Embed Size (px)

Citation preview

Minimising agency risks and complaints

Introduction to Evansdale Realty 2

Risky business 4What is risk? 5

Risks in business and at work 7

Risks in real estate 8

Duty of care 10The tort of negligence 10

In agency practice 11

Risk management procedures 12Analyse the risk 12

Evaluate and treat the risk 14

Who is reponsible? 17

Documentation in risk management 18Case study: a risk at Evansdale Realty. 18

Review and monitoring of risk management plans 21

Risk Management in real estate practice 22

Benefits of systematic risk management 22

Dealing with complaints 25Focus on the customer 26

Feedback to activities 30

17319B: 4 Minimising agency risks and complaints 1 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Summary 34Appendix 1: References 34

Introduction to Evansdale RealtyThroughout this topic you’ll see comments from the staff at Evansdale Realty. Here is some information about them and the agency.

Throughout this topic you’ll see comments from the staff at Evansdale Realty. Here is some information about them and the agency.

Evansdale Realty has been operating in Evansdale, Belmore Heights and surrounding areas, and as far out as Brunswick Park, for over 15 years. It specialises in commercial and residential sales and leasing.

Sarah Hampden, Manager

Sarah is the licensee-in-charge and manager of Evansdale Realty. As licensee, she oversees all aspects of the business: sales, property management, trust accounting and strata management. She manages all aspects of staffing, including induction and training.

Vince Berger, Sales manager

Vince is responsible for the day-to-day management of the sales team: listing, advertising, open house and other inspections for both commercial and residential properties.

Adrian Carrasco, Sales consultant

Adrian works on the sales team and helps Vince with all aspects of the sales process, both in the office and on the road.

2 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Jackie Mansour, Reception/sales support

Jackie wears two hats in Evansdale Realty – she’s the receptionist and also supports the sales team. She’s in charge of all office procedures and helps with the advertising, listings and photo displays.

Ellen Chu, Property manager

Ellen manages Evansdale Realty’s rental property division. She’s responsible for tracking down, inspecting, listing and letting properties and collecting rent on behalf of the owners. She has responsibility for tenant selection and sign-up for all tenancy agreements as well as for the financial aspects of leasing.

Dave Mathews, Assistant property manager

Dave helps Ellen in all aspects of her work by keeping the internal property management systems running smoothly. He’s also involved in advertising properties for lease and organising repairs and maintenance.

17319B: 4 Minimising agency risks and complaints 3 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Risky business

Life is full of risks. From the moment we get out of bed, we encounter risks in everything we do: from drinking hot beverages to driving a car to work to investing on the stock exchange. But what, exactly, is risk and how can we measure it?

Activity 1 What do you know about risk?

Choose the correct answer, then check your answer in the Feedback to activities section at the end of this topic.

1 More people are killed by donkeys than die in air crashes.

True

False

2 A person will die from total lack of sleep sooner than from starvation.

True

False

3 In Australia there are over 15 occurrences of serious injury every hour in the workplace.

True

False

4 The industry with the highest incidence and frequency rates of injury is the Construction industry.

True

False

4 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

5 Professionals have the highest average cost for each compensation claim.

True

False

What is risk?Risk can mean different things to different people. What’s unacceptably risky to one person may be merely an adrenaline rush to another.

Take BASE-jumping, for example. This is an extreme sport, similar to sky-diving, that involves jumping off tall fixed objects: buildings, antennas, spans (bridges) or earth (cliffs), using a large parachute. People who leap from all four items are given a BASE-jumping number. There are only 76 Australians with a BASE-jumping number.

For some, BASE-jumping might be unacceptably risky, perhaps even a sign of craziness, and for others it is the adrenaline rush they live—and hopefully not – die for.

So defining risk in everyday life is difficult. A risk is a hazard, something that is likely to cause danger. It involves the chance or possibility of something unpleasant happening, so it is unpredictable.

It is possible to describe risks statistically, in other words how likely it is that a particular event will occur, based on past experience. The other aspect of risk is people’s perceptions: how worried they are about a certain event happening.

17319B: 4 Minimising agency risks and complaints 5 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Activity 2 What are the odds?

What do you think are the chances of the following happening in your lifetime? Rank them from the most likely to happen (1) to the least likely to happen (8). Then check your answer in the Feedback to activities section at the end of this topic.

Rank Event

Winning Oz Lotto

Being killed by lightning

Having your house burgled

Being kidnapped

Winning a Trifecta (picking the first three horses in a 13-horse race)

Having your car stolen

Dying from a venomous bite/sting

Winning Powerball

6 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Risks in business and at work

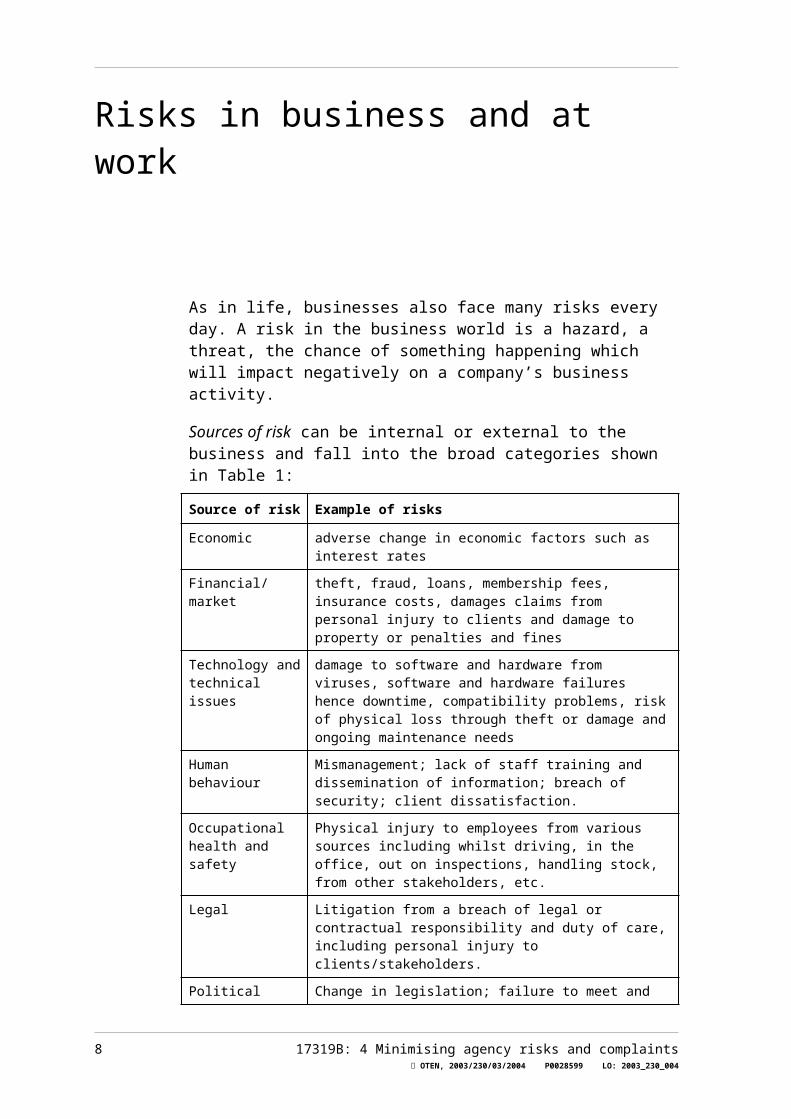

As in life, businesses also face many risks every day. A risk in the business world is a hazard, a threat, the chance of something happening which will impact negatively on a company’s business activity.

