Embed Size (px)

Citation preview

FISCAL POLICY INSTITUTE

PROJECT REPORT

Optimization Model for Food

Grain Distribution and

Movement Planning in

Karnataka

Submitted as part of Summer Internship

By

Varun Chhabra

Indian Institute of Management, Lucknow-226013

June 2011

i

Letter of Transmittal

6th

June 1, 2011

Shri P. R. Devi Prasad,

Director,

Fiscal Policy Institute,

Finance Department,

Government of Karnataka,

Bangalore.

Dear Sir,

I am pleased to submit the project report titled ‘Optimization Model for Food Grain

Distribution and Movement Planning in Karnataka’. I hereby declare that this is an original

work done by me and the findings of this work have not been previously submitted for any

publication.

Please feel free to revert to me with any questions and/or comments regarding this report.

Sincerely

(Varun Chhabra)

Summer Intern,

Indian Institute of Management,

Lucknow

Enclosure: Project Report

ii

Certificate

This is to certify that the project report titled ‘Optimization Model for Food Grain

Distribution and Movement Planning in Karnataka’ submitted by Shri Varun Chhabra as

part of Summer Internship is the result of the work done by him at Fiscal Policy Institute,

Bangalore, Finance Department, Government of Karnataka, from April to June 2010 under

our guidance.

Place: Bangalore

Date: 01/05/2011

Shri P.R. Devi Prasad IES

Director,

Fiscal Policy Institute,

Finance Department,

Government of Karnataka

Place: Bangalore

Date: 01/05/2011

Shri Shivakumar Y.C.

Deputy Director (Admn.)

Fiscal Policy Institute,

Finance Department,

Government of Karnataka

iii

Acknowledgements

I am deeply indebted to Shri P.R. Devi Prasad, Director, Fiscal Policy Institute, Bangalore,

under whose guidance the present study was conducted. He has been giving valuable

suggestions, generous help and corrections during all the phases of the project, without which

the efforts could not have been completed successfully.

I would like to extend my indebtedness and gratitude to my guide Shri Shivakumar Y.C.

Deputy Director (Administration), FPI for the invaluable guidance and feedback provided by

him at every stage of the project.

I am indebted to Shri Srinivas Kumar Advisor, FPI, Smt. Anita V Nazare, Smt. Margaret

Abraham, Smt. Nelleri Umeshwari, all Special Officers at FPI, Shri Balasubramanyam H.S

Special Officer, FPA and Shri Anilkumar M. Special Officer, FDA for their guidance and

support from time to time.

I would like to extend my gratefulness to Shri Mandar Nayak Consultant, ERC and Kum.

Munawwara Shakila Consultant, FPI for their guidance and invaluable inputs during all the

phases of the project.

I am indebted to Shri B.A. Harish Gowda Secretary, FCS&CA , Shri S Narasimaiah

Additional Secretary, FCS & CA for their guidance and invaluable help in getting

information from FCS & CA Department.

I am indebted to the following officials for their guidance and invaluable help in getting

responses.

1. Shri M.C. Gangadhara, Additional Director & Deputy Director (PDS), FCS & CA

2. Smt T.R Shobha, ex-Chief Accounts Officer & HQA, FCS & CA

3. Shri Shivana Gowda, Chief Accounts Officer, FCS & CA

4. Shri Azizuddin Hafiz, Deputy Director (FCS & CA) & CIO (Akshaya Kosha), FCS &

CA

5. Shri M. Muralidhar, Financial Adviser to Transport Commissioner

6. Koshy Eipe, General Manager, Finance IOCL

7. Mr. A.P. Verma Senior Manager, BPCL, Retail sales

8. Elumalai Kannan, ADRTC, ISEC, Bangalore

I am deeply thankful to my fellow interns Shri Abhilash Kumar and Shri Santosh Kamble for

their enormous support, guidance and help at every juncture through exchange of ideas and

views on the study.

iv

I am thankful to Officers and Staff at FPI and FPAC who have shown tremendous

cooperation and support throughout the course of study. I am thankful to Kiran, Nagaraj,

Namitha and Sangeeta for helping me with the translation of crucial documents.

I am also thankful to Officers, Case Workers and Staff in the Transport Division of FCS &

CA especially Arun, Naveen, Ervin D’Souza, Radha and Sudha for valuable inputs and

support at every stage of the project.

I would also like to thank Shri B K Bhattacharya ex-IAS, Chairman, Expenditure Reforms

Commission, Government of Karnataka for his support and encouragement.

I would also like to thank Government of Karnataka for giving me an opportunity to work on

this project at FPI.

I would also like to thank all the respondents for giving their time and invaluable responses

for this study.

The author alone is responsible for any errors and omissions.

Varun Chhabra,

Summer Intern,

Indian Institute of Management,

Lucknow

v

Table of Contents

Letter of Transmittal ................................................................................................................................ i

Certificate ................................................................................................................................................ ii

Acknowledgements ................................................................................................................................ iii

Table of Contents .................................................................................................................................... v

List of Figures ....................................................................................................................................... vii

List of Tables ....................................................................................................................................... viii

Abbreviations ......................................................................................................................................... ix

Abstract ................................................................................................................................................... x

1. Introduction ..................................................................................................................................... 1

1.1 Problem Statement ........................................................................................................................ 1

1.2 Objectives of the Study ................................................................................................................. 1

1.3 Significance of the Study .............................................................................................................. 2

1.4 Research Design ............................................................................................................................ 2

1.4.1 Exploratory Research ............................................................................................................. 2

1.5 Tools of the Study ......................................................................................................................... 2

1.6 Research Elements ........................................................................................................................ 3

1.7 Limitations of the Study ................................................................................................................ 4

2. PDS in Karnataka ............................................................................................................................ 5

2.1 Food, Civil Supplies and Consumer Affairs Department ............................................................. 5

2.2 Administrative Set Up ................................................................................................................... 5

2.3 Targeted Public Distribution System ............................................................................................ 6

2.4 Details of shops and cards ............................................................................................................. 8

2.5 Costing Sheet for Prices and Margin .......................................................................................... 10

2.6 Panchtantra .................................................................................................................................. 11

3. Analysis of Distribution System ................................................................................................... 12

3.1 Procurement Concerns ................................................................................................................ 12

3.2 Transportation & Distribution of PDS commodities .................................................................. 13

3.2.1 Tender Process (Transport Note, 2009) ............................................................................... 13

3.2.2 Tender Systems .................................................................................................................... 15

3.3 Direct Sourcing ........................................................................................................................... 17

3.3.1 Costing Sheet for Transportation charges ............................................................................ 17

3.3.2 Application of the Costing Sheet ......................................................................................... 20

vi

3.3.3 Handling Charges ................................................................................................................. 22

4. Conclusions ................................................................................................................................... 25

5. Recommendations ......................................................................................................................... 27

6. Scope for Further Research ........................................................................................................... 29

7. Bibliography ................................................................................................................................. 30

8. Annexure ....................................................................................................................................... 31

8.1 Annexure 1: List of Questions asked during interviews ............................................................. 31

8.2 Annexure 2: Copy of an APL Ration Card ................................................................................. 34

8.3 Annexure 3: Transport Rate Prevalent in Different Districts of Karnataka in 2004-05 .............. 35

8.4 Annexure 4: Tender Advertisement in English ........................................................................... 37

8.5 Annexure 5: Government Order (dated 11.04.2011) for fixing of Transport and Handling

Charges ............................................................................................................................................. 38

8.6 Annexure 6: Accounting to calculate Benchmark Rates ............................................................. 39

8.6.1 Indian Oil Tender Schedule iii for Changes in Different rates ............................................ 41

8.7 Annexure 7: Copy of Goods Carriage Permit showing Actual Load Capacity .......................... 42

8.8 Annexure 8: Motor Vehicle Taxation Schedules ........................................................................ 43

8.9 Annexure 9: Tender Notification (FCI to Wholesale) Dated 18-08-09 ...................................... 44

8.10 Annexure 10: Tender Notification (Wholesale to FPD Transportation) – Points of Difference

.......................................................................................................................................................... 53

8.10.1 Technical Conditions: ........................................................................................................ 53

8.10.2 Commercial Conditions: .................................................................................................... 53

8.11 Annexure 11: Wholesale Average Distance, Benchmark Rate over the years and Agreed Rate

for 2008-09........................................................................................................................................ 54

8.12 Annexure 12: Rural Transportation Average Distance, Bench Mark Rates and Agreed Rate for

the year 2008-09 ............................................................................................................................... 55

vii

List of Figures Figure 1: District wise plot of Average number of cards per FPD and average number of FPD per

wholesale nominee .................................................................................................................................. 9

Figure 2: Year wise trend of Food Subsidy in Karnataka ..................................................................... 10

Figure 3: Flow of PDS commodities to beneficiaries ........................................................................... 12

Figure 4: Different between Bench Mark rates and Agreed Rates ....................................................... 14

Figure 5: Fair Price Shops operating with less than the prescribed number of ration cards ................. 21

