Embed Size (px)

Citation preview

COST AUDIT HANDBOOK

2nd Edition

By Global CMA

CMA FINAL

PAPER-19

COST & MANAGEMENT AUDIT HANDBOOK

Updated With Companies (Cost Records and Audit) Amendment Rules, 2017

CMA FINAL

PAPER – 19

SYLLABUS - 2016

By Global CMA

Disclaimer :- The booklet has been prepared by team of Global CMA. The objective of the Booklet is to provide teaching material to the students to enable them to obtain knowledge in the subject. All rights reserved. No part of this book may be reproduced, print, stores in retrieval system, or transmitted in any form or by means, electronic, mechanical, photocopying, recording, or otherwise, without prior permission in writing from the GLOBAL CMA and CMA Sandeep Bhatt. Through all the efforts have been made to ensure that there is no error in the book but if you come across any mistake, kindly bring it into the notice of the Global CMA or write directly to us. Neither the author nor the publisher shall be responsible for any mistake that might have crept in the book.

Second Edition : January, 2019

Email Support: [email protected] / [email protected]

Website: www.globalcma.in

PREFACE

“If you want to achieve something extraordinary, you have to go through a lot of pain and sacrifice many things in day to day life” It is indeed a privilege to present before you "COST AUDIT HANDBOOK" - a guidance to facilitate your study of Cost Audit subject in CMA Final to achieve success in your examination and to accomplish to a greater height. This "COST AUDIT HANDBOOK" which is prepared by the Global CMA Team, which aims strengthen the skills, developing in-depth knowledge and confidence of a student in the subject through handbook and this handbook shall be a road map for your all-round success. In the Cost Audit subject, student should gain enough knowledge about various components of Cost Records, Cost Audit, Management Audit, Internal Audit etc. with a view to strike all points, this book is written considering practical approach and is meant to cater to the needs of CMA Students.

Prepared by CMA professionals and

students under my guidance. 167 fully solved problems interspersed

in the text to reinforce concepts and aid comprehension.

Short notes with 100% coverage of

Study Material.

In any project, the first and most important contribution is obviously made by the team of the project. This book reflects the efforts of many people. It would be remiss of me not to acknowledge and thank for the assistance given to me by members of Global CMA team who supported me to made this handbook.

It is my hope and expectation that this book will provide an “Effective Learning Experience” and referenced resource for all CMA Final students in Paper-19 “Cost and Management Audit”. Any further improvement in the contents of this handbook by making corrections and inclusions is a keen to be achieved based on suggestions from the readers for which the author shall be obliged. I wish you great success and glorious future.

CMA Sandeep Bhatt CMA Vibhu Rustagi

(Authors)

SECTIONS

COMPANIES (COST RECORDS & AUDIT) RULES, 2014

BASICS OF COST AUDIT

COST ACCOUNTING/AUDITING STANDARDS - CAS, GACAP

PERFORMANCE ANALYSIS

4

1

2

3

5

MANAGEMENT AUDIT, INTERNAL AUDIT, OPERATIONAL AUDIT

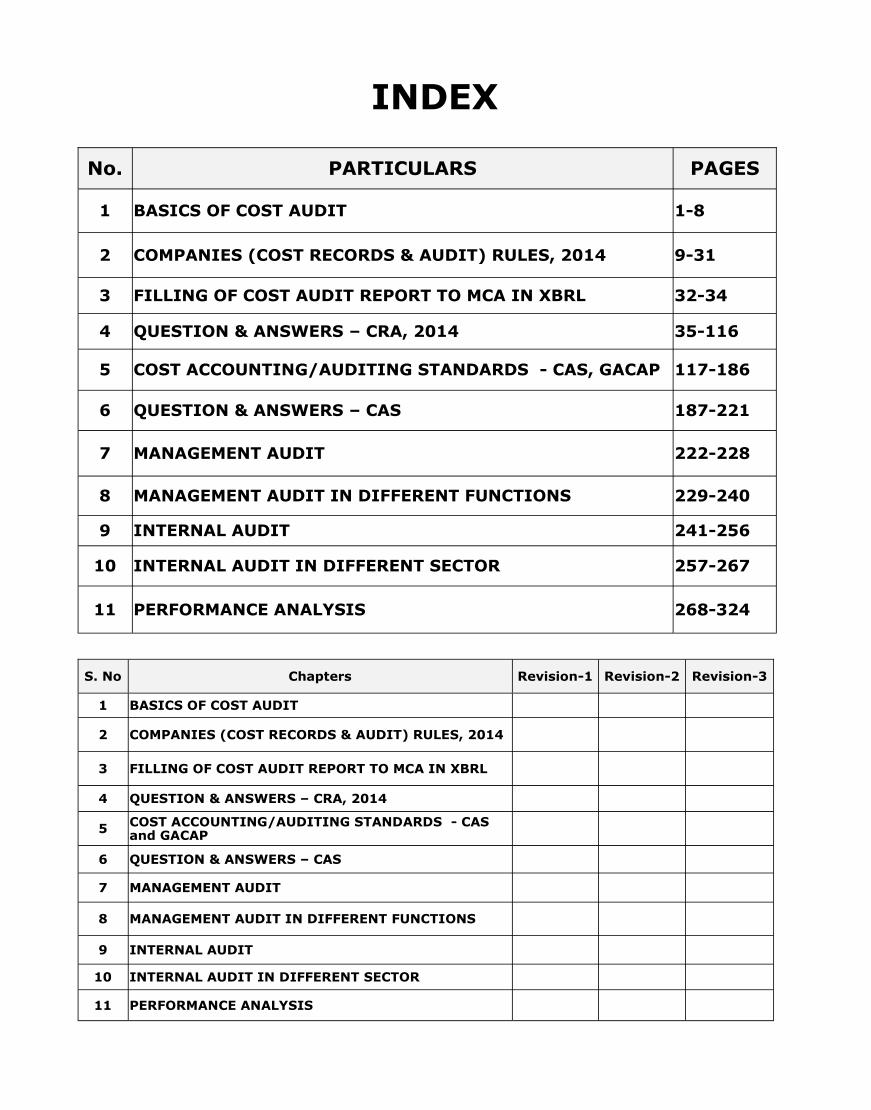

INDEX

No. PARTICULARS PAGES

1 BASICS OF COST AUDIT 1-8

2 COMPANIES (COST RECORDS & AUDIT) RULES, 2014 9-31

3 FILLING OF COST AUDIT REPORT TO MCA IN XBRL 32-34

4 QUESTION & ANSWERS – CRA, 2014 35-116

5 COST ACCOUNTING/AUDITING STANDARDS - CAS, GACAP 117-186

6 QUESTION & ANSWERS – CAS 187-221

7 MANAGEMENT AUDIT 222-228

8 MANAGEMENT AUDIT IN DIFFERENT FUNCTIONS 229-240

9 INTERNAL AUDIT 241-256

10 INTERNAL AUDIT IN DIFFERENT SECTOR 257-267

11 PERFORMANCE ANALYSIS 268-324

S. No Chapters Revision-1 Revision-2 Revision-3

1 BASICS OF COST AUDIT

2 COMPANIES (COST RECORDS & AUDIT) RULES, 2014

3 FILLING OF COST AUDIT REPORT TO MCA IN XBRL

4 QUESTION & ANSWERS – CRA, 2014

5 COST ACCOUNTING/AUDITING STANDARDS - CAS and GACAP

6 QUESTION & ANSWERS – CAS

7 MANAGEMENT AUDIT

8 MANAGEMENT AUDIT IN DIFFERENT FUNCTIONS

9 INTERNAL AUDIT

10 INTERNAL AUDIT IN DIFFERENT SECTOR

11 PERFORMANCE ANALYSIS

9

9

■ Rules, 2014

■ Formats

■ Practical Questions

2

10

10

Domestic or Foreign Company

Regulated

Listed in Table of Rule 3 (Pg.-16)

Overall turnover from all of its products and services ≥ ₹ 35 crores (preceding financial year)

Engaged in Production of goods or providing services

Non-regulated

Rule-3: Application of

Cost Records Companies engaged in the production of the goods or providing

services, mentioned in table of Rule-3 (pg-16), having an overall

turnover from ALL its products and services of ₹ 35 crores or more

during the immediately preceding financial year, shall include Cost

Records for such products or services in their books of accounts.

11

11

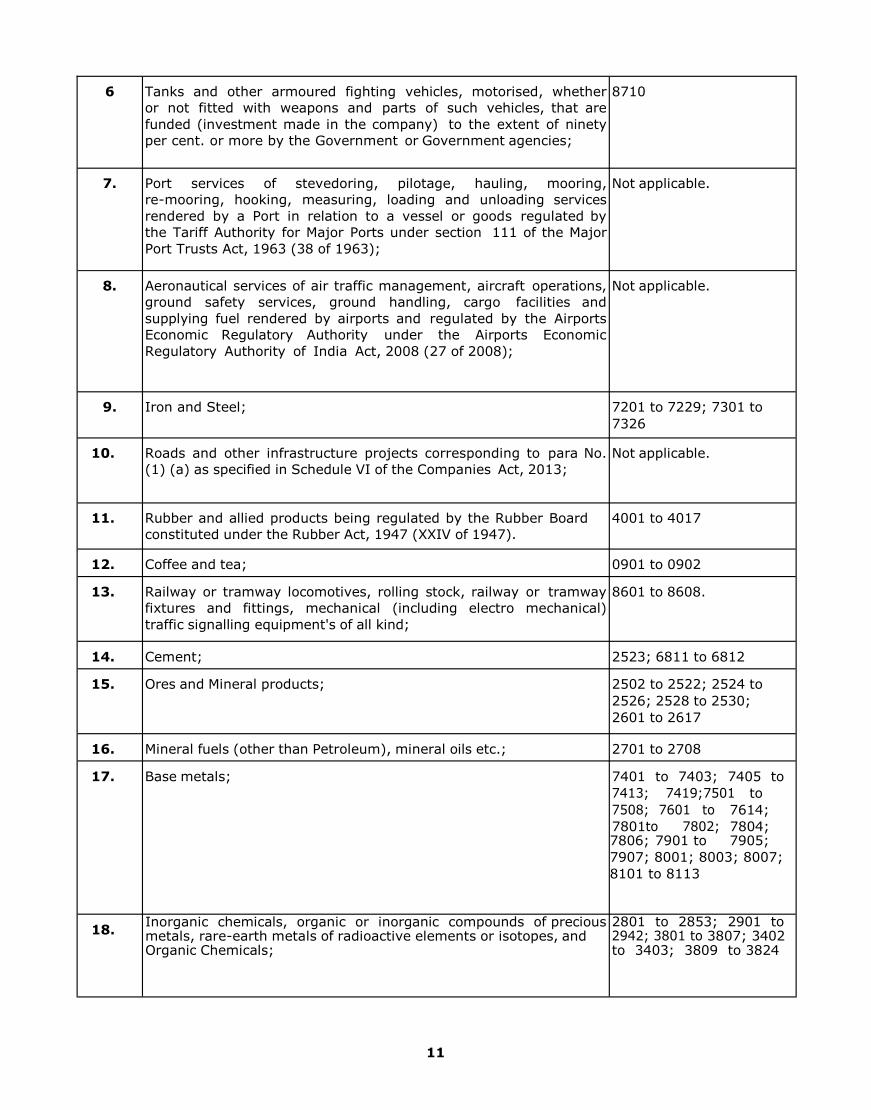

6 Tanks and other armoured fighting vehicles, motorised, whether

or not fitted with weapons and parts of such vehicles, that are

funded (investment made in the company) to the extent of ninety

per cent. or more by the Government or Government agencies;

8710

7. Port services of stevedoring, pilotage, hauling, mooring,

re-mooring, hooking, measuring, loading and unloading services

rendered by a Port in relation to a vessel or goods regulated by

the Tariff Authority for Major Ports under section 111 of the Major

Port Trusts Act, 1963 (38 of 1963);

Not applicable.

8. Aeronautical services of air traffic management, aircraft operations,

ground safety services, ground handling, cargo facilities and

supplying fuel rendered by airports and regulated by the Airports

Economic Regulatory Authority under the Airports Economic

Regulatory Authority of India Act, 2008 (27 of 2008);

Not applicable.

9. Iron and Steel; 7201 to 7229; 7301 to

7326

10. Roads and other infrastructure projects corresponding to para No.

(1) (a) as specified in Schedule VI of the Companies Act, 2013;

Not applicable.

11. Rubber and allied products being regulated by the Rubber Board

constituted under the Rubber Act, 1947 (XXIV of 1947).

4001 to 4017

12. Coffee and tea; 0901 to 0902

13. Railway or tramway locomotives, rolling stock, railway or tramway

fixtures and fittings, mechanical (including electro mechanical)

traffic signalling equipment's of all kind;

8601 to 8608.

14. Cement; 2523; 6811 to 6812

15. Ores and Mineral products; 2502 to 2522; 2524 to

2526; 2528 to 2530;

2601 to 2617

16. Mineral fuels (other than Petroleum), mineral oils etc.; 2701 to 2708

17. Base metals; 7401 to 7403; 7405 to

to

7614;

7801 7804; 7806; 7901 to 7905;

7907; 8001; 8003; 8007;

8101 to 8113

18. Inorganic chemicals, organic or inorganic compounds of precious metals, rare-earth metals of radioactive elements or isotopes, and Organic Chemicals;

2801 to 2853; 2901 to 3807; 3402

to 3403; 3809 to 3824

12

12

Name of Service

Service Code (if applicable)

Unit of Measure

Particulars Services Provided

Captive Consumption

Other Adjustm

ent

Services rendered

Current year

Previous year

S No.

Particular

Current year Previous Year

Amount (Rs.)

Rate Per Unit (Rs.)

Amount (Rs.)

Rate Per Unit (Rs.)

