Embed Size (px)

Citation preview

OKLAHOMAOILANDGASINDUSTRYTAXATION

ComparativeEffectiveTaxRatesintheMajorProducingStates

January2018

Page|1 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

ContentsI. Introduction.........................................................................................................................................2

II. SeveranceTaxes...................................................................................................................................4

RecentTaxLawChanges.................................................................................................................4

OklahomaSeveranceTaxPayments...............................................................................................4

OklahomaEffectiveSeveranceTaxRate.........................................................................................7

OklahomaVersusOtherProducingStates......................................................................................8

StateTrendsinSeveranceTaxRates.............................................................................................10

III. AdValoremTaxes...............................................................................................................................11

IV. MeasuringtheBroaderTaxContributionofOil&Gas......................................................................16

PersonalIncomeTaxesandOilandGasEarnings.........................................................................17

OilandGas-RelatedSalesTax.......................................................................................................22

OverallEffectiveTaxRate.............................................................................................................25

EffectofRecentTaxLawChange..................................................................................................29

HigherSeveranceTaxRateScenarios...........................................................................................29

FurtherStudy................................................................................................................................31

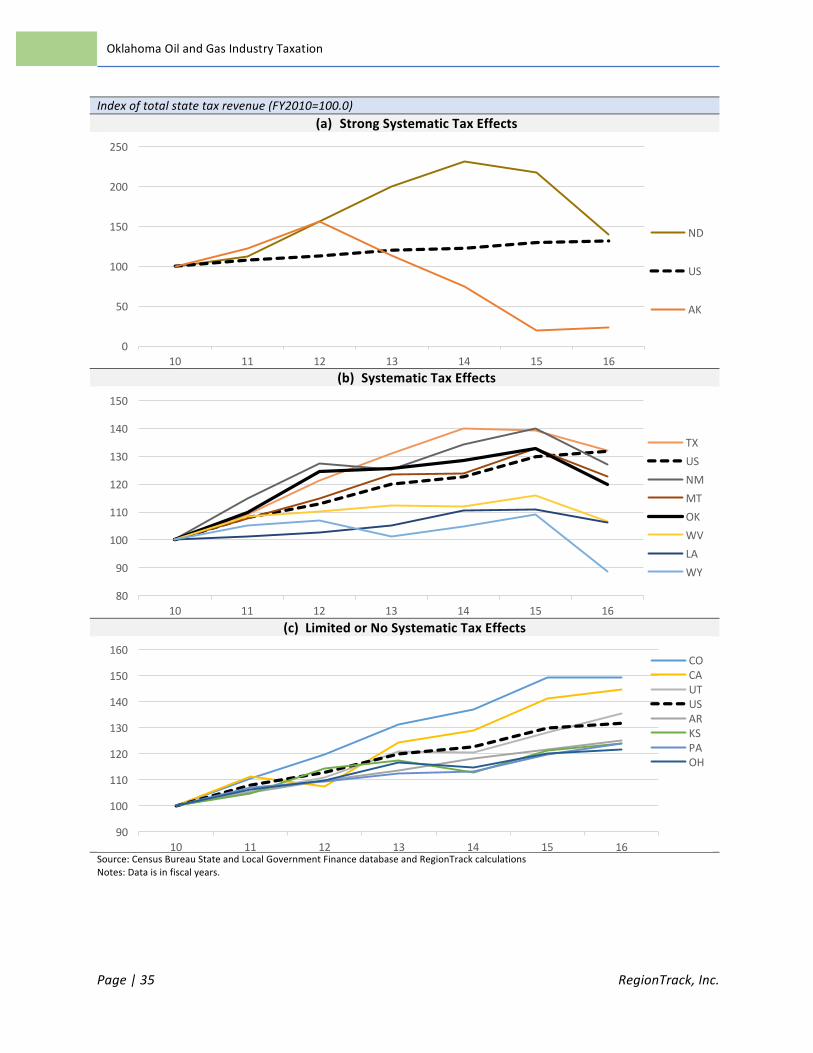

V. SystematicLaborMarketandTaxEffects..........................................................................................32

SystematicLaborMarketEffects...................................................................................................32

SystematicTaxRevenueEffects....................................................................................................32

SystematicOilandGasRiskinOklahoma.....................................................................................33

VI. Appendix............................................................................................................................................36

VII. References.........................................................................................................................................40

VIII. Endnotes............................................................................................................................................41

Page|2 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

OklahomaOilandGasIndustryTaxation

I. IntroductionThisreportprovidesestimatesoftheeffectivetaxburdenfacedbytheoilandgasindustryinOklahomaandfifteenothermajorenergy-producingstates.Evaluationsofoilandgastaxburdenaretypicallyrestrictedtotheroleofseverancetaxesandadvaloremtaxesrelatedtooilandgasproduction.Dataisreadilyavailableforthesetaxesandtheycapturemuchofthedirecttaxcontributionfromoilandgasproduction.However,thesetwotaxstreamsdonotcapturethetaxcontributionoftheoilandgasindustrymorebroadly.Theindustryanditsemployeesmakesignificantcontributionstoseveralothermajortaxstreamsaswell.InOklahoma,themostimportantamongthesearepersonalincometaxandsalestax,twoofthelargestsourcesofrevenuetostateandlocalgovernment.Othersmallertaxstreamsincludecorporateincometax,franchisetax,motorvehicletax,andmotorfueltax.

Whendoingcross-statecomparisons,theuseofanarrowsetoftaxescanproduceagrosslymisleadingviewoftheoveralltaxcontributionoftheoilandgasindustry.Themajorenergy-producingstatesassessarangeoftaxesandrelyonthemtovaryingdegrees.Someproducingstatesdonotlevyapersonalincomeorsalestaxandrelymuchmoreheavilyonseveranceandadvaloremtaxestofundstateandlocalgovernmentspending.Evenamongstatesthatdolevyincomeandsalestaxes,theeffectiveratesvarygreatly.Thesizeoftheoilandgasindustryvariesaswell,asstateswithalargeoilandgasemploymentbasereceiverelativelymoretaxrevenuefromtheindustry.Drilling-activestatesalsotendtoreceivesignificantcurrenttaxrevenuefromincreasinglycapital-intensivewellsrelativetoproducingstateswithlittledrillingactivity.

ThepurposeofthisreportistoprovideabroadercomparisonofthetaxburdenfacedbytheoilandgasindustryinOklahoma.Estimatesofthecombinedeffectivetaxrateforseverance,advalorem,personalincome,andsalestaxareprovidedforOklahomaandfifteenothermajorproducingstates.Whilethisdoesnotprovideanexhaustivereviewofthetotaltaxpaymentsmadebytheindustry,thesetaxescomprisethetwolargestsourcesofstateandlocaltaxesinOklahomaandcapturethemajortaxestypicallyderivedfromoilandgasdrillingandproductionactivity.

Inthefirstsectionofthereport,historicalseverancetaxpaymentsinOklahomaareexamined,andupdatedestimatesoftheeffectiverateinOklahomaandotheroilandgas-producingstatesareprovided.TheinfluenceofseverancetaxratechangesandproductionvaluationchangesonseverancetaxpaymentsinOklahomaisalsoexamined.Finally,theprojectedeffectofrecentincreasesinseverancetaxratesonrevenueprojectionsinthecurrentandnextfiscalyearareevaluated.

ThesecondsectionprovidesestimatesofannualadvaloremtaxpaymentsandeffectiveadvaloremtaxratesforOklahomaandthesampleofproducingstates.Acombinedeffectivetaxrateincludingbothseveranceandadvaloremtaxesisthenestimatedforthesixteenstates.

Page|3 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

ThethirdsectionbroadenstheanalysisoftheOklahomaoilandgasindustrytaxburdentopersonalincomeandsalestaxes.Anoveralleffectiveratethatincludesseverance,advalorem,personalincome,andsalestaxesisestimatedforOklahomaandtheotherfifteenstatesinthesample.Oklahoma’soveralleffectiverateisthenevaluatedunderboththerecentincreaseintheseverancetaxrateandpotentialadditionalincreasesintherate.

Thefourthandfinalsectionofthereporthighlightstheoverallsensitivityofthetotaltaxbaseinthesixteenstatestofluctuationsintheoilandgasindustryintherecentenergypricecycle.ThisprovidesabetterperspectiveontheoverallsensitivityoftotaltaxrevenueinOklahomarelativetotheotherproducingstates.Italsohighlightsthedirectandindirectinfluenceofoilandgasactivityontheoverallvolatilityofstatetaxrevenue.Producingstateswithanoveralleconomiccyclethatremainshighlysensitivetooilandgasactivitymustgivespecialconsiderationtoboththedirectandindirectactivityinfluencedbytaxpolicydecisions.

ThefindingsofthereporthaveimportantimplicationsforOklahomapolicymakerssettingtaxpolicyinthestate.WhiletheFY2016effectivetaxrateinOklahomaranks12thamongthe16thlargestproducingstatesbasedsolelyonseveranceandadvaloremtaxes,theoveralleffectiveraterisesto8thwhenpersonalincomeandsalestaxesareconsidered.Manyofthemajorproducingstateshaveeithernopersonalincometaxorverylowsalestaxrates,orboth,andareheavilyreliantupontraditionalseveranceandadvaloremtaxestofundstateandlocalgovernment.Oklahoma,ontheotherhand,leviesrelativelylowseveranceandadvaloremtaxesbutreliesheavilyuponabove-averagesalesandpersonalincometaxespaidbytheindustry.

Moreimportantly,therecentlyimplementedincreaseinthestate’sseverancetaxrateispushingthestate’soveralleffectivetaxrateonoilandgasproductionmuchhigherthisfiscalyearandnext.BasedonOklahomaTaxCommissionforecasts,theseverancetaxrateincreaseisprojectedtopushthestate’soveralleffectivetaxrateto5thhighestinthecurrentfiscalyear(FY2018),risingabovetheoverallrateleviedbydominant-producerTexas.

Furtherincreasesinseverancetaxrateswouldraisethestate’soveralleffectivetaxratetoamongthehighestleviedbythemajoroilandgas-producingstates.AscenarioofshiftingallprojectedFY2019productioninthe2%taxbrackettoa4%severancetaxratewouldgiveOklahomathe3rdhighestoveralleffectivetaxrate.AscenarioofshiftingalloilandgasproductioninFY2019toa7%severancetaxratewouldgiveOklahomathe2ndhighestoveralleffectivetaxrateamongthesixteenlargestproducingstates.

Page|4 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

II. SeveranceTaxesSeverancetaxeshavelongbeenleviedonoilandgasproductioninOklahomaandareakeysourceoffundingforstateandlocalgovernment.SometimesreferredtoasgrossproductiontaxesinOklahoma,theyareoftenviewedastheprimarytaxpaidbytheoilandgasindustry.1TheanalysisinthissectionexaminesrecentchangesinseverancetaxratesinOklahomaandtheeffectontotalseverancetaxpayments.Theeffectiveannualseverancetaxrateisthencalculatedforthestatethepasttwodecades.Effectiveratesarecalculatedforfifteenadditionaloil-andgas-producingstatesintheFY2012toFY2017period.Finally,effectiveratesinOklahomaareevaluatedunderOklahomaTaxCommissionprojectionsofseverancetaxrevenuebasedonrecentlyincreasedseverancetaxrates.

RecentTaxLawChanges.Historically,Oklahomahasassesseda7percentmarginalseverancetax

rate(beforedeductions,exemptions,andrebates)onmostcrudeoilandnaturalgasproduction.

EffectiveJuly2011,theLegislaturechangedtheincentiveinplaceforhorizontally-drilledwellsandcertaindeepwells.Inlieuofarebate,theseverancetaxratewaschangedto1%for48monthsonproductionfromnewhorizontally-drilledwellsand4%fordeepwells.2

In2014,theLegislaturestreamlinedoilandgastaxationfurther,andseverancetaxrateswerechangedonceagain.AllwellsdrilledafterJuly2015aresubjecttoataxof2%forthefirst36monthsofproduction,withtheraterevertingto7%thereafter.Somedeepwellsarestilltaxedat4%for48months,revertingto7%thereafter.Wellstaxedundertheprevious1%rateforhorizontalwellsretainedtheiroriginaldatetorevertto7%.Asaresult,wellsinOklahomaarecurrentlytaxedateither1%,2%,4%,or7%,withallproductionultimatelytransitioningto7%.

Alongstandingexcisetaxof0.095%ofproductionvalueoncrudeoilandnaturalgasproductionisstillleviedaswell.

OklahomaSeveranceTaxPayments.Figure1providesanoverviewoftotalannualseverancetaxpaymentsmadebyOklahomaoilandgasproducersthepasttwodecades.Severancetaxreceiptsaveragedapproximately$385millionannuallybetweenFY1997andFY2002beforerisingsubstantiallyalongwithbothenergypricesandproductionbeginninginFY2003.Paymentsaveragedalmost$1billionannuallybetweenFY2005andFY2012,boostedbyhighpricesforbothcrudeoilandnaturalgas.

Totalseverancetaxreceiptsaveraged$503millionannuallyfromFY2013throughFY2017.Thelowinreceiptsof$331millioninFY2016reflectsseverancetaxrelieffromtheLegislatureforhorizontally-drilledwellscoupledwithanunusuallyadversesetofindustryconditions.InFY2016,severancetaxreceiptsweredrivendownwardbyacollapseincrudeoilprices($38/bblaverage),anearly20-yearlowinnaturalgasprices($2.26/mBtuaverage),relativelyflatstatenaturalgasproduction,andadeclineinstatecrudeoiloutput.FromFY2014toFY2016,thetotalvalueofcrudeoilandnaturalgasproducedinthestatedeclinedbynearlyhalftothelowestlevelinmorethanadecade.Thestatesimilarlyremainedmiredinanearlytwo-yearstate-levelrecessiontiedtotheoilandgasindustryslowdown.