Sources of risk can be internal or external to the business and fall into the broad categories shown in Table 1:

Source of risk Example of risks

Economic adverse change in economic factors such as interest rates

Financial/market theft, fraud, loans, membership fees, insurance costs, damages claims from personal injury to clients and damage to property or penalties and fines

Technology and technical issues

damage to software and hardware from viruses, software and hardware failures hence downtime, compatibility problems, risk of physical loss through theft or damage and ongoing maintenance needs

Human behaviour Mismanagement; lack of staff training and dissemination of information; breach of security; client dissatisfaction.

Occupational health and safety

Physical injury to employees from various sources including whilst driving, in the office, out on inspections, handling stock, from other stakeholders, etc.

Legal Litigation from a breach of legal or contractual responsibility and duty of care, including personal injury to clients/stakeholders.

Political Change in legislation; failure to meet and follow statutory regulations and controls. Also deficiencies in financial controls and reporting as required by law.

Social Unfavourable publicity.

Property and equipment

Failure of machinery or equipment eg. cars, printers, cameras, etc.

Environmental Environmental damage due to mismangement of maintenace and repairs.

Natural events Earthquake, fire, flood and tempests causing disruption to business and hindrance to potential.

Table 1: Sources of risk

17319B: 4 Minimising agency risks and complaints 7 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Risks in real estate

To identify the risks in your area of work, you must first establish the context and the stakeholders.

The context is the environment in which your organisation operates. For instance, the risks to an organisation that operates a coal mine would be different to those in the property industry. Even within the property industry, the risks, and the people who could be affected, would differ for different sectors, for example Stock and Station or Strata Management.

Individuals who may affect, or be affected by, your approach to the various sources of risk in your working environment are called stakeholders. They could be employees, managers, volunteers, unions, financial and insurance organisations, customers, government, suppliers and service providers.

Stakeholders in the property industry may include:

potential vendors

vendors

potential purchasers

purchasers

prospective landlords

existing landlords

prospective tenants

existing tenants

owners corporation and community title groups

agents/third parties for purchasers and vendors

in-house staff and office contractors

other agency staff.

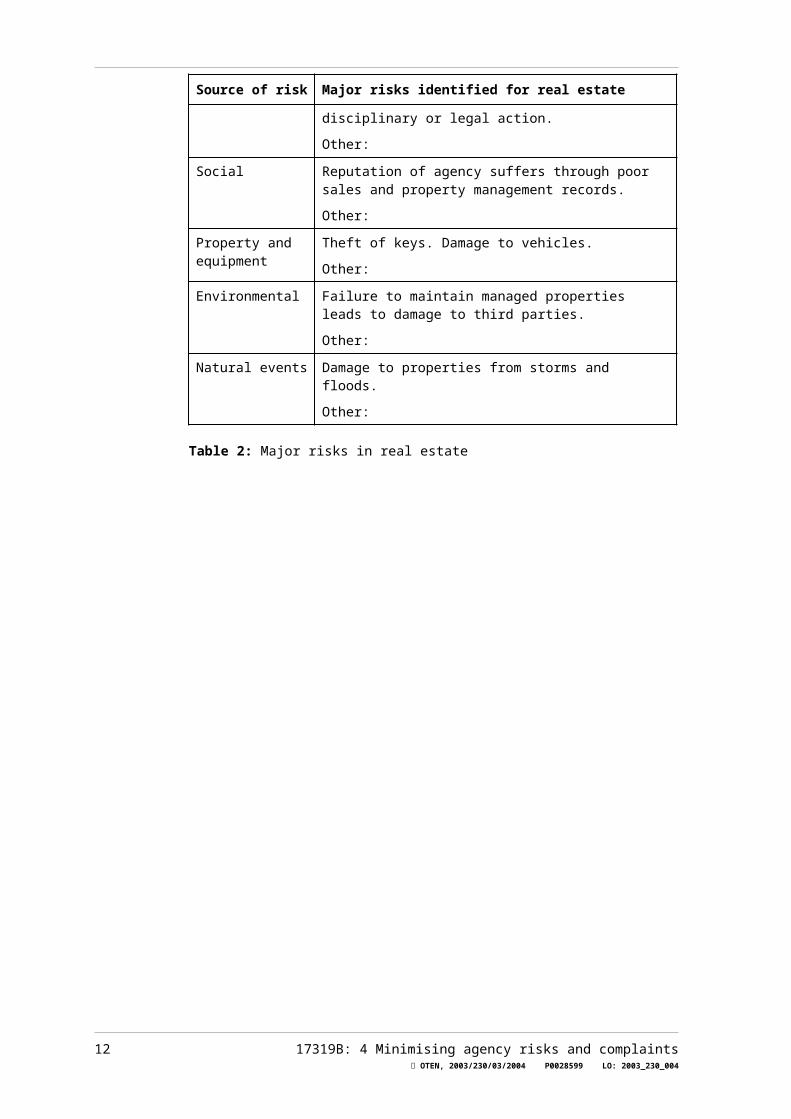

Table 2 shows some of the most common risks identified in real estate, arranged by source. Can you think of any other examples in each category, relating to other sectors of the property industry, for example strata management and stock and station agency?

Source of risk Major risks identified for real estate

Economic Interest rate rises: buyers are reluctant to purchase, sellers are less likely to list.

8 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Source of risk Major risks identified for real estate

Other:

Financial/market Finance for purchases falling through.

Other:

Technology and technical issues

Security of confidential files on computer: unauthorised staff access, theft of computers. System failures: data unavailable.

Other:

Human behaviour Misappropriation of funds; intellectual property (knowledge that staff take with them when they leave, or that they might divulge to others).

Other:

Occupational health and safety

Safety of clients.

Safety and security of staff on the road, when inspecting property, in the office. Damages claims for personal injury to tenants, clients.

Other:

Legal Badly written contracts. Agents breaching duty of care, privacy or anti-discrimination requirements. Failure to follow principal’s directions on maintenance.

Other:

Political/Legislation Agents and managers not aware of or ignoring changes to legislation, regulations, rules of conduct; possible disciplinary or legal action.

Other:

Social Reputation of agency suffers through poor sales and property management records.

Other:

Property and equipment

Theft of keys. Damage to vehicles.

Other:

Environmental Failure to maintain managed properties leads to damage to third parties.

Other:

Natural events Damage to properties from storms and floods.

Other:

Table 2: Major risks in real estate

17319B: 4 Minimising agency risks and complaints 9 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Duty of care

Sarah Hampden, Manager

When you are assessing the risks involved in the property industry, you need to be particularly aware of the possibility of litigation and your Duty of Care obligations.

