Embed Size (px)

Citation preview

Outperform your loss provisions: Increase recoveries through loan restructuringSept. 2, 2020

CARISSA ROBBPresident, Constant

JEFFREY BERNSTEINSr. Principal Consultant, FICO

MIKE SISKContributing Editor, American Banker

WEBINARPANELISTS

Am

eric

an B

anke

rCon

stan

t

TODAY'S DISCUSSION

TIMELINE

Timeline to accelerated delinquency, charge-off and bankruptcy, Q4 and beyond.

PLAYBOOK EDITS TO MAKE NOW

Proactive loan restructuring, recasts as an alternative to refinancing, and short payoffs for auto.

THE CURRENT LANDSCAPE

Sharp increases of loss provisions with no visibility on duration or recovery. Why consumer/auto is particularly at risk.

A WORD ABOUT COMPLIANCE

Monitoring exams in flight, manual errors and lack of workflow are driving risk.

AMERICAN BANKER, MAY 2020

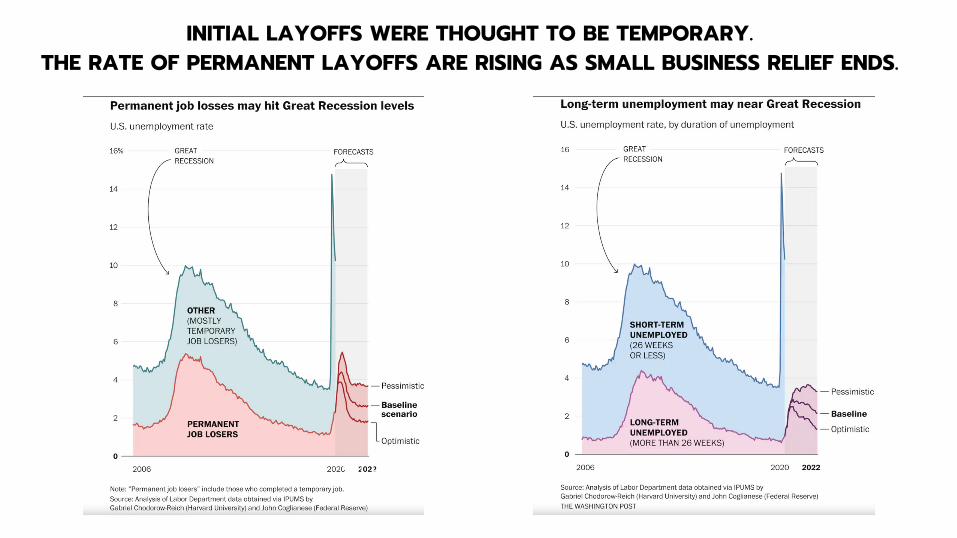

FORBEARANCE, WHILE IT CAN GO ON FOR MONTHS, DOESN’T LAST FOREVER, LEAVING BANKERS AND INDUSTRY OBSERVERS TO SPECULATE ON HOW MANY DEFERRED LOANS WILL BE UNRECOVERABLE. THE POTENTIAL DAMAGE WILL DEPEND HEAVILY ON THE SEVERITY AND DURATION OF THE PANDEMIC AND ITS AFTERMATH.

AN OBSCURED VIEW OF CREDIT QUALITY ALSO MAKES IT MORE CHALLENGING FOR BANKS TO PRICE FOR RISK AND ESTABLISH TERMS AND CONDITIONS FOR NEW LOANS, INDUSTRY OBSERVERS SAID.

THE

CU

RREN

T ST

ATE

STEVE JOBS

INITIAL LAYOFFS WERE THOUGHT TO BE TEMPORARY. THE RATE OF PERMANENT LAYOFFS ARE RISING AS SMALL BUSINESS RELIEF ENDS.

MACROECONOMIC UNCERTAINTY

Lack of visibility around duration and recovery is driving sharp increases in loan loss provisions.

UNIQUE IMPACT ON AUTO

As payment holidays expire, loss severities are likely to be impacted by used vehicle prices as repossession moratoriums expire and the fact that pre-crisis loans were underwater.

THE PERFECT STORM

The perfect storm is brewing with bank and stimulus relief slowing or expiring, continued unemployment pressures, and moratoriums lifting.

CURRENT LANDSCAPE

MARCH-JUNE

Extensions and deferral plans offered withoutproof of hardship or ability to pay.

