Embed Size (px)

Citation preview

Regenerating Hardcore Brownfield Sites Seminar

Urban Regeneration: overview of research at

University of UlsterStanley McGreal

Built Environment Research InstituteUniversity of Ulster

Regeneration Issues

Definitions Reversing social, economic and physical decline in towns and cities where market forces alone will not suffice.

Creating sustainable communities, raising value, promoting entrepreneurialism and developing innovative ways of attracting investment.

Output EvaluationsNumber of houses built, floor space developed, land reclaimed, jobs created and investment secured.

Access to services, community well-being, crime, economic deprivation, education, health, housing, physical environment, work deprivation.

Mixed-Use shemes and brownfield developmentFundamental to the sustainability of regeneration schemes driven by a confluence of planning policy, social, economic and political pressures

Attracting Private Sector Investment into Regeneration

Focus on property-led regeneration

Barriers to private sector investment

Mechanisms and incentives used

Issues of transparency – investment returns

Investment vehicles

Private sector investors lacked confidence in returns received from regeneration investments

Lack of performance data acted as a disincentive to invest

Varying perceptions of investors v non-investors

Quantification of returns on a time series basis to aid transparency

Benchmarking of regeneration performance

1998 Study for Joseph Rowntree Foundation Attracting Private Investment into Regeneration

Approach used: “bottom-up” based on policy initiatives, areas and properties

2 approaches to index construction:

total returns index - IPD approach beacon index - CBRE approach

Facilitated benchmarking with prime commercial property market indices

2003 Study: Construction of a regeneration performance index (ESRC, ODPM and RICS)

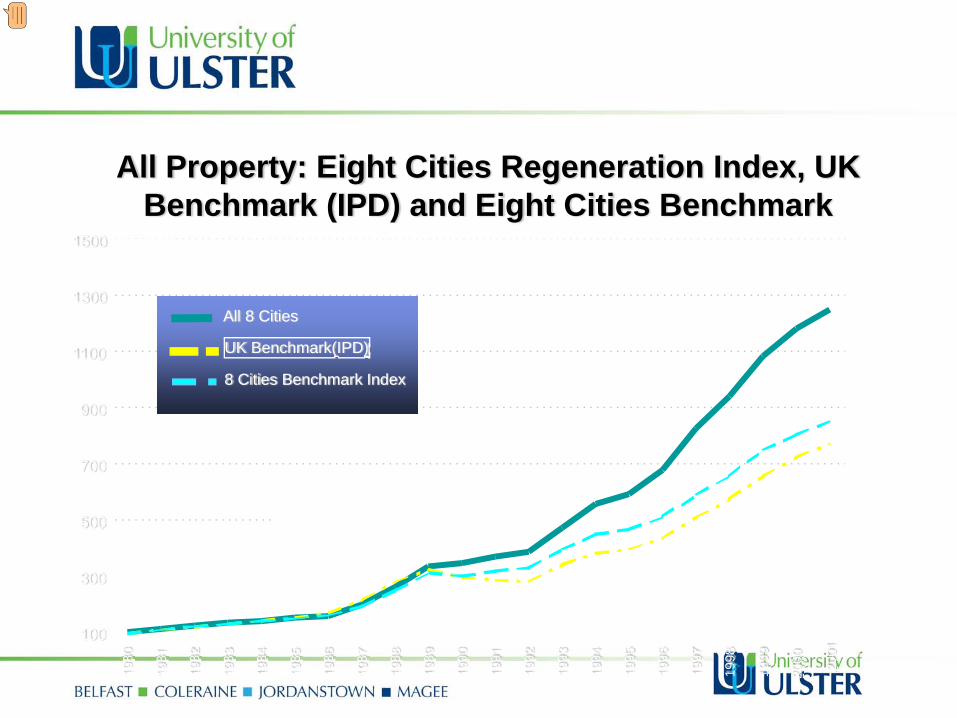

All Property: Eight Cities Regeneration Index, UK Benchmark (IPD) and Eight Cities Benchmark

100

300

500

700

900

1100

1300

1500

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000 2001

All 8 Cities

UK Benchmark(IPD)

