Embed Size (px)

Citation preview

11

Optimal Turnover and the Single Optimal Turnover and the Single Period Assumption in Portfolio Period Assumption in Portfolio OptimizationOptimization

Dan diBartolomeoDan diBartolomeoAsia Seminar Series Asia Seminar Series

November 2006 November 2006

22

This Presentation in OutlineThis Presentation in Outline

•• Review the main four sources of uncertainty in meanReview the main four sources of uncertainty in mean--variance optimizationvariance optimization

•• Consider how to encompass all sources of uncertainty by Consider how to encompass all sources of uncertainty by augmenting the objective functionaugmenting the objective function

•• Focus the discussion on a “structural” form of estimation Focus the discussion on a “structural” form of estimation error that has been relatively less explored in the error that has been relatively less explored in the literatureliterature–– the “single period” assumption built into the Markowitz meanthe “single period” assumption built into the Markowitz mean--

variance optimization processvariance optimization process•• Introduce a “rule of thumb” into traditional MVO to Introduce a “rule of thumb” into traditional MVO to

produce more efficient tradeoffs between riskproduce more efficient tradeoffs between risk--adjusted adjusted returns and transaction costsreturns and transaction costs

33

We Walk From Where We StandWe Walk From Where We Stand

•• Markowitz and Levy (1979) propose a function of mean Markowitz and Levy (1979) propose a function of mean variance as a representation of investor utilityvariance as a representation of investor utility

U = R U = R –– SS22/ T/ T

•• This is just risk adjusted return where the size of the risk This is just risk adjusted return where the size of the risk penalty can be scaled to fit the investor’s risk tolerancepenalty can be scaled to fit the investor’s risk tolerance

•• AssumptionsAssumptions–– The parameters of return distributions are known with certainty.The parameters of return distributions are known with certainty.

In the real world, we can get it wrong. In the real world, we can get it wrong.

–– The future is one long period in which our input parameters The future is one long period in which our input parameters values (that are both correct and certain) never change.values (that are both correct and certain) never change.

44

Four Sources of UncertaintyFour Sources of Uncertainty•• We assert there are four main sources of uncertainty in We assert there are four main sources of uncertainty in

an optimizationan optimization–– Market and security risks (the kind that risk models are meant tMarket and security risks (the kind that risk models are meant to o

deal with)deal with)–– Parameter estimation error in the return estimatesParameter estimation error in the return estimates–– Parameter estimation error in the risk estimatesParameter estimation error in the risk estimates–– The single period framework that is assumed for MVOThe single period framework that is assumed for MVO

•• If you consider that each of these effects can interact If you consider that each of these effects can interact with the otherswith the others–– you have a 4*4 matrix of sixteen thingsyou have a 4*4 matrix of sixteen things–– the matrix is symmetric about the diagonal so there are really the matrix is symmetric about the diagonal so there are really

ten terms we have to worry about, of which traditional ten terms we have to worry about, of which traditional optimization considers only oneoptimization considers only one

–– If you think trading costs are uncertain, now you have a 5 * 5 If you think trading costs are uncertain, now you have a 5 * 5 matrix with fifteen termsmatrix with fifteen terms

•• To my knowledge no one has tried dealing with all tenTo my knowledge no one has tried dealing with all ten

55

More Thoughts on Single PeriodMore Thoughts on Single Period

•• In the real world, things change and our parameter In the real world, things change and our parameter estimates for return and risk (even if initially exactly estimates for return and risk (even if initially exactly correct) are likely to change as well.correct) are likely to change as well.

•• If transaction costs are zero, we can simply adjust our If transaction costs are zero, we can simply adjust our portfolio composition to optimally reflect our new beliefs portfolio composition to optimally reflect our new beliefs whenever they change. whenever they change.

•• If transaction costs are not free, the single period If transaction costs are not free, the single period assumption is a serious problem.assumption is a serious problem.

•• If transaction costs are large (e.g. capital gain taxes), the If transaction costs are large (e.g. capital gain taxes), the single period assumption is wholly unrealistic. Tax single period assumption is wholly unrealistic. Tax authorities also seem to be interested in things like weeks, authorities also seem to be interested in things like weeks, months and especially “tax years.” months and especially “tax years.”

