Embed Size (px)

Citation preview

OIC LogoTriangle Signifies the strength and represents 3 roles of the office which are supervision, promotion and development and the protection of the rights and benefits.

Two triangles that from a squareSignifies 4 main stakeholders that has important role to the develop-ment of Thai insurance business, the enterpriser of insurance business, the insured, people, and the Insurance Intermediaries and a symmetrical square signifies the impartiality, the credibility and the justice.

The gold picture in the middle is a tall gold lighthouse that lights the way. It shows the roles and duties of the office of insurance commission in being careful, supervising, supporting, promoting and recommending the way in solving insurance-related problems.

Gold & BlueSignifies the fact that the office is the organization that drives the insurance business.

WE For Insurance Excellence

OICOffice of Insurance Commission

SECTOR 1Organization

SECTOR 2Organization Structure

SECTOR 3Overview of Insurance

Business in 2014

12 20

24

SECTOR 5Direction and Trend

of Insurance

Business in 2015

SECTOR 4Operations and

Significant Development In 2014

CONTENTS

SECTOR 6Appendix

30 60

64

6 Office of Insurance Commission (OIC)

Mr. Rangsan Sriworasart

Permanent SecretaryMinistry of Finance Chairman

Ms. Chutima Boonyaprapas

Permanent Secretary Ministry of Commerce Commission Member (Since June 2014)

7

Executive Board

Mr. Prasarn Trairatvorakul

Governor, Bank of Thailand Commission Member

Mr. Vorapol Socatiyanurak

Secretary-General Securities and Exchange Commission Commission Member

Annual Report 2014

8 Office of Insurance Commission (OIC)

Mr. Amphol Wongsiri

Secretary-General Consumers Protection Commission Member

Mr. Payungsak Chartsuthipol

Commission Member in Business Administration

9

Ms. Tarisa Watanagase

Commission Member in Economics

Mr. Kowit Poshayananda

Commission Member in Finance

Executive Board

Annual Report 2014

10 Office of Insurance Commission (OIC)

Prof. Emeritus Chukiat Pramoolpol

Commission Member in Insurance

Mr. Karun Kittisathaporn

Commission Member in Insurance

11

Mr. Wattana Ratanavijit

Commission Member in Law

Mr. Pravej Ongartsittigul

Secretary-General

Executive Board

Annual Report 2014

SECTOR

1

Organization

VISION To be a continuously developing

organization that ensures the insurance

system will serve as a mechanism in

providing stability to the people and in

preparing for challenges in the future.

MISSION 1.To build confidence in and

accessibilities to the insurance system

2. To strengthen the capacity of

the insurance system

3. To develop laws and policyholders

protection system

4. To promote the infrastructure

of the insurance system

Sector 1 Organization

ROLES AND FUNCTIONS OF THE OIC

1.TheOfficeofInsurance

Commission(OIC)

The Insurance Commission Act

has been effective since September

1, 2007. As a result, the Department

of Insurance, initially a government

agency, has changed its status to

become the Office of Insurance

Commission (OIC), now an independent

state agency and a public company

similar to the Bank of Thailand and the

OfficeoftheSecuritiesandExchange

Commission. The OIC is responsible

for regulating and developing the

insurance business as well as protecting

theinsurancebenefitsandrightsof

the people.

16 Office of Insurance Commission (OIC)

Under this Act, the structure for the supervision of the insurance business comprises as follows:

1.1 TheInsuranceCommissionisresponsiblefortheformulationofrelevantpoliciesaswellasforthesupervision,promotionanddevelopmentoftheinsurancebusiness.TheCommissioniscomposedof:

Mr. Sriworasart obtained his master degree in business administration from Prince of Songkla University andfinishedNationalDefenceCollegeCourseClass2549,with extensive knowledge and experience infinancialandfiscalmanagement.Priortohisappoint-ment as Permanent Secretary, he used to head various important departments under the Ministry of Finance such as Deputy Permanent Secretary, Head of Income Group, Director General of the Central Accounting Department and Inspector General of the Ministry ofFinance.Hecurrentlyholdshisexecutivepositionin various organizations, including Chairman of Thai Military Bank, Chairman of the Board of Directors of the NationalCreditBureauCo.,Ltd.andChairmanoftheBoard of Directors of the Government Pension Fund.

Mr. Rangsan SriworasartPermanent Secretary Ministry of Finance, Chairman

Mrs. Boonyaprapas obtained her master degree in economics from Western Michigan University, USA and finishedNational DefenceCollegeCourseClass 2550, withextensiveknowledgeandspecializationineconomics. Prior to her appointment as Permanent Secretary, she has held important positions in the Ministry, including Director General of the Department of International TradeNegotiation,DirectorGeneraloftheDepartmentof International Trade and Director General of the Department of Internal Trade. Apart from her chief position at the Ministry of Commerce, she currently holds her key commerce-related positions such as Advisor to the Subcommittee on Trade Rules and Regulations, Industrial Council of Thailand and Advisor to the Board of the Council ofMarineMerchandiseExporters’AssociationofThailand.

Ms. Chutima BoonyaprapasPermanent Secretary Ministry of CommerceCommission Member (Since June 2014)

Mr. Trairatvorakul holds a doctorate degree in Business Administration from Harvard University, USA. Hepossessessubstantialbackgroundandexperienceworkingasanexecutiveinvariouspublicandprivateagenciesrelatingtofinancialandcapitalmarkets.Before assuming the position of Governor of the Bank of Thailand,hehasheldseveralexecutivepositions ina number of organizations such as Secretary-General oftheSecuritiesandExchangeCommissionandtheStockExchangeofThailand,andManagingDirectorofKasikornBankPCL.ApartfromworkingattheBankofThailand, he plays a contributive role in the communal and educational sectors, serving as Board member of theThaiRedCrossSocietyandSeniorExpertmemberof the Chulalongkorn University Council.

Mr. Prasarn Trairatvorakul Governor, Bank of Thailand, Commission Member

17

Mr. Socatiyanurak holds a doctorate degree in finance from theWharton School,University ofPennsylvania,USA.Anexpertintheareasofeconomics andfinance,hehasheldmanykeyexecutivepositions suchasViceChairpersonoftheNationalEconomic and Social Advisory Council and Chairperson of the Committee for Providing Comments and RecommendationsonNationalEconomicandSocial Development Plan to be submitted to the cabinet. He currently holds several senior positions, i.e. memberoftheNationalIndustrialDevelopmentBoard,the Thai Trade Competition Commission (TCC), and the Research and Development Commission of the Thai Senate.

Mr. Vorapol SocatiyanurakSecretary-General Securities and Exchange Commission, Commission Member

Mr. Wongsiri obtained his master degree in Development Administration (Public Administration) inthefieldofPublicPolicyandProjectManagementfrom theNationalInstituteofDevelopmentAdministration(NIDA).Asanexpertonlegalaffairs,hehascontinuallycontributed to social development and public charity activities, especially the creation of the network for the protection of consumers in the public, private and civic sectors. He used to hold several important positions in the Ministry of Justice, including Secretary-General of the Anti-Corruption in the Public Sector Commission (ACPSC) and Inspector General of the MOJ. Apart from his present position as Secretary-General of the Consumers Protection Commission, he also holds positionsofchairmanandseniorexpertmemberofcommittees and subcommittees of both public and private organizations such as the Committee for the Consideration of Market Dumping and Subsidizing (CCMDS), International Trade Department, the Committee oftheInstituteofISOCertificationandtheCommitteefortheNationalCreditDataProtection,theBankofThailand.

Mr. Amphol Wongsiri Secretary-General Consumers Protection Commission Member

Mr. Chartsuthipol obtained his bachelors degree inElectricalEngineeringfromChulalongkornUniversity and completed his executive program for Senior Administration of Justice (2nd class) and the Pillar of the Kingdom Program : The Royal Initiative for Advanced Leadership (Class 2012). He has vast knowledge andexperienceinbusinessadministration,presentlyholdingexecutivepositions inthepublicandprivatesectors,namely board member of Bangkok Bank, chairman of the Corporate Governance and Social Responsibility Committee of Krungthai Bank and chairman and senior boardmemberoftheNationalCatastropheInsurancePromotion Fund Commission.

Mr. Payungsak Chartsuthipol Commission Member in Business Administration

Annual Report 2014

18 Office of Insurance Commission (OIC)

Ms. Watanagase holds an honorary doctorate degree in Economics from Keio University, Japan,andhascompletedtheNationalDefenseCourseforpublic, private and political sectors (Class 3) from the NationalDefenseCollege.Sheisanexpertineconomicsand finance, havingworked inmany key positions in the Bank of Thailand such as the Governor of the Bank of Thailand, the Deputy Governor for Financial Institutions Stability, the Assistant Governor (Financial Markets Operations Group), the Assistant Governor (Financial Institutions Policy Group), and the Assistant Governor (Financial Institutions Supervision Group).