8 Cities Benchmark Index

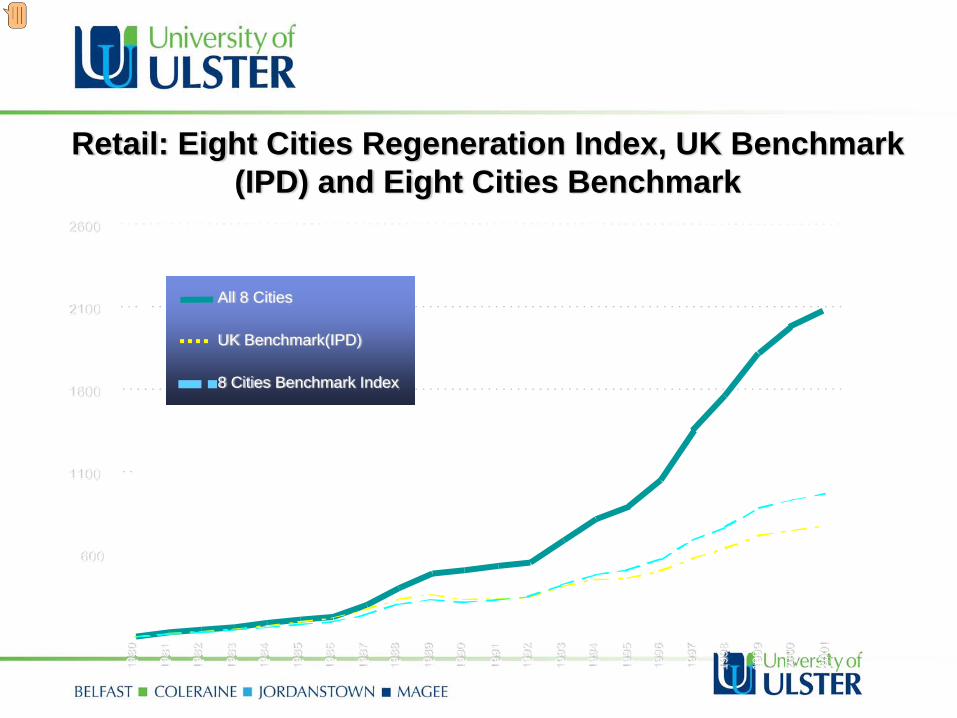

Retail: Eight Cities Regeneration Index, UK Benchmark (IPD) and Eight Cities Benchmark

100

600

1100

1600

2100

2600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

All 8 Cities

UK Benchmark(IPD)

