Embed Size (px)

Citation preview

FALIA Invitational Seminar in Japan

“Risk Management Course”

Overview of Life Ins. Industryin Japan

November 9th, 2016Genjiro Saito

Chief, International AffairsThe Life Insurance Association of Japan

Contents

I Basic Information of Japan

II Japan’s Position in the World Life Insurance Market

III Overview of Life Insurance Business in Japan

IV Brief History of Japanese Life Insurance Industry

V Addressing the issues

VI The Life Insurance Association of Japan

2

I Basic Information of Japan

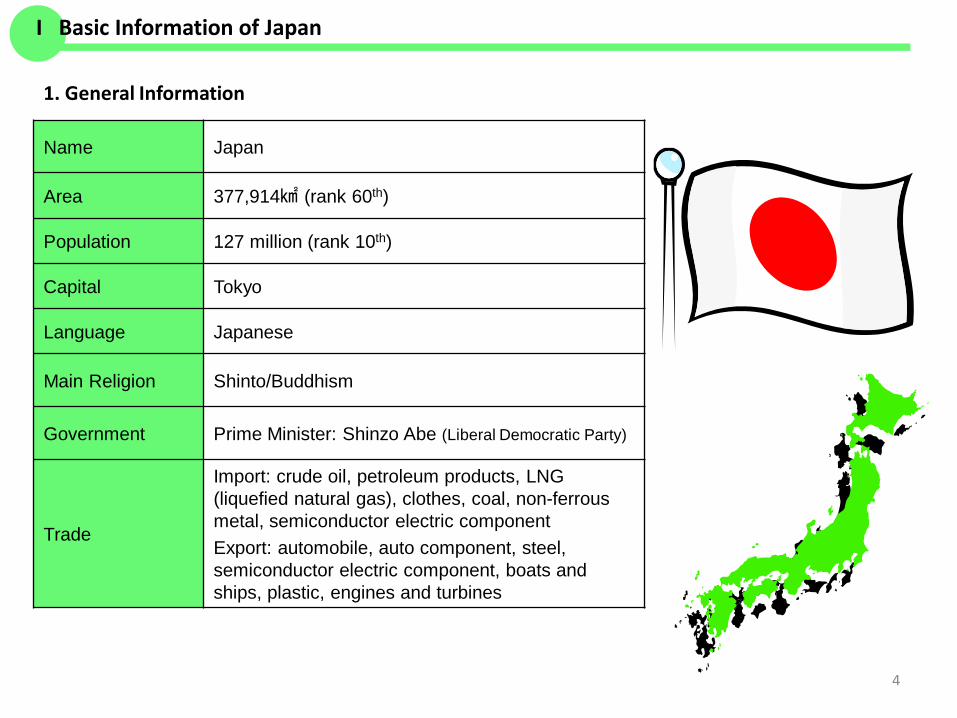

I Basic Information of Japan

1. General Information

4

Name Japan

Area 377,914㎢ (rank 60th)

Population 127 million (rank 10th)

Capital Tokyo

Language Japanese

Main Religion Shinto/Buddhism

Government Prime Minister: Shinzo Abe (Liberal Democratic Party)

Trade

Import: crude oil, petroleum products, LNG (liquefied natural gas), clothes, coal, non-ferrous metal, semiconductor electric componentExport: automobile, auto component, steel, semiconductor electric component, boats and ships, plastic, engines and turbines

0

100

200

300

400

500

600

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

I Basic Information of Japan

5

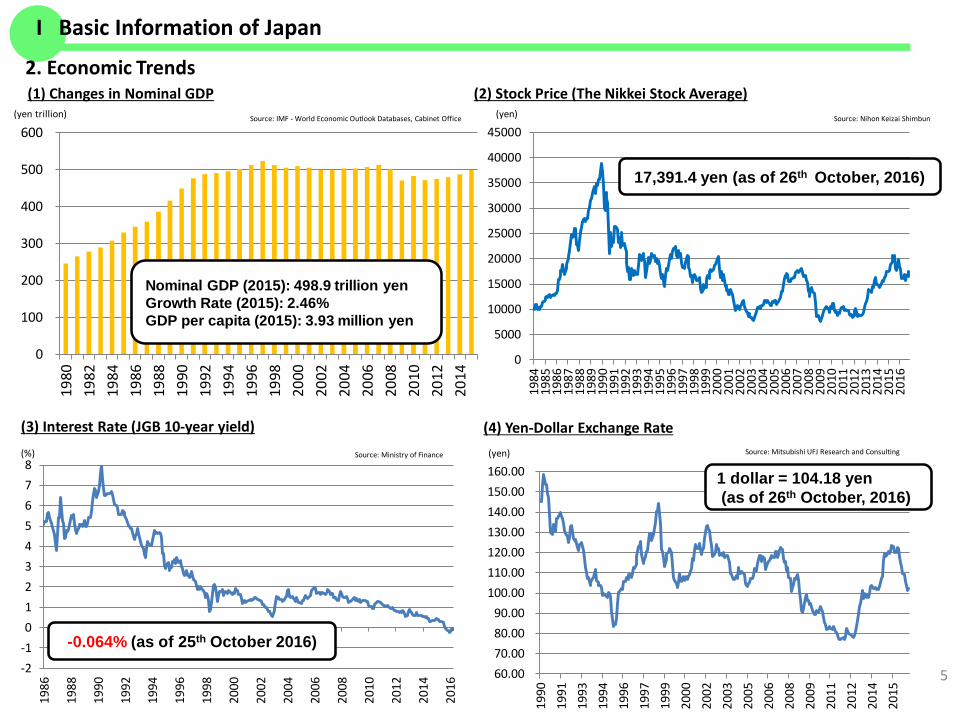

2. Economic Trends

(yen trillion)

(1) Changes in Nominal GDP (2) Stock Price (The Nikkei Stock Average)(yen)Source: IMF - World Economic Outlook Databases, Cabinet Office Source: Nihon Keizai Shimbun

(3) Interest Rate (JGB 10-year yield)

Source: Ministry of Finance(%)

(4) Yen-Dollar Exchange Rate(yen) Source: Mitsubishi UFJ Research and Consulting

Nominal GDP (2015): 498.9 trillion yenGrowth Rate (2015): 2.46%GDP per capita (2015): 3.93 million yen

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

17,391.4 yen (as of 26th October, 2016)

-2-1012345678

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-0.064% (as of 25th October 2016)

60.0070.0080.0090.00

100.00110.00120.00130.00140.00150.00160.00

1990

1991

1993

1994

1996

1997

1999

2000

2002

2003

2005

2006

2008

2009

2011

2012

2014

2015

1 dollar = 104.18 yen(as of 26th October, 2016)

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00%

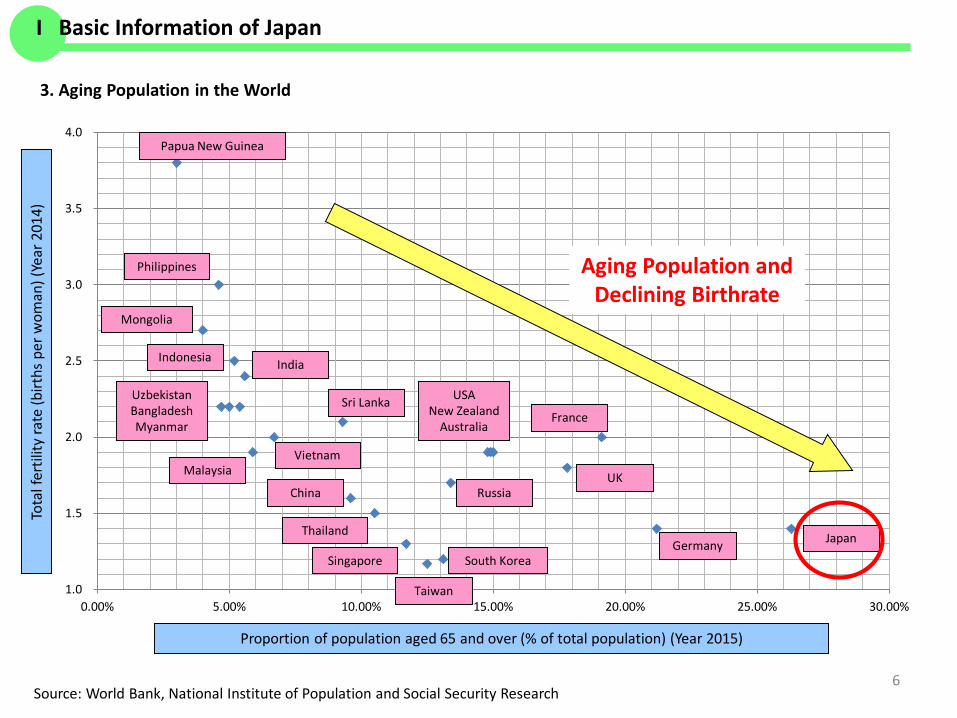

3. Aging Population in the World

Proportion of population aged 65 and over (% of total population) (Year 2015)

Tota

l fer

tility

rate

(birt

hs p

er w

oman

) (Ye

ar 2

014)

Germany

France

Japan

UK

USANew Zealand

Australia

UzbekistanBangladeshMyanmar

China

South Korea

Taiwan

India

Malaysia

Indonesia

Philippines

Singapore

Thailand

Vietnam

Aging Population and Declining Birthrate

Mongolia

Papua New Guinea

Source: World Bank, National Institute of Population and Social Security Research 6

I Basic Information of Japan

Sri Lanka

Russia

7

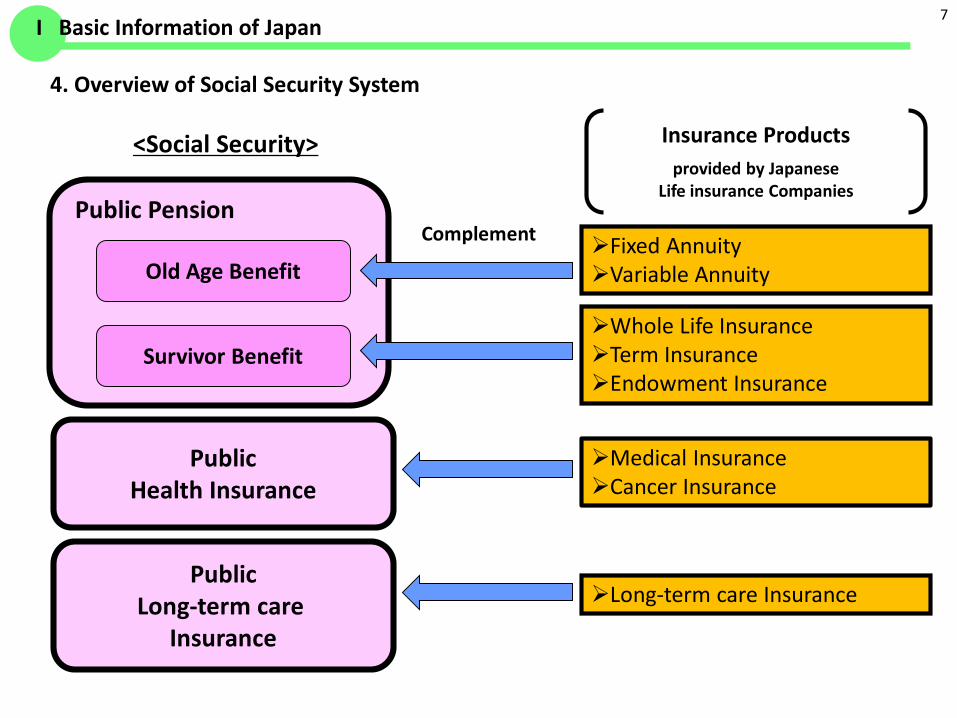

4. Overview of Social Security System

Public Pension

Old Age Benefit

Survivor Benefit

Public Health Insurance

Public Long-term care

Insurance

<Social Security>

Fixed AnnuityVariable Annuity

Whole Life InsuranceTerm InsuranceEndowment Insurance

Medical InsuranceCancer Insurance

Long-term care Insurance

Complement

Insurance Productsprovided by Japanese

Life insurance Companies

I Basic Information of Japan

Old Age Benefit Survivor Benefit

Cost National Government Subsidies Premium

• self-employed ・・・ ¥16,260/M• employee ・・・ 18.182% of salary

Public Pension can use fund (¥135 trillion) to ensure paying benefit sustainably.

Benefit Starting age

• 65 years old Some older people can receive it from 60 years old.

Amount• self-employed ・・・ ¥780,100/Y• employee ・・・ income-related amount/Y

Amount is adjusted not only for price fluctuation but also for a decrease in population.

Eligibility to receive pension benefit• premium payment for 25 years(to be10 years after Oct 2017)

CostPaid as Public Pension (Old Age Benefit)

Benefit Survivors’ Employees’ Pension

• Eligibility ・・・ Employee• Amount ・・・ 3/4 of Old Age Benefit(Pension)

Widow’s Pension• Eligibility ・・・ Self-employed

Age of widow in age 60-65• Amount ・・・ 3/4 of Old Age Benefit(Pension)

Survivors’ Basic Pension• Eligibility ・・・ Employee and Self-employed

Survivors have children• Amount ・・・ ¥780,100/Y

+ ¥224,500/Y per childLump-sum payment・ Eligibility ・・・ Not falling under abovementioned categories・ Amount ・・・ ¥120,000~320,000 proportional to the payment period

Basic Pension

(Self-employed)

Employees’ Pension Insurance

(Employee)

8

(a) Public Pension

( Self-employed ) ( Employee )

65Widow’s Pension

ORSurvivors’ Employees’

Pension

Survivors’Basic

Pension

+

Widow’s Age

60

If a survivor has a child

I Basic Information of Japan

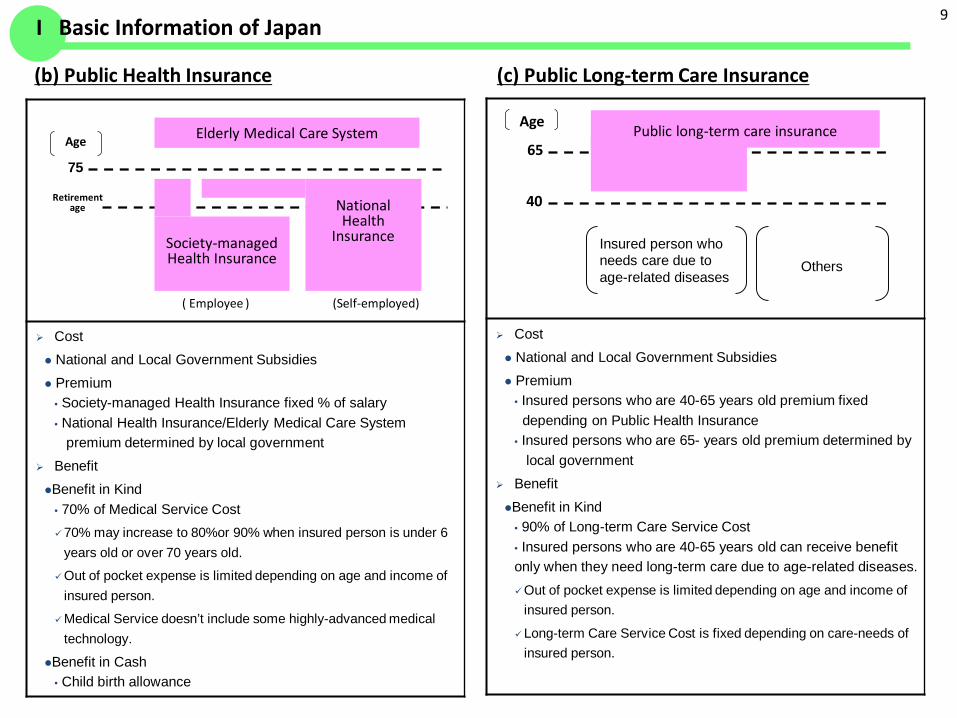

Cost National and Local Government Subsidies Premium

• Society-managed Health Insurance fixed % of salary• National Health Insurance/Elderly Medical Care System

premium determined by local government BenefitBenefit in Kind

• 70% of Medical Service Cost70% may increase to 80%or 90% when insured person is under 6

years old or over 70 years old.

