Embed Size (px)

Citation preview

ICE (LS) Gasoil Markets Forum

Oil futures forward curves:

economics explained

www.pjk-international.com

www.enfx.net

Oil futures forward curves

• ir. Patrick Kulsen, MSc. B.

Mail: [email protected]

Tel: +31-(0)76-7676 325

• Managing Director @ PJK International B.V.

• PJK International:

‘Market research company specialized in NWE oil markets’

– ARA / Rhine barge freight rates

– ARA oil product stocks

– Market analysis reports

– Consultancy & Quant research

– Freight Control App

Contents

1. Forward curves in focus

2. Economics of forward curves

3. Relevance of ARA gasoil stocks for ICE gasoil forward curve

4. ICE gasoil & Brent forward curves: analysis of recent

developments

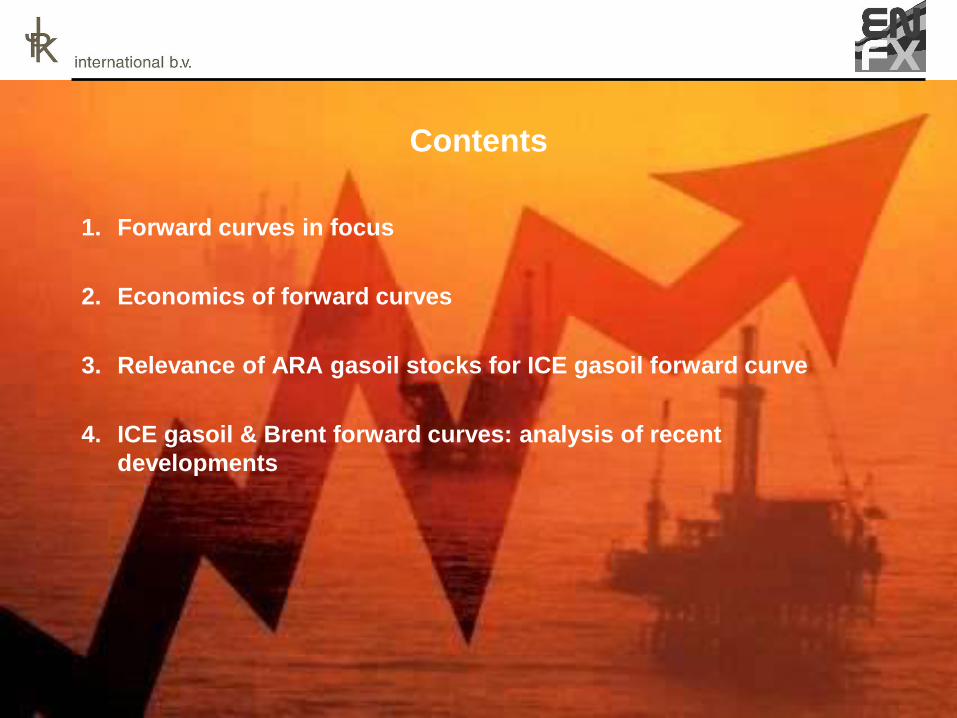

Forward curves in focus (1)

Oil futures forward curves??

Futures prices on Nov. 11th 2012 at 14:14 CET:

Forward curves in focus (2)

What do we know about forward curves….

….. and why is this important?

• Relevance for various market players

• Stylized facts of oil forward curves

Forward curves in focus (3)

Relevance for various market players:

1. Physical traders:

– Physical differentials (Gasoil 0.1% barges fob ARA)

– Basis risk of hedge using derivatives (futures / swaps)

– Inventory management: max. inventory or JIT

– Availability of product / storage capacity

2. Tank storage companies:

– Demand for tank capacity is linked to shape

• Contango: much demand

• Backwardation: little demand

3. Futures traders:

– Speculative spread trading

Forward curves in focus (4)

Stylized facts of oil forward curves:

Most important:

1. Shape of curve:

– Upwards sloping (contango) or

– Downwards sloping (backwardation)

2. Shape is persistent and fairly independent of daily

swings in futures prices

3. Crude and oil products forward curves are linked

Forward curves in focus (5)

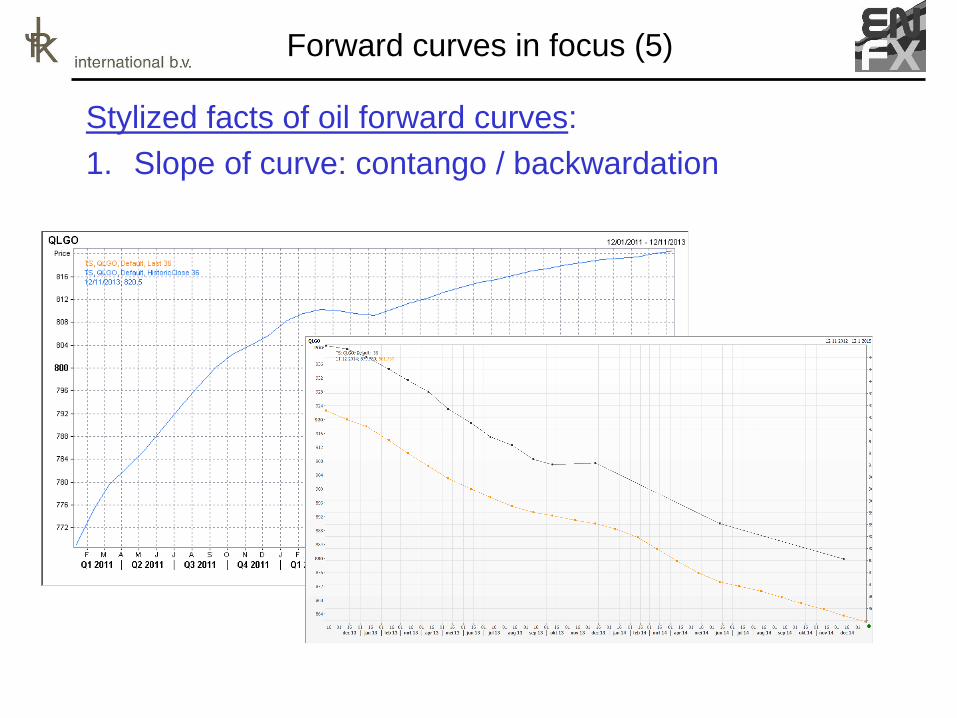

Stylized facts of oil forward curves:

1. Slope of curve: contango / backwardation

Forward curves in focus (6)

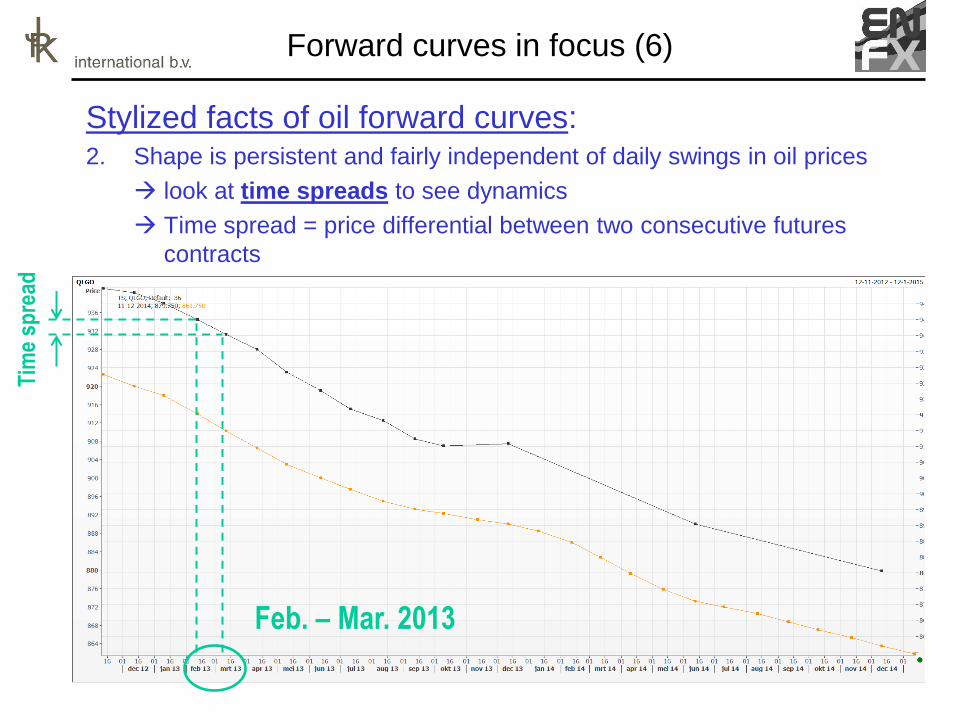

Stylized facts of oil forward curves: 2. Shape is persistent and fairly independent of daily swings in oil prices

