Embed Size (px)

Citation preview

www.farminstitute.org.au

Opportunities for Australian agriculture

www.farminstitute.org.au

Australia’s Independent Farm Policy Research InstituteAustralia’s Independent Farm Policy Research Institute

Mick Keogh

Executive Director,

Australian Farm Institute.

www.farminstitute.org.au

Where to for agriculture ?Where to for agriculture ?

• Some big picture trends

– Animal protein consumption

– Biofuels

Australia’s Independent Farm Policy Research Institute

– Biofuels

• Positioning Australian agriculture

for the future

www.farminstitute.org.au

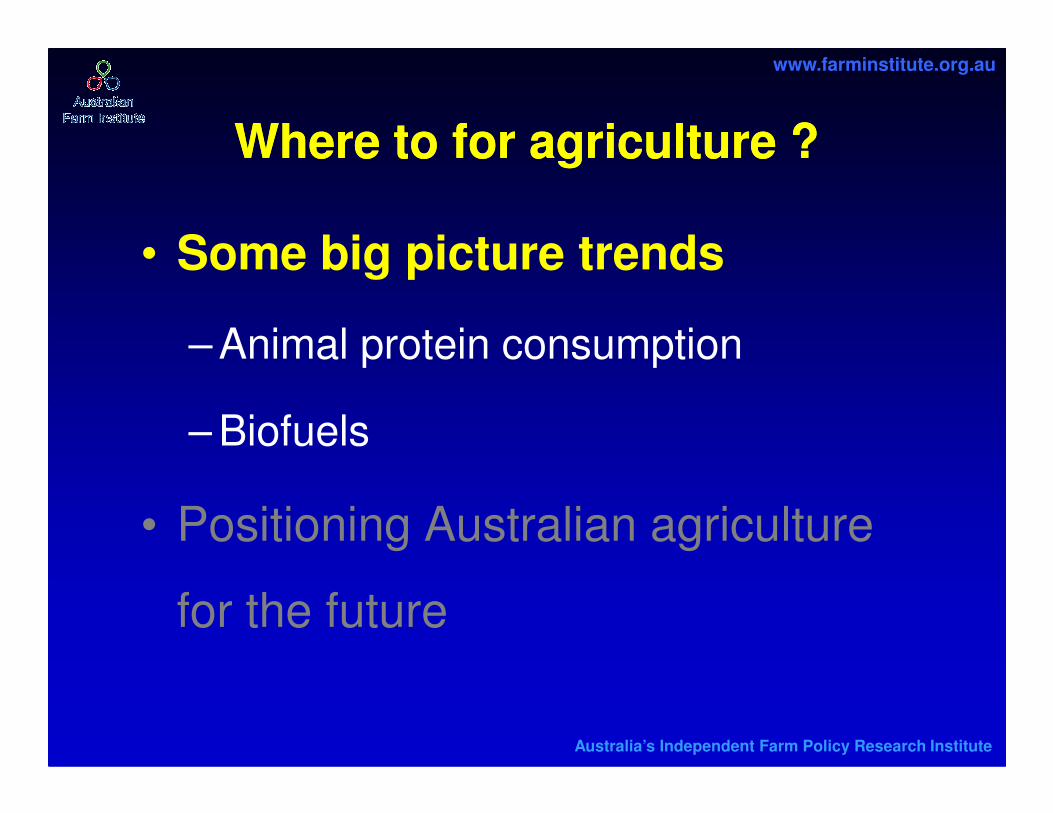

Signs of a fundamental change are emergingSigns of a fundamental change are emerging

200

250

300

350

Australia’s Independent Farm Policy Research Institute

0

50

100

150

Index of real net value of farm production Farmers Terms of Trade

www.farminstitute.org.au

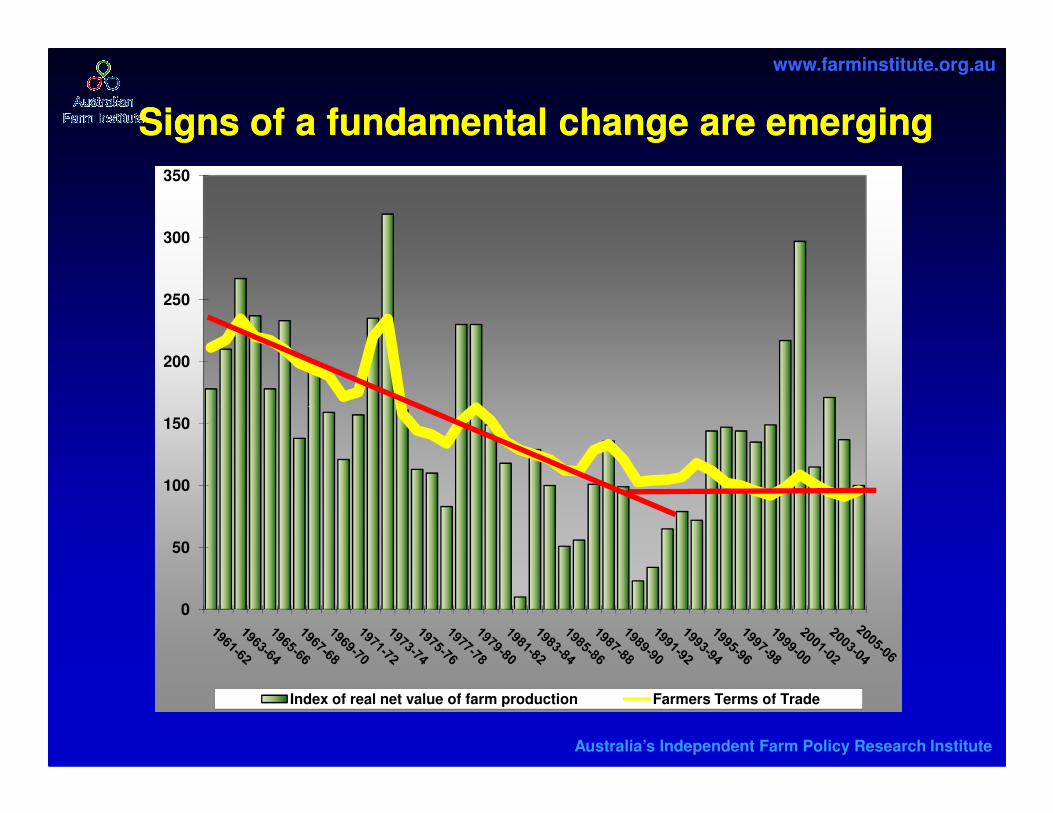

Australian farm commodity price trendsAustralian farm commodity price trends(nominal basis)(nominal basis)

