Embed Size (px)

Citation preview

PACIFIC UNIVERSITY

Financial Statements

June 30, 2007

(With Independent Auditors’ Report Thereon)

KPMG, LLP. KPMG LLP, a limited liability partnership, is a member of KPMG International, a Swiss association.

KPMG LLP Suite 3800 1300 South West Fifth Avenue Portland, OR 97201

Independent Auditors’ Report

The Board of Trustees Pacific University:

We have audited the accompanying statement of financial position of Pacific University (the University) as of June 30, 2007, and the related statements of activities and cash flows for the year then ended. These financial statements are the responsibility of the University’s management. Our responsibility is to express an opinion on these financial statements based on our audit. The prior year summarized comparative information has been derived from the University’s 2006 financial statements and, in our report dated November 10, 2006, we expressed an unqualified opinion on those financial statements.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the University’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Pacific University as of June 30, 2007, and the changes in its net assets and its cash flows for the year then ended in conformity with U.S. generally accepted accounting principles.

As discussed in Notes 2 and 14 to the financial statements, the University adopted the recognition and disclosure provisions of Statement of Financial Accounting Standards No. 158, Employers’ Accounting for Defined Pension and Other Postretirement Plans, as of June 30, 2007.

November 15, 2007

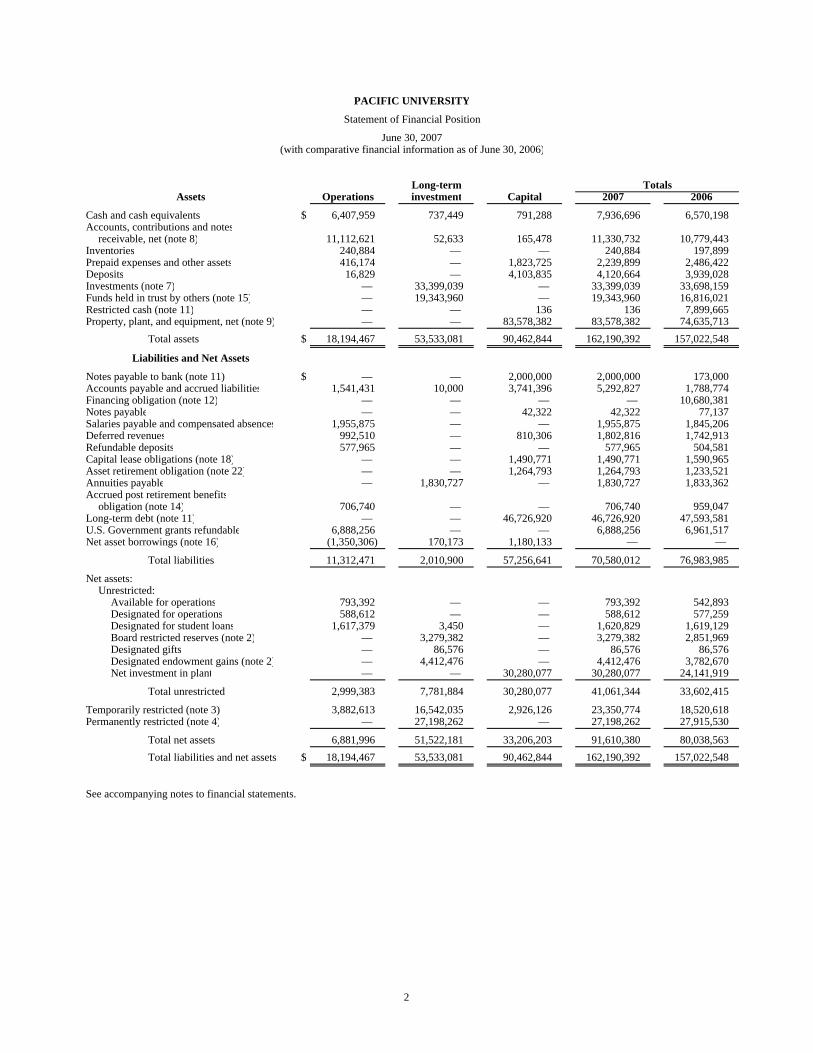

PACIFIC UNIVERSITY

Statement of Financial Position

June 30, 2007(with comparative financial information as of June 30, 2006)

Long-term TotalsAssets Operations investment Capital 2007 2006

Cash and cash equivalents $ 6,407,959 737,449 791,288 7,936,696 6,570,198 Accounts, contributions and notes

receivable, net (note 8) 11,112,621 52,633 165,478 11,330,732 10,779,443 Inventories 240,884 — — 240,884 197,899 Prepaid expenses and other assets 416,174 — 1,823,725 2,239,899 2,486,422 Deposits 16,829 — 4,103,835 4,120,664 3,939,028 Investments (note 7) — 33,399,039 — 33,399,039 33,698,159 Funds held in trust by others (note 15) — 19,343,960 — 19,343,960 16,816,021 Restricted cash (note 11) — — 136 136 7,899,665 Property, plant, and equipment, net (note 9) — — 83,578,382 83,578,382 74,635,713

