Embed Size (px)

Citation preview

ODIN MINING AND EXPLORATION LTD.

CONSOLIDATED FINANCIAL STATEMENTS

December 31, 2014

BDO Canada LLP, a Canadian limited liability partnership, is a member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms.

Tel: 604 688 5421 Fax: 604 688 5132 www.bdo.ca

BDO Canada LLP 600 Cathedral Place 925 West Georgia Street Vancouver BC V6C 3L2 Canada

Independent Auditor’s Report

To the Shareholders of Odin Mining and Exploration Ltd. (An Exploration Stage Company)

We have audited the accompanying consolidated financial statements of Odin Mining and Exploration Ltd. which comprise the consolidated balance sheets as at December 31, 2014 and 2013 and the consolidated statements of comprehensive loss, changes in equity and cash flows for the years then ended and a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Odin Mining and Exploration Ltd. as at December 31, 2014 and 2013, and the financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards.

Emphasis of Matter Without qualifying our opinion, we draw attention to Note 2 in the consolidated financial statements, which indicates that the Company has a deficit of $19,110,365 since inception and is expecting to incur further losses in the development of its business. These conditions, along with other matters as set forth in Note 2, indicate the existence of a material uncertainty that may cast significant doubt upon the Company’s ability to continue as a going concern.

Also, without modifying our opinion, we draw attention to Note 3 in the financial statements, which explains that certain comparative information has been restated as a result of a change in the Company’s accounting policy in respect of the exploration and evaluation assets.

(signed) “BDO Canada LLP” Chartered Accountants Vancouver, British Columbia March 18, 2015

See Accompanying Notes to the Consolidated Financial Statements

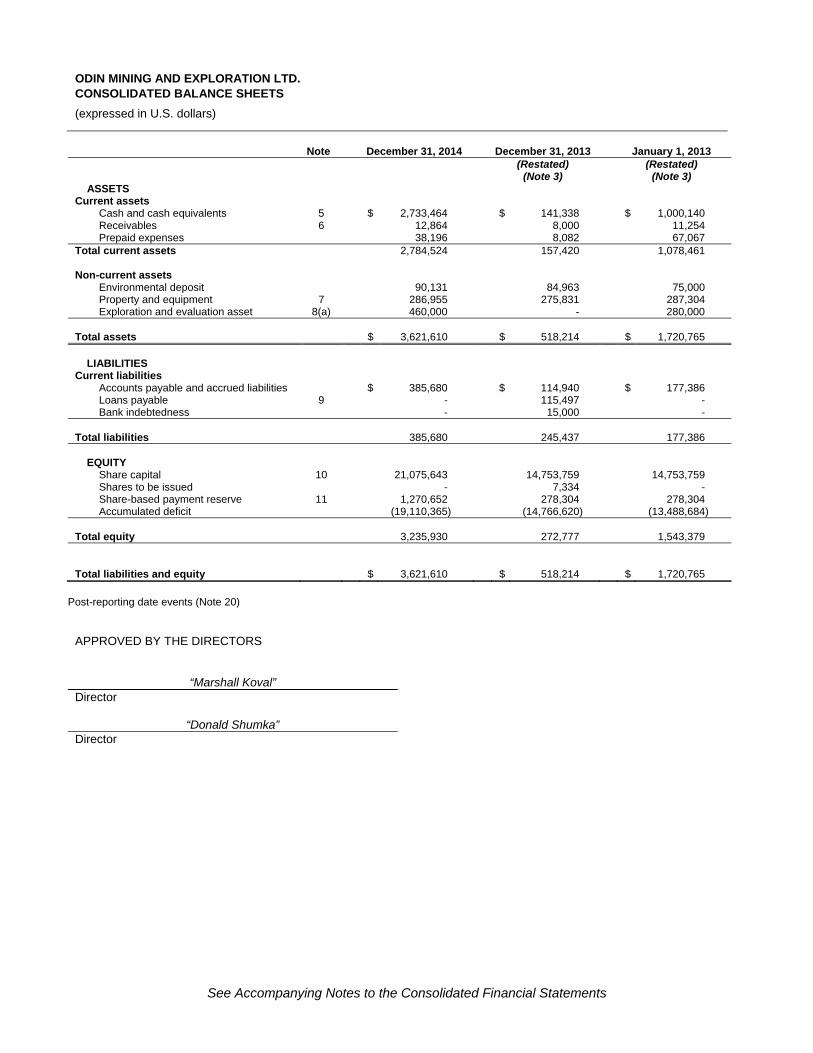

ODIN MINING AND EXPLORATION LTD. CONSOLIDATED BALANCE SHEETS

(expressed in U.S. dollars)

Note December 31, 2014 December 31, 2013 January 1, 2013

(Restated) (Restated) (Note 3) (Note 3) ASSETS Current assets Cash and cash equivalents 5 $ 2,733,464 $ 141,338 $ 1,000,140 Receivables 6 12,864 8,000 11,254 Prepaid expenses 38,196 8,082 67,067 Total current assets 2,784,524 157,420 1,078,461 Non-current assets Environmental deposit 90,131 84,963 75,000 Property and equipment 7 286,955 275,831 287,304 Exploration and evaluation asset 8(a) 460,000 - 280,000 Total assets $ 3,621,610 $ 518,214 $ 1,720,765 LIABILITIES Current liabilities Accounts payable and accrued liabilities $ 385,680 $ 114,940 $ 177,386 Loans payable 9 - 115,497 - Bank indebtedness - 15,000 - Total liabilities 385,680 245,437 177,386 EQUITY Share capital 10 21,075,643 14,753,759 14,753,759 Shares to be issued - 7,334 - Share-based payment reserve 11 1,270,652 278,304 278,304 Accumulated deficit (19,110,365) (14,766,620) (13,488,684) Total equity 3,235,930 272,777 1,543,379

Total liabilities and equity

$ 3,621,610

$ 518,214

$ 1,720,765

Post-reporting date events (Note 20)

APPROVED BY THE DIRECTORS

“Marshall Koval” Director

“Donald Shumka” Director

See Accompanying Notes to the Consolidated Financial Statements

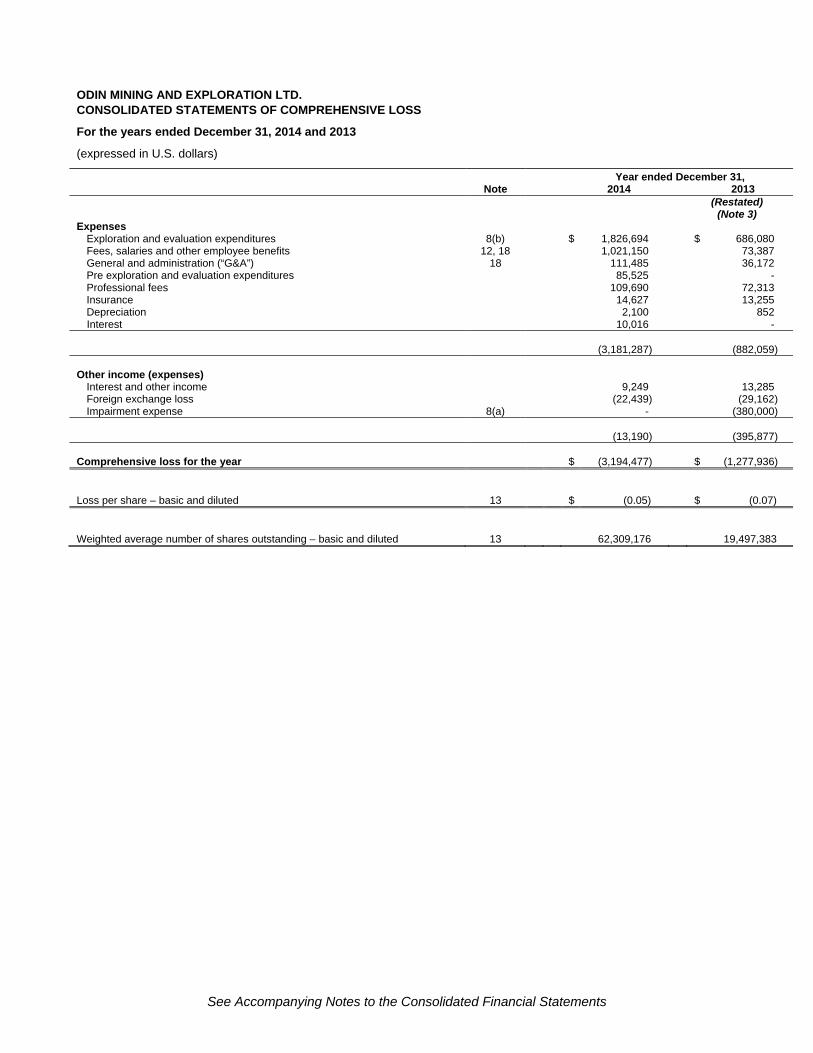

ODIN MINING AND EXPLORATION LTD. CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

For the years ended December 31, 2014 and 2013

(expressed in U.S. dollars)

Year ended December 31, Note 2014 2013 (Restated) (Note 3) Expenses Exploration and evaluation expenditures 8(b) $ 1,826,694 $ 686,080 Fees, salaries and other employee benefits 12, 18 1,021,150 73,387 General and administration (“G&A”) 18 111,485 36,172 Pre exploration and evaluation expenditures 85,525 - Professional fees 109,690 72,313 Insurance 14,627 13,255 Depreciation 2,100 852

Interest 10,016 - (3,181,287) (882,059) Other income (expenses) Interest and other income 9,249 13,285 Foreign exchange loss (22,439) (29,162) Impairment expense 8(a) - (380,000) (13,190) (395,877) Comprehensive loss for the year

$ (3,194,477) $ (1,277,936)

Loss per share – basic and diluted

13 $ (0.05) $ (0.07)

Weighted average number of shares outstanding – basic and diluted 13

62,309,176

19,497,383

See Accompanying Notes to the Consolidated Financial Statements

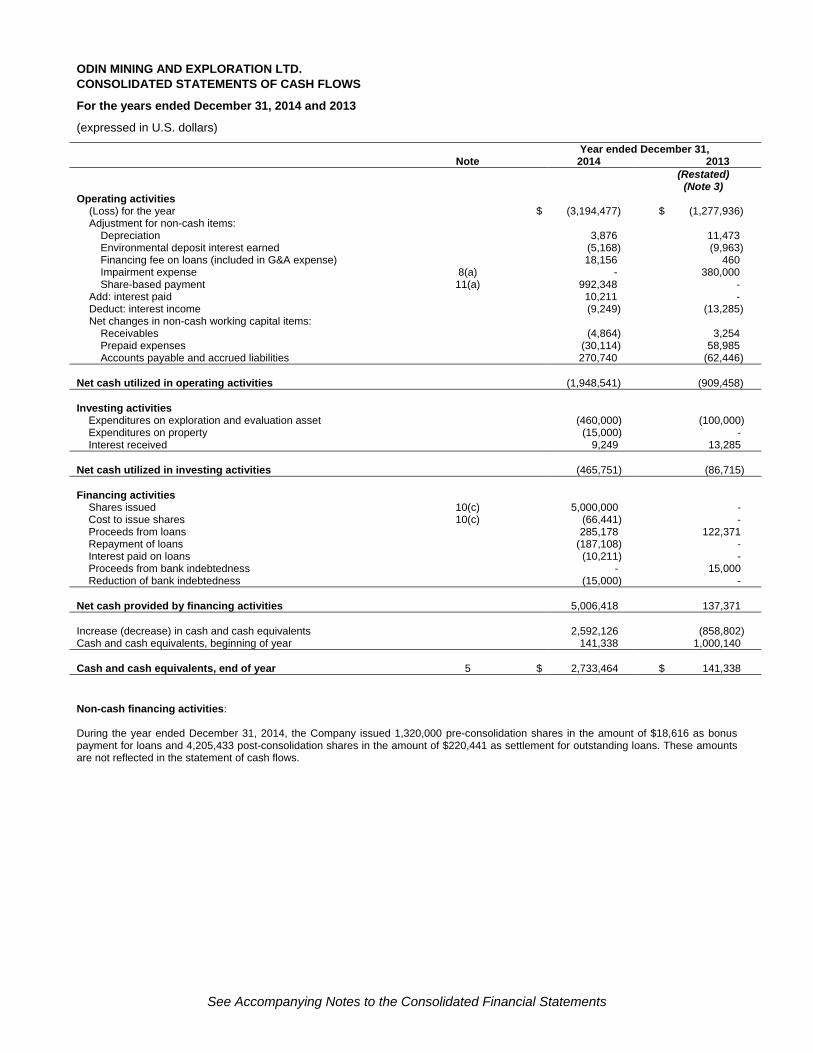

ODIN MINING AND EXPLORATION LTD. CONSOLIDATED STATEMENTS OF CASH FLOWS

For the years ended December 31, 2014 and 2013

(expressed in U.S. dollars)