Prof. Pramoolpol holds a master degree in Insurance from the Wharton School, University of Pennsylvania, USA, which he had achieved through the scholarship awarded by the Thai Government (theOfficeofCivilServiceCommission).He isveryknowledgeablewithmorethan40years'experiencein insurance, having worked in a great number of key positions in various agencies including Director of the insuranceOffice, theMinistryofCommerce,BoardChairmanofThaiCharoenLifeInsurancePCL;and Director of Thailand Insurance Institutes. He also contributed to the educational sector serving as a special instructor for a number of public and private universities, and as the Dean for the Faculty of Risk Management and Servicing Industry (Insurance), Assumption University. Currently he serves as a senior expertmemberoftheCommitteeforRoadAccidentVictims Protection.

Mr. Poshyananda holds a doctorate degree in EconomicsfromCornellUniversity,USA.andgraduated from the National Defense College (Class 30). Hewas also awarded an honorary doctorate degree in Economics fromChulalongkornUniversity.He isanexpert in economics andfinance, currently servingas chairman of the Directors, Sansiri PCL, and anexpertmemberofvariouscommitteesinpublicandprivate sectors such as chairperson of the Board, Thai Institute of Directors (IOD), the Director, Cambridge Thai Foundation (CTF) under the patronage of Her MajestytheQueen;themember,WalailakUniversityCouncil;andthemember,theOfficeoftheCouncilof State of Thailand.

Ms. Tarisa Watanagase Commission Member in Economics

Mr. Kowit PoshayanandaCommission Member in Finance

Prof. Emeritus Chukiat Pramoolpol Commission Member in Insurance

19

Mr.RatanavijitholdsamasterdegreeinPublic Administration from Indiana University, USA and graduatedfromtheNationalDefenseCollege(Class21). He is an expert in law and currently holds a number of key positions in the legal and political bodies such asCouncilMember, theOfficeof theCouncil of State of Thailand, Member in Monitoring andEvaluationCommittee,theOfficeofthePublicSector Development Commission (OPDC), Member of the By-laws Consideration Committee, the Secretariat to the Cabinet, and Member of the Administrative ProcedureCommittee,theOfficeoftheCouncilofState. of Thailand

Mr. Ongartsittigul holds a master degree in Business Administration (Finance) from New Hamp-shire College, USA. He is an expert in the area of finance and insurance, with vast experience in managing a number of agencies in public and private sectors. For example, he was the Vice President of J.P. Morgan Securities (Thailand) Ltd., Senior Vice President, Bank of America NA., Bangkok Branch, and Senior Assistant Secretary General, Securities and Exchange Commission. He has also taken part in some activities that contribute to the benefit of the public. For example, he serves as member of the Investment Advisory Committee for the Thai Red Cross Society and member of Code of Ethics Committee for the Federation of Accounting Professions.

Mr. Kittisathaporn holds a master degree in EconomicsfromSyracuseUniversity,USAandcompleted the National Defense course for participants frompublic, private and political sectors (Class 8) from the NationalDefenseCollege.Heisknowledgeableandhasalotofexperienceintheareaofeconomicsandinsurance. He used to hold a number of key positions in the Ministry of Commerce such as the Permanent Secretary of the Ministry of Commerce, Deputy Permanent Secretary of the Ministry of Commerce, Director General of the Insurance Department, Director General oftheDepartmentofBusinessEconomics,andDirectorGeneral of the Department of Foreign Trade. Currently he serves as Director in various companies in the privatesectorsuchastheBankofAyudhyaPCL,andCentralPattanaPCL.

Mr. Karun Kittisathaporn Commission Member in Insurance

Mr. Wattana Ratanavijit Commission Member in Law

Mr. Pravej Ongartsittigul Secretary-General

Annual Report 2014

SECTOR

2

Organizational Structure

22 Office of Insurance Commission (OIC)

Secretary-General

Strategic Planning & Enabler

Assistant Secretary-General

(Organization Strategic)

Assistant Secretary-General

(OIC Advanced insurance Institute)

Assistant Secretary-General

(General Administration)

Insurance Promotionand Development

Assistant Secretary-General

(Insurance Promotion)

Assistant Secretary-General

(Development)

Assistant Secretary -General

(Regional Insurance)

Deputy Secretary-General (Promotion and Development)

Organizational Structure of OIC

Insurance Commission

23

Audit Committee

Primacy Activities

Legal, Litigation and Policyholder ProtectionInsurance Stability

Deputy Secretary-General (Examination)

Deputy Secretary-General (Supervision)

Deputy Secretary-General (Legal, Litigation and

Policyholder Protection)

Assistant Secretary-General

(Legal)

Assistant Secretary-General

(Policyholder Protection)

Assistant Secretary-General

(Litigation)

Assistant Secretary-General

(Insurance Products

Supervision)

Assistant Secretary-General

(Investment (Insurance

Supervision)

Assistant Secretary General

(Supervisory Standard

Development)

Assistant Secretary-General

(On-site Examination)

Assistant Secretary-General

(Financial Analysis and Examination

Development)

Annual Report 2014

SECTOR

3

Overview of Insurance Business in 2014

26 Office of Insurance Commission (OIC)

1. The Thai 12 Months Insurance Business in 2014

1.1 The Growth of Insurance Business

The Thai economy in the fourth quarter of

2014 grew 2-3%, an increase from 0.6% in the previous

quarter, leading to an annual growth rate of 0.7% as

a result of the growth of 2.7% of the non-agricultural

sector whereas the agricultural sector shrank 1.6%.

Both domestic and foreign demands also grew. The

total spending on investment grew from 2.9% in the

previousquarterto3.2%.Thenetexportsofgoods

and services grew 21.9% as a result of the increase in

the foreign demand and the decrease in the volume

ofimports.Meanwhile,thegovernment’sspending

during the same quarter grew 5.5%, resulting from

net spending on goods and services which grew 8.7%,

whereastheprivatesector’sspendingonconsumption

grew 1.9%, a decrease from 2.2% in the previous

quarter(Source:NESDB).

Despite the overall slow-down of the Thai

economy, the insurance business could still grow,

earning totally 704,000 million baht for its 12 months

(Jan.-Dec.) direct premiums for 2014, a growth of

9.23%. Of this, 498,752 million baht came from life

insurance direct premiums, and 205,247 million baht

came from non-life insurance direct premiums, a

growth of 13.00% and 1.05% from the previous year,

respectively.

LifeNon-Life

Total

100,000 -

300,000

500,000

700,000

200,000

400,000

600,000

800,000

2010

296,213

122,756418,969

2011

328,897

138,755467,652

390,517

179,530570,047

2013

441,372

203,121644,492

2014

498,752

205,247704,000

%Million baht

14.57 11.03 18.74 13.02 13.00

13.86 13.03 29.39 13.14 1.05

14.36 11.62 21.90 13.06 9.23

35.00

25.00

30.00

20.00

10.0015.00

5.00

-2010 2011 2012 2013 2014

Growthrateofinsurancebusiness(%YOY)

Jan.-Dec.2010-2014

PremiumJan.-Dec.2010-2014

LifeNon-Life

Total

2012

27

1.2 Growth of insurance Penetration

Premium(millionbaht)

2013 2014

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Nov. Dec. Jan.-

Dec.

GDP(QoQ%) 5.40 2.90 2.70 0.60 -0.50 -0.40 0.60 2.30 - - 0.70

Total

YoY%

Ins. Penetration

159,392

20.77

5.31

153,891

14.05

5.21

157,500

13.08

5.39

173,579

5.94

5.75

185,362

16.29

6.09

170,243

10.63

5.62

164,657

4.54

5.54

183,738

5.84

5.94

58,566

8.20

68,249

6.81

704,000

9.23

Life

YoY%

Ins. Penetration

108,273

20.73

3.61

104,564

12.93

3.54

108,577

14.40

3.72

119,935

5.82

3.97

133,698

23.48

4.39

120,173

14.93

3.97

117,128

7.88

3.94

127,753

6.50

4.13

43,511

10.62

48,383

6.83

498,752

13.00

Non-life

YoY%

Ins. Penetration

51,118

20.85

1.70

49,328

16.48

1.67

48,923

10.26

1.67

53,652

6.22

1.78

51,664

1.07

1.70

50,070

1.50

1.65

47,528

-2.85

1.60

55,985

4.15

1.81

15,055

1.77

19,865

6.13

205,247

1.05

A total of 61,182,771 insurance policies

were sold in 2014, an increase of 6.40% from the

previous year, of which 6,567,283 were life-insurance

policies and 54,615,488 were non-life insurance

policies, an increase of 20.77% and 4.90%, respec-

tively.