Out of pocket expense is limited depending on age and income of insured person.

Medical Service doesn’t include some highly-advanced medical technology.

Benefit in Cash• Child birth allowance

9

(b) Public Health Insurance

(Self-employed) ( Employee )

75

Age Elderly Medical Care System

Retirement age

Society-managed Health Insurance

National Health

Insurance

Cost National and Local Government Subsidies Premium

• Insured persons who are 40-65 years old premium fixed depending on Public Health Insurance

• Insured persons who are 65- years old premium determined by local government

BenefitBenefit in Kind

• 90% of Long-term Care Service Cost• Insured persons who are 40-65 years old can receive benefit only when they need long-term care due to age-related diseases.Out of pocket expense is limited depending on age and income of

insured person.

Long-term Care Service Cost is fixed depending on care-needs of insured person.

65

Age

40

Public long-term care insurance

Insured person who needs care due to age-related diseases

Others

(c) Public Long-term Care Insurance

I Basic Information of Japan

II Japan’s Position in the World Life Insurance Market

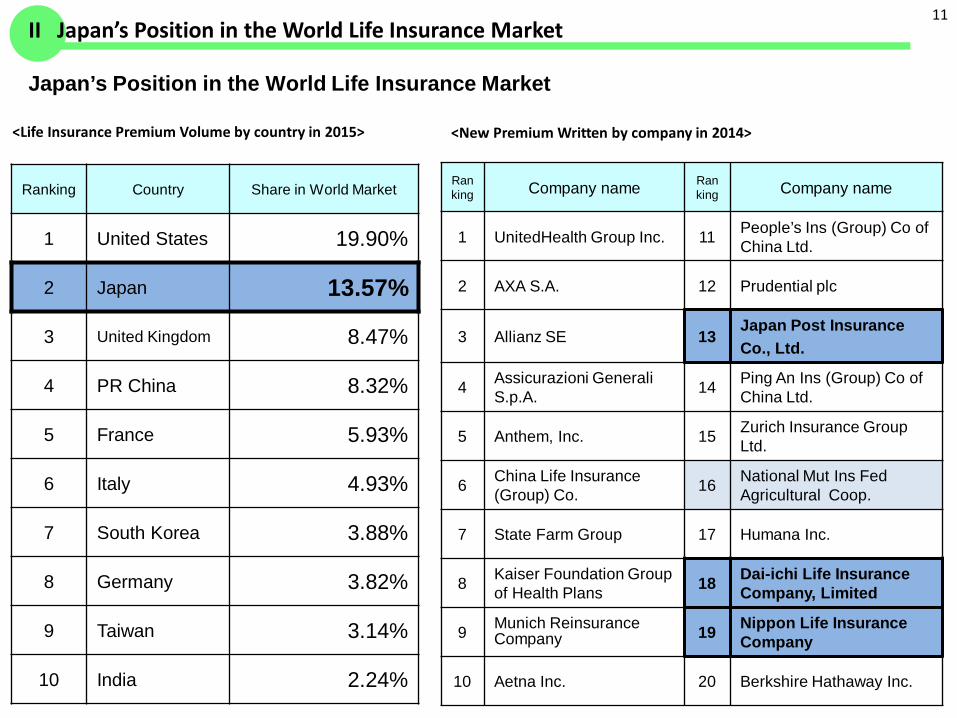

Japan’s Position in the World Life Insurance Market

<Life Insurance Premium Volume by country in 2015>

11

Ranking Country Share in World Market

1 United States 19.90%

2 Japan 13.57%

3 United Kingdom 8.47%

4 PR China 8.32%

5 France 5.93%

6 Italy 4.93%

7 South Korea 3.88%

8 Germany 3.82%

9 Taiwan 3.14%

10 India 2.24%

Ranking Company name Ran

king Company name

1 UnitedHealth Group Inc. 11 People’s Ins (Group) Co of China Ltd.

2 AXA S.A. 12 Prudential plc

3 Allianz SE 13Japan Post Insurance Co., Ltd.

4 Assicurazioni GeneraliS.p.A. 14 Ping An Ins (Group) Co of

China Ltd.

5 Anthem, Inc. 15 Zurich Insurance Group Ltd.

6 China Life Insurance (Group) Co. 16 National Mut Ins Fed

Agricultural Coop.

7 State Farm Group 17 Humana Inc.

8 Kaiser Foundation Group of Health Plans 18 Dai-ichi Life Insurance

Company, Limited

9 Munich Reinsurance Company 19 Nippon Life Insurance

Company

10 Aetna Inc. 20 Berkshire Hathaway Inc.

<New Premium Written by company in 2014>

II Japan’s Position in the World Life Insurance Market

III Overview ofLife Insurance Business in Japan

71

88 89.4 88.5 89.6 90.592.3 91.3 91.6

93.7 9593 91.8

89.687.5 86 85.8

40

50

60

70

80

90

100

1965 1968 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 201213

(1) Changes in Life Insurance Ownership Rate per Households (including Annuity)

Source: Japan Institute of Life Insurance: Consumer SurveyNote: The data includes the total of private life insurance (including Japan Post Insurance), postal insurance and JA cooperative

(%)

III Overview of Life Insurance Business in Japan

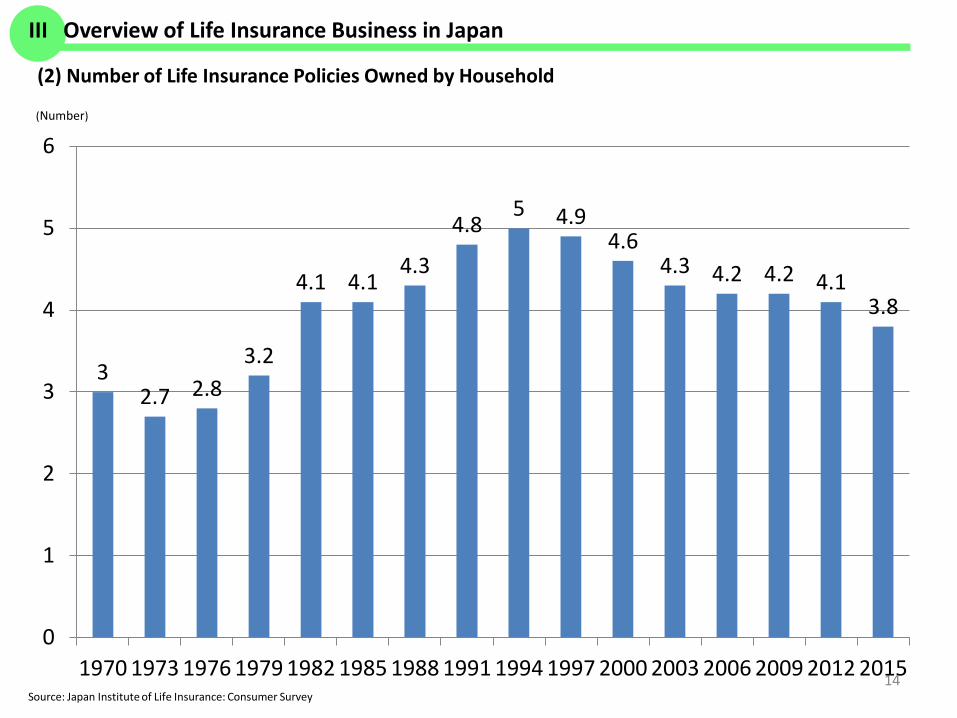

14

(2) Number of Life Insurance Policies Owned by Household

Source: Japan Institute of Life Insurance: Consumer Survey

(Number)

32.7 2.8

3.2

4.1 4.14.3

4.85 4.9

4.64.3 4.2 4.2 4.1

3.8

0

1

2

3

4

5

6

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

III Overview of Life Insurance Business in Japan

15

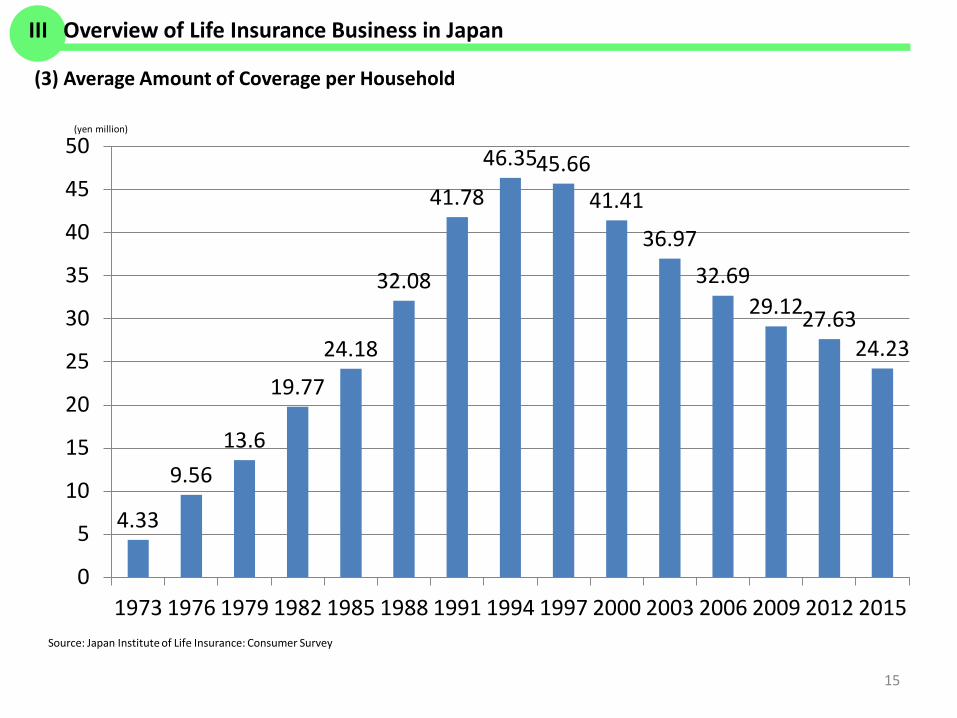

(3) Average Amount of Coverage per Household

Source: Japan Institute of Life Insurance: Consumer Survey

(yen million)

4.33

9.5613.6

19.77

24.18

32.08

41.78

46.3545.6641.41

36.9732.69

29.1227.6324.23

0

5

10

15

20

25

30

35

40

45

50

1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

III Overview of Life Insurance Business in Japan

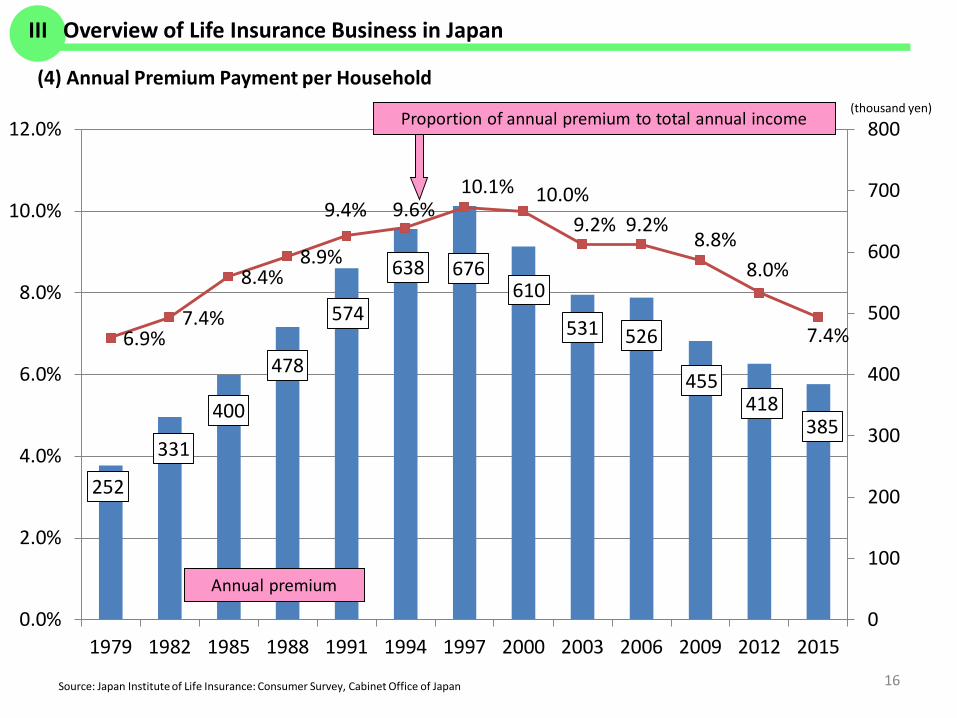

252

331

400

478

574

638 676 610

531 526

455 418

385

6.9%7.4%

8.4%8.9%

9.4% 9.6%10.1% 10.0%

9.2% 9.2%8.8%

8.0%

7.4%

0

100

200

300

400

500

600

700

800

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 201516

(4) Annual Premium Payment per Household

Source: Japan Institute of Life Insurance: Consumer Survey, Cabinet Office of Japan