1 Materials Consumed (specify details as per Para 2A)

2 Utilities (specify details as per 2B)

3 Direct Employees Cost

4 Direct Expenses

5 Consumable Stores and Spares

6 Repairs and Maintenance

7 Quality Control Expenses

8 Research and Development Expenses

9 Technical know-how Fee / Royalty

10 Depreciation/ Amortization

11 Other Overheads

12 Industry Specific Operating Expenses( specify details as per Para 2C)

13 Total (1 to 12)

14 Less:- Credits for Recoveries, if any

15 Cost of Services provided (13-14)

16 Cost of Outsourced/ Contractual Services

17 Total Services available

18 Less:- Self/ Captive Consumption

19 Other Adjustments (if any)

20 Cost of Services Sold (17-18+19)

21 Administrative Overheads

22 Selling and Distribution Overheads

23 Cost of Sales before Interest (20+21+22)

24 Finance Cost

25 Cost of Sales (23+24 )

26 Net Sales Realization (Net of Taxes and Duties)

27 Margin [Profit/(Loss) as per Cost Accounts] (26-25)

2. ABRIDGED COST STATEMENT (for each service separately)

13

13

FILLING OF COST AUDIT

REPORT TO MCA (XBRL)

2.2

14

14

PRACTICAL QUESTIONS

2.3

15

15

Question-39 : MENZ (IND) LTD., a manufacturing Company is engaged in manufacturing of multiple products. Some of the products are covered under the Companies (Cost Records and Audit) Rules, 2014 and some are not. Part-A, Para 4 of the Annexure to the Cost Audit Report (product/Service Details for the company as a whole) requires Net Operational Revenue to be reported for each CTA Heading for both the current year and the previous year. Can the Net Operational Revenue of all the Products that are not covered under the Rules be reported in this Para as a single line item? Solution: Part-A, Para 4 of the Annexure to the Cost Audit Report of the Companies (Cost Records and Audit) Rules, 2014 require reporting of Net Operational Revenue of every CTA Heading separately comprised in the Total Operational Revenue as per Financial Accounts. Hence, the company would be required to report Net Revenue of every CTA Heading irrespective of whether the same is covered under maintenance of cost accounting records and cost audit or not. In case some of the Products are under the same CTA Heading but having different units of measurement (UOM), then Net Revenue is to be reported for separate UOMs. It may be noted that the number of quantitative details and abridged cost statements will have to be provided for each unique combination of CTA Heading and UOM of the Products which are covered under cost audit. If the company is engaged in manufacturing of products as well as providing of services and/or trading, such services which are covered under the Companies (Cost Records and Audit) Rules, 2014 will be required to be reported separately according to the definition provided in the Rules classified under different types of services within the same class of service. It may be noted that the number of quantitative details and abridged cost statements will have to be provided for each classification of service covered under cost audit. Other services that are not covered under the Rules and Revenue from Trading Activity may be reported under suitable heads denoting the service/activity. The New Taxonomy has introduced a separate line item in this para to report "Other Operating Incomes" which will form part of the Total Operating Revenue. Question-40 : The Companies Act, 2013 has introduced provision regarding rotation of Auditors. Is the provision of rotation of Auditors applicable to Cost Auditors also? Solution: The provisions for maintenance of cost accounting records and cost audit are governed by Section 148 of the Companies Act, 2013. The provisions of Section 148 clearly states that no person appointed under Section 139 as an auditor of the company shall be appointed for conducting audit of Cost Records of the company. Section 148 also provides that qualifications, disqualifications, rights, duties and obligations applicable to auditors (financial) shall apply to a cost auditor appointed under this section. The eligibility, qualifications and disqualifications are provided in Section 141 of the Act and powers and duties are provided in Section 143. Section 143 (14) specifically states that the provisions of Section 143 shall mutatis mutandis apply to a cost auditor appointed under Section 148. There are no other provisions governing the appointment of a cost auditor. Section 139 (3) of the Act, applicable to appointment of auditors (financial), and Rule 6 of Companies (Audit and Auditors) Rules, 2014 deals with the provision of rotation of auditors and these provisions are applicable only to appointment of auditors (Financial). The Act does not provide for rotation in case of appointment of cost auditors and the same is not applicable to a cost auditor. It may, however, be noted that though there is no statutory provision for rotation of cost auditors, individual companies may do so as a part of their policy, as is the practice with Public Sector Undertakings.

16

16

Question-51 : Whether each and every transactions with Related Parties is to be disclosed under Para D-5 of Annexure to the Cost Audit Report? Solution: Details of related Party Transaction are required to be provided in respect of each Related Party and each Product/Service for the year as a whole and not transaction-wise. Question-52 : The Companies (Cost Records and Audit) Rules, 2014 requires submission of a single cost audit report at company level. What is the procedure of certifying and submission of cost audit report of a company where more than one cost auditor is appointed? Solution: In case of a company having more than one cost auditor, it would be necessary for the company to appoint/designate one cost auditor as the lead cost auditor for consolidation of the report. The individual cost auditors appointed for specific units/products would be required to audit and provide Para numbers A-4, B-1, B-2, B-2A, B-2B, B-2C, C-1, C-2, C-2A, C-2B, C-2C (as applicable), D-1 in respect of the products/services coming under the purview of their respective audits. The individual auditors would also be required to submit to the Board of Directors the individual cost audit report as per Form of the Cost Audit Report given in CRA-3. Question-53 : As a Cost Auditor of a company how would you dealt with treat the head office expenses of a company? Solution: A company may have a number of factories w ith a head office. In a multi -locational/ multi-product company, there are common activities carried out at Head Office like purchase, inventory management, finance, personnel, R & D, Quality Assurance, security etc. These activities sometimes, are centralized at one place i.e. Head Office for business convenience and scale of economy and booked as head office expenses along with other activities like secretarial, project, treasury, investment, trading, etc. They do not form part of the Administration overheads. For example: Industrial Relation Department; Material management; Operation/ production Planning Department; Human Resources, System Design & Development Set Up and the like are production related activities. Nomenclature or place where the activity takes place is not relevant. In such a situation, activities at Head Office/Corporate level are to be clearly demarcated and segregated so as to distinguish activities that contribute clearly and directly to production activities from general management and administration activities. It is necessary to properly analyze the expenses of such activities of head office and allocate these to plants/products on rational basis. Question-54 : A company is engaged in manufacturing of multiple products. Some of the products are covered under the Companies (Cost Records and Audit) Rules, 2014 and some are not. Part-A, Para 4 of the Annexure to the Cost Audit Report (Product/Service Details for the company as a whole) requires Net Operational Revenue to be reported for each CTA Heading for both the current year and the previous year. Can the Net Operational Revenue of all the Products that are not covered under the Rules be reported in this Para as a single line item? Solution: Part-A, Para 4 of the Annexure to the Cost Audit Report of Companies (Cost Records and Audit) Rules, 2014 require reporting of Net Operational Revenue of every CTA Heading separately comprised in the Total Operational Revenue as per Financial Accounts. Hence, the company would be required to report Net Revenue of every CTA Heading irrespective of whether the same is covered under maintenance of cost accounting records and cost audit or not. In case some of the Products are under the same CTA Heading but having different units of measurement (UOM), then Net Revenue is to be reported for separate UOMs. It may be noted that the number of quantitative details and abridged cost statements will have to be provided for each unique combination of CTA Heading and UOM of the Products which are covered under cost audit. If the company is engaged in manufacturing of products as well as providing of services and/or trading, such services which are covered under the Companies (Cost Records and Audit) Rules, 2014 will be required to be reported separately according to the definition provided in the Rules classified under different types of services within the same class of service. It may be noted that the number of quantitative details and abridged cost statements will have to be provided for each classification of service covered under cost audit.

17

17

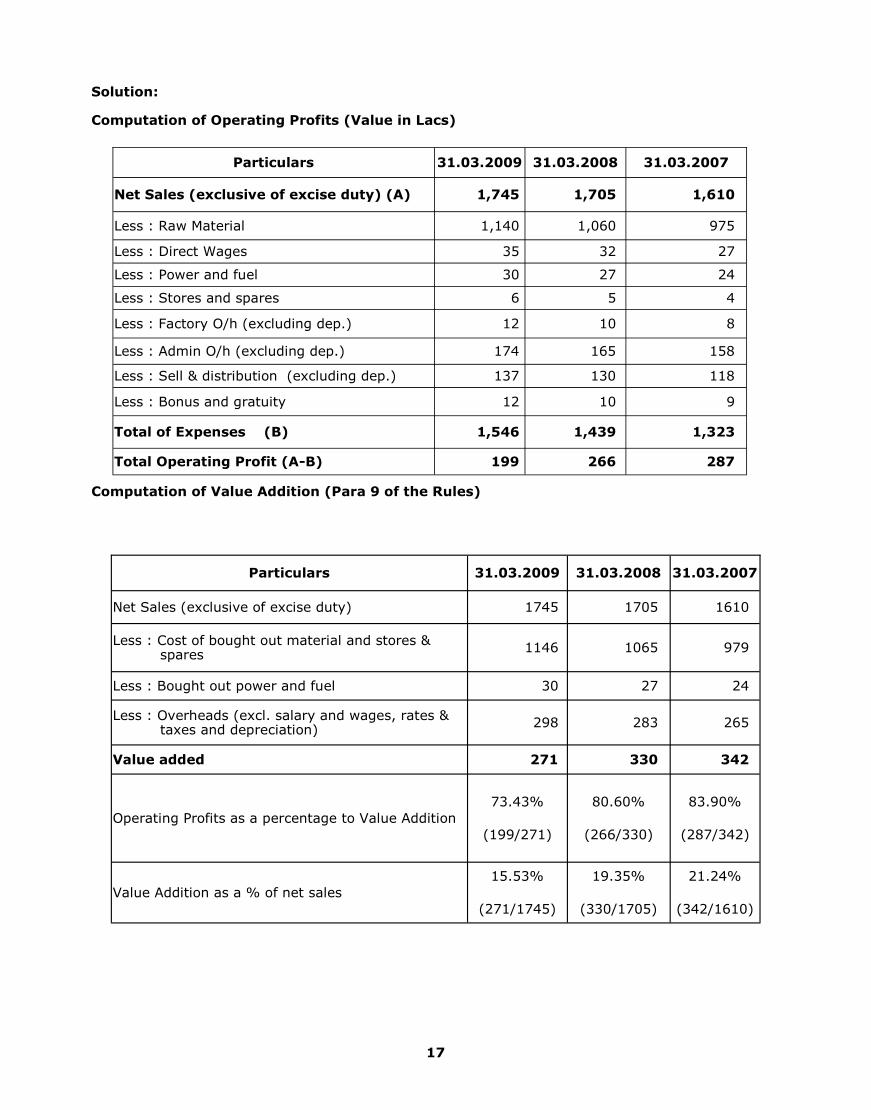

Solution: Computation of Operating Profits (Value in Lacs)

Computation of Value Addition (Para 9 of the Rules)

Particulars 31.03.2009 31.03.2008 31.03.2007

Net Sales (exclusive of excise duty) (A) 1,745 1,705 1,610

Less : Raw Material 1,140 1,060 975

Less : Direct Wages 35 32 27

Less : Power and fuel 30 27 24

Less : Stores and spares 6 5 4

Less : Factory O/h (excluding dep.) 12 10 8

Less : Admin O/h (excluding dep.) 174 165 158

Less : Sell & distribution (excluding dep.) 137 130 118

Less : Bonus and gratuity 12 10 9

Total of Expenses (B) 1,546 1,439 1,323

Total Operating Profit (A-B) 199 266 287

Particulars 31.03.2009 31.03.2008 31.03.2007

Net Sales (exclusive of excise duty) 1745 1705 1610

Less : Cost of bought out material and stores & spares

1146 1065 979

Less : Bought out power and fuel 30 27 24

Less : Overheads (excl. salary and wages, rates & taxes and depreciation)

298 283 265

Value added 271 330 342

Operating Profits as a percentage to Value Addition

73.43%

(199/271)

80.60%

(266/330)

83.90%

(287/342)

Value Addition as a % of net sales

15.53%

(271/1745)

19.35%

(330/1705)

21.24%

(342/1610)

18

18

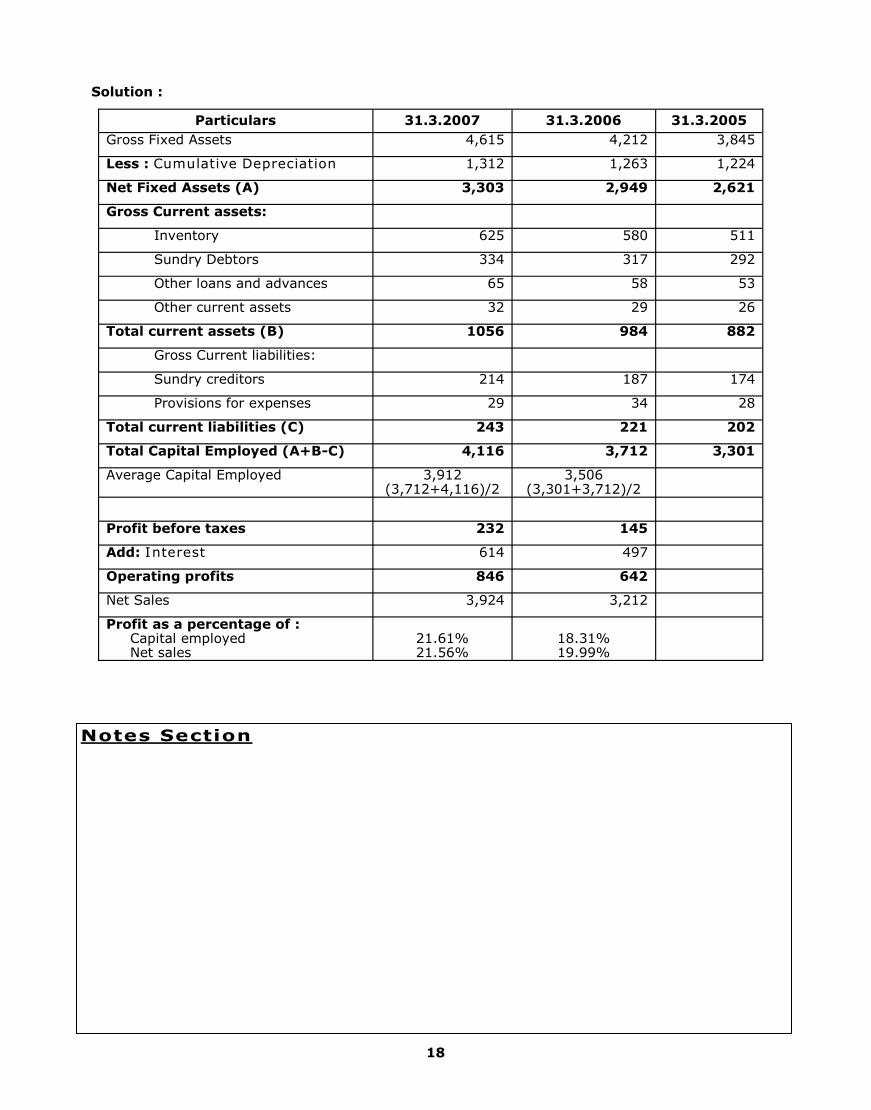

Solution :

Particulars 31.3.2007 31.3.2006 31.3.2005

Gross Fixed Assets 4,615 4,212 3,845

Less : Cumulative Depreciation 1,312 1,263 1,224

Net Fixed Assets (A) 3,303 2,949 2,621

Gross Current assets:

Inventory 625 580 511

Sundry Debtors 334 317 292

Other loans and advances 65 58 53

Other current assets 32 29 26

Total current assets (B) 1056 984 882

Gross Current liabilities:

Sundry creditors 214 187 174

Provisions for expenses 29 34 28

Total current liabilities (C) 243 221 202

Total Capital Employed (A+B-C) 4,116 3,712 3,301

Average Capital Employed 3,912 (3,712+4,116)/2

3,506 (3,301+3,712)/2

Profit before taxes 232 145

Add: Interest 614 497

Operating profits 846 642

Net Sales 3,924 3,212

Profit as a percentage of : Capital employed Net sales

21.61% 21.56%

18.31% 19.99%

19

19

Profit and Loss Account for the year ended March 31, 2014 You are required to compute the following figures/ratios as stipulated in PARA-9 of the Annexure to Cost Audit Report under Companies (Cost Audit Report) Rules 2011 for the year ended March 31, 2013 and 2014. a. Capital Employed b. Net Worth c. Net Sales d. PBT to Capital Employed e. PBT to Net Worth f. PBT to Net Sales g. Current Assets to Current liabilities h. Debt-Equity Ratio

Particulars 2014 2013

(Amount in ₹ lakhs)

Sales (including Excise duty) 14,520 12,255

Expenditure:

Material Consumed 5,670 4,504

Excise duty on dispatches 3,345 3,426

Employee Costs 825 690

Other Manufacturing expenses 550 480

Selling and distribution expenses 1,551 1,401

Administration expenses 250 230

Interest on:

Term Loans 346 201

Debentures 120 120

Others 80 100

Depreciation 302 200

Difference in stock 826 268

Total Expenditures 13865 11620

Profit Before Taxation (PBT) 655 635

Provisions for Taxation 100 230

Profit After Taxation (PAT) Transferred to Balance Sheet

555 405

20

20

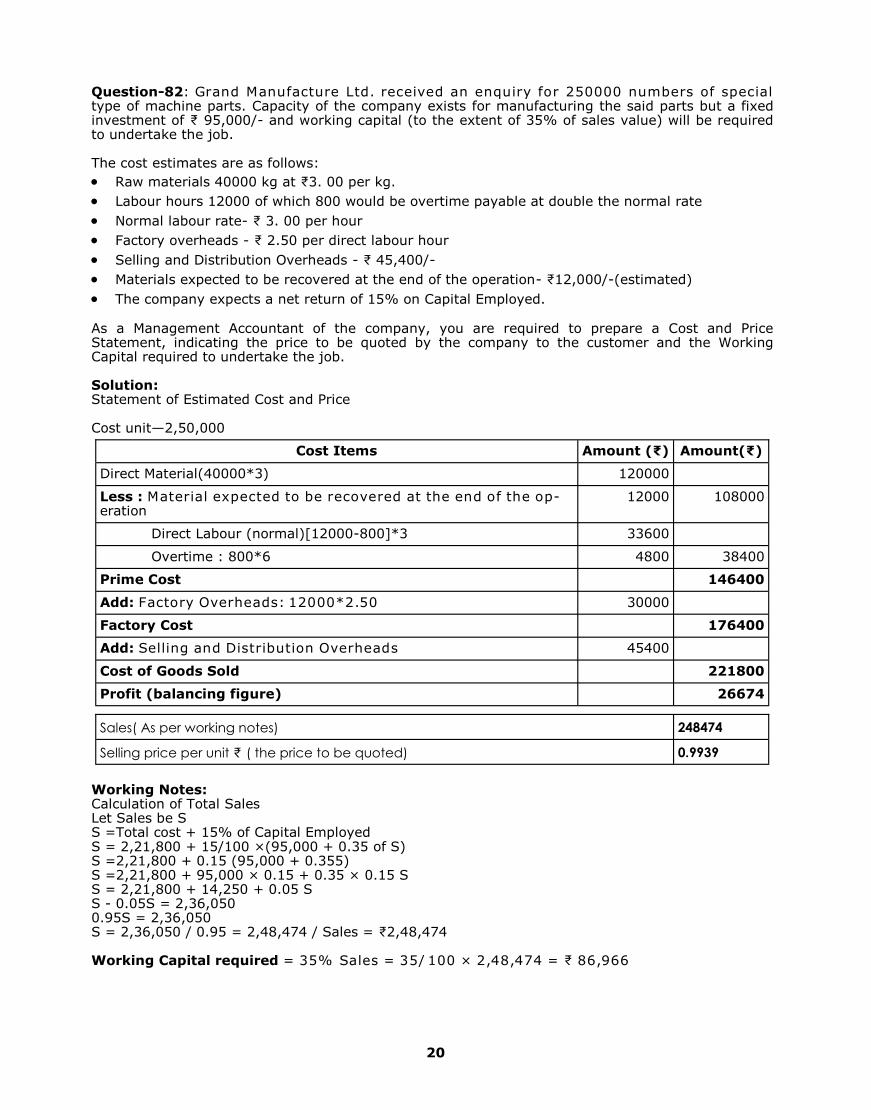

Question-82: Grand Manufacture Ltd. received an enquiry for 250000 numbers of special type of machine parts. Capacity of the company exists for manufacturing the said parts but a fixed investment of ₹ 95,000/- and working capital (to the extent of 35% of sales value) will be required to undertake the job. The cost estimates are as follows:

Raw materials 40000 kg at ₹3. 00 per kg.

Labour hours 12000 of which 800 would be overtime payable at double the normal rate

Normal labour rate- ₹ 3. 00 per hour

Factory overheads - ₹ 2.50 per direct labour hour

Selling and Distribution Overheads - ₹ 45,400/-

Materials expected to be recovered at the end of the operation- ₹12,000/-(estimated)

The company expects a net return of 15% on Capital Employed. As a Management Accountant of the company, you are required to prepare a Cost and Price Statement, indicating the price to be quoted by the company to the customer and the Working Capital required to undertake the job. Solution: Statement of Estimated Cost and Price Cost unit—2,50,000

Working Notes: Calculation of Total Sales Let Sales be S S =Total cost + 15% of Capital Employed S = 2,21,800 + 15/100 ×(95,000 + 0.35 of S) S =2,21,800 + 0.15 (95,000 + 0.355) S =2,21,800 + 95,000 × 0.15 + 0.35 × 0.15 S S = 2,21,800 + 14,250 + 0.05 S S - 0.05S = 2,36,050 0.95S = 2,36,050 S = 2,36,050 / 0.95 = 2,48,474 / Sales = ₹2,48,474 Working Capital required = 35% Sales = 35/ 100 × 2,48,474 = ₹ 86,966

Cost Items Amount (₹) Amount(₹)

Direct Material(40000*3) 120000

Less : Material expected to be recovered at the end of the op-eration

12000 108000

Direct Labour (normal)[12000-800]*3 33600

Overtime : 800*6 4800 38400

Prime Cost 146400

Add: Factory Overheads: 12000*2.50 30000

Factory Cost 176400

Add: Selling and Distribution Overheads 45400

Cost of Goods Sold 221800

Profit (balancing figure) 26674

Sales( As per working notes) 248474

Selling price per unit ₹ ( the price to be quoted) 0.9939

21

21

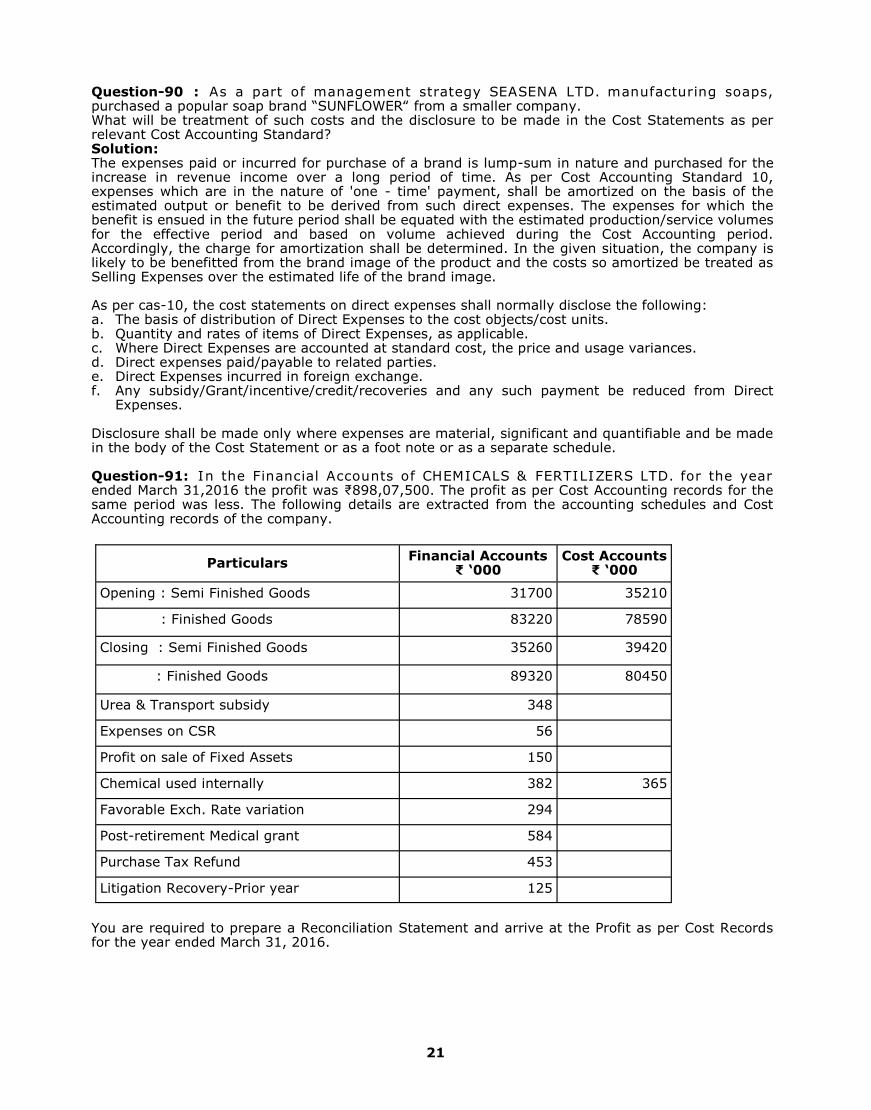

Question-90 : As a part of management strategy SEASENA LTD. manufacturing soaps, purchased a popular soap brand “SUNFLOWER‟ from a smaller company. What will be treatment of such costs and the disclosure to be made in the Cost Statements as per relevant Cost Accounting Standard? Solution: The expenses paid or incurred for purchase of a brand is lump-sum in nature and purchased for the increase in revenue income over a long period of time. As per Cost Accounting Standard 10, expenses which are in the nature of 'one - time' payment, shall be amortized on the basis of the estimated output or benefit to be derived from such direct expenses. The expenses for which the benefit is ensued in the future period shall be equated with the estimated production/service volumes for the effective period and based on volume achieved during the Cost Accounting period. Accordingly, the charge for amortization shall be determined. In the given situation, the company is likely to be benefitted from the brand image of the product and the costs so amortized be treated as Selling Expenses over the estimated life of the brand image. As per cas-10, the cost statements on direct expenses shall normally disclose the following: a. The basis of distribution of Direct Expenses to the cost objects/cost units. b. Quantity and rates of items of Direct Expenses, as applicable. c. Where Direct Expenses are accounted at standard cost, the price and usage variances. d. Direct expenses paid/payable to related parties. e. Direct Expenses incurred in foreign exchange. f. Any subsidy/Grant/incentive/credit/recoveries and any such payment be reduced from Direct

Expenses. Disclosure shall be made only where expenses are material, significant and quantifiable and be made in the body of the Cost Statement or as a foot note or as a separate schedule. Question-91: In the Financial Accounts of CHEMICALS & FERTILIZERS LTD. for the year ended March 31,2016 the profit was ₹898,07,500. The profit as per Cost Accounting records for the same period was less. The following details are extracted from the accounting schedules and Cost Accounting records of the company.

You are required to prepare a Reconciliation Statement and arrive at the Profit as per Cost Records for the year ended March 31, 2016.

Particulars Financial Accounts

₹ ‘000 Cost Accounts

₹ ‘000

Opening : Semi Finished Goods 31700 35210

: Finished Goods 83220 78590

Closing : Semi Finished Goods 35260 39420

: Finished Goods 89320 80450

Urea & Transport subsidy 348

Expenses on CSR 56

Profit on sale of Fixed Assets 150

Chemical used internally 382 365

Favorable Exch. Rate variation 294

Post-retirement Medical grant 584

Purchase Tax Refund 453

Litigation Recovery-Prior year 125

22

22

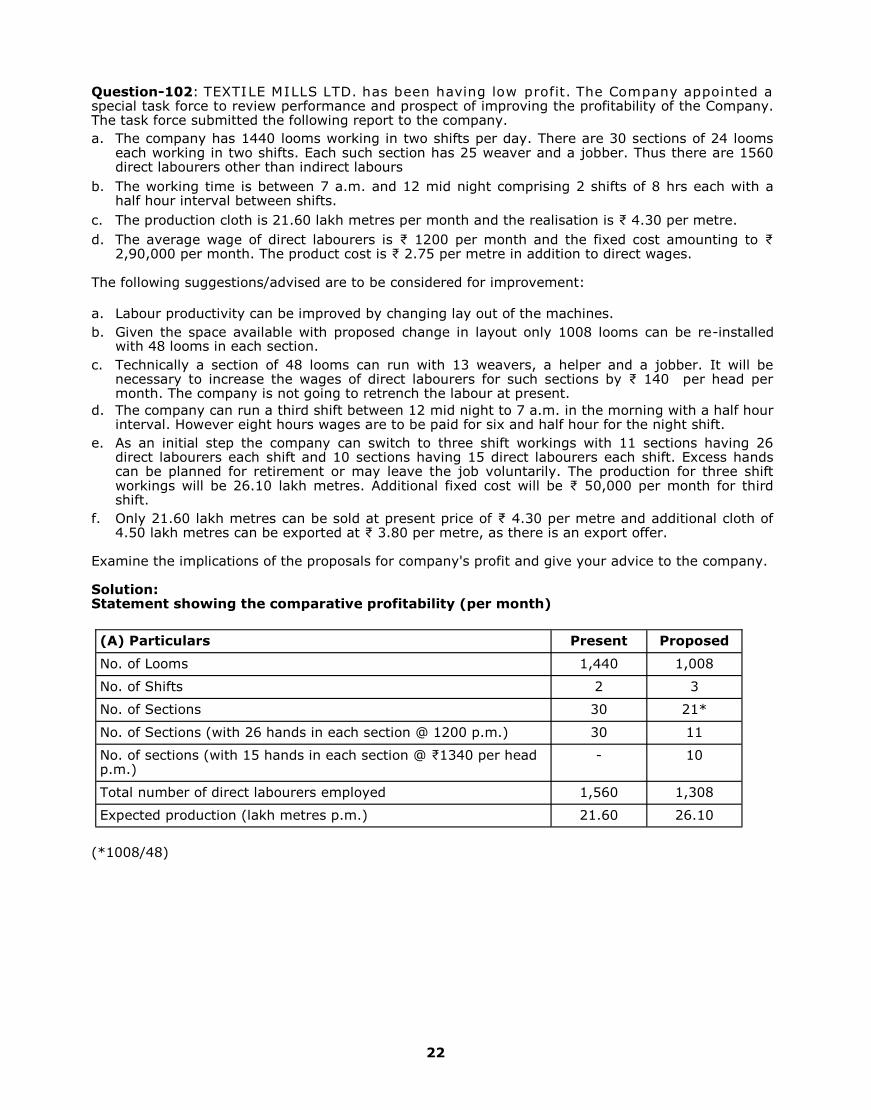

Question-102: TEXTILE MILLS LTD. has been having low profit. The Company appointed a special task force to review performance and prospect of improving the profitability of the Company. The task force submitted the following report to the company.

a. The company has 1440 looms working in two shifts per day. There are 30 sections of 24 looms each working in two shifts. Each such section has 25 weaver and a jobber. Thus there are 1560 direct labourers other than indirect labours

b. The working time is between 7 a.m. and 12 mid night comprising 2 shifts of 8 hrs each with a half hour interval between shifts.

c. The production cloth is 21.60 lakh metres per month and the realisation is ₹ 4.30 per metre.

d. The average wage of direct labourers is ₹ 1200 per month and the fixed cost amounting to ₹ 2,90,000 per month. The product cost is ₹ 2.75 per metre in addition to direct wages.