You owe a duty of care to those who rely on your advice and representations. A ‘duty of care’ simply means that, at law, you must demonstrate you are employing reasonable care and diligence when you provide information or advice. You are offering a professional service and people who engage you should reasonably be able to rely on the information and advice you give them.

You need to be familiar with any legislation that may have a bearing on property or agency matters. The Rules of Conduct contained in the Property Stock and Business Agents Act, contract law, common law and industry body codes all work together to form standards that you must be aware of and work to.

Your conduct is measured against these standards in any case of negligence. If you don’t have the expected knowledge and skill levels or don’t act with care and diligence, the law protects the victim.

The tort of negligenceA tort is a civil wrong. That is, it’s a wrong committed against an individual’s personal rights which society considers unreasonable.

The infringement can be against a person, their property or their reputation. Where someone’s careless statements or conduct results in financial, physical loss or emotional hurt, the injured party can sue the offender.

There are many types of tort. Two you may have heard of are trespass and nuisance. The tort that we hear most about in relation to business matters is negligence.

The duty of care that a property professional owes to their principal, and in fact to anyone who would reasonably rely on their advice, is at the heart of any claim for negligence.

If it can be shown that a property professional owed a duty of care to a person and was negligent in the exercise of that duty, and that the person suffered physical, financial loss or emotional hurt as a result of relying on

10 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

the professional’s advice or actions, then the property professional may be found liable for negligence.

In agency practiceIn real estate practice, charges of negligence can translate into substantial claims for damages. It is no defence to show that your error or misrepresentation was made honestly and in good faith—it’s not good enough to be well meaning; you must also be conscientious and competent. This is often referred to as acting with ‘due diligence’.

Adrian Carrasco, Sales consultant

Here are some examples involving due diligence and duty of care. The first one: if you sold a block of flats on the understanding that it could be subdivided into strata lots, and the purchaser later found out that the property was held under qualified title, you would have misrepresented the property. A purchaser could take an action against your agency because you should have been aware that only property registered under Torrens title could be converted to separate strata titles.

Alternatively, if a vendor tells you that there’s a drainage easement across the back of her block and asks how this might affect the price she could get, then your duty of care dictates that you must know (or find out) the impact of this encumbrance on the land’s market price.

Realistically, although clients and customers will expect you to provide good advice, you can’t be an expert on everything. Where you don’t know, find out or recommend an appropriately qualified professional who can answer that specific question. You must always ensure that the opinions you offer your clients and customers are both correct and well informed.

17319B: 4 Minimising agency risks and complaints 11 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Risk management procedures

We have identified a range of risks in the property industry: risks to the health and safety of employees, clients and others; an agency’s or agent’s reputation; the risk of legal action, risks coming from technology, risks to equipment, financial risks and so on. Ignoring these risks could impact substantially on an agency’s viability. But what is the best way to identify and manage these risks?

In everyday life, all we often have time for is a snap decision based on minimal information and a gut feeling. But in business, it may be worth investing more time and effort and consulting with stakeholders to try to identify risks before they can cause damage to the business, or before making a particularly risky decision that could have a major impact.

A systematic approach to managing risk is now regarded as good management practice. Standards Australia has recognised this and developed the world’s first Risk Management Standard, AS/NZS 4360:1999, Risk management. This standard outlines the generic procedures and processes that need to be implemented for effective Risk Management. The procedures identified can help you establish the context and identify, analyse, treat and monitor risks.

Hint

Want to know more? A copy of AS/NZS 4360:1999, Risk management can be purchased from the Standards Australia website. For details, see under Links and references in Appendix 1.

Analyse the riskMost people use their experience, intuition and judgement to analyse risks. However, to be able to make rational, informed decisions about risks, we also need to understand some basic concepts of risk analysis and decision making.

Risk involves both uncertainty and unpleasant outcomes. In analysing risk, you need to address both these aspects. You need to consider the likelihood

12 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

of something happening and the likely consequences if any one or all of the things that could happen, do happen.

The Australian/New Zealand Standard for Risk Management AS/NZS 4360:1999 has established a table to assist in the analysis of the level of risk based on the likelihood of occurrence and the consequences. By evaluating the likelihood of a risk occurring, and the consequences of the incident, you are able to determine the level of risk to your business.

How does it work?

The likelihood of an event occurring is described as rare, unlikely, possible, likely and almost certain. The consequences of an event occurring are described as insignificant, minor, moderate, major and catastrophic. Combining the likelihood and the consequences of an event gives a risk level of low, moderate, high or extreme.

For example, a risk which is unlikely to occur (eg. car runs out of fuel on the way to an Open For Inspection) and has moderate consequences (eg. late for conducting and monitoring inspection which could have a detrimental impact on public relations with stakeholders) poses a moderate level of risk. On the other hand, an event which is unlikely to occur (someone hacking into the agency’s computer records) but which would have major implications for the agency and its clients poses a high level of risk.

The level of risk you have determined influences the way in which you treat the risk. A low level of risk would be treated with routine procedures. The treatment of a moderate level of risk would be to make a particular member of staff responsible for dealing with this situation and implementing monitoring or response procedures. A high level of risk requires action, as it has the potential to be damaging to the business, whilst an extreme level of risk requires immediate action, as it has the potential to be devastating to your business.

Therefore, our example above (the car running out of fuel on the way to an Open For Inspection) presented a moderate level of risk. Therefore it would be treated by allocating specific responsibility for maintenance of vehicles and establishing response procedures, for example sending another member of staff to the OFI.

Hint

There is more information about the level of risk table in the Australian/New Zealand Standard for Risk Management AS/NZS 4360:1999.

17319B: 4 Minimising agency risks and complaints 13 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Risk analysis case study

Adrian Carrasco, Sales consultant

In developing Evansdale Realty’s risk management strategy for Open For Inspections, we consulted former vendors through informal discussions.

We reviewed our records for the preceeding 12 months to see if there were any letters of complaint about OFIs, any OH&S incidents, incidents of personal injury and breaches of security related to OFIs.

Then we had group meetings to draw on the experience of staff.

We established the following:

agency staff had been late for the start of three OFIs

on one occasion in the previous 12 months items had allegedly been stolen from the vendor’s property

one prospective purchaser had slipped on a wet bathroom floor, fallen and seriously injured her knee

a staff member had had a car accident rushing from one OFI to another so as not to be late

After gathering this information, the agency staff identified the levels of risk shown in Table 3.

No. Risk Likelihood Consequences Level of risk

1 Staff late for OFIs Possible Minor Moderate

2 Items stolen from premises

Rare Major High

3 Personal injury to prospective purchasers

Unlikely Major High

4 Staff car accidents Likely Catastrophic Extreme

Table 3: Levels of risk

Evaluate and treat the riskAfter identifying and analysing the risks to your business, you will need to evaluate those that you are willing to accept and those that will require attention.