Annual premium

Proportion of annual premium to total annual income(thousand yen)

III Overview of Life Insurance Business in Japan

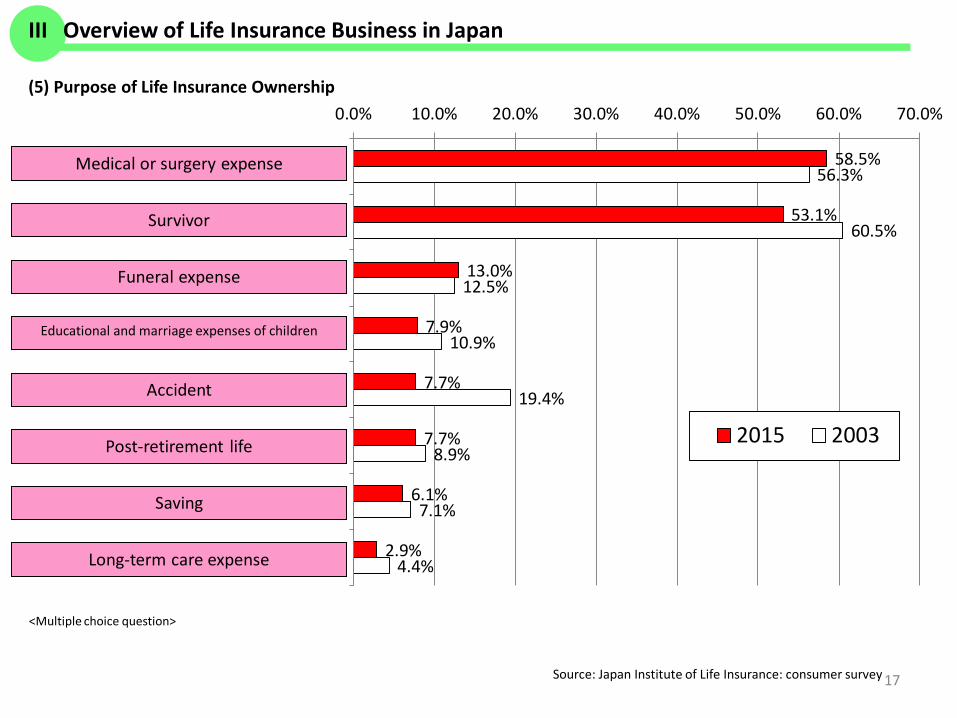

17Source: Japan Institute of Life Insurance: consumer survey

<Multiple choice question>

(5) Purpose of Life Insurance Ownership

58.5%

53.1%

13.0%

7.9%

7.7%

7.7%

6.1%

2.9%

56.3%

60.5%

12.5%

10.9%

19.4%

8.9%

7.1%

4.4%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

1

2

3

4

5

6

7

8

2015 2003

Long-term care expense

Saving

Post-retirement life

Accident

Educational and marriage expenses of children

Funeral expense

Survivor

Medical or surgery expense

III Overview of Life Insurance Business in Japan

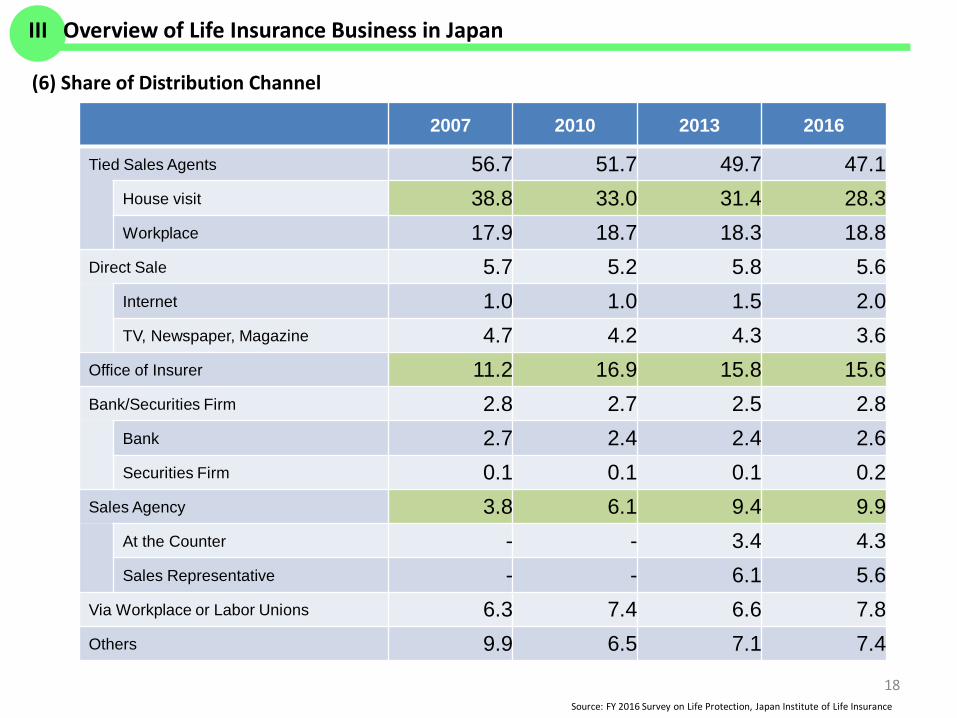

18

(6) Share of Distribution Channel

Source: FY 2016 Survey on Life Protection, Japan Institute of Life Insurance

2007 2010 2013 2016

Tied Sales Agents 56.7 51.7 49.7 47.1 House visit 38.8 33.0 31.4 28.3 Workplace 17.9 18.7 18.3 18.8

Direct Sale 5.7 5.2 5.8 5.6 Internet 1.0 1.0 1.5 2.0 TV, Newspaper, Magazine 4.7 4.2 4.3 3.6

Office of Insurer 11.2 16.9 15.8 15.6 Bank/Securities Firm 2.8 2.7 2.5 2.8

Bank 2.7 2.4 2.4 2.6 Securities Firm 0.1 0.1 0.1 0.2

Sales Agency 3.8 6.1 9.4 9.9 At the Counter - - 3.4 4.3 Sales Representative - - 6.1 5.6

Via Workplace or Labor Unions 6.3 7.4 6.6 7.8 Others 9.9 6.5 7.1 7.4

III Overview of Life Insurance Business in Japan

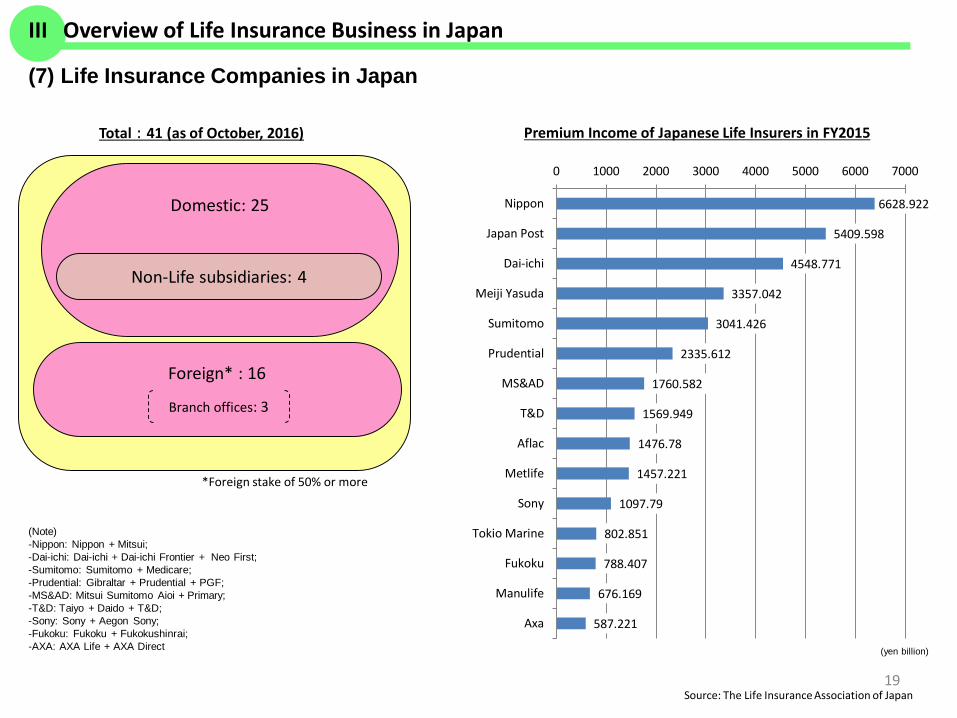

19

Total : 41 (as of October, 2016)

Foreign* : 16

Branch offices: 3

Domestic: 25

*Foreign stake of 50% or more

Premium Income of Japanese Life Insurers in FY2015

Source: The Life Insurance Association of Japan

(yen billion)

(7) Life Insurance Companies in Japan

Non-Life subsidiaries: 4

III Overview of Life Insurance Business in Japan

(Note) -Nippon: Nippon + Mitsui;-Dai-ichi: Dai-ichi + Dai-ichi Frontier + Neo First; -Sumitomo: Sumitomo + Medicare; -Prudential: Gibraltar + Prudential + PGF; -MS&AD: Mitsui Sumitomo Aioi + Primary; -T&D: Taiyo + Daido + T&D;-Sony: Sony + Aegon Sony; -Fukoku: Fukoku + Fukokushinrai;-AXA: AXA Life + AXA Direct

6628.922

5409.598

4548.771

3357.042

3041.426

2335.612

1760.582

1569.949

1476.78

1457.221

1097.79

802.851

788.407

676.169

587.221

0 1000 2000 3000 4000 5000 6000 7000

Nippon

Japan Post

Dai-ichi

Meiji Yasuda

Sumitomo

Prudential

MS&AD

T&D

Aflac

Metlife

Sony

Tokio Marine

Fukoku

Manulife

Axa

20

Source: The Life Insurance Association of Japan

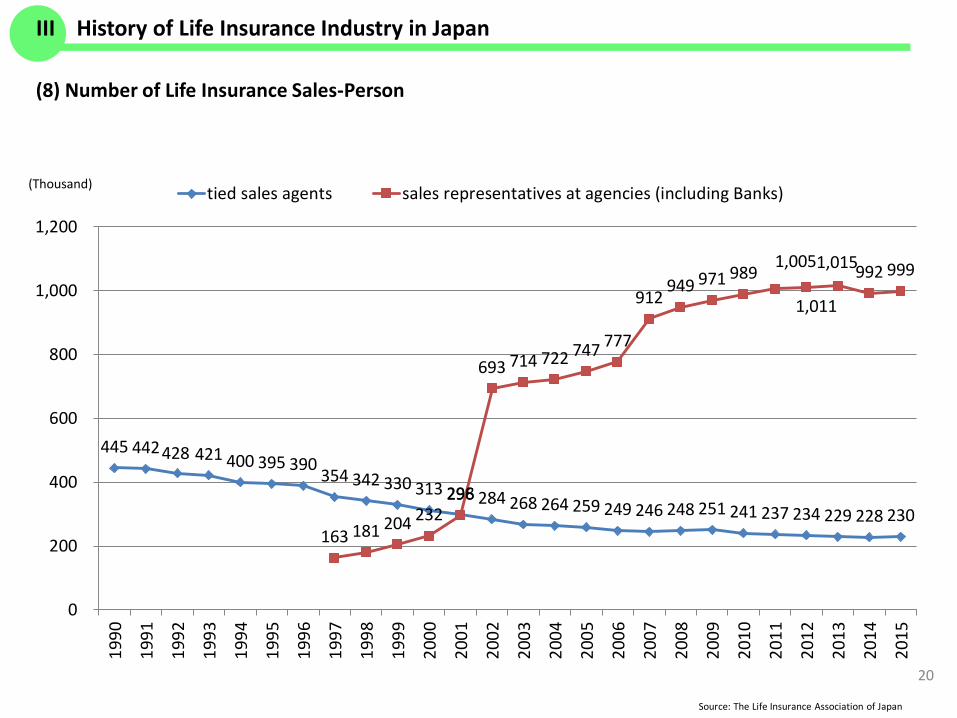

(Thousand)

(8) Number of Life Insurance Sales-Person

III History of Life Insurance Industry in Japan

445 442 428 421 400 395 390 354 342 330 313 298 284 268 264 259 249 246 248 251 241 237 234 229 228 230 163 181 204 232

296

693 714 722 747 777

912 949 971 989 1,005

1,011

1,015 992 999

0

200

400

600

800

1,000

1,200

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

tied sales agents sales representatives at agencies (including Banks)

21

New policies

(Number; million)

Policies in Force

(Number; million)

