Embed Size (px)

Citation preview

Macroeconomicand Country Risk Outlook

EconomicOutlook no. 1214January 2015

www.eulerhermes.com

Overview 2015Not such a Grimm talebut no fabled happy ending

Economic Research

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

2

economic Research euler Hermes Group

economic Outlookno. 1214macroeconomicand Country Risk outlook

Contents

The economic outlook is a monthlypublication released by the EconomicResearch Department of Euler HermesGroup. This publication is for the clientsof Euler Hermes Group and available onsubscription for other businesses andorganizations. Reproduction is authorised,so long as mention of source is made.Contact the Economic Research Depart-ment Publication director and Chief eco-nomist: Ludovic Subran macroeconomic Research and CountryRisk: David Semmens (Head), FrédéricAndrès, Andrew Atkinson, Ana Boata,Mahamoud Islam, Dan North, DanielaOrdóñez, Manfred Stamer (Country Econ-omists), Lukas Boeckelmann (ResearchAssistant)Sector and Insolvency Research:Maxime Lemerle (Head), Farah Allouche,Yann Lacroix, Marc Livinec, Didier Moizo(Sector Advisors), Sergey Zuev (ResearchAssistant)Support: Lætitia Giordanella (Office Man-ager), Arthur Stalla-Bourdillon (ResearchAssistant)editor: Martine Benhadj Graphic design: Claire Mabille Photo credit: AllianzFor further information, contact theEconomic Research Department ofEuler Hermes Group at 1, place desSaisons 92048 Paris La Défense Cedex– Tel.: +33 (0) 1 84 11 50 46 – e-mail:[email protected] > EulerHermes Group is a limited companywith a Directoire and SupervisoryBoard, with a capital of EUR 14 509 497,RCS Paris B 388 236 853 Photoengraving: Imprimerie Adelinet –Permit January 2015; issn 1 162–2 881◾ January 20, 2015

3 edIToRIal

4 oveRvIew

8 CounTRY RISk ouTlook

10 Tale #1 - killing the goose thatlaid the Golden egg?

10 ◼ united States: The Fed will raise rates in 2015

11 ◼ united kingdom: BoE tightening; gentlydoes it...

12 Tale # 2 - The boy who criedwolf/Growth

12 ◼ brazil: Yelling “Growth”

13 ◼ mexico: Running for Growth

14 Tale # 3 - The Sleeping beauty and the Prince

14 ◼ France: Can investment jolt Sleeping Beauty back to life?

15 ◼ Germany : A prince with blind spots?

16 Tale # 4 - Hansel and Gretel lost in the woods

16 ◼ Spain: Leading the search for Growth

17 ◼ Italy: Trailing behind in the hunt

18 Tale # 5 - The Fox and the Cat

18 ◼ Russia: The Fox has many tricks

19 ◼ Poland: The Cat scaled the tree

20 Tale # 6 - The Tortoise and the Hare

20 ◼ ethiopia: First a Tortoise, now a Hare. Next?

21 ◼ South africa: Forever the Tortoise andnever crossing the finishing line?

22 Tale # 7 - The ant and the Grasshopper

22 ◼ China: Kick the saving habit

23 ◼ India: Restructuring the economy and achieving potential - Modi-nomics

24 eConomIC ouTlook SeRIeS and oTHeR PublICaTIonS

26 SubSIdIaRIeS

3

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

edIToRIal

Once upon a time…ludovIC SubRan

As the nights become increasingly dark, at least in the nor-thern hemisphere, those of us with children may pass thetime telling fables and short-stories by the fireplace – heaterswork too. Euler Hermes’ seven fairy tales on the 2015 eco-nomic outlook is a Tiger Mom’s best companion to start (al-beit very early) the development of her child’s economicskills. It all starts with: Once upon a time in a global economicmess, and ends with and the Central Banker lived happily everafter.More seriously though, 2014 ended in horror story mode.The end of the balance sheet magic conducted by the FederalReserve, the twists of political hotspots and the enchantedlower oil prices changed the plot for many companies aroundthe globe. As we turn the page to 2015, hopefully we foreseea happier ending. In high school, I had to read The Uses of Enchantment byBruno Bettelheim – I had a weird teacher that year: I know.The book unveils the impact of dark fairy tales such as theones by the Brothers Grimm for children. The darkness ofabandonment, death, wicked witches, and injuries are sup-posed to allow children to grapple with their fears and tou-ghen up all the way to adulthood. Let us hope that our ma-croeconomic fairy tales will help countries grow.[Our] NeverEnding Story starts in the US and the UK whichfind it hard to eventually kill the goose that laid the Golden

Egg: their aggressive monetary policy. In the Americas, Brazilis much like the boy who cried Wolf: it has been shoutinggrowth for quite some time without much happening, whileMexico has been acting on it. In Europe, Spain and Italy areour Hansel and Gretel, lost in the forest, in spite of somelight at the end of the tunnel: the long-awaited QuantitativeEasing. In the merry go round of money printing, it is indeedthe ECB’s turn! One question remains though: Will the Ger-man Prince awake the French Sleeping Beauty? Flying east,Russia’s many tricks have not prevented it being hunted bythe market hounds, while Poland scaled the tree like a cat. InAfrica, the South African hare may never cross the finishingline while the (many) unconventional tortoises such as Ethio-pia are doing wonders. Our volume 1 of economic fairy talesends in Asia where the fable of the Ant and the Grasshopperdepicts China’s old habits of savings (which die hard) whileModi-nomics may be India’s spring.Again, looking at 2015, story-telling (and hope) will be keyas growth continues to be fragile without the assistance of aFairy God Mother.

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

4

oveRvIew

2015 global growth should show a marginalimprovement to 2.8%, before finally expanding by3.1% in 2016. While the world started 2014 withmuch optimism it was ultimately a year ofpersistent economic disappointment andfrustration across the globe.

This year we anticipate that policy action from both the Eu-ropean and Japanese central banks will boost growth, inflationand inflation expectations but all of these are part of a multi-year recovery scenario. We believe cautious optimism re-mains vital, as in 2014, only Spain, the UK, Ireland and Indiatruly outperformed our broadly below consensus expecta-tions and even then these outperformances were modest. In 2015 advanced economies can be expected to grow at2.1%, the fastest pace since 2010. We look for the US (3.1%in 2015) to expand over 2.5 times as fast as the Eurozonewhich we anticipate will finally rise above the 1.0% mark at1.1%, the highest in four years. We expect more supportiveand importantly decisive policy to come from both the BoJand Japanese government, which will boost GDP from ananemic 2014 at 0.1% to 1.0% in 2015. Emerging Economieswill barely recover from a sub-par 3.8% performance in 2014to expand 3.9% in 2015. Emerging markets will show twocrucial, albeit very different, slowdowns. Firstly China’s policydriven and well managed slowdown to 7.3% in 2015 vs. 7.4%in 2014 will continue the focus on more domestic drivengrowth and crucially lessening over investment and excesscapacity. This contrasts strongly with the collapse in RussianGDP, with economic sanctions, capital flight and the nearhalving of the value of both the RUB and oil saw a paltry 0.2%

overview 2015Not such a Grimm tale but no fabled happy endingDAvID SEMMENS

U.S.

UK

Germany

Japan

Brazil

China

France 0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0% 1% 2% 3% 4% 5% 6% 7% 8%

Aver

age

priva

te co

nsum

ptio

n gr

owth

, 200

9-20

14

Average private consumption growth, 2000-2007

Pre versus Post crisis consumption growth

Sources: IHS, Euler Hermes

+0.2%Forecast

GDP growthin Russia

in 2014

Euler Hermes Economic Outlook no. 1214 | 2-January 2015 | Macroeconomic and Country Risk Outlook

5

in 2014, however these problems will only be compoundedinto a dire drop of -5.5% in 2015, followed by -4.0% in 2016.

Developed market demand: Time is the grea-test healer Despite recovering since the recession, across the boardconsumer demand is still weaker than previous experiencewould have expected at this point in the cycle. US, UK andGerman consumers are slowly returning towards trend levelsbut their caution following the depth of the recession is un-likely to wane in the near term. This pick up in brightest inthe US, where the pass through of lower oil prices has a moredirect impact on consumer spending and sentiment, howe-ver there is still significant underemployment and wagegrowth broadly remains unthreatening.In Europe the continued slowness of the recovery and thelack of impetus means consumers are caught in a cycle ofrighteous caution with their spending intentions, compoun-ded by anemic inflation and a lack of wage pressure. Thismaintains a lack of impetus in demand, stunting investmentgrowth. It is this vicious cycle that the ECB intends to break.We look for the ECB to provide additional monetary supportby purchasing sovereign debt in Q1-2015, possibly followedby non-financial corporate purchases later in the year, to

boost inflation expectations, increase liquidity in the marketand create appetite for portfolio diversification, lower thespread between peripheral yields, increase credit to non-fi-nancial sector and investment appetite. These moves shouldalso see further Euro weakness (1.12 at year end 2015) andhelp Eurozone exports through competitiveness gains.

Emerging market demand: Companies andconsumers need more encouragement to taketheir hands out of their pockets First for the good news, 2015 is likely to see Chinese consu-mer spending rise strongly, Euler Hermes anticipates 8.0%y/y. This is supported by strong wage growth but the rate offurther increases in consumer spending will remain muted

+7.3%China’s growth 2015 forecast to be theslowest in 25 years

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

6

while there is little downward momentum inthe savings rate. This increase will be enough inour opinion to offset the much slower growthin government spending (3.2% vs. 7.1%). We arenot concerned by the managed slowdown, butremain watchful for any signs of weakness, inparticular insolvencies. India’s continued Modi-fication should see growth accelerate further,rising 6.4% in 2015 and 5.8% in 2014. Continuedimprovement in policy credibility, both on themonetary (inflation targeting) and fiscal (greateropenness to FDI and infrastructure investment)fronts, has boosted investment and consump-tion. By contrast, Brazil is likely to see growth of0.5% in 2015 and 1.3% in 2016, below our ex-pectations for the Eurozone. Unfortunatelymuch of Brazil’s economic boom was driven byconsumer spending rather than industrial di-

versification. The new government will need toaddress the structural issues that are indicativeof stagflation, make it difficult to tackle the chro-nic under investment and ultimately are crip-pling consumer sentiment.

