Embed Size (px)

Citation preview

Ohio UniversityJanuary 27, 2010

OPERS has a long history of proactively addressing issues as early as possible (examples include the Choices Health Care Plan, the Healthcare Preservation Plan, separating pension trust from healthcare trust).

OPERS has a long history of responsible funding and conservative fiscal practices (examples include intergenerational equity value, funding healthcare benefits at inception in 1974, best practices in actuarial assumptions).

OPERS is committed to member involvement and communication.

2

3

More Than Needed Less Than Needed

May cause undue hardship on members

May create need for more drastic changes

later

Goal:Finding the Right Balance

Key to Achieving Balance Incremental Changes Over Time

Retirees living longer in retirement and we need to adjust our benefits to recognize that

Eliminate unfair subsidization of benefits of subsets of members

Encourage member engagement in their retirement planning

Economic environment4

5

Year

55 55 65 65Male Female Male Female Male Female

1940 61.4 65.7 6.4 10.7 -3.6 0.71945 62.9 68.4 7.9 13.4 -2.1 3.41950 65.6 71.1 10.6 16.1 0.6 6.11955 66.7 72.8 11.7 17.8 1.7 7.81960 66.7 73.2 11.7 18.2 1.7 8.21965 66.8 73.8 11.8 18.8 1.8 8.81970 67.2 74.9 12.2 19.9 2.2 9.91975 68.7 76.6 13.7 21.6 3.7 11.61980 69.9 77.5 14.9 22.5 4.9 12.51985 71.1 78.2 16.1 23.2 6.1 13.21990 71.8 78.9 16.8 23.9 6.8 13.9

1995 72.5 79.1 17.5 24.1 7.5 14.11996 73.0 79.2 18 24.2 8 14.21997 73.4 79.4 18.4 24.4 8.4 14.41998 73.7 79.4 18.7 24.4 8.7 14.41999 73.8 79.3 18.8 24.3 8.8 14.32000 74.0 79.4 19 24.4 9 14.42001 74.1 79.5 19.1 24.5 9.1 14.52002 74.2 79.5 19.2 24.5 9.2 14.52003 74.4 79.6 19.4 24.6 9.4 14.62004 74.8 80.0 19.8 25 9.8 152005 74.8 80.0 19.8 25 9.8 152006 75.1 79.9 20.1 24.9 10.1 14.92007 75.2 79.9 20.2 24.9 10.2 14.92008 75.4 80.0 20.4 25 10.4 15