Page|5 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Totalseverancetaxreceiptsreboundedby28%inFY2017to$425millionasmarketpricesforcrudeoilandnaturalgasrecoveredfromrecentlows.Themostrecenttaxlawchangeisalsoliftingseverancetaxesinthecurrentfiscalyear(FY2018)aswellspreviouslytaxedateitherthe1%,2%,or4%ratearenowmovingintothe7%marginaltaxbracket.Asaresult,currentforecastsbytheOklahomaTaxCommissionsuggestthatseverancetaxreceiptswillreboundmuchfurtherinthenearterm.December2017projectionsbytheOklahomaTaxCommissionsuggestareboundintotalseverancetaxreceiptsto$639millioninthecurrentfiscalyearand$722millioninFY2019.3

TheshiftingshareofproductionateachseverancetaxrateforbothcrudeoilandnaturalgasisdetailedinFigure2.OklahomaTaxCommissionsforecastssuggestthat70.9%oftotalstateproductionwillbetaxedat7%inFY2018,risingto81.5%byFY2019.Relativelysmallsharesofproductionwillbetaxedateitherthe1%or4%legacyratesinFY2018.Noproductionofeithercrudeoilornaturalgasisexpectedtoremainatthe1%or4%ratesinFY2019.

Figure2.OklahomaSeveranceTaxRevenueProjections

TaxRate

CrudeOil NaturalGas Total

FY2018 FY2019 FY2018 FY2019 FY2018 FY2019

1% $3,223,000 $0 $3,662,000 $0 $6,885,000 $0

2% 74,865,000 76,497,000 51,875,000 56,866,000 126,740,000 133,363,000

4% 24,123,000 0 28,269,000 0 52,392,000 0

7% 211,740,000 290,053,000 240,991,000 298,544,000 452,731,000 588,597,000

Total $313,951,000 $366,550,000 $324,797,000 $355,410,000 $638,748,000 $721,960,000Source:OklahomaTaxCommission.StateofOklahomaFY2018-19RevenueCertification.December20,2017.Notes:Petroleumexcisetaxpaymentsof0.095%areincludedintheseprojections.

Figure1.OilandGasSeveranceTaxPayments–Oklahoma(FiscalYear)

Source:OklahomaTaxCommissionNotes:Includesbothseverancetaxesandthe0.095%petroleumexcisetax.

351310

221

389

671

373

582

692

860

1,136

986

1,141

917869

978895

529

686

560

331

425

639722

0

200

400

600

800

1,000

1,200

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

$Millions

Page|6 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

TaxChangesApportionedtoValueandRateChanges.Itisimportanttounderstandthedegreetowhichtaxlawchangesversusshiftsinthevalueofproductionhavedrivenrecentyear-to-yearchangesinstateseverancetaxpayments.Figure3apportionstheannualchangeinseverancetaxes(panelA)intochangesduetoproductionvalueandchangesduetotaxrate(panelB).

Mostoftheeffectiveshiftfromthetaxratechangein2011wasfullyabsorbedbyFY2013.NosignificantchangesduetotaxrateshavetakenplacesinceFY2014,withweakseverancetaxrevenueinFY2015andFY2016tracedalmostfullytodecliningproductionvalue.

HigherproductionvaluecontributednearlyallthenetgainintaxpaymentsinFY2017.GoingforwardintoFY2018andFY2019,taxratechangesareexpectedtocontributenearlyallnewseverancetaxrevenuegrowth.Approximately$300millioninnetnewannualseverancetaxrevenueisprojectedthroughFY2019relativetoFY2017,mostlyfromtaxrateincreases.

Figure3.OklahomaSeveranceTax–SourceofAnnualChanges(FiscalYears)(A) AnnualSeveranceTaxChange

(B) AnnualChangeApportionedtoProductionValueandEffectiveTaxRateChanges

Source:OklahomaTaxCommissionandRegionTrackcalculations

-41 -89

168

282

-297

208

110168

276

-150

155

-224

-48

109

-83

-366

157

-126

-229

94

214

83

-400

-300

-200

-100

0

100

200

300

400

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

$Millions

-750

-500

-250

0

250

500

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Millions

ValueofProductionChange

EffectiveSeveranceTaxRateChange

Page|7 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

OklahomaEffectiveSeveranceTaxRate.Figure4providesestimatesoftheeffectiveseverance

taxrateinOklahomathepasttwodecades.ProjectionsforFY2018andFY2019areprovidedtoillustratetheexpectedchangeintherateinresponsetorecentlyenactedtaxlawchanges.SeeFigureA1intheAppendixfordetailedcomponentsoftheratecalculations.

Methodology.Theeffectiverateiscalculatedastotalseverancetaxesdividedbythetotalmarketvalueofoilandgasproduction.ThevalueofproductioniscalculatedusingEnergyInformationAdministration(EIA)estimatesofmonthlyproductionwhichareconvertedtofiscalyears.ThepriceofcrudeoilisthefirstpurchasepriceatthestatelevelprovidedbyEIA.Thisprovidespriceestimatesthatcloselytrackstate-levelpricesusedforseverancetaxreportingpurposesandcanbeusedinmakingconsistentcross-statecomparisons.ThevalueofnaturalgasproductionisdeterminedusingtheHenryHubspotpriceofnaturalgas.Thesepricesforcrudeoilandnaturalgasarealsousedinthecalculationofproductionvaluesincross-statecomparisonsforconsistency.4

HistoricalRates.TheeffectiveseverancetaxrateinOklahomafluctuatedaroundanaverageof6.0%betweenFY1997andFY2009.Ratesthenbouncedhighertoanaverageof7.0%betweenFY2010andFY2012beforefallinginresponsetoseverancetaxrelieflegislation.Theratehasaveraged3.0%sinceFY2013,approximatelyhalfthe6.2%averageratefromFY1997toFY2012.ThesteepdeclineintheeffectiveratefromFY2012toFY2013reflects,inpart,theshiftinseverancetaxpolicyfromtheuseofarefundedrebatetoareducedseverancetaxrate.PriortoFY2011,severancetaxeswerecollectedandthenreturnedtotaxpayersinarrearsasrebates,whilethereplacementlegislationcollectsrevenuefromnon-exemptproductiononly.

Themostrecenttaxlawchangeswillproduceasignificantriseinthestate’seffectiveseverancetaxrate

Figure4.EffectiveSeveranceTaxRate–Oklahoma

Source:EnergyInformationAdministration,OklahomaTaxCommission,andRegionTrackcalculations

5.9% 5.7% 5.4%

6.1% 6.2% 6.3% 6.1% 6.4% 6.4%

6.1% 6.2%

5.3% 5.8%

7.0% 7.1% 6.9%

3.2% 3.2% 3.0% 2.9% 3.0%

4.4% 4.8%

0%

1%

2%

3%

4%

5%

6%

7%

8%

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Page|8 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

asproductiontransitionstothe7%taxbracket.BasedonOklahomaTaxCommissionforecastsforseverancetaxreceipts,theeffectiverateisprojectedtoriseto4.4%inFY2018and4.8%inFY2019.TheeffectiverateforecastisbasedonestimatesofflatproductionquantitiesforcrudeoilandnaturalgasinbothFY2018andFY2019,oilpricesof$47.49perbarrelinFY2018and$51.08perbarrelinFY2019,andnaturalgaspricesof$2.94inFY2018and$2.99inFY2019.

AsillustratedinFigure3,theprimarycontributortotheriseintheeffectiveseverancetaxrateinFY2018andFY2019willberisingtaxrates,withlittlecontributionfromrisingproductionvalue.

OklahomaVersusOtherProducingStates.Oklahoma’sFY2017effectiveseverancetaxrateis

comparedtofifteenadditionalenergy-producingstatesinFigure5.Thestatesinthesampleallrankamongthetoptenproducersofeithercrudeoilornaturalgas,orboth.Asagroup,theyrepresentthesixteenlargestproducingstatesbasedonvalueofproduction,witheachproducingatleast$1billionormoreincombinedvalueofcrudeoilandnaturalgasin2016.Thisprovidesforabroadrangeofcomparativeoilandgas-relatedtaxpoliciesacrosstheproducingstates.

Severancetaxesaredefinedastraditionalproductionorextractiontaxes,typicallybasedoneitherthevolumeormarketvalueofproduction.Thesetaxesvarywidelyacrossthestatesbutaregenerallylinkeddirectlytotheremovalofmineralsfromtheground.PaymentsforproductiononstatelandaregenerallyincludedwhileFederalpaymentsarenot.ExcludedareWyoming’sadvaloremtaxesbasedonproduction(whichareevaluatedinthenextsectiononadvaloremeffectiverates).Pennsylvania’simpactfeesareincludedasseverancetaxesintheinitialstageofthetaxrateanalysisbecausenoother

Figure5.EffectiveSeveranceTaxRate-16LargestProducingStates(FY2017)

Source:Variousstateoilandgasandtaxreportingagencies.Refertonotesattheendofthereportforlinkstoelectronicsources.CalculationsbyRegionTrack.Notes:Alldataarestatedonafiscalyearbasis.Theeffectiverateiscalculatedastotalseverancetaxesdividedbythetotalvalueofoilandgasproduction.Pennsylvania’seffectiverateincludesthestateimpactfeeinthisinitialstageoftheanalysis.

9.5%

8.4% 7.9%

4.5% 4.2%

3.8% 3.5% 3.0%

1.9% 1.5%

1.1% 1.0% 0.7% 0.7% 0.7% 0.0%

3.7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

MT ND NM LA TX WY WV OK KS AR PA CA OH CO UT AK 16-States

Page|9 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

taxesareassessedbythestateeitherdirectlyorindirectlyonproduction.

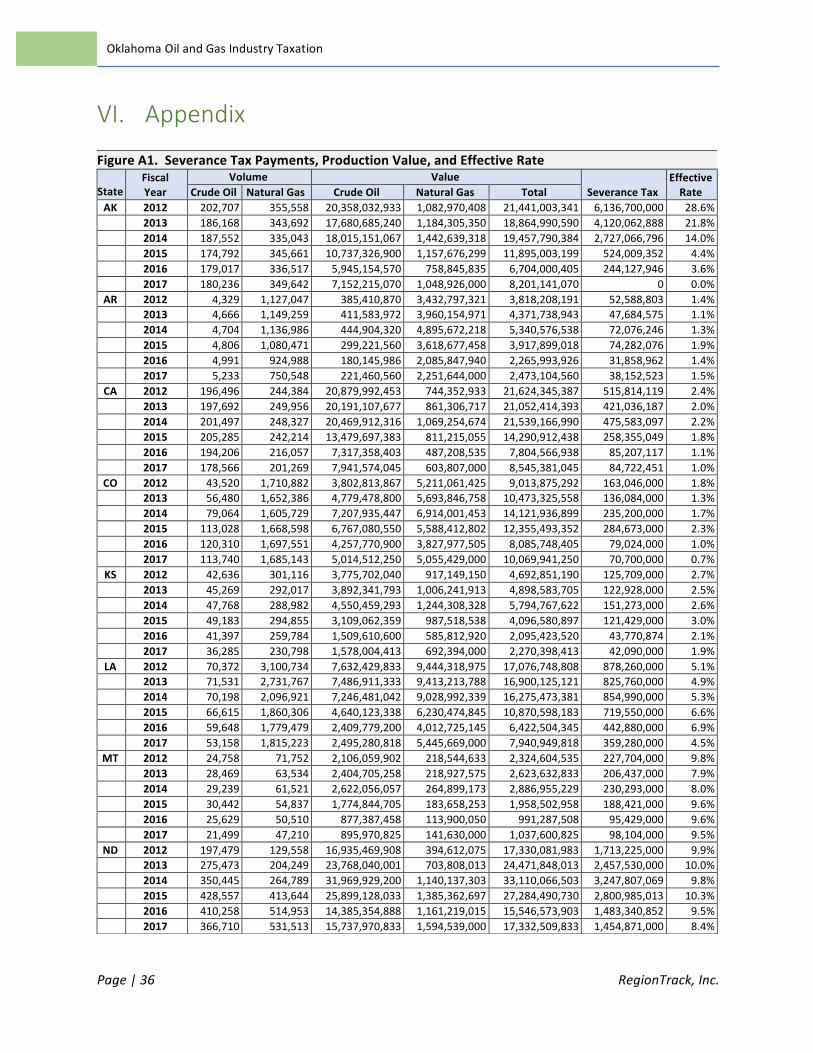

Avarietyofsourcesareusedtocollectseverancetaxdataforthesixteenstates.Theprimarysourcesarestatetaxreportingagenciesornaturalresourceadministrativeagencies.Sourcesavailableinelectronicformaredetailedinthenotestothereport.5FigureA1intheAppendixprovidessummarymeasuresunderlyingtheeffectiveseverancetaxratecalculationforeachofthesixteenstatesintheFY2012toFY2017period.Taxesarecalculatedbasedonthefiscalyearusedbyeachstate.6

Oklahoma’seffectiveseverancetaxrateis3.0%inFY2017,8thhighestamongthegroupandbelowthegroup’svalue-weightedaverageof3.7%.Thesimpleaverageofratesacrossthestatesis3.3%.Theoveralleffectiveseverancetaxrateforthegroupisalsoroughlyhalfthe6.6%effectiveratereportedinarecentstudyofIdahooilandgastaxation(Covenant,2016)coveringasmallersampleofnineproducingstates.

Threestates(Montana,NorthDakota,andNewMexico)compriseatoptierwithsignificantlyhighereffectiveratesofapproximately8%ormore.Thesestatesarecommonlyincludedincross-statereviewsofseverancetaxratesbutappearmoreasoutlierswhenviewedacrossabroadersetofproducingstates.