You may be willing to accept some risks because:

the level of risk is so low that it is not worth spending time and money treating it

14 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

the cost of treating the risk is greater than the cost of the consequences if the event happens

the benefits and opportunities offered by the risk are much greater than the threats, for example: using capital to invest in a development opportunity.

There are four ways of managing unacceptable business risks:

1. avoiding the risk

2. controlling the risk

3. transferring the risk

4. retaining the risk

Avoiding the risk

This is a method which we often employ in our own lives. We combat danger by using our common sense to avoid the risk in the first place, for example by not walking alone late at night in a city.

In a business environment you would avoid risk by deciding not to start or continue with an activity that poses a risk or by choosing another way to achieve the same result. For example, a landlord has a bad reputation for delaying repairs and maintenance on a building or not undertaking them at all. This could put tenants in danger. You avoid the risk by not accepting a property management listing from this landlord. Likewise, you would not recommend questionable tenants to a landlord. However, if the landlord does take on some questionable tenants, you should make sure you spell it out in writing to the landlord that he or she went against your recommendation.

Controlling the risk

This method of treating a risk is used to decrease the likelihood of the risk occurring and/or limit the consequences of the risk. Methods to reduce the likelihood of risk include:

implementing quality assurance procedures and systems

having induction programs

providing training and ongoing professional development for staff

having adequate supervision and mentoring

having inspection controls and audits

introducing preventative maintenance for equipment.

17319B: 4 Minimising agency risks and complaints 15 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

To reduce the consequences of risk you need to plan for contingencies, minimise exposure to sources of risk, possibly relocate activities and put physical barriers in place.

For example, to avoid lapsed sales and management agreements, you would need a procedure to monitor expiry dates. You would control the risk of badly written contracts and agreements with staff training. Constant monitoring of accounts would control the risk of the misappropriation of funds. The chance of injury to staff and clients would be controlled by using signs to warn of danger or by preventing access to dangerous places.

Transferring the risk

This is a common method. The business moves all or part of the responsibility for the risk to another organisation. Of course, the first organisation that springs to mind is an insurance company. Insuring against risk seems to infiltrate all areas of business and life nowadays, from income insurance to pet insurance.

Another way of moving risk is to contract out activities that the business doesn’t specialise in or that would be too time-consuming to do properly. For example, some small organisations now contract out valuations to businesses that specialise in this type of work, as opposed to having in-house valuation staff do them. The risk of litigation may be too high for these organisations to undertake the work themselves.

Another way to transfer risk, often used in real estate and valuation, is to include an exemption from liability clause in documentation. These disclaimers or waivers state that the agency does not accept responsibility for certain events. However, the legality of these disclaimers is often ambiguous and they do not release an organisation from its duty of care to the person who signs the waiver or protect organisations that act negligently or fail to act when they should have.

Retaining the risk

In reality, it is not possible to have a totally risk-free environment, nor may it be desirable. It may not be possible to avoid, reduce, eliminate or transfer all risks, nor may it be cost effective to do so, therefore some risks will need to be retained.

16 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Who is reponsible?Although the licensee-in-charge is ultimately responsible for everything that happens in the agency, every individual staff member has a responsibility to help avoid risk, both business and personal. Staff members need to be aware of potential or actual hazards in the office and on site and to either act to remove the risk or tell a responsible staff member.

Team and staff meetings are a good place to discuss actual and potential risks and their management. Staff members need to look out for each other, particularly where personal safety is concerned. All staff members need to be aware of emergency procedures and need to know when and how to complete incident reports. Staff attitudes to risk and a team approach to minimising their impact are critical.

17319B: 4 Minimising agency risks and complaints 17 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Documentation in risk management

A risk management system should include written procedures to make it clear what action is needed and how, when and by whom it is to be carried out.

Once you have established the context of your business, identified the sources and types of risks present, analysed and evaluated those risks and considered appropriate methods of treatment, you should document this information in a risk management plan.

The plan sets out the information in a logical format and allocates responsibility for implementing the treatment options and describes resources needed to implement the risk treatment. As with all effective plans, it should also include a timetable for its implementation and an explanation of how the success of the treatment option will be evaluated or measured. One way of documenting a risk management plan is shown in Table 4.

Case study: a risk at Evansdale Realty.Evansdale Realty uses property management software that lists owners and tenants, tracks rents received, records notes about the tenancy and generates monthly and end-of-year financial reports for property owners. Dave and Ellen use the program constantly and enter a lot of data every day.

A back-up system has been installed on the server. Jackie has the task of running the back-up every business day at close of business. It’s one of her regular tasks. All she needs to do is load the appropriate storage medium; the program runs by itself. Neither Dave nor Ellen do this unless Jackie is on leave.

Unfortunately Jackie occasionally doesn’t have time to do this task, because the office gets so busy and, when it’s finishing time, she’s in a hurry to leave and Dave and Ellen have already left the office for the day. This means that the data entered during the day is not backed up.

Let’s complete the risk management plan for this situation. For the source of the risk, look at the categories in Table 1.

18 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Evansdale Realty

Risk Management Plan

Prompts Details

Source of risk How can the risk arise? Technology

Risk Event What can happen? The server could malfunction and all data added since the last back-up would be lost; individual could lose files; files could become corrupted

Likelihood of event occurring

Is this event rare, unlikely, possible, likely or almost certain?

Possible

Consequences of event occurring

Would the consequences of the event be insignificant, minor, moderate, major or catastrophic?

Depends on amount of date lost – ranges from major to moderate– lost data would need to be reconstructed from memory or other records, with implications for accuracy, completeness and the time it would take.