Global liquidity: The flood will conti-nue but from different cloudsGlobal liquidity has been an ever-rising tide sincethe Federal Reserve first began to cut interestrates in September 2007. Late 2014 saw an endto ultra-easy monetary policy in the US and 2015is likely to see the US central bank hike interestrates for the first time since 2006. At the sametime the BoJ has just increased its annual rateof QE purchases to JPY80trn from JPY60-70trn,and we anticipate that weak growth and defla-tionary concerns in the Eurozone will force theECB to act and trigger purchases of sovereigndebt. This will be supportive for financing in JPYand EUR but will also see USD strength as a fir-mer medium term trend. A stronger USD bringsits own problems as seen in taper tantrum inthe summer of 2013, however Emerging Mar-kets’ import coverage is firmer, Russia and ve-nezuela are notable exceptions. We cannotstress the importance of vigilance enough du-ring these changing times as the inter-linkagesof financial markets frequently give rise to veryreal corporate impacts. The ending of theEURCHF FX floor, earlier this year, is one suchevent. The appreciation of the CHF will benefitthose earning it and holidaying abroad, but onthe flip side Hungarian corporates have around

Real GDP growth, annual change, %

-6

-4

-2

0

2

4

6

8

10

12

Asia ex-JapanAfricaBRICU.S.Eurozone

15141312111009080706050403020100

forecasts

Regional growth rates%

Sources: IHS, Euler Hermes

40

50

60

70

80

90

100

110

120

65

60

55

50

45

40

35

30

25

20WTIRUB/USD

Dec-14

Nov-14

Oct-1

4

Sep-14

Aug-14

Jul-1

4

Jun-14

May-14

Apr-1

4

Mar-14

Feb-14

Jan-14

RUB and Oil, hand in handWeekly

Sources: Bloomberg, Euler Hermes

weights* 2013 2014e 2015f 2016f

woRld GdP GRowTH 100 2.4 2.5 2.8 3.1

advanced economies 62 1.4 1.7 2.1 2.2

emerging economies 38 4.2 3.8 3.9 4.5

north america 25 2.2 2.4 3.1 2.9

United States 23 2.2 2.4 3.1 3.0

Canada 3 2.0 2.3 2.4 2.3

latin america 8 2.7 0.9 1.3 2.3

Brazil 3 2.5 0.0 0.5 1.3

Mexico 2 1.1 2.3 3.2 3.7

western europe 23 0.0 1.2 1.3 1.6

United Kingdom 3 1.7 2.6 2.5 2.2

Sweden 1 1.3 1.8 1.5 2.1

eurozone members 17 -0.4 0.8 1.1 1.4

Germany 5 0.2 1.5 1.3 1.6

France 4 0.4 0.4 0.9 1.2

Italy 3 -1.9 -0.4 0.3 0.8

Spain 2 -1.2 1.4 1.9 1.9

Netherlands 1 -0.7 0.7 1.0 1.4

Central and eastern europe 6 1.9 1.3 -1.1 -0.1

Russia 3 1.3 0.2 -5.5 -4.0

Turkey 1 4.1 2.8 4.3 4.0

Poland 1 1.7 3.2 3.0 3.2

asia 29 4.9 4.3 4.7 5.2

China 11 7.7 7.4 7.3 7.3

Japan 8 1.6 0.1 1.0 1.5

India 3 5.0 5.8 6.4 6.8

oceania 2 2.1 2.7 2.7 2.9

Australia 2 2.1 2.7 2.6 2.9

middle east 4 2.7 3.2 3.6 3.6

Saudi Arabia 1 4.0 4.5 4.0 4.5

africa 2 4.1 4.0 4.5 5.4

South Africa 1 1.9 1.5 2.5 3.0

Morocco 0 4.4 3.0 4.2 4.5

* Weights in global GDP at market prices, 2013

Sources: IMF, IHS Global Insight, Euler Hermes forecasts

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

7

EUR4bn or 18% of total loans denominated inCHF, unhedged companies are likely to see anegative impact on profitability and their invest-ment capabilities.

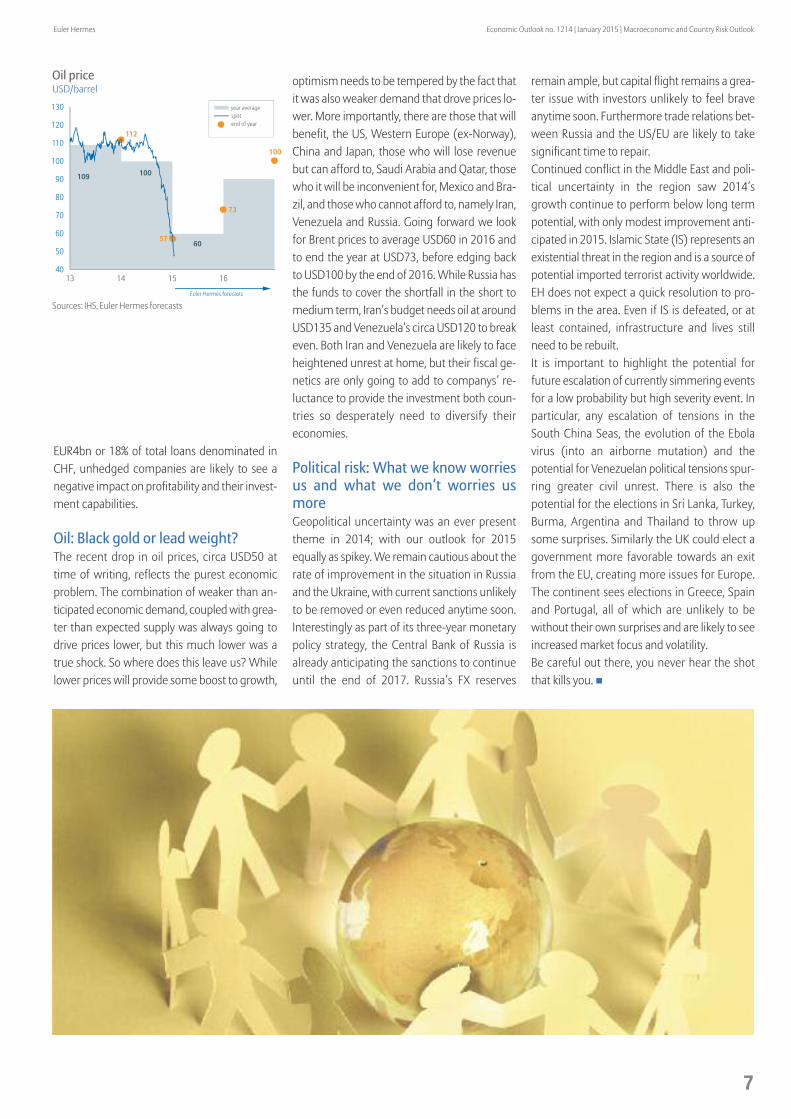

Oil: Black gold or lead weight?The recent drop in oil prices, circa USD50 attime of writing, reflects the purest economicproblem. The combination of weaker than an-ticipated economic demand, coupled with grea-ter than expected supply was always going todrive prices lower, but this much lower was atrue shock. So where does this leave us? Whilelower prices will provide some boost to growth,

optimism needs to be tempered by the fact thatit was also weaker demand that drove prices lo-wer. More importantly, there are those that willbenefit, the US, Western Europe (ex-Norway),China and Japan, those who will lose revenuebut can afford to, Saudi Arabia and Qatar, thosewho it will be inconvenient for, Mexico and Bra-zil, and those who cannot afford to, namely Iran,venezuela and Russia. Going forward we lookfor Brent prices to average USD60 in 2016 andto end the year at USD73, before edging backto USD100 by the end of 2016. While Russia hasthe funds to cover the shortfall in the short tomedium term, Iran’s budget needs oil at aroundUSD135 and venezuela’s circa USD120 to breakeven. Both Iran and venezuela are likely to faceheightened unrest at home, but their fiscal ge-netics are only going to add to companys’ re-luctance to provide the investment both coun-tries so desperately need to diversify theireconomies.

Political risk: What we know worriesus and what we don’t worries usmoreGeopolitical uncertainty was an ever presenttheme in 2014; with our outlook for 2015equally as spikey. We remain cautious about therate of improvement in the situation in Russiaand the Ukraine, with current sanctions unlikelyto be removed or even reduced anytime soon.Interestingly as part of its three-year monetarypolicy strategy, the Central Bank of Russia isalready anticipating the sanctions to continueuntil the end of 2017. Russia’s FX reserves

remain ample, but capital flight remains a grea-ter issue with investors unlikely to feel braveanytime soon. Furthermore trade relations bet-ween Russia and the US/EU are likely to takesignificant time to repair.Continued conflict in the Middle East and poli-tical uncertainty in the region saw 2014’sgrowth continue to perform below long termpotential, with only modest improvement anti-cipated in 2015. Islamic State (IS) represents anexistential threat in the region and is a source ofpotential imported terrorist activity worldwide.EH does not expect a quick resolution to pro-blems in the area. Even if IS is defeated, or atleast contained, infrastructure and lives stillneed to be rebuilt. It is important to highlight the potential forfuture escalation of currently simmering eventsfor a low probability but high severity event. Inparticular, any escalation of tensions in theSouth China Seas, the evolution of the Ebolavirus (into an airborne mutation) and thepotential for venezuelan political tensions spur-ring greater civil unrest. There is also thepotential for the elections in Sri Lanka, Turkey,Burma, Argentina and Thailand to throw upsome surprises. Similarly the UK could elect agovernment more favorable towards an exitfrom the EU, creating more issues for Europe.The continent sees elections in Greece, Spainand Portugal, all of which are unlikely to bewithout their own surprises and are likely to seeincreased market focus and volatility. Be careful out there, you never hear the shotthat kills you. ◽

