Embed Size (px)

Citation preview

www.pwc.co.uk/hrs

On red alertShareholder questionsput executive pay underthe spotlight

An overview ofFTSE 100 AGMs upto 31 May 2012

July 2012

PwC Contents

Contents

Preface 1

Shareholders want more answers 2

Section 1 – Summary of plans introduced 5

Quick reference 5

AGM voting outcomes grouped by ABI rating 6

Individual plan summaries 7

Section 2 – Summary of voting on remuneration reports 13

AGM voting outcomes 13

Individual summaries 16

Glossary 21

Contacts 22

PwC 1

Welcome to our annual review of the AGM seasonIt’s been another interesting year for executive compensation. The pay packages of executives remain very muchin the media spotlight and executive remuneration is a highly emotive topic amongst many businesses, theirshareholders and members of the general public. While there has been a great deal of noise made regarding afew specific cases, there have been fewer shareholder interventions in this AGM season than last year.

In this year’s review the first section looks at the details of new plans and material amendments to existingplans voted on by shareholders at an AGM in the period 1 January 2012 to 31 May 2012. A total of six plans arecovered. Our summaries of the plans themselves include comments by the Association of British Insurers (ABI)and Research, Recommendations and Electronic Voting (RREV) – a joint venture between the NationalAssociation of Pension Funds (NAPF) and Institutional Shareholder Services (ISS).

Section two of the review sets out the outcomes of the FTSE100 AGMs held between 1 January 2012 and 31 May2012. Where companies have received an amber top from the ABI and anything other than a FORrecommendation from RREV we’ve summarised the comments from these institutions to demonstrate the mostcommon topics that may or may not have contributed to the voting outcomes.

Looking forward to the next round of AGMs it’s important to bear in mind the changes being proposed by theDepartment for Business, Innovation and Skills (BIS). These changes are likely to have a significant impact oncompanies, particularly in the coming year as they are expected to transition to the new required practice. Ifyou’d like to discuss the impact of the BIS proposals on executive remuneration please get in touch.

I hope that you find this document to be user friendly, concise and helpful. We’ll continue to perform a reviewon an annual basis, capturing the core AGM season for FTSE 100 companies. Please do let us know if you haveany suggestions for improvement.

Sean O’HareRemuneration PartnerPwC

Preface

PwC 2

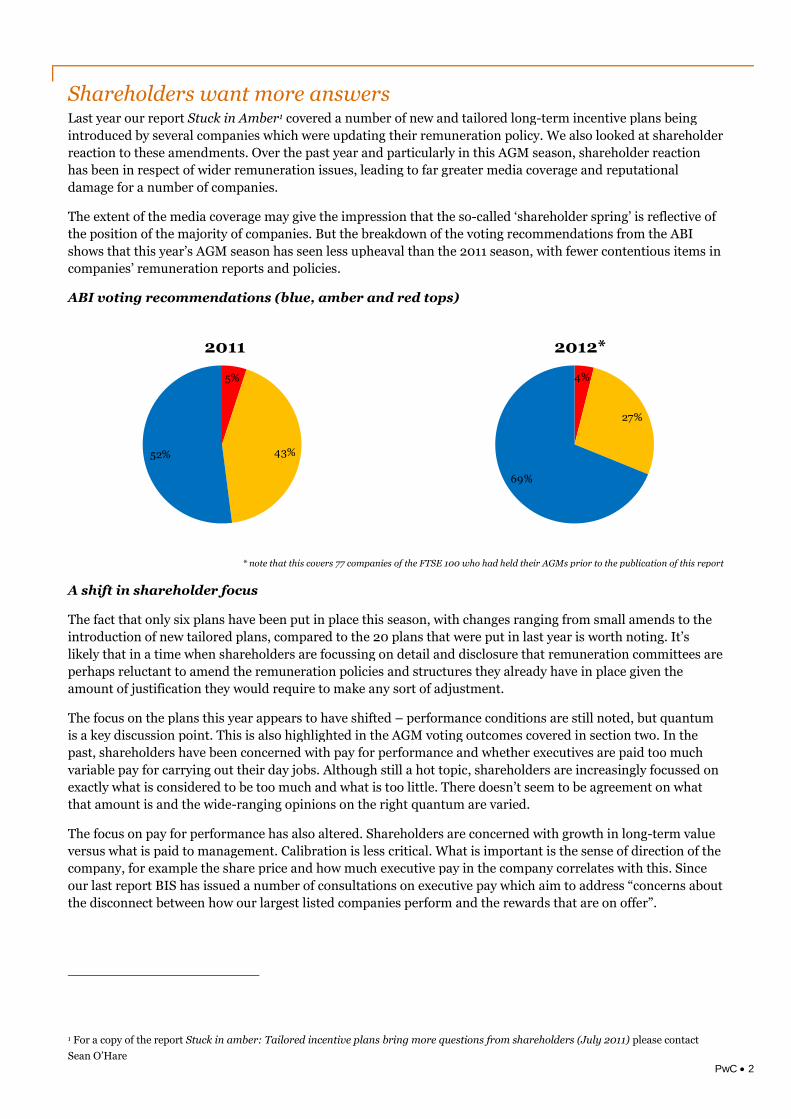

Shareholders want more answersLast year our report Stuck in Amber1 covered a number of new and tailored long-term incentive plans being

introduced by several companies which were updating their remuneration policy. We also looked at shareholder

reaction to these amendments. Over the past year and particularly in this AGM season, shareholder reaction

has been in respect of wider remuneration issues, leading to far greater media coverage and reputational

damage for a number of companies.

The extent of the media coverage may give the impression that the so-called ‘shareholder spring’ is reflective of

the position of the majority of companies. But the breakdown of the voting recommendations from the ABI

shows that this year’s AGM season has seen less upheaval than the 2011 season, with fewer contentious items in

companies’ remuneration reports and policies.

ABI voting recommendations (blue, amber and red tops)

* note that this covers 77 companies of the FTSE 100 who had held their AGMs prior to the publication of this report

A shift in shareholder focus

The fact that only six plans have been put in place this season, with changes ranging from small amends to the

introduction of new tailored plans, compared to the 20 plans that were put in last year is worth noting. It’s

likely that in a time when shareholders are focussing on detail and disclosure that remuneration committees are

perhaps reluctant to amend the remuneration policies and structures they already have in place given the

amount of justification they would require to make any sort of adjustment.

The focus on the plans this year appears to have shifted – performance conditions are still noted, but quantum

is a key discussion point. This is also highlighted in the AGM voting outcomes covered in section two. In the

past, shareholders have been concerned with pay for performance and whether executives are paid too much

variable pay for carrying out their day jobs. Although still a hot topic, shareholders are increasingly focussed on

exactly what is considered to be too much and what is too little. There doesn’t seem to be agreement on what

that amount is and the wide-ranging opinions on the right quantum are varied.

The focus on pay for performance has also altered. Shareholders are concerned with growth in long-term value

versus what is paid to management. Calibration is less critical. What is important is the sense of direction of the

company, for example the share price and how much executive pay in the company correlates with this. Since

our last report BIS has issued a number of consultations on executive pay which aim to address “concerns about

the disconnect between how our largest listed companies perform and the rewards that are on offer”.

1 For a copy of the report Stuck in amber: Tailored incentive plans bring more questions from shareholders (July 2011) please contact

Sean O’Hare

4%

27%

69%

2011 2012*

5%

43%52%

PwC 3

More disclosure around remuneration committee decisions

Another trend to emerge from voters is an implied acceptance of the use of remuneration committee discretion

but a need for greater insight as to how it’s been exercised. Shareholders may not disagree with the decisions

themselves but call into question the robustness of the remuneration committee’s processes to reach those

decisions. Voters are calling for further details and disclosure around this and improvement in the clarity of

communication.

The proposals put forward by BIS look to meet this demand for more information and will force remuneration

committees to be more transparent in their decisions. A potential binding vote by shareholders against a

proposition will help encourage a culture of greater transparency.

Proxy agencies playing a bigger role

One of the big changes we’ve seen is the increased reliance on and reference to advisory institutions (proxy

agencies) and the role they play in shareholder voting. It looks as though proxies are having a bigger influence

on pay – and indeed the scrutiny on it – than the actual shareholders themselves.

The issues we highlight here seem the most prevalent amongst dissatisfied shareholders, who are voting

against remuneration reports. By setting out the voting outcomes in order of FOR votes, it becomes a little

clearer how the opinions of the ABI and RREV affect voting outcomes:

Of the eight companies that received the lowest number of FOR votes, six received an AGAINST

recommendation from RREV.

One company in this group received a red top from the ABI – the company with lowest number of FOR

votes.

The effect of a FOR‡ vote from RREV or an amber top from the ABI is perhaps a little less clear,

although nine out of the 13 companies which received the lowest vote were put on negative watch by

both institutions.

What is not clear from this list the extent to which companies consulted with their key shareholders and the

effect that this might have had.

There have been a few notable examples of companies being cast into the spotlight with high percentages of

AGAINST votes. With the intensified media focus on executive pay, reputations of companies are at risk, with a

potential knock-on effect on the legitimacy and credibility of the corporate governance.

It’s also worth pointing out that this year we have seen an increased number of proxy agencies advising

shareholders to abstain from voting on the remuneration report. This is usually on the basis that the company

hasn’t provided sufficient rationale for changes to remuneration policy or proposed packages. Along with the

investor bodies suggesting such votes, we have seen an increased number of abstentions by shareholders. This

is seen as another way in which shareholders can express their discontent with remuneration policies as it still

sends a message to executives that they will not endorse unexplained reward or unacceptable behaviour.

One proposal put forward by BIS which has encouraged a lot of debate is the shareholder binding vote. If this

had been in place during the period this report covers, a few companies would have had sanctions to bear and

immediate procedures to follow. The reputational impact for such companies would be huge, but it doesn’t

mean that this hasn’t already been the case with only an advisory vote in place. Taking Aviva’s case as one

example of the impact of shareholder discontent and subsequent activism, soon after the vote of 49% AGAINST

was cast, the CEO resigned and it is unlikely media focus will relent for some time.

Announcements of amber tops are making the newspaper headlines whether shareholders share the concerns ofthe ABI or not. In previous years, the reliance placed on the reports and recommendations of shareholderrepresentative bodies such as the ABI, RREV and Pensions Investment Research Consulting (PIRC) has notalways been that clear, and these bodies have not always necessarily had the support of their members. Thisyear has been more interesting due to the fact that there has been an increase in shareholder activism. It’s notclear whether this is due to increased reliance on the proxy agencies’ reports or otherwise. It’s likely thatremuneration committees will have to review and check the appropriateness of the methods they use to judge

PwC 4

remuneration policies. This may take the form of increased contact with the proxy agencies to agree onappropriate policies.

Operating in a challenging environment

When considering executive pay and the shareholder reaction over the past AGM season, it’s important to

consider the context and fairly unique environment that companies are currently operating in. This may help to

explain why are we’re seeing this reaction: are we experiencing a brief trend in activism or have stakeholder

views on executive pay been changed for the foreseeable future?

Companies are currently trying to retain, motivate and recruit talent in an economy that hasn’t recovered as

well as many hoped after a recession which now looks set to continue. This has contributed to a focus on

performance as shareholders look for growth in the value obtained from their investments in exchange for the

rewards to management, with companies fighting to justify such payments. Cost control is an important

consideration which will undoubtedly continue to affect executive pay.

