Embed Size (px)

Citation preview

OPEC in the News

Michael Plante

Federal Reserve Bank of Dallas Research Department Working Paper 1802 https://doi.org/10.24149/wp1802

OPEC in the News ∗

Michael Plante

Current version: February 2018

First version: April 2015

ABSTRACT

This paper introduces a newspaper article count index related to OPEC that rises in re-sponse to important OPEC meetings and events connected with OPEC production levels. Iuse this index to measure how interest in OPEC varies over time and investigate how oil pricevolatility behaves when the index unexpectedly changes. I find that unexpected increases inthe newspaper index are strongly associated with higher levels of oil price volatility, both real-ized and implied. In some cases, interest levels and price volatility appear to be driven by theOPEC event itself, such as the Iraq invasion of Kuwait. In other cases, such as the oil price col-lapses in late 2008 and late 2014, price volatility and interest levels in an OPEC event appearto be responding endogenously to developments in the oil market or broader economy. Thenewspaper index is highly correlated with Google search volume data on OPEC, an alternativemeasure of the amount of attention paid to OPEC events.

Keywords: Oil price volatility; OPEC; Attention; Google search activityJEL Classifications: Q43; C32; D80; G12

∗Plante, Research Department, Federal Reserve Bank of Dallas, 2200 N Pearl St, Dallas, TX 75201([email protected]). This paper previously circulated under the title “OPEC in the News: The Effect ofOPEC on Oil Price Uncertainty.” I am grateful to Nathan Balke, Alex Chudik, Everett Grant, Soojin Jo, Alex Richterand participants of the Dallas Fed - Norges Bank joint workshop on applied econometrics for helpful comments onthis version. I also thank Justin Lee, Grant Strickler and the Dallas Fed library staff for excellent research assistance.All errors are my own. The views expressed in this paper are those of the author and do not necessarily reflect theviews of the Federal Reserve Bank of Dallas or the Federal Reserve System.

PLANTE: OPEC IN THE NEWS

1 INTRODUCTION

A growing literature has made use of news coverage and internet search volume data to analyzeeconomic phenomena. Barber and Odean (2008) [9], for example, use news coverage data tohelp explain the decisions of individual investors. Da, Engleberg and Gao (2011) [11] use GoogleSearch Volume Index (SVI) data to help explain stock price movements. Andrei and Hassler (2014)[4] use Google search volumes to study the relationship between investors’ attention levels andstock market volatility. Baker, Bloom and Davis (2016) [7], hereafter BBD, introduced a monthlyindex based on newspaper counts to track the level of economic policy uncertainty. Afkhami,Cormack and Ghoddusi (2017) [2] show that weekly Google SVI data on numerous keywordsrelated to energy have predictive power for energy price volatility. Baker and Fradkin (2017) [8]use Google search data to measure job search activity.

There is also an extended literature that has explored how OPEC and OPEC-related eventsaffect oil price volatility. Horan, Peterson and Mahar (2004) [19], for example, use an event studyapproach and find that market expectations of crude oil price volatility, given by an option-impliedvolatility, often rises in the days before an OPEC meeting but falls thereafter. Robe and Wallen(2016) [27] find that OPEC spare capacity has explanatory power for the implied volatility of oil. Anumber of other works have also documented a connection between OPEC and different measuresof oil price volatility.

In this paper, I make use of news coverage data to consider the connections between OPECand oil price volatility, the first work to do so to the best of my knowledge. A contribution ofthis work is to introduce a monthly newspaper article count variable that is used to measure howinterest in OPEC and OPEC events varies over time. This index, hereafter referred to as the OPECnewspaper index, is similar in spirit to the economic policy uncertainty index of BBD but is basedon the number of newspaper articles with references to OPEC. My hypothesis is that the numberof articles written about OPEC should vary from month to month depending upon the amount ofattention being paid to the group. During periods of intense scrutiny about OPEC, for example,there should be more articles written about the group and its members. This provides informationnot only on what events are considered important but also on how attention levels vary over time.I show that this index does indeed vary over time, and rises in response to a variety of importantevents related to OPEC, such the oil price collapse in 1986, the Iraq invasion of Kuwait and selectOPEC meetings.

I then use the index to explore how oil price volatility behaves around periods of unusual in-terest in the cartel. To do so, I incorporate the newspaper index into a variety of reduced-form,monthly vector autoregression (VAR) models and consider what happens when there is an unex-pected change in the OPEC newspaper index.1 To avoid making strong, and potentially incorrect,identifying assumptions about causality I use generalized impulse response functions to do theanalysis. In this case, the shocks to the newspaper index are the residuals from its regressionequation, i.e. the unforecastable changes in the index.

I begin with simple bi-variate VAR models that contain the newspaper index and either a mea-sure of realized volatility or implied volatility for West Texas Intermediate (WTI) crude oil. I findthat there is a very strong statistical connection between unexpected increases in the newspaper

1Monthly frequencies allow the newspaper index to be added into models that contain oil supply and demand data,variables known to be important for modeling the oil market but unavailable at daily or weekly frequencies. See Kilian(2009) [22] and related papers for recent examples.

1

PLANTE: OPEC IN THE NEWS

index and higher levels of oil price volatility, both realized and implied. Several robustness checksthen are undertaken to test the strength of these findings. In one check, the empirical models areexpanded to include data on global oil production, global oil demand, and oil prices, to control forthe possibility that movements in the newspaper index might be predictable given lagged values ofthese variables. Adding these variables has very little impact on the results. The results are alsorobust to using Brent crude price and volatility data in place of West Texas Intermediate crude, andto using an alternative formulation of the newspaper index that takes into account changes in thevolume of total newspaper articles that have occurred over time.

The OPEC newspaper index is constructed using a simple search method based on newspapercounts. This approach may be subject to concerns regarding its accuracy and reliability in measur-ing interest levels in OPEC. To alleviate these concerns, I compare the newspaper index to GoogleSVI data that tracks search frequency on the topic of OPEC, available since 2004. I find the OPECnewspaper index is highly correlated with SVI data, with a correlation coefficient of 0.78.2 Theempirical findings in the VAR are also robust to replacing the newspaper index with Google SVIdata. While highly correlated with the Google data, the OPEC newspaper index has several advan-tages over it. One is that it extends back to 1986, whereas Google data is only available startingin 2004. The index is also easily obtained over a long period of time in different frequencies,including weekly, monthly, quarterly or annually.