112

57

73

100

40

50

60

70

80

90

100

110

120

130

13 14 15 16

year average spot end of year

109 100

60

Euler Hermes forecasts

Oil priceUSD/barrel

Sources: IHS, Euler Hermes forecasts

bahamas

belize

Gambia

macedonia

malawi

Seychelles

Togo

bb1 bb2

d4 d3

d4 d3

d4 d3

d4 d3

d4 d3

d4 d3

→ oTHeR CHanGeS

uruguay

Economic slowdown is expected with +2.7%GDP growth in 2014 and +2.9% in 2015.Private consumption is hindered by elevatedinflation, while exports are suffering fromdownside pressures on commodity prices andweak performance of major trading partners(Brazil, Argentina).

bb1 bb2

15 changesin country risk ratings4th Quarter 2014

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

8

Country RiskOutlook4th Quarter 2014

maCRoeConomIC ReSeaRCH and CounTRY RISk Team

4countries with

deterioratedratings

l

11countries with

improvedratings

k

el Salvador

Growth is subdued and public accounts aredeteriorating. The current account deficit isexpected to widen to -5.4% of GDP in 2015while reserves only cover 3 months of importsand capital inflows are decelerating. As theeconomy is dollarized, liquidity shortages area major risk.

b1 b2

Rwanda

Poverty and reliance on commodities remainan issue but political stability has helped raiseeconomic growth by +6.8% on average overthe last 5 years. The risks of non-payment arelower while the ease of doing business iscomparatively high.

d4 C3

medium termrisk:the scale comprises 6 levels :aa represents the lowest risk, d the highest.

Short termrisk :the scale comprises 4 levels :1 represents the lowest risk, 4 the highest.

R U S S I AR U S S I A

Source: Euler Hermes, as of December 17, 2014

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

9

lithuania

The recovery following the 2009 recession hasbeen strong and resilient to the Eurozonecrisis. Despite the Russian crisis, Lithuania isforecast to reach +3% growth in 2014 and+2.8% in 2015. Accession to the Eurozone inJanuary 2015 will reduce external liquidityrisk.

b2 bb2

bangladesh

Economic growth reached +6.1% in theFY2014 despite political tensions. Theeconomy is expected to pick up in 2015,supported by rising public infrastructureinvestment and gradual improvement inglobal demand. The external position remainssolid thanks to remittances while reservescover 6 months of imports.

d4 d3

Cambodia

Strong economic growth projected (+7.3% in2015) with external trade the key driver.Domestic demand should pick up due tocredit growth, long term investment inflowsand low energy prices. The current accountdeficit (-11% of GDP), although large, is not aconcern in the short-term.

d4 d3

Russia

The RUB slide in H2 2014 escalated into acurrency crisis in December and severeliquidity shortages among domestic banks. Adeep recession of -5.5% is forecast in 2015.Capital and foreign exchange controls arepossible in 2015.

C3 C4

ethiopia

Despite high poverty and periodic famines,GDP growth has been very strong and Ethiopiaremains a favoured destination of global FDIflows, particularly from Asia. The governmentrecently issued a (oversubscribed) sovereignbond.

d4 d3

10

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

10

United States: The Fed will raise ratesin 2015

Golden monetary stimulusIn the midst of the Great Recession,the Federal Reserve embarked onan aggressive course of monetarypolicy easing by using QuantitativeEasing (QE), and by setting the FedFunds interest rate to zero percent.These efforts provided unprece-dented liquidity to the financial sys-tem and kept interest rates near re-cord lows, stimulating theeconomy and supporting assetprices. Monetary policy had be-come the goose that laid the gol-

den egg. Now the time has cometo consider beginning to raise theFed Funds rate for the first time inten years, and the Fed will have todo so without causing that gooseany harm, much less killing it. Rai-sing the Fed Funds rate too sooncould choke off economic growth,but raising it too late could createinflationary pressures.

but the golden effect won’t fadetoo quicklyEH expects that the Fed is more li-kely to avoid raising rates too soonsince that has been the Fed’s his-torical pattern, this recovery hasbeen particularly fragile, and infla-tion remains subdued. Expecta-tions are that the Fed will start rai-sing the Fed Funds rate at the endof Q2-2015, and continue to raiseit at a slow, measured pace thereaf-ter. An earlier tightening could re-sult from rapidly rising inflation orfaster than expected growth. A latertightening could result from a re-lapse in the labor market or exten-ded global weakness. But whateverthe Fed decides about the FedFunds rate, the stimulative effectsof QE won’t fade for some time

since the liquidity it created, whichtook six years to build, won’t disap-pear rapidly. The goose will keeplaying golden eggs.

The outlook for 2015EH expects U.S. GDP growth of3.1% in 2015, buoyed by higheremployment with a resultingincrease in income and consump-tion, higher consumer confidence,and continuing low energy prices.Furthermore, inflation is likely toremain close to the 2% target sinceslack will remain in the labor mar-ket (the U.S. should have 5-10million more jobs at this stage ofthe recovery despite rising employ-ment,) keeping wage pressures atbay. A weak global economy, a firmU.S. dollar, and the fall in energyprices will also put downward pres-sure on inflation.

dan noRTH

Tale # 1

killing the goose thatlaid the Golden egg?

0

2

4

6

8

10Federal funds rateCore PCE y/y

14090499948984

Low U.S. inflation allows Fed to move slowly%

Sources: IHS, Euler Hermes

10The number of years

since the Fed started totighten

11

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

11

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8Rates on credit to householdsRates on credit to firms

BoE key interest rate

1413121110090807060504

The BoE announcedthe QE program andcut interest rates at 0.5%

Record low interest ratesat least until Q3/Q4 2015

BoE Interest rates

Sources: IHS, Euler Hermes

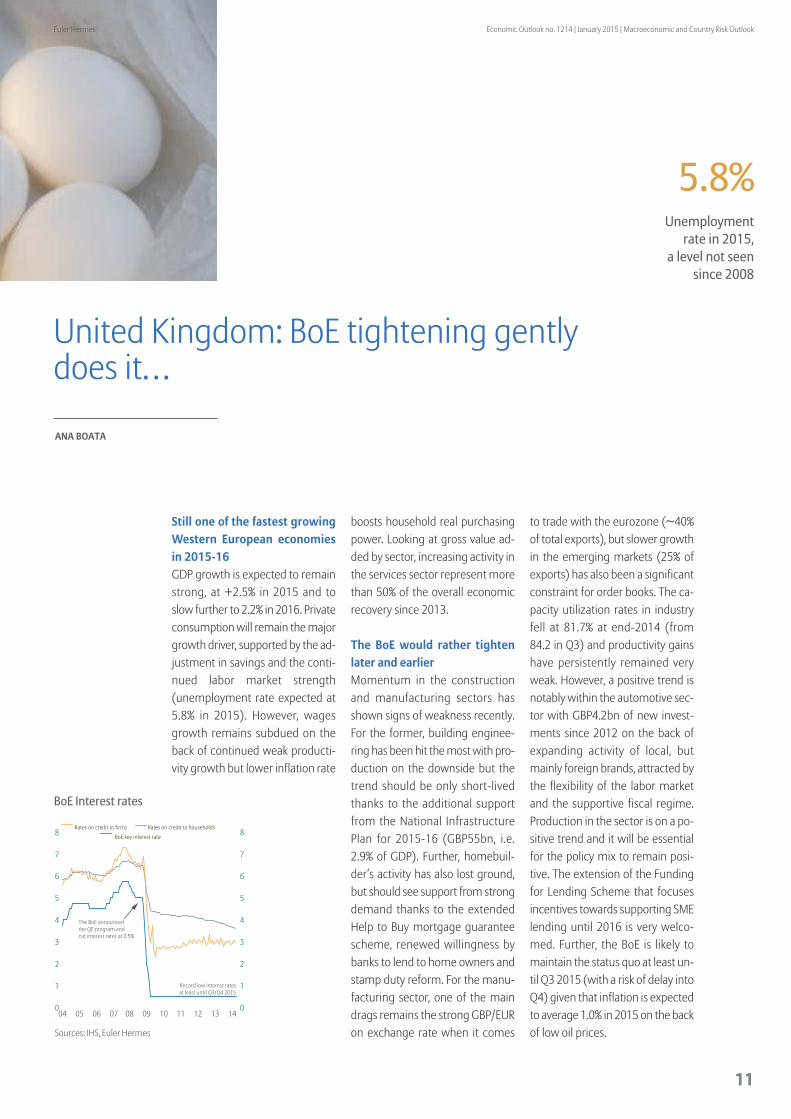

United Kingdom: BoE tightening gentlydoes it…

Still one of the fastest growingwestern european economiesin 2015-16 GDP growth is expected to remainstrong, at +2.5% in 2015 and toslow further to 2.2% in 2016. Privateconsumption will remain the majorgrowth driver, supported by the ad-justment in savings and the conti-nued labor market strength(unemployment rate expected at5.8% in 2015). However, wagesgrowth remains subdued on theback of continued weak producti-vity growth but lower inflation rate

boosts household real purchasingpower. Looking at gross value ad-ded by sector, increasing activity inthe services sector represent morethan 50% of the overall economicrecovery since 2013.

