Embed Size (px)

Citation preview

1

Overview of Financial Services in the 2008 SNA

Herman SmithUNSD/DESA

Workshop on the Implementation of the 2008 SNA, Kiev, 29 November – 2 December 2011

Agenda item 6c

2

Outline of Presentation

• Financial corporations sector and its subsectors• Breakdown of financial corporations• Output of financial services• Conclusion and way forward

3

Financial corporations sector and its subsectors

• Financial corporations consist of all resident corporations that are principally engaged in providing financial services, including insurance and pension funding services, to other institutional units

• Comprise following resident institutional units• All resident financial corporations (as understood in

the SNA and not just restricted to legally constituted corporations), regardless of the residence of their shareholders

• Branches of non-resident enterprises that are engaged in financial activity in economic territory on a long-term basis

• All resident NPIs that are market producers of financial services

4

Financial corporations sector and its subsectors

• Financial services are defined in paragraph 4.98 of the 2008 SNA:• The production of financial services is the result

of financial intermediation, financial risk management, liquidity transformation or auxiliary financial activities

• 2008 SNA’s definition of financial services is more explicit than 1993 SNA’s definition to also include financial services other than financial intermediation, specifically financial risk management and liquidity transformation

5

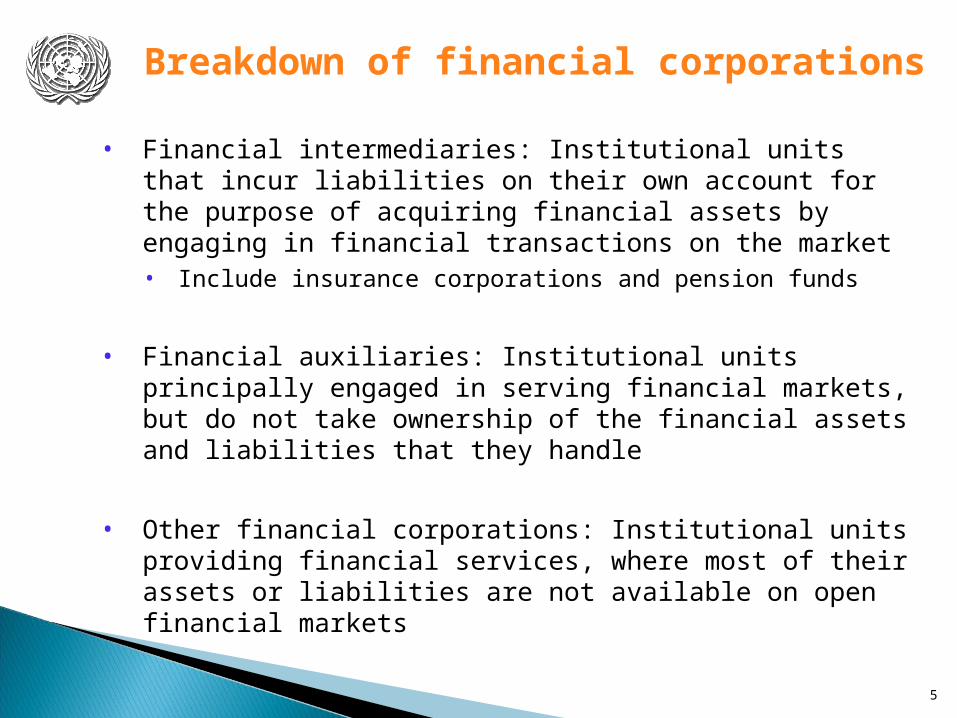

Breakdown of financial corporations

• Financial intermediaries: Institutional units that incur liabilities on their own account for the purpose of acquiring financial assets by engaging in financial transactions on the market• Include insurance corporations and pension funds

• Financial auxiliaries: Institutional units principally engaged in serving financial markets, but do not take ownership of the financial assets and liabilities that they handle

• Other financial corporations: Institutional units providing financial services, where most of their assets or liabilities are not available on open financial markets