look at time spreads to see dynamics

Time spread = price differential between two consecutive futures

contracts

Tim

e sp

read

Feb. – Mar. 2013

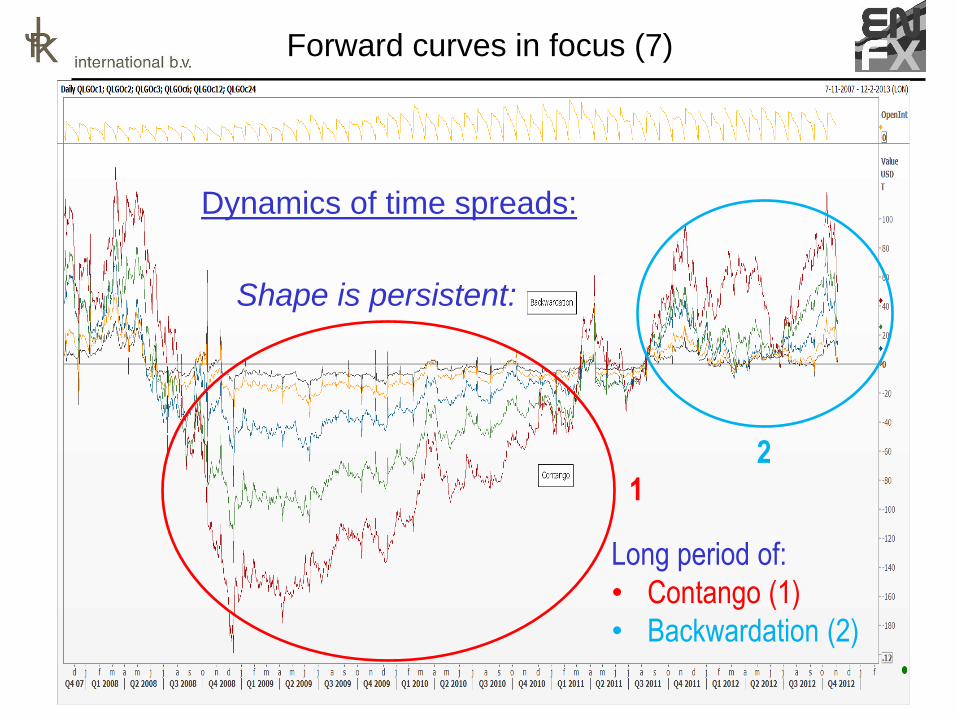

Forward curves in focus (7)

Dynamics of time spreads:

Shape is persistent:

Long period of:

• Contango (1)

• Backwardation (2)

1 2

Forward curves in focus (8)

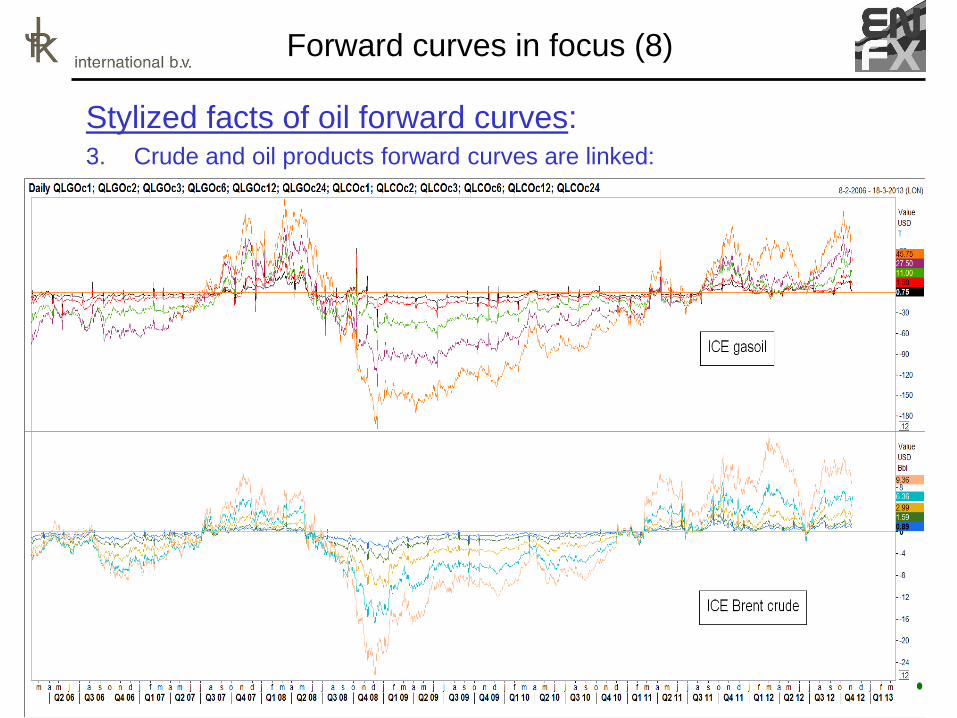

Stylized facts of oil forward curves: 3. Crude and oil products forward curves are linked:

Economics of forward curves (1)

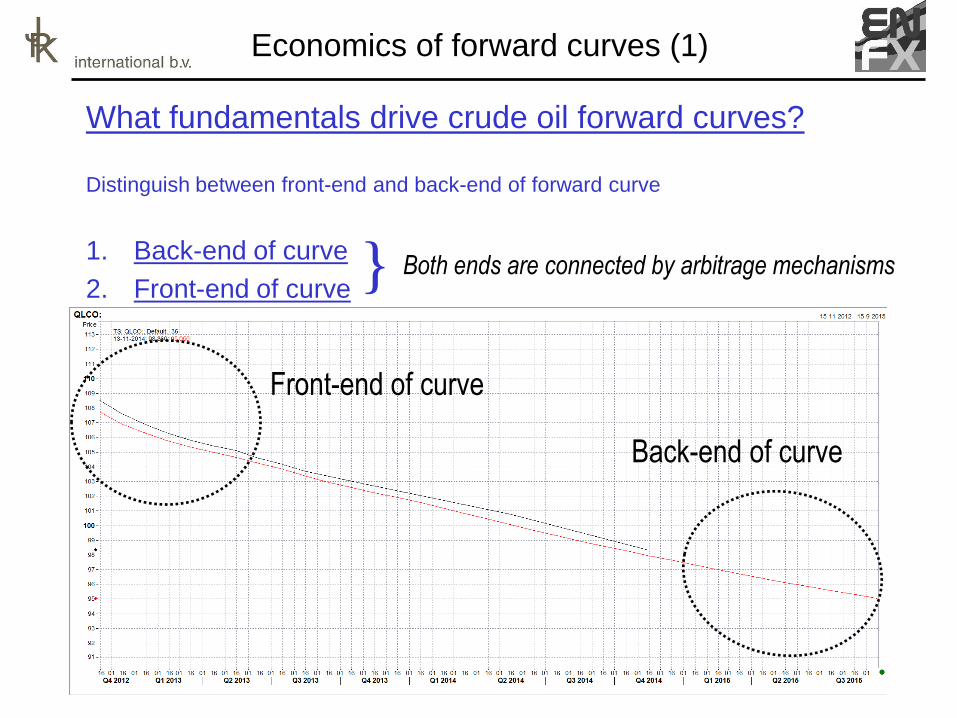

What fundamentals drive crude oil forward curves?