Life Expectancyif retire at age

Years in Retirement

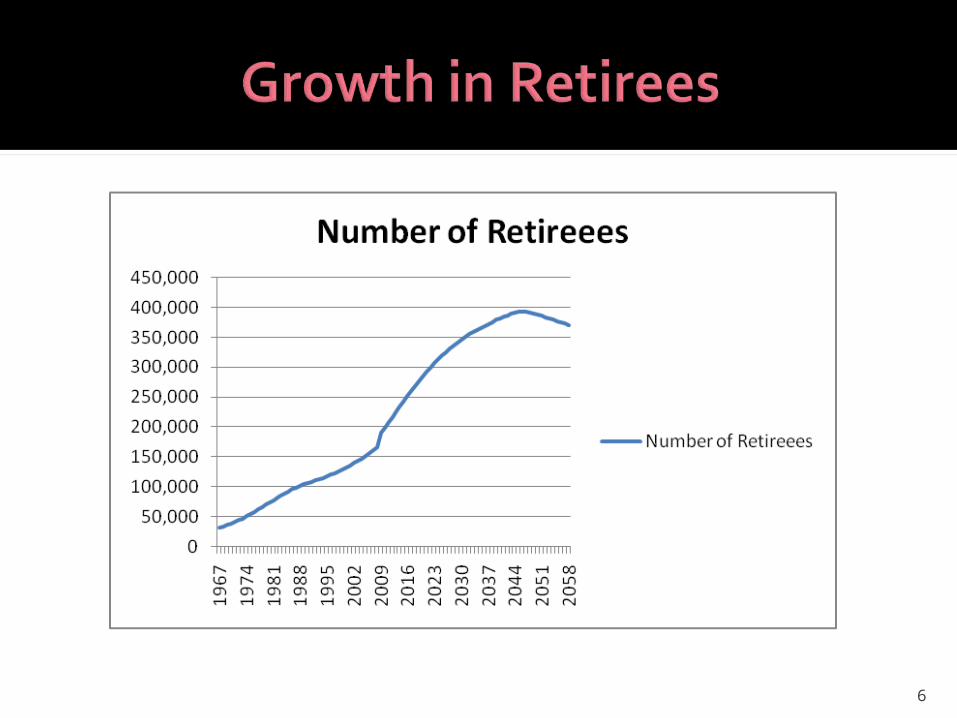

6

7

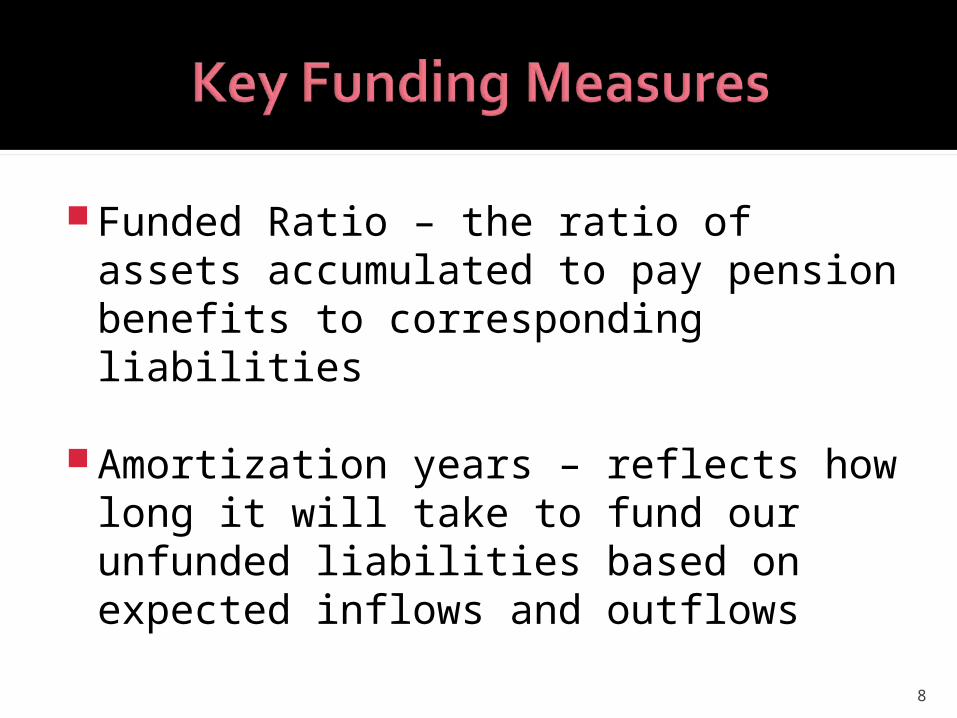

Funded Ratio – the ratio of assets accumulated to pay pension benefits to corresponding liabilities

Amortization years – reflects how long it will take to fund our unfunded liabilities based on expected inflows and outflows

8

9

Key Measures of OPERS Funding ($ in Millions)

ValuationYear

Actuarial AccruedLiabilities (AAL)

Pension ValuationAssets

Unfunded ActuarialAccrued Liabilities

(UAAL) Funded Ratio

PensionAmortization

Years

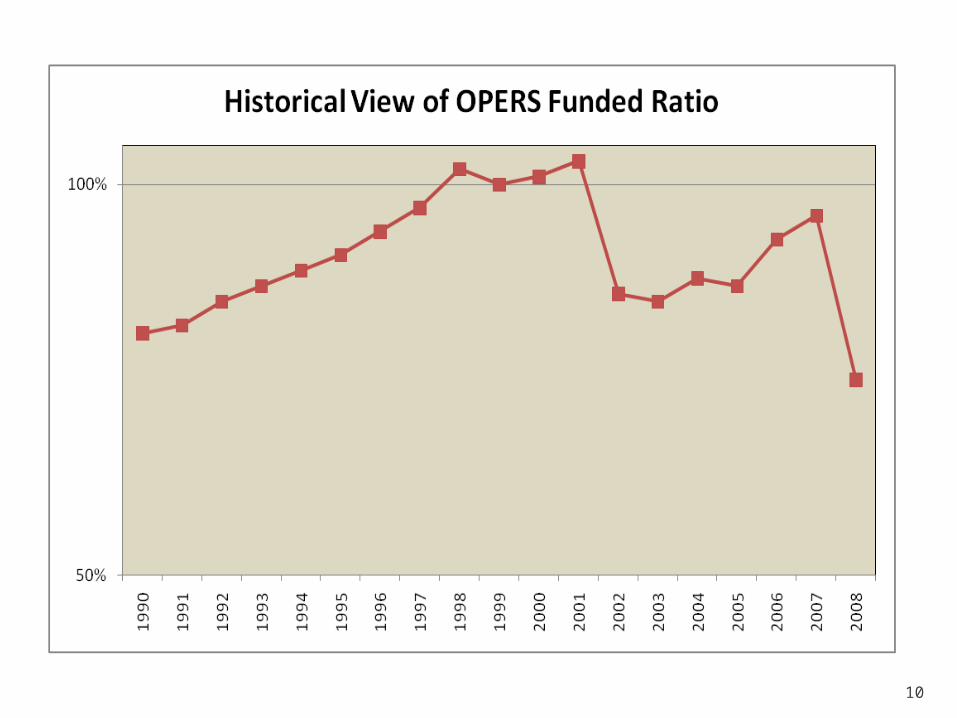

1990 $20,125 $16,245 $3,880 81% 36 **1991 22,027 18,108 3,919 82% 341992 23,961 20,364 3,597 85% 261993 26,506 23,063 3,443 87% 241994 28,260 25,066 3,194 89% 251995 * 30,224 27,651 2,573 91% 191996 32,631 30,534 2,097 94% 121997 34,971 33,846 1,125 97% 41998 37,714 38,360 (646) 102% n/a1999 43,070 43,060 10 100% 02000 46,347 46,844 (497) 101% n/a2001 * 47,492 48,748 (1,256) 103% n/a2002 50,872 43,706 7,166 86% 29

Results below include Combined Plan, initiated 1/1/20032003 54,774 46,746 8,028 85% 292004 57,604 50,452 7,152 88% 242005 62,498 54,473 8,025 87% 28 *2006 66,161 61,296 4,865 93% 262007 69,734 67,151 2,583 96% 142008 73,466 55,316 18,150 75% 30

* Revised actuarial assumptions** Precedes enactment of statutory requirement for 30 years funding