8 Cities Benchmark Index

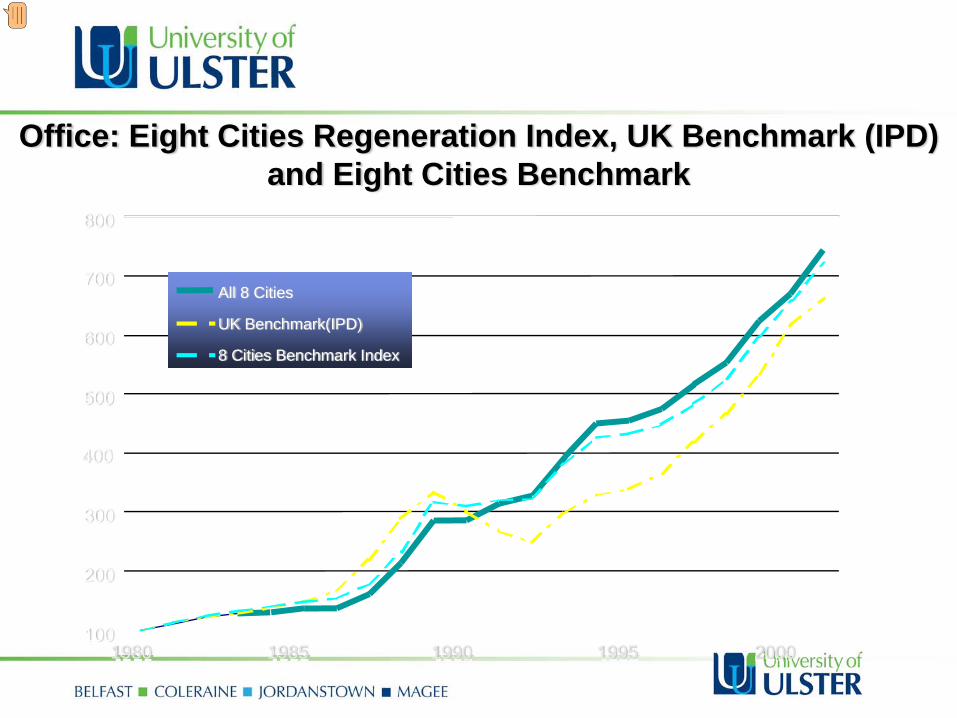

Office: Eight Cities Regeneration Index, UK Benchmark (IPD) and Eight Cities Benchmark

100

200

300

400

500

600

700

800

All 8 Cities

UK Benchmark(IPD)

8 Cities Benchmark Index

1980 1985 1990 1995 2000

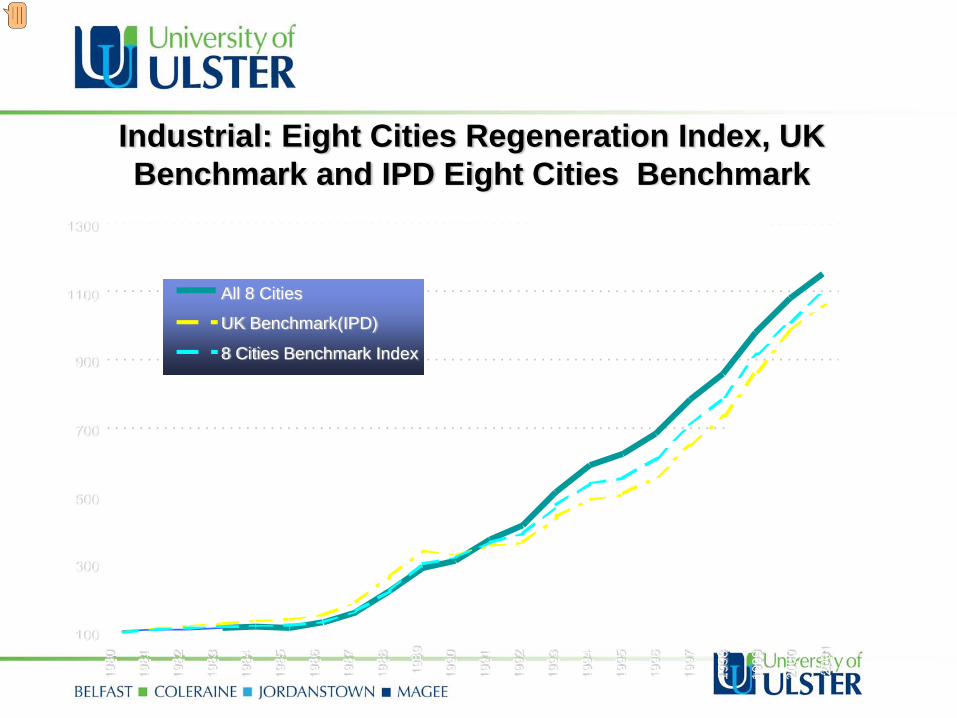

Industrial: Eight Cities Regeneration Index, UK Benchmark and IPD Eight Cities Benchmark

100

300

500

700

900

1100

1300

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

All 8 Cities

UK Benchmark(IPD)