66

MultiMulti--period Optimizationperiod Optimization•• MossinMossin (1968) suggests an explicit multi(1968) suggests an explicit multi--period period

formulation for portfolio optimizationformulation for portfolio optimization

•• Cargill and Meyer (1987) focus on the risk side of the Cargill and Meyer (1987) focus on the risk side of the multimulti--period problemperiod problem

•• Merton (1990) introduces continuous time analog to Merton (1990) introduces continuous time analog to MVOMVO

•• PliskaPliska (1997) provides a discrete time analog to MVO(1997) provides a discrete time analog to MVO

•• Li and Ng (2000) provide a framework for multiLi and Ng (2000) provide a framework for multi--period period MVO using dynamic programmingMVO using dynamic programming

•• Sneddon (2005) provides a closed form solution to the Sneddon (2005) provides a closed form solution to the multimulti--period optimization period optimization including optimal turnover including optimal turnover

77

MultiMulti--period Optimization, cont’dperiod Optimization, cont’d

•• Parameter estimation error is the killer Parameter estimation error is the killer herehere–– In practice, investors have enough difficulty In practice, investors have enough difficulty

estimating risk and return parameters as of estimating risk and return parameters as of “now” “now”

–– For multiFor multi--period optimization we must period optimization we must estimate now what the parameters will be for estimate now what the parameters will be for all future periodsall future periods

88

Smart RebalancingSmart Rebalancing

•• Numerous “smart” rebalancing rules have been proposed Numerous “smart” rebalancing rules have been proposed to avoid trading costs when the expected improvement to avoid trading costs when the expected improvement is not significantis not significant

•• Rubenstein (1991) examines the efficiency of continuous Rubenstein (1991) examines the efficiency of continuous rebalancing and proposes a rule for avoiding spurious rebalancing and proposes a rule for avoiding spurious turnoverturnover

•• KronerKroner and Sultan (1993) propose a “hurdle” rule for and Sultan (1993) propose a “hurdle” rule for rebalancing currency hedges when return distributions rebalancing currency hedges when return distributions are time varyingare time varying

•• Engle, Engle, MezrichMezrich and Yu (1998) propose a hurdle on alpha and Yu (1998) propose a hurdle on alpha improvement as the trigger for rebalancingimprovement as the trigger for rebalancing

99

Even Smarter RebalancingEven Smarter Rebalancing

•• BeyBey, Burgess, Cook (1990) use bootstrap resampling to , Burgess, Cook (1990) use bootstrap resampling to identify “indifference” regions, along a fuzzy efficient identify “indifference” regions, along a fuzzy efficient frontierfrontier

•• Michaud (1998) uses resampling to measure the Michaud (1998) uses resampling to measure the confidence interval on portfolio return and risk to form a confidence interval on portfolio return and risk to form a “when to trade rule”. Elaborated upon in Michaud and “when to trade rule”. Elaborated upon in Michaud and Michaud (2002) and patented.Michaud (2002) and patented.

•• Markowitz and Van Markowitz and Van DijkDijk (2003) propose a rebalancing (2003) propose a rebalancing rule designed to approximate multirule designed to approximate multi--period optimization, period optimization, but argue it is mathematically intractable (at least in but argue it is mathematically intractable (at least in closed form)closed form)

1010

Single Period Model with CostsSingle Period Model with Costs•• GrinoldGrinold and and StuckelmanStuckelman (1993) consider a value (1993) consider a value

added/turnover efficient frontier. They derive that under added/turnover efficient frontier. They derive that under certain common assumptions, value added is certain common assumptions, value added is approximately a square root function of turnoverapproximately a square root function of turnover

•• Common practice is extend the objective function to Common practice is extend the objective function to include transaction costs (C) that are linearly amortized at include transaction costs (C) that are linearly amortized at an period rate (A) that reflects the expected economic life an period rate (A) that reflects the expected economic life of the benefits of the transactionof the benefits of the transaction

U = R U = R –– SS22/ T / T –– (C (C ×× A)A)

•• The expected average holding period for the positions The expected average holding period for the positions resulting from a transaction is just the reciprocal of the resulting from a transaction is just the reciprocal of the expected oneexpected one--way turnoverway turnover

1111

Geometric Versus Linear TradeoffsGeometric Versus Linear Tradeoffs

•• For small transaction costs, arithmetic amortization is For small transaction costs, arithmetic amortization is sufficient, but if costs are large we need to consider sufficient, but if costs are large we need to consider compoundingcompounding

•• Assume a trade with 20% trading cost and an Assume a trade with 20% trading cost and an expected holding period of one year. expected holding period of one year. –– We can get an expected alpha improvement of 20%. But if We can get an expected alpha improvement of 20%. But if

we give up 20% of our money now, and invest at 20%, we we give up 20% of our money now, and invest at 20%, we only end up with 96% of the money we have now.only end up with 96% of the money we have now.

