Embed Size (px)

Citation preview

UU NN II VV EE RR SS II TT YY OO FF MM II SS KK OO LL CC F A C U L T Y O F E C O N O M I C S

ZZOOLLTTÁÁNN MMUUSSIINNSSZZKKII

TTHHEE IINNVVEENNTTOORRYY VVAALLUUEE BBAASSEEDD PPRROOCCEESSSS OORRIIEENNTTEEDD CCOOSSTTIINNGG OOFF AAGGRRIICCUULLTTUURRAALL PPRROODDUUCCEESS PPHH..DD.. TTHHEESSIISS

MISKOLC 2009

UU NN II VV EE RR SS II TT YY OO FF MM II SS KK OO LL CC F A C U L T Y O F E C O N O M I C S

ZZOOLLTTÁÁNN MMUUSSIINNSSZZKKII

TTHHEE IINNVVEENNTTOORRYY VVAALLUUEE BBAASSEEDD PPRROOCCEESSSS OORRIIEENNTTEEDD CCOOSSTTIINNGG OOFF AAGGRRIICCUULLTTUURRAALL PPRROODDUUCCEESS

PP HH .. DD .. TT HH EE SS II SS NAME OF DOCTORAL SCHOOL: VÁLLALKOZÁSELMÉLET- ÉS GYAKORLAT

DOKTORI ISKOLA HEAD OF DOCTORAL SCHOOL: DR. SZINTAY, ISTVÁN professor CSc ACADEMIC TUTOR: DR. GÁL, JOLÁN professor CSc

MISKOLC 2009

2

CCOONNTTEENNTTSS

1. The Objective of Study, Structure of Thesis ....................................................................................... 3 2. The Method of Research ................................................................................................................................... 6 3. Findings of the Research .................................................................................................................................. 8 4. Applying the Findings ...................................................................................................................................... 22 Bibliography ................................................................................................................................................................. 24 Publications of the Author on the Topic ................................................................................................. 26

3

11.. TTHHEE OOBBJJEECCTTIIVVEE OOFF SSTTUUDDYY,, SSTTRRUUCCTTUURREE OOFF TTHHEESSIISS In the early years of the development of accounting the main aim was to record credits and debts. The usefulness of accounting was only recognised by company managers by the increasing company sizes and complexity of processes. At the dawn of the nineteenth century cost accounting focused solely on the average costs of the product. The followers of Frederich Taylor and his engineers' man‐agement doctrines took into consideration first, the possibility of allocating over‐head costs to products. The goal of responsibility based accounting that was de‐veloped at the beginning of the twentieth century, was controlling the perform‐ance of highly independent organisational units. Johnson and Kaplan published in their paper, Relevance Lost: The Rise and Fall of Management Accounting, that although costing systems were developed in the nineteenth century and the early years of the twentieth century, they didn't change since the 20's and 30's, they couldn't keep pace with the changes of business environments (Johnson‐Kaplan, 1987). Since the middle of the 70's due to the global competition and technology innovations the changes in business resulted in outstanding results in using fi‐nancial and nonfinancial information of organisations (Kaplan‐Cooper, 2001, page 15). As a respond to the new expectations process costing1 emerged. The possibility of using this new tool for respond to the challenges of the new era for agricultural activities appeared in national and international studies as well. Studying the theories, the issue of their usability came up, taking into considera‐tion the Hungarian legal environment, the elaborated practices of production and accounting of agricultural companies, as well as their procedures.

1 During costing – meaning activities and methods also − the resource using of the organisations is measured and assessed. Process oriented costing methods are based on those of activity based costing as well as process based costing.

4

I outlined my research objective as to elaborate a process oriented costing system that is: − based on the accounting practises and the expectations of Hungarian agri‐cultural companies, − using up‐to‐date data, − can be used for defining inventory values of agricultural produces. In the first part of the study I outline the establishing and development of costing systems (chapter 1), then the basic definitions of those systems (chapter 3). I go into the details of the classic, as well as the controlling based approaches of agri‐cultural process costing (chapter 2), and the costing of biological assets and agri‐cultural products (chapter 4). I accept that definition of costs, which states that cost is the value of resources used for activities, however, I would like to draw attention to the limits of the un‐derstanding of this definition. I consider prime cost to be the cost of a calculation unit (usually a product). By categorising prime cost I differentiate between direct, limited and full prime costs. For the common understanding of definition, I state limited and prime costs (defined by the accounting regulations) to be inter‐changeable phrases. In the second part of the study I publish my findings. In chapter 5 I summarise the methods of the research itself, and then in chapter 6 the results of the questionnaire related to the cost accounting practices of agricul‐tural companies. I consider an agricultural entity to be an incorporated, ltd or a cooperative farm, which is pursuing agricultural activities and completes its ac‐tions under the accounting act. I define a company as pursuing agricultural activi‐ties if its revenues from agricultural activities are higher than the 50% of the revenues corrected with the purchase value of sold goods and value of sold (me‐diated) services. In the questionnaire I worded questions regarding the allocation of agricultural activity related costs, the practices of prime costing of biological assets and agricultural produces, the evaluation of costing and prime costing, as

5

well as their technical background. When elaborating the inventory value based process oriented costing theory I amalgamated the results of previous studies as well into my questionnaire. Through theory building I try to adapt other universal process oriented costing procedures, and reconsider the techniques developed for agricultural activities. The framework of this reconsidering is provided by the part in the questionnaire where I are looking for the answers for the following questions: − how important the agricultural companies consider the factors affecting the operation of their costing and prime costing systems to be, − how they evaluate their current costing and prime costing systems, − on which areas of their current costing and prime costing systems they plan changes. The main elements of the basic model elaborated for plant produces are the cost centres, processes and units. The model, suitable for the expectations and needs of agricultural companies, is limited in complexity. It means that I pinpoint its prime usage area for calculating process costs and inventory values of produces. In chapter 8 I test the practical usability of the inventory value based process cost‐ing model, elaborated for plan producing, through a case study. I would like to highlight besides comparing the current costing system and the process costing system of a certain company that the current account records of agricultural com‐panies are able to satisfy the information needs of process costing without breach‐ing accounting regulations.

