Embed Size (px)

Citation preview

On The Transmission of Global Shocks to Latin AmericaBefore and After China’s Emergence in the World

Economy∗

Ambrogio Cesa-BianchiInter-American Development Bank

M. Hashem PesaranUniversity of Cambridge

Alessandro RebucciInter-American Development Bank

Cesar E. TamayoInter-American Development Bank

TengTeng XuUniversity of Cambridge

First Draft: June 4, 2010Preliminary and Incomplete.

Abstract

External shocks are very important for Latin America’s economic performance as the re-cent global crisis vividly illustrated. At the same time, the global economy has undergoneprofound structural changes over the past three decades. This paper investigates howchanged trade linkages between China, Latin America, and the rest of the world maybe affecting the transmission of global shocks to Latin America. Preliminary evidencebased on a GVAR model estimated with quarterly data from 1979(1) to 2008(2) for allmajor advanced and emerging economies of the world show that the impact of a globalGDP shock on the typical Latin American economy may have halved between 1995-97and 2005-07, due to the increased weight of China international trade in total trade forLatin America, the United States, and the euro area. Over the same period, we do notfind evidence of increased impact of regional GDP shocks in Latin America or emergingAsia excluding China as the popular decoupling hypothesis would imply. These resultssuggest that one reason why these regions are doing so well in the aftermath of the globalcrisis is sheer ”good luck”.

Keywords: China, Globalization, Trade Linkages, GVAR, Business Cycle.

JEL Classification Numbers:

∗The views expressed in this paper are exclusively those of the authors and not those of the IDB or itsExecutive Board.

1

1 Introduction

External factors are very important for Latin America’s economic performance as the impact

of the global crisis on the region has vividly illustrated.1 But the world economy has undergone

profound structural changes over the past two-three decades because of globalization and the

emergence of China, India, and other large developing economies (including Mexico and Brazil

in Latin America) as global economic players. As a result, the importance and the transmission

mechanisms of external shocks to Latin American economies may now have changed.

This paper focuses on the emergence of China as a global force in the world economy and

investigates how changed trade patterns between China and the rest of the world may have

affected the impact and transmission of external shocks to Latin America. We focus on China

because, as we shall see, its trade linkages with the rest of the world are those that have

undergone the most dramatic change over the period we consider. Specifically, we address

the following questions: Is the importance of external shocks for the typical Latin American

economy stable over time? What is the role of China and the rest of emerging Asia in the

transmission of global shocks to Latin America? Are shocks originating from the US and the

euro area, which remain the largest trading partners, transmitted differently than shocks from

China and the rest of Asia? Are regional (i.e., LAC shocks) becoming more important over

time for LAC?

To conduct the empirical analysis we use a variant of the global vector autoregression

model (GVAR) originally presented by Pesaran, Schuermann, and Weiner (2004) and further

developed by Dees, di Mauro, Pesaran, and Smith (2007). The model includes 25 major

advanced and emerging economies and the euro area, covering more than 90 percent of world

GDP, and including five large Latin American economies (Argentina, Brazil, Chile, Mexico,

and Peru). The data set is quarterly, starting in 1979(1), and is updated to 2008(2).

One characteristic of the GVAR model is its remarkable parameter stability. Even for Latin

American economies that have experienced frequent changes in policy regime and other deep

structural changes, standard statistical tests do not identify widespread parameter instability.

We build on this strength of the GVAR, and use a different set of trade weights to construct

counter factual simulations of what would the impact of external shocks and their transmission

mechanisms be under alternative configurations of the trade linkages between China and the

rest of the world.

To address the questions above we thus simulate a given set of external shocks in the GVAR

model using alternative sets of trade weights that capture one important aspect of China’s

changed role in the world economy: its new pattern of trade linkages with the rest of the world.

The focus of our study is on real shocks. In particular, we analyze shocks to global output,

to US output, to euro area output, China output, as well as regional (i.e., Latin American and

1For empirical analyses of the impact of external factors on Latin American’s economic performance see,among many other contributions, Little et al (1993), Hoffmaister and Roldos (1998), Canova (2005), Osterholmand Zettelmeyer (2007), Izquierdo, Romero, and Talvi (2008), and Rebucci (2008).

2

Rest of Emerging Asia) output.

Preliminary empirical results show that the importance of a global GDP shock for the

typical Latin American economy may have halved over time. At the same time, we do not

find evidence that regional shocks have increased their importance over time, contrary to the

popular notion of decoupling.

The rest of the paper is organized as follows. In the next section, we discuss how the trade

linkages between China and the rest of the world, and particularly LAC, have evolved over

time. In Section 3, we describe the GVAR model that we use and we discuss its estimation

based on the updated data set we constructed. Section 4 reports the counter factual simulation

results. Section 5 concludes. Two appendices describe in details the update of the data set and

report a full set of the baseline estimation results for the GVAR model based on 2001-03 trade

weights.

2 The Changing Weight of China in the World Economy

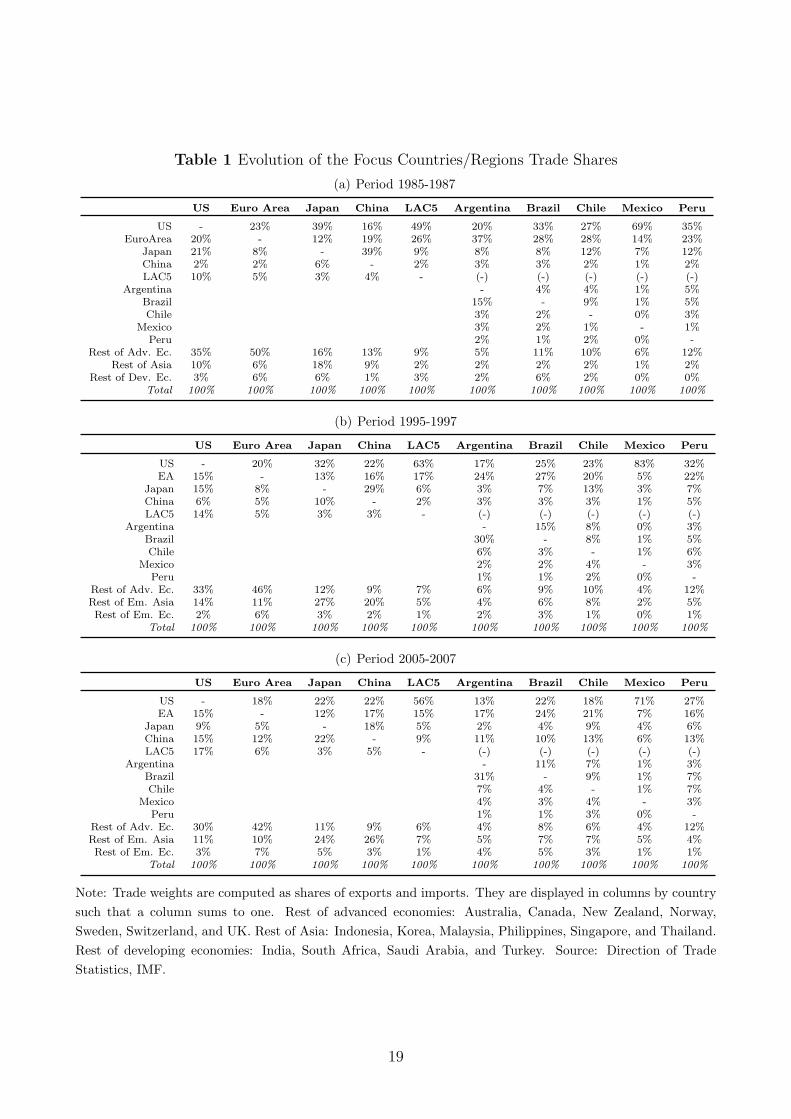

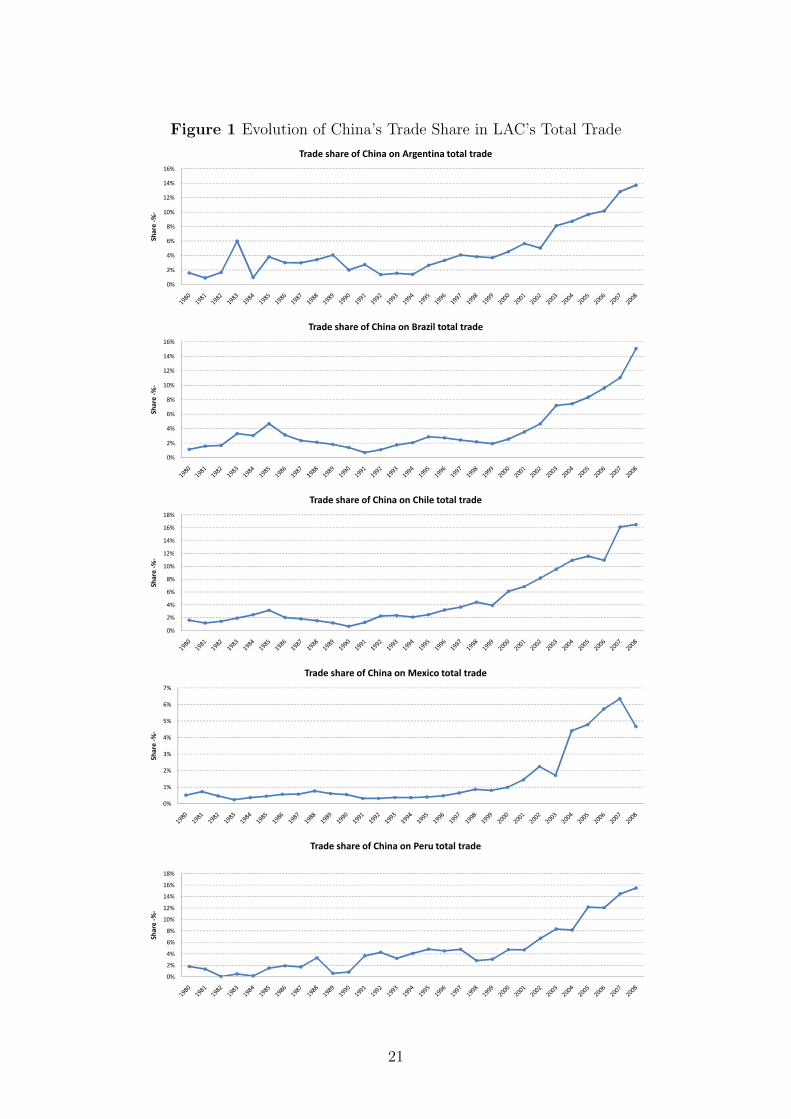

The importance of China for LAC trade has increased more than three-fold over the past

ten years. Figure 1 shows the yearly evolution of China’s trade share in LAC’s total trade.

From this figure we can see that the take off of China’s trade share in LAC trade starts in

the mid-1990s, with little or no change in the previous decade. In Table 1 we report a more

complete set of trade weights for the U.S., euro area, Japan, China and LAC economies (both

individually and as an aggregate), at three different points in time, averaging over 1985-87,

1995-97, and 2005-07, respectively.

As we can see, even at the end of the sample period, the United States and the euro area

continue to be the largest trade partners of LAC, accounting on average for more than 70% of

total trade in the 2005-07 period (the United States 56% and the euro area 15%, respectively).

However their weight in LAC’s total trade is declining over time, as they were 49% and 27% in

the period 1995-97, respectively. In contrast, China’s trade share in LAC’s total trade surged

on average from 2% in 1995-97 to 9% in 2005-07.

China’s emergence as a global economic force affected also the largest economies in the

world: China’s trade share in total trade of the United States, the euro area, and Japan grew

to 12%, 15%, and 22% in 2005-07 from 6%, 5%, and 10% in 1995-97, respectively. Thus, China

may play an even more important role for LAC also through indirect effects via its impact on

LAC’s traditional and largest trading partners.