•• Solution is to adjust the amortization rate to reflect Solution is to adjust the amortization rate to reflect the correct geometric ratethe correct geometric rate

1212

Lets Define The Probability of Lets Define The Probability of RealizationRealization

•• We define the probability of realization, P, like a oneWe define the probability of realization, P, like a one--tailed T testtailed T test

P = P = N N ((((((UUoo--UUii) / ) / TETEioio) * (1/* (1/ A)A).5.5))

•• NN(x(x) is the cumulative normal function:) is the cumulative normal function:2 / 21

( )2

uxN x e du

π

−

−∞= ∫

1313

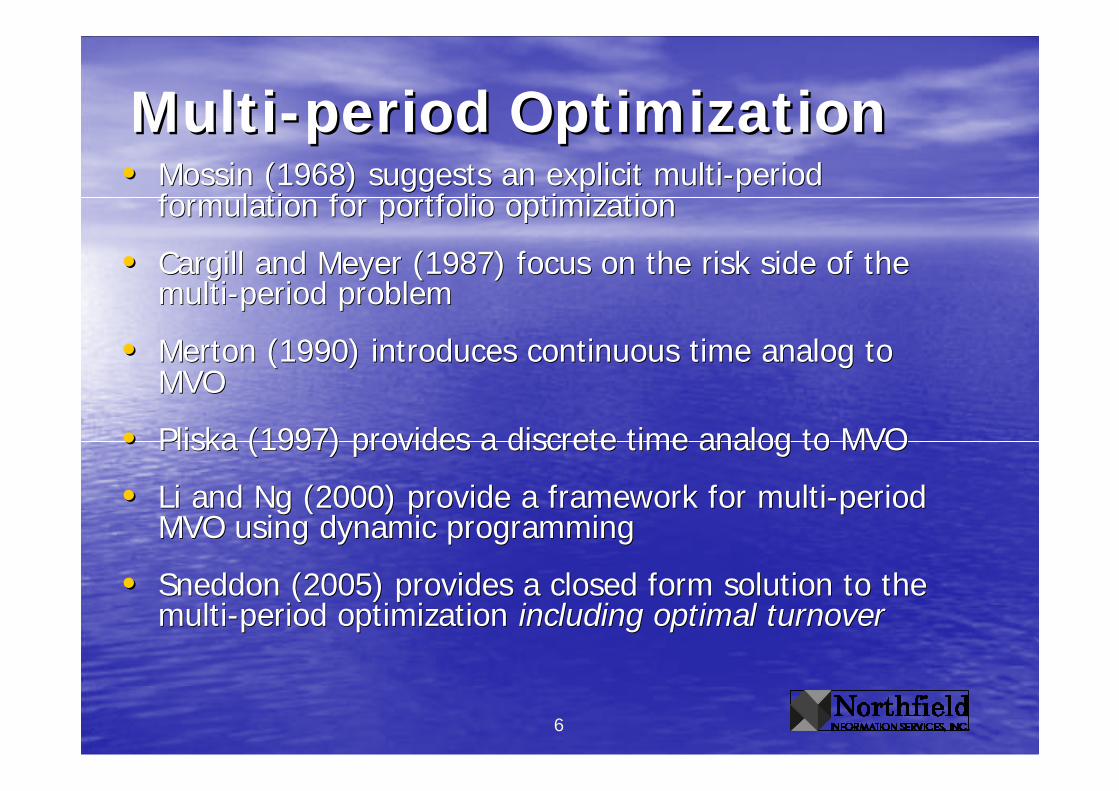

The Realization ProbabilityThe Realization Probability

•• The numerator is the improvement in risk adjusted The numerator is the improvement in risk adjusted return between the optimal and initial portfoliosreturn between the optimal and initial portfolios

•• The denominator is the tracking error between the The denominator is the tracking error between the optimal and initial portfolios. Essentially it’s the standard optimal and initial portfolios. Essentially it’s the standard error on the expected improvement in utilityerror on the expected improvement in utility–– If there is no tracking error between the initial and If there is no tracking error between the initial and

optimal portfolios, P approaches 100%. Consider optimal portfolios, P approaches 100%. Consider “optimizing a portfolio” by getting the manager to cut “optimizing a portfolio” by getting the manager to cut fees. The improvement in utility is certain no matter fees. The improvement in utility is certain no matter how short the time horizon.how short the time horizon.