6

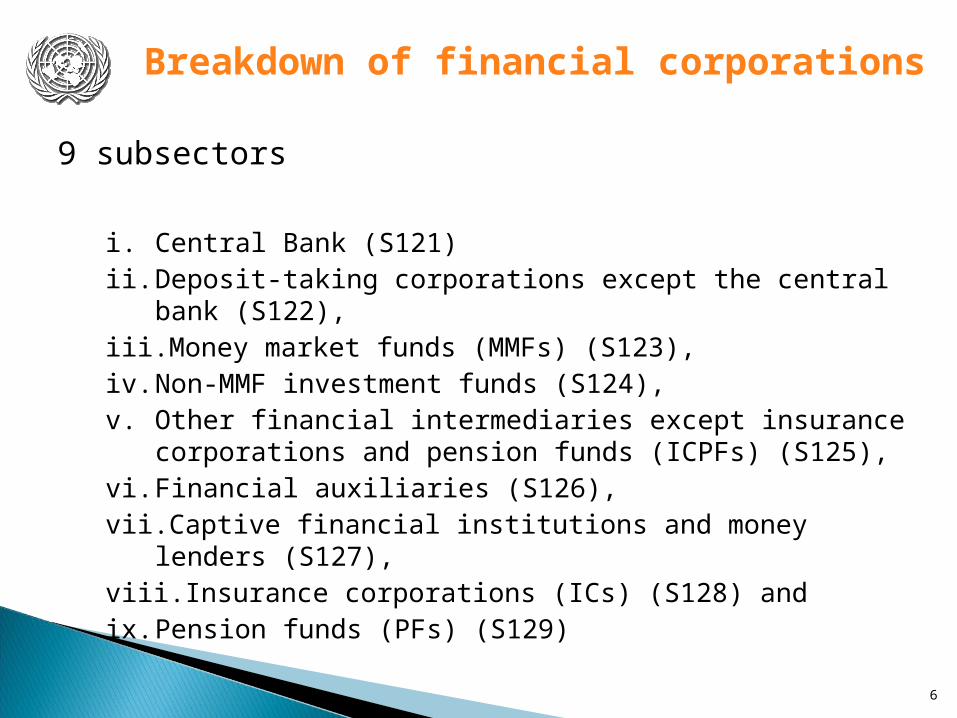

Breakdown of financial corporations

9 subsectors

i. Central Bank (S121)ii. Deposit-taking corporations except the central bank

(S122), iii. Money market funds (MMFs) (S123), iv. Non-MMF investment funds (S124), v. Other financial intermediaries except insurance

corporations and pension funds (ICPFs) (S125), vi. Financial auxiliaries (S126), vii. Captive financial institutions and money lenders (S127), viii. Insurance corporations (ICs) (S128) and ix. Pension funds (PFs) (S129)

7

Breakdown of financial corporations

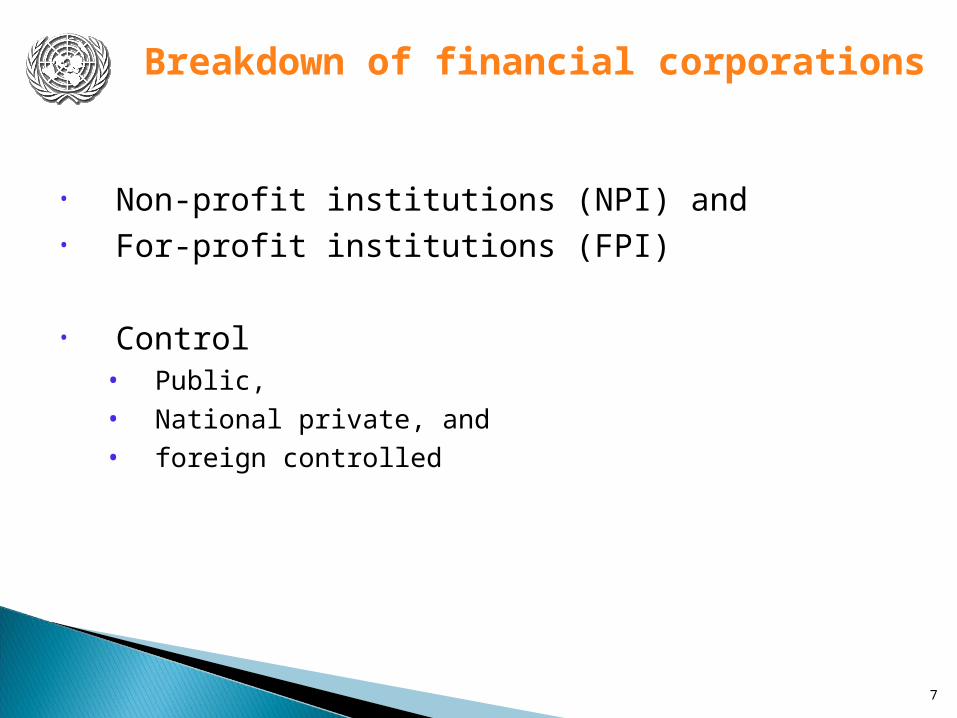

• Non-profit institutions (NPI) and• For-profit institutions (FPI)