Distinguish between front-end and back-end of forward curve

1. Back-end of curve

2. Front-end of curve

Front-end of curve

Back-end of curve

} Both ends are connected by arbitrage mechanisms

Economics of forward curves (2)

What fundamentals drive crude oil forward curves?

1. Back-end of curve long term fundamentals

Supply side of crude market

Price to justify investments/divestments in exploration and

development of oil wells

Demand side of crude market

Price to justify investment/divestment programs for

• developing alternative fuels

• increasing fuel efficiency

• Etc..

Price = expected marginal ‘exploration, development and

production’ costs to balance market in the “long run”

Economics of forward curves (3)

What fundamentals drive crude oil forward curves?

2. Front-end of curve short term fundamentals

– Current and expected supply and demand

– Current and expected inventory levels

If supply > demand: price drops to stimulate players to

increase inventories to balance market

If demand > supply: price rises to stimulate players to free up

inventories and/or lower or postpone consumption to an extent

that the market is balanced

Economics of forward curves (4)

Arbitrage mechanisms connect front and back end of curve

Storage arbitrage play

Prevents time spreads from becoming too large

Links futures prices along the curve

Economics of forward curves (5)

Storage arbitrage play?

If contango

and

-(time spread) > marginal storage cost:

Long 1st month, short 2nd month

Hold both futures contracts till expiry

After expiry 1st month: collect and store product

After expiry 2nd month: deliver product

Profit = -(time spread) – storage costs

Storage costs:

• Transportation costs (transport product to tank terminal)

• Tank Terminal lease fee (opportunity costs: only if ‘spot’ market for

storage capacity)

• Finance costs

Economics of forward curves (6)

Storage arbitrage play?

If backwardation

and

time spread > shipping costs - interest

Subject to:

inventory level > min. level + replenishment lot:

Short 1st month, long 2nd month

Hold futures contracts till expiry

After expiry 1st contract: deliver product from storage tank

After expiry 2nd contract: collect product stock is replenished

Profit = time spread – shipping costs + interest

Shipping costs:

• Freight rate

• Insurance

Economics of forward curves (7)

Link crude oil & oil products forward curves?

Crude oil is feedstock for refineries to produce oil products

Most important input cost!

Difference between oil product price and crude price:

“Crack spread”

Proportional to refiner’s gross profit margin

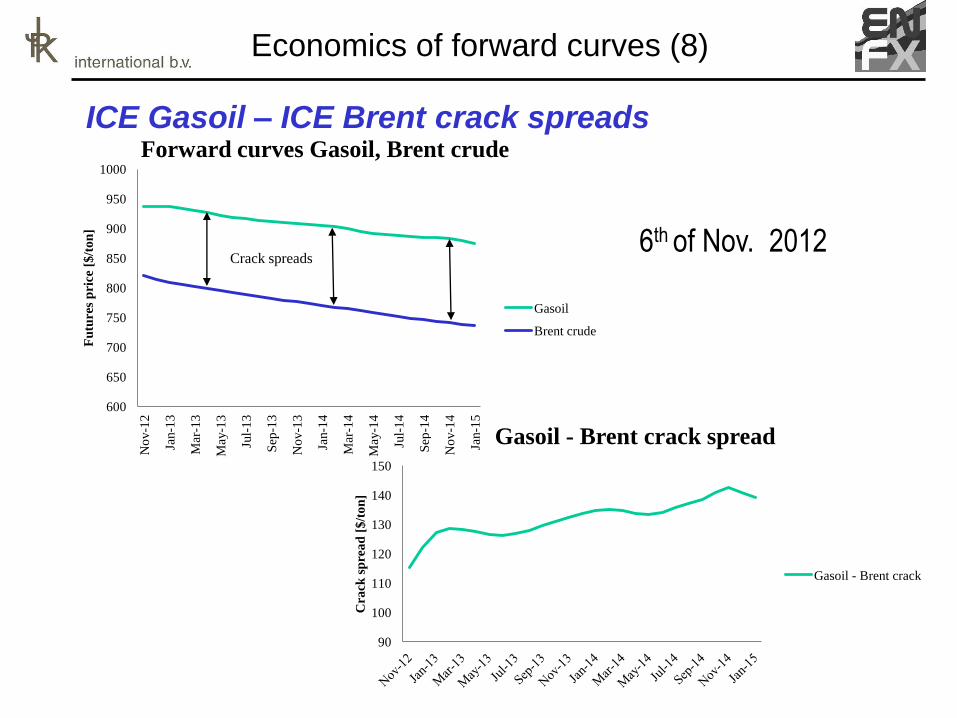

Economics of forward curves (8)

ICE Gasoil – ICE Brent crack spreads

600

650

700

750

800

850

900

950

1000

No

v-1

2

Jan-1

3

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan-1

4

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan-1

5

Fu

ture

s p

rice

[$

/to

n]

Forward curves Gasoil, Brent crude

Gasoil

Brent crude

Crack spreads

90

100

110

120

130

140

150

Cra

ck s

pre

ad

[$

/to

n]

Gasoil - Brent crack spread

Gasoil - Brent crack

6th of Nov. 2012

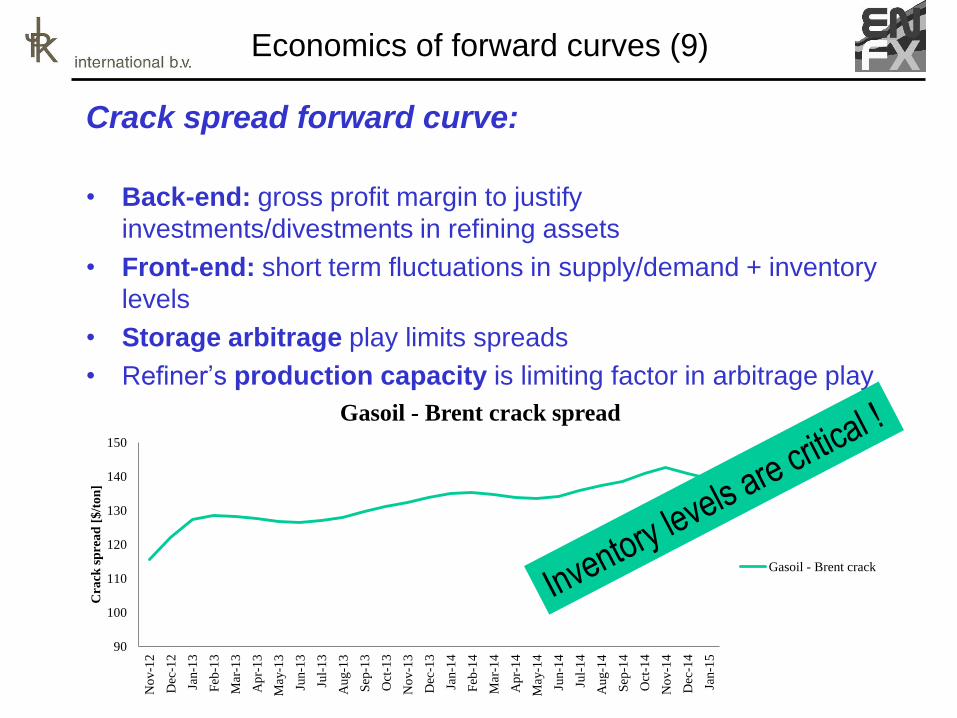

Economics of forward curves (9)

Crack spread forward curve:

• Back-end: gross profit margin to justify

investments/divestments in refining assets

• Front-end: short term fluctuations in supply/demand + inventory

levels

• Storage arbitrage play limits spreads

• Refiner’s production capacity is limiting factor in arbitrage play

90

100

110

120

130

140

150

No

v-1

2

Dec

-12

Jan-1

3

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun-1

3

Jul-

13

Aug-1

3

Sep

-13

Oct

-13

No

v-1

3

Dec

-13

Jan-1

4

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun-1

4

Jul-

14

Aug-1

4

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan-1

5

Cra

ck s

pre

ad

[$

/to

n]

Gasoil - Brent crack spread

Gasoil - Brent crack

Relevance of ARA oil product stocks (1)

ICE gasoil futures are traded all over the world….

