Embed Size (px)

Citation preview

Options

Dr. Lynn Phillips Kugele

FIN 338

OPT-2

Options Review

• Mechanics of Option Markets

• Properties of Stock Options• Valuing Stock Options:

–The Black-Scholes Model

OPT-3

Mechanics of Options Markets

OPT-4

Option Basics

• Option = derivative security– Value “derived” from the value of the

underlying asset

• Stock Option Contracts

– Exchange-traded

– Standardized

• Facilitates trading and price reporting.

– Contract = 100 shares of stock

OPT-5

Put and Call Options• Call option

– Gives holder the right but not the obligation to buy the underlying asset at a specified price at a specified time

• Put option– Gives the holder the right but not the

obligation to sell the underlying asset at a specified price at a specified time

OPT-6

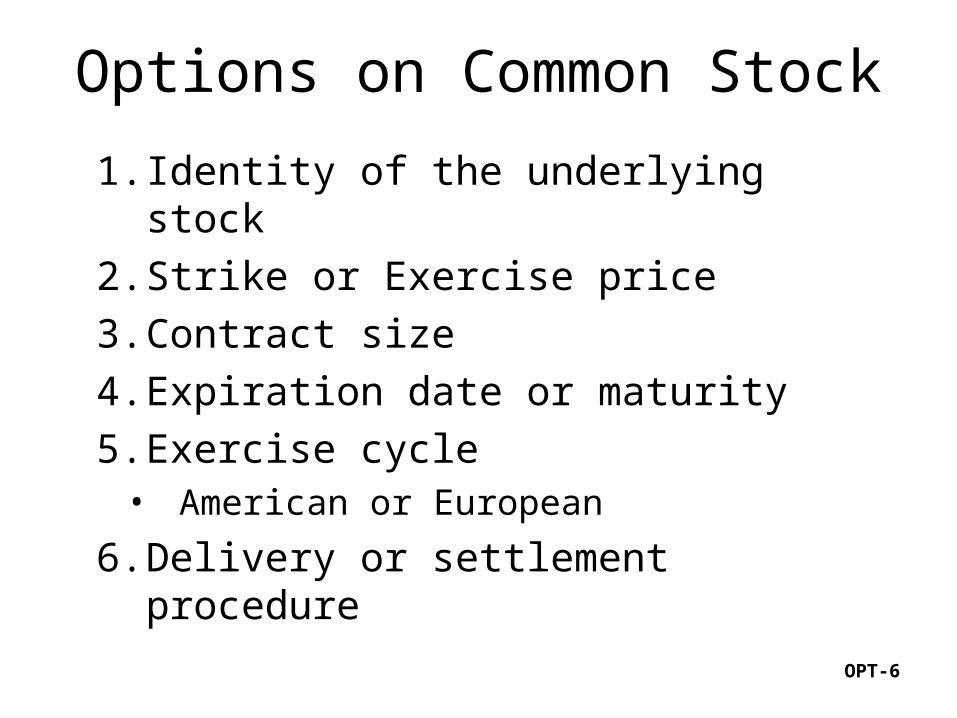

Options on Common Stock

1. Identity of the underlying stock

2. Strike or Exercise price

3. Contract size

4. Expiration date or maturity

5. Exercise cycle• American or European

6. Delivery or settlement procedure

OPT-7

Option Exercise

• American-style– Exercisable at any time up to and

including the option expiration date– Stock options are typically American

• European-style– Exercisable only at the option expiration

date

OPT-8

Option Positions• Call positions:

– Long call = call “holder”• Hopes/expects asset price will increase

– Short call = call “writer”• Hopes asset price will stay or decline

• Put Positions:– Long put = put “holder”

• Expects asset price to decline– Short put = put “writer”

• Hopes asset price will stay or increase

OPT-9

Option Writing

• The act of selling an option

• Option writer = seller of an option contract – Call option writer obligated to sell the

underlying asset to the call option holder– Put option writer obligated to buy the

underlying asset from the put option holder– Option writer receives the option premium

when contract entered

OPT-10

Option Payoffs & Profits

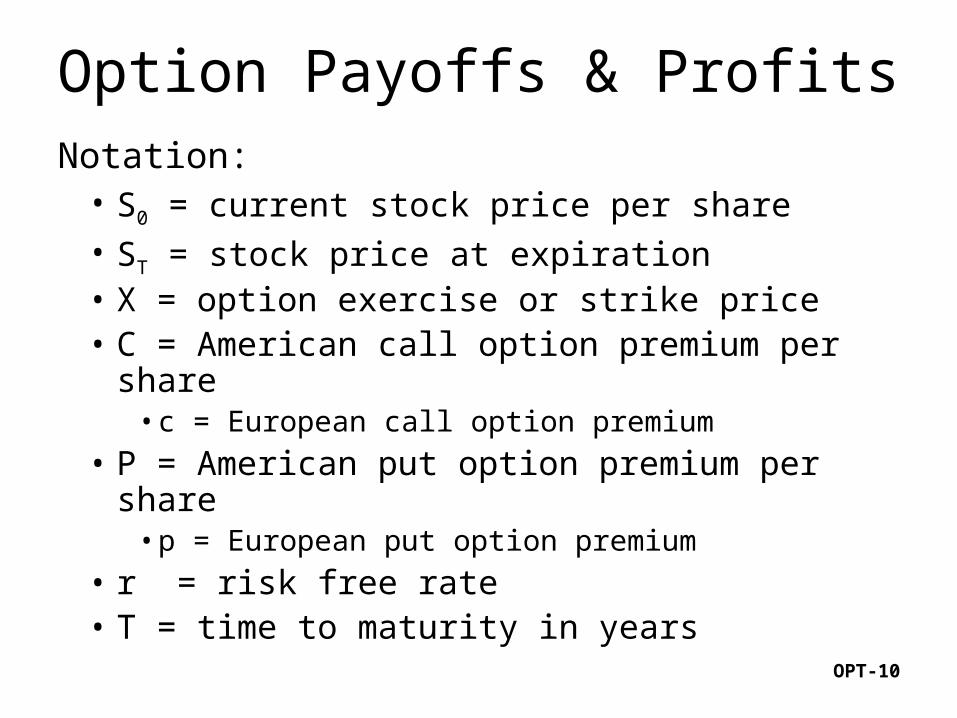

Notation:• S0 = current stock price per share• ST = stock price at expiration • X = option exercise or strike price• C = American call option premium per share

• c = European call option premium

• P = American put option premium per share• p = European put option premium

• r = risk free rate• T = time to maturity in years

OPT-11

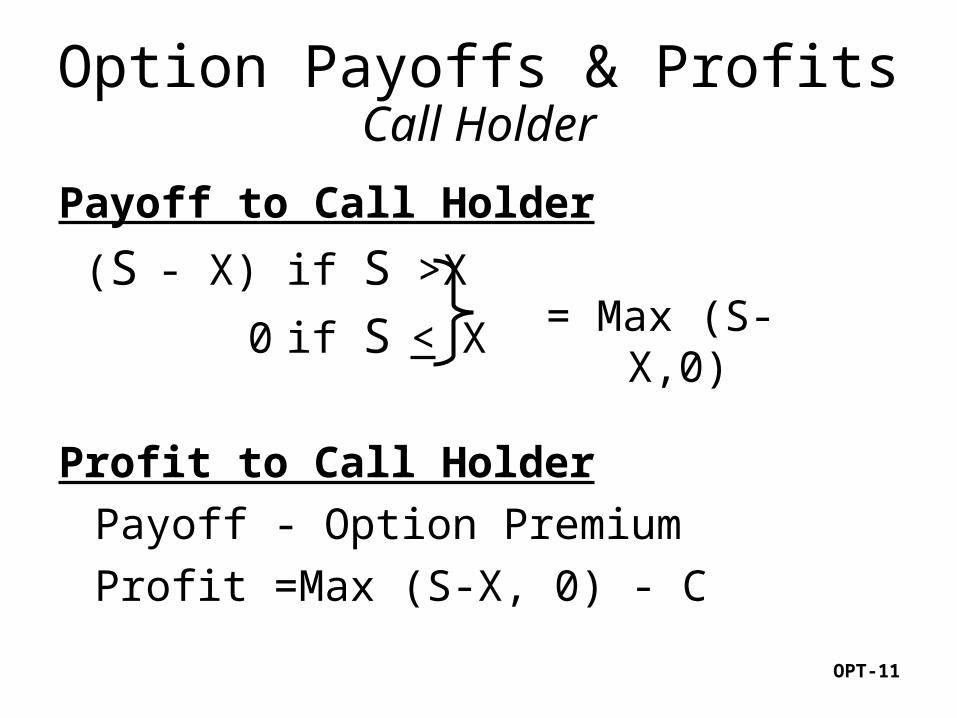

Payoff to Call Holder

(S - X) if S >X

0if S < X

Profit to Call Holder

Payoff - Option Premium

Profit =Max (S-X, 0) - C

Option Payoffs & ProfitsCall Holder

= Max (S-X,0)