Year ended December 31, Note 2014 2013

(Restated) (Note 3) Operating activities (Loss) for the year $ (3,194,477) $ (1,277,936) Adjustment for non-cash items: Depreciation 3,876 11,473 Environmental deposit interest earned (5,168) (9,963) Financing fee on loans (included in G&A expense) 18,156 460 Impairment expense 8(a) - 380,000 Share-based payment 11(a) 992,348 - Add: interest paid 10,211 - Deduct: interest income (9,249) (13,285) Net changes in non-cash working capital items: Receivables (4,864) 3,254 Prepaid expenses (30,114) 58,985 Accounts payable and accrued liabilities 270,740 (62,446) Net cash utilized in operating activities (1,948,541) (909,458) Investing activities

Expenditures on exploration and evaluation asset (460,000) (100,000) Expenditures on property (15,000) - Interest received 9,249 13,285

Net cash utilized in investing activities

(465,751)

(86,715)

Financing activities

Shares issued 10(c) 5,000,000 - Cost to issue shares 10(c) (66,441) - Proceeds from loans 285,178 122,371 Repayment of loans (187,108) - Interest paid on loans (10,211) - Proceeds from bank indebtedness - 15,000 Reduction of bank indebtedness (15,000) -

Net cash provided by financing activities

5,006,418

137,371

Increase (decrease) in cash and cash equivalents

2,592,126

(858,802)

Cash and cash equivalents, beginning of year 141,338 1,000,140 Cash and cash equivalents, end of year

5

$

2,733,464

$

141,338

Non-cash financing activities: During the year ended December 31, 2014, the Company issued 1,320,000 pre-consolidation shares in the amount of $18,616 as bonus payment for loans and 4,205,433 post-consolidation shares in the amount of $220,441 as settlement for outstanding loans. These amounts are not reflected in the statement of cash flows.

See Accompanying Notes to the Consolidated Financial Statements

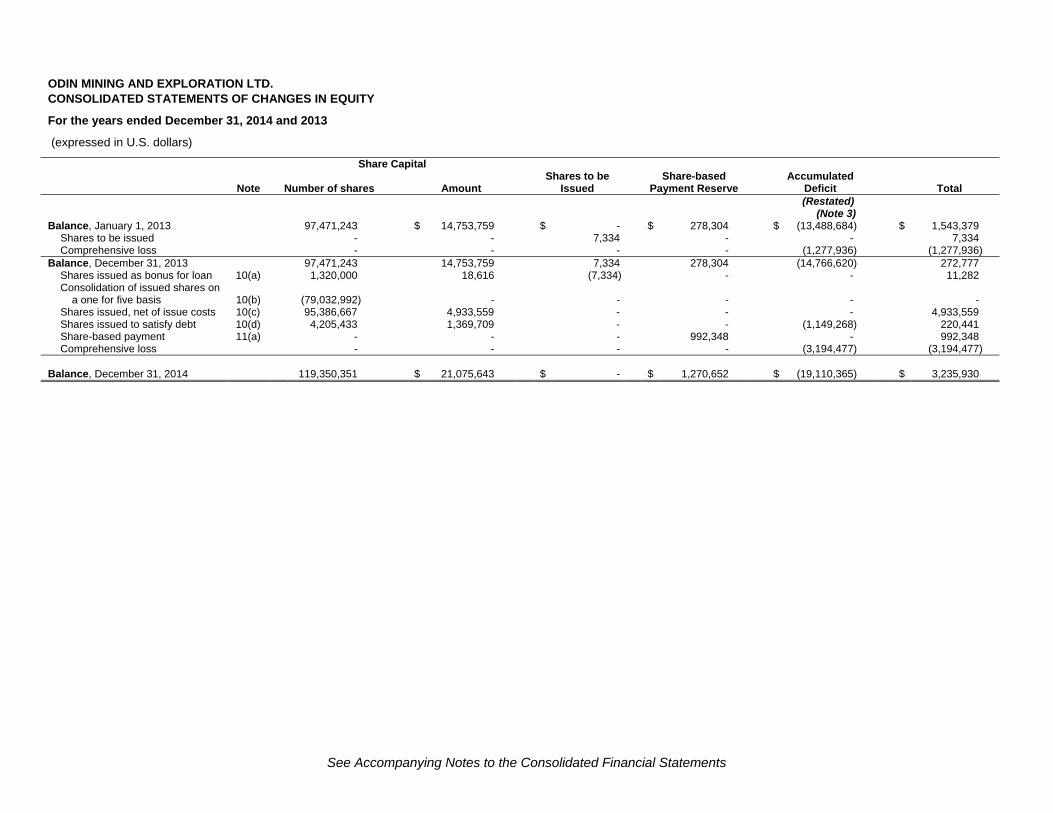

ODIN MINING AND EXPLORATION LTD. CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

For the years ended December 31, 2014 and 2013

(expressed in U.S. dollars)

Share Capital

Note Number of shares Amount Shares to be

Issued Share-based

Payment Reserve Accumulated

Deficit Total (Restated) (Note 3) Balance, January 1, 2013 97,471,243 $ 14,753,759 $ - $ 278,304 $ (13,488,684) $ 1,543,379 Shares to be issued - - 7,334 - - 7,334 Comprehensive loss - - - - (1,277,936) (1,277,936) Balance, December 31, 2013 97,471,243 14,753,759 7,334 278,304 (14,766,620) 272,777 Shares issued as bonus for loan 10(a) 1,320,000 18,616 (7,334) - - 11,282 Consolidation of issued shares on

a one for five basis

10(b)

(79,032,992)

-

-

-

-

- Shares issued, net of issue costs 10(c) 95,386,667 4,933,559 - - - 4,933,559 Shares issued to satisfy debt 10(d) 4,205,433 1,369,709 - - (1,149,268) 220,441 Share-based payment 11(a) - - - 992,348 - 992,348 Comprehensive loss - - - - (3,194,477) (3,194,477) Balance, December 31, 2014 119,350,351 $ 21,075,643 $ - $ 1,270,652 $ (19,110,365) $ 3,235,930

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 6 -

1. NATURE OF OPERATIONS

Odin Mining and Exploration Ltd. (“Odin” or the “Company”) is a publicly listed company incorporated under the Business Corporation Company Act of British Columbia on March 22, 1988. The Company is listed on the TSX-Venture Exchange, having the symbol ODN.V. Odin and its wholly-owned subsidiaries (collectively referred to as the “Group”) are engaged in the acquisition, exploration and development of mineral resources in Ecuador. The Group is considered to be in the exploration stage as it has not placed any of its mineral properties into production. The Company’s head office and principal business address is Suite 410, 625 Howe Street, Vancouver, British Columbia, V6C 2T6. The Company’s registered and records office is located at 10th Floor – 595 Howe Street, Vancouver, British Columbia, V6C 2T5.

2. BASIS OF PREPARATION AND GOING CONCERN (a) Statement of compliance

These consolidated financial statements of the Company have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). These consolidated financial statements were approved and authorised for issue by the Board of Directors on March 18, 2015.

(b) Basis of preparation

These consolidated financial statements have been prepared on a historical cost basis and are presented in U.S. dollars, except as specifically noted for Canadian dollar amounts shown as “C$”.

(c) Going concern

These consolidated financial statements have been prepared on the going concern basis which assumes that the Group will be able to realize, into the foreseeable future, its assets and liabilities in the normal course of business as they come due. The Group has incurred cumulative losses of $19,110,365 as at December 31, 2014 and has reported a net loss of $3,194,477 for the year ended December 31, 2014. The ability of the Group to continue as a going concern is dependent upon successfully obtaining additional financing, a joint venture, a merger or other business combination transaction involving a third party, sale of all or a portion of the Group’s assets, the outright sale of the Company or a combination thereof. The Company believes that, based on forecasts and the ability to reduce expenditures if required, along with indications of shareholder support, it will be able to continue as a going concern for the foreseeable future. However, as noted above, the Company will require additional funding in the future. There can be no assurance that management’s plans will be successful. These factors indicate the existence of a material uncertainty that may cast significant doubt upon the Company’s ability to continue as a going concern. These consolidated financial statements do not include any adjustments to the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern. Such adjustments could be material.

3. CHANGE IN ACCOUNTING POLICY

Effective September 30, 2014, following a change in management, the Company voluntarily changed its accounting policy for exploration and evaluation expenditures (“E&E”) to recognize these costs in the statement of loss in the period incurred, as permitted under IFRS 6 Exploration for and Evaluation of Mineral Resources. Previously, all these expenditures were capitalized as exploration and evaluation assets on the Company’s balance sheet. The Company changed its accounting policy as it believes that the new policy is more in line with the IFRS framework with respect to what constitutes an asset. The Company also believes that showing exploration and evaluation expenses separately on the statement of loss and in the operating activities section of the statement of cash flows more clearly represents the Company’s activities during the periods presented. The change in accounting policy has been applied retrospectively. No change in accounting policy was made with regard to costs of acquiring mineral property licenses or rights which are disclosed as E&E Assets.

The Company’s accounting policies for E&E expenditures and assets are described at Note 4(f).

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 7 -

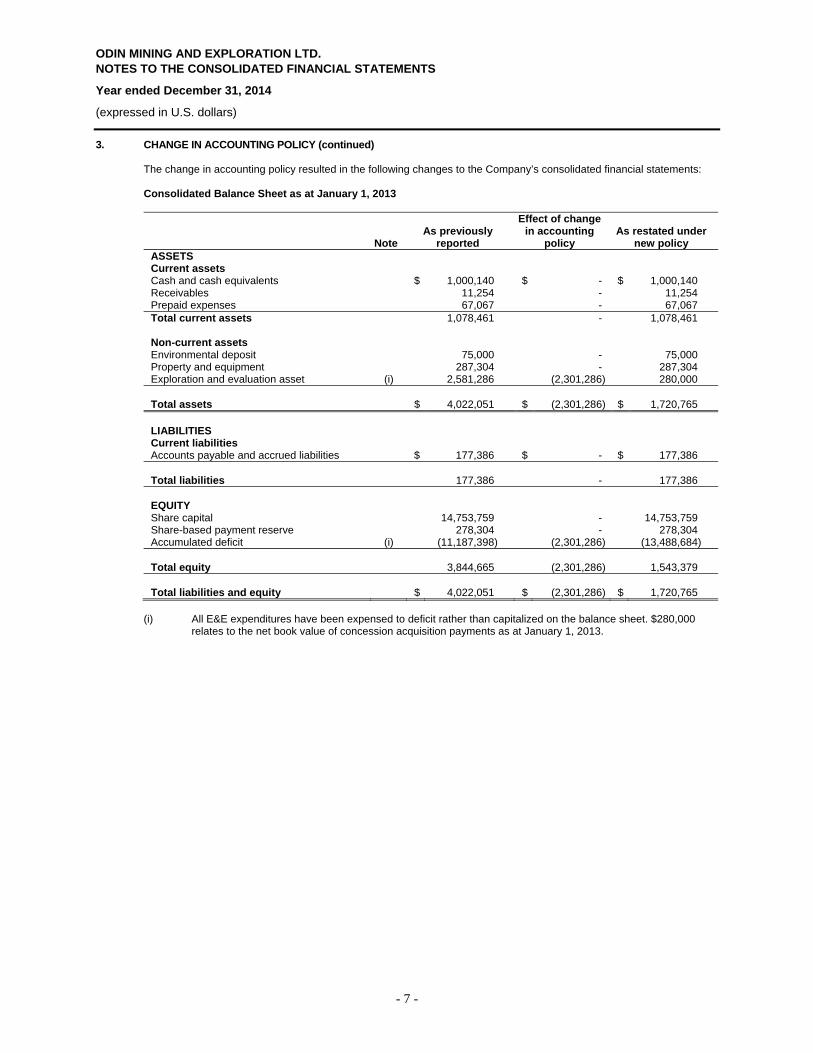

3. CHANGE IN ACCOUNTING POLICY (continued)

The change in accounting policy resulted in the following changes to the Company’s consolidated financial statements: Consolidated Balance Sheet as at January 1, 2013