…so why should ARA stocks be important?

Several reasons:

1. NWE main importer of middle distillates

2. ARA main trading hub in NWE

3. ARA physical delivery point of ICE gasoil contract

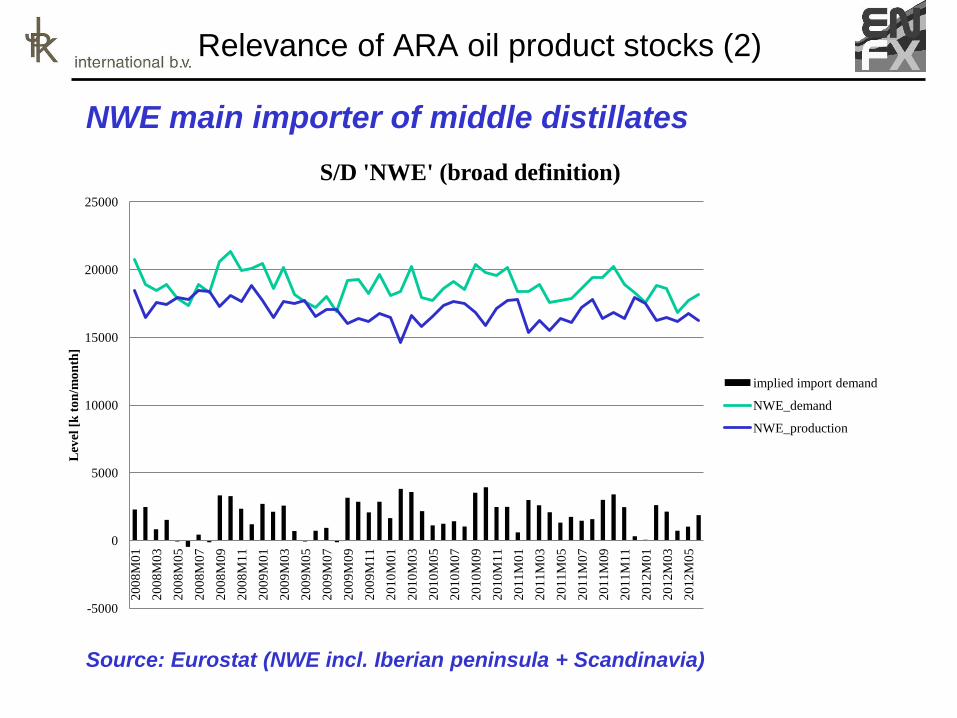

Relevance of ARA oil product stocks (2)

NWE main importer of middle distillates

Source: Eurostat (NWE incl. Iberian peninsula + Scandinavia)

-5000

0

5000

10000

15000

20000

25000

20

08

M0

1

20

08

M0

3

20

08

M0

5

20

08

M0

7

20

08

M0

9

20

08

M1

1

20

09

M0

1

20

09

M0

3

20

09

M0

5

20

09

M0

7

20

09

M0

9

20

09

M1

1

20

10

M0

1

20

10

M0

3

20

10

M0

5

20

10

M0

7

20

10

M0

9

20

10

M1

1

20

11

M0

1

20

11

M0

3

20

11

M0

5

20

11

M0

7

20

11

M0

9

20

11

M1

1

20

12

M0

1

20

12

M0

3

20

12

M0

5

Lev

el [

k t

on

/mo

nth

]

S/D 'NWE' (broad definition)

implied import demand

NWE_demand

NWE_production

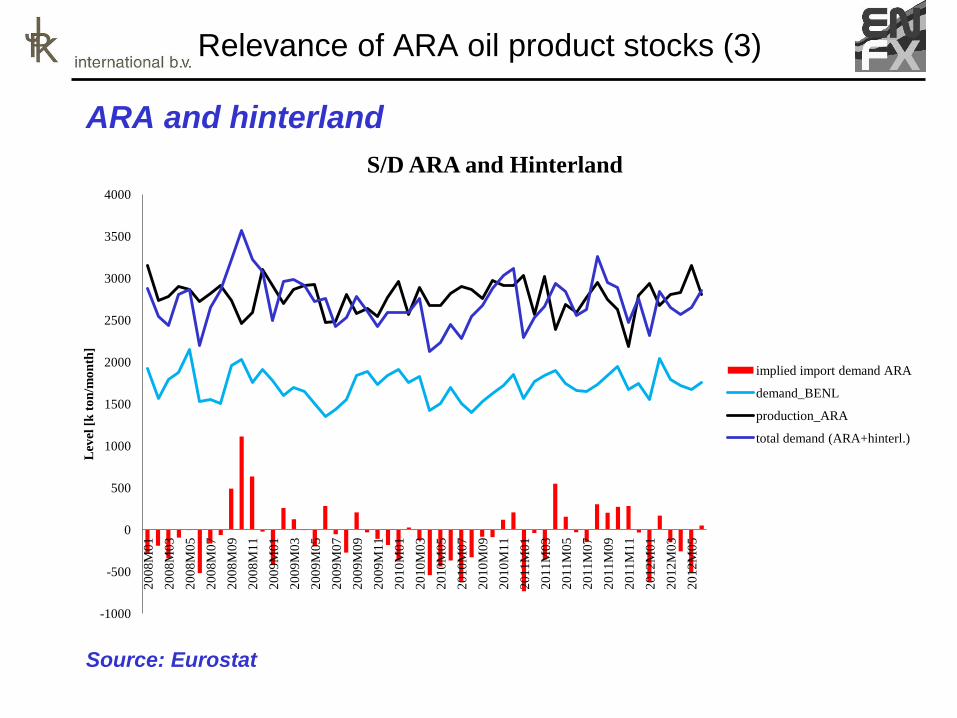

Relevance of ARA oil product stocks (3)

ARA and hinterland

Source: Eurostat

-1000

-500

0

500

1000

1500

2000

2500

3000

3500

4000

20

08

M0

1

20

08

M0

3

20

08

M0

5

20

08

M0

7

20

08

M0

9

20

08

M1

1

20

09

M0

1

20

09

M0

3

20

09

M0

5

20

09

M0

7

20

09

M0

9

20

09

M1

1

20

10

M0

1

20

10

M0

3

20

10

M0

5

20

10

M0

7

20

10

M0

9

20

10

M1

1

20

11

M0

1

20

11

M0

3

20

11

M0

5

20

11

M0

7

20

11

M0

9

20

11

M1

1

20

12

M0

1

20

12

M0

3

20

12

M0

5

Lev

el [

k t

on

/mo

nth

]

S/D ARA and Hinterland

implied import demand ARA

demand_BENL

production_ARA

total demand (ARA+hinterl.)