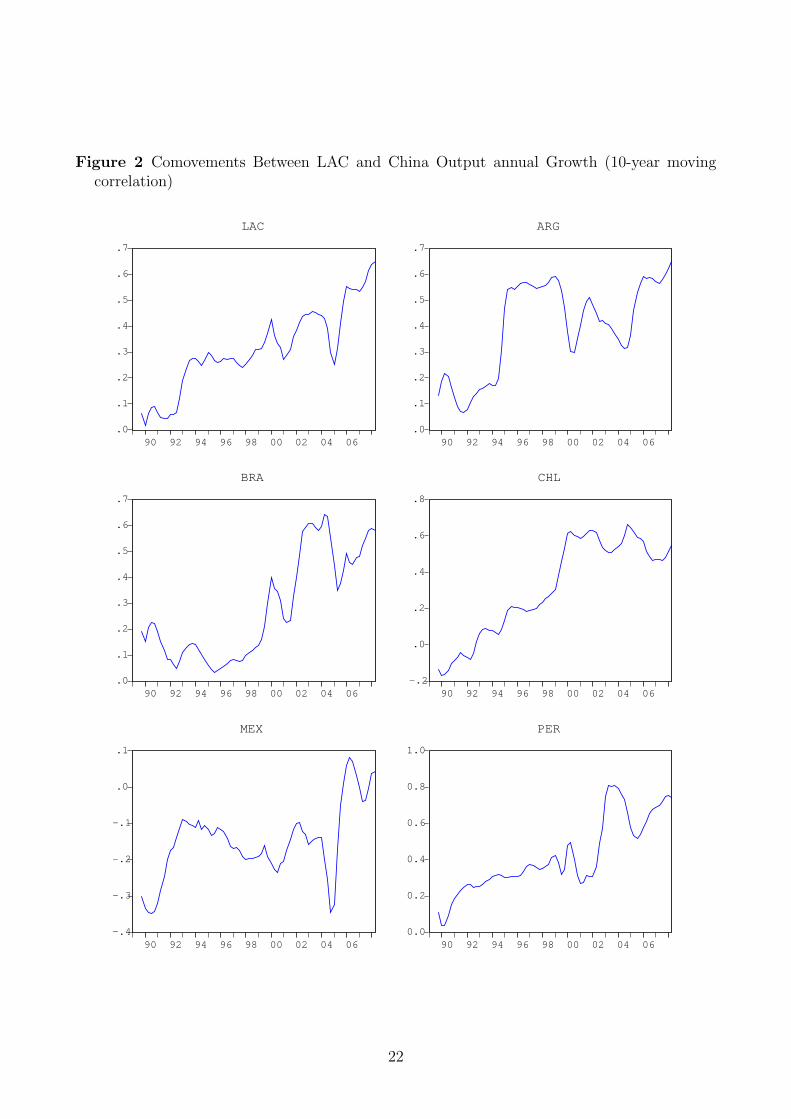

As it is well known, trade integration can lead to either more or less correlated business

cycles among countries.Figure 2 plots a ten-year moving average correlation between output

growth in LAC and in China, which is a rough measure of business cycle synchronization. As we

can see, this correlation increased steadily from the beginning of the nineties to the end of the

sample period. Compared to the period 1995-97, the average correlation in 2005-07 increased

3

by 84%, from 0,27 to 0,49.2 All countries considered display a pattern similar to the regional

one except Mexico, which goes from negative to about zero , and Brazil, which experiences a

650% increase of compared to the 1995-97 period.3

In sum, growing trade linkages between China and the rest of the world (including LAC) as

documented above are clearly associated with more synchronized business cycles between LAC

and China. And as we shall see below, this association can be interpreted as a causation.

3 The GVAR Model

The GVAR modelling strategy consists of three main steps. First, each country is modeled

individually as a small open economy by estimating a country-specific vector error-correction

model in which domestic macroeconomic variables (xit) are related to country-specific foreign

variables (x∗it). Global variables (dt), that are common among all countries such as the oil price,

are also included in each of the country-specific model and assumed to be weakly exogenous.

Second, a restricted reduced-form global model is built stacking the estimated country-specific

models and connecting them through a matrix of trade linkages (W). Third and finally, tak-

ing into account the possibility that the error terms of this restricted reduced form model

are correlated contemporaneously, Generalized Impulse Response Functions (GIRFs) and the

Generalized Forecast Error Variance Decompositions (GFEVDs)—developed in Koop, Pesaran,

and Potter (1996) and Pesaran and Shin (1998)—are computed to analyze the transmission of

shocks and their historical importance.

The foreign country-specific variables, x∗it, play a central role in the GVAR. They are con-

structed as trade-weighted averages of the corresponding variables in all the other countries in

the GVAR model and statistically they are assumed to be weakly exogenous. Thus:

x∗it =

N∑j=0

ωijxjt, (1)

where ωij is the trade weight of country j in the model for country i, with ωii = 0. Note also

that, although the number of countries does not need to be large for the GVAR to work, when

it is small, then, at least for one country this weak exogeneity assumption cannot be satisfied.

It is only when the number of countries tends to infinity and all countries are relatively small

that we can have a symmetric treatment of all of them in the GVAR. For this reason, as we

shall see below, we treat the united United States differently in GVAR.

Consider N +1 countries in the global economy, indexed by i = 0, 1, 2, ...N . In the first step,

2Notice that output growth rate in LAC is computed based on a weighted average of LAC countries outputusing PPP-GDP weights averaged over the period 2001-03. (Source PWT 6.1.)

3This is consistent with the evidence (up to end-2004) reported by Calderon (2008). Interestingly, Calderon(2008) finds that such an increased output correlation with China is better explained by China’s share of totaltrade of third parties and its large demand share in commodity markets rather than direct bilateral tradelinkages between LAC and China.

4

each country i is represented by a vector autoregressive model for the xit augmented by weakly

exogenous variables. Specifically a VARX*(pi,qi) model, in which the (ki × 1) country-specific

domestic variables are related to the (k∗i ×1) foreign-specific and (md×1) global variables, plus

constant and a deterministic time trend is set up for each country i:

Φi(L, pi)xit = ai0 + ai1t + Υi(L, qi)dt + Λi(L, qi)x∗it + uit, (2)

for i = 0, 1, ..., N and t = 1, ..., T . Notice that: Φi(L, pi) = I −∑pi

i=1 ΦiLi is the matrix lag

polynomial of the coefficients associated to the xit; ai0 is a ki × 1 vector of fixed intercepts; ai1

is a ki × 1 vector of coefficients of the deterministic time trend; Υi(L, qi) =∑qi

i=0 ΥiLi is the

matrix lag polynomial the coefficients associated to the dt; Λi(L, qi) =∑qi

i=0 ΛiLi is the matrix

lag polynomial of the coefficients associated to the x∗it; uit is a ki × 1 vector of country-specific

shocks, which we assume serially uncorrelated, with zero mean, and nonsingular covariance

matrix, uit ∼ i.i.d.(0,Σii). Notice also that for estimation purposes Φi(L, pi), Υi(L, qi), and

Λi(L, qi) can be treated as unrestricted and can differ across countries.

The error correction form of equation (2) may be written as

∆xit = ci0 − αiβ′i[ζ i,t−1 − γi(t− 1)] (3)

+ Υi0∆dt + Λi0∆x∗it + Υi1∆dt−1 + Γi∆zi,t−1 + uit,

where zit = (x′it,x

′∗it)

′, ζ i,t−1 = (z′i,t−1,d′t−1)

′, αi is a ki × ri matrix of rank ri and β is a

(ki + k∗i + md)× ri matrix of rank ri. By partitioning βi as βi = (β′ix, β

′ix∗ , β′

id)′ conformable to

ζ i,t = (x′it,x

′∗it,d

′t)′ the ri error correction terms implicit in equation 3 can now be written as:

β′(ζ it − γit) = β′ixxit + β′

ix∗x∗it + β′iddt + (β′

iγi)t,

which clearly allows for the possibility of cointegration both within xit, and between xit and

x∗it and consequently across xit and xjt for i 6= j. Interdependence among countries in the

GVAR model can thus arises through the interaction of xit with x∗it, through the dependence

of xit on global variables dt, and through the contemporaneous interdependence of shocks in

country i on the shocks in country j, as described by the cross-country covariances, Σij, where

Σij = Cov(uit,ujt) = E(uitu′jt) for i 6= j.

The above country-specific vector error-correction models (VECMXs) can now be consis-

tently estimated, treating dt and x∗it as weakly exogenous with respect to the long-run parame-

ters of the conditional model of equation 3. In practice, the weak exogeneity assumption allows

to consider each country as a small open economy with respect to the rest of the world and,

therefore, it allows a country-by-country estimation.

In the second step, once the individual country models are estimated, all the k =∑N

i=0 ki

endogenous variables of the global economy are stacked together in the k × 1 vector xt =

5

(x′0t,x

′1t, ...,x

′Nt)

′. To do this, first we stack domestic and the foreign country-specific variables

in the vector

zit = [x′it,x

′∗it]

′

and we re-write equation 2 as

Ai(L, pi, qi)zit = ϕit, i = 0, 1, 2, ..., N (4)

where

Ai(L, pi, qi) = [Φi(L, pi),−Λi(L, qi)],

ϕit = ai0 + ai1t + Υi(L, qi)dt + uit,

Let p = max(p0, p1, ..., pN , q0, q1, ..., qN) and construct Ai(L, p) from Ai(L, pi, qi) by augmenting

the p− pi or p− qi additional terms in powers of L by zeros.

Note now that, given 1, we can write zit as:

zit = Wixt, i = 0, 1, 2, ..., N, (5)

where Wi is a (ki + k∗i )× k matrix defined by the country specific trade weights, ωij. So 4 can

be written as

Ai(L, p)Wixt = ϕit, i = 0, 1, 2, ..., N.

And by stacking together the country specific models, we have:

G(L, p)xt = ϕt, (6)

where

G(L, p) =

A0(L, p)W0

A1(L, p)W1

...

AN(L, p)WN

, and ϕt =

ϕ0t

ϕ1t...

ϕN t

.

Assuming then that G is non-singular, the GVAR(p) (6) can be solved recursively and used

for forecasting or generalized impulse response and variance decomposition analysis in the usual

manner.

6

3.1 A Simple Three-Country Example

In order to illustrate how changing the trade weight matrices Wi may affect the transmission

of country-specific and global shocks in the GVAR model, in this subsection, we discuss a

slightly modified version of the three-country example of Pesaran, Schuermann, and Weiner

(2004). Specifically, consider a global model composed of three countries: country 0, 1 and 2,

with country 0 as the base country—say the United States. Assume also that we are interested

only in three variables–say output, inflation, and exchange rates:

x0t =

[y0t

π0t

], x∗0t =

y∗0t

π∗0t

e∗0t

x1t =

y1t

π1t

e1t

x∗1t =

[y∗1t

π∗1t

], x2t =

y2t

π2t

e2t

, x∗2t =

[y∗2t

π∗2t

].

Assume further there are no global variables (dt), no constant and trend, and that the lag

order is one, namely pi = qi = 1 ∀i. Thus:

x0t = Φ0x0,t−1 + Λ00x∗0t + Λ01x∗0,t−1 + u0t

x1t = Φ1x1,t−1 + Λ10x∗1t + Λ11x∗1,t−1 + u1t

x2t = Φ2x2,t−1 + Λ20x∗2t + Λ21x∗2,t−1 + u2t

Let’s focus first on country i = 0.4 Its country-specific VARX is

[y0t

π0t

]=

[φ0,11 φ0,12

φ0,21 φ0,22

] [y0,t−1

π0,t−1

]+

[λ00,11 λ00,12 λ00,13

λ00,21 λ00,22 λ00,23

] y∗0t

π∗0t

e∗0t

+

[λ01,11 λ01,12 λ01,13

λ01,21 λ01,22 λ01,23

] y∗0,t−1

π∗0,t−1

e∗0,t−1

+

[uy0,t

uπ0,t

]

Rewrite now the country-specific VARX* in terms of zit, as defined in equation 4

[1 0 −λ00,11 −λ00,12 −λ00,13

0 1 −λ00,21 −λ00,22 −λ00,23

]·

y0t

π0t

y∗0t

π∗0t

e∗0t

=

[φ0,11 φ0,12 λ01,11 λ01,12 λ01,13

φ0,21 φ0,22 λ01,21 λ01,22 λ01,23

]·

y0,t−1

π0,t−1

y∗0,t−1

π∗0,t−1

e∗0,t−1

+

[uy0,t

uπ0,t

],

which can then be written in a compact form as:

A0z0t = B0z0,t−1 + u0t,

with A0 = [I,−Λ00] and B0 = [Φ,Λ01]. Recalling from equation 5 that we can write the

4Strictly speaking, as we discussed briefly above, with N=3, we should include x∗0,t−1 rather than x∗0,t inthe model for country i = 0 to avoid violating the needed weak exogeneity assumption. For the purpose ofillustrating the role of changing trade weights in the transmission of shocks, therefore, we adopt the notationconvention that x∗0,t represents x∗0,t−1 in the model for country i = 0.

7

country-specific z0t in term of the 8× 1 vector xt = [y0t, π0t, y1t, π1t, e1t, y2t, π2t, e2t]′, we have

z0 = W0 · xt =

1 0 0 0 0 0 0 0

0 1 0 0 0 0 0 0

0 0 w01 0 0 w02 0 0

0 0 0 w01 0 0 w02 0

0 0 0 0 w01 0 0 w02

·

y0t

π0t

y1t

π1t

e1t

y2t

π2t

e2t

=

y0t

π0t

y∗0t

π∗0t

e∗0t

.

Now we can also rewrite the country specific VARX* of country i = 0 as

[1 0 −λ00,11 −λ00,12 −λ00,13

0 1 −λ00,21 −λ00,22 −λ00,23

]·

1 0 0 0 0 0 0 00 1 0 0 0 0 0 00 0 w01 0 0 w02 0 00 0 0 w01 0 0 w02 00 0 0 0 w01 0 0 w02

·

y0t

π0t

y1t

π1t

e1t

y2t

π2t

e2t

=

[φ0,11 φ0,12 λ01,11 λ01,12 λ01,13

φ0,21 φ0,22 λ01,21 λ01,22 λ01,23

]·

1 0 0 0 0 0 0 00 1 0 0 0 0 0 00 0 w01 0 0 w02 0 00 0 0 w01 0 0 w02 00 0 0 0 w01 0 0 w02

·

y0,t−1

π0,t−1

y1,t−1

π1,t−1

e1,t−1

y2,t−1

π2,t−1

e2,t−1

+

[uy0,t

uπ0,t

],

or in a more compact form

A0W0xt = B0W0xt−1 + u0t.

To obtain the global model, we can write first the country-specific model for country i = 1, 2

in the same manner and then we stack them together asA0

A1

A2

·W0

W1

W2

· xt =

B0

B1

B2

W0

W1

W2

· xt−1 +

[u0tu1tu2t

],

yields the following representation of the GVAR model:

Gxt = Hxt−1 + ut.