Managing the expectations of several stakeholders

Another important context to consider is the wider employee population. Below-management employees are

placing their own scrutiny on executive pay and many shareholders are looking at executive pay against the

backdrop of the remuneration of these other stakeholders. If the base pay of executives increases, all

stakeholders are likely to ask why the rest of the workforce population hasn’t seen similar increases. As and

when this happens, the need for remuneration committees to fully justify their decisions and actions will

continue.

The other key stakeholder to consider is the Government. BIS has released legislation that will bring in a

binding shareholder vote on remuneration policy, but perhaps the recent revolt and subsequent events are an

indication that the advisory vote works as it is. The increased level of justification required to avoid a negative

advisory vote may not be a bad thing for executive pay, and may be all that is needed to bring about change.

PwC 5

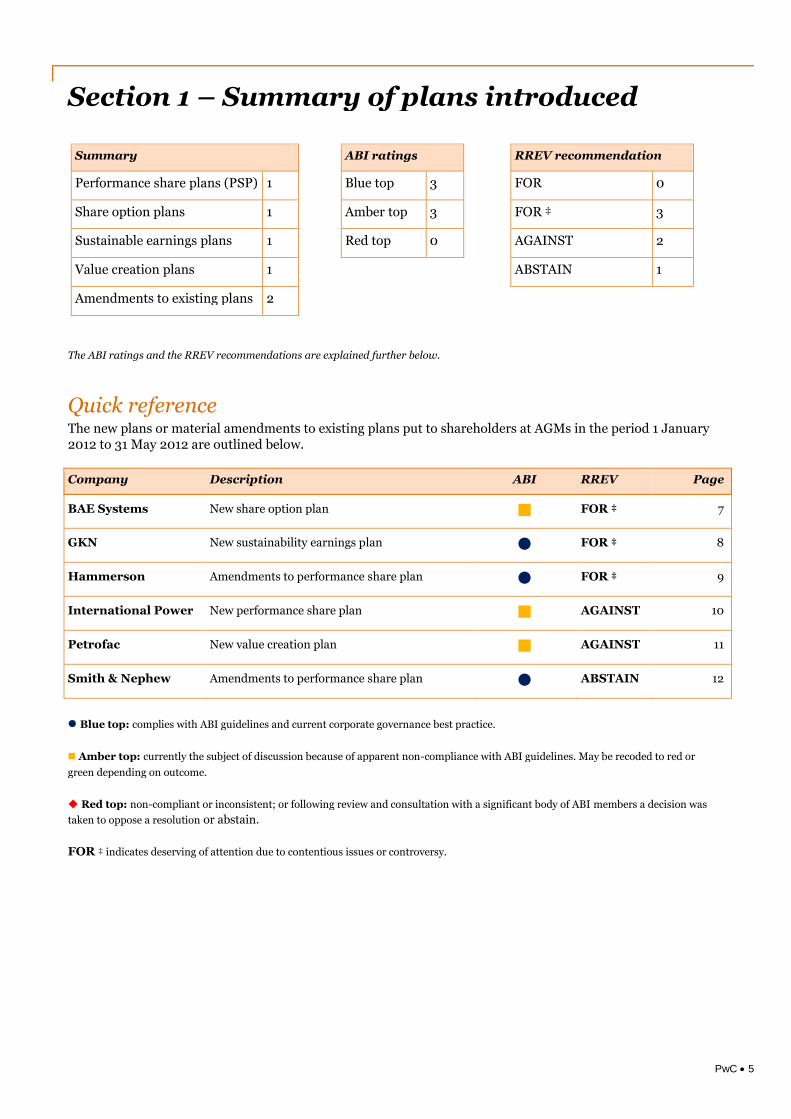

Section 1 – Summary of plans introduced

Summary ABI ratings RREV recommendation

Performance share plans (PSP) 1 Blue top 3 FOR 0

Share option plans 1 Amber top 3 FOR ‡ 3

Sustainable earnings plans 1 Red top 0 AGAINST 2

Value creation plans 1 ABSTAIN 1

Amendments to existing plans 2

The ABI ratings and the RREV recommendations are explained further below.

Quick referenceThe new plans or material amendments to existing plans put to shareholders at AGMs in the period 1 January2012 to 31 May 2012 are outlined below.

Company Description ABI RREV Page

BAE Systems New share option plan FOR ‡ 7

GKN New sustainability earnings plan FOR ‡ 8

Hammerson Amendments to performance share plan FOR ‡ 9

International Power New performance share plan AGAINST 10

Petrofac New value creation plan AGAINST 11

Smith & Nephew Amendments to performance share plan ABSTAIN 12

Blue top: complies with ABI guidelines and current corporate governance best practice.

Amber top: currently the subject of discussion because of apparent non-compliance with ABI guidelines. May be recoded to red or

green depending on outcome.

Red top: non-compliant or inconsistent; or following review and consultation with a significant body of ABI members a decision was

taken to oppose a resolution or abstain.

FOR ‡ indicates deserving of attention due to contentious issues or controversy.

PwC 6

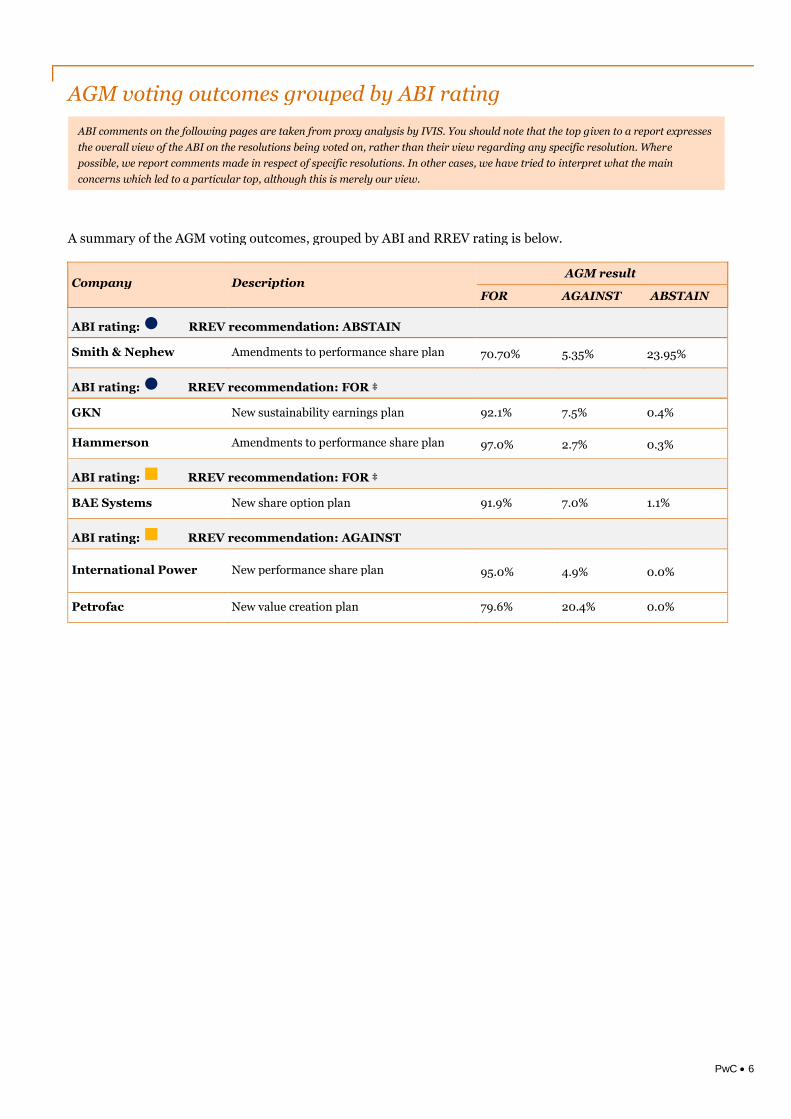

AGM voting outcomes grouped by ABI rating

A summary of the AGM voting outcomes, grouped by ABI and RREV rating is below.

Company DescriptionAGM result

FOR AGAINST ABSTAIN

ABI rating: RREV recommendation: ABSTAIN

Smith & Nephew Amendments to performance share plan 70.70% 5.35% 23.95%

ABI rating: RREV recommendation: FOR ‡

GKN New sustainability earnings plan 92.1% 7.5% 0.4%

Hammerson Amendments to performance share plan 97.0% 2.7% 0.3%

ABI rating: RREV recommendation: FOR ‡

BAE Systems New share option plan 91.9% 7.0% 1.1%

ABI rating: RREV recommendation: AGAINST

International Power New performance share plan 95.0% 4.9% 0.0%

Petrofac New value creation plan 79.6% 20.4% 0.0%

ABI comments on the following pages are taken from proxy analysis by IVIS. You should note that the top given to a report expresses

the overall view of the ABI on the resolutions being voted on, rather than their view regarding any specific resolution. Where

possible, we report comments made in respect of specific resolutions. In other cases, we have tried to interpret what the main

concerns which led to a particular top, although this is merely our view.

PwC 7

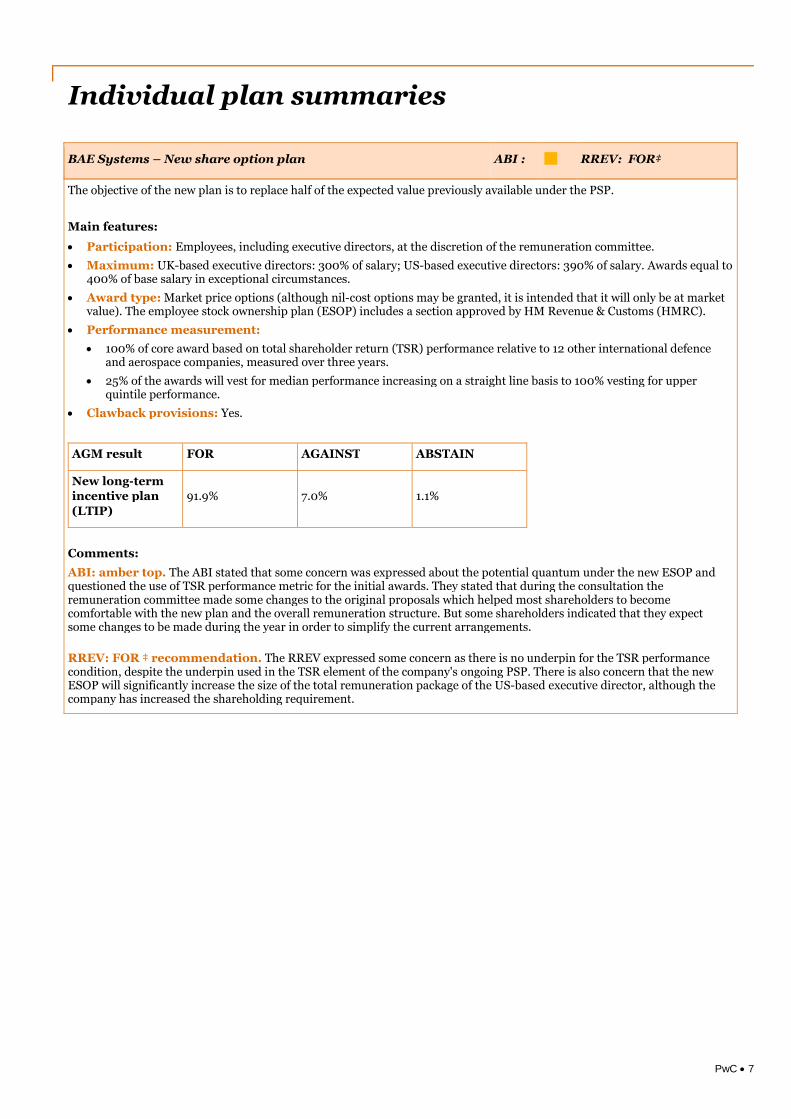

BAE Systems – New share option plan ABI : RREV: FOR‡

The objective of the new plan is to replace half of the expected value previously available under the PSP.