8 Cities Benchmark Index

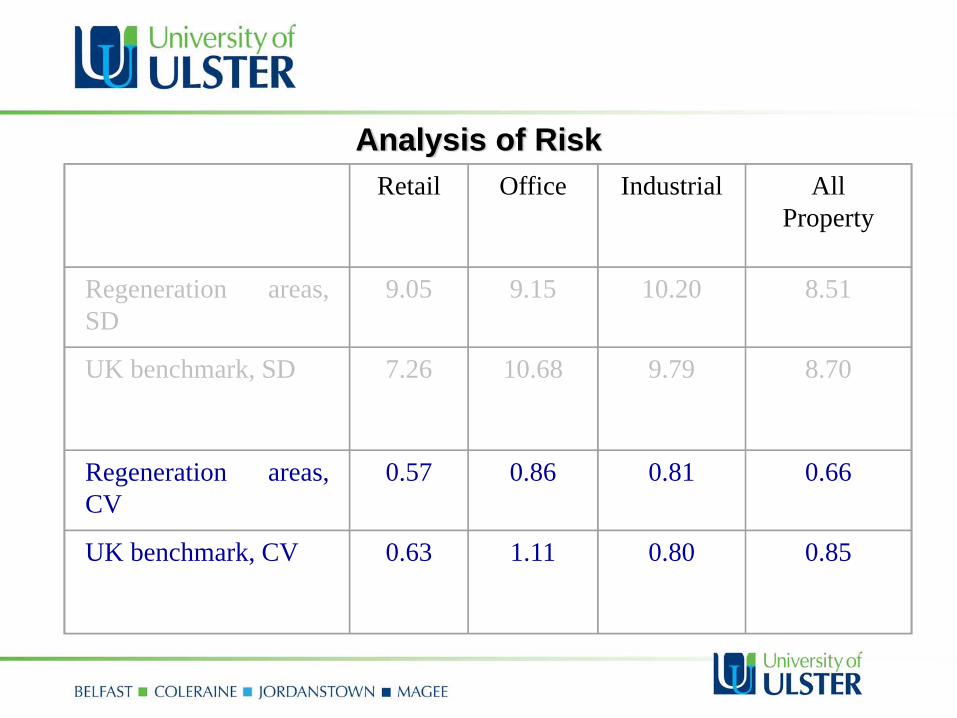

Retail Office Industrial All Property

Regeneration areas,SD

9.05 9.15 10.20 8.51

UK benchmark, SD 7.26 10.68 9.79 8.70

Regeneration areas,CV

0.57 0.86 0.81 0.66

UK benchmark, CV 0.63 1.11 0.80 0.85

Analysis of Risk

Regeneration property outperforming national & local benchmarks.

Systematic under-pricing of regeneration markets symptomatic of the information deficit

Sector differences highlight the strong retail performance

Misinformation regarding perceptions of regeneration risk

Maturing markets reflect success of regeneration policy

What were the Key Findings?

2006 Study: Institutional investment in regeneration (IPF, BPF, EP)

Approach: top UK investment institutions

Cross asset perspective: bonds, equityventure capital, securitised vehicles etc

Expectations of asset return, 3/5 year + longer time horizonsRisk tolerancesNature of security offeredAlternative financial models

Regeneration Investment Opportunities: Cross-asset perspective 1

Property has strongest linkages with institutional investment

New opportunities sought in brownfields, additional 4% return sought from development but higher risk premium of order of 3-4%

Institutions display growing appetite for long maturity bonds

20 year regeneration/infrastructure bond would be attractive to bonds/fixed income asset class - an alternative vehicle to increase exposure to the sector

Key issue is financing the coupon payments in the early years of regeneration/infrastructure with negative capital flows

Regeneration Investment Opportunities: Cross-asset perspective 2

Recognition that equities are less likely to yield regeneration opportunities than property or bonds

Introduction of REITs is perceived to offer significant investment opportunities going forward in time

Property companies developing and investing across a number of schemes could prove attractive from a diversification perspective

Potential for private equity through PFI, similar to mezzanine funds in terms of cash flow characteristics

Hedge funds have an open mind on regeneration investment opportunities/focus on the merits of each project in terms of cash flow and covenant strength