Notice here that G = A ·W and H = B ·W are square matrices with dimension k × k,

with k = 8 in this example. Notice also that all the matrices in the expressions above are either

8

known or estimated. Specifically, through the estimation of the country-specific VECMXs, we

pin down the matrices Φ0, Λ00, and Λ01 and, therefore, we can construct A0, B0. The vector of

constants, the coefficients on the time trend, and the estimated error terms are also estimated

within the VECMXs. In contrast, the matrix of trade linkages W0, is derived directly from

raw data on trade weights. Thus, the G is given by

G =

1 0 −λ00,11 −λ00,12 −λ00,13

0 1 −λ00,21 −λ00,22 −λ00,23

1 0 0 −λ10,11 −λ10,12

0 1 0 −λ10,21 −λ10,22

0 0 1 −λ10,31 −λ10,32

1 0 0 −λ20,11 −λ20,12

0 1 0 −λ20,21 −λ20,22

0 0 1 −λ20,31 −λ20,32

·

1 0 0 0 0 0 0 00 1 0 0 0 0 0 00 0 w01 0 0 w02 0 00 0 0 w01 0 0 w02 00 0 0 0 w01 0 0 w020 0 1 0 0 0 0 00 0 0 1 0 0 0 00 0 0 0 1 0 0 0

w10 0 0 0 0 w12 0 00 w10 0 0 0 0 w12 00 0 0 0 0 1 0 00 0 0 0 0 0 1 00 0 0 0 0 0 0 1

w20 0 w21 0 0 0 0 00 w20 0 w21 0 0 0 0

which is:

1 0 −λ00,11 · ω01 −λ00,12 · ω01 −λ00,13 · ω01 −λ00,11 · ω02 −λ00,12 · ω02 −λ00,13 · ω02

0 1 −λ00,21 · ω01 −λ00,22 · ω01 −λ00,23 · ω01 −λ00,21 · ω02 −λ00,22 · ω02 −λ00,23 · ω02

−λ10,11 · ω10 −λ10,12 · ω10 1 0 0 −λ10,11 · ω12 −λ10,12 · ω12 0

−λ10,21 · ω10 −λ10,22 · ω10 0 1 0 −λ10,21 · ω12 −λ10,22 · ω12 0

−λ10,31 · ω10 −λ10,32 · ω10 0 0 1 −λ10,31 · ω12 −λ10,32 · ω12 0

−λ20,11 · ω20 −λ20,12 · ω20 −λ20,11 · ω21 −λ20,12 · ω21 0 1 0 0

−λ20,21 · ω20 −λ20,22 · ω20 −λ20,21 · ω21 −λ20,22 · ω21 0 0 1 0

−λ20,31 · ω20 −λ20,32 · ω20 −λ20,31 · ω21 −λ20,32 · ω21 0 0 0 1

.

The G therefore is a mixture of the fixed country-specific trade weights and the estimated

coefficients of the country-specific VECMXs. The estimated λi0s in particular are elements

of the matrices Λi0, the effect of foreign variables, x∗it, on the endogenous variables, xit. As

we can see inspecting the expression above row-by-row (i.e. considering the equation of a

given variable in a given country), there are no contemporaneous effects between endogenous

variables within a given country-specific model (see the 0s and the 1s in every row). But these

endogenous variables can be contemporaneously affected by the foreign variables, and hence

by all the endogenous variables of the other models in the GVAR appropriately multiplied by

their respective weight, ωij, and the estimated foreign effect, λi0.

3.2 A Baseline GVAR Model for the World Economy

Our version of the GVAR model includes 33 country VECMs. We consider all major ad-

vanced and emerging economies in the world accounting for about 90% of world output, includ-

ing five large Latin American economies: Argentina, Brazil, Chile, Peru, and Mexico. Eight

9

countries belong to the euro area and are therefore analyzed as a group.5 The remaining 25

countries are modeled individually. Thus, the version of the GVAR model that we use contains

26 countries.

The variables included in each country model are real output (GDP, yit), the rate of inflation,

(πit = pit−pi,t−1), the real exchange rate (eit−pit), and, when available, real equity prices (qit),

a short rate (ρSit) and a long rate (ρL

it) of interest, where:6

yit = ln(GDPit/CPIit),

pit = ln(CPIit),

qit = ln(EQit/CPIit),

eit = ln(Eit),

ρSit = 0.25 · ln(1 + RS

it/100),

ρLit = 0.25 · ln(1 + RL

it/100),

with

GDPit = Nominal Gross Domestic Product of country i at time t, in domestic currency;

CPIit = Consumer Price Index in country i at time t, equal to 100 in a base year (2000);

EQit = Nominal Equity Price Index;

Eit = Exchange rate of country i at time t in terms of U.S. dollars;

RSit = Short rate of interest per annum, in per cent (typically a three month rate);

RLit = Long rate of interest per annum, in per cent (typically a ten year rate).

With the exception of the U.S. model, all country models include the country-specific foreign

variables, y∗it, π∗it, q∗it, ρ∗Sit , ρ∗Lit and the log of oil prices (po

t ) as weakly exogenous. In the case

of the U.S. model, the oil price is included as an endogenous variable. In addition, given

the importance of the U.S. financial variables in the global economy, the US-specific foreign

financial variables, q∗US,t, and ρ∗LUS,t, are not included in the U.S. model as they are not likely

to be long-run forcing for to the U.S. domestic variables. Note also that the value of the U.S.

dollar is determined outside the U.S. model, and the U.S.-specific foreign real exchange rate

variable (e∗US,t − p∗US,t) is included as a weakly exogenous variable in the U.S. model. Finally,

and differently from Dees, di Mauro, Pesaran, and Smith (2007), also the U.S.-specific foreign

short term interest rate, ρ∗SUS,t, is included as a weakly exogenous variable in the U.S. model.

The inclusion of the US foreign specific short-term interest rate serves the scope of improving

5The time series data for the euro area are constructed as weighted averages of yit, πit, qit, ρSit, ρL

it, overGermany, France, Italy, Spain, Netherlands, Belgium, Austria and Finland, using the average Purchasing PowerParity GDP weights, averaged over the 2001-2003 period. For the construction of the euro area exchangerate, each of the country members’ exchange rate was converted to an index using 2000 as the base year andpremultiplied by the euro/dollar rate of that year.

6A more detailed description of the variables and the data is reported in the Data Appendix.

10

the weak exogeneity tests for US specific foreign inflation and exchange rate.7

In the baseline model specification, the country-specific foreign variables, y∗it, π∗it, q∗it, ρ∗Sit ,

and ρ∗Lit are constructed using fixed trade weights based on the average trade flows over the

three-year period 2001-2003, as in equation 1.8

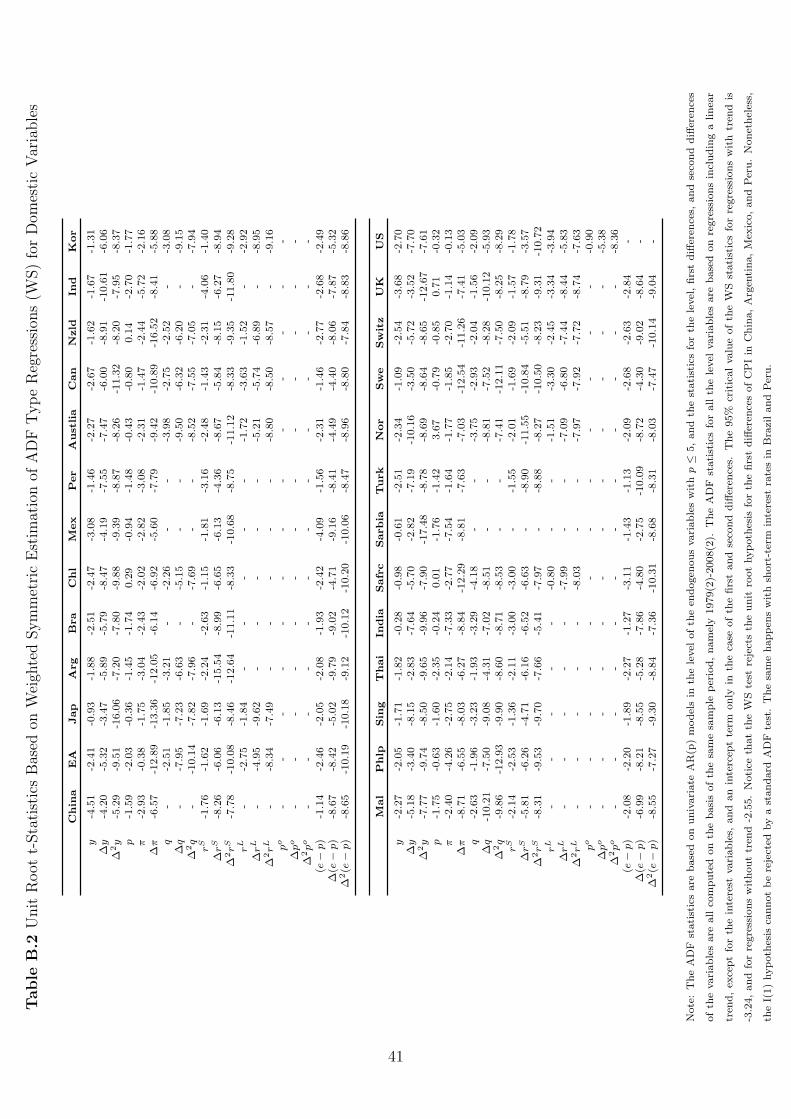

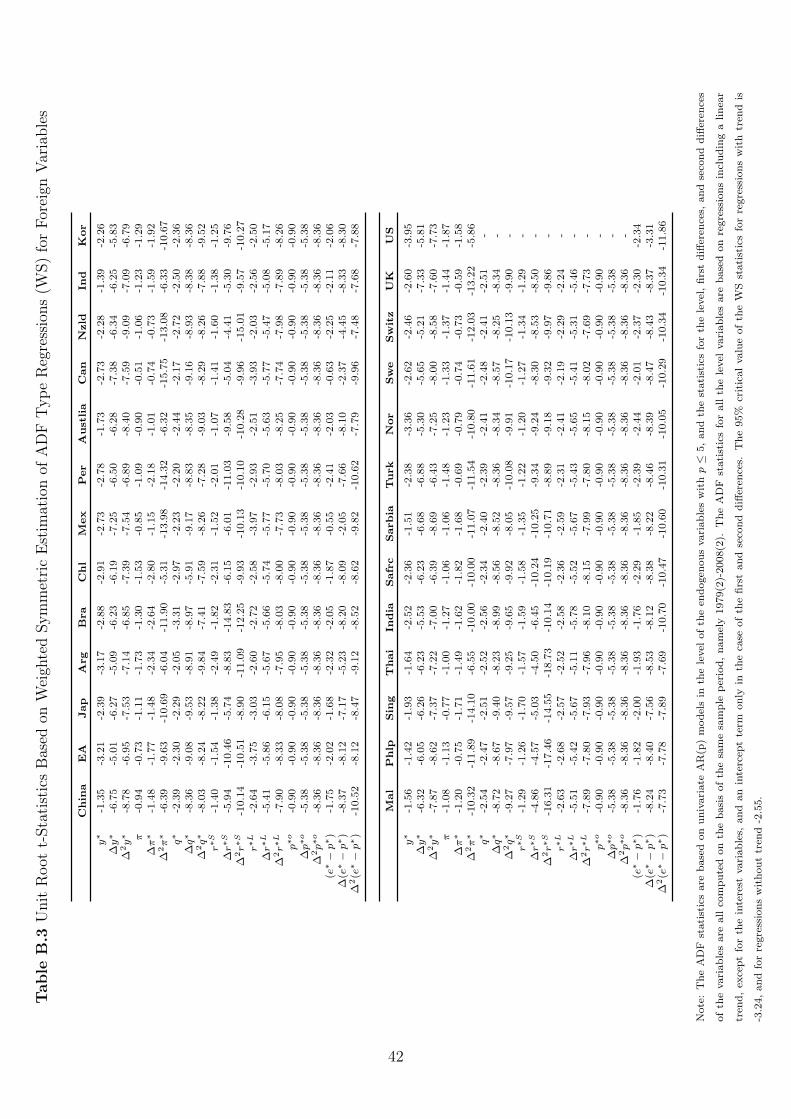

Detailed empirical evidence on the statistical assumptions made to specify the GVAR model

is reported in the Baseline Model Appendix, together with a description of the impact multi-

pliers and pair-wise correlations for all variables and countries included in the model.9 This

includes evidence on the degree of integration of all individual time series, the lag-length an

the cointegration rank for all country models, as well as test statistics on the weak exogeneity

assumptions made. Because of the importance of parameter stability for the counterfactual

simulation exercise that we conduct in the paper, however, evidence on parameter stability is

discussed here.

The possibility of structural breaks is likely to be particularly acute in the case of Latin

America which was subject to significant political, social and structural reforms. However, the

GVAR can readily accommodate co-breaking, implying that the VECMX models that underlie

the GVAR might be more robust to the possibility of structural breaks as compared to reduced

form single equation models. In any case, we perform formal stability tests following Dees,

di Mauro, Pesaran, and Smith (2007) and consider tests that are based on the residuals of the

individual equations of the country-specific error correction models.10

Among the tests included in our analysis are Ploberger and Kramer’s (1992) maximal OLS

cumulative sum (CUSUM) statistic, denoted by PKsup and its mean square variant PKmsq.

