Embed Size (px)

Citation preview

OFFICE OF THE AUDITOR

DEPARTMENT OF PUBLIC WORKS CASH KEY PARKING PROGRAM

PROGRAM AUDIT

FEBRUARY 2007

Dennis J. Gallagher Auditor

City and County of Denver 201 West Colfax Ave., Dept. 705 • Denver, Colorado 80202 • 720-913-5000, FAX 720-913-5247

www.denvergov.org/auditor Dennis J. Gallagher

Auditor

February 21, 2008 Mr. Guillermo “Bill” Vidal, Manager Department of Public Works City and County of Denver Dear Mr. Vidal: Attached is the Auditor’s Office Audit Services Division’s audit report of Public Works’ Cash Key parking program for the fiscal year ended December 31, 2006. The purpose of the audit was to determine whether program revenues were properly reported, internal controls and accounting processes were adequate, and the Agency complied with applicable City rules and regulations. The audit revealed reportable weaknesses related to contract administration, internal controls, and refund payments. These weaknesses are disclosed in detail within the accompanying report. If you have any questions, please contact Kip Memmott, Director of Audit Services, at 720-913-5029.

Sincerely,

Dennis J. Gallagher Auditor

DJG/kh cc: Honorable John Hickenlooper, Mayor

Honorable Members of City Council Members of Audit Committee David Fine, City Attorney Lauri Dannemiller, City Council Staff Director Kelly Brough, Chief of Staff Claude Pumilia, Chief Financial Officer Chris Henderson, Chief Operating Officer Beth Machann, Controller Barbara Puls, Manager, Public Works Finance and Administration

The prudent stewardship of Denver’s finances, resources and financial records! We are also committed to improving accountability, efficiency, effectiveness and performance in city government. We will scrupulously

protect the taxpayer’s interests and work collaboratively with all concerned to improve our city and its government 1

TABLE OF CONTENTS

Transmittal Letter 1

Table of Contents 2

Auditors’ Report 3

Executive Summary 4

Background, Scope, Objective, and Methodology 5

Findings and Recommendations 7

Exhibit A – Public Works’ Response 10

2

City and County of Denver 201 West Colfax Ave., Dept. 705 • Denver, Colorado 80202 • 720-913-5000, FAX 720-913-5247

www.denvergov.org/auditor Dennis J. Gallagher Auditor

AUDITORS’ REPORT We have completed an audit of the Public Works Cash Key parking program. The purpose of the audit was to determine whether Public Works (Agency) properly administered the program and complied with City rules and regulations. This audit was included in the Auditor’s Office Audit Services Division’s 2007 Annual Audit Plan and is authorized pursuant to the City and County of Denver Charter, Article V, Part 2, Section 1, General Powers and Duties of the Auditor. We conducted our audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain reasonable assurance that revenues were properly reported and internal controls were adequate. An audit includes examining, on a test basis, evidence supporting compliance with revenue reporting, accounting and internal controls, and City rules and regulations. The audit revealed Public Works did not comply with Executive Order No. 8, which governs City contracts, and City Fiscal Accountability Rules (Fiscal Rules) related to financial transactions and internal controls. We extend our appreciation to the personnel who assisted and cooperated with us during the audit. Audit Services Division

Kip R. Memmott, CGAP, CICA Director of Audit Services Date: February 21, 2008 Staff: Dick Wibbens, CPA, Audit Manager Philip Cummings, CPA, CFE, Audit Supervisor Mike Widner, Lead Auditor Rebecca Corral, Senior Auditor

The prudent stewardship of Denver’s finances, resources and financial records! We are also committed to improving accountability, efficiency, effectiveness and performance in city government. We will scrupulously

protect the taxpayer’s interests and work collaboratively with all concerned to improve our city and its government. 3

PUBLIC WORKS CASH KEY PARKING PROGRAM

EXECUTIVE SUMMARY FOR THE YEAR ENDED DECEMBER 31, 2006

This summary highlights the audit findings of the Public Works Cash Key parking program, which focused on determining proper reporting of revenue, whether all payments due the City were made, internal controls and accounting processes were adequate, and assessing the Agency’s compliance with applicable City rules and regulations. The audit revealed Public Works was not in compliance with Executive Order No. 8, Contracts and Other Written Instruments, as well as Fiscal Rules related to financial transactions and internal controls. The Findings and Recommendations section of the report beginning on page 7 further describes these issues in detail. The Agency’s response is contained in Exhibit A beginning on page 10.

Finding I – Weaknesses in Internal Controls We noted Public Works has significant weaknesses in internal controls related to management oversight of cash handling functions, proper segregation of duties, and timely accounting entries. The lack of segregation of duties and supervisory review provides employees with opportunity to misappropriate assets and increases the risk that management will not detect or prevent errors or theft. We recommend Public Works strengthen cash handling and accounting supervisory review, implement proper segregation of duties, and ensure accounting entries are prepared in a timely manner.

