Embed Size (px)

Citation preview

Capitalizing on the Retailization

of Health Care

Helena Foulkes

Executive Vice President &

President, CVS Pharmacy

2

Agenda

Retail Pharmacy

Partnering Through Enterprise Capabilities

Update on Key Assets

Front Store Growth Strategy

Retail Pharmacy

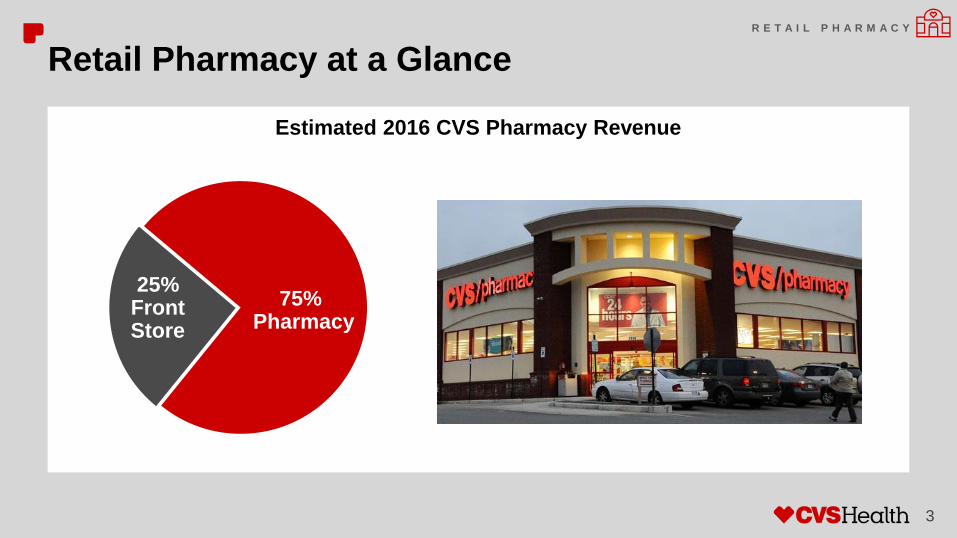

Retail Pharmacy at a Glance

3

Estimated 2016 CVS Pharmacy Revenue

75% Pharmacy

25%FrontStore

R E T A I L P H A R M A C Y

CVS Pharmacy Share of Total U.S. Retail Prescriptions

20.8%23.8%

2013 Sep YTD 2016 Sep YTD

+300bps

Strong Record of Pharmacy Share Growth Over the Past Several Years

4

R E T A I L P H A R M A C Y

Refer to endnotes for additional information.

5

Significant Presence in the U.S. Retail Pharmacy Market

• 9,600+ retail

locations

• More than 1.1B retail

scripts filled annually

Size and Scale

We own the last mile through our unmatched patient touchpoints and high frequency of consumer interaction

R E T A I L P H A R M A C Y

Refer to endnotes for additional information.

6

A Strong Track Record of Leading Performance

We deliver best-in-class clinical outcomes to all patients

74.579.1 80.180.6

84.9 83.5

High-CholesterolHypertensionDiabetes

Medication Possession Ratio

+610bps

+580bps

+340bps

CVS PharmacyTop Competitors

R E T A I L P H A R M A C Y

Refer to endnotes for additional information.

• Our history with CVS Caremark

has focused us on outcomes

• We have built clinical programs

into our workflow

• This ensures that performing

clinical programs is a key priority

An Integrated Approach

7

Our Success Is Driven by Integrating Clinical Programs Into Our Workflow System

We are now leveraging these “clinical pipes” with other PBMs and health plans

PATIENT CARE – GAP IN CARE

Smith, John Phone Number: 123-456-7899

DOB: 01/01/1900 Age: 56 Years Gender: Male Txt Message: Not added

If you have diabetes, its important to speak with your doctor about the best ways to manage

your condition

• Common long-term effects of diabetes can include reduced heart rate function

• Statin therapy may help prevent this complication

• Since we do not see a statin medication in your profile, we can contact your doctor to

review this information

• Your doctor will determine if a statin therapy is appropriate for you

Instructions: Confirm patient has gap in care and discuss reasons to close therapy

gap. If creating prescriber request, always confirm the correct prescriber to contact

with the patient.

Your pharmacist would like to speak with you today

about a potential gap in your care

R E T A I L P H A R M A C Y

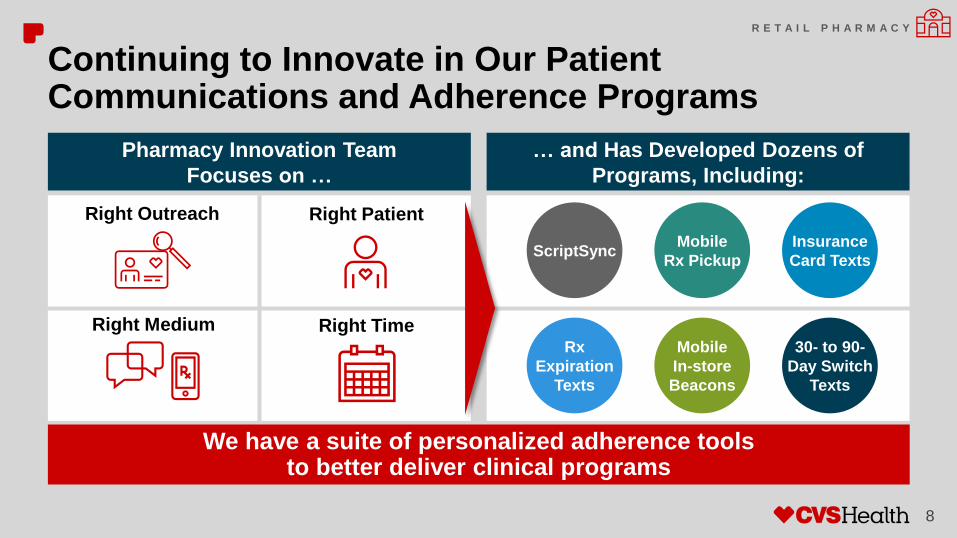

… and Has Developed Dozens of

Programs, Including:

Right Medium

Right Outreach

ScriptSync

8

Continuing to Innovate in Our Patient Communications and Adherence Programs

We have a suite of personalized adherence tools to better deliver clinical programs