Oklahomaandfourotherstates(Louisiana,Texas,Wyoming,andWestVirginia)formamiddletierwitheffectiveratesbetween3%and4.5%.Texas,thenation’slargestproducerofbothcrudeoilandnaturalgas,hasa4.2%effectiverate,1.2%aboveOklahomaandone-halfpercentagepointabovethegroupweightedaverage.

Athirdtierofeightstates–Kansas,Arkansas,Pennsylvania,California,Ohio,Colorado,Utah,andAlaska–hasrelativelyloweffectiveseverancetaxratesbelow2%inFY2017.NeighboringKansasandArkansasbothhaveratesbetween1.5%and2%.Kansasprovidesa3.67%credittowardseverancetaxesforpropertytaxespaid,leavinganetmarginalrateof4.33%butaneffectiverateofonly1.9%.RapidlygrowinggasproducersPennsylvaniaandOhiohaveeffectiveratesofabout1%orless.Pennsylvania,thesecondlargestgasproducingstate,isincludedinthecomparisondespitehavingnodirectseverancetax.Itisincludedintheinitialstageoftheanalysisbasedonitsimpactfeeservingastheonlydirectproductioncostassessedbythestate.

California,thethirdlargestoilproducingstate,hasonlya1.0%effectiveseverancetaxrate.7Thestatehaslongassessednodirectseveranceoradvaloremtaxesatthestatelevel,butdoesallowlocaladvaloremtaxes.Thestateassessesonlyasmallfeebasedonthevolumeofproductionofcrudeoilandnaturalgas.

LargeandrapidlygrowingproducerColoradohasaneffectiveratebelow1.0%duetoanallowedoffsetofseverancetaxesbyadvaloremtaxpayments.Thisfunctionslargelyasanadvaloremtaxinlieuofseverancetaxpayments,oppositetherelationshipinplaceinOklahoma.

Page|10 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

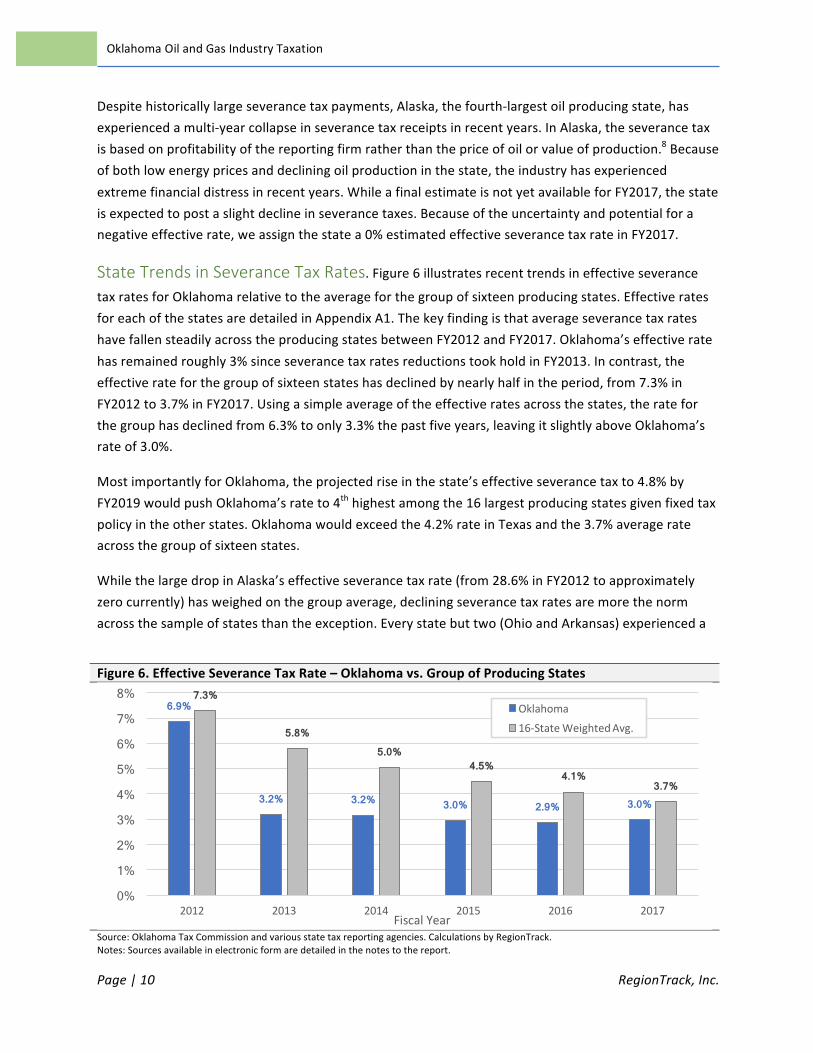

Despitehistoricallylargeseverancetaxpayments,Alaska,thefourth-largestoilproducingstate,hasexperiencedamulti-yearcollapseinseverancetaxreceiptsinrecentyears.InAlaska,theseverancetaxisbasedonprofitabilityofthereportingfirmratherthanthepriceofoilorvalueofproduction.8Becauseofbothlowenergypricesanddecliningoilproductioninthestate,theindustryhasexperiencedextremefinancialdistressinrecentyears.WhileafinalestimateisnotyetavailableforFY2017,thestateisexpectedtopostaslightdeclineinseverancetaxes.Becauseoftheuncertaintyandpotentialforanegativeeffectiverate,weassignthestatea0%estimatedeffectiveseverancetaxrateinFY2017.

StateTrendsinSeveranceTaxRates.Figure6illustratesrecenttrendsineffectiveseverancetaxratesforOklahomarelativetotheaverageforthegroupofsixteenproducingstates.EffectiveratesforeachofthestatesaredetailedinAppendixA1.ThekeyfindingisthataverageseverancetaxrateshavefallensteadilyacrosstheproducingstatesbetweenFY2012andFY2017.Oklahoma’seffectiveratehasremainedroughly3%sinceseverancetaxratesreductionstookholdinFY2013.Incontrast,theeffectiverateforthegroupofsixteenstateshasdeclinedbynearlyhalfintheperiod,from7.3%inFY2012to3.7%inFY2017.Usingasimpleaverageoftheeffectiveratesacrossthestates,therateforthegrouphasdeclinedfrom6.3%toonly3.3%thepastfiveyears,leavingitslightlyaboveOklahoma’srateof3.0%.

MostimportantlyforOklahoma,theprojectedriseinthestate’seffectiveseverancetaxto4.8%byFY2019wouldpushOklahoma’srateto4thhighestamongthe16largestproducingstatesgivenfixedtaxpolicyintheotherstates.Oklahomawouldexceedthe4.2%rateinTexasandthe3.7%averagerateacrossthegroupofsixteenstates.

WhilethelargedropinAlaska’seffectiveseverancetaxrate(from28.6%inFY2012toapproximatelyzerocurrently)hasweighedonthegroupaverage,decliningseverancetaxratesaremorethenormacrossthesampleofstatesthantheexception.Everystatebuttwo(OhioandArkansas)experienceda

Figure6.EffectiveSeveranceTaxRate–Oklahomavs.GroupofProducingStates

Source:OklahomaTaxCommissionandvariousstatetaxreportingagencies.CalculationsbyRegionTrack.Notes:Sourcesavailableinelectronicformaredetailedinthenotestothereport.

6.9%

3.2% 3.2% 3.0% 2.9% 3.0%

7.3%

5.8% 5.0%

4.5% 4.1%

3.7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2012 2013 2014 2015 2016 2017FiscalYear

Oklahoma16-StateWeightedAvg.

Page|11 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

declineintheeffectiverateinthefive-yearperiodfromFY2012toFY2017.TherateinTexasdeclinedfrom4.6%to4.2%,andwasaslowas3.6%asrecentlyasFY2016.Amongotherlargeproducingstates,theeffectiveratedeclinedfrom5.1%to4.5%inLouisiana,9.9%to8.4%inNorthDakota,1.8%to0.7%inColorado,5.7%to3.8%inWyoming,2.4%to1.0%inCalifornia,and9.8%to7.9%inNewMexico.

III. AdValoremTaxesAlongwithseverancetaxes,mostproducingstatesassesssomeformofadvalorem,orproperty,taxtiedtotheproductionofcrudeoilandnaturalgas.Thetaxistypicallyappliedtothevalueofeithermineralsinthegroundortheequipmentusedabovegroundforextractionandproduction,orboth.AnexceptionisWyoming,whichhasalocaladvaloremtaxbasedonthevalueofproduction.

InOklahoma,theseverancetaxisleviedinlieuofalocalpropertytaxonthevalueofmineralsinthegroundandtheequipmentthatisessentialtotheproductionofawell.Localgovernmentsinthestatedo,however,haveauthoritytoassessthevalueofotheroilandgas-relatedequipmentandinfrastructure.Hence,Oklahomaishistoricallyviewedasalowpropertytaxstateforoilandgasactivity.

OklahomaTaxes.Readilyavailablestate-leveldataonoilandgas-relatedpropertytaxpaymentsinOklahomaissparse.Statewidedataareavailablefor2012,2014,and2016basedonvaluationsasofNovember1forthestatedcalendaryear.9Weinterpolatetaxpaymentsfor2013and2015usingthemidpointbetweenactualpaymentsinthesurroundingyears.Giventhesmoothnessinherentinadvaloremtaxreceiptsovertime,wedonotbelievetheresultsaresensitivetothisapproach.

Twocategoriesofreportedseverancetaxesareusedintheanalysis:1)Refineries,GasPlants,Gathering&Compressionand2)OtherOil,Gas&MiningProperty.RefineriesareviewedasmanufacturingandareremovedfromthetotalforfourcountiesinOklahoma(Kay,Carter,Tulsa,andGarvin).Theadjustedtotal(exrefineries)forthefirstcategoryisaddedtothesecondtoreflecttotaloilandgas-relatedpropertytaxpaymentsinOklahoma.Itisimportanttonotethatthismeasuresubstantiallyunderstatesthetotalpropertytaxpaymentspaidbytheoilandgasindustry.Thetotalincludesonlypropertyusedintheproductionofoilandgasandexcludesbuildingsandotherrealproperty,aswellassignificantpersonalpropertyusedintheoperationsofoilandgasfirmsacrossthestate.Effectivepropertytaxratesarecalculatedasannualpropertytaxesdividedbythetotalvalueofoilandgasproduction.

Figure7illustratesannualOklahomapropertytaxpaymentsrelatedtooilandgasproductionandeffectiveadvaloremtaxratesfromFY2012toFY2016.Paymentstotaled$157.6millioninFY2016,up42%from$110.7millioninFY2012.Theeffectiveratewas1.4%inFY2016basedon$157.6millioninpropertytaxesand$11.51billioninproductionvalue.OvertheFY2012toFY2015period,propertytaxesaveragedslightlylessthan1%ofproductionvalue.TheeffectiverateincreasedsharplyinFY2016becauseofbothhighertaxpaymentsandfallingproductionvalue.

State-LevelReportingChallenges.Wenextexamineestimatedannualpropertytaxpaymentsforthesixteenlargestproducingstates.ThetargetedcomparisonyearisFY2016,themostrecentlyavailable

Page|12 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

dataformoststates.Avarietyofsourcesareusedtoformadvaloremtaxestimatesforthesixteenstates.Theprimarysourcesarestatetaxreportingagencies.Sourcesavailableinelectronicformaredetailedinthenotestothereport.10

Numerouschallengesarefacedinassemblingastate-levelcomparativeviewofoilandgas-relatedadvaloremtaxation.Forexample:

1. Propertyvaluationsarenotdeterminedatauniformpointintimeacrossthestates;2. Thedefinitionusedfortheoilandgasindustrydiffersgreatlyacrossthestates;3. Thespecificassetsdeemedoilandgas-relateddiffergreatlyacrossthestates;4. Propertytaxesaregenerallyassessedbylocalgovernmentsratherthanthestateanda

consolidatedsourceoftaxreportingmaynotbeavailable;5. Therearetimingdifferencesassociatedwiththeschedulegoverningwhenpropertytaxesare

calculated,reported,andpaidthatmayaffectthecomparativebaseyearforsomestates;6. Somestatessimplyreportvaluationsandmillageratesthatrequireadirectcalculationor

estimationoftaxes;7. Therearegenerallynofollow-uprevisionstothedatatoreflectvaluationchallenges,rebates,

reassessments,andothersubsequentchangestoactualtaxreceipts.

Amongthe16largestproducingstates,therearenopropertytaxesassessedonoilandgasactivityinNorthDakotaandPennsylvania.TheestimatesforColorado,NewMexico,Texas,andOhioreflectFY2015taxpayments,thelatestdataavailable.TaxesinWestVirginiaforFY2016arebasedonthevalueofproductionfromtwoyearsprior.TaxesreportedforArkansasarefor2016paymentbutbasedonFY2015valuations.Californiapropertytaxesareonlyreportedatthelocallevelandmustbeextrapolatedtothestatelevel.11

Figure7.OilandGas-RelatedAdValoremTaxPaymentsandEffectiveRate-OklahomaPayments EffectiveRate

Source:OklahomaTaxCommissionandRegionTrackcalculations.Notes:Alldataareforfiscalyears.Paymentsin2013and2015areinterpolatedasthemidpointbetweenadjacentyears.Theeffectiverateiscalculatedasadvaloremtaxpaymentsdividedbythetotalvalueofoilandgasproduction.

110.7

128.6

146.6 152.1 157.6

0

20

40

60

80

100

120

140

160

180

2012 2013 2014 2015 2016

$Millions

0.8% 0.8%

0.7% 0.8%

1.4%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

2012 2013 2014 2015 2016

Page|13 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Estimatesofoilandgas-relatedadvaloremtaxreceiptsforeachstateandtheunderlyingeffectiveratecalculationsaredetailedinAppendixA2.SeeRaimiandNewell(2016)fordetailedcomparativeestimatesofadvaloremtaxespaidbytheoilandgassectorintheproducingstates.