Note

As previously

reported

Effect of change in accounting

policy

As restated under

new policy ASSETS Current assets Cash and cash equivalents $ 1,000,140 $ - $ 1,000,140 Receivables 11,254 - 11,254 Prepaid expenses 67,067 - 67,067 Total current assets 1,078,461 - 1,078,461 Non-current assets Environmental deposit 75,000 - 75,000 Property and equipment 287,304 - 287,304 Exploration and evaluation asset (i) 2,581,286 (2,301,286) 280,000 Total assets $ 4,022,051 $ (2,301,286) $ 1,720,765 LIABILITIES Current liabilities Accounts payable and accrued liabilities $ 177,386 $ - $ 177,386 Total liabilities 177,386 - 177,386 EQUITY Share capital 14,753,759 - 14,753,759 Share-based payment reserve 278,304 - 278,304 Accumulated deficit (i) (11,187,398) (2,301,286) (13,488,684) Total equity 3,844,665 (2,301,286) 1,543,379

Total liabilities and equity

$ 4,022,051

$ (2,301,286) $ 1,720,765

(i) All E&E expenditures have been expensed to deficit rather than capitalized on the balance sheet. $280,000 relates to the net book value of concession acquisition payments as at January 1, 2013.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 8 -

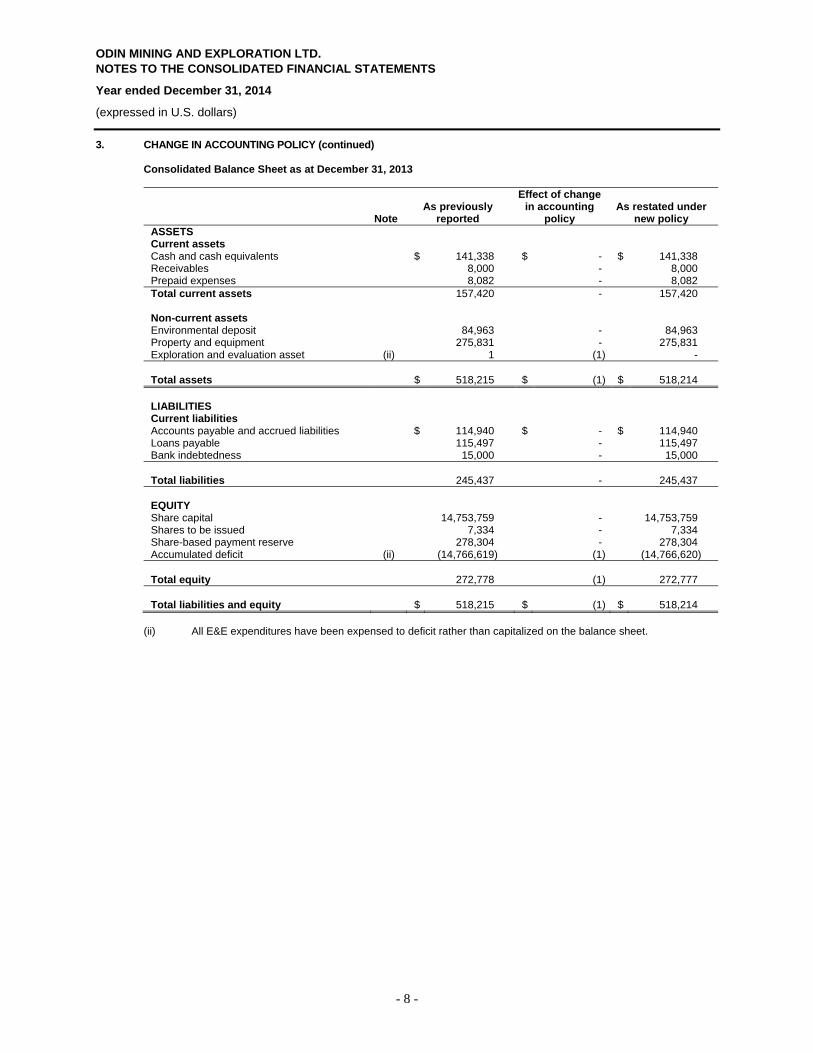

3. CHANGE IN ACCOUNTING POLICY (continued) Consolidated Balance Sheet as at December 31, 2013

Note

As previously

reported

Effect of change in accounting

policy

As restated under

new policy ASSETS Current assets Cash and cash equivalents $ 141,338 $ - $ 141,338 Receivables 8,000 - 8,000 Prepaid expenses 8,082 - 8,082 Total current assets 157,420 - 157,420 Non-current assets Environmental deposit 84,963 - 84,963 Property and equipment 275,831 - 275,831 Exploration and evaluation asset (ii) 1 (1) - Total assets $ 518,215 $ (1) $ 518,214 LIABILITIES Current liabilities Accounts payable and accrued liabilities $ 114,940 $ - $ 114,940 Loans payable 115,497 - 115,497 Bank indebtedness 15,000 - 15,000 Total liabilities 245,437 - 245,437 EQUITY Share capital 14,753,759 - 14,753,759 Shares to be issued 7,334 - 7,334 Share-based payment reserve 278,304 - 278,304 Accumulated deficit (ii) (14,766,619) (1) (14,766,620) Total equity 272,778 (1) 272,777

Total liabilities and equity

$ 518,215

$ (1) $ 518,214

(ii) All E&E expenditures have been expensed to deficit rather than capitalized on the balance sheet.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 9 -

3. CHANGE IN ACCOUNTING POLICY (continued)

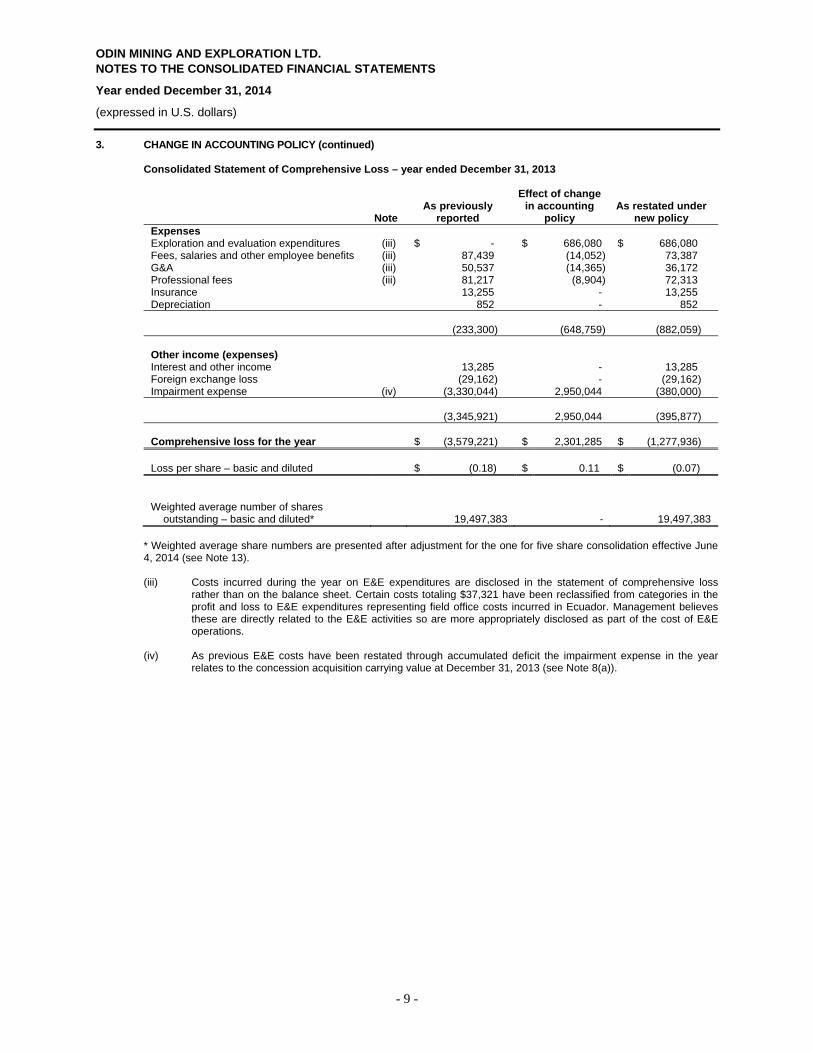

Consolidated Statement of Comprehensive Loss – year ended December 31, 2013

Note

As previously

reported

Effect of change in accounting

policy

As restated under

new policy Expenses Exploration and evaluation expenditures (iii) $ - $ 686,080 $ 686,080 Fees, salaries and other employee benefits (iii) 87,439 (14,052) 73,387 G&A (iii) 50,537 (14,365) 36,172 Professional fees (iii) 81,217 (8,904) 72,313 Insurance 13,255 - 13,255 Depreciation 852 - 852 (233,300) (648,759) (882,059) Other income (expenses) Interest and other income 13,285 - 13,285 Foreign exchange loss (29,162) - (29,162) Impairment expense (iv) (3,330,044) 2,950,044 (380,000) (3,345,921) 2,950,044 (395,877) Comprehensive loss for the year

$ (3,579,221) $ 2,301,285 $ (1,277,936)

Loss per share – basic and diluted $ (0.18) $ 0.11 $ (0.07)

Weighted average number of shares outstanding – basic and diluted*

19,497,383

-

19,497,383

* Weighted average share numbers are presented after adjustment for the one for five share consolidation effective June 4, 2014 (see Note 13).

(iii) Costs incurred during the year on E&E expenditures are disclosed in the statement of comprehensive loss

rather than on the balance sheet. Certain costs totaling $37,321 have been reclassified from categories in the profit and loss to E&E expenditures representing field office costs incurred in Ecuador. Management believes these are directly related to the E&E activities so are more appropriately disclosed as part of the cost of E&E operations.

(iv) As previous E&E costs have been restated through accumulated deficit the impairment expense in the year

relates to the concession acquisition carrying value at December 31, 2013 (see Note 8(a)).

