Embed Size (px)

Citation preview

J A P A N C R E D I T P E R S P E C T I V E S

Koyo OzekiMarch 2007

The recent increase in United States subprime mortgage defaults has significantly impacted global financial markets. While Japan is not facing any immediate concern toward the residential mortgage market itself, the global situation calls for an overview of the structure of the Japanese market in comparison with U.S. and European markets. The focus on housing also warrants a look at the relationship between Japan’s housing market and macro economy and at the outlook for Japan’s residential mortgage-backed securities (RMBS) market.

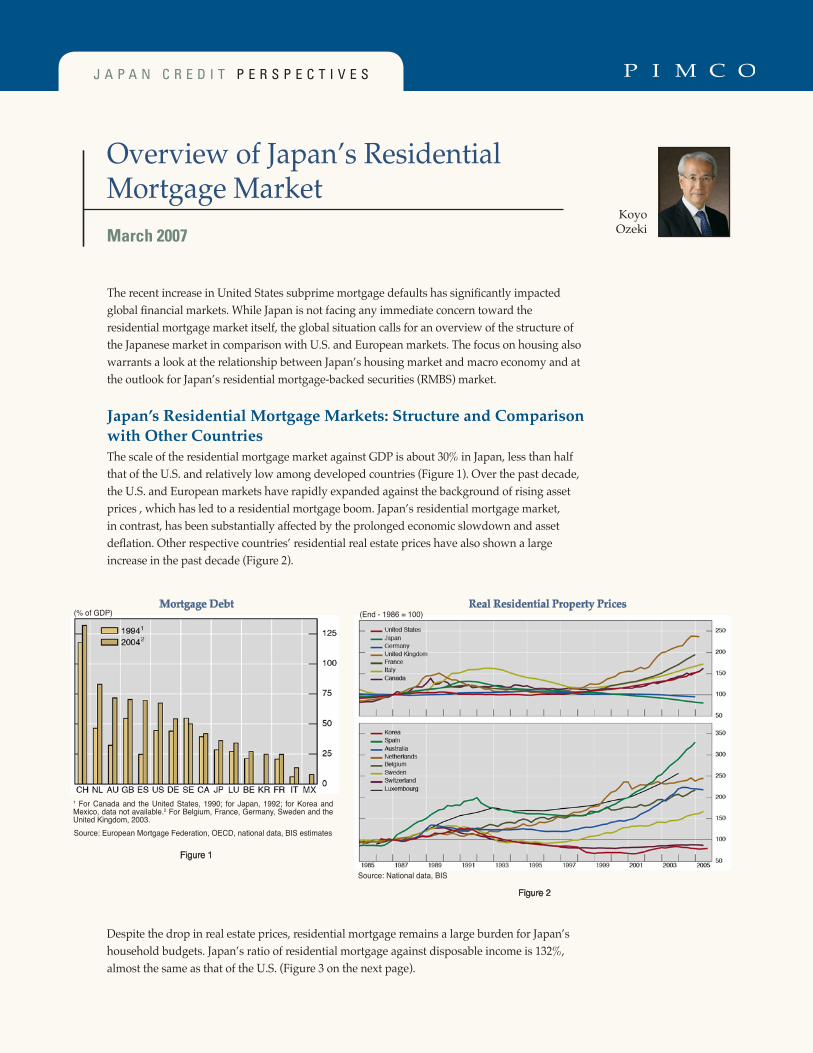

Japan’s Residential Mortgage Markets: Structure and Comparison with Other CountriesThe scale of the residential mortgage market against GDP is about 30% in Japan, less than half that of the U.S. and relatively low among developed countries (Figure 1). Over the past decade, the U.S. and European markets have rapidly expanded against the background of rising asset prices , which has led to a residential mortgage boom. Japan’s residential mortgage market, in contrast, has been substantially affected by the prolonged economic slowdown and asset deflation. Other respective countries’ residential real estate prices have also shown a large increase in the past decade (Figure 2).