10

11

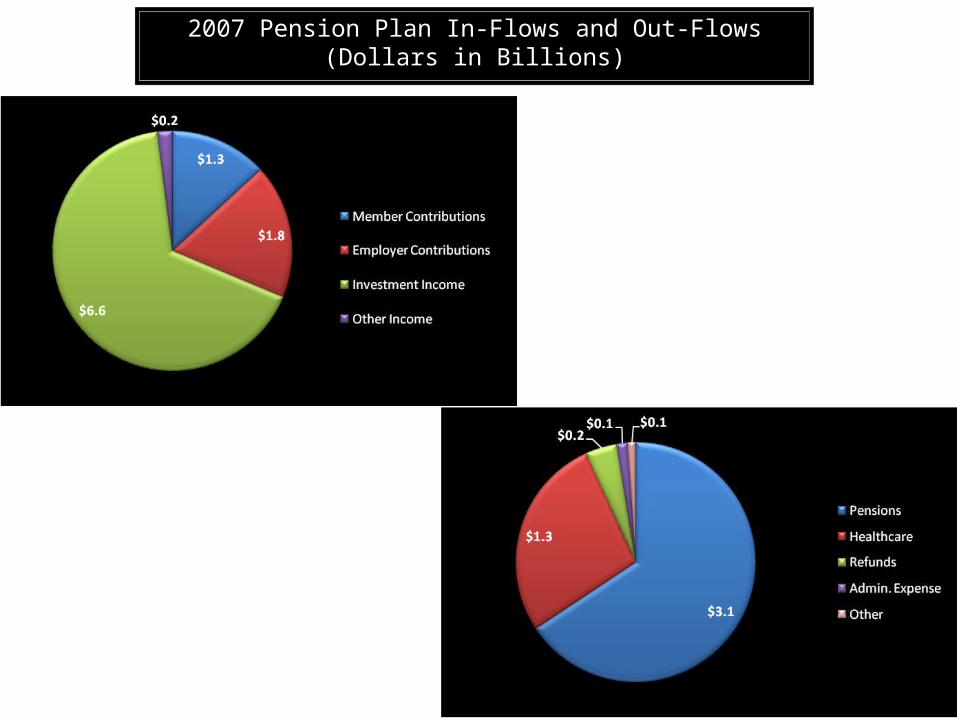

2007 Pension Plan In-Flows and Out-Flows(Dollars in Billions)

12

Historical Fluctuation of Market Returns

Top 4 Market Losses

2008 -26.9%

2002 -10.7%

2001 -4.6%

2000 -0.70%

Top 5 Market Gains

1982 28.3%

1985 25.6%

2003 25.4%

1995 20.5%

1989 18.4%

Data regarding OPERS investment returns is available back to 1979. A review of this historical data shows that OPERS has only had 4 years with negative investment returns since 1979.

13

2007 2008 Projected 2009

Funded Ratio 96% 75% 73%

Amortization Years

14 30 * 36

Healthcare Solvency

31 years 10 years 9 years* In order to stay within 30 years of funding, OPERS adopted a schedule of decreasing healthcare funding down to 0% by 2015, which means the healthcare fund would run out within 10 years

Recent Changes in Key Funding Measures

14

Keys to Changing Funding

15

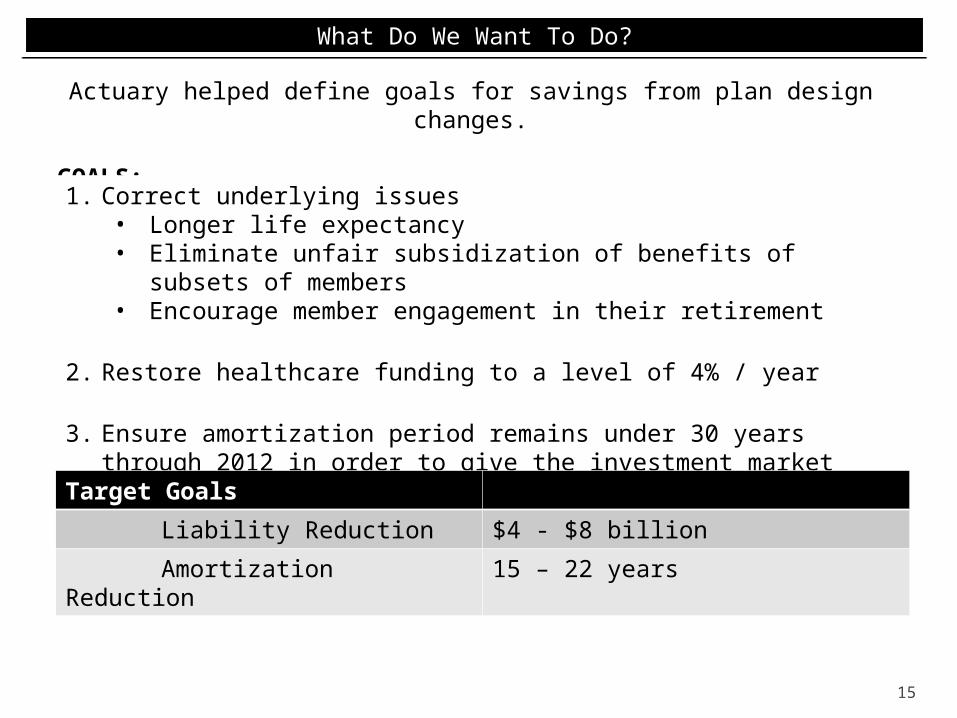

Actuary helped define goals for savings from plan design changes.

GOALS:

1. Correct underlying issues• Longer life expectancy• Eliminate unfair subsidization of benefits of subsets of

members• Encourage member engagement in their retirement

2. Restore healthcare funding to a level of 4% / year

3. Ensure amortization period remains under 30 years through 2012 in order to give the investment market time to recover

Target Goals

Liability Reduction $4 - $8 billion

Amortization Reduction 15 – 22 years

What Do We Want To Do?What Do We Want To Do?