Figure 6: Route Map prior to Direct Sourcing (Circular, Left Image) and post Direct Sourcing (Hub

and Spoke, Right Image) ....................................................................................................................... 23

Figure 7: Percentage increase of agreed rate over bench mark rates for 2008-09 ................................ 25

viii

List of Tables Table 1: Roles and Responsibilities of various officials ......................................................................... 6

Table 2: Category wise monthly allocation and price details ................................................................. 7

Table 3: District wise standing of FPD, Wholesale Depots, Total Cards, Average No. of Cards per

FPD and Average number of FPDs per wholesale nominees ................................................................. 9

Table 4: Costing Sheet (for 1 quintal of grains) for different category of cards ................................... 10

Table 5: Bench Mark Rates prevalent in slab rate system .................................................................... 16

Table 6: Costing Sheet for Transportation charges ............................................................................... 17

Table 7: Computation of Total Demand of Wheat, Rice and Sugar .................................................... 20

Table 8: Computation of total margin on Rice, Wheat and Sugar by Retailer ..................................... 21

Table 9: Long term rates as quoted by transporters .............................................................................. 22

Table 10: Impact Assessment of Direct sourcing Vs Slab Rate System ............................................... 26

ix

Abbreviations

APL Above Poverty Line

AAY Antyodaya Anna Yojana

BPL Below Poverty Line

CAS – 5 Cost Accounting Standard – 5

CCI Central warehouse Corporation of India

CIP Common Issue Price

DCP Decentralized Procurement Programme

EAC Economic Advisory Committee

EBPL Extra Below Poverty Line

FCI Food Corporation of India

FPAC Fiscal Policy Analysis Cell

FPD Fair Price Depot

FPI Fiscal Policy Institute

FPS Fair Price Shop

FI Food Inspector

FSC Food Security Committee

FC&CA Food, Civil Supplies and Consumer Affairs

GOI Government of India

GP Gram Panchayat

ICWAI Institute of Cost and Work Accountants

IRA Informal Rationing Area

JIT Just In Time

KFCSC Karnataka Food and Civil Supplies Corporation

MSP Minimum Support Price

NAC National Advisory Council

PAC Public Accounts Committee

PDS Public Distribution System

RDS Ration Distribution System

TAPCMS Taluk Agriculture Produce and Co-operative Marketing Society

TP Taluk Panchayat

TPDS Targeted Public Distribution System

ZP Zilla Panchayat

x

Abstract

The report begins with description of the concerns faced by the Food, Civil Supplies and

Consumer Affairs Department in relation to the Public Distribution System. The objectives

have been to do an exploration research which can help us gain useful insights into the

Department in general and transportation system for distribution in particular. These insights

can be set as the basis for designing an Optimized Model for Food Grain Distribution and

Movement Planning in Karnataka. The scope of this study has been limited to the micro-level

cost analysis of present and earlier systems; their understanding can help us set realistic and

just bench mark rates. The rates along with distance and time constraints are the useful

parameters for designing a Transport Model.

In the Chapter 2 of the report, we have done a macro level analysis of the Public Distribution

System in Karnataka. Here we have tried to understand the roles and responsibilities of

various officials in the Department in relation to procurement and distribution. Thereafter, we

have done an analysis on the distribution of Fair Price Shops, Wholesale Depots and card

holders in the system. This analysis is the followed by pricing analysis of essential

commodities in the system and a discussion on the implications of the recent contemplated

changes at the Central Level.

The next chapter highlights the micro-level analysis of the transportation system prevalent in

the distribution of the commodities. We have tried to have a look at some of the concerns

relating to procurement and distribution of food-grains. This is followed by an analysis on the

tender process and related systems. Thereafter, we have done the cost-analysis on the

transportation and the handling charges of Direct Sourcing. Then we had a look at the

strategic implications of the current system in terms of ensuring a lean transportation system.

We also conducted an analysis on the current system in terms of time efficiency and derived

value.

In the chapter of conclusions, we stated the findings of the study and did an impact analysis

of the current system for six months tenure. Then, we have stated some of the

recommendations that can help us mitigate the irrelevant cost expenditure in the system along

with the formation of a robust distribution system in the future.

Further research areas have also been highlighted in light of the recent study.

1

1. Introduction

Public Distribution System (PDS) programme in India has been introduced for achieving

multiple objectives. Its primary objective is to provide subsidized food grains and other items

of daily necessity such as oil, sugar and Kerosene etc. to weaker sections of the population

The programme also aims to stabilize market prices of food grains in times of unusual

inflationary tendencies, to provide food security to areas suffering from drought and similar

natural calamities and manmade disasters, to provide support prices to farmers and to

maintain buffer stock. The PDS programme is implemented in welfare state mode with

universal beneficiary approach and hence it has been under criticism for being non-specific

and wasteful. It has also been found to be an inadequate programme to fully address the food

security problem of the poor and vulnerable. PDS is a centrally planned programme and each

state in India implements the design set by the Central Government.

In Karnataka, the PDS is implemented by the Department of Food, Civil Supplies and

Consumer Affairs. The recent performance audit revealed that Karnataka was the first State

in the country to launch computerization of ration cards for creating a data base of

beneficiaries of PDS by capturing digital photographs and bio-metrics of the family

members. However, the system is fraught with its problems, concerns and inefficiencies.

1.1 Problem Statement

The current study has its focus on the distribution of the food grains and optimization of

various parameters which can help us derive value from the system. The distribution chain

here consists of lifting, transportation and delivery of various essential commodities1 under

the PDS. Some of the key factors that need to be considered are given below:

How are card holders, Fair Price Depots and wholesale nominees distributed across

the state?

What could be possible reasons for existing of different bench mark rates across

different districts of the state?

Whether or not the present system is Time and Cost Efficient?

What is the value generation by the present system?

Whether or not the present system strategically important?

Whether or not the measures taken to reach the targeted public segment are effective?

1.2 Objectives of the Study

The purpose of the study is given below:

1 ‘Essential Commodities’ means essential commodities as defined under the Essential Commodities

Act 1955, and meant for Public Distribution System by the State or Central Government or any other

authority authorized in that behalf by such Government .

2

To do analysis of the distribution of Fair Price Depots and Wholesale Depots across

different districts of the State

To do analysis of the distribution of cardholders across different Fair Price Depots

A look into the Tender Process, its system for fixing bench mark & agreed rates and

problems faced therein

Cost analysis of various systems in order to understand the fixation and changing of

bench mark rates

Understanding changes in various models of Transportation (like Circular Route Map

and Hub and Spoke Route map) and its cost implications on the system

Macro-level Analysis of the Retailer’s Margin and impact assessment of introducing

new system

1.3 Significance of the Study

This study gives a macro-level understanding of the PDS in Karnataka. It also gives micro-

level analysis of transportation and loading/unloading system present in the distribution

chain. The analysis of cost criteria for establishing bench mark rates in various tender

systems and costing sheet of direct sourcing can prove to be very effective in developing an

Optimized Transport Model for food grain distribution and movement planning.

1.4 Research Design

The following research techniques were used in this study.

1.4.1 Exploratory Research

Exploratory research has the goal of formulating problems more precisely, clarifying

concepts, gathering explanations, gaining insight, eliminating impractical ideas, and forming

hypotheses. It provides insights into and comprehension of an issue or situation2.The initial

phase of the project demanded an exploratory research to capture the knowledge and

understanding of the PDS in Karnataka. Thereafter, we moved into a combination of both the

formal in-depth interviews with higher officials and informal discussions with concerned case

workers. Interactions with focused groups and analysis of primary data collected through

field work helped in gaining of crucial insights.

1.5 Tools of the Study

Interviews were conducted to collect data from top officials. The interviews were mainly

unstructured3 where questions had been changed or adapted to meet the respondent's intelligence,

understanding or belief. These set of questions are hence open-ended unlike a structured interview

where a pre-set range of answers for a respondent to choose, but instead we advocated listening to

how each individual person is responding to the question.

2http://en.wikipedia.org/wiki/Exploratory_research Date of Retrieval: 01/05/2011

3 http://en.wikipedia.org/wiki/Unstructured_interview Date of Retrieval: 01/05/2011

3

1.6 Research Elements

Interviews

Interviews were designed after studying secondary information and in consultation with

experts. The following information was gathered:

Reasons for increase in the transportation and loading/unloading rates (Hamali

charges)

Concerns related to the tender process

Reasons for the increasing subsidy in the system

Reasons for the delay in implementation of the crucial changes in the system

Reasons for introducing direct sourcing

Process for removing ineligible cards

Reasons for differences between bench mark and actual quotes

Concerns of the transporters

Possible effects of empowering FPS owner

Conference

The author also attended the 39th

Annual Conference of Expenditure Reform Commission

where in important insights relating to types and kind of subsidy are obtained.

Discussions with officials of Oil-marketing companies

Further the author also had discussions with officials of oil marketing companies for

understanding of various pricing mechanisms pertaining to diesel pricing and subsidy.

