Embed Size (px)

Citation preview

Nyack College

Master of Business Administration

Submitted to: Professor Joseph Reid

Submitted by: Christopher Knott-Craig

110 W. 76th

Street Apt BR

NY, NY 10023

Work Phone: 310-923-5975

Home/Cell Phone: 310-923-5975

Email: [email protected]

Course Location: NCMC

Submission Date: September 30, 2015

Capstone Project Title:

EZESOFT DUBAI

CERTIFICATE OF AUTHORSHIP: I certify that I am the author of this paper and that any assistance I receive in its preparation is fully

acknowledged and disclosed in this paper. I have also cited any sources from which I used data,

ideas, or works, either quoted directly or paraphrased. I also certify that this paper was prepared by

me specifically for this course.

Student’s E-Signature:

Invalid signature

X Christopher Knott-Craig

Christopher Knott-Craig

Associate Director of Consulting

Signed by: [email protected]

Adviser’s Comments:

1

EzeSoft Dubai – A Business Proposal

September 2015

EzeSoft Dubai

Christopher Knott-Craig

A Capstone Research Project

Submitted in partial fulfillment

of the requirements for the degree

Master in Business Administration

School of Business and Leadership

Nyack College

September 30, 2015

Capstone Project Committee:

Dr. Gerard Becker, MBA Director

Professor Joseph Reid, Capstone Advisor

2

EzeSoft Dubai – A Business Proposal

September 2015

Table of Contents

Executive Summary ................................................................................................................ 6

Mission, Vision, Core Values ................................................................................................ 7

EzeSoft Mission Statement ......................................................................................... 7

EzeSoft Vision Statement ........................................................................................... 7

EzeSoft Principles ....................................................................................................... 8

EzeSoft Dubai Core Values ........................................................................................ 9

Industry and Proposed Company ............................................................................................ 10

Competitive Advantage .............................................................................................. 11

Complexity .................................................................................................................. 12

PEST Analysis ............................................................................................................ 12

Products and Services ............................................................................................................ 14

Product Description ................................................................................................... 14

Differentiation ............................................................................................................. 15

Product Delivery ......................................................................................................... 15

Potential Obstacles ...................................................................................................... 16

Future Growth ............................................................................................................. 16

Market Analysis ...................................................................................................................... 17

Market Size ................................................................................................................. 17

Growth Trends ............................................................................................................ 19

Economics of the Business ..................................................................................................... 20

Break-Even ................................................................................................................. 21

Competitor Intrusion ................................................................................................... 21

3

EzeSoft Dubai – A Business Proposal

September 2015

Marketing Plan ........................................................................................................................ 22

Strategic Partnership ................................................................................................... 22

Value Proposition............................................................................................ 23

Local Market Knowledge ............................................................................... 23

Direct Access to Customers ............................................................................ 23

Promotional Strategy .................................................................................................. 25

Brand Awareness ............................................................................................ 25

Client Prospecting ........................................................................................... 26

Decision to Purchase ....................................................................................... 26

Promotional Budget ........................................................................................ 27

Design and Development Plan ................................................................................................ 28

Manufacturing and Operations Plan ....................................................................................... 29

Location ...................................................................................................................... 29

Alignment ................................................................................................................... 31

Performance and Productivity ..................................................................................... 31

Profitability ..................................................................................................... 32

Customer Satisfaction ..................................................................................... 32

Consulting Return on Investment ................................................................... 33

Transparency ............................................................................................................... 34

Management Team.................................................................................................................. 36

Hiring .......................................................................................................................... 36

Reporting Structure ..................................................................................................... 37

4

EzeSoft Dubai – A Business Proposal

September 2015

Compensation and Benefits ........................................................................................ 37

Unexpected Departures ............................................................................................... 38

Overall Schedule ..................................................................................................................... 39

Phase 0: Ramp-Up ...................................................................................................... 39

Phase I: Go-Live ........................................................................................................ 40

Phase II: Growth Strategy ........................................................................................... 40

Critical Risks, Problems and Assumptions ............................................................................. 41

Internal Risks .............................................................................................................. 41

External Risks ............................................................................................................. 42

The Financial Plan .................................................................................................................. 44

Sales Forecasts ............................................................................................................ 44

Operating Costs ........................................................................................................... 46

Cash Flow Analysis .................................................................................................... 47

Profitability ................................................................................................................. 48

Proposed Funding Requirements ............................................................................................ 49

References ............................................................................................................................... 50

Appendix A ............................................................................................................................. 53

Appendix B ............................................................................................................................. 54

Appendix C ............................................................................................................................. 55

List of Tables

Table I: EzeSoft Company Principles ..................................................................................... 8

Table II: EzeSoft Corporate Pricing Policy ............................................................................ 22

Table III: EzeSoft Dubai Promotional Budget ........................................................................ 27

5

EzeSoft Dubai – A Business Proposal

September 2015

Table IV: Operating Costs – Most Likely Scenario ................................................................ 46

Table V: Operating Costs – Best Case Scenario ..................................................................... 46

Table VI: Operating Costs – Worst Case Scenario ................................................................. 46

Table VII: Profitability Forecasts – Most Likely Scenario ..................................................... 48

Table VIII: Profitability Forecasts – Best Case Scenario ....................................................... 48

Table IX: Profitability Forecasts – Worst Case Scenario ....................................................... 48

List of Figures

Figure 1: EzeSoft Dubai C.O.R.E. Values .............................................................................. 9

Figure 2: MENA Total Assets under Management by Country ............................................. 17

Figure 3: MENA Total Funds by Country .............................................................................. 18

Figure 4: MENA Global Competitiveness 2015 ..................................................................... 19

Figure 5: EzeSoft Dubai Promotional Strategy ...................................................................... 25

Figure 6: EzeSoft Dubai Overall Schedule ............................................................................. 39

Figure 7: EzeSoft Dubai SWOT Analysis .............................................................................. 41

Figure 8: EzeSoft Dubai Sales Forecast.................................................................................. 44

Figure 9: EzeSoft Dubai Cash Flow Projections .................................................................... 47

Figure 10: Allocation of Funding Requirements .................................................................... 49

6

EzeSoft Dubai – A Business Proposal

September 2015

Executive Summary

The Eze Software Group is entering an exciting and challenging new era of growth

marked by revenue and earnings goals for each of the next five years. This aggressive growth

strategy has spawned several, separate top-down initiatives stretching the short, medium, and

long-term with varying levels of success. With the increasingly competitive landscape in

EzeSoft’s primary markets of New York, London and Hong Kong, the firm has already

decided to pivot on the highly anticipated migration from on-premise to cloud-based

architecture in favor of alternative strategies requiring less time and fewer resources.

In order to achieve the ambitious growth, the firm should explore new geographic

markets as a potential for capturing additional market share and generating sustainable new

revenue streams. Ideal opportunities would only require limited planning and oversight from

senior management and the executive committee given their focus on large-scale initiatives

underway.

Such an opportunity can be created by expanding into the rapidly-growing United

Arab Emirates market and launching a new regional branch office in the Dubai International

Financial Centre. The manageable risks are easily justified by the impact of establishing a

strong foothold in this developing yet unchallenged market. With less than 1% of the 2016

R&D budget, EzeSoft Dubai will be operational by January 1, 2016, with a 9-month break-

even and 35% operating margins at the end of the three-year period including repayment of

startup funding.

7

EzeSoft Dubai – A Business Proposal

September 2015

Mission, Vision, Core Values

The Dubai regional office (EzeSoft Dubai) will embody the corporate mission, vision

and guiding principles of the Eze Software Group to ensure alignment with the company’s

culture and values.

EzeSoft Mission Statement

The corporate mission of the Eze Software Group is to “be a partner, not a vendor”.

EzeSoft Dubai will also strive for meaningful, lasting customer relationships by partnering

alongside every client to deliver inspiration, efficiency and opportunity through exceptional

products, services and experiences.

EzeSoft Vision Statement

The corporate vision of the Eze Software Group is “to be a leading global technology-

enabled solution provider for the financial services industry’s entire investment lifecycle.”

EzeSoft Dubai will embrace the same corporate vision is to become the unanimous global

leader in financial service technologies by fostering enduring, transformative growth at the

individual, team and organizational levels.

8

EzeSoft Dubai – A Business Proposal

September 2015

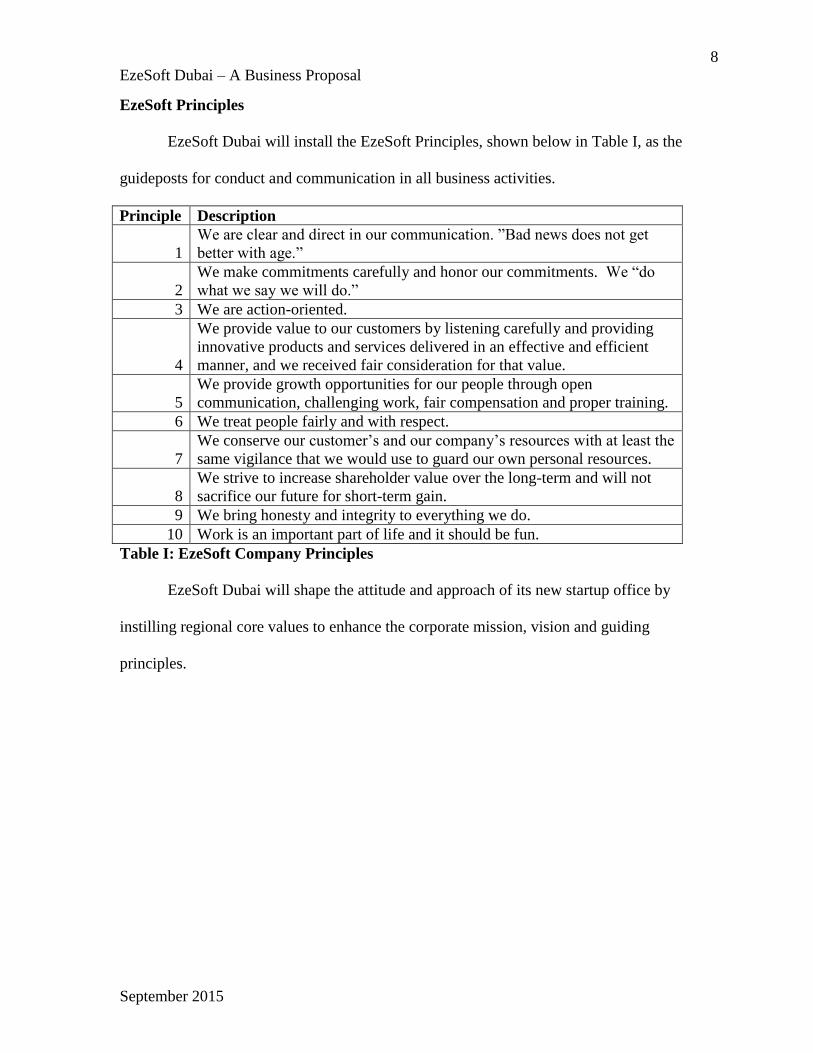

EzeSoft Principles

EzeSoft Dubai will install the EzeSoft Principles, shown below in Table I, as the

guideposts for conduct and communication in all business activities.