6

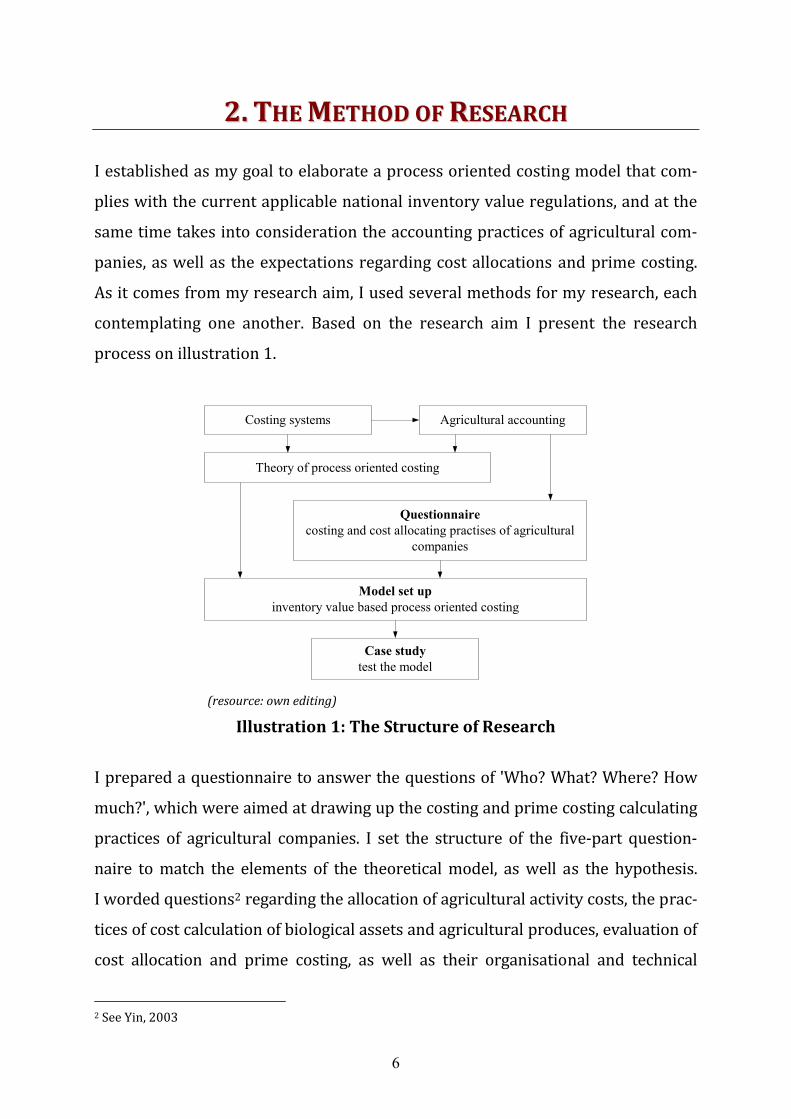

22.. TTHHEE MMEETTHHOODD OOFF RREESSEEAARRCCHH I established as my goal to elaborate a process oriented costing model that com‐plies with the current applicable national inventory value regulations, and at the same time takes into consideration the accounting practices of agricultural com‐panies, as well as the expectations regarding cost allocations and prime costing. As it comes from my research aim, I used several methods for my research, each contemplating one another. Based on the research aim I present the research process on illustration 1. Costing systems Agricultural accounting

Theory of process oriented costing

Questionnairecosting and cost allocating practises of agricultural

companies

Model set upinventory value based process oriented costing

Case studytest the model

(resource: own editing)

Illustration 1: The Structure of Research I prepared a questionnaire to answer the questions of 'Who? What? Where? How much?', which were aimed at drawing up the costing and prime costing calculating practices of agricultural companies. I set the structure of the five‐part question‐naire to match the elements of the theoretical model, as well as the hypothesis. I worded questions2 regarding the allocation of agricultural activity costs, the prac‐tices of cost calculation of biological assets and agricultural produces, evaluation of cost allocation and prime costing, as well as their organisational and technical 2 See Yin, 2003

7

background. The completion of the questionnaire took place in February and March

2008. I posted the questionnaire to 150 companies and I got it back filled in from 74. The returned forms I considered to be useful – complying with the current regula‐tions – if the company is an incorporated, ltd or a cooperative farm pursuing its ac‐tivity under the accounting act. 66 forms were chosen as fully completed. I used SPSS 14.0 statistical software and Microsoft Excel for processing and evaluating the data from the questionnaire, and for preparing the charts as well. I used the method defined by Babbie (Babbie, 2003) for setting up the inventory value based process oriented costing model. I defined the topic, the area, identified and defined the main definitions, collected the connections between variables and drew my conclusions. The studies of Kaplan and Cooper made a significant effect on my theoretical approach. Taking into consideration the results of the previous studies focusing on the agricultural usage of process oriented costing3, when I pre‐pared my model I took the method elaborated by Körmendi and Tóth (Körmendi‐Tóth, 2002) as the basic step. I tested the usability of the basic model of inventory value based process oriented costing for field production through a case study. The object of the case study was an incorporated located in Borsod‐Ababúj‐Zemplén County. When choosing the company I set as a criteria that the company has to be involved in several areas of agricultural activity, and that the main elements of its costing and unit costing sys‐tems have to reflect the practices of the – from accounting point of view − most im‐portant Hungarian agricultural companies. The constructive approach of the com‐pany was an important issue, since it ensured that I could process its accounting database as thoroughly as even to check invoices for the sake of case study.

3 See: Véry, 1999, Farm Financial Standards Councit, 2006

8

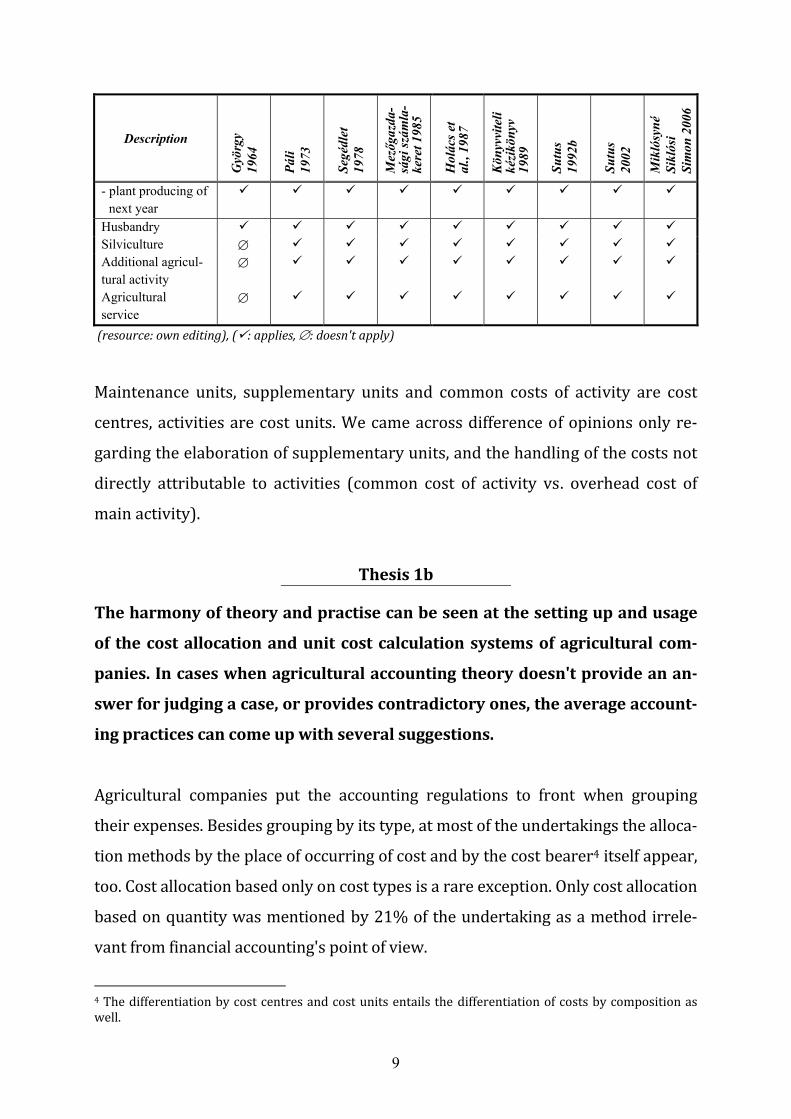

33.. FFIINNDDIINNGGSS OOFF TTHHEE RREESSEEAARRCCHH Books and studies dealing with agricultural accounting present the special costing needs of agricultural activities only through the establishing of cost centres and cost units, they don't suggest the allocation of costs by cost types. Thesis 1a

The literature of agricultural cost accounting presents the definition of the

cost centres and cost units, the contents of the accounts, the procedures and

methods for cost allocation and unit cost allocation without any significant

change for decades now. In the era of accounting legislation in existence, they

still build upon procedures and methods set up for state farms and farmers'

cooperative farms. In the below spreadsheet I summarised the suggestions and regulations regard‐ing the setting up of cost centres and cost units issued in the past four decades. Spreadsheet 1: Agricultural Cost Centres and Cost Units

Description

Gyö

rgy

1964

Páli

1973

Segé

dlet

19

78

Mezőg

azda

-sá

gi sz

ámla

-ke

ret 1

985

Hol

ács e

t al

., 19

87

Köny

vvite

li ké

zikön

yv

1989

Sutu

s 19

92b

Sutu

s 20

02

Mik

lósy

né

Sikl

ósi

Sim

on 2

006

Maintenance unit Supplementary unit - tractor unit - lorry unit - combine unit - irrigation unit ∅ - live stock ∅ - drying unit ∅ ∅ ∅ - heavy machinery ∅ ∅ ∅ ∅ Common cost of activities

