Embed Size (px)

Citation preview

ONLINE SHOPPER INTELLIGENCE - UK

Confectionery OnlineWhat You’ll Gain from this ReportThis report focuses on the online confectionery shopping market in the UK, looking at data from February to July 2013. By examining key metrics – derived from Kantar Media Compete’s behavioural data – we’ll offer insight into which levers marketers and category teams can pull to increase online sales.

www.kantarmedia.compete.com2

HoW Do PeoPle BUY ConFeCTioneRY online?

UK consumers are spending more time at home and shopping online these days, which is good news for confectionery companies that are benefiting from increased demand in the bite-sized and share bag sub-category. We take a closer look into the behaviours of online confectionery purchasers as they navigate grocery websites in search of a sweet reward.

online ConFeCTioneRY PURCHase is PaRT oF THe oveRall GRoCeRY Mission

among the 7m online grocery shoppers that visit a supermarket website each month, our clickstream research shows that 12% visit a confectionery-related page. Given that total penetration of confectionery is 91%* and that just half of online visitors make a confectionery purchase online, there is clearly room for growth in this market.

Consumers turn to online grocery websites for convenience – they can shop at any time of day and home delivery saves them from carrying staples or heavy items back from the store. Moreover, increasing familiarity with online grocery (along with cost-reducing delivery incentives) leads to higher frequency and thus to an expansion of shoppers’ category repertoire. Coming as it does with growing online shopping penetration and emerging use of mobile apps, products previously thought of as impulse are set to make a greater appearance in online shopping baskets.

OvERaLL CHaRaCTERISaTION Of THE ONLINE CONfECTIONERy PURCHaSE SESSION

SUPERMARKET direct

Search GO BASKET

My favourites

Over 86% of sessions begin with the

supermarket homepage

Referral to 1st confectionery

page visit

Confectionery page visit

Destination after 1st confectionery

page visit

Referral to shopping basket

INTERNAL SEARCH

HOMEPAGE

FOOD / DRINK

OTHER PRODUCTS

INTERNAL SEARCH

HOMEPAGEHOMEPAGE

FOOD / DRINK

FOOD / DRINK

HOMEPAGE

OTHER PRODUCTS

FAVOURITES

FAVOURITES

FAVOURITES

SPECIAL OFFERS

SPECIAL OFFERS

SPECIAL OFFERS

OTHER PRODUCTS

source: Kantar Media Compete clickstream panel (Monthly average: February-July 2013).*GB TGi Q3 2013 (april 2012 – March 2013), all adults: ‘chocolate assortments, other boxed chocolate’ or other sweets (including sweets for children).

3www.kantarmedia.compete.com

59%

42%

19%

Tesco.com Asda.com Sainsburys.co.uk

i99

i74

i76

Ret

aile

r Sh

are

of C

onfe

ctio

nery

Vi

sito

rs (

% U

V’s)

ConFeCTioneRY sHoPPinG PaTTeRns vaRY BY sUPeRMaRKeT siTe

analysis of our clickstream data shows that of the top 3 supermarket websites, Tesco.com attracts the highest number of confectionery shoppers with 59% of them visiting the site’s confectionery section.

looking at market share does not of course tell the whole story. and just because Tesco.com is the overall leader, it would be unwise to try and use Tesco.com as a model for the whole market – each layer of data reveals important variance which can drive competitive advantage.

For example, while this percentage (59%) is in line (i99) with Tesco.com’s share of all grocery visitors, its share of confectionery purchasers is 13% greater (i113) than its share of total online grocery purchasers. it is therefore clear that Tesco.com is more effective at converting visitors to buyers within the category.

SHaRE Of CONfECTIONERy vISITORS amONG TOP 3 ONLINE GROCERy RETaILERS

SHaRE Of CONfECTIONERy PURCHaSERS amONG TOP 3 ONLINE GROCERy RETaILERS

i113 i84 i73

64%

26%

12%

Tesco.com Asda.com Sainsburys.co.uk

Ret

aile

r Sh

are

of C

onfe

ctio

nery

P

urch

aser

s ( %

Con

vert

ers)

Note: share percentages sum greater than 100% due to shoppers who visit multiple grocery websites in the same period.Source: Kantar Media Compete clickstream panel (Monthly average: February – July 2013).