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 10 -

3. CHANGE IN ACCOUNTING POLICY (continued)

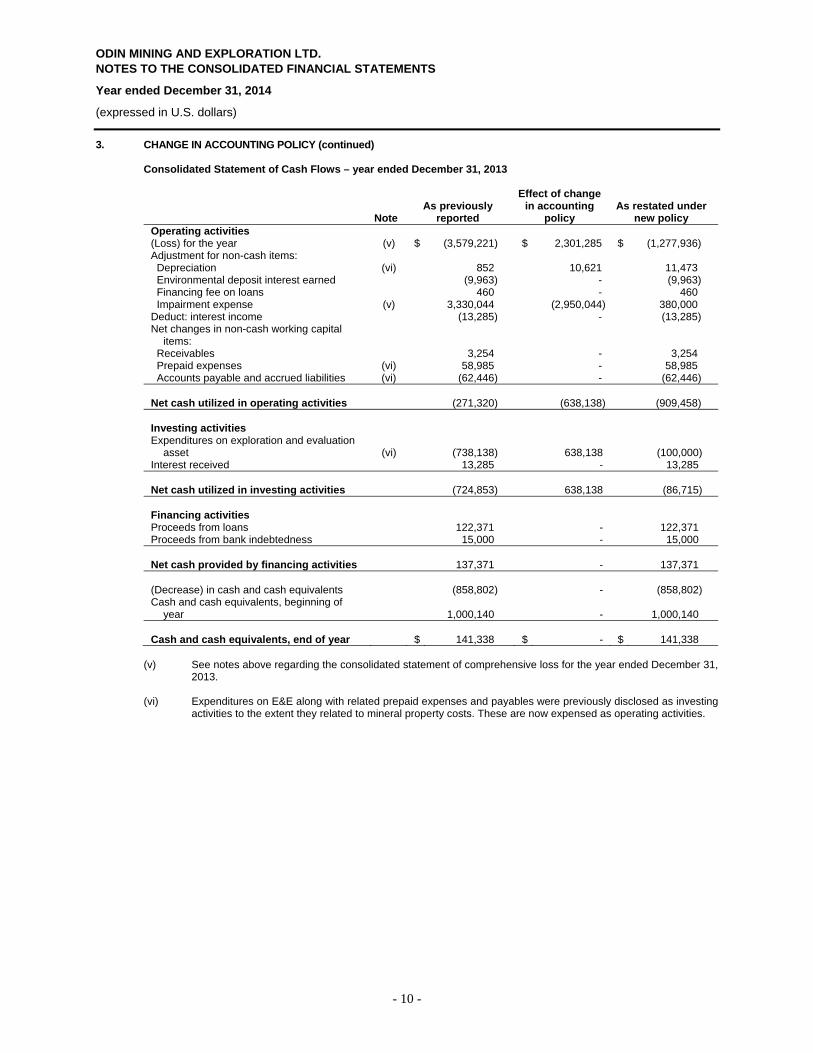

Consolidated Statement of Cash Flows – year ended December 31, 2013

Note

As previously

reported

Effect of change in accounting

policy

As restated under

new policy Operating activities (Loss) for the year (v) $ (3,579,221) $ 2,301,285 $ (1,277,936) Adjustment for non-cash items: Depreciation (vi) 852 10,621 11,473 Environmental deposit interest earned (9,963) - (9,963) Financing fee on loans 460 - 460 Impairment expense (v) 3,330,044 (2,950,044) 380,000 Deduct: interest income (13,285) - (13,285) Net changes in non-cash working capital

items:

Receivables 3,254 - 3,254 Prepaid expenses (vi) 58,985 - 58,985 Accounts payable and accrued liabilities (vi) (62,446) - (62,446) Net cash utilized in operating activities

(271,320) (638,138) (909,458)

Investing activities Expenditures on exploration and evaluation

asset

(vi)

(738,138) 638,138 (100,000) Interest received 13,285 - 13,285 Net cash utilized in investing activities

(724,853)

638,138

(86,715)

Financing activities Proceeds from loans 122,371 - 122,371 Proceeds from bank indebtedness 15,000 - 15,000 Net cash provided by financing activities

137,371

-

137,371

(Decrease) in cash and cash equivalents

(858,802)

-

(858,802)

Cash and cash equivalents, beginning of year

1,000,140

-

1,000,140

Cash and cash equivalents, end of year

$

141,338

$

-

$

141,338

(v) See notes above regarding the consolidated statement of comprehensive loss for the year ended December 31,

2013.

(vi) Expenditures on E&E along with related prepaid expenses and payables were previously disclosed as investing activities to the extent they related to mineral property costs. These are now expensed as operating activities.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 11 -

4. SIGNIFICANT ACCOUNTING POLICIES a) Overall considerations

The significant accounting policies that have been applied in the preparation of these consolidated financial statements are summarized below. These accounting policies have been used throughout all periods presented in the consolidated financial statements.

b) Basis of consolidation

These consolidated financial statements include the financial statements of Odin and its wholly-owned subsidiaries, which are controlled by the Company. Control is achieved when Odin (as the parent company) is exposed, or has rights, to variable returns from its involvement with the investees and has the ability to affect those returns through its power over the investee. Specifically, the Group controls an investee if, and only if, the Group has all of the following: (i) power over the investee (i.e. existing rights that give it the current ability to direct the relevant activities of the investee); (ii) exposure, or rights, to variable returns from its involvement with the investee; and (iii) the ability to use its power over the investee to affect its returns. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases. All significant intercompany transactions, balances, income and expenses are eliminated on consolidation. The consolidated financial statements of the Company include its wholly-owned subsidiaries: Odin Mining del Ecuador S.A. and Prospeccion Proyectos y Minas S.A. Prominas.

c) Presentation currency and foreign currency translation

The consolidated financial statements are presented in United States dollars which is also the functional currency of each company in the Group.

Foreign currency transactions are translated into the functional currency of each entity within the Group using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the re-measurement of foreign currency denominated monetary items at reporting period end exchange rates are recognized in profit or loss.

Non-monetary assets and liabilities that are measured at historical cost are translated using the exchange rates in effect at the time of the initial transaction and are not subsequently re-measured at reporting period ends. Non-monetary assets and liabilities that are measured at fair value or a re-valued amount are translated using the exchange rates at the date when the value was determined and the related translation differences are recognized in net income or other comprehensive loss consistent with where the gain or loss on the underlying non-monetary asset or liability has been recognized.

d) Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and demand deposits, together with other short-term, highly liquid investments that are readily convertible into known amounts of cash with original maturities of three months or less and which are subject to an insignificant risk of changes in value.

e) Exploration and evaluation licenses

All direct costs related to the acquisition of mineral property interests (E&E Assets) are capitalized into intangible assets on a property by property basis. License costs paid in connection with a right to explore in an exploration area, for a period in excess of one year, are capitalized and amortized over the term of the license.

f) Exploration and evaluation expenditures

Exploration and evaluation activities prior to acquiring an interest in a mineral concession area are charged to

operations as pre exploration and evaluation expenditures. Exploration costs, net of incidental revenues, are charged to operations in the year incurred until such time as it has been determined that a property has economically recoverable resources, in which case subsequent exploration costs and the costs incurred to develop a property are capitalized into property, plant and equipment. On the commencement of commercial production, depletion of each mining property will be provided on a unit-of-production basis using estimated reserves as the depletion base.

Although the Group has taken steps to verify the title to the exploration and evaluation assets in which it has an

interest, in accordance with industry practices for the current stage of exploration of such properties, these procedures do not guarantee the Group’s title. Title may be subject to unregistered prior agreements or transfers and title may be affected by undetected defects.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 12 -

4. SIGNIFICANT ACCOUNTING POLICIES (continued)

g) Environmental Deposits

Cash which is subject to contractual restrictions on use is classified separately as deposits. Security deposits required to be made to regulatory bodies, such as environmental or reclamation deposits, are classified as deposits.

h) Property and Equipment

Property and equipment is stated at cost less accumulated depreciation and accumulated impairment losses, if any. The cost of an item of property and equipment consists of the purchase price and any costs directly attributable to bringing the asset to the location and condition necessary for its intended use and an estimate of the costs of dismantling and removing the item and restoring the site on which it is located. Depreciation is provided at rates calculated to expense the cost of equipment, less its estimated residual value over the following expected useful lives:

Equipment 20% to 30% declining balance basis Motor Vehicles 20% to 30% straight-line basis

Items of property and equipment are derecognized upon disposal or when no future economic benefits are expected from their use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in profit or loss when the asset is derecognized. The assets’ residual values, useful lives and methods of depreciation are reviewed at each reporting period, and adjusted prospectively if appropriate. Land held is stated at cost. As no finite useful life for land can be determined, related carrying amounts are not depreciated.

i) Interest income

Interest income is recorded on an accrual basis using the effective interest method.

j) Provisions

Provisions are recognized when the Group has a present obligation (legal or constructive) that has arisen as a result of a past event and it is probable that a future outflow of resources will be required to settle the obligation, provided that a reliable estimate can be made of the amount of the obligation. Provisions are measured at management’s best estimate of the present value of the expenditures expected to be required to settle the obligation using a pre-tax rate that reflects current market assessments of the time value of money and the risk specific to the obligation. The increase in any provision due to passage of time is recognized as accretion expense.

k) Decommissioning, restoration and similar liabilities (“asset retirement obligation” or “ARO”)

The Group recognizes provisions for statutory, contractual, constructive or legal obligations, including those associated with the reclamation of mineral interests and decommissioning of equipment, when those obligations result from the acquisition, construction, development or normal operation of the assets. Initially, a provision for an ARO is recognized at its present value in the period in which it arises. Upon initial recognition of the liability, the corresponding ARO is added to the carrying amount of the related asset and the cost is amortized as an expense over the economic life of the asset. Following the initial recognition of the ARO, the carrying amount of the liability is increased for the passage of time and adjusted for changes to the current market-based discount rate, and the amount or timing of the underlying cash flows needed to settle the obligation. As at December 31, 2014 and 2013, the Group did not have any asset retirement obligations. The Group is subject to the laws and regulations relating to environmental matters in all jurisdictions in which it operates, including provisions relating to property reclamation, discharge or hazardous material and other matters. The Group may be held liable should environmental problems be discovered that were caused by former owners and operators of its properties and also on properties in which it has previously had an interest. The Group believes it conducts its mineral exploration activities in compliance with applicable environmental protection legislation. The Group is not aware of any existing environmental problems related to any of its current or former properties that may result in material liability to the Group.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 13 -

4. SIGNIFICANT ACCOUNTING POLICIES (continued)

l) Financial Instruments

Financial assets and financial liabilities are recognized when the Group becomes a party to the contractual provisions of the financial instrument. Financial assets are derecognized when the contractual rights to the cash flows from the financial asset expire, or when the financial asset and all substantial risks and rewards are transferred. A financial liability is derecognized when it is extinguished, discharged, cancelled or expires. Financial assets and financial liabilities are measured initially at fair value plus transaction costs, except for financial assets and liabilities carried at fair value through profit or loss, which are measured initially at fair value. Financial assets and financial liabilities are subsequently measured as described below.

Financial Assets For the purpose of subsequent measurement, financial assets are classified into the following categories upon initial recognition:

loans and receivables; financial assets at fair value through profit or loss; held-to-maturity investments; and available-for-sale financial assets.

The category determines how the asset is subsequently measured and whether any resulting income or expense is recognized in profit or loss or in other comprehensive income. All financial assets except for those at fair value through profit or loss are subject to review for impairment at least at each reporting date. Financial assets are considered impaired when there is objective evidence that a financial asset or a group of financial assets has been impaired. Different criteria to determine impairment are applied for each category of financial assets which are described below. Loans and receivables Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initial recognition these are measured at amortized cost using the effective interest method. Loans and receivables comprise cash and cash equivalents and receivables (other than goods and services tax (GST”) receivable from Canadian government taxation authorities). Financial assets at fair value through profit or loss Financial assets at fair value through profit or loss include financial assets that are either classified as held for trading or that meet certain conditions and are designated at fair value through profit or loss upon initial recognition. Assets in this category are measured at fair value with gains or losses recognized in profit or loss. The Group currently does not have any financial assets in this category. Held-to-maturity investments Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturity other than loans and receivables. Investments are classified as held-to-maturity if the Group has the intention and ability to hold them until maturity. Held-to-maturity investments are subsequently measured at amortized cost using the effective interest method. If there is objective evidence that the investment is impaired, determined for example by reference to external credit ratings, the financial asset is measured at the present value of estimated future cash flows. Any changes to the carrying amount of the investment, including impairment losses, are recognized in profit or loss. The Group currently does not have any financial assets in this category. Available-for-sale financial assets Available-for-sale financial assets are non-derivative financial assets that are either designated to this category or do not qualify for inclusion in any of the other categories of financial assets. Available-for-sale financial assets are measured at fair value. Gains and losses are recognized in other comprehensive income and reported within the available-for-sale reserve within equity, except for impairment losses and foreign exchange differences on monetary assets, which are recognized in profit or loss. When the asset is disposed of or is determined to be impaired the cumulative gain or loss recognized in other comprehensive income is reclassified from the equity reserve to profit or loss and presented as a reclassification adjustment within other comprehensive income. Interest calculated using the effective interest method is recognized in profit or loss. Reversals of impairment losses are recognized in other comprehensive income, except for financial assets that are debt securities which are recognized in profit or loss only if the reversal can be objectively related to an event occurring after the impairment loss was recognized. The Group currently does not have any financial assets in this category.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 14 -

4. SIGNIFICANT ACCOUNTING POLICIES (continued) l) Financial Instruments (continued)

Financial Liabilities Financial liabilities are measured subsequently at amortized cost using the effective interest method, except for financial liabilities held for trading or designated at fair value through profit or loss, that are carried subsequently at fair value with gains and losses recognized in profit or loss. The effective interest method is a method of calculating the amortized cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments through the expected life of the financial liability, or, where appropriate, a shorter period. The Group’s financial liabilities measured at amortized cost include accounts payable and accrued liabilities, bank indebtedness and loans payable.