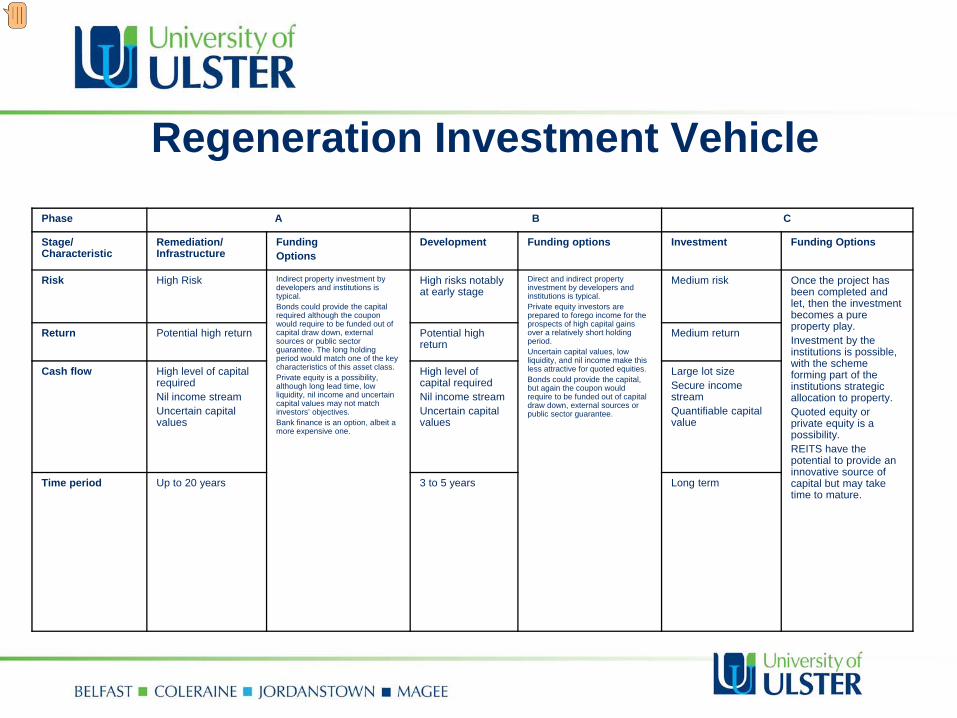

Regeneration Investment VehiclePhase A B C

Stage/ Characteristic

Remediation/ Infrastructure

Funding Options

Development Funding options Investment Funding Options

Risk High Risk Indirect property investment by developers and institutions is typical.Bonds could provide the capital required although the coupon would require to be funded out of capital draw down, external sources or public sector guarantee. The long holding period would match one of the key characteristics of this asset class.Private equity is a possibility, although long lead time, low liquidity, nil income and uncertain capital values may not match investors’ objectives.Bank finance is an option, albeit a more expensive one.

High risks notably at early stage

Direct and indirect property investment by developers and institutions is typical.Private equity investors are prepared to forego income for the prospects of high capital gains over a relatively short holding period.Uncertain capital values, low liquidity, and nil income make this less attractive for quoted equities.Bonds could provide the capital, but again the coupon would require to be funded out of capital draw down, external sources or public sector guarantee.

Medium risk Once the project has been completed and let, then the investment becomes a pure property play. Investment by the institutions is possible, with the scheme forming part of the institutions strategic allocation to property.Quoted equity or private equity is a possibility.REITS have the potential to provide an innovative source of capital but may take time to mature.

Return Potential high return Potential high return

Medium return

Cash flow High level of capital requiredNil income streamUncertain capital values