Main features:

Participation: Employees, including executive directors, at the discretion of the remuneration committee.

Maximum: UK-based executive directors: 300% of salary; US-based executive directors: 390% of salary. Awards equal to400% of base salary in exceptional circumstances.

Award type: Market price options (although nil-cost options may be granted, it is intended that it will only be at marketvalue). The employee stock ownership plan (ESOP) includes a section approved by HM Revenue & Customs (HMRC).

Performance measurement:

100% of core award based on total shareholder return (TSR) performance relative to 12 other international defenceand aerospace companies, measured over three years.

25% of the awards will vest for median performance increasing on a straight line basis to 100% vesting for upperquintile performance.

Clawback provisions: Yes.

AGM result FOR AGAINST ABSTAIN

New long-termincentive plan

(LTIP)

91.9% 7.0% 1.1%

Comments:

ABI: amber top. The ABI stated that some concern was expressed about the potential quantum under the new ESOP andquestioned the use of TSR performance metric for the initial awards. They stated that during the consultation theremuneration committee made some changes to the original proposals which helped most shareholders to becomecomfortable with the new plan and the overall remuneration structure. But some shareholders indicated that they expectsome changes to be made during the year in order to simplify the current arrangements.

RREV: FOR ‡ recommendation. The RREV expressed some concern as there is no underpin for the TSR performancecondition, despite the underpin used in the TSR element of the company's ongoing PSP. There is also concern that the newESOP will significantly increase the size of the total remuneration package of the US-based executive director, although thecompany has increased the shareholding requirement.

Individual plan summaries

PwC 8

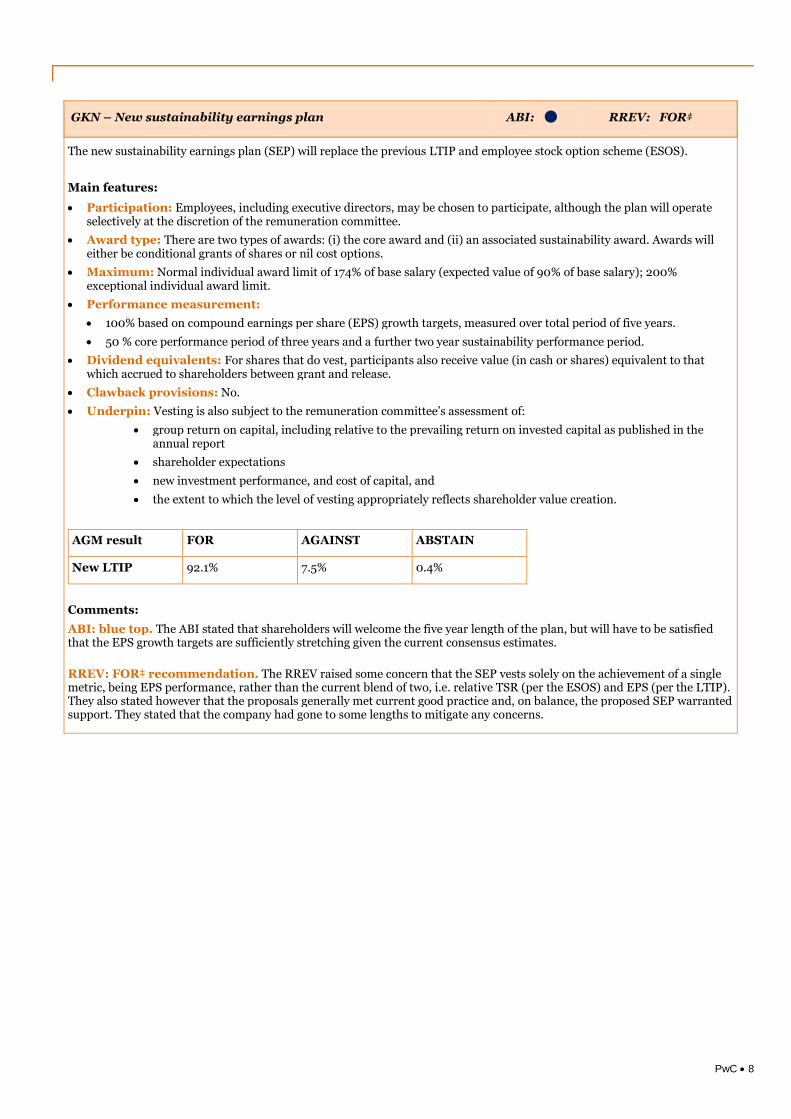

GKN – New sustainability earnings plan ABI: RREV: FOR‡

The new sustainability earnings plan (SEP) will replace the previous LTIP and employee stock option scheme (ESOS).

Main features:

Participation: Employees, including executive directors, may be chosen to participate, although the plan will operateselectively at the discretion of the remuneration committee.

Award type: There are two types of awards: (i) the core award and (ii) an associated sustainability award. Awards willeither be conditional grants of shares or nil cost options.

Maximum: Normal individual award limit of 174% of base salary (expected value of 90% of base salary); 200%exceptional individual award limit.

Performance measurement:

100% based on compound earnings per share (EPS) growth targets, measured over total period of five years.

50 % core performance period of three years and a further two year sustainability performance period.

Dividend equivalents: For shares that do vest, participants also receive value (in cash or shares) equivalent to thatwhich accrued to shareholders between grant and release.

Clawback provisions: No.

Underpin: Vesting is also subject to the remuneration committee’s assessment of:

group return on capital, including relative to the prevailing return on invested capital as published in theannual report

shareholder expectations

new investment performance, and cost of capital, and

the extent to which the level of vesting appropriately reflects shareholder value creation.

AGM result FOR AGAINST ABSTAIN

New LTIP 92.1% 7.5% 0.4%

Comments:

ABI: blue top. The ABI stated that shareholders will welcome the five year length of the plan, but will have to be satisfiedthat the EPS growth targets are sufficiently stretching given the current consensus estimates.

RREV: FOR‡ recommendation. The RREV raised some concern that the SEP vests solely on the achievement of a singlemetric, being EPS performance, rather than the current blend of two, i.e. relative TSR (per the ESOS) and EPS (per the LTIP).They also stated however that the proposals generally met current good practice and, on balance, the proposed SEP warrantedsupport. They stated that the company had gone to some lengths to mitigate any concerns.

PwC 9

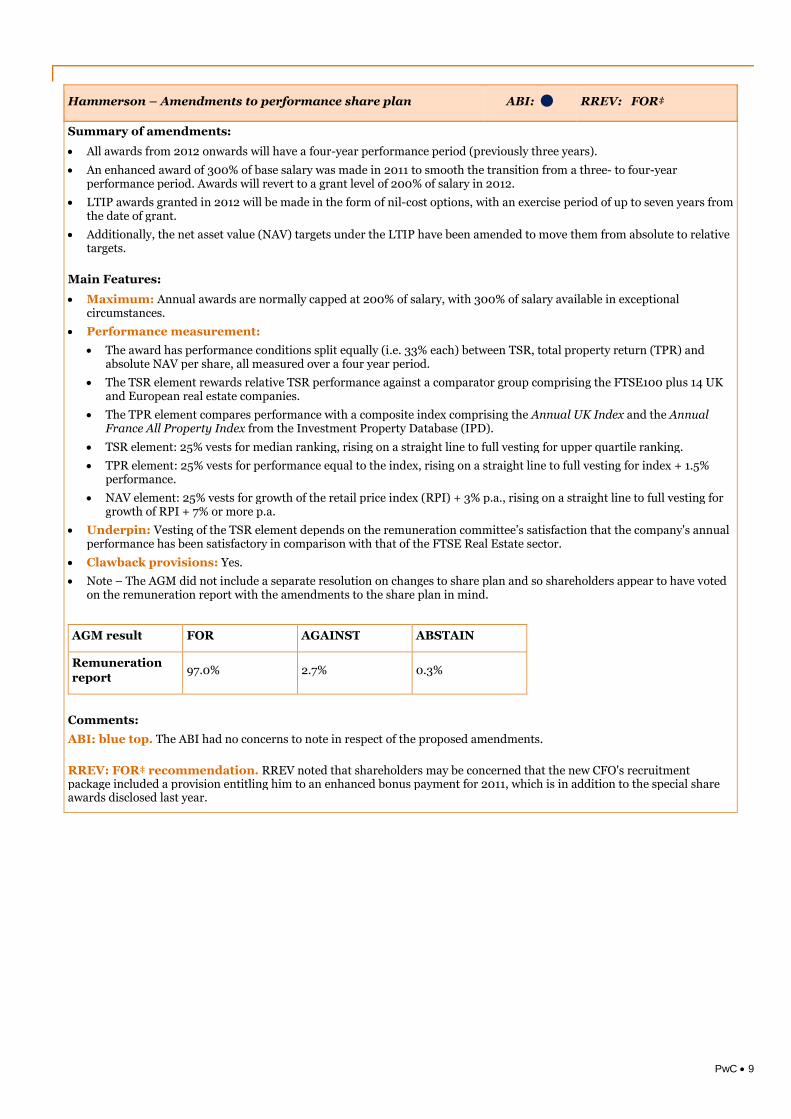

Hammerson – Amendments to performance share plan ABI: RREV: FOR‡

Summary of amendments:

All awards from 2012 onwards will have a four-year performance period (previously three years).

An enhanced award of 300% of base salary was made in 2011 to smooth the transition from a three- to four-yearperformance period. Awards will revert to a grant level of 200% of salary in 2012.

LTIP awards granted in 2012 will be made in the form of nil-cost options, with an exercise period of up to seven years fromthe date of grant.

Additionally, the net asset value (NAV) targets under the LTIP have been amended to move them from absolute to relativetargets.

Main Features:

Maximum: Annual awards are normally capped at 200% of salary, with 300% of salary available in exceptionalcircumstances.

Performance measurement:

The award has performance conditions split equally (i.e. 33% each) between TSR, total property return (TPR) andabsolute NAV per share, all measured over a four year period.

The TSR element rewards relative TSR performance against a comparator group comprising the FTSE100 plus 14 UKand European real estate companies.

The TPR element compares performance with a composite index comprising the Annual UK Index and the AnnualFrance All Property Index from the Investment Property Database (IPD).

TSR element: 25% vests for median ranking, rising on a straight line to full vesting for upper quartile ranking.

TPR element: 25% vests for performance equal to the index, rising on a straight line to full vesting for index + 1.5%performance.

NAV element: 25% vests for growth of the retail price index (RPI) + 3% p.a., rising on a straight line to full vesting forgrowth of RPI + 7% or more p.a.

Underpin: Vesting of the TSR element depends on the remuneration committee’s satisfaction that the company's annualperformance has been satisfactory in comparison with that of the FTSE Real Estate sector.

Clawback provisions: Yes.

Note – The AGM did not include a separate resolution on changes to share plan and so shareholders appear to have votedon the remuneration report with the amendments to the share plan in mind.

AGM result FOR AGAINST ABSTAIN

Remunerationreport

97.0% 2.7% 0.3%

Comments:

ABI: blue top. The ABI had no concerns to note in respect of the proposed amendments.