1.00-

2.003.004.00

5.006.007.00

%

2007

2.37 2.44 2.86 2.93 3.12 3.44 3.71 4.11

1.07 1.12 1.19 1.21 1.32 1.58 1.71 1.69

3.44 3.56 4.05 4.15 4.44 5.02 5.42 5.80

2008 2009 2010 2011 2012 2013 2014

Insurance Penetration end of year 2007-2014

Life

Non-Life

Total

Annual Report 2014

28 Office of Insurance Commission (OIC)

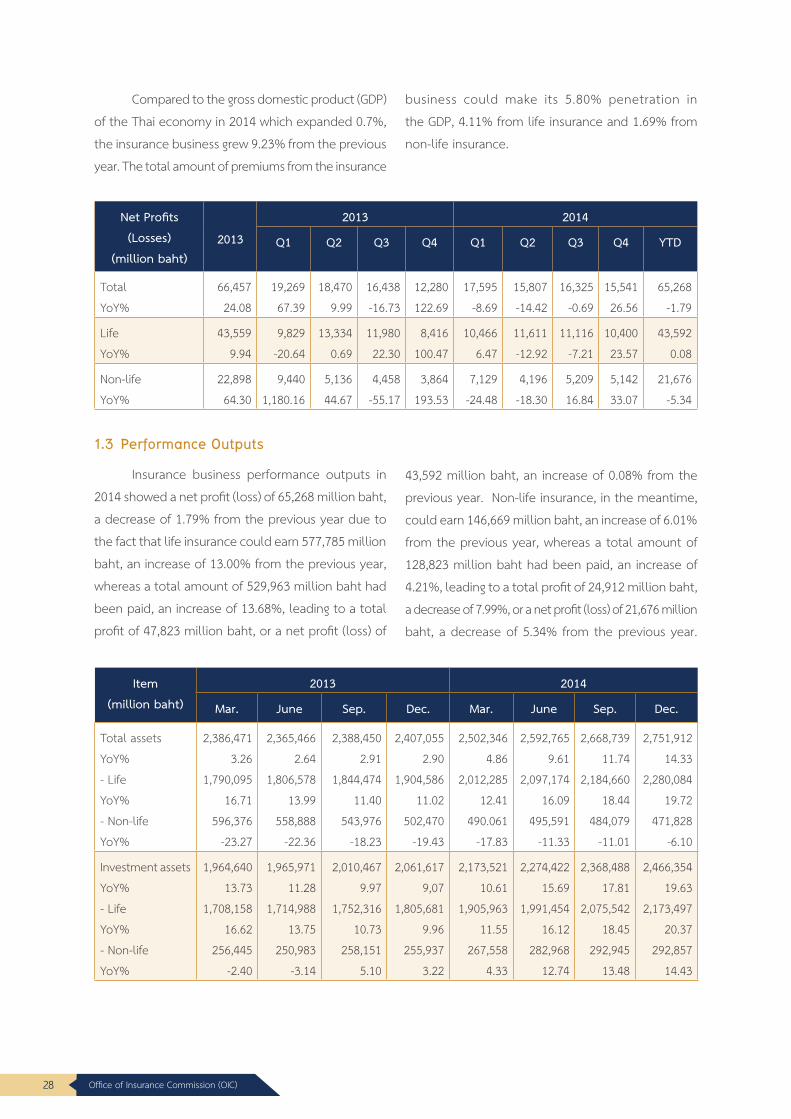

1.3 Performance Outputs

Insurance business performance outputs in

2014showedanetprofit(loss)of65,268millionbaht,

a decrease of 1.79% from the previous year due to

the fact that life insurance could earn 577,785 million

baht, an increase of 13.00% from the previous year,

whereas a total amount of 529,963 million baht had

been paid, an increase of 13.68%, leading to a total

profitof47,823millionbaht,oranetprofit(loss)of

Compared to the gross domestic product (GDP)

oftheThaieconomyin2014whichexpanded0.7%,

the insurance business grew 9.23% from the previous

year. The total amount of premiums from the insurance

business could make its 5.80% penetration in

the GDP, 4.11% from life insurance and 1.69% from

non-life insurance.

Item

(millionbaht)

2013 2014

Mar. June Sep. Dec. Mar. June Sep. Dec.

Total assets

YoY%

-Life

YoY%

-Non-life

YoY%

2,386,471

3.26

1,790,095

16.71

596,376

-23.27

2,365,466

2.64

1,806,578

13.99

558,888

-22.36

2,388,450

2.91

1,844,474

11.40

543,976

-18.23

2,407,055

2.90

1,904,586

11.02

502,470

-19.43

2,502,346

4.86

2,012,285

12.41

490.061

-17.83

2,592,765

9.61

2,097,174

16.09

495,591

-11.33

2,668,739

11.74

2,184,660

18.44

484,079

-11.01

2,751,912

14.33

2,280,084

19.72

471,828

-6.10

Investment assets

YoY%

-Life

YoY%

-Non-life

YoY%

1,964,640

13.73

1,708,158

16.62

256,445

-2.40

1,965,971

11.28

1,714,988

13.75

250,983

-3.14

2,010,467

9.97

1,752,316

10.73

258,151

5.10

2,061,617

9,07

1,805,681

9.96

255,937

3.22

2,173,521

10.61

1,905,963

11.55

267,558

4.33

2,274,422

15.69

1,991,454

16.12

282,968

12.74

2,368,488

17.81

2,075,542

18.45

292,945

13.48

2,466,354

19.63

2,173,497

20.37

292,857

14.43

NetProfits

(Losses)

(millionbaht)2013

2013 2014

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 YTD

Total

YoY%

66,457

24.08

19,269

67.39

18,470

9.99

16,438

-16.73

12,280

122.69

17,595

-8.69

15,807

-14.42

16,325

-0.69

15,541

26.56

65,268

-1.79

Life

YoY%

43,559

9.94

9,829

-20.64

13,334

0.69

11,980

22.30

8,416

100.47

10,466

6.47

11,611

-12.92

11,116

-7.21

10,400

23.57

43,592

0.08

Non-life

YoY%

22,898

64.30

9,440

1,180.16

5,136

44.67

4,458

-55.17

3,864

193.53

7,129

-24.48

4,196

-18.30

5,209

16.84

5,142

33.07

21,676

-5.34

43,592 million baht, an increase of 0.08% from the

previousyear.Non-lifeinsurance,inthemeantime,

could earn 146,669 million baht, an increase of 6.01%

from the previous year, whereas a total amount of

128,823 million baht had been paid, an increase of

4.21%,leadingtoatotalprofitof24,912millionbaht,

adecreaseof7.99%,oranetprofit(loss)of21,676million

baht, a decrease of 5.34% from the previous year.

29

1.4 Total Assets and Investment Assets

Up to December 31, 2014, the insurance

business had its total assets worth 2,751,912 million

baht, a growth of 14.33% from the previous year. Of

this, 2,280,084 million baht belonged to life insurance

business, a 19.72% increase from the previous year,

whereas 471,828 million baht belonged to non-life

insurance business, a 6.10% decrease from the previous

year.

Investment assets of the insurance business

up to December 31, 2014 total 2,466,354 million

baht, a 19.63% increase from the previous year, or

89.62% of the total assets. Of this, 2,173,497 million

baht belonged to life-insurance business, a 20.37%

increase from the previous year, or 95.33% of the

total assets of life-insurance business, and 292,857

million baht belonged to non-life insurance business,

a 14.43% increase from the previous year, or 62.07%

of the total assets of non-life insurance business.

Investment assets of life insurance business and non-life insurance business differ in terms of the specificnatureofinsuranceasfollows:

❖ Investment assets of life-insurance

business were used for :

-Lowriskinvestment:Atotalamountof

1,245,797 million baht was used to buy bonds

accounting for 57.32% of the total investment

assets, an increase of 17.59% from the previous year.

- High risk investment : A total amount of

159,811 million baht was used to buy capital shares,

accounting for 7.35% of the total investment assets,

an increase of 22.59% from the previous year.

❖ Investment assets of non-life insurance

business were used for :

-Lowriskinvestment:Atotalamountof

111,008 million baht was deposited in the bank,

accounting for 37.91% of the total investment assets,

an increase of 12.83% from the previous year.

- High risk investment : A total amount of

75,105 million baht was used to buy capital shares,

accounting for 25.06% of the total investment assets,

an increase of 29.73% from the previous year.