High level of capital requiredNil income streamUncertain capital values

Large lot sizeSecure income streamQuantifiable capital value

Time period Up to 20 years 3 to 5 years Long term

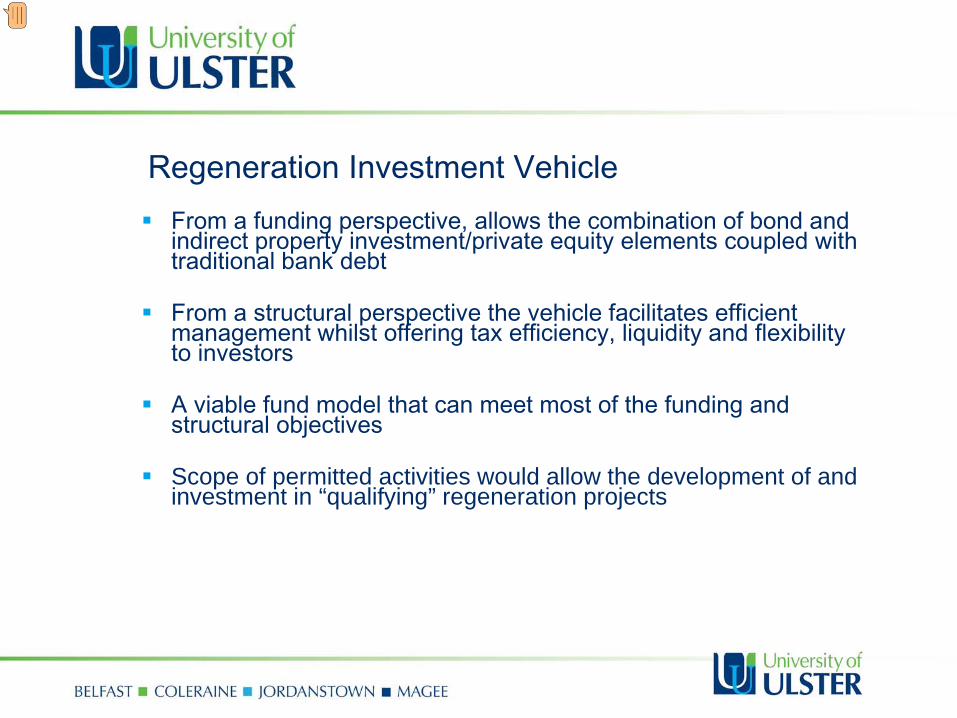

Regeneration Investment Vehicle From a funding perspective, allows the combination of bond and indirect property investment/private equity elements coupled with traditional bank debt

From a structural perspective the vehicle facilitates efficient management whilst offering tax efficiency, liquidity and flexibility to investors

A viable fund model that can meet most of the funding and structural objectives

Scope of permitted activities would allow the development of and investment in “qualifying” regeneration projects

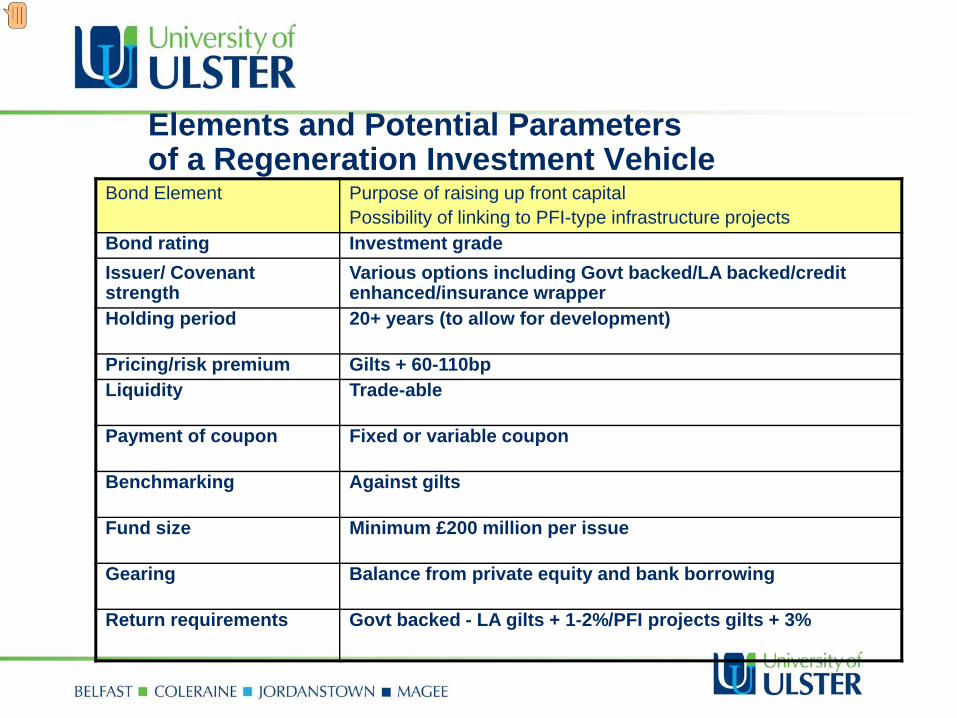

Elements and Potential Parameters of a Regeneration Investment Vehicle

Bond Element Purpose of raising up front capitalPossibility of linking to PFI-type infrastructure projects

Bond rating Investment gradeIssuer/ Covenant strength

Various options including Govt backed/LA backed/credit enhanced/insurance wrapper

Holding period 20+ years (to allow for development)