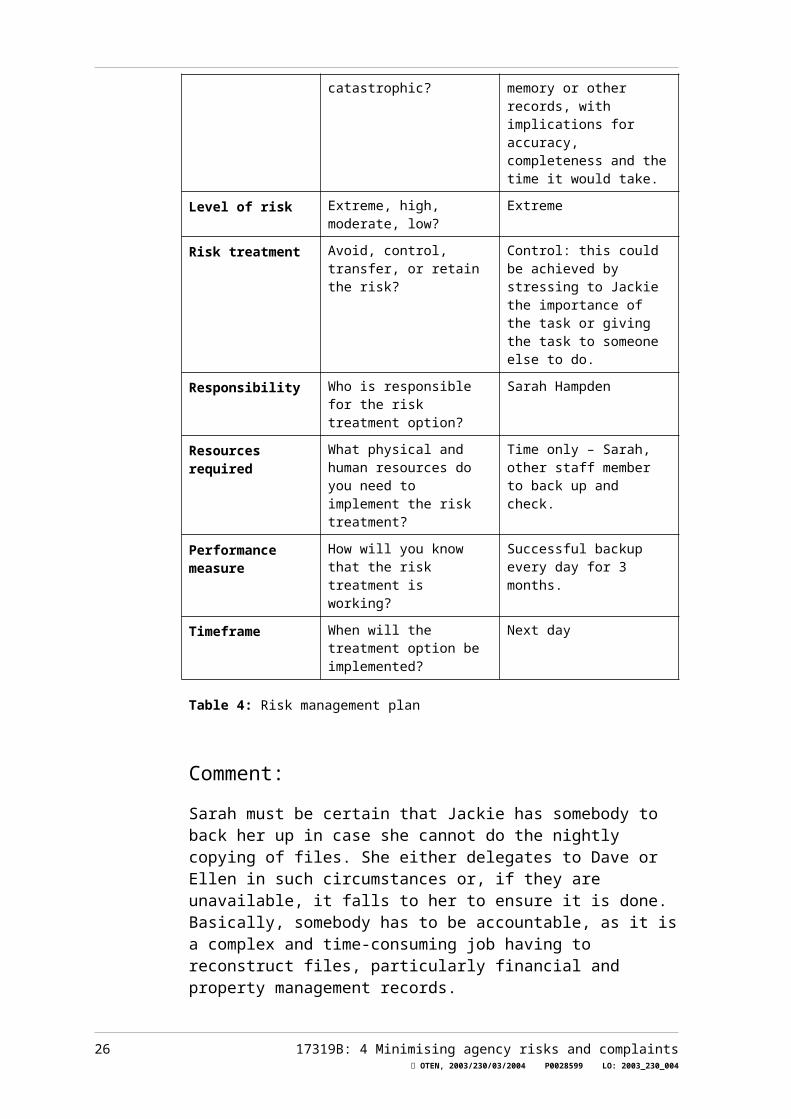

Level of risk Extreme, high, moderate, low? Extreme

Risk treatment Avoid, control, transfer, or retain the risk?

Control: this could be achieved by stressing to Jackie the importance of the task or giving the task to someone else to do.

Responsibility Who is responsible for the risk treatment option?

Sarah Hampden

Resources required

What physical and human resources do you need to implement the risk treatment?

Time only – Sarah, other staff member to back up and check.

Performance measure

How will you know that the risk treatment is working?

Successful backup every day for 3 months.

Timeframe When will the treatment option be implemented?

Next day

Table 4: Risk management plan

17319B: 4 Minimising agency risks and complaints 19 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Comment:

Sarah must be certain that Jackie has somebody to back her up in case she cannot do the nightly copying of files. She either delegates to Dave or Ellen in such circumstances or, if they are unavailable, it falls to her to ensure it is done. Basically, somebody has to be accountable, as it is a complex and time-consuming job having to reconstruct files, particularly financial and property management records.

Activity 3 Completing a risk management plan

The Property Manager has asked Adrian to do a market appraisal at Unit 6 Kensington Gardens for the landlord, who wishes to sell the property when the tenant vacates. Unit 6 is on the first floor. During the inspection Adrian finds that the handrail on the balcony is loose. Adrian realises that this may be a safety problem if it gets any looser.

Complete the following risk management plan then compare your answer with ours (at the end of this topic).

Evansdale Realty

Risk Management Plan

Prompts Details

Source of risk How can the risk arise?

Risk Event What can happen?

Likelihood of event occurring

Is this event rare, unlikely, possible, likely or almost certain?

Consequences of event occurring

Would the consequences of the event be insignificant, minor, moderate, major or catastrophic?

Level of risk Extreme, high, moderate, low?

Risk treatment Avoid, control, transfer, or retain the risk?

Responsibility Who is responsible for the risk treatment option?

Resources required What physical and human resources do you need to implement the risk treatment?

20 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Performance measure

How will you know that the risk treatment is working?

Timeframe When will the treatment option be implemented?

Review and monitoring of risk management plansRegularly reviewing the risk management plan is necessary because risks do not stay the same forever. New risks can emerge and existing risks may change or disappear. Changes will also occur within a business and industry to warrant review of the risk management strategies. Examples of this are changes to stakeholders, changes in priorities, changes in a company’s business focus, or, as we have witnessed recently in the real estate sector, changes in legislation. While we cannot control what the legislation says, we can control how we comply with this legislation.

The process and methods used to identify the original risk can be used to review the plan, for example interviews with stakeholders, accident reports and physical inspections.

Risk Management in real estate practiceThe Office of Fair Trading has identified a range of areas where risk management procedures may be described, including:

Relevant Federal/State/Territory legislation and regulations

Occupational Health and Safety policies, procedures and programs

Professional idemnity insurance requirements

Practice standards

Ethical practices and rules of conduct

Best practice models

Internal agency procedures and complaints management guidelines, including:

- Business and performance plans- Strategic plans- Sales, marketing and leasing/management procedures manuals- Quality assurance and/or procedures manual- Goals, objectives, plans, systems and processes

17319B: 4 Minimising agency risks and complaints 21 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

- Organisational policy/guidelines- Access and equity principles and practice guidelines- Ethical standards- Occupational Health and Safety policies, procedures and programs- Quality and continuous improvement processes and standards.

Benefits of systematic risk management Risk management has many benefits, ranging from protecting people’s safety to assisting the success of businesses by protecting them from legal liability and improving their reputation.

Other benefits of an organised and considered approached to risk management procedures include:

Increased knowledge and understanding of exposure to risk

Creating a best practice and quality organisation

Strengthened culture for continued improvement

Enhanced shareholder value by minimising losses and maximising opportunities

More effective strategic planning

A systematic, well-informed and thorough method of decision making

Better utilisation of resources

Increased preparedness for outside review

Minimised disruptions

Better cost control

Activity 4 Putting it into practice

Answer the question, then compare your answer to ours, in the Feedback to activities section at the end of this topic.

Guy and Samantha are tenants at 11 Somerville Street, Belmore Heights, which is managed by Evansdale Realty. Their four-bedroom property has a swimming pool. The latch on the swimming pool gate does not always lock properly. They have a 3-year-old son who has managed to open the pool gate on a number of occasions. They

22 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

have sent a letter to Evansdale Realty asking for the lock to be fixed. However the landlord is unwilling to pay for a locksmith to do this.

How would you handle this situation?

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

Activity 5 Jackie’s accident

Answer the question, then compare your answer to ours, in the Feedback to activities section at the end of this topic.

Jackie, on one of her first site visits as a salesperson at Evansdale Realty, is taking prospective purchasers to an inspection in the agency’s car. On the way she has a minor accident. Some days later Sarah is chasing up insurance cover for the repairs to the car and can’t find any documentation at all about the accident.

What are the risks in this situation? What does Sarah need to do?

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

17319B: 4 Minimising agency risks and complaints 23 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

______________________________________________________________________

24 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Dealing with complaints

Recent changes to statutory regulations and controls (the Property, Stock and Business Agents Act 2002 and Regulation 2003) have had a significant impact on the property industry in terms of defining the rights and responsibilities of real estate agents, employees and clients. The Act introduced significant cultural changes for all the licensing categories covered by the legislation.