The following suggestions/advised are to be considered for improvement:

a. Labour productivity can be improved by changing lay out of the machines.

b. Given the space available with proposed change in layout only 1008 looms can be re-installed with 48 looms in each section.

c. Technically a section of 48 looms can run with 13 weavers, a helper and a jobber. It will be necessary to increase the wages of direct labourers for such sections by ₹ 140 per head per month. The company is not going to retrench the labour at present.

d. The company can run a third shift between 12 mid night to 7 a.m. in the morning with a half hour interval. However eight hours wages are to be paid for six and half hour for the night shift.

e. As an initial step the company can switch to three shift workings with 11 sections having 26 direct labourers each shift and 10 sections having 15 direct labourers each shift. Excess hands can be planned for retirement or may leave the job voluntarily. The production for three shift workings will be 26.10 lakh metres. Additional fixed cost will be ₹ 50,000 per month for third shift.

f. Only 21.60 lakh metres can be sold at present price of ₹ 4.30 per metre and additional cloth of 4.50 lakh metres can be exported at ₹ 3.80 per metre, as there is an export offer.

Examine the implications of the proposals for company's profit and give your advice to the company. Solution: Statement showing the comparative profitability (per month)

(*1008/48)

(A) Particulars Present Proposed

No. of Looms 1,440 1,008

No. of Shifts 2 3

No. of Sections 30 21*

No. of Sections (with 26 hands in each section @ 1200 p.m.) 30 11

No. of sections (with 15 hands in each section @ ₹1340 per head p.m.)

- 10

Total number of direct labourers employed 1,560 1,308

Expected production (lakh metres p.m.) 21.60 26.10

23

23

117

■ Cost Accounting Standards

■ Cost Auditing Standards

■ Practical Questions

3

118

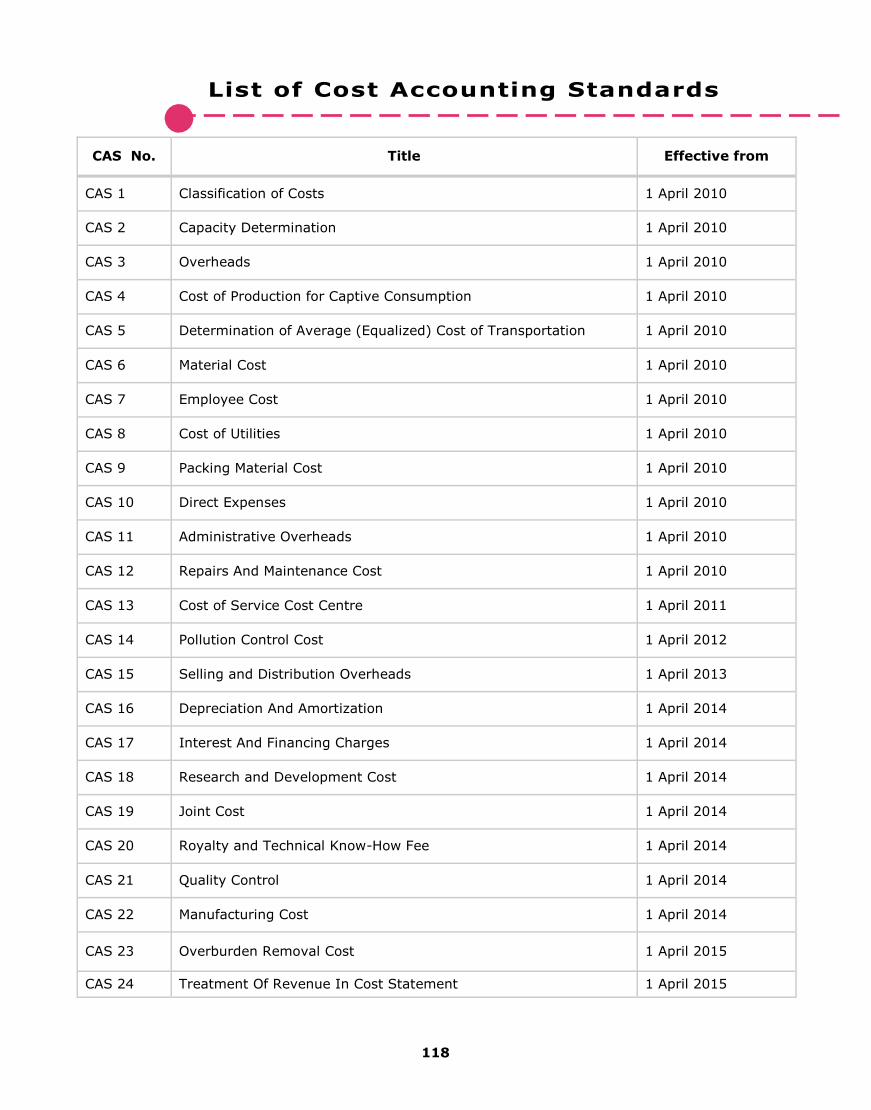

CAS No. Title Effective from

CAS 1 Classification of Costs 1 April 2010

CAS 2 Capacity Determination 1 April 2010

CAS 3 Overheads 1 April 2010

CAS 4 Cost of Production for Captive Consumption 1 April 2010

CAS 5 Determination of Average (Equalized) Cost of Transportation 1 April 2010

CAS 6 Material Cost 1 April 2010

CAS 7 Employee Cost 1 April 2010

CAS 8 Cost of Utilities 1 April 2010

CAS 9 Packing Material Cost 1 April 2010

CAS 10 Direct Expenses 1 April 2010

CAS 11 Administrative Overheads 1 April 2010

CAS 12 Repairs And Maintenance Cost 1 April 2010

CAS 13 Cost of Service Cost Centre 1 April 2011

CAS 14 Pollution Control Cost 1 April 2012

CAS 15 Selling and Distribution Overheads 1 April 2013

CAS 16 Depreciation And Amortization 1 April 2014

CAS 17 Interest And Financing Charges 1 April 2014

CAS 18 Research and Development Cost 1 April 2014

CAS 19 Joint Cost 1 April 2014

CAS 20 Royalty and Technical Know-How Fee 1 April 2014

CAS 21 Quality Control 1 April 2014

CAS 22 Manufacturing Cost 1 April 2014

CAS 23 Overburden Removal Cost 1 April 2015

CAS 24 Treatment Of Revenue In Cost Statement 1 April 2015

119

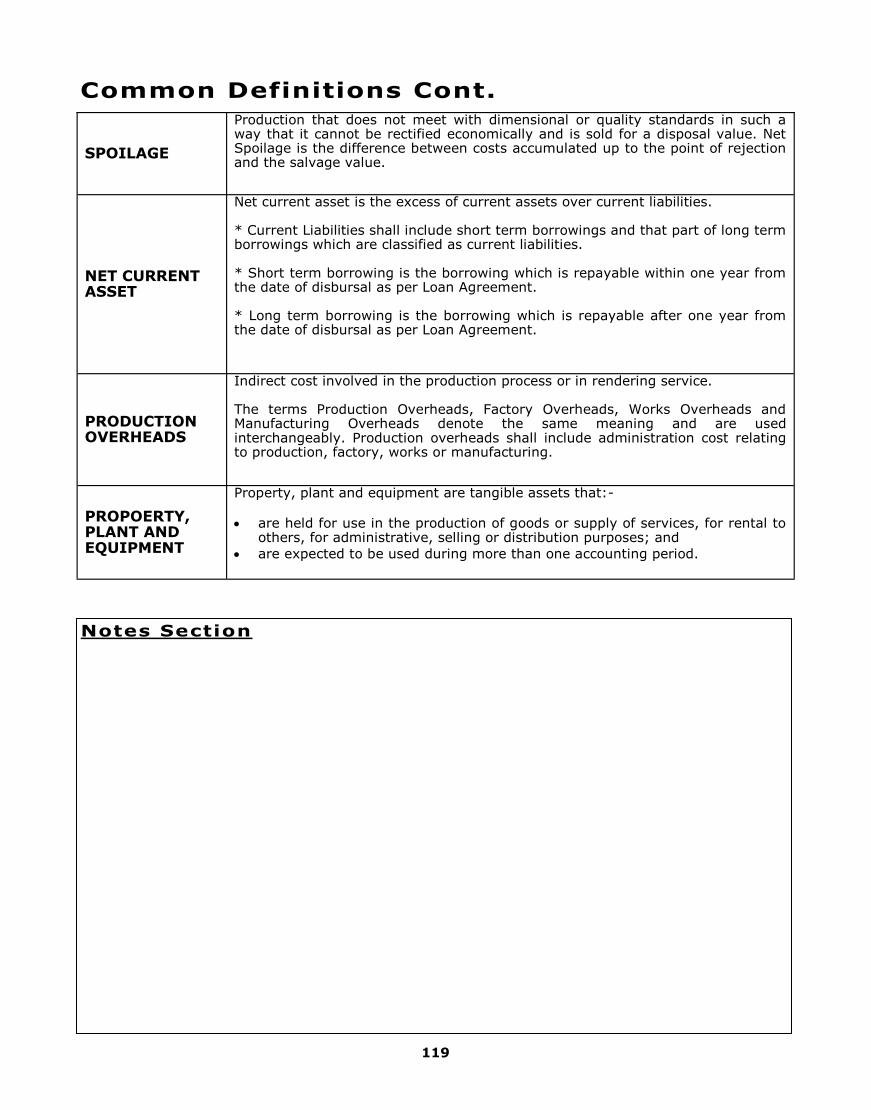

SPOILAGE

Production that does not meet with dimensional or quality standards in such a way that it cannot be rectified economically and is sold for a disposal value. Net Spoilage is the difference between costs accumulated up to the point of rejection and the salvage value.

NET CURRENT ASSET

Net current asset is the excess of current assets over current liabilities. * Current Liabilities shall include short term borrowings and that part of long term borrowings which are classified as current liabilities. * Short term borrowing is the borrowing which is repayable within one year from the date of disbursal as per Loan Agreement. * Long term borrowing is the borrowing which is repayable after one year from the date of disbursal as per Loan Agreement.

PRODUCTION OVERHEADS

Indirect cost involved in the production process or in rendering service. The terms Production Overheads, Factory Overheads, Works Overheads and Manufacturing Overheads denote the same meaning and are used interchangeably. Production overheads shall include administration cost relating to production, factory, works or manufacturing.

PROPOERTY, PLANT AND EQUIPMENT

Property, plant and equipment are tangible assets that:-

are held for use in the production of goods or supply of services, for rental to others, for administrative, selling or distribution purposes; and

are expected to be used during more than one accounting period.

120

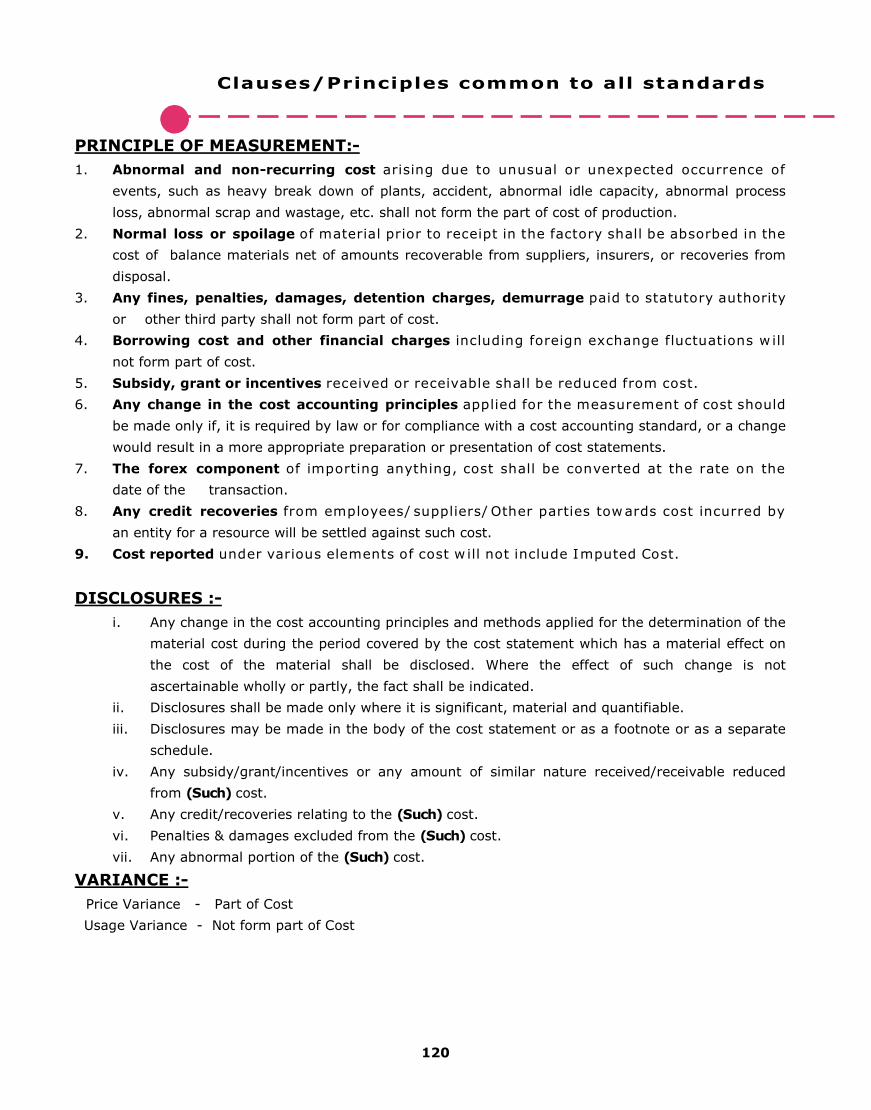

PRINCIPLE OF MEASUREMENT:-

1. Abnormal and non-recurring cost arising due to unusual or unexpected occurrence of

events, such as heavy break down of plants, accident, abnormal idle capacity, abnormal process

loss, abnormal scrap and wastage, etc. shall not form the part of cost of production.