∅ ∅ ∅

Overhead cost of main activity

∅

Plant producing - plant producing of

current year

9

Description

Gyö

rgy

1964

Páli

1973

Segé

dlet

19

78

Mezőg

azda

-sá

gi sz

ámla

-ke

ret 1

985

Hol

ács e

t al

., 19

87

Köny

vvite

li ké

zikön

yv

1989

Sutu

s 19

92b

Sutu

s 20

02

Mik

lósy

né

Sikl

ósi

Sim

on 2

006

- plant producing of next year

Husbandry Silviculture ∅ Additional agricul-tural activity

∅

Agricultural service

∅

(resource: own editing), ( : applies, ∅: doesn't apply) Maintenance units, supplementary units and common costs of activity are cost centres, activities are cost units. We came across difference of opinions only re‐garding the elaboration of supplementary units, and the handling of the costs not directly attributable to activities (common cost of activity vs. overhead cost of main activity). Thesis 1b

The harmony of theory and practise can be seen at the setting up and usage

of the cost allocation and unit cost calculation systems of agricultural com-

panies. In cases when agricultural accounting theory doesn't provide an an-

swer for judging a case, or provides contradictory ones, the average account-

ing practices can come up with several suggestions. Agricultural companies put the accounting regulations to front when grouping their expenses. Besides grouping by its type, at most of the undertakings the alloca‐tion methods by the place of occurring of cost and by the cost bearer4 itself appear, too. Cost allocation based only on cost types is a rare exception. Only cost allocation based on quantity was mentioned by 21% of the undertaking as a method irrele‐vant from financial accounting's point of view. 4 The differentiation by cost centres and cost units entails the differentiation of costs by composition as well.

10

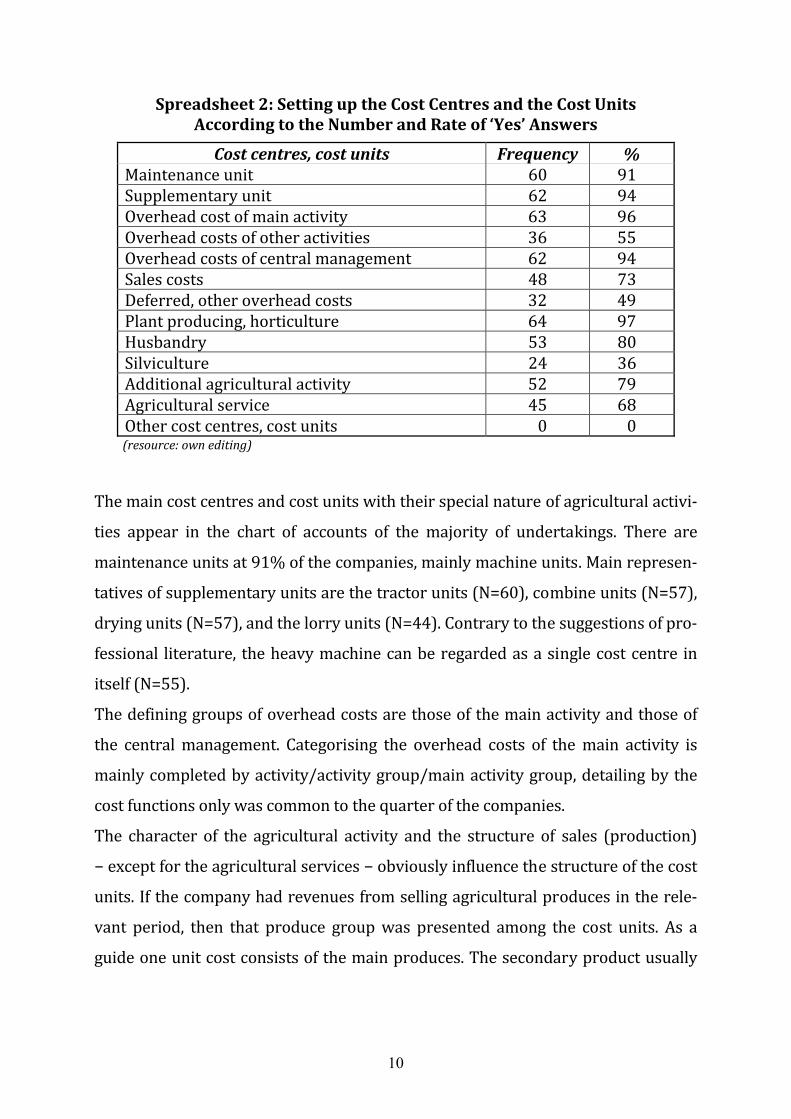

Spreadsheet 2: Setting up the Cost Centres and the Cost Units According to the Number and Rate of ‘Yes’ Answers

Cost centres, cost units Frequency % Maintenance unit 60 91 Supplementary unit 62 94 Overhead cost of main activity 63 96 Overhead costs of other activities 36 55 Overhead costs of central management 62 94 Sales costs 48 73 Deferred, other overhead costs 32 49 Plant producing, horticulture 64 97 Husbandry 53 80 Silviculture 24 36 Additional agricultural activity 52 79 Agricultural service 45 68 Other cost centres, cost units 0 0 (resource: own editing) The main cost centres and cost units with their special nature of agricultural activi‐ties appear in the chart of accounts of the majority of undertakings. There are maintenance units at 91% of the companies, mainly machine units. Main represen‐tatives of supplementary units are the tractor units (N=60), combine units (N=57), drying units (N=57), and the lorry units (N=44). Contrary to the suggestions of pro‐fessional literature, the heavy machine can be regarded as a single cost centre in itself (N=55). The defining groups of overhead costs are those of the main activity and those of the central management. Categorising the overhead costs of the main activity is mainly completed by activity/activity group/main activity group, detailing by the cost functions only was common to the quarter of the companies. The character of the agricultural activity and the structure of sales (production) − except for the agricultural services − obviously influence the structure of the cost units. If the company had revenues from selling agricultural produces in the rele‐vant period, then that produce group was presented among the cost units. As a guide one unit cost consists of the main produces. The secondary product usually