Right Patient

Right Time

Pharmacy Innovation Team

Focuses on …

Mobile

Rx Pickup

Insurance

Card Texts

Rx

Expiration

Texts

Mobile

In-store

Beacons

30- to 90-

Day Switch

Texts

R E T A I L P H A R M A C Y

9

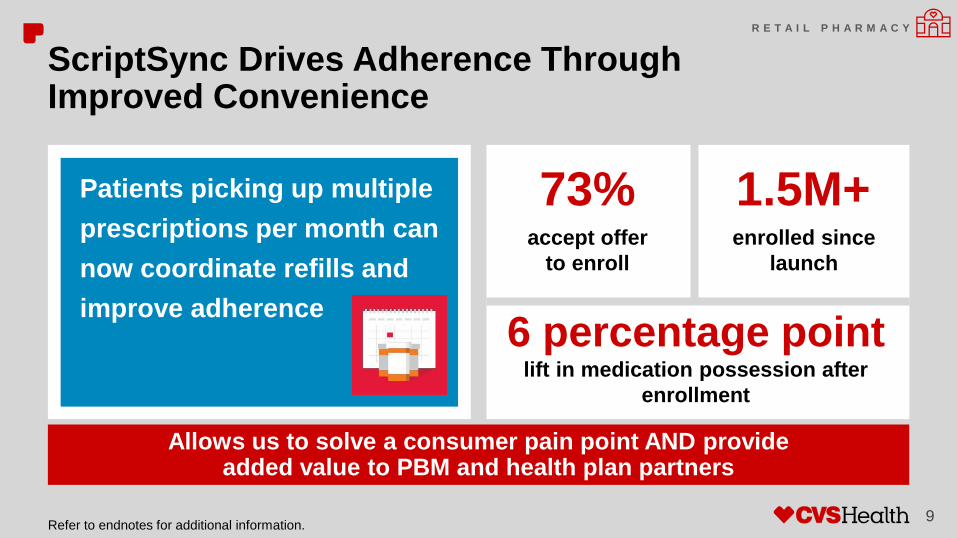

ScriptSync Drives Adherence Through Improved Convenience

Allows us to solve a consumer pain point AND provide added value to PBM and health plan partners

Patients picking up multiple

prescriptions per month can

now coordinate refills and

improve adherence

1.5M+ enrolled since

launch

73%accept offer

to enroll

6 percentage pointlift in medication possession after

enrollment

R E T A I L P H A R M A C Y

Refer to endnotes for additional information.

10

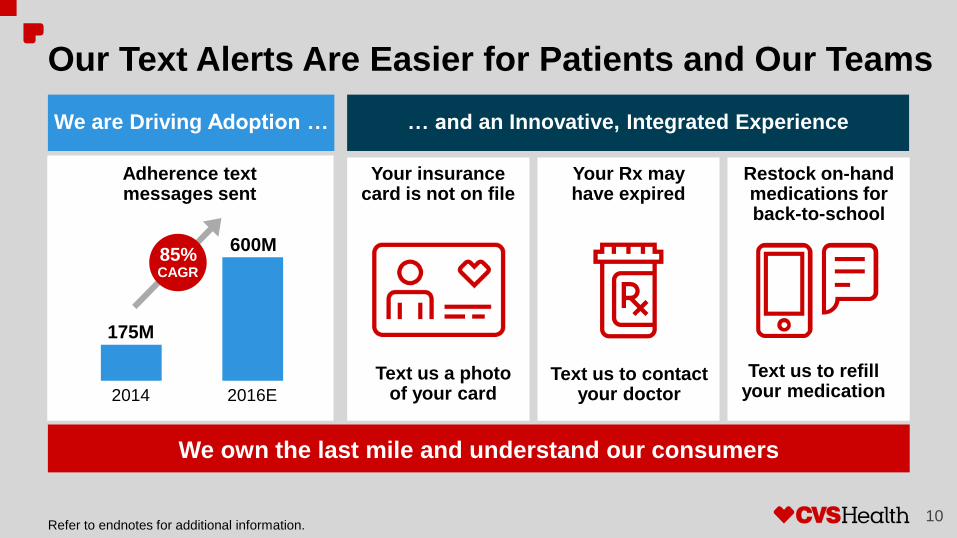

Our Text Alerts Are Easier for Patients and Our Teams

We own the last mile and understand our consumers

We are Driving Adoption … … and an Innovative, Integrated Experience

175M

2016E2014

600M

Adherence text messages sent

Your insurance card is not on file

Your Rx mayhave expired

Restock on-hand medications for back-to-school

85%CAGR

Text us to refill your medication

Text us to contact your doctor

Text us a photo of your card

Refer to endnotes for additional information.

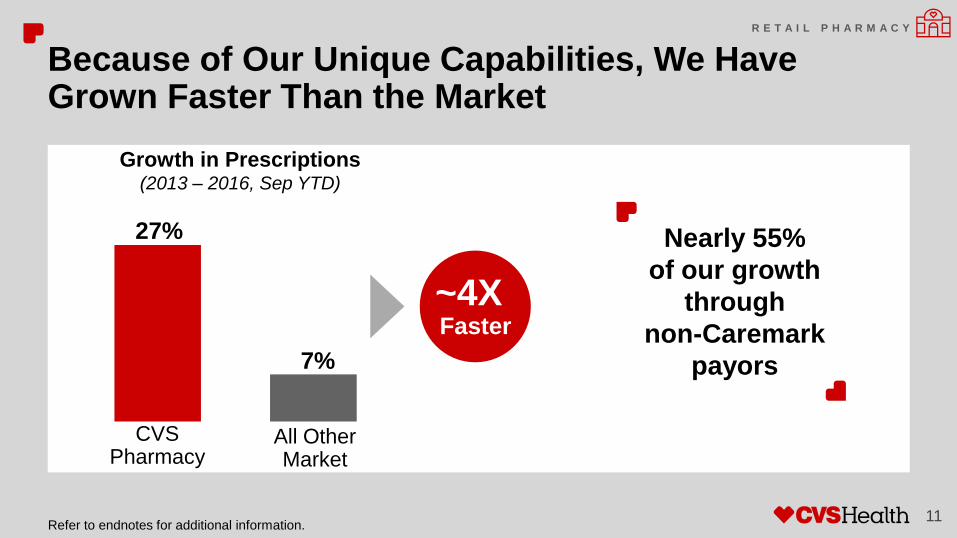

Nearly 55%

of our growth

through

non-Caremark

payors

11

Because of Our Unique Capabilities, We Have Grown Faster Than the Market

27%

7%

All OtherMarket

CVSPharmacy

~4XFaster

Growth in Prescriptions(2013 – 2016, Sep YTD)

R E T A I L P H A R M A C Y

Refer to endnotes for additional information.