Finding II – Weaknesses in the Refund Process Public Works does not have written policies and procedures in place concerning proper documentation and processing of customer refunds. Additionally, the Agency failed to research, review, and present proper documentation to support refund amounts in accordance with Fiscal Rules and Denver Revised Municipal Code (DRMC). As a result, 20% of the refund requests tested were issued for incorrect amounts. We recommend Public Works prepare written policies and procedures governing refund requests, payments, and reconciliations.

Finding III – Contract Administration Public Works does not have written contracts to govern the Tattered Cover Bookstore and Downtown Denver Partnership’s responsibilities for receiving Cash Key revenues on behalf of the City as required by Executive Order No. 8. As a result, the Agency placed the City and vendors at risk since there are no contract provisions governing payment due dates, late payment penalties, and financial reporting requirements. We recommend Public Works work with the City Attorney’s Office to immediately initiate contracts with third party vendors which outline specific Agency and vendor responsibilities in administration of the Cash Key parking program.

4

PUBLIC WORKS CASH KEY PARKING PROGRAM

BACKGROUND, SCOPE, OBJECTIVE, AND METHODOLOGY FOR THE YEAR ENDED DECEMBER 31, 2006

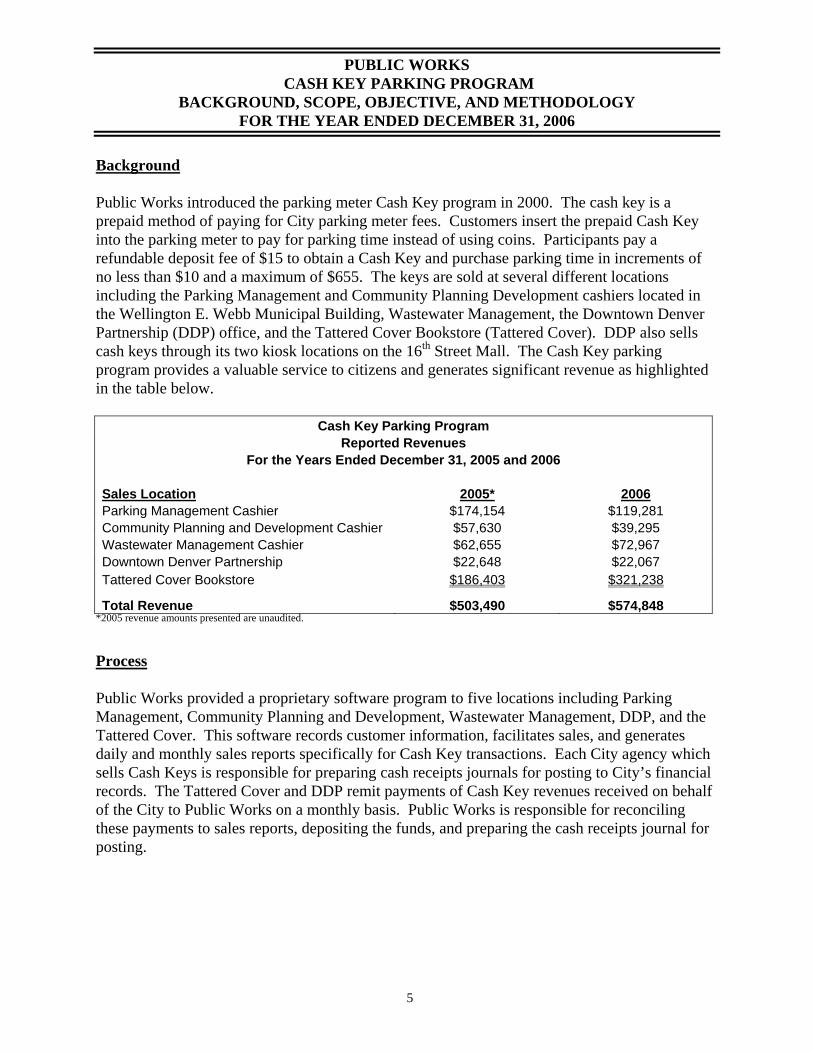

Background Public Works introduced the parking meter Cash Key program in 2000. The cash key is a prepaid method of paying for City parking meter fees. Customers insert the prepaid Cash Key into the parking meter to pay for parking time instead of using coins. Participants pay a refundable deposit fee of $15 to obtain a Cash Key and purchase parking time in increments of no less than $10 and a maximum of $655. The keys are sold at several different locations including the Parking Management and Community Planning Development cashiers located in the Wellington E. Webb Municipal Building, Wastewater Management, the Downtown Denver Partnership (DDP) office, and the Tattered Cover Bookstore (Tattered Cover). DDP also sells cash keys through its two kiosk locations on the 16th Street Mall. The Cash Key parking program provides a valuable service to citizens and generates significant revenue as highlighted in the table below.