m) Impairment of assets

Financial Assets

A financial asset that is not carried at fair value through profit or loss is assessed at each reporting date to determine whether there is objective evidence that it is impaired. A financial asset is impaired if objective evidence indicates that a loss event has occurred after the initial recognition of the asset, and that the loss event had a negative effect on the estimated future cash flows of that asset that can be estimated reliably. An impairment loss in respect of a financial asset measured at amortized cost is calculated as the difference between its carrying amount and the present value of the estimated future cash flows discounted at the asset’s original effective interest rate. The amount of the impairment loss is recognized in profit or loss. If, in a subsequent period, the amount of impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed through the profit or loss, except for equity instruments classified as available-for-sale where the reversal is recorded in other comprehensive income. Non-financial assets At the end of each reporting period, the Group reviews the carrying amounts of its tangible and intangible assets to determine whether there is an indication that the assets are impaired. For exploration and evaluation assets (and tangible assets related thereto such as equipment), the Group considers the following indicators of impairment: (i) whether the period for which the Group has the right to explore has expired in the period or will expire in the near future, and is not expected to be renewed; (ii) substantive expenditures on further exploration for and evaluation of mineral resources is neither budgeted nor planned; (iii) exploration and evaluation have not led to the discovery of commercially viable mineral resources and activities are to be discontinued; (iv) sufficient data exists to indicate that, although a development in the area is likely to proceed, the carrying amount of the exploration and evaluation asset is unlikely to be recovered in full from successful development of by sale; and (v) other factors that may be applicable such as a significant drop in metal prices or deterioration in the availability of equity financing. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment, if any. Where the asset does not generate largely independent cash inflows, the Group estimates the recoverable amount of the cash-generating unit to which the asset belongs. A cash-generating unit is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets. Recoverable amount is the higher of fair value less costs to sell, and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (or cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognized in profit or loss. An impairment loss recognized in respect of a cash-generating unit is allocated first to reduce the carrying amount of any goodwill allocated to the cash-generating unit and then to reduce the carrying amount of the other assets in the cash-generating unit on a pro-rata basis. With the exception of goodwill, all assets are subsequently reassessed for indications that an impairment loss previously recognized may no longer exist. Where an impairment loss subsequently reverses, the carrying amount of the asset (or cash-generating unit) is increased to the revised estimate of its recoverable amount, but to an amount that does not exceed the carrying amount that would have been determined had no impairment loss been recognized for the asset (or cash-generating unit) in prior periods. A reversal of an impairment loss is recognized in profit or loss.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 15 -

4. SIGNIFICANT ACCOUNTING POLICIES (continued)

n) Taxes Tax expense comprises current and deferred tax. Current tax and deferred tax are recognized in profit or loss

except to the extent that it relates to a business combination, or items recognized directly in equity or in other comprehensive income.

Current tax

Current tax is the expected tax payable or receivable on the taxable income or loss for the year, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax payable in respect of previous years. Deferred tax Deferred taxes are calculated using the liability method on temporary differences between the carrying amounts of assets and liabilities and their tax bases. However, deferred tax is not recognized on the initial recognition of goodwill, on the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit or loss at the time of the transaction, and on temporary differences relating to investments in subsidiaries and jointly controlled entities where the reversal of these temporary differences can be controlled by the Group and it is probable that reversal will not occur in the foreseeable future. Deferred tax assets and liabilities are measured, without discounting, at the tax rates that are expected to apply when the assets are recovered and the liabilities settled, based on tax rates that have been enacted or substantively enacted by the reporting date.

A deferred tax asset is recognized for unused tax losses, tax credits and deductible temporary differences, to the extent that it is probable that future taxable profits will be available against which they can be utilized. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow the related tax benefit to be utilized.

Deferred tax assets and liabilities are offset if there is a legally enforceable right to set off current tax assets against current tax liabilities, and they relate to income taxes levied by the same tax authority on the same taxable entity, or on different taxable entities which intend either to settle current tax liabilities and assets on a net basis, or to realize the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax liabilities and assets are expected to be settled or recovered. Sales tax Expenses and assets are recognized net of the amount of sales tax except:

When the sales tax incurred on a purchase of assets or services is not recoverable from the taxation authority, in which case the sales tax is recognized as part of the cost of acquisition of the asset or as part of the expense item, as applicable; or

When receivables and payables are stated with an amount of sales tax included.

The net amount of sales tax recoverable from, or payable to, the taxation authority is included as part of receivables or payables in the balance sheet.

o) Share capital

Equity instruments are contracts that give a residual interest in the net assets of the Company. Financial instruments issued by the Company are classified as equity only to the extent that they do not meet the definition of a financial liability or financial asset. The Company’s common shares are classified as equity instruments. Incremental costs directly attributable to the issue of new shares are shown in equity as a deduction, net of tax, from the proceeds.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 16 -

4. SIGNIFICANT ACCOUNTING POLICIES (continued)

p) Earnings (loss) per share

Basic earnings (loss) per common share is computed by dividing the net income (loss) available to common shareholders of the Company by the weighted average number of shares outstanding or committed to issue for the relevant year. Diluted earnings (loss) per common share is computed by dividing the net income (loss) applicable to common shareholders by the sum of the weighted average number of common shares outstanding or committed plus all additional common shares that would have been outstanding, if potentially dilutive instruments were converted.

q) Share-based payments

The Company has a stock option plan under which it grants stock options to directors, employees, consultants and service providers. Where equity-settled share options are awarded to employees, the fair value of the options at the date of grant is charged to the statement of comprehensive loss/income over the vesting period. Performance vesting conditions are taken into account by adjusting the number of equity instruments expected to vest at each reporting date so that, ultimately, the cumulative amount recognized over the vesting period is based on the number of options that eventually vest. Non-vesting conditions and market vesting conditions are factored into the fair value of the options granted. As long as all other vesting conditions are satisfied, a charge is made irrespective of whether these vesting conditions are satisfied. The cumulative expense is not adjusted for failure to achieve a market vesting condition or where a non-vesting condition is not satisfied. Where the terms and conditions of options are modified before they vest, the increase in fair value of the options, measured immediately before and after the modification, is also charged to the statement of comprehensive loss/income over the remaining vesting period. Where equity instruments are granted to employees, they are recorded at the fair value of the equity instrument granted at the grant date. The grant date fair value is recognized in the consolidated statement of comprehensive loss/income over the vesting period, described as the period during which all the vesting conditions are to be satisfied. Where equity instruments are granted to non-employees, they are recorded at the fair value of the goods or services received in the statement of comprehensive loss/income. Options or warrants granted related to the issuance of shares are recorded as a reduction of share capital. When the value of goods or services received in exchange for the share-based payment cannot be reliably estimated, the fair value is measured by use of a valuation model. The Company issued shares to creditors as a bonus for providing debt financing to the Company. These bonus shares are valued at the market value of the shares on the date the Company has the legal obligation to issue the shares. The value of the shares is recorded as deferred financing fees and netted against the related indebtedness. The amount of deferred financing costs is amortized on a straight-line basis over the term of the indebtedness. All equity-settled share-based payments are reflected in share-based payment reserve, until exercised. Upon exercise the fair value of is credited to share capital, along with the cash consideration, with an offsetting reduction in the share-based payment reserve. Where a grant of options is cancelled or settled during the vesting period, excluding forfeitures when vesting conditions are not satisfied, the Company immediately accounts for the cancellation as an acceleration of vesting and recognizes the amount that otherwise would have been recognized for services received over the remainder of the vesting period. Any payment made to the employee on the cancellation is accounted for as the repurchase of an equity interest except to the extent the payment exceeds the fair value of the equity instrument granted, measured at the repurchase date. Any such excess is recognized as an expense.

(r) Significant accounting judgments and estimates The preparation of the Group’s consolidated financial statements in accordance with IFRS requires management to make certain judgments, estimates and assumptions about recognition and measurement of assets, liabilities, income and expenses. Actual results are likely to differ from these estimates. Information about the significant judgments, estimates and assumptions that have the most significant effect on the recognition and measurement of assets, liabilities, income and expenses in these consolidated financial statements are discussed below.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 17 -

4. SIGNIFICANT ACCOUNTING POLICIES (continued)

(r) Significant accounting judgments and estimates (continued) Judgments Exploration and evaluation assets: The application of the Group’s accounting policy for exploration and evaluation assets requires judgment in determining whether it is likely that such acquisition costs incurred will be recovered through successful exploration and development or sale of the asset under review. Furthermore, the assessment as to whether economically recoverable resources exist is itself an estimation process. Estimates and assumptions made may change if new information becomes available. If, after expenditure is capitalized, information becomes available suggesting that the recovery of expenditure is unlikely, the amount capitalized is written off to profit or loss in the period when the new information becomes available. The carrying value of these assets is detailed at Note 8. Title to Mineral Property Interests: Although the Company has taken steps to verify title to mineral properties in which it has an interest, these procedures do not guarantee the Company’s title. Such properties may be subject to prior agreements or transfers and title may be affected by undetected defects. Estimates and assumptions Share-based payments: The Company utilizes the Black-Scholes Option Pricing Model (“Black-Scholes”) to estimate the fair value of stock options granted to directors, officers and employees. The use of Black-Scholes requires management to make various estimates and assumptions that impact the value assigned to the stock options including the forecast future volatility of the stock price, the risk-free interest rate, dividend yield and the expected life of the stock options. Any changes in these assumptions could have a material impact on the share-based payment calculation value. Deferred tax assets: The assessment of the probability of future taxable income against which deferred tax assets can be utilized is based on the Group’s future planned activities, supported by budgets that have been approved by the Board of Directors. Management also considers the tax rules of the various jurisdictions in which the Group operates. Should there not be a forecast of taxable income that indicates the probable utilization of a deferred tax asset or any portion thereof, the Group does not recognize the deferred tax asset.

(s) Changes in accounting policies – new and amended standards and interpretations

There were a number of new standards and interpretations effective from January 1, 2014, that the Group applied for the first time in the current year. The nature and impact of each new standard and/or amendment is described below. Other than the changes described below, the accounting policies adopted are consistent with those of the previous financial year. Certain other new standards and interpretations applied for the first time in 2014 but are not discussed as they were not relevant to the Company. IAS 32 – Offsetting Financial Assets and Financial Liabilities (Amendments to IAS 32): IAS 32 Financial Instruments: Presentation was amended to address inconsistencies in current practice when applying the offsetting criteria. The amendments clarify the meaning of “currently has a legally enforceable right to set-off.” The amendments had no impact on the Group’s consolidated financial statements. IFRIC 21 – Levies IFRIC 21, Levies, is an interpretation of IAS 37, Provisions, Contingent Liabilities and Contingent Assets, which sets out criteria for the recognition of a liability, one of which is the requirement for an entity to have a present obligation as a result of a past event. The Interpretation clarifies that the obligating event that gives rise to a liability to pay a levy is the activity described in the relevant legislation that triggers the payment of the levy. The Interpretation did not have a material impact on the Group’s consolidated financial statements. Annual Improvements In December 2013, the IASB issued “Annual Improvements to IFRSs 2010-2012 Cycle” which included certain amendments to IAS 24 Related Party Disclosures, including an amendment to the definition of a “related party” in order to include “management entities” that provide key management personnel services to the reporting entity. This amendment is effective for annual periods beginning on or after July 1, 2014, with earlier adoption permitted. The Company adopted the amendment with effect January 1, 2014. The Company’s related party disclosure note (Note 18) complies with the disclosure requirements.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 18 -

4. SIGNIFICANT ACCOUNTING POLICIES (continued) (t) Standards issued but not yet effective The standards and interpretations that are issued, but not yet effective, up to the date of authorization of these

condensed consolidated interim financial statements are disclosed below. Management anticipates that all of the pronouncements will be adopted in the Group’s accounting policy for the first period beginning after the effective date of the pronouncement. Information on new standards, amendments and interpretations that are expected to be relevant to the Group’s financial statements is provided below. Certain other new standards and interpretations have been issued but are not expected to have a material impact on the Group’s consolidated financial statements.