Principle Description

1

We are clear and direct in our communication. ”Bad news does not get

better with age.”

2

We make commitments carefully and honor our commitments. We “do

what we say we will do.”

3 We are action-oriented.

4

We provide value to our customers by listening carefully and providing

innovative products and services delivered in an effective and efficient

manner, and we received fair consideration for that value.

5

We provide growth opportunities for our people through open

communication, challenging work, fair compensation and proper training.

6 We treat people fairly and with respect.

7

We conserve our customer’s and our company’s resources with at least the

same vigilance that we would use to guard our own personal resources.

8

We strive to increase shareholder value over the long-term and will not

sacrifice our future for short-term gain.

9 We bring honesty and integrity to everything we do.

10 Work is an important part of life and it should be fun.

Table I: EzeSoft Company Principles

EzeSoft Dubai will shape the attitude and approach of its new startup office by

instilling regional core values to enhance the corporate mission, vision and guiding

principles.

9

EzeSoft Dubai – A Business Proposal

September 2015

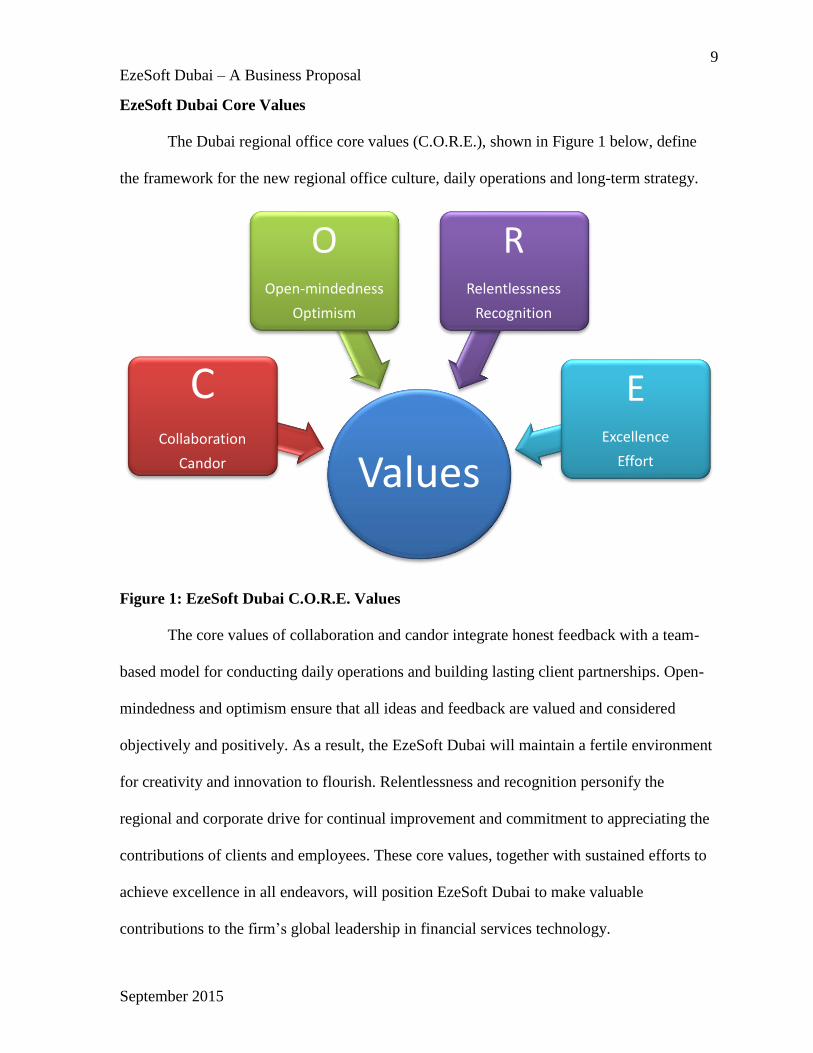

EzeSoft Dubai Core Values

The Dubai regional office core values (C.O.R.E.), shown in Figure 1 below, define

the framework for the new regional office culture, daily operations and long-term strategy.

Figure 1: EzeSoft Dubai C.O.R.E. Values

The core values of collaboration and candor integrate honest feedback with a team-

based model for conducting daily operations and building lasting client partnerships. Open-

mindedness and optimism ensure that all ideas and feedback are valued and considered

objectively and positively. As a result, the EzeSoft Dubai will maintain a fertile environment

for creativity and innovation to flourish. Relentlessness and recognition personify the

regional and corporate drive for continual improvement and commitment to appreciating the

contributions of clients and employees. These core values, together with sustained efforts to

achieve excellence in all endeavors, will position EzeSoft Dubai to make valuable

contributions to the firm’s global leadership in financial services technology.

Values

C Collaboration

Candor

O Open-mindedness

Optimism

R Relentlessness

Recognition

E Excellence

Effort

10

EzeSoft Dubai – A Business Proposal

September 2015

Industry and Proposed Company

In a recent study, Price Waterhouse Cooper estimated that as of 2012 the global

investment management industry managed a total of $64 trillion across pension funds,

mutual funds, insurance funds, alternative funds and wealth funds (Shooler, 2014). Further

analysis by Boston Consulting Group estimated that global assets under management

increased to $68.7 trillion in 2013, with similar increases in operating margins from 37% in

2012 to 39% in 2013 (Bartletta et al., 2014). General market sentiments agree that similar

increases can be expected in the assets under global investment management over the next 10

years. Furthermore, hedge fund participation in stock markets has accelerated considerably

over the last decade (Bianchi & Drew, 2010). Recent data from Hedge Fund Research

illustrates that total assets under management (AUM) have expanded to a record USD2.85trn,

with inflows of $71.2 billion into the largest number of active hedge funds (10,119) since the

initial onset of the global financial crisis in 2007. (Corporate Financing Week, Feb 2015).

With both fund inflows and the total number of funds on the rise, hedge fund AUM is

expected to reach a record high by year-end (2015).

The Eze Software Group is already well-positioned to benefit from this forecasted

growth in the firm’s established and emerging regional offices; however, stiff competition in

the primary markets in U.S. and Europe have required sales teams to become more

aggressive on pricing, reducing margins on new client sales. EzeSoft has recognized the

potential for additional revenue streams by strategically deploying local resources in

underserviced geographic regions with heightened growth expectations.

EzeSoft’s detailed internal market analysis revealed the United Arab Emirates (UAE)

as one of the strongest candidates for a new regional office, with over $80 billion in assets

11

EzeSoft Dubai – A Business Proposal

September 2015

under management and a greater concentration of funds – approximately 140 – than any

other nation in the Middle East (Eze Software Group, 2014). Additionally, the UAE boasts

over $600 billion in sovereign wealth fund assets available to invest in local hedge funds

(Research Monitor, 2015). Several Middle East and North Africa (MENA) industry experts

oblige that the UAE can capture the greatest market share in the $3.5 trillion global hedge

fund industry by continuing to promote local fund development through domestically

managed funds (Corporate Financing Week, Feb 2015).

Competitive Advantage

In terms of competitive threats, EzeSoft and the competitors currently conduct UAE

sales efforts remotely; however, EzeSoft internal market analysis revealed minimal on-the-

ground competition in the UAE (Eze Software Group, 2014). The nearest primary competitor

is located in Mumbai, India, which is approximately five hours closer by air than EzeSoft’s

Hong Kong and London regional offices. EzeSoft stands to gain a substantial competitive

advantage as the first buy-side technology provider to establish a branch office in the heart of

the Dubai International Financial Center, requiring less than a half-hour to visit prospective

and existing client offices. EzeSoft’s local presence can instantly boost the value proposition

and closing potential for the six local sales prospects in the immediate pipeline. Additionally,

the local office provides new opportunities to unlock new value and strengthen partnerships

with EzeSoft’s five existing UAE clients, who are currently serviced remotely by the London

and Hong Kong consulting teams.

12

EzeSoft Dubai – A Business Proposal

September 2015

Complexity

Compared with EzeSoft’s recent regional office launches in Brazil and Australia, the

prospect of a UAE office is substantially more appealing. Both Brazil and Australia have

proven to be substantially complex markets for EzeSoft to penetrate. In each emerging

region, new clients require lengthy, resource-intensive implementation plans including

several custom developments to accommodate client workflows unique to each region.

In contrast, the majority of UAE hedge funds are simple long-only equity or fixed

income funds and can be fully supported with the canned functionality available in the

EzeSoft platforms (Eze Software Group, 2014). Each of EzeSoft’s five existing UAE clients

was implemented without any custom development required and minimal support after go-

live.

PEST Analysis

The World Economic Forum (WEF) ranked the UAE as the best country globally in

terms of overall financial policies, with the government shaping fiscal policy to expand the

market through tax-free business zones and aggressive investing in infrastructure (2014). The

UAE boasts the strongest economy in the region, boosted by Dubai’s emerging reputation as

the next time zone hub to bridge Europe and Asia, and the country currently ranks 12th

on the

WEF’s Global Competitiveness Index (2014). A new generation of technology-focused,

sophisticated and open-minded locals, combined with a large ex-pat community, provides a

large talent pool for potential clients and employees (Euromonitor International, 2015). From

a technology standpoint, the UAE is leading the charge in Information and Communication

Technology (ICT) and continues to invest heavily in ICT infrastructure (2015). Furthermore,

the nation already owns the highest broadband penetration rates in the world (2015).