OPT-12

Payoff to Call Writer

- (S - X) if S > X = -Max (S-X, 0)

0 if S < X = Min (X-S, 0)

Profit to Call Writer

Payoff + Option Premium

Profit = Min (X-S, 0) + C

Option Payoffs & ProfitsCall Writer

OPT-13

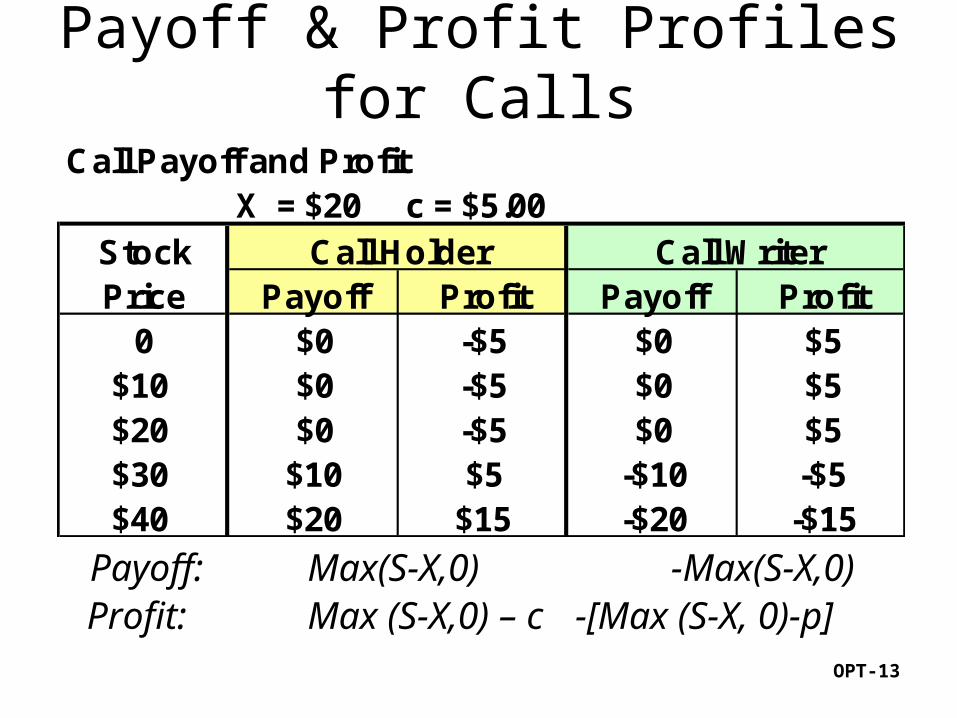

Payoff & Profit Profiles for Calls

Call Payoff and ProfitX = $20 c = $5.00

StockPrice Payoff Profit Payoff Profit

0 $0 -$5 $0 $5$10 $0 -$5 $0 $5$20 $0 -$5 $0 $5$30 $10 $5 -$10 -$5$40 $20 $15 -$20 -$15

Call Holder Call Writer

Payoff: Max(S-X,0) -Max(S-X,0) Profit: Max (S-X,0) – c -[Max (S-X, 0)-p]

OPT-14

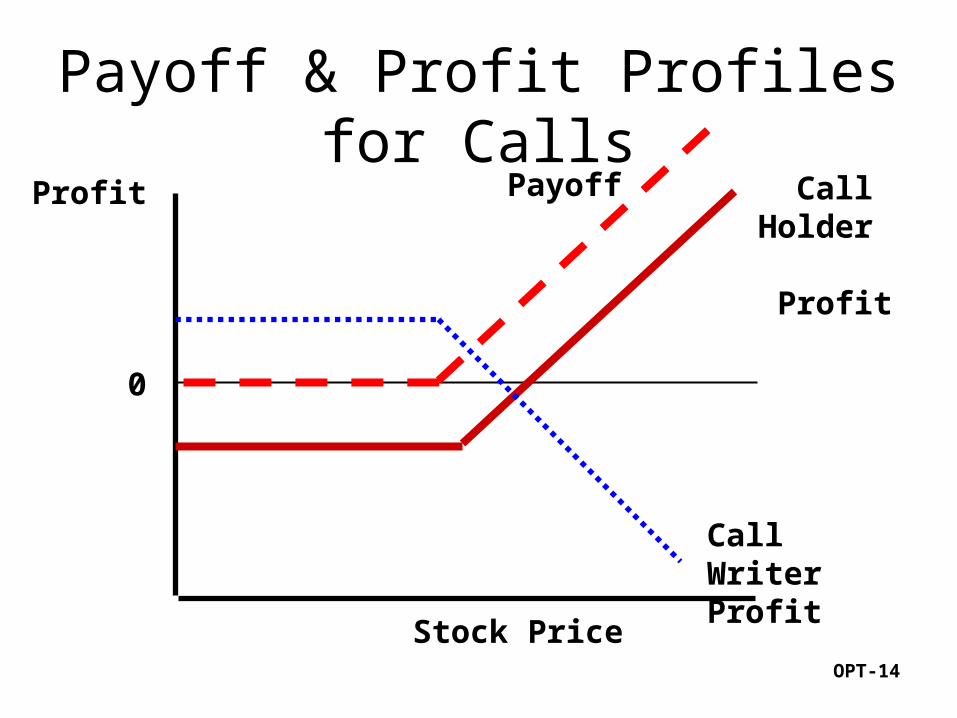

Payoff & Profit Profiles for Calls

Profit

Stock Price

0

Call Writer Profit

Call Holder Profit

Payoff

OPT-15

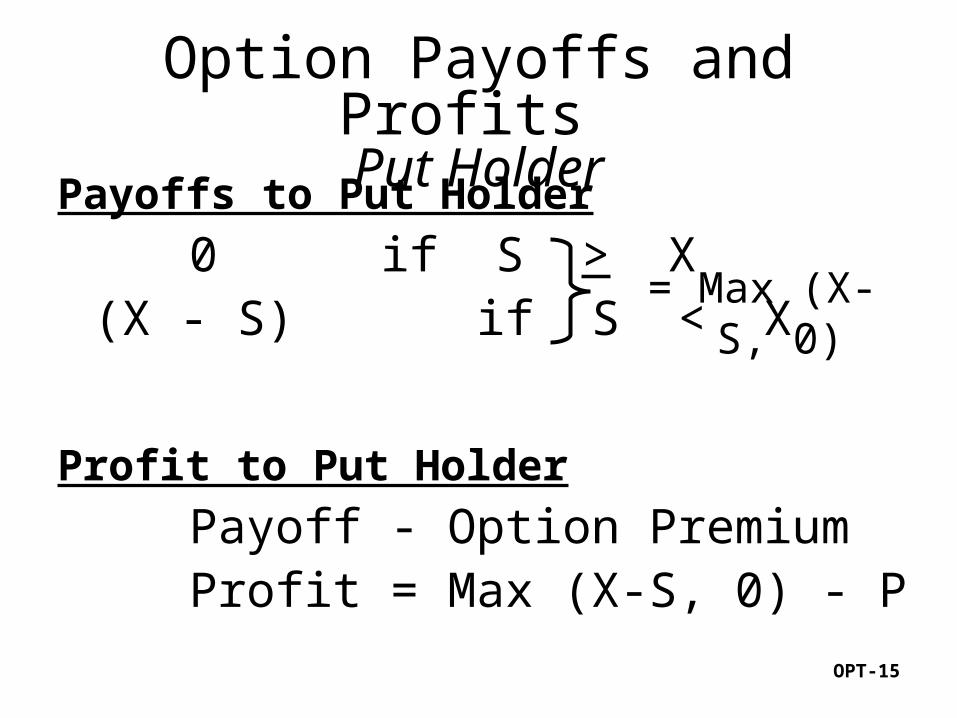

Payoffs to Put Holder

0 if S > X(X - S) if S < X

Profit to Put Holder Payoff - Option PremiumProfit = Max (X-S, 0) - P

Option Payoffs and Profits Put Holder

= Max (X-S, 0)

OPT-16

Payoffs to Put Writer

0 if S > X = -Max (X-S, 0)-(X - S) if S < X = Min (S-X, 0)