Total assets $ 18,194,467 53,533,081 90,462,844 162,190,392 157,022,548

Liabilities and Net Assets

Notes payable to bank (note 11) $ — — 2,000,000 2,000,000 173,000 Accounts payable and accrued liabilities 1,541,431 10,000 3,741,396 5,292,827 1,788,774 Financing obligation (note 12) — — — — 10,680,381 Notes payable — — 42,322 42,322 77,137 Salaries payable and compensated absences 1,955,875 — — 1,955,875 1,845,206 Deferred revenues 992,510 — 810,306 1,802,816 1,742,913 Refundable deposits 577,965 — — 577,965 504,581 Capital lease obligations (note 18) — — 1,490,771 1,490,771 1,590,965 Asset retirement obligation (note 22) — — 1,264,793 1,264,793 1,233,521 Annuities payable — 1,830,727 — 1,830,727 1,833,362 Accrued post retirement benefits

obligation (note 14) 706,740 — — 706,740 959,047 Long-term debt (note 11) — — 46,726,920 46,726,920 47,593,581 U.S. Government grants refundable 6,888,256 — — 6,888,256 6,961,517 Net asset borrowings (note 16) (1,350,306) 170,173 1,180,133 — —

Total liabilities 11,312,471 2,010,900 57,256,641 70,580,012 76,983,985

Net assets:Unrestricted:

Available for operations 793,392 — — 793,392 542,893 Designated for operations 588,612 — — 588,612 577,259 Designated for student loans 1,617,379 3,450 — 1,620,829 1,619,129 Board restricted reserves (note 2) — 3,279,382 — 3,279,382 2,851,969 Designated gifts — 86,576 — 86,576 86,576 Designated endowment gains (note 2) — 4,412,476 — 4,412,476 3,782,670 Net investment in plant — — 30,280,077 30,280,077 24,141,919

Total unrestricted 2,999,383 7,781,884 30,280,077 41,061,344 33,602,415

Temporarily restricted (note 3) 3,882,613 16,542,035 2,926,126 23,350,774 18,520,618 Permanently restricted (note 4) — 27,198,262 — 27,198,262 27,915,530

Total net assets 6,881,996 51,522,181 33,206,203 91,610,380 80,038,563 Total liabilities and net assets $ 18,194,467 53,533,081 90,462,844 162,190,392 157,022,548

See accompanying notes to financial statements.

2

PACIFIC UNIVERSITY

Statement of Activities

Year ended June 30, 2007(with comparative financial information as of June 30, 2006)

Long-term TotalsOperations investment Capital 2007 2006

Changes in unrestricted net assets:Revenues and gains:

Tuition and fees $ 58,575,303 — — 58,575,303 50,563,332 Scholarships and fellowships (12,903,769) — — (12,903,769) (10,956,636)

Net tuition and fees 45,671,534 — — 45,671,534 39,606,696

Contributions 479,826 — 16,875 496,701 1,067,279 Contracts and other exchange transactions 1,168,675 — 564,150 1,732,825 529,509 Investment income on endowment 465,331 — — 465,331 430,391 Other investment income 372,575 1,700 371,343 745,618 969,941 Net realized and unrealized gains 97 476,356 — 476,453 189,016 Unrealized gains on endowment — 235,133 — 235,133 866,410 Sales of services at clinics 2,012,070 — — 2,012,070 1,830,341 Sales of services of auxiliary enterprises 5,965,054 — 53,000 6,018,054 4,926,632 Other sources 223,081 (27,353) 36,518 232,246 17,812

Total unrestricted revenues and gains 56,358,243 685,836 1,041,886 58,085,965 50,434,027

Net assets released from restrictions (note 5) 4,017,500 3,823,293 — 7,840,793 10,921,859

Total revenues and gains and net assets released 60,375,743 4,509,129 1,041,886 65,926,758 61,355,886

Expenses and losses:Education and general:

Instruction 21,337,256 — — 21,337,256 19,240,317 Research 499,172 — — 499,172 530,713 Public service 180,164 — — 180,164 132,182 Academic support 7,296,729 — — 7,296,729 6,053,072 Clinics 2,902,096 — — 2,902,096 2,580,844 Student services 6,090,208 — — 6,090,208 5,862,703 Institutional support 7,609,701 — — 7,609,701 7,308,185 Operation and maintenance of plant 3,092,696 — — 3,092,696 2,786,604 Interest on long-term debt — — 2,188,374 2,188,374 1,966,674 Depreciation and amortization — — 2,625,876 2,625,876 2,583,575 Loss-extinguishment of debt (note 11) — — — — 1,993,238 Other — — 26,684 26,684 (40,563)

Total education and general 49,008,022 — 4,840,934 53,848,956 50,997,544

Auxiliary enterprises 4,859,995 — 4,859,995 3,367,524

Total expenses and losses 53,868,017 — 4,840,934 58,708,951 54,365,068

Transfers:Debt service 2,350,690 — (2,350,690) — — Capital purchases 683,996 — (683,996) — — Long-term investment to operations (450,211) 3,450,211 (3,000,000) — — Operating to plant 3,902,521 — (3,902,521) — —

Total expenses and losses and transfers 60,355,013 3,450,211 (5,096,273) 58,708,951 54,365,068

Increase in unrestricted net assets before cumulativeeffect of changes in accounting principle 20,730 1,058,918 6,138,159 7,217,807 6,990,818

Cumulative effect of changes in accounting principle (note 22) — — — — (1,123,088) Change in accounting principle - FAS 158 (notes 2 and 14) 241,122 — — 241,122 —