13

EzeSoft Dubai – A Business Proposal

September 2015

In summary, the UAE represents a largely underrepresented region with minimal

competition and substantial revenue potential through a large and growing pool of

prospective hedge fund clients. By establishing a local presence in the UAE, the Eze

Software Group can create instant opportunities to strengthen existing client partnerships and

accelerate the decision to purchase for active and future sales prospects. Reasonable growth

estimates extrapolated from the firm’s internal market analysis suggest that EzeSoft can

capture over 20% of the available market share in the UAE within three years of launching

the new EzeSoft Dubai office.

14

EzeSoft Dubai – A Business Proposal

September 2015

Products and Services

It is widely accepted that hedge funds today receive pressure from investors to

demonstrate active management and mitigation of operational risk in their day-to-day

processes. Along the same lines, it is increasingly common for investors to perform their own

due diligence before investing in hedge funds (Waksman, 2009). Consequently, hedge funds

are finding greater incentives to rely on third party software and services to facilitate daily

operational workflows and ensure alignment with industry best practices. Of the software

platforms available across the investment lifecycle, the order management system is single-

most valuable offering for hedge funds, providing a central hub for position analysis, PL

monitoring, order entry and execution, downstream transmission for settlement purposes, and

end of day reconciliation and reporting (cite). The order management system is used across

all business functions within the typical hedge fund structure, including portfolio managers,

analysts, traders, risk and compliance officers, and operations teams. As such, EzeSoft stands

to make the greatest impact on the UAE region by entering the market with its most

competitive offering and launching the EzeOMS as the primary product.

Product Description

The Eze Software Group established its foothold in the industry in the late nineties by

marketing its first product – the Eze order management system (EzeOMS) - to basic, long-

only equity funds. Similarly, the UAE hedge fund target market consists primarily of vanilla,

long-only investment strategies (Eze Software Group, 2014). As a result, EzeSoft will enter

the UAE market by promoting its most mature, competitive and relevant product – the

EzeOMS.

15

EzeSoft Dubai – A Business Proposal

September 2015

While the EzeOMS product offering remains attractive to various firms in the hedge

fund community, the product positioning and key differentiator versus competitors are

personified by the software consulting services and support included with the product. These

services enable the EzeSoft mission to be a partner, not just a vendor, and the unlimited

consulting support available to new clients is the heart of the EzeOMS value proposition.

Differentiation

The financial services industry includes a plethora of vendors with order management

system offerings; however, virtually all competitors charge clients separately for

implementation costs and bill clients at hourly rates for ongoing project management and

consulting services. The distinguishing factor between EzeSoft and other market competitors

lies in EzeSoft’s availability of experienced, collaborative consulting services that come with

the product. The new regional office provides EzeSoft with the local consulting presence

necessary for new local clients to take full advantage of the unlimited consulting resources

that are included with the EzeOMS licensing costs. Ultimately EzeSoft’s local presence in

the UAE will enable the firm to forge lasting partnerships with every existing and future

client, integrating client needs and requirements into the ongoing roadmap for industry best

practice.

Product Delivery

The delivery plan will align with EzeSoft’s corporate LEAN initiative, which targets

a seven week deadline for delivery, excluding any setbacks or delays from the client-side.

The aggressive implementation timeline starts as soon as the new client’s IT provides

EzeSoft with server access. Substantial tools and scripts have been created by EzeSoft’s

Consulting Strategy unit to automate the initial configuration of new client environments in

16

EzeSoft Dubai – A Business Proposal

September 2015

line with organizational best practice. In addition to system configuration, new client

implementations will adhere to EzeSoft’s current standard implementation plan to ensure

client on boarding is on track or ahead of schedule.

Potential Obstacles

The only potential obstacle regarding new client implementations revolves around the

unnecessary consulting support burden that arises when new clients are implemented with

poor workflow automation, inadequate user training or a failed adherence to best practice.

EzeSoft’s Consulting Strategy department has proactively countered these risks through

detailed documentation of the current Consulting-wide standards for new implementations. If

the new implementation standards and guidelines are followed, EzeSoft Dubai can mitigate,

if not eliminate, this overhead risk to consulting resources.

Future Growth

EzeSoft Dubai’s expansion strategy will promote the EzeOMS as the flagship product

during the initial launch; however, the firm’s historical performance has validated the

opportunity for continued growth by upselling existing EzeOMS clients with additional

offerings in the product suite, including EzeRisk, EzeTCA, EzeCompliance, EzeInterfacing

and EzeLocates. Each of these supplemental products integrates seamlessly with the

EzeOMS and requires minimal consulting resources to activate. EzeSoft Dubai is also

favorably positioned for long-term growth potential by expanding into neighboring markets

of Oman, Qatar and Saudi Arabia.

17

EzeSoft Dubai – A Business Proposal

September 2015

Market Analysis

With regional offices in the U.S., Brazil, Europe, Hong Kong, Singapore and

Australia, the established global presence of the Eze Software Group affords convenient

access to most of the leading financial markets. EzeSoft identified the Middle East and North

Africa (MENA) as a highly underrepresented region and key focus for geographic expansion.

The MENA region accounts for 15% market share of hedge fund assets under management,

with no local presence from any of EzeSoft’s largest competitors (Eze Software Group,

2014).

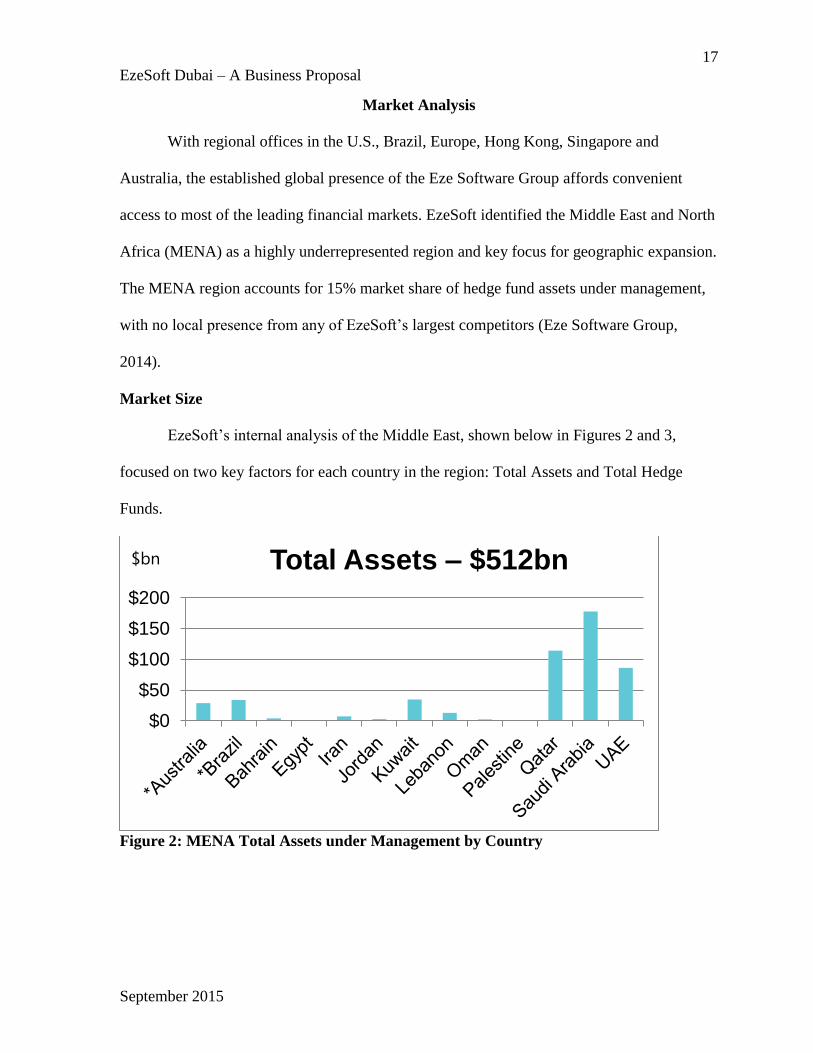

Market Size

EzeSoft’s internal analysis of the Middle East, shown below in Figures 2 and 3,

focused on two key factors for each country in the region: Total Assets and Total Hedge

Funds.

Figure 2: MENA Total Assets under Management by Country

$0

$50

$100

$150

$200

Total Assets – $512bn $bn

18

EzeSoft Dubai – A Business Proposal

September 2015

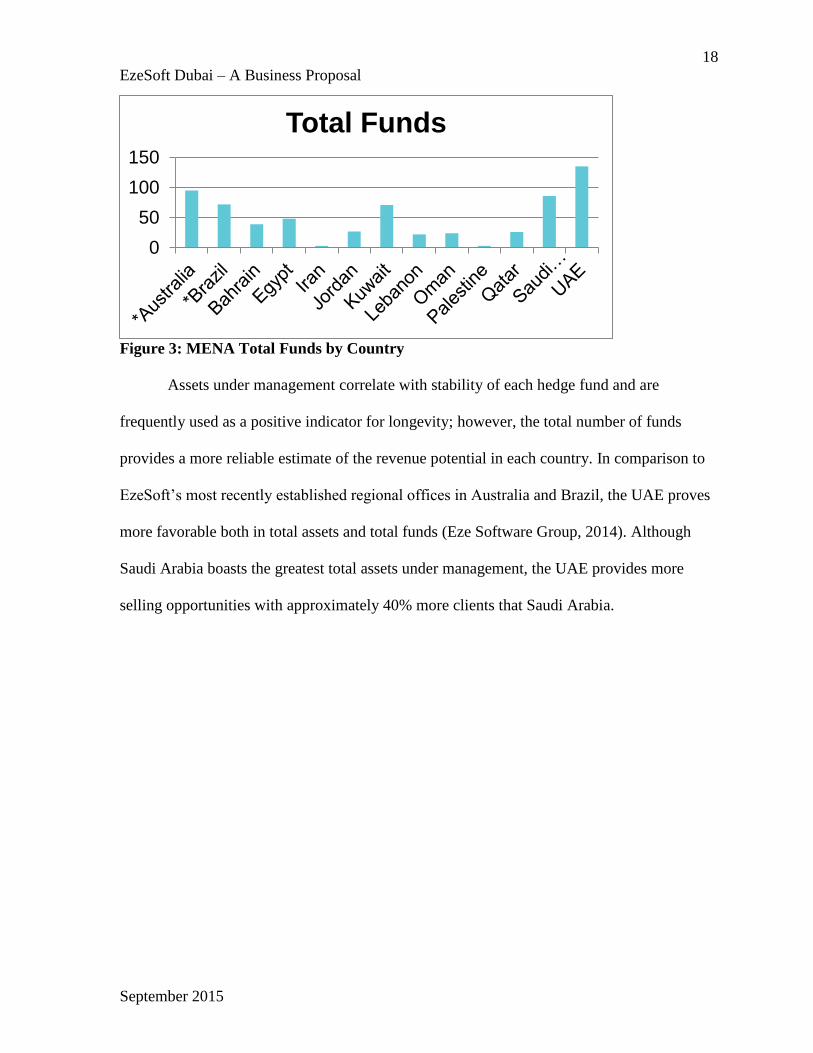

Figure 3: MENA Total Funds by Country

Assets under management correlate with stability of each hedge fund and are

frequently used as a positive indicator for longevity; however, the total number of funds

provides a more reliable estimate of the revenue potential in each country. In comparison to