OklahomaVersusOtherProducingStates.ComparativeestimatesofeffectiveadvaloremtaxratesareshowninFigure8forthe16largestproducingstates.TheratesaretargetedatabaseyearofFY2016,subjecttotheinherentvariabilityinstate-to-statereporting.Giventhehistoricalsmoothnessinaggregatestate-leveladvaloremtaxdataovertime,thisvariationisnotbelievedtoaltertheoverallresultsinanymeaningfulway.

Theaverageeffectiveadvaloremtaxrateis2.7%acrossthegroupofsixteenstates,rangingfrom0%inNorthDakotaandPennsylvaniato5.4%inColorado.

Threestates–Colorado,California,andWyoming–haveeffectiveadvaloremtaxratesabove4.5%.Coloradousesprimarilypropertytaxesbecauseitallowsanoffsetof87.5%ofadvaloremtaxespaidasacredittowardseverancetaxes,leavinglittlenetseverancetaxliabilityformostpayers.Californiaassessesalocaladvaloremtax,withnostatewideorlocalseverancetax.Wyominghasalocaladvaloremtaxleviedonproductionvalueaswellasataxonequipment.

Fouradditionalstates–Texas,WestVirginia,Kansas,andLouisiana–levypropertytaxesbetween3%and4%ofproductionvalue.Texasappliespropertytaxestobothmineralvalueandequipment.

Oklahomafallsinathirdtierofstates–Utah,NewMexico,Alaska,Arkansas,andOklahoma–witheffectiveadvaloremtaxratesbetweenapproximately1.5%and2.5%.AlaskaandNewMexicohavehistoricallyreliedmoreheavilyonseverancetaxes.Utah,Arkansas,andOklahomahavehistoricallyfavoredlimitedrelianceonpropertytaxes.

Figure8.EffectiveAdValoremTaxRate(FY20161)

Page|14 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Thefinalfourstates–Ohio,Montana,NorthDakota,andPennsylvania–haveeffectiveadvaloremtaxratesbelow1%ofproductionvalue.Fast-growinggasproducerOhiocontinuestolevylowoveralloilandgas-relatedtaxes.NorthDakotaandPennsylvaniadonotpermitlocalgovernmentstoassessadvaloremtaxesonoilandgasproductionactivity.

CombinedSeveranceandAdValoremTaxRates.Figure9providesacomparativeviewofcombinedseveranceandadvaloremeffectivetaxrateswithabaseyearofFY2016forseverancetaxesandanapproximatebaseyearofFY2016(subjecttodatalimitations)foradvaloremtaxes.AppendixA2providesdetailsofthecomponentcalculationsforthecombinedeffectiverates.

Oklahoma’scombinedeffectiverateis4.24%,composedofaseverancetaxrateof2.87%andadvaloremrateof1.37%.Thisranks12thamongthesixteenstatesinthesample.

Theaveragecombinedeffectiverateis6.8%acrossallsixteenstates-4.1%forseveranceand2.7%foradvalorem.

Atoptieroffivestates–NewMexico,Wyoming,Montana,Louisiana,andNorthDakota–havecombinedeffectiveratesofapproximately10%.Amongthesestates,allbutWyomingareheavilytiltedtowardhighseverancetaxesandrelativelylowpropertytaxes.Montanalevieslessthan0.5%ineffectivepropertytaxes.Montanaalsohasnoadvaloremtaxesonthevalueofmineralsbutallowslocalpropertytaxesonsomesurfaceequipment.Wyomingisuniqueinthatitassessesarelativelyhighshareofbothseveranceandpropertytaxes.Louisianaassessesalargeseverancetaxinlieuofadvaloremtaxonproductionbutallowslocaladvaloremtaxesonequipment.NorthDakotaallowsnopropertytaxesonoilandgasassetsbutreliesheavilyonhighseverancetaxes.

Notes:Dataarecollectedfromvariousstatereportingagency.Sourcesavailableinelectronicformaredetailedinthenotestothereport.SeeFigure15foradvaloremtaxpaymentsbystate.1TheeffectiverateshaveatargetedbaseyearofFY2016,subjecttotheinherentvariabilityinstate-to-statereporting.

Figure9.CombinedSeverance&AdValoremEffectiveTaxRates(FY2016)

5.4% 5.1%

4.6%

3.5% 3.3% 3.3% 3.1%

2.3% 2.0%

1.7% 1.7% 1.4%

0.8% 0.4%

0.0% 0.0%

2.7%

0%

1%

2%

3%

4%

5%

6%

CO CA WY TX WV KS LA UT NM AK AR OK OH MT ND PA 16-States

Page|15 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Asecondtierofsixstates–WestVirginia,Texas,Colorado,California,Kansas,andAlaska–hascombinedeffectiveratesbetween5%and8%.Thesestatesgenerallyuseamorebalancedcombinationofseveranceandpropertytaxes.LeadingproducerTexashasa7.1%ratethatissplitalmostevenlybetweenthetwotaxes.ColoradoandCaliforniaareheavilyweightedtowardpropertytaxesandhaveamongthelowestseverancetaxratesatapproximately1%.Kansasassessesadvaloremtaxesonbothequipmentandreserves.Alaskahastransitionedfromheavyrelianceonseverancetaxestoamorebalancedshareofeachfollowingacollapseinstateseverancetaxesinrecentyears.

Oklahoma’scombinedrateof4.2%isgroupedamongafinaltieroffivestates–Oklahoma,Utah,Arkansas,Ohio,andPennsylvania–withcombinedeffectiveratesbelow5%.Utahmaintainsalowcombinedrateof3.5%,includingadvaloremtaxesonreservesandaconservationtaxof0.2%.

NeighboringArkansasassessesa3.1%combinedrate.Bothfast-growinggas-producingstatesofOhioandPennsylvaniahaveverylowcombinedeffectiveratesof1.7%and1.5%,respectively.

Forward-LookingCombinedRate.TheexpectedreboundinOklahomaseverancetaxesinresponsetorecenttaxlawchangeswillraisethecombinedseveranceandadvaloremtaxrategoingforward.Figure10providesprojectionsofthecombinedratethroughFY2019.TheseverancetaxoutlookisbasedonOklahomaTaxCommissionprojectionsofseverancetaxpaymentsdescribedinthepriorsection.Theadvaloremtaxassumptionsassumepropertytaxpaymentsincreaseby2%annuallyintheFY2017toFY2019period.Theoilandgasproductionvalueassumptionsarethesameusedtoestimateprojectedseverancetaxratesinthepriorsectionofthereport.FigureA1intheAppendixprovidesdetailsonthecomponentsoftheprojectedeffectiveratecalculations.

Figure10.ProjectedCombinedSeverance&AdValoremEffectiveTaxRate-Oklahoma

8.6%

5.5%

9.6%

6.9%

9.5%

4.2% 3.6%

1.0% 1.1% 2.1%

3.6% 2.87% 1.2% 1.4% 0.9% 1.5%

4.1%

2.0%

4.6%

0.4%

3.1%

0.0%

3.3% 3.5%

5.4% 5.1% 3.3% 1.7%

1.37%

2.3% 1.7% 0.8% 0.0%

2.7%

0%

2%

4%

6%

8%

10%

12%

NM10.6%

WY10.1%

MT10.0%

LA10.0%

ND9.5%

WV7.5%

TX7.1%

CO6.4%

CA6.2%

KS5.4%

AK5.3%

OK4.2%

UT3.5%

AR3.1%

OH1.7%

PA1.5%

16-States6.8%

Severance AdValorem

Page|16 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

ThecombinedseveranceandadvaloremeffectivetaxrateinOklahomawillrisetoaprojected5.3%inthecurrentfiscalyear(FY2018)andto5.7%inFY2019.Assumingconstanttaxpolicyinotherstates,thiswouldrankOklahoma10thamongthe16statesbasedonFY2019combinedeffectiveseveranceandadvaloremtaxrates.TheadjustedeffectiveratewouldfalljustaboveKansas(5.4%)andAlaska(5.3%)andjustbelowCalifornia(6.2%).Thestatewouldfall1.4%belowtheeffectiverateof7.1%inTexas.

IV. MeasuringtheBroaderTaxContributionofOil&GasThecombinedeffectiveseveranceandadvaloremtaxrateisoftenusedasameasureofthetaxcontributionofthestate’soilandgasindustry.Cross-statecomparisonsalsofrequentlyusethetwotaxesasabasisforcomparingrelativetaxburdensontheindustry.Forrecentexamplesofmulti-statecomparisonsbasedonthesemeasures,seeCovenant(2017)andRaimiandNewell(2018).ForexamplesofadvocacygroupsusingseveranceandadvaloremtaxesasevidenceofalowoilandgastaxburdeninOklahoma,seeHeadwaters(2013)andBlatt(2017).

Basedsolelyonthesetwotaxes,Oklahomaappearstobearelativelylow-taxstatewithrespecttooilandgasactivity,withacombined4.2%effectiveseveranceandadvaloremtaxrate(seeFigure9).Whilethesetaxestendtocapturethedirecttaxationappliedtoproduction,theyprovideawhollyineffectivemeasureoftheoveralltaxcontributionoftheoilandgasindustrywithinthestate.Alongwithseveranceandadvaloremtaxes,Oklahomaalsoleviesrelativelyhighpersonalincomeandsalestaxes.ThesearealsothetwolargestsourcesoftotalstateandlocalgovernmenttaxrevenueinOklahoma.

Instead,theoverallstructureofastate’staxsystemcanhaveasmuchinfluenceonthetotaltaxburdenoftheoilandgasindustryastheamountofseveranceandadvaloremtaxeslevied.Theotheroilandgas-producingstateslevyawidelyvaryingrangeoftaxes,includingvariouslevelsofpersonalincomeandsalestaxes.Forexample,thethreemajorproducingstatesofAlaska,Texas,andWyominglevyno

Source:OklahomaTaxCommission,EnergyInformationAdministration,andRegionTrackcalculations.Notes:AdvaloremtaxpaymentsinFY2017,FY2018,andFY2019assume2%annualgrowth.SeverancetaxreceiptsinFY2018andFY2019arebasedonestimatesbytheOklahomaTaxCommission.Valueofcrudeoilandnaturaliscalcluatedasthetotalmarketvalueofcrudeoilandnaturalgasproduction.Theeffectiverateisthecalculatedasthesumoftheeffectiveseverancetaxrateandeffectiveadvaloremtaxrateineachperiod.

7.7%

4.0% 3.8% 3.8% 4.2% 4.0%

5.3% 5.7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2012 2013 2014 2015 2016 2017 f2018 f2019

Severance AdValorem

Page|17 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

personalincometax.Householdearningsinthesestatesaccruetowageandsalaryworkers,self-employedproprietors,royaltyowners,andothersintheoilandgassector,buttheseearningsdonotcontributetototalstatetaxrevenuethroughpersonalincometaxpayments.InOklahoma,personalincometaxeshavecomprisedalmostone-thirdoftotalstatetaxrevenuethepasttwodecades.Evenamongenergystatesthatdolevyanincometax,taxratescandiffergreatly.

Notallstatescollectsalestaxeseither,withrateshighlyvariableaswell.AlaskaandMontana,twotraditionallyhighseverancetaxstates,haveonlysmalllocalsalestaxes.Infact,Alaskahaslongreliedpredominatelyonproductiontaxesfromoilandgastofundstategovernmentandistheonlystatethatdoesnotcollectstatesalestaxorlevyanindividualincometaxonpersonalincome.

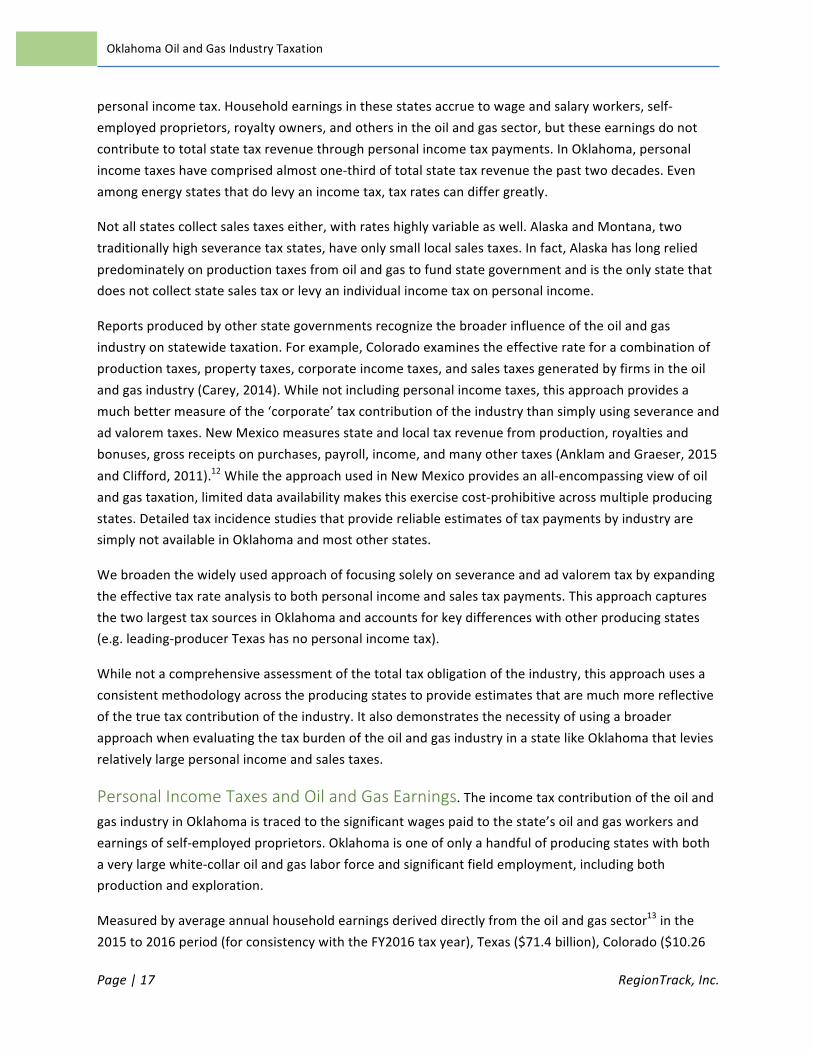

Reportsproducedbyotherstategovernmentsrecognizethebroaderinfluenceoftheoilandgasindustryonstatewidetaxation.Forexample,Coloradoexaminestheeffectiverateforacombinationofproductiontaxes,propertytaxes,corporateincometaxes,andsalestaxesgeneratedbyfirmsintheoilandgasindustry(Carey,2014).Whilenotincludingpersonalincometaxes,thisapproachprovidesamuchbettermeasureofthe‘corporate’taxcontributionoftheindustrythansimplyusingseveranceandadvaloremtaxes.NewMexicomeasuresstateandlocaltaxrevenuefromproduction,royaltiesandbonuses,grossreceiptsonpurchases,payroll,income,andmanyothertaxes(AnklamandGraeser,2015andClifford,2011).12WhiletheapproachusedinNewMexicoprovidesanall-encompassingviewofoilandgastaxation,limiteddataavailabilitymakesthisexercisecost-prohibitiveacrossmultipleproducingstates.DetailedtaxincidencestudiesthatprovidereliableestimatesoftaxpaymentsbyindustryaresimplynotavailableinOklahomaandmostotherstates.