12

A Majority of Our Scripts Are Non-Caremark

CVS Pharmacy Scripts by PBM(Oct 2016 YTD)

CVS Caremark35%65%

We are committed to partnering with other PBMs by leveraging the assets of CVS Health

Other PBMs

and Payors

R E T A I L P H A R M A C Y

13

Agenda

Retail Pharmacy

Partnering Through Enterprise Capabilities

Update on Key Assets

Front Store Growth Strategy

Partnering Through Enterprise Capabilities

…enabling us to deliver superior outcomes at a lower cost

14

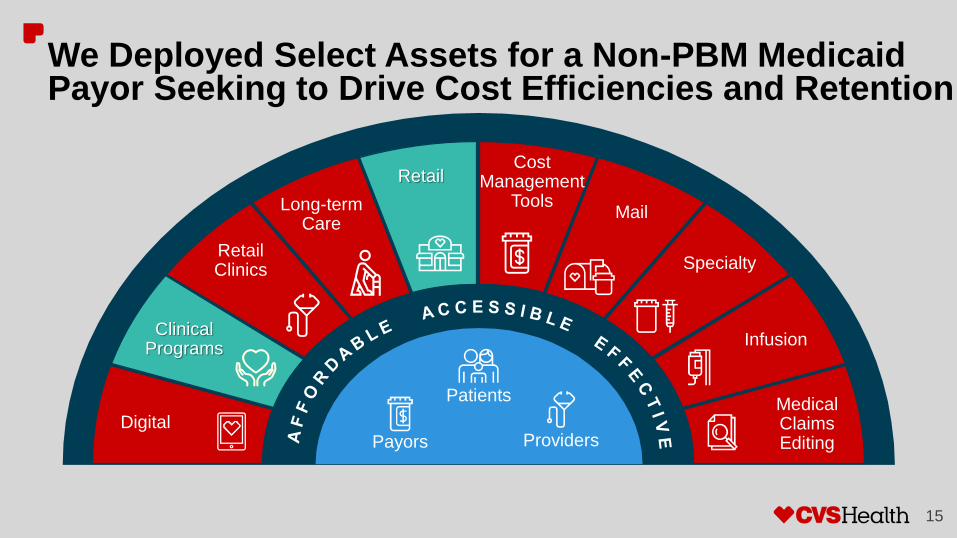

Bringing Together Assets From All of CVS Health to Win With PBMs and Health Plans

Patients

Payors Providers

Retail

MailLong-term Care

Infusion

Medical Claims Editing

Digital

RetailClinics Specialty

Clinical Programs

Cost Management

Tools

Clinical Programs

15

We Deployed Select Assets for a Non-PBM Medicaid Payor Seeking to Drive Cost Efficiencies and Retention

Patients

Payors Providers

MailLong-term Care

Infusion

Medical Claims Editing

Digital

RetailClinics Specialty

Cost Management

Tools

Retail

16

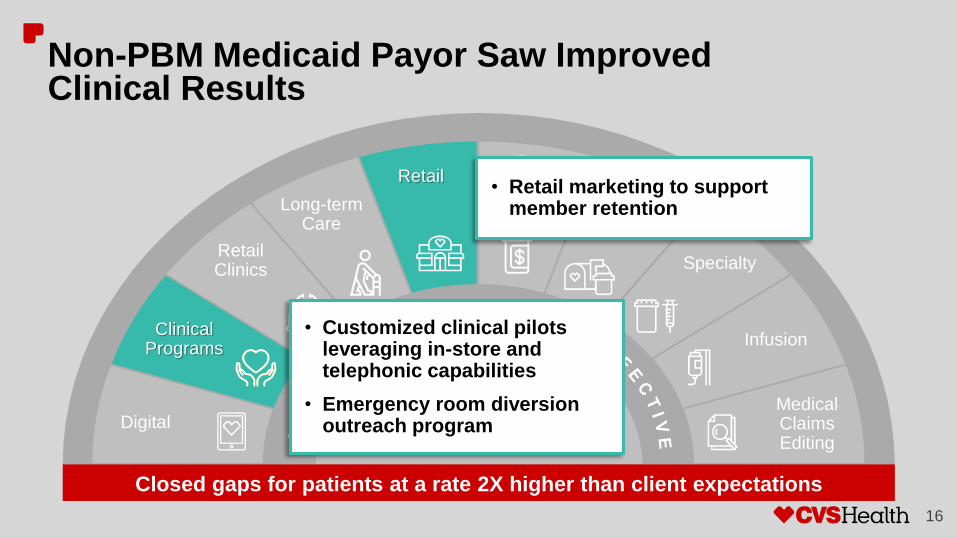

Non-PBM Medicaid Payor Saw Improved Clinical Results

Patients

Payors Providers

MailLong-term Care

Infusion

Medical Claims Editing

Digital

RetailClinics Specialty

Retail

Clinical Programs

• Customized clinical pilots leveraging in-store and telephonic capabilities

• Emergency room diversion outreach program

Closed gaps for patients at a rate 2X higher than client expectations

Cost Management

Tools• Retail marketing to support

member retention

17

For Another Non-PBM Client, We Used Our Clinical Programs to Improve Star Ratings

Patients

Payors Providers

MailLong-term Care

Infusion

Medical Claims Editing

Digital

RetailClinics Specialty

Retail

Clinical Programs

Cost Management

Tools

18

Non-PBM Client Achieved Improvements in Star Ratings Across Multiple Plans

Patients

Payors Providers

MailLong-term Care

Infusion

Medical Claims Editing

Digital

RetailClinics Specialty

Retail

Clinical Programs

• Clinical interventions and future initiatives:− Client clinical rules engine

− ScriptSync

− CVS Pharmacy Clinical call center

Assisted plan in improving Star rating from 3 to 4 and achieved 4% increase in adherence