EzeSoft’s most recently established regional offices in Australia and Brazil, the UAE proves

more favorable both in total assets and total funds (Eze Software Group, 2014). Although

Saudi Arabia boasts the greatest total assets under management, the UAE provides more

selling opportunities with approximately 40% more clients that Saudi Arabia.

0

50

100

150

Total Funds

19

EzeSoft Dubai – A Business Proposal

September 2015

Growth Trends

Since the global financial crisis, the UAE has aggressively worked to diversify the

national economy away from oil and real estate sectors by targeting aggressive growth in the

financial services, textiles and industrial sectors (Research Monitor, 2015). These efforts

have accelerated the UAE’s recovery and expanded appeal to the global economy, as

illustrated in Figure 4 below.

Figure 4: MENA Global Competitiveness 2015

The UAE currently ranks 12th

in terms of global competitiveness, outperforming all

other countries in the region and gaining ground year over year (World Economic Forum,

2015). The future outlook for wealth management is equally promising. Over the next five

years, the UAE is expected to double the world average in annual growth of investment

inflows, due in part to Dubai’s growing reputation as a major global center for finance

(Manyika et al., 2014). These inflows and Dubai’s rise as a finance hub are only a subset of

the various indicators supporting general expert sentiments that the nation is poised to see

further acceleration of growth and prosperity in the next five years.

20

EzeSoft Dubai – A Business Proposal

September 2015

Economics of the Business

The economics of the EzeSoft Dubai regional office have been determined by

conducting a historical analysis of the firm’s annual sales targets, average revenue per client,

average client support difficulty and average consulting hours per client across all major

regions globally. The analysis and cost estimates also emphasized the simple long-only fund

structure and low support burden of the five existing clients in the UAE. This historical

analysis was integrated with the existing UAE sales pipeline and EzeSoft market analysis to

generate three-year sales forecasts for the most likely, best-case and worst-case scenarios.

The sales targets for each distinct scenario were then used to extrapolate corresponding

projections for the total number of employees and associated fixed and marginal labor costs

required to service the region, including the implementation of new clients and ongoing

support of the expected client base expansion. Detailed estimates of the annual overhead

costs for the leasing office space, equipment and utilities were similarly derived from

EzeSoft’s internal market analysis and actual overhead cost figures from other recent

regional expansions. The firm’s internal analysis also incorporated the additional budget

required for initial and ongoing back-office functions including operations, finance,

accounting, marketing and legal to service the Dubai regional office. Finally, revenue

estimates for each scenario were generated based on sales targets, EzeSoft’s globally

standardized pricing schedule and the average revenue per existing client across all regions.

All revenue estimates leverage cash-based accounting and incorporate both aged receivables

and an allowance for doubtful accounts.

21

EzeSoft Dubai – A Business Proposal

September 2015

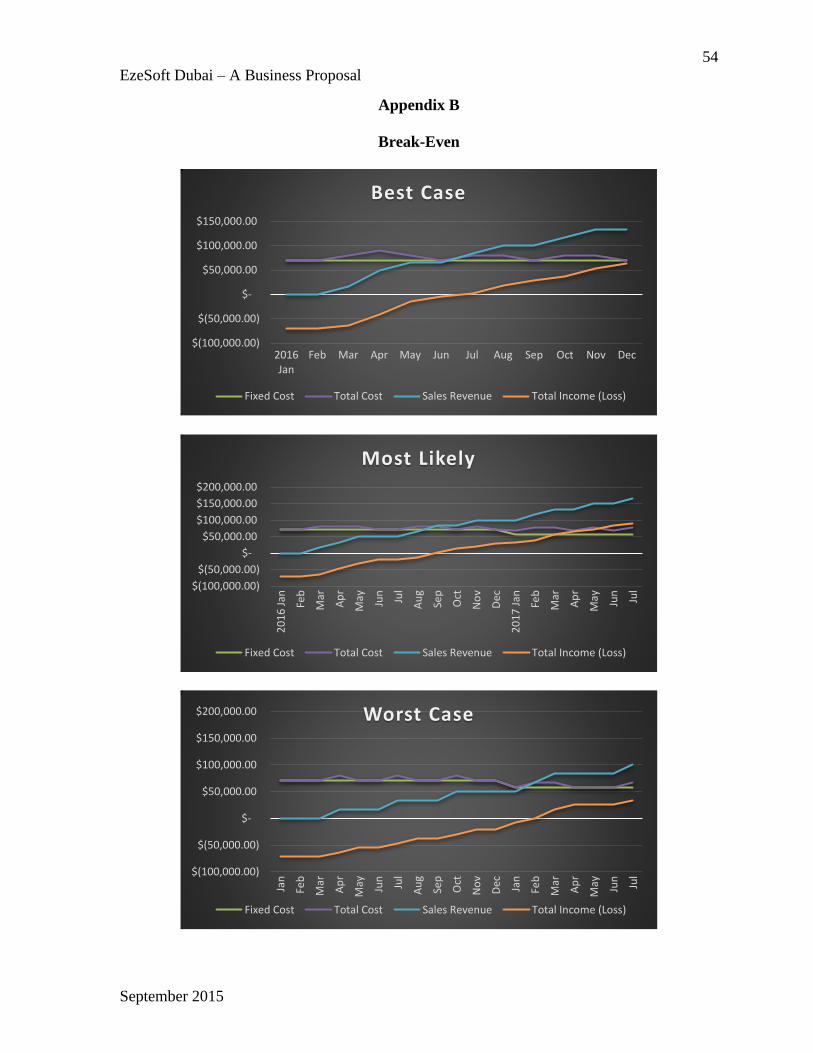

Break-Even

Based on the above-mentioned annual sales goals and estimated operating costs, a

three-year outlook of the most-likely scenario achieves break-even status in nine months,

with a 75% operating margin and 20% of the current client market share at the end of year

three. Similarly, the best case scenario reaches break-even in seven months, with 80%

operating margins and 25% market share after year three. Finally, the worst-case scenario

surpasses the break-even mark in fourteen months and ends the three-year outlook with a

61% operating margin and 12% of the hedge fund market. Detailed sales forecasts and break-

even analysis for each scenario are listed in Appendix A and Appendix B, respectively.

Competitor Intrusion

When EzeSoft competes against other vendors for new business, pricing often plays a

secondary role to reliability of the product and the quality of service. While EzeSoft’s

EzeOMS has been an award-winning product for over a decade, the firm’s partnership

framework and high-touch customer service model continues to serve as the key

differentiator. EzeSoft remains one of the industry’s most highly-valued buy-side technology

providers because no other competitors – large or small – have been able to mirror the firm’s

customer service model without disadvantageous pricing increases (Eze Castle Integration,

2015). While competitors may attempt to copy the EzeSoft Dubai strategy by entering the

UAE market, they will encounter the same challenges in matching customer service

excellence while staying competitive on pricing. Additionally, since the UAE business

environment operates on a trust basis, EzeSoft Dubai’s first mover advantage provides a head

start to establish trust and build local loyalty networks. This further limits the effectiveness of

any competitive intrusions into the UAE market.

22

EzeSoft Dubai – A Business Proposal

September 2015

Marketing Plan

The marketing plan for EzeSoft Dubai aligns with the organizational standards in

several areas; however, the success of the new regional office depends heavily on several key

region-specific elements.

EzeSoft Dubai will follow the model for all other regional offices by leveraging the

existing systems, tools and business processes available at the firm level. Similarly, product

pricing and contract negotiations, shown below, will remain standardized across the

organization. As with all other regions, the pricing and contract terms will continue to be

managed by EzeSoft’s global sales and business development functions.

User Count Annual License Fee Minimum Contract Length (Years)

1 100,000 3

6 200,000 3

11 275,000 3

16 325,000 3

Table II: EzeSoft Corporate Pricing Policy

23

EzeSoft Dubai – A Business Proposal

September 2015

Strategic Partnerships

With the right strategic partner, the sales team can gain immediate access to new

prospects in the region and accelerate sales efforts. EzeSoft’s existing alliance with Apex

Fund Service provides the best opportunity to achieve this based on the following

qualification criteria:

1. Value Proposition for Apex Fund Services

2. Demonstrated Local Market Knowledge and Experience

3. Direct Access to Local Customer Base

Value Proposition

Apex Fund Services and the EzeSoftware Group have already established a

healthy, collaborative relationship through a subset of mutual clients. While Apex Fund

Services has established a strong presence in the Middle East region, the firm faces stiffer

competition in the larger financial markets such as New York, London and Hong Kong.

EzeSoft’s sizeable footprint in these larger markets provides a substantial opportunity for

Apex Fund Services to expand their revenue streams through EzeSoft client referrals.

EzeSoft’s vast network of vendor relationships can be extended to Apex Fund Services,

allowing Apex to streamline electronic interfacing and integration with the auxiliary

platforms of other financial technology providers.