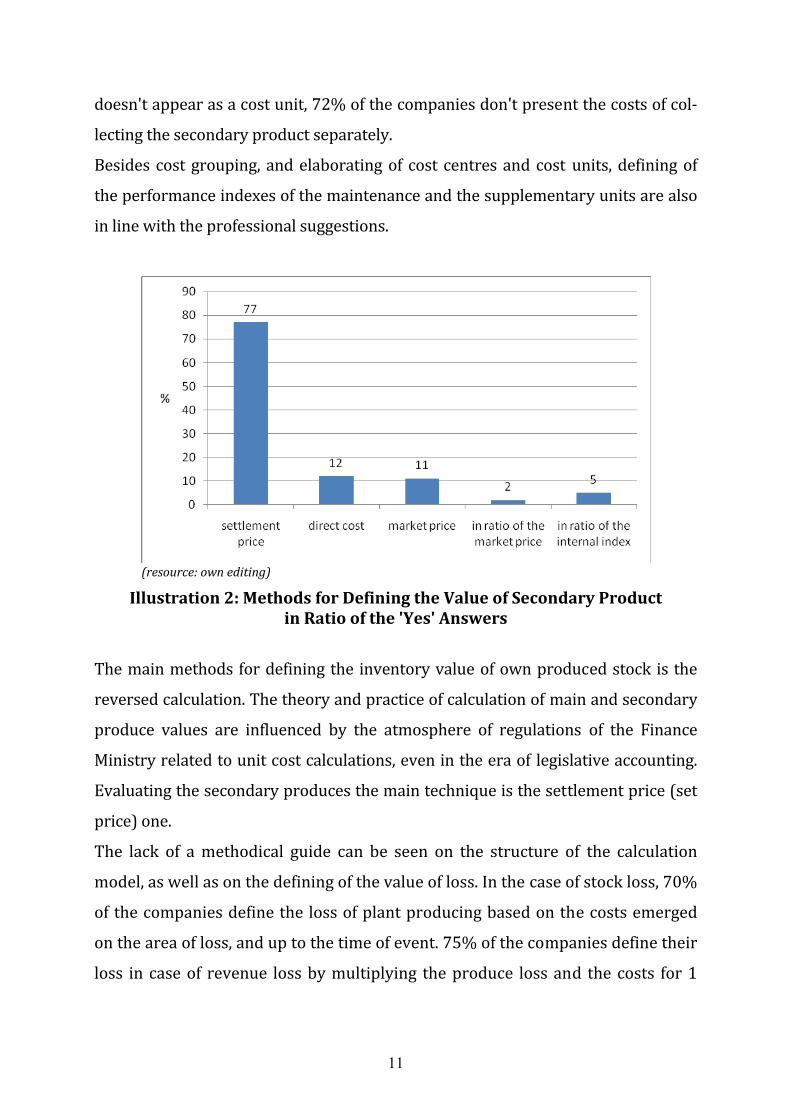

11

doesn't appear as a cost unit, 72% of the companies don't present the costs of col‐lecting the secondary product separately. Besides cost grouping, and elaborating of cost centres and cost units, defining of the performance indexes of the maintenance and the supplementary units are also in line with the professional suggestions.

(resource: own editing)

Illustration 2: Methods for Defining the Value of Secondary Product in Ratio of the 'Yes' Answers The main methods for defining the inventory value of own produced stock is the reversed calculation. The theory and practice of calculation of main and secondary produce values are influenced by the atmosphere of regulations of the Finance Ministry related to unit cost calculations, even in the era of legislative accounting. Evaluating the secondary produces the main technique is the settlement price (set price) one. The lack of a methodical guide can be seen on the structure of the calculation model, as well as on the defining of the value of loss. In the case of stock loss, 70% of the companies define the loss of plant producing based on the costs emerged on the area of loss, and up to the time of event. 75% of the companies define their loss in case of revenue loss by multiplying the produce loss and the costs for 1

12

unit of produce (the amount of the actual produce and the loss defined in the minutes about loss) emerged up till the time of damage. The calculation of living weight unit cost mirrors the theory too for agricultural companies. If the approach of professional literature for defining living weight is unanimous, that entails that the practices of the companies will be too. 96% of the companies using living weight cost unit calculation derive their opening balance from the closing balance of the previous year, which is by equalling the closing and opening balance. 98% of the companies define the values of living stock by their actual inventory cost, their ageing by the cost unit of the age group, and the value of stock and weight increasing by taking the direct costs into consideration. As the cost unit of living stock weight, 98% of the companies define it as the ratio of the value of living weight and its quantity. The lack of common guideline can be seen at defining the value of the porker, as in this case the ratio of the ’yes’ an‐swers was only 64% compared to the usual 96‐98% averages. Kaplan and Cooper (Kaplan‐Cooper, 2001) distinguish four levels of costing sys‐tems. According to their opinion most of the companies have second level systems, which revolve around financial reports. Second level systems attribute costs to cost centres, not to activities or processes, they only allocate cost of production to the produces based on direct work and material cost of the machines hours. Data pro‐vided by second level systems are not proper, not actual and they can only be used for management information in a limited way. Thesis 2

The cost allocation and unit costing practices of Hungarian agricultural com-

panies are identical to the features of the second level cost systems in many

details.

13

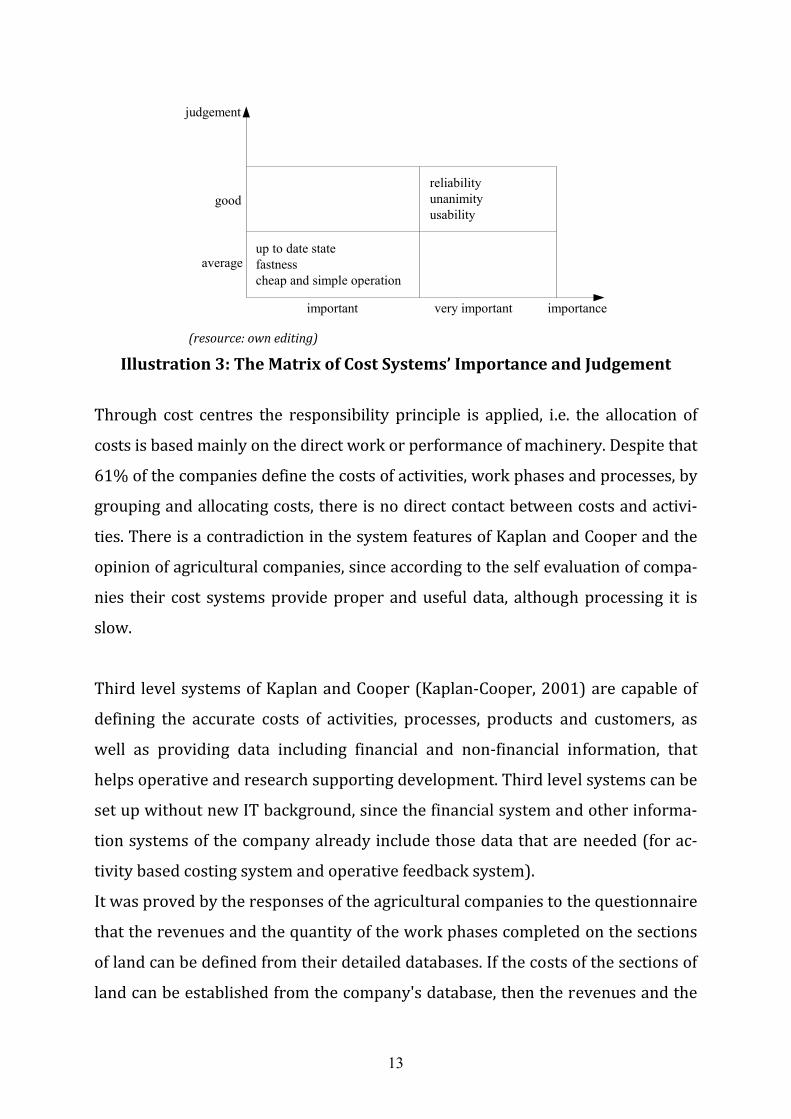

judgement

good

average

important very important importance

reliabilityunanimityusability

up to date statefastnesscheap and simple operation

(resource: own editing)

Illustration 3: The Matrix of Cost Systems’ Importance and Judgement Through cost centres the responsibility principle is applied, i.e. the allocation of costs is based mainly on the direct work or performance of machinery. Despite that 61% of the companies define the costs of activities, work phases and processes, by grouping and allocating costs, there is no direct contact between costs and activi‐ties. There is a contradiction in the system features of Kaplan and Cooper and the opinion of agricultural companies, since according to the self evaluation of compa‐nies their cost systems provide proper and useful data, although processing it is slow. Third level systems of Kaplan and Cooper (Kaplan‐Cooper, 2001) are capable of defining the accurate costs of activities, processes, products and customers, as well as providing data including financial and non‐financial information, that helps operative and research supporting development. Third level systems can be set up without new IT background, since the financial system and other informa‐tion systems of the company already include those data that are needed (for ac‐tivity based costing system and operative feedback system). It was proved by the responses of the agricultural companies to the questionnaire that the revenues and the quantity of the work phases completed on the sections of land can be defined from their detailed databases. If the costs of the sections of land can be established from the company's database, then the revenues and the