Annual Report 2014

30 Office of Insurance Commission (OIC)

Sector

4

31

Operations and Significant Development in 2014

Annual Report 2014

32 Office of Insurance Commission (OIC)

Operations and Significant Development in 2014

The Office of Insurance Commission (OIC) conducted its operations under the framework of the Second Insurance Development Plan (2010-2014) which is the principal guideline for supervising and promoting the overall insurance system development to achieve high efficiency, transparency, credibility and to protect the people’s insurance benefits and

rights as follows :

33

OIC and Tourism Authority of Thailand (TAT) sign an MOU on cooperation in tourism insurance

Measure 1 : To build confidence and gain access to the insurance system in every sector

First and foremost priority in developing the Thai insurance system is

to gain wide acceptance by the general public and the society as a whole

that the insurance system is an important mechanism in building stability

of life and property earned out of business and investment against risks of

unexpectedincidents,assurednessofearninganincomefortheinsured

personsandtheirfamiliesaswellasinstrengtheningthecountry’ssocial

and economic system through the following measures :

1.InsuranceLiteracy

1.1 The OIC took initiatives to promote and develop insurance

by signing MOU with public and private organizations to integrate

their cooperation in providing the general public with knowledge and

understandingabout insuranceanditsbenefits.TheTourismAuthority

ofThailand (TAT), forexample, signedanMOUwithOIConpromoting

tourism insurance, whereas the Department of Rights and Liberty

Protection, the Thai Life Insurance Association and the Thai Non-Life

Insurance Association signed an MOU on promoting knowledge about

theinsured’srightsandbenefitsaccordingtotheActonRemuneration

fortheDamagedandCompensationandExpensesforDefendantsinCriminal

CasesB.E.2554

Themainobjectivewastoencouragethepeopletogaintheirbest

benefitsandalsostrengthenthecountry’ssocialandeconomicsystem.

Major issues focusedonsuchmattersas life insuranceandnon-life in-

surance,maintainingbenefitsfrominsurance,compulsorymotorvehicle

insuranceaccordingtoprotectionforMotorVehicleVictimsActB.E.2535

(1992) (amended inB.E.2551)andmicro-insurance. Activities included

the following :

Annual Report 2014

34 Office of Insurance Commission (OIC)

1.3 Setting up insurance youth programs in

schools to implant knowledge and understanding

of insurance, particularly life insurance and the

compulsory motor insurance. Activities took the

form of games and contests in which schools and

teachers nation wide participated, with prizes given

to schools and teachers who had efficiently incorpo-

rated insurance into their teaching curriculum. Grants

and scholarships were also awarded to students

with outstanding performance in their study and

presentation of information on insurance in various

forms such as songs, shows and talk shows. Details

are as follows :

Year 2012 2013 2014

Number of participating schools

513 554 603

There were two categories of awards, one

for schools and the other for students, consisting of

three levels each i.e. provincial, regional/Bangkok, and

national levels. Those national outstanding award

winners, i.e. 1st, 2nd and 3rd prize winners received the

awards at “Insurance Day” Fair where the awarding

ceremonywasheldonNovember14,2014.

OIC organizes its campaigns on road safety in insurance organizations and road accident reduction during

Songkran Festival 2014 and New Year Festival 2015

1.4 Organizing insurance volunteers program

to train a total of 7.391 insurance volunteers in

communities and regional areas. Activities consisted

of dissemination of information on insurance so that

the local communities are accurately and adequately

informed and can learn how to manage their risk

appropriately.

1.5 Organizing PR Project on “Modern

Generations Care for Motor Insurance”. Activities

consisted of short advertisement (minimum length

30 seconds) contest on compulsory motor insurance

to inform students of the benefits and importance of

compulsory motor insurance.

Short Advert isement Contest Awarding

Ceremony for higher education level under the

theme “Compulsory”

1.2 Organizing insurance promotional activities

at the main and regional offices with the participation

of organizations from both the public and private

sectors, e.g. campaigning on road safety at agencies

in the insurance-industry sector and on prevention

and minimization of road accidents during Songkran

Festival 2014 and New Year Festival 2015.

35

2. Promotion of Good Governance inInsuranceBusiness

The OIC, seeing the importance of corporate

management structure and a sufficient number of

qualified personnel to support each company with

good governance, issued its announcement on

Criteria, Method and Conditions on Money Receiving

and Paying, Auditing and Internal Control for Life/

Non-Life Insurance Companies B.E. 2014, effective

on October 16, 2014, which required such companies

to appoint an auditing committee consisting of at

least three members two of whom, at least, must be

independent members. An Internal Audit Unit, Law

Compliance Supervising Unit as well as a Compliance

Officer who is to act as the coordinator with the OIC

on the company’s behalf must also be appointed.

3.National CatastropheInsuranceFund

(NCIF)

National Catastrophe Insurance Fund has been

modified to embrace four additional natural disasters,

i.e. storms, floods, earthquakes and hailstorms, apart

from the original six types of risks consisting of fires,

lightings, explosions, vehicles, aircraft and water-relat-

ed risks, with the insurance amount of 20,000 baht/

year for a premium of 100 baht. The main purpose

of this modification, to take effect as of January 1,

2015, is to provide the general public with access to

wider protection.

The Fund’s performance results (as of

December 29, 2014) are as follows :

1) Summary of Catastrophe Insurance

Policies sold :

❖ the number of policies still active :

1,371,083 policies

❖ the insured amount for current

protection : 63,667 million baht

❖ the accrued amount of premiums :

1,275 million baht

❖ the reinsurance premium amount

in proportion to the Fund for current protection :

19,245 million baht❖ the accrued amount of reinsurance

premiums in proportion to the Fund : 731

million baht

2) The total number of companies with

non-life insurance policies sold : 51 companies

3) No compensation claims and reinsurance

premiums overdue for payment

Annual Report 2014

36 Office of Insurance Commission (OIC)

DataonCatastrorheInsurancebyArea*

4.DevelopmentofDiverseInternationalInsuranceProducts

4.1 Development of 2014 In-Season Rice Crop

Insurance Policy : This was joint cooperation between

the OIC and the Bank of Agriculture and Agricultural

Cooperatives (BAAC), the Office of Financial Economics

(OFE), the Department of Agricultural Extension (DAE)

and the Thai General Insurance Association (TGIA) to

help minimize farmers’ risk of seven natural disasters,

including flooding/heavy rainfall, drought/long period

of absence of rain, storm/typhoon, cold weather/

frost, hailstorm, and fire. The compensation amount

is 1,111 baht/rai, whereas that for damage by pets/

epidemic diseases is 555 baht/rai. Insurance Is

classified into five categories according to the risk level

of each area, i.e. area with lowest risk (light green),

area with very low risk (green), area with low risk (dark

green), area with moderate risk (yellow) and area with

high risk (red). Premium rates differ according to the

risk level, of course, and the farmers are to pay the

premium 60-100 baht/rai, depending on the risk level

of their area, whereas the government is to subsidize

the excess amount of premium. The total amount of

annual rice insurance premium for the year 2014 was

360,348,544 baht from 100,715 policies.

4.2 Development of Domestic Travel Accident

Insurance Policy (for Foreign Tourists) : This product

was launched to promote tourism insurance under

the “Project on Insurance for Foreign Tourists”, a kind

of voluntary insurance, the main objective of which

is to provide tourists with confidence in their safety

while travelling in Thailand. This will not only lead to

a good image but also promote tourism of the country.

4.3 Modification of Medical Expense Coverage

for In-Patients who did not need to be admitted

(Day Case). Due to medical advancement, patients

with some diseases do not have to be admitted to

hospital, and insures who bought daily compensation

benefit will be paid one-day compensation like an

in-patient for their operation under 1 of 18 specified

items. This new regulation has become effective

according to the registrar’s Announcement on Daily

Compensation for Day-Case Patients, which insurance

companies must keep their customers informed of

this additional benefit.

Area

No.oflocationsofinsuranceproperties

Premium(millionbaht)

Insuredamount(millionbaht)

Houses SMEs Industries Total

Provinces in risk areas according to estimation**

570,555 159 25,500 909 1,727 28,136

Other 72 provinces 800,528 185 34,128 1,016 387 35,531

Total 1,371,083 344 59,628 1,925 2,114 63,667

* Referring to policies currently under protection

** ReferencebasedonestimationofCatastropheInsuranceundertheNationalCatastropheInsuranceFundinfive

provinces,i.e.Ayudhya,Pathumthani,Nonthaburi,NakhonPathomandBangkok

Sources:1)http://www.ndwc.go.th2)http://www.thaiflood.com3)http://flood.gistda.or.th4)http://www.nirapai.com

37

For all that, the OIC, being fully aware of

suitability and compliance with medical treatment by

operation/medical procedure in terms of the number

of days needed for each day-case patient, issued its

Announcement on Appointment of Working Group for

Considering Payment of Daily Compensation to Day-Case

Patientstobebestsuitedtothose18itemsspecified

under "treatment by operation/medical procedure"

category.