Pricing/risk premium Gilts + 60-110bp Liquidity Trade-able

Payment of coupon Fixed or variable coupon

Benchmarking Against gilts

Fund size Minimum £200 million per issue

Gearing Balance from private equity and bank borrowing

Return requirements Govt backed - LA gilts + 1-2%/PFI projects gilts + 3%

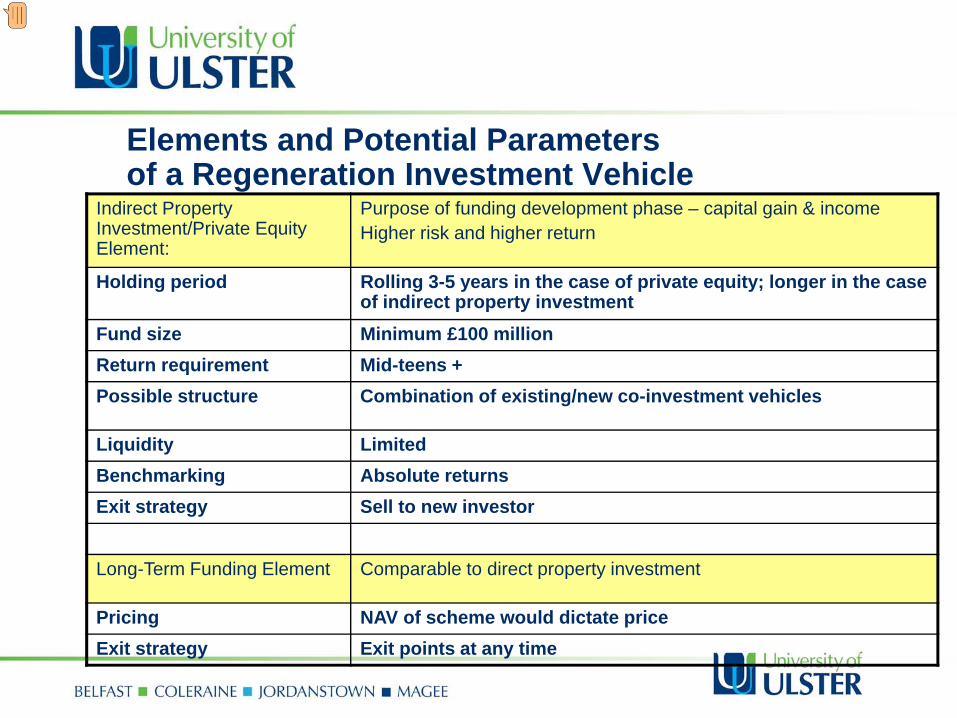

Elements and Potential Parameters of a Regeneration Investment Vehicle

Indirect Property Investment/Private Equity Element:

Purpose of funding development phase – capital gain & incomeHigher risk and higher return

Holding period Rolling 3-5 years in the case of private equity; longer in the case of indirect property investment

Fund size Minimum £100 millionReturn requirement Mid-teens +Possible structure Combination of existing/new co-investment vehicles