Source: Kantar Media Compete clickstream panel (Monthly average: February – July 2013).

i = index to share of total grocery visitors

i = index to share of total grocery purchasers

www.kantarmedia.compete.com4

This has two implications. Firstly that the value of any investment to drive traffic could result in a 28% variance in effectiveness depending on where it is allocated and which retailer it directs customers to – if based on current metrics. secondly, of course, it offers brand and communications teams as well as category managers the opportunity to drive change provided they know precisely what levers to pull to affect sales.

as we know, in addition to the profile “quality” of shopper attracted to the site in the first place, overall category prioritisation, inventory and navigation contribute to each retailer’s performance within a category. once shoppers arrive on a grocery website, site design and configuration of shopping tools also influence how consumers manoeuvre their way toward the check-out process. Retailers can offer some insight based on their own data, but they miss the wider picture and have no read of best practice – the traditional role of the manufacturer being to gain this insight through greater market knowledge.

We observed some notable differences in how confectionery shoppers use these site features across supermarket websites:

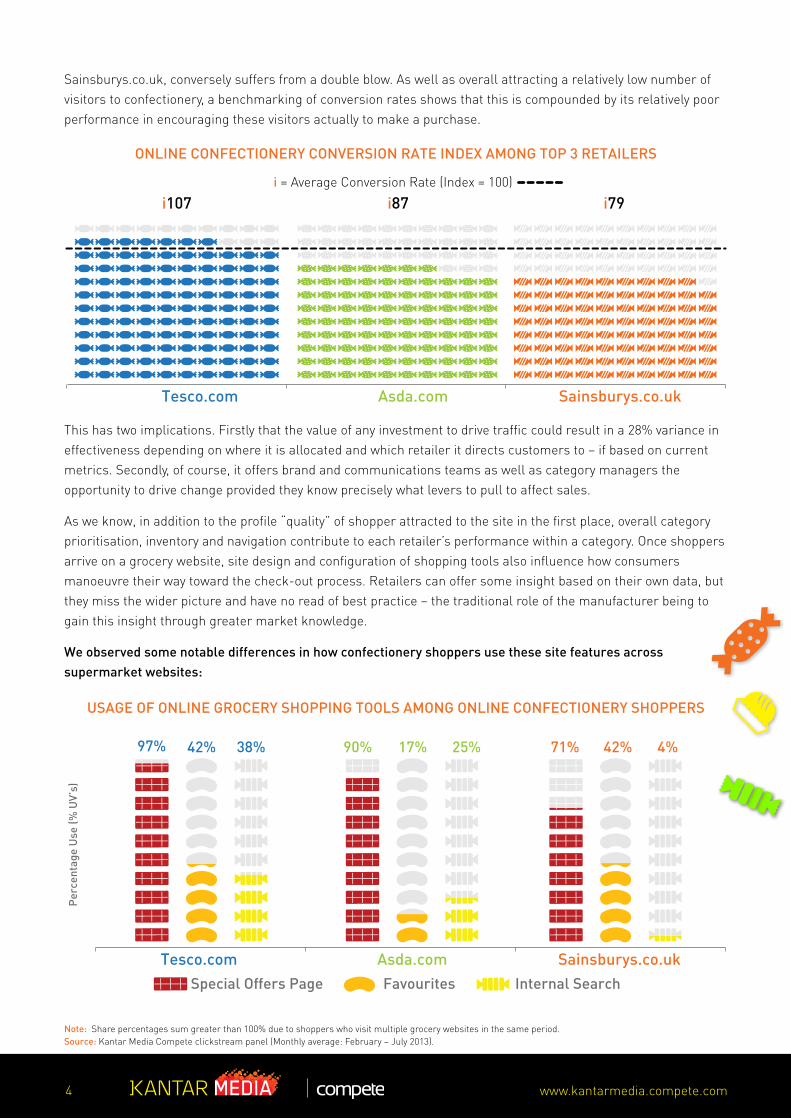

sainsburys.co.uk, conversely suffers from a double blow. as well as overall attracting a relatively low number of visitors to confectionery, a benchmarking of conversion rates shows that this is compounded by its relatively poor performance in encouraging these visitors actually to make a purchase.