Profits to Put Writer

Payoff + Option PremiumProfit = Min (S-X, 0) + P

Option Payoffs and Profits Put Writer

OPT-17

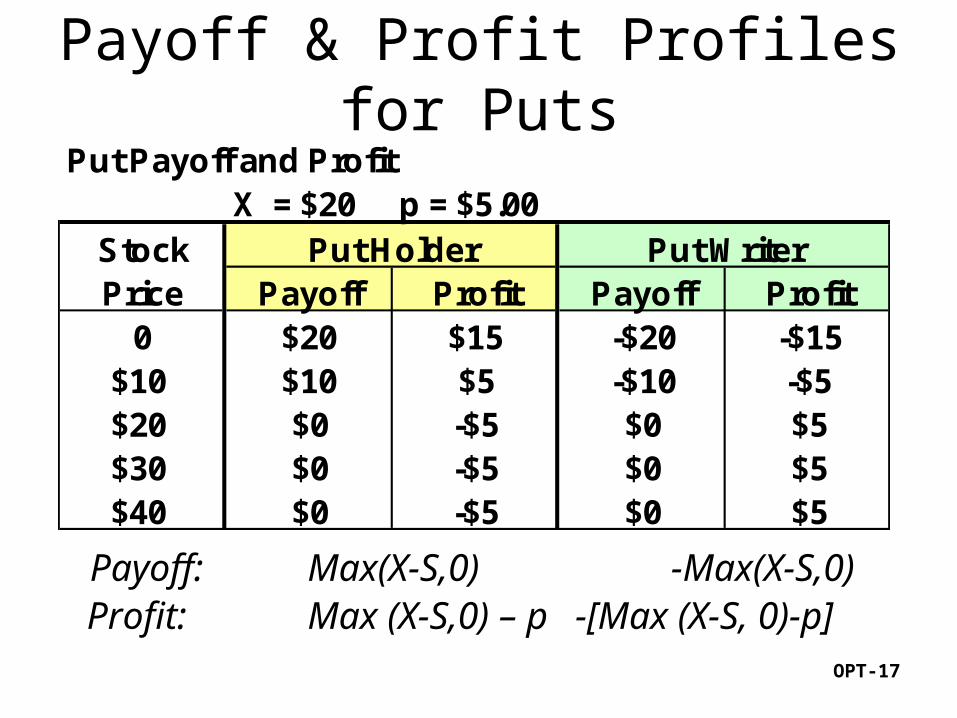

Put Payoff and ProfitX = $20 p = $5.00

StockPrice Payoff Profit Payoff Profit

0 $20 $15 -$20 -$15$10 $10 $5 -$10 -$5$20 $0 -$5 $0 $5$30 $0 -$5 $0 $5$40 $0 -$5 $0 $5

Put Holder Put Writer

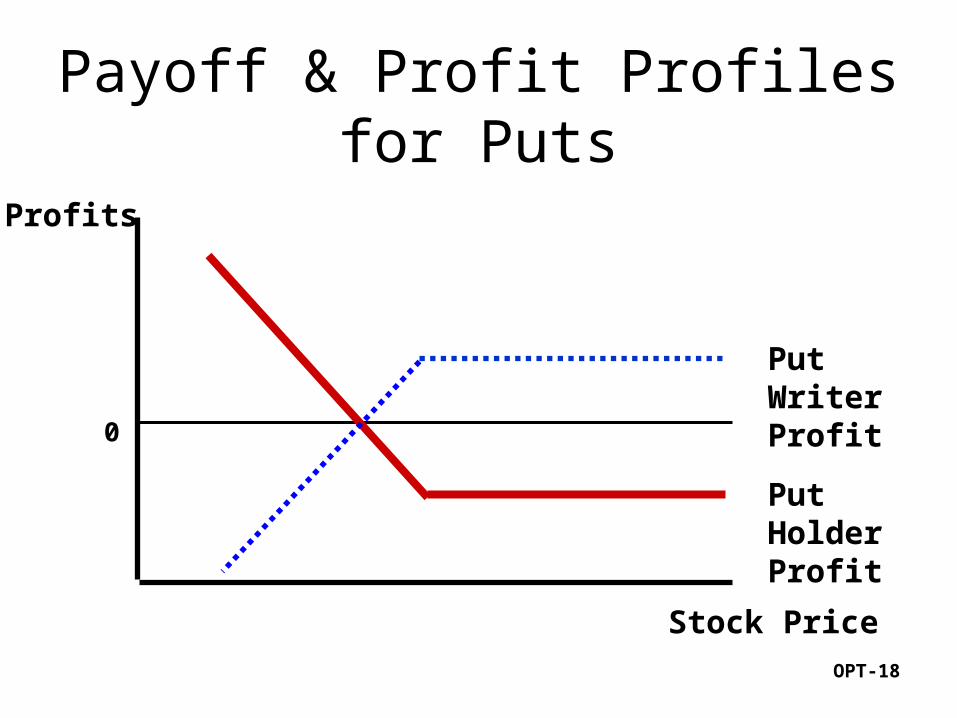

Payoff & Profit Profiles for Puts

Payoff: Max(X-S,0) -Max(X-S,0) Profit: Max (X-S,0) – p -[Max (X-S, 0)-p]

OPT-18

Payoff & Profit Profiles for Puts

0

Profits

Stock Price

Put Writer Profit

Put Holder Profit

OPT-19

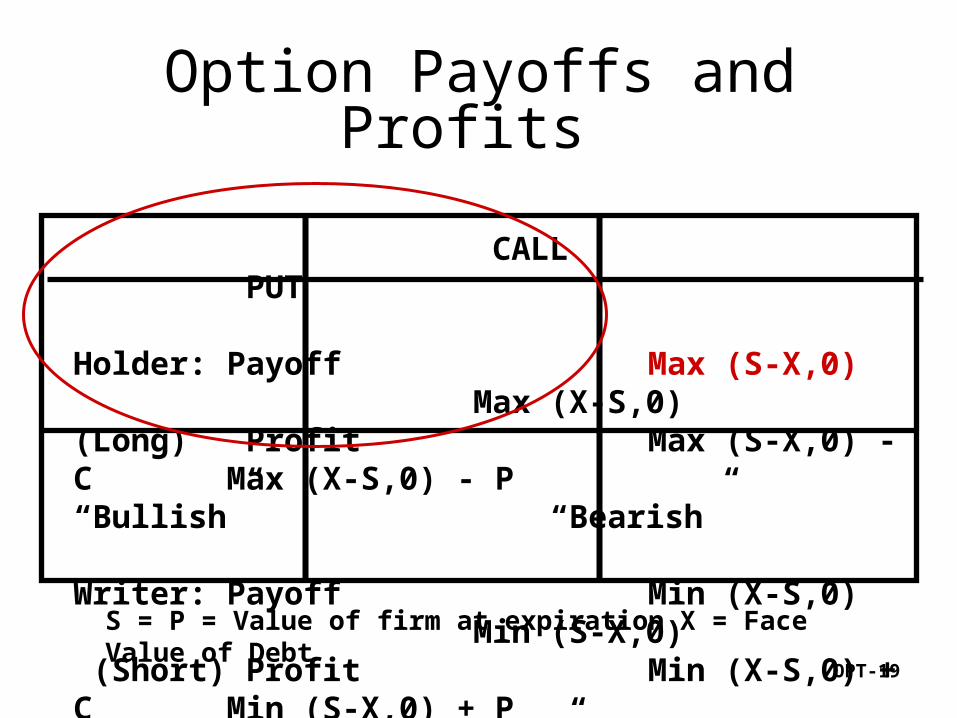

CALL PUT

Holder: Payoff Max (S-X,0) Max (X-S,0)(Long) Profit Max (S-X,0) - C Max (X-S,0) - P

“Bullish” “Bearish”

Writer: Payoff Min (X-S,0) Min (S-X,0) (Short) Profit Min (X-S,0) + C Min (S-X,0) + P

“Bearish” “Bullish”

Option Payoffs and Profits

S = P = Value of firm at expiration X = Face Value of Debt

OPT-20

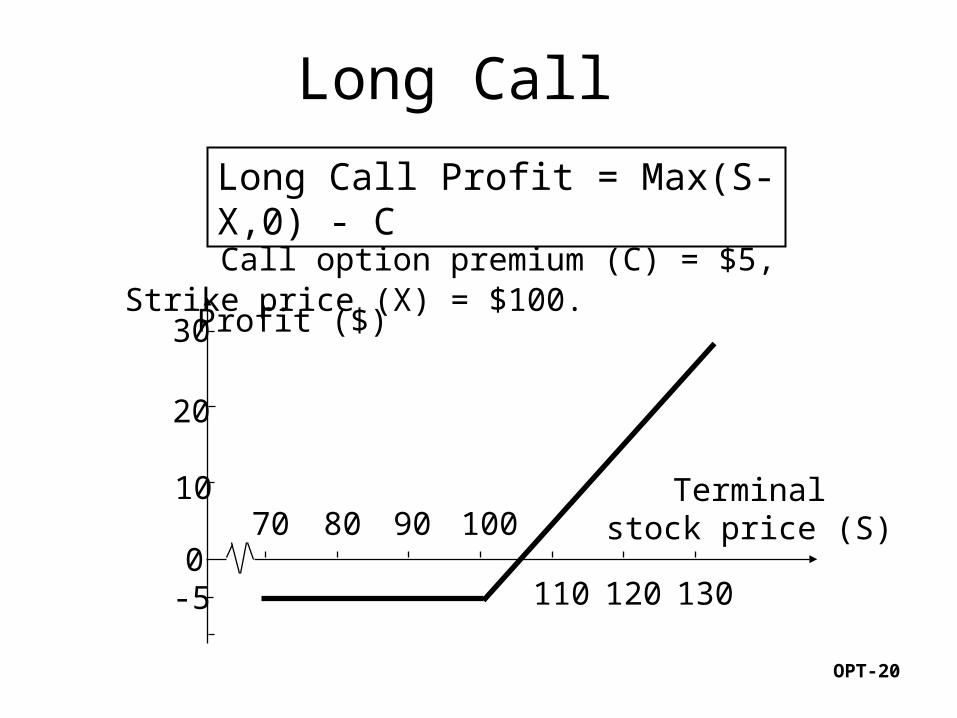

Long Call

Call option premium (C) = $5, Strike price (X) = $100.