The boe would rather tightenlater and earlierMomentum in the constructionand manufacturing sectors hasshown signs of weakness recently.For the former, building enginee-ring has been hit the most with pro-duction on the downside but thetrend should be only short-livedthanks to the additional supportfrom the National InfrastructurePlan for 2015-16 (GBP55bn, i.e.2.9% of GDP). Further, homebuil-der’s activity has also lost ground,but should see support from strongdemand thanks to the extendedHelp to Buy mortgage guaranteescheme, renewed willingness bybanks to lend to home owners andstamp duty reform. For the manu-facturing sector, one of the maindrags remains the strong GBP/EURon exchange rate when it comes

to trade with the eurozone (~40%of total exports), but slower growthin the emerging markets (25% ofexports) has also been a significantconstraint for order books. The ca-pacity utilization rates in industryfell at 81.7% at end-2014 (from84.2 in Q3) and productivity gainshave persistently remained veryweak. However, a positive trend isnotably within the automotive sec-tor with GBP4.2bn of new invest-ments since 2012 on the back ofexpanding activity of local, butmainly foreign brands, attracted bythe flexibility of the labor marketand the supportive fiscal regime.Production in the sector is on a po-sitive trend and it will be essentialfor the policy mix to remain posi-tive. The extension of the Fundingfor Lending Scheme that focusesincentives towards supporting SMElending until 2016 is very welco-med. Further, the BoE is likely tomaintain the status quo at least un-til Q3 2015 (with a risk of delay intoQ4) given that inflation is expectedto average 1.0% in 2015 on the backof low oil prices.

ana boaTa

5.8%Unemployment

rate in 2015,a level not seen

since 2008

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

12

Brazil: Yelling “Growth”

a reality slapBrazilian economy largely benefi-ted from raw material revenuesand large capital inflows over 2003-2008, and scored an average an-nual growth of +5%. These re-sources were however verydemand-oriented as consumption(public+private) accounted forover 70% of real growth, while in-vestment remained relatively weak. Less favorable external conditions(slowdown of China, fall in com-modity prices, normalization ofFed’s policy, BRL depreciation)highlighted the weaknesses inhe-rent to the Brazilian economic mo-del. Local production could notkeep up the momentum of domes-

tic demand, generating internal (in-flation) and external (current ac-count deficit) imbalances, and fi-nally weighing on growth.

The main problem is lack ofinvestmentEuler Hermes estimates that the in-vestment deficit cumulated by theBrazilian economy over the 10 pastyears reaches USD1100 bn. A re-sources reallocation from consump-tion and imports to investmentwould have allowed Brazil to in-crease its investment rate to almost35% since the early 2000s. Howe-ver, the latter has remained low andstands currently at 17%, the lowestamong the BRICs and well belowthe Latin American average of 23%.The lack of investment in infra-structure combined with the per-sistent problems of protectionism,excessive bureaucracy, high laborcosts, and a complex and punitivetax system greatly hinders the na-tional business environment andcripples competitiveness.

Trying to go back on track? The newly re-elected PresidentDilma Rousseff pledged to combatinflation (+6.3% y/y in 2014) in hersecond term. Consequently, the

monetary policy tightening cyclebegun by the Central Bank in 2014(the SELIC has been raised by+75bps to 11.75%) is expected tobe pursued in 2015. Alongside, thenew Finance Minister, JoaquimLevy, committed to address fiscalaccounts. The target is to reach aprimary surplus of +1.3% of GDP in2015 and +2% in 2016-2017. Alongwith huge ongoing investment pro-grams, these policies are a welco-med first step to address macro-economic imbalances. However,they will also weigh on overall acti-vity levels, at least in the short term.Euler Hermes expects real GDP togrow by only +0.5% in 2015, afterstagnating in 2014.

danIela oRdóñez

Tale # 2

The boy who criedwolf/Growth

100

150

200

250

300

350

400MexicoBrazil

141312111009080706

Flatlining Brazilian Exports Exports, USD bn, over 12 months

Sourcs: INEGI, Central Bank of Brazil

USD1,100bn

Estimated investmentdeficit cumulated over

the 10 past years

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

13

90

95

100

105

110

115

120

MexicoBrazil

141312111009080706

Mexico marches onIndustrial Production, 100=2006, over 12 months

Sources: INEGI, IBGE

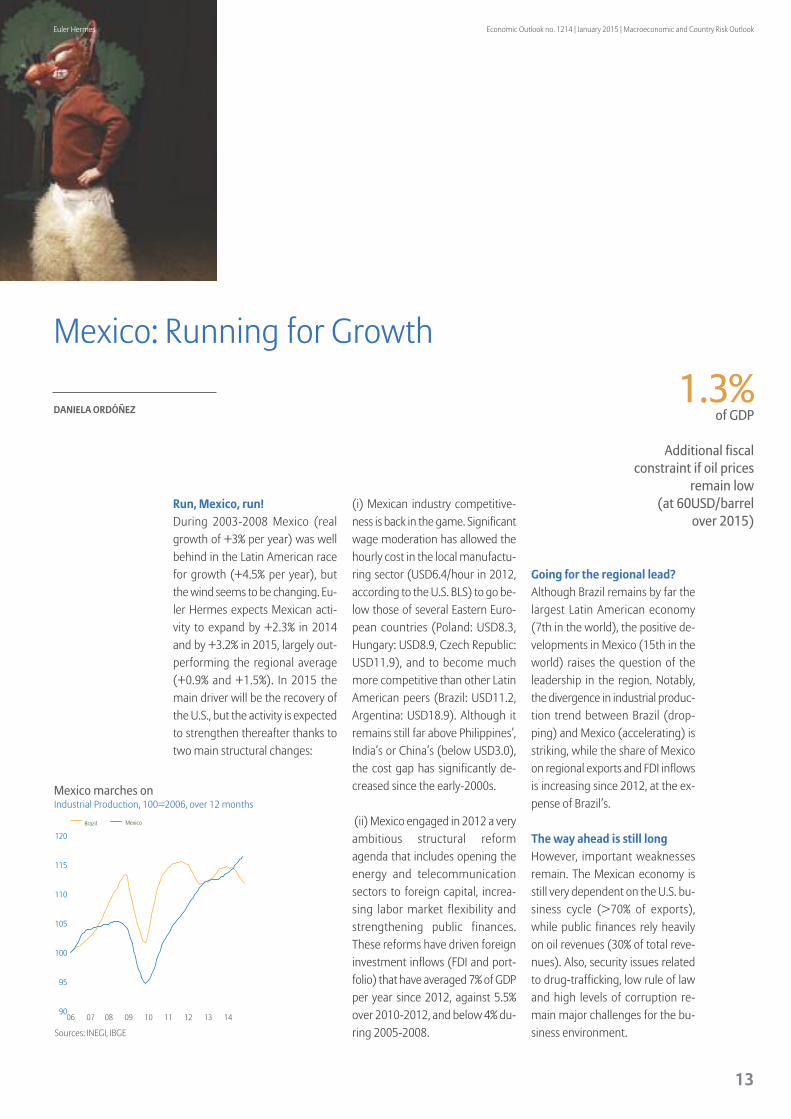

Mexico: Running for Growth

Run, mexico, run! During 2003-2008 Mexico (realgrowth of +3% per year) was wellbehind in the Latin American racefor growth (+4.5% per year), butthe wind seems to be changing. Eu-ler Hermes expects Mexican acti-vity to expand by +2.3% in 2014and by +3.2% in 2015, largely out-performing the regional average(+0.9% and +1.5%). In 2015 themain driver will be the recovery ofthe U.S., but the activity is expectedto strengthen thereafter thanks totwo main structural changes:

(i) Mexican industry competitive-ness is back in the game. Significantwage moderation has allowed thehourly cost in the local manufactu-ring sector (USD6.4/hour in 2012,according to the U.S. BLS) to go be-low those of several Eastern Euro-pean countries (Poland: USD8.3,Hungary: USD8.9, Czech Republic:USD11.9), and to become muchmore competitive than other LatinAmerican peers (Brazil: USD11.2,Argentina: USD18.9). Although itremains still far above Philippines’,India’s or China’s (below USD3.0),the cost gap has significantly de-creased since the early-2000s.

(ii) Mexico engaged in 2012 a veryambitious structural reformagenda that includes opening theenergy and telecommunicationsectors to foreign capital, increa-sing labor market flexibility andstrengthening public finances.These reforms have driven foreigninvestment inflows (FDI and port-folio) that have averaged 7% of GDPper year since 2012, against 5.5%over 2010-2012, and below 4% du-ring 2005-2008.

Going for the regional lead? Although Brazil remains by far thelargest Latin American economy(7th in the world), the positive de-velopments in Mexico (15th in theworld) raises the question of theleadership in the region. Notably,the divergence in industrial produc-tion trend between Brazil (drop-ping) and Mexico (accelerating) isstriking, while the share of Mexicoon regional exports and FDI inflowsis increasing since 2012, at the ex-pense of Brazil’s.

The way ahead is still long However, important weaknessesremain. The Mexican economy isstill very dependent on the U.S. bu-siness cycle (>70% of exports),while public finances rely heavilyon oil revenues (30% of total reve-nues). Also, security issues relatedto drug-trafficking, low rule of lawand high levels of corruption re-main major challenges for the bu-siness environment.

danIela oRdóñez1.3%

of GDP

Additional fiscalconstraint if oil prices

remain low(at 60USD/barrel

over 2015)

14

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

14

France: Can investment jolt Sleeping Beautyback to life?

Residential and public invest-ment will continue to stifle therecovery in 2015... One explanation behind France’ssleepy economic performance is anacute lack of investment. In realterms, investment is -9.7% belowpre-crisis levels. This deficit isbroad-based, echoing throughoutall components of investment. First,residential investment by house-holds has declined for 11 consecu-tive quarters and is now -24% belowthe previous peak in December2007. Following a 150% rise in hou-

sing prices between 1999 and 2011,a correction has barely begun, asevidenced by the modest -3.7% fallsince 2011. Prices-to-income ratiosremain close to all-time highs andabout 27% above long-term ave-rage, pricing most French house-holds out of the market. Second, asusual in a post-electoral year, publicinvestment is falling markedly. Assuch, orders books in private worksare about 1.5 standard deviationsbelow their long-run average, thelowest they have been since 1996.