The PKsup statistic is similar to the CUSUM test suggested by Brown, Durbin and Evans

(1975), although the latter is based on recursive rather than OLS residuals. Also considered

are tests for parameter constancy against non-stationary alternatives proposed by Nyblom

(1989), denoted by N, as well as sequential Wald type tests of a one-time structural change at

an unknown change point. The latter include the Wald form of Quandt’s (1960) likelihood ratio

statistic (QLR), the mean Wald statistic (MW ) of Hansen (1992) and Andrews and Ploberger

(1994) and the Andrews and Ploberger (1994) Wald statistic based on the exponential average

(APW ). The heteroskedasticity-robust version of the above tests is also presented.

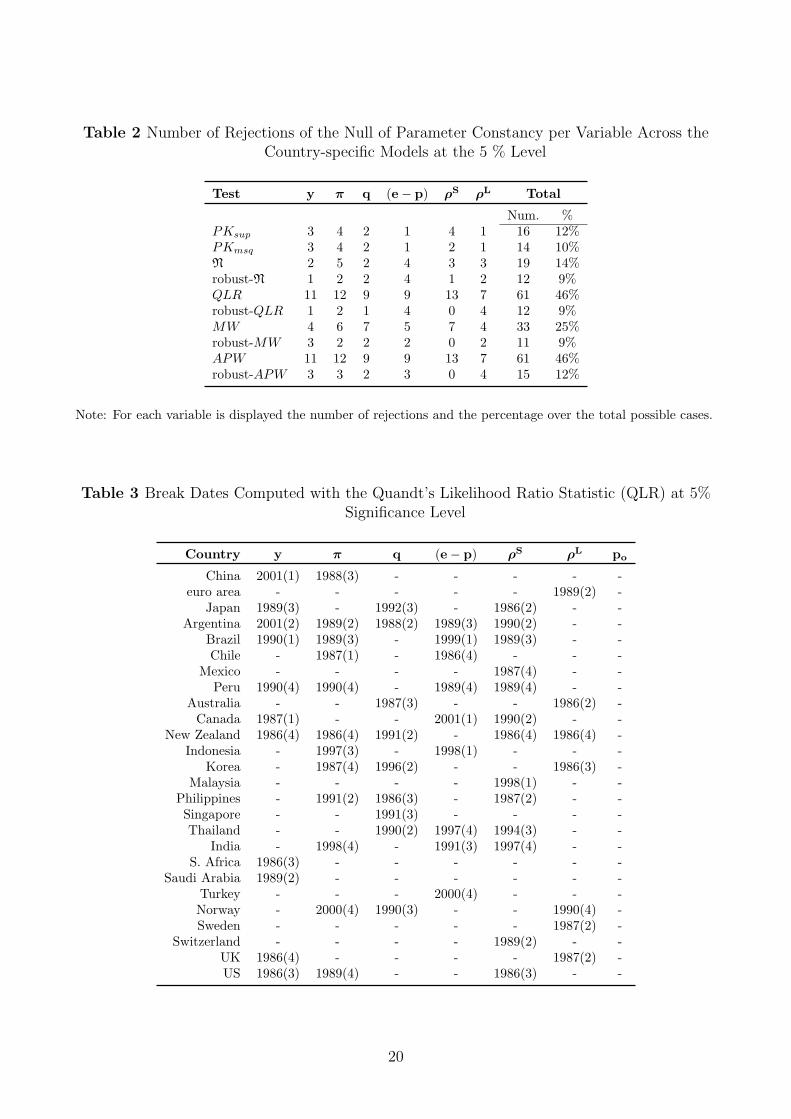

Table 2 summarizes the results of the tests by variable at the 5% significance level. The

critical values of the tests, computed under the null of parameter stability, are computed using

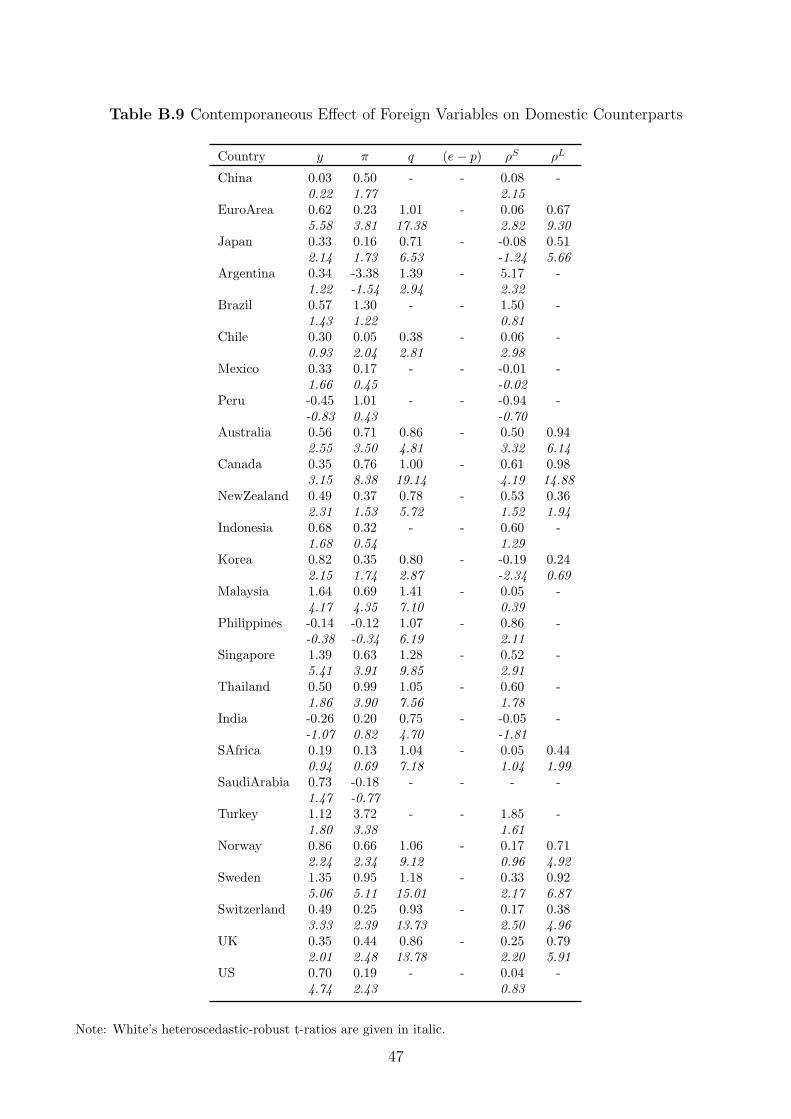

7Under this assumption, the U.S. model passes the test statistics for weak exogeneity more satisfactorily aswe describe in the Baseline Model Appendix table B.8. (Table B.4 summarizes the model specification for allthe countries included in the GVAR.)

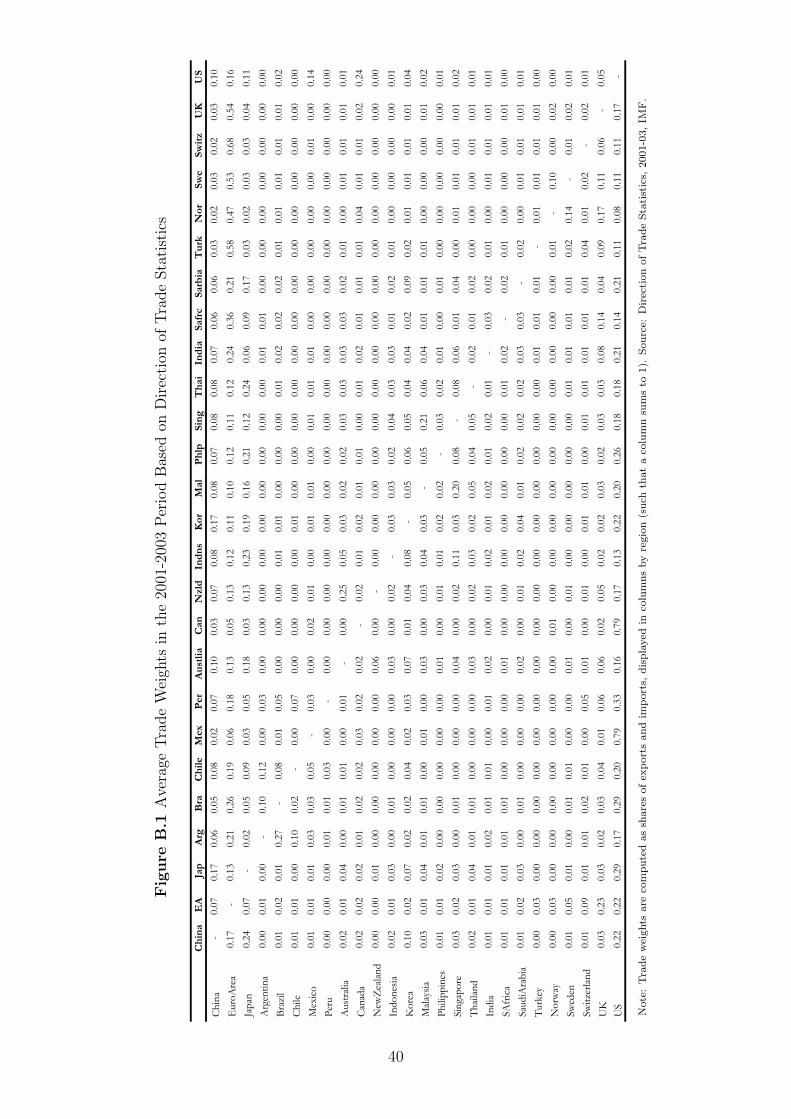

8The weight, ωij , representing the trade share of country j in the total trade of country i, is measured inU.S. dollars and Figure B.1 reports the 26 by 26 matrix which links together the the countries in the model.

9A full set of GIRFs for the baseline model is not reported but is available from the authors on request. Thetransmission properties of the baseline model with 2001-03 trade weights are fully consistent with earlier GVARwork based earlier vintages of the GVAR data set.

10It is well known that these residuals only depend on the rank of the cointegrating vectors and do not dependon the way the cointegrating relations are exactly identified. In this way we render the structural stability testsof the short-run coefficients invariant to exact identification of the long run relations

11

the sieve bootstrap samples obtained from the solution of the GVAR(p) model given by equation

6. The tests show that there is some evidence of structural instability after performing the

aforementioned tests. However, looking at the robust version of these tests, we can see that

this instability is mainly confined to error variances and does not seem to affect many of the

coefficient estimates. We deal with this problem of unstable error variances by using robust

standard errors when investigating the impact effects of the foreign variables and impulse

responses. Some parameter instability remains even after accounting for heteroskedasticity in

the error variances, as presented in table 3.

Focusing on Latin American real GDP variables, structural breaks are found in years when

these countries were subject to severe shocks such as the 2001-2002 Argentine crisis and the

start and end of hyperinflation periods in Brazil and Peru. While acknowledging that this

remaining evidence of parameter instability is problematic, we follow earlier GVAR work (see,

for example, Dees, di Mauro, Pesaran, and Smith (2007) and Pesaran, Schuermann, and Weiner

(2004)) and base our analysis on the bootstrap means and confidence bounds rather than the

point estimates.

4 Transmission of External Shocks Before and After the

Emergence of China in the World Economy

To quantify the change in the transmission of external shocks to the typical Latin American

economy before and after the sharp acceleration of the globalization process at the beginning of

the 1990s, we conduct two counter-factual simulations based on the same model specification.

That is, we keep fixed the specification of the baseline model with 2001-03 trade weights and

re-estimate the GVAR model with two different set of trade weights computed based on average

1995-97 and average 2005-2007 trade data. We focus on these two set of trade weights because,

as we saw earlier, trade weights were relatively stable over time in earlier parts of our sample

period. We analyze the transmission of shocks leaving the model specification unchanged

because changing trade weights alone does not alter the size of the shock on impact if the

model specification stays unchanged (since the change in trade weights does not enter the

initial impact). Of course, changing trade weights can change the response to these shocks

after the initial impact.11

In addition to a global GDP shock, we also look at both country-specific and regional GDP

shocks—namely a LAC GDP shock, a U.S. GDP shock, a euro area GDP shock a China GDP

shock, and a rest of Asia GDP shock—in order to better understand the transmission of the

global output shock, but also because these other shocks are interesting in their own right.

We focus on GDP or output shocks because they are of particular interest in light of the

11The analysis of the transmission of the same shocks reported in the paper changing both the trade weightsas well as the model specification is still work in progress. One would expect, however, lager differences betweenthe two set of simulations changing both trade weights and model specification.

12

recent global crisis. We should note here that a GDP shock at the county or global level can

ultimately be stemming from a shift in demand or supply of output, and we do not attempt to

distinguish between these two different sources of output change in the analysis. So we shall

focus on output shocks which in turn could have been triggered by more fundamental sources

of disturbances that are not identified separately in the analysis.

In the analysis of the transmission of the output shocks we look at both regional responses

to country-specific and country-specific responses to regional and global shocks. The regional

responses are a weighted average of the country responses, aggregated using weights based

on the PPP valuation of country GDPs. Importantly, the regional and the global shocks are

obtained by aggregating in the same fashion country-specific shocks for all countries in the

same region or the whole GVAR model. Hence, in principle, we can either shock and observe

the responses for all countries/regions defined in Table B.1.12

To investigate the transmission of these different output shocks we use GIRFs.13 Thus, we

do not need to assume that the residuals of the output equations in the GVAR model that are

being shocked are uncorrelated with other variables within a given country or across countries.