Australia’s Independent Farm Policy Research Institute

www.farminstitute.org.au

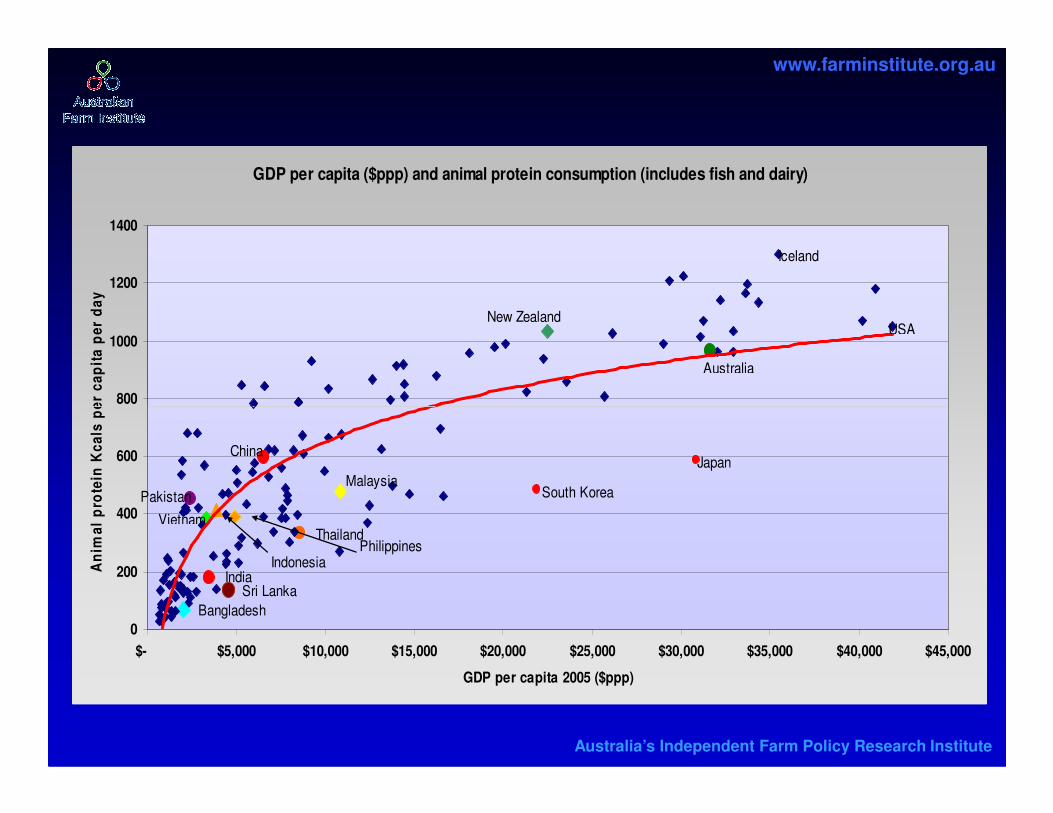

GDP per capita ($ppp) and animal protein consumption (includes fish and dairy)

800

1000

1200

1400

An

ima

l p

rote

in K

ca

ls p

er

ca

pit

a p

er

da

y

USA

Iceland

Australia

New Zealand

Australia’s Independent Farm Policy Research Institute

0

200

400

600

$- $5,000 $10,000 $15,000 $20,000 $25,000 $30,000 $35,000 $40,000 $45,000

GDP per capita 2005 ($ppp)