...but corporate investmentmight finally show signs of life More worrying though is the lack ofcorporate investment. According toour forecasts, the corporate ‘invest-ment-gap’ will continue to widenin 2015, up to a cumulative EUR 78billion (or 3.5% of GDP)! The onlytwo sectors where investment hasrecovered from the crisis are Busi-ness services and Information &Communication. Investment re-mains in the doldrums in the equip-ment goods (-16% below Q1 2008levels), construction (-12%) and‘Other industrial products’ (-9%)sectors. The explanation behind this

lack of investment is twofold. First,there is a clear lack of aggregatedemand stemming from a lacklus-ter nominal growth rate (c. 1% in2014). Second, corporate marginsremain at a very low level. We be-lieve they will recover in 2015, onthe back of a moderation in inputcosts. The CICE will lower laborcosts by 2-3% whereas lower oilprices will be a boon to many sec-tors. We estimate that a sustainablefall of 25% in oil prices could leadto c. 9bn increase in total value-ad-ded and an increase of c. 0.35pp inmargins on average. The main be-neficiaries would be the Transportsector (+2.4pp rise in margins),then the 'Manufacturing of otherindustrial products' (+1.2pp). Ho-wever, we believe that the 'Loi Ma-cron' will benefit neither invest-ment nor growth in 2015. Eventhough its aims are noble (e.g., li-beralization of regulated profes-sions, reforms of labor tribunals,opening of bus transport), its scopeis probably too wide and diluted bypolitical haggling. As such, we ex-pect it to bolster GDP growth by+0.05pp (at most) per annum forthe next five years.

FRÉdÉRIC andRÈS

Tale # 3

The Sleeping beautyand the Prince

180

200

220

240

260

280

300

320

340

-25%

-20%

-15%

-10%

-5%

0%

Quarterly Investment Gap (R)

Real Investment, adjusted-pre-crisis trend

Real Investment from NFCs

15141312111009080706050403020100

forecasts

French corporate investment gap EUR bn

Source: INSEE

EUR78bn

Corporateinvestment gap

15

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

15

51.0

51.5

52.0

52.5

53.0

53.5

54.0

54.5

55.0

4

5

6

7

8

9

10

11

12

13

True unemployment rate (in %, RHS)

UE rate rate with constant participation rate (in %, RHS)

Participation rate (in %, LHS)

True participation rate (in %, LHS)

141312111009080706050403020100

Continued German labor market improvementto support growth

Sources: Bundesbank, Euler Hermes

Germany: A prince with blind spots?

on course for a moderate recov-ery...After 2 years of stagnating growth,Germany looks ahead to a path ofa modest recovery. Consumerspending has remained a swordwith a sharp blade so far. Wage andemployment growth are expectedto remain solid. On the one handthe introduction of the new mini-mum wage at EUR8.50, will helplift wages 3.3% y/y. On the otherhand we predict 274,000 low-wagejobs will be eliminated by thischange, but unemployment will

stay low, circa 6.5%. Consumerspending should gather furthermomentum, reaching full-year ex-pansion of +1.3% in 2015 after anincrease of +1.1% in 2014. After adisappointing performance in2013, deducting -0.5% from GDPgrowth, net exports are about toregain its role as one of Germany’sgrowth engines – or as the Prince’shorse to stay with the picture. Tradesanctions in Russia, the slowinggrowth in China and Brazil and theerosion of the competitive positionare certainly negatives. However,the depreciation of the Euro andthe impact of lower oil price morethan offset those. In 2015 as awhole, Euler Hermes expects ex-ports to rise by +4.1% and importsby +3.8%. As a result, net exportsshould contribute 0.4-0.5pps tooverall growth in 2015.

...but investments are a blindspotOn the downside, low private in-vestment activity is holding Ger-many back from higher GDPgrowth. This reflects: i) a weak in-dustry production (down to -0.5%y/y in November from +4.8% y/y inJanuary) and a capacity utilization

rate that remains little above itslong term average (83%), sugges-ting that economic activity is notbuoyant enough to support addi-tional investment into equipment;ii) insufficient additional demandon the back of weak GDP growthin the last three quarters of 2014;and iii) cautious surrounding theeconomic outlook caused by geo-politics. While much needed publicinvestment continues to be de-layed, residential investment in-creased since 2010 by 5.9% on ave-rage each year. Given the resilientlabor market, a supply bottleneckin urban housing and positive fi-nancing conditions we expect acontinuation of residential invest-ment growth in 2015.

lukaS boeCkelmann

+1.3%Growth of consumer

spending in 2015

16

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

16

Spain: Leading the search for growth

The sun is finally risingAfter 5 years of recession combinedwith difficult adjustments and re-forms, the Spanish economy ap-pears to have finally found the wayout of the economic woods. EulerHermes expects real GDP to ex-pand by +1.4% in 2014, beforepicking up to +1.9% in 2015 and+1.9% in 2016, outperforming Ger-many, Italy and France. Investmentand exports - further boosted bythe lower euro - will continue to bethe main drivers of the recovery,

also helped by the fall in oil prices.Private consumption should alsocontinue growing, but without ac-celerating since consumer confi-dence is on a downward trendsince June 2014.

but the way back is very steep... The recovery begins from very lowlevels. The real GDP still stands -6%below pre-crisis level, while GDPper capita has fallen to 2003 levels.More worrying, both industrial pro-duction and retail sales stand ap-proximately at -30% below pre-cri-sis level and the recovery is verygradual. Public and private debtsremain very elevated, while finan-cing conditions for corporations arestill stretched. Credit to NFC is stillcontracting (-13% y/y in November2014) and interest rates remainhigh despite ECB action. Last butnot least, despite on a downwardtrend, insolvencies remain morethan five times above 2007.

...and full of risks Several risks hamper our centralscenario. Lower than expected per-formance of trade partners (Euro-zone, but also Latin America) could

limit export expansion. If the ECBactions do not succeed to addressdeflationary pressures, the ongoingdeleveraging process could be obs-tructed. Finally, political issues arenot to be underestimated. Notably,Catalonia’s (20% of GDP) potentialindependence could remain a ma-jor issue in the near term, notablyas we get closer to the December2015 general elections.

SaRaH boSSe-PlaTIÈRe, danIela oRdóñez

Tale # 4

Hansel and Gretellost in the woods

-15

-10

-5

0

5

10

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Real retails sales growth (y/y, %, left axis)Consumer confidence (%, balance of opinion, right axis)

14131211100908070605

Spanish consumer confidence and retail sales %

Sources: Central Bank of Spain, INE

-25%Gap of the credit

to the private sectorrelative to pre-crisis

levels

17

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

17

-20

-17

-14

-11

-8

-5

-2

1

4

60

62

64

66

68

70

72

74

76

78

80

Investment Q4/Q4 (lhs)Capacity utilization rate (rhs)

16151413121110090807

forecasts

Italian investment and capacity utilizationrates in industry4Q/4Q

Sources: IHS Global Insight, Euler Hermes forecasts

Italy: Trailing behind in the hunt

Three straight years of reces-sion to finally end in 2015...GDP growth is expected to turn po-sitive in 2015 (+0.3% after -0.4% in2014) thanks to slowly recoveringprivate consumption and positivenet exports. Although, Italian ex-ports still lag peer group perfor-mance on the back of slow com-petitiveness adjustment, Italy willbe one of the main winners from alower euro (expected at 1.12 in Q42015) given that 60% of total ex-ports are extra-eurozone and thatthe export structure remains highly

sensitive to price variations. Further,the Italian export culture has stron-gly developed over the past yearswith 212,000 exporting companiescompared to 120,000 in France and270,000 in Germany.

…but more than 10 years willbe needed to fill in the invest-ment gapWe do not expect investmentgrowth to turn positive until 2016,continuing the major drag ongrowth after eight consecutiveyears of contraction (-28% declinein real terms since Q1 2007 peak).In 2015, the total investment gapcompared to 2007 would reachEUR60bn. Part of the issue seemsto be structural as even prior to thecrisis GDP growth has been veryweak (+1.5% on average on realterms between 2000 and 2007 and2% of average inflation). As a conse-quence, firms’ turnover growth hasbeen flat and even dropped by -20%over the past ten years for durableconsumer goods. Indeed, weaklong-term consumer spendinggrowth (+1.1% pre-crisis average)has impaired volumes and increa-sing deflationary pressures since

2013 have amplified downsidepressures on firms’ revenues. Fur-ther, over the past years, the envi-ronment has increased theconstraints from expenses. First,firms’ high indebtedness (70% ofGDP) and the weak state of thebanking sector have been a majordrag on financing. Second, still ele-vated fiscal pressure (total tax ratestands at 65% of profits vs 44% inthe eurozone) have added to al-ready very high input prices. Profi-tability stands at record lows andalthough we are still far from ahappy ending, a slightly positivetrend is expected in 2015 thanks tolower oil prices, a slight improve-ment in financing conditions, sta-bilizing wages and payment terms(although at an elevated level of100 days).

ana boaTa

2016slightly positive

investment growth forthe first time in eight

years

18

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

18

Russia: The Fox has many tricks

lack of structural change back-firesRussia has avoided serious econo-mic transformation ever since thedissolution of the Soviet Union in1991. Large windfall oil revenuesthanks to the rapid rise of global oilprices from 2000 to 2008 helpedthe “fox” to achieve a lasting boom,large current account surplusesand the consolidation of its publicfinances after the 1998 sovereigndefault, but also aggravated its de-pendence on hydrocarbon pro-ducts and its vulnerability to eco-nomic and political shocks. Theunwillingness to improve the un-

favourable economic structure ingood times backfired heavily du-ring the Great Recession when theglobal financial crisis combinedwith sharply lower oil prices pus-hed Russia into a severe recession(-7.8% in 2009).

baseline scenario: Currency cri-sis will cause a sharp recessionin 2015In 2014, U.S. and EU sanctionsagainst Russia combined with shar-ply falling global oil prices sincemid-year have pushed the Russianeconomy again on the brink of asevere recession. Market confi-dence has deteriorated with increa-sing speed, reflected in large netcapital outflows, sharply falling in-vestment, rising borrowing costsfor Russian banks and companiesand the depreciation of the RUBwhich turned into a full-fledged ex-change rate crisis in late 2014. RealGDP growth, already on a down-trend in 2013 (+1.3%), will comein at just +0.2% in 2014 and EulerHermes expects a swing to a sharpcontraction of about -5.5% in 2015.The much weaker RUB in 2015 willresult in marked declines of consu-mer spending and investment

while lower oil prices will limit po-tential fiscal stimulus. Both exportsand imports are forecast to de-crease but the latter will drop moresharply owing to the depreciatedcurrency. The introduction of capi-tal controls on investment flowsand foreign exchange controls (for-ced RUB buying by companies) islikely in 2015. However, a sovereigndefault in not expected in 2015 asthe government’s reserves aremuch higher than in 1998. The re-cession is forecast to continue in2016, with GDP declining by about-4.0%.