Increase in unrestricted net assets 261,852 1,058,918 6,138,159 7,458,929 5,867,730

Changes in temporarily restricted net assets:Contributions 4,275,264 150,001 1,019,392 5,444,657 5,296,106 Investment income on endowment 516,281 45,915 — 562,196 566,541 Investment income on annuities/life income and other 455,111 305,954 32,797 793,862 581,826 Net realized gains on endowment investments — 2,096,836 — 2,096,836 1,135,648 Net realized gains on other investments — 180,136 19,228 199,364 71,361 Changes in net unrealized gains on endowment investments — 1,056,535 — 1,056,535 309,664 Changes in unrealized gains on other investments — 276,014 — 276,014 358,181 Net assets released from restrictions (note 5) (4,017,500) (954,957) — (4,972,457) (10,921,859) Management/trustee fees — (46,098) — (46,098) (17,038) Actuarial adjustments — (580,753) — (580,753) (505,726)

Increase (decrease) in temporarily restrictednet assets 1,229,156 2,529,583 1,071,417 4,830,156 (3,125,296)

Changes in permanently restricted net assets:Contributions — 219,232 — 219,232 50,575 Investment income on endowment — 329,429 — 329,429 344,987 Actuarial adjustments — 1,602,407 — 1,602,407 (761,210) Net assets released from restriction (note 5) — (2,868,336) — (2,868,336) —

Decrease in permanently restrictednet assets — (717,268) — (717,268) (365,648)

Increase in net assets 1,491,008 2,871,233 7,209,576 11,571,817 2,376,786

Net assets at beginning of year 5,390,988 48,650,948 25,996,627 80,038,563 77,661,777 Net assets at end of year $ 6,881,996 51,522,181 33,206,203 91,610,380 80,038,563

See accompanying notes to financial statements.

3

PACIFIC UNIVERSITY

Statement of Cash Flows

Year ended June 30, 2007(with comparative financial information as of June 30, 2006)

Totals2007 2006

Cash flows from operating activities:Increase in net assets $ 11,571,817 2,376,786 Cumulative effect of change in accounting principle — 1,123,088 Adjustments to reconcile change in net assets to cash

provided by operating activities:Depreciation and amortization 2,597,434 2,555,125 Loss on extinguishment of debt — 1,993,238 Net gains on investments (6,380,733) (2,720,374) Actuarial adjustments (2,635) (43,521) FAS 158 implementation (241,122) — Noncash contributions (16,875) (414,722) Contribution of marketable securities — (473,211) Contributions and net gains on investments restricted to long-term (1,388,624) (1,784,905) (Increase) decrease in accounts and notes receivable (551,289) 440,413 Decrease (increase) in prepaid expenses and other assets 203,538 (1,384,907) Increase (decrease) in accounts payable and accrued liabilities 231,380 (1,323,897) Increase in deferred revenues 59,903 518,041 Increase in refundable deposits 73,384 82,961 Increase in asset retirement obligation - FIN 47 31,272 — Decrease in U.S. Government grants refundable (73,261) (3,526)

Net cash provided by operating activities 6,114,189 940,589

Cash flows from investing activities:Purchase of property, plant, and equipment (18,589,866) (20,982,043) Purchases of investment securities (7,104,096) (8,923,225) Proceeds from sale of investment securities 11,885,494 9,822,817 Change in bond deposits (181,636) (2,221,284) Changes in restricted cash for purchase of property, plant, and equipment 7,899,529 (7,899,663)

Net cash used in investing activities (6,090,575) (30,203,398)

Cash flows from financing activities:Proceeds (borrowings) on line of credit and note payable 1,792,186 (205,994) Contributions and net gains on investments restricted to long-term 1,388,624 1,784,905 Payments on long-term debt (838,220) (7,731) Redemption of 2000 series bonds — (17,863,238) New bond issue 2005 series — 46,625,000 Premium on 2005 bond issue — 881,708 Payments on capital lease obligations (370,221) (524,853) Annuity disbursements (629,485) (554,677)

Net cash provided by financing activities 1,342,884 30,135,120

Net increase in cash and cash equivalents 1,366,498 872,311

Cash and cash equivalents at beginning of year 6,570,198 5,697,887 Cash and cash equivalents at end of year $ 7,936,696 6,570,198

Supplemental cash flow disclosure:Cash paid for interest, net of amount capitalized $ 2,460,079 2,236,867

Supplemental disclosure of noncash investing and financing activities:Capital lease obligation $ 270,027 1,746,502 Contribution of funds held in trust by others — 473,211 Financing obligation (10,680,381) 10,680,381

See accompanying notes to financial statements.

4

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

5 (Continued)

(1) Organization and History

Pacific University (the University) was established through an act passed by the Legislative Assembly of the Territory of Oregon on September 26, 1849, for the purpose of establishing a seminary of learning, in Washington County, for the instruction of persons of both sexes in science and literature. The University consists of an undergraduate College of Arts and Sciences, graduate and/or professional schools including the College of Education, College of Optometry and the College of Health Professions, which include occupational therapy, physical therapy, clinical psychology, physicians’ assistant, dental health science and pharmacy.

(2) Summary of Significant Accounting Policies

(a) Accrual Basis

The financial statements of Pacific University have been prepared on the accrual basis of accounting.