30

20

10

0-5

70 80 90 100

110 120 130

Profit ($)

Terminalstock price (S)

Long Call Profit = Max(S-X,0) - C

OPT-21

Properties of Stock Options

OPT-22

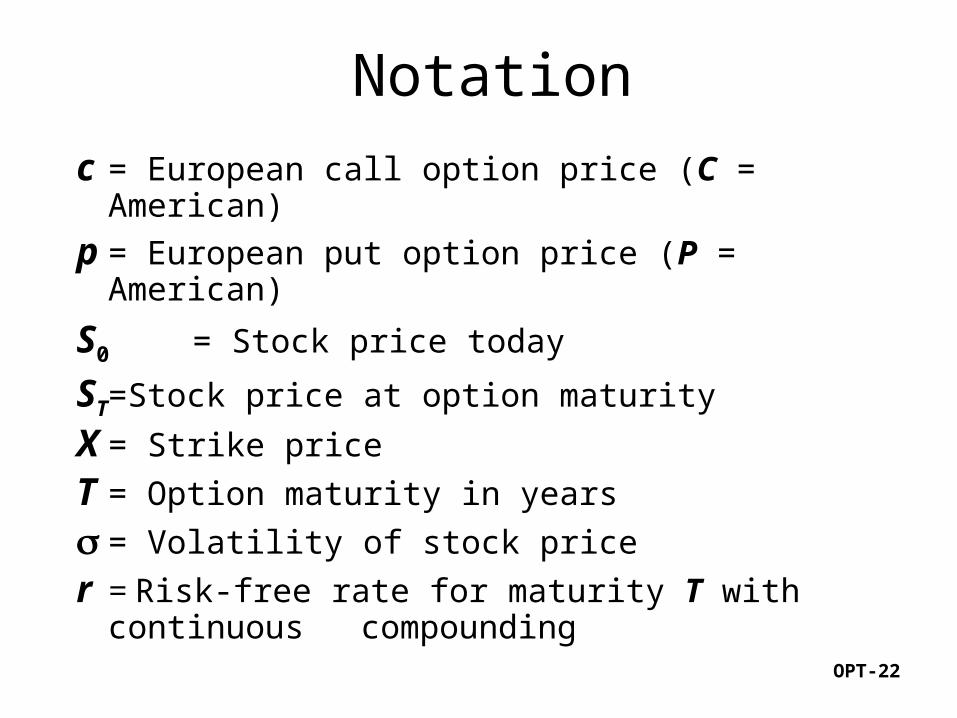

Notation

c = European call option price (C = American)

p = European put option price (P = American)

S0 = Stock price today

ST =Stock price at option maturity

X = Strike price

T = Option maturity in years

= Volatility of stock price

r = Risk-free rate for maturity T with continuous compounding

OPT-23

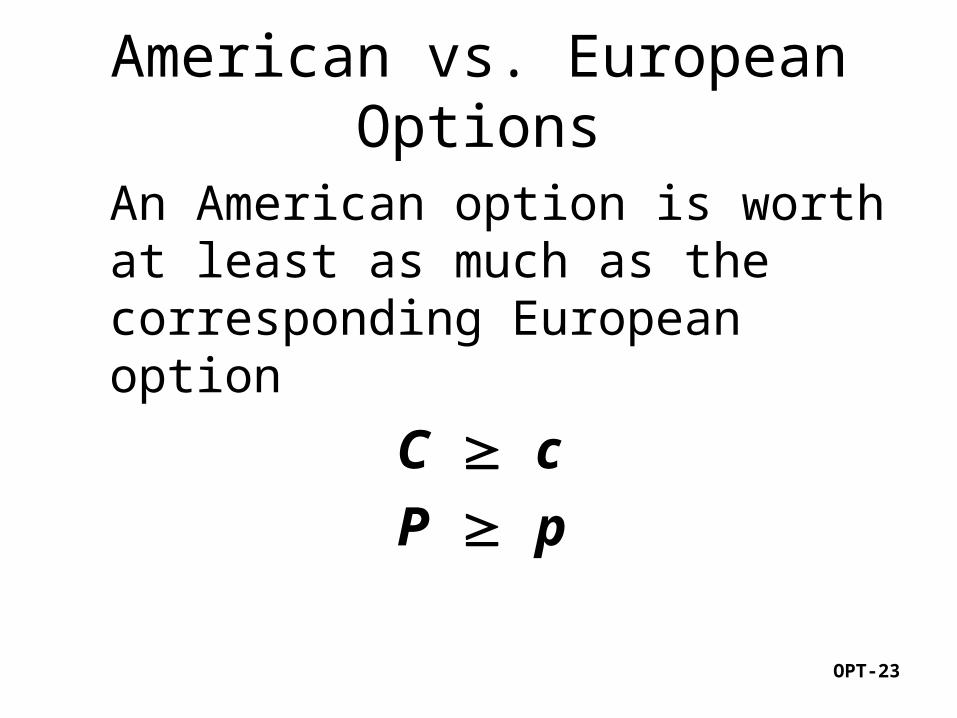

American vs. European Options

An American option is worth at least as much as the corresponding European option

C c

P p

OPT-24

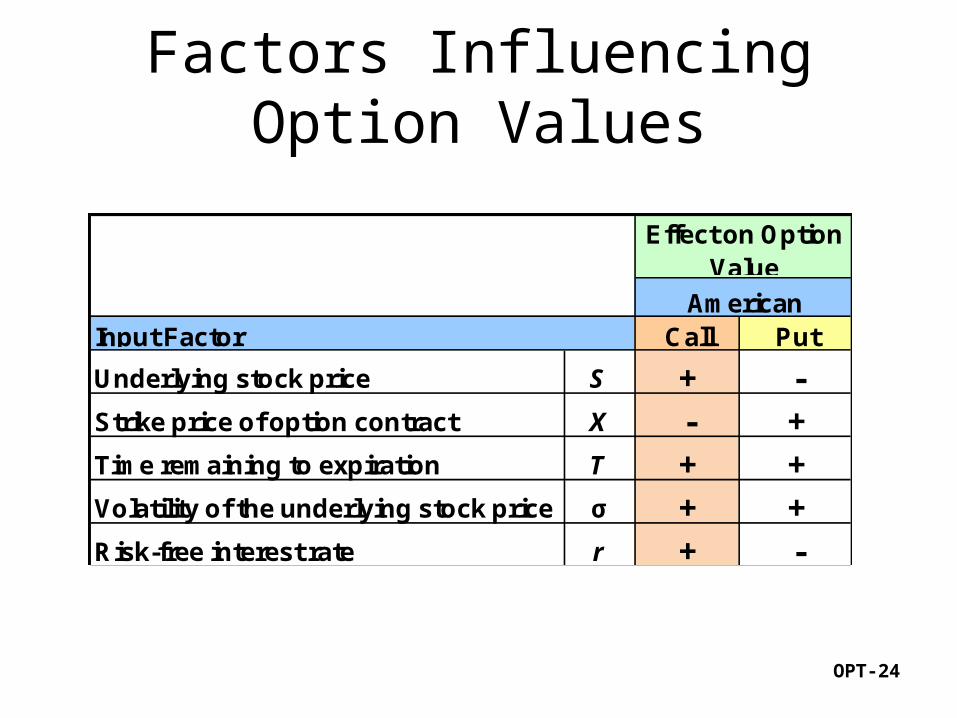

Factors Influencing Option Values

Call Put

Underlying stock price S + -Strike price of option contract X - +Time remaining to expiration T + +Volatility of the underlying stock price σ + +Risk-free interest rate r + -