downside risks of a black SwaneventWhile the probability of a ‘Back tonormal in 2015’ scenario is negli-gible, there are considerable down-side risks to our baseline scenario.An escalation of Western sanctions(for example on the SWIFT pay-ment system) or full-fledged capi-tal controls (including current ac-count transactions) would mostlikely result in a severe economiccollapse, with real GDP decliningby as much as -15%. A sovereigndefault would be possible in 2016in such a worst case scenario.

manFRed STameR

Tale # 5

The Fox and the Cat

-10

-5

0

5

10

15

20 Current account balance (% of GDP)GDP growth

15141312111009080706050403020100

forecasts

Russian GDP growth and current account balance

Sources: Central Bank of Russia, Euler Hermes

-5.5% GDP contraction

expected in 2015

1919

-7-6-5-4-3-2-1012345678

Central Europe EU ex. PolandPoland

1615141312111009080706050403020100

forecasts

Polish GDP growth%

Sources: IHS Global Insight, Euler Hermes

Poland: The Cat scaled the tree

Cats tend to land on their feetIn the early 2000s, Poland was oftenreferred to as the laggard in Centraland Eastern Europe (CEE), trailingits fellow EU members in the regionin terms of GDP growth and re-forms. But thanks to embarking onsound monetary policy, includinga flexible exchange rate, and ade-quate fiscal policy, combined withan enhanced structural reformagenda, Poland has overtaken itsregional peers since 2007. Suppor-ted by solid economic policies andless dependence on external de-mand as compared to the peers,

the Polish economy showed mar-ked resilience to the 2009 globaleconomic crisis, being the only EUeconomy that avoided recession inthat year. Notably, Poland got ac-cess to a USD20 bn arrangementunder the IMF’s Flexible Credit Line(FCL) in 2009, a facility which is onlyoffered to strongly performing eco-nomies with a solid record of timelyand effective economic policy ad-justments. Meanwhile, the FCL hasbeen increased to USD34 bn andextended until January 2015. Whilethe authorities have never tappedthe FCL, the precautionary arran-gement provides important insu-rance against external risks.

Rebound in 2014 despite nega-tive impact from RussiaFollowing a slowdown to averageannual growth of +1.8% in 2012-2013, the economy rebounded to+3.4% y/y growth in the first threequarters of 2014, driven by robustprivate and public consumptionand surging investment. Thecontribution of net exports shiftedinto negative territory as real im-port growth accelerated to +8% y/y,outpacing real exports which in-

creased by +5.2% y/y, roughly thesame as in full-year 2013. Russia isthe main reason why exportgrowth did not pick up. While Po-lish total nominal exports of goodsrose by +4.7% y/y (those to the EUby +7.4% y/y) in the first 10 monthsof 2014, exports of goods to Russiacontracted by -13% y/y, reducingthe Russian share in Polish exportsto 4.4% from 5.3% in 2013.

Growth to remain resilientGoing forward, Euler Hermes ex-pects the servant-turned-princessCinderella to remain one of the fas-test growing CEE economies in2014-2016. Real GDP is on track toexpand by about +3.2% in full-year2014. Robust consumer spendingand investment should continue tosupport the economy in the nexttwo years while a further declineof exports to Russia will weigh so-mewhat on external demand, sothat annual growth of about +3%is forecast in 2015-2016.

manFRed STameR +3% GDP growth

in 2015

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

20

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

20

Ethiopia: First a Tortoise, now a hare. Next?

left behind at the gun? nowhare-like rate of growth Despite its geographic size andlarge population (almost 92 millionin 2012), Ethiopia was seen as asleeping giant among regionaleconomies. Media coverage ofdrought and human distress did lit-tle to dispel that image. Annual realGDP growth averaged only +2.9%in 1991-2000 but +9% since thatlatter year. Moreover, annual GDPgrowth was in double digits in se-ven out of the ten years up to end-

2013 and the annual average overthat period was +10.9%, comparedwith an average +5.1% for Sub-Sa-haran Africa as a whole. Such highgrowth rates reflect factors that in-clude: (i) the low starting base, (ii)external debt relief that freed upresources for more productive use,(iii) improved economic manage-ment and (iv) large inflows of FDI.Indeed, the Ethiopian tortoise (slowto get going) is likely to continuewith hare-like economic expansion,with GDP growth this year of +8.5%and +8% in 2015.

ethiopia is the africa Risingstory, but for how long ?In a 2014 assessment, UNCTAD lis-ted Ethiopia as one of the world’stop destinations for FDI. Total in-flows in 2013 were USD953 million,with a large proportion comingfrom Asia to boost the country’s in-dustrial base and improve and ex-tend infrastructure. Moreover, a re-cent sovereign bond issue of USD1billion was heavily subscribed, sug-gesting that investor confidence inthe country’s potential remainsstrong. Ethiopia is living the dream,or fable.

The longer-term outlook forgrowth is generally positive, al-though much depends on mainte-nance of domestic and regionalstability and on uncertain availabi-lity of water supplies. The WorldBank estimates that Ethiopia hashydropower generation potentialsecond only to DR Congo in Africa.The government has ambitiousplans for the country to becomethe “water tower of Africa”. A 25-year programme to increase hydro-electric capacity to 37,000 MW by2037 includes a 6,000 MW GrandEthiopian Renaissance Dam on theBlue Nile (scheduled for comple-tion in 2018). However, there areenvironmental concerns relating todam building on major rivers andEgypt, in particular of neighbouringcountries, is concerned about thecontrol of Nile waters that will beexerted if these projects are com-pleted.

andRew aTkInSon

Tale # 6

The Tortoise and theHare

0

200

400

600

800

1,000

1312111009080706050403020100

Ethiopia inward FDI flowsUSD mn

Sources: UNCTAD, IHS, Euler Hermes

+10.9%Ethiopia’s annual

avearge GDP growth2004-13, compared

with…

…South Africa’s

+3.4%annual average GDP

growth 2004-13

21

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

21

-4

-2

0

2

4

6

8

10

12

14

Ethiopia GDP growth

South Africa GDP growth

161514131211100908070605040302

Ethiopia GDP per capita average growth

South Africa GDP per capita average growth

forecasts

South Africa and Ethiopia GDP growth%

Sources: IHS, Euler Hermes forecasts

South Africa: Forever the tortoiseand never crossing the finishing line?

a successful political transitionis not enough South Africa’s metamorphosis froman apartheid state to a rainbow na-tion was almost unilaterally applau-ded. Indeed, it was a significant po-litical/social transition. However,long-term (1999-2013) averageannual GDP growth is +3.3%, com-pared with a generally acceptedminimum of around +5% each yearrequired to be able to provide abackground to generate jobs andaddress well-established social ine-qualities. We expect GDP growthof +1.5% in 2014 and +2.5% in2015, so the outlook remains mar-kedly below potential (tortoise-like)and also below requirements of anemerging nation.

GDP growth this year will be the lo-west since the recession in 2009and the outlook does not appear li-kely to bring about hare-like ratesof expansion. This partly reflectsglobal developments (weak de-mand for commodities and weakprices) but also domestic structuralfactors (including large income ine-qualities, an active labour move-ment, weak job growth, stubborninflationary pressures and powershortages). Policymakers have tocontend with a deteriorating inves-tor climate and dependence on ex-ternal capital, with financial mar-kets under pressure, exemplifiedby current ZAR weakness. The tor-toise looks likely to remain a tor-toise.

others in the race Ethiopia and South Africa are buttwo in the race. Ethiopia’s track re-cord (slow to get going but puttingin a current sprint) is not withoutsome regional competition. Somewho were relatively quick out of thestarting blocks (including Ghanaand Zambia) are having a breatherat the side and taking on IMF waterbut others (including Angola, Mo-zambique, Nigeria, Rwanda andTanzania that also recorded annual

average GDP growth of over +7%in 2004-13) appear likely to carryon recording hare-like rates ofgrowth. But who will hit the mara-thon’s infamous ‘wall’ and staggeroff course and who will get overthe finishing line? In reality, ofcourse, it is not a race with a win-ning line and medals, it is a deve-lopment process. There will alwaysbe hares and tortoises and coun-tries will sometimes be one and so-metimes the other. So, the winnerin our fable is…Africa!

andRew aTkInSon

•

22

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

22

China: Kick the saving habit

economic growth is supportedby rise in external trade and pol-icy stimulusEconomic growth remained resi-lient in 2014 (+7.4%) supported byimproving external demand andaccommodative macro-policies.EH expects the economy to stabi-lize at 7.3% in both 2014 and 2015.Investment is set to decelerate fur-ther reflecting onging adjustmentin real estate and construction, andlocal governement deleveraging.Exports are set to pick up speedwith the gradual improvement in

global demand. The policy mix willlikely remain accomodative to keepgrowth in an acceptable range (7%to 7.5%) , maintain absolute em-ployment growth (+10 million jobsper year) and ease deflationnarypressures (inflation at +1.5% in De-cember far below 2014 target of+3.5%). Fiscal stimulus will focuson supply side measures (tax cutsfor SME) and rising infrastructurespending to limit distortions. Mo-netary policy will likely be more ac-comodative. PBOC move in No-vember (-40 bps policy rate cut)showed a shift in the authority’sstrategy. Whereas previously itsgoal has been to use only targetedmeasures, it now aknoweledgedthe need to use more conventionalmeasures to keep growth steady.With elevated deflationary pres-sures and surveys pointing to weakdemand growth in the short term,further support in H1 2015 is likely.