Cost Management

Tools

• Adherence and refill opportunities

executed and enabled:− ReadyFill and 90-Day Retail

− Care 1-on-1

…enabling us to deliver superior outcomes at a lower cost

CVS Health Is Launching a Strategic Relationship With Optum

Patients

Payors Providers

Retail

MailLong-term Care

Infusion

Medical Claims Editing

Digital

RetailClinics Specialty

Clinical Programs

19

Cost Management

Tools

20

CVS Health Is Launching a Strategic Relationship With Optum

Partnering to Offer Employers a

New Pharmacy Network Option

• Fill 90-day scripts at any CVS Pharmacy or via OptumRx

home delivery

• Help improve consumer engagement and help health

outcomes by leveraging CVS Pharmacy’s unmatched clinical

capabilities

• Going forward, Optum and CVS Pharmacy will continue

to develop new pharmacy and health solutions leveraging

our suite of assets

By continuingto partner with

other PBMs and health plans we

will grow our prescription

share

Goal

21

Agenda

Retail Pharmacy

Partnering Through Enterprise Capabilities

Update on Key Assets

MinuteClinic

Omnicare

Target

Front Store Growth Strategy

MinuteClinic

More than 50% of the U.S. population is within 10 miles of a MinuteClinic

• Fully integrated 79

Target clinic locations

• > 50% retail clinic

market share

• Approximately three times

larger footprint than closest

competitor

22

MinuteClinic Footprint Covers Most Populous U.S. Areas

1,136Total Clinics

MinuteClinicClinic State

M I N U T E C L I N I C

Refer to endnotes for additional information.

23

MinuteClinic Enhances the CVS Value Proposition to Patients, Providers, Payors and PBMs

• Address gaps in care with

providers, payors and PBMs

• Provide health risk

assessments/biometric

screenings

• Electronic record integration

with health systems

Investing in:

• Scheduling tools and

walk-in options

• Expansion of primary

care services

• Telehealth

• Up to 80% less expensive

than other sites of care

• MinuteClinic Savings

Strategy can further reduce

costs

Low-Cost Care Population HealthPatient Engagement

and Access

M I N U T E C L I N I C

24

Agenda

Retail Pharmacy

Partnering Through Enterprise Capabilities

Update on Key Assets

MinuteClinic

Omnicare

Target

Front Store Growth Strategy

Omnicare

25

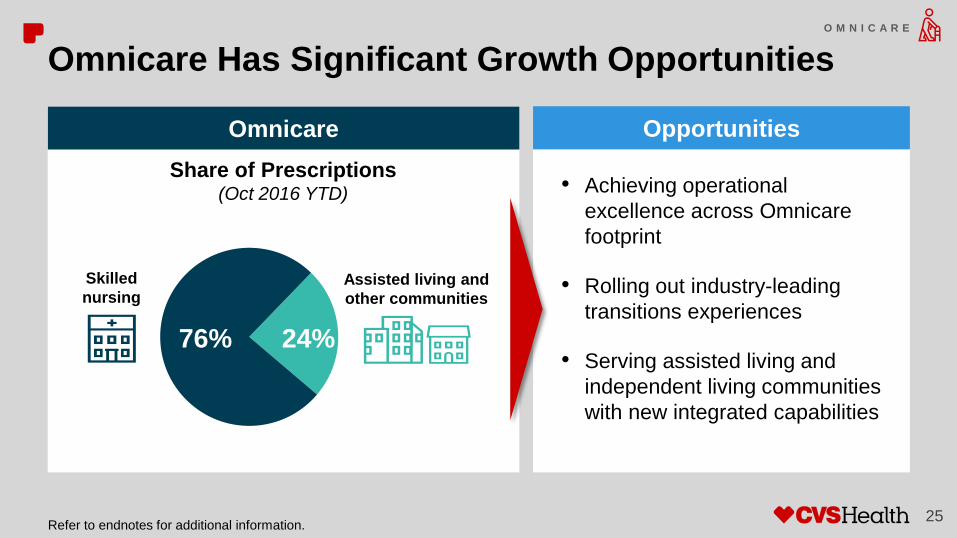

Omnicare Has Significant Growth Opportunities

76% 24%

Skilled

nursingAssisted living and

other communities

• Achieving operational

excellence across Omnicare

footprint

• Rolling out industry-leading

transitions experiences

• Serving assisted living and

independent living communities

with new integrated capabilities

Omnicare Opportunities

Share of Prescriptions(Oct 2016 YTD)

O M N I C A R E

Refer to endnotes for additional information.

26

We Have Applied CVS Operational Excellence Across the Omnicare Footprint

• New workflow and intake process for

assisted living move-ins

• Technology upgrades and

investments including:

− Labor scheduling tools

− Prescribing enhancements to

staff workflow

Additional Operational Improvements

• STAT Fill Services now leverage

national CVS Pharmacy network for

urgent medication needs

• 77% of Omnicare-served senior living

communities are within three miles of a

CVS Pharmacy

STAT Fill

O M N I C A R E

27

Investments in Transitions Enhances Our Market Positioning

Skilled nursing

Residential home

Acute care hospital

O M N I C A R E

Goal of reducing medication

transfer time from ten hours to

two and a half hours

Reinvented

admission

experience

Transitions

of care

solution

Diverting hospital readmissions

through greater pharmacy care

oversight

These new services will further reduce hospital readmissions for clients

28

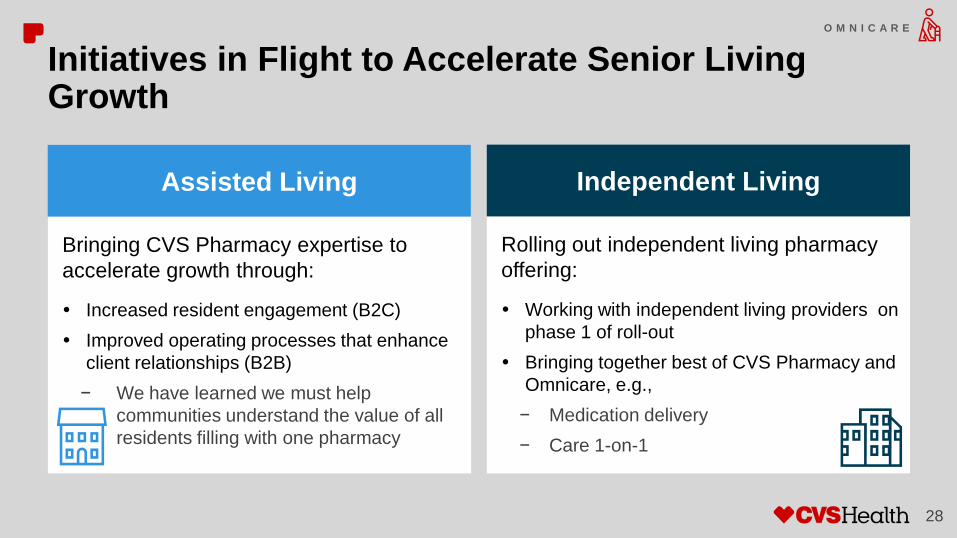

Initiatives in Flight to Accelerate Senior Living Growth

Assisted Living

Rolling out independent living pharmacy

offering:

Working with independent living providers on

phase 1 of roll-out

Bringing together best of CVS Pharmacy and

Omnicare, e.g.,

− Medication delivery

− Care 1-on-1

Independent Living

Bringing CVS Pharmacy expertise to

accelerate growth through:

Increased resident engagement (B2C)

Improved operating processes that enhance

client relationships (B2B)

− We have learned we must help

communities understand the value of all

residents filling with one pharmacy

O M N I C A R E

29

Agenda

Retail Pharmacy

Partnering Through Enterprise Capabilities

Update on Key Assets

MinuteClinic

Omnicare

Target

Front Store Growth Strategy

Target

30

Acquisition of Target Pharmacies Is Helping Fill in Our Geographic Footprint

Nationwide store

count increased

>20%

Percent increase in store

count after acquisition

>100%

45-99%

11-44%

<10%

T A R G E T P A R T N E R S H I P

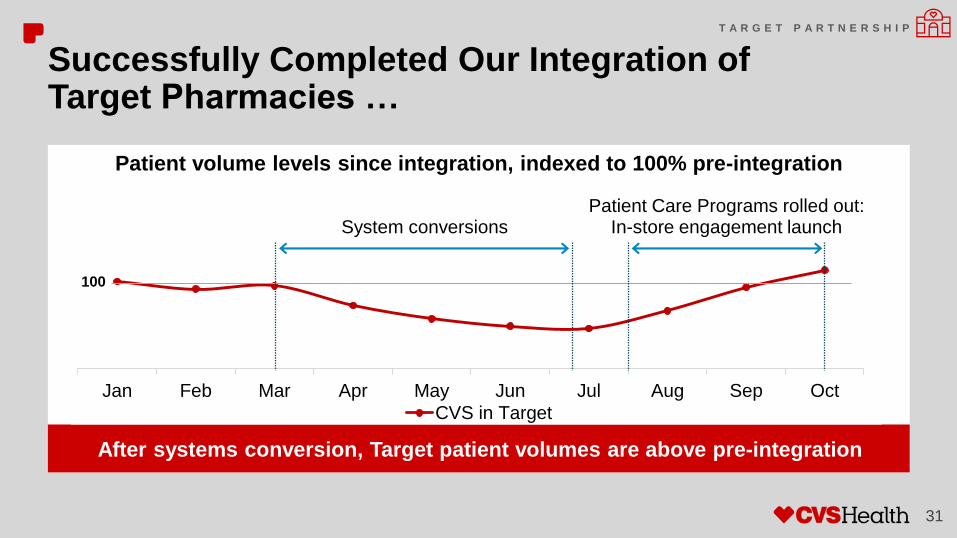

Successfully Completed Our Integration of Target Pharmacies …

31

Patient volume levels since integration, indexed to 100% pre-integration

After systems conversion, Target patient volumes are above pre-integration

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

CVS in Target

System conversions

100

Patient Care Programs rolled out: In-store engagement launch

T A R G E T P A R T N E R S H I P

32

… and Are Already Driving Traffic and Business Into Target, With More to Come in 2017

Proprietary Program Growth(prescription growth, 2017E vs. 2016E)

2.2x

1.4xMaintenance

Choice

Patient Care Programs

Patient and In-Store

Experience

Successful in-store engagements

to accelerate in 2017

T A R G E T P A R T N E R S H I P

33

Agenda

Retail Pharmacy

Partnering Through Enterprise Capabilities

Update on Key Assets

Front Store Growth StrategyFront Store Growth Strategy

• Expand personalization to

deepen relationships with our most

loyal customers

• Invest in digital to deliver

convenience to our customers

• Leverage front store to enhance

pharmacy customer experience

• Continue to elevate Health,

Healthy Food and Beauty

• Help customers discover

innovative products

3434

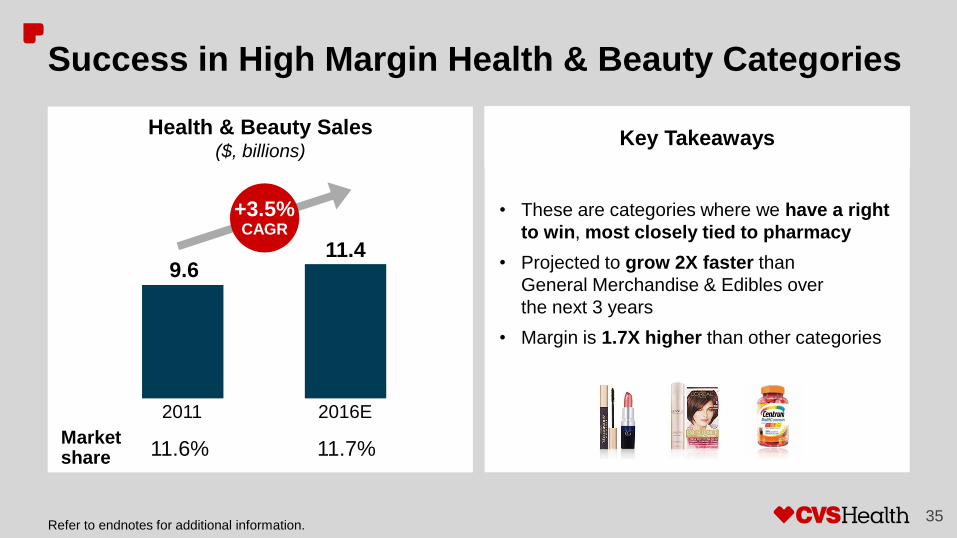

We Believe the Role of the Front Store Is to Support Our Pharmacy and Drive Margin

Key TakeawaysHealth & Beauty Sales

($, billions)

9.611.4

2016E2011

+3.5% CAGR

35

Success in High Margin Health & Beauty Categories

• These are categories where we have a right

to win, most closely tied to pharmacy

• Projected to grow 2X faster than

General Merchandise & Edibles over

the next 3 years

• Margin is 1.7X higher than other categories

Marketshare 11.6% 11.7%

Refer to endnotes for additional information.