In formulating the new licensing requirements the NSW Office of Fair Trading undertook an extensive survey of all industry sectors to identify the areas in which consumers had the most complaints about agents. The following specific areas are only some of those identified by the survey:

Failure to deposit monies in the trust account

Failure to act fairly and honestly

Security issues

Failure to liase with owners on repairs and maintenance

Lack of knowledge of relevant legislation

Failure to act in the principal’s best interest

Poor customer relations behaviour

Failure to communicate services offered and fees for services

Misrepresentation

Errors in Agency Agreements

Existence of conflict of interest

Failure to liase with tenants about repairs

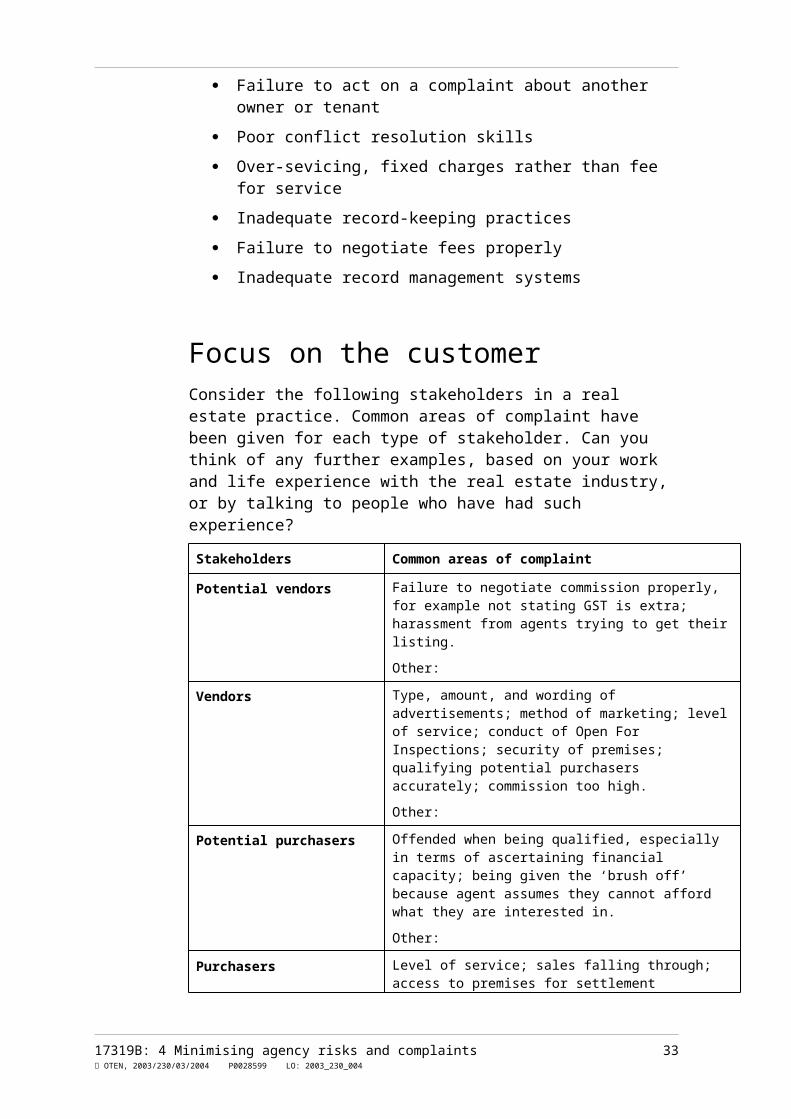

Failure to act on a complaint about another owner or tenant

Poor conflict resolution skills

Over-sevicing, fixed charges rather than fee for service

Inadequate record-keeping practices

Failure to negotiate fees properly

Inadequate record management systems

17319B: 4 Minimising agency risks and complaints 25 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Focus on the customerConsider the following stakeholders in a real estate practice. Common areas of complaint have been given for each type of stakeholder. Can you think of any further examples, based on your work and life experience with the real estate industry, or by talking to people who have had such experience?

Stakeholders Common areas of complaint

Potential vendors Failure to negotiate commission properly, for example not stating GST is extra; harassment from agents trying to get their listing.

Other:

Vendors Type, amount, and wording of advertisements; method of marketing; level of service; conduct of Open For Inspections; security of premises; qualifying potential purchasers accurately; commission too high.

Other:

Potential purchasers Offended when being qualified, especially in terms of ascertaining financial capacity; being given the ‘brush off’ because agent assumes they cannot afford what they are interested in.

Other:

Purchasers Level of service; sales falling through; access to premises for settlement inspection.

Other:

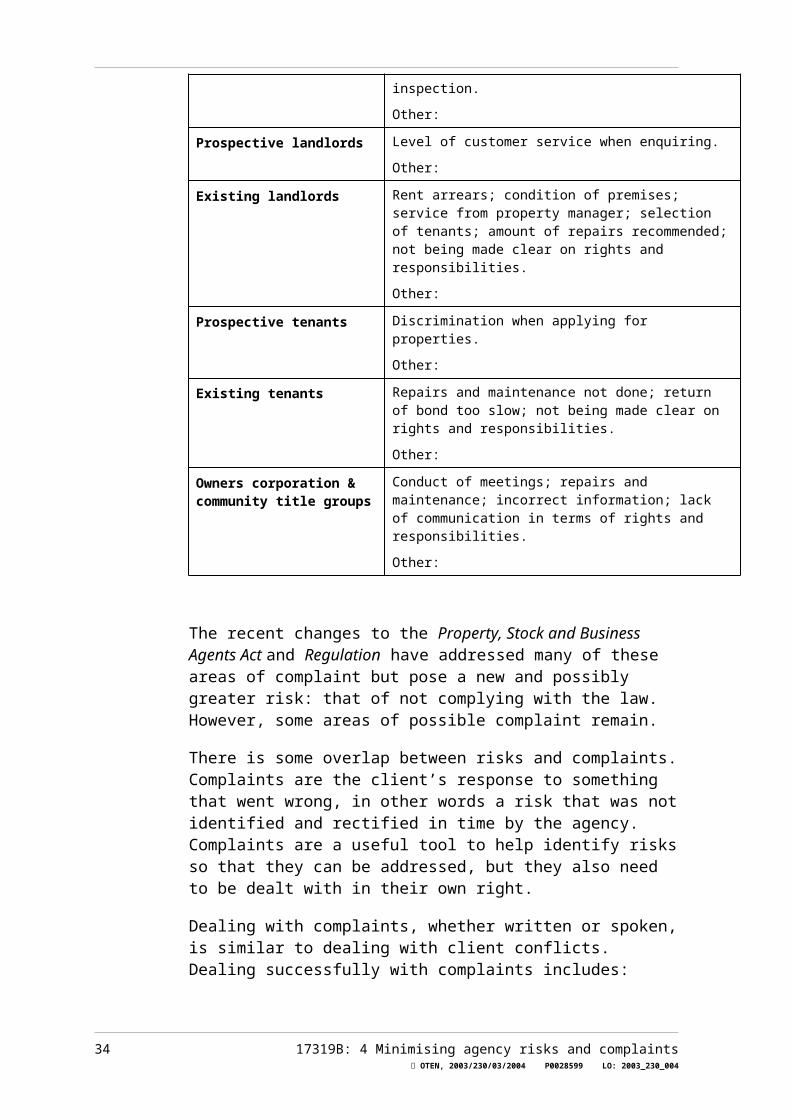

Prospective landlords Level of customer service when enquiring.