unlock savings will be key toenhance long term growthCounter-cyclical macro policies willbe accompanied with structural re-forms to generate self-sustaininggrowth in private demand. With

national saving averaging 50% GDP,China has the potential to generatea firm domestic consumption led-growth model with its own re-sources. However, structural bot-tleneck including weak socialsecurity system and still highly re-gulated financial market continueto fuel precautionary saving (andthus limiting consumptiongrowth). Going forward, the go-vernment is set to accelerate re-forms to address these issues. No-vember’s rate cut wasaccompanied with two positive de-velopments on the financial libera-lization front: the Central Bank rai-sed the maximum deposit rate to1.2 times the benchmark (from 1.1times previously); the authoritiesissued a draft of plan to insure upto RMB500,000 per saver at eachbank covered. Removing control ondeposit rates will be pivotal for fu-ture consumption with higher re-turns for savers. While household’sconsumption represented circa36.4% GDP (USD3.6 trillion ≈ Ger-man GDP) in 2014, EH expects agradual increase from 2015 on-wards (+9% in nominal terms in2015).

maHamoud ISlam

Tale # 7

The ant and theGrasshopper

0

10

20

30

40

50

60

141312111009080706050403020100

forecasts

China national saving rates(% GDP)

Source: National Statistical Office

USD 3.6trillion

Householdconsumption

23

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

23

0

2

4

6

8

10

12

14

16

0

5

10

15

20

25

30

35

40Domestic bank loans (y/y; rhs)Policy rate (lhs)

14131211100908070605040302

India policy rate and domestic bank loans

Sources: IHS Global Insight, Euler Hermes

India: Restructuring the economyand achieving potential – Modi-nomics

Phase 1: lower inflation andstop capital outflows (2014)Economic fundamentals are im-proving with evidence being showin stronger GDP growth (above 5%y/y in Q2 and Q3 2014) supportedby services activities and privateconsumption. Inflationary pres-sures have eased significantly (CPIy/y at 5% in December 2014 com-pared to 9.9% end 2013) due tomonetary tightening and weakcommodity prices. The current ac-count deficit narrowed (-1.5% GDPin 2014 from -2.3% in 2013) reflec-ting a rise in exports and a reduc-tion in commodities imports bill.

The combination of more proactivecentral bank policy and the changeof leadership have strengthenedconfidence, sustained capital in-flows (FDI inflows up to 2% GDP in2014 from 1.5% in 2013) and hel-ped stabilize the currency. The out-look is broadly positive for 2015 and2016 with growth to exceed 6%. Ri-sing demand in the US and the Eu-rozone will support further impro-vement in the trade balance.Private consumption is set to reco-ver gradually on the back of lowerinflation. vulnerabilities to externalshocks have eased with import co-ver exceeding 6 months, twins de-ficit reducing and increased policycredibility.

Phase 2: Rebuild buffer to sup-port growth (2015 onwards)Fostering investment will probablybe the first priority of the authoritiesin 2015. Despite a rise in confi-dence, investment growth did notreally pick up - mainly due constrai-ned by difficult credit conditionsand concerns about the global en-vironment. The government willneed to build a sufficient buffer toraise public investment withoutworsening debt sustainability. It isalso vital to take further steps to

improve the business environmentto make India more attractive forforeign direct investment. Regar-ding these two items, the Modi go-vernment has made significantprogress ending diesel subsidiesand increasing foreign direct in-vestment limits in key sectors (De-fense, insurance, real estate andrailway infrastructure). This pro-gress should accelerate in 2015 asthe Expenditure ManagementCommission should deliver recom-mendations to reduce the deficit inFebruary and reform subsidies(which cost 2.3% GDP in FY2013-2014). Regarding monetary policy,the Central Bank stance will haveto provide greater support to creditgrowth while ensuring macro-fi-nancial stability: Bank credit dece-lerated to 11% y/y in H2 2014 from14% in H1. Falling commodityprices will probably keep inflationbelow 6% In H1 2015 (RBI target is6% by January 2016) allowing mo-netary easing. However, ongoingfiscal consolidation, divergence inadvanced economies monetary po-licies and uncertainties about oilprices suggest a gradual approachwith another rate cut (-25bp) in H12015, after a first one (- 25bp) inJanuary 2015.

maHamoud ISlam

2.3%GDP

Cost of subsidies(FY2013-2014)

24

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

economic Researcheuler Hermes Group

economic outlookand otherpublications

Already issued:

no. 1195-1196 ◽ macroeconomic, Risk and Insolvency outlook The world at a crossroads

no. 1197 ◽ Global Sector outlook Reconciling economic (dis)illusions and financial risks

no. 1198 ◽ Special Report The Mediterranean: Turning the tide

no. 1199 ◽ macroeconomic and Country Risk outlook Half-baked recovery

no. 1200-1201 ◽ business Insolvency worldwide Patching things up: Fewer insolvencies, except in Europe

no. 1202-1203 ◽ macroeconomic and Country Risk outlook Top Ten Game Changers in 2014: Getting back in the game

no. 1204 ◽ Global Sector outlook All things come to those who wait: Green shoots for one out of four sectors

no. 1205-1206 ◽ macroeconomic and Country Risk outlook Hot, bright and soft spots: Who could make or break global growth?

no. 1207 ◽ business Insolvency worldwide Insolvency World Cup 2014: Who will score fewer insolvencies?

no. 1208-1209 ◽ macroeconomic, Country Risk and Global Sector outlook Growth: A giant with feet of clay

no. 1210 ◽ Special Report The global automotive market: Back on four wheels

no. 1211-1212 ◽ business Insolvency worldwide A rotten apple can spoil the barrel Payment terms, past dues, non-payments and insolvencies: What to expect in 2015?

no. 1213 ◽ Special Report International debt collection:The Good, the Bad and the Ugly

no. 1214 ◽ macroeconomic and Country Risk outlook Overview 2015: Not such a Grimm tale but no fabled happy ending

To come:

no. 1215 ◽ Special Report

Economic Outlookno.1210 August September 2014

Special Reportwww.eulerhermes.com

The globalautomotive marketBack on four wheels

Economic Research

Economic Outlookno.1213 December 2014

Special Reportwww.eulerhermes.com

Internationaldebt collectionThe Good, the Bad and the Ugly

Economic Research

Business Insolvency Worldwide

Economic Outlookno. 1211-1212October-November 2014

www.eulerhermes.com

A rotten applecan spoil the barrelPayment terms, past dues, non-paymentsand insolvencies: What to expect in 2015?

Economic Research

Macroeconomic, Country Riskand Global Sector Outlook

Economic Outlookno. 1208-1209June-July 2014

www.eulerhermes.com

Growth: A giantwith feet of clay10 industry short stories exposemacroeconomic fragility

Economic Research

https://www.youtube.com/watch?v=xYS8qaNrUaU

25

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

◽An aditional USD88bn of U.S. exports in 2015 > 2014-12-02◽Chinese growth - What could possibly go wrong? > 2014-12-02◽U.S. businesses’payment behaviors point to slowed GDP and mixedpicture for key industries > 2014-11-18◽Spain: Cautiously taking the bull by the horns > 2014-10-08◽Chinese exports 2014-2015: Another US300bn > 2014-10-07◽Russia and the West: Tough Love? > 2014-09-12 ◽Non-payments in Italy: It’s not over… yet! > 2014-09-04 ◽Don’t cry too much for Argentina > 2018-08-08 ◽ Fertilizer: The seed growing secretly > 2014-08-05◽ Road transport: Labor costs explain the large gap in profitability inEurope > 2014-07-08 ◽The European electricity market under strong pressure > 2014-07-05◽Thailand: Another coup challenges the country’s economicresiliencel > 2014-06-06◽2014 World Cup : more inflation than growth in Brazil > 2014-06-06◽Tire industry on a roll >2014-04-17◽Putinomics: Tightrope walking > 2014-04-10

EconomicInsight

◽Azerbaijan > 2014-12-17◽Bangladesh > 2014-12-17◽Cambodia > 2014-12-17◽Denmark > 2014-12-17◽El Salvador > 2014-12-17◽Ethiopia > 2014-12-17◽Gabon > 2014-12-17◽Germany > 2014-12-17◽Honduras > 2014-12-17◽Iceland > 2014-12-17◽Israel > 2014-12-17◽Laos >2014-12-17◽Latvia > 2014-12-17◽Lithuania > 2014-12-17

◽Mali > 2014-12-17◽Mozambique > 2014-12-17◽Myanmar > 2014-12-17◽Norway > 2014-12-17◽Paraguay > 2014-12-17◽Rwanda > 2014-12-17◽Sri Lanka > 2014-12-17◽Sweden > 2014-12-17◽Switzerland > 2014-12-17◽Taiwan > 2014-12-17◽Trinidad & Tobago > 2014-12-17◽Turkey > 2014-12-17◽Uganda > 2014-12-17◽Uruguay > 2014-12-17

CountryReport

weeklyexport RiskOutlook

◽The paper industry in Italy: Time to turn the page > 2014-12-16◽Consumer electronics: Only a timid rebound in 2015 > 2014-12◽Construction in Italy: Only a timid rebound in 2015 > 2014-12-02◽Textile & Clothing in Germany: A two-geared reality > 2014-10-31◽Textile & Clothing in Italy: Bronze medal on the international podium, but facing obstacles > 2014-10-31◽Italian car sector: Time to do an oil change > 2014-10-22 ◽U.S Automotive > 2014-10-03◽U.S. Construction > 2014-10-03◽Italian steel at a crossroads > 2014-09-30◽Der Automobilweltmarkt: Wieder auf allen vier Rädern > 2014-09-19◽Agrifood in the Netherlands The bumpy road continues > 2014-09-18

IndustryReport

http://www.eulerhermes.com/economic-research/economic-publi-cations/Pages/Weekly-Export-Risk-Outlook.aspxN

TheEconomicTalk

N

26

Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook Euler Hermes

> argentinaSolunionAv. Corrientes 299 C1043AAC CBA,Buenos AiresPhone: + 54 11 4320 9048