Cash Key Parking Program Reported Revenues

For the Years Ended December 31, 2005 and 2006 Sales Location 2005* 2006Parking Management Cashier $174,154 $119,281 Community Planning and Development Cashier $57,630 $39,295 Wastewater Management Cashier $62,655 $72,967 Downtown Denver Partnership $22,648 $22,067 Tattered Cover Bookstore $186,403 $321,238

Total Revenue $503,490 $574,848 *2005 revenue amounts presented are unaudited.

Process Public Works provided a proprietary software program to five locations including Parking Management, Community Planning and Development, Wastewater Management, DDP, and the Tattered Cover. This software records customer information, facilitates sales, and generates daily and monthly sales reports specifically for Cash Key transactions. Each City agency which sells Cash Keys is responsible for preparing cash receipts journals for posting to City’s financial records. The Tattered Cover and DDP remit payments of Cash Key revenues received on behalf of the City to Public Works on a monthly basis. Public Works is responsible for reconciling these payments to sales reports, depositing the funds, and preparing the cash receipts journal for posting.

5

PUBLIC WORKS BACKGROUND, SCOPE, OBJECTIVE AND METHODOLOGY CASH KEY PARKING PROGRAM

6

The Cash Key deposit and any remaining dollar value are refunded to the customer if the key is defective or the customer no longer wants the key. Refund transactions are initiated at any of the five locations but payments are made only through the City voucher system. A request for refund form and supporting documentation is required for each refund. The documentation is submitted for processing through Public Works. Public Works is responsible for verifying the refund amounts, providing supporting documentation, and preparing refund voucher requests for payment to customers. Scope The audit of the Public Works Cash Key Program (PeopleSoft fund/org. 01010/5032500) was for the fiscal year ended December 31, 2006 and was conducted in accordance with generally accepted government auditing standards. The scope of the audit focused on determining whether program revenues were properly reported, internal controls and accounting processes were adequate, and the Agency complied with applicable City rules and regulations. Objective The objective of our audit was to determine whether all revenues due were received by the City, properly recorded in the City’s financial records, and internal controls and accounting processes were adequate. Our audit also determined whether Public Works administered the program in compliance with City rules and regulations. Methodology The evidence gathering and analysis techniques used in order to meet the objectives included, but were not limited to:

• Examination and testing of revenues on a sample basis • Examination and testing of customer refunds on a sample basis • Tracing source documents to revenues reported on check payments and the City’s

financial system • Determination of timeliness of payments • Review of internal controls • Discussions with management • Determination of compliance with Cash Key parking program written policies and

procedures • Determination of compliance with City Fiscal Rules, Executive Orders, and other

regulations • Testing of computer processed data

PUBLIC WORKS CASH KEY PARKING PROGRAM

FINDINGS AND RECOMMENDATIONS FOR THE YEAR ENDED DECEMBER 31, 2006

7

Finding I – Weaknesses in Internal Controls We identified weaknesses in internal controls related to management oversight of cash handling functions, proper segregation of duties, and timely accounting entries. Specifically, we noted: Lack of Oversight of the Cashiering Function - The supervisor does not conduct surprise counts of cash drawers, deposit amounts, or change funds reflecting a lack of management control and increased risk that theft would not be detected or prevented. Cash Receipt and Endorsement Weakness – The supervisor did not date stamp check payments to show the date of receipt, log the payments to create an independent record of funds received, or restrictively endorse the checks to discourage inappropriate negotiation. Lack of Segregation of Duties - One person is responsible for preparing deposits of vendor check payments, making deposits, and preparing cash receipt journals. Additionally, we noted this person has custody of the check endorsement stamp and receives and reconciles the bank statements. Assignment of one employee to an entire fiscal process creates opportunity for accounting impropriety and theft. Untimely Deposit Practices – Audit work revealed 6 of 13 (46%) Downtown Denver Partnership payments were recorded between 17 and 33 days after the check issue date indicating deposits were not made in a timely manner. Untimely Accounting Entries - The accounting technician did not submit cash receipts journals for recordation on a daily basis causing revenues to be posted between 6 and 27 days subsequent to the date of transaction. As a result, revenue for the sample period was overstated by $4,300 (16%) for November 2006. Fiscal Rule 2.4 establishes separation and rotation of duties as the basis of a good internal control system which acts as preventative and detective measures. This rule further outlines the responsibilities of the Agency to properly segregate job duties so that one person does not have control over an entire fiscal activity and assign responsibilities in a manner which encourages checks and balances. Additionally, Fiscal Rule 2.6 requires deposits which exceed certain dollar amounts be deposited by the following business day and revenues be reported in a timely manner.