An

ima

l p

rote

in K

ca

ls p

er

ca

pit

a p

er

da

y

Japan

South Korea

China

IndiaIndonesia

Malaysia

Thailand

Bangladesh

Vietnam

Pakistan

Philippines

Sri Lanka

www.farminstitute.org.au

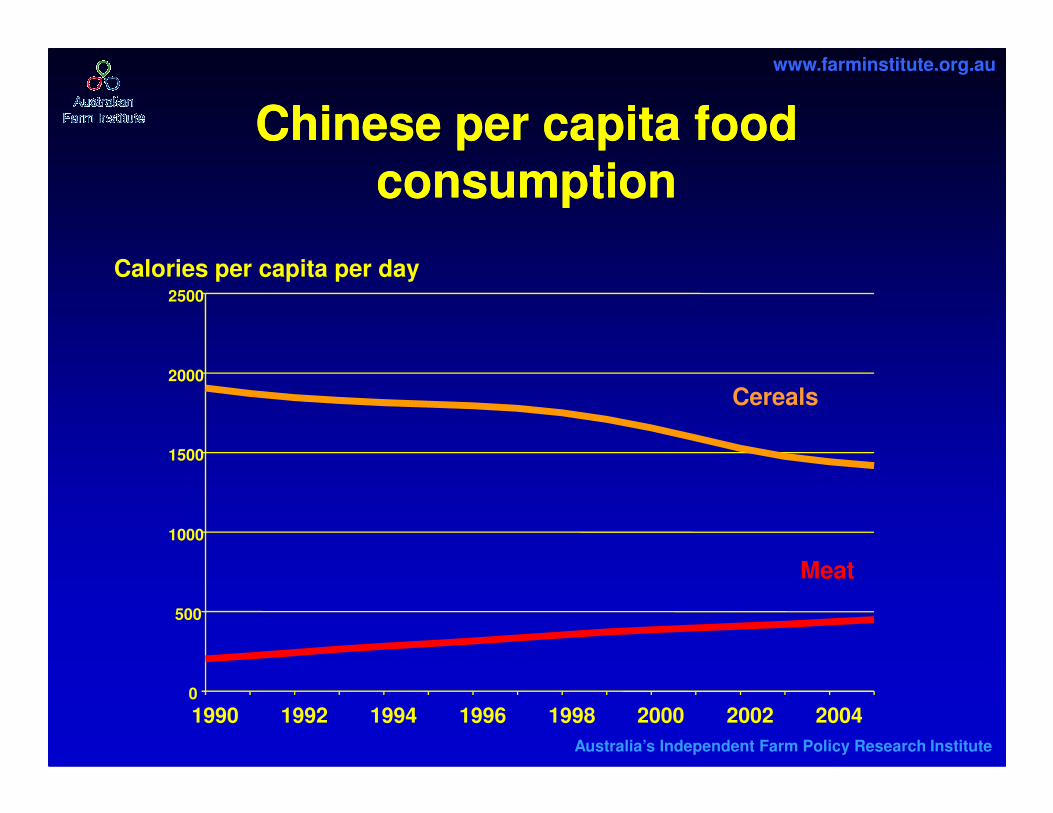

Chinese per capita food Chinese per capita food consumptionconsumption

2000

2500

Cereals

Calories per capita per day

Australia’s Independent Farm Policy Research Institute

0

500

1000

1500

1990 1992 1994 1996 1998 2000 2002 2004

Meat

Cereals

www.farminstitute.org.au

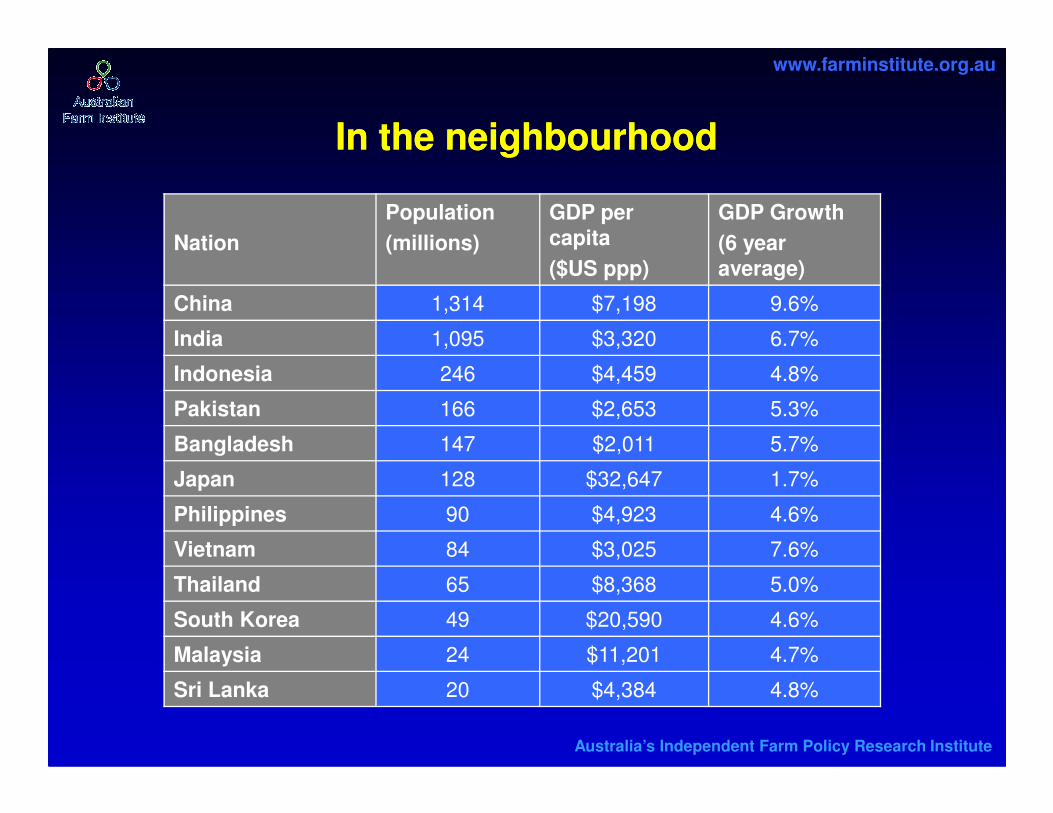

In the neighbourhoodIn the neighbourhood

Nation

Population

(millions)

GDP per capita

($US ppp)

GDP Growth

(6 year average)