Local Market Knowledge

EzeSoft Dubai will need to build on existing knowledge of the client base in order to

continue providing excellence customer service and striving to be a partner, not just a vendor.

EzeSoft Dubai can benefit greatly from Apex Fund Services’ extensive experience and

proven success in the Middle East region and the UAE in particular through mutual

24

EzeSoft Dubai – A Business Proposal

September 2015

knowledge-sharing and education on best practice. Apex Fund Services has also established

key relationships with local governments and regulatory bodies in the region, from which the

EzeSoft Dubai office may benefit further.

Direct Access to Customers

Apex Fund Services has built up a healthy client base in the region over the last

decade. EzeSoft Dubai can substantially reduce sales timelines for new customer sales by

leveraging leads and referrals from Apex Fund Services. Similarly, EzeSoft Dubai and Apex

Fund Services can mutually benefit by packaging offerings together for prospective clients.

In summary, by establishing a strategic alliance with Apex Fund Services,

EzeSoftware Group provides a clear value proposition for our partner’s business offerings. In

return, EzeSoft Dubai may gain traction with the local customer base and acquire essential,

local market insights to better cope with the social, cultural, and organizational nuances

specific to the region. This in turn will help EzeSoft Dubai respond quickly to MENA

customer needs, thereby fulfilling our overarching corporate strategy of delivering top-tier

customer service. Overall, EzeSoft Dubai’s strategic partnership with Apex Fund Services

will allow each firm to secure greater competitive advantages in the MENA region while co-

creating additional long-term viability through additional growth opportunities globally.

25

EzeSoft Dubai – A Business Proposal

September 2015

Promotional Strategy

Before deploying resources on the ground, a four month promotional strategy will

enhance brand awareness and establish meaningful relationships with local market

participants. EzeSoft Dubai has identified three key communications objectives, shown

below in Figure 5.

Figure 5: EzeSoft Dubai Promotional Strategy

The promotional strategy has been formulated with specific components to address

each critical communications objective during the startup phase. A separate promotional

budget has been drawn up based on the anticipated costs of each promotional component.

Brand Awareness

The EzeSoftware Group’s Public Relations (PR) team will strategically target

regionally established electronic and print publications with an official press release of the

EzeSoft Dubai initiative. The firm will outsource to local PR experts to craft targeted

communications to local government and financial regulatory bodies in the region with the

intent of establishing new relationships with agency stakeholders participating in the

registration process for new hedge funds and asset management firms. EzeSoft will also

engage with existing UAE clients for guidance and assistance in raising awareness. These

relationships will be pursued further by the on-the-ground sales force to enhance brand

26

EzeSoft Dubai – A Business Proposal

September 2015

awareness. Print collateral, company supplies and other marketing material will be created

for sales teams to distribute as needed.

Client Prospecting

EzeSoft Dubai will appoint existing new client sales expert to ramp up the customer

base in during the first three years. Despite the abovementioned objective of enhancing brand

awareness through strategic networking and relationship building, the primary role of the

sales champion will be to prospect for new clients, close potential clients and engage existing

clients for referrals and leads. The EzeSoftware Group’s global cold-calling sales team may

augment local client prospecting efforts by cold-calling to set up meetings with potential

clients. A discretionary sales incentive will also be awarded to the sales representative for

exceeding the first-year sales goal.

Decision to Purchase

EzeSoft Dubai’s dedicated sales champion will be the primary component for moving

potential clients through the sales pipeline and converting prospects into new clients. In an

effort to accelerate growth of the client base, the sales member and global sales director will

have greater flexibility for aggressive pricing in order to close new client sales. If the sales

team requires additional pricing discounts in order to close the deal, the promotional

discounts will be noted in EzeSoft Dubai’s Microsoft Dynamics CRM and debited to EzeSoft

Dubai’s promotional budget under the sales incentives line item.

27

EzeSoft Dubai – A Business Proposal

September 2015

Promotional Budget

EzeSoft Dubai has estimated a total promotion budget of $350,000 for the first year to

cover all major components of the promotion strategy, illustrated in the table below.

Table III: EzeSoft Dubai Promotional Budget

While the final promotion budget encompasses planned expenditures for promotional

PR, marketing collateral and sales incentives, the running public relations and personal

selling components will remain separate from promotion budgeting and are incorporated into

EzeSoft Dubai’s annual overhead cost estimates. While sales incentives are limited to the

first year of expansion, EzeSoft Dubai will extend a slightly lower public relations and

marketing collateral budget year over year in order to further solidify the firm’s brand

awareness and secure the trust of local asset management participants.

Promotional Activity Year 1 Year 2 Year 3

Public Relations 130,000.00$ 100,000.00$ 100,000.00$

Collateral & Marketing Supplies 20,000.00$ 20,000.00$ 20,000.00$

Sales Incentives 200,000.00$ - -

Total Budget 350,000.00$ 120,000.00$ 120,000.00$

28

EzeSoft Dubai – A Business Proposal

September 2015

Design and Development Plan

The Eze Software Group has a fully viable product in the EzeOMS, with multiple

existing clients using the product for all daily operational needs. Each of the five existing

UAE clients was implemented without any custom development required and minimal

support after go-live. This fully substantiates that the local client base can be fully supported

with the canned functionality available. No further design and development will be required.

29

EzeSoft Dubai – A Business Proposal

September 2015

Manufacturing and Operations Plan

As a global competitor in the arena of financial technology providers, the chief

objective of the EzeSoft Dubai operations plan is to realize the unique strategic advantages

arising from establishing a local presence in the UAE. The proposed Dubai office does not

require any warehousing, plant facilities or manufacturing equipment and will consist solely

of client-facing business consultants and the local sales force for new client sales and

business development. While the EzeSoftware Group currently centralizes all Research and

Development (R&D), Quality Assurance (QA) and Tier II support functions, cost estimates

and planning have been conducted to ensure the Dubai regional office launches as scheduled

on January 1st, 2016. The relevant costs and planning and milestones are outlined in the

Overall Schedule section of the proposal.

The remainder of the operations plan will briefly expound on the rationale for

selecting Dubai as the UAE office location. The operations plan will then highlight the

regional strategy, Key Performance Indicators (KPIs) for measuring productivity, along with

the underlying business processes and transparencies required to sustain employee

motivation, maintain productivity and ensure regional alignment with the overarching

regional strategy.

Location

Research has shown that customer service oriented enterprises participating in the

financial services technology space can strategically benefit from establishing regional office

locations in close proximity to high-density customer bases. For technology providers, such

as the Eze Software Group, proximity to client offices promotes greater overall customer

30

EzeSoft Dubai – A Business Proposal

September 2015

satisfaction, existing client referrals, existing client sales, and new client sales (Cagliano, De

Marco, Rafele & Arese, 2012).

EzeSoft has already established a strong global presence, with regional offices in San

Francisco, Chicago, New York, Boston, London, Hong Kong, Singapore, Sydney, and Sao

Paolo. Despite the existing global presence, however, the sales strategy unit identified the

Middle East and North Africa as an underrepresented region with strong potential for new

client sales. The United Arab Emirates (UAE), and Dubai in particular, experienced notable

losses during the global financial crisis of 2008, especially in the financial industry and real

estate markets (Euromonitor International, 2015). Since the crisis, however, the UAE has

seen recoveries in both sectors along with a return to consistent economic growth (2015).

The recovery is being shaped primarily by a shift in government policy to reduce the UAE’s

dependency on oil by boosting growth in non-oil industries, especially manufacturing and

industrials, tourism, and the financial industry (Buckley & Hanieh, 2014). The UAE’s

financial development – the growth of local exchanges, institutions and banking sectors – has

produced a significant positive impact on economic growth, attracting hedge funds and other

institutional asset managers to the region (Masoud & Hardaker, 2012).

In summary, Dubai represents an invaluable geographic opportunity to establish

proximity to an under-represented, growing customer base of buy-side investment managers.

Furthermore, Dubai’s emergence as a transportation and tourism hub promote easy access to

neighboring markets within the MENA region.

31

EzeSoft Dubai – A Business Proposal

September 2015

Alignment

Over the years, extensive academic research has added credence to the notion that the

alignment of corporate and business strategies with operations management is considered

imperative for organizational success (Mitra & Bhardwaj, 2010). This entails a strategic fit of

the organization’s competitive strategy and operations management strategy – all functioning

units within the business should be incentivized to and rewarded by achieving the common

goal (2010).

The primary objectives of Dubai regional office will align with the Eze Software

Group’s primary competitive strategies: delivering client-driven, cutting edge products and

solutions, maintaining the highest levels of customer satisfaction, and increasing annual

operating margins year over year. The development, integration and delivery of new products

and services falls primarily under the Research and Development (R&D) and Product

Management (PM) business functions; however, the Dubai business consulting and sales

team holds the key to success in contributing to revenue targets and establishing and

maintaining superior customer satisfaction as EzeSoft establishes its presence in the UAE

region.

Performance and Productivity

Competitiveness favors those organizations that can continuously monitor and

improve the effectiveness of production and personnel alike, in addition to being able to

predict and act on new trends quickly (Prahalad & Krishnan, 2008). These abilities are

contingent upon structured measurement metrics, dynamic business processes and real-time

performance analytics (2008). Operations management teams rely on these critical elements

32

EzeSoft Dubai – A Business Proposal

September 2015

– performance measurement – in order to increase the productivity and profitability of the

enterprise (Domanović, Jakšić & Mimović, 2014).

Profitability

EzeSoft measures profitability using two Key Performance Indicators (KPIs):

Revenue and Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA).

The overarching organizational strategy is contingent on the ambitious goal of improving

“operating leverage” by generating higher revenues without increasing operating expenses.

Firm-wide KPIs currently target annual growth of 12% revenue and 8% EBITDA for each of

the next three years. In the spirit of competition, the Dubai regional office aims to outperform

both corporate KPIs based on the most likely scenario sales forecasts. If the Dubai region is

lagging on the revenue target, consulting resources will be redirected to increase sales to

existing customers. Similarly, any drag in earnings (EBITDA) will require the

implementation of proactive expense management procedures to scale back on spending.