2. Normal loss or spoilage of material prior to receipt in the factory shall be absorbed in the

cost of balance materials net of amounts recoverable from suppliers, insurers, or recoveries from

disposal.

3. Any fines, penalties, damages, detention charges, demurrage paid to statutory authority

or other third party shall not form part of cost.

4. Borrowing cost and other financial charges including foreign exchange fluctuations w ill

not form part of cost.

5. Subsidy, grant or incentives received or receivable shall be reduced from cost.

6. Any change in the cost accounting principles applied for the measurement of cost should

be made only if, it is required by law or for compliance with a cost accounting standard, or a change

would result in a more appropriate preparation or presentation of cost statements.

7. The forex component of importing anything, cost shall be converted at the rate on the

date of the transaction.

8. Any credit recoveries from employees/ suppliers/ Other parties towards cost incurred by

an entity for a resource will be settled against such cost.

9. Cost reported under various elements of cost w ill not include Imputed Cost.

DISCLOSURES :-

i. Any change in the cost accounting principles and methods applied for the determination of the

material cost during the period covered by the cost statement which has a material effect on

the cost of the material shall be disclosed. Where the effect of such change is not

ascertainable wholly or partly, the fact shall be indicated.

ii. Disclosures shall be made only where it is significant, material and quantifiable.

iii. Disclosures may be made in the body of the cost statement or as a footnote or as a separate

schedule.

iv. Any subsidy/grant/incentives or any amount of similar nature received/receivable reduced

from (Such) cost.

v. Any credit/recoveries relating to the (Such) cost.

vi. Penalties & damages excluded from the (Such) cost.

vii. Any abnormal portion of the (Such) cost.

VARIANCE :-

Price Variance - Part of Cost

Usage Variance - Not form part of Cost

121

Expenses Mentioned In Mentioned Under

a. Corporate Social Responsibility Expenses (CSR)

Profit Reconciliation

Expenses Not Considered in Cost Records*

b. Profit/Loss on Foreign Exchange

Profit Reconciliation

Profit—Income Not Considered in Cost Records Loss - Expense Not Considered in Cost Records

c. Profit/Loss on sale of Fixed Asset

Profit Reconciliation

Profit—Income Not Considered in Cost Records Loss - Expense Not Considered in Cost Records

d. Any Adjustment Profit Reconciliation

Depends on type of adjustment

e. Assets written off/ Write Back

Profit Reconciliation

Write Off - Expense Not Considered in Cost Records

Write Back - Income Not Considered in Cost Records

Note: *

CSR expense is an expense not related to the business; it does not have any direct impact on cost of

production/operations. Even the assets created out of CSR expenditure are not recognized as 'asset' in

the company's books but charged as an expense to the statement of profit and loss.

All CSR expenses are incurred in activities that are in the nature of philanthropic activities whose present

or future economic benefits do not flow to the company or any surplus/profits arising from such activities

cannot be recognized as business profits of the company. Hence, CSR expenses are not included in the

cost of sales.

They are presented in the Profit Reconciliation Statement. Similarly, any incomes generated or surplus

arising from CSR activities shall not be so recognized and to be exhibited in the Profit Reconciliation

Statement.

122

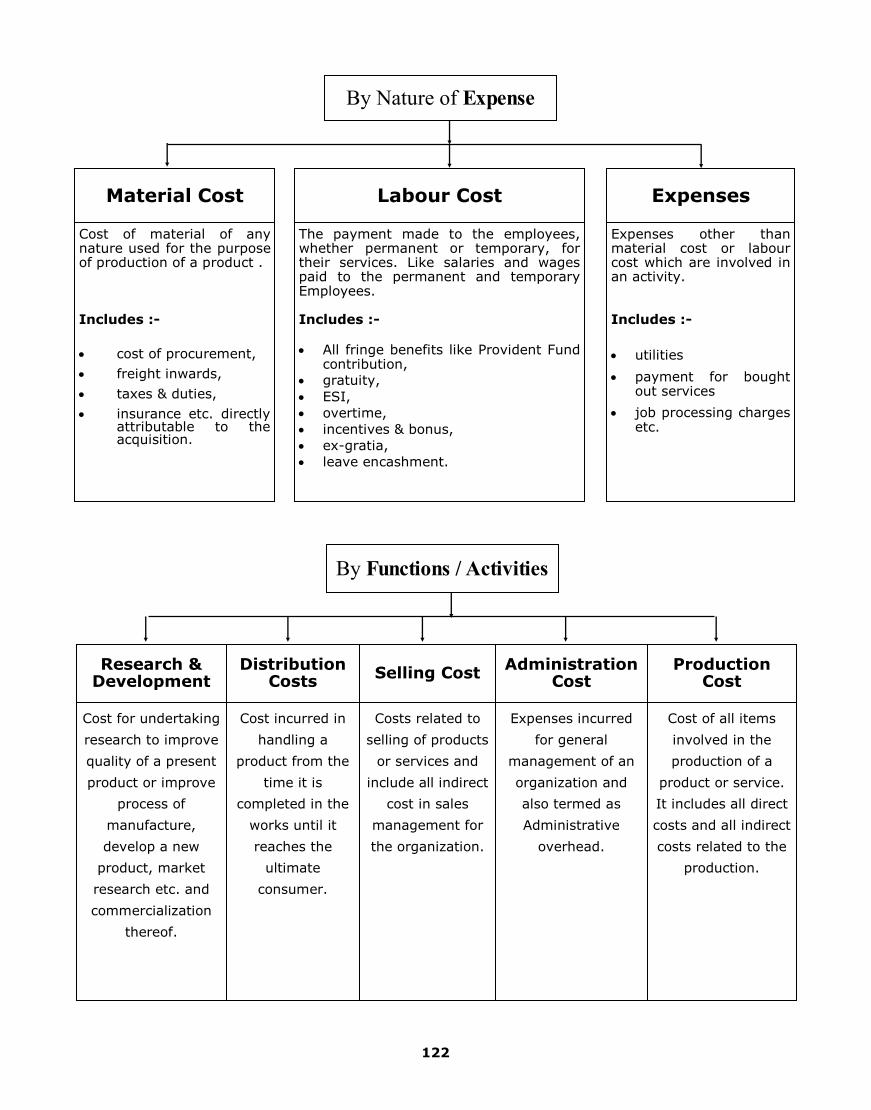

Cost of material of any nature used for the purpose of production of a product . Includes :-

cost of procurement,

freight inwards,

taxes & duties,

insurance etc. directly attributable to the acquisition.

Material Cost

The payment made to the employees, whether permanent or temporary, for their services. Like salaries and wages paid to the permanent and temporary Employees. Includes :-

All fringe benefits like Provident Fund contribution,

gratuity,

ESI,

overtime,

incentives & bonus,

ex-gratia,

leave encashment.

Labour Cost

Expenses other than material cost or labour cost which are involved in an activity. Includes :-

utilities

payment for bought out services

job processing charges etc.

Expenses

By Nature of Expense

Cost for undertaking

research to improve

quality of a present

product or improve

process of

manufacture,

develop a new

product, market

research etc. and

commercialization

thereof.

Research & Development

By Functions / Activities

Cost incurred in

handling a

product from the

time it is

completed in the

works until it

reaches the

ultimate

consumer.

Distribution Costs

Costs related to

selling of products

or services and

include all indirect

cost in sales

management for

the organization.

Selling Cost

Expenses incurred

for general

management of an

organization and

also termed as

Administrative

overhead.

Administration Cost

Cost of all items

involved in the

production of a

product or service.

It includes all direct

costs and all indirect

costs related to the

production.

Production Cost

123

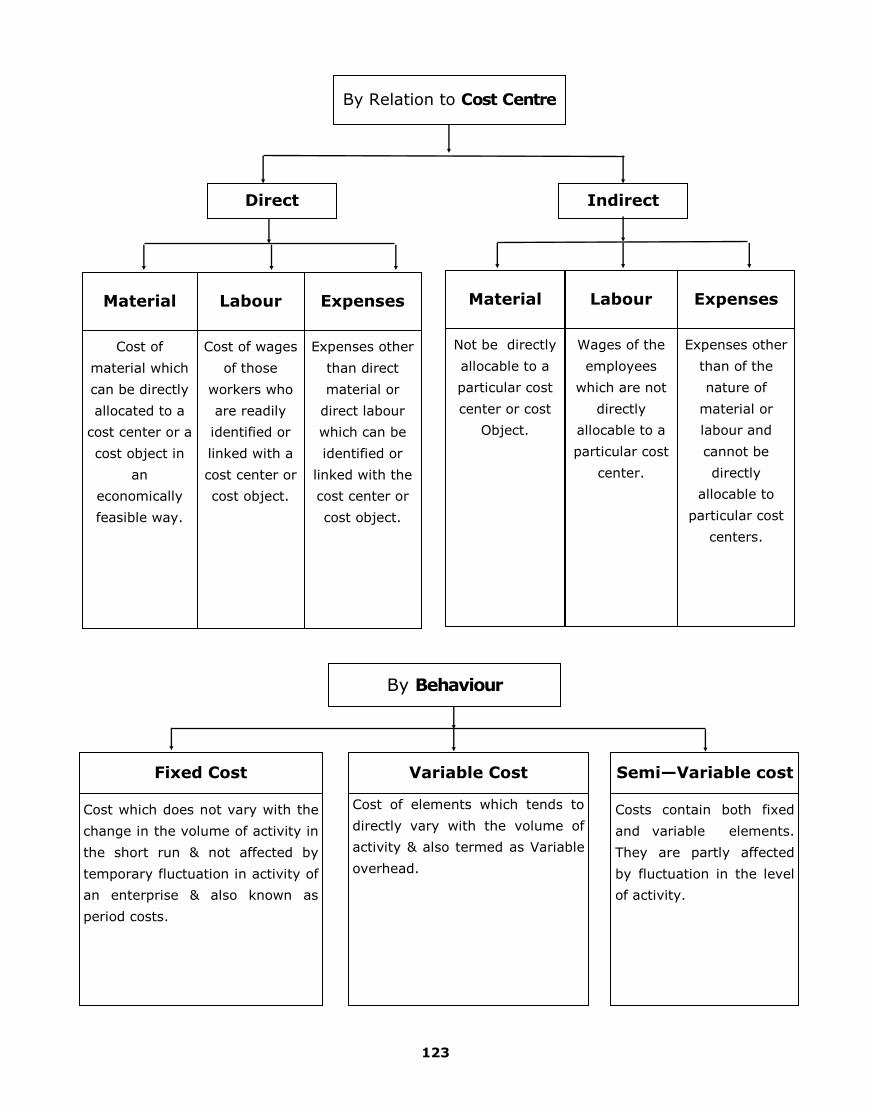

Cost which does not vary with the

change in the volume of activity in

the short run & not affected by

temporary fluctuation in activity of

an enterprise & also known as

period costs.

Fixed Cost

Cost of elements which tends to

directly vary with the volume of

activity & also termed as Variable

overhead.

Variable Cost

Costs contain both fixed

and variable elements.

They are partly affected

by fluctuation in the level

of activity.

Semi—Variable cost

By Behaviour

By Relation to Cost Centre

Cost of

material which

can be directly

allocated to a

cost center or a

cost object in

an

economically

feasible way.

Material

Cost of wages

of those

workers who

are readily

identified or

linked with a

cost center or

cost object.

Labour

Expenses other

than direct

material or

direct labour

which can be

identified or

linked with the

cost center or

cost object.

Expenses

Direct

Not be directly

allocable to a

particular cost

center or cost

Object.

Material

Wages of the

employees

which are not

directly

allocable to a

particular cost

center.

Labour

Expenses other

than of the

nature of

material or

labour and

cannot be

directly

allocable to

particular cost

centers.

Expenses

Indirect

124

OBJECTIVE &

SCOPE

Objective of this standard is to bring uniformity and consistency in the

principles and methods of determining the overheads with reasonable accuracy.

Overheads Overheads comprise costs of indirect materials, indirect employees and indirect expenses which are not directly identifiable or allocable to a cost object in an economically feasible manner.

Absorption of Overheads

Absorption of overheads is charging of overheads to cost objects by means of appropriate absorption rate. Overhead Absorption Rate = Overheads of the cost object / quantum of base.

Distribution of Overheads

Distribution overheads, also known as Distribution Cost, are the cost incurred in handling a product from the time it is ready for dispatch until it reaches the ultimate consumer.

DEFIN

ITIO

NS

A. The cost which can be traced directly to a cost object shall be directly assigned.

B. Assignment of overhead to the cost objects shall be based on either of the

following two principles;

I. Cause and Effect: Cause is the process or operation or activity and effect is the

incurrence of cost.

II. Benefits received: Overheads are to be apportioned to the various cost objects

in proportion to the benefits received by them.

C. Absorption of production or Operation Overheads

Variable Overheads = Absorbed to product or services based on ACTUAL PRODUCTION

Fixed Overheads = Absorbed to product or services based on NORMAL CAPACITY

A. Overheads shall be presented as separate cost heads like production, administration

and marketing.

B. Element wise and behavior wise details of the overheads shall be presented, if material.

C. Any under-absorption or over-absorption of overheads shall be presented in the

reconciliation

D. The cost statements shall disclose the following:

1. The basis of assignment of overheads to the cost objects.

2. Overheads incurred in foreign exchange.

3. Overheads relating to resources received from or supplied to related parties.

4. Any Subsidy / Grant / Incentive or any amount of similar nature received /

receivable reduced from overheads.