China 1,314 $7,198 9.6%

India 1,095 $3,320 6.7%

Indonesia 246 $4,459 4.8%

Pakistan 166 $2,653 5.3%

Australia’s Independent Farm Policy Research Institute

Pakistan 166 $2,653 5.3%

Bangladesh 147 $2,011 5.7%

Japan 128 $32,647 1.7%

Philippines 90 $4,923 4.6%

Vietnam 84 $3,025 7.6%

Thailand 65 $8,368 5.0%

South Korea 49 $20,590 4.6%

Malaysia 24 $11,201 4.7%

Sri Lanka 20 $4,384 4.8%

www.farminstitute.org.au

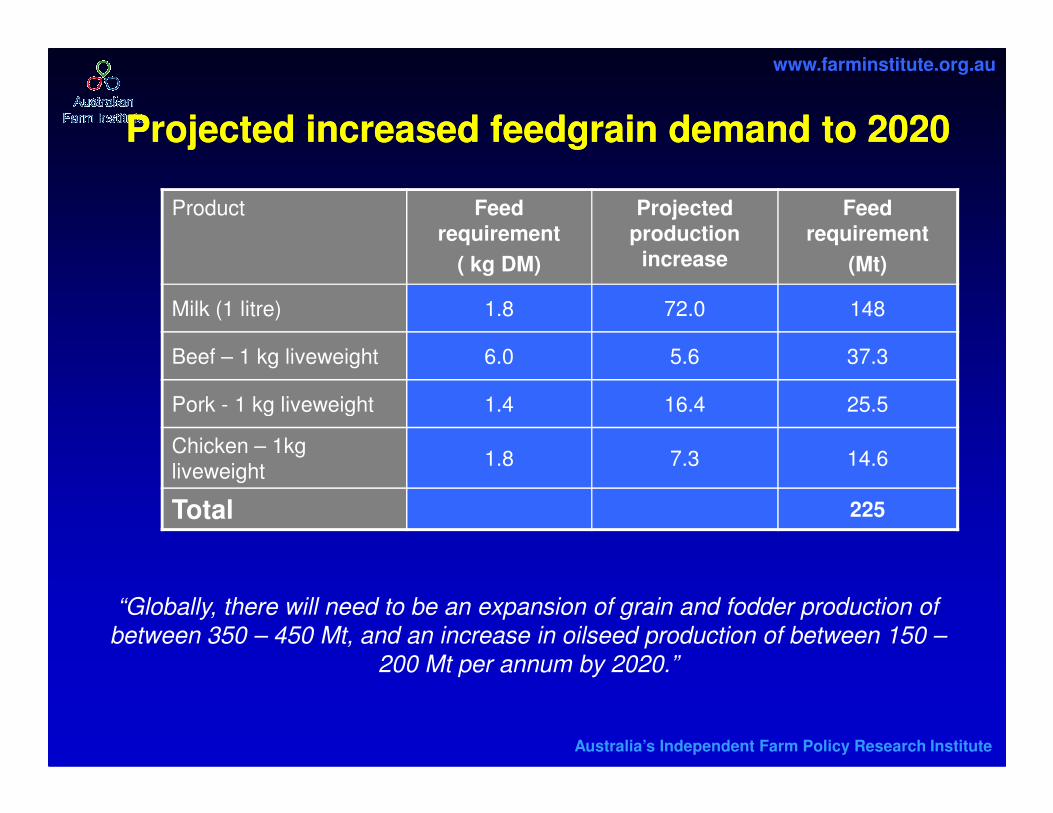

Projected increased feedgrain demand to 2020Projected increased feedgrain demand to 2020

Product Feed requirement

( kg DM)

Projected production

increase

Feed requirement

(Mt)

Milk (1 litre) 1.8 72.0 148

Beef – 1 kg liveweight 6.0 5.6 37.3

Pork - 1 kg liveweight 1.4 16.4 25.5

Australia’s Independent Farm Policy Research Institute

Pork - 1 kg liveweight 1.4 16.4 25.5

Chicken – 1kg liveweight

1.8 7.3 14.6

Total 225

“Globally, there will need to be an expansion of grain and fodder production of

between 350 – 450 Mt, and an increase in oilseed production of between 150 –

200 Mt per annum by 2020.”

www.farminstitute.org.au

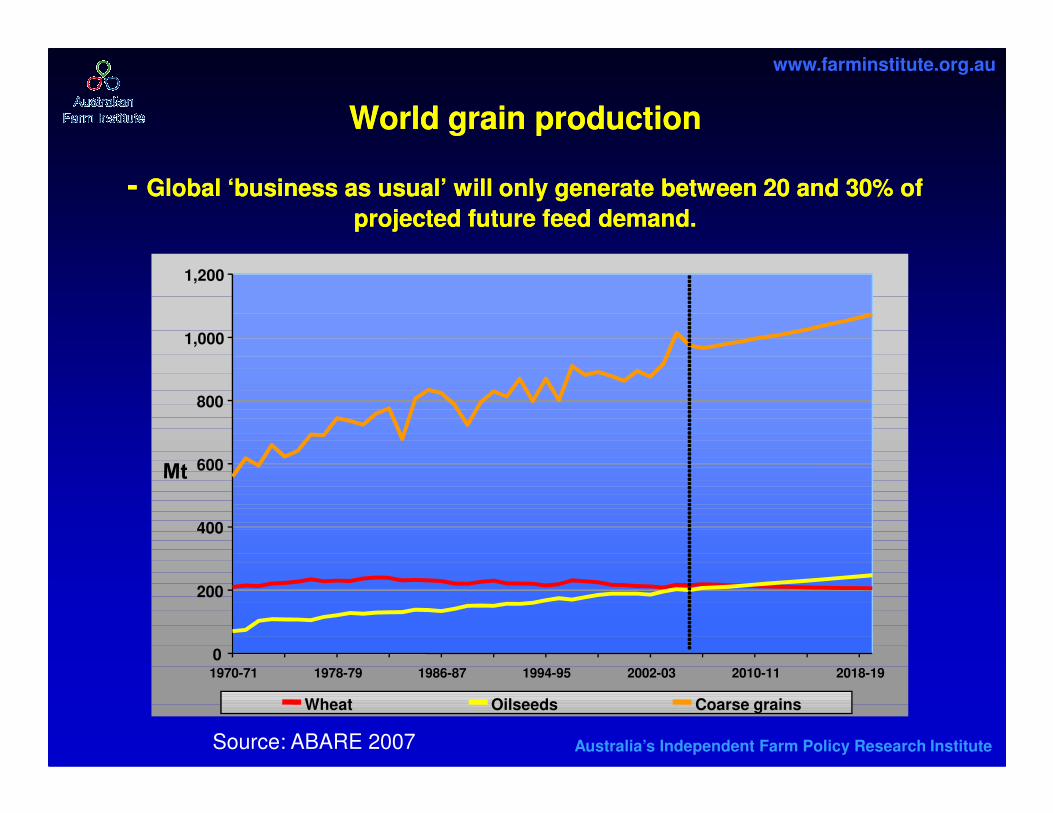

World grain productionWorld grain production

-- Global ‘business as usual’ will only generate between 20 and 30% of Global ‘business as usual’ will only generate between 20 and 30% of

projected future feed demand.projected future feed demand.