Customer Satisfaction

Customer satisfaction will be assessed using two independent KPIs: implementation

life cycles for the primary suite of order management software and annual client-wide

satisfaction surveys. The implementation life cycle KPI will target a seven week timeframe

for standard implementations. Delays will need to be documented and categorized as client-

delays, internal delays, or external third party delays. For internal delays, additional

documentation of the each contributing factor to the delay will be required and reviewed for

opportunities to mitigate or avoid during future implementations.

EzeSoft corporate headquarters will circulate annual client satisfaction questionnaire

across all clients, with invoice credits offered as an incentive for clients to fully complete the

33

EzeSoft Dubai – A Business Proposal

September 2015

survey. For each customer, individual question responses are input through a complex,

proprietary algorithm that returns a “Net Promoter Score” (NPS). The company-wide KPI

aims for customers to score above a 7 (out of 10). Any client returning a score below 7 is

labeled as a “detractor” and special focus is given to the client until the client trends

positively out of the “detractor” zone. Customers with a NPS greater than 7 are considered

promoters, and are petitioned individually for potential new client referrals.

Consulting Return on Investment

A third, auxiliary KPI will leverage an internal timecard logging system to track and

categorize the number of consulting hours required per client. On a daily basis, client-facing

business consultants will log the number of hours spent working on individual clients in 30

minute increments and label the nature of work under one of three possible (Core 3)

categories: Production Support, Project Management and Account/Relationship

Management. Detailed criteria have already been established and on-going training is

provided to help consultants discern the appropriate Core 3 category to use to specific tasks.

Weekly, automated timecard reports are delivered to individual consultants for review,

breaking down the total hours spent with each client, and the nature of work required by

client. The Dubai consulting region will receive automated timecard reports illustrating the

total consulting hours invested per client, with drilldown capabilities to breakdown the type

of work completed for each client.

There primary purpose for this auxiliary KPI is to assess the Consulting Return on

Investment (CROI) for each client. By measuring the number of consulting hours invested

against the revenue generated for each client, the Dubai consulting region can identify low-

revenue clients demanding high volumes of consulting support. As a result, operations

34

EzeSoft Dubai – A Business Proposal

September 2015

management teams will be empowered to prioritize low CROI clients when identifying

methods to improve efficiency by reducing consulting workloads.

Currently CROI across global consulting averages out at $4000 revenue per hour of

Consulting support for live clients. EzeSoft Dubai ambitiously seeks to double this efficiency

metric by establishing day one precedents for best practice in workflow automation, thorough

user training up front and strict policy enforcement of client ownership and accountability

when it comes to managing their data and processes.

Transparency

Each of the abovementioned KPIs will be communicated clearly and consistently to

the Dubai consulting teams in an effort to promote transparency into the effectiveness of new

software implementations, overall client satisfaction levels and efficiency of consulting

teams in supporting clients. Additionally, this transparency initiative will help participants in

the Dubai regional office attach significance and relevance to their day-to-day operational

activities and their contributions to the long-term viability of the Eze Software Group (Harris,

Componation & Farrington, 2010). Financial incentives and bonus compensation will be

tiered-based according to year-end numbers versus the KPIs, providing consultants with

tangible motivators for achieving the overarching corporate strategy.

Conclusion

In summary, the launching of a new Dubai regional consulting office will afford the

Eze Software Group new avenues for profitability and sustained the competitive advantage

through closer proximity to an underrepresented, growing consumer base. By aligning with

EzeSoft’s overarching corporate strategy, adopting specific KPIs to measure performance

and productivity, and embracing transparency at each level within the business unit, the

35

EzeSoft Dubai – A Business Proposal

September 2015

Dubai regional office will be well-positioned as a new, meaningful contributor to the long-

term success of the Eze Software Group.

36

EzeSoft Dubai – A Business Proposal

September 2015

Management Team

The EzeSoft Dubai office launch will require the creation of three initial positions:

Business Consultant, Associate Director of Sales and Regional Director of Consulting. The

position titles are standardized across the Eze Software Group, and the EzeSoft Dubai office

will follow the firm’s formal role descriptions and requirements to determine eligible

candidates for relocation and, if warranted, promotion. Candidates for the Regional Director

of Consulting and Associate Director of Sales roles will be required to make a three-year

commitment. A two-year commitment will be required for applicants to the Business

Consultant role. Based on EzeSoft Dubai’s forecasted sales and growth, an additional

Business Consultant will be necessary in the second year of operation. EzeSoft Dubai will

attempt to fill this role by hiring locally. If no qualified candidates are accessible from the

local talent pool, the role will be filled internally by following the above-mentioned process.

This second consultant role will only require a one-year commitment.

Hiring

A formal company-wide memorandum will announce the new roles and give eligible

employees the opportunity to apply. The Eze Software Group already provides employees

with similar opportunities to apply for temporary stints in overseas offices. These

opportunities generate large interest across the firm, and it is likely there will be several

qualified candidates to evaluate for the three primary roles. Regardless, senior management

will separately evaluate EzeSoft’s global talent pool in search of top candidates to promote

up to the EzeSoft Dubai team. In addition to the standard role requirements, evaluation

criteria will favor tenacious candidates with proven outperformance in any combination of

client sales, new client implementations and relationship management. Further preference

37

EzeSoft Dubai – A Business Proposal

September 2015

will be given to individuals with multi-cultural backgrounds or extensive international travel

experience. As will all other international stints, senior management will conduct the

interview and decision-making process; however, a preliminary review of eligible employees

suggests that EzeSoft Dubai will have the greatest likelihood of success with Chris Knott-

Craig overseeing as Regional Director of Consulting. Still, the executive committee will need

to approve this recommendation before Chris can be appointed to the role.

Reporting Structure

EzeSoft Dubai will follow the same reporting structure as the London regional office,

reporting up to the EMEA unit. The Dubai Regional Director of Consulting will report to the

EMEA Senior Director of Consulting, and the Dubai Associate Director of Sales will report

to the EMEA Director of Sales. The Dubai Business Consultant will report in directly to the

Dubai Regional Director of Consulting.

Compensation and Benefits

The Eze Software Group leverages highly confidential salary bands to manage

employee compensation across the firm. Since only senior management and executives have

access to these figures, employee compensation must adhere to these role-related salary

ranges and will be managed as part of the interview process. Similarly, EzeSoft’s centralized

Human Resources function manages a standard, international benefits package for all

employees abroad. The HR team will provide the same standard benefits to EzeSoft Dubai

employees.

Unexpected Departures

EzeSoft Dubai must be prepared to quickly fill vacancies should any members of the

initial staff break their commitment and leave the firm. In the event of an unexpected

38

EzeSoft Dubai – A Business Proposal

September 2015

departure at the Associate Director of Sales or Business Consultant role, the role can be

temporarily filled internally with a six-month “air support” stint while EzeSoft interviews

local candidates as potential replacements. If the firm fails to fill the roles with local hires,

the positions will be filled internally following the same process for initial hiring. Air support

stints can by cycled through every six months until permanent replacements are found.

In the unlikely event that the Dubai Regional Director of Consulting resigns

unexpectedly, the Business Consultant will be promoted as an interim Regional Director

Senior management and the executive committee can determine whether to promote the

interim Regional Director or evaluate other internal candidates to permanently fill the

Regional Director of Consulting role. The vacancy created at the Business Consultant

position will be temporarily augmented with air support and permanently filled with either a

local hire or internal relocation, as described above.

39

EzeSoft Dubai – A Business Proposal

September 2015

Overall Schedule

EzeSoft Dubai will be fully operational as of January 1, 2016. The overall schedule,

shown in the figure below, will consist of three separate phases to focus on the preparation,

execution and expansion of the new regional office.

Figure 6: EzeSoft Dubai Overall Schedule

Phase 0: Ramp-Up

Phase 0 includes all the prerequisite administration required for the new office

launch. In accordance with EzeSoft’s consolidation of all employees under a single U.S.

entity, the EzeSoft Dubai office will be structured as an onshore foreign branch office and

located in the Dubai International Financial Centre (DIFC).The DIFC is a free zone that

awards zero tax liabilities and exemption from all cultural traditions and local laws to

financial services entities operating in the zone. The Dubai International Financial Centre

(DIFC) has enhanced the appeal to foreign firms by creating a surprisingly simple and

efficient process for business registration as a foreign branch office that takes a maximum of

four weeks to complete. The Eze Software Group’s middle office and back office teams

estimate that the new region can be fully set up internally within eight weeks. The ramp-up

Phase 0: Ramp-Up - Sep 2015 through Dec 2015

Dubai Business Registration

EzeSoft Middle and Back Office Administration

Marketing - Ramp-Up Promotion Strategy

Relocation and Office Launch 4 weeks

Phase 1: Go-Live - Dec 2015 through Dec 2018

Existing UAE Clients - Coverage Transition from London to Dubai 1 week

Consulting Support of Existing UAE Clients

Marketing - Start-Up Promotion Strategy

Concentrated Sales Focus on New Clients in UAE (Dubai & Abu Dhabi)

New Client Implementations (Sales Dependent)

Phase 2: Growth Strategy - Jan 2019 and Beyond

Consulting Support of Existing Clients

Continued Sales Focus on New Clients in UAE

Expanded Sales Focus on New Clients in Neighboring Markets

(Qatar, Saudi Arabia, Oman)

New Client Implementations (Sales Dependent)

ongoing

ongoing

ongoing

ongoing

8 weeks

12 weeks

4 weeks

Timeline for Completion

Timeline for Completion

Timeline for Completion

1 year

3 years

3 years

3 years

40

EzeSoft Dubai – A Business Proposal

September 2015

promotional campaign will run the last 12 weeks of the year to generate publicity, enhance

brand awareness and enable the Sales team to hit the ground running. In the final eight weeks

of ramp-up, a series of cross-training sessions will be coordinated for all existing UAE

clients to ensure detailed and comprehensive documentation and transfer of account

knowledge between the London and Dubai teams. The ramp-up phase will conclude with the

setup of the new office and relocation of each EzeSoft Dubai employee during the last

month.

Phase I: Go-Live

Phase I focuses on the execution and establishment of the new office. During the first

week of operation in the new office, the existing UAE clients will be the top priority. All

members of the Dubai team will participate in on-site client transitions to meet the members

at each firm. The start-up promotion strategy will continue through the first year of operation

in Dubai to facilitate the sales effort to exceed goals and expand the client base. The sales

effort will concentrate solely on the UAE, with special focus on Dubai and Abu Dhabi as the

major nerve centers for hedge funds. Consulting resources will be limited to the support of

existing UAE clients until sales delivers new customers to implement.