(b) Basis of Presentation

Net assets and revenues, expenses, gains and losses are classified based on the existence or absence of donor imposed restrictions. Accordingly, net assets of the University and changes therein are classified and reported as follows:

• Unrestricted net assets – Net assets that are not subject to donor-imposed restrictions or donor restricted contributions whose restrictions are met in the same reporting period.

• Temporarily restricted net assets – Net assets subject to donor-imposed restrictions that will be met either by actions of the University and/or the passage of time.

• Permanently restricted net assets – Net assets subject to donor-imposed restrictions that they be permanently maintained by the University. Generally the donors of these assets permit the University to use all or part of the income earned on related investments for general or specific purposes.

Revenues are reported as increases in unrestricted net assets unless their use is limited by donor-imposed restrictions. Expenses are reported as decreases in unrestricted net assets except for actuarial adjustments. Gains and losses on investments and other assets or liabilities are reported as increases or decreases in unrestricted net assets unless their use is restricted by explicit donor restrictions or by law. Expirations of temporary restrictions on net assets (i.e., the donor stipulated purpose has been fulfilled and/or the stipulated time period has elapsed) are reported as reclassifications between the applicable classes of net assets.

The University follows a practice of classifying its assets, liabilities, net assets, revenues and expenses as operating, long-term investment or capital. Items classified as long-term investment include accounts and transactions related to annuity and life income funds, endowment funds, and student loan funds. Items classified as capital include accounts and transactions related to plant facilities. All other accounts and transactions are classified as operating.

Contributions, including unconditional promises to give, are recognized as revenues in the period in which the unconditional promise is received. Conditional promises to give are not recognized until

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

6 (Continued)

they become unconditional, that is when the conditions on which they depend are substantially met. Contributions of assets other than cash are recorded at their estimated fair value. Contributions to be received after one year are discounted at an appropriate discount rate commensurate with the risks involved. Amortization of the discount is recorded as additional contribution revenue in accordance with donor imposed restrictions, if any, on the contributions. An allowance for uncollectible contributions receivable is provided based upon management’s judgment, including such factors as prior collection history, type of contribution and nature of fund raising activity. Restrictions related to contributions for the purchase of capital additions are released when the asset is placed in service.

Income and net gains on investments of endowment and similar funds are reported as follows:

• As increases in permanently restricted net assets if the terms of the gift require that they be added to the principal of a permanently restricted net asset.

• As increases in temporarily restricted net assets if the terms of the gift impose restrictions on the use of the income or net realizable gains.

• As increases in unrestricted net assets in all other cases.

(c) Board Restricted Reserves

Board restricted reserves represent unrestricted “operating” funds transferred to “long-term investment” for investment in the endowment pool. The University’s board of trustees must approve of all quasi endowment activity.

(d) Designated Endowment Gains

A majority of the University’s endowment agreements restrict interest or dividend income and unrealized and realized gains for particular purposes. The University has met the donor restrictions and released the restricted amounts, however for budget purposes, the Board designates these endowment gains for future use. The following summarizes the University’s calculation and current year activity:

July 1, 2006 designated endowment gains $ 3,782,670

Unrestricted realized and unrealized gains, net 241,786 Gains transferred to operations (494,935) Unrestricted transfers to endowment fund and other distributions (2,927,354) Net assets released from restriction 3,810,309

June 30, 2007 designated endowment gains $ 4,412,476

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

7 (Continued)

(e) Split Interest Agreements

The University uses the actuarial method of recording certain split interest arrangement. Under this method, the present value of the payments to beneficiaries is determined based upon life expectancy tables when the gift is received. The present value of those payments is recorded as a liability and the remainder as temporarily or permanently restricted net assets depending on donor-imposed restrictions. Annual adjustments are made between the liability and the net assets to record actuarial gains and losses. The discount rate used by the University in calculating present value of all split interest agreements ranges from 5.0% – 8.2% at June 30, 2007.

(f) Cash and Cash Equivalents

Cash equivalents of $5,322,602 as of June 30, 2007 consist of short-term, highly liquid investments with original maturities of three months or less.

(g) Restricted Cash

Restricted cash totaling $136 at June 30, 2007 represents amounts designated for future capital projects as defined in the bond agreement.

(h) Investments

Investments in marketable equity securities with readily determinable fair values and all investments in debt securities are carried at fair value based on published market values. Investments in real estate and securities for which fair value is not readily determinable are carried at cost, if purchased, or at fair value at the date of receipt, if acquired by donation. The alternative investments, which are not readily marketable, are carried at estimated fair values. Pacific University reviews and evaluates the values provided by the investment managers and estimates the fair value of the alternative investments. Those estimated fair values may differ significantly from the values that would have been used had a ready market for those securities existed.

Net appreciation (depreciation) in the fair value of those investments that are accounted for at fair value, including realized gains or losses and unrealized appreciation (depreciation) on those investments, as well as all dividends, interest, and other investment income, is shown in the statement of activities. Gains and investment income that are limited to specific uses by donor-imposed restrictions are reported as increases in unrestricted net assets if the restrictions are met in the same reporting period that the gains and income are recognized. Losses on investments related to gifts that the donor required to be invested in perpetuity (i.e., endowment funds) are classified as decreases in unrestricted net assets; subsequent gains that restore the fair value of the assets of the endowment funds to the required level are classified as increases in unrestricted net assets.