800

1,000

1,200

Australia’s Independent Farm Policy Research Institute

0

200

400

600

800

1970-71 1978-79 1986-87 1994-95 2002-03 2010-11 2018-19

Wheat Oilseeds Coarse grains

Source: ABARE 2007

www.farminstitute.org.au

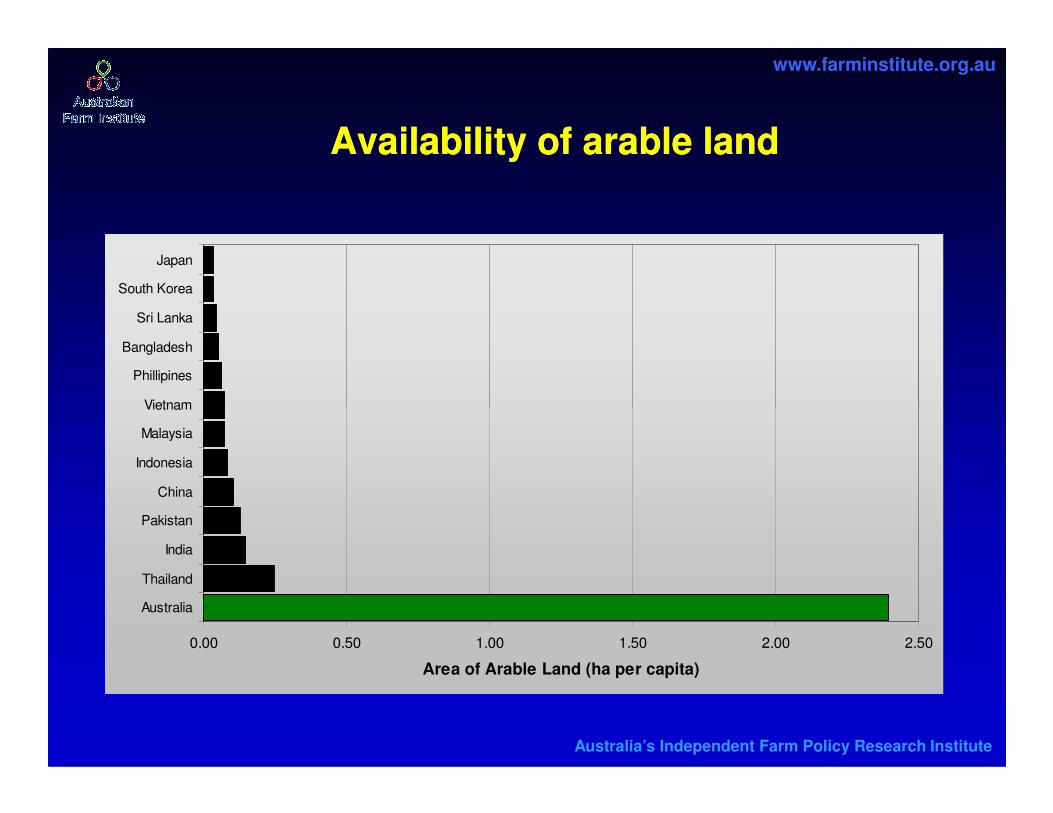

Availability of arable land Availability of arable land

Vietnam

Phillipines

Bangladesh

Sri Lanka

South Korea

Japan

Australia’s Independent Farm Policy Research Institute

0.00 0.50 1.00 1.50 2.00 2.50

Australia

Thailand

India

Pakistan

China

Indonesia

Malaysia

Vietnam

Area of Arable Land (ha per capita)

www.farminstitute.org.au

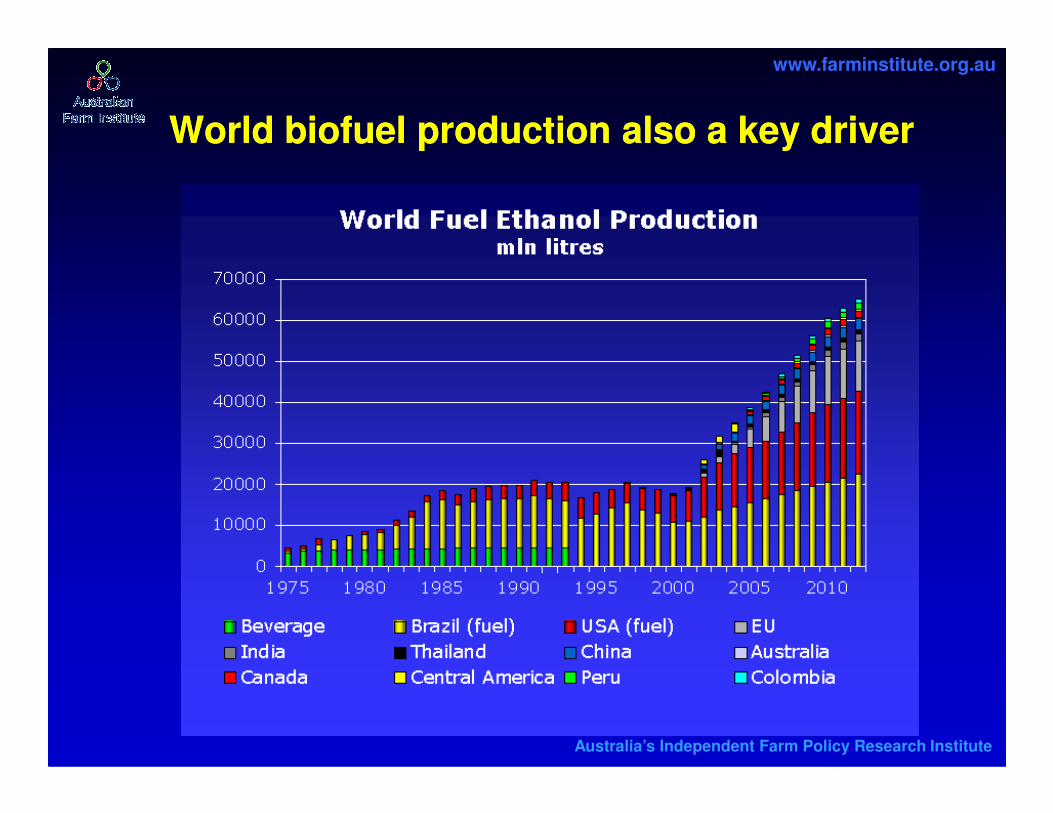

World biofuel production also a key driverWorld biofuel production also a key driver