–– Not something to which we usually pay attentionNot something to which we usually pay attention•• If turnover is very low, A will approach zero, so P will If turnover is very low, A will approach zero, so P will

approach 100%. For long time horizons, we have the approach 100%. For long time horizons, we have the classical case that assumes certaintyclassical case that assumes certainty

1414

Some Possible Uses for Some Possible Uses for “Probability of Realization”“Probability of Realization”•• Create an indifference trading rule Create an indifference trading rule

–– Optimize but don’t trade at all if P is less than some thresholdOptimize but don’t trade at all if P is less than some thresholdvalue that you consider statistically significantvalue that you consider statistically significant

•• Create a “hurdle” trading ruleCreate a “hurdle” trading rule–– Optimize but don’t trade at all if the probability of realizatioOptimize but don’t trade at all if the probability of realization n

weighted valueweighted value--added (P * valueadded (P * value--added) is less than some added) is less than some threshold valuethreshold value

•• Pick your spot on the “turnover/valuePick your spot on the “turnover/value--added frontieradded frontier–– Such that P is maximizedSuch that P is maximized–– Such that probability of realization weighted valueSuch that probability of realization weighted value--added (P * added (P *

valuevalue--added) is maximizedadded) is maximized•• Use P to adjust the amortization rate so your Use P to adjust the amortization rate so your

optimization gets closer to the optimal amount of optimization gets closer to the optimal amount of turnoverturnover

1515

Empirical ExampleEmpirical Example

•• Initial Portfolio 85 Large StocksInitial Portfolio 85 Large Stocks•• S&P 500 BenchmarkS&P 500 Benchmark•• Random ZRandom Z--scores as alphasscores as alphas•• Risk Tolerance = 40Risk Tolerance = 40•• Expected Turnover 25% per annumExpected Turnover 25% per annum•• No position bigger than 3%No position bigger than 3%•• No position smaller than .25%No position smaller than .25%•• 20 cents per share trading costs20 cents per share trading costs

1616

Probability of RealizationProbability of Realization

Probability of Realization

0

0.2

0.4

0.6

0.8

1

1.2

0 50 100 150 200

2 Way Turnover

Pro

bab

ility

1717

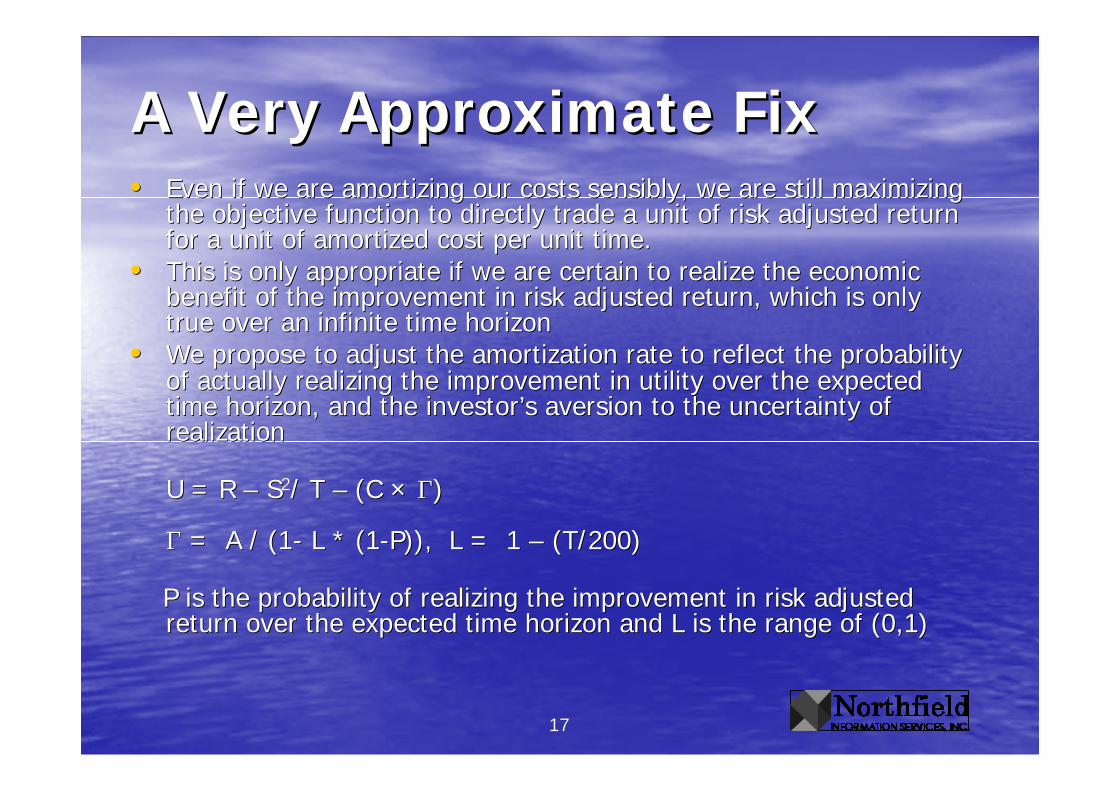

A Very Approximate FixA Very Approximate Fix•• Even if we are amortizing our costs sensibly, we are still maximEven if we are amortizing our costs sensibly, we are still maximizing izing