16

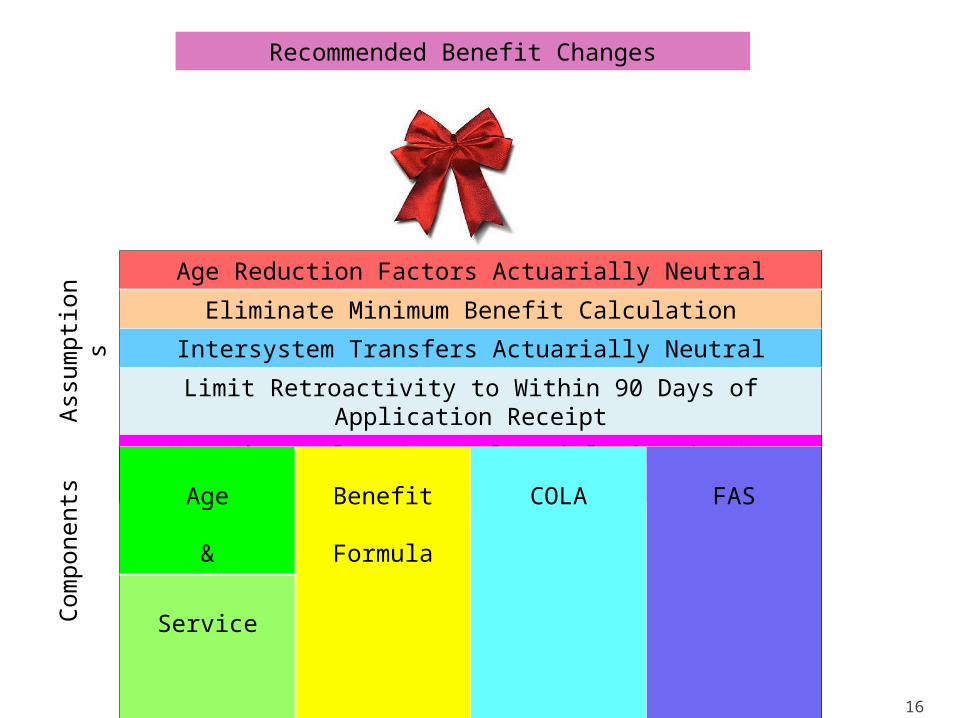

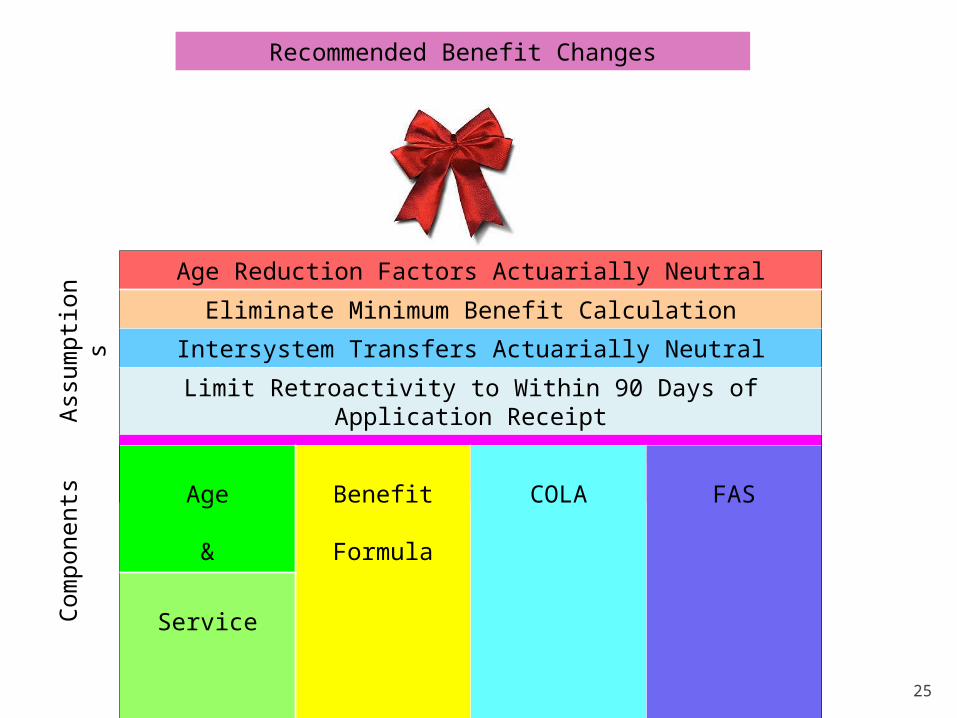

Recommended Benefit Changes

Age Reduction Factors Actuarially Neutral

Eliminate Minimum Benefit Calculation

Intersystem Transfers Actuarially Neutral

Limit Retroactivity to Within 90 Days of Application Receipt

New Hires After Date of Legislation in New Package

Age

&

Benefit

Formula

COLA FAS

Service

Ass

umpt

ions

Com

pone

nts

Changes in RetirementAge and Service (A)

(current)

General

Unreduced - 30 years/ any age, or age 65 w/5 yrs of service

Reduced - age 55 w/25 yrs of service, or age 60 w/5 yrs of service

Law

Unreduced - age 48 w/25 yrs of service, or age 62 w/15 yrs of service

Reduced - age 52 w/15 yrs of service

Public Safety

Unreduced - age 52 w/25 yrs of service or age 62 w/15 yrs of service

Reduced - age 48 w/25 yrs of service, or age 52 w/15 yrs of service

Benefit Formula (B)(current)