Random discussions

Random discussions with case-workers and various managers in the transport department of

FSC&CA, financial advisory services of officials of RTO and test-check with a few local

transporters & mandi operators have also brought about crucial insights which were helpful

in drawing conclusions.

Analysis of Tender Files

Another form of Primary data collection has been the disclosures obtained from (Tender File,

2004-05), (Tender File, 2005-06), (Tender File, 2007-08), (Tender File, 2008-09).

Secondary Resources

The secondary resources of information includes Annual Report of FC&CA for the year

2007-08, 2008-09, 2009-10; (Citizen's Charter); (Cost Accounting Standard - 5); (Transport

Note, 2009); (Performance Audit, 2009); (Government Order, April, 2011) other than these

citations we have also refered to web portal of FC&CA Karnataka, Ministry of Petroleum4,

4 http://petroleum.nic.in/ last visited on 30-04-2011

4

CAG office5, and parliamentary discussions

6. Newspapers discussions pertaining to draft of

Food Security Bill, 2011 have also been another form of secondary resources.

1.7 Limitations of the Study

The study has the following limitations:

The non-availability of any manual explaining the different tender systems has been a

cause of concern because a lot of data has been obtained without any explanation

The author also had language constraints because almost all the information available

in tender files is in Kannada. There is no secondary language documentation in the

files

Crucial files of important orders were obtained at a later stage due to which author has

to restrict the scope of this project to cost analysis only

The author also observed serious problems of knowledge transfer in the system due to

which most of the information was coming in bits and pieces thus scope of the project

has to be restricted

5 http://www.cag.gov.in/ last visited on 06-05-2011

6 http://www.cag.gov.in/ last visited on 24-04-2011

5

2. PDS in Karnataka

The Ration Distribution System under the public distribution system has been implemented in

Karnataka state with specific aim. The department strives to distribute the ration to the

sections and the families below poverty line identified by various sources under this scheme

and to provide food security to all other families.

2.1 Food, Civil Supplies and Consumer Affairs Department

Department of Food, Civil Supplies and Consumer Affairs has the responsibility of

implementing the Essential Commodities Act, 1955 (Central Act) and the following Act and

Rules coming under it, issued by Central and State Governments.

1. Karnataka Essential Commodities (Public Distribution System) Control Order, 1992

The Karnataka Prevention Of Unauthorized Possession of Ration Cards Order, 1977

2. The Karnataka Essential Commodities Licensing Order, 1986

3. The Karnataka Essential Commodities (Maintenance of Accounts, Display of Prices

and Stocks) Order, 1981

4. The Karnataka Rice Milling Regulation and Rice and Paddy Procurement (Levy)

Order, 1999

5. The Edible Oil Packaging (Regulation ) Order, 1998

6. The Sugar Control Order, 1966

7. The Kerosene (Restriction on use and Fixation of Ceiling Price ) Order, 1993

8. The Liquefied Petroleum Gas (Regulation of Supply and Distribution ) Order, 2000

9. The Lubricating Oils and Greases ( Processing, Supply and Distribution Regulation )

Order, 1987

10. The Motor Spirit and High Speed Diesel (Regulation of Supply and Distribution and

Prevention of Malpractices) Order, 2005

11. The Naphtha (Acquisition, Sale, Storage and Prevention of Use in Automobiles )

Order, 2000

12. The Solvent, Raffinate and Slop ( Acquisition, Sale, Storage and Prevention of Use in

Automobiles ) Order, 2000

13. The Petroleum Products ( Maintenance of Production, Storage and Supply) Order,

1999

2.2 Administrative Set Up

The Principal Secretary, Department of Food, Civil Supplies and Consumer Affairs

(FC&CA) assisted by the Commissioner (FC&CA) was responsible for implementation of

the scheme at the State level. The Commissioner was assisted by the Deputy Commissioners,

Deputy Directors (FC&CA) and Chief Executive Officers of Zilla Panchayats at the district

level and by the Tahsildars and Executive Officers of Taluk Panchayat at taluk level. The

relevant roles and responsibilities of different officials of the state have been described in the

table below:

Roles Responsibilities

6

Commissioner Distribute the ration items released by the central

government based on district wise demand

Responsible for changes in bench mark rates of

transport tenders

Deputy

Commiss

ioner

Chief Executive

Officer of Zilla

Panchayat

Taluk-wise Allotment

Fixes bench mark rates and agreed rates for

transport tenders

Deputy

Director

(Districts

)

Range

Officers

(I.R.A.)7

Assistant

Director

(I.R.A.)

Sub-allotment of commodities as per allotment

made by Joint Director (PDS)/ Deputy

Commissioner

Monitoring the lifting performance of wholesale

nominees/ fair price depots and taking necessary

action in cases of poor lifting

Cursory Inspections of FPD, Wholesale depots

Report the detailed inspections

Assistant Directors Collection of various data from subordinate Offices

including lifting and distribution and balance of

food grains and compiling the same and submit the

same to the Deputy Commissioner/Head Office

Food

Shirestedars

Food

Inspectors Ensuring the proper distribution of food grains,

sugar and Kerosene oil & all such rationed articles

to the cardholders through Fair Price Depots

Prevention of diversion of Essential commodities

issued through the public Distribution system at all

levels

Cursory, Detailed and Intensive inspections as per

the schedule specified

Accounts Superintendent Scrutiny of transport and other tenders

Table 1: Roles and Responsibilities of various officials8

2.3 Targeted Public Distribution System

The Targeted Public Distribution System has been implemented in the State from 01-06-1997

on the direction of the Government of India. The main objective of this system is to ensure

food security by ensuring minimum supply of food grains to the population below poverty

line. For this purpose, households belonging to vulnerable sections of the society and living

below poverty line in the rural areas and in urban areas have been identified. These families

are being supplied food grains at subsidized prices.

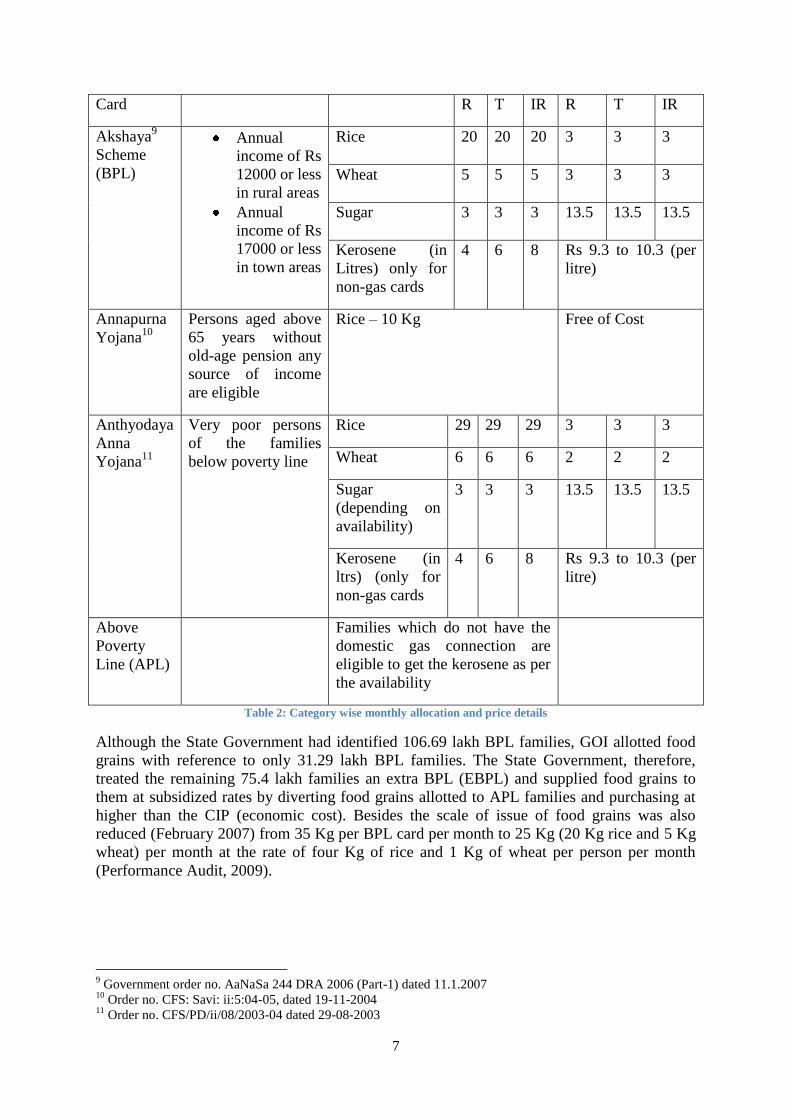

Different types of Ration Card holders, their eligibility criteria and monthly allocation details

are given below (Citizen's Charter): Remark – (R – Rural, T – Town, IR – Informal Rationing

Area)

Type of Eligibility Criteria Maximum Quantity (in Kgs) Price (in Rs)