the objective function to directly trade a unit of risk adjustedthe objective function to directly trade a unit of risk adjusted return return for a unit of amortized cost per unit time.for a unit of amortized cost per unit time.

•• This is only appropriate if we are certain to realize the economThis is only appropriate if we are certain to realize the economic ic benefit of the improvement in risk adjusted return, which is onlbenefit of the improvement in risk adjusted return, which is only y true over an infinite time horizontrue over an infinite time horizon

•• We propose to adjust the amortization rate to reflect the probabWe propose to adjust the amortization rate to reflect the probability ility of actually realizing the improvement in utility over the expectof actually realizing the improvement in utility over the expected ed time horizon, and the investor’s aversion to the uncertainty of time horizon, and the investor’s aversion to the uncertainty of realizationrealization

U = R U = R –– SS22/ T / T –– (C (C ×× ΓΓ))

ΓΓ = A / (1= A / (1-- L * (1L * (1--P)), L = 1 P)), L = 1 –– (T/200)(T/200)

P is the probability of realizing the improvement in risk adP is the probability of realizing the improvement in risk adjusted justed return over the expected time horizon and L is the range of (0,1return over the expected time horizon and L is the range of (0,1))

1818

One Last IdeaOne Last Idea

•• Another approach would be to add the uncertainty of Another approach would be to add the uncertainty of realization to the objective functionrealization to the objective function

U = R U = R –– SSbb22/ T/ Tbb –– (C (C ×× AA) ) –– (A * TE(A * TEIOIO

2 2 // TTIOIO))

•• Wang (1999) provides an analytical solution Wang (1999) provides an analytical solution

1919

ConclusionsConclusions

•• The single period assumption in MVO implies that The single period assumption in MVO implies that trading costs and improvements in utility can be traded trading costs and improvements in utility can be traded as if both are certainas if both are certain

•• In addition to other sources of estimation error, finite In addition to other sources of estimation error, finite holding periods imply that the improvement in utility is holding periods imply that the improvement in utility is uncertainuncertain

•• We must therefore consider the probability of realizing We must therefore consider the probability of realizing an improvement in utility arising from an optimization as an improvement in utility arising from an optimization as being between 50% and 100%being between 50% and 100%

•• The tracking error between the initial portfolio and the The tracking error between the initial portfolio and the optimal portfolio is an approximation of the standard optimal portfolio is an approximation of the standard error of the increase in utility, so probability of error of the increase in utility, so probability of realization can be computed. realization can be computed.