IFRS 15 – Revenue from Contracts with Customers: The IASB issued IFRS 15 in May 2014. The new standard

provides a comprehensive framework for recognition, measurement and disclosure of revenue from contracts with customers, excluding contracts within the scope of the standards on leases, insurance contracts and financial instruments. IFRS 15 is effective for annual periods beginning on or after January 1, 2017 and is to be applied retrospectively with early adoption permitted. Management is currently evaluating the impact the final standard is expected to have on the Group’s consolidated financial statements; however, as the Company currently has no operating revenues, this is not anticipated to be significant.

IFRS 9 – Financial Instruments: The IASB published the final version of IFRS 9 in July 2014. The final standard

brings together the classification, measurement, impairment and hedge accounting phases of the IASB’s project to replace IAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 includes a loss impairment model, amends the classification and measurement model for financial assets and provides additional guidance on how to apply the business model and contractual characteristics test. This final version of IFRS 9 supersedes all previous versions of IFRS 9 and is effective for annual periods commencing on or after January 1, 2018, with early adoption permitted. Management is currently evaluating the impact the final standard is expected to have on the Group’s consolidated financial statements.

5. CASH AND CASH EQUIVALENTS

The Group’s cash and cash equivalents at December 31, 2014, consisted of cash of $530,028 and cash equivalents of $2,203,436 (2013 – cash of $141,338). The Group’s cash and cash equivalents are denominated in the following currencies and include the following components:

December 31, 2014

December 31, 2013

Cash at bank and in hand – Canadian dollars $ 16,736 $ 140,958 Cash at bank and in hand – U.S. dollars 513,292 380 Short-term deposits – U.S. dollars 2,203,436 - Cash and cash equivalents

$ 2,733,464

$ 141,338

6. RECEIVABLES

December 31, 2014

December 31, 2013

GST $ 12,861 $ - Other 3 8,000 Total receivables

$

12,864

$

8,000

All amounts are short-term and the net carrying value of receivables is considered a reasonable approximation of fair value. The Group anticipates full recovery of these amounts and therefore no impairment has been recorded against receivables. The Group’s receivables are all considered current and are not past due. The Group does not hold any collateral related to these assets.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 19 -

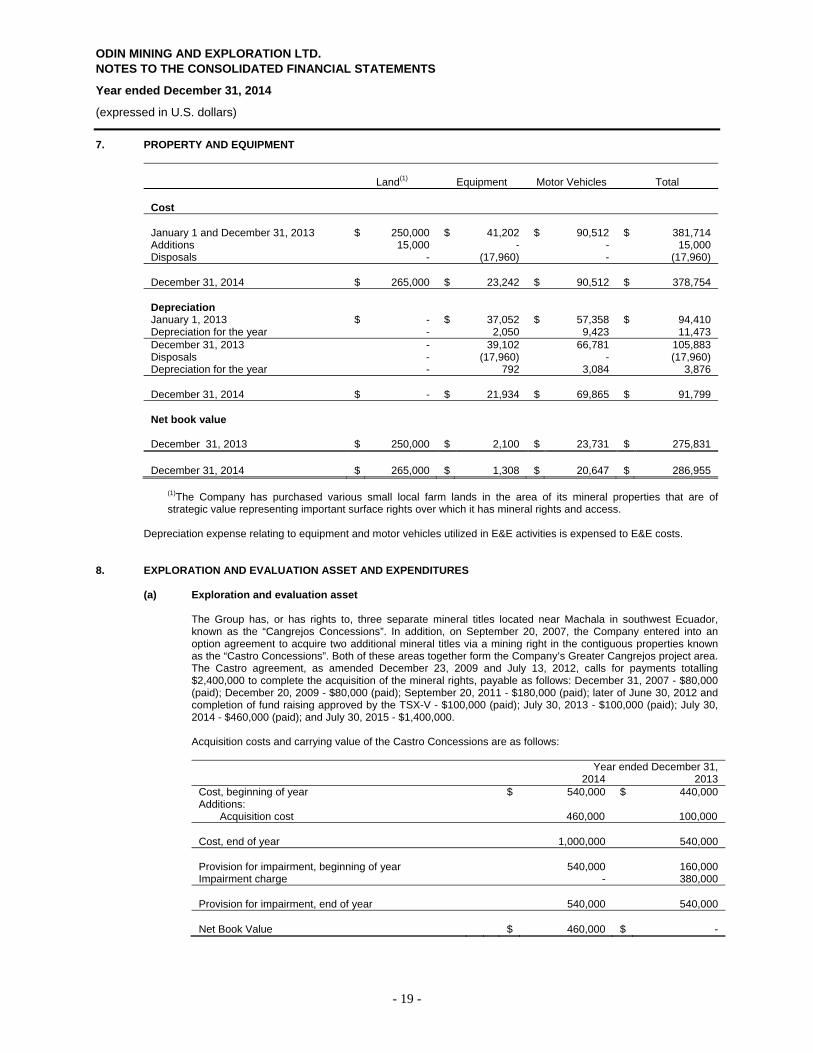

7. PROPERTY AND EQUIPMENT

Land(1) Equipment Motor Vehicles Total Cost January 1 and December 31, 2013 $ 250,000 $ 41,202 $ 90,512 $ 381,714 Additions 15,000 - - 15,000 Disposals - (17,960) - (17,960) December 31, 2014

$ 265,000

$ 23,242

$ 90,512 $ 378,754

Depreciation January 1, 2013 $ - $ 37,052 $ 57,358 $ 94,410 Depreciation for the year - 2,050 9,423 11,473 December 31, 2013 - 39,102 66,781 105,883 Disposals - (17,960) - (17,960) Depreciation for the year - 792 3,084 3,876 December 31, 2014

$ -

$ 21,934

$ 69,865 $ 91,799

Net book value December 31, 2013 $ 250,000 $ 2,100 $ 23,731 $ 275,831 December 31, 2014 $ 265,000 $ 1,308 $ 20,647 $ 286,955

(1)The Company has purchased various small local farm lands in the area of its mineral properties that are of strategic value representing important surface rights over which it has mineral rights and access.

Depreciation expense relating to equipment and motor vehicles utilized in E&E activities is expensed to E&E costs. 8. EXPLORATION AND EVALUATION ASSET AND EXPENDITURES (a) Exploration and evaluation asset

The Group has, or has rights to, three separate mineral titles located near Machala in southwest Ecuador, known as the “Cangrejos Concessions”. In addition, on September 20, 2007, the Company entered into an option agreement to acquire two additional mineral titles via a mining right in the contiguous properties known as the “Castro Concessions”. Both of these areas together form the Company’s Greater Cangrejos project area. The Castro agreement, as amended December 23, 2009 and July 13, 2012, calls for payments totalling $2,400,000 to complete the acquisition of the mineral rights, payable as follows: December 31, 2007 - $80,000 (paid); December 20, 2009 - $80,000 (paid); September 20, 2011 - $180,000 (paid); later of June 30, 2012 and completion of fund raising approved by the TSX-V - $100,000 (paid); July 30, 2013 - $100,000 (paid); July 30, 2014 - $460,000 (paid); and July 30, 2015 - $1,400,000. Acquisition costs and carrying value of the Castro Concessions are as follows:

Year ended December 31, 2014 2013 Cost, beginning of year $ 540,000 $ 440,000 Additions:

Acquisition cost 460,000 100,000 Cost, end of year

1,000,000

540,000

Provision for impairment, beginning of year

540,000

160,000

Impairment charge - 380,000

Provision for impairment, end of year

540,000

540,000 Net Book Value $ 460,000 $ -

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 20 -

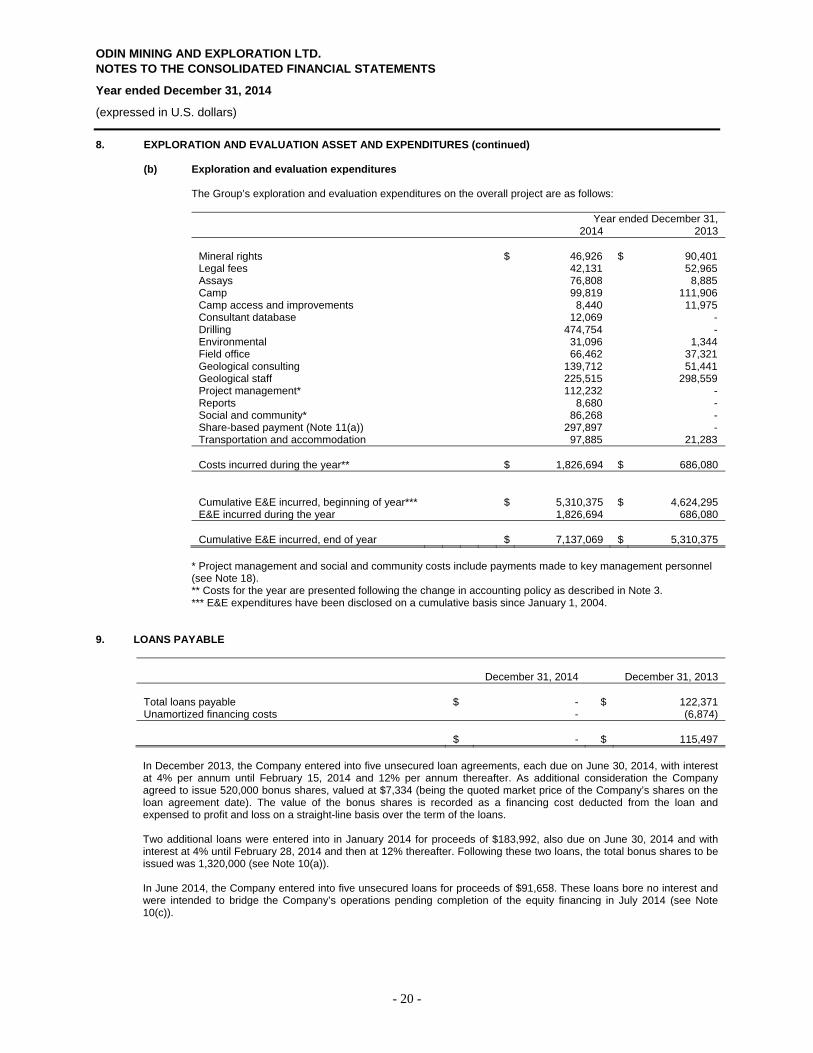

8. EXPLORATION AND EVALUATION ASSET AND EXPENDITURES (continued) (b) Exploration and evaluation expenditures

The Group’s exploration and evaluation expenditures on the overall project are as follows:

Year ended December 31, 2014 2013 Mineral rights $ 46,926 $ 90,401 Legal fees 42,131 52,965 Assays 76,808 8,885 Camp 99,819 111,906 Camp access and improvements 8,440 11,975 Consultant database 12,069 - Drilling 474,754 - Environmental 31,096 1,344 Field office 66,462 37,321 Geological consulting 139,712 51,441 Geological staff 225,515 298,559 Project management* 112,232 - Reports 8,680 - Social and community* 86,268 - Share-based payment (Note 11(a)) 297,897 - Transportation and accommodation 97,885 21,283 Costs incurred during the year**

$

1,826,694 $

686,080

Cumulative E&E incurred, beginning of year***

$

5,310,375 $

4,624,295 E&E incurred during the year 1,826,694 686,080

Cumulative E&E incurred, end of year

$

7,137,069 $

5,310,375 * Project management and social and community costs include payments made to key management personnel (see Note 18). ** Costs for the year are presented following the change in accounting policy as described in Note 3. *** E&E expenditures have been disclosed on a cumulative basis since January 1, 2004. 9. LOANS PAYABLE

December 31, 2014

December 31, 2013 Total loans payable $ - $ 122,371 Unamortized financing costs - (6,874)

$

-

$

115,497

In December 2013, the Company entered into five unsecured loan agreements, each due on June 30, 2014, with interest at 4% per annum until February 15, 2014 and 12% per annum thereafter. As additional consideration the Company agreed to issue 520,000 bonus shares, valued at $7,334 (being the quoted market price of the Company’s shares on the loan agreement date). The value of the bonus shares is recorded as a financing cost deducted from the loan and expensed to profit and loss on a straight-line basis over the term of the loans. Two additional loans were entered into in January 2014 for proceeds of $183,992, also due on June 30, 2014 and with interest at 4% until February 28, 2014 and then at 12% thereafter. Following these two loans, the total bonus shares to be issued was 1,320,000 (see Note 10(a)). In June 2014, the Company entered into five unsecured loans for proceeds of $91,658. These loans bore no interest and were intended to bridge the Company’s operations pending completion of the equity financing in July 2014 (see Note 10(c)).