Input Factor

Effect on Option Value

American

OPT-25

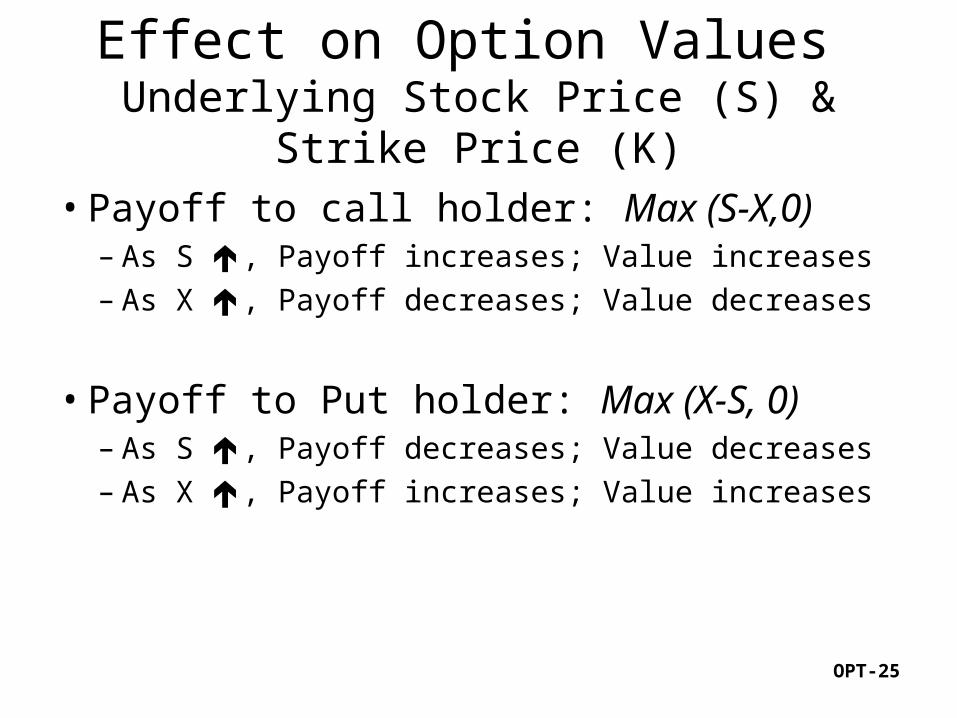

Effect on Option Values Underlying Stock Price (S) & Strike Price (K)

• Payoff to call holder: Max (S-X,0)– As S , Payoff increases; Value increases– As X , Payoff decreases; Value decreases

• Payoff to Put holder: Max (X-S, 0)– As S , Payoff decreases; Value decreases– As X , Payoff increases; Value increases

OPT-26

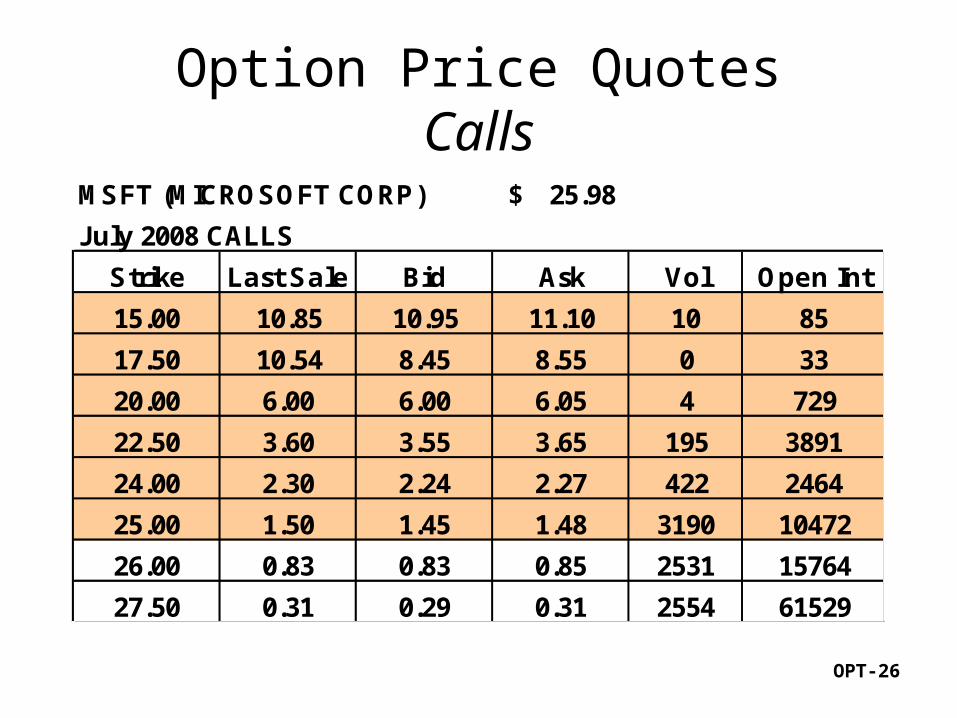

Option Price QuotesCalls

MSFT (MICROSOFT CORP) 25.98$

July 2008 CALLS

Strike Last Sale Bid Ask Vol Open Int

15.00 10.85 10.95 11.10 10 85

17.50 10.54 8.45 8.55 0 33

20.00 6.00 6.00 6.05 4 729

22.50 3.60 3.55 3.65 195 3891

24.00 2.30 2.24 2.27 422 2464

25.00 1.50 1.45 1.48 3190 10472

26.00 0.83 0.83 0.85 2531 15764

27.50 0.31 0.29 0.31 2554 61529

OPT-27

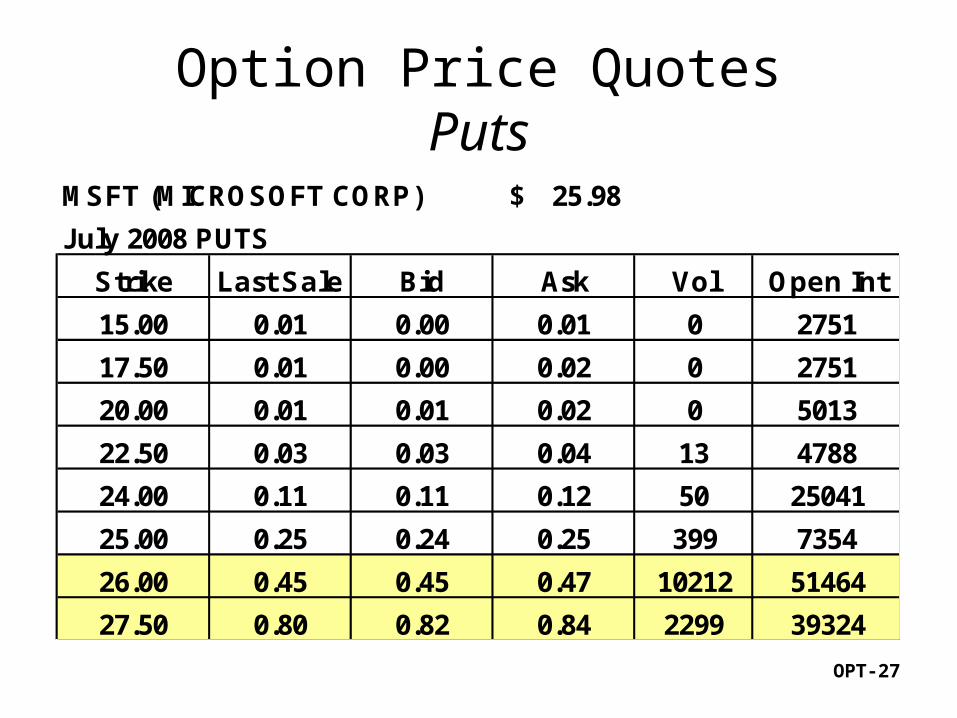

Option Price QuotesPuts

MSFT (MICROSOFT CORP) 25.98$

July 2008 PUTS

Strike Last Sale Bid Ask Vol Open Int

15.00 0.01 0.00 0.01 0 2751

17.50 0.01 0.00 0.02 0 2751

20.00 0.01 0.01 0.02 0 5013

22.50 0.03 0.03 0.04 13 4788

24.00 0.11 0.11 0.12 50 25041

25.00 0.25 0.24 0.25 399 7354

26.00 0.45 0.45 0.47 10212 51464

27.50 0.80 0.82 0.84 2299 39324

OPT-28

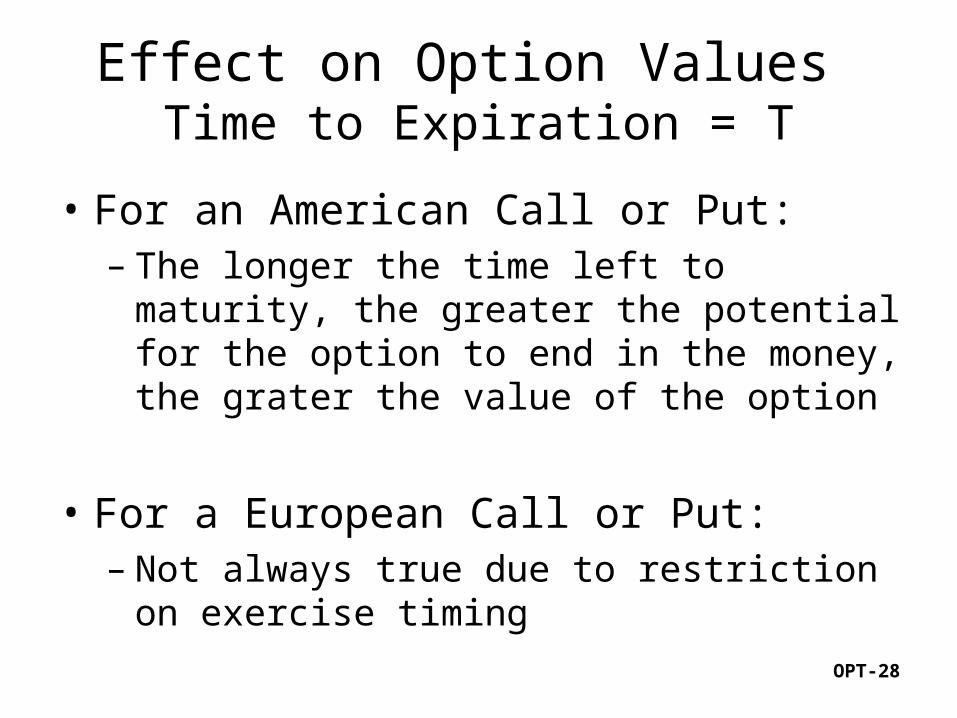

Effect on Option Values Time to Expiration = T

• For an American Call or Put:– The longer the time left to maturity, the

greater the potential for the option to end in the money, the grater the value of the option

