rate tax

payer. From: [email protected] To: [email protected] Sent: 22 June 2007 Subject: Re: Advice

21

This page is for the continuation of your e-mail. You may not need all of it.

22

Note: You may use this page for your workings.

23

Note: You may use this page for your workings.

NVQ/SVQ qualification codes Technician (2003 standards) - 100/2942/4 / G794 24 Unit number (PTC) – M/101/8116 Diploma pathway qualification codes Diploma (2003 standards) – 100/5925/8 Unit number (PTC) – T/103/6455 © Association of Accounting Technicians (AAT) 06.07 154 Clerkenwell Road, London EC1R 5AD, UK t: +44 (0)20 7837 8600 fax: +44 (0)20 7837 6970 e-mail: [email protected] w: www.aat.org.uk

For Assessor’s use only

Section 1 Section 2 TASK 1.1 TASK 2.1

TASK 1.2 TASK 2.2

TASK 1.3 TASK 2.3

TASK 1.4 TASK 2.4

TASK 1.5 TASK 2.5

TASK 1.6

TOTAL TOTAL

For Assessor’s use only

Section 1 Section 2 TASK 1.1 TASK 2.1

TASK 1.2 TASK 2.2

TASK 1.3 TASK 2.3

TASK 1.4 TASK 2.4

TASK 1.5 TASK 2.5

TASK 1.6

TOTAL TOTAL