General

Unreduced - 2.2% x FAS for first 30 yrs of service, 2.5% thereafter

Law

Unreduced - 2.5% x FAS for the first 25 yrs of service; 2.1% thereafter

Reduced - age 52 and 15 yrs of service - 1.5% x FAS x yrs of service

Public SafetyUnreduced - 2.5% x FAS for the first 25 yrs of service; 2.1% thereafter

Reduced - age 52 and 15 yrs of service - 1.5% x FAS x yrs of service

Reduced - age 48 and 25 yrs of service

COLA (C)(current)

Percentage - 3% simple COLA

Timing - COLA begins 12 months after retirement

FAS (F)(current)

3 year FAS

Current

17

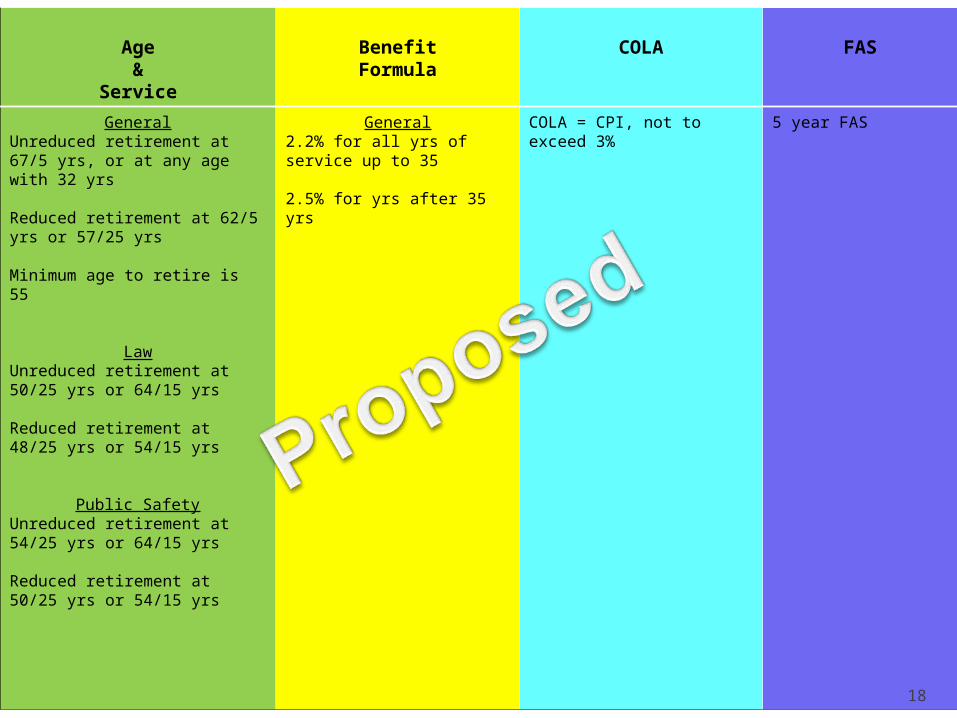

Age&

Service

BenefitFormula

COLA FAS

GeneralUnreduced retirement at 67/5 yrs, or at any age with 32 yrs

Reduced retirement at 62/5 yrs or 57/25 yrs

Minimum age to retire is 55

LawUnreduced retirement at 50/25 yrs or 64/15 yrs

Reduced retirement at 48/25 yrs or 54/15 yrs

Public SafetyUnreduced retirement at 54/25 yrs or 64/15 yrs

Reduced retirement at 50/25 yrs or 54/15 yrs

General2.2% for all yrs of service up to 35

2.5% for yrs after 35 yrs

COLA = CPI, not to exceed 3%

5 year FAS

18

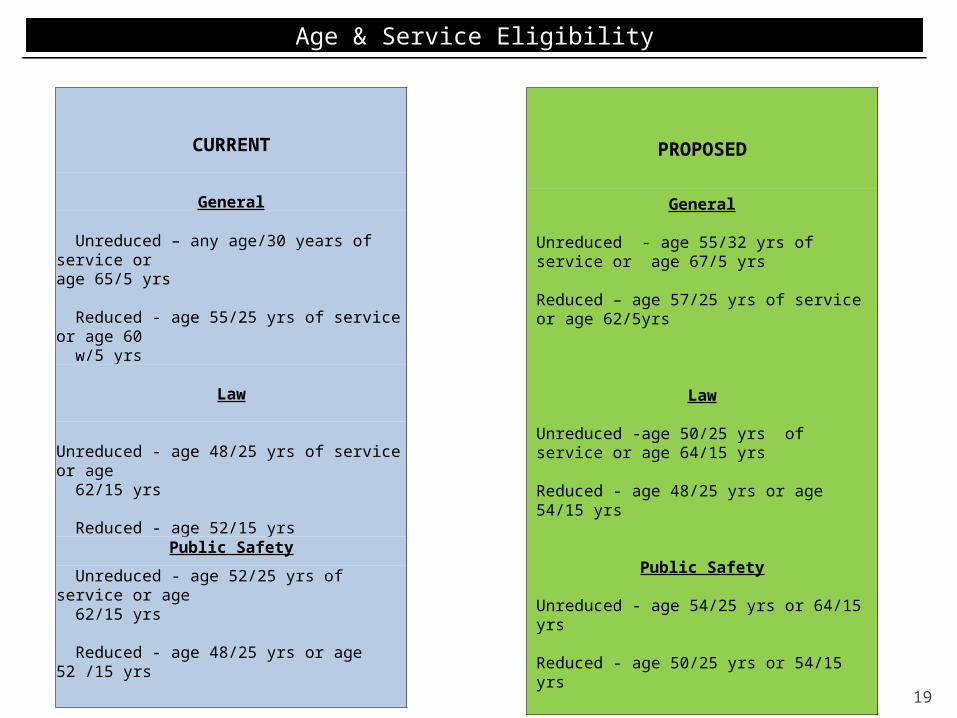

CURRENT

General

Unreduced – any age/30 years of service or age 65/5 yrs

Reduced - age 55/25 yrs of service or age 60 w/5 yrs

Law

Unreduced - age 48/25 yrs of service or age 62/15 yrs

Reduced - age 52/15 yrsPublic Safety

Unreduced - age 52/25 yrs of service or age 62/15 yrs