Australia’s Independent Farm Policy Research Institute

www.farminstitute.org.au

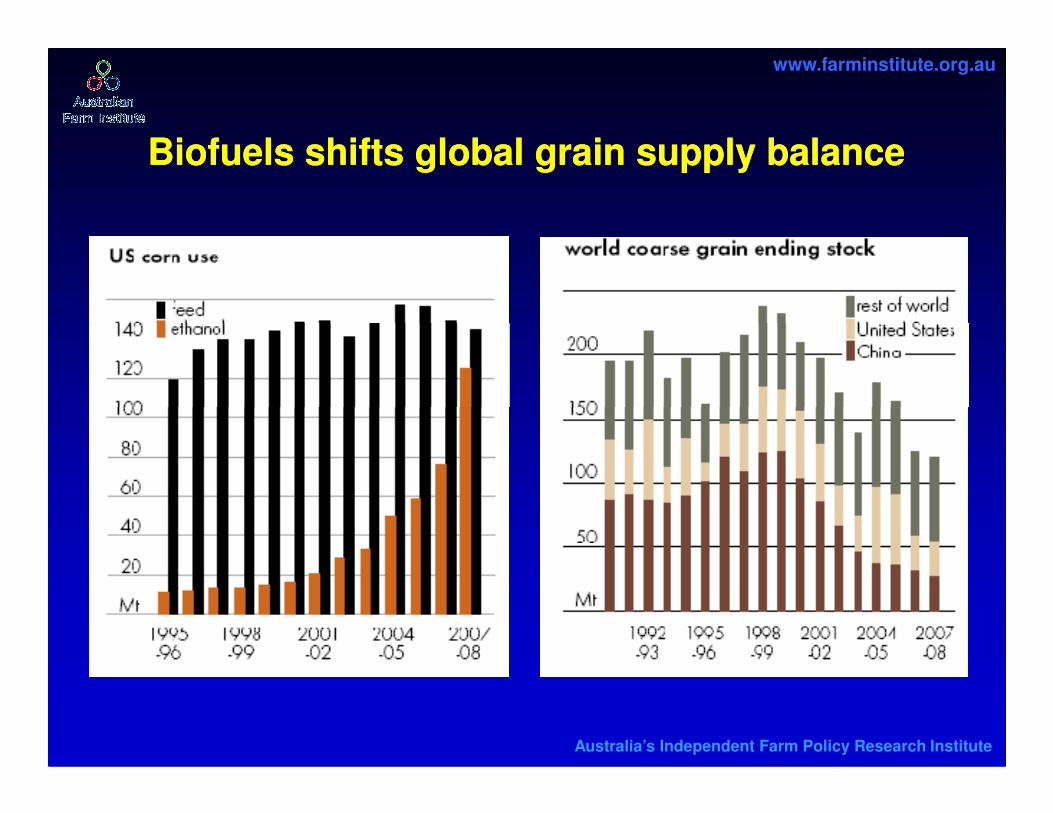

Biofuels shifts global grain supply balanceBiofuels shifts global grain supply balance