Unlike more conventional IRF based on orthogonalized residuals, GIRF are attractive precisely

because they allow for such correlations. But as noted above they prevent us from interpreting

structurally the GDP shocks we consider as either demand or supply disturbances (either global

or country specific). Nonetheless, note here that once xit is conditioned on x∗it, like in the GVAR

model, then the estimated country specific shocks have effectively very little correlation across

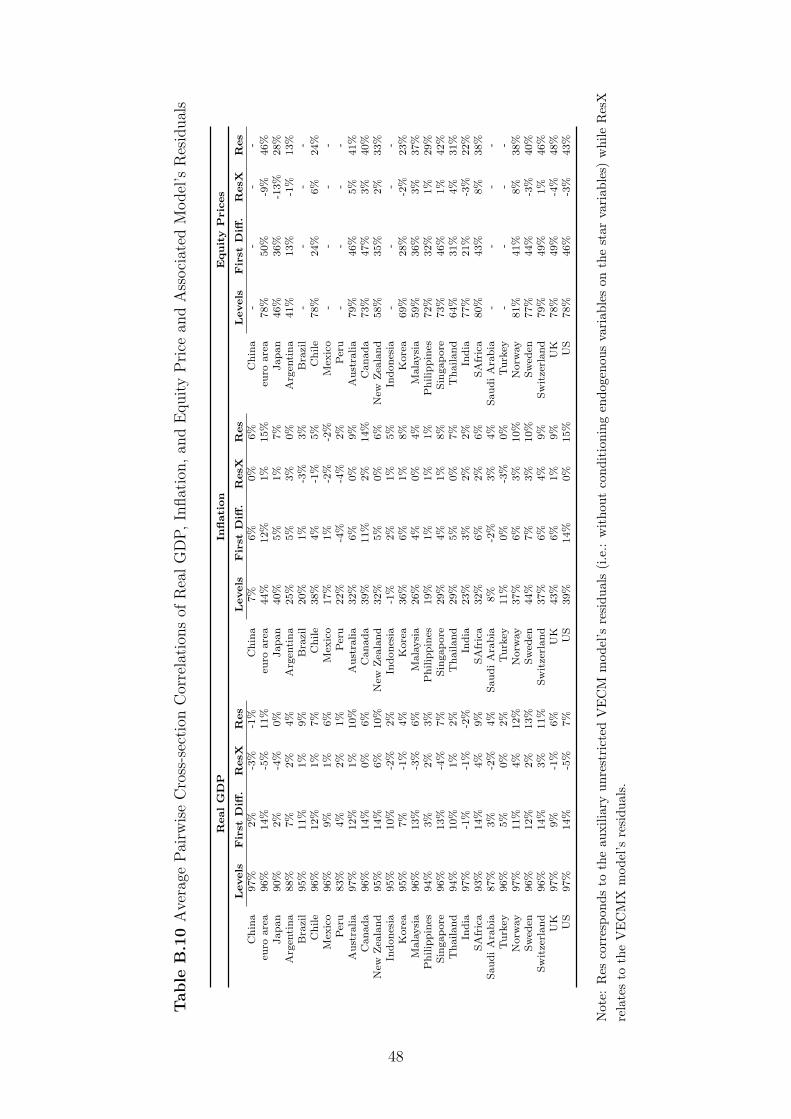

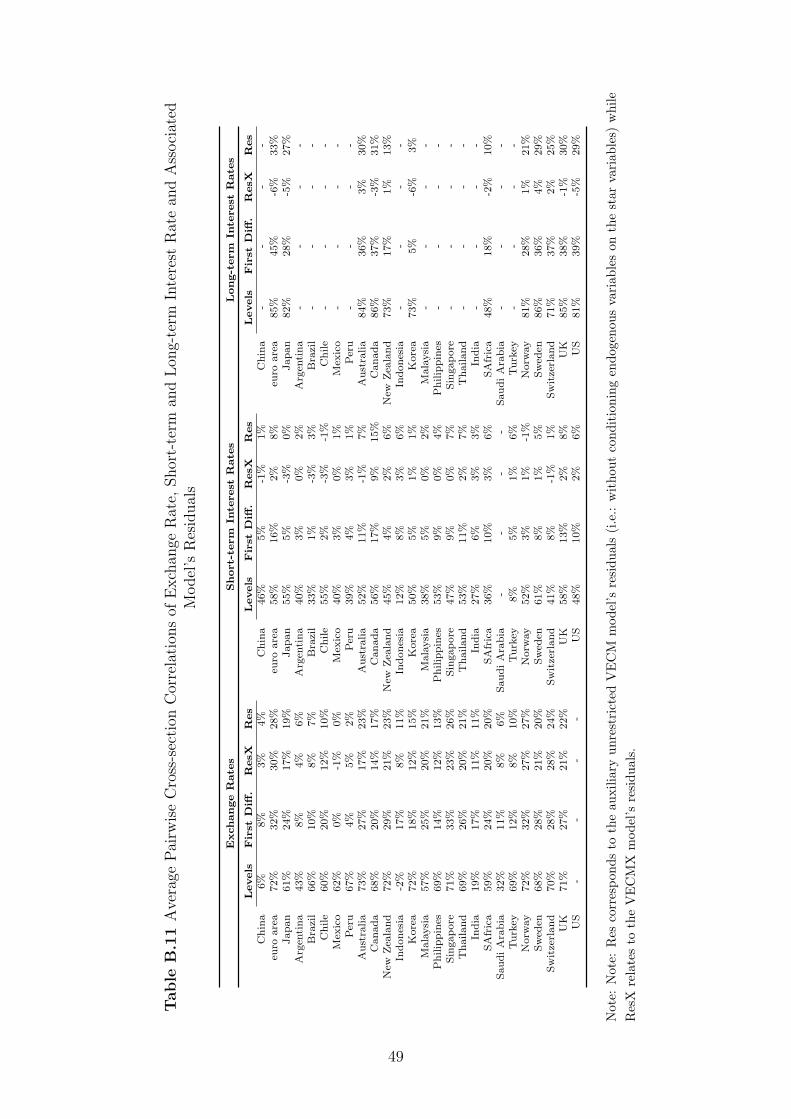

countries as evidenced by Tables B.11 and B.10 in the Baseline Model Appendix. Country

specific GDP shocks can therefore be interpreted as conditional on the global GDP shock,

albeit they will not be perfectly orthogonal as they would obtain in a standard IRF analysis

or factor analysis. In other words, the conditioning on the foreign variables in the GVAR

implicitly addresses the problem of cross-country correlations of the country-specific residuals

we shock because the GVAR models explicitly most of the contemporaneous cross-country and

common dependence in the residuals via the foreign (x∗it) variables. Of course, when we consider

a global output shock, given that it is defined as a weighted average of all GDP disturbances

in the model, this issue do not arise. But the lack of structural interpretation because of the

contemporaneous correlation with all other global shocks in the models remains.

With these preliminary considerations in mind, in the rest of this section, we report and

discuss the results from the two counterfactual simulations we constructed, looking at regional

and country specific shocks first, and then the global GDP shock. Figures from 3 to 8 report

the results, with the blue (clearer line) and black (darker line) corresponding to the 1995-97

and 2005-07 set of trade weights, respectively.

12Notice that in our simulation we used PPP-GDP weights based on Penn World Table 6.1, and that versions6.2 and 6.3 were released with substantial changes in the weight of China and India over global GDP. Resultsbased on the updated PPP weights are available on request and are similar to those reported.

13Notice that these GIRFs are computed using the same bootstrap procedure used to test the model forparameter stability, which is described in detail in the appendix of Dees, di Mauro, Pesaran, and Smith (2007)

13

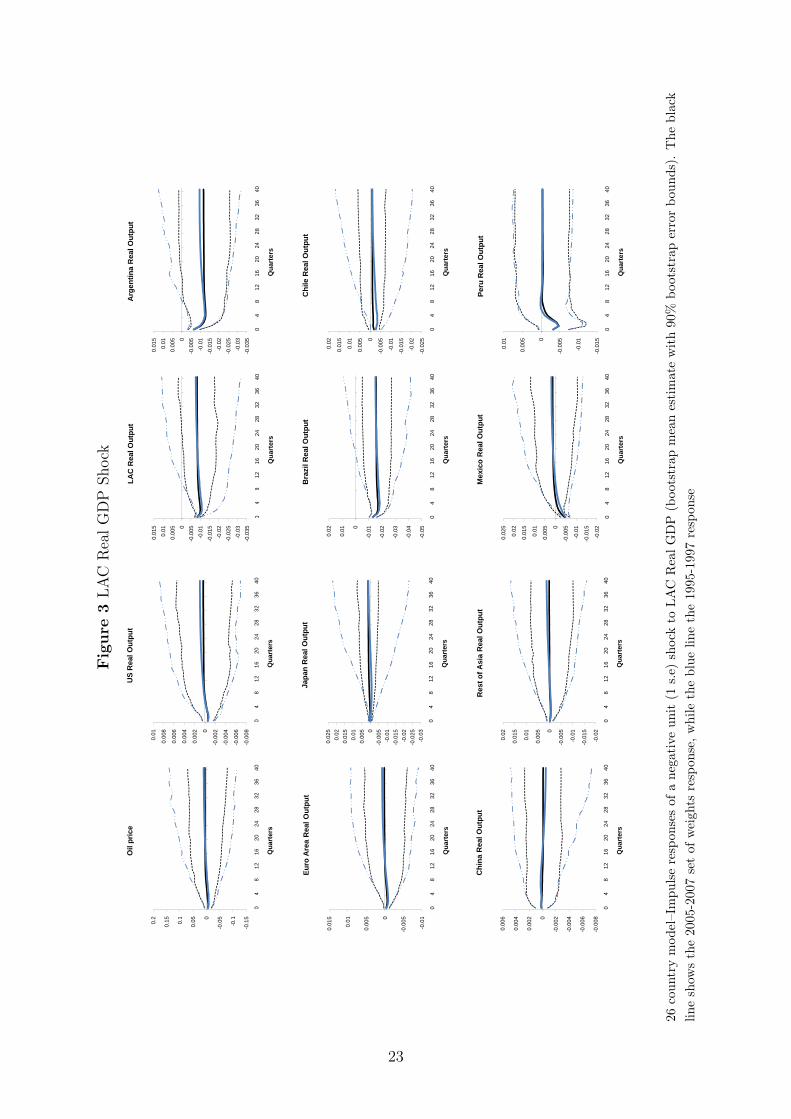

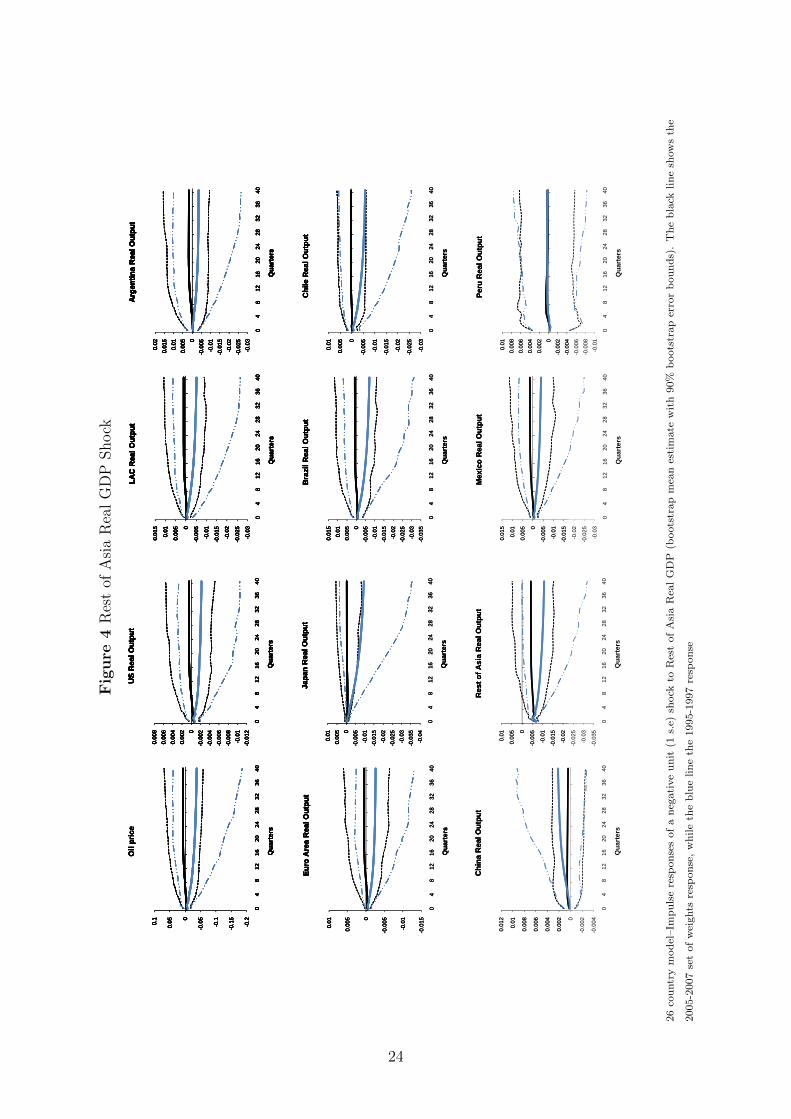

4.1 A Regional GDP Shock in LAC and the Rest of Emerging Asia

Consider first a one standard deviation negative shock to LAC GDP. This shock is con-

structed as the PPP-GDP average of output shocks originated in Latin American country-

specific models and it is equivalent to a decline of LAC GDP of 0.8 percent per quarter under

both set of trade weights.