4.4 Provision of Mortgage Reducing Term

Assurance (MRTA) Policy. The kind of policy is offered

as an additional choice for customers who can buy

the policy through various channels other than

commercial banks. The main purpose is to promote

the business regulation via the market mechanism

and the people can buy their policy directly from

insurance companies instead of from the bank they

areapplying for the loan,whichwillbenefit them

as follows :

1. The premium will be cheaper because

there is no commission.

2. It will be easier for insures to make a

refinance because there is no need to terminate

the current policy to buy a new one.

3. The policy can be terminated within

30 days (free-look period) in case a loan contract

has not been signed.

4.5 Standardization of Coverage under

Temporary Receipts Presently insurance companies

provide coverage during their screening process

basedondifferenttermsandconditionsasspecified

in the temporary receipt. The OIC, in cooperation

withthelifeinsurancesectorandtheLifeInsurance

Association of Thailand, drafted standard coverage

conditions for the temporary receipt to be used by

all insurance companies. This will also set the same

guideline for practice for life insurance business to

follow in terms of determination of coverage date

under different situations, the period of appeal right,

suicide and pending period.

Annual Report 2014

38 Office of Insurance Commission (OIC)

5.MicroInsurancePromotion

The OIC promotes and supports micro

insurance’s sustainable growth. With the cooperation

of the private sector, the OIC developed a micro

insurance product so-called “Insurance Policy 200”

and held a training course and promotion event under

the theme “Micro Insurance Campaign for the People

2014”. The details are as follows :

Insurance Policy 200 for Individuals (Micro

Insurance) was inaugurated at “Micro Insurance

seminar was held by the Non-Life Insurance Association

of Thailand on September 19, 2014 at the Tawanna

Hotel, Bangkok.

2.2 Lecture on “The Role and Function

of the Office of Insurance Commission and Micro Insur-

ance” as part of the training course for the provincial

consumers protection subcommittees, municipalities

and Tambon Administration Organizations (TAOs)

organized by the Office of Consumers Protection

Commission in cooperation with the National Institute

Campaign for the People” where four provincial

insurance exhibitions were organized as follows :

1. 16th Anniversary of Country-Wide

Debt Clearing Exposition, April 26, 2014 at Chonburi

City Hall Yard

2. Happiness Building Man Exposition,

August 2, 2014 at Suratthani Provincial Sports Complex

3. Happiness Building Man Exposition,

August 17, 2014 at Nong Prachak Park, Udornthani

4. Happiness Building Man Exposition,

September 13, 2014 at Phra Pathom Chedi compound,

Nakhon Pathom

2) Training/Lecturing/Seminar on Micro

Insurance or “Insurance Policy 200”

2.1 Lecture on Micro Insurance Direction

and Insurance Business in the seminar on “Guideline

for Good Practice of Micro Insurance” by Assistant

Secretary-General, Promotion Department. The

of Development Administration (NIDA) on June 18,

2014 and July 23, 2014 at the Palasso Hotel. The

lecture was attended by lord mayors, TAO chairmens,

department heads, municipality secretaries and

deputy secretaries, TAO secretaries and deputy

secretaries, public health officers.

2.3 Lectureon“RiskManagementwith

Insurance” The lecture described the reason and

need to buy insurance, types of insurance, micro

insurance and insurance for risk management, savings

and investment under the Project on Financial

KnowledgeintheWorkPlaceorganizedbytheOffice

ofSecuritiesandStockExchangeCommissiononJune

27,2014attheNovotelHotel,Bangkok.Thelecture

wasattendedbyHRstaffoftheOfficeofSecurities

andStockExchangeCommission.

Inauguration of “Insurance 200”, or micro insurance at Insurance Zone in “Micro Insurance for the

Public” Fair in the provinces

39

3) Campaigning on Micro Insurance

(Insurance Policy 200) Knowledge Promotion

3.1Anexhibitiontodisseminateinsurance

knowledge and publicize Insurance Policy 200

(Micro Insurance) was held at 7 Innovation Awards

2014 Fair on March 5, 2014 at Panyapiwat Auditorium,

Panyapiwat Institute of Management (PIM). The fair

wasorganizedby(PallPublicCompanyLimitedand

was attended by 600 people from companies with

productson7-Eleven’sshelves,includingthoseaward

winners. The OIC itself sent “Insurance Policy 200”

(or “Insurance 200” for short), in the contest and

won an award for creating an outstanding concrete

producttrulybenefittingsociety

3.2An exhib i t ion to d isseminat

insurance knowledge and publicize Insurance 200

(Micro Insurance) was held at “Happiness Returning

Concert”ontourwhichwasinitiatedbytheNational

Peace Keeping Council (NPKC) and organized by

WeitheeThaiCo.,Ltd.forthreetimesasfollows:

Exhibition to disseminate insurance knowledge and run campaigns on Insurance 200 at “Happiness

Returning to the People” Concert on tour organized by the National Peace Keeping Party

“2014 7 Innovation Awards” Ceremony held on March 5, 2014 at Panyapiwat Institute of Management

Annual Report 2014

40 Office of Insurance Commission (OIC)

1st exhibition on Saturday, July 12,

2014 at Ayudhya Government Complex

2nd exhibition on Saturday, September

6, 2014 at Nakhon Phanom Government Complex

3rd exhibition on Saturday, September

27, 2014 at Central Festival Department Store,

Had Yai, Songkhla

4) Developing New Selling Channels for

Insurance 200. Consultation had been made to

consider additional selling channels for Insurance 200

other than the gift voucher so as to facilitate easier

access by all people.

6) Cooperating with the Bank of Agriculture

and Agricultural Cooperatives (BAAC) and the Depart-

ment of Agricultural Extension in running the project

on “Micro Insurance” by giving knowledge about

Insurance 200 to farmers along with annual rice crop

insurance. Insurance 200 brochures had also been

distributed along with the BAAC’s crop insurance

brochures.

By December 2014 total of 811,054 micro

insurance policies had been sold, consisting of 83,342

for life insurance 609,150 for non-life insurance,

and a total of 118,562 policies sold by 23 insurance

5) Cooperating with various selling channels,

e.g. broker companies which joined the project in

providing the public with wider access to selling

channels, whereas 7-Eleven helped promote Insurance

200 on its bags.

companies which joined the micro insurance project.

This last quarter sale grew 27.38% from the previous

quarter, earning a total premium of 23.7 million baht,

whereas 6.1 million baht had been paid for compen-

sation claims.

41

TypeExamination

(Cases)

License Issuance (Cases)

License Renewal (Cases)

Registration

Universal Life

Unit rink

Life insurance agents 232,195 119,270 87,131 1,508 1,715

Non-life insurance agents 5,000 3,886 5,901 - -

Life insurance brokers 32,450 22,715 30,078 9 749

Non-life insurance brokers 49,832 30,288 31,355 - -

Total 319,477 176,159 154,465 1,517 2,464

6.2 Making OIC Announcement on Criteria

for Insurance Policy Issuance and Selling and Duty

Performance of Life/Non-Life Insurance Agents/

Brokers (No.3) B.E. 2557 Dated March 17, 2014.

The announcement was made in conformity with the

BankofThailand’spolicyonregulationofbrokerage

in selling securities and insurance products through

commercial banks.

The OIC places emphasis on development

of the quality of selling channels so that the general

public can get quality services from insurance

personnel by applying the following measures :

6.1 Regulating and supervising 479,632

individual insurance agents/brokers registered in the

OIC’s database, comprising 275,548 life insurance

agents, 21,357 non-life insurance agents, 85,053

life insurance brokers and 97,674 non-life insurance

brokers.In2014,examinationsforlicenses,license

issuance and renewal, and registration as universal

life insurance agents and unit-link insurance agents

are as follows :

6.DevelopmentofinsuranceChannelsofDistribution

6.3 Protection of the public’s insurance

benefitsandrightsbyregisteringthenamesof life

(non-life) insurance agents/brokers who applied for

licenses and renewal of licenses for selling insurance

on telephone as “universal life” / “unit-link” insurance

sellers, as well as the names of those whose licenses

hadbeenwithdrawnandpostingthemontheOIC’s

website so that the public and related persons can

cheek those agents/brokers status. This is just to

make sure of legal insurance business transactions.

Annual Report 2014

42 Office of Insurance Commission (OIC)

6.4 Development of the linkage system

for sending examination papers from Bangkok to

otherexaminationcenterscountry-widetomaintain

safe, quick, convenient, reliable and transparent

managementofexaminationpapersandexamination

procedure. The system had already been tested and

training of personnel had also been held. The system

hadalreadybeeninstalledatOIC’ssixexamination

centers inOIC regional offices, namelyOICOffice

Region1 (Chiangmai),OICOfficeRegion3 (Nakhon

Sawan),OICOfficeRegion4(Udornthani),OICOffice

Region6(NakhonRatchasima),OICOfficeRegion10

(NakhonPathom)andOICOfficeRegion12(Songkhla).