I also investigate what particular events correspond with unexpectedly high interest levels inOPEC. To do this, I use a narrative-type approach and examine the residuals from the empiricalmodel to see whether they line up with an OPEC-related event, focusing on the largest shocks.The largest unexpected increase occurred in August 1990 when Iraq invaded Kuwait. The secondlargest was in October 2014, when a rapid decline in oil prices fueled unusual interest in OPEC’sNovember 2014 meeting. Other notable, unpredicted increases occurred in August 1986 during anOPEC meeting in Geneva that led to a surprise production agreement; OPEC meetings in 1992 and1993 during the return of Kuwaiti production; OPEC meetings in late 1997 and early 1998 duringthe Asian financial crisis; the post 9-11 meeting in November 2001; and several other meetings inthe mid-2000s.

The models and methodology used here do not make any direct assumptions or statementsabout the causality between the newspaper index and volatility levels. It could be the case thatsome OPEC events are unusually important, and that this drives attention and volatility levels.Or it could be that unexpectedly high levels of oil price volatility are driven by events in the oilmarket or broader economy, and these events in turn make OPEC events, particularly meetings,more important and more widely watched than is usually the case. To the extent one can makesuch statements, the residual analysis suggests that both explanations play a role. For example,the Iraq invasion of Kuwait was an exogenous event that was important in its own right. Likewise,although not exogenous in the sense of a war, the unexpected increase in the index in August 1986was related to Saudi Arabia’s decision to dramatically increase production levels from historiclows in the summer of 1985. On the other extreme, unusual interest in OPEC in October 2014 wasclearly related to developments in the oil market. Likewise, the OPEC meeting in October 2008garnered unusual interest due to recent developments in the economy, i.e. intense concern aboutdemand levels due to the financial crisis and how OPEC might respond to those developments.

2A third alternative, Bloomberg News Trends data, is available from 2007 onwards. The newspaper index is alsohighly correlated with this data.

2

PLANTE: OPEC IN THE NEWS

These findings have some potential implications for thinking about the connections between oilprice volatility and the economy, as they suggest that while certain periods of high volatility seemto be due to exogenous OPEC events, other periods appear to be endogenous variations in volatilitylinked, in part, to events in the broader economy.

This work has connections with the literature that makes use of news and internet search baseddata to analyze economic phenomena. In addition to previously cited papers, important works inthis area include Tetlock (2007) [29], Engelberg and Parsons (2011) [14] and Yuan (2015) [30].This paper differs from the previous literature in that it uses news and internet search data tomeasure interest in OPEC events. To the best of my knowledge, this approach has not been usedfor thinking about how attention levels towards OPEC have varied over time.

This paper also has connections with the literature that focuses on OPEC and oil price volatility.Some important examples include Guo and Kliesen (2005) [18], Demirer and Kutan (2010) [12],Schmidbauer and Rosch (2012) [28], Amelier and Darne (2014) [3] and Mensi, Hammoudeh andYoon (2014) [24]. My work differs from these in my approach to the question. Many previousworks have used event study analysis of various types. Here, I consider the behavior of oil pricevolatility around those events that attract unexpectedly high levels of interest, as given by thenewspaper index or Google SVI data. Such an approach has not been used before in the literature.

Finally, there is also a literature that discusses the connections between oil price uncertaintyand economic activity. Bernanke (1983) [10], for example, showed increased uncertainty aboutoil prices could negatively affect investment spending when there is an irreversible investment de-cision. Numerous empirical works have also found evidence of a negative relationship betweenvarious measures of oil price uncertainty and macroeconomic activity. Notable examples includeFerderer (1996) [15], Guo and Kliesen (2005) [18], Elder and Serletis (2010) [13], and Jo (2013)[20], amongst many others. Kellogg (2014) [21] shows that oil price uncertainty affects the invest-ment decisions of oil and gas companies.

The rest of the paper is organized as follows. In the next section I introduce the newspaperindex and other data used in the analysis. In Section 3 I discuss the empirical methods while inSection 4 I present the results. Section 5 concludes.

2 DATA

2.1 OPEC NEWSPAPER INDEX I am interested in measuring how attention paid to OPEC andOPEC events varies over time. To do so, I construct an article count variable similar in spirit tothe economic policy uncertainty index in BBD (2016) [7]. The article count variable, hereafterreferred to as the OPEC newspaper index, is constructed using monthly article counts from severalmajor newspapers. The use of monthly data allows the index to be incorporated into empiricalmodels of the oil market, which are often monthly in frequency due to limitations on supply anddemand data. It is possible to generate the index at other frequencies, as well, such as weekly orquarterly. The time series for the monthly index is available online.3

The source for the raw counts is the Dow Jones Factiva database. The search is based on thekeyword “OPEC” and generates a monthly count for four major newspapers: the Financial Times,the Houston Chronicle, the New York Times and the Wall Street Journal. The appendix providesthe exact search criteria. These four papers were chosen given the fact that they are widely read,have many articles devoted to the economy, and devote space to writing about the oil market. As a

3The data is available at sites.google.com/site/michaelplanteecon/research.

3

PLANTE: OPEC IN THE NEWS

result, major events related to OPEC that capture the interest of oil market participants are likely tobe written about in these papers. The index begins in 1986, the first year that Factiva provides fulldata for the Houston Chronicle. It is possible to go back to the early 1980s using the other threepapers. The series could be extended even further given access to more detailed newspaper recordsthan those available with Factiva. The search finds a total of 22,183 articles over the full sampleperiod. The average number each month is 59.6 articles per month, while the median count is 46.

A first step to creating the index is to aggregate across newspapers. One issue is that the countsdiffer across newspapers, so simply summing across the raw article counts could overweight theinfluence of papers with systematically larger article counts. To deal with this, I follow BBD andfirst standardize the individual newspaper time-series to unit standard deviation. More specifically,for each newspaper i I calculate the sample standard deviation, σi, for the full sample from January1986 to December 2016. I then divide the time series for newspaper i by σi. This provides fourtime series that provide easily interpretable information on when there are unusually large numberof articles being written about OPEC in each specific paper. Table 1 shows the correlations betweenthe four measures. Most are highly correlated with each other, although the correlations betweenthe FT and the other papers are somewhat weaker.

Financial Times 1

Houston Chronicle 0.57 1

New York Times 0.64 0.86 1

Wall Street Journal 0.72 0.84 0.85 1

Table 1: Correlations between the newspaper article counts. The sample runs from Jan. 1986 to Dec. 2016.