Webroadenthewidelyusedapproachoffocusingsolelyonseveranceandadvaloremtaxbyexpandingtheeffectivetaxrateanalysistobothpersonalincomeandsalestaxpayments.ThisapproachcapturesthetwolargesttaxsourcesinOklahomaandaccountsforkeydifferenceswithotherproducingstates(e.g.leading-producerTexashasnopersonalincometax).

Whilenotacomprehensiveassessmentofthetotaltaxobligationoftheindustry,thisapproachusesaconsistentmethodologyacrosstheproducingstatestoprovideestimatesthataremuchmorereflectiveofthetruetaxcontributionoftheindustry.ItalsodemonstratesthenecessityofusingabroaderapproachwhenevaluatingthetaxburdenoftheoilandgasindustryinastatelikeOklahomathatleviesrelativelylargepersonalincomeandsalestaxes.

PersonalIncomeTaxesandOilandGasEarnings.Theincometaxcontributionoftheoiland

gasindustryinOklahomaistracedtothesignificantwagespaidtothestate’soilandgasworkersandearningsofself-employedproprietors.Oklahomaisoneofonlyahandfulofproducingstateswithbothaverylargewhite-collaroilandgaslaborforceandsignificantfieldemployment,includingbothproductionandexploration.

Measuredbyaverageannualhouseholdearningsderiveddirectlyfromtheoilandgassector13inthe2015to2016period(forconsistencywiththeFY2016taxyear),Texas($71.4billion),Colorado($10.26

Page|18 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

billion),Louisiana($8.41billion),Oklahoma($7.27billion),andCalifornia($4.38billion)havefarhigherlevelsoftotaloilandgasindustryearningsthantheremainingproducingstates.Thepotentialforpersonalincometaxpaymentsinthesefivestatesisfargreaterthaninthesmallerproducingstates.AsecondtierofstatesbasedonoilandgasearningsbyhouseholdsincludesPennsylvania($2.18billion),Kansas($2.12billion),NorthDakota($2.06billion),Alaska($2.06billion),NewMexico($2.05billion),andWyoming($1.08billion).Nootherproducingstategenerates$1billionormoreannuallyinhouseholdoilandgasearnings.

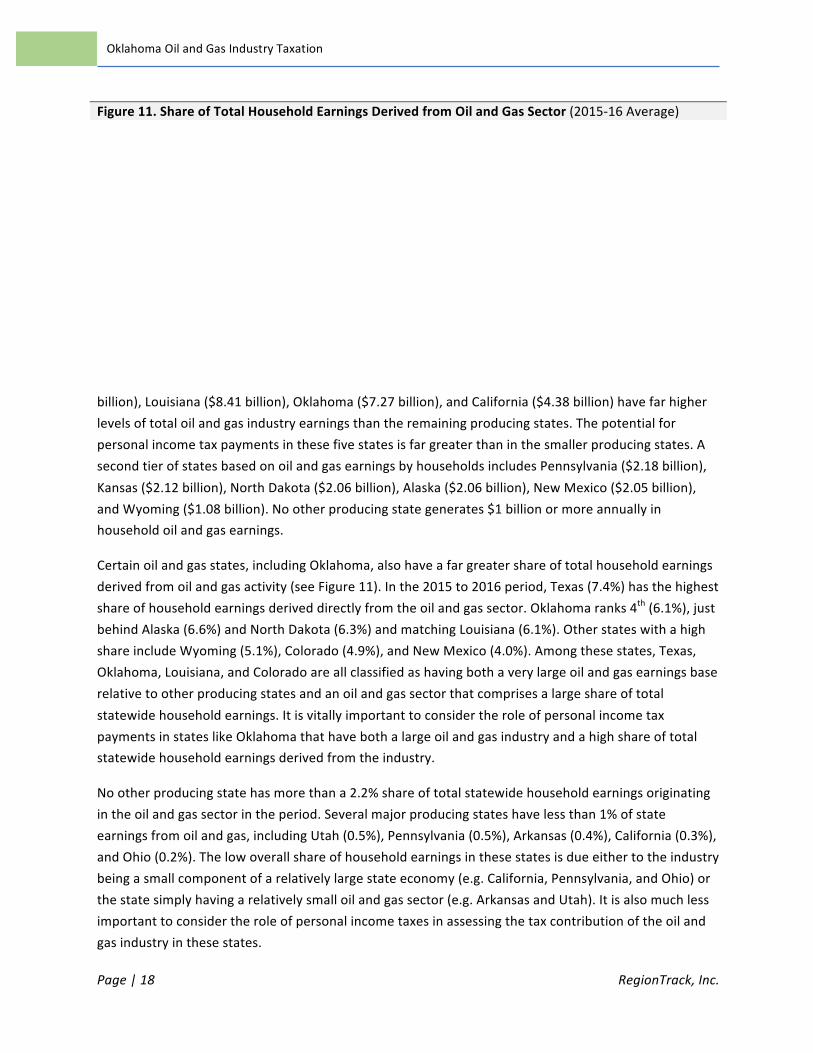

Certainoilandgasstates,includingOklahoma,alsohaveafargreatershareoftotalhouseholdearningsderivedfromoilandgasactivity(seeFigure11).Inthe2015to2016period,Texas(7.4%)hasthehighestshareofhouseholdearningsderiveddirectlyfromtheoilandgassector.Oklahomaranks4th(6.1%),justbehindAlaska(6.6%)andNorthDakota(6.3%)andmatchingLouisiana(6.1%).OtherstateswithahighshareincludeWyoming(5.1%),Colorado(4.9%),andNewMexico(4.0%).Amongthesestates,Texas,Oklahoma,Louisiana,andColoradoareallclassifiedashavingbothaverylargeoilandgasearningsbaserelativetootherproducingstatesandanoilandgassectorthatcomprisesalargeshareoftotalstatewidehouseholdearnings.ItisvitallyimportanttoconsidertheroleofpersonalincometaxpaymentsinstateslikeOklahomathathavebothalargeoilandgasindustryandahighshareoftotalstatewidehouseholdearningsderivedfromtheindustry.

Nootherproducingstatehasmorethana2.2%shareoftotalstatewidehouseholdearningsoriginatingintheoilandgassectorintheperiod.Severalmajorproducingstateshavelessthan1%ofstateearningsfromoilandgas,includingUtah(0.5%),Pennsylvania(0.5%),Arkansas(0.4%),California(0.3%),andOhio(0.2%).Thelowoverallshareofhouseholdearningsinthesestatesisdueeithertotheindustrybeingasmallcomponentofarelativelylargestateeconomy(e.g.California,Pennsylvania,andOhio)orthestatesimplyhavingarelativelysmalloilandgassector(e.g.ArkansasandUtah).Itisalsomuchlessimportanttoconsidertheroleofpersonalincometaxesinassessingthetaxcontributionoftheoilandgasindustryinthesestates.

Figure11.ShareofTotalHouseholdEarningsDerivedfromOilandGasSector(2015-16Average)

Page|19 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Whiletheamountofoilandgasearningsinfluencespersonalincometaxrevenueinmanyproducingstates,ithasnoeffectinstateswithnoincometax.TheseincludeTexas,thenation’slargestproducer,aswellasmajorproducersAlaskaandWyoming.Evenamongtheproducingstatesthatlevyincometaxes,therearelargedifferencesinaverageincometaxrates.Measuredusingtotalpersonalincometaxpaymentsasashareoftotalhouseholdearnings,Oklahomapaid2.62%oftotalhouseholdearningsinincometaxesversus3.06%nationallyand3.02%inthesixteenmajorproducingstatesinFY2016.Amongtheproducingstates,averageincometaxratesrangefrom0%inTexas,Wyoming,andAlaskato5.1%inCalifornia(seeFigure12).

Figure12providescomparativeestimatesofthepersonalincometaxcontributionofoilandgasactivityinOklahomaandtheothermajorproducingstates.Theincometaxestimatesarederivedbymultiplyingthetotalhouseholdearningsofworkersandproprietorsintheoilandgassectorbytheaverageincometaxratewithineachstate.Theuseoftheaveragetaxratewillsubstantiallyunderstatetheamountofoilandgas-relatedincometaxespaidinOklahomaandmostproducingstatesgiventhehighaverageearningsintheoilandgasindustryandprogressivetaxratesinmoststates.Nonetheless,itprovidesaconsistentmeasureforcomparingtaxrelativetaxburdensacrossstates.Earningsintheoilandgassectorareaveragedacrossthe2015to2016periodforconsistencywithFY2016taxdata.

Becauseoilandgasactivityisacomponentofthebroaderminingsector,weremovenon-oilandgasminingactivity.TheshareofearningsineachstatederivedfromoilandgasactivityiscalculatedasthesumofNAICS201(Oilandgasextraction)plusashareofNAICS203(Supportactivitiesformining).TheshareofNAICS203includedisdeterminedbytheratioofNAICS201/(NAICS201+NAICS202(Mining–exceptoilandgas)).

Notes:HouseholdearningsisdefinedbyBureauofEconomicAnalysisasemployeecompensationplusproprietors’income.Proprietor’sincomeconsistsprimarilyoftheincomeofsoleproprietorsandpartnerships.TheshareofhouseholdearningsineachstatederivedfromoilandgasactivityiscalculatedasthesumofNAICS201(Oilandgasextraction)plusashareofNAICS203(Supportactivitiesformining).TheshareofNAICS203includedisdeterminedbytheratioofNAICS201/(NAICS201+NAICS202(Mining–exceptoilandgas)).

Figure12.PersonalIncomeTaxContributionofOil&GasSector(FY2016)

7.4%

6.6% 6.3% 6.1% 6.1%

5.1% 4.9%

4.0%

2.2% 2.1% 1.6%

0.5% 0.5% 0.4% 0.3% 0.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

TX AK ND OK LA WY CO NM MT KS WV UT PA AR CA OH

Page|20 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

InOklahoma,estimatedpersonalincometaxpaymentsbyworkersandproprietorsintheoilandgassectoratthestateaveragetaxratetotal$190.7millioninFY2016.Thisisapproximately6.4%ofthe$3.0billionintotalpersonalincometaxpaymentsmadeinthestateinFY2016.Again,thisprovidesahighlyconservativeestimatebasedontheaverageincometaxrateinthestate,whichunderstatestheactualrateinthehigh-wageoilandgasindustry.

Colorado($316.7million)derivesconsiderablymorepersonalincometaxrevenuefromoilandgasthanOklahoma,dueprimarilytoahigheraverageincometaxrate.California($224.1million)slightlyexceedstheincometaxpaymentsinOklahoma,buthasafarlowerlevelofearningscombinedwithafarhighertaxrate.Louisianaalsoproducessignificantpersonalincometaxrevenueof$178.2million.

Amongtheremainingstates,noneproducesevenone-thirdtheincometaxrevenuereceivedinOklahomafromoilandgasactivity.InFY2016,Oklahomaproducedapproximately$150millionormoreinincometaxrevenuethanArkansas,Kansas,Montana,NorthDakota,NewMexico,Ohio,Pennsylvania,Texas,Utah,WestVirginia,andWyoming.Again,Texas,Alaska,andWyomingderivenopersonalincometaxrevenuefromtheactivityoftheoilandgasindustry.

State

Oil&GasSectorHouseholdEarnings1

(2015-16avg.)