(i) Inventory

Inventory consists primarily of eye glass frames and are stated at cost which approximates lower of cost or market under the first in, first out method.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

8 (Continued)

(j) Property, Plant, and Equipment

Property, plant, and equipment are stated at cost at date of acquisition or, in the case of gifts, fair market value on the date received. Normal repair and maintenance expenses and equipment replacement costs are expensed as incurred. Estimated useful lives used to calculate depreciation are land improvements and buildings (thirty to fifty years), building improvements (ten to twenty years), library books (fifteen years), and furniture and equipment (three to ten years). Capital leases are being amortized using the straight line method over the lives of the capital leases. Depreciation is calculated using the straight line method.

(k) Deferred Revenues

Deferred revenues consist primarily of prepayments of tuition and fees related to future academic periods.

(l) Debt Issuance Costs

Legal and accounting fees, printing costs, and other expenses associated with the issuance of the City of Forest Grove, Oregon, Pacific University Campus Improvement and Refunding Bonds, Series 2005, are being amortized on a method that approximates effective yield over the terms of the bonds, which is thirty-one years. During the fiscal year, the University amortized $62,887 of debt issuance costs and are included in depreciation and amortization in the accompanying statement of activities. The unamortized debt issuance costs at June 30, 2007 were $1,823,725 and are included in prepaid expenses and other assets in the accompanying statement of financial position.

(m) Income Taxes

The Internal Revenue Service has recognized the University as exempt from tax under the provisions of Section 501(c)(3) of the Internal Revenue Code except to the extent of unrelated business income under Sections 511 through 515. Unrelated business income tax, if any, is immaterial and therefore, no tax provision has been made.

(n) Self-Insurance

The University is self-insured for certain medical and dental benefits through a benefit trust. Annual contributions to the trust are recorded as expenses of unrestricted net assets. Reserves for unpaid claims are estimated using actuarial methods. It is possible that the amounts paid in connection with self-insured risks will vary from amounts accrued as self-insurance reserves as of June 30, 2007.

(o) Postretirement Benefits

The University maintains a postretirement benefit plan and accounts for the plan within the framework of Statement of Financial Accounting Standards (SFAS) No. 158, Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans and, as still applicable, SFAS No. 106, Employers’ Accounting for Postretirement Benefits Other than Pensions, respectively. SFAS No. 158 is discussed in the note titled Recently Issued Accounting Standard.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

9 (Continued)

The University measures the costs of the obligation based on its best estimate. Critical actuarial assumption includes the discount rate to estimate the liability at June 30, 2007. The University evaluates assumptions annually and modifies them as appropriate. The net periodic costs are recognized as employees render the services necessary to earn the postretirement benefits (see note 14).

(p) Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from these estimates.

(q) Recently Issued Accounting Standard

In September 2006, the Financial Accounting Standards Board issued SFAS No. 158, Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans. This Statement is generally effective for fiscal years ending after December 15, 2006 for public companies and for years ending after June 15, 2007 for nonpublic companies. The adoption of SFAS No. 158 is reflected in these financial statements and resulted in a reduction of accrued postretirement benefits obligation of $241,122 in the University’s June 30, 2007 statement of financial position and an increase in unrestricted net assets for the year ended June 30, 2007.

SFAS No. 158 requires that companies recognize on their balance sheet the funded status of defined pension and other retirement benefit plans. The offset for newly created liabilities (or assets if overfunded) is to net assets. The University has historically recognized the unfunded status of its postretirement plan.

In addition, SFAS No. 158 requires employers to use their fiscal year end as the measurement date and the option to use a date as much as 90 days prior to fiscal year end is no longer available. The effective date for this change is fiscal years ending December 15, 2008. The University has historically used a June 30th measurement date.

The incremental effect of applying SFAS No. 158 on the University’s financial statements as of June 30, 2007 was as follows:

Accruedpostretirement

benefitobligation

Before application of SFAS No. 158 $ 947,862 Adjustment to unrestricted net assets (241,122) After application of SFAS No. 158 $ 706,740

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

10 (Continued)

Amounts recognized in unrestricted net assets consist of:

Net loss $ 111,675 Prior service cost 129,447

$ 241,122

(3) Temporarily Restricted Net Assets

Temporarily restricted net assets at June 30, 2007 are available for:

Long-termOperations investment Capital Total

Student services $ 645,447 — — 645,447 Instruction 133,013 — — 133,013 Research 591,080 — — 591,080 Public service 173,188 — — 173,188 Academic support 577,378 — — 577,378 Clinics 60,757 — — 60,757 Institutional support 33,048 — — 33,048 Operation and maintenance

of plant 7,635 — — 7,635 Scholarships and fellowships 1,661,067 — — 1,661,067 Split-interest agreements — 6,051,812 — 6,051,812 Endowment earnings — 6,692,515 — 6,692,515 Funds held in trust by

others – time restricted — 3,797,708 — 3,797,708 Capital — — 2,926,126 2,926,126

$ 3,882,613 16,542,035 2,926,126 23,350,774

(4) Permanently Restricted Net Assets

Income from permanently restricted net assets at June 30, 2007 are restricted to:

Long-terminvestment

Scholarships $ 15,826,810 Student cultural activities 2,189,689 Student short-term loans 211,488 Endowed chairs and other 2,646,305 Unrestricted operational use 6,323,970

$ 27,198,262

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

11 (Continued)

On June 22, 2007 the Uniform Prudent Management of Institutional Funds Act (UPMIFA) was signed into law in the State of Oregon. UPMIFA will be implemented effective January 1, 2008. This new law revises the Uniform Management of Institutional Funds Act (UMIFA) which has governed Oregon charitable institutions with respect to the management, investment and expenditure of endowment funds since 1972. UPMIFA builds upon UMIFA’s rule on appreciation, but it will eliminate the concept of “historic dollar value.” UPMIFA, instead, provides guidance on prudence and makes the need for a floor on spending unnecessary.