Other:

Existing landlords Rent arrears; condition of premises; service from property manager; selection of tenants; amount of repairs recommended; not being made clear on rights and responsibilities.

Other:

Prospective tenants Discrimination when applying for properties.

Other:

Existing tenants Repairs and maintenance not done; return of bond too slow; not being made clear on rights and responsibilities.

Other:

Owners corporation & community title groups

Conduct of meetings; repairs and maintenance; incorrect information; lack of communication in terms of rights and responsibilities.

Other:

26 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

The recent changes to the Property, Stock and Business Agents Act and Regulation have addressed many of these areas of complaint but pose a new and possibly greater risk: that of not complying with the law. However, some areas of possible complaint remain.

There is some overlap between risks and complaints. Complaints are the client’s response to something that went wrong, in other words a risk that was not identified and rectified in time by the agency. Complaints are a useful tool to help identify risks so that they can be addressed, but they also need to be dealt with in their own right.

Dealing with complaints, whether written or spoken, is similar to dealing with client conflicts. Dealing successfully with complaints includes:

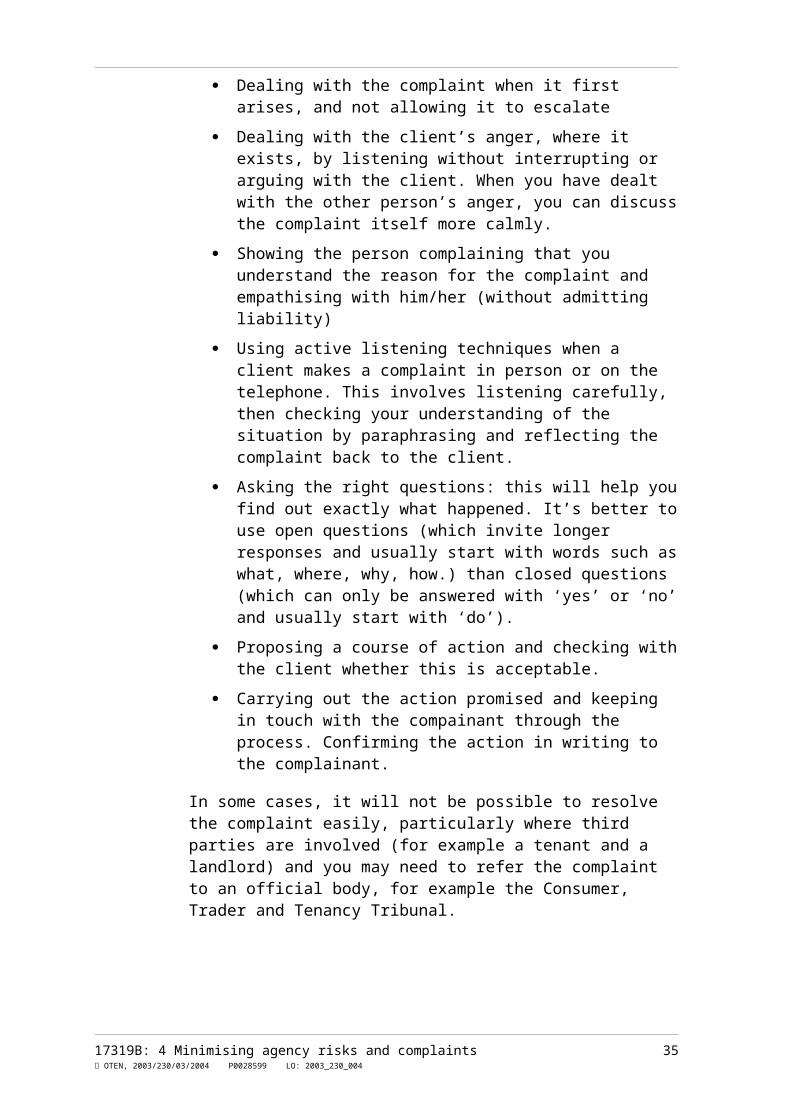

Dealing with the complaint when it first arises, and not allowing it to escalate

Dealing with the client’s anger, where it exists, by listening without interrupting or arguing with the client. When you have dealt with the other person’s anger, you can discuss the complaint itself more calmly.

Showing the person complaining that you understand the reason for the complaint and empathising with him/her (without admitting liability)

Using active listening techniques when a client makes a complaint in person or on the telephone. This involves listening carefully, then checking your understanding of the situation by paraphrasing and reflecting the complaint back to the client.

Asking the right questions: this will help you find out exactly what happened. It’s better to use open questions (which invite longer responses and usually start with words such as what, where, why, how.) than closed questions (which can only be answered with ‘yes’ or ‘no’ and usually start with ‘do’).

Proposing a course of action and checking with the client whether this is acceptable.

Carrying out the action promised and keeping in touch with the compainant through the process. Confirming the action in writing to the complainant.

In some cases, it will not be possible to resolve the complaint easily, particularly where third parties are involved (for example a tenant and a landlord) and you may need to refer the complaint to an official body, for example the Consumer, Trader and Tenancy Tribunal.

17319B: 4 Minimising agency risks and complaints 27 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Reducing the number of complaints usually involves staff training. For example, if clients are complaining that they don’t have enough information about their rights and responsibilities, then training would involve making sure all staff know which publications (for example the Renting Guide) they are legally obliged to give to clients, which ones it is useful to give clients (for example the Agency’s Privacy Policy) and other types of information that they need to give orally.

Activity 6 Handling complaints

How would you deal with the following three complaints? Compare your answers to ours, in the Feedback to activities section at the end of this topic.

a) A vendor is complaining about the advertisements you have placed for his house. He is not happy with the type setting, number of words and the wording.

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

b) Several clients (landlords, vendors, purchasers) complain that they are not getting good service.

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

28 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

(c) A landlord complains that one of his tenants is in arrears and the agency doesn’t seem to be doing anything about it.

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

____________________________________________________________________

17319B: 4 Minimising agency risks and complaints 29 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Feedback to activities

Activity 1 1. This statement is true – which should make you feel more

comfortable about flying!

2. This statement is true – death will occur if you go without sleep for about 10 days, while death by starvation takes a few weeks.

3. This statement is true. It is astonishing that, in a developed country such as Australia, there are over 15 serious injuries and at least one death daily at work, representing an enormous human – and economic – cost.

4. This statement is false. Nationally, the Mining industry leads in the injury stakes, followed by Transport and Storage and Manufacturing, Agriculture, Forestry and Fishing, and then the Construction industry.

5. True. Professionals are the occupation with the highest average cost per occurrence for compensation claims, but labourers and related workers account for the highest proportion of total costs.

Activity 2

Life is in fact a risky business. Below are the events in rank order. We’ve added the chances of the event happening to you in Australia in your lifetime.