Note: share percentages sum greater than 100% due to shoppers who visit multiple grocery websites in the same period.Source: Kantar Media Compete clickstream panel (Monthly average: February – July 2013).

ONLINE CONfECTIONERy CONvERSION RaTE INDEX amONG TOP 3 RETaILERS

USaGE Of ONLINE GROCERy SHOPPING TOOLS amONG ONLINE CONfECTIONERy SHOPPERS

i107 i87 i79

Tesco.com Asda.com Sainsburys.co.uk

Per

cent

age

Use

(% U

V’s)

Tesco.com Asda.com Sainsburys.co.uk Special Offers Page Favourites Internal Search

97% 90% 71% 42% 17% 42% 38% 25% 4%

i = average Conversion Rate (index = 100)

5www.kantarmedia.compete.com

SaINSbURyS.CO.UK GROCERy CaTEGORy mENU

special offers are a key driver, much more so than Favourites. But although internal search is at a reasonable level at Tesco.com, it would be wrong to conclude that search is important to sainsburys.co.uk or, in the same way, Favourites to asda.com.

Tesco.com’s confectionery visitors are the most engaged in using different site features to aid in the shopping process. While retailer engagement is certainly likely to drive higher conversion, it would be too simplistic to assume that visitors should be encouraged to engage more with multiple site features to encourage sales. sainsburys.co.uk visitors are less likely than those on other sites to visit special offers or use internal search for confectionery. instead, they opt to click on the “snacks & Treats” button on the navigational menu which is clearly differentiated from the broader “Food” categories that confectionery falls under on the other sites.

visitors to sainsburys.co.uk do not seem to need to use internal search for confectionery because they are able to find what they want more quickly and easily through other means (alternatively consumers find the search function less effective so rely more on navigating through clicks). either way the implication is that there is not necessarily one right blueprint for how a retailer site should be configured as long as different site elements work seamlessly together to meet shoppers’ needs.

inTeRnal seaRCH is PoPUlaR WHen sHoPPinG FoR ConFeCTioneRY. WHaT TYPes oF TeRMs aRe sHoPPeRs UsinG?

on asda.com and to a lesser extent, Tesco.com, shoppers are more likely to type in generic search terms when looking for sweets. sainsburys.co.uk visitors seem to have less of a problem accessing the confectionery pages they want through other means – their search activity is more heavily weighted to brand names. across all sites, it is clear that chocolate is by far the most searched for confectionery.

Tesco.com

BRANDED58%

UNBRANDED62%

CHOCOLATE92%

SWEETS10%

MINTS3%

GUM2%

GUM2%

BRANDED53%

UNBRANDED62%

CHOCOLATE94%

SWEETS8%

MINTS2%

GUM2%

BRANDED67%

UNBRANDED39%

CHOCOLATE93%

SWEETS6%

MINTS0%

GUM2%

Asda.com Sainsburys.co.uk

71% Of CONfECTIONERy vISITORS CLICK ON

“SNaCKS & TREaTS”