As presented in Figure 3, the output response in all other countries and regions is not

statistically different from zero, which is not surprising given the region’s relatively small share

in global trade and output. More importantly, though, the effects on LAC itself are virtually

unchanged with 2005-07 trade weights, compared to the 1995-97 weights.

By looking at individual country responses, the short-run reaction of output in Chile is

slightly smaller with more recent trade weights, while the response of Argentina appears to

be slightly stronger. But these differences are very small and are dwarfed by the responses of

Brazil and Mexico, given their relative importance in LAC’s total output (45 and 32 percent,

respectively) and the small number of LAC countries considered. It is interesting to contrast

these responses with those originated by a shock to emerging Asia, which is a traditional

comparator for the five LAC countries we consider. Like a LAC regional shock, a regional GDP

shock in the rest of emerging Asia (excluding China and India) has a similar zero impact on

the rest of the world with 2005-07 trade weights. Unlike a LAC regional shock, however, with

1995-97 trade weights, a regional shocks to the rest of emerging Asia does have a much larger

impact on the rest of the world, albeit estimated very imprecisely, and hence a larger effect on

the region itself.

The two set of results speak to an extent to the much-debated ”decoupling” hypothesis.

According to this hypothesis, emerging markets have decoupled from more advanced economies

in recent years in the sense that their growth performance is less affected by growth at the center

of the world economy and more affected by its own internal dynamics, in part also due to the

process of globalization. In terms of the response of LAC and the rest of emerging Asia to

a regional shock, this should translate into a larger sensitivity of regional output to shocks

emanating in the region itself and smaller responses to shocks emanating outside the region.

The results reported, however, suggest the that the significant changes in the geographical

distribution of international trade that we documented in the paper are not associated with a

major increase in the importance of regional shocks for these two regions themselves. While

this evidence is not necessarily inconsistent with the decoupling hypothesis, it does suggest

that, if decoupling is taking place, it is not going through a key component of the globalization

process: the changed geographical patterns of international trade. In this sense, these results

lend no support to the decoupling hypothesis.

14

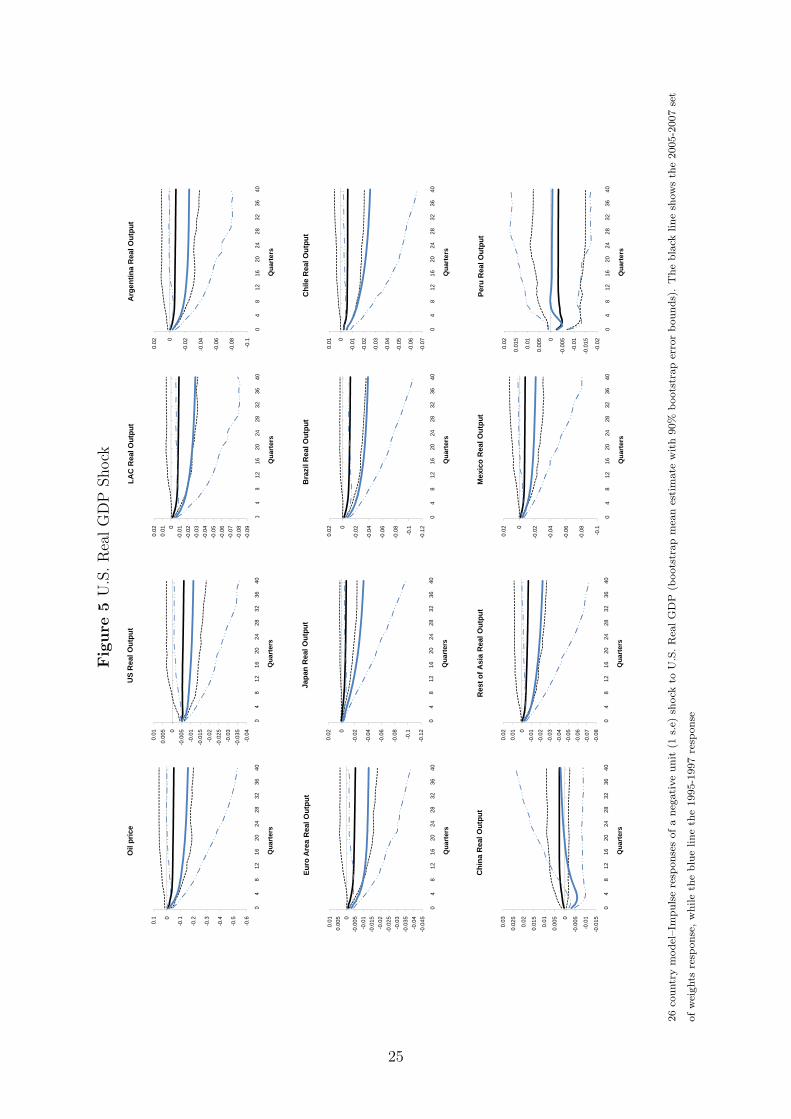

4.2 A U.S. GDP Shock

Figure 5 presents the GIRF to a negative one standard error shock to U.S. output, which is

equivalent to a GDP fall of about 0.5% on impact. Nonetheless, with the 2005-07 weights, the

medium term effect of the shock on U.S. GDP is about half the size of the impact with 1995-97

weights at about -0,5% in the first two years. Thereafter it ceases to be statistically significant.

This evidence is consistent with the so-called ”great moderation” hypothesis according to which

the U.S. economy has become less volatile and more resilient to shocks because of its flexibility

and its full integration in the globalization process. In terms of the U.S. response to domestic

shocks this may translate in smaller impacts as we find.

Looking at the impact of the U.S. shocks on other countries and regions, it is notable that the

effects with 2005-07 trade weights are smaller in all cases reported. Particularly interesting are

the cases of China and the LAC. In the case of China, the response with 2005-07 trade weights

is not statistically significant, while it is much more pronounced and statistically significant

with 1995-97 trade weights.

LAC’s response is smaller with more recent trade weights, right after the first quarter, and

the difference gets larger in the long run, although it ceases to be statistically significant after

eight quarters. At the 2-year horizon output in the region falls by 0.7% (so the multiplier is

still larger than one), which is less than half of what it is with 1995-97 trade shares.

Notable is also the effect of a U.S. output shock on oil prices, which is an endogenous

variable in the U.S. model. As we can see, the oil price response is also smaller with 2005-07

trade weights, which helps to explain why the decrease of the impact of the shock on other

countries is even larger than in the case of the U.S..

These results have an important implications for the puzzles raised by the recent global

financial and economic crisis. In fact they suggest that one reason why economies not located

at the epicenter of the crisis recovered so quickly, is that they are now less affected by U.S. GDP

shocks, which in turn seems largely due to the fact that the U.S. itself is now significantly more

stable than in the past. This in turn suggests that while the great moderation may ultimately

prove to have been temporary, its presence and working up to the onset of the crisis may help

understanding why the global recovery was almost as precipitous as the global slump in the

2008Q4 and 2009Q1.

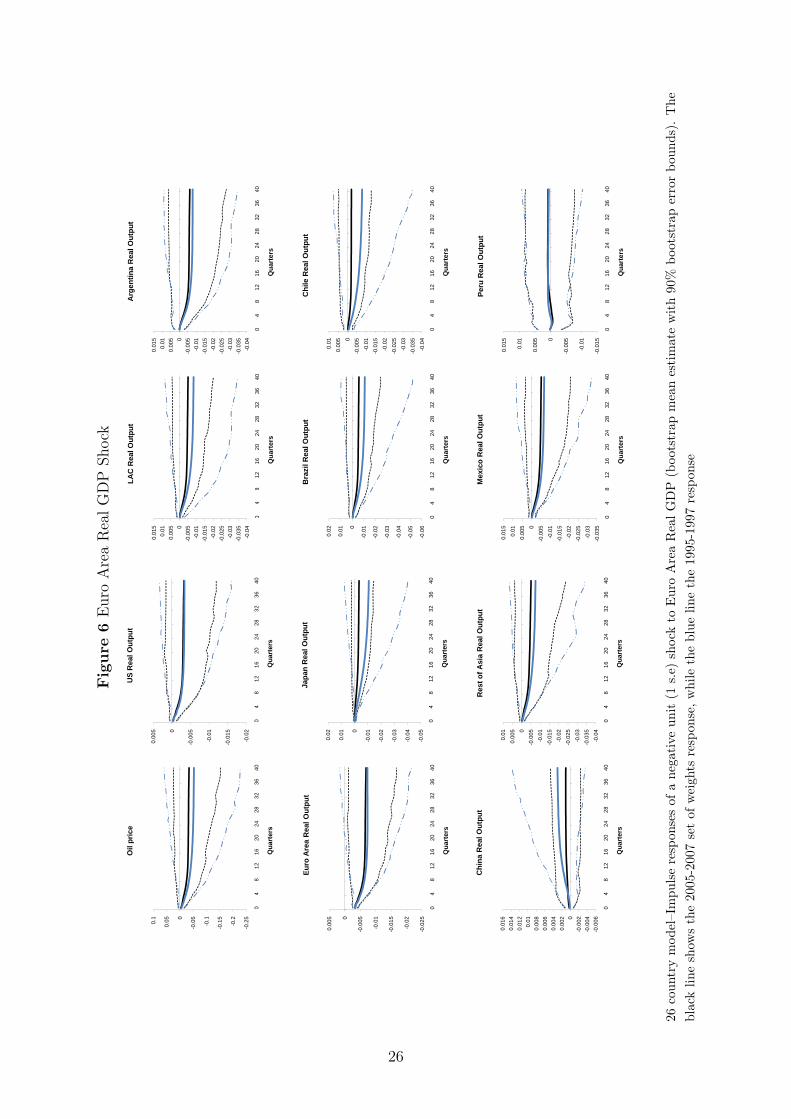

4.3 A Euro Area GDP Shock

Figure 6 displays a negative one-standard deviation shock to output in the euro area, corre-

sponding to a decline of euro area real GDP of 0.3% on impact and of about 0.5% per quarter

in the first two years, both for the recent and the past set of trade weights. Output response

in most other countries and regions is statistically insignificant, except for the euro area itself.

Note however that, although insignificant, the responses in LAC and ”rest of Asia” are smaller

with 2005-07 than with 1995-97 trade weights under the recent trade shares. In LAC, in partic-

15

ular, the long run (at 2-3-year horizon) is about 30% smaller than with 1995-97 trade weights,

and it is rather homogeneous across LAC countries.

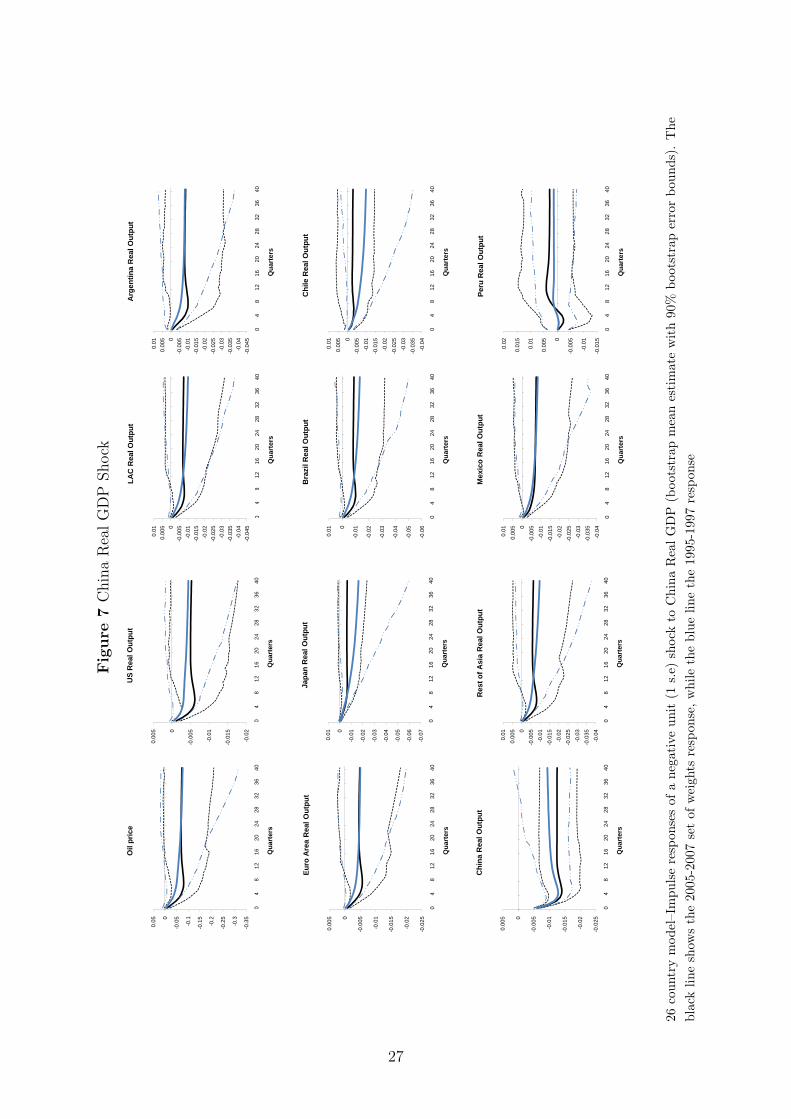

4.4 A China GDP Shock

Figure 7 reports a negative one-standard deviation shock to China’s output. The shock

amounts to a 0,6% fall in China’s real GDP on impact and peaks at -1% after a year, with both

the 1995-97 and the 2005-07 set of weights. With 2005-07 trade weights, however, the shock is

more persistent and its long run impact is larger.