7 50 cities with a population of 40000 and above have been notified as Informal Rationing Areas

8 http://ahara.kar.nic.in/jobchart.html Date of retrieval: 12 April, 2011

7

Card R T IR R T IR

Akshaya9

Scheme

(BPL)

Annual

income of Rs

12000 or less

in rural areas

Annual

income of Rs

17000 or less

in town areas

Rice 20 20 20 3 3 3

Wheat 5 5 5 3 3 3

Sugar 3 3 3 13.5 13.5 13.5

Kerosene (in

Litres) only for

non-gas cards

4 6 8 Rs 9.3 to 10.3 (per

litre)

Annapurna

Yojana10

Persons aged above

65 years without

old-age pension any

source of income

are eligible

Rice – 10 Kg Free of Cost

Anthyodaya

Anna

Yojana11

Very poor persons

of the families

below poverty line

Rice 29 29 29 3 3 3

Wheat 6 6 6 2 2 2

Sugar

(depending on

availability)

3 3 3 13.5 13.5 13.5

Kerosene (in

ltrs) (only for

non-gas cards

4 6 8 Rs 9.3 to 10.3 (per

litre)

Above

Poverty

Line (APL)

Families which do not have the

domestic gas connection are

eligible to get the kerosene as per

the availability

Table 2: Category wise monthly allocation and price details

Although the State Government had identified 106.69 lakh BPL families, GOI allotted food

grains with reference to only 31.29 lakh BPL families. The State Government, therefore,

treated the remaining 75.4 lakh families an extra BPL (EBPL) and supplied food grains to

them at subsidized rates by diverting food grains allotted to APL families and purchasing at

higher than the CIP (economic cost). Besides the scale of issue of food grains was also

reduced (February 2007) from 35 Kg per BPL card per month to 25 Kg (20 Kg rice and 5 Kg

wheat) per month at the rate of four Kg of rice and 1 Kg of wheat per person per month

(Performance Audit, 2009).

9 Government order no. AaNaSa 244 DRA 2006 (Part-1) dated 11.1.2007

10 Order no. CFS: Savi: ii:5:04-05, dated 19-11-2004

11 Order no. CFS/PD/ii/08/2003-04 dated 29-08-2003

8

2.4 Details of shops and cards

Every year new ration cards are issued and database is refined. The following table gives the

latest available figures:

S No. Districts

Total No.

of FPDs

Total No. of

Wholesale

Nominees

Average No. of

FPD

Total Cards

(AAY + Akshaya

+ APL)

Average

No. of

Cards per

FPD

As on

28.02.2011

As on

28.02.2011

As on 01.04.2011 As on

01.04.2011

1 Bangalore IR 1329 19 69.95 1317984 991.71

2 Bangalore (U) 504 7 72.00 527676 1046.98

3 Bangalore (Ru) 353 6 58.83 221770 628.24

4 Bagalkot 654 12 54.50 404339 618.26

5 Belgaum 1713 18 95.17 1143734 667.68

6 Bellary 594 11 54.00 514919 866.87

7 Bidar 743 6 123.83 386258 519.86

8 Bijapur 796 12 66.33 437820 550.03

9 Chamrajnagar 470 8 58.75 283169 602.49

10 Chickballapur 560 6 93.33 297448 531.16

11 Chickmagalore 494 10 49.40 280390 567.59

12 Chitradurga 578 9 64.22 420308 727.18

13 Davanagere 791 12 65.92 463790 586.33

14 D.Kannada 531 8 66.38 384787 724.65

15 Dharwad 515 8 64.38 434711 844.10

16 Gadag 362 7 51.71 246350 680.52

17 Gulbarga 988 9 109.78 537004 543.53

18 Hassan 851 11 77.36 442146 519.56

19 Haveri 436 7 62.29 366496 840.59

20 Kodagu 290 6 48.33 136805 471.74

21 Kolar 639 7 91.29 359553 562.68

22 Koppala 450 4 112.50 278774 619.50

23 Mandya 722 11 65.64 500331 692.98

24 Mysore 1062 17 62.47 735691 692.74

25 Ramnagar 559 7 79.86 306579 548.44

26 Raichur 679 5 135.80 374919 552.16

27 Shimoga 584 11 53.09 411941 705.38

28 Tumkur 1106 14 79.00 650461 588.12

29 Udupi 289 3 96.33 227598 787.54

30 U.Kannada 446 14 31.86 352858 791.16

31 Yadgiri 392 3 130.67 206678 527.24

9

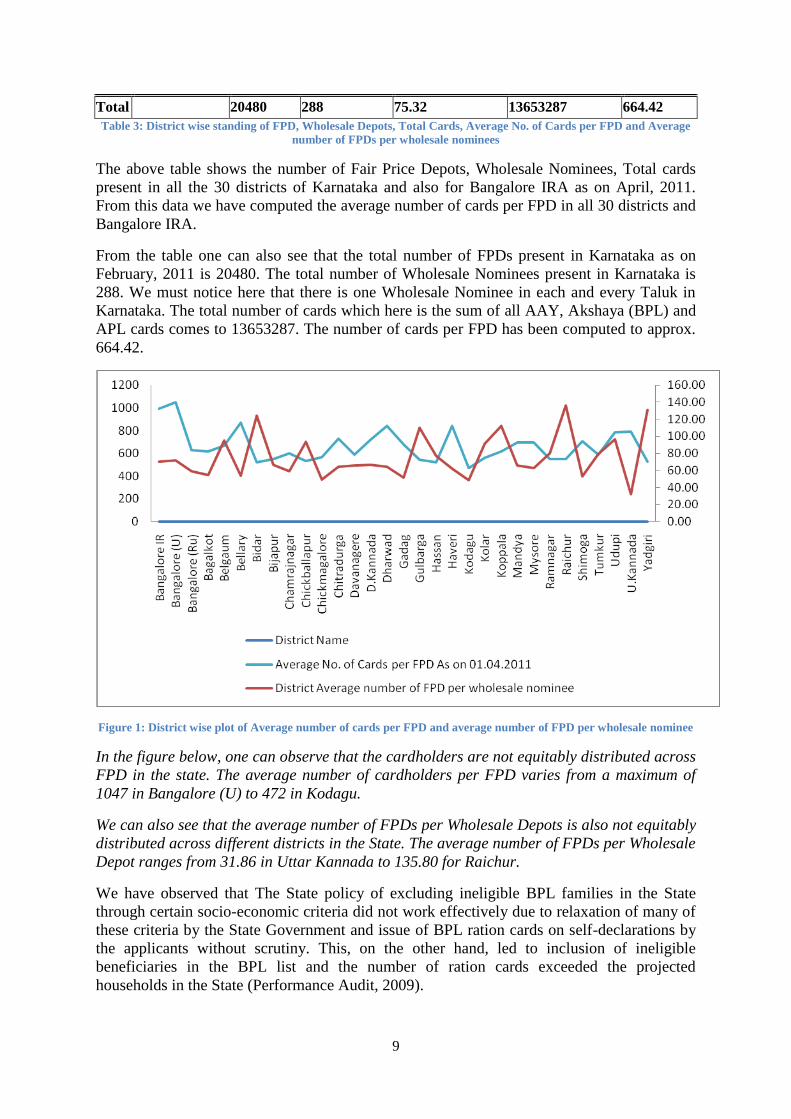

Total

20480 288 75.32 13653287 664.42

Table 3: District wise standing of FPD, Wholesale Depots, Total Cards, Average No. of Cards per FPD and Average

number of FPDs per wholesale nominees

The above table shows the number of Fair Price Depots, Wholesale Nominees, Total cards

present in all the 30 districts of Karnataka and also for Bangalore IRA as on April, 2011.

From this data we have computed the average number of cards per FPD in all 30 districts and

Bangalore IRA.

From the table one can also see that the total number of FPDs present in Karnataka as on

February, 2011 is 20480. The total number of Wholesale Nominees present in Karnataka is

288. We must notice here that there is one Wholesale Nominee in each and every Taluk in

Karnataka. The total number of cards which here is the sum of all AAY, Akshaya (BPL) and

APL cards comes to 13653287. The number of cards per FPD has been computed to approx.

664.42.

Figure 1: District wise plot of Average number of cards per FPD and average number of FPD per wholesale nominee

In the figure below, one can observe that the cardholders are not equitably distributed across

FPD in the state. The average number of cardholders per FPD varies from a maximum of

1047 in Bangalore (U) to 472 in Kodagu.

We can also see that the average number of FPDs per Wholesale Depots is also not equitably

distributed across different districts in the State. The average number of FPDs per Wholesale

Depot ranges from 31.86 in Uttar Kannada to 135.80 for Raichur.

We have observed that The State policy of excluding ineligible BPL families in the State

through certain socio-economic criteria did not work effectively due to relaxation of many of

these criteria by the State Government and issue of BPL ration cards on self-declarations by

the applicants without scrutiny. This, on the other hand, led to inclusion of ineligible

beneficiaries in the BPL list and the number of ration cards exceeded the projected

households in the State (Performance Audit, 2009).