www.kantarmedia.compete.com6

41%

45%

30%

21%

AVERAGE BASKET80% OF CONFECTIONERY

SHOPPERSAVG. # OF STEPS PER

SESSION: 15SUPERMARKET SESSIONS

PER MONTH: 3

SUPERMARKET direct

Search GO BASKET

My favourites

ASDA GROCERY HOME PAGE

31% 31%

INTERNAL SEARCH FOOD

OTHER PRODUCT PAGES

CONFECTIONERY

CONFECTIONERY

SPECIAL OFFERS

FOOD

FAVOURITES

INTERNAL SEARCH

OTHER PRODUCTPAGES

20%

20% SHOPPING BASKET

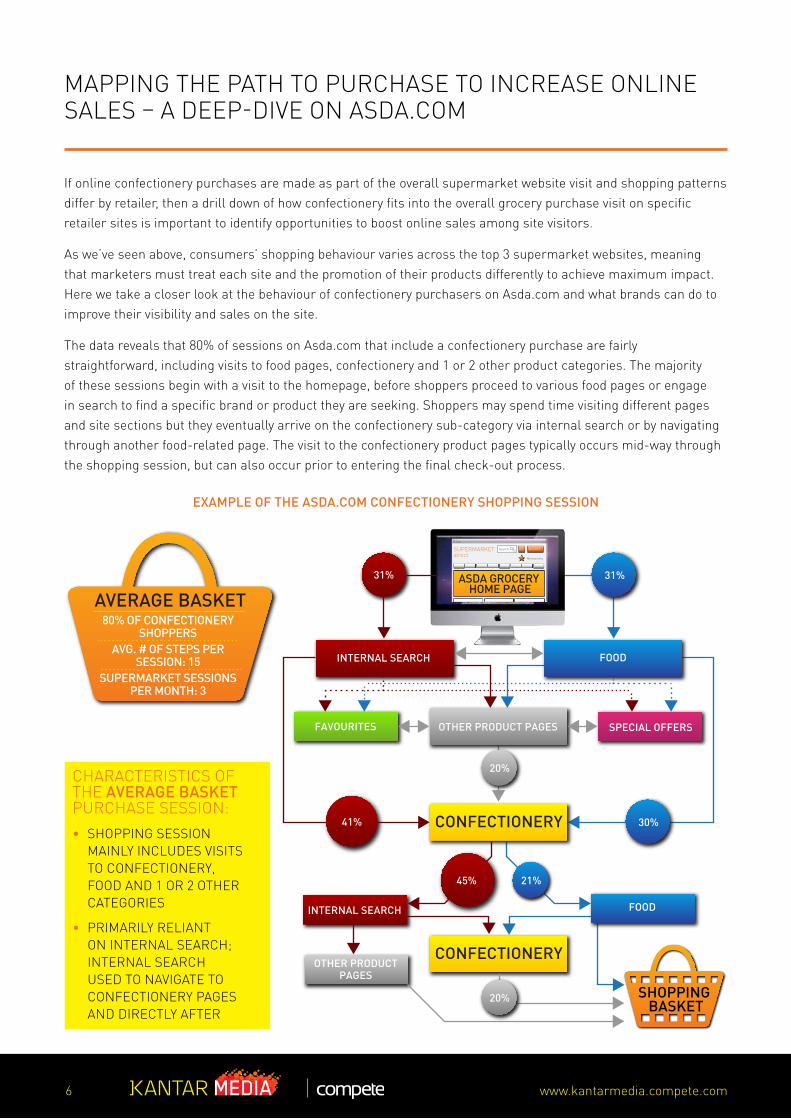

MaPPinG THe PaTH To PURCHase To inCRease online sales – a DeeP-Dive on asDa.CoM

if online confectionery purchases are made as part of the overall supermarket website visit and shopping patterns differ by retailer, then a drill down of how confectionery fits into the overall grocery purchase visit on specific retailer sites is important to identify opportunities to boost online sales among site visitors.

as we’ve seen above, consumers’ shopping behaviour varies across the top 3 supermarket websites, meaning that marketers must treat each site and the promotion of their products differently to achieve maximum impact. Here we take a closer look at the behaviour of confectionery purchasers on asda.com and what brands can do to improve their visibility and sales on the site.

The data reveals that 80% of sessions on asda.com that include a confectionery purchase are fairly straightforward, including visits to food pages, confectionery and 1 or 2 other product categories. The majority of these sessions begin with a visit to the homepage, before shoppers proceed to various food pages or engage in search to find a specific brand or product they are seeking. shoppers may spend time visiting different pages and site sections but they eventually arrive on the confectionery sub-category via internal search or by navigating through another food-related page. The visit to the confectionery product pages typically occurs mid-way through the shopping session, but can also occur prior to entering the final check-out process.