To construct the OPEC newspaper index, I then perform the following calculations. For eachmonth, I first average across the four standardized time-series. This new series is denoted as Zt.Next I calculate the mean of this series, denoted by M . Finally, I multiply the Zt by 100/M ,for all months. This produces a normalized series with an average of 100 over the sample periodconsidered.

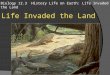

Figure 1 plots the OPEC newspaper index. The largest spike coincides with the Iraq invasionof Kuwait in August 1990, which itself was preceded by a very large jump in July 1990. There area number of spikes in 1986 following Saudi Arabia’s decision to rapidly increase production levelsfrom historic lows in the summer of 1985. Other notable spikes in 1987 and 1988 line up withOPEC meetings. Large spikes in March 2000 and September 2000 line up with OPEC meetings,and November 2001 lines up with an emergency OPEC meeting had after 9/11. Increases in lateMay 2004 picks up an OPEC meeting and militant attacks that occurred in Saudi Arabia. Laterin the sample, the index picks up OPEC meetings in October 2006, November 2007, emergencymeetings in October and December 2008, plus meetings at the end of 2014 and 2016. Whilethe index typically rises contemporaneously with an event, it can display some forward lookingbehavior and rise in advance of an event, such as the increase in October 2014. Overall, thereis strong evidence that the OPEC newspaper index is closely linked to events related to OPEC,typically meetings but occasionally other types of events as well.

Many increases in the index line up with the bi-annual OPEC conferences. The dates forthese meetings are publicly known well in advance and it seems quite plausible that the number

4

PLANTE: OPEC IN THE NEWS

of articles written about OPEC would naturally increase during those months, relative to othermonths. This would create a type of irregular, but predictable, seasonal pattern in the index. Ihave tested for this possibility by regressing the index on a constant and a dummy variable thatis set to 1 during a month with one of the bi-annual conferences. The results overwhelminglyconfirm the hypothesis that there is an increase in counts during those months, with the coefficienton the dummy variable having a p-value near zero. The empirical analysis, details of which areintroduced in the next section, controls for this predictable increase in the index.

2.1.1 ALTERNATIVE INDEX In the baseline newspaper index, it is the raw number of articleswritten about OPEC that is considered informative about the level of interest in the group. Oneissue with this approach is that print edition newspapers, in general, have been shrinking in sizeover time. As a result, the number of total articles being written about all subjects has been de-clining. To take this into account, I construct an alternative index that takes the total number ofarticles written about OPEC across the four papers each month and divides it by the total numberof articles produced by the four papers that month.4 A priori, it is not clear whether the baseline oralternative approach might be preferred. While the alternative index does control for trends in theoverall number of articles that appear in newspapers, it introduces noise because the total numberof articles can vary from month to month for any number of reasons. In any case, I find that thealternative index is closely related to the baseline index: the correlation coefficient between thetwo is 0.97.

1990 1995 2000 2005 2010 20150

100

200

300

400

500

600

Figure 1: Time series of the OPEC newspaper index. The index values average 100 over the full sample.

4The appendix describes the search criteria used to generate the estimate of the overall volume of articles.

5

PLANTE: OPEC IN THE NEWS

2.2 GOOGLE SEARCH VOLUME INDEX One alternative to using news coverage data to gaugeinterest in a topic is data based on internet search volumes. Google Search Volume Index (SVI)data, available from Google Trends, has been frequently used for this purpose in a number of otherresearch papers.5 This data allows one to measure search intensity for a particular keyword ortopic, over a specified period of time and within a geographic area.

There is a specific series that tracks search volumes for the topic of “OPEC” that incorporatessearches based on several different keywords. Data is available from 2004 to the present and comesin the form of an index that ranges from 0 to 100. The index is normalized such that 100 representsthe period of maximum search intensity over the sample period being considered.

I extract monthly SVI data from 2004 to 2016 based on worldwide searches related to the topicOPEC. Figure 2 plots the time series. The SVI reaches a maximum on May 2004, which lines upwith the militant attacks in Saudi Arabia. Several other notable periods with high values includeNovember 2007 (OPEC meeting), May 2008 (militant attacks in Nigeria), September - December2008 (financial crisis and OPEC meetings), November 2014 (OPEC meeting) and late 2016 (OPECmeeting). In general, the SVI and the newspaper index contemporaneously respond to many of thesame events, but not all. The correlation coefficient between the two is 0.78.

The monthly SVI data has a visible seasonal pattern, with a decline typically occurring inthe summer in July. The reason for this is unclear but given that it exists I seasonally adjust theSVI data before using it in the empirical analysis.6 There is also evidence that the SVI data risespredictably during the regularly scheduled bi-annual OPEC meetings, which I control for in theempirical analysis.

The newspaper index and SVI data each have their own pros and cons in terms of measuringattention levels towards OPEC events. One useful feature of the SVI data is that it is, as stated byDa et al. (2011) [11], a revealed attention measure. That is, people made an explicit attempt tosearch for OPEC on Google. A major advantage of the newspaper index is that it can be extendedmuch further back in time than SVI data. The current index starts in 1986, the first full year Factivaprovides data on the four newspapers used in the analysis.

2.3 OIL MARKET DATA The empirical analysis also makes use of data on world oil production,world industrial production (as a proxy for oil demand), crude oil prices, a measure of realizedvolatility for crude oil prices and an implied volatility series for crude oil. I now describe this datain more detail.

The oil production data is the Energy Information Administration’s world crude oil productionincluding lease condensate series. I use the world industrial production series from the Dallas Fed’sDatabase on Global Indicators as a proxy for oil demand. This series covers industrial productionfrom a large number of countries.7 My oil price variable is the inflation-adjusted spot price of WestTexas Intermediate crude oil. I take a monthly average of daily nominal spot prices available fromBloomberg and deflate the monthly average using the U.S. CPI excluding food and energy prices.I transform the supply, industrial production and real oil price data by taking logs, differencing,and multiplying by 100. The sample for these data runs from January 1986 to December 2016,providing a total of 372 observations.

5See for example Da, Engleberg and Gao (2011) [11], Afkhami, Cormack and Ghoddusi (2017) [2] and Baker andFradkin (2017) [8].

6The empirical results are not qualitatively affected by seasonally adjusting the data.7See Grossman, Mack and Martinez-Garcia (2014) [17] for more details.