Reduced - age 48/25 yrs or age 52 /15 yrs

PROPOSED

General

Unreduced - age 55/32 yrs of service or age 67/5 yrs

Reduced – age 57/25 yrs of service or age 62/5yrs

Law

Unreduced -age 50/25 yrs of service or age 64/15 yrs

Reduced - age 48/25 yrs or age 54/15 yrs

Public Safety

Unreduced - age 54/25 yrs or 64/15 yrs

Reduced - age 50/25 yrs or 54/15 yrs

Age & Service EligibilityAge & Service Eligibility

19

CurrentGeneral

Unreduced - 2.2% x FAS for first 30 yrs of service, 2.5% thereafter

Law

Unreduced - 2.5% x FAS for the first 25 yrs of service; 2.1% thereafter

Reduced - age 52 and 15 yrs of service - 1.5% x FAS x yrs of service

Public Safety

Unreduced - 2.5% x FAS for the first 25 yrs of service; 2.1% thereafter

Reduced - age 52 and 15 yrs of service - 1.5% x FAS x yrs of service (no age reduction factors apply)

Reduced - age 48 and 25 yrs of service – 2.5% x FAS x yrs of service (age reduction factors apply)

Proposed

GeneralUnreduced - 2.2% for all yrs of service up to 35; 2.5% thereafter

Law

No change to benefit formula

Public Safety

No change to benefit formula

Benefit FormulaBenefit Formula

20

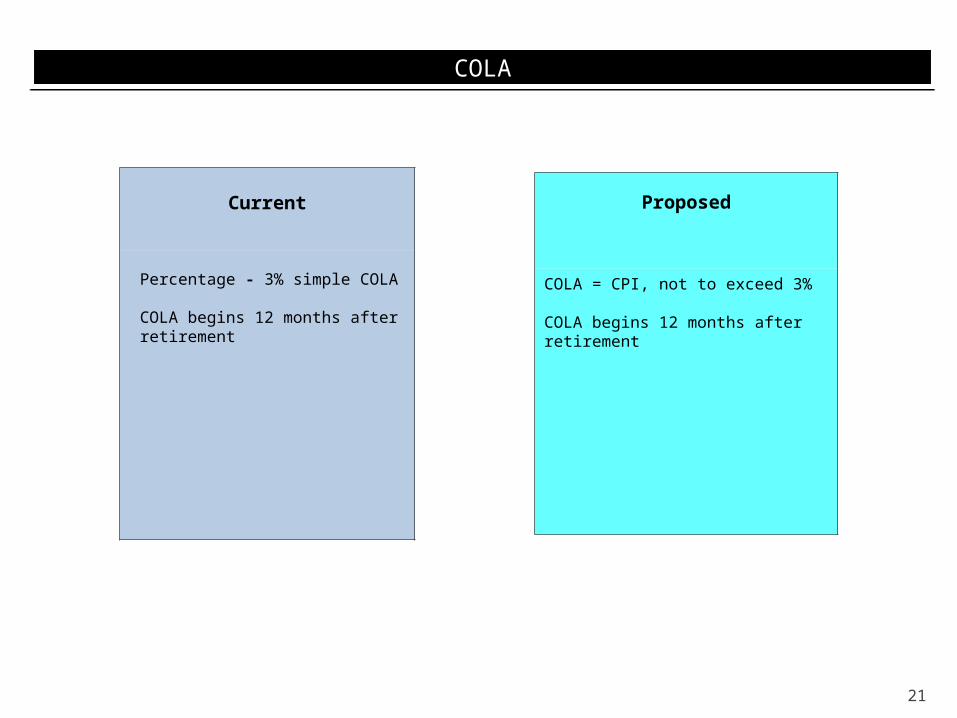

Current

Percentage - 3% simple COLA

COLA begins 12 months after retirement

Proposed

COLA = CPI, not to exceed 3%

COLA begins 12 months after retirement

COLACOLA

21

22

COLA Transition

Current retirees 3% (no change) 3% (no change)