10

The reduced quantities (25 Kg instead of 35 Kg) and inclusion of ineligible BPL families in

the BPL category has led to the denial of deserving share of food grains and hence food

security to genuine BPL families. It has also rendered the PDS system useless for APL

families. This is one of the many reasons for presence of ineligible cards in the system.

2.5 Costing Sheet for Prices and Margin

The table below represents the prices and margin at different levels in the system (rates are

constant since 2008). Thus they are not moving with the inflationary trends.

S No. Particulars BPL

EBPL12

AAY

Rice Wheat Rice Wheat Rice Wheat

1 Central Issue Price 565 415 830 610 300 200

2 State Subsidy 314 158 579 353 48 38

3 Wholesale Margin 20 20 20 20 19 15

4 Wholesale issue price 271 277 271 277 271 177

5 Retail Margin 29 23 29 23 29 23

6 Retail Issue Price 300 300 300 300 300 200

Table 4: Costing Sheet (for 1 quintal of grains) for different category of cards

The Government of India procure the food grains at MSP (Minimum Support Price) from the

farmers and issues it to the State Government at CIP (Common Issue Price). The State

Government issues rice at Rs 300 per quintal or wheat at Rs 300 or Rs 200 per quintal. We

have to realize here that both the MSP is increasing with time and the number of cardholders

in the BPL category is rising which has increased subsidy burden on both Centre and the

State. The figure below gives the year wise trend of food subsidy in the state:

Figure 2: Year wise trend of Food Subsidy in Karnataka

12

EBPL grains are actually grains diverted from APL category, therefore the prices stated here are on the higher

side.

11

The rising subsidy bill along with inefficiency in the present system has triggered a national

level debate which led to the inclusion of following things in the draft Food Security Bill13

:

The draft calls for improved "modern and scientific" storage and doorstep delivery of

grain to targeted public distribution system outlets

The draft Food Security Bill makes it compulsory for state governments to pay a food

security allowance to targeted sections in case of failure to supply food grain through

a sweeping welfare scheme targeted at nearly three-fourths of the population

The bill also guarantees 7 Kgs of grain to every person belonging to priority

households and 3 Kgs to individuals from general households every month at

subsidized prices

The draft bill says that the centre must periodically prescribe guidelines to identify

households selected for the food schemes, including exclusion criteria. It also says

these households must be reviewed and updated through periodic surveys

The inclusion of food security allowance instead of grains can have a bigger implication in

the system as it would enable FPD work as retail stores here all people can go make their

purchases for essential commodities. This can also lead to improved retailer’s margin.

The point three if implemented in combination with point four can result in people using APL

ration cards to obtain essential commodities.

2.6 Panchtantra

This initiative has been started by the Food, Civil Supply and Consumer Affairs Department

to identify bogus cards14

in their system. As part of this initiative, the Department is mapping

its computerized card holder’s data base with:

Property tax no. at rural level

RR no. (Electric meter reading no.) at urban level

Based upon author’s cursory look at the mapped database and explanation by a higher

official, the department has already mapped around 25 lakh cards out of the 96 lakh BPL

cards. The department has identified families who own as much as 10 cards. The efforts are

commendable and the initiative looks promising. Hopefully it will help the department

identify the 22 lakh bogus cards present in their system which can result in massive reduction

in food subsidy.

13

http://economictimes.indiatimes.com/news/economy/policy/states-should-pay-cash-if-they-fail-to-provide-

grain-draft-food-bill/articleshow/8641415.cms Date of Retrieval: 30 May, 2011 14

Bogus Card: if a family has more than one card then all but one of those cards are bogus cards

Ineligible Card: A card is an ineligible card if the author defaults on any criteria

12

3. Analysis of Distribution System

Food grains procured by GOI are stored in FCI godowns and made available to wholesale

nominees at CIP fixed by GOI for each commodity. Separate allocations are there for APL

and BPL categories. Whereas Levy sugar is made available to the wholesale nominees by the

designated sugar factories at rates fixed by GOI. Kerosene is supplied by the oil companies to

the wholesale nominees on the basis of allotment orders of the Commissioner. The

Department arranges transportation of PDS commodities from FCI godowns/sugar

factories/oil companies to wholesale nominees’ godowns (wholesale godowns) and wholesale

kerosene points and from there to the distribution points (FPD). The flow diagram of the PDS

commodities from the State level to FPD is given in the figure below (Performance Audit,

2009).

Figure 3: Flow of PDS commodities to beneficiaries

3.1 Procurement Concerns

Important Audit (Performance Audit, 2009) findings related to procurement are stated below:

Procurement of rice under the Decentralized Procurement Programme was only 1.24

percent of total rice production in the state

13

The shortfall in lifting of PDS food grains was high under APL category

The Department did not lift 3,171 MT rice and 19,697 MT wheat meant for BPL

families during the period 2004-09

The Department did not take action to lift 9,667.70 MT of levy sugar (2007-09) from

sugar factories

In the absence of norms for transit and handling losses, the shortages in the food

grains were passed on to the consumers

Blank delivery-cum-cash challans signed by food inspectors could have facilitated

diversion of food grains

The wholesale godowns did not have quality check and weighing facilities in place

3.2 Transportation & Distribution of PDS commodities

In this sub-section we will first state the important audit findings, thereafter author’s research

findings, understanding of various systems for awarding contracts and research conclusions

will be cited.

The important audit findings (Performance Audit, 2009) related to transport and distribution

of commodities are as stated below:

The FCI godowns assigned by the Government for lifting food grains were not the

nearest ones leading to an avoidable expenditure of Rs 2.82 crore

Levy sugar was lifted from far-off sugar factories entailing avoidable extra

expenditure on transportation

Action of the Department to award transport contracts at freak rates facilitated

diversion of food grains

The irregularities in the functioning of FPS were strongly indicative of diversion of

PDS commodities to black market

Fair price shops were economically unviable due to very poor profit margin

The deficiencies in the distribution and accounting of kerosene were suggestive of its

diversion to black market

3.2.1 Tender Process (Transport Note, 2009)

One the most crucial stage in the delivery of commodities is the awarding of tenders through

a transparent and a robust process at justifiable rates. The tender process and its underlying

rules have evolved over the years.

1) Earlier (before 2003-04) wholesale tenders15

would be issued through KFCSC while

the concerned district Deputy Commissioners would issue tenders for rural areas.

There were a lot of problems in this system. In this context, the tender applicants

have filed a writ petition on the tender rules.

2) Subsequent to this, in order to maintain uniformity, the wholesale transportation and

rural transportation tender rules are being drafted at the office of the Commissioner

since 2004-05 and tenders are being floated. Till 2007-08 the tender rates were being

submitted to the Commissioner for approval and the system was working

successfully.

15

Wholesale Tenders or rates at wholesale level means tenders for transportation from FCI/CCI godowns to

wholesale nominees;

Rural Tenders or rates at rural level means tenders for transportation from wholesale nominees to FPS

14

3) In the year 2007-08 Government had stopped this process (reasons are not available in

the files) and the Deputy Commissioners of the districts were appointed as Competent

Authority to fix tender rates and approve them. The Commissioner’s office has been

asked to prepare benchmark rates using scientific criteria and send it to the districts

and action has been taken accordingly. In the year 2007-08 tenders were issued

without any problems. But, in the year 2008-09 it has been observed that very high

tender rates have been fixed. At times these rates were as high as 50 to 100 percent of

that of benchmark rates ( Refer Annexure 11)

Figure 4: Different between Bench Mark rates and Agreed Rates

4) The Comptroller and Accountant General Audit team in their Performance audit for

the year of 2009-10 in the Department of Food and Civil Supplies have observed that

without approval of the Commissioner the transportation tender rates have been fixed.

Government has been spending crores of rupees on transportation of food and the

money has to be paid from the Commissioner’s office. But, it has been stated that the

Commissioner does not have any control over the transportation rates. Hence, the

Deputy Commissioners of the districts may be allowed to fix transportation rates at

10% more or less and incase it exceeds this rate, the permission of Commissioner has

to be obtained with appropriate explanation and contract may be entered into. This has

been achieved by introduction of slab-rate system for award of Tenders.

Till 2009 the tender was being issued once a year, but post performance audit only one tender

has been issued for the year 2009-10 and 2010-11.

A copy of Tender Advertisement is also available (See Annexure 4)

3.2.1.1 Fixing of Turn over: The concerned Deputy Commissioners have been asked to contact the wholesale transporters

and fix the Turnover in the current tender process. As a result, there is no uniformity in the

process of fixing the Turnover. On observing the transportation rates released it is found that

each wholesale tender applicant has a Turnover of Rs. 1 crore (Annexure 9). It means, the

annual release to the office of the Commissioner is Rs.70 to 75 crore. For example: The total

transportation costs for the year 2008-09 is Rs.73 crore. It averages to Rs.2.40 crore for 30

districts.