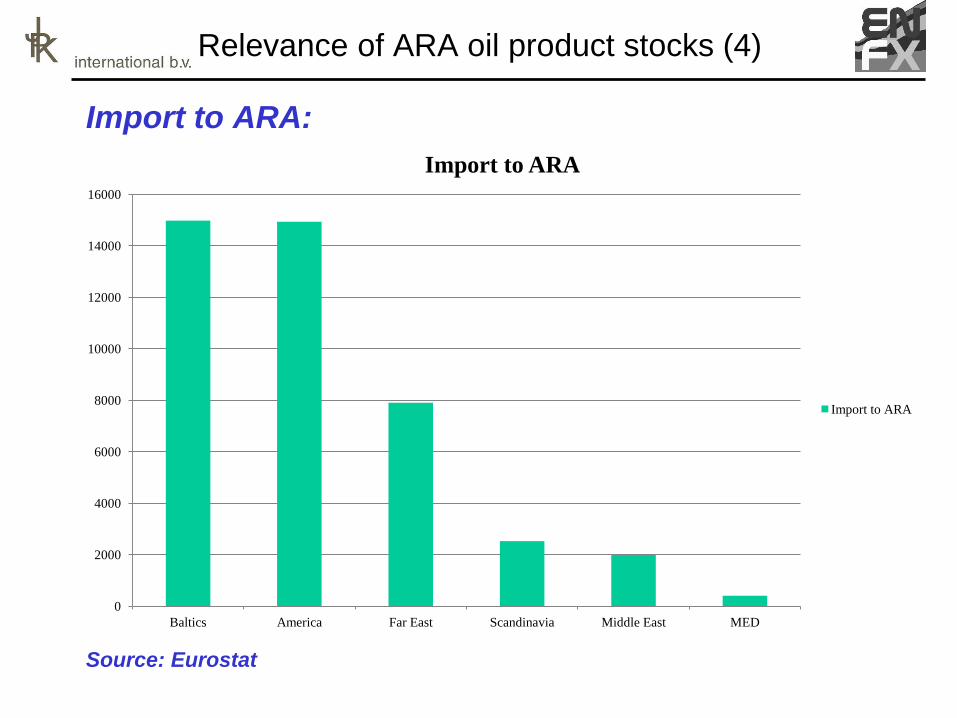

Relevance of ARA oil product stocks (4)

Import to ARA:

Source: Eurostat

0

2000

4000

6000

8000

10000

12000

14000

16000

Baltics America Far East Scandinavia Middle East MED

Import to ARA

Import to ARA

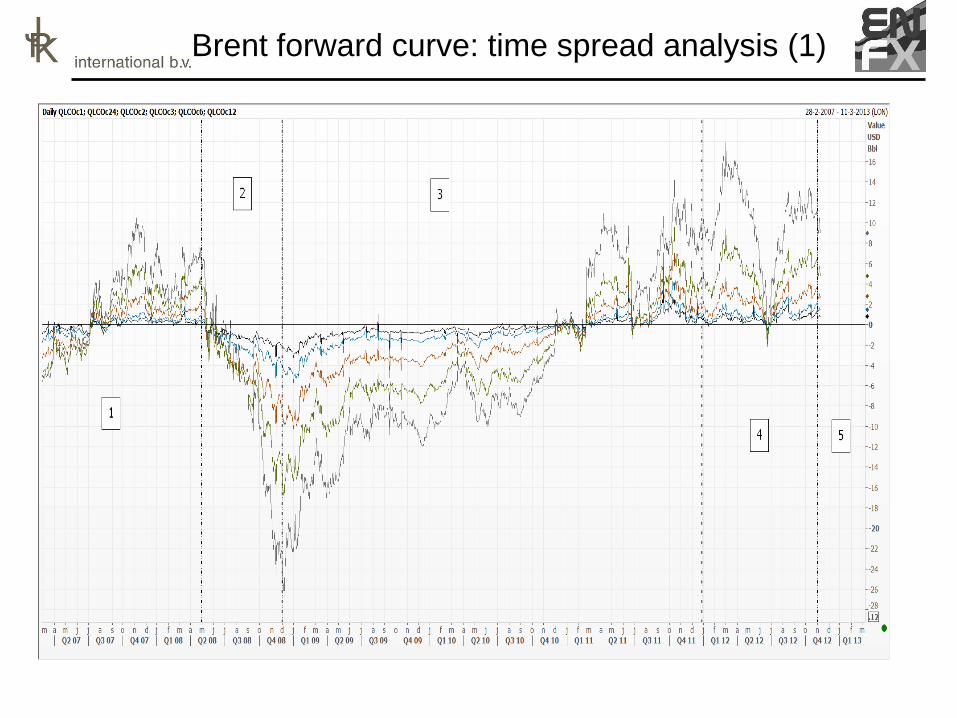

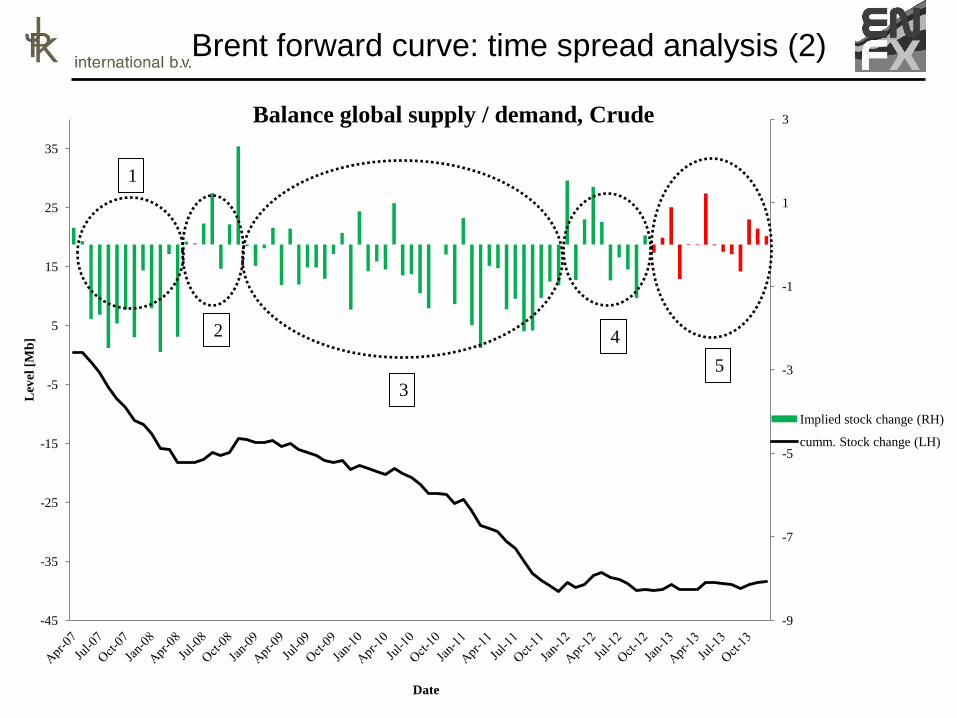

Brent forward curve: time spread analysis (1)

Brent forward curve: time spread analysis (2)

-9

-7

-5

-3

-1

1

3

-45

-35

-25

-15

-5

5

15

25

35

Lev

el

[Mb

]

Date

Balance global supply / demand, Crude

Implied stock change (RH)

cumm. Stock change (LH)