RREV: FOR‡ recommendation. RREV noted that shareholders may be concerned that the new CFO's recruitmentpackage included a provision entitling him to an enhanced bonus payment for 2011, which is in addition to the special shareawards disclosed last year.

PwC 10

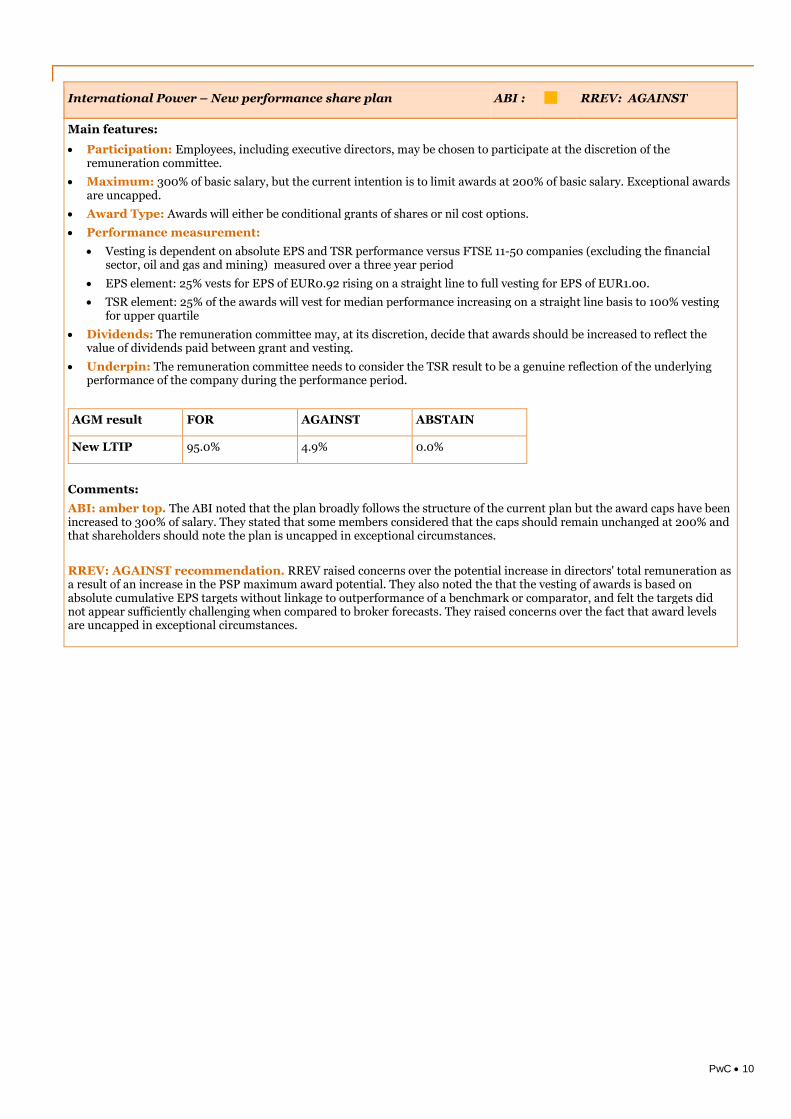

International Power – New performance share plan ABI : RREV: AGAINST

Main features:

Participation: Employees, including executive directors, may be chosen to participate at the discretion of theremuneration committee.

Maximum: 300% of basic salary, but the current intention is to limit awards at 200% of basic salary. Exceptional awardsare uncapped.

Award Type: Awards will either be conditional grants of shares or nil cost options.

Performance measurement:

Vesting is dependent on absolute EPS and TSR performance versus FTSE 11-50 companies (excluding the financialsector, oil and gas and mining) measured over a three year period

EPS element: 25% vests for EPS of EUR0.92 rising on a straight line to full vesting for EPS of EUR1.00.

TSR element: 25% of the awards will vest for median performance increasing on a straight line basis to 100% vestingfor upper quartile

Dividends: The remuneration committee may, at its discretion, decide that awards should be increased to reflect thevalue of dividends paid between grant and vesting.

Underpin: The remuneration committee needs to consider the TSR result to be a genuine reflection of the underlyingperformance of the company during the performance period.

AGM result FOR AGAINST ABSTAIN

New LTIP 95.0% 4.9% 0.0%

Comments:

ABI: amber top. The ABI noted that the plan broadly follows the structure of the current plan but the award caps have beenincreased to 300% of salary. They stated that some members considered that the caps should remain unchanged at 200% andthat shareholders should note the plan is uncapped in exceptional circumstances.

RREV: AGAINST recommendation. RREV raised concerns over the potential increase in directors' total remuneration asa result of an increase in the PSP maximum award potential. They also noted the that the vesting of awards is based onabsolute cumulative EPS targets without linkage to outperformance of a benchmark or comparator, and felt the targets didnot appear sufficiently challenging when compared to broker forecasts. They raised concerns over the fact that award levelsare uncapped in exceptional circumstances.

PwC 11

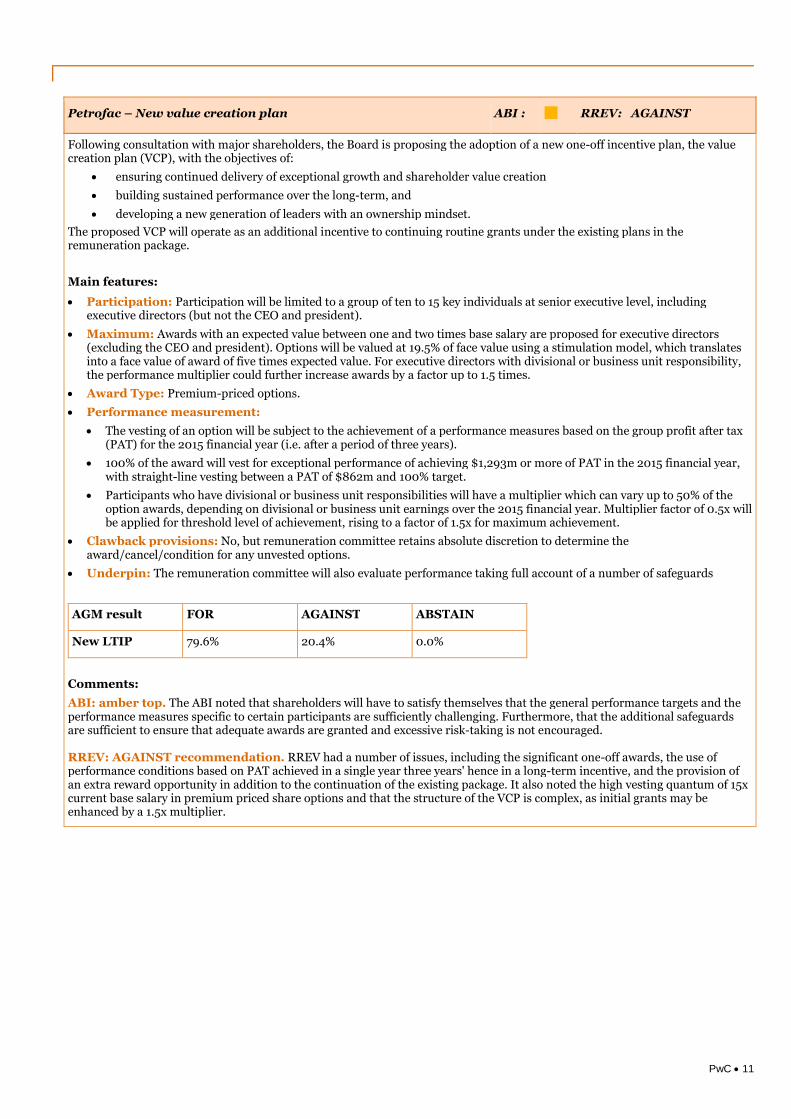

Petrofac – New value creation plan ABI : RREV: AGAINST

Following consultation with major shareholders, the Board is proposing the adoption of a new one-off incentive plan, the valuecreation plan (VCP), with the objectives of:

ensuring continued delivery of exceptional growth and shareholder value creation

building sustained performance over the long-term, and

developing a new generation of leaders with an ownership mindset.

The proposed VCP will operate as an additional incentive to continuing routine grants under the existing plans in theremuneration package.

Main features:

Participation: Participation will be limited to a group of ten to 15 key individuals at senior executive level, includingexecutive directors (but not the CEO and president).

Maximum: Awards with an expected value between one and two times base salary are proposed for executive directors(excluding the CEO and president). Options will be valued at 19.5% of face value using a stimulation model, which translatesinto a face value of award of five times expected value. For executive directors with divisional or business unit responsibility,the performance multiplier could further increase awards by a factor up to 1.5 times.

Award Type: Premium-priced options.

Performance measurement:

The vesting of an option will be subject to the achievement of a performance measures based on the group profit after tax(PAT) for the 2015 financial year (i.e. after a period of three years).

100% of the award will vest for exceptional performance of achieving $1,293m or more of PAT in the 2015 financial year,with straight-line vesting between a PAT of $862m and 100% target.

Participants who have divisional or business unit responsibilities will have a multiplier which can vary up to 50% of theoption awards, depending on divisional or business unit earnings over the 2015 financial year. Multiplier factor of 0.5x willbe applied for threshold level of achievement, rising to a factor of 1.5x for maximum achievement.

Clawback provisions: No, but remuneration committee retains absolute discretion to determine theaward/cancel/condition for any unvested options.

Underpin: The remuneration committee will also evaluate performance taking full account of a number of safeguards

AGM result FOR AGAINST ABSTAIN

New LTIP 79.6% 20.4% 0.0%

Comments:

ABI: amber top. The ABI noted that shareholders will have to satisfy themselves that the general performance targets and theperformance measures specific to certain participants are sufficiently challenging. Furthermore, that the additional safeguardsare sufficient to ensure that adequate awards are granted and excessive risk-taking is not encouraged.

RREV: AGAINST recommendation. RREV had a number of issues, including the significant one-off awards, the use ofperformance conditions based on PAT achieved in a single year three years' hence in a long-term incentive, and the provision ofan extra reward opportunity in addition to the continuation of the existing package. It also noted the high vesting quantum of 15xcurrent base salary in premium priced share options and that the structure of the VCP is complex, as initial grants may beenhanced by a 1.5x multiplier.