15

3.2.1.2 Technical Specifications/Conditions:

Change in number of lorry’s: Monthly or quarterly meetings with the Deputy

Directors, are being held in the office of the Commissioner, in such meetings one of

the important issues that is flagged is the time lag in lifting of food grains. When the

reason for this is observed it is found that the transporters have failed to lift more food

grains in the stipulated time. The Deputy Director is of the opinion that 10 Lorries are

insufficient. Also, in the tender process though it is stated that the tender applicants

who fail to lift the grains in the stipulated time must be black listed no action has been

taken. This issue has been observed and stated in the Justice Wadhwa Report as “Zero

tolerance” towards erring transporters. The number of Lorries have been increased to

15 (8 owned) for wholesale and 10 (5 owned) for rural transportation (Annexure 9,

10).

Lorry’s with uniform color: It has been made mandatory that the lorry’s designated

for PDS have to be ‘yellow’ in color and naming the lorry or writing across on it as

‘Public Distribution System Lorries’.

Capacity of the Lorries: For the tender process and calculation of the benchmark

rates, capacity of the lorry has been fixed to 10 Tonnes. But actual capacity of the

lorries being used has been found to be 16 Tonnes (Annexure 7).

3.2.2 Tender Systems

For award of tenders, two types of systems have been used:

I. Bench mark based tender quotes

II. Slab rate system

3.2.2.1 Bench mark based system This system has been introduced in the year 2004-05, where in bench marks has been

developed using following references:

Calculation of operational cost of auto by transport department (Annexure 6)

Prevalent Government Rates in 2004-05 (Annexure 6)

Prevalent KSRTC rates in 2004-05 (Annexure 6)

Prevalent PWD SR Rates in 2004-05 (Annexure 6)

Transport rates prevalent in different districts of Karnataka in 2004-05 (Annexure 3)

The author could not understand how benchmark rates have been established using the above

references as no explanation was given in the files (Tender File, 2004-05).

However, the criteria of changing the rates wrt to different parameters were available in the

file (See schedules iii-a, iii-b & iii-c Annexure 6). These formulas were never used to modify

the benchmark rates.

Changes in Bench mark rates

The author observed that, in practice, yearly change in bench mark rates is equal to the

yearly percentage change in the diesel prices in contrast to formula given in schedule iii-a,

where fuel mileage of the vehicle has also been considered. (Refer Annexure 6, 11)

An assumption has been made in this regard that changes in all other parameter is equal to

the change in diesel prices.

Distances for calculation of charges

16

The bench marks as well as agreed rates of the transportation are reported in per km per qtl.

This implies the important of distance covered as well as quantity of food grains transported.

The average distances for transportation at wholesale level for different districts are given in

Annexure 11. The average distances for transportation at rural level are given for 3 selected

districts in Annexure 12. It has to be noted here that these distances are available for other

districts as well and have been computes using average distances for transportation of goods

from wholesale nominees in each taluk to fair price shops in the respective taluk.

3.2.2.2 Slab rate system After the Performance Audit, the department had introduced this new system where in tender

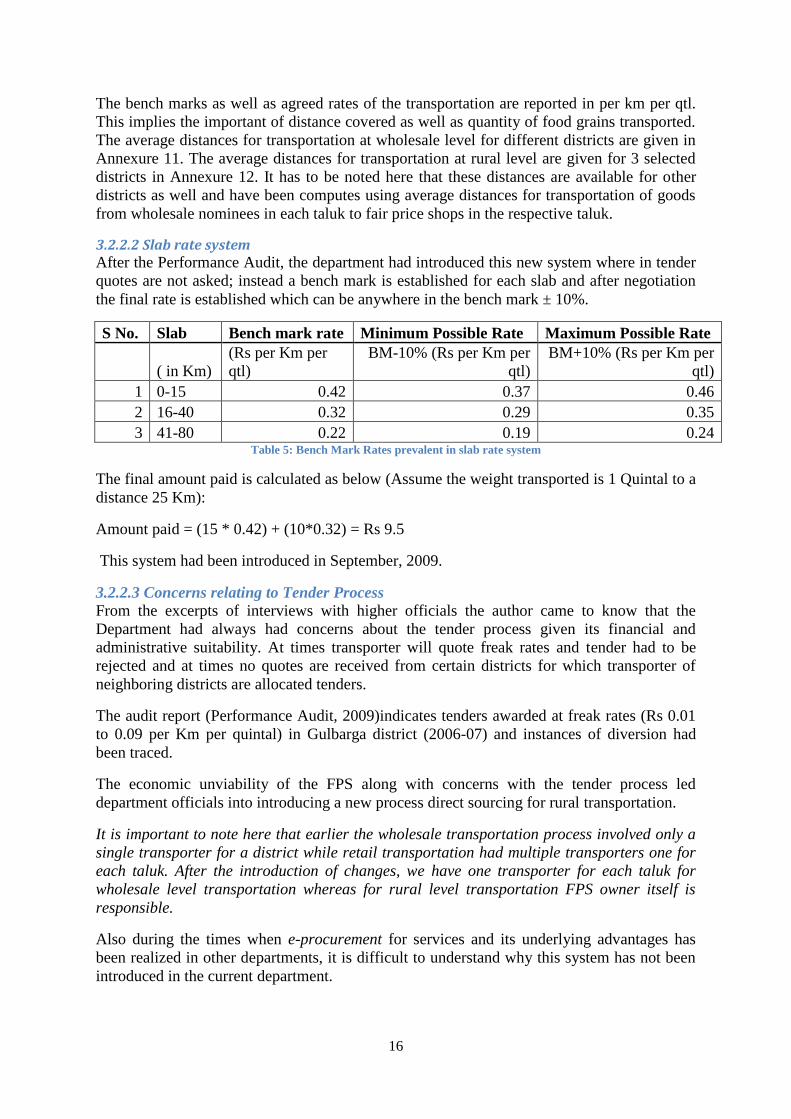

quotes are not asked; instead a bench mark is established for each slab and after negotiation

the final rate is established which can be anywhere in the bench mark ± 10%.

S No. Slab Bench mark rate Minimum Possible Rate Maximum Possible Rate

( in Km)

(Rs per Km per

qtl)

BM-10% (Rs per Km per

qtl)

BM+10% (Rs per Km per

qtl)

1 0-15 0.42 0.37 0.46

2 16-40 0.32 0.29 0.35

3 41-80 0.22 0.19 0.24 Table 5: Bench Mark Rates prevalent in slab rate system

The final amount paid is calculated as below (Assume the weight transported is 1 Quintal to a

distance 25 Km):

Amount paid = (15 * 0.42) + (10*0.32) = Rs 9.5

This system had been introduced in September, 2009.

3.2.2.3 Concerns relating to Tender Process

From the excerpts of interviews with higher officials the author came to know that the

Department had always had concerns about the tender process given its financial and

administrative suitability. At times transporter will quote freak rates and tender had to be

rejected and at times no quotes are received from certain districts for which transporter of

neighboring districts are allocated tenders.

The audit report (Performance Audit, 2009)indicates tenders awarded at freak rates (Rs 0.01

to 0.09 per Km per quintal) in Gulbarga district (2006-07) and instances of diversion had

been traced.

The economic unviability of the FPS along with concerns with the tender process led

department officials into introducing a new process direct sourcing for rural transportation.

It is important to note here that earlier the wholesale transportation process involved only a

single transporter for a district while retail transportation had multiple transporters one for

each taluk. After the introduction of changes, we have one transporter for each taluk for

wholesale level transportation whereas for rural level transportation FPS owner itself is

responsible.

Also during the times when e-procurement for services and its underlying advantages has

been realized in other departments, it is difficult to understand why this system has not been

introduced in the current department.

17

3.3 Direct Sourcing

This system has been introduced in the year 2011 (Government Order, April, 2011)

(Annexure 5) for a period of six months to transport food grains from Wholesale Nominees to

FPS. In this system, FPS owners have to arrange for the transport of Food grains & other

commodities. A price of Rs 1/ Km/ qtl has been fixed as Transportation charges while the

handling charges have been fixed as Rs 6 per qtl.

3.3.1 Costing Sheet for Transportation charges

The author collected the following costing sheet from the department.

S No

PARTICULARS CALCULATION AMOUNT IN Rs.

1 Salaries and wages

of drivers, cleaners

and others

Rs.16000 per month/30 Rs.533 per day. 533/day

2 Fuel and lubricants Rs.50/- towards fuel/5kms=10Rs,

Lubricant cost Rs.18000/12/50=1500

litres. Amount is calculated per month

for the minimum run of 50 kms per

month.