5. Credits / recoveries relating to the overheads.

6. Any abnormal cost not forming part of the overheads.

AS

SIG

NM

EN

T

OF C

OS

T

PR

ES

EN

TA

TIO

N &

D

IS

CLO

SU

RES

125

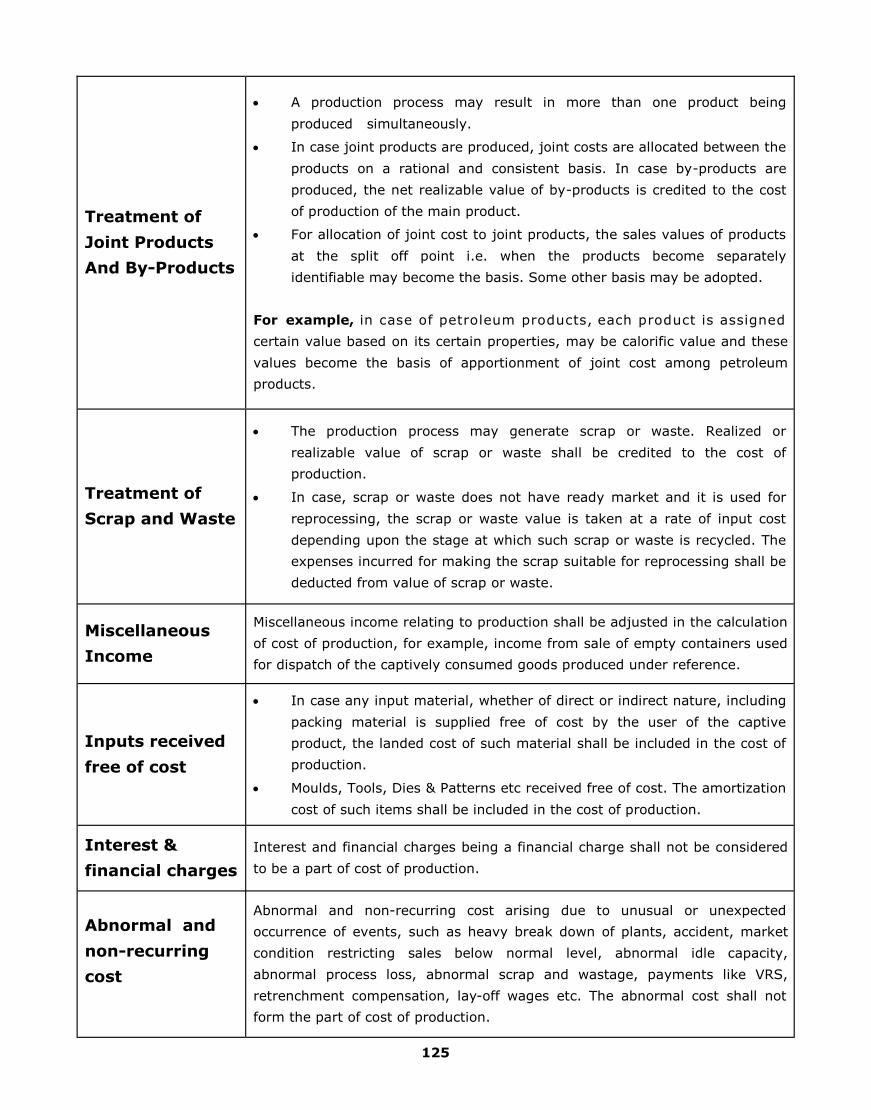

Treatment of

Joint Products

And By-Products

A production process may result in more than one product being

produced simultaneously.

In case joint products are produced, joint costs are allocated between the

products on a rational and consistent basis. In case by-products are

produced, the net realizable value of by-products is credited to the cost

of production of the main product.

For allocation of joint cost to joint products, the sales values of products

at the split off point i.e. when the products become separately

identifiable may become the basis. Some other basis may be adopted.

For example, in case of petroleum products, each product is assigned

certain value based on its certain properties, may be calorific value and these

values become the basis of apportionment of joint cost among petroleum

products.

Treatment of

Scrap and Waste

The production process may generate scrap or waste. Realized or

realizable value of scrap or waste shall be credited to the cost of

production.

In case, scrap or waste does not have ready market and it is used for

reprocessing, the scrap or waste value is taken at a rate of input cost

depending upon the stage at which such scrap or waste is recycled. The

expenses incurred for making the scrap suitable for reprocessing shall be

deducted from value of scrap or waste.

Miscellaneous

Income

Miscellaneous income relating to production shall be adjusted in the calculation

of cost of production, for example, income from sale of empty containers used

for dispatch of the captively consumed goods produced under reference.

Inputs received

free of cost

In case any input material, whether of direct or indirect nature, including

packing material is supplied free of cost by the user of the captive

product, the landed cost of such material shall be included in the cost of

production.

Moulds, Tools, Dies & Patterns etc received free of cost. The amortization

cost of such items shall be included in the cost of production.

Interest &

financial charges

Interest and financial charges being a financial charge shall not be considered

to be a part of cost of production.

Abnormal and

non-recurring

cost

Abnormal and non-recurring cost arising due to unusual or unexpected

occurrence of events, such as heavy break down of plants, accident, market

condition restricting sales below normal level, abnormal idle capacity,

abnormal process loss, abnormal scrap and wastage, payments like VRS,

retrenchment compensation, lay-off wages etc. The abnormal cost shall not

form the part of cost of production.

126

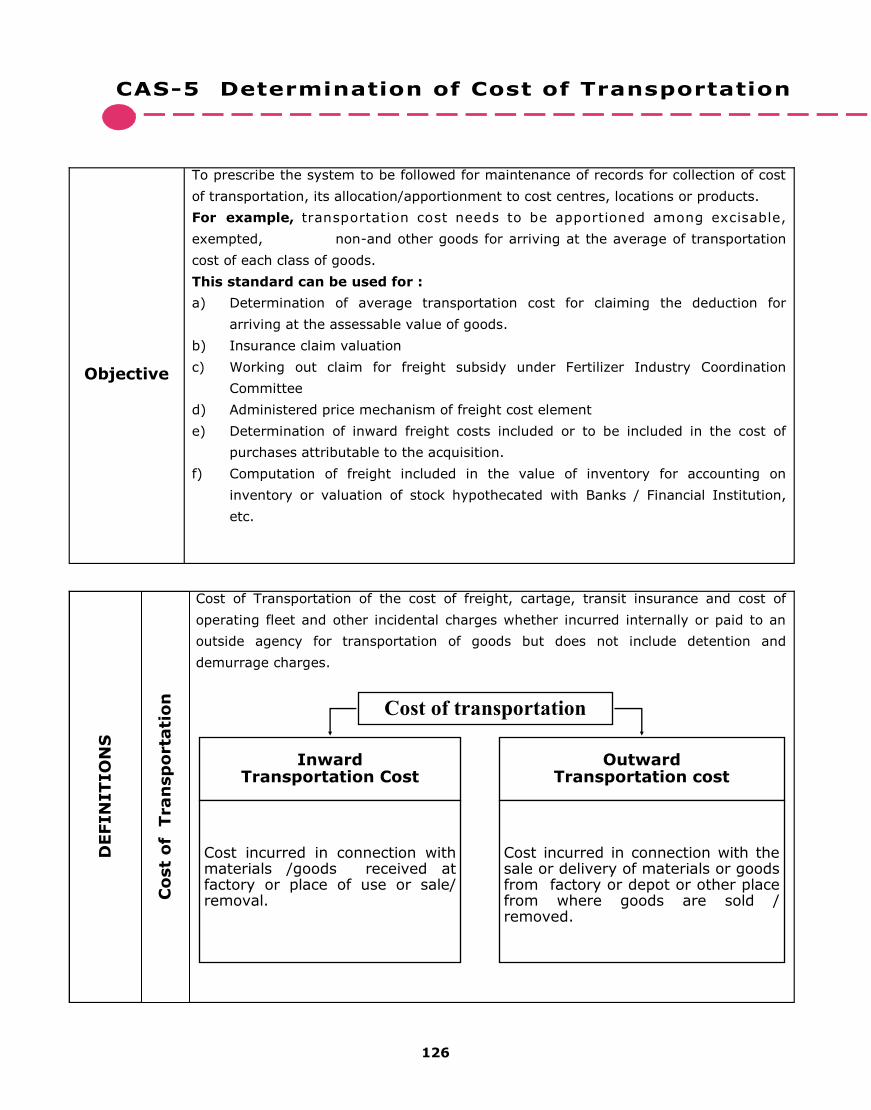

Objective

To prescribe the system to be followed for maintenance of records for collection of cost

of transportation, its allocation/apportionment to cost centres, locations or products.

For example, transportation cost needs to be apportioned among excisable,

exempted, non-and other goods for arriving at the average of transportation

cost of each class of goods.

This standard can be used for :

a) Determination of average transportation cost for claiming the deduction for

arriving at the assessable value of goods.

b) Insurance claim valuation

c) Working out claim for freight subsidy under Fertilizer Industry Coordination

Committee

d) Administered price mechanism of freight cost element

e) Determination of inward freight costs included or to be included in the cost of

purchases attributable to the acquisition.

f) Computation of freight included in the value of inventory for accounting on

inventory or valuation of stock hypothecated with Banks / Financial Institution,

etc.

Cost of Transportation of the cost of freight, cartage, transit insurance and cost of

operating fleet and other incidental charges whether incurred internally or paid to an

outside agency for transportation of goods but does not include detention and

demurrage charges.

Co

st

of

Tran

sp

orta

tio

n

Cost of transportation

Inward Transportation Cost

Cost incurred in connection with materials /goods received at factory or place of use or sale/removal.

Outward Transportation cost

Cost incurred in connection with the sale or delivery of materials or goods from factory or depot or other place from where goods are sold /removed.

DEFIN

ITIO

NS

127

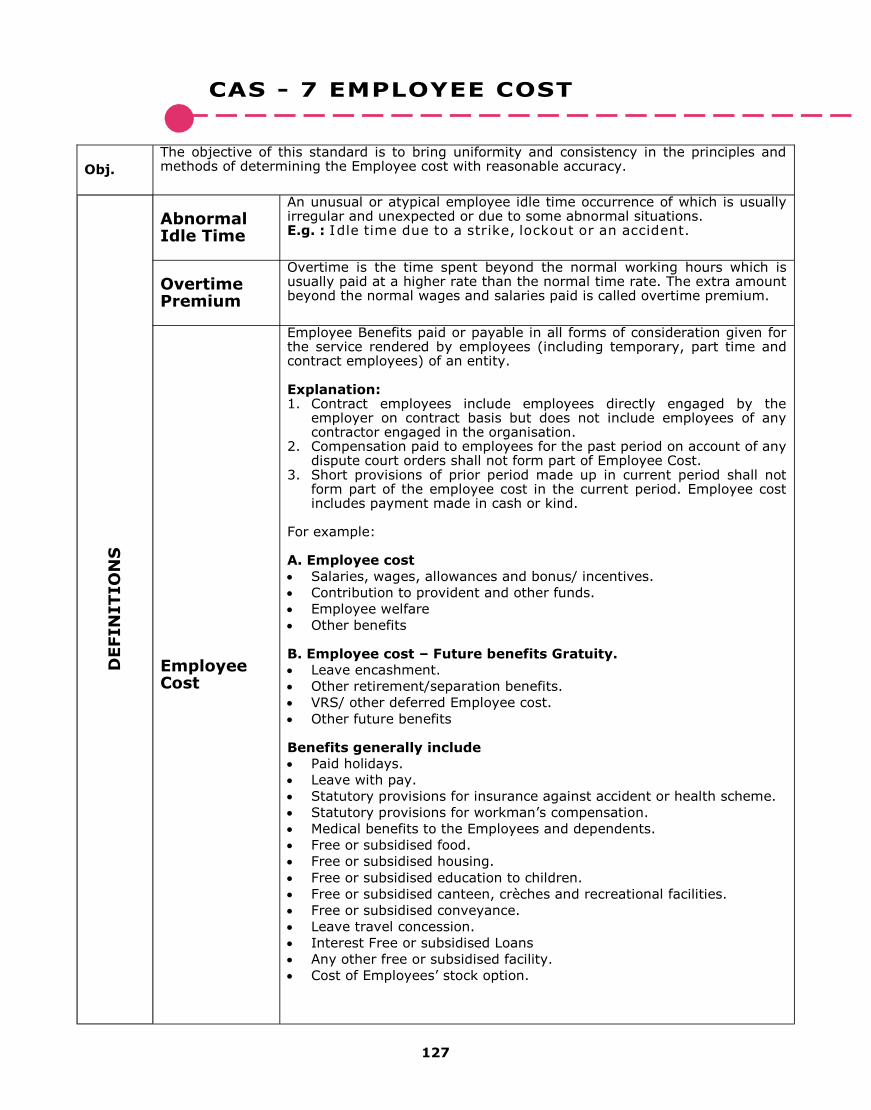

Obj.

The objective of this standard is to bring uniformity and consistency in the principles and methods of determining the Employee cost with reasonable accuracy.

Abnormal Idle Time

An unusual or atypical employee idle time occurrence of which is usually irregular and unexpected or due to some abnormal situations. E.g. : Idle time due to a strike, lockout or an accident.

Overtime Premium

Overtime is the time spent beyond the normal working hours which is usually paid at a higher rate than the normal time rate. The extra amount beyond the normal wages and salaries paid is called overtime premium.

Employee Cost

Employee Benefits paid or payable in all forms of consideration given for the service rendered by employees (including temporary, part time and contract employees) of an entity. Explanation: 1. Contract employees include employees directly engaged by the

employer on contract basis but does not include employees of any contractor engaged in the organisation.

2. Compensation paid to employees for the past period on account of any dispute court orders shall not form part of Employee Cost.

3. Short provisions of prior period made up in current period shall not form part of the employee cost in the current period. Employee cost includes payment made in cash or kind.

For example: A. Employee cost

Salaries, wages, allowances and bonus/ incentives.

Contribution to provident and other funds.

Employee welfare

Other benefits B. Employee cost – Future benefits Gratuity.

Leave encashment.

Other retirement/separation benefits.

VRS/ other deferred Employee cost.

Other future benefits Benefits generally include

Paid holidays.

Leave with pay.

Statutory provisions for insurance against accident or health scheme.

Statutory provisions for workman’s compensation.

Medical benefits to the Employees and dependents.

Free or subsidised food.

Free or subsidised housing.

Free or subsidised education to children.

Free or subsidised canteen, crèches and recreational facilities.

Free or subsidised conveyance.

Leave travel concession.

Interest Free or subsidised Loans

Any other free or subsidised facility.

Cost of Employees’ stock option.

DEFIN

ITIO

NS

128

IT (Information Technology) Environment and Control

The cost auditor shall evaluate and assess:

IT Architecture, Systems and programmes in use in the entity;

Controls on access to data;

Controls on changes to data in master files, systems or programmes;

An Integrity of information and security of the data

Identifying and Assessing the Risks of Material Misstatement

The cost auditor shall identify and assess the risks of material misstatement at the cost statement level; and at the assertion level including items of cost, cost heads and disclosures thereof. For this purpose, the cost auditor shall:

Identify risks including relevant controls that relate to the risk of material misstatements or a risk of fraud;

Assess whether the risk is related to recent significant economic, accounting or other developments and, therefore, requires specific attention;

Assess whether the risk involves significant transactions with related parties;

Assess the degree of subjectivity in the measurement of information related to the risk.

Assess whether there arises a need for revising the assessment of risk based on additional audit evidence obtained.

Documentation

The auditor shall document:

Key elements of the understanding obtained regarding each of the aspects of the entity and its environment and of each of the internal control components; the sources of information from which the understanding was obtained; and the risk assessment procedures performed;

The identified and assessed risks of material misstatement at the cost statement level and at the assertion level including items of cost, cost heads and disclosure thereof as required; and

The risks identified, and related controls about which the auditor has obtained an understanding.