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 21 -

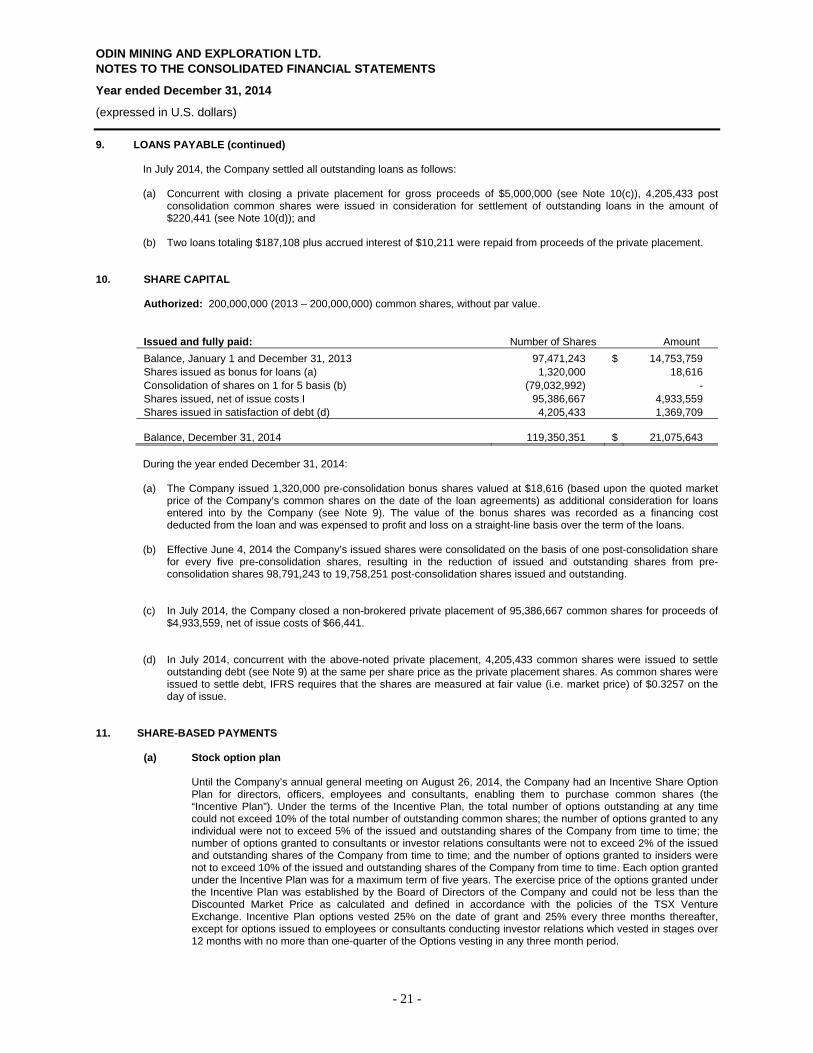

9. LOANS PAYABLE (continued) In July 2014, the Company settled all outstanding loans as follows: (a) Concurrent with closing a private placement for gross proceeds of $5,000,000 (see Note 10(c)), 4,205,433 post

consolidation common shares were issued in consideration for settlement of outstanding loans in the amount of $220,441 (see Note 10(d)); and

(b) Two loans totaling $187,108 plus accrued interest of $10,211 were repaid from proceeds of the private placement.

10. SHARE CAPITAL Authorized: 200,000,000 (2013 – 200,000,000) common shares, without par value.

Issued and fully paid: Number of Shares Amount

Balance, January 1 and December 31, 2013 97,471,243 $ 14,753,759 Shares issued as bonus for loans (a) 1,320,000 18,616 Consolidation of shares on 1 for 5 basis (b) (79,032,992) - Shares issued, net of issue costs I 95,386,667 4,933,559 Shares issued in satisfaction of debt (d) 4,205,433 1,369,709 Balance, December 31, 2014 119,350,351 $ 21,075,643 During the year ended December 31, 2014: (a) The Company issued 1,320,000 pre-consolidation bonus shares valued at $18,616 (based upon the quoted market

price of the Company’s common shares on the date of the loan agreements) as additional consideration for loans entered into by the Company (see Note 9). The value of the bonus shares was recorded as a financing cost deducted from the loan and was expensed to profit and loss on a straight-line basis over the term of the loans.

(b) Effective June 4, 2014 the Company’s issued shares were consolidated on the basis of one post-consolidation share for every five pre-consolidation shares, resulting in the reduction of issued and outstanding shares from pre-consolidation shares 98,791,243 to 19,758,251 post-consolidation shares issued and outstanding.

(c) In July 2014, the Company closed a non-brokered private placement of 95,386,667 common shares for proceeds of

$4,933,559, net of issue costs of $66,441. (d) In July 2014, concurrent with the above-noted private placement, 4,205,433 common shares were issued to settle

outstanding debt (see Note 9) at the same per share price as the private placement shares. As common shares were issued to settle debt, IFRS requires that the shares are measured at fair value (i.e. market price) of $0.3257 on the day of issue.

11. SHARE-BASED PAYMENTS (a) Stock option plan

Until the Company’s annual general meeting on August 26, 2014, the Company had an Incentive Share Option Plan for directors, officers, employees and consultants, enabling them to purchase common shares (the “Incentive Plan”). Under the terms of the Incentive Plan, the total number of options outstanding at any time could not exceed 10% of the total number of outstanding common shares; the number of options granted to any individual were not to exceed 5% of the issued and outstanding shares of the Company from time to time; the number of options granted to consultants or investor relations consultants were not to exceed 2% of the issued and outstanding shares of the Company from time to time; and the number of options granted to insiders were not to exceed 10% of the issued and outstanding shares of the Company from time to time. Each option granted under the Incentive Plan was for a maximum term of five years. The exercise price of the options granted under the Incentive Plan was established by the Board of Directors of the Company and could not be less than the Discounted Market Price as calculated and defined in accordance with the policies of the TSX Venture Exchange. Incentive Plan options vested 25% on the date of grant and 25% every three months thereafter, except for options issued to employees or consultants conducting investor relations which vested in stages over 12 months with no more than one-quarter of the Options vesting in any three month period.

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 22 -

11. SHARE-BASED PAYMENTS (continued)

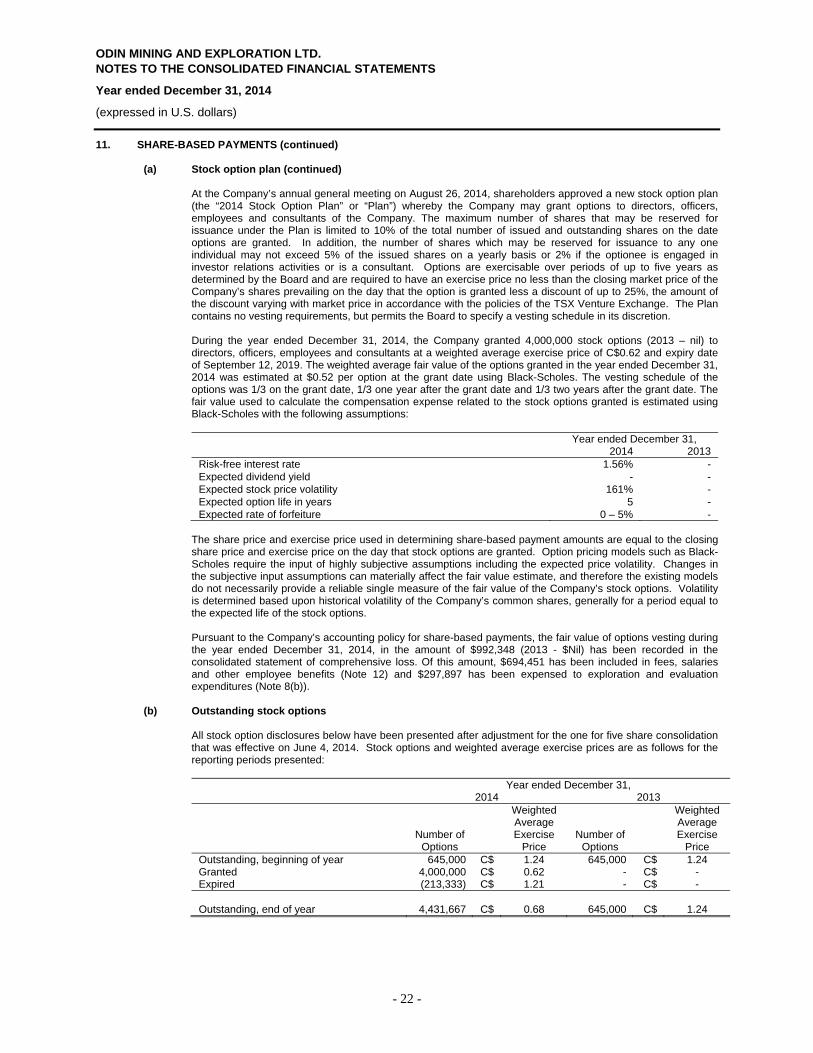

(a) Stock option plan (continued) At the Company’s annual general meeting on August 26, 2014, shareholders approved a new stock option plan (the “2014 Stock Option Plan” or “Plan”) whereby the Company may grant options to directors, officers, employees and consultants of the Company. The maximum number of shares that may be reserved for issuance under the Plan is limited to 10% of the total number of issued and outstanding shares on the date options are granted. In addition, the number of shares which may be reserved for issuance to any one individual may not exceed 5% of the issued shares on a yearly basis or 2% if the optionee is engaged in investor relations activities or is a consultant. Options are exercisable over periods of up to five years as determined by the Board and are required to have an exercise price no less than the closing market price of the Company’s shares prevailing on the day that the option is granted less a discount of up to 25%, the amount of the discount varying with market price in accordance with the policies of the TSX Venture Exchange. The Plan contains no vesting requirements, but permits the Board to specify a vesting schedule in its discretion. During the year ended December 31, 2014, the Company granted 4,000,000 stock options (2013 – nil) to directors, officers, employees and consultants at a weighted average exercise price of C$0.62 and expiry date of September 12, 2019. The weighted average fair value of the options granted in the year ended December 31, 2014 was estimated at $0.52 per option at the grant date using Black-Scholes. The vesting schedule of the options was 1/3 on the grant date, 1/3 one year after the grant date and 1/3 two years after the grant date. The fair value used to calculate the compensation expense related to the stock options granted is estimated using Black-Scholes with the following assumptions:

Year ended December 31, 2014 2013 Risk-free interest rate 1.56% - Expected dividend yield - - Expected stock price volatility 161% - Expected option life in years 5 - Expected rate of forfeiture 0 – 5% -

The share price and exercise price used in determining share-based payment amounts are equal to the closing share price and exercise price on the day that stock options are granted. Option pricing models such as Black-Scholes require the input of highly subjective assumptions including the expected price volatility. Changes in the subjective input assumptions can materially affect the fair value estimate, and therefore the existing models do not necessarily provide a reliable single measure of the fair value of the Company’s stock options. Volatility is determined based upon historical volatility of the Company’s common shares, generally for a period equal to the expected life of the stock options. Pursuant to the Company’s accounting policy for share-based payments, the fair value of options vesting during the year ended December 31, 2014, in the amount of $992,348 (2013 - $Nil) has been recorded in the consolidated statement of comprehensive loss. Of this amount, $694,451 has been included in fees, salaries and other employee benefits (Note 12) and $297,897 has been expensed to exploration and evaluation expenditures (Note 8(b)).