> australiaEuler Hermes Australia Pty LtdLevel 9, Forecourt Building2 Market StreetSydney, NSW 2000Phone: + 61 2 8258 5108

> austriaAcredia Versicherung AGHimmelpfortgasse 291010 ViennaPhone: + 43 5 01 02-1111

Euler Hermes Collections GmbHZweigniederlassung ÖsterreichHandelskai 3881020 ViennaPhone: + 43 1 90 227 14000

> bahrainPlease contact United Arab Emirates

> belgiumEuler Hermes Europe SA (NV) Avenue des Arts — Kunstlaan, 56 1000 BrusselsPhone: + 32 2 289 3111

> brazilEuler Hermes Seguros de Crédito SAAvenida Paulista, 2.421 — 3° andarJardim PaulistaSão Paulo / SP 01311-300Phone: + 55 11 3065 2260

> CanadaEuler Hermes North America InsuranceCompany1155, René-Lévesque Blvd WestBureau 2810Montréal Québec H3B 2L2Phone: +1 514 876 9656 / +1 877 509 3224

> ChileSolunion Av. Isidora Goyenechea, 3520SantiagoPhone: + 56 2 2410 5400

> ChinaEuler Hermes Consulting(Shanghai) Co., Ltd. Unit 2103, Taiping Finance Tower, No. 488 Middle Yincheng Road, Pudong New Area, Shanghai, 200120Phone: + 86 21 6030 5900

> ColombiaSolunionCalle 7 Sur No. 42-70Edificio Fórum II Piso 8MedellinPhone : +57 4 444 01 45

SubsidiariesRegistered office:Euler Hermes Group 1, place des Saisons 92078 Paris La Défense - FrancePhone: + 33 (0) 1 84 11 50 50

www.eulerhermes.com

> Czech RepublicEuler Hermes Europe SA organizacni slozkaMolákova 576/11186 00 Prague 8Phone: + 420 266 109 511

> denmarkEuler Hermes Danmark,filial of Euler Hermes Europe SA, BelgienAmerika Plads 192100 Copenhagen OPhone: + 45 88 33 33 88

> estoniaPlease contact Finland

> FinlandEuler Hermes Europe SASuomen sivuliikeMannerheimintie 10500280 HelsinkiPhone: + 358 10 850 8500

> FranceEuler Hermes France SAEuler Hermes CollectionEuler Hermes World Agency1, place des SaisonsF-92048 Paris-La-Défense CedexPhone: + 33 1 84 11 50 50

> GermanyEuler Hermes Deutschland AGFriedensallee 25422763 HamburgPhone: + 49 40 8834 0

Euler Hermes AktiengesellschaftGaastraße 2722761 HamburgPhone: + 49 40 8834 9000

Euler Hermes Collections GmbHZeppelinstr. 4814471 PostdamPhone: + 49 331 27890 000

Euler Hermes Rating GmbHFriedensallee 25422763 HambourgPhone: + 49 40 8 34 640

Euler Hermes Liaison Office at AGCSAllianz Global Coroporate & Specialty AGFritz-Schäffer-Straße 981737 MünchenPhone: + 49 89 38 00 12 159

> GreeceEuler Hermes HellasCredit Insurance SA16 Laodikias Street & 1-3 Nymfeou StreetAthens Greece 11528 Phone: + 30 210 69 00 000

> Hong kongEuler Hermes Hong Kong Services LtdSuites 403-11, 4/F Cityplaza 412 Taikoo Wan Road Island EastHong KongPhone: + 852 3665 8901

> HungaryEuler Hermes Europe SAMagyarrorszagi FioktelepeEuler Hermes Magyar Követeléskezelõ Kft.(trade debt collection)Kiscelli u. 1041037 BudapestPhone: +36 1 453 9000

> IndiaEuler Hermes India Pvt.Ltd5th Floor, Vaibhav Chambers Opposite Income Tax OfficeBandra Kurla ComplexBandra (East)Mumbai 400 051Phone: +91 22 6623 2525

> IndonesiaPT Asuransi Allianz Utama IndonesiaSummitmas II. Building, 9th FloorJl. Jenderal Sudirman Kav 61-62Jakarta 12190Phone: +62 21 252 2470 ext. 6100

> IrelandEuler Hermes IrelandAllianz HouseElm ParkMerrion RoadDublin 4Phone: +353 (0)1 518 7900

> IsraelICIC2, Shenkar Street68010 Tel AvivPhone: +97 23 796 2444

> ItalyEuler Hermes Europe SARappresentanza generale per l’ItaliaVia Raffaello Matarazzo, 1900139 RomePhone: + 39 06 8700 1

> JapanEuler Hermes Deutschland AG, Japan BranchKyobashi Nisshoku Bldg. 7th floor8-7, Kyobashi, 1-chome,Chuo-KuTokyo 104-0031Phone: + 81 3 35 38 5403

> kuwaitPlease contact United Arab Emirates

> latviaPlease contact Sweden

27

Euler Hermes Economic Outlook no. 1214 | January 2015 | Macroeconomic and Country Risk Outlook

> lithuaniaPlease contact Denmark

> malaysiaEuler Hermes Singapore Services Pte Ltd.,Malaysia BranchSuite 3B-13-7, Level 13, Block 3BPlaza Sentral, Jalan Stesen Sentral 550470 Kuala LumpurPhone: +603 2264 8556 (or 8599)

> mexicoSolunionTorre PolancoMariano Escobedo 476, Piso 15Colonia Nueva Anzures11590 Mexico D.F.Phone: +52 55 52 01 79 00

> moroccoEuler Hermes Acmar37, bd Abdelatiff Ben Kaddour20 050 CasablancaPhone: + 212 5 22 79 03 30

> The netherlandsEuler Hermes NederlandPettelaarpark 20P.O. Box 707515201CZ’s-HertogenboschPhone: + 31 (0) 73 688 99 99 / 0800 385 37 65

Euler Hermes BondingDe Entree 67 (Alpha Tower)P.O. Box 124731100 AL AmsterdamPhone: +31 (0) 20 696 39 41

> new zealandEuler Hermes New Zeland LtdLevel 1, 152 Fanshawe StreetAuckland 1010Phone: + 64 9 354 2995

> norwayEuler Hermes NorgeHolbergsgate 21 P.O. Box 6 875St. Olavs Plass0130 OsloPhone: + 47 2 325 60 00

> omanPlease contact United Arab Emirates

> PhilippinesPlease contact Singapore

> PolandTowarzystwo Ubezpieczen Euler Hermes SAul. Domaniewska 50 B02-672 VarsawPhone: + 48 22 363 6363

> PortugalCOSEC Companhia de Seguro deCréditos, S.A.Avenida da República, nº 581069-057 LisbonPhone: + 351 21 791 3700

> QatarPlease contact United Arab Emirates

> RomaniaEuler Hermes Europe SA BruxellesSucursala BucurestiStr. Petru Maior Nr.6Sector 1 011264 BucarestPhone: + 40 21 302 0300

> RussiaEuler Hermes Credit Management OOOOffice C08, 4-th Dobryninskiy per., 8,Moscow, 119049Phone: + 7 495 9812 8 33 ext. 4000

> Saudi arabiaPlease contact United Arab Emirates

> SingaporeEuler Hermes Singapore Services Pte Ltd12 Marina View#14-01 Asia Square Tower 2Singapore 018961Phone: + 65 6297 8802

> SlovakiaEuler Hermes Europe SA, pobokapoist’ovne z ineho clenskeho statu2012: Plynárenská 7/A82109 BratislavaPhone: + 421 2 582 80 911

> South africaPlease contact Italy

> South koreaEuler Hermes Hong Kong ServicesKorea Liaison OfficeRm 1411, 14/F, SayongPlatinum Bldg.156, Cheokseon-dong,Chongro-ku,Seoul 110-052Phone: + 82 2 733 8813

> SpainSolunionAvda. General Perón, 40Edificio Moda ShoppingPortal C, 3a planta28020 MadridPhone: +34 91 581 34 00

> Sri lankaPlease contact Singapore

> SwedenEuler Hermes Sverige filialKlarabergsviadukten 90P.O. Box 729101 64 StockholmPhone: + 46 8 5551 36 00

> SwitzerlandEuler Hermes Deutschland AG,Zweigniederlassung ZürichEuler Hermes Reinsurance AGRichtiplatz 1Postfach8304 WallisellenPhone: + 41 44 283 65 65Phone: + 41 44 283 65 85 (Reinsurance)

> TaiwanPlease contact Hong Kong

> ThailandAllianz C.P. General Insurance Co., Ltd323 United Center Building30th FloorSilom RoadBangrak, Bangkok 10500Phone: + 66 2638 9000

> TunisiaPlease contact Italy

> TurkeyEuler Hermes Sigorta A.S.Büyükdere Cad. No:100-102Maya Akar Center Kat: 7 Esentepe34394 Şișli/ IstanbulPhone: +90 212 2907610

> united arab emiratesEuler Hermesc/o Alliance Insurance (PSC)Warba Center 4th Floor Office 405PO Box 183957DubaiPhone: + 971 4 211 6005

> united kingdomEuler Hermes UK1 Canada SquareLondon E14 5DXPhone: + 44 20 7 512 9333

> united StatesEuler Hermes North AmericaInsurance Company800 Red Brook BoulevardOwings Mills, MD 21117Phone: + 1 877 883 3224

> vietnamPlease contact Singapore

Euler Hermes Economic Outlookis published monthly by the Economic Research Departmentof Euler Hermes Group1, place des Saisons, F-92048 Paris La Défense Cedex e-mail: [email protected] - Tel. : +33 (0) 1 84 11 50 50

This document reflects the opinion of the Economic Research Department of Euler Hermes Group.

The information, analyses and forecasts contained herein are based on the Department's current

hypotheses and viewpoints and are of a prospective nature. In this regard, the Economic Research

Department of Euler Hermes Group has no responsibility for the consequences hereof and no

liability. Moreover, these analyses are subject to modification at any time.

www.eulerhermes.com

EconomicOutlook