2020

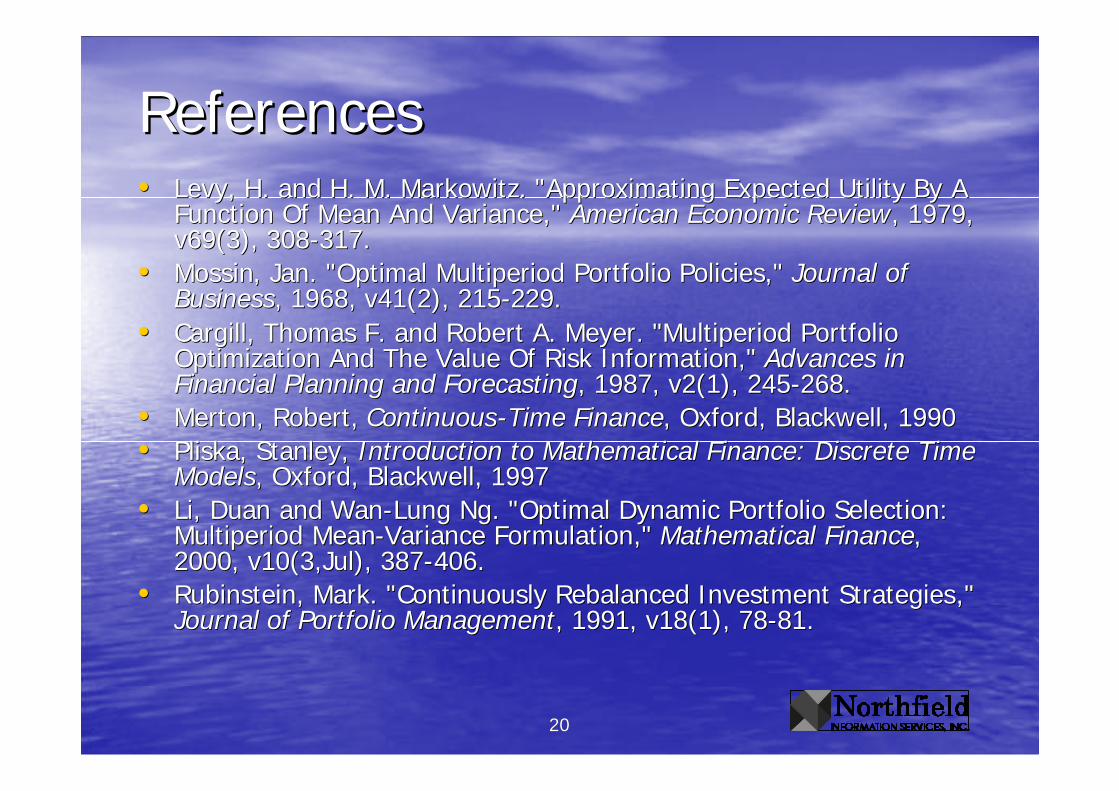

ReferencesReferences•• Levy, H. and H. M. Markowitz. "Approximating Expected Utility ByLevy, H. and H. M. Markowitz. "Approximating Expected Utility By A A

Function Of Mean And Variance," Function Of Mean And Variance," American Economic ReviewAmerican Economic Review, 1979, , 1979, v69(3), 308v69(3), 308--317.317.

•• MossinMossin, Jan. "Optimal , Jan. "Optimal MultiperiodMultiperiod Portfolio Policies," Portfolio Policies," Journal of Journal of BusinessBusiness, 1968, v41(2), 215, 1968, v41(2), 215--229.229.

•• Cargill, Thomas F. and Robert A. Meyer. "Cargill, Thomas F. and Robert A. Meyer. "MultiperiodMultiperiod Portfolio Portfolio Optimization And The Value Of Risk Information," Optimization And The Value Of Risk Information," Advances in Advances in Financial Planning and ForecastingFinancial Planning and Forecasting, 1987, v2(1), 245, 1987, v2(1), 245--268.268.

•• Merton, Robert, Merton, Robert, ContinuousContinuous--Time FinanceTime Finance, Oxford, Blackwell, 1990, Oxford, Blackwell, 1990•• PliskaPliska, Stanley, , Stanley, Introduction to Mathematical Finance: Discrete Time Introduction to Mathematical Finance: Discrete Time

ModelsModels, Oxford, Blackwell, 1997, Oxford, Blackwell, 1997•• Li, Li, DuanDuan and Wanand Wan--Lung Ng. "Optimal Dynamic Portfolio Selection: Lung Ng. "Optimal Dynamic Portfolio Selection:

MultiperiodMultiperiod MeanMean--Variance Formulation," Variance Formulation," Mathematical FinanceMathematical Finance, , 2000, v10(3,Jul), 3872000, v10(3,Jul), 387--406. 406.

•• Rubinstein, Mark. "Continuously Rebalanced Investment StrategiesRubinstein, Mark. "Continuously Rebalanced Investment Strategies," ," Journal of Portfolio ManagementJournal of Portfolio Management, 1991, v18(1), 78, 1991, v18(1), 78--81.81.