PwC 12

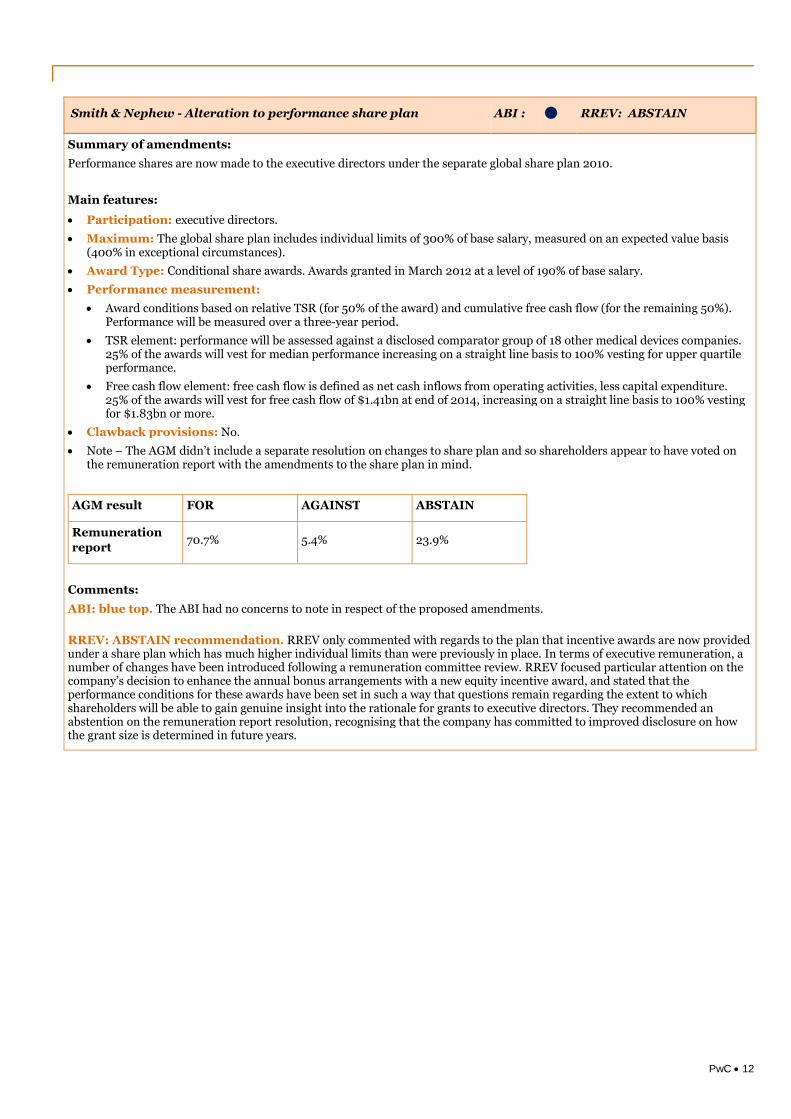

Smith & Nephew - Alteration to performance share plan ABI : RREV: ABSTAIN

Summary of amendments:

Performance shares are now made to the executive directors under the separate global share plan 2010.

Main features:

Participation: executive directors.

Maximum: The global share plan includes individual limits of 300% of base salary, measured on an expected value basis(400% in exceptional circumstances).

Award Type: Conditional share awards. Awards granted in March 2012 at a level of 190% of base salary.

Performance measurement:

Award conditions based on relative TSR (for 50% of the award) and cumulative free cash flow (for the remaining 50%).Performance will be measured over a three-year period.

TSR element: performance will be assessed against a disclosed comparator group of 18 other medical devices companies.25% of the awards will vest for median performance increasing on a straight line basis to 100% vesting for upper quartileperformance.

Free cash flow element: free cash flow is defined as net cash inflows from operating activities, less capital expenditure.25% of the awards will vest for free cash flow of $1.41bn at end of 2014, increasing on a straight line basis to 100% vestingfor $1.83bn or more.

Clawback provisions: No.

Note – The AGM didn’t include a separate resolution on changes to share plan and so shareholders appear to have voted onthe remuneration report with the amendments to the share plan in mind.

AGM result FOR AGAINST ABSTAIN

Remuneration

report70.7% 5.4% 23.9%

Comments:

ABI: blue top. The ABI had no concerns to note in respect of the proposed amendments.

RREV: ABSTAIN recommendation. RREV only commented with regards to the plan that incentive awards are now providedunder a share plan which has much higher individual limits than were previously in place. In terms of executive remuneration, anumber of changes have been introduced following a remuneration committee review. RREV focused particular attention on thecompany’s decision to enhance the annual bonus arrangements with a new equity incentive award, and stated that theperformance conditions for these awards have been set in such a way that questions remain regarding the extent to whichshareholders will be able to gain genuine insight into the rationale for grants to executive directors. They recommended anabstention on the remuneration report resolution, recognising that the company has committed to improved disclosure on howthe grant size is determined in future years.

PwC 13

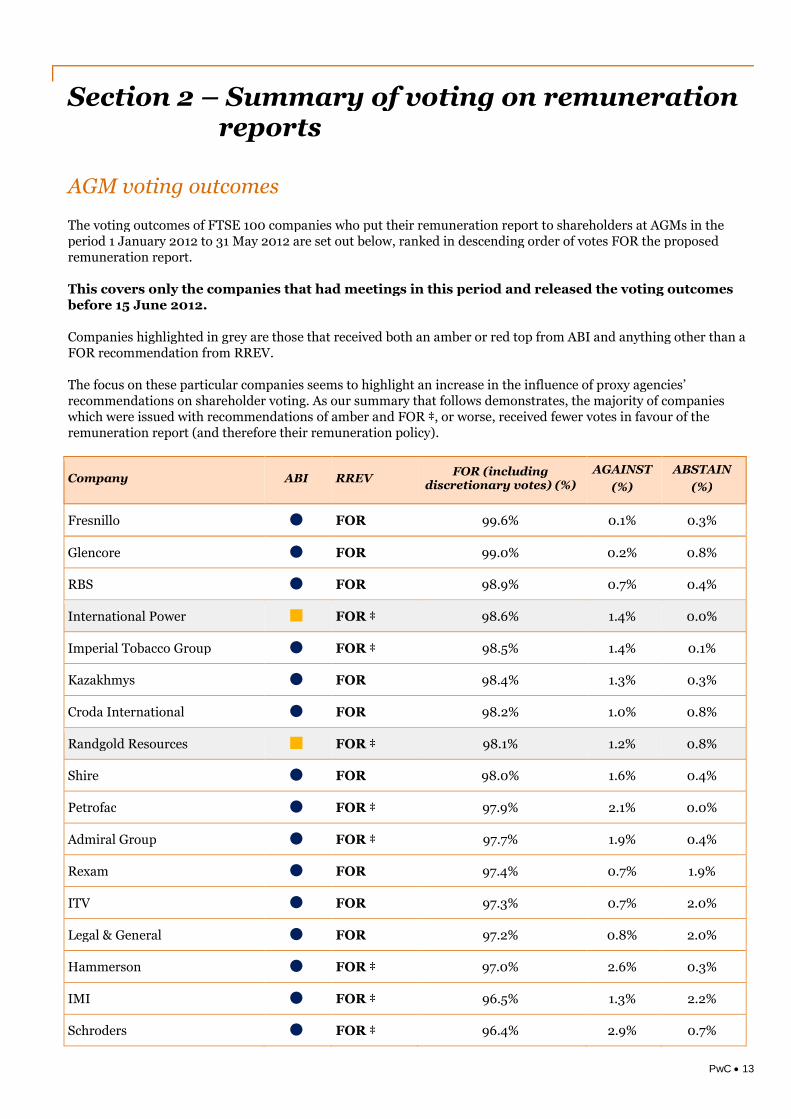

Section 2 – Summary of voting on remunerationreports

AGM voting outcomes

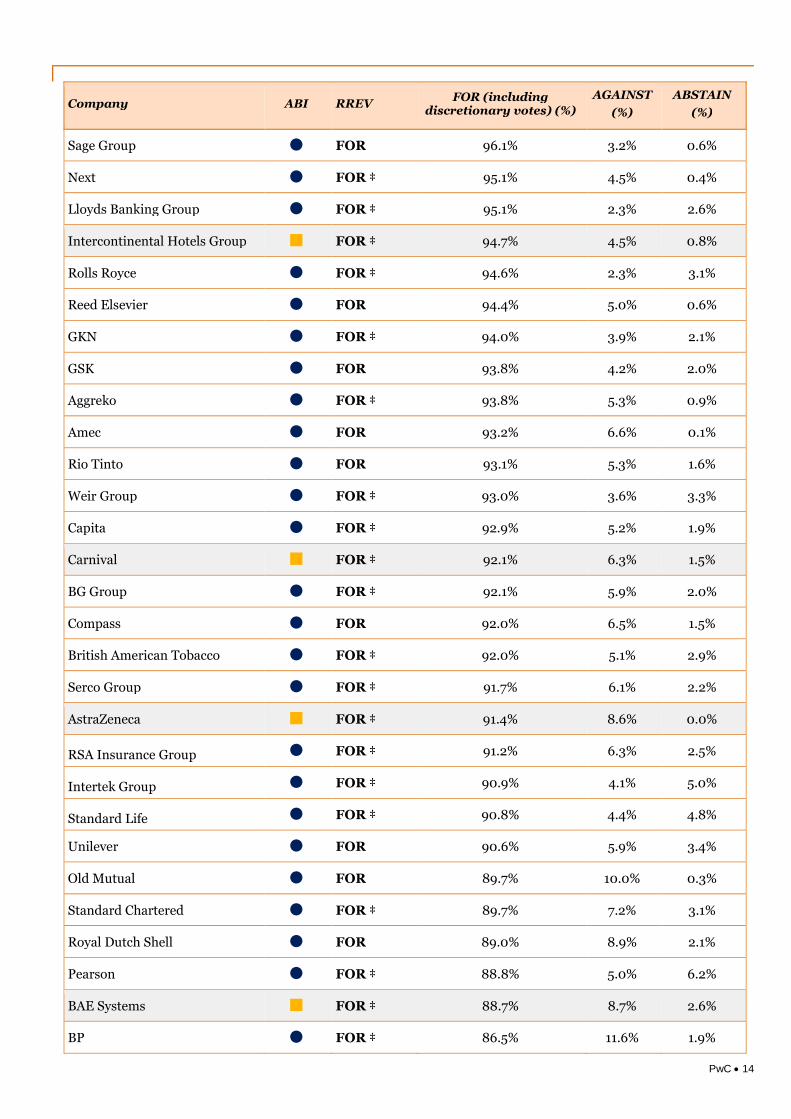

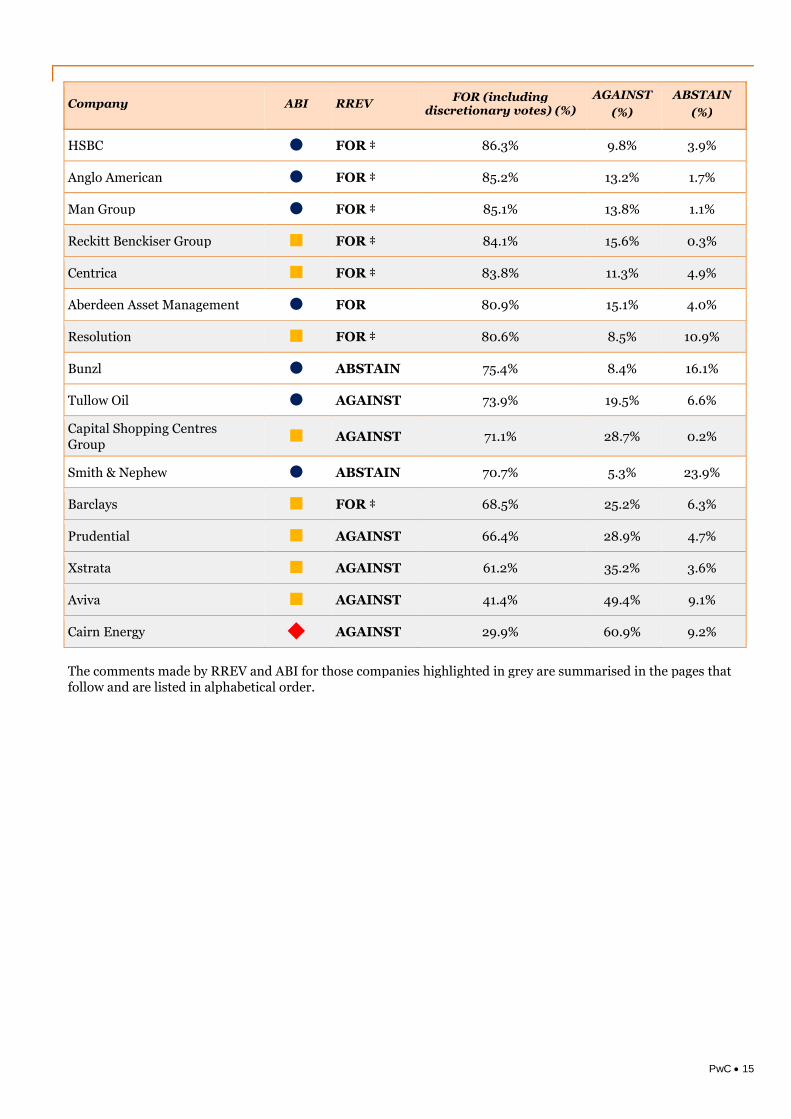

The voting outcomes of FTSE 100 companies who put their remuneration report to shareholders at AGMs in theperiod 1 January 2012 to 31 May 2012 are set out below, ranked in descending order of votes FOR the proposedremuneration report.