129

PRACTICAL QUESTIONS

3.3

130

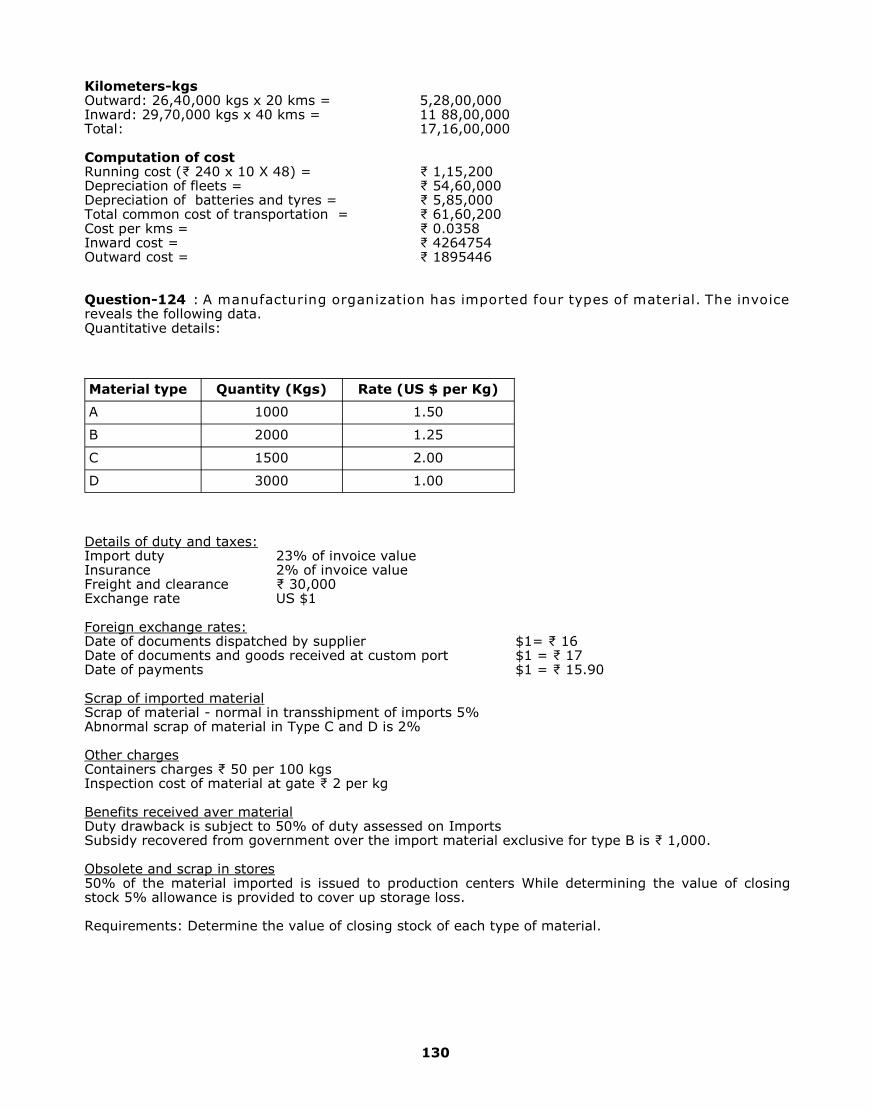

Kilometers-kgs Outward: 26,40,000 kgs x 20 kms = 5,28,00,000 Inward: 29,70,000 kgs x 40 kms = 11 88,00,000 Total: 17,16,00,000 Computation of cost Running cost (₹ 240 x 10 X 48) = ₹ 1,15,200 Depreciation of fleets = ₹ 54,60,000 Depreciation of batteries and tyres = ₹ 5,85,000 Total common cost of transportation = ₹ 61,60,200 Cost per kms = ₹ 0.0358 Inward cost = ₹ 4264754 Outward cost = ₹ 1895446 Question-124 : A manufacturing organization has imported four types of material. The invoice reveals the following data. Quantitative details:

Details of duty and taxes: Import duty 23% of invoice value Insurance 2% of invoice value Freight and clearance ₹ 30,000 Exchange rate US $1 Foreign exchange rates: Date of documents dispatched by supplier $1= ₹ 16 Date of documents and goods received at custom port $1 = ₹ 17 Date of payments $1 = ₹ 15.90 Scrap of imported material Scrap of material - normal in transshipment of imports 5% Abnormal scrap of material in Type C and D is 2% Other charges Containers charges ₹ 50 per 100 kgs Inspection cost of material at gate ₹ 2 per kg Benefits received aver material Duty drawback is subject to 50% of duty assessed on Imports Subsidy recovered from government over the import material exclusive for type B is ₹ 1,000. Obsolete and scrap in stores 50% of the material imported is issued to production centers While determining the value of closing stock 5% allowance is provided to cover up storage loss. Requirements: Determine the value of closing stock of each type of material.

Material type Quantity (Kgs) Rate (US $ per Kg)

A 1000 1.50

B 2000 1.25

C 1500 2.00

D 3000 1.00

268 268

Performance Analysis

5

269 269

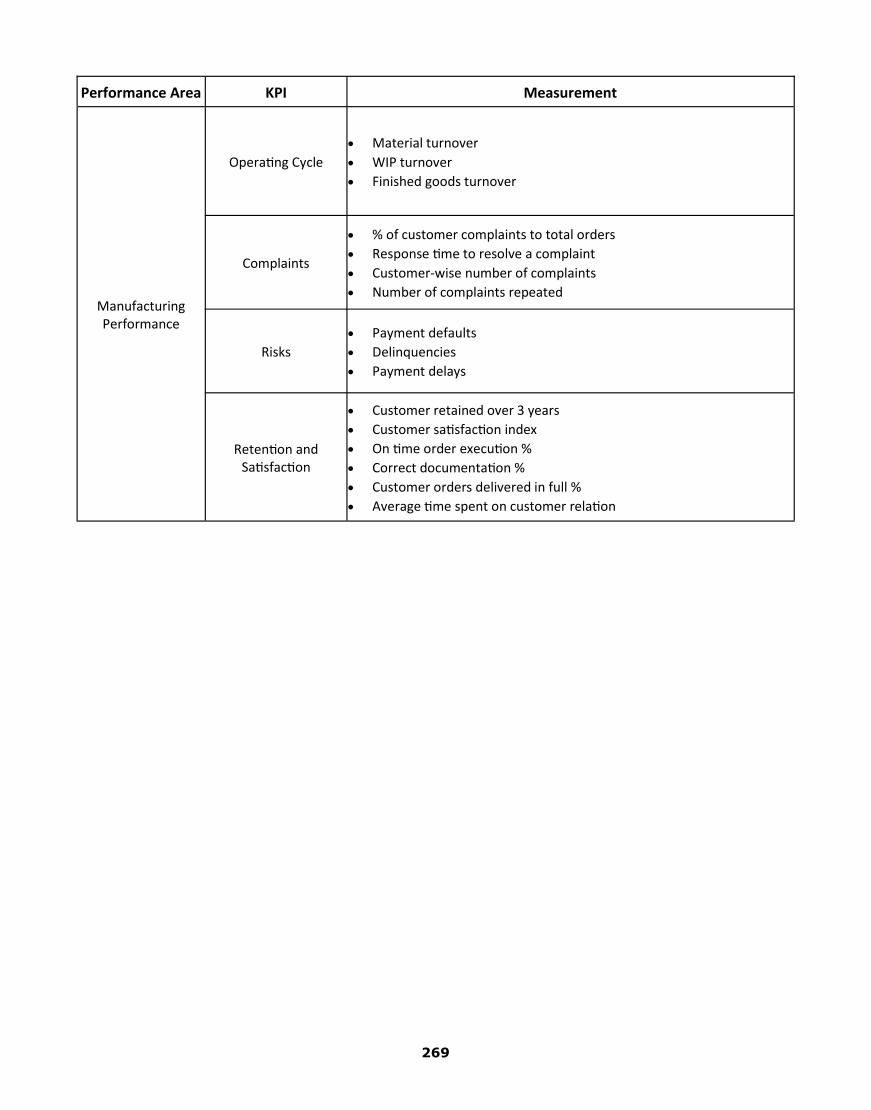

Performance Area KPI Measurement

Manufacturing Performance

Operating Cycle

Material turnover

WIP turnover

Finished goods turnover

Complaints

% of customer complaints to total orders

Response time to resolve a complaint

Customer-wise number of complaints

Number of complaints repeated

Risks

Payment defaults

Delinquencies

Payment delays

Retention and Satisfaction

Customer retained over 3 years

Customer satisfaction index

On time order execution %

Correct documentation %

Customer orders delivered in full %

Average time spent on customer relation

270 270

Practical Questions

5.1

271 271

Particular

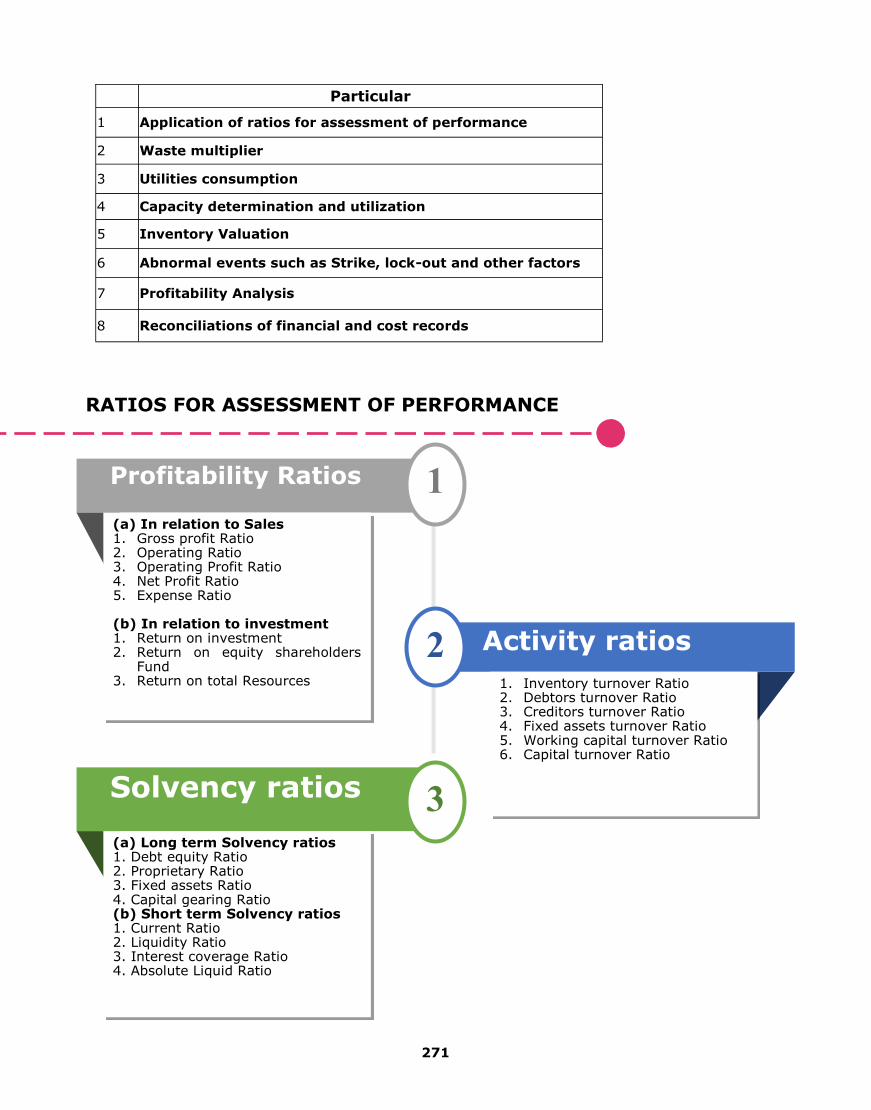

1 Application of ratios for assessment of performance

2 Waste multiplier

3 Utilities consumption

4 Capacity determination and utilization

5 Inventory Valuation

6 Abnormal events such as Strike, lock-out and other factors

7 Profitability Analysis

8 Reconciliations of financial and cost records

RATIOS FOR ASSESSMENT OF PERFORMANCE

Profitability Ratios 1

(a) In relation to Sales 1. Gross profit Ratio 2. Operating Ratio 3. Operating Profit Ratio 4. Net Profit Ratio 5. Expense Ratio (b) In relation to investment 1. Return on investment 2. Return on equity shareholders

Fund 3. Return on total Resources

Solvency ratios 3

(a) Long term Solvency ratios 1. Debt equity Ratio 2. Proprietary Ratio 3. Fixed assets Ratio 4. Capital gearing Ratio (b) Short term Solvency ratios 1. Current Ratio 2. Liquidity Ratio 3. Interest coverage Ratio 4. Absolute Liquid Ratio

Activity ratios 2

1. Inventory turnover Ratio 2. Debtors turnover Ratio 3. Creditors turnover Ratio 4. Fixed assets turnover Ratio 5. Working capital turnover Ratio 6. Capital turnover Ratio