• Control • Public, • National private, and• foreign controlled

8

Output of financial services

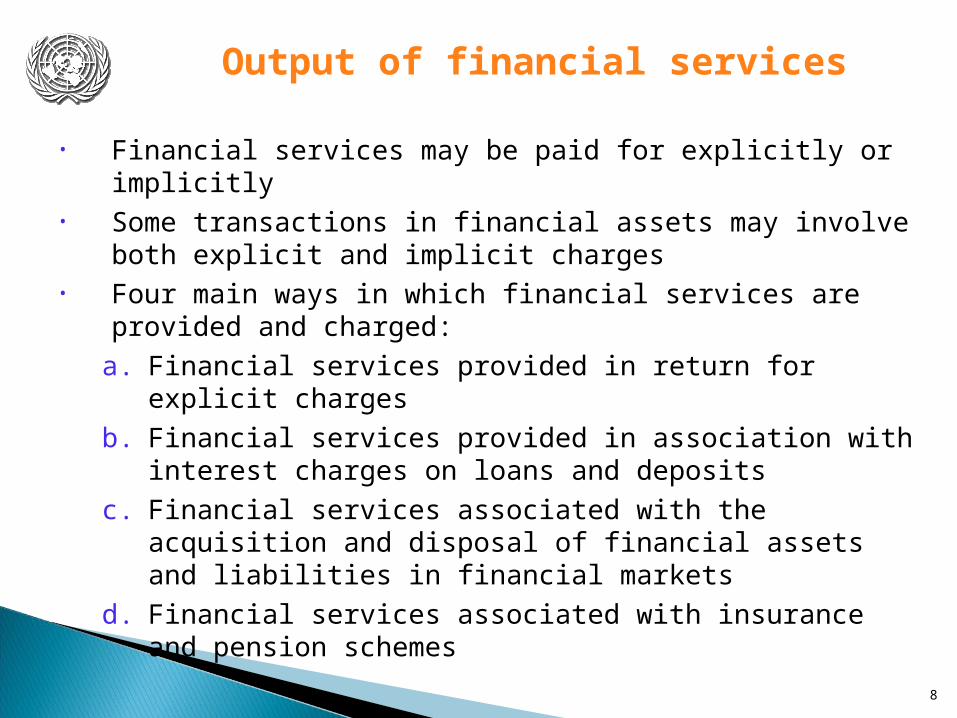

• Financial services may be paid for explicitly or implicitly • Some transactions in financial assets may involve both

explicit and implicit charges• Four main ways in which financial services are provided

and charged:a. Financial services provided in return for explicit

chargesb. Financial services provided in association with

interest charges on loans and depositsc. Financial services associated with the acquisition

and disposal of financial assets and liabilities in financial markets

d. Financial services associated with insurance and pension schemes

9

Output of financial services

a. Financial services provided in return for explicit charges

• Applies to many financial services • Provided by many categories of financial institutions• Examples:

• Credit card fees• Fees charged for floatation of shares• Fees charged to arrange mortgages, manage