This covers only the companies that had meetings in this period and released the voting outcomesbefore 15 June 2012.

Companies highlighted in grey are those that received both an amber or red top from ABI and anything other than aFOR recommendation from RREV.

The focus on these particular companies seems to highlight an increase in the influence of proxy agencies’recommendations on shareholder voting. As our summary that follows demonstrates, the majority of companieswhich were issued with recommendations of amber and FOR ‡, or worse, received fewer votes in favour of theremuneration report (and therefore their remuneration policy).

Company ABI RREVFOR (including

discretionary votes) (%)

AGAINST

(%)

ABSTAIN

(%)

Fresnillo FOR 99.6% 0.1% 0.3%

Glencore FOR 99.0% 0.2% 0.8%

RBS FOR 98.9% 0.7% 0.4%

International Power FOR ‡ 98.6% 1.4% 0.0%

Imperial Tobacco Group FOR ‡ 98.5% 1.4% 0.1%

Kazakhmys FOR 98.4% 1.3% 0.3%

Croda International FOR 98.2% 1.0% 0.8%

Randgold Resources FOR ‡ 98.1% 1.2% 0.8%

Shire FOR 98.0% 1.6% 0.4%

Petrofac FOR ‡ 97.9% 2.1% 0.0%

Admiral Group FOR ‡ 97.7% 1.9% 0.4%

Rexam FOR 97.4% 0.7% 1.9%

ITV FOR 97.3% 0.7% 2.0%

Legal & General FOR 97.2% 0.8% 2.0%

Hammerson FOR ‡ 97.0% 2.6% 0.3%

IMI FOR ‡ 96.5% 1.3% 2.2%

Schroders FOR ‡ 96.4% 2.9% 0.7%

PwC 14

Company ABI RREVFOR (including

discretionary votes) (%)

AGAINST

(%)

ABSTAIN

(%)

Sage Group FOR 96.1% 3.2% 0.6%

Next FOR ‡ 95.1% 4.5% 0.4%

Lloyds Banking Group FOR ‡ 95.1% 2.3% 2.6%

Intercontinental Hotels Group FOR ‡ 94.7% 4.5% 0.8%

Rolls Royce FOR ‡ 94.6% 2.3% 3.1%

Reed Elsevier FOR 94.4% 5.0% 0.6%

GKN FOR ‡ 94.0% 3.9% 2.1%

GSK FOR 93.8% 4.2% 2.0%

Aggreko FOR ‡ 93.8% 5.3% 0.9%

Amec FOR 93.2% 6.6% 0.1%

Rio Tinto FOR 93.1% 5.3% 1.6%

Weir Group FOR ‡ 93.0% 3.6% 3.3%

Capita FOR ‡ 92.9% 5.2% 1.9%

Carnival FOR ‡ 92.1% 6.3% 1.5%

BG Group FOR ‡ 92.1% 5.9% 2.0%

Compass FOR 92.0% 6.5% 1.5%

British American Tobacco FOR ‡ 92.0% 5.1% 2.9%

Serco Group FOR ‡ 91.7% 6.1% 2.2%

AstraZeneca FOR ‡ 91.4% 8.6% 0.0%

RSA Insurance Group FOR ‡ 91.2% 6.3% 2.5%

Intertek Group FOR ‡ 90.9% 4.1% 5.0%

Standard Life FOR ‡ 90.8% 4.4% 4.8%

Unilever FOR 90.6% 5.9% 3.4%

Old Mutual FOR 89.7% 10.0% 0.3%

Standard Chartered FOR ‡ 89.7% 7.2% 3.1%

Royal Dutch Shell FOR 89.0% 8.9% 2.1%

Pearson FOR ‡ 88.8% 5.0% 6.2%

BAE Systems FOR ‡ 88.7% 8.7% 2.6%

BP FOR ‡ 86.5% 11.6% 1.9%

PwC 15

Company ABI RREVFOR (including

discretionary votes) (%)

AGAINST

(%)

ABSTAIN

(%)

HSBC FOR ‡ 86.3% 9.8% 3.9%

Anglo American FOR ‡ 85.2% 13.2% 1.7%

Man Group FOR ‡ 85.1% 13.8% 1.1%

Reckitt Benckiser Group FOR ‡ 84.1% 15.6% 0.3%

Centrica FOR ‡ 83.8% 11.3% 4.9%

Aberdeen Asset Management FOR 80.9% 15.1% 4.0%

Resolution FOR ‡ 80.6% 8.5% 10.9%

Bunzl ABSTAIN 75.4% 8.4% 16.1%

Tullow Oil AGAINST 73.9% 19.5% 6.6%

Capital Shopping CentresGroup AGAINST 71.1% 28.7% 0.2%

Smith & Nephew ABSTAIN 70.7% 5.3% 23.9%

Barclays FOR ‡ 68.5% 25.2% 6.3%

Prudential AGAINST 66.4% 28.9% 4.7%

Xstrata AGAINST 61.2% 35.2% 3.6%

Aviva AGAINST 41.4% 49.4% 9.1%

Cairn Energy AGAINST 29.9% 60.9% 9.2%

The comments made by RREV and ABI for those companies highlighted in grey are summarised in the pages thatfollow and are listed in alphabetical order.

PwC 16

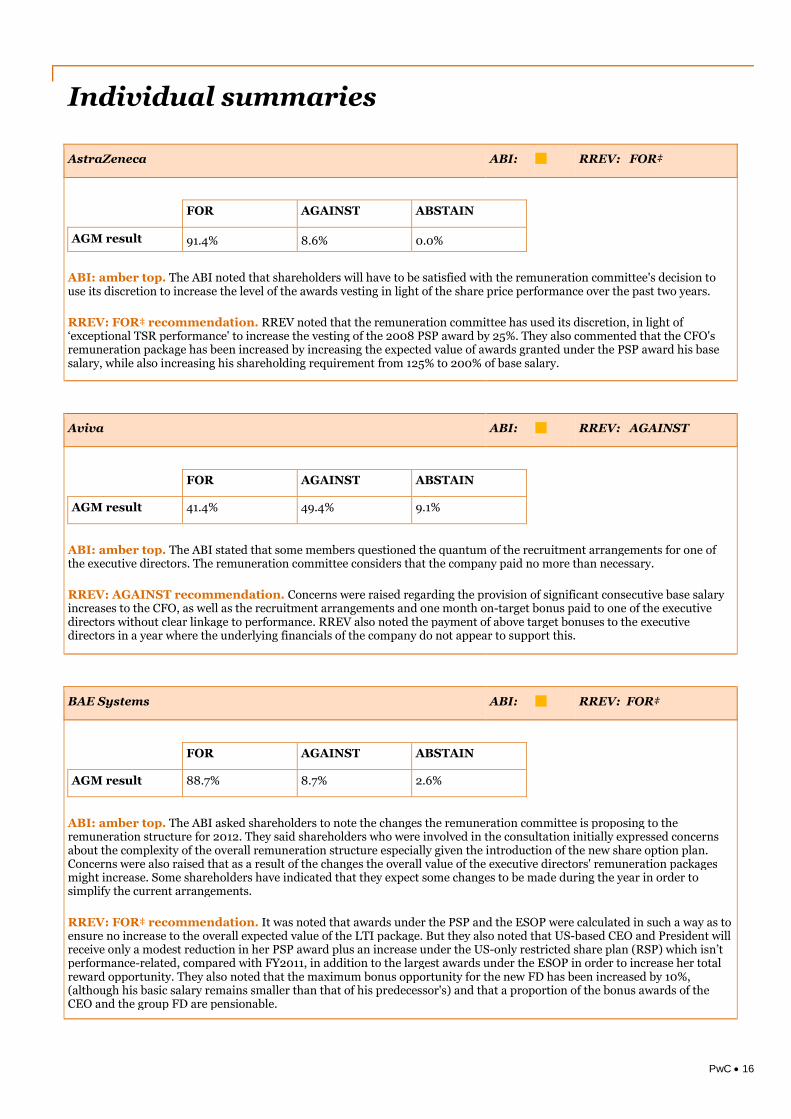

Individual summaries

AstraZeneca ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 91.4% 8.6% 0.0%

ABI: amber top. The ABI noted that shareholders will have to be satisfied with the remuneration committee's decision touse its discretion to increase the level of the awards vesting in light of the share price performance over the past two years.

RREV: FOR‡ recommendation. RREV noted that the remuneration committee has used its discretion, in light of‘exceptional TSR performance' to increase the vesting of the 2008 PSP award by 25%. They also commented that the CFO'sremuneration package has been increased by increasing the expected value of awards granted under the PSP award his basesalary, while also increasing his shareholding requirement from 125% to 200% of base salary.

Aviva ABI: RREV: AGAINST

FOR AGAINST ABSTAIN

AGM result 41.4% 49.4% 9.1%

ABI: amber top. The ABI stated that some members questioned the quantum of the recruitment arrangements for one ofthe executive directors. The remuneration committee considers that the company paid no more than necessary.

RREV: AGAINST recommendation. Concerns were raised regarding the provision of significant consecutive base salaryincreases to the CFO, as well as the recruitment arrangements and one month on-target bonus paid to one of the executivedirectors without clear linkage to performance. RREV also noted the payment of above target bonuses to the executivedirectors in a year where the underlying financials of the company do not appear to support this.

BAE Systems ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 88.7% 8.7% 2.6%

ABI: amber top. The ABI asked shareholders to note the changes the remuneration committee is proposing to theremuneration structure for 2012. They said shareholders who were involved in the consultation initially expressed concernsabout the complexity of the overall remuneration structure especially given the introduction of the new share option plan.Concerns were also raised that as a result of the changes the overall value of the executive directors' remuneration packagesmight increase. Some shareholders have indicated that they expect some changes to be made during the year in order tosimplify the current arrangements.

RREV: FOR‡ recommendation. It was noted that awards under the PSP and the ESOP were calculated in such a way as toensure no increase to the overall expected value of the LTI package. But they also noted that US-based CEO and President willreceive only a modest reduction in her PSP award plus an increase under the US-only restricted share plan (RSP) which isn’tperformance-related, compared with FY2011, in addition to the largest awards under the ESOP in order to increase her totalreward opportunity. They also noted that the maximum bonus opportunity for the new FD has been increased by 10%,(although his basic salary remains smaller than that of his predecessor's) and that a proportion of the bonus awards of theCEO and the group FD are pensionable.