Australia’s Independent Farm Policy Research Institute

www.farminstitute.org.au

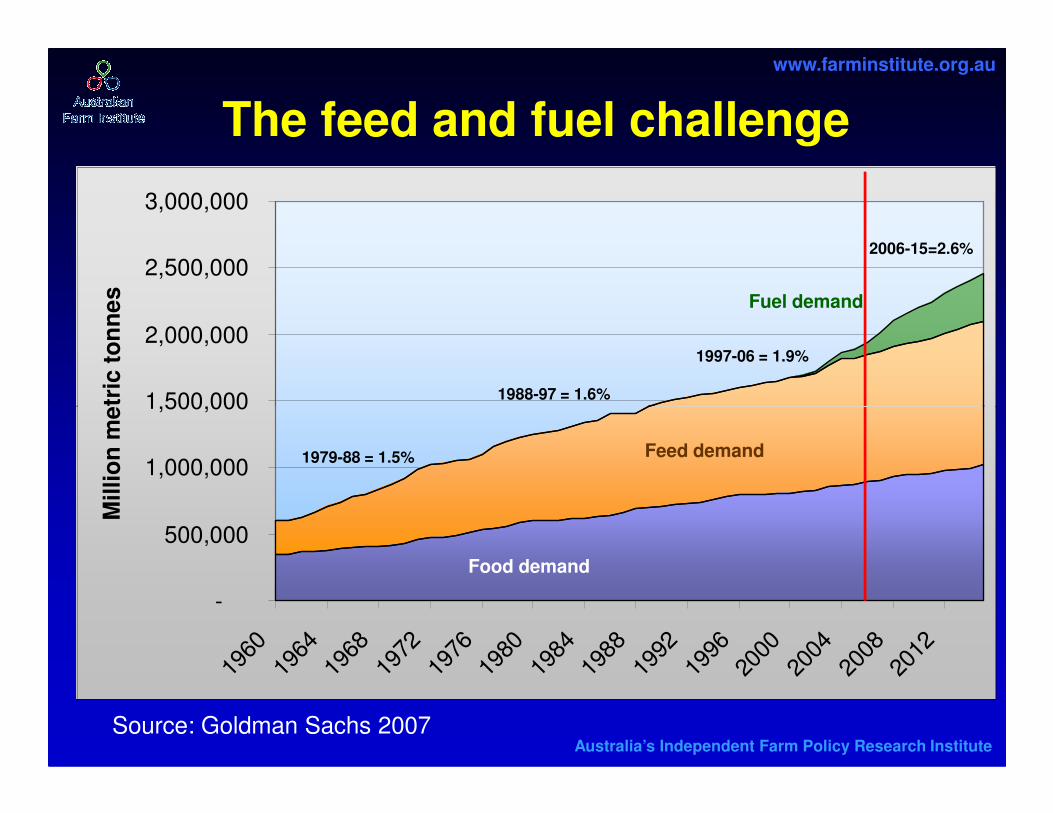

The feed and fuel challenge

1,500,000

2,000,000

2,500,000

3,000,000

Milli

on

me

tric

to

nn

es Fuel demand

1997-06 = 1.9%

1988-97 = 1.6%

2006-15=2.6%

Australia’s Independent Farm Policy Research InstituteSource: Goldman Sachs 2007

-

500,000

1,000,000

1,500,000

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

Milli

on

me

tric

to

nn

es

Food demand

Feed demand1979-88 = 1.5%

www.farminstitute.org.au

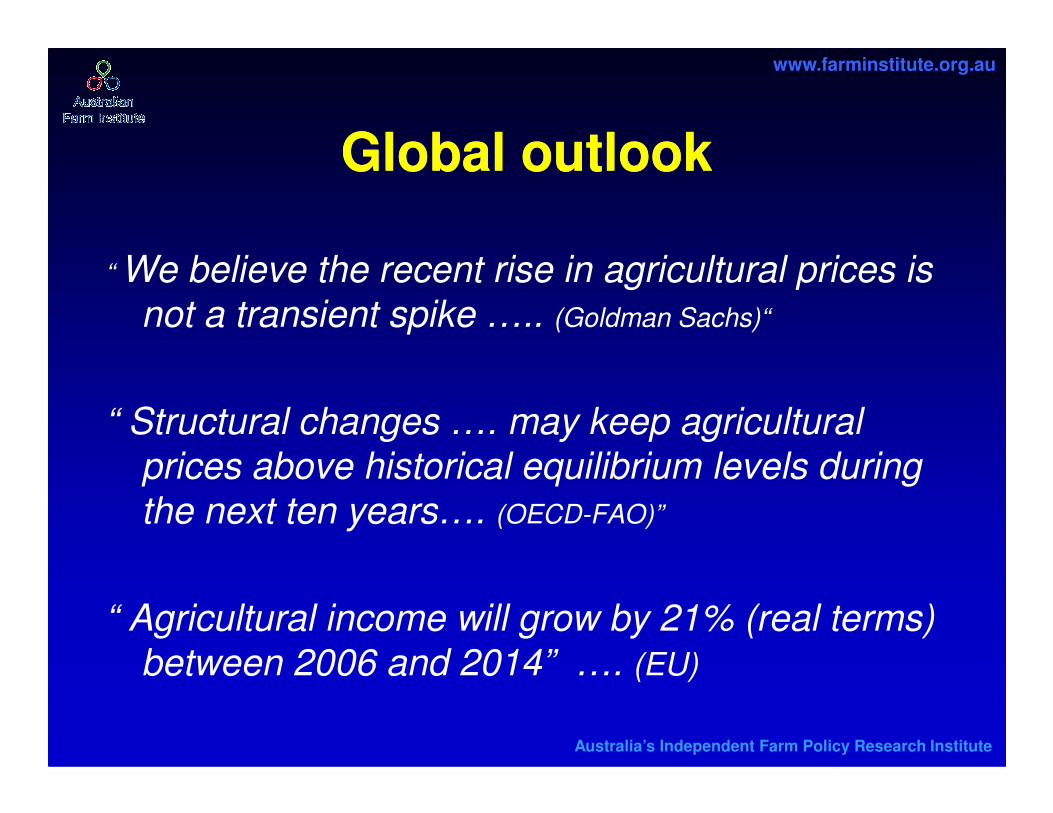

Global outlookGlobal outlook

“ We believe the recent rise in agricultural prices is

not a transient spike ….. (Goldman Sachs)“

“ Structural changes …. may keep agricultural

Australia’s Independent Farm Policy Research Institute

“ Structural changes …. may keep agricultural

prices above historical equilibrium levels during

the next ten years…. (OECD-FAO)”

“ Agricultural income will grow by 21% (real terms)

between 2006 and 2014” …. (EU)

www.farminstitute.org.au

Cargill chief in warning over biofuels boomCargill chief in warning over biofuels boom

By Doug Cameron in Chicago Published: May 30 2007

Australia’s Independent Farm Policy Research Institute

Nestlé chief fears food price inflationNestlé chief fears food price inflationBy Geoff Dyer in Beijing Published: July 5 2007

Commodities surge set to raise food pricesCommodities surge set to raise food pricesBy Javier Blas and Chris Flood in London and Adam Jones in Paris

Published: August 8 2007

www.farminstitute.org.au

Where to for agriculture ?Where to for agriculture ?

• Some big picture trends

– Animal protein consumption

– Biofuels

Australia’s Independent Farm Policy Research Institute

– Biofuels

• Positioning Australian agriculture

for the future

www.farminstitute.org.au

What of the future ?What of the future ?

• Animal protein and fuel demand creating a very positive medium term price outlook

• Australian agriculture will not win a “commodity drag

Australia’s Independent Farm Policy Research Institute

• Australian agriculture will not win a “commodity drag race” with developing nation exporters.

• A focus on consumer/market requirements, and in particular the needs of affluent Asian consumers will be the key to a successful new era of farm profitability.