Mortgage Debt Real Residential Property Prices

Source: National data, BIS

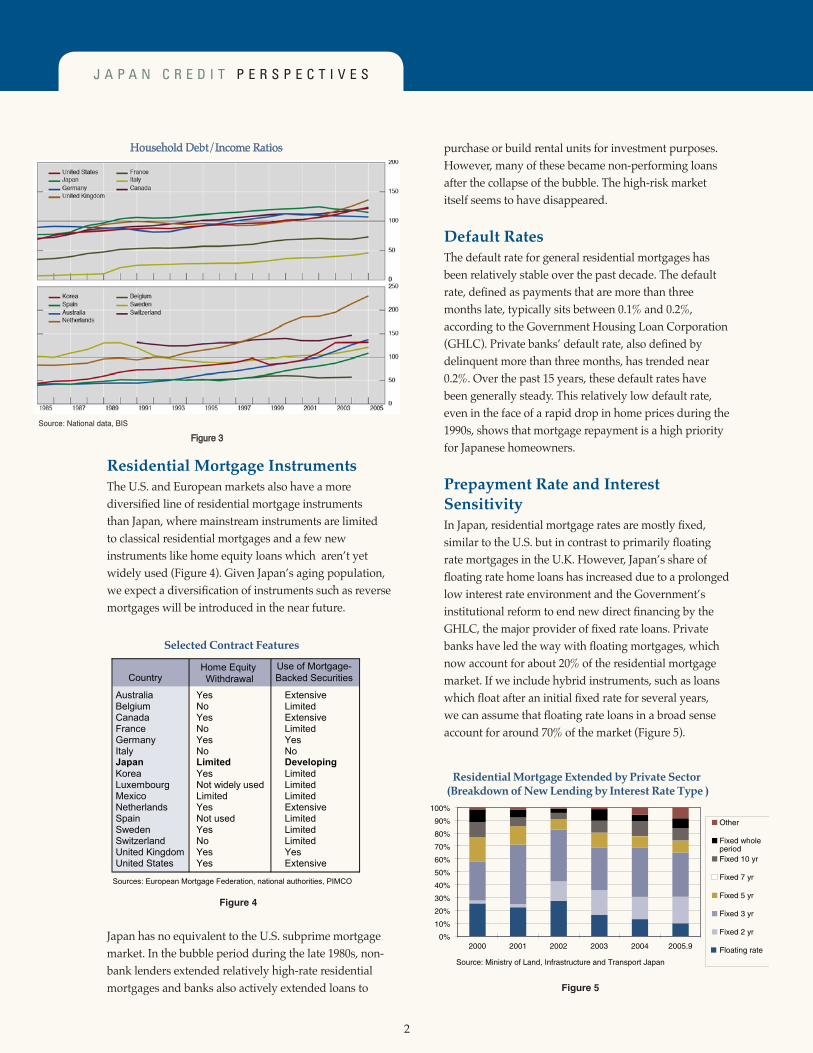

Despite the drop in real estate prices, residential mortgage remains a large burden for Japan’s household budgets. Japan’s ratio of residential mortgage against disposable income is 132%, almost the same as that of the U.S. (Figure 3 on the next page).

Figure 2

Figure 1

Source: European Mortgage Federation, OECD, national data, BIS estimates

1 For Canada and the United States, 1990; for Japan, 1992; for Korea and Mexico, data not available.2 For Belgium, France, Germany, Sweden and the United Kingdom, 2003.

(% of GDP) (End - 1986 = 100)

Overview of Japan’s ResidentialMortgage Market

�

J A P A N C R E D I T P E R S P E C T I V E S

Residential Mortgage InstrumentsThe U.S. and European markets also have a more diversified line of residential mortgage instruments than Japan, where mainstream instruments are limited to classical residential mortgages and a few new instruments like home equity loans which aren’t yet widely used (Figure 4). Given Japan’s aging population, we expect a diversification of instruments such as reverse mortgages will be introduced in the near future.

Japan has no equivalent to the U.S. subprime mortgage market. In the bubble period during the late 1980s, non-bank lenders extended relatively high-rate residential mortgages and banks also actively extended loans to

purchase or build rental units for investment purposes. However, many of these became non-performing loans after the collapse of the bubble. The high-risk market itself seems to have disappeared.

Default RatesThe default rate for general residential mortgages has been relatively stable over the past decade. The default rate, defined as payments that are more than three months late, typically sits between 0.1% and 0.2%, according to the Government Housing Loan Corporation (GHLC). Private banks’ default rate, also defined by delinquent more than three months, has trended near 0.2%. Over the past 15 years, these default rates have been generally steady. This relatively low default rate, even in the face of a rapid drop in home prices during the 1990s, shows that mortgage repayment is a high priority for Japanese homeowners.