PwC 17

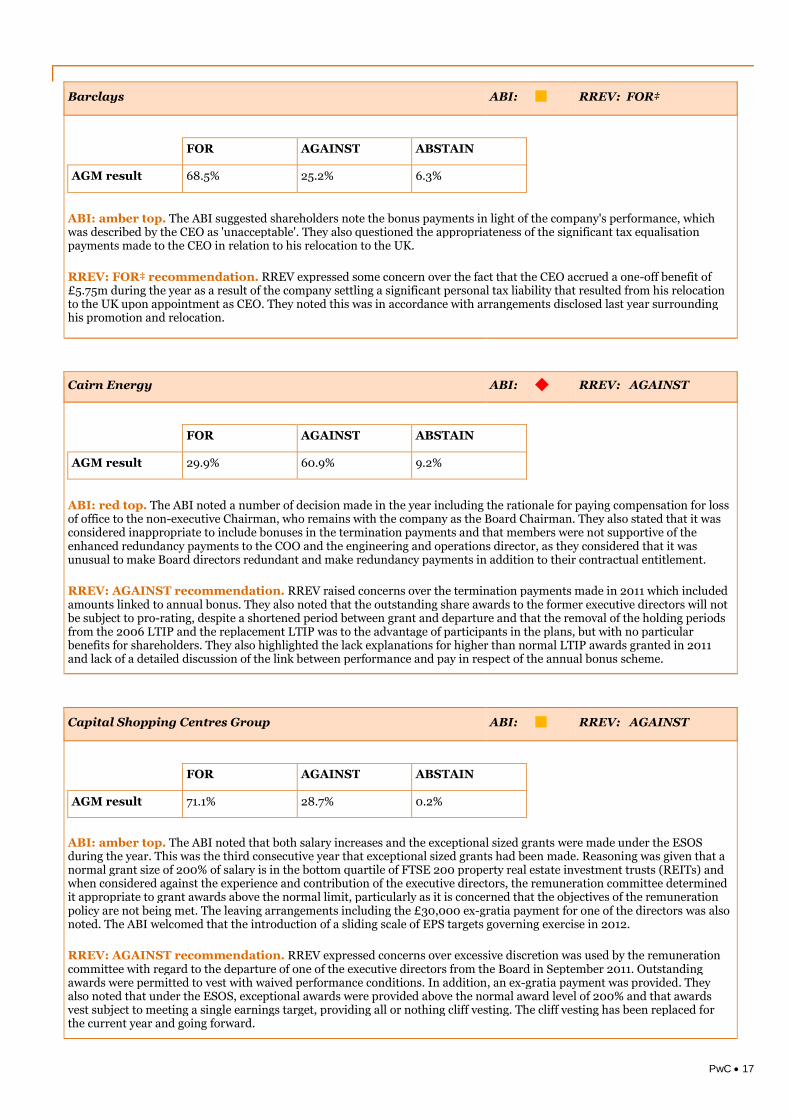

Barclays ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 68.5% 25.2% 6.3%

ABI: amber top. The ABI suggested shareholders note the bonus payments in light of the company's performance, whichwas described by the CEO as 'unacceptable'. They also questioned the appropriateness of the significant tax equalisationpayments made to the CEO in relation to his relocation to the UK.

RREV: FOR‡ recommendation. RREV expressed some concern over the fact that the CEO accrued a one-off benefit of£5.75m during the year as a result of the company settling a significant personal tax liability that resulted from his relocationto the UK upon appointment as CEO. They noted this was in accordance with arrangements disclosed last year surroundinghis promotion and relocation.

Cairn Energy ABI: RREV: AGAINST

FOR AGAINST ABSTAIN

AGM result 29.9% 60.9% 9.2%

ABI: red top. The ABI noted a number of decision made in the year including the rationale for paying compensation for lossof office to the non-executive Chairman, who remains with the company as the Board Chairman. They also stated that it wasconsidered inappropriate to include bonuses in the termination payments and that members were not supportive of theenhanced redundancy payments to the COO and the engineering and operations director, as they considered that it wasunusual to make Board directors redundant and make redundancy payments in addition to their contractual entitlement.

RREV: AGAINST recommendation. RREV raised concerns over the termination payments made in 2011 which includedamounts linked to annual bonus. They also noted that the outstanding share awards to the former executive directors will notbe subject to pro-rating, despite a shortened period between grant and departure and that the removal of the holding periodsfrom the 2006 LTIP and the replacement LTIP was to the advantage of participants in the plans, but with no particularbenefits for shareholders. They also highlighted the lack explanations for higher than normal LTIP awards granted in 2011and lack of a detailed discussion of the link between performance and pay in respect of the annual bonus scheme.

Capital Shopping Centres Group ABI: RREV: AGAINST

FOR AGAINST ABSTAIN

AGM result 71.1% 28.7% 0.2%

ABI: amber top. The ABI noted that both salary increases and the exceptional sized grants were made under the ESOSduring the year. This was the third consecutive year that exceptional sized grants had been made. Reasoning was given that anormal grant size of 200% of salary is in the bottom quartile of FTSE 200 property real estate investment trusts (REITs) andwhen considered against the experience and contribution of the executive directors, the remuneration committee determinedit appropriate to grant awards above the normal limit, particularly as it is concerned that the objectives of the remunerationpolicy are not being met. The leaving arrangements including the £30,000 ex-gratia payment for one of the directors was alsonoted. The ABI welcomed that the introduction of a sliding scale of EPS targets governing exercise in 2012.

RREV: AGAINST recommendation. RREV expressed concerns over excessive discretion was used by the remunerationcommittee with regard to the departure of one of the executive directors from the Board in September 2011. Outstandingawards were permitted to vest with waived performance conditions. In addition, an ex-gratia payment was provided. Theyalso noted that under the ESOS, exceptional awards were provided above the normal award level of 200% and that awardsvest subject to meeting a single earnings target, providing all or nothing cliff vesting. The cliff vesting has been replaced forthe current year and going forward.

PwC 18

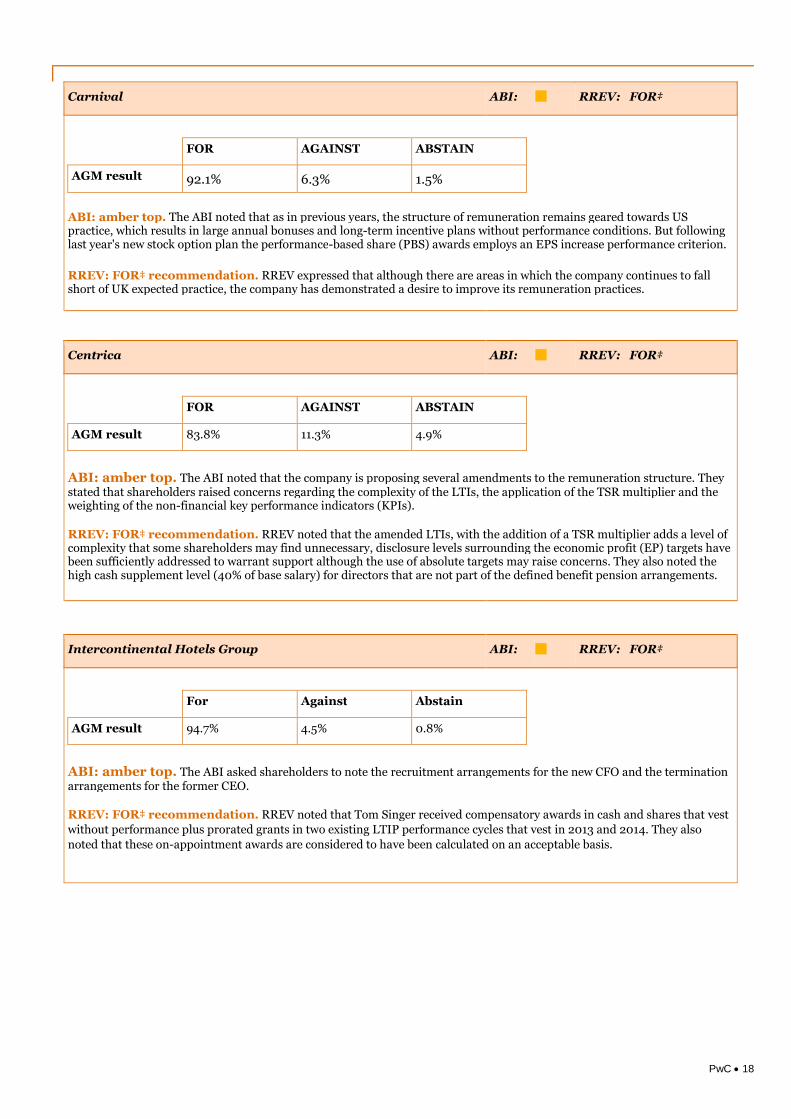

Carnival ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 92.1% 6.3% 1.5%

ABI: amber top. The ABI noted that as in previous years, the structure of remuneration remains geared towards USpractice, which results in large annual bonuses and long-term incentive plans without performance conditions. But followinglast year's new stock option plan the performance-based share (PBS) awards employs an EPS increase performance criterion.

RREV: FOR‡ recommendation. RREV expressed that although there are areas in which the company continues to fallshort of UK expected practice, the company has demonstrated a desire to improve its remuneration practices.

Centrica ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 83.8% 11.3% 4.9%

ABI: amber top. The ABI noted that the company is proposing several amendments to the remuneration structure. Theystated that shareholders raised concerns regarding the complexity of the LTIs, the application of the TSR multiplier and theweighting of the non-financial key performance indicators (KPIs).

RREV: FOR‡ recommendation. RREV noted that the amended LTIs, with the addition of a TSR multiplier adds a level ofcomplexity that some shareholders may find unnecessary, disclosure levels surrounding the economic profit (EP) targets havebeen sufficiently addressed to warrant support although the use of absolute targets may raise concerns. They also noted thehigh cash supplement level (40% of base salary) for directors that are not part of the defined benefit pension arrangements.

Intercontinental Hotels Group ABI: RREV: FOR‡

For Against Abstain

AGM result 94.7% 4.5% 0.8%

ABI: amber top. The ABI asked shareholders to note the recruitment arrangements for the new CFO and the terminationarrangements for the former CEO.

RREV: FOR‡ recommendation. RREV noted that Tom Singer received compensatory awards in cash and shares that vestwithout performance plus prorated grants in two existing LTIP performance cycles that vest in 2013 and 2014. They also

noted that these on-appointment awards are considered to have been calculated on an acceptable basis.