2121

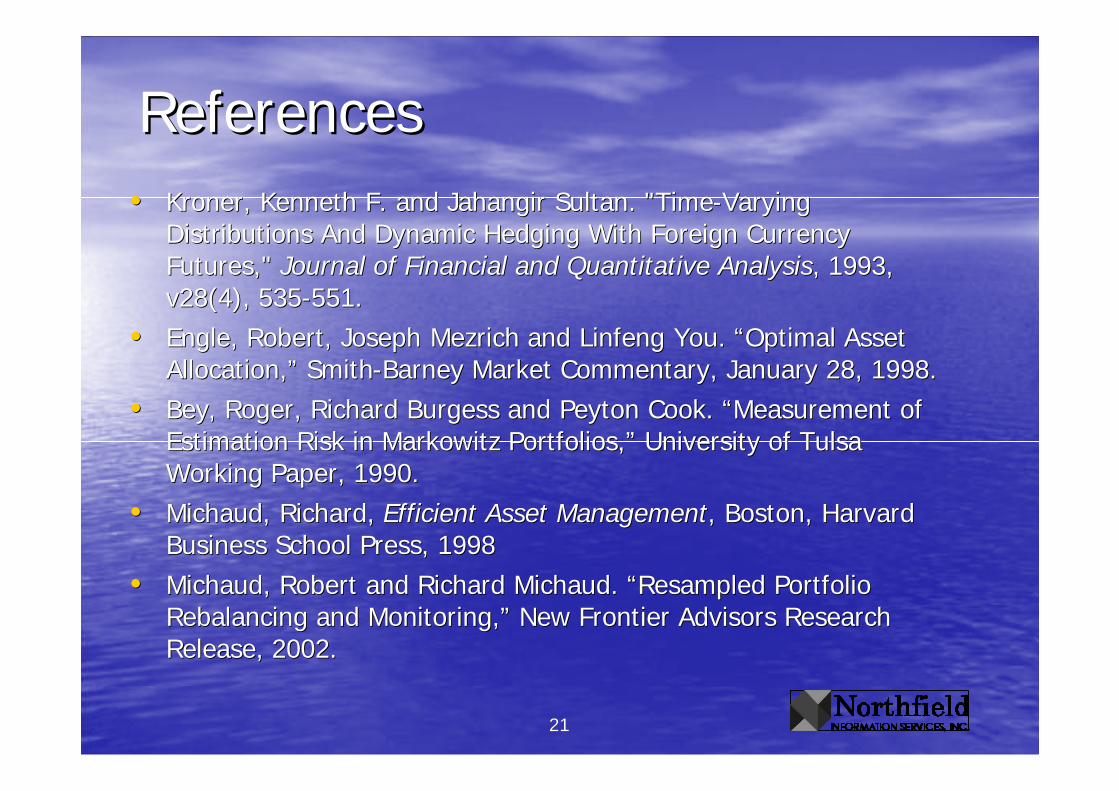

ReferencesReferences•• KronerKroner, Kenneth F. and , Kenneth F. and JahangirJahangir Sultan. "TimeSultan. "Time--Varying Varying

Distributions And Dynamic Hedging With Foreign Currency Distributions And Dynamic Hedging With Foreign Currency Futures," Futures," Journal of Financial and Quantitative AnalysisJournal of Financial and Quantitative Analysis, 1993, , 1993, v28(4), 535v28(4), 535--551. 551.

•• Engle, Robert, Joseph Engle, Robert, Joseph MezrichMezrich and and LinfengLinfeng You. “Optimal Asset You. “Optimal Asset Allocation,” SmithAllocation,” Smith--Barney Market Commentary, January 28, 1998. Barney Market Commentary, January 28, 1998.

•• BeyBey, Roger, Richard Burgess and Peyton Cook. “Measurement of , Roger, Richard Burgess and Peyton Cook. “Measurement of Estimation Risk in Markowitz Portfolios,” University of Tulsa Estimation Risk in Markowitz Portfolios,” University of Tulsa Working Paper, 1990. Working Paper, 1990.

•• Michaud, Richard, Michaud, Richard, Efficient Asset ManagementEfficient Asset Management, Boston, Harvard , Boston, Harvard Business School Press, 1998Business School Press, 1998

•• Michaud, Robert and Richard Michaud. “Resampled Portfolio Michaud, Robert and Richard Michaud. “Resampled Portfolio Rebalancing and Monitoring,” New Frontier Advisors Research Rebalancing and Monitoring,” New Frontier Advisors Research Release, 2002. Release, 2002.

2222

ReferencesReferences•• GrinoldGrinold, Richard C. and Mark , Richard C. and Mark StuckelmanStuckelman. "The Value. "The Value--

Added/Turnover Frontier," Added/Turnover Frontier," Journal of Portfolio ManagementJournal of Portfolio Management, 1993, , 1993, v19(4), 8v19(4), 8--17.17.

•• Sneddon, Leigh. “The Dynamics of Active Portfolios”, Sneddon, Leigh. “The Dynamics of Active Portfolios”, Proceedings of Proceedings of the Northfield Research Conference 2005the Northfield Research Conference 2005, , http://www.northinfo.com/documents/180.pdfhttp://www.northinfo.com/documents/180.pdf

•• Wang, Ming Yee. "MultipleWang, Ming Yee. "Multiple--Benchmark And MultipleBenchmark And Multiple--Portfolio Portfolio Optimization," Optimization," Financial Analyst JournalFinancial Analyst Journal, 1999, v55(1,Jan/Feb), 63, 1999, v55(1,Jan/Feb), 63--72.72.