(5) Net Assets Released from Restrictions

Net assets were released from donor restrictions by incurring expenses satisfying the restricted purposes or by occurrence of other events specified by donors. Net assets released from restriction during the year ended June 30, 2007 are as follows:

Long-termOperations investment Capital Total

Purpose restrictionsaccomplished:

Instruction $ 670,214 — — 670,214 Research 357,885 — — 357,885 Public service 35,951 — — 35,951 Academic support 215,425 — — 215,425 Clinics 5,446 — — 5,446 Student services 368,258 — — 368,258 Institutional support 192,786 — — 192,786 Operation and

maintenance of plant 11,074 — — 11,074 Scholarships and

fellowships 2,160,461 — — 2,160,461 Endowment and split

interest agreements — 3,823,293 — 3,823,293 $ 4,017,500 3,823,293 — 7,840,793

In 2007, a donor released $2,868,336 from permanently restricted net assets that was used in operations by the University in the current year.

(6) Fair Value of Financial Instruments

The following methods and assumptions were used to estimate the fair value of each class of financial instruments for which it is practicable to estimate that value:

(a) Cash and Cash Equivalents

The carrying amount approximates fair value, based on the short maturity of those instruments.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

12 (Continued)

(b) Loans Receivable

The fair value of student loans receivable approximates their carrying value, based on current comparable loan rates.

(c) Investments

The fair value of investments is estimated based on quoted market prices for those investments that are invested in actively traded securities. For other investments for which there are no quoted market prices, an estimate of the amount that could be realized in a sale is made by management. As of June 30, 2007, management believes the fair value of all investments for which there are no quoted market prices approximates the carrying value.

(d) Bonds Payable

The fair value of the University’s long-term debt is estimated based on the current rates available to the University for debt of the same remaining maturities. Taking into account current borrowing rates as of June 30, 2007, the fair value of the University’s bonds approximates $49,455,742 as compared to its carrying value of $46,726,920 (see note 11).

(7) Investments

The fair values of investments by type are as follows at June 30, 2007:

Fair value

Equity securities $ 3,895,954 Mutual funds:

Fixed Income 8,172,652 Large Cap 7,418,866 Small Cap 5,635,590 International 4,173,099

Alternative investments 3,387,878 Real estate 715,000

Total investments $ 33,399,039

The board of trustees has approved a “total return concept” policy, where the University may appropriate up to 5% of the endowment based on a three year moving average value at July 1 each year. In accordance with this policy, in 2007, the University transferred $580,969 and $537,227 of investment income and net appreciation, respectively, from the endowment pool to operations.

Endowment income from “pooled” and “nonpooled” investments, including realized and unrealized gains and losses, totaled $5,221,815. Income, realized and unrealized gains and losses, from other funds totaled $2,014,956. Investment expense related to investment income was $59,148 for the year ended June 30, 2007.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

13 (Continued)

(8) Accounts, Contributions and Notes Receivable

(a) Accounts, contributions and notes receivable consist of the following at June 30, 2007:

Long-termOperations investment Capital Total

Student accounts receivable $ 1,467,778 — — 1,467,778 Collections 170,358 — — 170,358 Clinics receivable 460,279 — — 460,279 Perkins loans 5,464,736 — — 5,464,736 Health professional loans 2,076,378 — — 2,076,378 Grants and contracts receivable 550,251 — — 550,251 Pledges and contributions — — — —

receivable, net of discountsof $192,616 776,799 22,036 174,923 973,758

Other receivables 439,143 31,952 — 471,095

11,405,722 53,988 174,923 11,634,633

Less allowance for doubtfulaccounts (293,101) (1,355) (9,445) (303,901)

$ 11,112,621 52,633 165,478 11,330,732

The Perkins and Health professional (HPL) loan funds generally are payable, including interest at 5% over approximately ten years following university attendance. Principal payments, interest, and losses due to cancellation are shared by the University and the U.S. Government in proportion to their share of funds provided. The Perkins program provides for cancellation of loans if the student is employed in certain occupations following graduation (employment cancellations). Such employment cancellations are absorbed in full by the U.S. Government.