• For a European Call or Put:– Not always true due to restriction on exercise

timing

OPT-29

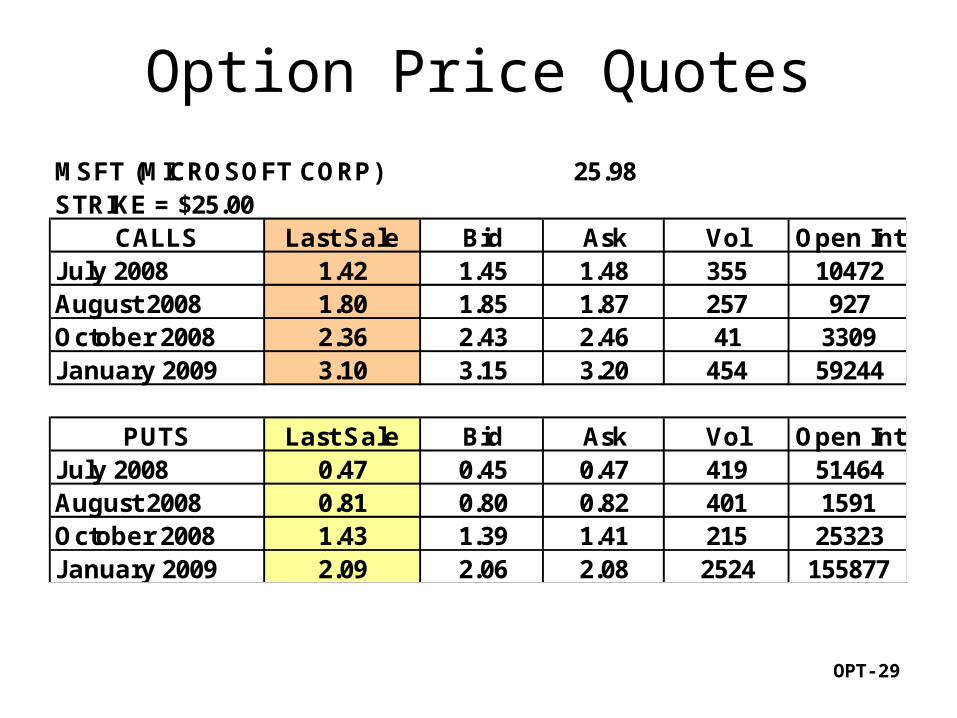

Option Price Quotes

MSFT (MICROSOFT CORP) 25.98STRIKE = $25.00

CALLS Last Sale Bid Ask Vol Open IntJuly 2008 1.42 1.45 1.48 355 10472August 2008 1.80 1.85 1.87 257 927October 2008 2.36 2.43 2.46 41 3309January 2009 3.10 3.15 3.20 454 59244

PUTS Last Sale Bid Ask Vol Open IntJuly 2008 0.47 0.45 0.47 419 51464August 2008 0.81 0.80 0.82 401 1591October 2008 1.43 1.39 1.41 215 25323January 2009 2.09 2.06 2.08 2524 155877

OPT-30

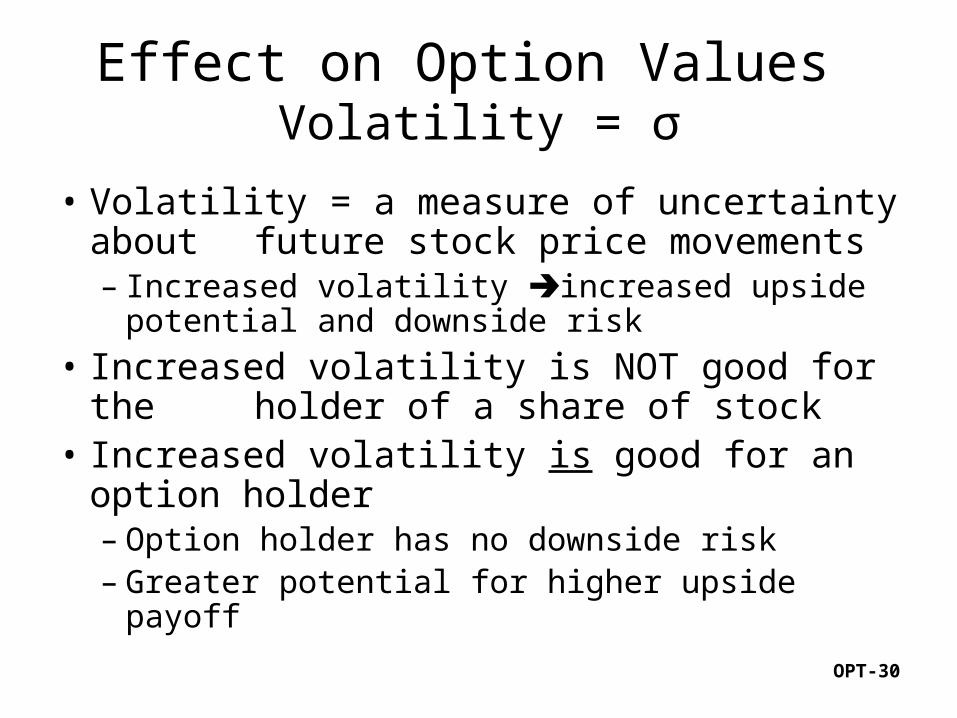

Effect on Option Values Volatility = σ

• Volatility = a measure of uncertainty about future stock price movements

– Increased volatility increased upside potential and downside risk

• Increased volatility is NOT good for the holder of a share of stock

• Increased volatility is good for an option holder– Option holder has no downside risk– Greater potential for higher upside payoff