6

PLANTE: OPEC IN THE NEWS

2004 2006 2008 2010 2012 2014 20160

20

40

60

80

100

Figure 2: Time series of Google Search Volume Index data on OPEC.

I use daily spot prices for West Texas Intermediate crude oil to derive a realized volatility series.The price on any given day in month t is denoted as Pd,t. The daily return on day d in month t iscalculated as

rd,t = ln

(Pd,t

Pd−1,t

). (1)

For each month, I calculate an average return which I denote as rt. The monthly volatility, denotedas HVt for month t is calculated as

HVt = 100×

√√√√ 260

ndayt − 1

ndayt∑d=1

(rd,t − rt)2, (2)

where ndayt is the number of trading days in month t.The implied volatility series is from options on the one-month ahead futures contract for West

Texas Intermediate (WTI) crude oil. The series measures the market’s expectations of near-termvolatility in the nominal price of WTI. Data from Bloomberg provides a daily series of impliedvolatilities starting in July 1993. A monthly series is generated by averaging across the dailyobservations in each month. The series runs July 1993 to December 2016 for a total of 282 obser-vations.

7

PLANTE: OPEC IN THE NEWS

3 METHODS

3.1 MODELS The empirical models are monthly vector autoregression (VAR) models given by

xt = c+ΨDt +

p∑i=1

Φixt−i + ϵt, (3)

where p is the lag length. The baseline models are bi-variate and include the newspaper index anda measure of oil price volatility. The vector xt is a 2× 1 vector of jointly determined variables, c isa 2× 1 vector of constants, Φi are 2× 2 matrices parameters, and ϵt is a 2× 1 vector of residuals.The Dt term is a deterministic dummy variable set to 1 during months with one of the bi-annualOPEC conference meetings, while Ψ is a 2 × 1 vector. I denote Σ as the variance-covariancematrix of the residuals. The lag length p is determined using the Akaike information criterion(AIC). In the robustness check section, a set of larger VAR models are also considered that includeoil production, demand and prices as variables in the model.

3.2 IMPULSE RESPONSE FUNCTIONS To examine the effects of an unexpected increase in thenewspaper index on oil price volatility I employ generalized impulse response functions, developedby Pesaran and Shin (1998) [26]. This section provides a brief overview of the method.

The generalized impulse response function for variable xℓ, ℓ = 1, ..., k, at time t in response toa shock to variable j is given by

GIℓ (n, δj,Ωt−1) = E(xℓ,t+n|ϵjt = δj,Ωt−1)− E(xℓ,t+n|Ωt−1), (4)

where n = 0, 1, 2, ..., is the forecast horizon, Ωt−1 = xt−1, xt−2, ... is the information set of alllagged observables and δj is the size of the shock.

In the context of the model in (3), my question is analogous to asking what happens if theresidual in the newspaper index equation is non-zero at time t. The exercise considers a positive,one-standard deviation size shock. Equation (4) then provides the answer about how expectationsregarding all of the variables in the model should be adjusted due to this shock, relative to whatwould happen if there were no shock at all.

Generalized impulse response functions are used as I do not wish to take a strong stance onidentifying what underlying structural shocks might be behind a particular unforecastable changein the newspaper index. While identifying causal connections is of significant interest, the strongassumptions necessary to do so may give mis-leading answers about causality if those assumptionsare incorrect. A more detailed discussion on causality is found in section 4.3.2.

4 RESULTS

4.1 BI-VARIATE VARS I begin the analysis with a pair of reduced-form, bi-variate VAR modelsthat include just the log of the newspaper index and a measure of oil price volatility. The first modeluses the realized volatility series for WTI prices given by equation (2). The sample for this modelruns from January 1986 to December 2016, a total of 372 observations. The lag length is set to 4lags, based on an AIC test done with 12 lags as the maximum lag length considered. The secondmodel uses the WTI implied volatility series in place of realized volatility. My data on implied

8

PLANTE: OPEC IN THE NEWS

volatility begins in July 1993, providing 282 observations. I continue to use 4 lags for this model,as well.8

I consider a positive, one-standard deviation shock to the newspaper index. Figure 3 plots theresponses of the variables. The top panel is for the model with realized volatility, the bottom forthe model with implied volatility. For each variable, the solid line is the point estimate for theresponse, the dotted and dashed lines are one and two standard-error bands, respectively.

For both models, I find that shocks to the newspaper index lead to a persistent increase inthe index itself. The initial effect subsides rapidly after one month but remains positive for manymonths thereafter. The path of the index is basically indistinguishable between models. There isvery strong statistical evidence that this shock is associated with higher oil price volatility, whetherit be measured by realized volatility or implied volatility. The initial increase is one to two per-centage points and the response is statistically significant at the 95 percent level. The increases involatility are persistent and generally statistically significant over a 12 month horizon.

The impulse responses pick up a strong statistical connection between unexpected changes inthe newspaper index and changes in oil price volatility. One explanation for this result is that un-expected increases in the newspaper index occur during a month when there is greater speculationor uncertainty about OPEC production levels. Given that OPEC is a large player in the marketand that some members of OPEC are very large producers in their own right, questions about theirproduction levels could certainly generate price volatility. At a deeper level, such unusual specu-lation could be driven by several different types of events. These could include unexpected supplydisruptions in an OPEC country, disagreement between OPEC members about current or futureproduction levels, or events in the oil market or broader economy that raise questions about howOPEC will respond. I discuss these issues in greater detail in Section 4.3 when I look into theevents the model picks up as shocks.

4.2 ROBUSTNESS CHECKS I considered several checks to document how robust the previousresults are to modifications in the model and data. Overall, I find that the connection betweenshocks to the newspaper index and oil price volatility are quite robust. Figure 5 plots the gen-eralized impulse response functions for oil price volatility to the newspaper index shock for thedifferent cases considered. The left and right panels plot realized volatility and implied volatility,respectively.

4.2.1 EXPANDED VAR MODEL The bi-variate VAR models provide strong statistical evidencethat unexpected changes in the OPEC newspaper index are associated with changes in oil pricevolatility. However, there are many other variables that have been shown to be important whenmodeling the oil market. Thus, as a robustness check I now expand the VAR models to includesupply, demand and price variables, as in Kilian (2009) [22]. Adding these variables also allowsthe model to take into account potentially predictable movements in the index due to changes inlags of those three variables. For my models, I specifically use the log difference of world oilproduction, the log difference of world industrial production, and the log difference of real WestTexas Intermediate spot prices. These variables are multiplied by 100. As before, I consider oneVAR model that includes WTI realized volatility and another that uses WTI implied volatility.