investment portfolios, provide tax advice, administer estates, etc

10

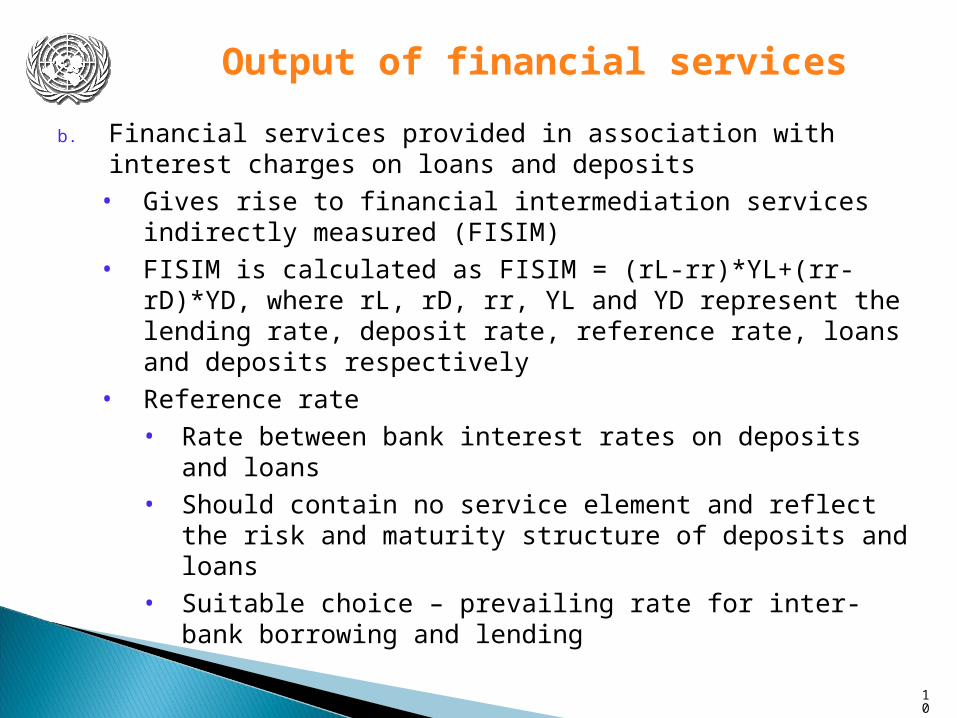

Output of financial services

b. Financial services provided in association with interest charges on loans and deposits

• Gives rise to financial intermediation services indirectly measured (FISIM)

• FISIM is calculated as FISIM = (rL-rr)*YL+(rr-rD)*YD, where rL, rD, rr, YL and YD represent the lending rate, deposit rate, reference rate, loans and deposits respectively

• Reference rate• Rate between bank interest rates on deposits and

loans• Should contain no service element and reflect the

risk and maturity structure of deposits and loans• Suitable choice – prevailing rate for inter-bank

borrowing and lending

11

Output of financial services

b. Financial services provided in association with interest charges on loans and deposits

• FISIM only applies to loans and deposits provided by, or deposited with, financial institutions

• Not necessary for financial institutions to offer deposit-taking facilities as well as make loans

• Examples: • Financial subsidiaries of retailers• Money lenders

12

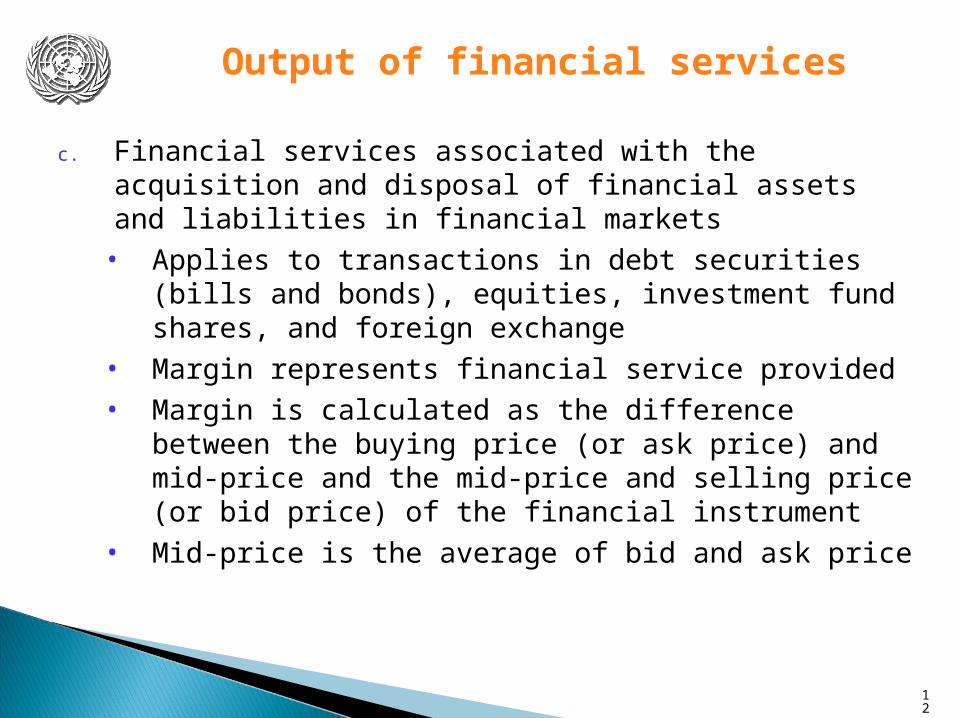

Output of financial services

c. Financial services associated with the acquisition and disposal of financial assets and liabilities in financial markets

• Applies to transactions in debt securities (bills and bonds), equities, investment fund shares, and foreign exchange