OPT-31

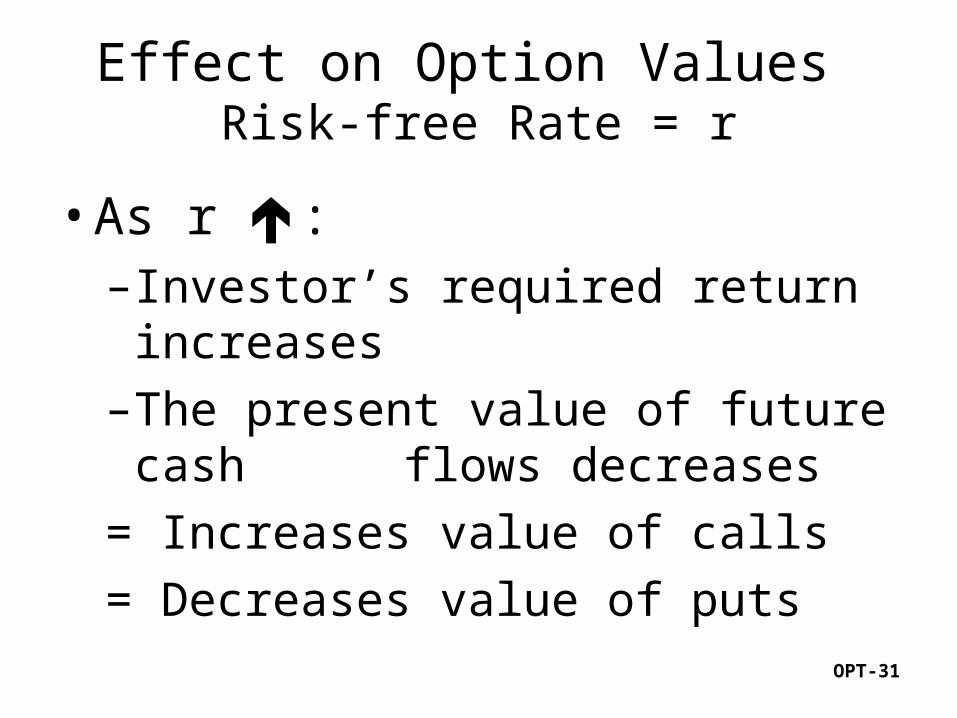

Effect on Option Values Risk-free Rate = r

• As r : –Investor’s required return increases

–The present value of future cash flows decreases

= Increases value of calls

= Decreases value of puts

OPT-32

Valuing Stock Options: The Black-Scholes Model

OPT-33

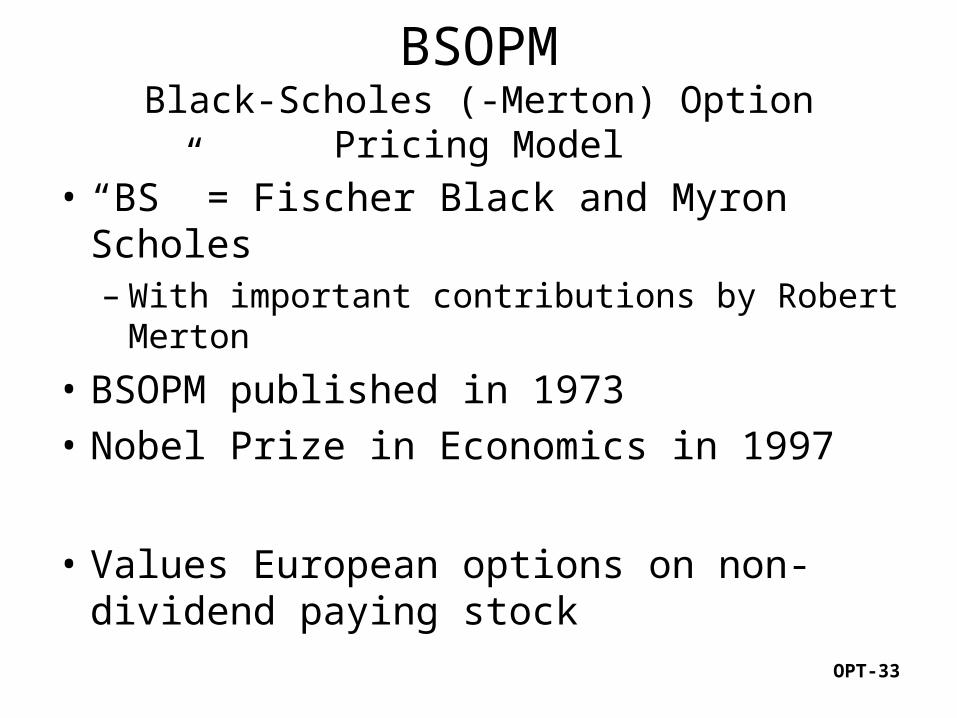

BSOPMBlack-Scholes (-Merton) Option Pricing Model

• “BS” = Fischer Black and Myron Scholes– With important contributions by Robert Merton

• BSOPM published in 1973

• Nobel Prize in Economics in 1997

• Values European options on non-dividend paying stock

OPT-34

Concepts Underlying Black-Scholes

• Option price and stock price depend on same underlying source of uncertainty

• A portfolio consisting of the stock and the option can be formed which eliminates this source of uncertainty (riskless).– The portfolio is instantaneously riskless

– Must instantaneously earn the risk-free rate

OPT-35

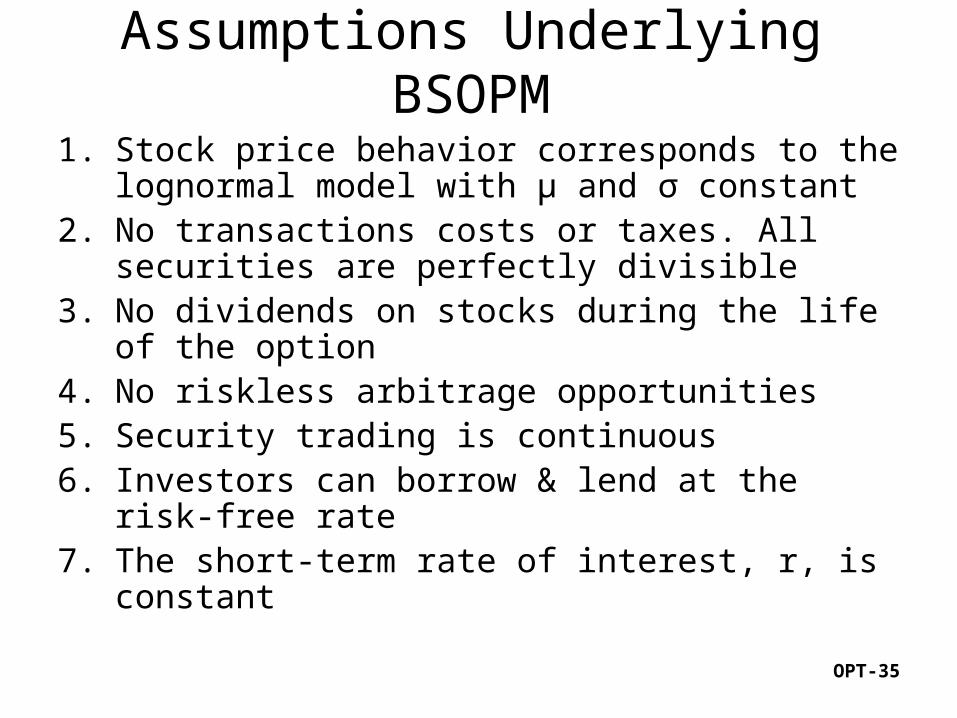

Assumptions Underlying BSOPM

1. Stock price behavior corresponds to the lognormal model with μ and σ constant

2. No transactions costs or taxes. All securities are perfectly divisible

3. No dividends on stocks during the life of the option

4. No riskless arbitrage opportunities5. Security trading is continuous6. Investors can borrow & lend at the risk-free

rate7. The short-term rate of interest, r, is constant

OPT-36

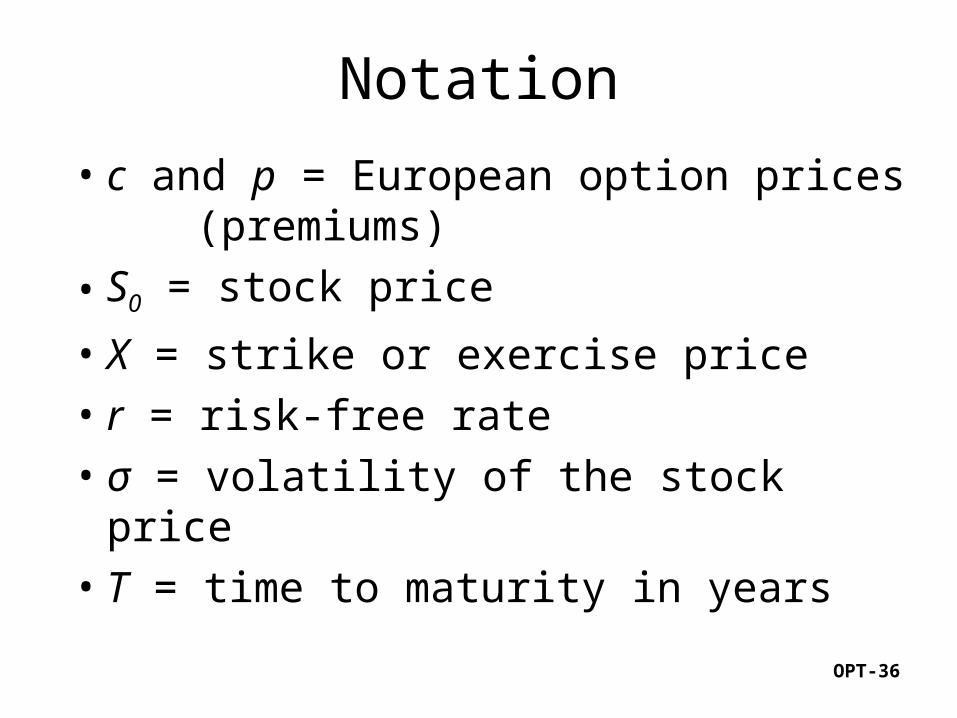

Notation

• c and p = European option prices (premiums)

• S0 = stock price

• X = strike or exercise price• r = risk-free rate• σ = volatility of the stock price• T = time to maturity in years

OPT-37

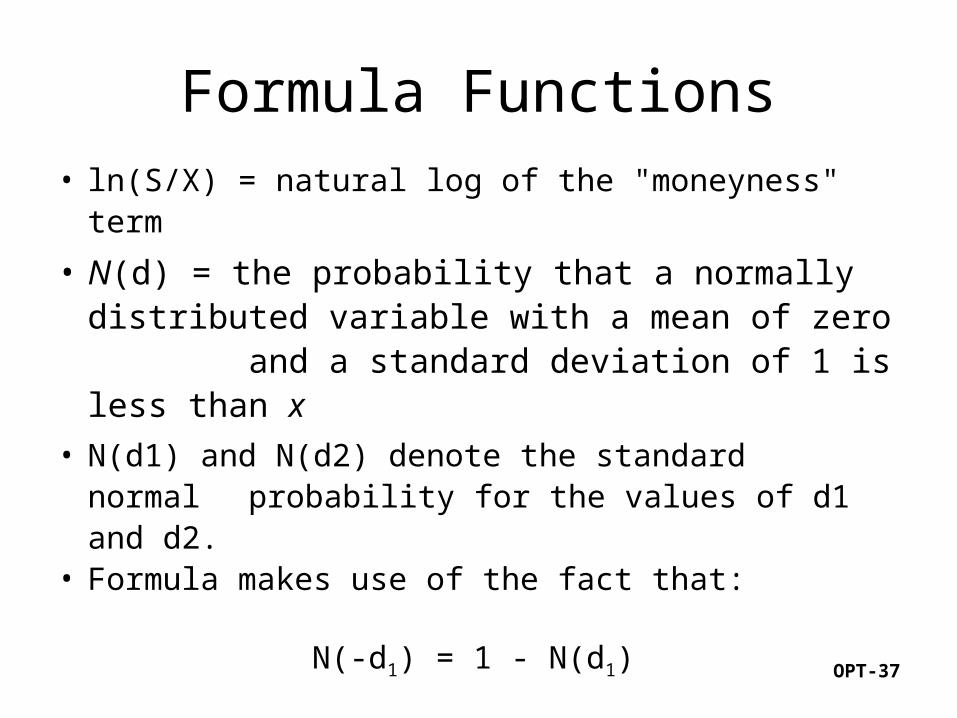

Formula Functions

• ln(S/X) = natural log of the "moneyness" term

• N(d) = the probability that a normally distributed variable with a mean of zero and a standard deviation of 1 is less than x

• N(d1) and N(d2) denote the standard normal probability for the values of d1 and d2.