6.5 Regulation of individual insurance

brokers.Licenseshadbeenissuedto32juristicpersons

to act as brokers and 280 licenses had been renewed.

Inspectionof18insurancebrokersasjuristicpersons,

including commercial banks, to make sure that they

conformedtoLife/Non-LifeInsuranceActB.E.2535

as well as related laws had also been carried out.

6.6 Approval of a total of 45 organizations to

serve as training institutes in the licensing and renewal

of license for life insurance and non-life insurance

agents and brokers. A total of 381,557 persons parti

cipated in the training. Approval had also been given

to seven institutes to organize seminars on insurance

to be counted as part of the training (starting from the

fourth one). A total of 2,590 persons participated.

6.7 Inspection of 45 organizations approved

to serve as training institutes to make sure that they

conformedtotheOIC’sannouncementonthetraining

course and method for the year 2013, and to give

advices concerning formation of a practice guideline

for self-supervision.

6.8 TheOICproudlygainedcertificationof

its quality management system (ISO 9001 : 2008) from

ManagementSystemCertificationInstitute(Thailand

: MASCI) for the system of “issuing life insurance and

non-life insurance licenses for agents/brokers” in late

August2011.ThecertificationexpiredonJune14,

2014 and the OIC, after a new assessment, gained

extensionofthecertificationforanotherthreeyears,

expiringonAugust10,2017.

43

Measure 2 : To Strengthen the Stability and

Competitiveness of the Insurance System

Insurance is the business that offers service

or “insurance contract” which is a “promise”

that itwill giveprotectionof the insuredperson’s

life and properties against future accidents/disasters.

Buildingastrong,stableandefficientinsurancesystem

that can meet future challenges which requires

professional management and supervision to strengthen

the insurance business is the key to developing public

trustandconfidence.Thefollowingstepswerethen

implemented :

1.StressTest

The OIC developed its supervision by using

the so-called “Stress Test” as an important tool for

riskmanagementneededtodeterminethefinancial

stability and flexibility of insurance companies to

meet the risk of losses and, at the same time, to

sustaininternationalstandardoffinancialstabilityof

thecountry’sinsurancebusinessinordertogaina

goodbalancebetweenexpectedrateofreturnsand

acceptable risk level.

For 2014 the OIC implemented its stress

test as follows :

1) Three meetings had been held to

consider the stress test framework for life insurance

businessbyconsultingon formingQIS2 framework

and its parameters to be used by every life insurance

companyforformingQIS2.

2) A stress test framework had been

drafted to be used by life insurance companies as

the manual for conducting their second quantitative

impactstudyofthestresstest(QIS2).

3) All the life insurance companies

wererequiredtoconducttheirQIS2andsubmittheir

report to the OIC.

4) TheQIS2reportswerecompiledand

summarized to be submitted to the OIC meeting.

Annual Report 2014

44 Office of Insurance Commission (OIC)

Regarding non-life insurance stress test,

the following steps had been taken :

1) Three meetings had been held to

consider the stress test framework for non-life

insurance business, Suggestions had been made on

improvementofdefinitionsanddetailsabouthow

tofilloutdatapertainingtogreatdisasterincidents.

2) A meeting of non-life insurance

companies had been held to give them information

and knowledge about the stress test for non-life

insurancebusiness,coveringbackground,objectives,

andbenefitsof the stress test, essential pointsof

the stress test for non-life insurance companies and

stress test reporting form.

3) A manual and reporting form for the

firstquantitativeimpactstudyofthestresstesthad

been produced and presented to every non-life

insurance company.

4)Everynon-lifeinsurancecompanywas

required to start conducting their firstquantitative

impact study of the stress test for non-life insurance

business on July 1, 2014 and to submit their result

on October 31, 2014.

5)Asummaryreportonthefirstquanti-

tative impact study of the stress test was produced.

2. Revision of Announcement on

Risk-Based Capital (RBC)

The OIC proposed revision of the Announce

ment on Risk-Based Capital (RBC) and had been

approved by the Insurance Commission in the 11/2014

meeting on October 31, 2014 and the 13/2014 meeting

on December 26, 2014. The revised aspects are as

follows :

1) Reduction of repetitive criteria for risk

control of insurance company assets.

2)Specificationofassetvaluesobtained

throughviolationoflawsexceptimmovableproperty

with deducted depreciated value to be counted as

one of the components of items deducted from the capital.

3) Revision of the wording for easy and

correct understanding by clarifying the guideline for

considering credit ranking of payable bond for capital

calculation for credit risk based on the same principle

andtransferoftheitem“otherextendedinsurance

debtor”totheextendedinsuranceassetsection.

4) Extension of the valuation period

forcapitalbonds invested insubsidiariesand joint

companies permitted to do life insurance or non-life

insurance business for one more year.

5) Calculation of capital for the risk of

insurance for long-term insurance by taking the

following steps :

45

(1) Each company is required to

maintain its capital for the risk in the amount equal

to the differentiated amount between the net

committed burden according to the long-term

insurance contract after extended insurance at

percentile 95 and 75 calculated by GPV.

(2) Each company is required to

maintain additional capital for the surrender risk

capital charge (SRC) in case the total surrender

amount of all the insured is higher than the total

amount of capital for all risks from every aspect of

normal business running plus insurance reserves

according to the Announcement on Assessment of

Insurance Company Properties and Debts.

3. RevisionoftheFrameworkfortheSupervisionofRisk-BasedCapital Phase2(RBC2)

The OIC kept monitoring the implementa-

tionofthefirstRBCsupervisionframeworkassoon

as it took effect in 2011 to review its suitability in

comparison with the RBC supervision in other related

countries.Thenin2014theOICstarteditsProjecton

Development of Risk-Based Capital Phase 2 (RBC2) for

insurance business in succession to RBC1 which ended

in2013.Themainobjectivesare1)toimproveand

develop criteria for determining capital, parameters,

and how to assess prices of properties and debts

currently being in effect with a view to meeting the

standardspecifiedbyIAIS;and2)todevelopaguideline

for the supervision of capital for those risks which

had not been required to provide capital so far, e.g.

operational risk, group risk and liquidity risk, etc. The

RBCprojectismanagedbyaworkinggroup,consisting

of representatives of life insurance and non-life

insurancecompanies,theLifeInsuranceAssociation

of Thailand, the Non-Life Insurance Association of

Thailand,theInsuranceMathematicians’Association

ofThailand,qualifiedexpertsandOICofficers.Towers

Watson Co.,Ltd. is the project’s consultant giving

advices on the supervision of foreign capital maintaining

as well as technical comments.

The OIC required every life-insurance and

non-life insurance company to run its Market test to

analyze the impact of the parameters for calculating

various risks and to obtain related suggestions to

be used as baseline data for updating the RBC2

supervision framework.

The OIC, in addition, designed its RBC2 Road

Map which is divided into three phases, comprising

Short-Term Plan (2015-2016), Medium-Term Plan

(2017-2019) and Long-Term Plan (2020 onwards).

Implementation of those plans needs close cooperation

between the OIC and the business sector in the

form of a working group so as to develop the RBC2

towardsfittingbestthecurrentsituation.

Annual Report 2014

46 Office of Insurance Commission (OIC)

4. Analysis and Audit Operations

4.1 Analysis and Audit of Insurance

Companies

1) Analysis of financial stability from

the financial andenterprise status reports, reports

on maintenance of capital and adequacy as well as

financialbalanceof87lifeinsurancecompaniesand

non-life insurance companies (data as of December

31,2014).Itwasfoundthat87ofthemhadfinancial

status according to legal standard.

2) On-site assessment of 32 insurance

companies (during January 1 - December 31, 2014)

focusing on corporate risk found that most of them

had quite good or strong level of control system and

risk management, whereas some of them still needed

improvement of their risk management. However, two

ofthem(ThailandHealthCenterPublicCo.,Ltd.and

UnionInterInsurancePublicCo.,Ltd.)themfoundto

have their very weak or critical level of risk management,

so the OIC had their permit revoked.

3) Revision of the framework and

methodofsupervisionfortheOIC’sInspectionSection

toachievemoreefficientassessmentandinspection

ofinsurancecompanies.Theexistingproceduresof

the Inspection Section were compared with those

international standard practices of insurance business

supervision organizations in advanced countries.

Advices and suggestions were then proposed for

improvement along with training of personnel to

achieve active and prompt action in monitoring,

preventing and solving financial problems and

business operations of insurance companies so that

they could meet international practices. The approved

revised supervision framework and method has been

put into practice since February 2014.