• Margin represents financial service provided• Margin is calculated as the difference between the

buying price (or ask price) and mid-price and the mid-price and selling price (or bid price) of the financial instrument

• Mid-price is the average of bid and ask price

13

Output of financial services

d. Financial services associated with insurance and pension schemes

• 5 types of activitiesi. Non-life insuranceii. Life insurance and annuitiesiii. Reinsuranceiv. Social insurance schemesv. Standardized guarantee schemes

14

Output of financial services

d. Financial services associated with insurance and pension schemes

i. Non-life insurance• Insurer sets level of actual premiums to be such

that sum of actual premiums plus property income earned on them (premium supplements) less expected claim leaves a margin insurance can retain

• Margin represents output which can be computed using 3 methods• Expectations approach• Accounting approach• Cost approach

15

Output of financial services

d. Financial services associated with insurance and pension schemes

i. Non-life insurance output – Expectations approach• Ex-ante model• Insurers consider expectation of claims and

premiums and premium supplements in setting premiums

• Output = actual premiums earned + expected premium supplements – expected claims

16

Output of financial services

d. Financial services associated with insurance and pension schemes

i. Non-life insurance output – Accounting approach• Output = actual premiums earned + premium

supplements – adjusted claims incurred• Adjusted claims incurred determined by using

claims due plus changes in equalization provisions and, if necessary, changes to own funds

17

Output of financial services

d. Financial services associated with insurance and pension schemes

i. Non-life insurance output – Cost approach• Use if data are not available to apply the

expectations and accounting approaches• Output is estimated as sum of costs (including

intermediate costs, labor and capital inputs) plus allowance for “normal profit”

18

Output of financial services

d. Financial services associated with insurance and pension schemes

ii. Life insurance• Method to calculate output follows same general

principles as for non-life insurance• However, changes in technical reserves must be

taken into account due to the time interval between when premiums are received and when benefits are paid

• Output = actual premiums earned + premium supplements – benefits due – increases (+decreases) in life insurance technical reserves

• If data are insufficient to use this formula, compute output using sum of costs plus allowance for “normal” profit

19

Output of financial services

d. Financial services associated with insurance and pension schemes

iii. Reinsurance• Output is calculated in a way similar to that for

non-life insurance• However, there is a need to account for

payments peculiar to reinsurance (i.e., commissions payable to direct insurer under proportionate insurance and profit sharing in excess of loss reinsurance)

• Output = actual premiums earned less commissions payable + premium supplements – adjusted claims incurred and profit sharing

20

Output of financial services

d. Financial services associated with insurance and pension schemes

iv. Social insurance schemes• 4 different ways of organization

• Social security – provided by government• Employer may organize a social security

scheme for employees• Employer may have insurance corporation run

scheme for employer• Multiemployer scheme (insurance corporation

runs scheme for several employers in return for any property income and holding gains it may make in excess of what is owed to participants in the scheme)

• Output for each mode is calculated differently

21

Output of financial services

d. Financial services associated with insurance and pension schemes

iv. Social insurance schemes – social security• Run as part of operation of general government• If separate units are distinguished, output is

calculated in the same way as non-market output as sum of costs

• If separate units are not distinguished, output is included with the level of government at which it operates

22

Output of financial services

d. Financial services associated with insurance and pension schemes

iv. Social insurance schemes – employer-organized schemes• Output is calculated as sum of costs including an

estimates for return to capital• Applies even if employer establishes a segregated

pension fund to manage scheme

23

Output of financial services

d. Financial services associated with insurance and pension schemes

iv. Social insurance schemes – employers get insurance corporations to run schemes • Output is value of fee charged by insurance

corporation

iv. Social insurance schemes – multiemployer schemes• Output is measured as for life insurance policies• Output is calculated as actual contributions

earned plus contribution supplements minus benefits due minus increases (plus decreases) in pension entitlements.

24

Output of financial services

d. Financial services associated with insurance and pension schemes

v. Standardized guarantee schemes• Market producer – value of output is

calculated in same way as non-life insurance• Non-market producer – sum of costs

25

Conclusion and Way Forward

• 2008 SNA has expanded the scope of financial services

• Financial services now include risk management and liquidity transformation, in addition to financial intermediation

• UNSD and ECB are currently preparing a Handbook on National Accounting on “Financial Production, Flows and Stocks in the System of National Accounts”

• Handbook will include a number of worked examples to illustrate how to compute output of financial services

• Handbook is scheduled to be completed by end-2012• A draft is available at:

26

Thank You