(b) Contributions Receivable

Included in accounts receivable are the following unconditional promises to give as of June 30, 2007:

Unconditional promises to give before unamortized discount and allowancefor uncollectibles $ 1,166,374

Less unamortized discount (192,616) Allowance for uncollectibles (58,318)

Net unconditional promises to give $ 915,440

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

14 (Continued)

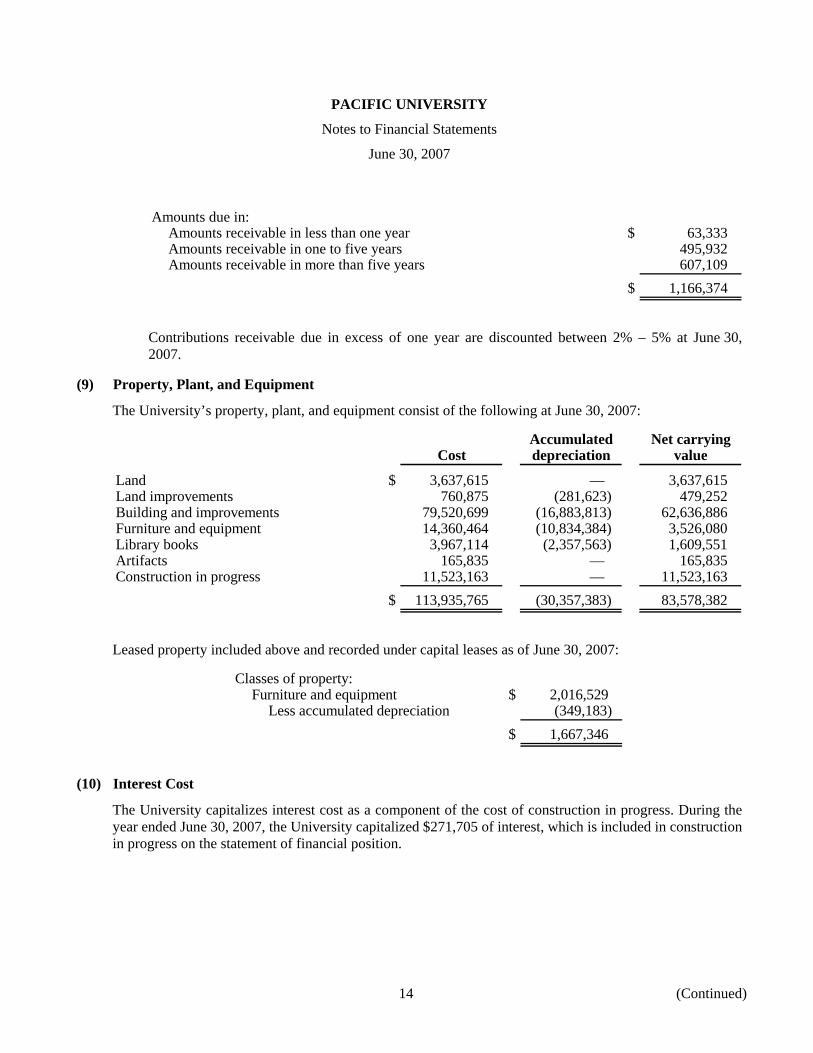

Amounts due in:Amounts receivable in less than one year $ 63,333 Amounts receivable in one to five years 495,932 Amounts receivable in more than five years 607,109

$ 1,166,374

Contributions receivable due in excess of one year are discounted between 2% – 5% at June 30, 2007.

(9) Property, Plant, and Equipment

The University’s property, plant, and equipment consist of the following at June 30, 2007:

Accumulated Net carryingCost depreciation value

Land $ 3,637,615 — 3,637,615 Land improvements 760,875 (281,623) 479,252 Building and improvements 79,520,699 (16,883,813) 62,636,886 Furniture and equipment 14,360,464 (10,834,384) 3,526,080 Library books 3,967,114 (2,357,563) 1,609,551 Artifacts 165,835 — 165,835 Construction in progress 11,523,163 — 11,523,163

$ 113,935,765 (30,357,383) 83,578,382

Leased property included above and recorded under capital leases as of June 30, 2007:

Classes of property:Furniture and equipment $ 2,016,529

Less accumulated depreciation (349,183) $ 1,667,346

(10) Interest Cost

The University capitalizes interest cost as a component of the cost of construction in progress. During the year ended June 30, 2007, the University capitalized $271,705 of interest, which is included in construction in progress on the statement of financial position.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

15 (Continued)