2011 2016E Long-TermGoal

Store Brands Penetration

~17%

~22%25%

Store Brands penetration up 300 basis points since 2014

36

Continued Success in Store Brands

Rebranding and

messaging of Health

OTC-on-the-go packs

at the Pharmacy

Gold Emblem

Abound

Exclusive

MUA offering

Cold and Flu single

serve cups

Driving Innovation

Refer to endnotes for additional information.

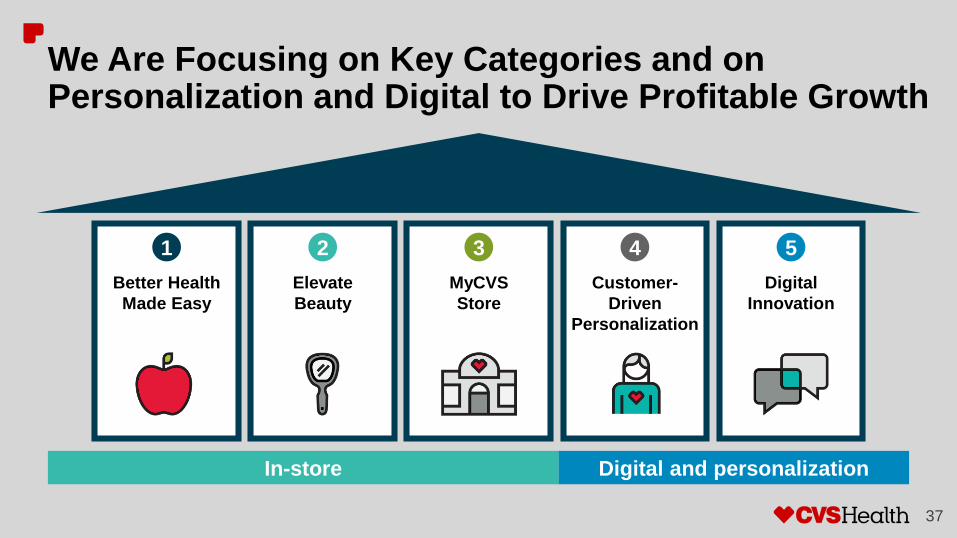

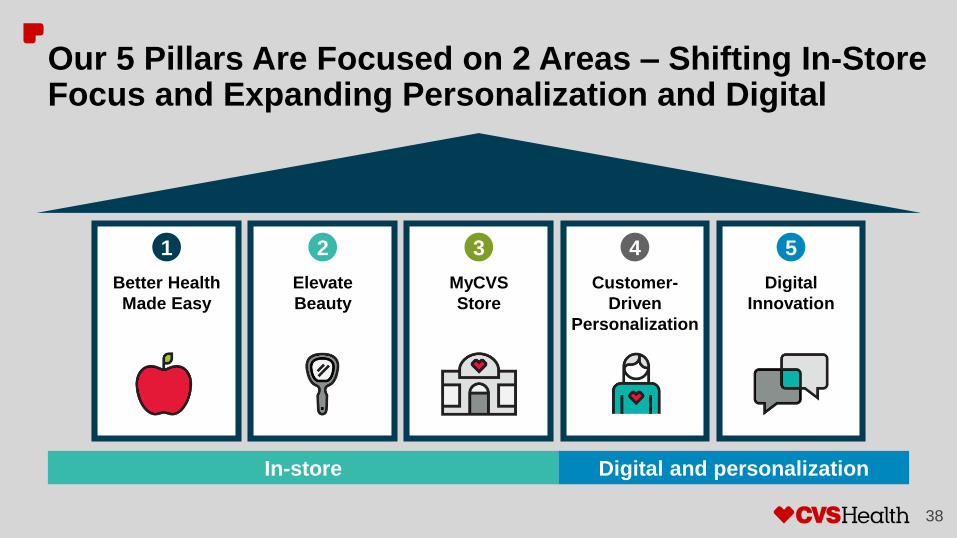

MyCVS

Store

Elevate

Beauty

Better Health

Made Easy

Digital

Innovation

Customer-

Driven

Personalization

In-store Digital and personalization

37

We Are Focusing on Key Categories and on Personalization and Digital to Drive Profitable Growth

1 2 3 54

MyCVS

Store

Elevate

Beauty

Better Health

Made Easy

Digital

Innovation

Customer-

Driven

Personalization

In-store Digital and personalization

38

1 2 3 54

Our 5 Pillars Are Focused on 2 Areas – Shifting In-Store Focus and Expanding Personalization and Digital

39

We Are Updating Our Stores by Growing Core Categories

No costs beyond standard reset

Health & Beauty Other Categories

% Health & Beauty

2014

~50%

Today (~800 stores)

~65%

Future State

80%

I N - S T O R E

40

Expanding and Elevating Our Health Assortment

“Discovery Zones” highlight

emerging products

New endcaps

elevate OTC at

front of store …

… and emphasize

our health expertise

to the customer

I N - S T O R E

41

“Discovery Zone”

brings variety of

healthy snack, food

and drink options

Innovative store

brand options

developed

“Trend Zone”