272 272

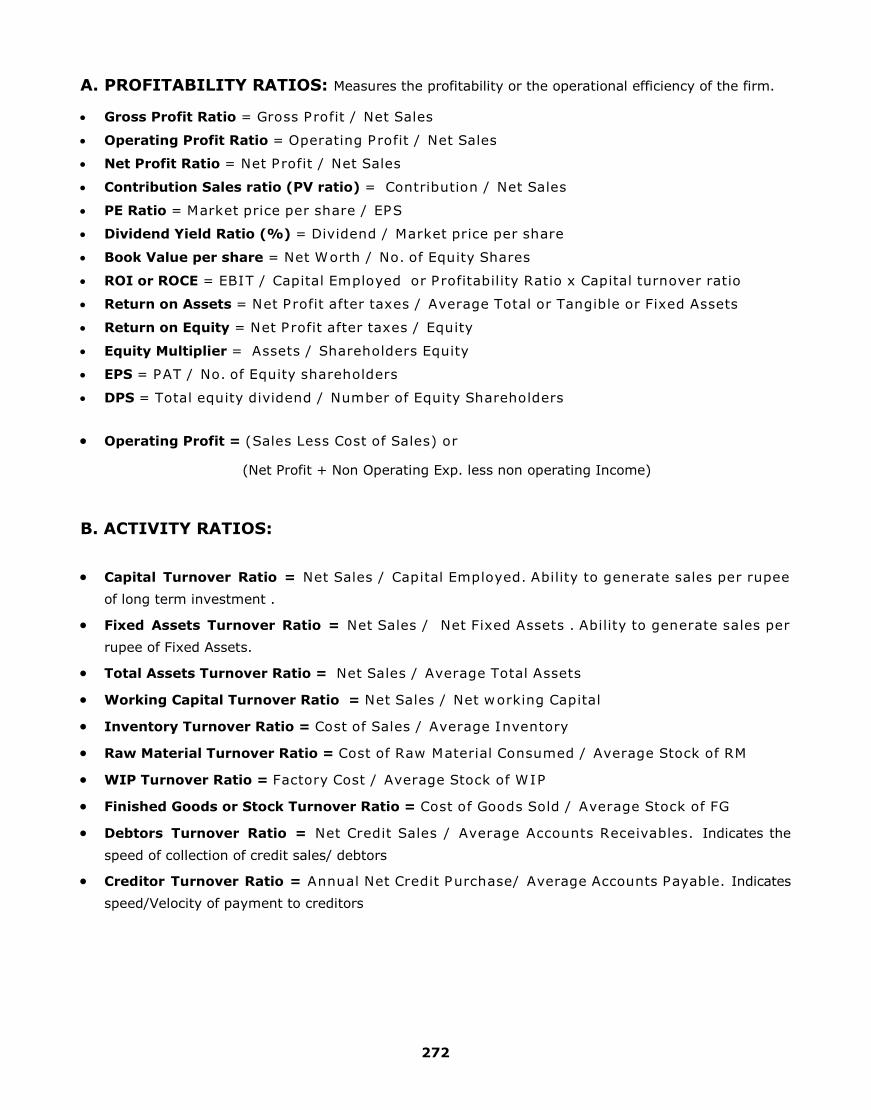

A. PROFITABILITY RATIOS: Measures the profitability or the operational efficiency of the firm.

Gross Profit Ratio = Gross Profit / Net Sales

Operating Profit Ratio = Operating Profit / Net Sales

Net Profit Ratio = Net Profit / Net Sales

Contribution Sales ratio (PV ratio) = Contribution / Net Sales

PE Ratio = Market price per share / EPS

Dividend Yield Ratio (%) = Dividend / Market price per share

Book Value per share = Net Worth / No. of Equity Shares

ROI or ROCE = EBIT / Capital Employed or Profitability Ratio x Capital turnover ratio

Return on Assets = Net Profit after taxes / Average Total or Tangible or Fixed Assets

Return on Equity = Net Profit after taxes / Equity

Equity Multiplier = Assets / Shareholders Equity

EPS = PAT / No. of Equity shareholders

DPS = Total equity dividend / Number of Equity Shareholders

Operating Profit = (Sales Less Cost of Sales) or

(Net Profit + Non Operating Exp. less non operating Income)

B. ACTIVITY RATIOS:

Capital Turnover Ratio = Net Sales / Capital Employed. Ability to generate sales per rupee

of long term investment .

Fixed Assets Turnover Ratio = Net Sales / Net Fixed Assets . Ability to generate sales per

rupee of Fixed Assets.

Total Assets Turnover Ratio = Net Sales / Average Total Assets

Working Capital Turnover Ratio = Net Sales / Net working Capital

Inventory Turnover Ratio = Cost of Sales / Average Inventory

Raw Material Turnover Ratio = Cost of Raw Material Consumed / Average Stock of RM

WIP Turnover Ratio = Factory Cost / Average Stock of WIP

Finished Goods or Stock Turnover Ratio = Cost of Goods Sold / Average Stock of FG

Debtors Turnover Ratio = Net Credit Sales / Average Accounts Receivables. Indicates the

speed of collection of credit sales/ debtors

Creditor Turnover Ratio = Annual Net Credit Purchase/ Average Accounts Payable. Indicates

speed/Velocity of payment to creditors

273 273

C. SOLVENCY RATIOS: Ability of the business to pay its short term liabilities , short term lenders and creditors of a business are very much interested to know its state of liquidity because of their financial state.

Current Ratio = Current Assets / Current liabilities *

Quick Ratio or Acid test ratio = Ideal ratio is 1:1 = Quick Assets ** / Current liabilities

Debt Equity Ratio = Total Liabilities or Long term liabilities / Equity**** Ideal ratio is 2:1.

Debt to Total Assets ratio = Total Liabilities / Total Assets

Proprietary Ratio = proprietary Fund (Equity) / Total Assets

Capital gearing Ratio = (Preference Capital + Debt)/ Equity Shareholders fund

Interest Coverage Ratio = EBIT / Interest

* Current Assets = Inventories + Sundry Debtors + Cash and Bank Balances + Receivables/

Accruals + loan Advances + Disposables investors

* Current Liabilities = Creditors for goods Services + Short term loans + Bank Overdraft +

Cash credit + Outstanding Expenses + Provision for taxation + proposed Divided + Unclaimed Divided

** Quick Assets = Current Assets—( Inventories + Prepaid Expenses )

*** Total Debt = Debentures + Lon term loans etc. (Long term liabilities)

**** Equity = ( Equity Share Capital + Preference share capital + Reserve & Surplus) -

Miscellanies expenditure and accumulated losses

274 274

Average capital employed = (2,196 + 2,220)/2 = 2,208 Total Earning = Profit after tax + Interest on debt funds + Non-Operating Adjustments

= (900 – 144 – 360) + 144 = 540 ∴ Return on capital employed = / average capital employed = 540/2208*100 =24.46 % Alternative method of computation of capital employed Capital Employed means average of net fixed assets (excluding effect of revaluation of fixed assets) plus non-current investments and net current assets existing at the beginning and close of the financial year.

Notes to the computation of capital employed

1. Current assets includes stock, debtors, cash and other current assets 2. Assumed that the investments in Balance sheet are non-current investments 3. Refer Financial statements of 2014-15 for the ‘ Information not available’

It is normally expressed as a percentage. It indicates the rate of return earned by an enterprise from its total Capital Employed in the business. It is also an indicator of the profit earning capacity of an enterprise. A higher return reveals a better profitability on the total Capital Employed in the business. B. Stock turnover Ratio = Net sales excluding excise duty & sales tax / average stock = 3600 / (720+600)/2 = 5.45 times This ratio indicates the movement of stock during a particular period. In other words, it indicates how fast goods are sold out from the stock of those goods. Higher ratio indicates a faster movement of stock.

Particulars 2016 2015 Opening Net Fixed assets 1200 Info. not available Closing Net Fixed assets 1,560 1200

Average Net Fixed assets (1) 1,380

Particulars 2016 2015 Opening non-current investments 0 0 Closing non-current investments 0 0 Average non-current investments (2) 0 0

Particulars 2016 2015

Opening net-current assets 1,020 Info. not available

Closing net-current assets 636 1,170

Average net-current assets (3) 828

Capital employed (1+2+3) 2,208

275 275

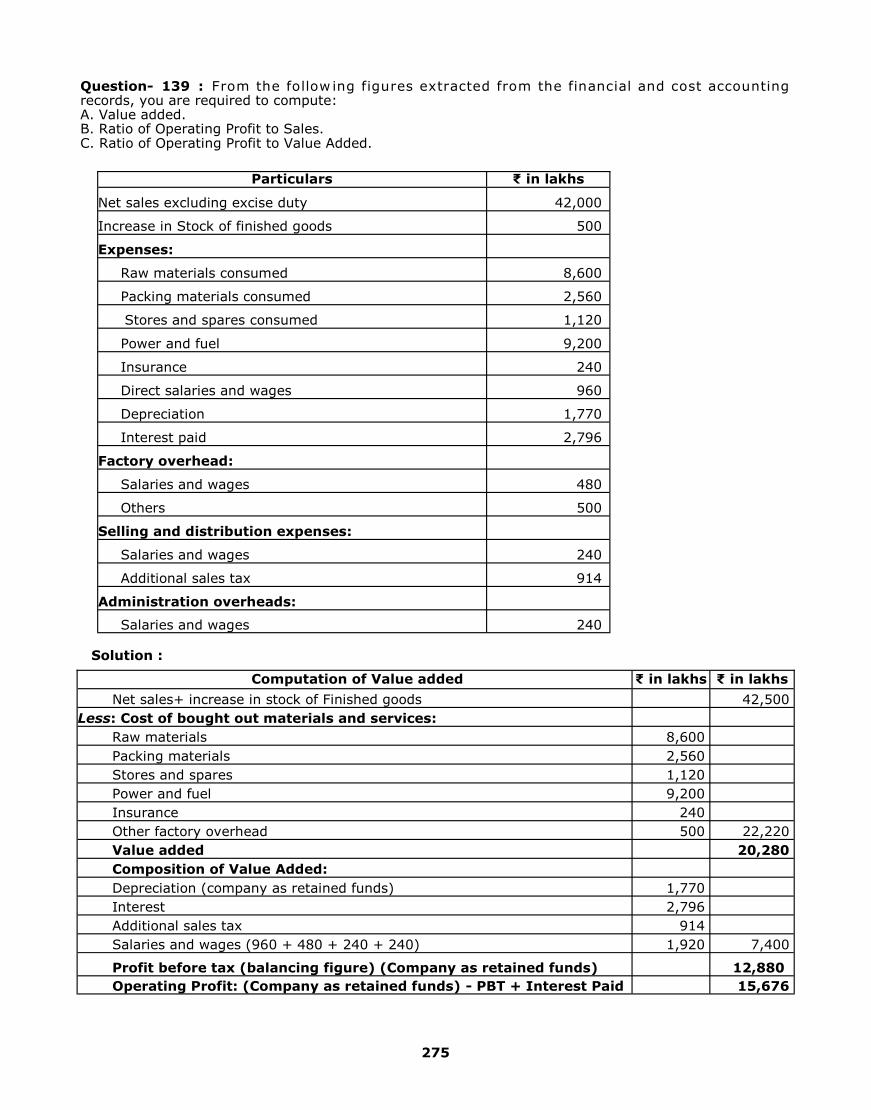

Question- 139 : From the follow ing figures extracted from the financial and cost accounting records, you are required to compute: A. Value added. B. Ratio of Operating Profit to Sales. C. Ratio of Operating Profit to Value Added.

Solution :

Particulars ₹ in lakhs

Net sales excluding excise duty 42,000

Increase in Stock of finished goods 500

Expenses:

Raw materials consumed 8,600

Packing materials consumed 2,560

Stores and spares consumed 1,120

Power and fuel 9,200

Insurance 240

Direct salaries and wages 960

Depreciation 1,770

Interest paid 2,796

Factory overhead:

Salaries and wages 480

Others 500

Selling and distribution expenses:

Salaries and wages 240

Additional sales tax 914

Administration overheads:

Salaries and wages 240

Computation of Value added ₹ in lakhs ₹ in lakhs

Net sales+ increase in stock of Finished goods 42,500

Less: Cost of bought out materials and services:

Raw materials 8,600

Packing materials 2,560

Stores and spares 1,120

Power and fuel 9,200

Insurance 240

Other factory overhead 500 22,220

Value added 20,280

Composition of Value Added:

Depreciation (company as retained funds) 1,770

Interest 2,796

Additional sales tax 914

Salaries and wages (960 + 480 + 240 + 240) 1,920 7,400

Profit before tax (balancing figure) (Company as retained funds) 12,880

Operating Profit: (Company as retained funds) - PBT + Interest Paid 15,676

276 276

Question-142 : The Balance Sheets of S Ltd for the last 3 years read as follows:

A. Calculate & analyse for the year 2014-15 and 2015-16:

i. Fixed asset turnover Ratio ii. Stock turnover Ratio iii. Debtors’ ‘turnover Ratio in terms of number of days’ iv. Debt-equity Ratio v. Current assets to current liability

B. Briefly comment on the performance of the company. Solution: Calculation of ration for the year 2014-15& 2015-16

Particulars 2014 2015 2016

Sources of Fund:

Share capital [share of ₹10 each] 2,200 2,200 3,200 Securities Premium 1,900 2,000 700 Reserves [after 10% dividend] 1,900 2,100 1,900 Long-term Loan 1,750 1,550 2,600

Total Funds 7,750 7,850 8,400

Represented by:

Fixed assets 2,800 3,200 3,500

Less: Depreciation 800 1,050 1,300

2,000 2,150 2,200

Capital WIP [work-in-progress] 1,000 1,100 1,200 Investment 600 700 650

A. 3,600 3,950 4,050

Net Current Assets:

Current Assets:

Debtors 1,800 1,950 2,150 Stock 1,900 2,050 2,700

Cash & Bank 800 800 800 Others 550 750 1,800

5,050 5,550 7,450

Less: Current Liabilities 900 1,650 3,100

B. 4,150 3,900 4,350

Total assets [A+B] 7,750 7,850 8,400

Sales [excluding excise duty and sales tax @ 20%] 4,050 4,200 5,400

Particulars 2014-15 2015-16

A. Fixed asset turnover Ratio = net sales excluding excise duty & sales tax / average Fixed asset

4200/2075 = 2.02 times

5400/2175= 2.48 Times

B. Stock turnover Ratio = Net sales excluding excise duty & sales tax / average stock

4200/1975= 2.13 times

5400/2375= 2.27 times

C. Debtors turnover ratio = Average receivables X No of days in the yr Credit sales including excise duty and sales tax

1875/5040 X 365 = 136 Days

2050/6480X 365= 115 Days

D. Debt Equity Ratio = Debt / Equity 1550/6300 = 0.25 2600/5800 = 0.45

E. Current Ratio = Current Assets / Current liability 5550/1650 = 3.36 7450/3100 = 2.40

277 277

In the costing records, Factory overhead is charged at 100% of Wages, administration overhead 10%

factory cost and selling and distribution overhead at the rate of ₹ 20 per unit sold. Prepare a statement reconciling the profit as per Cost Records with the profit as per Financial Records. Solution: :

Cost Profit & Loss Statement (For the year ended 31st march, 2016)

Particulars ₹ in lakhs

Materials 20,00,000

Wages 10,00,000

Prime cost 30,00,000

Add: Factory overhead @ 100% of wages 10,00,000

40,00,000

Less: Closing Work-in-progress 1,40,000

Factory cost (20,000 + 1,230) units 38,60,000

Administrative overheads @ 10% of Factory cost 3,86,000

42,46,000

Less: Closing stock of Finished goods 1,230 units (See Note) 2,46,000

Cost of Production (20,000 units) 40,00,000

Selling & distribution overhead @ ₹20 per unit 4,00,000

Cost of sales (20,000 units) 44,00,000

Sales Revenue (20,000 units) 50,00,000

Profit 6,00,000

BSI ltd.

Profit & Loss Account

(For the year ended 31st march, 2016)

Dr. Cr.

Particulars ₹ in

Lakhs Particulars ₹ in Lakhs

To Opening stock Nil By Sales (20,000 units) 50,00,000

To Materials 20,000 By Closing stock (1,230 units) 3,00,000

To Wages 10,00,000 By Work-in-progress 1,40,000

To Factory overheads 9,00,000

To Administrative overheads 5,20,000

To Selling & distribution over-heads

3,60,000

To Goodwill written off 4,00,000

To Interest on capital 40,000

To Net Profit 2,20,000

Total 54,40,000 Total 54,40,000

COST & MANAGEMENT AUDIT HANDBOOK

Global CMA CMA Final