Members retiring with effective dates during 5 yr transition period

3% until end of 5 yr transition period following legislation

Legislation would remove vesting in 3% COLA effective immediately

All COLAs after end of 5 yr transition period equal to CPI not to exceed 3%

Members retiring after end of 5 yr transition period

N/A All COLAs equal to CPI not to exceed

3%

Effective date of legislation

End of 5 yr transition period

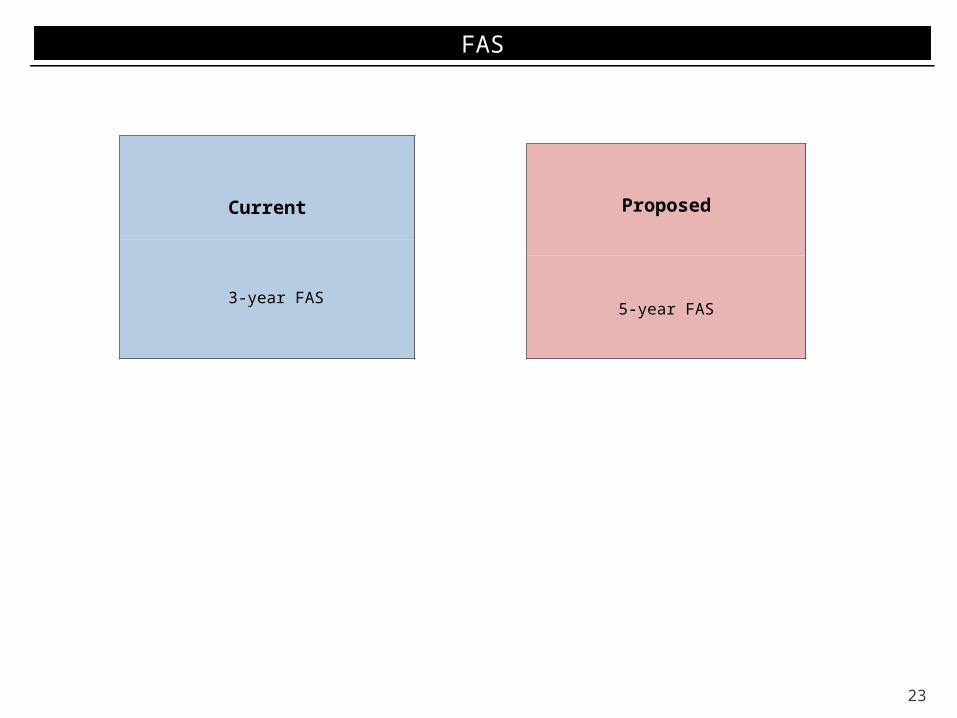

Current

3-year FAS

Proposed

5-year FAS

FASFAS

23

24

Assumptions

Age reduction factors for early retirement will be determined by actuary, not statute. (Similar to SERS change enacted previously)

Minimum benefit calculation ($86 per year x years of service) will be eliminated.

Intersystem transfers would be actuarially neutral.

Limit retroactive benefit effective dating to within 90 days of application receipt date.

New hires as of the effective date of legislation (example 2010) would be under new package (no delay until 2015).

25

Recommended Benefit Changes

Age Reduction Factors Actuarially Neutral

Eliminate Minimum Benefit Calculation

Intersystem Transfers Actuarially Neutral

Limit Retroactivity to Within 90 Days of Application Receipt

New Hires After Date of Legislation in New Package

Age

&

Benefit

Formula

COLA FAS

Service

Ass

umpt

ions

Com

pone

nts

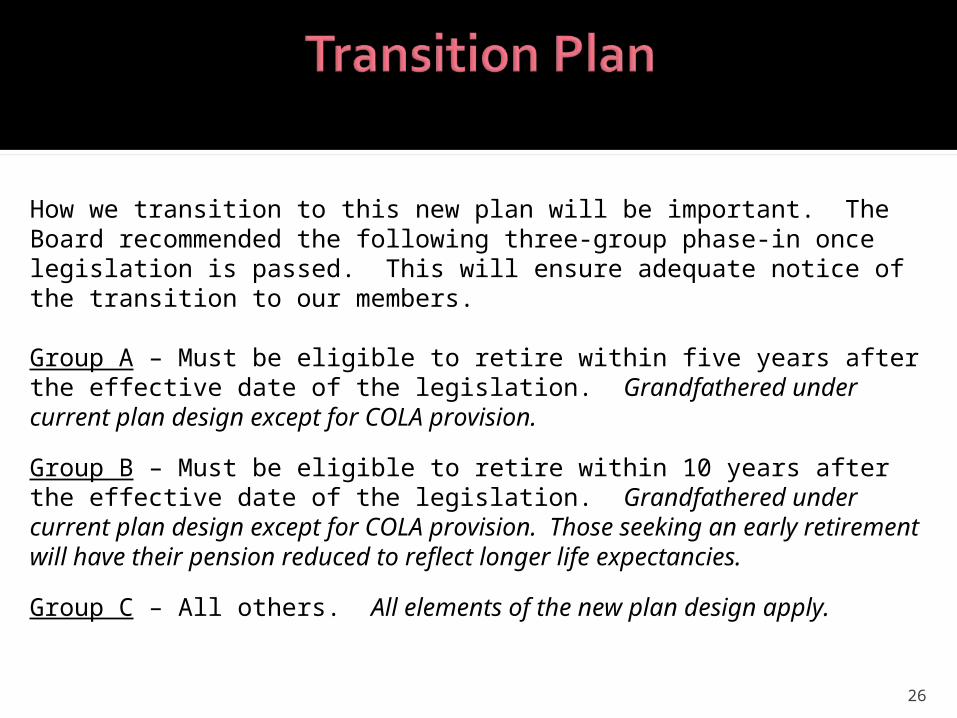

How we transition to this new plan will be important. The Board recommended the following three-group phase-in once legislation is passed. This will ensure adequate notice of the transition to our members.

Group A – Must be eligible to retire within five years after the effective date of the legislation. Grandfathered under current plan design except for COLA provision.

Group B – Must be eligible to retire within 10 years after the effective date of the legislation. Grandfathered under current plan design except for COLA provision. Those seeking an early retirement will have their pension reduced to reflect longer life expectancies.

Group C – All others. All elements of the new plan design apply.