14

quantity of the work phases completed on the sections of land can be established as well. The majority of companies have detailed databases on the costs and per‐formance of heavy machinery. Companies recording the performance of their heavy machinery will more than likely have a detailed database about the costs of machinery, the work phases completed and the revenues from the sections of land as well. Recording the time demand of work phases is not significant among the companies. Thesis 3

Agricultural companies using their current detailed databases can determine

without significant extra costs by process costing the direct unit costs – in

line with the stipulations for inventory value by accounting act – of agricul-

tural produces. Limited unit cost is the amount of direct unit cost and the operating costs – in our case this latter is the overhead cost of the main activity – per one product. I treat direct unit costs and limited unit costs – defined by the accounting act – as syno‐nyms. Process oriented approach used for detailing main activities' overhead costs can be used for defining limited unit costs as well. The overhead costs of main activities are categorised by the majority of the companies by activity/activity groups/main activity groups. This differentiation makes it difficult to connect the overhead cost of the main activity and the process. Work and time demanding data collection is not in line with the companies' expectations. Process oriented approach needs the categorising of overhead cost of main activity by cost functions. In this case a part of the overhead cost of main activity can be allocated to the processes without any major extra workload needed. However, categorising by cost functions is only used by 40% of the agricultural companies.

15

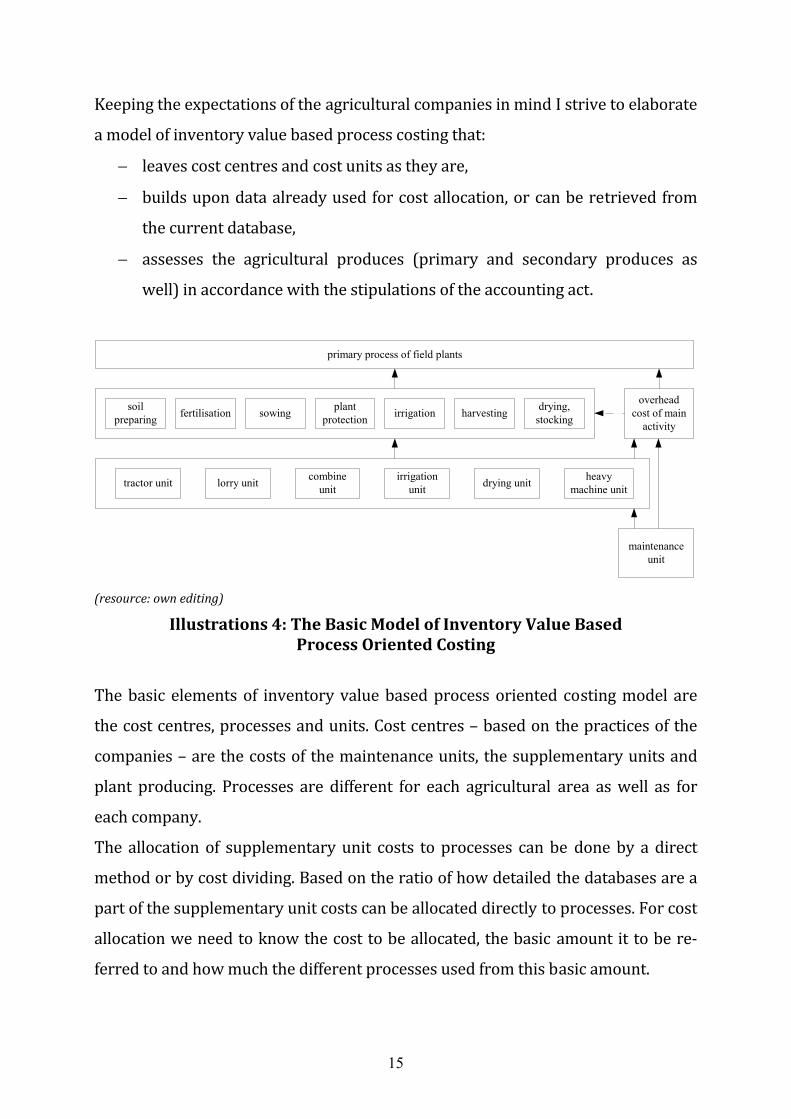

Keeping the expectations of the agricultural companies in mind I strive to elaborate a model of inventory value based process costing that: − leaves cost centres and cost units as they are, − builds upon data already used for cost allocation, or can be retrieved from the current database, − assesses the agricultural produces (primary and secondary produces as well) in accordance with the stipulations of the accounting act.

primary process of field plants

soilpreparing fertilisation sowing plant

protection irrigation harvesting drying,stocking

overheadcost of main

activity

tractor unit lorry unit combineunit

irrigationunit drying unit heavy

machine unit

maintenanceunit

(resource: own editing)

Illustrations 4: The Basic Model of Inventory Value Based Process Oriented Costing The basic elements of inventory value based process oriented costing model are the cost centres, processes and units. Cost centres – based on the practices of the companies – are the costs of the maintenance units, the supplementary units and plant producing. Processes are different for each agricultural area as well as for each company. The allocation of supplementary unit costs to processes can be done by a direct method or by cost dividing. Based on the ratio of how detailed the databases are a part of the supplementary unit costs can be allocated directly to processes. For cost allocation we need to know the cost to be allocated, the basic amount it to be re‐ferred to and how much the different processes used from this basic amount.

16

I don't mean to define an 'ideal' base for allocating the process costs. Considering the complexity of the processes and the different practices of cost allocation and unit costing of companies, I only submit suggestions. The cost of the processes (phases) can be allocated to cost units by the amount of work phases completed, based on the company databases. The work completed can be measured of course, but the same base can be used for its calculation as for dividing the current relevant supplementary unit costs. In case of processes consist of similar process phases advisable to allocate the costs not by process phases but by calculation units using the process phases. The timing of the work phases could be well used too, but recording the time needs of the work phases is not typical of the Hungarian agricultural companies. Thesis 4a

The inventory value based process oriented costing can be used not only for

allocating supplementary unit costs, but for assessment secondary products

and natural losses as well. With the help of a different approach to cost units, the assessment of the secondary products and the natural losses as well can be completed. Consider the cost unit to be not just the reaped main product, but the unharvested main product and the secondary product too! The loss recorded due to damage is the amount of the direct costs up to the event of damage, either in full or pro rata the reaped product value. In my opinion the principles of cost reference and reliability is applied to the most if I define the loss value by the costs allotted to the section of land. Since in this case we have losses regarding unharvested crop, thus the reaping, drying and storing process is not applicable.