The impact of the shocks on all other countries and regions is larger except in the case

of Japan. In the United States, in particular, the response is remarkably larger and more

persistent: at its peak, output contracts by 0.6%, compared to about 0.3% with 1995-97 trade

weights. Via its effects on the U.S. economy, the shock to China GDP has larger effects also

on the oil price with more recent trade weights.

LAC output, and especially Argentina and Brazil, responds in a similar fashion reflecting

the importance of the indirect effects via the impact on the United States. Interestingly, even

in the case of a shock to China, Chile becomes virtually isolated with 2005-07 trade weights,

while Mexico is surprisingly immune to the shocks despite its strong ties with the U.S. economy

and the importance of oil for the economy.

The response to a GDP shock in China also helps to understand why economies not located

at the epicenter of the crisis recovered so quickly: with more recent trade weights, the world

economy is more responsive to China GDP and relatively less responsive to U.S. GDP compared

to the 1995-97 period. As China GDP has recovered much faster than U.S. GDP one would

expect those economies not at the epicenter of the global crisis to recover faster than in the

past.

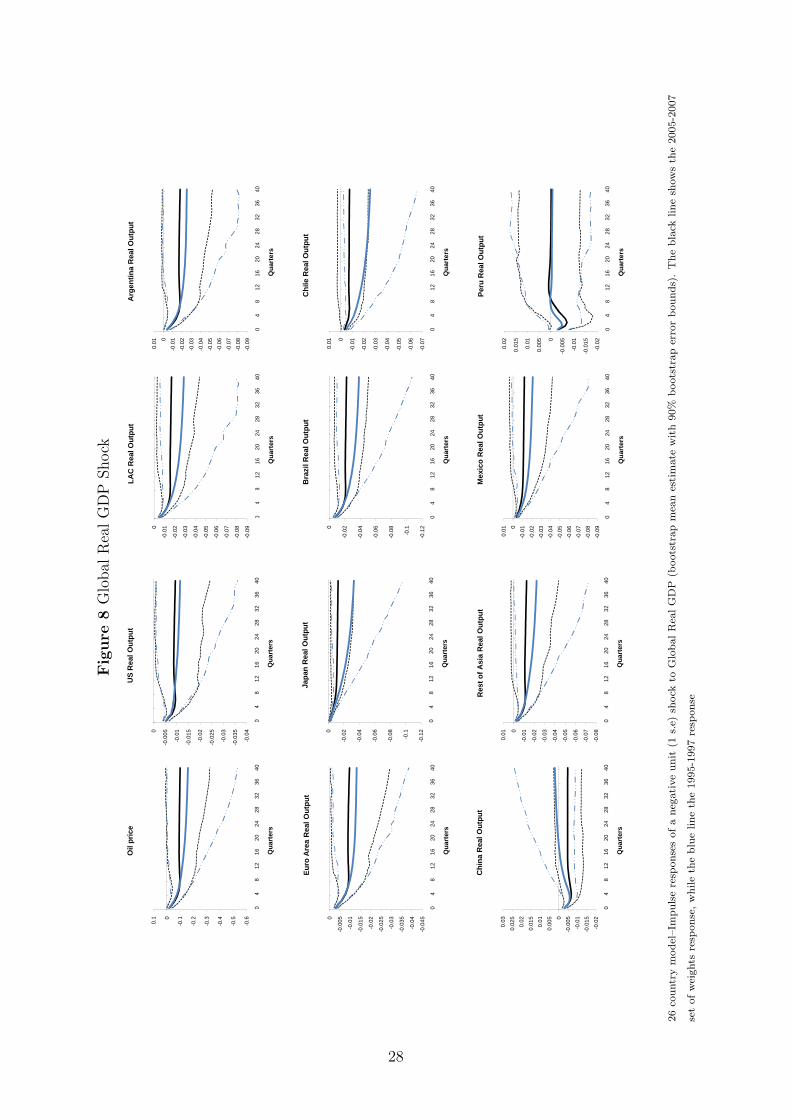

4.5 A Global GDP Shock

Consider finally a one-standard deviation negative shock to global output reported in Figure

8. Such a shock can be interpreted as an autonomous change in global GDP triggered by either

a demand or a supply disturbance. The shock amounts to a fall on impact of about 0.4% per

quarter in global output and about -1.55% and -0.89% with 1995-97 and 2005-07 trade weights,

respectively in the long run.14

In the case of China, the response to the global shock is larger with 2005-07 than with

1995-97 trade shares, at 0.7% and about zero, respectively. Possibly, this is due to the larger

effect of domestic shocks consistent with a decoupling hypothesis. In the case of the United

States, instead, a larger impact of shocks from China is offset by a smaller impact of domestic

shocks. As a result, the impact on the United States is essentially unchanged.

14To evaluate the fall in global output, we aggregate all the country-specific GDP impulse responses using asweights the GDP-PPP shares in global output.

16

In the case of LAC the impact of the shock more than halves in the long run, from about

0.3% with 1995-97 trade weights to about 0.15% with 2005-07 trade weights. This pattern is

common across three of the five countries in the region, with Peru and Chile exhibiting the

highest and the lowest exposure, respectively.

For all countries and regions except the US and China, the impact of the shock is signifi-

cantly smaller with 2005-07 than with 1995-97 trade weights. Based on the discussion of the

transmission of regional and country-specific shocks, the results likely reflect the offsetting in-

fluences of the larger impact of GDP shocks from China and smaller impact of GDP shocks

from the United States, with the latter dominating the transmission of the global shock. In

fact, while trade shares of most countries with China have increased very sharply from mid-

1990s to mid-2000s (alongside with the spectacular increase in the degree of openness of the

Chinese economy), the United States remains a very large trade partner for most economies of

the world.

Nonetheless, looking forward, it is likely that the trade share of China will continue to grow

over time. The analysis of the transmission of a global GDP shock therefore suggests that, if

the globalization process were to continue with the same international trade patterns realized

in recent years, it is possible that the world economy will become more volatile possibly because

more affected by China’s own GDP dynamics.

5 Conclusions

In this paper we investigate how China’s emergence in the world economy may have changed

the transmission of global output shocks to the Latin America region and the rest of the world

economy. Based on a GVAR model for the 26 largest emerging and advanced economies of

the world, estimated with an updated dataset up to 2008Q2, we conducted a counterfactual

exercise in which the same shocks were simulated with the same model specification but under

two different sets of trade weights, based on 1995-97 and 2005-07 average trade data.

We found that the impact of a global GDP shock has almost halved in the case of LAC,

and has fallen significantly in all other major countries and region of the world, except China

and the United States. We interpreted this finding as reflecting the fact that China and the US

have become, respectively, more and less responsive to their own output shock. This evidence

is consistent with the decoupling hypothesis for the case of China and the great moderation

hypothesis for the case of the United States.

The evidence reported in the paper helps to understand the pattern of global recovery ob-

served in the aftermath of the global crisis, and in particular why emerging markets such as

the Latin American economies we considered have recovered much faster than initially antic-

ipated. The empirical analysis in the paper also has implications for the future evolution of

world economy. To the extent to which, going forward, the world economy will load more on

China and less on the US, it is likely to become more volatile, at least in the medium term.

17

The analysis of the same counterfactual exercise changing both the model specification and

the trade weights is an important area of further work.

18

Table 1 Evolution of the Focus Countries/Regions Trade Shares

(a) Period 1985-1987

US Euro Area Japan China LAC5 Argentina Brazil Chile Mexico Peru

US - 23% 39% 16% 49% 20% 33% 27% 69% 35%EuroArea 20% - 12% 19% 26% 37% 28% 28% 14% 23%

Japan 21% 8% - 39% 9% 8% 8% 12% 7% 12%China 2% 2% 6% - 2% 3% 3% 2% 1% 2%LAC5 10% 5% 3% 4% - (-) (-) (-) (-) (-)

Argentina - 4% 4% 1% 5%Brazil 15% - 9% 1% 5%Chile 3% 2% - 0% 3%

Mexico 3% 2% 1% - 1%Peru 2% 1% 2% 0% -

Rest of Adv. Ec. 35% 50% 16% 13% 9% 5% 11% 10% 6% 12%Rest of Asia 10% 6% 18% 9% 2% 2% 2% 2% 1% 2%

Rest of Dev. Ec. 3% 6% 6% 1% 3% 2% 6% 2% 0% 0%Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

(b) Period 1995-1997

US Euro Area Japan China LAC5 Argentina Brazil Chile Mexico Peru

US - 20% 32% 22% 63% 17% 25% 23% 83% 32%EA 15% - 13% 16% 17% 24% 27% 20% 5% 22%

Japan 15% 8% - 29% 6% 3% 7% 13% 3% 7%China 6% 5% 10% - 2% 3% 3% 3% 1% 5%LAC5 14% 5% 3% 3% - (-) (-) (-) (-) (-)

Argentina - 15% 8% 0% 3%Brazil 30% - 8% 1% 5%Chile 6% 3% - 1% 6%

Mexico 2% 2% 4% - 3%Peru 1% 1% 2% 0% -

Rest of Adv. Ec. 33% 46% 12% 9% 7% 6% 9% 10% 4% 12%Rest of Em. Asia 14% 11% 27% 20% 5% 4% 6% 8% 2% 5%Rest of Em. Ec. 2% 6% 3% 2% 1% 2% 3% 1% 0% 1%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

(c) Period 2005-2007

US Euro Area Japan China LAC5 Argentina Brazil Chile Mexico Peru

US - 18% 22% 22% 56% 13% 22% 18% 71% 27%EA 15% - 12% 17% 15% 17% 24% 21% 7% 16%

Japan 9% 5% - 18% 5% 2% 4% 9% 4% 6%China 15% 12% 22% - 9% 11% 10% 13% 6% 13%LAC5 17% 6% 3% 5% - (-) (-) (-) (-) (-)

Argentina - 11% 7% 1% 3%Brazil 31% - 9% 1% 7%Chile 7% 4% - 1% 7%

Mexico 4% 3% 4% - 3%Peru 1% 1% 3% 0% -

Rest of Adv. Ec. 30% 42% 11% 9% 6% 4% 8% 6% 4% 12%Rest of Em. Asia 11% 10% 24% 26% 7% 5% 7% 7% 5% 4%Rest of Em. Ec. 3% 7% 5% 3% 1% 4% 5% 3% 1% 1%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Note: Trade weights are computed as shares of exports and imports. They are displayed in columns by countrysuch that a column sums to one. Rest of advanced economies: Australia, Canada, New Zealand, Norway,Sweden, Switzerland, and UK. Rest of Asia: Indonesia, Korea, Malaysia, Philippines, Singapore, and Thailand.Rest of developing economies: India, South Africa, Saudi Arabia, and Turkey. Source: Direction of TradeStatistics, IMF.

19

Table 2 Number of Rejections of the Null of Parameter Constancy per Variable Across theCountry-specific Models at the 5 % Level

Test y π q (e− p) ρS ρL Total

Num. %PKsup 3 4 2 1 4 1 16 12%PKmsq 3 4 2 1 2 1 14 10%N 2 5 2 4 3 3 19 14%robust-N 1 2 2 4 1 2 12 9%QLR 11 12 9 9 13 7 61 46%robust-QLR 1 2 1 4 0 4 12 9%MW 4 6 7 5 7 4 33 25%robust-MW 3 2 2 2 0 2 11 9%APW 11 12 9 9 13 7 61 46%robust-APW 3 3 2 3 0 4 15 12%

Note: For each variable is displayed the number of rejections and the percentage over the total possible cases.