PUBLIC WORKS FINDINGS AND RECOMMENDATIONS CASH KEY PARKING PROGRAM

Recommendation In order to strengthen management oversight, mitigate the risk of undetected errors and potential asset misappropriation, and improve timeliness of accounting entries, we recommend the Agency prepare written policies and procedures which require surprise cash counts by an employee who is independent of the cashiering function. Surprise counts should be regularly conducted in a spontaneous manner in order to identify whether proper cash handling controls have been circumvented. We also recommend Public Works designate an employee independent from the accounting function to receive, date stamp, and log all vendor payments. This employee should have custody of the restrictive endorsement stamp and stamp all check payments upon receipt. Deposits of vendor checks should be verified by the supervisor and made no later than the business day following receipt. Additionally, cash receipts journals should be prepared and submitted for posting on a daily basis to ensure timely accounting entries and avoid material overstatements of Cash Key revenue.

Finding II – Weaknesses in the Refund Process We noted Public Works does not have established policies and procedures which outline documentation, reconciliation, and authorization requirements for preparing refund vouchers on behalf of the various Agencies and vendors. Additionally, of the 51 refunds tested during the audit period, 10 refunds (20%) were issued for incorrect amounts, resulting in a combination of over and underpayments to customers. We also noted one refund on a daily sales report which did not have a completed customer request form. Subsequently, this refund was not issued to the customer. Public Works did not require City agencies and external parties to provide sufficient documentation to support the dollar amounts of customer refunds requested during the sample period. Our audit work revealed several instances where customer request forms were incomplete, transaction detail or receipts did not equal refund amounts or were not provided with the request form, and the refund amounts requested did not match daily sales report amounts. Additionally, it appears Public Works personnel did not review refund requests, ensure proper documentation was provided, or follow up with the agencies or vendors for additional information as necessary. It is Public Works responsibility to properly research, compile, and submit proper documentation for refund amounts in accordance with Fiscal Rules 2.5, 7.6, and DRMC Section 20-39 which require sufficient supporting documentation for all voucher requests, written policies and procedures for refunds, and thorough examination of each refund.

8

PUBLIC WORKS FINDINGS AND RECOMMENDATIONS CASH KEY PARKING PROGRAM

Recommendation In order to mitigate the risk of undetected errors and improper refund amounts, we recommend Public Works prepare written policies and procedures to guide agency personnel in properly researching, documenting, and processing requested refunds. Public Works should ensure all City agencies and vendors provide a completed customer request form which clearly delineates the amount of the refund and that supporting documentation equals the amount of the refund. Additionally, any issues or adjustments made to refund amounts and explanations for missing or incomplete documentation should be provided. Follow up procedures should be initiated with all entities if proper documentation is not provided. Backup documentation should also be organized, complete, and reconciled to daily sales reports and City financial records.

Finding III – Contract Administration Public Works does not have a written contract with the Tattered Cover which governs financial reporting requirements, payment due dates, or interest penalties for late payments. Additionally, we noted an expenditure contract between Public Works and the Downtown Denver Partnership which merely references DDP’s scope of work which includes, among other duties, promoting and selling Cash Keys. This contract does not outline financial reporting requirements, payment due dates, or interest penalties related to the Cash Key program. Public Works placed the City as well as the vendors at risk of financial loss. Without specific contract provisions, vendors are not mandated to remit funds collected on behalf of the City in a timely manner. Additionally, neither entity has available recourse in the event of employee theft, damage to City property, or nonpayment of City funds without specific insurance provisions designed to protect the City from loss. Executive Order No. 8, Contracts and Other Written Instruments, establishes City procedures related to contracts and mandates that Agencies initiate contracts in circumstances where the City is obligated, financially or otherwise. The order further requires that Public Works monitor all contracts and ensure compliance throughout the life of the contract.

Recommendation We recommend Public Works, in conjunction with the City Attorney’s Office, immediately initiate contracts with the Tattered Cover and DDP which outline specific responsibilities in the administration of the Cash Key program. The contracts should include financial reporting requirements and payment due dates, late payment penalties, specific insurance requirements including performance or fidelity bonds, and other provisions as required by Executive Order No. 8.

9

PUBLIC WORKS EXHIBIT A CASH KEY PARKING PROGRAM

10

PUBLIC WORKS EXHIBIT A CASH KEY PARKING PROGRAM

11

![[CEMETERY NAME] - Ohio Auditor of State Web viewThe Cemetery recognizes receipts when received in cash rather than when earned, ... (Delete the word “unencumbered”,](https://img.pdfslide.net/doc/110x75/5a98acb37f8b9aba4a8d2af4/cemetery-name-ohio-auditor-of-state-viewthe-cemetery-recognizes-receipts-when.jpg)