17

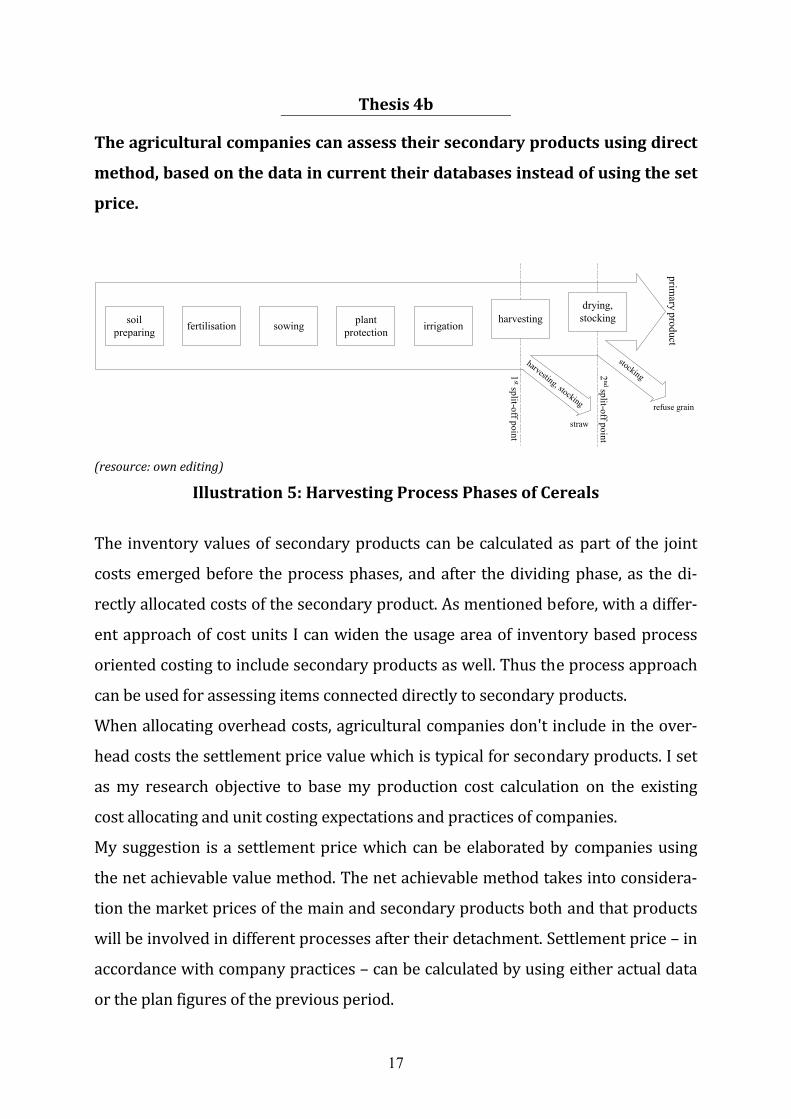

Thesis 4b

The agricultural companies can assess their secondary products using direct

method, based on the data in current their databases instead of using the set

price. soil

preparingharvesting

irrigationplantprotectionsowingfertilisation

drying,stocking

1st split-off point

primary product

harvesting, stocking

stocking

straw

refuse grain

2nd split-off point

(resource: own editing)

Illustration 5: Harvesting Process Phases of Cereals The inventory values of secondary products can be calculated as part of the joint costs emerged before the process phases, and after the dividing phase, as the di‐rectly allocated costs of the secondary product. As mentioned before, with a differ‐ent approach of cost units I can widen the usage area of inventory based process oriented costing to include secondary products as well. Thus the process approach can be used for assessing items connected directly to secondary products. When allocating overhead costs, agricultural companies don't include in the over‐head costs the settlement price value which is typical for secondary products. I set as my research objective to base my production cost calculation on the existing cost allocating and unit costing expectations and practices of companies. My suggestion is a settlement price which can be elaborated by companies using the net achievable value method. The net achievable method takes into considera‐tion the market prices of the main and secondary products both and that products will be involved in different processes after their detachment. Settlement price – in accordance with company practices – can be calculated by using either actual data or the plan figures of the previous period.

18

The machinery‐heavy machinery differentiation is not the same kind as the differ‐entiation of tractor‐machinery worked out when setting up cost centres. 61% of the companies record the costs of machinery and the lorries' on the same line as the costs of tractors. If we allocate the tractor operation costs without any correc‐tion, we will have a contradiction to deal with. Thesis 5

By correcting ledger accounts we can eliminate the contradiction in calculat-

ing unit costs of agricultural produces by inventory value based process ori-

ented costing. The costs of heavy machinery, trailers and tows we handle together on the level of ledger accounts, however when reallocating the costs we have to differentiate between them. If we categorise the cost of tractor units into at least two groups – group of prime movers and group of trailers and tows – then the allocation will produce a value with no contradictions regarding the relationship of the cost elements and the process. The part of the model so far presented can be used for calculating the costs of supplementary units; however, the objective is calculating the cost of processes. For this purpose we suggested the following two‐dimension scheme, instead of the one‐dimension scheme used by professional literature:

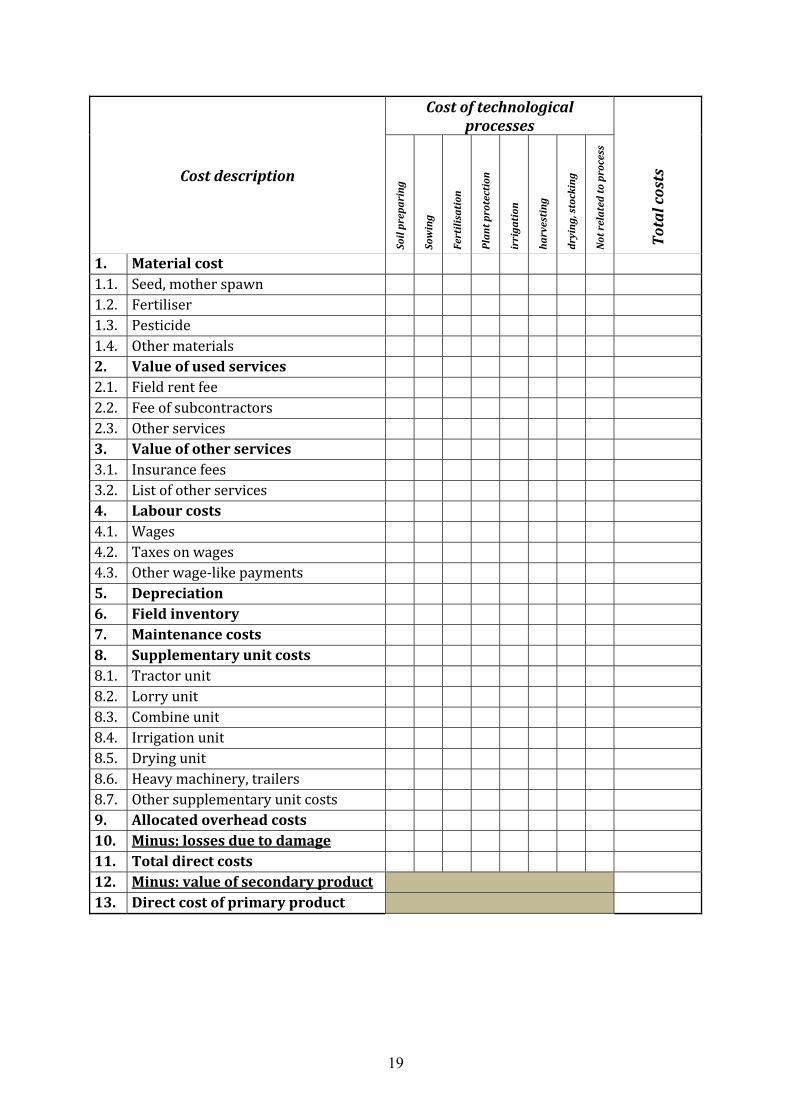

19

Cost description

Cost of technological processes

Tot

al c

osts

Soil

pre

pari

ng

Sow

ing

Fert

ilis

atio

n

Pla

nt p

rote

ctio

n

irri

gati

on

harv

esti

ng

dryi

ng,

sto

ckin

g

Not

rel

ated

to

proc

ess

1. Material cost 1.1. Seed, mother spawn 1.2. Fertiliser 1.3. Pesticide 1.4. Other materials 2. Value of used services 2.1. Field rent fee 2.2. Fee of subcontractors 2.3. Other services 3. Value of other services 3.1. Insurance fees 3.2. List of other services 4. Labour costs 4.1. Wages 4.2. Taxes on wages 4.3. Other wage‐like payments 5. Depreciation 6. Field inventory 7. Maintenance costs 8. Supplementary unit costs 8.1. Tractor unit 8.2. Lorry unit 8.3. Combine unit 8.4. Irrigation unit 8.5. Drying unit 8.6. Heavy machinery, trailers 8.7. Other supplementary unit costs 9. Allocated overhead costs 10. Minus: losses due to damage 11. Total direct costs 12. Minus: value of secondary product 13. Direct cost of primary product