EXamPLE Of THE aSDa.COm CONfECTIONERy SHOPPING SESSION

CHaRaCTeRisTiCs oF THe avERaGE baSKET PURCHase session:• sHoPPinG session

MainlY inClUDes visiTs To ConFeCTioneRY, FooD anD 1 oR 2 oTHeR CaTeGoRies

• PRiMaRilY RelianT on inTeRnal seaRCH; inTeRnal seaRCH UseD To naviGaTe To ConFeCTioneRY PaGes anD DiReCTlY aFTeR

7www.kantarmedia.compete.com

38% LARGE BASKET20% OF CONFECTIONERY

SHOPPERSAVG. # OF STEPS PER

SESSION: 45SUPERMARKET SESSIONS

PER MONTH: 2.6

SUPERMARKET direct

Search GO BASKET

My favourites

ASDA GROCERY HOME PAGE

28%

20%14%

INTERNAL SEARCH FOOD

OTHER PRODUCT PAGES CONFECTIONERY

SPECIAL OFFERS

FOOD

FAVOURITES

INTERNAL SEARCH

OTHER PRODUCTPAGES

46%26%

SHOPPING BASKET

46%

TOILETRIES, HEALTH & BEAUTY DRINKS ASDA GROCERY

HOMEPAGELAUNDRY,

HOUSEHOLD, PET

ReCoMMenDaTions

Favourites and special offers are more popular among a subset of online confectionery purchasers who shop online less often, but shop for a greater variety and number of products during each session. Due to the size and breadth of the shopping basket, they rely more heavily on Favourites to help facilitate the shopping process and are likely to be more interested in special offers to reduce the cost of the overall basket.

#1. The asda.com grocery homepage is prime

real estate to feature your brand / product.

Homepages are generally prime real estate on any site, and this is no less true on asda.com. as 90% of site visitors enter through the homepage, visibility is key to driving brand choice and encouraging grocery shoppers who hadn’t included confectionery on their shopping list to make an impulse purchase.

#2. among different website tools, internal search

results are most important in driving confectionery purchases.

Two-fifths of visits to confectionery product pages are driven by search on asda.com’s website. ensuring that the retailer site is optimised to prioritise your brand above the fold on search results pages increases the likelihood that shoppers will not only see your products, but are primed to select them for purchase.

#3. Cross-promotions on other food pages.

Confectionery is classified as a Food sub-category on the navigation menu on asda.com, meaning it makes sense to cross-promote confectionery products on other food pages: online grocery shoppers primarily shop online for food products, making food pages the area to achieve greatest reach on the supermarket website to drive more traffic to the confectionery section.

HOW SHOULD favOURITES aND SPECIaL OffERS bE USED TO INCREaSE ONLINE CONfECTIONERy SaLES?

CHaRaCTeRisTiCs oF THe LaRGE baSKET PURCHase session: • all sHoPPinG sessions

inClUDe visiTs To ConFeCTioneRY anD FooD, anD MoRe liKelY To also inClUDe DRinKs, HealTH & BeaUTY anD HoUseHolD GooDs

• TWiCe as liKelY THan aveRaGe To visiT sPeCial oFFeRs anD FavoURiTes PaGes

leaRn MoReFor more information about our role in advancing your online marketing effectiveness, please contact:

Jeremy Radcliffe UK Managing [email protected]

@competeUK www.kantarmedia.compete.com

We help the world’s top brands, agencies and publishers improve their performance based on in-depth insights into consumers’ online behaviour.

Clients in the retail, FMCG, Telecoms, Travel and Media markets rely on our insights and expertise to create engaging online experiences and highly effective advertising campaigns. our solutions cover the entire digital marketing spectrum, including

audience segmentation, competitive intelligence, market sizing, and marketing and online channel effectiveness. With our behavioural panel of over 300,000 UK online consumers and industry expertise, we deliver custom solutions that match your exact needs.

only with our granular data is it possible to uncover new metrics and insights that chart the entire path to purchase, monitor how key metrics change over time and attribute Roi to marketing campaigns.