1510/month

3 Amortized cost of

tyre, tube and

battery

Tube and tyres Rs 25000 per pair gives

40000 Kms, battery expenses Rs 4000

per annum

335 / month (Rs 333

per month + Rs 1.6

per Km)

4 Spares, repairs and

imminences

Approximate cost of Rs 20000 per

month

400/ month /km

5 Other variable cost Toll Tax, Hamali cost etc. 50 / Month/km

6 Insurance (20,000/12)/50 33/month/km

7 Licence fee,

permit fee and

taxes

Rs.10 lakh is taken for calculation as

annual turnover (10,00,000 X 5 /100)/12

4166 / month

8 Other fixed cost Rs.10 lakh is taken for calculation as

annual turnover (10,00,000 X 1/100)/12

833/month

Total 7860

9 Profit 1572

Total Cost 9432

Since the above calculation is done for 10 MT capacity lorries, per kilometer per quintal cost

would be 9432 / 1000 = Rs.0.94

This can be rounded off to Re. 1/ Km/ Quintal

Table 6: Costing Sheet for Transportation charges

The author observed that the above costing sheet has following implicit or explicit

assumptions:

1. The Fair Price Shop owner already owns a truck

2. Price of Diesel is Rs 50 per litre

3. He has employed one truck driver and two cleaners

4. The owned truck travels only 50 Km/ month

18

5. The annual turnover for transportation to each FPS is Rs 10 lakh

6. All expenses are calculates for a 10 Tonne capacity lorry

7. Basis is per km and not per day or per month or per month per Km

First of all we need to understand that once a basis of apportionment is adopted, the same

should be followed consistently. (Cost Accounting Standard - 5) Section 6.3

Salary and Wages of Drivers, cleaners and others:

Salary of one driver (Rs 8000) and two cleaners (Rs 4000 each) has been considered. This

amounts to Rs 16000 per month or Rs 533 per day (as a month has 30 days).

Now we have to understand that this cannot be accounted as it is and we need to convert it

into per Km basis. From the above assumption, Rs 16000 divided by 50 gives us Rs 320 per

Km.

Fuel and Lubricants

A fuel mileage of 5 Km per litre and an annual consumption of 180 litres have been

considered. In addition to this, price of diesel has been assumed to be Rs 50 per litre and price

of lubricants has been assumed to be Rs 100.

This gives Rs 30/ Km + Rs 10/ Km = Rs 40 / Km

Here the unit is per Km and not per month as stated in the sheet.

The author has also observed a lube oil requirement of 400 litre lube oil for a truck

(Schedule iii-b Annexure 6) this will give lube oil cost of Rs 66.67/ Km +Rs 10 / Km =Rs

76.67 per Km

Amortized cost of tyre, tube and battery

An expense of Rs 25000 per pair gives 40000 Km and a battery expense Rs 4000 per annum.

Here the calculation has been done as 40000 divided by 25000 = Rs 1.6 per Km

And Rs 4000 divided by 12 = Rs 333.33 per month and then both have been added to Rs 335

per month

As per author’s understanding calculation should have been as follows:

Total no. of tyres in the truck = 10 or 5 pairs

This gives an expense of 25000 * 5 = Rs 125000

Now 3 figures have been observed for life of tyre 40000 Km (Costing Sheet above), 36000

Km (Annexure 6) and 50000 Km (Annexure 6, Schedule iii-b). We are taking 40000 Km for

our calculation. Since our requirement is 12 * 50 = 600 Km annually.

But we have to understand here that the expense will be paid for the full year (Assuming that

Rs 125000 is expense for full year) and not according to our requirement. A truck runs 54750

Kms annually (Annexure 6).

This gives a total of Rs 129000 (an expense of Rs 10750 per month) or Rs 215 per Km

Spares, repairs and imminences:

19

An expense of Rs 400/ month/ Km has been reported which is Rs 400 / Km.

Toll Tax, Hamali cost etc:

An expense of Rs 50/ month/ Km has been reported which is Rs 50 / Km.

Insurance:

An expense of Rs 33/ month/ Km has been reported which is Rs 33 / Km.

License fee, permit fee and Taxes:

Here Rs 10 lakh has been assumed as annual turnover.

Cost computed is 5% of Rs 1000000 divided by 12 = Rs 4166 per month

This cost has to be divided by 50 to convert it to per Km basis. Thus, actual cost here would

be only Rs 83.32 per Km.

Our research on Motor Vehicle Taxation schedules have revealed following observations:

A road tax of Rs 2200 + Cess of 11% payable on a quarterly basis (Refer Annexure 8)

A permit fee of Rs 850 for 5 years permit and a license fee of Rs 250 for obtaining a

smart card

Depreciation:

This is one parameter that has not been accounted (Cost Accounting Standard - 5).

We are assuming that the present price of one such vehicle is Rs 1000000 (Annexure 6).

Assuming Salvage value of 15% = Rs 150000 and Life of 15 years

Depreciation = Rs 56666.67 per annum or (56666.67 divided by 12*50 = Rs 94.44 per Km

Other fixed cost:

Cost computed is 1% of Rs 1000000 divided by 12 = Rs 833 per month

This cost has to be divided by 50 to convert it to per Km basis

Thus actual cost here would be only Rs 16.66 per Km

Total Cost w/o profit =Rs 320+Rs 76.67+Rs 215+Rs 400+Rs 50+Rs 33+Rs 83.32+Rs

94.44+Rs 16.66 = Rs 1286.67 per Km

Profit: 20% of 1286.66 = Rs 257.334 per Km

This means Total Cost = Rs 1544 per Km for 10 Tonne capacity or Rs 0.1544 per Km per

Quintal much in line with figure arrived at in 2004-05 ( Refer Annexure 6)

Note: We have tried to demonstrate here the computation procedures given the above stated

assumptions and prices. We have not verified any of the prices stated above due to time

constraints.

20

3.3.2 Application of the Costing Sheet

This costing sheet cannot be applied for cost-estimation for direct sourcing because of the

following loopholes in the assumptions:

It is not possible to buy truck or parts thereof if one has to travel only 50 Km per

month

Parameters like spares, repairs and imminences; insurance are out of question once

we know that there is no truck

Full month salary of one driver and two cleaners is again questionable. Their

requirement is there only when truck is purchased or hired. We need to hire people

(as per vehicle used) only for a few days i.e. only when trip is planned.

We need not use a 10 Tonne truck as the quantity that we need to transport is only

150 quintal per FPS (see calculations below)

Life span of Truck should be 10 years only for our calculations, we have restricted

truck life in our tender rules

The above sheet does not take into account times and effort devoted by FPS owner

himself i.e.it does not pay FPS owner for making trips to collect grains

The above costing sheet is ideal for long-term distances with a few changes. Cost of

Amortization of tyres, tubes will increase on account of increase in usage (Refer Annexure 6

schedule iii-c).

No. of APL

cards

Rice (6 Kg/ Card)

(in Tonnes)

Wheat (1 Kg/ Card)

(in Tonnes)

Demand (APL) 4031576 24189.456 4031.576

No. of BPL

cards

Rice (20 Kg/ Card)

(in Tonnes)

Wheat (5 Kg/ Card)

(in Tonnes)

Sugar (3 Kg/

Card)

(in Tonnes)

Demand (BPL) 8482648 169652.96 42413.24 25447.944

No. of AAY

cards

Rice (29 Kg/Card)

(in Tonnes)

Wheat (3 Kg/ Card)

(in Tonnes)

Sugar (3 Kg/

Card)

(in Tonnes)

Demand (AAY) 1139063 33032.827 3417.189 3417.189

No. of Police

Cards

Rice (13 Kg/ Card)

(in Tonnes)

Wheat (3 Kg/ Card)

(in Tonnes)

Demand

(Police) 79701 1036.113 239.103

Total Demand

(in Tonnes)

227911.356 50101.108 28865.133

Table 7: Computation of Total Demand of Wheat, Rice and Sugar

From the above table one can observe that total quantity of grains and sugar that has to be

lifted is the sum of Rice (227911.356), Wheat (50101.108) and Sugar (28865.133) which is

equal to 306877.597 Tonnes or 3068775.97 quintals.

Total number of Fair Price Depots in the state = 20480

Total quantity to be lifted per FPD = 150 quintals

21

This can also be shown as the sum of 111.3 quintals of rice/ FPD, 24.5 quintal of wheat / FPD

and 14.1 quintals of sugar/ FPD. From this we can compute Retailers (FPD owner’s) margin

as

Quantity (qtls/FPD) Retailer Margin/

Quintal16

Margin (in Rs)

Rice 111.3 29 3228

Wheat 24.5 23 563

Sugar 14.1 27 381

4172

Table 8: Computation of total margin on Rice, Wheat and Sugar by Retailer

The above calculations have been made on the assumptions that:

1. There is no other commodity than Rice, Wheat and Sugar

2. Kerosene Margins have not been considered

3. There is no other way to compensate FPS owner

The average monthly income of an FPS owner with 300 cards was around Rs 2,600 after

reckoning the expenditure towards ground rent, salary for assistants, electricity,

transportation and that of the FPS owner with 500 cards around Rs 4,200, the FPS were found

economically unviable. With the number of cards assigned to each FPS being less than the

prescribed norm and with the reduction in the scale of food grains supplied to each

beneficiary the viability of the FPS was further reduced. The irregularities brought out could

be attributed to the non-viability of the FPS. (Performance Audit, 2009)

Figure 5: Fair Price Shops operating with less than the prescribed number of ration cards

We need to see this already stated economic non-viability wrt following things:

16

Costing Sheet 2010-11

22

We are refining our card database this will reduce the number of cards

The reduced number of cards means the number of cardholders per FPS will decrease

further

Retail margin is fix in the costing sheet and there is no account for inflation on his

compensation

Therefore we have to realize the need to reduce the number of fair price shops so that FPS

owner can distribute more quantity per shop and earn more revenues.