highlights rotating

and limited quantity

set of snacks and

drinks

Expanding and Elevating Our Healthy Food SelectionI N - S T O R E

42

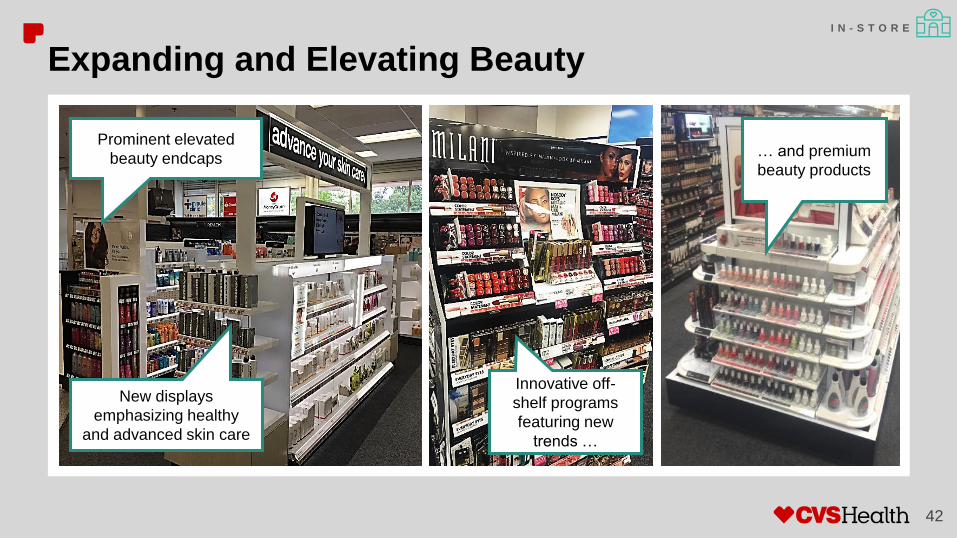

Expanding and Elevating Beauty

Innovative off-

shelf programs

featuring new

trends …

… and premium

beauty products

Prominent elevated

beauty endcaps

New displays

emphasizing healthy

and advanced skin care

I N - S T O R E

43

We Are Seeing Positive Run-Rate Resultsin 400 Stores

Potential to scale-up resets in 3,000 stores over next several years

After

Sample Store Reset Run-Rate Results

Consumables

Beauty

Health

General Merchandise

Front Store Total

+9%

+4%

+2%

-6%

+2.5%

Before

After

I N - S T O R E

Refer to endnotes for additional information.

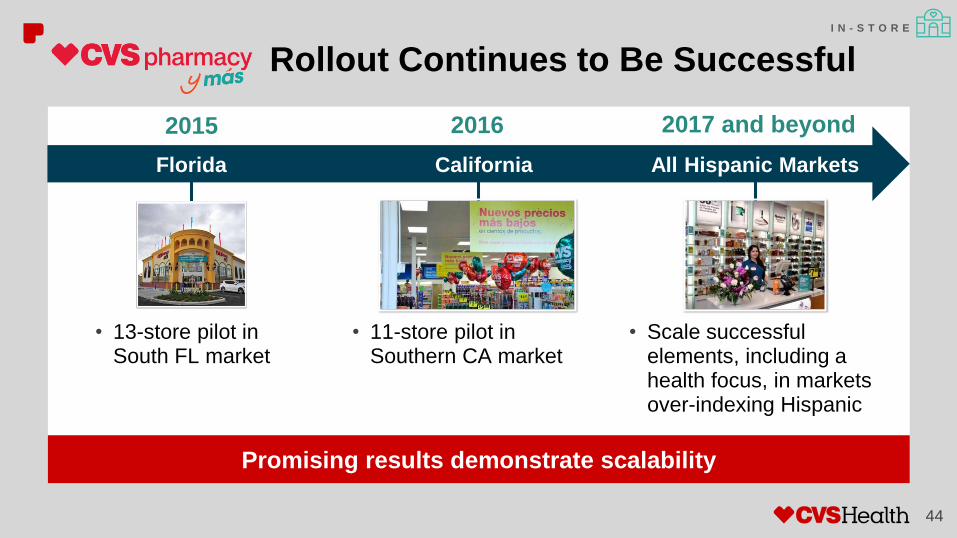

• Scale successful elements, including a health focus, in markets over-indexing Hispanic

• 11-store pilot in Southern CA market

• 13-store pilot in South FL market

44

Florida California All Hispanic Markets

Promising results demonstrate scalability

Rollout Continues to Be Successful

2015 2016 2017 and beyond

I N - S T O R E

45

Traditional Circular Vehicles Are in Decline

• Shifting promotional dollars from

mass to digital and personalized

• Targeting top customers who drive

majority of our margin

100

70

2020+

Continued decline

2016E2010

CVS Circular DistributionIndexed to 2010

We are leading the market by scaling back on our circular promotions

Our Focus

P E R S O N A L I Z A T I O N A N D D I G I T A L

Refer to endnotes for additional information.