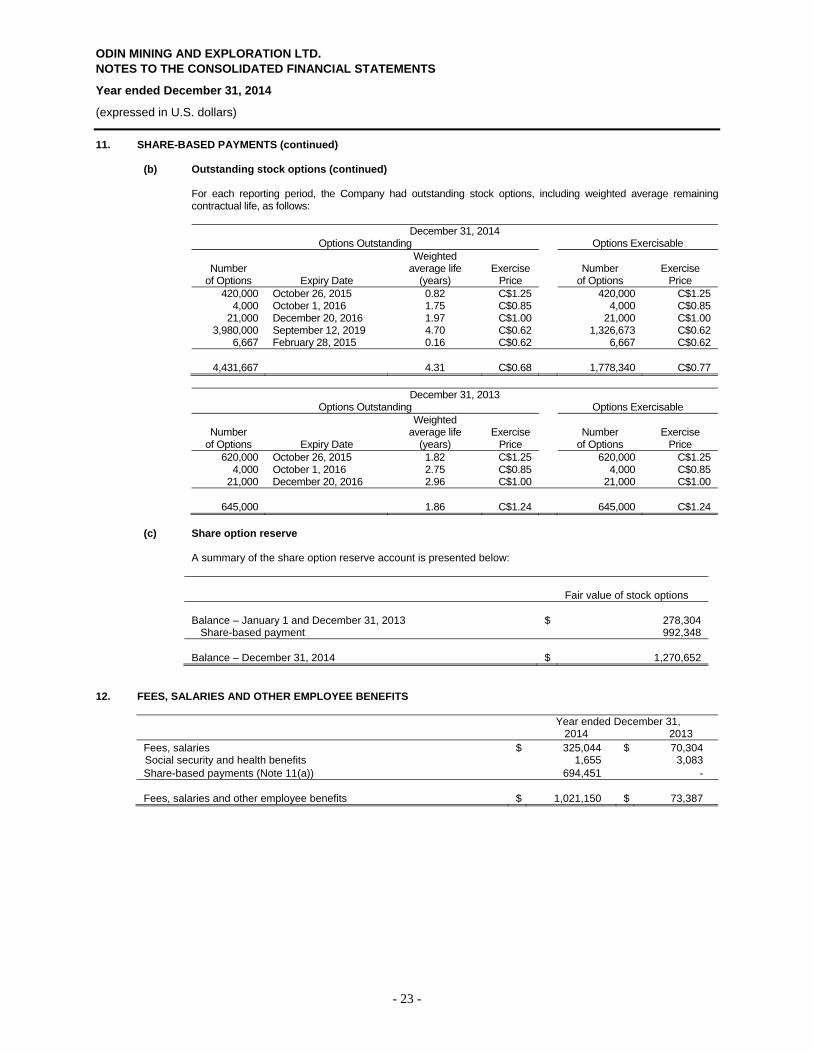

(b) Outstanding stock options

All stock option disclosures below have been presented after adjustment for the one for five share consolidation that was effective on June 4, 2014. Stock options and weighted average exercise prices are as follows for the reporting periods presented:

Year ended December 31, 2014 2013

Number of Options

Weighted Average Exercise

Price Number of

Options

Weighted Average Exercise

Price Outstanding, beginning of year 645,000 C$ 1.24 645,000 C$ 1.24 Granted 4,000,000 C$ 0.62 - C$ - Expired (213,333) C$ 1.21 - C$ - Outstanding, end of year 4,431,667 C$ 0.68 645,000 C$ 1.24

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 23 -

11. SHARE-BASED PAYMENTS (continued) (b) Outstanding stock options (continued)

For each reporting period, the Company had outstanding stock options, including weighted average remaining contractual life, as follows:

December 31, 2014 Options Outstanding Options Exercisable

Number of Options Expiry Date

Weighted average life

(years) Exercise

Price

Number

of Options Exercise

Price 420,000 October 26, 2015 0.82 C$1.25 420,000 C$1.25

4,000 October 1, 2016 1.75 C$0.85 4,000 C$0.85 21,000 December 20, 2016 1.97 C$1.00 21,000 C$1.00

3,980,000 September 12, 2019 4.70 C$0.62 1,326,673 C$0.62 6,667 February 28, 2015 0.16 C$0.62 6,667 C$0.62

4,431,667 4.31 C$0.68 1,778,340 C$0.77

December 31, 2013

Options Outstanding Options Exercisable

Number of Options Expiry Date

Weighted average life

(years) Exercise

Price

Number

of Options Exercise

Price 620,000 October 26, 2015 1.82 C$1.25 620,000 C$1.25

4,000 October 1, 2016 2.75 C$0.85 4,000 C$0.85 21,000 December 20, 2016 2.96 C$1.00 21,000 C$1.00

645,000 1.86 C$1.24 645,000 C$1.24

(c) Share option reserve

A summary of the share option reserve account is presented below:

Fair value of stock options Balance – January 1 and December 31, 2013

$

278,304

Share-based payment 992,348 Balance – December 31, 2014

$

1,270,652

12. FEES, SALARIES AND OTHER EMPLOYEE BENEFITS

Year ended December 31, 2014 2013 Fees, salaries $ 325,044 $ 70,304 Social security and health benefits 1,655 3,083 Share-based payments (Note 11(a)) 694,451 - Fees, salaries and other employee benefits $ 1,021,150 $ 73,387

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 24 -

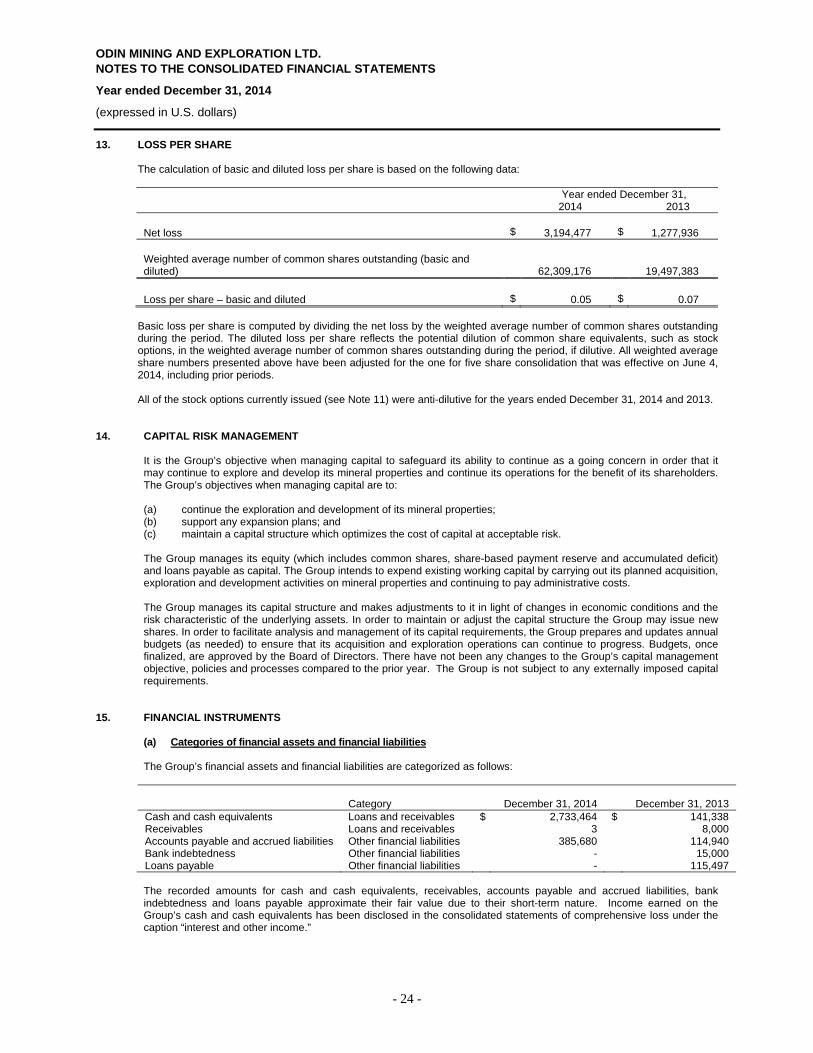

13. LOSS PER SHARE

The calculation of basic and diluted loss per share is based on the following data:

Year ended December 31, 2014 2013 Net loss $ 3,194,477 $ 1,277,936 Weighted average number of common shares outstanding (basic and diluted)

62,309,176

19,497,383

Loss per share – basic and diluted $ 0.05 $ 0.07

Basic loss per share is computed by dividing the net loss by the weighted average number of common shares outstanding during the period. The diluted loss per share reflects the potential dilution of common share equivalents, such as stock options, in the weighted average number of common shares outstanding during the period, if dilutive. All weighted average share numbers presented above have been adjusted for the one for five share consolidation that was effective on June 4, 2014, including prior periods. All of the stock options currently issued (see Note 11) were anti-dilutive for the years ended December 31, 2014 and 2013.

14. CAPITAL RISK MANAGEMENT

It is the Group’s objective when managing capital to safeguard its ability to continue as a going concern in order that it

may continue to explore and develop its mineral properties and continue its operations for the benefit of its shareholders. The Group’s objectives when managing capital are to:

(a) continue the exploration and development of its mineral properties; (b) support any expansion plans; and (c) maintain a capital structure which optimizes the cost of capital at acceptable risk.

The Group manages its equity (which includes common shares, share-based payment reserve and accumulated deficit)

and loans payable as capital. The Group intends to expend existing working capital by carrying out its planned acquisition, exploration and development activities on mineral properties and continuing to pay administrative costs.

The Group manages its capital structure and makes adjustments to it in light of changes in economic conditions and the

risk characteristic of the underlying assets. In order to maintain or adjust the capital structure the Group may issue new shares. In order to facilitate analysis and management of its capital requirements, the Group prepares and updates annual budgets (as needed) to ensure that its acquisition and exploration operations can continue to progress. Budgets, once finalized, are approved by the Board of Directors. There have not been any changes to the Group’s capital management objective, policies and processes compared to the prior year. The Group is not subject to any externally imposed capital requirements.

15. FINANCIAL INSTRUMENTS

(a) Categories of financial assets and financial liabilities

The Group’s financial assets and financial liabilities are categorized as follows:

Category December 31, 2014 December 31, 2013 Cash and cash equivalents Loans and receivables $ 2,733,464 $ 141,338 Receivables Loans and receivables 3 8,000 Accounts payable and accrued liabilities Other financial liabilities 385,680 114,940 Bank indebtedness Other financial liabilities - 15,000 Loans payable Other financial liabilities - 115,497

The recorded amounts for cash and cash equivalents, receivables, accounts payable and accrued liabilities, bank indebtedness and loans payable approximate their fair value due to their short-term nature. Income earned on the Group’s cash and cash equivalents has been disclosed in the consolidated statements of comprehensive loss under the caption “interest and other income.”

ODIN MINING AND EXPLORATION LTD. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Year ended December 31, 2014

(expressed in U.S. dollars)

- 25 -

15. FINANCIAL INSTRUMENTS (continued) (b) Fair Value Measurements

The fair value of financial assets and financial liabilities at amortized cost is determined in accordance with generally accepted pricing models based on discounted cash flow analysis or using prices from observable current market transactions. The fair value of the Group’s cash and cash equivalents, receivables, accounts payable and accrued liabilities, bank indebtedness and loans payable approximate their carrying amounts largely due to the short-term maturities of these instruments.

The fair value of financial instruments that are measured subsequent to initial recognition at their fair value, is measured within a ‘fair value hierarchy’ which has the following levels:

(i) Level 1: quoted prices (unadjusted) in active markets for identical assets or liabilities (ii) Level 2: valuation techniques using inputs other than quoted prices included in Level 1 that are

observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

(iii) Level 3: valuation techniques using inputs for the asset or liability that are not based on observable market data (unobservable inputs).

The Company did not have any financial instruments that were measured at Level 2 or 3 valuation techniques.

16. FINANCIAL INSTRUMENT RISKS

The Group is exposed to various risks in relation to financial instruments. The main types of risk are credit risk, liquidity risk and market risk. These risks arise from the normal course of the Group’s operations and all transactions undertaken are to support the Group’s ability to continue as a going concern. The risks associated with these financial instruments and the policies on mitigation of such risks are set out below. Management manages and monitors these exposures to ensure appropriate measures are implemented in a timely and effective manner.

(a) Credit Risk

The Group considers that its cash and cash equivalents and receivables are exposed to credit risk, representing