4.2 Criteria for Classification of Insurance

Contractsaccordingtothefourthfinancialreporting

standard(IFRS4)andExtendedInsuranceRecording.

SinceIFRS4onthepartofextendedinsurancewill

take effect on January 1, 2016, the OIC appointed

a working group to manage it, comprising represen-

tatives of the OIC, the business sector, Accounting

ProfessionCouncilofThailandandcertifiedauditors.

47

Resource persons specialized in IFRS4 were hired to

givetrainingsandpreparecriteriaforclassificationof

insurance contracts to be used as the practice guideline

for the business sector and audit and analysis staff in

examiningaccuracyofdatarecording.

4.3 A framework for controlling insurance

companies which are prone to causing losses to the

public had been prepared by using Article 52 of

Non-Life InsuranceActB.E.2535 (amendedbythe

secondNon-LifeInsuranceActB.E.2551(LifeInsurance:

Article52).Themainobjectiveistominimizedisputes

oftheuseoftheArticlebyone’sown judgement

by specifying a guideline for giving a notice to the

respective life insurance/non-life insurance company

in two cases, i.e.1) cases of corruption, and 2) cases

ofseriouserror.Lifeinsurancecompanieswithsuch

cases will then be required to correct their status or

performance.

5. Revision of Regulation and Conditions for Investment in Other Businesses

The OIC has made its second Announcement

onInvestmentinOtherBusinessesbyLife/Non-Life

InsuranceCompaniesB.E.2558byadjustingwording

about investment in trust funds for investment in

immovable and accumulated fund for infrastructure

for the sake of clarity and readiness for investment

in payable bonds or loan allowances. Additional

qualifications of the person(s) responsible for

supervisingtherespectivecompany’sinvestmentunit

intermsofforbiddentraitshavealsobeenspecified

in the sameway as those specified for directors,

managers and other persons authorized to act on

behalfoftheircompanyaccordingtoArticle35ofLife

InsuranceActandArtile34ofNon-LifeInsuranceAct

in order to place more emphasis on the importance

of their role towards their company.

6. Preparation of Code of Practice on Structure, Qualifications and Good Practices of Life/Non-Life Insurance Companies’ Directors

The OIC places emphasis on good gover-

nance of insurance companies, so it has continually

promoted their operation with good governance

based on appropriate and efficient performance

and internal audit, a clear guideline for dealing with

stakeholders’ rights, role, duty and responsibility,

cross-checking system, appropriate returns,

minimizationofconflictofinterests,allofwhichare

essentialfactorscontributingtoinsurancecompanies’

stabilityandconfidenceintheinsurancesystem.

Annual Report 2014

48 Office of Insurance Commission (OIC)

The OIC therefore set up a practice guideline

fordealingwiththestructure,qualificationsandgood

practiceofinsurancecompanies’boardofdirectorsso

that each company could concretely and effectively

conform to them. Following are the main points :

1)Specificationofthestructure,qualifications,

forbidden traits, components and duty and

responsibility of the board of directors of life and

non-life insurance companies.

2) Good practice of the board of directors

in the management of their company.

3)Appointment, qualifications and duty

and responsibility of each subcommittee and

independent committee members.

7. InternationalCooperation

7.1Cooperation with foreign countries’

insurance business supervision organizations :

OIC and China Insurance Regulatory Commission

(CIRC) sign an MOU on development of insurance

regulation in Beijing, People’s Republic of China

Exchange of Letters for Cooperation (EoL)

agreement between OIC and Financial Services

Agency (FSA), Japan

❖ Participation in 115 50th Annual

Seminar held during June 22-25, 2014 in London,

U.K., to share knowledge and opinions on insurance

business development, guidelines for development

of various aspects of insurance industry. Resource

persons from different organizations/agencies

aswellasexecutivesfromtheinsurancesectorjoined

the seminar.

❖ A Memorandum of Understanding

(MOU) on promotion of cooperation in the development

of insurance business supervision between the OIC

and China Insurance Regulatory Commission (CIRC)

was signed during the Asian Forum of Insurance

Regulators (AFIR) held during July 17-18, 2014 in

Beijing,People’sRepublicofChina.

49

❖ Participation in the 17th ASEAN

Insurance Regulators’ Meeting (17th AIRM) held

duringNovember24-26,2014inBruneiDarussalamto

share opinions, enhance cooperation with insurance

business supervision organizations from ASEAN

member countries, and prepare for the upcoming

ASEANEconomicCommunity(AEC)in2015.

OIC Secretary-General attends the 17th ASEAN Insurance Regulators’ Meeting (the 17th AIRM) during

November 24-26, 2014 in Brunei Darussalam

OIC hosts “The U.S. Insurance Regulation and Supervision Seminar on Solvency Monitoring and Risk

Governance” during August 4-6, 2014 at the Four Seasons Hotel, Bangkok

❖ An Exchange of Letter (EOL) was

made between the OIC and Financial Services Agency

(FSA) of Japan with a view to initiating cooperation

in various aspects such as personnel development,

exchange of data concerning insurance business

supervision and auditing. A summary of the meeting

with the FSA had been made on July 10, 2014.

Annual Report 2014

50 Office of Insurance Commission (OIC)

7.2 Cooperation with Public Agencies and

International Organizations

❖Co-hostingalongwiththeU.S.National

Association of Insurance Commissioners (NAIC) a

seminar/training on “The U.S. Insurance Regulation

and Supervision Seminar on Solvency Monitoring and

Risk Governance” during August 4-6, 2014 in Bangkok.

ThemainobjectivesweretoprovidetheOICstaff

and those staffs from insurance business supervision

organizations in Asia with an opportunity to learn infor-

mation about U.S. modern insurance business supervision

andexchangeknowledgeandideasforapplication

toappropriatedevelopmentoftheirowncountry’s

insurancebusinesssupervisionformaximumbenefits.

❖ Participation in the meeting with

World Bank staff under the project on “Solvency

Modernization along with Risk Based Capital for the

InsuranceSector”undertheWorldBank’stechnical

assistancewiththeobjectiveofupgradingThailand’s

insurance business supervision, particularly in respect

of risk levels, business auditing and related law and

regulations. The World bank representatives and the

project’s consultants visited Thailand beforehand

to collect data and make inquiry into the current

situation as well as related laws. They also had meetings

with the private sector including both insurance

companies and associations. The study results were

then presented along with the training for auditing

personnel and on-the-job training held during

August 18-29, 2014 and the seminar on “Solvency

Modernization along with Risk Based Capital for the

Insurance Sector” held on December 9, 2014.

❖Co-hostingalongwithASEANInsurance

Training and Research Institute (AITRI) a training/

seminar on “Extended Insurance for Insurance

Business Supervisors” during December 15-19, 2014

in Bangkok, where OIC staff and representatives from

insurancebusinesssupervisionorganizationsinASEAN

and other regions such as Azerbaijan, Uzbekistan,

Bahrain,PapuaNewGuinea,Kenya,Tanzania,thePhilippines,

Malaysia,Cambodia,LaosandVietnamattended.

8.GuidelineforInsuranceBusinessDevelopmenttoCopewithFreeTradeAgree-mentofASEANEconomicCommunity(AEC)

The OIC, the business sector and related

organizations joined hands in conducting a study

on Thailand’s insurance business’s prospect and

its competitiveness in comparison with the other

ASEANmember countries. They consulted on deter-

51

mination of a guideline for developing capability and

competitivenessofthecountry’sinsurancebusiness

togetreadyforAECtradeliberalizationaswellas

readiness of insurance companies to respond to the

needs of every sector by placing emphasis on three

aspects, namely:

1) Preparation of insurance companies

tobesecureand ready forexpansion toembrace

demands for additional insurance products.

2) Creation of a good competition

environment favouring stable growth.

3) Development of infrastructure

favouring sustainable insurance business growth and

expansion.

The guideline/road map for developing

insurancebusinesstocopewithAECtradeliberalization

(AECRoadMap)consistsofreactivemeasures,proactive

measures and supporting strategies as follows :

Type Complaints Resolved Percentage Sum Paid in Resolved Cases

Life 2,327 2,053 88.23 331

Non-life 8,353 7,716 92.37 2,432

Compulsory Motor Vehicle Accident Insurance 662 623 94.11 553

Arbitrator 295 283 95.93 4,105

Total 11,637 10,675 91.73 7,421

1. InsuranceDisputeResolution

Data as of December 31, 2014

❖ Reactive Measures comprise in-

creasing domestic“players’”capacitythroughincreasingminimum capital level, increasing the ratio of foreign shareholders,upgradinginsurancecompanies’goodgovernance and operation standard, and creating competition atmosphere favouring growth through reduction of supervision of premium rates and pension fees as well as issuance of reciprocative insurance business licenses.