Table 3 Break Dates Computed with the Quandt’s Likelihood Ratio Statistic (QLR) at 5%Significance Level

Country y π q (e− p) ρS ρL po

China 2001(1) 1988(3) - - - - -euro area - - - - - 1989(2) -

Japan 1989(3) - 1992(3) - 1986(2) - -Argentina 2001(2) 1989(2) 1988(2) 1989(3) 1990(2) - -

Brazil 1990(1) 1989(3) - 1999(1) 1989(3) - -Chile - 1987(1) - 1986(4) - - -

Mexico - - - - 1987(4) - -Peru 1990(4) 1990(4) - 1989(4) 1989(4) - -

Australia - - 1987(3) - - 1986(2) -Canada 1987(1) - - 2001(1) 1990(2) - -

New Zealand 1986(4) 1986(4) 1991(2) - 1986(4) 1986(4) -Indonesia - 1997(3) - 1998(1) - - -

Korea - 1987(4) 1996(2) - - 1986(3) -Malaysia - - - - 1998(1) - -

Philippines - 1991(2) 1986(3) - 1987(2) - -Singapore - - 1991(3) - - - -Thailand - - 1990(2) 1997(4) 1994(3) - -

India - 1998(4) - 1991(3) 1997(4) - -S. Africa 1986(3) - - - - - -

Saudi Arabia 1989(2) - - - - - -Turkey - - - 2000(4) - - -Norway - 2000(4) 1990(3) - - 1990(4) -Sweden - - - - - 1987(2) -

Switzerland - - - - 1989(2) - -UK 1986(4) - - - - 1987(2) -US 1986(3) 1989(4) - - 1986(3) - -

20

Figure 1 Evolution of China’s Trade Share in LAC’s Total Trade

0%

2%

4%

6%

8%

10%

12%

14%

16%

Sh

are

-%

-Trade share of China on Argentina total trade

0%

2%

4%

6%

8%

10%

12%

14%

16%

Sh

are

-%

-

Trade share of China on Brazil total trade

12%

14%

16%

18%

Trade share of China on Chile total trade

0%

2%

4%

6%

8%

10%

12%

Sh

are

-%

-

0%

1%

2%

3%

4%

5%

6%

7%

Sh

are

-%

-

Trade share of China on Mexico total trade

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Sh

are

-%

-

Trade share of China on Peru total trade

21

Figure 2 Comovements Between LAC and China Output annual Growth (10-year movingcorrelation)

.0

.1

.2

.3

.4

.5

.6

.7

90 92 94 96 98 00 02 04 06

LAC

.0

.1

.2

.3

.4

.5

.6

.7

90 92 94 96 98 00 02 04 06

ARG

.0

.1

.2

.3

.4

.5

.6

.7

90 92 94 96 98 00 02 04 06

BRA

-.2

.0

.2

.4

.6

.8

90 92 94 96 98 00 02 04 06

CHL

-.4

-.3

-.2

-.1

.0

.1

90 92 94 96 98 00 02 04 06

MEX

0.0

0.2

0.4

0.6

0.8

1.0

90 92 94 96 98 00 02 04 06

PER

22

Fig

ure

3LA

CR

ealG

DP

Shock

-0.0

35

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

LA

C R

eal O

utp

ut

-0.0

35

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Arg

enti

na

Rea

l Ou

tpu

t

-0.1

5

-0.1

-0.0

50

0.050.1

0.150.2

04

812

1620

2428

3236

40

Oil

pri

ce

-0.0

08

-0.0

06

-0.0

04

-0.0

020

0.00

2

0.00

4

0.00

6

0.00

8

0.01

04

812

1620

2428

3236

40

US

Rea

l Ou

tpu

t

-0.0

5

-0.0

4

-0.0

3

-0.0

2

-0.0

10

0.01

0.02

04

812

1620

2428

3236

40

Qu

arte

rs

Bra

zil R

eal O

utp

ut

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

0.02

04

812

1620

2428

3236

40

Qu

arte

rs

Ch

ile R

eal O

utp

ut

04

812

1620

2428

3236

40

Qu

arte

rs

04

812

1620

2428

3236

40

Qu

arte

rs

04

812

1620

2428

3236

40

Qu

arte

rs

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

0.02

0.02

5

04

812

1620

2428

3236

40

Qu

arte

rs

Jap

an R

eal O

utp

ut

04

812

1620

2428

3236

40

Qu

arte

rs

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qu

arte

rs

Eu

ro A

rea

Rea

l Ou

tpu

t

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

0.02

0.02

5

04

812

1620

2428

3236

40

Qu

arte

rs

Mex

ico

Rea

l Ou

tpu

t

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qu

arte

rs

Per

u R

eal O

utp

ut

-0.0

08

-0.0

06

-0.0

04

-0.0

020

0.00

2

0.00

4

0.00

6

04

812

1620

2428

3236

40

Qu

arte

rs

Ch

ina

Rea

l Ou

tpu

t

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

0.02

04

812

1620

2428

3236

40

Qu

arte

rs

Res

t o

f A

sia

Rea

l Ou

tpu

t

26co

untr

ym

odel

–Im

puls

ere

spon

ses

ofa

nega

tive

unit

(1s.

e)sh

ock

toLA

CR

ealG

DP

(boo

tstr

apm

ean

esti

mat

ew

ith

90%

boot

stra

per

ror

boun

ds).

The

blac

klin

esh

ows

the

2005

-200

7se

tof

wei

ghts

resp

onse

,w

hile

the

blue

line

the

1995

-199

7re

spon

se

23

Fig

ure

4R

est

ofA

sia

Rea

lG

DP

Shock

LAC

Rea

l Out

put

Arg

entin

a R

eal O

utpu

tO

il pr

ice

US

Rea

l Out

put

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

LAC

Rea

l Out

put

-001

-0.0

0500.

005

0.01

0.01

50.

02

Arg

entin

a R

eal O

utpu

t

-0.0

50

0.050.1

Oil

pric

e

-000

4-0

.0020

0.00

20.

004

0.00

60.

008

US

Rea

l Out

put

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

LAC

Rea

l Out

put

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

010.

015

0.02

04

812

1620

2428

3236

40

Qua

rter

s

Arg

entin

a R

eal O

utpu

t

-0.2

-0.1

5

-0.1

-0.0

50

0.050.1

04

812

1620

2428

3236

40

Qua

rter

s

Oil

pric

e

-0.0

12-0

.01

-0.0

08-0

.006

-0.0

04-0

.0020

0.00

20.

004

0.00

60.

008

04

812

1620

2428

3236

40

Qua

rter

s

US

Rea

l Out

put

00.

005

0.01

0.01

5

Bra

zil R

eal O

utpu

t

0

0.00

5

0.01

Chi

le R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

LAC

Rea

l Out

put

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

010.

015

0.02

04

812

1620

2428

3236

40

Qua

rter

s

Arg

entin

a R

eal O

utpu

t

-0.2

-0.1

5

-0.1

-0.0

50

0.050.1

04

812

1620

2428

3236

40

Qua

rter

s

Oil

pric

e

-0.0

0500.

005

0.01

Japa

n R

eal O

utpu

t

-0.0

12-0

.01

-0.0

08-0

.006

-0.0

04-0

.0020

0.00

20.

004

0.00

60.

008

04

812

1620

2428

3236

40

Qua

rter

s

US

Rea

l Out

put

0.00

5

0.01

Euro

Are

a R

eal O

utpu

t

-0.0

35-0

.03

-0.0

25-0

.02

-0.0

15-0

.01

-0.0

0500.

005

0.01

0.01

5

04

812

1620

2428

3236

40

Bra

zil R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Chi

le R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

LAC

Rea

l Out

put

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

010.

015

0.02

04

812

1620

2428

3236

40

Qua

rter

s

Arg

entin

a R

eal O

utpu

t

-0.2

-0.1

5

-0.1

-0.0

50

0.050.1

04

812

1620

2428

3236

40

Qua

rter

s

Oil

pric

e

-0.0

4-0

.035

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

01

04

812

1620

2428

3236

40

Japa

n R

eal O

utpu

t

-0.0

12-0

.01

-0.0

08-0

.006

-0.0

04-0

.0020

0.00

20.

004

0.00

60.

008

04

812

1620

2428

3236

40

Qua

rter

s

US

Rea

l Out

put

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Euro

Are

a R

eal O

utpu

t

-0.0

35-0

.03

-0.0

25-0

.02

-0.0

15-0

.01

-0.0

0500.

005

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

Bra

zil R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qua

rter

s

Chi

le R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

LAC

Rea

l Out

put

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

010.

015

0.02

04

812

1620

2428

3236

40

Qua

rter

s

Arg

entin

a R

eal O

utpu

t

0.01

5

Mex

ico

Rea

l Out

put

0.01

Peru

Rea

l Out

put

-0.2

-0.1

5

-0.1

-0.0

50

0.050.1

04

812

1620

2428

3236

40

Qua

rter

s

Oil

pric

e

-0.0

4-0

.035

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

01

04

812

1620

2428

3236

40

Qua

rter

s

Japa

n R

eal O

utpu

t

-0.0

12-0

.01

-0.0

08-0

.006

-0.0

04-0

.0020

0.00

20.

004

0.00

60.

008

04

812

1620

2428

3236

40

Qua

rter

s

US

Rea

l Out

put

0.01

2

Chi

na R

eal O

utpu

t

0.01

Res

t of A

sia

Rea

l Out

put

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qua

rter

s

Euro

Are

a R

eal O

utpu

t

-0.0

35-0

.03

-0.0

25-0

.02

-0.0

15-0

.01

-0.0

0500.

005

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

Bra

zil R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qua

rter

s

Chi

le R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

LAC

Rea

l Out

put

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

010.

015

0.02

04

812

1620

2428

3236

40

Qua

rter

s

Arg

entin

a R

eal O

utpu

t

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

Mex

ico

Rea

l Out

put

-000

6-0

.004

-0.0

0200.

002

0.00

40.

006

0.00

80.

01

Peru

Rea

l Out

put

-0.2

-0.1

5

-0.1

-0.0

50

0.050.1

04

812

1620

2428

3236

40

Qua

rter

s

Oil

pric

e

-0.0

4-0

.035

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

01

04

812

1620

2428

3236

40

Qua

rter

s

Japa

n R

eal O

utpu

t

-0.0

12-0

.01

-0.0

08-0

.006

-0.0

04-0

.0020

0.00

20.

004

0.00

60.

008

04

812

1620

2428

3236

40

Qua

rter

s

US

Rea

l Out

put

0

0.00

2

0.00

4

0.00

6

0.00

8

0.01

0.01

2

Chi

na R

eal O

utpu

t

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

Res

t of A

sia

Rea

l Out

put

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qua

rter

s

Euro

Are

a R

eal O

utpu

t

-0.0

35-0

.03

-0.0

25-0

.02

-0.0

15-0

.01

-0.0

0500.

005

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

Bra

zil R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qua

rter

s

Chi

le R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

LAC

Rea

l Out

put

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

010.

015

0.02

04

812

1620

2428

3236

40

Qua

rter

s

Arg

entin

a R

eal O

utpu

t

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

0.01

5

04

812

1620

2428

3236

40

Qua

rter

s

Mex

ico

Rea

l Out

put

-0.0

1-0

.008

-0.0

06-0

.004

-0.0

0200.

002

0.00

40.

006

0.00

80.

01

04

812

1620

2428

3236

40

Qua

rter

s

Peru

Rea

l Out

put

-0.2

-0.1

5

-0.1

-0.0

50

0.050.1

04

812

1620

2428

3236

40

Qua

rter

s

Oil

pric

e

-0.0

4-0

.035

-0.0

3-0

.025

-0.0

2-0

.015

-0.0

1-0

.0050

0.00

50.

01

04

812

1620

2428

3236

40

Qua

rter

s

Japa

n R

eal O

utpu

t

-0.0

12-0

.01

-0.0

08-0

.006

-0.0

04-0

.0020

0.00

20.

004

0.00

60.

008

04

812

1620

2428

3236

40

Qua

rter

s

US

Rea

l Out

put

-0.0

04

-0.0

020

0.00

2

0.00

4

0.00

6

0.00

8

0.01

0.01

2

04

812

1620

2428

3236

40

Qua

rter

s

Chi

na R

eal O

utpu

t

-0.0

35

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qua

rter

s

Res

t of A

sia

Rea

l Out

put

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

Qua

rter

s

Euro

Are

a R

eal O

utpu

t

26

countr

ym

odel

–Im

puls

ere

sponse

sofa

neg

ative

unit

(1s.

e)sh

ock

toR

est

ofA

sia

Rea

lG

DP

(boots

trap

mea

nes

tim

ate

wit

h90%

boots

trap

erro

rbounds)

.T

he

bla

ckline

show

sth

e

2005-2

007

set

ofw

eights

resp

onse

,w

hile

the

blu

eline

the

1995-1

997

resp

onse

24

Fig

ure

5U

.S.R

ealG

DP

Shock

-0.0

9

-0.0

8

-0.0

7

-0.0

6

-0.0

5

-0.0

4

-0.0

3

-0.0

2

-0.0

10

0.01

0.02

04

812

1620

2428

3236

40

LA

C R

eal O

utp

ut

-0.1

-0.0

8

-0.0

6

-0.0

4

-0.0

20

0.02

04

812

1620

2428

3236

40

Arg

enti

na

Rea

l Ou

tpu

t

-0.6

-0.5

-0.4

-0.3

-0.2

-0.10

0.1

04

812

1620

2428

3236

40

Oil

pri

ce

-0.0

4

-0.0

35

-0.0

3

-0.0

25

-0.0

2

-0.0

15

-0.0

1

-0.0

050

0.00

5

0.01

04

812

1620

2428

3236

40

US

Rea

l Ou

tpu

t

-0.1

2

-0.1

-0.0

8

-0.0

6

-0.0

4

-0.0

20

0.02

04

812

1620

2428

3236

40

Qu

arte

rs

Bra

zil R

eal O

utp

ut

-0.0

7

-0.0

6

-0.0

5

-0.0

4

-0.0

3

-0.0

2

-0.0

10

0.01

04

812

1620

2428

3236

40

Qu

arte

rs

Ch

ile R

eal O

utp

ut

04

812

1620

2428

3236

40

Qu

arte

rs

04

812

1620

2428

3236

40

Qu

arte

rs

04

812

1620

2428

3236

40

Qu

arte

rs

-0.1

2

-0.1

-0.0

8

-0.0

6

-0.0

4

-0.0

20

0.02

04

812

1620

2428

3236

40

Qu

arte

rs

Jap

an R

eal O

utp

ut

04

812

1620

2428

3236

40

Qu

arte

rs

-0.0

45