3.3.2.1 Fieldwork for Transportation Costing We have test-check a few transporters and obtained following quotes:

S No. From To Distance (Km)

Capacity of Lorry (Tonne) Rate

Rate ( Rs per Km per Quintal)

1 Bangalore Chandigarh 2298 27 Rs 85000 0.137

2 Bangalore Delhi 2061 27 Rs 75000 0.135

3 Bangalore Kolkata 1881 27 Rs 65000 0.128

4 Bangalore Agra 1858 - Rs 340 per Qtl 0.183

5 Bangalore Udaipur 1751 - Rs 250 per Qtl 0.143

6 Bangalore Jaipur 1985 - Rs 280 per Qtl 0.141 Table 9: Long term rates as quoted by transporters

We also enquired about the prevalent short distance rates. Short-distance quotes are

negotiable rates in the range Rs 2500 to 3000 for a lorry capacity ranging (10 – 15 – 21

Tonnes) to cover a distance to the tune of 50 Km.

Note: We have to observe here that long-distance rates are much in line with the rates

calculated by us using CAS – 5 standards whereas short distance rates are negotiable and

market driven for the same vehicle

3.3.3 Handling Charges

From the excerpts of an interview with a higher official, we have observed that these rates

have been increased from existing Rs 4.5 per quintal to Rs 6 per quintal. The possible reasons

for this increase are increase in the number of loading and unloading points and reduced

quantity for transport. As shown in the figure below, earlier lorries used to follow a circular

map with higher capacities and go on distributing goods through various FPS falling in

between but now the present system is like a hub and spoke system.

Earlier a full truck load could have been used to transport grains at a single time but now only

small quantities will be transported. All this has diminished the possibilities of a cost bargain.

3.3.3.1 Fieldwork for Handling Charges We have done some test-studies which reveal the following real life scenarios:

1. There is a contract with the labor for the loading and unloading of the full truck. The

amount for this is anywhere in the range Rs 500 to Rs 700. The test case here had a

capacity 300 bags of 50 Kg each which gives a total weight of 15 Tonnes or 150

quintals. This gives the charges in the range of Rs 3.33 per quintal to Rs 4.66 per

quintal.

23

2. If a transporter has a large volume or multiple trucks, he will hire labor on a day wage

basis and get the loading and unloading done. This gives even more cost advantage to

him.

The analysis of the test-cases clearly suggests that the current system is cost inefficient.

Figure 6: Route Map prior to Direct Sourcing (Circular, Left Image) and post Direct Sourcing (Hub and Spoke,

Right Image)

Now to transport reduced quantities a FPS owner has to go for multiple trips. For example, a

transporter covers a distance of 50 Km in a month (Assumption given in the cost sheet). Let

us make another assumption that his shop is at a distance of 5 Km from the wholesale depot.

Thus, he is making 10 trips in a month transporting around 15 quintals each time. We can

transport 15 quintals using a rickshaw or a hand cart and need not hire a lorry. However, the

point we are trying to make here is that more time is required to transport grains now which

makes the system inefficient with respect to time required.

Any decision for direct sourcing is seen with respect to following 4 parameters:

Cost Efficiency

Time Efficiency

Derived Value

Strategic Importance

We have demonstrated earlier how system is inefficient both with respect to Cost and Time,

now we will see value derived from or strategic importance of the direct sourcing in the

system.

Derived Value: We have seen in the costing sheet provided by the department that how

generously we are paying FPS owner for the expenditure he is not actually incurring. Though

such freebies make him realize astronomical economic gains (with respect to delivery of a

commodity i.e. valued at Rs 3 per Kg), they never ensure that there will be no diversion in the

system. Instead it substantially increases the control of FPS owner on the entire supply chain

which can be disadvantageous in the long run.

24

We understand the current tender process is fraught with challenges but e-procurement will

ensure that we generate value in terms of:

Reduced time period between issue of tenders and receipt of tenders

Substantial Tender Premium17

can be obtained

Reduced Time Cycle18

Strategic Importance:

In the times, when the whole world is going lean we are introducing one system which by

nature of its operation is inefficient.

A lean – transportation system is designed by accounting for following elements:

Organizational Structure: Change the organization to meet JIT requirements. Instead

we are introducing a system where FPS owner will making frequent trips to wholesale

godowns. Hence there will be times when delivery of the commodity will not be

possible because of unavailability of owner or transportation of small quantities of

fewer items

Number of Carriers: Reduce the number of carriers to four or fewer--one for each

region. This can be ensured if we use large vehicles for transportation but we are even

reducing the quantity transported for each cycle

Contract Basis: Put 100 percent of transportation services on a contract basis.

Interestingly, we are here removing a system in which transportation is done on

contractual basis

Computer Interface: Establish extensive computer interface with all contracted

carriers. This can be achieved if we introduce GPS and e-procurement but with direct

sourcing in place this installation is not possible

Regular Pickup and Delivery: Pick up all freight from suppliers and deliver on a

scheduled basis. Direct sourcing will make the basis ad-hoc instead of already

scheduled basis

Efficient Handling Equipment: Use state-of-the-art technology and handling

equipment. These equipments can be installed at FCI and wholesale godowns can

reduce our expenditure on handling charges.

Thus, we can state that the current system is also not capable of achieving strategically

important goals.

17

The premium offered on the current market price 18

The average value of time from Line estimate preparation to Agreement signing in your department

25

4. Conclusions

From our study of the PDS system in Karnataka we can draw following conclusions:

1. The distribution of average number of cards per FPS is not uniform across different

districts in the state

2. The distribution of average number of FPS per wholesale depot is also not uniform

across different districts in the state

3. The rising food-subsidy, the presence of ineligible and bogus cards have rendered the

system useless for the APL families

4. The Department’s efforts for identifying bogus cards look promising

5. In the bench mark system, the following discrepancies have been detected:

Agreed rates were as high as 100% higher than the bench mark rates

Figure 7: Percentage increase of agreed rate over bench mark rates for 2008-09

The changes made in the bench mark rates as compared to previous years did

not take into account the fuel mileage of the vehicle

6. The slab rate system looked promising and more efficient the bench mark rate system

7. The costing sheet of transportation for direct sourcing is not applicable on account of

faulty assumptions and is leaving a lot on table for the FPS owners

8. FPS have been seen to be non-viable, but extensive study needs to be done before we

can give some conclusive output on this

9. Direct sourcing had increased the number of loading/unloading points. This system is

both cost and time inefficient

10. Larger capacity vehicles are being used in the system

11. E-procurement must be introduced in the system to get rid of burdensome current

tender process; to achieve reduced tender cycles & achieve substantial tender

premium

12. Direct sourcing in the system scenario (small no. of items with fixed quantity) is not

capable of achieving strategically important goals of lean transportation systems

13. In the market for shorter distances rates are negotiable with respect to quantity but not

distance i.e. they are the same irrespective of the distance

26

Impact Assessment

Average Monthly distance covered by FPS

owner

50 Km

Average Monthly Quantity/ FPS 150 Qtl

Total no. of FPS 20480

Total Monthly Quantity 3068776 Qtl

Direct Sourcing:

Transportation Charges = Rs 1 per Km per Qtl

Handling Charges = Rs 6 per Qtl

Total Monthly Transport Charges 1*50*150*20480 Rs 15.36 Crore

Total Handling Charges 6*3068776 Rs 1.8412 Crore

Total DS TC Rs 17.2012 Crore

Slab Rate:

Transport Charges: Rs 0.42 per Km per Qtl

Handling Charges: Rs 4.5 per Qtl

Total Monthly Transport Charges 0.42*50*150*20480 Rs 6.4512 Crore

Total Monthly Handling Charges 4.5*3068776 Rs 1.3809 Crore

Total SR TC Rs 7.8321 Crore

Total Monthly Impact Rs 9.3691 Crore

Total Impact of 6 months Rs 56.214 Crore Table 10: Impact Assessment of Direct sourcing Vs Slab Rate System

Any number less than this is a clear indicative that distance travelled is less than 50 Km/

month.

27

5. Recommendations

1. The average no. of FPS per wholesale depot and average no. of cards per whole sale

depot must be distributed equitably

2. The department must refine cardholders data to remove all the bogus and ineligible

cards present in the system

3. One can introduce payment of food security allowance to target sections through

channels like banking. The system can thus be made cashless but the biggest

constraint here would be the availability of the refined database.