26

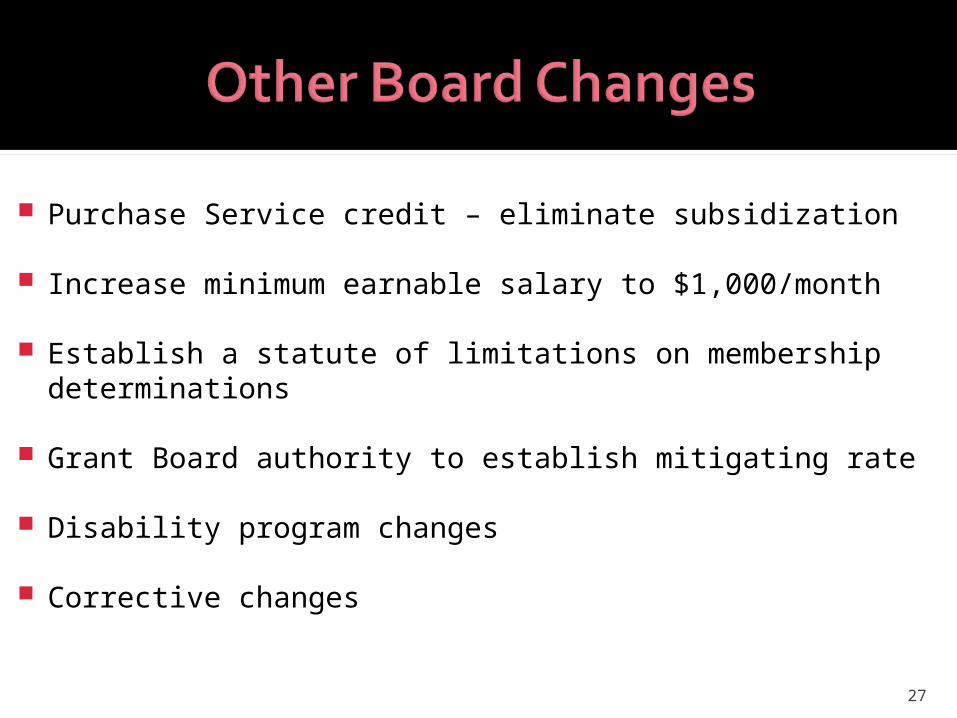

Purchase Service credit – eliminate subsidization

Increase minimum earnable salary to $1,000/month

Establish a statute of limitations on membership determinations

Grant Board authority to establish mitigating rate

Disability program changes

Corrective changes

27

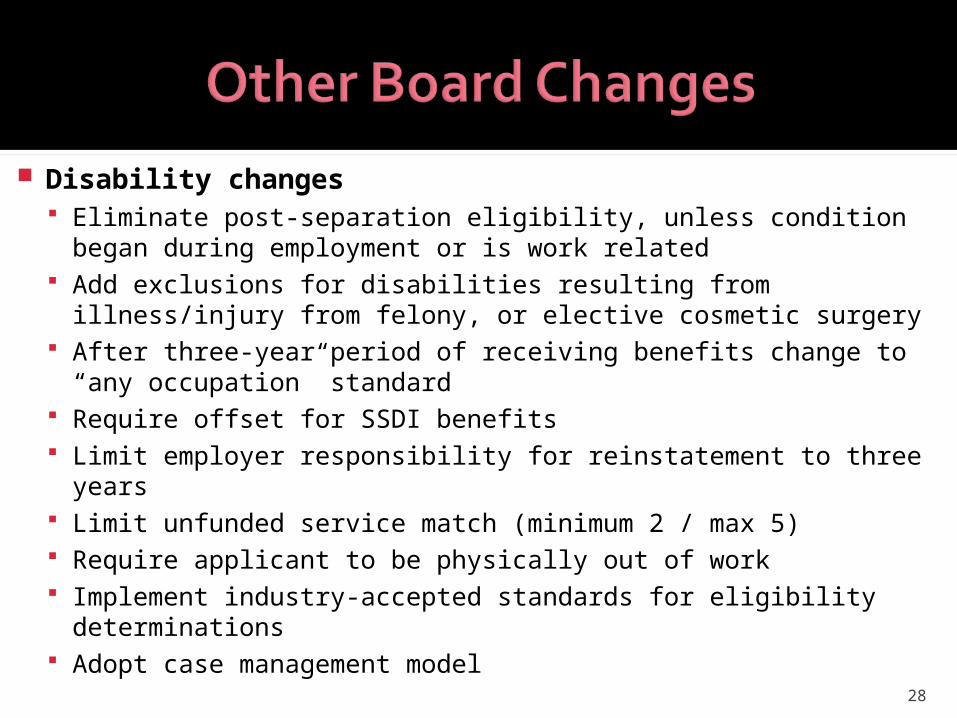

Disability changes Eliminate post-separation eligibility, unless condition began

during employment or is work related Add exclusions for disabilities resulting from illness/injury

from felony, or elective cosmetic surgery After three-year period of receiving benefits change to

“any occupation” standard Require offset for SSDI benefits Limit employer responsibility for reinstatement to three

years Limit unfunded service match (minimum 2 / max 5) Require applicant to be physically out of work Implement industry-accepted standards for eligibility

determinations Adopt case management model

28

Amortization

Purchase Service Credit actuarially neutral

Increase Minimum Earnable Salary to $1,000 per month

Establish Membership Determination statute of limitations

Board authority to establish mitigating rate

Disability changes

Retirement Age Eligibility/Benefit Formula/FAS/COLA(Alternative Plan Design)

Change RMA vesting schedule to 5 years *

*Does not require statutory authority for change

Estimated Total Impact Estimated 12.26 years

2009-10 Funding Plan2009-10 Funding Plan

29

Continue communication to members, stakeholders

Work with legislators

30

31