FY2016AverageIncomeTaxRate2

Oil&Gas-RelatedIncomeTaxatAverageRate3

Oil&Gas-RelatedIncomeTaxat

OKRate(2.58%)4

FY2016Oil&GasProduction

Value

EffectiveIncomeTaxRate

Alaska $2,059,141,152 0.00% $0 $54,019,749 $6,704,000,405 0.00%Arkansas 312,181,427 3.73% 11,643,239 8,189,804 2,265,993,926 0.51%California 4,382,463,364 5.11% 224,129,405 114,970,054 7,804,566,938 2.87%Colorado 10,258,354,390 3.09% 316,683,019 269,118,863 8,085,748,405 3.92%Kansas 2,116,304,923 2.28% 48,205,166 55,519,390 2,095,423,520 2.30%Louisiana 8,412,495,955 2.12% 178,176,948 220,694,398 6,422,504,345 2.77%Montana 626,211,317 4.07% 25,459,759 16,428,101 991,287,508 2.57%NorthDakota 2,055,294,361 1.36% 28,008,974 53,918,832 15,546,573,903 0.18%NewMexico 2,048,685,420 2.69% 55,099,020 53,745,452 8,329,094,006 0.66%Ohio 749,459,851 2.30% 17,213,991 19,661,417 3,742,552,340 0.46%Oklahoma 7,269,059,179 2.62% 190,697,345 190,697,345 11,514,670,836 1.66%Pennsylvania 2,175,342,862 2.61% 56,863,547 57,068,198 11,819,866,993 0.48%Texas 71,388,693,090 0.00% 0 1,872,819,284 63,591,098,355 0.00%Utah 450,381,628 3.53% 15,890,641 11,815,364 1,996,888,030 0.80%WestVirginia 673,791,358 4.54% 30,604,998 17,676,321 3,177,522,760 0.96%Wyoming 1,083,658,766 0.00% 0 28,428,830 6,717,027,690 0.00% 16-States $116,061,519,042 3.02% $1,198,676,051 $3,044,771,400 $160,804,819,959 0.75%Source:BureauofEconomicAnalysis,CensusBureau,andRegionTrackcalculations.Notes:1HouseholdearningsisdefinedbyBureauofEconomicAnalysisasemployeecompensationplusproprietors’income.Earningsareaveragedinthe2015-2016periodforconsistencywiththeFY2016taxyear.Proprietor’sincomeconsistsprimarilyoftheincomeofsoleproprietorsandpartnerships.TheshareofhouseholdearningsineachstatederivedfromoilandgasactivityiscalculatedasthesumofNAICS201(Oilandgasextraction)plusashareofNAICS203(Supportactivitiesformining).TheshareofNAICS203includedisdeterminedbytheratioofNAICS201/(NAICS201+NAICS202(Mining–exceptoilandgas)).2Theaverageincometaxrateforeachstateiscalculatedastotalindividualincometaxpaymentsdividedbytotalhouseholdearnings.3Incometaxpaidbytheoilandgasindustryisestimatedasoilandgasearningstimestheaverageincometaxrateinthestate.4Oilandgasearningsineachstatemultipliedbythe2.62%averagerateinOklahoma.

Figure13.EffectiveIncomeTaxRateonOilandGasProduction(FY2016)

Page|21 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Togaugethesignificanceofoilandgas-relatedincometaxpaymentsinOklahomarelativetothestateswithnoincometax,potentialincometaxreceiptsarecalculatedinFigure12foreachstatebasedontheprevailing2.62%averageincometaxrateinOklahoma.Amongthestateswithnopersonalincometax,Texaswouldderive$1.87billioninpersonalincometaxrevenueatOklahoma’saveragerate.Alaskawouldraiseanadditional$54million,whileWyomingwouldcollect$28million.Californiawouldlose$110millioninincometaxduetoitshighaveragetaxrate.Louisianawouldgainmorethan$40millionbecauseofitsloweraverageincometaxrate.

EffectivePersonalIncomeTaxRates.Figure13illustratesthewidevariationineffectiveincometaxratesonoilandgasproductionacrossthesixteenproducingstates.TheeffectiverateiscalculatedasestimatedincometaxpaidonhouseholdearningsfromtheoilandgasindustrydividedbythetotalvalueofoilandgasproductioninFY2016.Acrossallsixteenstates,theeffectiveincometaxraterelativetoproductionis0.84%.Oklahomahasaneffectiveincometaxraterelativetoproductionof1.7%,6thhighestamongthesixteenstatesanddoubletheoverallaveragerate.Coloradohasthehighesteffectiverateat3.9%,morethandoubleOklahoma’srate.CaliforniaandLouisianahaveeffectiveratesjustbelow3%,whileKansasandMontanahaveeffectiveratesofapproximately2.5%.

Allotherstateshaveaneffectiveincometaxrateof1%orless,withAlaska,Texas,andWyominghavingzeropercenteffectiverates.Thegas-producingstatesofOhioandPennsylvaniabothhaveeffectiveincometaxratesofapproximately0.5%.LargeoilproducerNorthDakota(0.2%)hasthelowesteffectiveincometaxrateamongthestatesthathaveanincometaxinplace.

ParticularlynoteworthyisthatmanyofthestateswithacombinedseveranceandadvaloremeffectivetaxratehigherthanOklahoma’shaveverylowpersonalincometaxrates.TheseincludeNorthDakota,NewMexico,andWestVirginia,plusthethreeproducingstateswithnoincometax–Texas,Alaska,and

Notes:Incometaxiscalculatedasaveragehouseholdearningsintheoilandgassectorinthe2015-2016periodtimestheaverageincometaxrateinthestateinFY2016.Theeffectiveincometaxrateisincometaxrelatedtooilandgasactivitydividedbytotalvalueofoilandgasproduction.HouseholdearningsisdefinedbyBureauofEconomicAnalysisasemployeecompensationplusproprietors’income.Proprietor’sincomeconsistsprimarilyoftheincomeofsoleproprietorsandpartnerships.TheshareofhouseholdearningsineachstatederivedfromoilandgasactivityiscalculatedasthesumofNAICS201(Oilandgasextraction)plusashareofNAICS203(Supportactivitiesformining).TheshareofNAICS203includedisdeterminedbytheratioofNAICS201/(NAICS201+NAICS202(Mining–exceptoilandgas)).

3.9%

2.9% 2.8% 2.6%

2.3%

1.7%

1.0% 0.8% 0.7% 0.5% 0.5% 0.5%

0.2% 0.0% 0.0% 0.0%

0.84%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

CO CA LA MT KS OK WV UT NM AR PA OH ND AK TX WY 16-States

Page|22 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Wyoming.This,again,underscorestheimportanceofincludingpersonalincometaxeswhenusingthesestatestoevaluatetheoilandgas-relatedtaxcontributioninOklahoma.

OilandGas-RelatedSalesTax.Firmsintheoilandgasindustryalsopaysignificantamountsof

salestax,withmanystateandlocalgovernmentshighlydependentuponthesetaxestofundgovernmentactivities.14SalestaxesareanespeciallycriticalsourceofrevenueatthelocallevelinOklahoma,giventhatadvaloremtaxrevenuecannotbeusedtofundgeneralmunicipalexpenditures.

Thedifferentialinbothsalestaxratesandthepropensitytotaxeconomicactivityacrossthestatesresultsingreatvariationinthesalestaxcontributionofoilandgasactivityacrosstheproducingstates.Salestaxratesvaryconsiderablyaswell.BasedontheongoingannualsurveyproducedbytheTaxFoundation,Oklahomahasthe6thhighestaveragestateandlocalsalestaxrateamongallstatesat8.86%in2017,andthe3rdhighestrateamongenergy-producingstates.15

Louisiana(9.98%)andArkansas(9.30%)havethehighestaverageratesamongthemajorenergy-producingstates,aswellasthehighestand3rdhighestrates,respectively,acrossallfiftystates.Otherproducingstateswithratesabove8%includeKansas(8.62%),California(8.25%),andTexas(8.19%).However,otherproducingstateshavemuchlowerrates.Theaveragesalestaxrateisonly7.55%inNewMexico,7.50%inColorado,7.14%inOhio,6.78%inNorthDakota,6.76%inUtah,6.34%inPennsylvania,6.29%inWestVirginia,and5.40%inWyoming.Alaska(1.76%)hasthelowestrate,whileMontanahasnogeneralsalestax.

Incomparingtheoveralleffectivetaxburdenacrosstheproducingstates,manystatesaremuchlessreliantthanOklahomaonsalestaxes.Ofthefivestateswiththehighesteffectiveseveranceandadvaloremtaxrates(NewMexico,Wyoming,Montana,Louisiana,andNorthDakota),fourhavesalestaxratesthatarebetween1.3%and3.3%lowerthaninOklahoma.Leviedacrossthebroadretailbaseofastate,thesesalestaxratedifferentialscanproducesignificantlydifferentamountsofrevenue.

Differencesintheoveralllevelofoilandgasactivityacrossthestatesalsoproducesmuchdifferentsalestaxcontributions.Stateswithlargeroilandgasindustries,ingeneral,tendtogeneraterelativelymoresalestaxrevenuefromoilandgasactivitythanstateswithasmallerindustry.Stateswithmoredrillingactivityalsotendtoproducesignificantlymoresalestaxrevenue.Oklahomahasbothalargeoilandgasindustryandhighlevelsofdrillingactivity.

Collectingcomparablestate-leveldataonsalestaxpaidbytheoilandgasindustryfromstatetaxagenciesisgenerallynotpossible.Differencesintaxlaw,reportingstandards,paymentprocesses,collectingandremittingparties,andtreatmentofout-of-statepurchasesmakesassemblingcomparativesalestaxdatarelatedtooilandgasactivityvirtuallyimpossibleinmoststates.Themostsignificanthurdleisthatitisnotpossibleinmoststatestodifferentiatebetweensalestaxpaymentsremittedbytheoilandgasindustryontheirowntaxablesalesversustaxespaidinconjunctionwiththeirowntaxablepurchases.Asaresult,thesalestaxpayableonmanyofthepurchasesbytheoilandgasindustryareremittedbyfirmsinotherindustriesandcannotbetracked.Thetaxcomparisoninthis

Page|23 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

reportismostconcernedwithestimatesofsalestaxespaiddirectlybyoilandgasfirms,notnecessarilytheamountremittedbytheoilandgasindustrybasedonthepurchasesofothers.Thisisacommonmisuseofsalestaxdatareportedattheindustrylevel.Comparativeoverallmeasuresofsalestaxburdenarefurthercomplicatedbydifferencesintheshareofthetaxthatispaidbyresidentsversusnonresidents,particularlybytourists.

Comparativestate-levelestimatesofthesalestaxcontributionoftheoilandgasindustryareformedbyapportioningtotalstateandlocalsalestaxreceiptstoeachindustrybasedonitsaveragecontributiontostateGDPinthe2015to2016period(forconsistencywithFY2016taxdata).Thisfollowstheapproachcommonlyusedtoapportionstateandlocaltaxesattheindustrylevelinwidely-usedeconomicimpactmodels.16ThisisalsoconsistentwiththebasicapproachusedinColorado’soverallassessmentofoilandgasindustrytaxburden(Carey,2014).Theunderlyingassumptionisthatsalestaxpaymentsrelatedtotheoilandgasindustryareproportionaltotheoverallsizeoftheindustry.Hence,theamountofpurchasesmadebytheindustry,incomepaidtoworkers,andearningsofproprietorswhooperateoilandgas-relatedbusinesseswouldbecloselyrelatedtosalestaxespaid.Thisapproachisappliedconsistentlytoeachstatewherebytheoilandgasindustry’sshareoftotalstateeconomicactivitydeterminestheoverallshareofstatesalestaxpaymentsderivedfromtheindustry.17Italsoaccountsforoveralldifferencesinthesizeofthetaxablesalesbaseacrosstheproducingstates.TheoverallestimatesarenothighlysensitivetothechoiceofGDPtoapportionthedata.Therelativesizesofthecross-stateestimatesareessentiallyunchangedwhenusingothermeasuresofeconomicactivitysuchastotalhouseholdearningsshare,wageandsalaryincomeshare,ortotalcompensationshareinplaceofGDP.

AllsalestaxdatausedintheanalysisarederivedfromtheCensusBureau’sStateandLocalGovernmentFinancedatabase.18Thedatabaseprovidesastandardizedmeasureoftaxcollectionsbytypeoftaxatboththestateandlocallevel.TotalsalestaxesatthestateandlocallevelarebasedonFY2016dataatthestatelevelandFY2015dataatthelocallevel.Thesemeasuresreflectthemostrecentlyavailabledataonaconsistentbasisacrossthestates.Onlygeneralsalesandgrossreceiptsareincluded.Targetedsalestaxessuchasalcohol,parimutuel,tobacco,andmotorfueltaxesareexcluded.

Becauseoilandgasactivityisacomponentofthebroaderminingsector,weremovenon-oilandgas-relatedminingactivityfromGDPusingthesameapproachusedwithoilandgas-relatedhouseholdearningsinthepriorsectionofthereport.TheshareofGDPineachstatederivedfromoilandgasactivityiscalculatedasthesumofNAICS201(Oilandgasextraction)plusashareofNAICS203(Supportactivitiesformining).TheshareofNAICS203includedisdeterminedbytheratioofNAICS201/(NAICS201+NAICS202(Mining–exceptoilandgas)).

Page|24 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

SalesTaxPayments.Figure13detailsestimatedsalestaxpaymentsforthesixteenproducingstatesinthesample.Texasproducesthelargestamountat$3.14billion.Oklahomaranks2ndwith$536.4millioninestimatedstateandlocalsalestaxpayments(outofatotalof$4.56billionstatewide)inFY2016.Thestate’shighshareofGDPfromoilandgasactivityisreflectedintheestimatedsalestaxtotal.Oklahoma’soilandgassectorcomprisesthesecondlargestshareoftotalstateGDP(11.8%)amongtheproducingstates,trailingonlyAlaska(13.9%),andisconsiderablyhigherthanWyoming(9.7%),NorthDakota(8.9%),Texas(7.9%),andNewMexico(6.8%).

Otherstatesproducingmorethan$200millioninestimatedsalestaxfromoilandgasactivityincludeLouisiana($300.0million),NewMexico($208.6million),andColorado($210.7million).