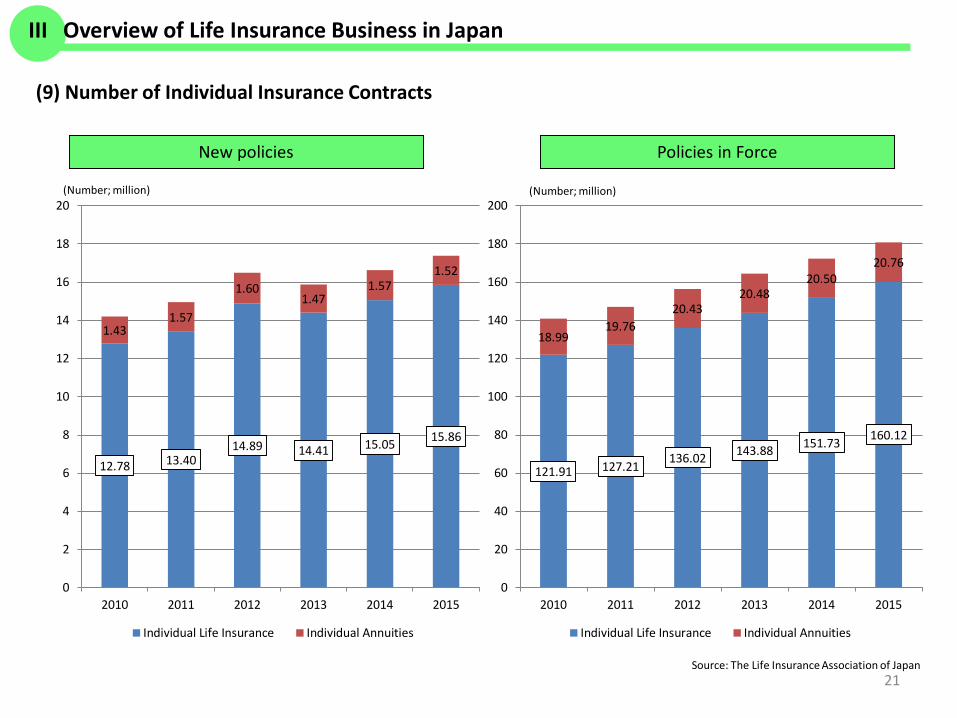

(9) Number of Individual Insurance Contracts

Source: The Life Insurance Association of Japan

III Overview of Life Insurance Business in Japan

12.78 13.40 14.89 14.41 15.05 15.86

1.43 1.57

1.60 1.47

1.57 1.52

0

2

4

6

8

10

12

14

16

18

20

2010 2011 2012 2013 2014 2015

Individual Life Insurance Individual Annuities

121.91 127.21 136.02 143.88 151.73 160.12

18.99 19.76

20.43 20.48

20.50 20.76

0

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013 2014 2015

Individual Life Insurance Individual Annuities

22

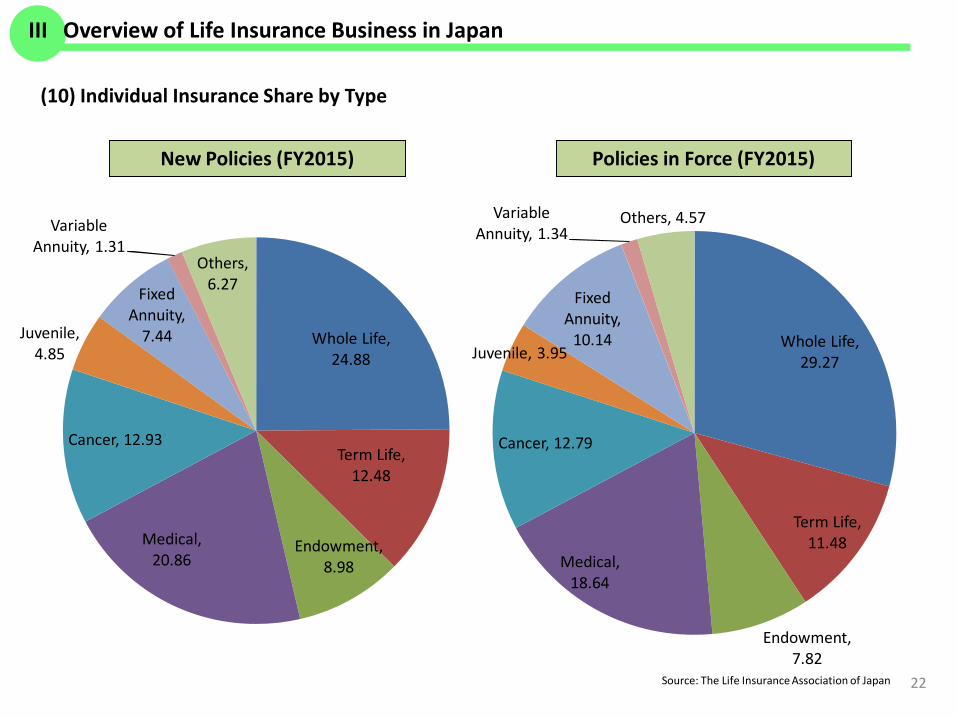

(10) Individual Insurance Share by Type

Source: The Life Insurance Association of Japan

Policies in Force (FY2015)New Policies (FY2015)

III Overview of Life Insurance Business in Japan

Whole Life, 24.88

Term Life, 12.48

Endowment, 8.98

Medical, 20.86

Cancer, 12.93

Juvenile, 4.85

Fixed Annuity,

7.44

Variable Annuity, 1.31

Others, 6.27

Whole Life, 29.27

Term Life, 11.48

Endowment, 7.82

Medical, 18.64

Cancer, 12.79

Juvenile, 3.95

Fixed Annuity,

10.14

Variable Annuity, 1.34

Others, 4.57

20,448 22,734 24,099 22,721

24,546 25,607

4,802

4,679 4,374

4,312

5,154 4,730

1,116

1,114 1,109

1,113

1,119 1,125

3,813

3,926 3,684

3,852

4,176 4,563

4,276

3,836 3,874

2,740

2,227 1,724

0

5000

10000

15000

20000

25000

30000

35000

40000

2010 2011 2012 2013 2014 2015

Individual Life Insurance Individual Annuities Group Life Insurance Group Annuities Others

23

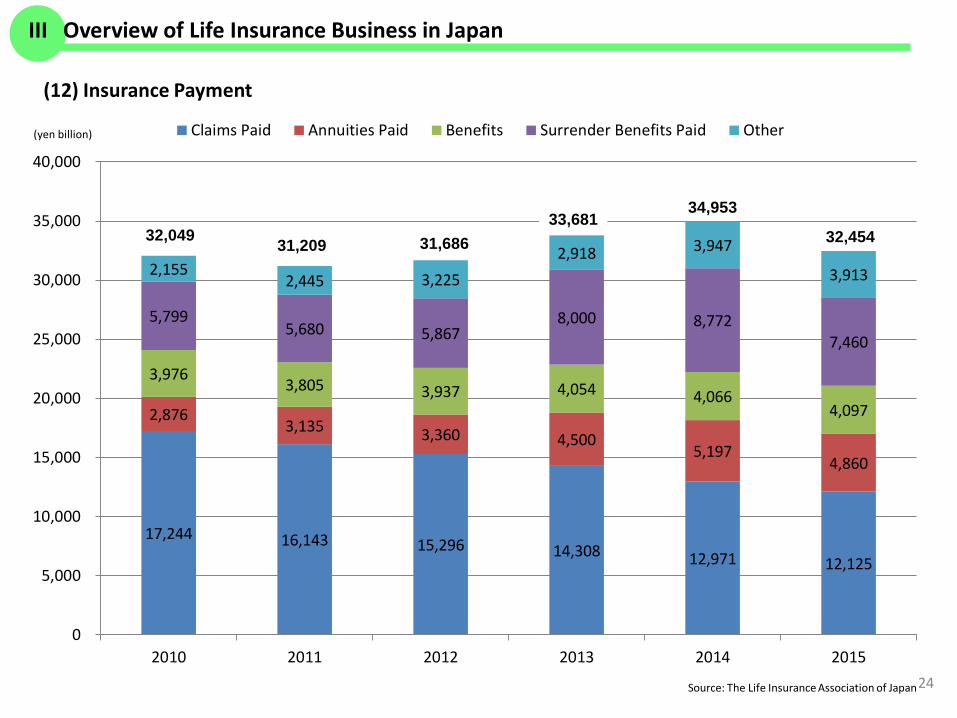

(11) Premium Income

(yen billion)

Source: The Life Insurance Association of Japan

37,22234,454

36,289 37,14034,738

III Overview of Life Insurance Business in Japan

37,748

17,244 16,143 15,296 14,308 12,971 12,125

2,876 3,135 3,360 4,500

5,197 4,860

3,976 3,805 3,937 4,054 4,066

4,097

5,799 5,680 5,867

8,000 8,772 7,460

2,155 2,445 3,225

2,918 3,947

3,913

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2010 2011 2012 2013 2014 2015

Claims Paid Annuities Paid Benefits Surrender Benefits Paid Other

24

(12) Insurance Payment

(yen billion)

Source: The Life Insurance Association of Japan

33,68131,68631,20932,049

34,953

III Overview of Life Insurance Business in Japan

32,454

25

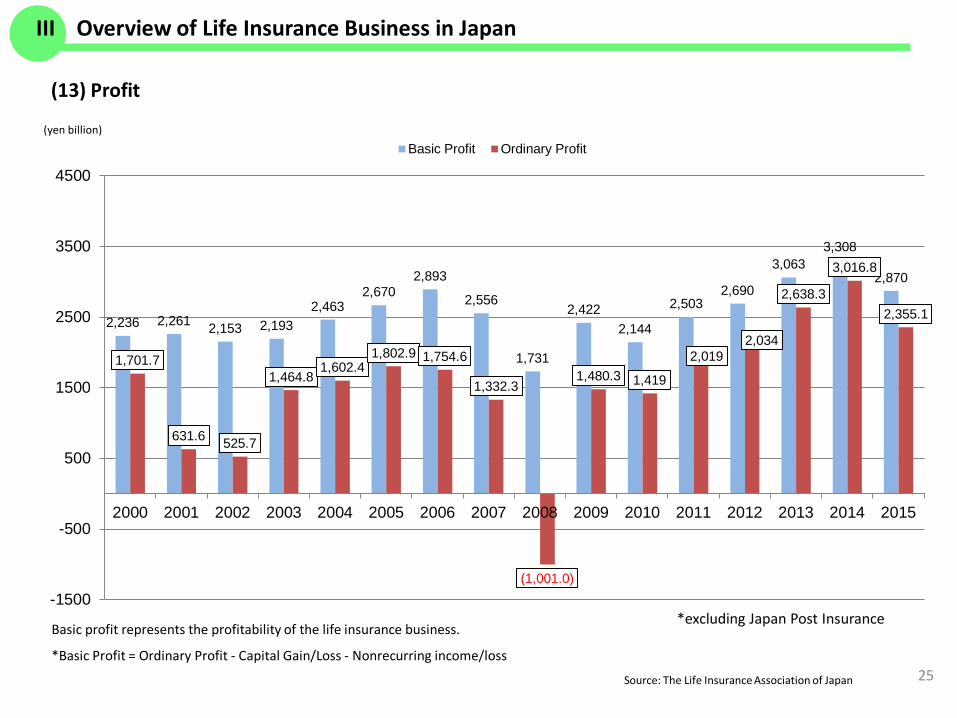

(13) Profit

(yen billion)

Source: The Life Insurance Association of Japan

Basic profit represents the profitability of the life insurance business.

*Basic Profit = Ordinary Profit - Capital Gain/Loss - Nonrecurring income/loss

III Overview of Life Insurance Business in Japan

2,236 2,261 2,153 2,1932,463

2,6702,893

2,556

1,731

2,4222,144

2,5032,690

3,0633,308

2,870

1,701.7

631.6 525.7

1,464.8 1,602.4

1,802.9 1,754.6

1,332.3

(1,001.0)

1,480.3 1,419

2,0192,034

2,638.3

3,016.8

2,355.1

-1500

-500

500

1500

2500

3500

4500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Basic Profit Ordinary Profit

*excluding Japan Post Insurance

IV Brief History ofLife Insurance Industry in Japan

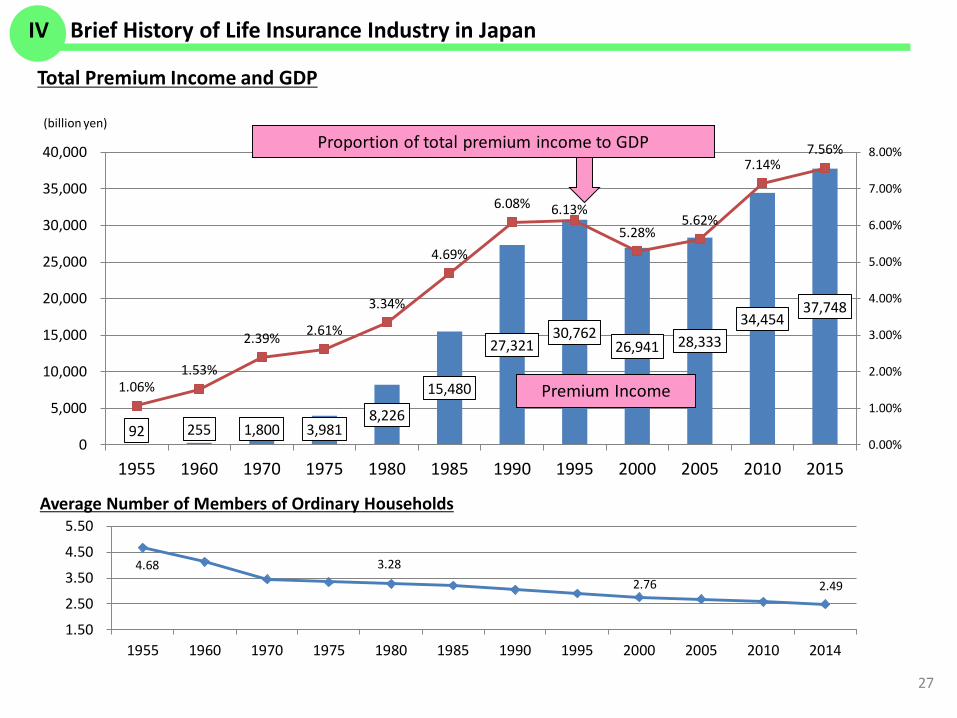

92 255 1,800 3,981 8,226

15,480

27,321 30,762

26,941 28,333 34,454

37,748

1.06%1.53%

2.39% 2.61%

3.34%

4.69%

6.08% 6.13%5.28%

5.62%

7.14%7.56%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1955 1960 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

27

Total Premium Income and GDP

(billion yen)Proportion of total premium income to GDP

Premium Income

IV Brief History of Life Insurance Industry in Japan

Average Number of Members of Ordinary Households

4.68 3.28 2.76 2.49

1.50

2.50

3.50

4.50

5.50

1955 1960 1970 1975 1980 1985 1990 1995 2000 2005 2010 2014

28

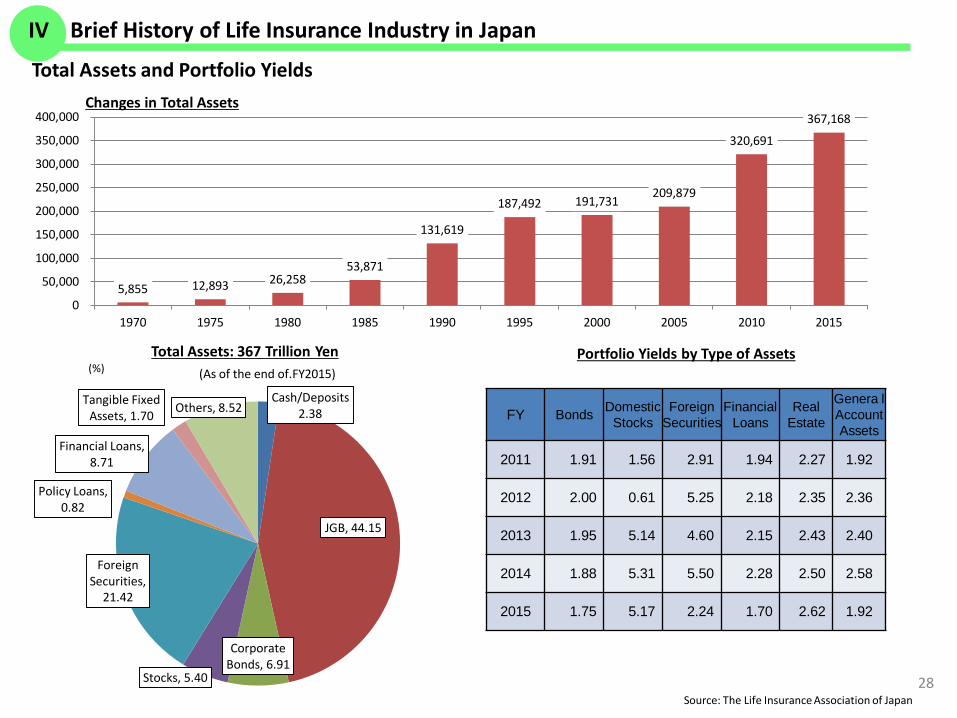

Total Assets and Portfolio Yields

(%)