Phase II: Growth Strategy

At the end of the three year mark, once the EzeSoft Dubai has established a strong

presence in the UAE, the organization may augment new client sales in the UAE by

allocating business development resources to upsell the existing client-base with product

add-ons to the EzeOMS. The high-impact growth strategy will expand sales efforts the

neighboring markets of Oman, Qatar and Saudi Arabia as a growth strategy for acquiring

additional market share.

41

EzeSoft Dubai – A Business Proposal

September 2015

Critical Risks, Problems and Assumptions

The EzeSoft Dubai proposal to establish a local presence in the UAE market provides

clear, substantial and immediate strategic and financial benefits for the firm. In addition to

the favorable three-year outlook, the long-term growth opportunities in the region provide

even more upside for EzeSoft in terms of revenue, profitability, market share and sustainable

competitive advantage. At the same time, the favorable outlook includes certain risks,

obstacles and inherent assumptions, included in the figure below, with varying degrees of

impact on EzeSoft Dubai’s success.

Figure 7: EzeSoft Dubai SWOT Analysis

The SWOT analysis balances these key internal and external concerns with the

strengths and opportunities available for risk mitigation.

Internal Risks

The chief weaknesses associated with EzeSoft Dubai in essence also represent the

main reasons establishing a presence in the region. Despite the global strength and awareness

of the EzeSoft brand, the lack of awareness and poor local network in the UAE are a direct

42

EzeSoft Dubai – A Business Proposal

September 2015

result of the EzeSoft’s lack of a nearby regional office. EzeSoft’s closest offices – in London

and Hong Kong – are four time zones away and over seven hours away by air. This

separation greatly impedes EzeSoft’s partnership framework and client service excellence,

which hinge on being close to client offices to maximize face-time. By eliminating the time

zone differences and travel time, EzeSoft Dubai can efficiently concentrate local resources to

establish a strong, trust-based local network and build the brand awareness necessary to

exceed sales forecasts. These efforts also receive a boost from EzeSoft Dubai’s three year

marketing promotion strategy. If brand awareness and local networks do not progress as

expected, sales projections under the most likely scenario may not be achievable; however,

the worst-case scenario accounts for this potential risk and still generates positive financial

returns with additional market share worthy of consideration.

External Risks

The UAE’s free trade zones, including the DIFC, currently include a no-tax policy for

foreign companies. While there is a minor risk for tax (VAT) to be added in the next five

years, the VAT would be marginal and no more than 5% (McKinsey Global Institute, 2015).

Even though potential taxes would reduce operating margins, it is highly unlikely that sales

forecasts would be impacted.

The possibility of competitive intrusions into the UAE market must also be

considered, but EzeSoft’s core value proposition to clients – the partnership framework – can

be expected to mitigate competitive risk as it does in the primary global markets.

Furthermore, by being the first vendor on the ground, EzeSoft Dubai benefits from a head

start in joining local networks, building trust and establishing customer loyalty, which

represent the most valued elements for operating in the local business environment. EzeSoft

43

EzeSoft Dubai – A Business Proposal

September 2015

Dubai’s competitive advantage is also enhanced by the pricing incentives and discounts

included in the promotional strategy, which allow for more aggressive pricing in the first

year.

The most significant threat to EzeSoft Dubai’s success stems from uncertainty

regarding the region’s political climate. Islamic fundamentalist groups, notable ISIS, and

geopolitical instability in nearby countries such as Syria and Yemen remain unpredictable.

While the UAE currently falls in the low to moderate country risk tier, economic experts

generally agree that regional stability remains a concern even though the UAE is not

generally impacted by the social and political unrest in the region (A.M. Best Company,

2015). The UAE government in particular continues to distance itself from Arab protests by

tightening its political control and limiting refuge immigration (Coface, 2015). In the event

that tensions create an unjustifiable or unmanageable risk associated with EzeSoft’s UAE

presence, the firm may elect to temporarily or permanently shut down the EzeSoft Dubai

office, evacuate employees and service existing clients remotely via the London and Hong

Kong regional offices.

44

EzeSoft Dubai – A Business Proposal

September 2015

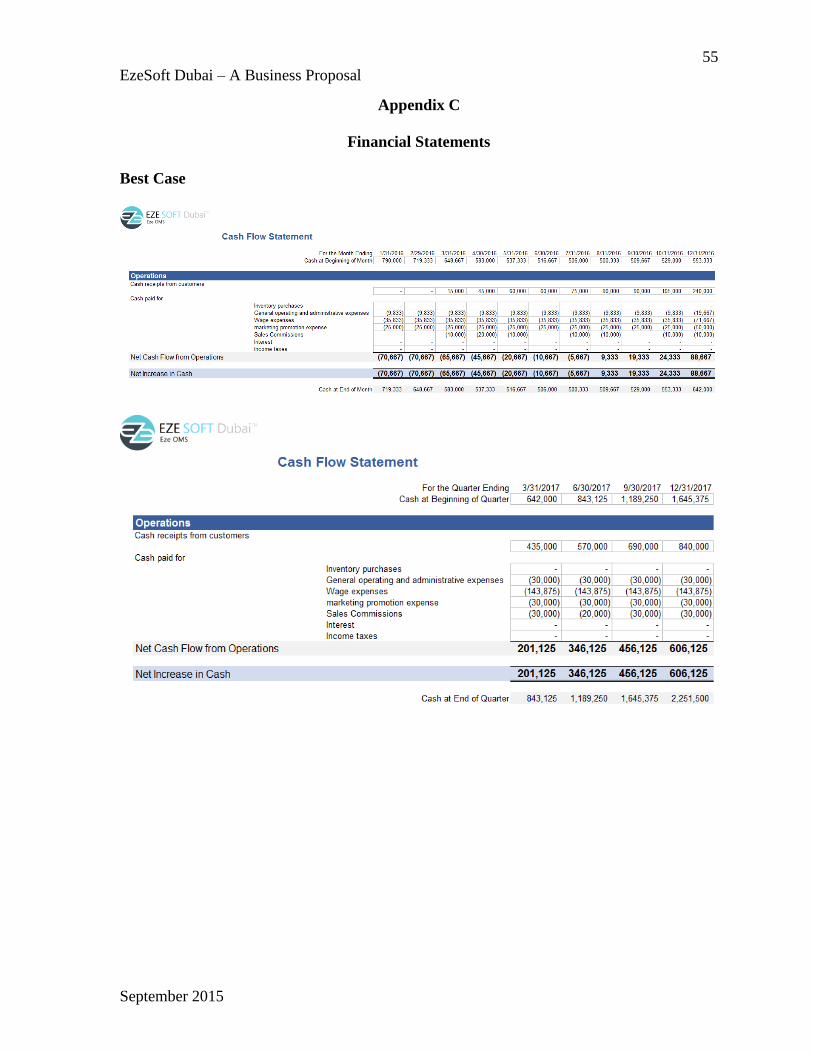

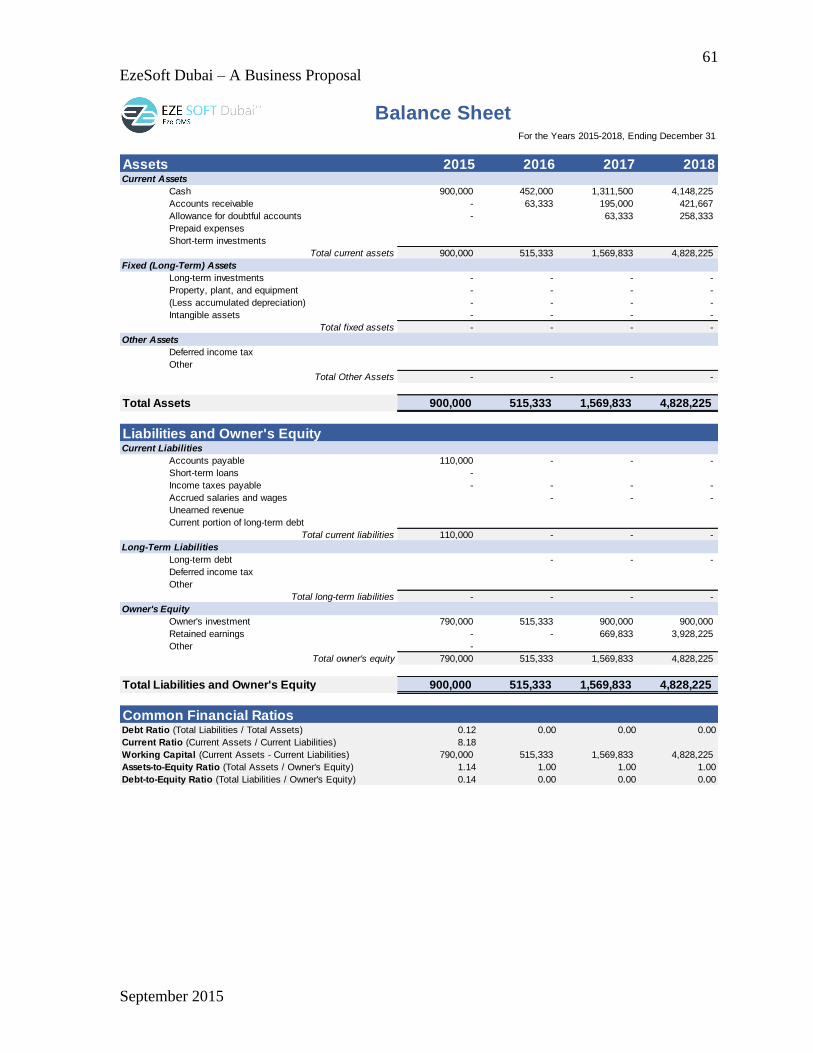

The Financial Plan

The EzeSoft Dubai financial plan provides a three-year performance outlook based on

projected sales for the most-likely scenario as well as the best and worst case scenarios. A

separate cash flow analysis, pro forma balance sheet and income statement for each the three

possible scenarios can be found in Appendix C. The financial forecasts include several

assumptions based on EzeSoft’s historical performance across all regional offices globally, as

well as experiences drawn from the most recent new office launches in Brazil and Australia.