Figure 4 compares the responses of oil price volatility to a shock to the newspaper index forthe small and large VAR models. The left panel shows realized volatility, the right implied volatil-

8The AIC test generally picks a lag length of 3 or 4 lags for most of the models considered in this paper.

9

PLANTE: OPEC IN THE NEWS

0 2 4 6 8 10

Months

0

0.5

1

0 2 4 6 8 10

Months

-2

0

2

4

6

0 2 4 6 8 10

Months

0

0.5

1

0 2 4 6 8 10

Months

0

1

2

3

Figure 3: Generalized impulse response functions for a shock to the OPEC newspaper index. Dashed lines are 2 s.e.bands, dotted lines 1 s.e. bands. The top set of figures is for the model with realized volatility. The bottom set is forthe model with implied volatility.

ity. Although the model now includes a number of other variables, I find that the responses of thevolatility variables are quite similar between the bi-variate case and the larger VAR model. An un-expected increase in the newspaper index continues to be associated with increased price volatility.Although not shown here, I find that the impulse response for the newspaper index itself is verysimilar across all four models.

4.2.2 BRENT PRICES The second robustness check uses data based on Brent crude as a substi-tute for WTI price and volatility data in the larger VAR model. For the model that uses realizedvolatility the sample size remains the same. Data on implied volatility for Brent crude is availablestarting in 1997, instead of 1993. The dotted lines in Figure 5 show the responses. I find that usingBrent crude data does not significantly alter the results.

4.2.3 GOOGLE SVI Another variant replaces the newspaper index with the Google SVI vari-able. These models are estimated from 2004 to 2016, due to the data limitations on the SVI. Theseresponses are the dashed lines in Figure 5. Overall, I find that unexpected increases in the SVI areassociated with higher levels of volatility compared with the models that use the newspaper index.

4.2.4 ALTERNATIVE INDEX The circles in Figure 5 plots the responses when the alternativeformulation of the newspaper index is used where the OPEC count is divided by the total volumeof articles each month. The circles almost perfectly track the responses of the large VAR thatincludes the baseline index.

10

PLANTE: OPEC IN THE NEWS

0 2 4 6 8 10

Months

0

1

2

3

4

Small VARLarge VAR

0 2 4 6 8 10

Months

0

1

2

3

4

Small VARLarge VAR

Figure 4: Generalized impulse response functions for a shock to the OPEC newspaper index. The left panel is forVAR models with realized volatility. The right figure for models that include implied volatility.

4.2.5 ALTERNATIVE EXPERIMENT Finally, I also consider an alternative experiment where Iask what happens if there is an unexpected increase in the newspaper index now but no contempo-raneous response in any of the other variables. I implement this using a Cholesky decomposition ofthe VAR model with the newspaper index ordered last. The dashed-dotted line in Figure 5 showsthe response of volatility under these assumptions. An unexpected increase in the index foreshad-ows higher levels of both realized and implied volatility in the near future. The response furtherout in time is very similar to the responses from the other cases considered.

4.3 ANALYSIS OF RESIDUALS For generalized impulse response functions, the shocks to thenewspaper index are the residuals from its equation, i.e. the unforecastable changes in the indexat time t. Given this, as part of the analysis I investigated the time series of the residuals to seeif they corresponded with particular OPEC events. For this analysis, I used the five-variable VARmodel with realized volatility. This model allows me to conduct the analysis back to 1986, and theuse of the five-variable model ensures that I have eliminated movements in the newspaper indexthat might be predictable given lagged values of supply, demand and prices. This exercise was alsodone using Google SVI data but those results are relegated to the appendix, as they were similar innature to the results for the newspaper index.

4.3.1 NEWSPAPER INDEX Table 2 lists the ten largest shocks from the model. The largest,in August 1990, picks up the Iraq invasion of Kuwait. The others line up with OPEC meetings ofvarious sorts. In one case, May 2004, the shock picks up an OPEC meeting and militant attacks thatoccurred in Saudi Arabia that month.9 The newspaper index is forward-looking and occasionally

9A majority of the articles that month focused on the meeting. Of the 161 articles that contained the keywordOPEC, only 17 matched the keywords OPEC and terrorist and only 3 matched OPEC and militant.

11

PLANTE: OPEC IN THE NEWS

0 2 4 6 8 10

Months

0

1

2

3

4

5

Large VARBrentGoogleCholeskyAlt. Index

0 2 4 6 8 10

Months

0

1

2

3

4

Large VARBrentGoogleCholeskyAlt. Index

Figure 5: Generalized impulse response function for a shock to the OPEC newspaper index.

picks up unusual interest in events that occur later on. This is the case in October 2014, forexample, when the index jumped in anticipation of a meeting in the following month. Beyondthe top ten, many of the shocks also reflect meetings, with the next three largest shocks pickingup an emergency ministers’ meeting in April 1988, the OPEC meeting in October 2008 duringthe financial crisis and a regularly scheduled meeting in November 1997.10 While many periodsof unusual interest in OPEC line up with meetings, not every meeting generates the same interestlevels. There were more than 90 official OPEC meetings from 1986 to 2016 but only a handful,those ranked from 2 to 6 in the table, resulted in shocks greater than 2 standard deviations in size.

Of the nine meetings listed in Table 2, there was one regularly scheduled bi-annual conference,four emergency meetings, one Ministerial Monitoring Committee (MMC) meeting, and three meet-ings that are more difficult to categorize. With regards to the latter, the first of these is the August1986 meeting in Geneva, which ostensibly was a reconvening of the 78th OPEC meeting, a bi-annual conference meeting that occurred in June of that year. The second was an informal meetingheld in Amsterdam in May 2004 that preceded an emergency meeting in early June 2004. Thethird was the meeting in November 2007, which was an OPEC “summit” held in Saudi Arabia.

One question of interest is why the amount of attention focused on OPEC was unusually highduring those months listed in Table 2. To shed some light on this, I discuss some of the factsbehind the three largest shocks associated with meetings: October 2014, October 2006 and March1998. I also discuss the August 1986 meeting, given its unusual nature and the fact that it led to aproduction agreement. Discussion about the invasion of Kuwait, the largest shock, is omitted forbrevity’s sake given its well-known importance for the oil market.