•• IdzorekIdzorek, Thomas. “A Step, Thomas. “A Step--byby--Step Guide to the BlackStep Guide to the Black--LittermanLittermanModel”, Model”, Zephyr Associates Working PaperZephyr Associates Working Paper, 2003., 2003.

•• Ceria, S. and Robert Stubbs. “Incorporating Estimation Error in Ceria, S. and Robert Stubbs. “Incorporating Estimation Error in Portfolio Optimization: Robust Efficient Frontiers”, Portfolio Optimization: Robust Efficient Frontiers”, AxiomaAxioma Inc. Inc. Working Paper,Working Paper, 2004.2004.

2323

ReferencesReferences

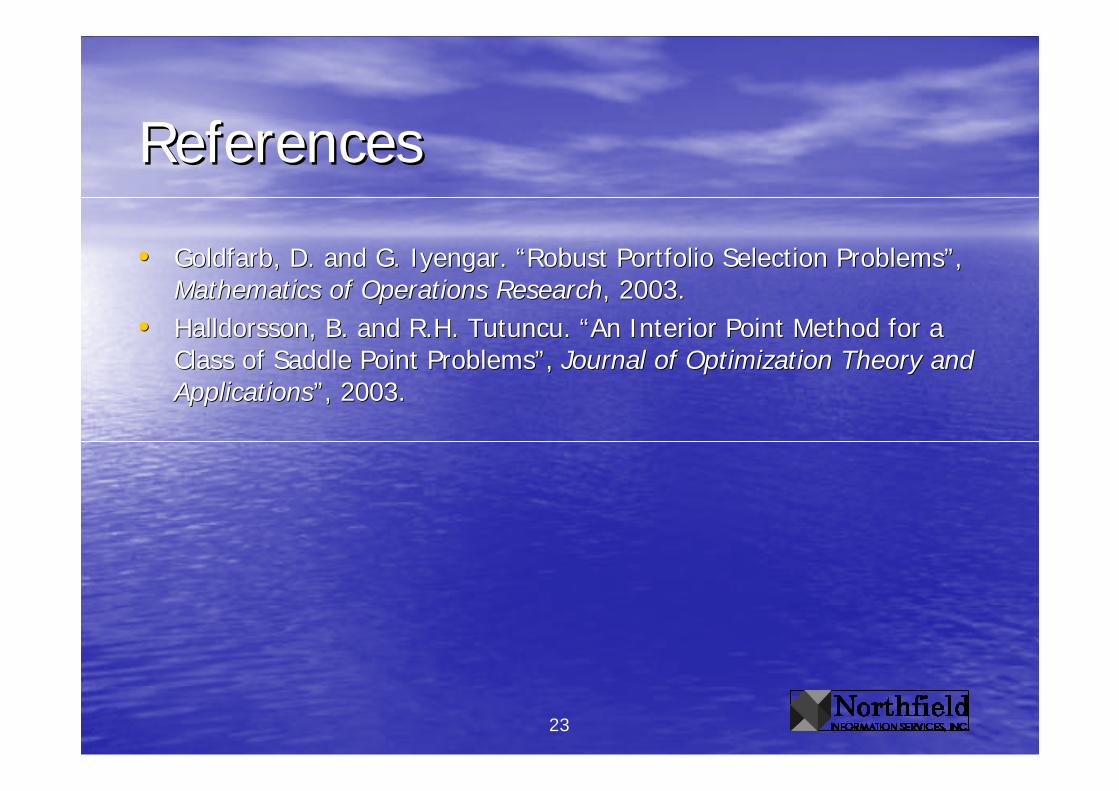

•• Goldfarb, D. and G. Goldfarb, D. and G. IyengarIyengar. “Robust Portfolio Selection Problems”, . “Robust Portfolio Selection Problems”, Mathematics of Operations ResearchMathematics of Operations Research, 2003. , 2003.

•• HalldorssonHalldorsson, B. and R.H. , B. and R.H. TutuncuTutuncu. “An Interior Point Method for a . “An Interior Point Method for a Class of Saddle Point Problems”, Class of Saddle Point Problems”, Journal of Optimization Theory and Journal of Optimization Theory and ApplicationsApplications”, 2003. ”, 2003.