20

In the columns the processes of the basic model are presented, as well as the items not allocated to any process. When elaborating the lines, I took into consideration the one‐dimension schemes presented in chapter 4, and the average scheme used in practice by agricultural companies. In detailing the lines I mirrored the cost centres of the basic model, and the data structure of the Agricultural Research Institution for cost systems5 and unit costs. Thesis 6

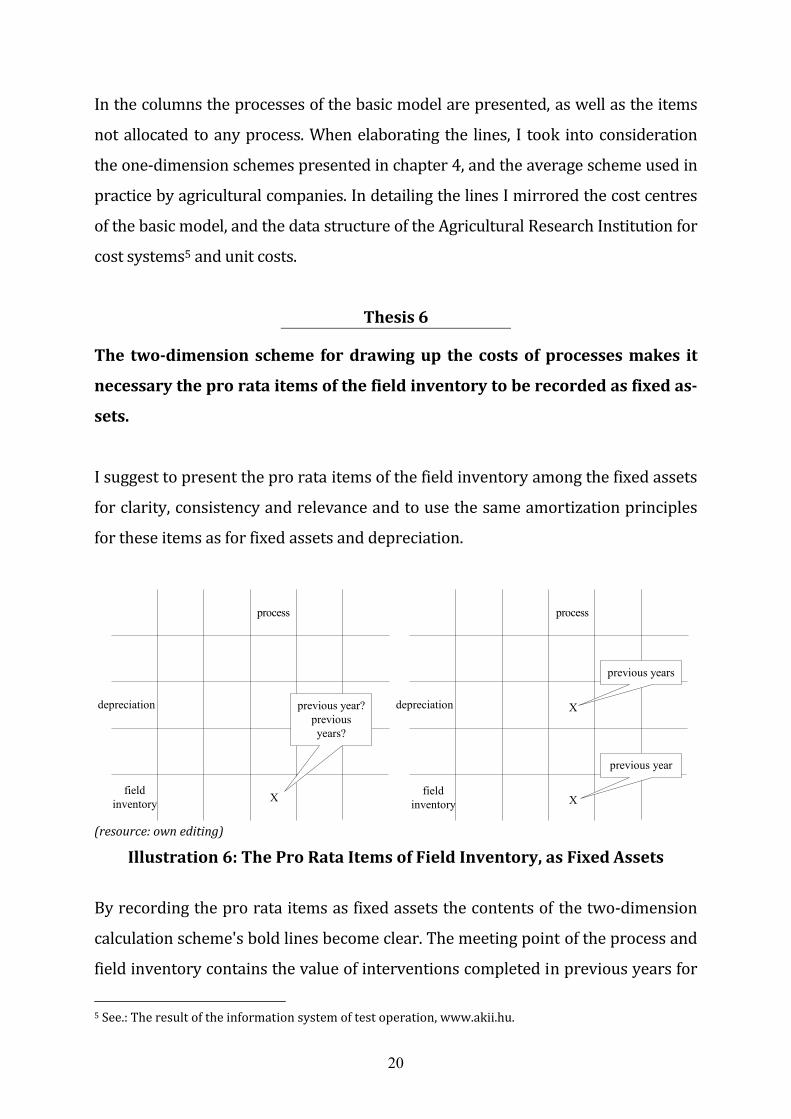

The two-dimension scheme for drawing up the costs of processes makes it

necessary the pro rata items of the field inventory to be recorded as fixed as-

sets. I suggest to present the pro rata items of the field inventory among the fixed assets for clarity, consistency and relevance and to use the same amortization principles for these items as for fixed assets and depreciation.

previous year?previousyears?

depreciation

fieldinventory X

process

previous year

previous years

fieldinventory

depreciation X

X

process

(resource: own editing)

Illustration 6: The Pro Rata Items of Field Inventory, as Fixed Assets By recording the pro rata items as fixed assets the contents of the two‐dimension calculation scheme's bold lines become clear. The meeting point of the process and field inventory contains the value of interventions completed in previous years for 5 See.: The result of the information system of test operation, www.akii.hu.

21

the sake of current year's crop, and the meeting point of the process and amortisa‐tion presents the pro rata value of works completed in previous years, but influenc‐ing several following years.

22

44.. AAPPPPLLIICCAATTIIOONN OOFF FFIINNDDIINNGGSS The inventory value based process oriented costing model elaborated for plant producing complies with the financial reporting and the management needs as well. From financial accounting's point of view agricultural companies consider the evaluation of their own stock as a primary task of unit cost calculations. Comply‐ing with the accounting regulations this model provides more accurate unit cost figures of primary and secondary products as well, while this latter were mainly assessed on dictated prices so far. Another significant area for using cost data is management advising and informa‐tion. This need can be satisfied with the information provided by the extended model explained earlier. Using the current accounting databases of companies the assessment of primary and secondary products can be completed in line with the regulations, while expanding the calculation scheme directly informs the decision maker about the relationship of cost elements and processes. The phases of time demanding production and biological transformation bring up the issue of evaluation on market value. International Accounting Standards Committee favoured accounting on market value during elaborating the stan‐dards of agricultural activities' accounting. IAS 41 International Accounting Stan‐dard (Agriculture) refers to biological assets as the carrier instruments with agri‐cultural specialty. Biological assets are the live stock and plants, while agricul‐tural assets are the harvested results of biological assets. The process oriented model can be used for assessing biological assets besides agricultural produces too. The model can be further developed for areas of time demanding agricultural activities such as plantation and forest transplantations, development and main‐tenance. I focused in my research on incorporated, ltd or cooperative farms pursuing agri‐cultural activities. The expand of the research to other agricultural companies

23

would ensure that we could get familiar with the cost accounting of small compa‐nies and use their data for management purposes. One of the emphasised objectives of basic financial and accounting training is to train professionals who can set up, develop and maintain costing systems. Using the results of the questionnaire we can make further steps to bring the practical needs and the theoretical training in line. One of the objectives of the accounting master course is to train professionals who can process the national and international accounting literature, as well as add their own share them. They know those special techniques that enable them to research and use the theoretical issues of this science. The agricultural adapta‐tion of process costing is a good example that an already existing method can be used in a different area successfully. Preparing models can develop the problem recognition and solving abilities of students. For a certain problem others might have already come up with a solution, and in the classes, armed with these solu‐tions, the processing of case studies and preparing other alternatives can be car‐ried out.

24

BBIIBBLLIIOOGGRRAAPPHHYY Alpár, Gy. – Buzás, Gy. – Csonka, I. – Jávor, A. – Kalmár, S. – Lengyel, L. – Magda, S. – Marselek, S. – Miller, Gy. – Molnár, M. – Nábrádi, A. – Pfau, E. – Pupos, T. – Salamon, L. – Stündl, L. – Szélés, Gy. – Szűcs, I. – Tégla, Zs. (2002): Mezőgazdasági üzemtan II. Szaktudás Kiadó Ház, Budapest, Babbie, E. (2003): Társadalomtudományi kutatás gyakorlata. Balassi, Budapest, Chandler, A. D. (1995): The visible hand. 13. kiadás, Harvard University Press, Cambridge, Massachusetts, London, György, E. (1964): Mezőgazdasági számviteli ismeretek. Mezőgazdasági Kiadó, Budapest, Johnson, H. T. – Kaplan, R. S. (1987): Relevance lost. The Rise and Fall of Man‐agement Accounting. Harvard Business School Press, Boston, Kaplan, R. S. – Cooper, R. (2001): Költség & Hatás, Integrált költségszámítási rendszerek: az eredményes vállalati működés alapjai. Panem – IFUA Horváth & Partner, Budapest, Körmendi, L. – Tóth, A. (2002): A controlling tudományos megközelítése és al‐kalmazása. Perfekt, Budapest, Miklósyné Ács, K. – Siklósi, Á. – Simon, Sz. (2006): A mezőgazdasági vál‐lalkozások számviteli sajátosságai. Saldo Kiadó, Budapest, Páli, L. (1973): A mezőgazdasági nagyüzemek számviteli információs rendszere. Tankönyvkiadó, Budapest, Sutus, I. (1992): A 6., 7. számlaosztályok a mezőgazdasági vállalkozások vezetői számvitelében. Számvitel és Könyvvizsgálat. 1992/7‐8. sz. 344‐348. o. Sutus, I. (2002): Gyakorlati számvitel a mezőgazdaságban. Szaktudás Kiadó Ház, Budapest, Véry Zoltán (1999): Mezőgazdasági üzemek Controlling rendszere. OTKA ta‐nulmány Yin, R. K. (2003): Case Study Research: Design and Methods. 3. kiadás, Sage, Thousand Oaks,