The August 1986 meeting was officially a reconvening of an earlier meeting held in June 1986.It was preceded by a substantial decline in oil prices during 1986, due in part to a large Saudi

10Additional details about the shocks, including negative shocks, can be found in the appendix.

12

PLANTE: OPEC IN THE NEWS

Arabian production increase from record lows in mid-1985. The August meeting attracted muchattention due to the fact that it led to a surprise agreement on production levels.11 WTI pricesjumped almost 30 percent the week of the announcement. Unlike many of the other meetingslisted in Table 2, in this case prices remained fairly stable for many months after the meeting.

Rank Date Events

1 August 1990 Iraq invades Kuwait

2 October 2014 Month prior to OPEC meeting (ordinary)

3 October 2006 OPEC meeting (emergency)

4 March 1998 OPEC meeting (emergency)

5 September 1993 OPEC meeting (emergency)

6 May 2004 Informal OPEC meeting

Militant attacks in Saudi Arabia

7 September 1992 Ministerial Monitoring Committee meeting

8 August 1986 OPEC meeting, production agreement

9 November 2007 OPEC meeting (summit)

10 November 2001 OPEC meeting (emergency)

Table 2: This table lists the top ten shocks from the five variable VAR model with realized volatility.

Understanding the March 1998 meeting first requires discussing the November 1997 meeting,which was ranked as the 13th largest shock, as the two are connected. In early November 1997,Saudi Arabia’s oil minister announced a desire to raise the OPEC production ceiling, interpretedby many as indicating Saudi Arabia’s intention to increase production.12 Indeed, Saudi productiondid increase in late 1997 and early 1998, as did output in the United Arab Emirates and Kuwait.In this particular meeting, there was an unexpected shift in OPEC policy that did not appear to beconnected with a recent movement in oil prices.

The outcome of the November meeting eventually had implications for oil prices, which felldramatically due to the increased supply, the return of Iraqi production and the impacts of theAsian financial crisis on demand. The March 1998 meeting attracted significant attention becausethere was internal disagreement between OPEC countries over how to respond to recent pricedeclines. Reporting through most of March suggested no agreement would be reached. However,a surprise announcement regarding a production cut was made over the weekend of March 21 and22.13 Although prices stabilized temporarily, they eventually declined until they were close to $10a barrel by year-end 1998.

No OPEC meeting was originally scheduled for October 2006 but an emergency meeting washeld by the group on October 19 and 20. This meeting was spurred by a sharp decline in oilprices in the preceding months, with WTI having dropped more than 15 percent. This led tosuggestions in early October of a possible meeting in the middle of month, although there were

11See “OPEC reaches tentative accord” (1986) [1].12See Bahree and Fritsch (1997) [6] for more details.13See Lucchetti and Ewing (1998) [23] for more details.

13

PLANTE: OPEC IN THE NEWS

apparent disagreements over a potential production cut. An agreement was reached at the meeting,although there was some uncertainty reported among market participants about the deal.14

Finally, the events of October 2014 are not so distant in the past and perhaps require lessdiscussion. Oil prices had fallen since mid-summer and by early October WTI prices were closeto $90 a barrel. By the end of the month they were close to $80 a barrel. This is one case wherethe newspaper index exhibits some forward looking behavior, as the media was already writing anunusual number of articles mentioning OPEC despite the fact that its upcoming meeting was notuntil later in November. Similar to the October 2006 shock, media attention was focused on howOPEC might respond to the recent decline in oil prices.

A common feature across many of the meetings in table 2 is that they were preceded by anotable change in oil prices. Price declines occurred before the meetings in 1986, 1993, 1998,2006 and in 2014, while increases preceded the meetings in May 2004 and November 2007. Toillustrate this more concretely, I took the average (real) price of WTI in the month prior to the shockand compared it to the average price three months prior to the shock. So for example, comparingthe average price in July 1986 to May 1986 I find that prices had declined by 29 percent. Pricesdeclined by 10.1 percent, 23.1 percent, 15.8 percent and 10 percent for the 1993, 1998, 2006 and2014 shocks, respectively. In the two periods where prices rose before the meetings, the increasewas 5 percent for the 2004 event and more than 16 percent for the 2007 event. Newspaper articlessuggest these price changes often helped generate increased interest in the OPEC event, as they ledto discussion about how or if OPEC would respond.

One other interesting aspect of the October 2014 shock is that it is the result of events in theoil market that go beyond an OPEC meeting. The meeting in November 2014 was a regularlyscheduled meeting and would have occurred regardless of those events but would probably nothave garnered much, if any, unusual media interest had it not been for the price declines precedingit. This differs from the November 1997 shock, for example, which picked up a surprise policychange in production levels due to Saudi Arabia prodding. It also differs from the 1986 shockwhich, although driven by events in the oil market, was intimately connected with Saudi Arabia’sdecision to increase production in 1985 and 1986. Although not discussed in detail in this section,the October 2008 shock in this regard resembles the 2014 shock, as it was clearly being driven byevents beyond OPEC, in this case the financial crisis.

4.3.2 DISCUSSION ON CAUSALITY The models and methodology used here do not make anydirect statements about causality between unexpected changes in the newspaper index and oil pricevolatility levels. It could be the case that some OPEC events are just unusually important, whichdrive media attention and volatility levels. Or it could be that other developments in the oil marketor broader economy make an OPEC meeting or event more important and, thus, more widelywatched while simultaneously leading to unexpectedly high levels of oil price volatility.

To the extent one can make such statements, the residual analysis suggests that both explana-tions play a role. For example, events such as the Iraq invasion of Kuwait are arguably exogenousevents and garner unusual interest because of their importance. Likewise, although not the same asa war, the unexpected increase in the index that occurred in August 1986 was due to an event thatwas directly related to Saudi Arabia’s prior decision to dramatically increase production levels.This has the sense of an OPEC policy shock, as it were. A similar argument could be made for the

14Please see Bahree (2006) [5], Foss (2006) [16] and Mouawad (2006) [25] for more details.