1

2

3

4

5

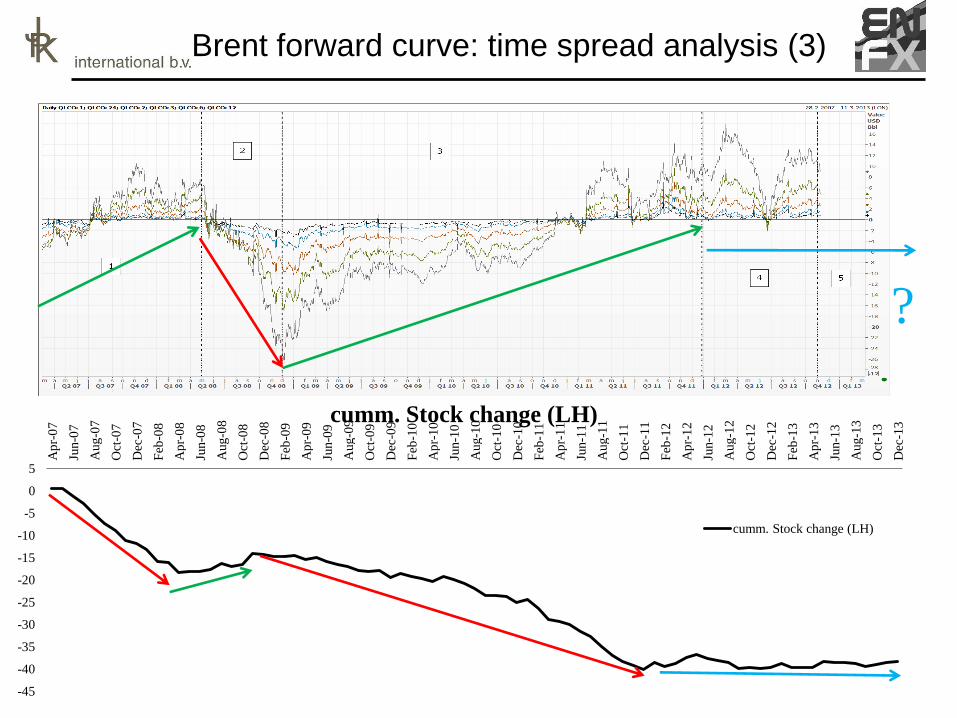

Brent forward curve: time spread analysis (3)

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

Ap

r-0

7

Jun-0

7

Aug-0

7

Oct

-07

Dec

-07

Feb

-08

Ap

r-0

8

Jun-0

8

Aug-0

8

Oct

-08

Dec

-08

Feb

-09

Ap

r-0

9

Jun-0

9

Aug-0

9

Oct

-09

Dec

-09

Feb

-10

Ap

r-1

0

Jun-1

0

Aug-1

0

Oct

-10

Dec

-10

Feb

-11

Ap

r-1

1

Jun-1

1

Aug-1

1

Oct

-11

Dec

-11

Feb

-12

Ap

r-1

2

Jun-1

2

Aug-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun-1

3

Aug-1

3

Oct

-13

Dec

-13

cumm. Stock change (LH)

cumm. Stock change (LH)

?