www.farminstitute.org.au

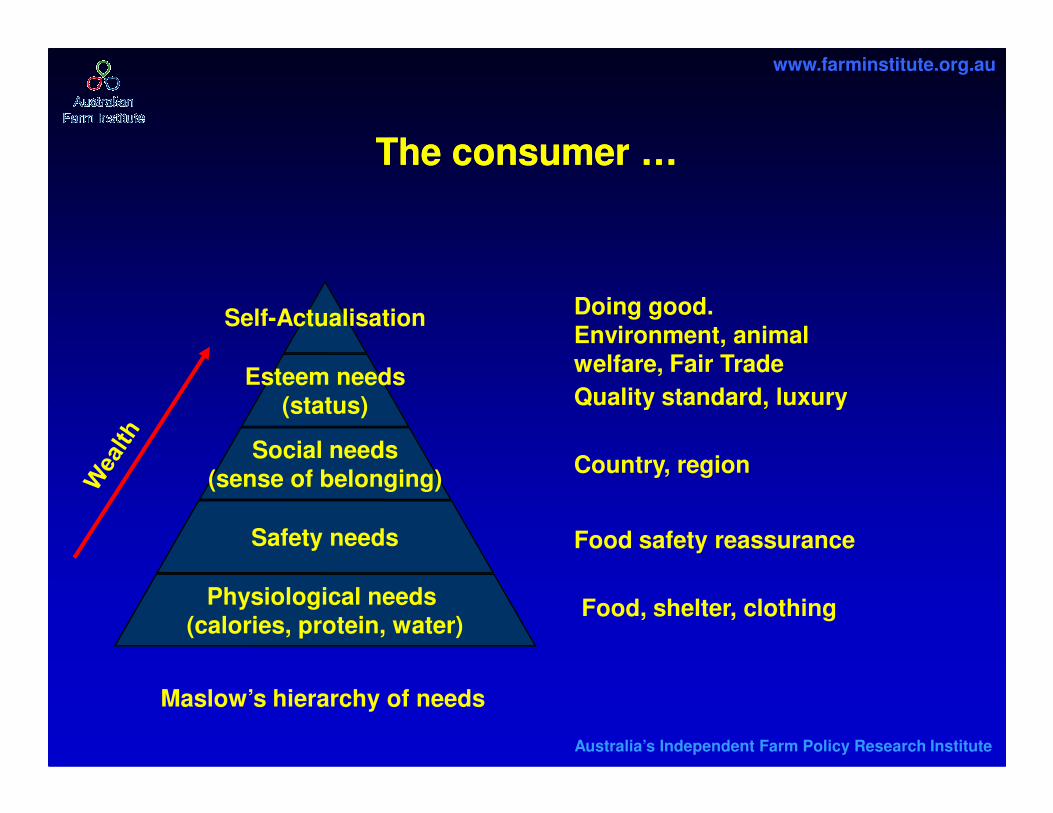

The consumer … The consumer …

Self-Actualisation

Esteem needs(status) Quality standard, luxury

Doing good. Environment, animal welfare, Fair Trade

Australia’s Independent Farm Policy Research Institute

(status)

Social needs(sense of belonging)

Safety needs

Physiological needs (calories, protein, water)

Food, shelter, clothing

Food safety reassurance

Country, region

Quality standard, luxury

Maslow’s hierarchy of needs

www.farminstitute.org.au

Like an egg?Like an egg?

Australia’s Independent Farm Policy Research Institute

www.farminstitute.org.au

Or how about some milk ?Or how about some milk ?

Australia’s Independent Farm Policy Research Institute

www.farminstitute.org.au

Some fish ?

Australia’s Independent Farm Policy Research Institute

www.farminstitute.org.au

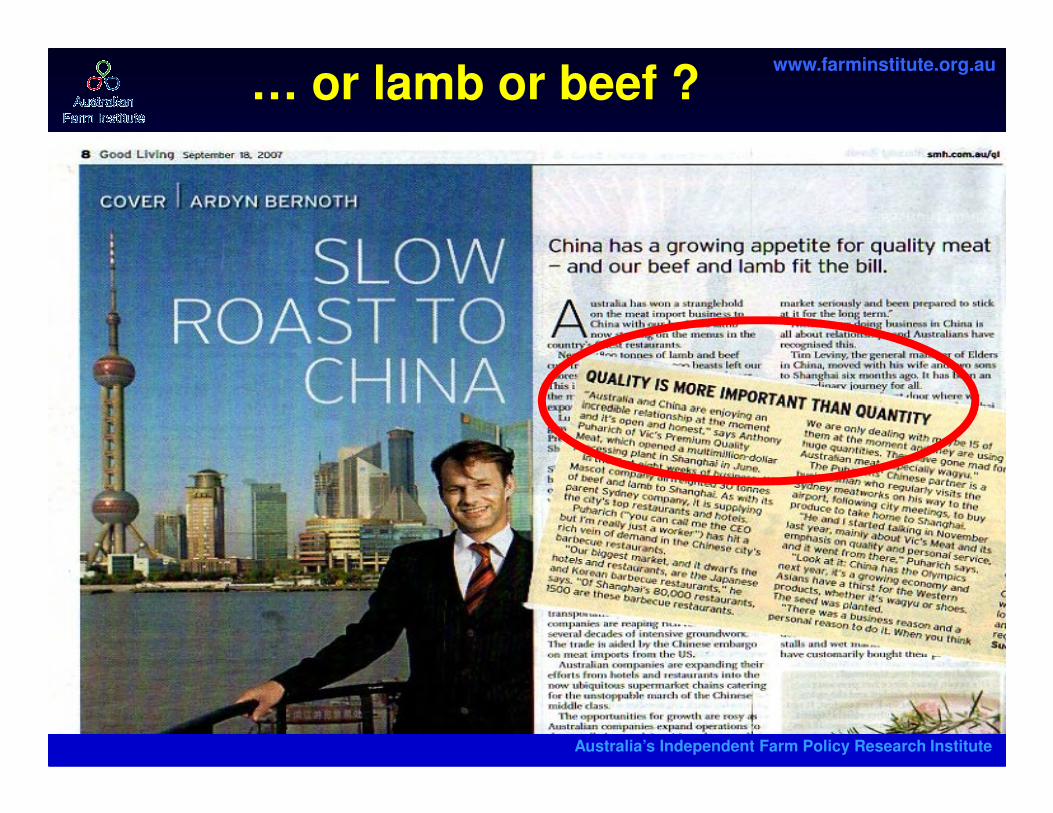

… or lamb or beef ?

Australia’s Independent Farm Policy Research Institute

www.farminstitute.org.au

Customer focus rather than production Customer focus rather than production focus ?focus ?

• No longer “the market” but many markets in which consumers are kings.

• The ‘brand’ – and associated supply chain - is

Australia’s Independent Farm Policy Research Institute

• The ‘brand’ – and associated supply chain - is everything (can be retailer brand).

• Productivity and efficiency are as important as they have ever been

• Market specialisation and ability to differentiate are becoming critical.

www.farminstitute.org.au

Australia’s Independent Farm Policy Research Institute