Estimates also take into account EzeSoft’s internal analysis of the UAE market startup and

overhead costs.

Sales Forecasts

Three-year sales forecasts for each scenario are highlighted in the figure below.

Figure 8: EzeSoft Dubai Sales Forecast

Projects sales for each month were determined by incorporating both monthly

historical sales trends in new and existing markets, along with factors specific to the UAE

market. The forecasts assume no sales in the first two months in operation to allow the sales

team to establish sufficient trust with prospective funds. Analysis of EzeSoft’s historical

0

5

10

15

20

25

30

35

40

20

16

Jan Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

Dec

20

17

Jan Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

Dec

20

18

Jan Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

Dec

TOTA

L C

LIEN

TS

Three-Year Sales Forecast

Best Most Likely Worst

45

EzeSoft Dubai – A Business Proposal

September 2015

sales performance revealed that very few sales occur in December and January due to the

holidays, and as a result EzeSoft Dubai’s sales forecast projects minimal sales in either

month. The Muslim holiday of Ramadan occurs in June, and sales forecasts assume a similar

decline in June sales followed by a corresponding sales uptick in July of each year. Lastly,

the months of February, July and October have consistently proven to yield the higher sales

volumes annually for EzeSoft, and EzeSoft Dubai’s sales forecasts reflect this assumption in

the second and third year of operation.

46

EzeSoft Dubai – A Business Proposal

September 2015

Operating Costs

A summary of the annual operating costs for each scenario are illustrated in the tables

below.

Table IV: Operating Costs – Most Likely Scenario

Table V: Operating Costs – Best Case Scenario

Table VI: Operating Costs – Worst Case Scenario

Startup costs and fixed costs remain constant across all scenarios. Variable costs

include a 5% sales commission paid upfront for each new client signing. Operating costs are

adjusted annually to allow for an estimated 5% raise for all non-commission employees. The

estimated variable costs also account for additional personnel required to service the growing

client base, with the assumption that a business consultant and support specialist will be

required for every twelve clients.

Totals: 2016 2017 2018

Total Cost 908,000$ 895,500$ 958,275$

Fixed Costs (848,000)$ (685,500)$ (701,775)$

Variable Costs (60,000)$ (210,000)$ (256,500)$

Most Likely

Totals: 2016 2017 2018

Total Cost 928,000$ 925,500$ 1,118,275$

Fixed Costs (848,000)$ (685,500)$ (701,775)$

Variable Costs (80,000)$ (240,000)$ (416,500)$

Best

Totals: 2016 2017 2018

Total Cost 878,000$ 715,500$ 911,775$

Fixed Costs (848,000)$ (665,500)$ (701,775)$

Variable Costs (30,000)$ (50,000)$ (210,000)$

Worst

47

EzeSoft Dubai – A Business Proposal

September 2015

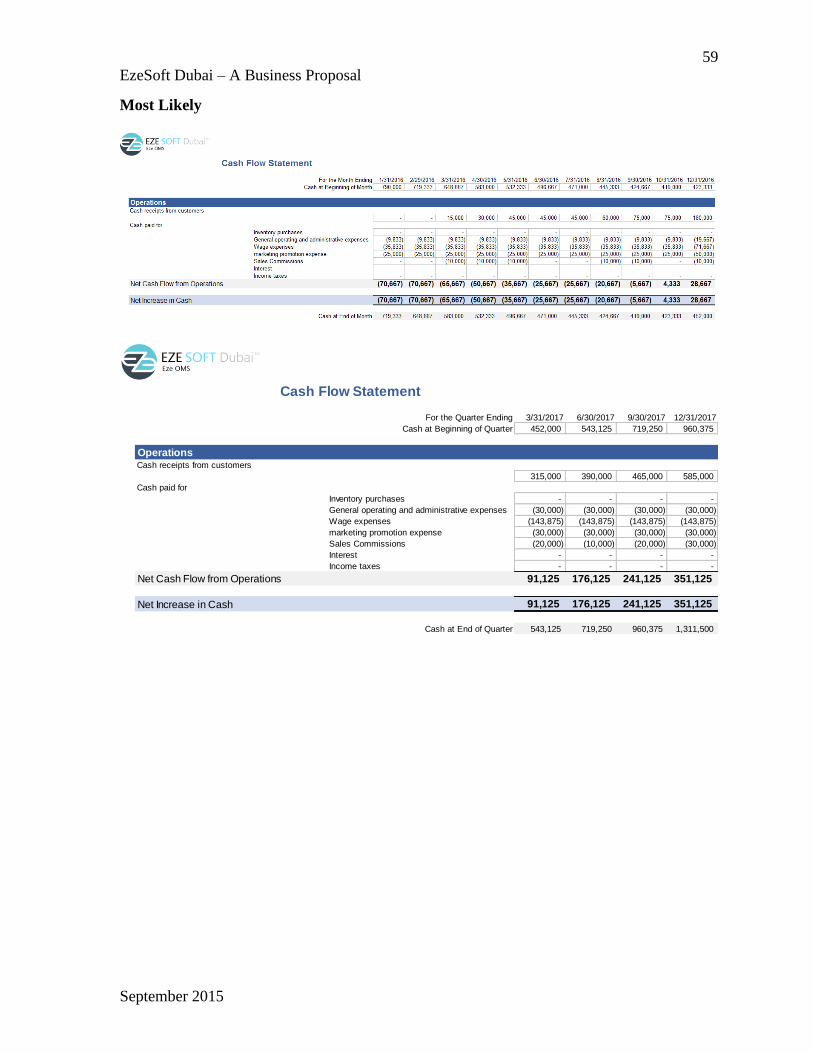

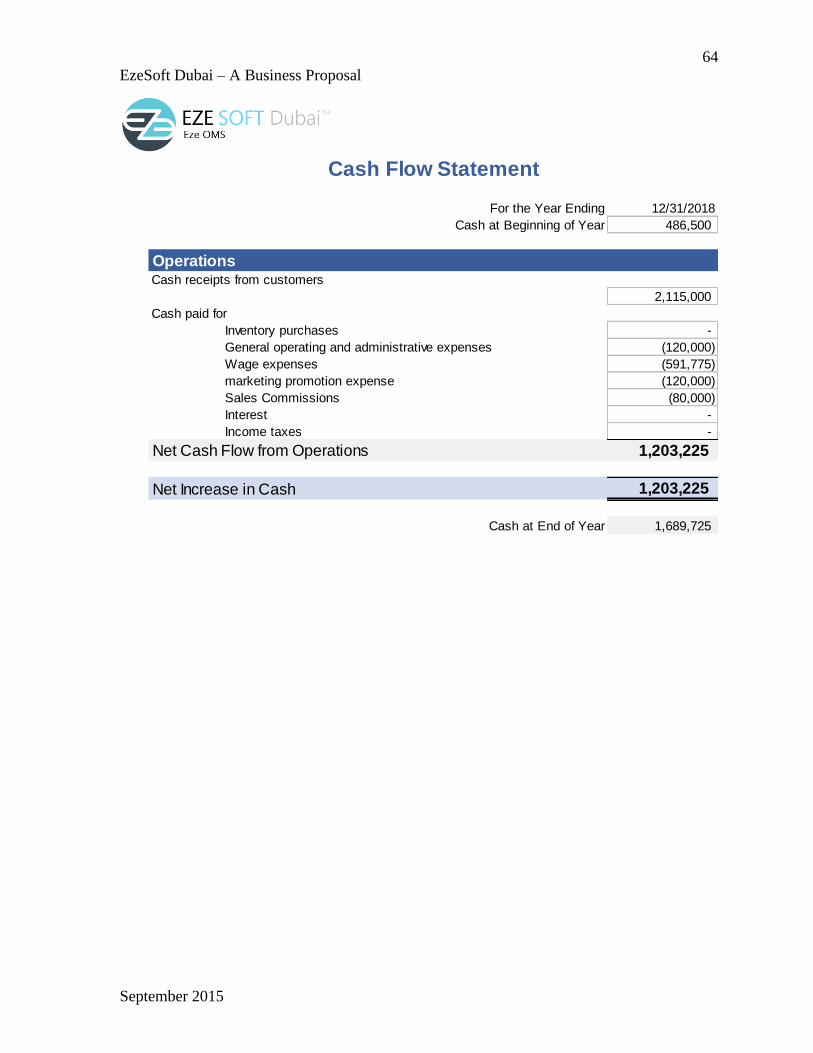

Cash Flow Analysis

The figure below summarizes the real-time cash flow projections for each scenario.

Figure 9: EzeSoft Dubai Cash Flow Projections

In order to provide a more accurate representation of financial forecasts, the estimated

cash flows reflect recurring monthly payments instead of recognizing the full annual revenue

for new clients on the signing date. For additional precision, the cash flow analyses assume

that only 90% of expected receivables will be paid each month. This assumption was

influenced by a comprehensive assessment of EzeSoft clients’ payment history. A second

assumption treats the remaining 10% of unpaid invoices as uncollectible, and these aged

receivables are converted to an allowance for doubtful accounts on the pro forma balance

sheets at the end of each fiscal year.

$-

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,0001

2/1

/20

15

3/1

/20

16

6/1

/20

16

9/1

/20

16

12

/1/2

01

6

3/1

/20

17

6/1

/20

17

9/1

/20

17

12

/1/2

01

7

3/1

/20

18

6/1

/20

18

9/1

/20

18

12

/1/2

01

8

Cash Flow Projections

Most Likely Best Worst

48

EzeSoft Dubai – A Business Proposal

September 2015

Profitability

Using the abovementioned sales forecasts, projected operating costs and

corresponding cash flow analysis, a summary of the profitability shown in the tables below

for each scenario.

Table VII: Profitability Forecasts – Most Likely Scenario

Table VIII: Profitability Forecasts – Best Case Scenario

Table IX: Profitability Forecasts – Worst Case Scenario

These tables demonstrate the strong profitability projections, high operating margins,

and additional market share even under the worst case scenario. The projected forecasts stand

to make a notable impact on EzeSoft’s bottom line at the firm level.

Totals: 2016 2017 2018