Source: The Life Insurance Association of Japan

Total Assets: 367 Trillion Yen(As of the end of.FY2015)

Portfolio Yields by Type of Assets

FY Bonds Domestic Stocks

Foreign Securities

Financial Loans

Real Estate

Genera lAccount Assets

2011 1.91 1.56 2.91 1.94 2.27 1.92

2012 2.00 0.61 5.25 2.18 2.35 2.36

2013 1.95 5.14 4.60 2.15 2.43 2.40

2014 1.88 5.31 5.50 2.28 2.50 2.58

2015 1.75 5.17 2.24 1.70 2.62 1.92

Changes in Total Assets

IV Brief History of Life Insurance Industry in Japan

5,855 12,893 26,258 53,871

131,619

187,492 191,731 209,879

320,691

367,168

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Cash/Deposits 2.38

JGB, 44.15

Corporate Bonds, 6.91

Stocks, 5.40

Foreign Securities,

21.42

Policy Loans, 0.82

Financial Loans, 8.71

Tangible Fixed Assets, 1.70 Others, 8.52

29

Changes in Product Portfolio (the number of new policies)

Source: The Life Insurance Association of Japan

IV Brief History of Life Insurance Industry in Japan

87.00 77.78

81.81 79.36 83.35

73.79

47.00

36.64

17.68 12.51 9.83

4.58 12.63 8.98

1.62 1.23

1.28 1.57

1.78

8.61

10.53

12.24

12.67 24.55

17.73

14.52

9.29 12.48

4.30 5.13

5.51 17.69

22.45

23.00

31.53

23.02

27.75 24.88

7.70

14.71

12.32 21.16

35.43

33.30 33.78

0.42

0.77 0.10

1.49

3.86 13.58

14.36 7.97 13.50

10.05 8.75

11.38

20.99 16.89 18.64

9.80 12.37

35.47

21.87 18.91 13.25 11.78 8.95 6.98

11.12

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Endowment Term Whole Life Medical Annuties Others

30

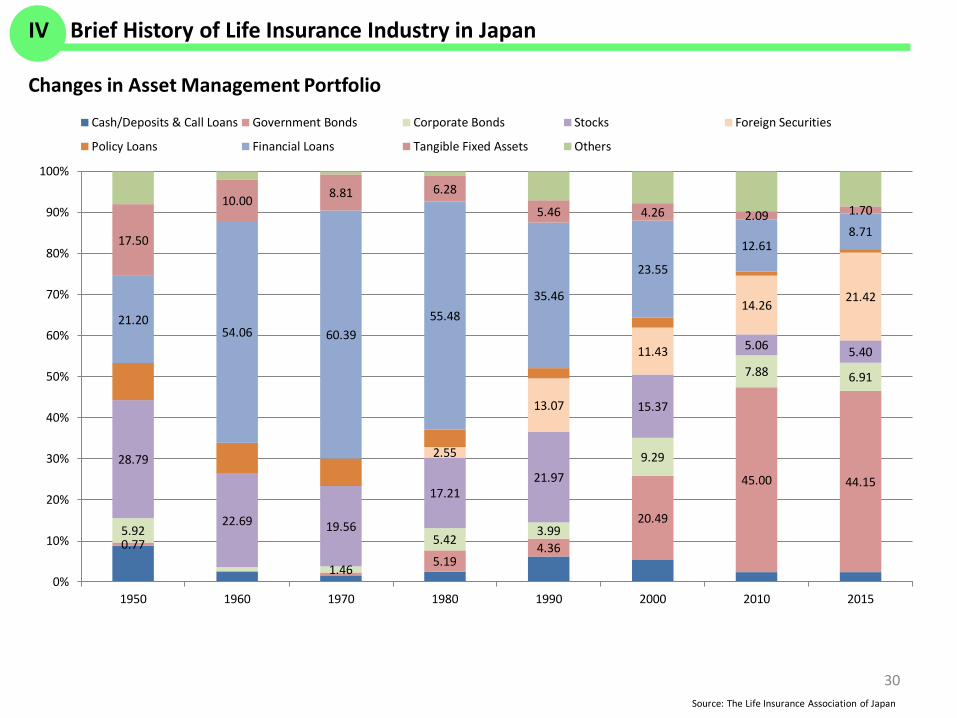

Changes in Asset Management Portfolio

Source: The Life Insurance Association of Japan

IV Brief History of Life Insurance Industry in Japan

0.77 5.19

4.36

20.49

45.00 44.15

5.92

1.46

5.42 3.99

9.29

7.88 6.91

28.79

22.69 19.56

17.21 21.97

15.37

5.06 5.40

2.55

13.07

11.43

14.26 21.42

21.20 54.06 60.39

55.48 35.46

23.55

12.61 8.71

17.50

10.00 8.81 6.28

5.46 4.26 2.09 1.70

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 1960 1970 1980 1990 2000 2010 2015

Cash/Deposits & Call Loans Government Bonds Corporate Bonds Stocks Foreign Securities

Policy Loans Financial Loans Tangible Fixed Assets Others

V Addressing the issues

-2-1012345678

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

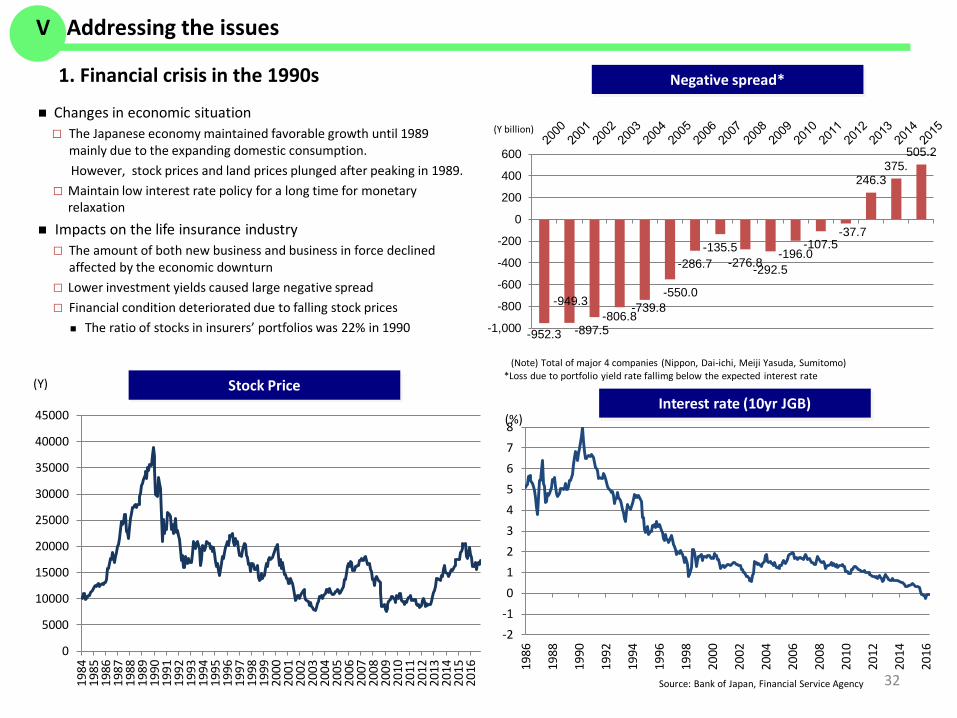

Changes in economic situation The Japanese economy maintained favorable growth until 1989

mainly due to the expanding domestic consumption. However, stock prices and land prices plunged after peaking in 1989.

Maintain low interest rate policy for a long time for monetary relaxation

Impacts on the life insurance industry The amount of both new business and business in force declined

affected by the economic downturn Lower investment yields caused large negative spread Financial condition deteriorated due to falling stock prices

The ratio of stocks in insurers’ portfolios was 22% in 1990

Stock PriceInterest rate (10yr JGB)

(Y)

(%)

Negative spread*

(Y billion)

Source: Bank of Japan, Financial Service Agency

*Loss due to portfolio yield rate fallimg below the expected interest rate

32

(Note) Total of major 4 companies (Nippon, Dai-ichi, Meiji Yasuda, Sumitomo)

V Addressing the issues

1. Financial crisis in the 1990s

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-952.3

-949.3

-897.5-806.8

-739.8-550.0

-286.7-135.5

-276.8-292.5-196.0

-107.5-37.7

246.3375.

505.2

-1,000

-800

-600

-400

-200

0

200

400

600

Bankruptcy cases of life insurers

Nissan Life Toho Life Daihyaku Life Taisho Life Chiyoda Life Kyoei Life Tokyo Life Yamato Life

Procedure Administrative Administrative Administrative Administrative Judicial Judicial Judicial Judicial

Excess liabilities (a)-(b)

Approx. 302.9(April 1997)

Approx .650(June 1999)

Approx. 317.7(May 2000)

Approx. 36.5(August 2000)

Approx. 595(October 13, 2000)

Approx. 689.5(October 23, 2000)

Approx. 73.1(March 31, 2001)

Approx. 64.3(October 17, 2008)

Asset (a)(billion yen)

1,822.7 2,190 1,300 154.5 2,233 3,725 690 194.9

Liability(b)(billion yen)

2,125.6 2,840 1,617.6 191 2,828 4,414.5 763.2 259.2

Relief Insurance Company

Aoba Life(Prudential Life)

GE Edison Life(Gibraltar Life)

Manulife LifeAzami Life(PGF Life)

AIG Star Life(Gibraltar Life)

Gibraltar Life T&D Financial Life

Prudential Financial Japan

Life(PGF Life)

Aid amount by LIPPCJ (billion yen) 200 366.3 145 26.7 0 0 0 27.8

Changes in Policy

Reduction of policy reserve No reduction 10% 10% 10% 10% 8% No reduction

10%(additional

reduction for high-interest

policy)

Post-reduction expected interest rate

2.75% 1.5% 1.0% 1.0% 1.5% 1.75% 2.6% 1.0%

Date of ResolutionOctober 1, 1997

Transfer of contract

March 1, 2000Transfer of

contract

April 2, 2001Transfer of contract

March 31, 2001Transfer of contract

April 20, 2001 Conversion to a stock company

(Restart business)

April 3, 2001Restart business

October 19, 2001Conversion to a stock company

(Restart business)

June 1, 2009Restart business

33

V Addressing the issues

012345678

b) Stock Holding

34

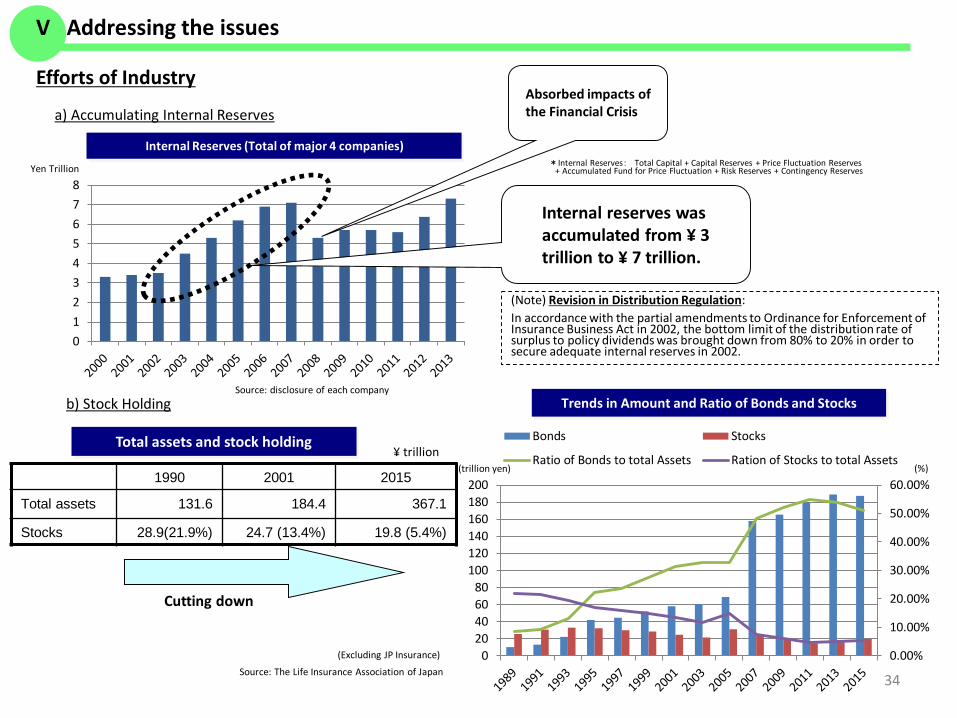

Efforts of Industry

a) Accumulating Internal Reserves

Yen Trillion

Internal Reserves (Total of major 4 companies)

Internal reserves was accumulated from ¥ 3 trillion to ¥ 7 trillion.

Source: disclosure of each company

*Internal Reserves: Total Capital + Capital Reserves + Price Fluctuation Reserves+ Accumulated Fund for Price Fluctuation + Risk Reserves + Contingency Reserves

Total assets and stock holding

1990 2001 2015

Total assets 131.6 184.4 367.1

Stocks 28.9(21.9%) 24.7 (13.4%) 19.8 (5.4%)

Cutting down

¥ trillion(%)(trillion yen)

Trends in Amount and Ratio of Bonds and Stocks

(Excluding JP Insurance)

Source: The Life Insurance Association of Japan

(Note) Revision in Distribution Regulation: In accordance with the partial amendments to Ordinance for Enforcement of Insurance Business Act in 2002, the bottom limit of the distribution rate of surplus to policy dividends was brought down from 80% to 20% in order to secure adequate internal reserves in 2002.