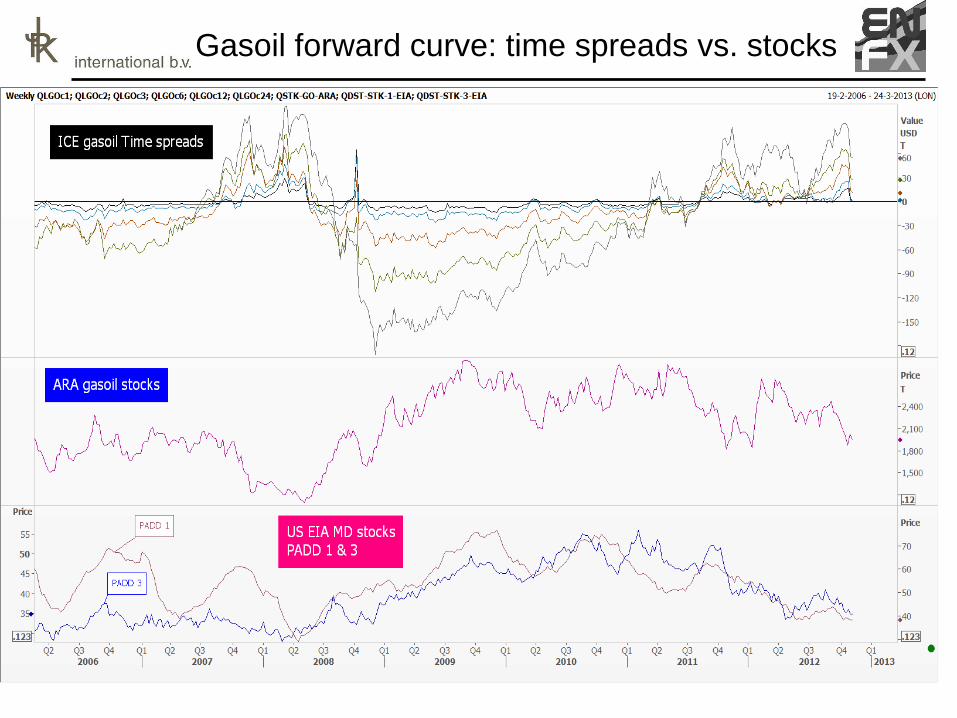

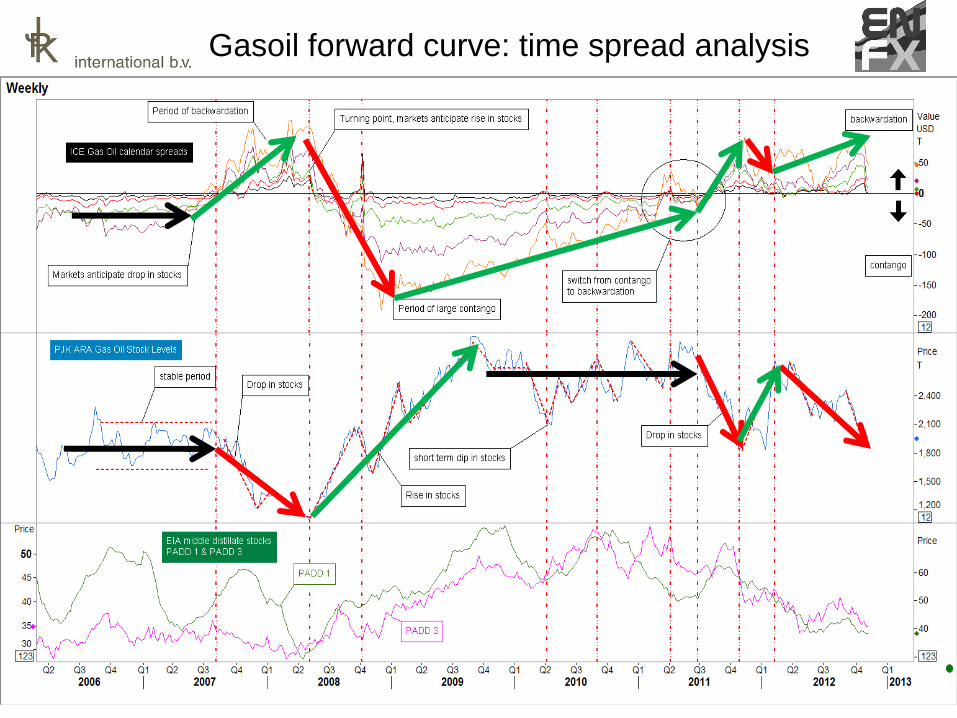

Gasoil forward curve: time spreads vs. stocks

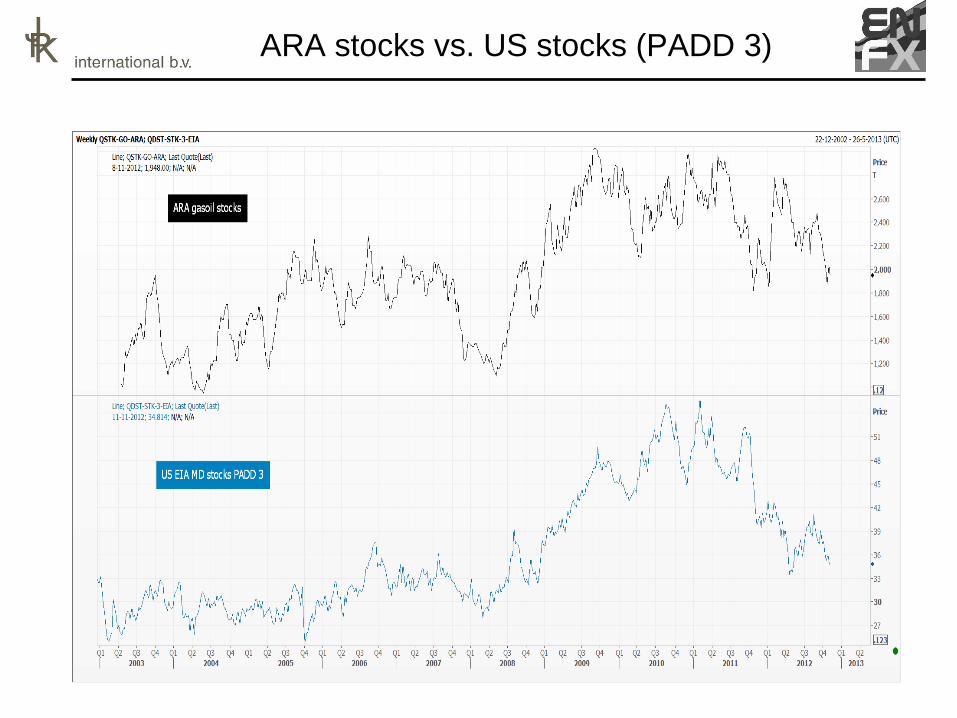

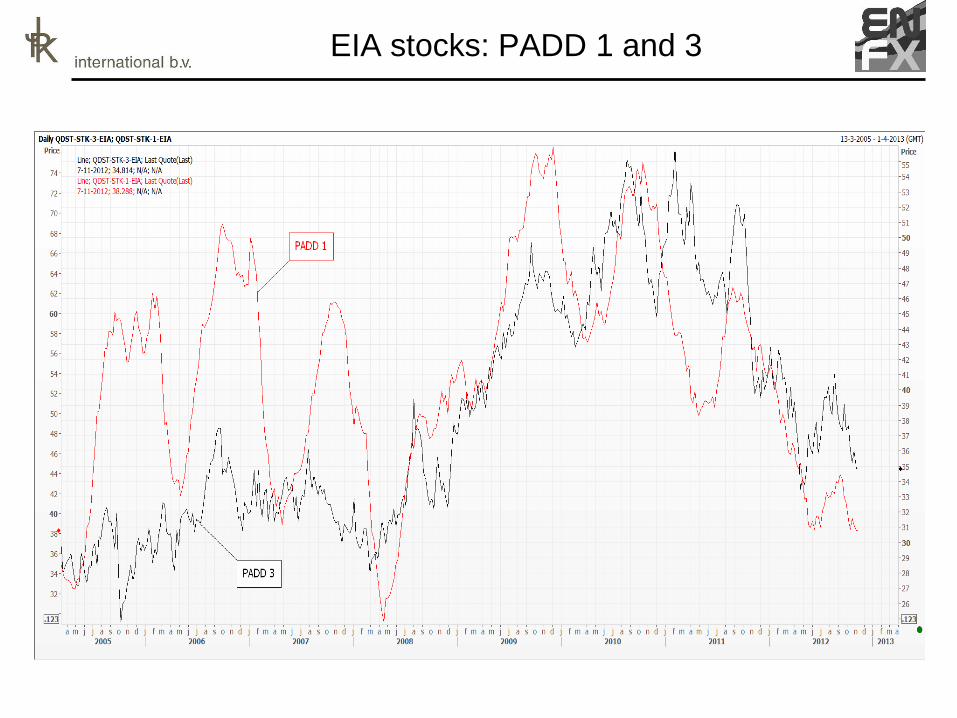

ARA stocks vs. US stocks (PADD 3)

Gasoil forward curve: time spread analysis

More information:

Visit PJK website

For outlook on oil forward curves see:

www.pjk-international.com/scenarios

For more theory on forward curves see:

www.pjk-international.com/downloads

?? – Questions - ??

?

Outlook for forward curves

Crude oil market: main themes

Downside risks:

• Global economic slowdown

• Demand destruction due to high oil prices

• Political risks: Eurozone crisis & Fiscal Cliff

• Further surge in US tight oil production

Upside risks:

• Unrest Middle-East

• Militant clashes in Libya

• North-Sea production outages

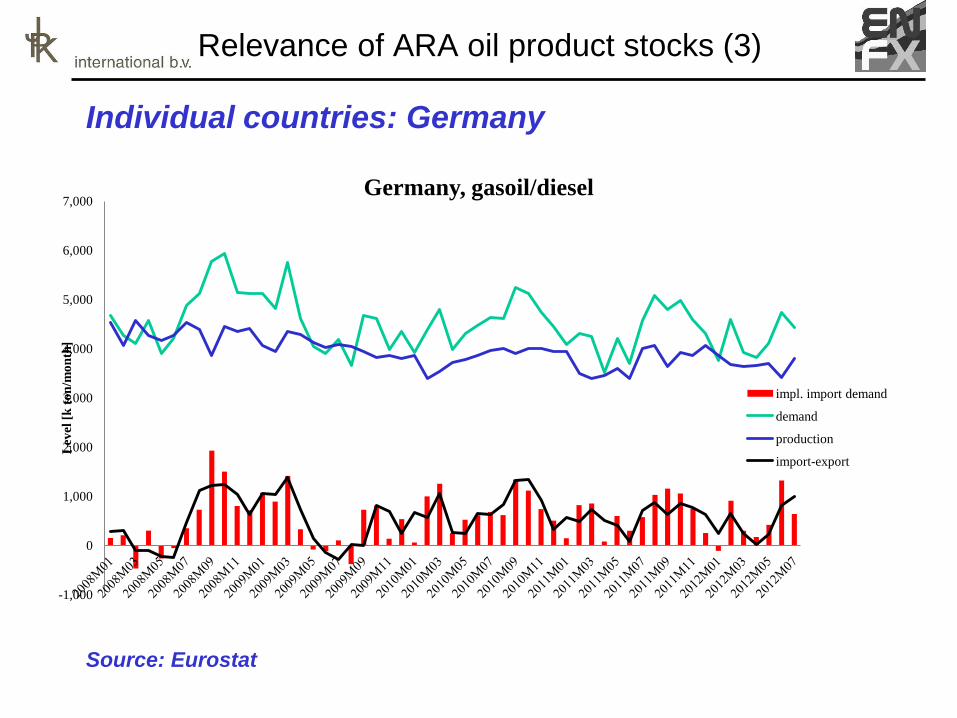

Relevance of ARA oil product stocks (3)

Individual countries: Germany

Source: Eurostat

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Lev

el [

k t

on

/mo

nth

]