TIMELINEACCELERATED DELINQUENCY, CHARGE-OFF & BANKRUPTCY AMID MARKET DISTORTIONS

JULY-SEPTEMBER

Initial round of short-term relief begins to expire, moratoriums lifted. Extended relief likely needed.

Q4 2020-Q1 2021

Stimulus and government relief expires, delinquency worsens, charge-off accelerates. Few relief options exist torestructure and return borrowers to performing.

UDAAP IMPACT

UDAAP violations will stem from inconsistent relief options offered to qualifying customers which will be further complicated by high numbers of case-by-case analyses expected once deferral programs end.

MILLIONS IN DEFERRAL PROGRAMS

Lack of work flow in most servicing systems forced investors to track deferrals in Excel or ad-hoc programs. Manual errors, lost files and inability to meet customer service volumes create compliance risk.

ABILITY TO REPAY ANALYSIS

New to consumer / auto is the burden to show 1) willingness and ability to repay, and 2) the solutions offered are appropriate to benefit the customer.

REGULATORYCOMPLIANCE

TOOLS AVAILABLE TODAY TO STEM LOSSES

THER

E'S

NO

SL

IVER

BU

LLET

Recast for a nominal fee to maintain current rates and protect margins.

Allow for short pay-offs to reach an amicable exit versus nominal recovery on secondary market post-repossession.

Update playbook to sustainably restructure debt beyond temporary payment relief to reduce charge-offs and increase recoveries.

DEMO OF AN AUTMATED LOAN

MODIFICATION

http://www.constant.ai/american-banker-demo

An extended demo of other relief options, voluntary surrender of collateral,

recovery/settlement and other features is available.

To see a demo, email [email protected]

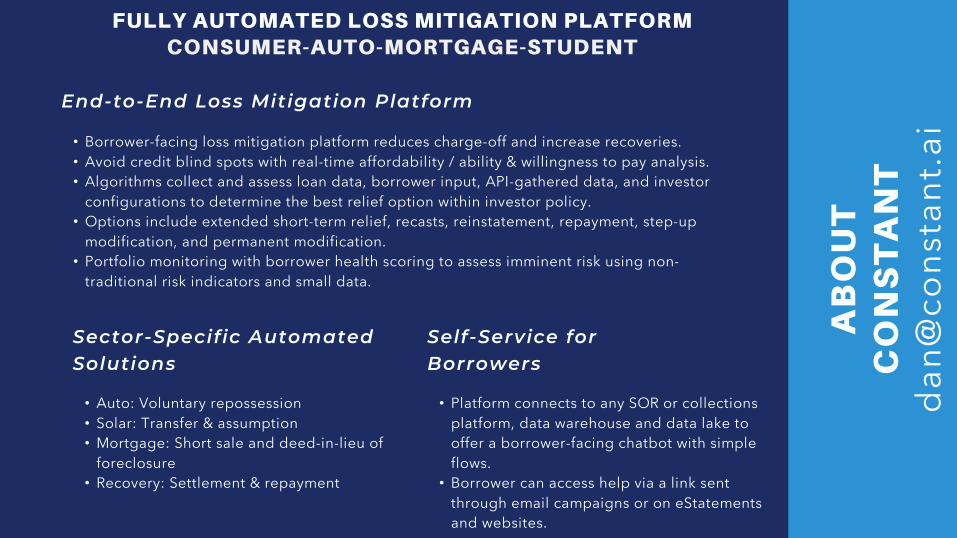

FULLY AUTOMATED LOSS MITIGATION PLATFORMCONSUMER-AUTO-MORTGAGE-STUDENT

End-to-End Loss Mitigation Platform

• Borrower-facing loss mitigation platform reduces charge-off and increase recoveries.• Avoid credit blind spots with real-time affordability / ability & willingness to pay analysis.• Algorithms collect and assess loan data, borrower input, API-gathered data, and investor

configurations to determine the best relief option within investor policy.• Options include extended short-term relief, recasts, reinstatement, repayment, step-up

modification, and permanent modification.• Portfolio monitoring with borrower health scoring to assess imminent risk using non-

traditional risk indicators and small data.

Self-Service for Borrowers

• Platform connects to any SOR or collections platform, data warehouse and data lake to offer a borrower-facing chatbot with simple flows.

• Borrower can access help via a link sent through email campaigns or on eStatementsand websites.

Sector-Specific Automated Solutions

• Auto: Voluntary repossession• Solar: Transfer & assumption• Mortgage: Short sale and deed-in-lieu of

foreclosure• Recovery: Settlement & repayment

AB

OU

T

CO

NS

TA

NT

dan@

cons

tant.ai