Absorbed impacts of the Financial Crisis

V Addressing the issues

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

020406080

100120140160180200

Bonds Stocks

Ratio of Bonds to total Assets Ration of Stocks to total Assets

0

1

2

3

4

5

6

7

8

9

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Standard Interest Rate Portfolio Yield of General Account Assets

10.00

12.00

14.00

16.00

18.00

35

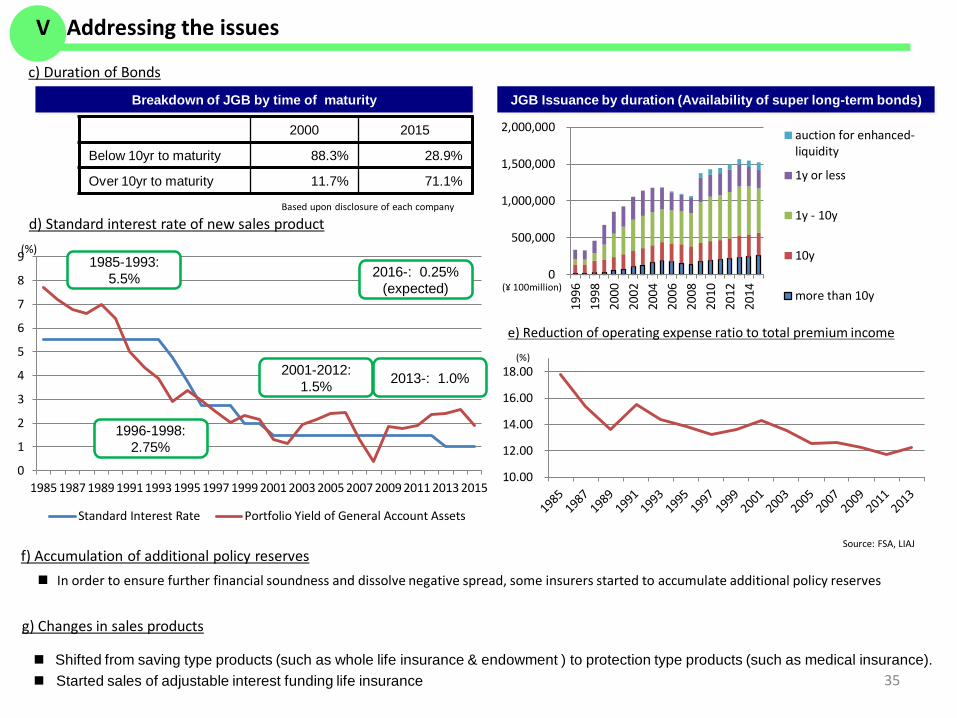

c) Duration of Bonds

Breakdown of JGB by time of maturity

2000 2015

Below 10yr to maturity 88.3% 28.9%

Over 10yr to maturity 11.7% 71.1%

Based upon disclosure of each company

d) Standard interest rate of new sales product(%)

Source: FSA, LIAJ

g) Changes in sales products

Shifted from saving type products (such as whole life insurance & endowment ) to protection type products (such as medical insurance). Started sales of adjustable interest funding life insurance

1985-1993: 5.5%

1996-1998: 2.75%

2001-2012: 1.5% 2013-: 1.0%

f) Accumulation of additional policy reserves In order to ensure further financial soundness and dissolve negative spread, some insurers started to accumulate additional policy reserves

e) Reduction of operating expense ratio to total premium income

(%)

V Addressing the issues

2016-: 0.25%(expected)

0

500,000

1,000,000

1,500,000

2,000,000

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

auction for enhanced-liquidity

1y or less

1y - 10y

10y

more than 10y(¥ 100million)

JGB Issuance by duration (Availability of super long-term bonds)

(%)

36

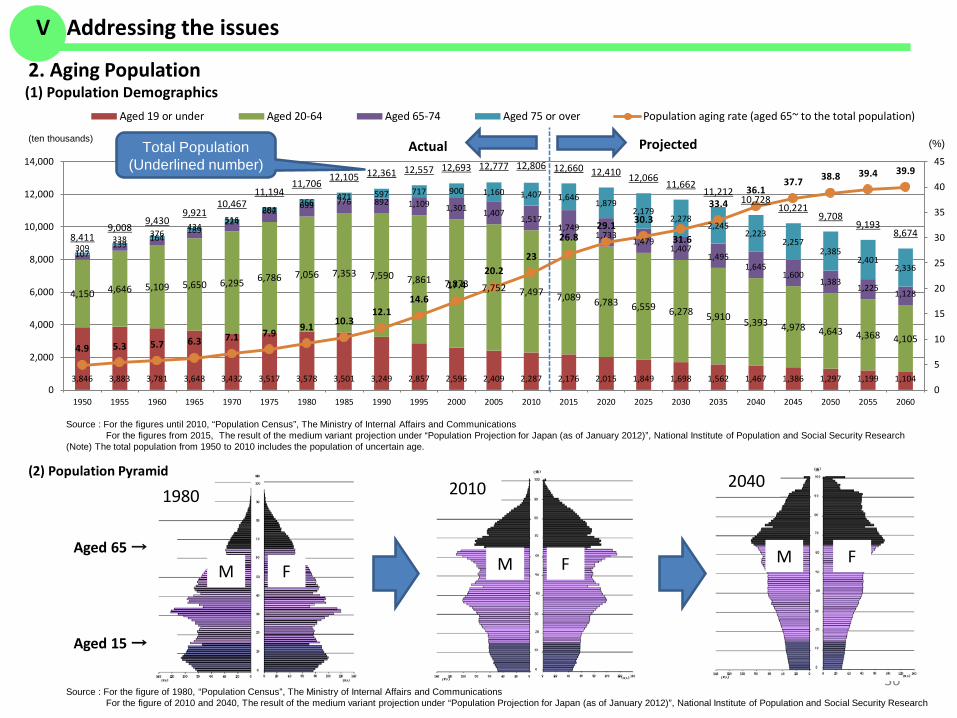

2. Aging Population

3,846 3,883 3,781 3,648 3,432 3,517 3,578 3,501 3,249 2,857 2,596 2,409 2,287 2,176 2,015 1,849 1,698 1,562 1,467 1,386 1,297 1,199 1,104

4,150 4,646 5,109 5,650 6,295 6,786 7,056 7,353 7,590 7,861 7,873 7,752 7,497 7,089 6,783 6,559 6,278 5,910 5,393 4,978 4,643 4,368 4,105

309338

376434

516602 699 776 892 1,109 1,301 1,407

1,5171,749

1,7331,479

1,4071,495

1,6451,600

1,3831,225 1,128

107139

164189

224284

366 471 597 717 900 1,160 1,407 1,6461,879

2,1792,278

2,2452,223

2,2572,385

2,4012,336

8,4119,008

9,4309,921

10,46711,194

11,706 12,105 12,361 12,557 12,693 12,777 12,806 12,660 12,410 12,066 11,66211,212

10,72810,221

9,7089,193

8,674

4.9 5.3 5.7 6.3 7.1 7.9 9.1 10.312.1

14.617.4

20.223

26.829.1 30.3

31.6

33.436.1

37.7 38.8 39.4 39.9

0

5

10

15

20

25

30

35

40

45

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

Aged 19 or under Aged 20-64 Aged 65-74 Aged 75 or over Population aging rate (aged 65~ to the total population)

ProjectedActual(ten thousands)

(2) Population Pyramid

M F M F M F

2010 20401980

Aged 65 →

Aged 15 →

Source : For the figures until 2010, “Population Census”, The Ministry of Internal Affairs and CommunicationsFor the figures from 2015, The result of the medium variant projection under “Population Projection for Japan (as of January 2012)”, National Institute of Population and Social Security Research

(Note) The total population from 1950 to 2010 includes the population of uncertain age.

Source : For the figure of 1980, “Population Census”, The Ministry of Internal Affairs and CommunicationsFor the figure of 2010 and 2040, The result of the medium variant projection under “Population Projection for Japan (as of January 2012)”, National Institute of Population and Social Security Research

Total Population(Underlined number)

(1) Population Demographics

V Addressing the issues

37

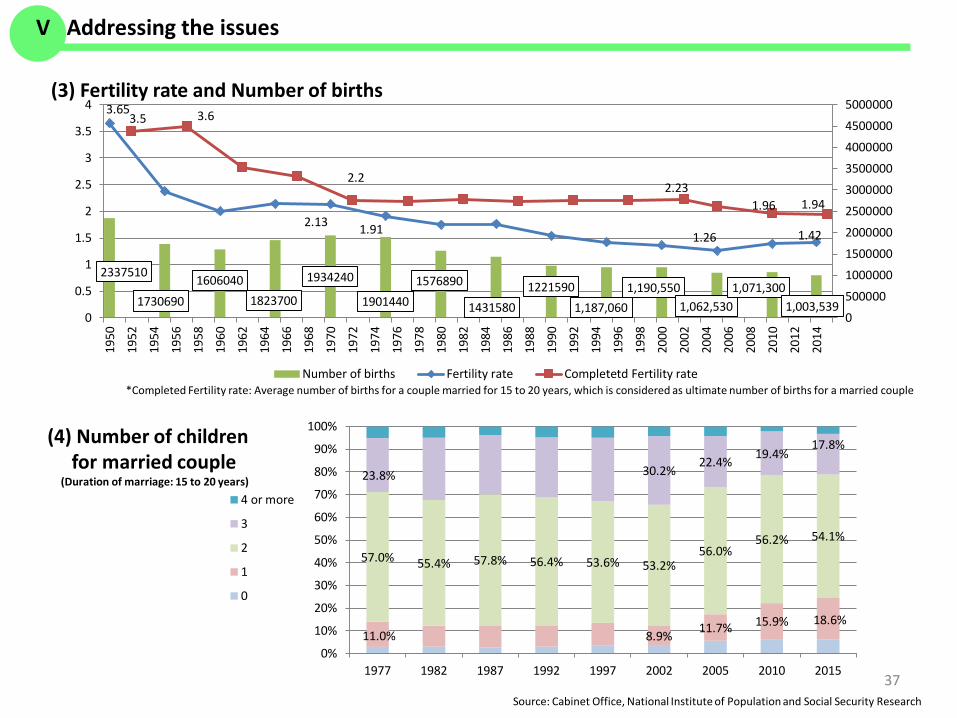

(3) Fertility rate and Number of births

Source: Cabinet Office, National Institute of Population and Social Security Research

V Addressing the issues

2337510

17306901606040

1823700

1934240

19014401576890

14315801221590

1,187,0601,190,550

1,062,5301,071,300

1,003,539

3.65

2.13 1.91 1.26 1.42

3.5 3.6

2.22.23

1.96 1.94

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

5000000

0

0.5

1

1.5

2

2.5

3

3.5

419

50

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Number of births Fertility rate Completetd Fertility rate

11.0% 8.9% 11.7% 15.9% 18.6%

57.0% 55.4% 57.8% 56.4% 53.6% 53.2%56.0%

56.2% 54.1%

23.8% 30.2%22.4% 19.4%

17.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1977 1982 1987 1992 1997 2002 2005 2010 2015

4 or more

3

2

1

0

(4) Number of childrenfor married couple

(Duration of marriage: 15 to 20 years)

*Completed Fertility rate: Average number of births for a couple married for 15 to 20 years, which is considered as ultimate number of births for a married couple

65.32

69.31

73.35

75.9277.72

79.6480.93

81.95 82.82 83.55 84.19

70.19

74.66

78.76

81.9

84.686.39

87.6588.68 89.55 90.29 90.93

60

65

70

75

80

85

90

95

1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060

Male Female

Estimated

38

(5) Average Life Expectancy

Source: Ministry of Health, Labour and Welfare; Ministry of Internal Affairs and Communications

V Addressing the issues

0

10

20

30

40

50

60

70

80

90

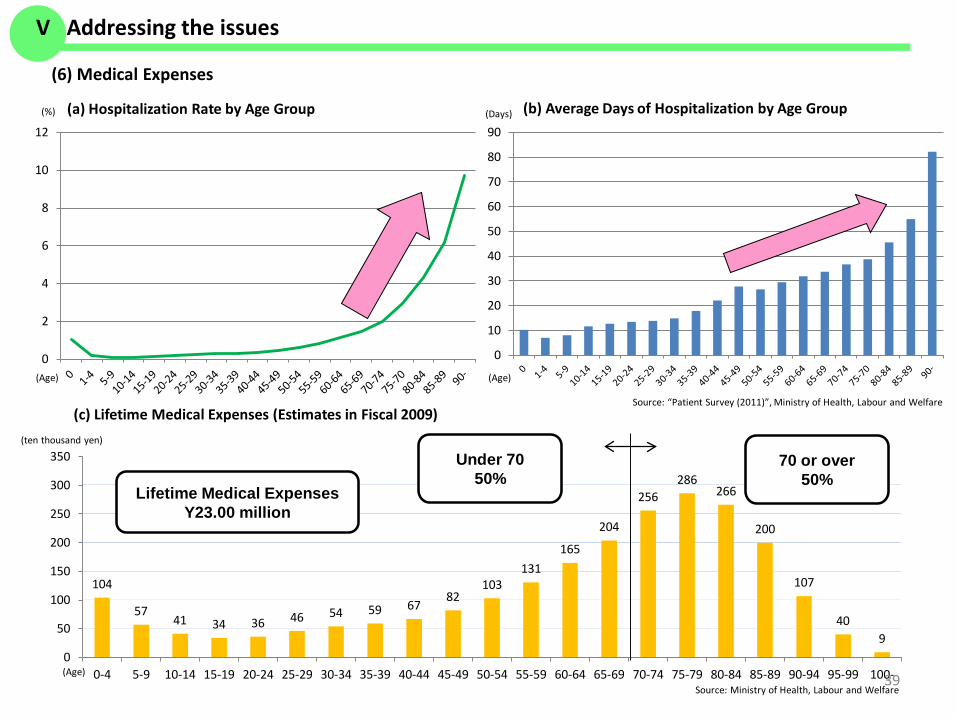

(a) Hospitalization Rate by Age Group (b) Average Days of Hospitalization by Age Group(%) (Days)

Source: “Patient Survey (2011)”, Ministry of Health, Labour and Welfare

(6) Medical Expenses

(c) Lifetime Medical Expenses (Estimates in Fiscal 2009)