Rank Event Chance

1 Having your house burgled 1 in 25

2 Having your car stolen 1 in 142

3 Winning a Trifecta (picking the first three horses in a 13-horse race)

1 in 1716

4 Being kidnapped 1 in 33,223

5 Dying from a venomous bite/sting 1 in 1,159,364

6 Being killed by lightning 1 in 1,603,250

7 Winning Oz Lotto 1 in 8,145,060

8 Winning Powerball 1 in 27,489,577

30 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Activity 3

Evansdale Realty

Risk management plan

Prompts Details

Source of risk How can the risk arise? OH&S

Risk Event What can happen? Current tenant, person attending OFI or future purchaser (child or adult) could lean on the handrail and fall off the balcony. Injuries could be serious.

Likelihood of event occurring

Is this event rare, unlikely, possible, likely or almost certain?

Possible

Consequences of event occurring

Would the consequences of the event be insignificant, minor, moderate, major or catastrophic?

Major to catastrophic

Level of risk Extreme, high, moderate, low? Extreme

Risk treatment Avoid, control, transfer, or retain the risk?

Transferring the risk: notify the owner of the property, recommend that he fix the handrail and warn him of the legal consequences of not doing so. His tenants are already at risk.

Avoiding the risk: if the landlord doesn’t fix the handrail before the first OFI, lock the balcony door during OFIs. Warn the existing tenants not to go onto the balcony.

Responsibility Who is responsible for the risk treatment option?

Adrian or Vince to contact the landlord and confirm in writing.

Resources required

What physical and human resources do you need to implement the risk treatment?

Tradesman to repair handrail if authorised by landlord. Cost payable by landlord.

If not repaired, agent running OFI to ensure balcony door remains locked.

Performance measure

How will you know that the risk treatment is working?

Adrian to inspect handrail or Adrian to check balcony door at OFIs.

Timeframe When will the treatment option be implemented?

As soon as possible, subject to the landlord’s approval and availability of tradesman.

17319B: 4 Minimising agency risks and complaints 31 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Comment

Adrian is well aware of the risk posed by the broken handrail. He needs to make the landlord aware of the risk and the consequences of ignoring the risk.

Activity 4

This example is based on a real situation, although fortunately cases such as this are rare. This situation represents an extreme risk. The three-year-old has managed to open the gate several times so it is likely he will succeed in future. The consequences of his falling into the pool could be catastrophic.

I would write to the landlord again, pointing out that he would be legally liable if the boy drowned in the pool. I would also explain that, if he doesn’t fix the gate immediately, I would be obliged to report him to the Consumer, Trader and Tenancy Tribunal for serious breach of duties and obligations, and that I would end my management of the property immediately. I would need to keep copies of all correspondence since they might be needed in court.

Activity 5

Jackie hasn’t followed agency procedures and OH&S requirements that require her to fill in an incident report form as soon as possible after an incident occurs. If any of the prospective purchasers were injured and made claims against Evansdale Realty, the lack of documentation would also be a problem.

It’s not clear why Jackie didn’t fill in the form. Her induction training should have covered this. Perhaps she forgot, was too busy or was unsure of exactly how to fill it in. Sarah needs to stress again how important it is to complete this documentation and the consequences of not doing so, and take Jackie through the form section by section, showing her how to fill it in.

Activity 6a) Staff training is needed on creating advertisements, making sure the

sales agreement stipulates where and how often the advertisements will appear and explaining to vendors exactly what they will get and give them examples; then confirm in writing. If, in this case, the agency hasn’t done what was agreed, it will need to make amends in some way. If the agency did the right thing but the vendor misunderstood, the agent can only empathise.

b) In this case it is worth questioning these clients about the specifics of their expectations and the reality. Staff training and/or counselling or mentoring will be needed, since client expectations must be met or exceeded. Clients who are unhappy with an agency’s service will go elsewhere and will tell others about their bad experiences. The agent may need to make amends.

32 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

c) The property officer should follow to the letter the procedures for tenants who are in arrears. If this is not happening, for example the property officer feels sorry for the tenant, counselling/mentoring is needed to reinforce that the agency’s client is the landlord, not the tenant. Copies of all correspondence should be available to the landlord. If the tenant remains in breach of his/her tenancy agreement, the matter has to be referred to the Consumer, Trader and Tenancy Tribunal unless the landlord says not to and confirms this in writing to the agent.

17319B: 4 Minimising agency risks and complaints 33 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Summary

The skills you have learnt in this topic should help you identify workplace and business risks and recognise your responsibility in dealing with them.

Check your progress

Here is a check-list of the things you should now know or be able to do. Put a tick beside each one you feel confident about.

I can …

… describe what risk is

… identify different types of risk in the property industry and who is affected

… explain what an agent’s ‘duty of care’ involves

… analyse risks: how likely and how serious they are

… describe four ways to deal with risks

… document risks and their management in the property industry

… describe the benefits of risk management to an organisation

… describe and deal with common complaints in the property industry

How did you go? If there are some areas you’re not sure of, you may like to revise them before attempting your assessment tasks.

Appendix 1: ReferencesThe Office of Fair Trading website:

http://www.fairtrading.nsw.gov.au/

(Use the site search engine to find the Act and Regulation.)

For information about continuing professional development:

http://www.fairtrading.nsw.gov.au/pdfs/realestaterenting/guidelinesforcpd04.pdf

The Consumer, Trader and Tenancy Tribunal

http://www.fairtrading.nsw.gov.au/secondarymenus/cttt.html

The Australian www.accc.gov.au

34 17319B: 4 Minimising agency risks and complaints OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004

Competition and Consumer Commission

(You can read the Trade Practices Act here, or use the site search engine to find Fair and Square, relating specifically to the Real Estate Industry)

Land and Property Information Office

http://lpi-online.lpi.nsw.gov.au/

Australasian Legal Information Network

http://www.austlii.edu.au/

(another site where you can view the PSBA Act and Regulation and related legal matters, as well as the Trade Practices Act)

For the Act: Click on NSW Consolidated Acts, go to ‘P’ and scroll to find the Property Stock and Business Agents Act , 2002.

For the Regulation:

Click on NSW Consolidated Regulations, go to ‘P’ and Scroll down to Property Stock and Business Agents Regulation, 2003.

Office of Federal Privacy Commissioner

http://www.privacy.gov.au

NSW Anti-discrimination Board

http://www.lawlink.nsw.gov.au/adb.nsf/pages/fairgoindex

Administrative Decisions Tribunal

http://www.lawlink.nsw.gov.au/adt.nsf/pages/index

(The board makes decisions in cases of discrimination by NSW Government departments)

Real Estate Institute (REI) of Australia

http://www.reiaustralia.com.au

REI – Victoria http://www.reiv.com.au

REI – NSW http://www.reinsw.com.au

REI—Queensland www.reiq.com.au

REI—Tasmania www.reitas.com

REI – South Australia www.reisa.com.au

REI—WA www.reiwa.com.au

Real Estate Employers Federation

www.reef.org.au

(for information about employment conditions, contracts etc)

Standards Australia www.standards.com.au

17319B: 4 Minimising agency risks and complaints 35 OTEN, 2003/230/03/2004 P0028599 LO: 2003_230_004