Figure13.Oil&GasSectorSalesTaxContributionandEffectiveRate(FY2016)

State

Oil&GasShareofGDP(2015-16avg.)1

FY2016TotalStateandLocalSalesTax2

FY2016Oil&Gas-RelatedSalesTax

FY2016Oil&GasProduction

ValueEffectiveRate

Alaska 13.9% $231,195,000 $32,042,117 $6,704,000,405 0.5%Arkansas 1.4% 4,398,654,000 61,395,130 2,265,993,926 2.7%California 0.3% 50,668,814,000 171,938,465 7,804,566,938 2.2%Colorado 3.2% 6,614,809,000 210,727,019 8,085,748,405 2.6%Kansas 0.7% 4,208,361,000 30,226,613 2,095,423,520 1.4%Louisiana 4.1% 7,363,508,000 300,005,145 6,422,504,345 4.7%Montana 1.1% 0 0 991,287,508 0.0%NorthDakota 8.9% 1,239,506,000 110,340,583 15,546,573,903 0.7%NewMexico 6.8% 3,068,551,000 208,579,820 8,329,094,006 2.5%Ohio 1.1% 14,486,920,000 162,944,461 3,742,552,340 4.4%Oklahoma 11.8% 4,564,158,000 536,442,228 11,514,670,836 4.7%Pennsylvania 1.6% 11,079,520,000 182,638,361 11,819,866,993 1.5%Texas 7.9% 39,534,846,000 3,139,486,542 63,591,098,355 4.9%Utah 0.7% 2,837,403,000 19,381,583 1,996,888,030 1.0%WestVirginia 4.3% 1,302,750,000 56,616,453 3,177,522,760 1.8%Wyoming 9.7% 879,911,000 84,967,844 6,717,027,690 1.3%

16-States 3.2% $152,478,906,000 $5,307,732,364 $160,804,819,959 3.3%Source:BureauofEconomicAnalysis,CensusBureau,andRegionTrackcalculations.Notes:Oilandgas-relatedsalestaxiscalculatedbymultiplyingtheshareofGDPintheoilandgassectorbytotalstateandlocalsalestaxes.1TheshareofGDPineachstatederivedfromoilandgasactivityiscalculatedasthesumofNAICS201(Oilandgasextraction)plusashareofNAICS203(Supportactivitiesformining).TheshareofNAICS203includedisdeterminedbytheratioofNAICS201/(NAICS201+NAICS202(Mining–exceptoilandgas)).GDPisaveragedinthe2015-16periodforconsistencywithFY2016taxdata.2Includesbothstateandlocalsalesandusetax,aswellasgeneralgrossreceipts.BasedonthedefinitionintheCensusStateandLocalGovernmentFinancedatabase.StatesalestaxisforFY2016,thelatestyearavailable.LocalsalestaxisforFY2015,thelatestyearavailable.

Oklahoma’sestimatedtotalsalestaxcontributionissecondhighestamongthesixteenstates,behindonlythe$3.14billionestimateforTexas.Louisiana($300.0million),Colorado($210.7million),andNewMexico($208.6million)aretheonlyotherstatesestimatedtocollectmorethan$200million.NorthDakotaisestimatedtogenerateonly$110.3million,roughlyone-fifththetotalinOklahoma,whichreflectsbothasmalleroilandgasindustryandloweraveragesalestaxrates.

Figure14.EffectiveSalesTaxRateonOilandGasProduction(FY2016)

Page|25 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Severalofthekeyproducingstatesgeneratemuchlessestimatedsalestaxrevenue.TheseincludeArkansas($61.4million),WestVirginia($56.6million),Alaska($32.0million),Kansas($30.2million),andUtah($19.4million).Montanaproducednone.Mostofthelowsalestax-producingstateshaverelativelysmalllevelsofoilandgasemploymentandlowaveragestateandlocalsalestaxrates.

EffectiveSalesTaxRates.Figure14ranksthesixteenproducingstatesbyeffectivesalestaxratesonoilandgasproductionintheperiod.Theeffectiverateiscalculatedasestimatedoilandgas-relatedsalestaxdividedbytotalvalueofoilandgasproductioninFY2016.

TheeffectivesalestaxratesvaryfromalowofzeroinMontanatoahighof4.9%inTexas.Oklahoma’seffectivesalestaxrateof4.7%isjustbelowTexas,3rdhighestamongthe16states,and1.4%abovetheaveragerateof3.3%acrossall16states.Louisiana(4.7%)andOhio(4.4%)aretheonlyotherstateswithaneffectivesalestaxrateabove2.7%.

Fourstates–Arkansas,Colorado,NewMexico,andCalifornia–formamiddletierwitheffectivesalestaxratesbetween2.2%and2.7%.Fiveadditionalstates–WestVirginia,Pennsylvania,Kansas,Wyoming,andUtah–haveaneffectiveratebetween1%and2%.Stateswithaneffectivesalestaxratebelow1%includeNorthDakota(0.5%),Alaska(0.3%),andMontana(0.0%).Alaska,Montana,NorthDakota,andWyomingarealltraditionallyviewedashightaxstates,yettheyreceiverelativelylittlecontributionfromoilandgasactivityintheformofsalestaxes.

OverallEffectiveTaxRate.Figure15summarizestotaltaxpaymentsacrossallfourtaxcategories

examined-severance,advalorem,personalincome,andsales–alongwiththecombinedeffectivetaxrateonproductionforthesixteenproducingstates.Oklahoma’soilandgasindustrycontributedanestimated$1.22billioninFY2016acrossthefourtaxesusingthemethodologydescribedineachsection

Notes:Includesbothstateandlocalsalesandusetax,aswellasgrossreceiptstax.BasedonthedefinitionusedintheCensusBureauStateandLocalGovernmentFinanceDatabase.StatesalestaxisforFY2016,thelatestyearavailable.LocalsalestaxisforFY2015,thelatestyearavailable.Theeffectiverateisstateandlocalsalestaxfromoilandgasactivitydividedbytotalvalueofoilandgasproduction.HouseholdearningsisdefinedbyBureauofEconomicAnalysisasemployeecompensationplusproprietors’income.Proprietor’sincomeconsistsprimarilyoftheincomeofsoleproprietorsandpartnerships.TheshareofhouseholdearningsineachstatederivedfromoilandgasactivityiscalculatedasthesumofNAICS201(Oilandgasextraction)plusashareofNAICS203(Supportactivitiesformining).TheshareofNAICS203includedisdeterminedbytheratioofNAICS201/(NAICS201+NAICS202(Mining–exceptoilandgas)).

4.9% 4.7% 4.7%

4.4%

2.7% 2.6% 2.5% 2.2%

1.8% 1.5% 1.4% 1.3%

1.0% 0.7% 0.5%

0.0%

3.3%

0%

1%

2%

3%

4%

5%

6%

TX LA OK OH AR CO NM CA WV PA KS WY UT ND AK MT 16-States

Page|26 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

ofthereport.Paymentsinclude$536millioninsalestax,$331millioninseverancetax,$191millioninpersonalincometax,and$158millioninadvaloremtaxes.

Oklahomahasthethirdlargesttotaltaxcontribution,trailingonlyTexas($7.65billion)andNorthDakota($1.62billion).Threeotherstatesproducedmorethan$1billionacrossthefourtaxesincludingNewMexico($1.15billion),Louisiana($1.12billion),andColorado($1.04billion).

Effectivetaxratesonproductionacrossthefourtaxesrangefromalowof3.5%inPennsylvaniatoahighof17.4%inLouisiana.Louisiana’srateismorethan3.5%aboveNewMexico,thestatewiththesecondhighestrate.Oklahoma’seffectiverateof10.6%ranks8thamongthesixteenstates,slightlybelowtheoverallaveragerateof10.8%.Thestate’soverallrateisjustbelowWyoming(11.4%)andCalifornia(11.3%)andjustabovetherateinNorthDakota(10.4%).BothWyomingandNorthDakotaaretraditionallyviewedashightaxstates.TheoverallrateinTexas(12.0%)isfifthhighestand1.4%higherthaninOklahoma.

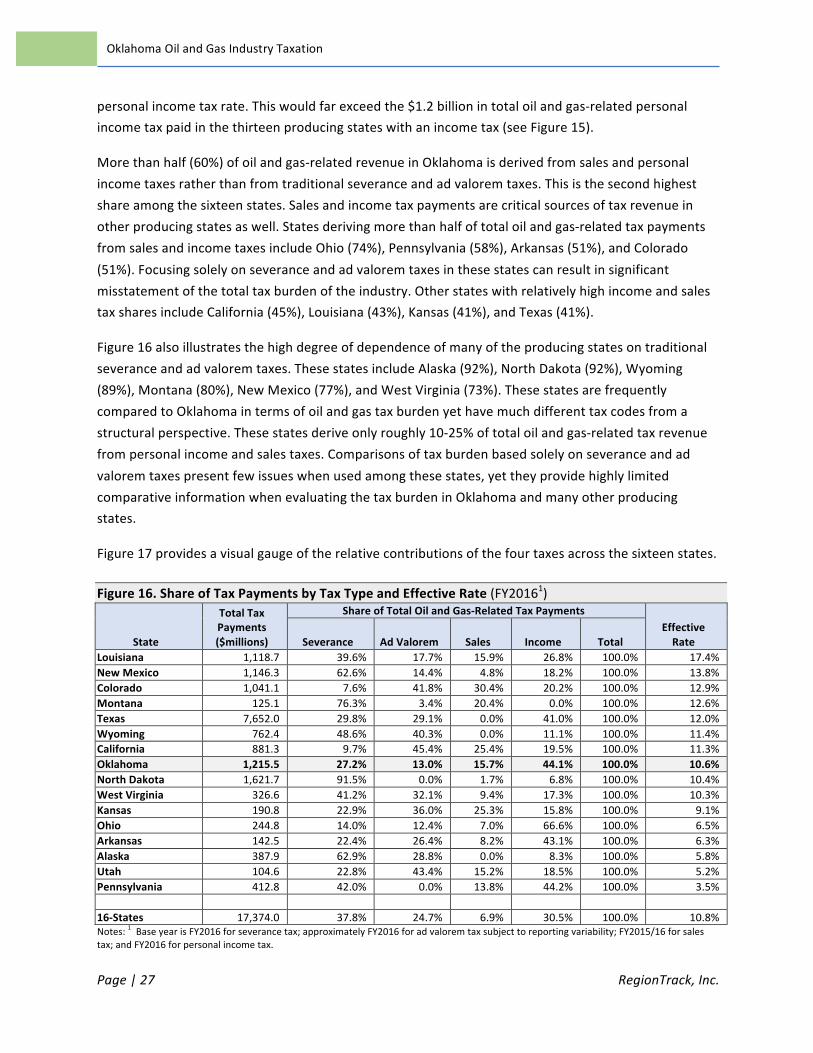

Figure16illustratestherelativecontributionshareofeachtaxcategoryacrossthestates.Oklahoma’staxburdenisdividedinto44%salestax,27%severancetax,16%incometax,and13%advaloremtax.

Thetaxsharesacrossthesixteenstatesarerelativelybalancedinthreeofthefourcategories,witha38%severancetaxshare,a30%salestaxshare,anda25%advaloremtaxshare,alongwithasmaller7%shareforincometax.Thesmallincometaxshareacrossthestatesreflectsinlargepartthelackofapersonalincometaxindominant-producerTexas.Again,anadditional$1.87billioninpersonalincometaxonoilandgas-relatedhouseholdearningswouldbecollectedinTexasatOklahoma’saverage

Figure15.OilandGas-RelatedTaxPaymentsandCombinedEffectiveTaxRate

State

OilandGas-RelatedTaxes($millions) 2016Oil&GasProductionValue($mil.)

CombinedEffectiveRateSeverance

AdValorem

PersonalIncome Sales Total

Louisiana $442.9 $197.6 $178.2 $300.0 $1,118.7 $6,422.5 17.4%NewMexico 717.6 165.0 55.1 208.6 1,146.3 8,329.1 13.8%Colorado 79.0 434.7 316.7 210.7 1,041.1 8,085.7 12.9%Montana 95.4 4.2 25.5 0.0 125.1 991.3 12.6%Texas 2,282.7 2,229.8 0.0 3,139.5 7,652.0 63,591.1 12.0%Wyoming 370.4 307.0 0.0 85.0 762.4 6,717.0 11.4%California 85.2 400.0 224.1 171.9 881.3 7,804.6 11.3%Oklahoma 330.7 157.6 190.7 536.4 1,215.5 11,514.7 10.6%NorthDakota 1,483.3 0.0 28.0 110.3 1,621.7 15,546.6 10.4%WestVirginia 134.4 105.0 30.6 56.6 326.6 3,177.5 10.3%Kansas 43.8 68.6 48.2 30.2 190.8 2,095.4 9.1%Ohio 34.3 30.3 17.2 162.9 244.8 3,742.6 6.5%Arkansas 31.9 37.6 11.6 61.4 142.5 2,266.0 6.3%Alaska 244.1 111.7 0.0 32.0 387.9 6,704.0 5.8%Utah $23.9 $45.4 $15.9 $19.4 $104.6 $1,996.9 5.2%Pennsylvania 173.3 0.0 56.9 182.6 412.8 11,819.9 3.5%

16-States $6,572.9 $4,294.7 $1,198.7 $5,307.7 $17,374.0 $160,804.8 10.8%Notes:BaseyearisFY2016forseverancetax;approximatelyFY2016foradvaloremtaxsubjecttoreportingvariability;FY2015/16forsalestax;andFY2016forpersonalincometax.

Page|27 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

personalincometaxrate.Thiswouldfarexceedthe$1.2billionintotaloilandgas-relatedpersonalincometaxpaidinthethirteenproducingstateswithanincometax(seeFigure15).

Morethanhalf(60%)ofoilandgas-relatedrevenueinOklahomaisderivedfromsalesandpersonalincometaxesratherthanfromtraditionalseveranceandadvaloremtaxes.Thisisthesecondhighestshareamongthesixteenstates.Salesandincometaxpaymentsarecriticalsourcesoftaxrevenueinotherproducingstatesaswell.Statesderivingmorethanhalfoftotaloilandgas-relatedtaxpaymentsfromsalesandincometaxesincludeOhio(74%),Pennsylvania(58%),Arkansas(51%),andColorado(51%).Focusingsolelyonseveranceandadvaloremtaxesinthesestatescanresultinsignificantmisstatementofthetotaltaxburdenoftheindustry.OtherstateswithrelativelyhighincomeandsalestaxsharesincludeCalifornia(45%),Louisiana(43%),Kansas(41%),andTexas(41%).