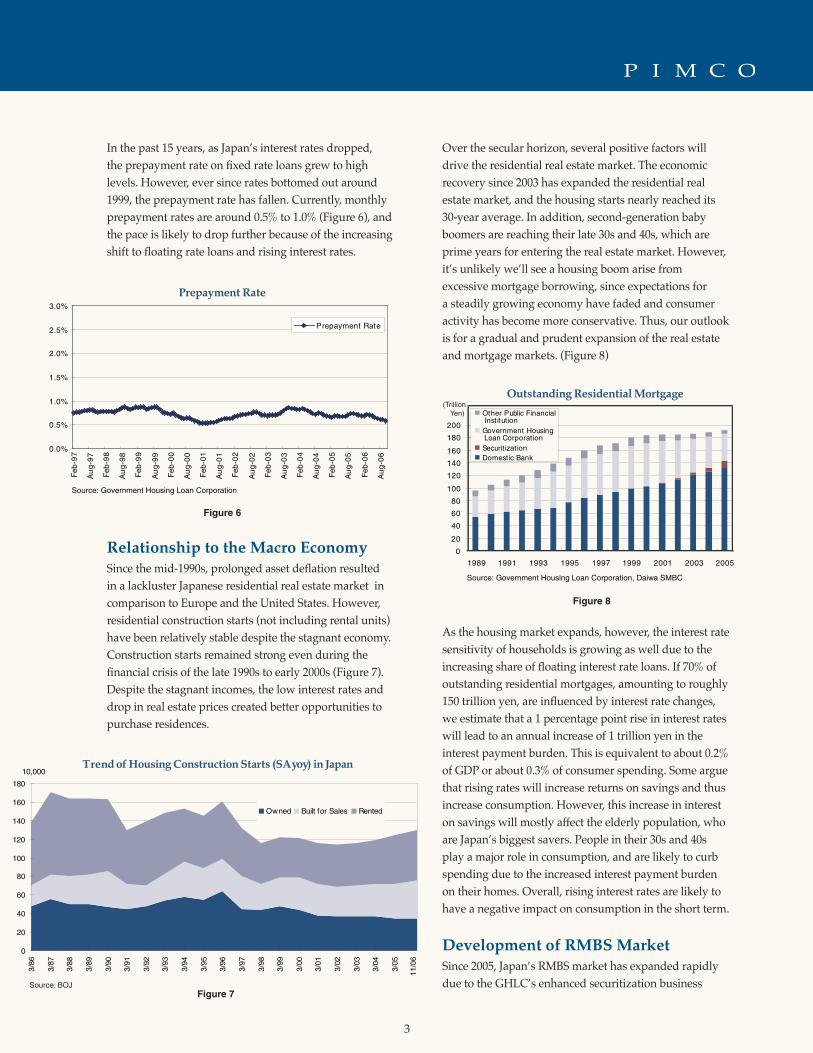

Prepayment Rate and Interest SensitivityIn Japan, residential mortgage rates are mostly fixed, similar to the U.S. but in contrast to primarily floating rate mortgages in the U.K. However, Japan’s share of floating rate home loans has increased due to a prolonged low interest rate environment and the Government’s institutional reform to end new direct financing by the GHLC, the major provider of fixed rate loans. Private banks have led the way with floating mortgages, which now account for about 20% of the residential mortgage market. If we include hybrid instruments, such as loans which float after an initial fixed rate for several years, we can assume that floating rate loans in a broad sense account for around 70% of the market (Figure 5).

Residential Mortgage Extended by Private Sector(Breakdown of New Lending by Interest Rate Type )

Source: Ministry of Land, Infrastructure and Transport Japan

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005.9

Other

Fixed wholeperiodFixed 10 yr

Fixed 7 yr

Fixed 5 yr

Fixed 3 yr

Fixed 2 yr

Floating rate

Figure 5

Figure 3Source: National data, BIS

Household Debt/Income Ratios

Selected Contract Features

AustraliaBelgiumCanadaFranceGermanyItalyJapanKoreaLuxembourgMexicoNetherlandsSpainSwedenSwitzerlandUnited KingdomUnited States

YesNoYesNoYesNoLimitedYesNot widely usedLimitedYesNot usedYesNoYesYes

ExtensiveLimitedExtensiveLimitedYesNoDevelopingLimitedLimitedLimitedExtensiveLimitedLimitedLimitedYesExtensive

Sources: European Mortgage Federation, national authorities, PIMCO

CountryHome EquityWithdrawal

Use of Mortgage-Backed Securities

Figure 4

�

In the past 15 years, as Japan’s interest rates dropped, the prepayment rate on fixed rate loans grew to high levels. However, ever since rates bottomed out around 1999, the prepayment rate has fallen. Currently, monthly prepayment rates are around 0.5% to 1.0% (Figure 6), and the pace is likely to drop further because of the increasing shift to floating rate loans and rising interest rates.