Liquidity LimitedBenchmarking Absolute returnsExit strategy Sell to new investor

Long-Term Funding Element Comparable to direct property investment

Pricing NAV of scheme would dictate priceExit strategy Exit points at any time

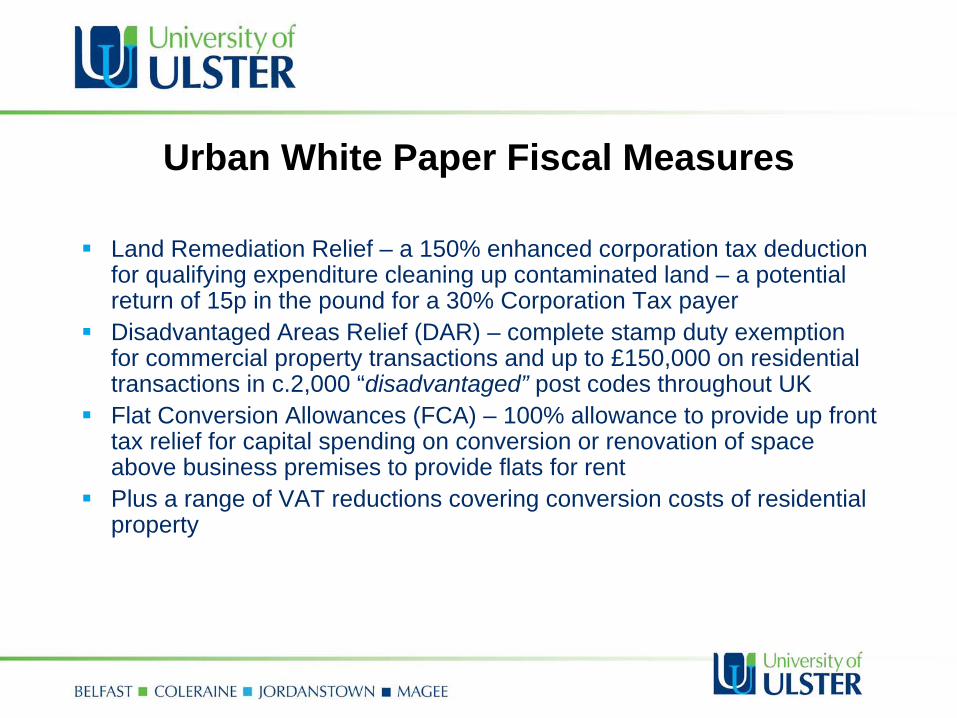

Urban White Paper Fiscal Measures

Land Remediation Relief – a 150% enhanced corporation tax deduction for qualifying expenditure cleaning up contaminated land – a potential return of 15p in the pound for a 30% Corporation Tax payerDisadvantaged Areas Relief (DAR) – complete stamp duty exemption for commercial property transactions and up to £150,000 on residential transactions in c.2,000 “disadvantaged” post codes throughout UKFlat Conversion Allowances (FCA) – 100% allowance to provide up front tax relief for capital spending on conversion or renovation of space above business premises to provide flats for rentPlus a range of VAT reductions covering conversion costs of residential property

Tax Credits – some issues that need to be addressed

How are they designed? Who designs them?How does one know of their existence?Ease, Transparency, Scope and Certainty of them?How are they measured?Have they caused a change in behaviour? Is there additionality or deadweight?Over what period are they evaluated?What barriers prevent their uptake?

LRR – Some Conclusions

Knowledge of LRR outside the developer community was patchy at time of undertaking the studyIncreased use will mean increasing cost to HMRCBrownfield development is contingent to property development in generalLRR is one aspect in the consideration of how to clean up sitesThe vast majority of sites are judged on commercial profitability rather than tax incentivesLRR reckoned to be less than 1.5% of total development costsLocal authorities are major players in terms of ownership, clean up and being development partnersCentral government should market LRR more effectively, particularly with local authorities

2009 Current State of Regeneration in the UK (IPF)

New generation of regionally focussed Regeneration Investment Vehicles (RIVs)

Property Regeneration Partnerships/Asset Backed Structures: Regional Development Agencies (RDAs) commit a portfolio of land/property for regeneration matched by an investment partner.

The devolution in regeneration decision making has seen the Asset Backed Structure rolled out to local authority level – Local Asset Backed Vehicles (LABVs) eg “Croydon Council Urban Regeneration Vehicle”

The LABV model will be complemented by the introduction of Community Infrastructure Levy (CIL) and Supplementary Business Rates (SBR).

Property Market Downturn: Implications for Regeneration

Investor appetite for risk has receded in the wake of the current property market downturn – as a result regeneration schemes are likely to find it difficult to attract investment in the current climate.

Regeneration investment vehicles which include a public sector partner may however prove an attractive option for investors as they provide reassurance and reduce risk.

Major development and infrastructure projects have been shelved amidst the ongoing uncertainty in both the property and financial markets.

Government proposals to increase pubic sector spending on major projects including social housing provision may provide some stimulus for regeneration schemes.

Future Research

Examination of Regeneration Investment Vehicles in the UK drawing comparison with international models such as TIFs.

International models of best practice: Empowering local authorities to make strategic regeneration decisions.

The retail sector along with house price growth were fundamental to the performance and commercial viability of regeneration schemes – what are the prospects in a post-recessionary environment?

What is the future prospects for large scale commercial property development in the UK including regeneration schemes.