104

5741 34 36 46 54 59 67

82103

131165

204

256286

266

200

107

409

0

50

100

150

200

250

300

350

0-4 5-9 10-14 15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85-89 90-94 95-99 100-Source: Ministry of Health, Labour and Welfare

(ten thousand yen)

Lifetime Medical ExpensesY23.00 million

Under 7050%

70 or over50%

39

(Age) (Age)

(Age)

0

2

4

6

8

10

12

V Addressing the issues

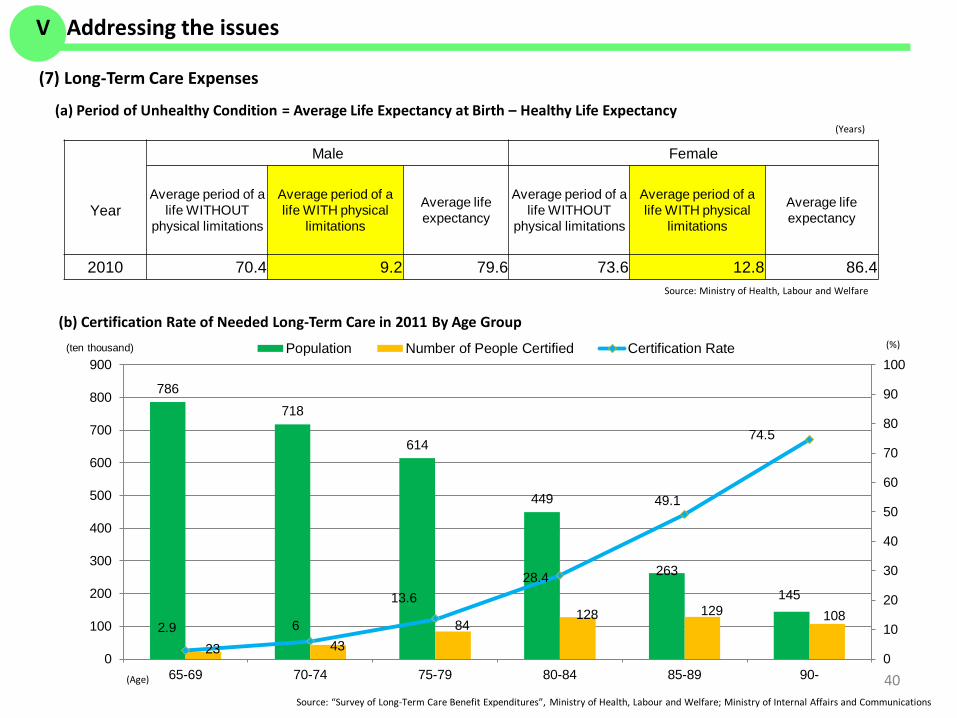

(a) Period of Unhealthy Condition = Average Life Expectancy at Birth – Healthy Life Expectancy

Male Female

YearAverage period of a

life WITHOUT physical limitations

Average period of a life WITH physical

limitations

Average life expectancy

Average period of a life WITHOUT

physical limitations

Average period of a life WITH physical

limitations

Average life expectancy

2010 70.4 9.2 79.6 73.6 12.8 86.4 Source: Ministry of Health, Labour and Welfare

(b) Certification Rate of Needed Long-Term Care in 2011 By Age Group

786718

614

449

263

145

23 4384

128 129 1082.9 6

13.628.4

49.1

74.5

0

10

20

30

40

50

60

70

80

90

100

0

100

200

300

400

500

600

700

800

900

65-69 70-74 75-79 80-84 85-89 90-

Population Number of People Certified Certification Rate(ten thousand) (%)

Source: “Survey of Long-Term Care Benefit Expenditures”, Ministry of Health, Labour and Welfare; Ministry of Internal Affairs and Communications

(7) Long-Term Care Expenses

(Age) 40

(Years)

V Addressing the issues

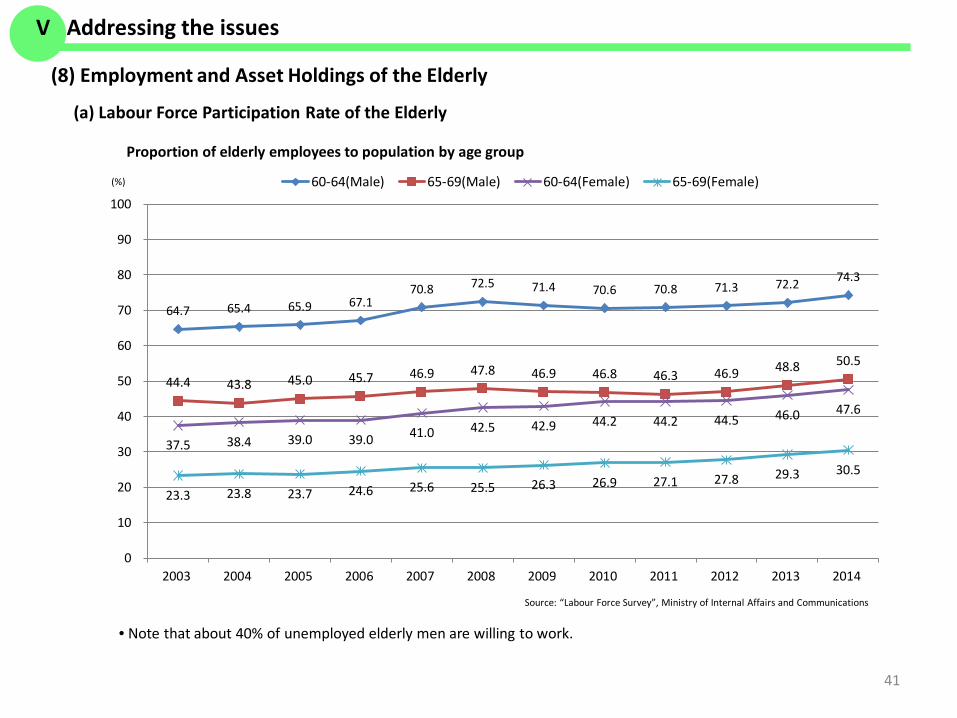

64.7 65.4 65.9 67.170.8 72.5 71.4 70.6 70.8 71.3 72.2 74.3

44.4 43.8 45.0 45.7 46.9 47.8 46.9 46.8 46.3 46.9 48.8 50.5

37.5 38.4 39.0 39.0 41.0 42.5 42.9 44.2 44.2 44.5 46.0 47.6

23.3 23.8 23.7 24.6 25.6 25.5 26.3 26.9 27.1 27.8 29.3 30.5

0

10

20

30

40

50

60

70

80

90

100

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

60-64(Male) 65-69(Male) 60-64(Female) 65-69(Female)

(a) Labour Force Participation Rate of the Elderly

Proportion of elderly employees to population by age group

Source: “Labour Force Survey”, Ministry of Internal Affairs and Communications

(%)

(8) Employment and Asset Holdings of the Elderly

• Note that about 40% of unemployed elderly men are willing to work.

41

V Addressing the issues

2.51

6.89

10.45

17.82

24.14 24.82

4.896.17

7.41 8.135.7

4.54

0

5

10

15

20

25

30

~29 30~39 40~49 50~59 60~69 70~

Savings(million yen)

Yearly income(million yen)

Amounts of Savings and Yearly income per Household by Age Group of Household Head

Source: “Family Income and Expenditure Survey (2013)”, Ministry of Internal Affairs and Communications

(million yen)

The Elderly

(b) Assets of the Elderly

(Age)

42

V Addressing the issues

43

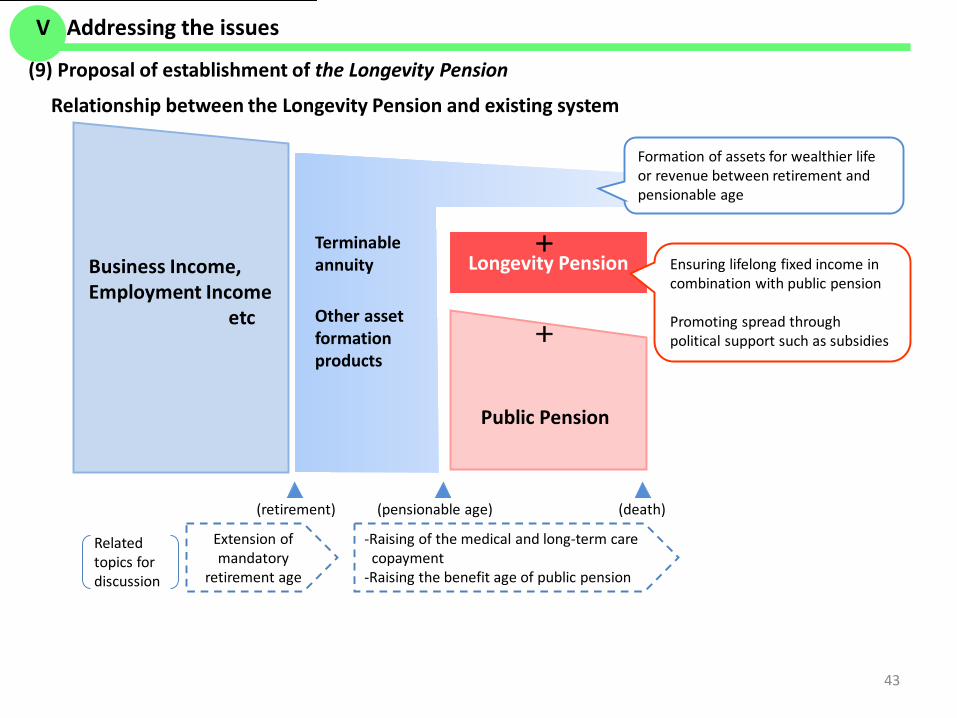

(9) Proposal of establishment of the Longevity Pension

Relationship between the Longevity Pension and existing system

Longevity Pension+

+

Public Pension

Terminable annuity

Other asset formation products

Business Income,Employment Income

etc

(retirement) (pensionable age) (death)

Formation of assets for wealthier life or revenue between retirement and pensionable age

Ensuring lifelong fixed income in combination with public pension

Promoting spread through political support such as subsidies

Related topics for discussion

Extension of mandatory

retirement age

-Raising of the medical and long-term care copayment

-Raising the benefit age of public pension

V Addressing the issues

VI The Life Insurance Association of Japan

VI The Life Insurance Association of Japan

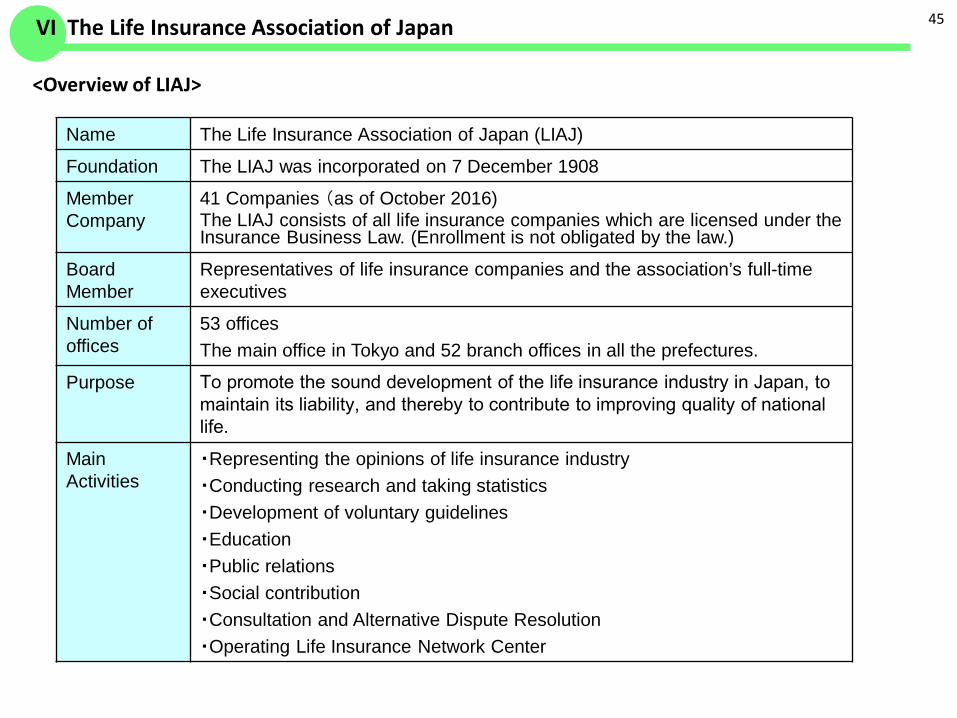

<Overview of LIAJ>

45

Name The Life Insurance Association of Japan (LIAJ)

Foundation The LIAJ was incorporated on 7 December 1908

Member Company

41 Companies (as of October 2016)The LIAJ consists of all life insurance companies which are licensed under the Insurance Business Law. (Enrollment is not obligated by the law.)

Board Member

Representatives of life insurance companies and the association’s full-time executives

Number of offices

53 officesThe main office in Tokyo and 52 branch offices in all the prefectures.

Purpose To promote the sound development of the life insurance industry in Japan, to maintain its liability, and thereby to contribute to improving quality of national life.