❖ Proactive Measures comprise

development of infrastructure necessary for and

favouringinsurancebusinessexpansiontothewhole

ASEANregionalongwithpromotionofthesalesof

insurance products in the region.

❖ Supporting Strategies comprise

development of insurance business supervision frame-

work to meet international standard, enhancement of

supervision capacity, knowledge and specialization of

supervisionorganizations’personnel,insurancedata

linking, enhancement of public understanding of and

access to insurance system

Annual Report 2014

52 Office of Insurance Commission (OIC)

Measure 3 : Development of Insurance Law and Integrated Rights and Benefits Protection System

The OIC has been continuously engaged in

upgrading service quality of both the OIC itself and

the insurance business sector as well as protecting

insurancerightsandbenefitsofthe insured,which

are themain factors directly affecting confidence

in insurance industry and its image, by taking the

following steps :

Type of Insurance

Claimed Cases Claims Paid In Progress

Number of Cases

Amount (Million Baht)

Number of Cases

(%)Amount (Million Baht)

(%)Num-ber of Cases

Amount (Million Baht)

1. Life insurance & PA 213 27 213 100.00 27 100.00 - -

2. Motor vehicle insurance 39,927 4,107 39,927 100.00 4,107 100.00 - -

3. Assets insurance- Fire insurance (residence)- Fire insurance (commercial)

36,389

3,885

3,175

10,812

36,389

3,842

100.00

98.89

3,175

10,361

100.00

95.83

-

43

-

450

4. (IAR) 10,688 392,377 9,960 93.19 381,041 97.11 728 11,336

Total 91,102 410,498 90,331 99.15 398,711 97.13 771 11,786

TheOIC initiated its project on emergency

payment from Motor Vehicle Victims Fund for

emergency cases so that road accident victims can

be admitted for immediate treatment by hospitals

without the need to pay medical bills in order

to make it convenient for them and minimize

disbursementstepsbydevelopingtheE-claimsystem

through which online - real time hospital data will be

automatically linked to insurance companies whereby

2. AssistingFloodsVictims

The great floods in Thailand in late 2011

became the country’s disaster with far-reaching

effectsonalargenumberofhouseholds,SMEsand

large industries. The OIC stepped in to see to it that

thosefloodvictims’insurancerightsandbenefitswere

protected. Following is the summary of all claims

and compensations :

medicalexpenseswillbecompensated.Insurance

companieshavealsobeenurgedtousetheE-claim

systemforpayingmedicalexpensestoroadaccident

victims while having their own IT developed to meet

standard practicewith flexibility and to establish

inter-organizationdatabaselinkageforthepublic’s

bestbenefits.Atotalof1,917hospitals/clinicsand

45 insurance companies country-wide have joined

theprojectsofar.

3. IncreasingEfficiencyoftheE-claimSystem

Data as of January 15, 2015

53

4. Increasing Protection Expenses forRoad Accident Victims according toMotorVehicleVictimsProtectionActB.E.2535

The OIC, in its realization of the need to

increasemedicalexpensesforinitialclaimsunderthe

Compulsory Motor Vehicle Insurance to suit the current

economic situation and highermedical expenses,

submitted its proposal to the Ministry of Finance to

increase the initial pay from 150,000 baht/person to

30,000baht/personbutnotexceeding65,000baht/

person for the total claims for loss of life/permanent

disability/loss of organ(s) (35,000 baht/person) without

additional charge for premium. The proposal was

approved by the Cabinet on December 23, 2014 and

took effect on December 25, 2014. The increased

coverageamountwillbenefitroadaccidentvictims,

especially those who have not bought an insurance

policy or those who become victims of hit-and-run

accidents. Road accident victims will receive their

initial compensation amount from Road Accident

Victims Compensation Fund.

5. Research on the Framework andSuggestionsforPolicyonInsuranceSystemDevelopmentunderMotorVehicleVictimsProtectionActB.E.2535

With the dynamic socio-economic and

technologicalenvironmentsandtheadventofASEAN

EconomicCommunity(AEC)inlate2015whichwill

leadtofreeflowsofmanpower,goodsandinternational

transportation, the OIC, being in charge of Motor Vehicle

VictimsProtectionActB.E.2535,hadconductedits

research on the guideline for developing road accident

victims protection insurance system to be used for

long-term planning and implementing measures to

cope with long-term changes. It was found that the

currentActstillhasmajorproblemsasfollows:

(1) The problem about the protection principle

that does not intend to protect third person(s) only.

(2) The problem of coverage amount of

moneywhichisnotdividedbetweenmedicalexpenses

and compensation for loss of life/permanent disability.

(3) The problem of premium which is a

fixedrateandsodoesnotreflectactualrisks.

Annual Report 2014

54 Office of Insurance Commission (OIC)

(4) The problem of the structure of com-

pulsory motor vehicle insurance industry resulting

frompremiumfixing that requires cross-subsidyof

premium from insurance of other types of motor vehicle.

(5) The problem of the Compensation

Fund which specifies compensation formedical

expenses and loss of life/disability covering initial

damageonly,andthelackofoperationalfluency.

(6) The problem of the lack of standard

practice in payingmedical expenses to accident

victims, particularly papers required in application and

pending period for receiving compensation.

The OIC, therefore, proposed a guideline

for developing compulsory motor vehicle insurance

system into short-term development and long-term

development,e.g.adjustmentofcoverageamount

formedicalexpensesandlossoflife/disability,fixing

premiumsasmaximumandminimumceilings,etc.

Measure 4 : Development of Insurance Infrastructure

As insurance infrastructure is deemed as a key

mechanism in developing the insurance business, it

is necessary to promote human resource development,

IT development as well as insurance business

supervision organization development. The operations

that have been implemented are as follows :

1. InsuranceLawDevelopment

❖The Law Research Foundation of

the Council of State to conduct the parent law

revision based on collected ideas and suggestions/

recommendationsonthedraftParentLawonInsurance.

The revision focuses on criteria for the supervision of

insurance companies, brokers/agents, penalty and

temporary provisions to be best suited to the dynamic

socio-economic circumstances and meet international

insurance supervision standard by comparing with

related foreign and domestic laws, including the

law on financial institution business and the law

on securities and securities market supervision. The

rationale for the revision had already been presented

tointernalunitsviatheCommitteeonAuditandLegal

Cases.ThedraftisnowundertheOIC’sconsideration

before proposing it to the Insurance Commission and

the Ministry of Finance for consideration, respectively.

❖DraftLifeinsuranceAct(No.….)B.E.….

AndDraftNon-LifeInsuranceAct(No.….)B.E.….had

been urged with particular reference to shareholders

of life/non-life insurance companies. The revision

will affect the structure of shareholders and directors

of the insurance companies that responds to the

samecriteriaasenforcedunderthelawonfinancial

institution business, andwill thus fit the current

55

economicsituation,leadingtoinsurancecompanies’

financial strength and insurance business’s greater

stability. Payment for compensation from Life

InsuranceFundandNon-LifeInsuranceFundwillalso

benefitinsuredpeopleaswellasinsurancebusiness

entrepreneurs. Insured people will receive initial

sum of money more quickly in case any insurance

company’slicenseisrevoked.Bothdraftshavebeen

consideredandapprovedbytheNationalLegislative

Council on December 2, 2014, and have been

proposed to be signed by H.M. the King before being

announced in the Royal Gazette.

2. CreatingInsuranceBureauSystem

The Insurance Bureau System has been

designed as the insurance information center to help

regulate, support and promote the insurance business

in its operations, its market conduct, management of

claimsandbenefits,assessmentofinsurancereserve,

risk management and establishment of premium rates

according to risk factors to cope with the easing of

premium rate regulation in the future. In addition, the

system is able to help bring about better operational

stabilityandefficiencythatcreatestrustamongthe

public as well as related industrial sectors both within

the country and abroad. There have lately been

consultationsbetweentheOIC,TIDCo.,Ltd.andother

relatedorganizations/agenciestoimprovetheexisting

non-life insurance information structure to achieve

higherefficiencyandbetterreportingsystem.

3. OICCorporateGoodGovernance

3.1 Under the Guideline for OIC Good

Governance, approved by the OIC Meeting on April

19, 2013, the OIC urges putting good governance into

practice on a sustainable basis both at the commission

levelandtheoffice-levelwithaviewtosettingagood

exampletothosebeingundertheOIC’ssupervision

as well as showing its strong will and determination

to create good governance in the insurance business.

The OIC issued criteria and code of practice, consisting of :

3.1.1 Criteria and code of practice for

the commission on the following four matters :

(1) Good governance in perfor-

manceaccordingtotheInsuranceCommissionLaw.

(2) Commission meeting procedure.

(3) Reporting form for individual

Insurance Commissionmembers’management of

conflictofinterests.

(4) Commission performance

assessment criteria.

Annual Report 2014