25

Farm Financial Standards Council (2006): Management Accounting Guidelines For Agricultural Producers, Casy Study No. 1. February 2006 Könyvviteli kézikönyv a mezőgazdasági vállalkozások számára I‐II. kötet. Müszi Rt., 1989. Mezőgazdasági számlakeret módosításokkal és kiegészítésekkel egybeszerkesz‐tett szöveg. Szervezési és Ügyvitelgépesítési Vállalat, Budapest, 1985. Segédlet a mezőgazdasági számlakeret alkalmazásához. Pénzügyminisztérium Szervezési és Ügyvitelgépesítési Intézete, Budapest, 1978.

26

PPUUBBLLIICCAATTIIOONNSS OOFF TTHHEE AAUUTTHHOORR OONN TTHHEE TTOOPPIICC Articles, books A bekerülési érték alapú folyamatorientált költségszámítás − szántóföldi növény‐termelésre kidolgozott − alapmodellje, A Controller, V. évfolyam, 2009. szeptem‐ber, ISSN 1787 3983 (to be published) Aktuális számviteli kérdések. In: Ujvári Géza (szerk.): A számvitel és adózás aktu‐ális kérdései 2009. NovoSchool Kft. – Saldo Zrt, 2009. 14‐21. o. ISBN 978 963 87656 5 9 Aktuális számviteli kérdések. In: Ujvári Géza‐Paróczai Péterné (szerk.): A szám‐vitel és adózás aktuális kérdései 2008. NovoSchool Kht. – Saldo Zrt, 2008. 11, 16‐19. o. ISBN 978 963 87656 2 8 Időbeli elhatárolások. In: Dr. Pál Tibor (szerk.): Mérlegtételek elszámolásai. Mis‐kolci Egyetem, 2008. 141‐162. o. ISBN 978 963 661 832 2 Céltartalékok. In: Dr. Pál Tibor (szerk.): Mérlegtételek elszámolásai. Miskolci Egyetem, 2008. 199‐206. o. ISBN 978 963 661 832 2 Elméleti tesztek. In: Dr. Pál Tibor (szerk.): Bevezetés a számvitelbe Példatár és munkafüzet. Economix Kiadó, 2008. 125‐129. o. ISBN 978 963 87392 30 Időbeli elhatárolások. In: Dr. Pál Tibor (szerk.): Pénzügyi számvitel példatár. Economix Kiadó, 2007. 116‐132. o. ISBN 978 963 87392 2 3 Céltartalékok. In: Dr. Pál Tibor (szerk.): Pénzügyi számvitel példatár. Economix Kiadó, 2007. 143‐149. o. ISBN 978 963 87392 2 3 Az eredmény és a jövedelmezőség számbavétele a társas mezőgazdasági vállalko‐zásoknál, SzámAdó, XVI. évfolyam 3. szám, 2007. március, 3‐9. o. ISSN 1216 5093 Kontrolling HEFOP‐3.2.2‐P.‐2004‐10‐0011‐/1.0 sz. projekt támogatásával, Miskolc, Miskolc‐Térségi Integrált Szakképző Központ, 2007. Számviteli sajátosságok a mezőgazdaságban. In: Dr. Pál Tibor (szerk.): Számviteli rendszerek. Economix Kiadó, 2006. 129‐173. o. ISBN 963 06 1124 4 Új irányzatok a számvitelben. In: Dr. Pál Tibor (szerk.): Számviteli rendszerek. Economix Kiadó, 2006. 55‐68. o. ISBN 963 06 1124 9

27

Időbeli elhatárolások. In: Dr. Pál Tibor (szerk.): Pénzügyi számvitel. Economix Ki‐adó, 2006. 148‐169. o. ISBN 963 87392 0 7 Céltartalékok In: Dr. Pál Tibor (szerk.): Pénzügyi számvitel. Economix Kiadó, 2006. 208‐215. o. ISBN 963 87392 0 7 Támogatások számvitele. In: Dr. Pál Tibor (szerk.): Speciális számviteli eljárások. Economix Kiadó, 2006. 260‐279. o. ISBN‐10 963 200 100 1 ISBN‐13 978 963 200 100 5 Hungarian Farm Accountancy Data Network Transactions of the Universities of Košice, 3/2005, 41‐47. o. Technická Univerzita, Košice, ISSN 1335‐2334 Költségelszámolás, önköltségszámítás a húshasznú tehenészetekben Miskolc, Egyetemi Kiadó, Gazdaságtudományi Közlemények, 2005, 4. Kötet, 75‐83. o. HU ISSN 1586 0655 Előrejelzés, TQM, kreatív számvitel. A jövőkép változásai a számvitelben. In: Dr. Pál Tibor (szerk.): Számviteli rendszerek, speciális eljárások. Economix Kiadó, 2004. 227‐243. o. ISBN 963 214 114 8 Példatár a vállalkozások tevékenységének gazdasági elemzéséhez I. kötet, Economix Kiadó, 2004. 138‐289. o. ISBN 963 661 626 4 A Balanced Scorecard „alkalmazotti” nézőpontjának szerepe a szellemi tőkével való stratégiai gazdálkodás területén. In: Gyakorlati controlling kézikönyv, Raabe Tanácsadó és Kiadó Kft., Budapest, 2002. ISBN 963 85920 5 2 A vállalatok pénzügyi elemzése, In: Dr. Bozsik Sándor‐Dr. Vigvári András (szerk.): Pénzügytan II. Szöveggyűjtemény. Bíbor Kiadó, 2002, 334‐341. o. Conference lectures Kontrolling HEFOP‐3.2.2‐P.‐2004‐10‐0011‐/1.0 sz. projekt támogatásával, Fórum az oktatásban résztvevő szakiskolai és középiskolai tanárok részére, Mis‐kolc, 2008. április 10. Az EU csatlakozás hatása a társas mezőgazdasági vállalkozások jövedelmezőségé‐re, XXVII. OTDK PhD Szekció, Miskolc, 2007. április 25‐27. Prime Cost Calculation Related to Crop Farming: Accounting Act vs.FADN microCAD 2006, International Scientific Conference, Miskolc, 2006. március 16‐17.

28

Az állami támogatások elszámolása az erdőgazdasági tevékenységek alapján Doktoranduszok Fóruma, Miskolc, 2006. november 9. Agrárvállalkozások jövedelmezőségének mérése Doktoranduszok Fóruma, Miskolc, 2005. november 9. Tevékenység alapú költségszámítás alkalmazása a segédüzemi költségek felosztá‐sakor II. Országos Közgazdaságtudományi Doktorandusz Konferencia, Miskolc‐Lillafü‐red, 2003. május 26‐28. Költségtervezési problémák a mezőgazdasági vállalkozásoknál Doktoranduszok Fóruma, Miskolc, 2002. november 6. Az EU csatlakozással együtt járó érdekellentétek a magyar mezőgazdaságban Doktoranduszok Fóruma, Miskolc, 2001. november 6. Gazdálkodj okosan! Közösen vagy családban? Helyzetkép a birtokviszonyokról az EU csatlakozás előtt XXIV. OTDK, Gödöllő, 1999. március 30‐31.