• Formula makes use of the fact that:

N(-d1) = 1 - N(d1)

OPT-38

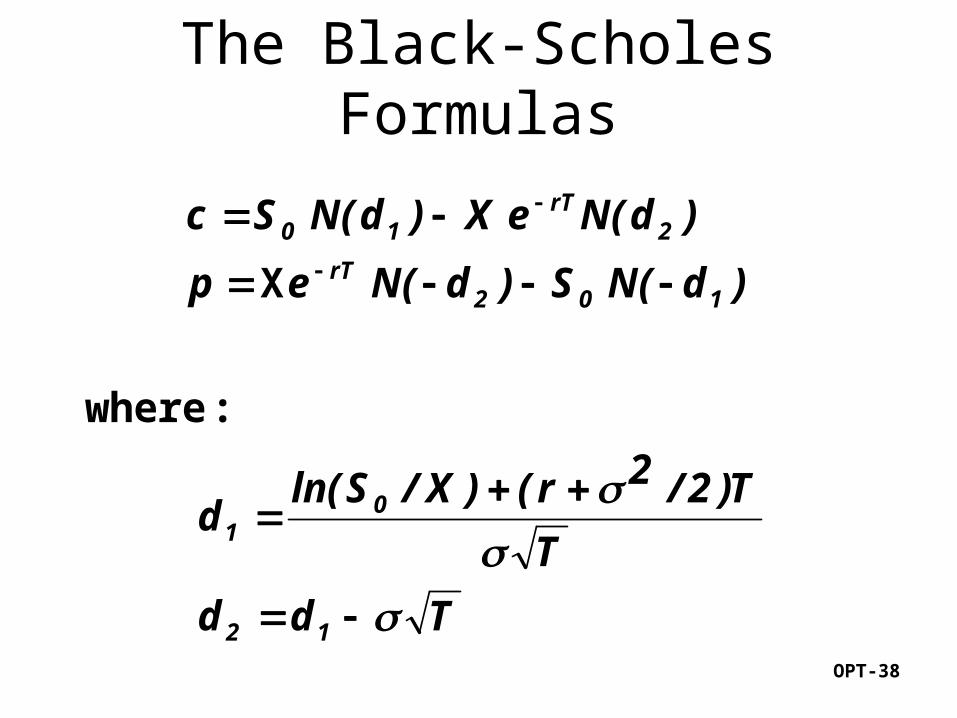

The Black-Scholes Formulas

Tdd

T

T)2/2r()X/Sln(d

)d(NS)d(Nep

)d(NeX)d(NSc

12

01

102rT

2rT

10

: where

X

OPT-39

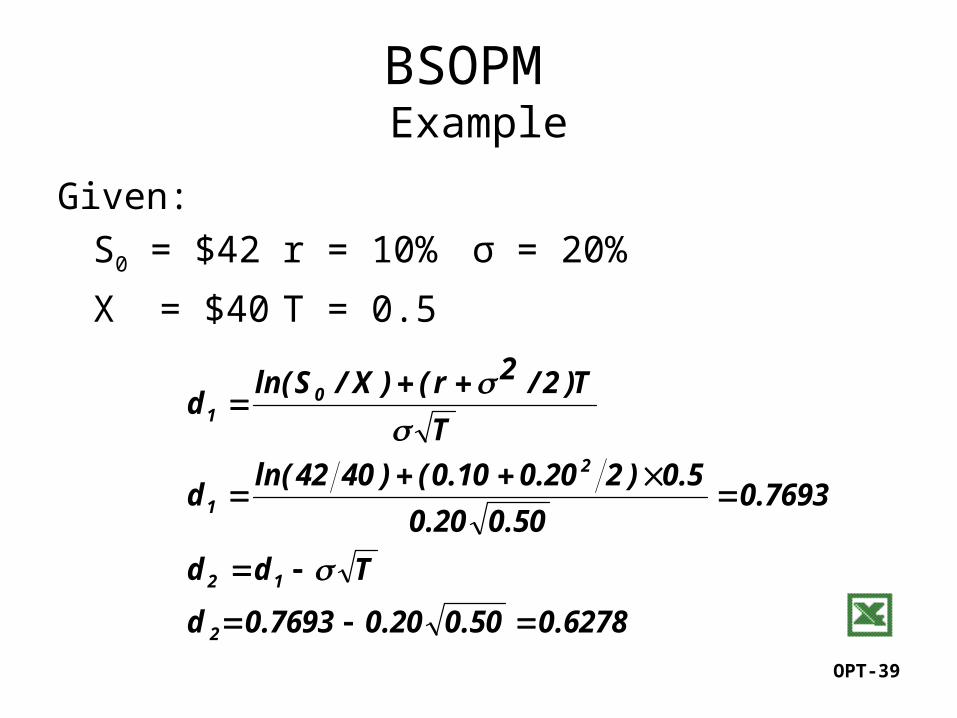

BSOPM Example

Given:

S0 = $42 r = 10% σ = 20%

X = $40 T = 0.5

6278.050.020.07693.0d

Tdd

7693.050.020.0

5.0)220.010.0()4042ln(d

T

T)2/2r()X/Sln(d

2

12

2

1

01

OPT-40

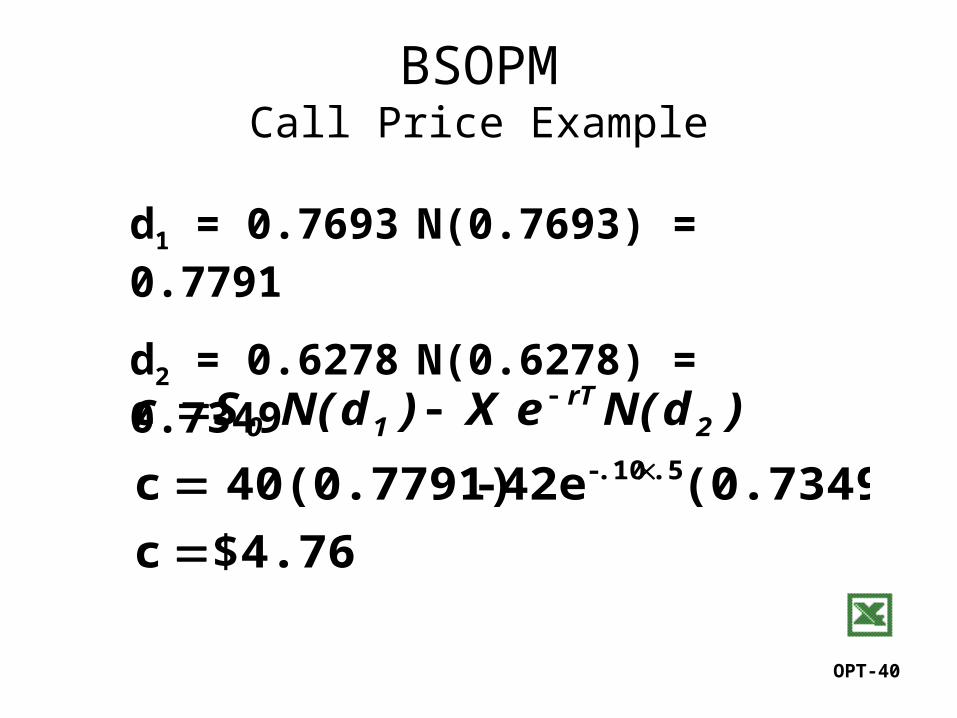

BSOPMCall Price Example

$4.76 c

(0.7349)42e - 40(0.7791) c

.5.10-

)d(NeX)d(NSc 2rT

10

d1 = 0.7693 N(0.7693) = 0.7791

d2 = 0.6278 N(0.6278) = 0.7349

OPT-41

BSOPM in Excel

• N(d1):

=NORMSDIST(d1)Note the “S” in the function“S” denotes “standard normal”~ Φ(0,1)

=NORMDIST() → Normal distributionMean and variance must be specified~N(μ,σ2 )