Germany, gasoil/diesel

impl. import demand

demand

production

import-export

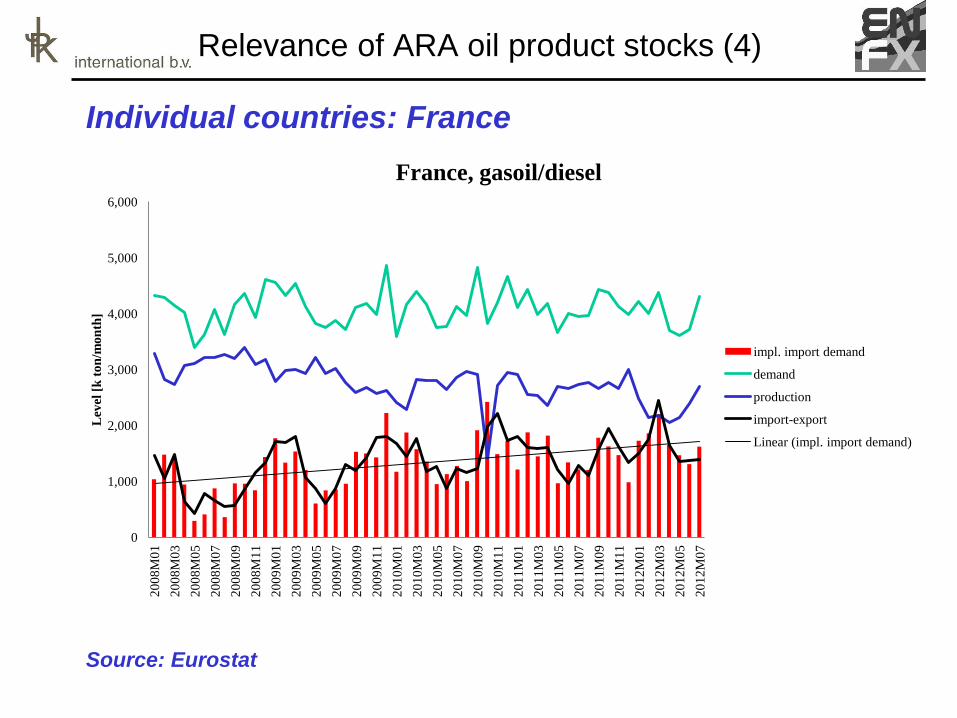

Relevance of ARA oil product stocks (4)

Individual countries: France

Source: Eurostat

0

1,000

2,000

3,000

4,000

5,000

6,000

20

08

M0

1

20

08

M0

3

20

08

M0

5

20

08

M0

7

20

08

M0

9

20

08

M1

1

20

09

M0

1

20

09

M0

3

20

09

M0

5

20

09

M0

7

20

09

M0

9

20

09

M1

1

20

10

M0

1

20

10

M0

3

20

10

M0

5

20

10

M0

7

20

10

M0

9

20

10

M1

1

20

11

M0

1

20

11

M0

3

20

11

M0

5

20

11

M0

7

20

11

M0

9

20

11

M1

1

20

12

M0

1

20

12

M0

3

20

12

M0

5

20

12

M0

7

Lev

el [

k t

on

/mo

nth

]

France, gasoil/diesel

impl. import demand

demand

production

import-export

Linear (impl. import demand)

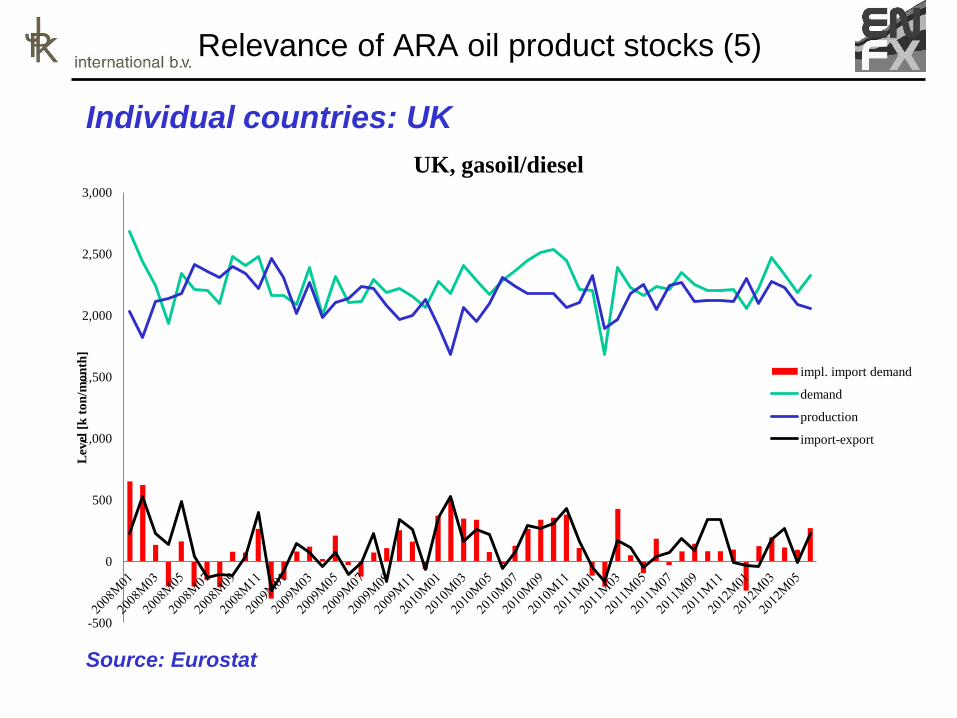

Relevance of ARA oil product stocks (5)

Individual countries: UK

Source: Eurostat

-500

0

500

1,000

1,500

2,000

2,500

3,000

Lev

el [

k t

on

/mo

nth

]

UK, gasoil/diesel

impl. import demand

demand

production

import-export

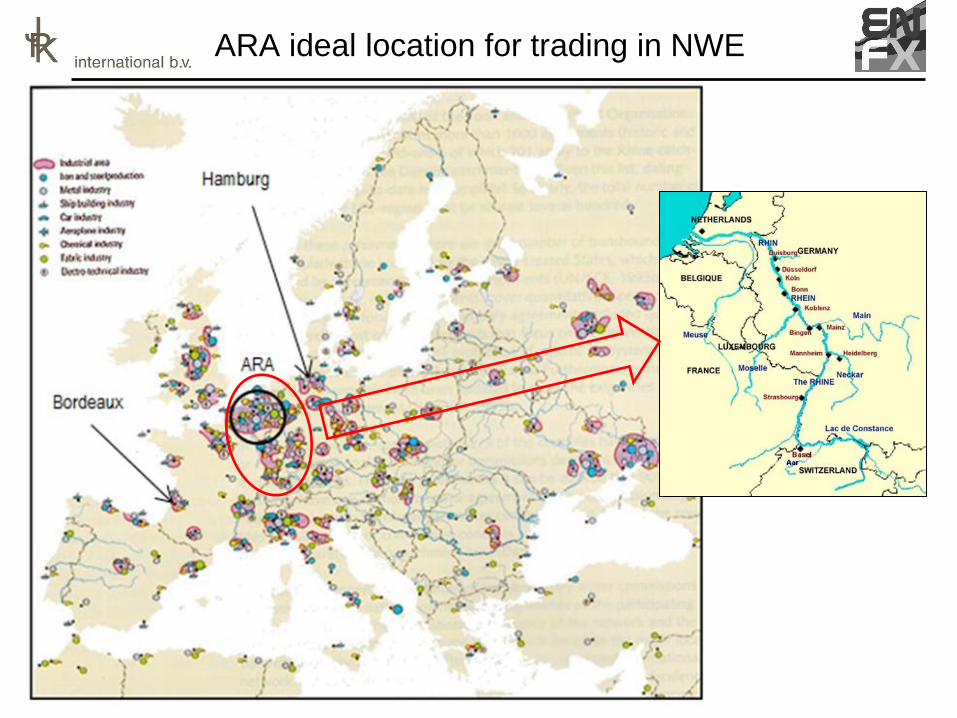

ARA ideal location for trading in NWE

ARA: key benefits

• Ideal topographical position in NWE:

– North Sea oil fields

– Large consumer markets in Benelux, Germany, France, Switzerland and UK

– Highly industrialized area and hinterland

– Good logistics: sea ports, Rhine & canals

• Large oil infrastructure: refineries + tank terminals

• Global trading hub, links to: Med, USA, Caribbean, South-

America, West Africa, the Mid East and the Far-East

• Liquid physical oil products market and oil derivatives market

• ICE Europe futures exchange and OTC swap markets for

hedging physical positions

• Brent crude, a worldwide oil pricing benchmark

EIA stocks: PADD 1 and 3