Main Activities

・Representing the opinions of life insurance industry・Conducting research and taking statistics・Development of voluntary guidelines・Education・Public relations・Social contribution・Consultation and Alternative Dispute Resolution ・Operating Life Insurance Network Center

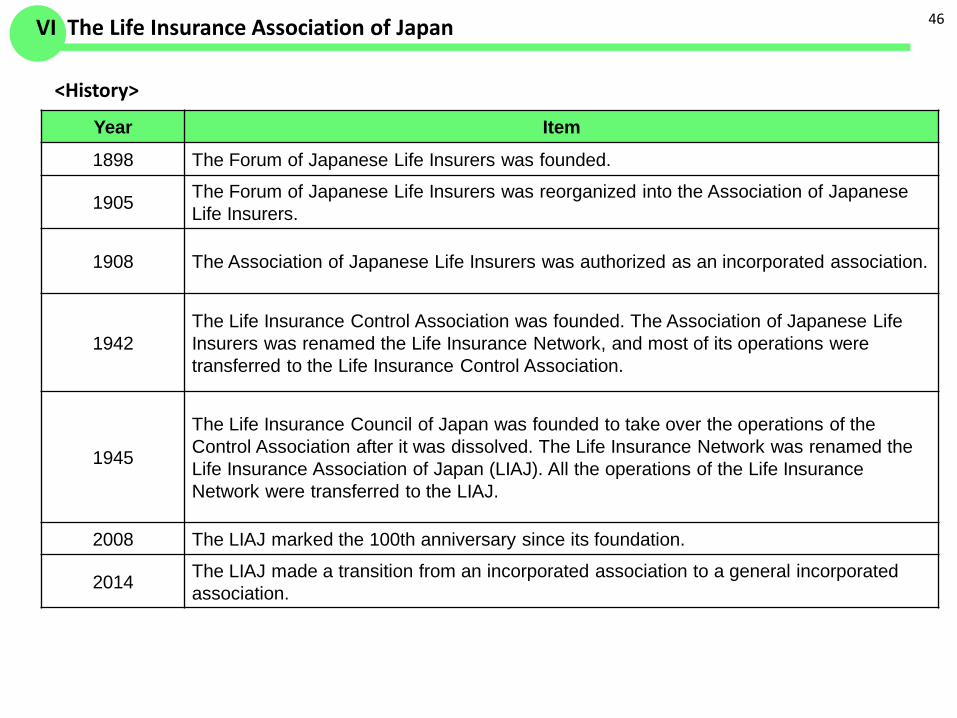

Year Item

1898 The Forum of Japanese Life Insurers was founded.

1905 The Forum of Japanese Life Insurers was reorganized into the Association of Japanese Life Insurers.

1908 The Association of Japanese Life Insurers was authorized as an incorporated association.

1942The Life Insurance Control Association was founded. The Association of Japanese Life Insurers was renamed the Life Insurance Network, and most of its operations were transferred to the Life Insurance Control Association.

1945

The Life Insurance Council of Japan was founded to take over the operations of the Control Association after it was dissolved. The Life Insurance Network was renamed the Life Insurance Association of Japan (LIAJ). All the operations of the Life Insurance Network were transferred to the LIAJ.

2008 The LIAJ marked the 100th anniversary since its foundation.

2014 The LIAJ made a transition from an incorporated association to a general incorporated association.

<History>

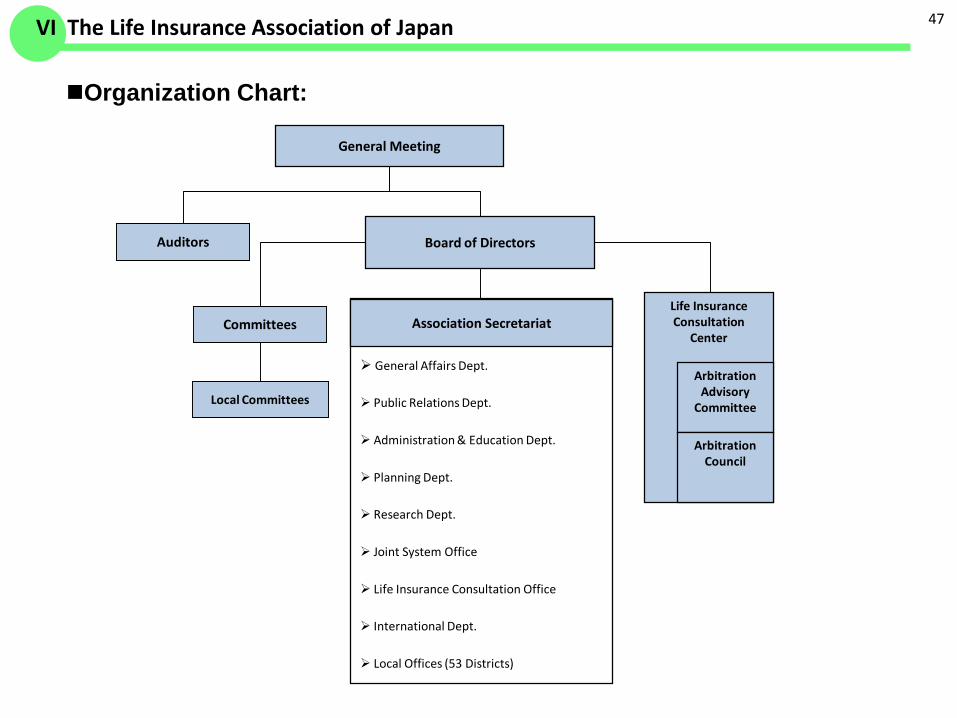

46VI The Life Insurance Association of Japan

Life Insurance Consultation

Center

Organization Chart:

General Meeting

Board of Directors

Arbitration Advisory

Committee

ArbitrationCouncil

Auditors

Committees

Local Committees

Association Secretariat

General Affairs Dept.

Public Relations Dept.

Administration & Education Dept.

Planning Dept.

Research Dept.

Joint System Office

Life Insurance Consultation Office

International Dept.

Local Offices (53 Districts)

47VI The Life Insurance Association of Japan

48

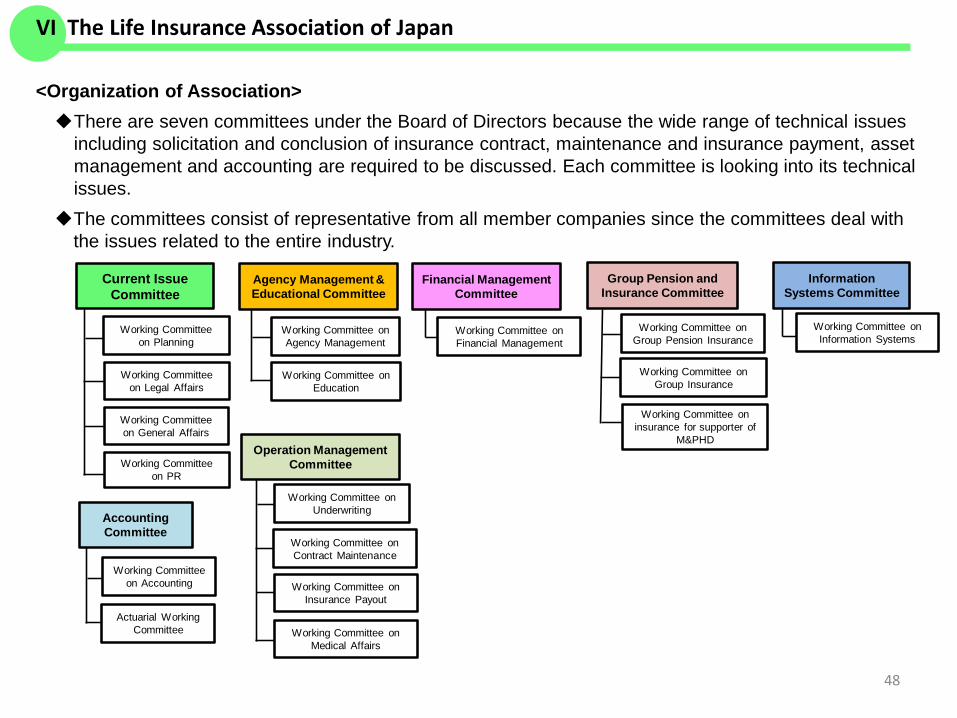

<Organization of Association>There are seven committees under the Board of Directors because the wide range of technical issues

including solicitation and conclusion of insurance contract, maintenance and insurance payment, asset management and accounting are required to be discussed. Each committee is looking into its technical issues.

The committees consist of representative from all member companies since the committees deal with the issues related to the entire industry.

Group Pension and Insurance Committee

Information Systems Committee

Accounting Committee

Operation Management Committee

Current Issue Committee

Agency Management & Educational Committee

Financial Management Committee

Working Committee on Planning

Working Committee on Legal Affairs

Working Committee on General Affairs

Working Committee on PR

Working Committee on Education

Working Committee on Agency Management

Working Committee on Financial Management

Working Committee on insurance for supporter of

M&PHD

Working Committee on Group Insurance

Working Committee on Group Pension Insurance

Working Committee on Information Systems

Actuarial Working Committee

Working Committee on Accounting

Working Committee on Medical Affairs

Working Committee on Insurance Payout

Working Committee on Contract Maintenance

Working Committee on Underwriting

VI The Life Insurance Association of Japan

49

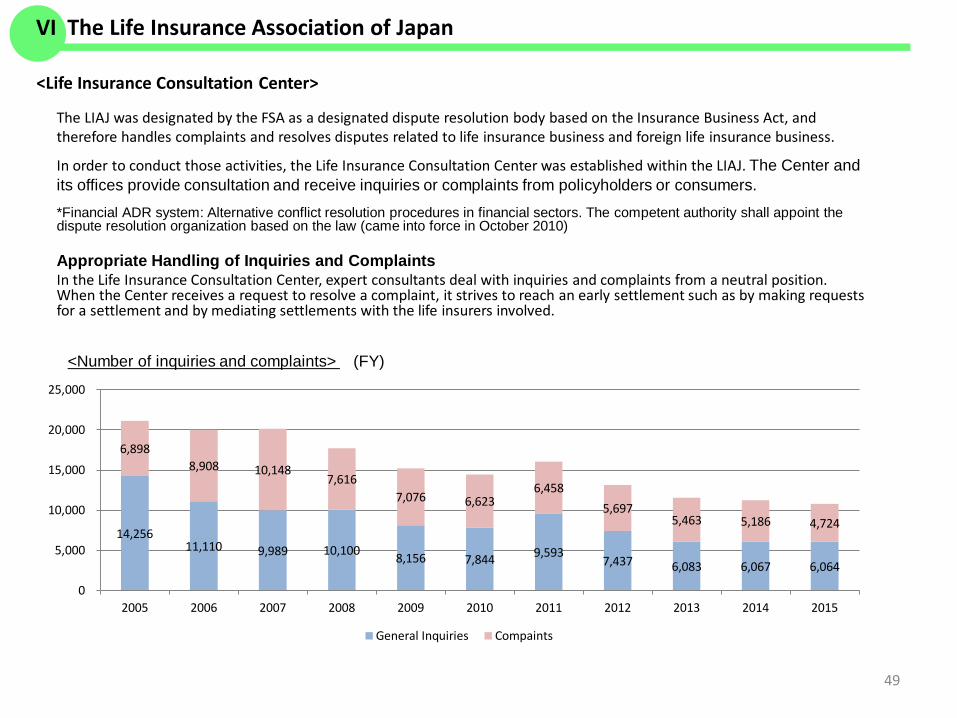

<Life Insurance Consultation Center>

The LIAJ was designated by the FSA as a designated dispute resolution body based on the Insurance Business Act, and therefore handles complaints and resolves disputes related to life insurance business and foreign life insurance business.

In order to conduct those activities, the Life Insurance Consultation Center was established within the LIAJ. The Center and its offices provide consultation and receive inquiries or complaints from policyholders or consumers.

*Financial ADR system: Alternative conflict resolution procedures in financial sectors. The competent authority shall appoint the dispute resolution organization based on the law (came into force in October 2010)

Appropriate Handling of Inquiries and ComplaintsIn the Life Insurance Consultation Center, expert consultants deal with inquiries and complaints from a neutral position. When the Center receives a request to resolve a complaint, it strives to reach an early settlement such as by making requestsfor a settlement and by mediating settlements with the life insurers involved.

<Number of inquiries and complaints> (FY)

VI The Life Insurance Association of Japan

14,256 11,110 9,989 10,100 8,156 7,844 9,593

7,437 6,083 6,067 6,064

6,898 8,908 10,148

7,616 7,076 6,623

6,458 5,697

5,463 5,186 4,724

0

5,000

10,000

15,000

20,000

25,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

General Inquiries Compaints

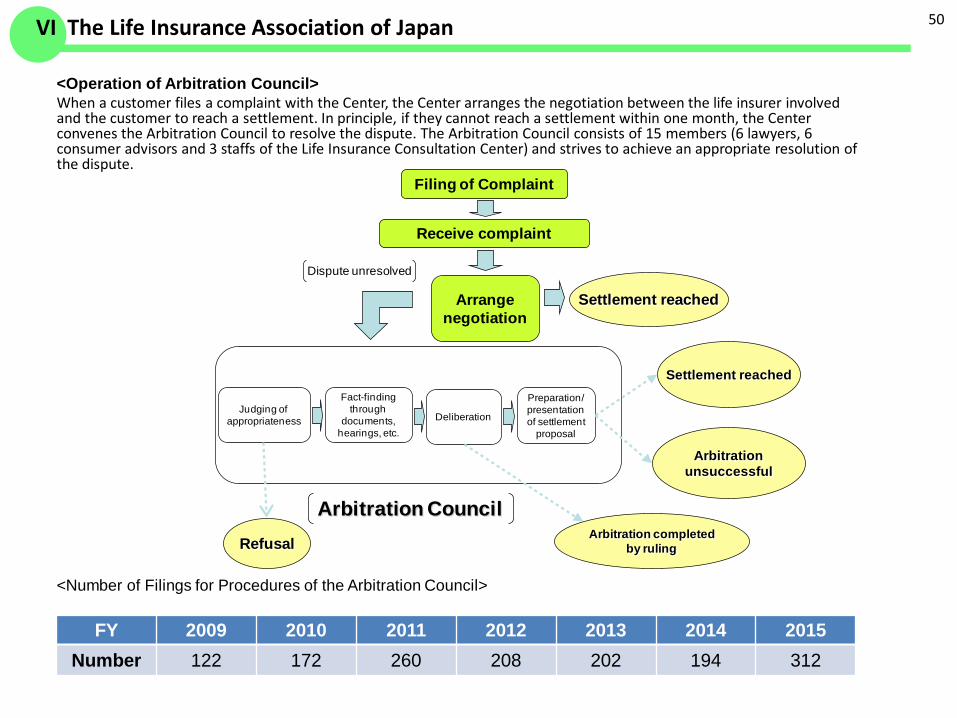

<Operation of Arbitration Council>When a customer files a complaint with the Center, the Center arranges the negotiation between the life insurer involved and the customer to reach a settlement. In principle, if they cannot reach a settlement within one month, the Center convenes the Arbitration Council to resolve the dispute. The Arbitration Council consists of 15 members (6 lawyers, 6 consumer advisors and 3 staffs of the Life Insurance Consultation Center) and strives to achieve an appropriate resolution of the dispute.

<Number of Filings for Procedures of the Arbitration Council>

50

Arbitration Council

Filing of Complaint

Judging of appropriateness

Receive complaint

Arrange negotiation

Settlement reached

Dispute unresolved

Fact-finding through

documents, hearings, etc.

Deliberation

Preparation/presentation of settlement

proposal

RefusalArbitration completed

by ruling

Settlement reached

Arbitration unsuccessful

VI The Life Insurance Association of Japan

FY 2009 2010 2011 2012 2013 2014 2015Number 122 172 260 208 202 194 312