PwC 19

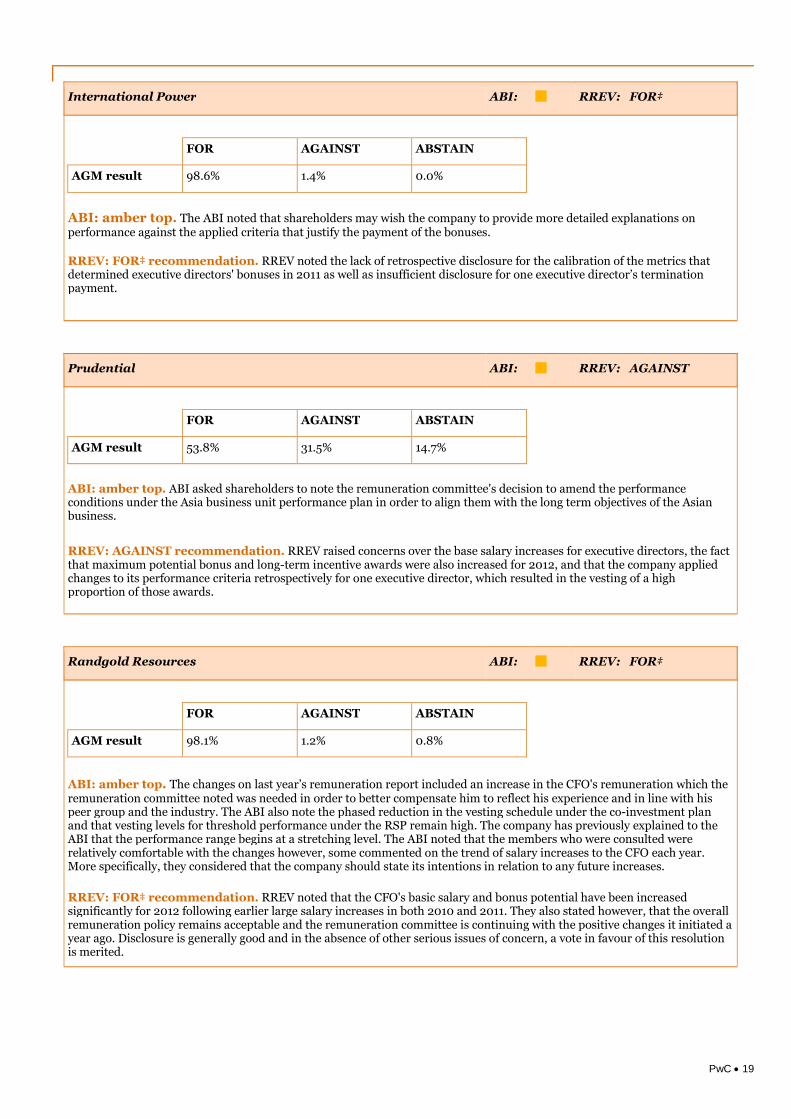

International Power ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 98.6% 1.4% 0.0%

ABI: amber top. The ABI noted that shareholders may wish the company to provide more detailed explanations onperformance against the applied criteria that justify the payment of the bonuses.

RREV: FOR‡ recommendation. RREV noted the lack of retrospective disclosure for the calibration of the metrics thatdetermined executive directors' bonuses in 2011 as well as insufficient disclosure for one executive director’s terminationpayment.

Prudential ABI: RREV: AGAINST

FOR AGAINST ABSTAIN

AGM result 53.8% 31.5% 14.7%

ABI: amber top. ABI asked shareholders to note the remuneration committee's decision to amend the performanceconditions under the Asia business unit performance plan in order to align them with the long term objectives of the Asianbusiness.

RREV: AGAINST recommendation. RREV raised concerns over the base salary increases for executive directors, the factthat maximum potential bonus and long-term incentive awards were also increased for 2012, and that the company appliedchanges to its performance criteria retrospectively for one executive director, which resulted in the vesting of a highproportion of those awards.

Randgold Resources ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 98.1% 1.2% 0.8%

ABI: amber top. The changes on last year’s remuneration report included an increase in the CFO's remuneration which theremuneration committee noted was needed in order to better compensate him to reflect his experience and in line with hispeer group and the industry. The ABI also note the phased reduction in the vesting schedule under the co-investment planand that vesting levels for threshold performance under the RSP remain high. The company has previously explained to theABI that the performance range begins at a stretching level. The ABI noted that the members who were consulted wererelatively comfortable with the changes however, some commented on the trend of salary increases to the CFO each year.More specifically, they considered that the company should state its intentions in relation to any future increases.

RREV: FOR‡ recommendation. RREV noted that the CFO's basic salary and bonus potential have been increasedsignificantly for 2012 following earlier large salary increases in both 2010 and 2011. They also stated however, that the overallremuneration policy remains acceptable and the remuneration committee is continuing with the positive changes it initiated ayear ago. Disclosure is generally good and in the absence of other serious issues of concern, a vote in favour of this resolutionis merited.

PwC 20

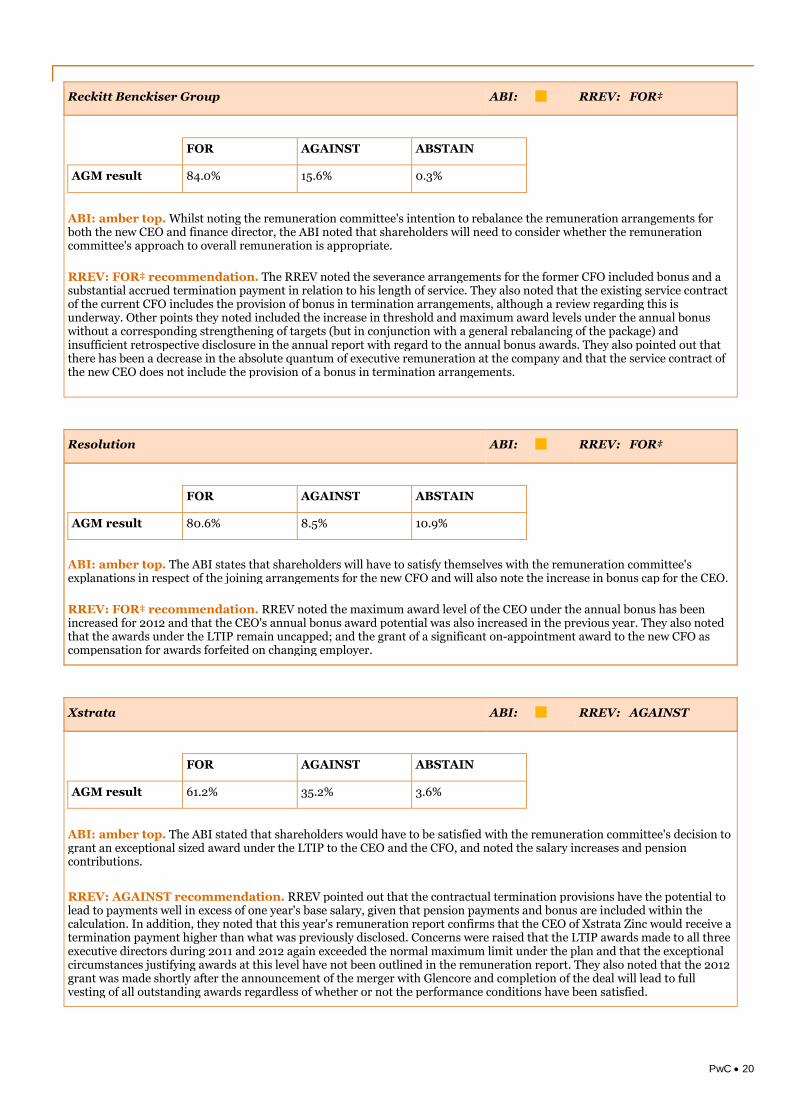

Reckitt Benckiser Group ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 84.0% 15.6% 0.3%

ABI: amber top. Whilst noting the remuneration committee's intention to rebalance the remuneration arrangements forboth the new CEO and finance director, the ABI noted that shareholders will need to consider whether the remunerationcommittee's approach to overall remuneration is appropriate.

RREV: FOR‡ recommendation. The RREV noted the severance arrangements for the former CFO included bonus and asubstantial accrued termination payment in relation to his length of service. They also noted that the existing service contractof the current CFO includes the provision of bonus in termination arrangements, although a review regarding this isunderway. Other points they noted included the increase in threshold and maximum award levels under the annual bonuswithout a corresponding strengthening of targets (but in conjunction with a general rebalancing of the package) andinsufficient retrospective disclosure in the annual report with regard to the annual bonus awards. They also pointed out thatthere has been a decrease in the absolute quantum of executive remuneration at the company and that the service contract ofthe new CEO does not include the provision of a bonus in termination arrangements.

Resolution ABI: RREV: FOR‡

FOR AGAINST ABSTAIN

AGM result 80.6% 8.5% 10.9%

ABI: amber top. The ABI states that shareholders will have to satisfy themselves with the remuneration committee'sexplanations in respect of the joining arrangements for the new CFO and will also note the increase in bonus cap for the CEO.

RREV: FOR‡ recommendation. RREV noted the maximum award level of the CEO under the annual bonus has beenincreased for 2012 and that the CEO's annual bonus award potential was also increased in the previous year. They also notedthat the awards under the LTIP remain uncapped; and the grant of a significant on-appointment award to the new CFO ascompensation for awards forfeited on changing employer.

Xstrata ABI: RREV: AGAINST

FOR AGAINST ABSTAIN

AGM result 61.2% 35.2% 3.6%

ABI: amber top. The ABI stated that shareholders would have to be satisfied with the remuneration committee's decision togrant an exceptional sized award under the LTIP to the CEO and the CFO, and noted the salary increases and pensioncontributions.

RREV: AGAINST recommendation. RREV pointed out that the contractual termination provisions have the potential tolead to payments well in excess of one year's base salary, given that pension payments and bonus are included within thecalculation. In addition, they noted that this year's remuneration report confirms that the CEO of Xstrata Zinc would receive atermination payment higher than what was previously disclosed. Concerns were raised that the LTIP awards made to all threeexecutive directors during 2011 and 2012 again exceeded the normal maximum limit under the plan and that the exceptionalcircumstances justifying awards at this level have not been outlined in the remuneration report. They also noted that the 2012grant was made shortly after the announcement of the merger with Glencore and completion of the deal will lead to fullvesting of all outstanding awards regardless of whether or not the performance conditions have been satisfied.

PwC 21

ABI The Association of British Insurers

AGM Annual general meeting

AOSC Asset optimisation supply chain

CEO Chief executive officer

CFO Chief financial officer

COO Chief operating officer

EP Economic profit

EPS Earnings per share

ESOS Employee share option scheme

ESOP Employee stock ownership plan

FD Finance director

FSA Financial Services Authority

IVIS Institutional Voting Information Service – the service provided by ABI

KPI Key performance indicators

LTIP Long-term incentive plan

NAV Net asset value

PAT Profit after tax

PBS Performance based share

PBT Profit before tax

PSP Performance share plan

REITs Real estate investment trust

RPI Retail price index

RREV Research, Recommendations and Electronic Voting – a joint venture between the NationalAssociation of Pension Funds (NAPF) and Institutional Shareholder Services (ISS)

RSP Restricted share plan

SEP Sustainability earnings plan

TPR Total property return

TSR Total shareholder return

VCP Value creation plan

Glossary

PwC 22

Sean O’HareTel: 020 7804 9264Mob: 07802 739959Email: [email protected]

Roz CrawfordTel: 020 7212 3103Mob: 07801 956376Email: [email protected]

Contacts

PwC 23

This publication has been prepared for general guidance on matters of interest only, anddoes not constitute professional advice. You should not act upon the informationcontained in this publication without obtaining specific professional advice. Norepresentation or warranty (express or implied) is given as to the accuracy orcompleteness of the information contained in this publication, and, to the extentpermitted by law, PricewaterhouseCoopers LLP, its members, employees and agents donot accept or assume any liability, responsibility or duty of care for any consequences ofyou or anyone else acting, or refraining to act, in reliance on the information contained inthis publication or for any decision based on it.

© 2012 PricewaterhouseCoopers LLP. All rights reserved. In this document, "PwC" refersto PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom),which is a member firm of PricewaterhouseCoopers International Limited, each memberfirm of which is a separate legal entity.