Figure16alsoillustratesthehighdegreeofdependenceofmanyoftheproducingstatesontraditionalseveranceandadvaloremtaxes.ThesestatesincludeAlaska(92%),NorthDakota(92%),Wyoming(89%),Montana(80%),NewMexico(77%),andWestVirginia(73%).ThesestatesarefrequentlycomparedtoOklahomaintermsofoilandgastaxburdenyethavemuchdifferenttaxcodesfromastructuralperspective.Thesestatesderiveonlyroughly10-25%oftotaloilandgas-relatedtaxrevenuefrompersonalincomeandsalestaxes.Comparisonsoftaxburdenbasedsolelyonseveranceandadvaloremtaxespresentfewissueswhenusedamongthesestates,yettheyprovidehighlylimitedcomparativeinformationwhenevaluatingthetaxburdeninOklahomaandmanyotherproducingstates.

Figure17providesavisualgaugeoftherelativecontributionsofthefourtaxesacrossthesixteenstates.

Figure16.ShareofTaxPaymentsbyTaxTypeandEffectiveRate(FY20161)

State

TotalTaxPayments($millions)

ShareofTotalOilandGas-RelatedTaxPaymentsEffectiveRateSeverance AdValorem Sales Income Total

Louisiana 1,118.7 39.6% 17.7% 15.9% 26.8% 100.0% 17.4%NewMexico 1,146.3 62.6% 14.4% 4.8% 18.2% 100.0% 13.8%Colorado 1,041.1 7.6% 41.8% 30.4% 20.2% 100.0% 12.9%Montana 125.1 76.3% 3.4% 20.4% 0.0% 100.0% 12.6%Texas 7,652.0 29.8% 29.1% 0.0% 41.0% 100.0% 12.0%Wyoming 762.4 48.6% 40.3% 0.0% 11.1% 100.0% 11.4%California 881.3 9.7% 45.4% 25.4% 19.5% 100.0% 11.3%Oklahoma 1,215.5 27.2% 13.0% 15.7% 44.1% 100.0% 10.6%NorthDakota 1,621.7 91.5% 0.0% 1.7% 6.8% 100.0% 10.4%WestVirginia 326.6 41.2% 32.1% 9.4% 17.3% 100.0% 10.3%Kansas 190.8 22.9% 36.0% 25.3% 15.8% 100.0% 9.1%Ohio 244.8 14.0% 12.4% 7.0% 66.6% 100.0% 6.5%Arkansas 142.5 22.4% 26.4% 8.2% 43.1% 100.0% 6.3%Alaska 387.9 62.9% 28.8% 0.0% 8.3% 100.0% 5.8%Utah 104.6 22.8% 43.4% 15.2% 18.5% 100.0% 5.2%Pennsylvania 412.8 42.0% 0.0% 13.8% 44.2% 100.0% 3.5%

16-States 17,374.0 37.8% 24.7% 6.9% 30.5% 100.0% 10.8%Notes:1BaseyearisFY2016forseverancetax;approximatelyFY2016foradvaloremtaxsubjecttoreportingvariability;FY2015/16forsalestax;andFY2016forpersonalincometax.

Page|28 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Again,Oklahomaranks8thamongthestatesandfallsjustabovethemidpointofthestatesbetweenWyomingandNorthDakota,twostateswithamuchdifferenttaxstructure.Oklahomahasamorebalanceduseofallfourtaxes,whileNorthDakotaoilandgas-relatedtaxrevenuecomesalmostentirelyfromseverancetaxrevenue.Wyomingderivesalmostallitsrevenuefromacombinationofseveranceandadvaloremtaxes.

Manyofthestateswiththehighestoveralleffectiveratestendtolevyverylargeseverancetaxesrelativetotheothertaxcategories.Threeofthefourstateswiththehighestoveralleffectiverate–Louisiana,NewMexico,andMontana–haveamongthehighesteffectiveseverancetaxrates.

LikeOklahoma,otherstateshavearelativelybalancedshareofallfourtaxes,withatleasta1%effectiverateforeachtaxcategory.ThesestatesincludeLouisiana,Colorado,WestVirginia,California,andKansas.

BycomponentoftheoveralleffectiverateinFigure17,the10.8%averageacrossthesixteenstatesiscomprisedofa4.1%severancetaxrate,a3.3%salestaxrate,a2.7%advaloremtaxrate,anda0.7%personalincometaxrate.Relativetothegroupofsixteenstates,Oklahomahasalowerthanaverageeffectiverateforseveranceandadvaloremtaxesandahigherthanaverageeffectiverateforsalesandincometaxes.

Figure17.EffectiveSeverance,AdValorem,Sales,andIncomeTaxRatebyState(FY2016)

6.9% 8.6%

1.0%

9.6%

3.6% 5.5%

1.1% 2.9%

9.5%

4.2% 2.1% 0.9% 1.4%

3.6% 1.2% 1.5%

4.1%

3.1% 2.0%

5.4%

0.4%

3.5%

4.6%

5.1% 1.4%

0.0%

3.3%

3.3%

0.8% 1.7%

1.7%

2.3% 0.0%

2.7%

2.8% 0.7%

3.9%

2.6%

0.0%

0.0%

2.9%

1.7%

0.2%

1.0% 2.3%

0.5% 0.5%

0.0% 0.8%

0.5%

0.7%

4.7%

2.5% 2.6%

0.0%

4.9% 1.3% 2.2%

4.7%

0.7% 1.8%

1.4%

4.4% 2.7%

0.5% 1.0%

1.5%

3.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

LA17.4%

NM13.8%

CO12.9%

MT12.6%

TX12.0%

WY11.4%

CA11.3%

OK10.6%

ND10.4%

WV10.3%

KS9.1%

OH6.5%

AR6.3%

AK5.8%

UT5.2%

PA3.5%

16-States10.8%

Severance AdValorem Income Sales

Page|29 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

EffectofRecentTaxLawChange.GivenrecentincreasesinseverancetaxratesinOklahoma,

thestate’soveralleffectiveratewillrisesharplyinbothFY2018andFY2019asmoreproducingwellsmoveintothe7%taxbracket.Figure18illustratestheoveralleffectivetaxrateandrelativerankingofOklahomabasedonbothFY2016severancetaxratesandprojectedseverancetaxratesinFY2018andFY2019.Theeffectiveseverancetaxrateforthestateisprojectedtoriseto4.4%inFY2018and4.8%inFY2019.

Whilethestate’sFY2016overalleffectiverateof10.6%ranksjustabovethemidpointofthesixteenstates,theoverallrateisprojectedtoriseto12.1%inthecurrenttaxyear(FY2018)andto12.6%inFY2019.Givenconstanttaxpolicyinotherstates,Oklahomawouldhavethe5thhighestoveralleffectivetaxrateamongthesixteenstatesthisfiscalyearandnext.Thestate’sratewillexceedthe10.8%overallrateacrossthesixteenstatesandmove0.6%abovethe12.0%overalleffectiverateinTexasbyFY2019.

Inshort,basedontaxlawchangesalreadyimplemented,Oklahomaisprojectedtohavethe5thhighestoveralleffectivetaxrateamongthesixteenstatesthisfiscalyear.Ofthefourstateswithahighereffectiverate,onlyLouisianawillexceedOklahoma’sFY2019ratebymorethanapproximately1percentagepoint.TheeffectiverateinOklahomaalreadyexceedstheeffectiverateinNorthDakotaandisprojectedtosoonexceedtherateinWyomingandroughlymatchtherateinMontana.NorthDakota,Wyoming,andMontanaarealltraditionalproducingstateslongviewedashavinghighoilandgastaxes.

HigherSeveranceTaxRateScenarios.GivenrecentpolicydebatesoverthesufficiencyofoveralltaxrevenueinOklahoma,itisimportanttounderstandtheresultingeffectontheoveralleffectivetaxratefacedbytheoilandgasindustryifseverancetaxratesareincreasedfurther.Although

Figure18.ProjectedOverallEffectiveRateinOklahoma–FY2018/FY2019EffectiveSeveranceTaxRates

6.9% 8.6%

1.0%

9.6%

4.8% 4.4% 3.6% 5.5%

1.1% 2.9%

9.5%

4.2% 2.1%

0.9% 1.4% 3.6%

1.2% 1.5% 4.1%

3.1% 2.0%

5.4%

0.4%

1.4% 1.4% 3.5%

4.6%

5.1% 1.4%

0.0%

3.3%

3.3%

0.8% 1.7%

1.7%

2.3% 0.0%

2.7%

2.8% 0.7%

3.9%

2.6%

1.7% 1.7% 0.0%

0.0%

2.9%

1.7%

0.2%

1.0%

2.3%

0.5% 0.5%

0.0%

0.8%

0.5%

0.7%

4.7%

2.5% 2.6%

0.0%

4.7% 4.7% 4.9% 1.3% 2.2%

4.7%

0.7% 1.8%

1.4%

4.4% 2.7%

0.5% 1.0%

1.5%

3.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

LA17.4% NM13.8% CO12.9% MT12.6% OK12.5% OK12.1% TX12.0% WY11.4%CA11.3% OK10.6% ND10.4% WV10.3% KS9.1% OH6.5%AR6.3% AK5.8%UT5.2% PA3.5% 16-States10.8%

Severance AdValorem Income Sales@FY19EffectiveSeverancetaxRate

@FY18EffectiveSeverancetaxRate

@FY16EffectiveSeverancetaxRate

Page|30 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

Oklahomaisoftencastasalow-taxstatewhenviewedsimplybyseveranceandadvaloremtaxes,theoveralleffectiverateinthestateisalreadyabovethemidpointofthemajorproducingstateswhenincomeandsalestaxesareincluded,andtheratewillrisefurtherunderrecenttaxlawchanges.Therecentincreaseinthestate’sseverancetaxratewillpushtheoveralleffectiverateinOklahomato5thhighestamongthemajorproducingstatesthisfiscalyear.

Raisingseverancetaxratesfurtherhasthepotentialtogreatlyshifttheoveralloilandgastaxburdeninthestateevenhigherrelativetocompetingstates.Weexaminetwopotentialscenariosforraisingseverancetaxrates:1)raisingtheseverancetaxrateonproductiontaxedatthe2%rateto4%,and2)taxingallproductionat7%.Figure19providesestimatesoftheoveralleffectiveOklahomaoilandgastaxrateunderthetwoscenariosassumingconstanttaxpolicyinotherproducingstates.TheestimatesassumethechangesareimplementedinFY2019,theupcomingfiscalyear.TheprojectedoveralleffectiverateisbasedonFY2019estimatesforseverancetaxesandFY2016estimatesoftheeffectiveratesforadvalorem,sales,andpersonalincometaxesusedinthepriorcross-statecomparisons.

Bothproposedscenarioswouldproducesignificantincreasesinboththeeffectiveseverancetaxrateandtheoveralleffectivetaxratepaidbythestate’soilandgasindustry.BasedonOklahomaTaxCommissionsestimatesofoilandgasproductionbybracketdetailedinFigure2,adoublingoftheseverancetaxrateonproductioninthe2%bracketto4%wouldraisetotalseverancetaxrevenueby$133.363millioninFY2019.Totalseverancetaxcollectionswouldreach$855.3millioninFY2019.ThistaxrateincreasewouldincreaseOklahoma’seffectiveseverancetaxrateinFY2019to5.46%andthe

Figure19.ProjectedFY2019OverallEffectiveRateinOklahoma–IncreasedSeveranceTaxRates

Notes:AssumesFY2019productioninthe2%taxratebracketistaxedateither4%or7%.Totalprojectedseverancetaxesassuminganincreasedrateon2%productionare$855.3millioninFY2019ata4%severancetaxrateand$1,055.4millioninFY2019ata7%severancetaxrate.

6.9% 6.7% 8.6%

5.5%

1.0%

9.6%

3.6% 5.5%

1.1% 2.9%

9.5%

4.2% 2.1%

0.9% 1.4% 3.6%

1.2% 1.5% 4.1%

3.1% 1.4%

2.0%

1.4%

5.4%

0.4%

3.5%

4.6%

5.1% 1.4%

0.0%

3.3%

3.3%

0.8% 1.7%

1.7%

2.3% 0.0%

2.7%

2.8%

1.7%

0.7%

1.7% 4.1%

2.5%

0.0%

0.0%

2.9%

1.7%

0.2%

1.0%

2.3%

0.5% 0.5%

0.0% 0.8%

0.5%

0.7%

4.7%

4.7% 2.5%

4.7% 2.6%

0.0%

4.9% 1.3% 2.2%

4.7%

0.7% 1.8%

1.4%

4.4% 2.7% 0.5%

1.0%

1.5%

3.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

LA17.4%

OK14.4%

NM13.8%

OK13.1%

CO13.1%

MT12.6%

TX12.0%

WY11.4%

CA11.3%

OK10.6%

ND10.4%

WV10.3%

KS9.1%

OH6.5%

AR6.3%

AK5.8%

UT5.2%

PA3.5%

16-States10.8%

Severance AdValorem Income SalesFY192%

ProductionTaxed at7%Rate

FY192%ProductionTaxedat4%Rate

@FY16EffectiveSeverancetaxRate

Page|31 RegionTrack,Inc.

OklahomaOilandGasIndustryTaxation

overalleffectivetaxrateto13.1%.Oklahomawouldhavethe3rdhighestoveralltaxrateamongtheproducingstates,trailingonlyLouisiana(17.4%)andNewMexico(13.8%).Severancestaxeswouldbecomethelargestcomponentoftaxcontribution,exceedingthecontributionofsalestaxes.