Relationship to the Macro EconomySince the mid-1990s, prolonged asset deflation resulted in a lackluster Japanese residential real estate market in comparison to Europe and the United States. However, residential construction starts (not including rental units) have been relatively stable despite the stagnant economy. Construction starts remained strong even during the financial crisis of the late 1990s to early 2000s (Figure 7). Despite the stagnant incomes, the low interest rates and drop in real estate prices created better opportunities to purchase residences.

Over the secular horizon, several positive factors will drive the residential real estate market. The economic recovery since 2003 has expanded the residential real estate market, and the housing starts nearly reached its 30-year average. In addition, second-generation baby boomers are reaching their late 30s and 40s, which are prime years for entering the real estate market. However, it’s unlikely we’ll see a housing boom arise from excessive mortgage borrowing, since expectations for a steadily growing economy have faded and consumer activity has become more conservative. Thus, our outlook is for a gradual and prudent expansion of the real estate and mortgage markets. (Figure 8)

As the housing market expands, however, the interest rate sensitivity of households is growing as well due to the increasing share of floating interest rate loans. If 70% of outstanding residential mortgages, amounting to roughly 150 trillion yen, are influenced by interest rate changes, we estimate that a 1 percentage point rise in interest rates will lead to an annual increase of 1 trillion yen in the interest payment burden. This is equivalent to about 0.2% of GDP or about 0.3% of consumer spending. Some argue that rising rates will increase returns on savings and thus increase consumption. However, this increase in interest on savings will mostly affect the elderly population, who are Japan’s biggest savers. People in their 30s and 40s play a major role in consumption, and are likely to curb spending due to the increased interest payment burden on their homes. Overall, rising interest rates are likely to have a negative impact on consumption in the short term.

Development of RMBS MarketSince 2005, Japan’s RMBS market has expanded rapidly due to the GHLC’s enhanced securitization business

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Feb

-97

Au

g-9

7

Feb

-98

Au

g-9

8

Feb

-99

Au

g-9

9

Feb

-00

Au

g-0

0

Feb

-01

Au

g-0

1

Feb

-02

Au

g-0

2

Feb

-03

Au

g-0

3

Feb

-04

Au

g-0

4

Feb

-05

Au

g-0

5

Feb

-06

Au

g-0

6

Prepayment Rate

Prepayment Rate

Figure 6

Source: Government Housing Loan Corporation

0

20

40

60

80

100

120

140

160

180

200

1989 1991 1993 1995 1997 1999 2001 2003 2005

Other Public FinancialInstitutionGovernment HousingLoan CorporationSecurit izationDomestic Bank

Outstanding Residential Mortgage

Figure 8

(Trillion Yen)

Source: Government Housing Loan Corporation, Daiwa SMBC

Trend of Housing Construction Starts (SAyoy) in Japan

0

20

40

60

80

100

120

140

160

180

3/86

3/87

3/88

3/89

3/90

3/91

3/92

3/93

3/94

3/95

3/96

3/97

3/98

3/99

3/00

3/01

3/02

3/03

3/04

3/05

11/0

6

Owned Built for Sales Rented

10,000

Figure 7Source: BOJ

PER038-122606

840 Newport Center Drive

Newport Beach, CA 92660

949.720.6000

Past performance is no guarantee of future results. This article contains the current opinions of the author but not necessarily those of Pacific Investment Management Company LLC. Such opinions are subject to change without notice. This article has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

Mortgage-backed securities may be sensitive to changes in prevailing interest rates; when they rise, the value generally declines. There is no assurance that the private guarantors or insurers will meet their obligations. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio. The charts and graphs are for illustrative purposes only and are not indicative of the past or future performance of any PIMCO product.

No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Pacific Investment Management Company LLC, 840 Newport Center Drive, Newport Beach, CA 92660. ©2007, PIMCO.

and increase in private banks’ residential mortgage securitization (Figure 9). The RMBS market is likely to continue its expansion, not just because rising rates will increase demand for fixed loans, but also because of private banks’ need to manage interest rate risk. We are at a turning point, shifting from the decreasing interest rate environment of the past 15 years to a rising interest rate environment.

While any significant change in the underlying credit quality of the RMBS market is unlikely, we continue to monitor and analyze the market. The importance of microeconomic factors, such as the influence of changing prepayment patterns on duration, is likely to increase.

Koyo OzekiExecutive Vice President

0

20

40

60

80

100

120

140

160

180

1999 2000 2001 2002 2003 2004 2005 2006

Government Housing

Loan Corporation

Private Sector

Source: Daiwa SMBCNote: On a fiscal year basis. Data for 2006 includes January and February.

(Trillion Yen)

Accumulated Securitization of Residential Mortgage (Amount Issued)

Figure 9