46

We Are Optimizing Our Approach to Promotions and Investing in Personalization

From To

• Readership down

• Pages and blocks down

• Social media (Facebook,

Pinterest) up

• Digital circular (Flipp) up

• Personalized messages up

P E R S O N A L I Z A T I O N A N D D I G I T A L

Predictive Modeling Offer Optimization Tailored Creative

47

Personalization Helps Us Deliver the Right Messages to the Right Customers

Expanding personalization’s reach to accelerate the shift from mass

P E R S O N A L I Z A T I O N A N D D I G I T A L

48

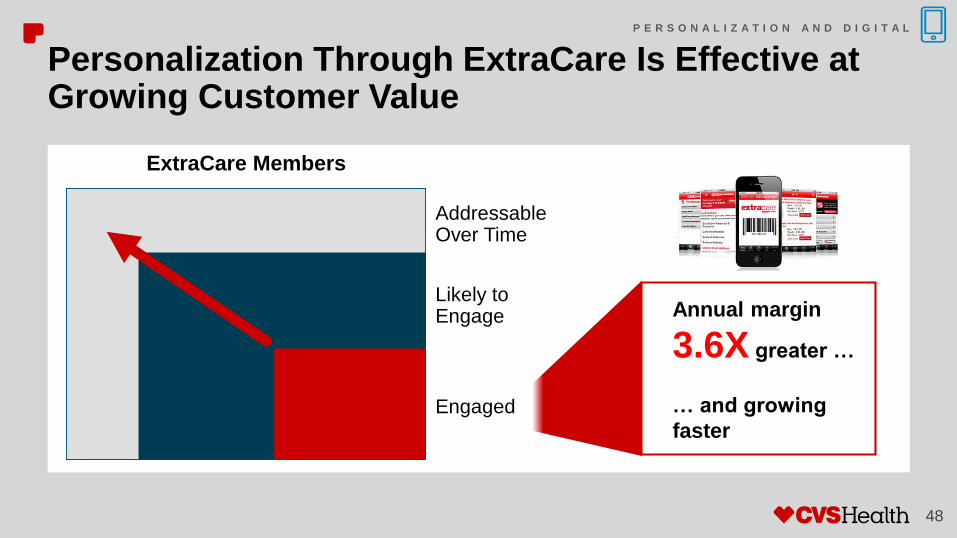

Personalization Through ExtraCare Is Effective at Growing Customer Value

Engaged

Likely to Engage

Addressable Over Time

ExtraCare Members

P E R S O N A L I Z A T I O N A N D D I G I T A L

Annual margin

3.6X greater …

… and growing

faster

We Have Invested in Digital While Leveraging Our 9,600+ Store Locations

49

Omnichannel Innovations

• On Demand In Hours− Front Store pilot in process

− Rx (with Front Store) pilot

coming soon

• Front Store and CVS Curbside− Rx Curbside pilot coming soon

− Front Store available in 4,000

stores

P E R S O N A L I Z A T I O N A N D D I G I T A L

50

Front Store Future Plans

We are focused on

driving profitable

growth across our

stores

• Grow our profitable Health,

Healthy Food and Beauty categories

• Continue to deliver innovative

products and digital experiences to

our customers

• Expand personalization to build

stronger relationships with loyal

customers

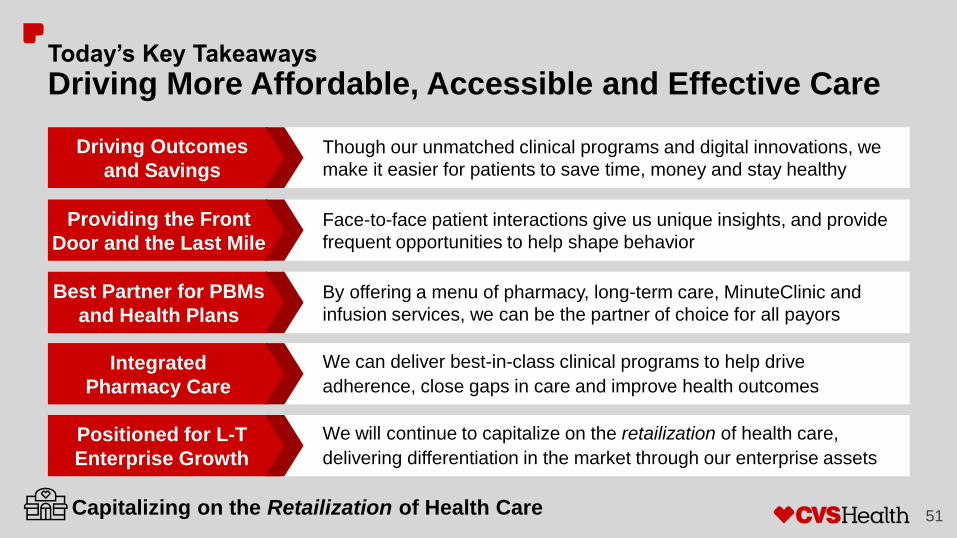

Today’s Key Takeaways

Driving More Affordable, Accessible and Effective Care

Though our unmatched clinical programs and digital innovations, we

make it easier for patients to save time, money and stay healthy

Driving Outcomes

and Savings

Face-to-face patient interactions give us unique insights, and provide

frequent opportunities to help shape behavior

Providing the Front

Door and the Last Mile

By offering a menu of pharmacy, long-term care, MinuteClinic and

infusion services, we can be the partner of choice for all payors

Best Partner for PBMs

and Health Plans

We will continue to capitalize on the retailization of health care,

delivering differentiation in the market through our enterprise assets

Positioned for L-T

Enterprise Growth

51

We can deliver best-in-class clinical programs to help drive

adherence, close gaps in care and improve health outcomes

Integrated

Pharmacy Care

Capitalizing on the Retailization of Health Care

52

EndnotesSlide 4

1. Compares 2016 90-day adjusted scripts from January through September to 2013 January through September. 2016

includes Target. Source: IMS. Retail scripts include the adjustment to convert 90-day prescriptions to the equivalent of

three 30-day prescriptions. This adjustment reflects the fact that these prescriptions include three times the amount of

product days supplied compared to a normal 30-day prescription.

Slide 5

1. Reflects 90 day adjusted scripts filled at all CVS retail locations. Source: CVS Health internal data analysis. Retail scripts

include the adjustment to convert 90-day prescriptions to the equivalent of three 30-day prescriptions.

Slide 6

1. Reflects unadjusted scripts filled at all CVS retail locations by Caremark PBM members in the last twelve months through

October 2016. Source: CVS Health internal data analysis.

Slide 9

1. Retail ScriptSync™ Lift in Medical Possession Ratio: internal data analysis based on first 4 months of program enrollment.

2. Days on Hand Ratio measures how adherent patients are to all of their medications and number of days a patient had

access to medications compared to the number of days in the measurement period.

Slide 10

1. Texts expected for 2016 through year end. Source: CVS Health internal data analysis.

Slide 11

1. Total CVS Pharmacy reflects prescriptions for 90 day adjusted scripts January through September for 2013 compared with

January through September for 2016. 2016 CVS includes Target. Total market reflects 90 day adjusted scripts January

through September for 2013 compared with January through September for 2016 excluding CVS Pharmacy. Source: IMS.

Retail scripts include the adjustment to convert 90-day prescriptions to the equivalent of three 30-day prescriptions.

53

EndnotesSlide 22

1. MinuteClinic count as of December 8, 2016.

Slide 25

1. Omnicare prescriptions year-to-date October, 2016. Source: CVS Health internal data analysis.

Slide 35

1. Market is defined as remainder of Food/Drug/Mass; Compares 2016 year-to-date through August to January 2011 through

August 2011. Source: IRI, CVS Health internal data analysis.

2. Source: CVS Health internal data analysis, IRI, Mintel market reports, Global-Markets reports, ITE Beauty.

Slide 36

1. Based on Store Brand Drug Store market. 2016 year-to-date through August. Source: CVS Health internal data analysis;

IRI.

Slide 43

1. Incremental lift based on 2015 full store resets vs. control stores, steady-state measurement; Source: CVS Health internal

data analysis.

Slide 45

1. Sources: State of the News Media, The Pew Research Center, http://www.journalism.org/2015/04/29/newspapers-fact-

sheet/, April 2015; The State of Radio, Newspapers & Magazines, The Video Advertising Bureau, www.thevab.com,

November 2015.

![-ravichandran@uiowa.edu] CVS Health (CVS) September … · Through the above service, CVS helps clients in designing ... Improvement, and Modernization ... prescriptions at CVS Pharmacy](https://img.pdfslide.net/doc/110x75/5b5140327f8b9a056a8bdae7/-ravichandranuiowaedu-cvs-health-cvs-september-through-the-above-service.jpg)