14

PLANTE: OPEC IN THE NEWS

November 1997 shock.On the other extreme, some unexpected increases in the newspaper index and price volatility

appear to be driven by developments in the oil market or broader economy. For example, the largeunexpected increase in the index in October 2014, reflecting an upcoming meeting, was obviouslydriven by oil price declines occurring around that time. This situation then raised questions abouthow OPEC might respond. A similar example would be the unexpected increase in October 2008,which was connected with developments in the broader economy. By October, the financial crisishad already affected oil prices, generated intense concern about future demand levels and lead toincreased oil price volatility (both implied and realized). Here, developments in the economy thatwere also fueling volatility sparked interest in how OPEC might respond. In cases such as these,disentangling how much of the variation in oil price volatility is due to the underlying state of theworld and how much is due to the OPEC events themselves appears to be a non-trivial task.

5 CONCLUSIONS

In this paper I introduce a monthly newspaper index that measures interest in OPEC events. I showthat this index rises in response to important OPEC meetings, the Iraq invasion of Kuwait, and otherevents related to OPEC production levels, such as Saudi Arabia’s decision to flood the market inthe mid-1980s. The newspaper index is shown to be highly correlated with other measures ofthe public’s interest in OPEC, such as Google Search Volume Index data. An advantage of thenewspaper index is that it can be extended back much further in time than these alternatives.

I investigate the behavior of oil price volatility when there are unexpected changes in the news-paper index. There is very strong statistical evidence that unexpected increases in the index areassociated with higher levels of oil price volatility, whether measured by implied volatility or real-ized volatility. This result is robust to several variations of the model, including using a differentoil price in the model, using Google SVI data or employing an alternative formulation of the index.I find that many of the largest, unexpected increases in the index line up with specific events, pri-marily but not exclusively OPEC meetings. In some cases, interest levels in those events and pricevolatility appear to be endogenously responding to events in the oil market or broader economy.

Many possibilities present themselves for future research. One could envision doing morecomplicated textual analysis of the articles picked up in the search. Or extending this work toconsider a broader set of events that have affected the oil market beyond those related to OPEC.The author is also currently investigating the potential usefulness of a higher frequency newspaperindex for forecasting oil price volatility (or vice-versa).

REFERENCES

[1] Opec reaches tentative accord on iranian plan to limit output. The New York Times, August 5,1986.

[2] Afkhami, M., Cormack, L., and Ghoddusi, H. (2017). Google search keywords that bestpredict energy price volatility. Energy Economics, 67:17–27.

[3] Amelier, C. and Darne, O. (2014). Volatility persistence in crude oil markets. Energy Policy,65:729–742.

15

PLANTE: OPEC IN THE NEWS

[4] Andrei, D. and Hassler, M. (2014). Investor attention and stock market volatility. The Reviewof Financial Studies, 28 (1):33–72.

[5] Bahree, B. Opec encounters hurdles in effort to trim output. The Wall Street Journal, October6, 2006.

[6] Bahree, B. and Fritsch, P. Saudis signal desire to produce more oil as opec session looms. TheWall Street Journal, November 6, 1997.

[7] Baker, S. R., Bloom, N., and Davis, S. J. (2016). Measuring economic policy uncertainty. TheQuarterly Journal of Economics, 131(4):1593–1636.

[8] Baker, S. R. and Fradkin, A. (2017). The impact of unemployment insurance on job search:Evidence from google search data. The Review of Economics and Statistics, 99(5):756–768.

[9] Barber, B. M. and Odean, T. (2008). All that glitters: The effect of attention and news on thebuying behavior of individual and institutional investors. Review of Financial Studies, 21:785–818.

[10] Bernanke, B. S. (1983). Irreversibility, unvertainty, and cyclical investment. The QuarterlyJournal of Economics, 98(1):85–106.

[11] Da, Z., Engleberg, J., and Gao, P. (2011). In search of attention. Journal of Finance, LXVI,no. 5:1461–1499.

[12] Demirer, R. and Kutan, A. M. (2010). The behavior of crude oil spot and futures prices aroundopec and spr announcements: An event study perspective. Energy Economics, 32:1467–1476.

[13] Elder, J. and Serletis, A. (2010). Oil price uncertainty. Journal of Money, Credit and Banking,42(6):1137–1159.

[14] Engleberg, J. E. and Parsons, C. A. (2011). The causal impact of media in financial markets.Journal of Finance, LXVI (1):67–97.

[15] Ferderer, J. (1996). Oil price volatility and the macroeconomy. Journal of Macroeconomics,18(1):1–26.

[16] Foss, B. Opec move leaves doubts. Houston Chronicle, October 21, 2006.

[17] Grossman, V., Mack, A., and Martinez-Garcia, E. (2014). A new database of global economicindicators. Journal of Economic and Social Measurement, 39(3):163–97.

[18] Guo, H. and Kliesen, K. L. (2005). Oil price volatility and u.s. macroeconomic activity.Federal Reserve Bank of St. Louis Review, 87(6):669–683.

[19] Horan, S. M., Peterson, J. H., and Mahar, J. (2004). Implied volatility of oil futures optionssurrounding opec meetings. The Energy Journal, 25(3):103–125.

[20] Jo, S. (2013). The effects of oil price uncertainty on the macroeconomy. forthcoming, Journalof Money, Credit and Banking.

16

PLANTE: OPEC IN THE NEWS

[21] Kellogg, R. (2014). The effect of uncertainty on investment: Evidence from texas oil drilling.American Economic Review, 104(6):1698–1734.

[22] Kilian, L. (2009). Not all oil price shocks are alike: Disentangling demand and supply shocksin the crude oil market. American Economic Review, 99(3):1053–69.

[23] Lucchetti, A. and Ewing, T. Oil prices rocket 13%, stir commodity sector. The Wall StreetJournal, March 24, 1998.

[24] Mensi, W., Hammoudeh, S., and Yoon, S.-M. (2014). How do opec news and structuralbreaks impact returns and volatility in crude oil markets? further evidence from a long memoryprocess. Energy Economics, 42:343–354.

[25] Mouawad, J. From opec, conflicting talk of output cut. The New York Times, October 6, 2006.

[26] Pesaran, H. H. and Shin, Y. (1998). Generalized impulse response analysis in linear multi-variate models. Economics Letters, 58:17–29.

[27] Robe, M. A. and Wallen, J. (2016). Fundamentals, derivates market information, and oil pricevolatility. Journal of Futures Markets, 36(4):317–344.

[28] Schmidbauer, H. and Rosch, A. (2012). Opec news announcements: Effects on oil priceexpectation and volatility. Energy Economics, 34(5):1656–1663.

[29] Tetlock, P. C. (2007). Giving content to investor sentiment: The role of media in the stockmarket. The Journal of Finance, LXII (3):1139–1168.

[30] Yuan, Y. (2015). Market-wide attention, trading and stock returns. Journal of FinancialEconomics, 116:548–564.

17

PLANTE: OPEC IN THE NEWS

NOT FOR PUBLICATION

A APPENDIX

A.1 FACTIVA DATA The Factiva searches make use of the Search Builder command. I performa “Free Text Search” using the keyword OPEC. The duplicates toggle is set to “Identical.” Theexact sources are The New York Times, print edition (newspaper icon); The Wall Street Journal,print edition (newspaper icon); the Financial Times (Available through Third Party SubscriptionServices), print edition (newspaper icon); and the Houston Chronicle, print edition (newspapericon). The toggles “Search Source Name/Alias only” and “Exclude Discontinued Sources” arechecked. In some months, Factiva erroneously reports duplicates of an article as being distinctfrom each other. To deal with this, the articles were checked by hand and those duplicates removedfrom the counts. The results are not very different whether or not these duplicates are removed.Figure 6 plots the standardized time series for each of the four newspaper articles.

To generate the estimate for the total volume of news articles each month I repeat the searchbut replace the keyword “OPEC” with “the or a or an.” Given the grammatical structure of English,which requires these three words to appear frequently in sentences, this should capture most, if notall, of the articles written in the newspapers considered.

1990 1995 2000 2005 2010 20150

2

4

6

1990 1995 2000 2005 2010 20150

2

4

6

1990 1995 2000 2005 2010 20150

2

4

6

8

1990 1995 2000 2005 2010 20150

2

4

6

8

Figure 6: Standardized time series for the individual newspaper series.

18

PLANTE: OPEC IN THE NEWS

A.2 GOOGLE DATA AND RESULTS The Google search volume data is produced in the followingmanner. I use the Google Trends web site and get the data for OPEC as a topic, not a keyword.The geographic area is the entire world. The sample runs from 2004 to 2016 and Google Trendsreturns the data in monthly frequency.

Table 3 presents the correlations between the Google data, the OPEC newspaper index and theindividual counts. The Google data has a fairly high correlation with the newspaper index and theindividual counts.

Residual analysis was also done with the model using Google SVI data. As the sample starts in2004, only a subset of the events that might be picked up by the newspaper index are covered withthe SVI data. Table 4 lists the top 10 shocks. Many of the events that lay behind these unexpectedincreases in search activity on OPEC were also picked out as unusual events in the baseline model.

Google SVI 1.00

Financial Times 0.75 1.00

Houston Chronicle 0.72 0.76 1.00

New York Times 0.74 0.70 0.73 1.00

Wall Street Journal 0.62 0.79 0.78 0.70 1.00

OPEC index 0.78 0.93 0.89 0.83 0.92 1.00

Table 3: Correlations between Google SVI, the OPEC index and the individual newspaper counts. The sample runsfrom Jan. 2004 to Dec. 2016.

Rank Date Events

1 November 2014 OPEC meeting

2 November 2007 OPEC summit

3 October 2008 OPEC meeting (emergency)

4 October 2006 OPEC meeting (emergency)

5 May 2004 Informal OPEC meeting

Militant attacks in Saudi Arabia

6 August 2005 Oil price surge, month prior to meeting

7 December 2015 OPEC meeting

8 May 2008 Militant attacks in Nigeria

9 June 2004 OPEC meeting (emergency)

10 September 2016 OPEC meeting (emergency)

Table 4: This table lists the top ten shocks for the VAR model that uses Google data in place of the OPEC newspaperindex.

19

PLANTE: OPEC IN THE NEWS

A.3 ADDITIONAL RESULTS Table 5 lists the top 20 positive shocks from the baseline model.In general, the shocks ranked 11 to 20 occur either one month prior to or during the month of anOPEC meeting. The 14th largest shock, which is in April 1997, does not pick up any particularevent. Instead, it is statistical in nature and driven by the fact that in the prior month there wasan exceptionally low amount of articles written on OPEC. As the index is persistent in nature, theincrease that occurred in April appears as a large positive shock to the index. The 16th largestshock picks up the Venezuela coup attempt in April 2002.

Rank Date Events

1 August 1990 Iraq invades Kuwait

2 October 2014 Month prior to OPEC meeting (ordinary)

3 October 2006 OPEC meeting (emergency)

4 March 1998 OPEC meeting (emergency)

5 September 1993 OPEC meeting (emergency)

6 May 2004 Informal OPEC meeting

Militant attacks in Saudi Arabia

7 September 1992 Ministerial Monitoring Committee meeting

8 August 1986 OPEC meeting, production agreement

9 November 2007 OPEC meeting (summit)

10 November 2001 OPEC meeting (emergency)

11 April 1988 Ministerial meeting (emergency)

12 October 2008 OPEC meeting (emergency)

13 November 1997 OPEC meeting (ordinary)

14 April 1997 No event (index jumps from low in March 1997)

15 February 2000 Month prior to OPEC meeting

16 April 2002 Venezuela coup

17 August 2002 Month prior to OPEC meeting

18 March 1991 Ministerial Monitoring Committee meeting

19 June 2000 OPEC meeting (emergency)

20 July 2001 OPEC conference

Table 5: This table lists the top twenty shocks from the five variable VAR model with realized volatility.

20

PLANTE: OPEC IN THE NEWS

Table 6 lists the ten most negative shocks in the model. By construction, these occur duringmonths when there were unexpectedly low article counts. In some cases, this is literally becausethe number of articles written about OPEC was very low relatively to the norm. These shocks areclustered in the mid-1990s, a period of relatively stable oil prices. Several of the shocks occur in amonth following an OPEC meeting. This occurs for two reasons. First, in general there are morearticles written about OPEC during months with meetings. Second, the index is quite persistent, onaverage, so if following a meeting there is a sharp drop in articles, this will show up as a negativeshock in the model.

Rank Date Events

1 March 1997 Only two articles published

2 July 1994 Month following an OPEC meeting

3 February 1996 Only six articles published

4 July 1996 Month following an OPEC meeting

5 September 1994 Only eight articles published

6 December 1996 Only five articles published

7 June 1992 Month following an OPEC meeting

8 April 2004 Month following an OPEC meeting

9 September 1997 Only four articles published

10 February 2015 Sharp drop in articles published

Table 6: This table lists the most negative shocks from the five variable VAR model with realized volatility.

21