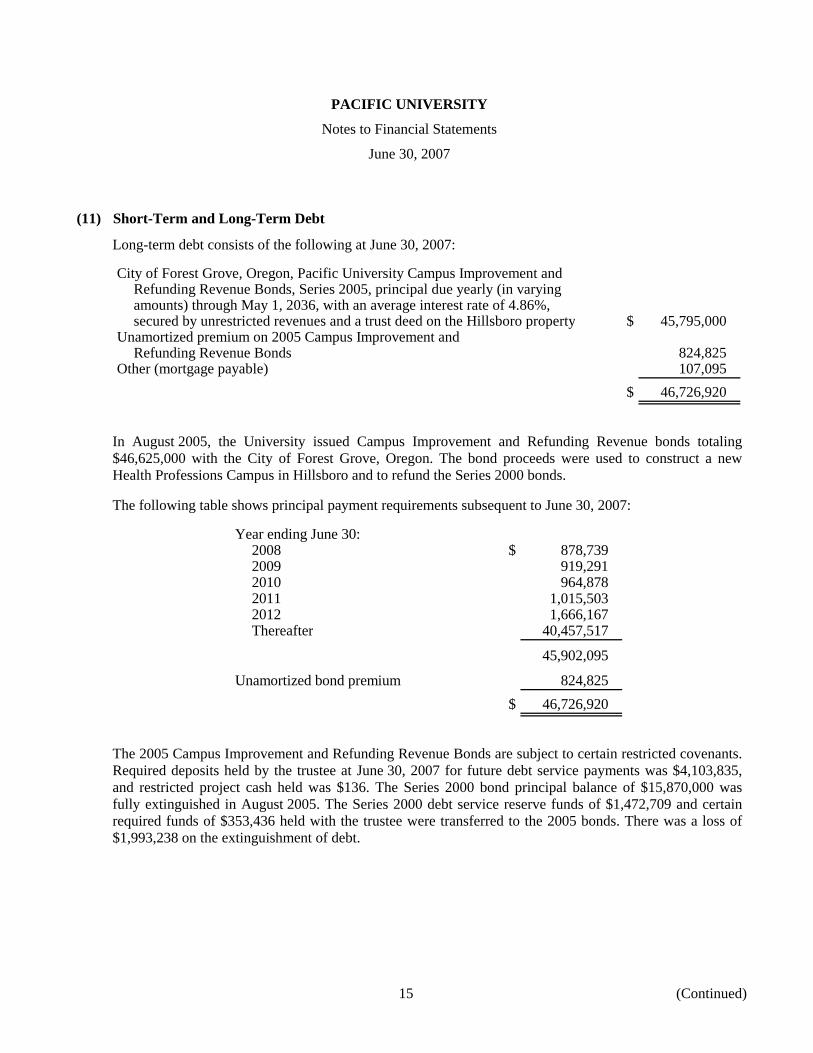

(11) Short-Term and Long-Term Debt

Long-term debt consists of the following at June 30, 2007:

City of Forest Grove, Oregon, Pacific University Campus Improvement andRefunding Revenue Bonds, Series 2005, principal due yearly (in varyingamounts) through May 1, 2036, with an average interest rate of 4.86%,secured by unrestricted revenues and a trust deed on the Hillsboro property $ 45,795,000

Unamortized premium on 2005 Campus Improvement andRefunding Revenue Bonds 824,825

Other (mortgage payable) 107,095 $ 46,726,920

In August 2005, the University issued Campus Improvement and Refunding Revenue bonds totaling $46,625,000 with the City of Forest Grove, Oregon. The bond proceeds were used to construct a new Health Professions Campus in Hillsboro and to refund the Series 2000 bonds.

The following table shows principal payment requirements subsequent to June 30, 2007:

Year ending June 30:2008 $ 878,739 2009 919,291 2010 964,878 2011 1,015,503 2012 1,666,167 Thereafter 40,457,517

45,902,095

Unamortized bond premium 824,825 $ 46,726,920

The 2005 Campus Improvement and Refunding Revenue Bonds are subject to certain restricted covenants. Required deposits held by the trustee at June 30, 2007 for future debt service payments was $4,103,835, and restricted project cash held was $136. The Series 2000 bond principal balance of $15,870,000 was fully extinguished in August 2005. The Series 2000 debt service reserve funds of $1,472,709 and certain required funds of $353,436 held with the trustee were transferred to the 2005 bonds. There was a loss of $1,993,238 on the extinguishment of debt.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

16 (Continued)

Notes payable to bank consists of the following at June 30, 2007:

The University has three revolving lines of credit in the aggregate amount of $4,000,000, which expire in February 2008. Use of the borrowings is used for general operating expenses. Borrowings pursuant to the revolving lines of credit bear interest at a fully floating variable interest rate equal to each banks’ prime lending rate. The lines have a commitment fee of 0.125%. As of June 30, 2007, the University had a balance of $2,000,000 borrowed against one of these lines which was repaid in September 2007. The interest rate on the amount outstanding as of June 30, 2007 was 8.25%.

(12) Related Party Transactions

In March, 2006, the University entered into a 30 year lease agreement with the Oak Tree Foundation (Foundation), an Oregon nonprofit corporation formed in 1994 to benefit Pacific University by providing financing and management assistance in on-campus and off-campus housing for University students, to lease a newly constructed residence hall. The Foundation has leased from the University the ground on which the residence hall is being constructed for a term of 99 years. For accounting purposes, under Emerging Issues Task Force (EITF) 96-21, Implementation Issues in Accounting for Leasing Transactions involving Special-Purpose Entities the University recorded the construction in progress and the corresponding financing obligation totaling $10.7 million in its June 30, 2006 statement of financial position. In 2007, under SFAS No. 98, Accounting for Leases, the University has met the criteria to account for this transaction as a sale-leaseback and has therefore removed the construction in progress and corresponding financial obligation from its statement of position at June 30, 2007.

The Foundation is governed by a seven member board of which there are four independent members and three members from the University. In accordance with Statement of Position 94-3, Reporting of Related Entities by Not-for-Profit Organizations, the University is not required to consolidate the Foundation but has chosen to disclose summarized financial data.

The Foundation’s financial data at June 30, 2007 is as follows:

Total assets $ 45,041,159 Total liabilities 44,711,426 Net assets 329,733 Total revenues 1,043,971 Total expenses 628,863

In June 2007, the University entered into a second 30 year lease agreement with the Oak Tree Foundation, to lease a future constructed residence hall. The Foundation has leased from the University the ground on which the residence hall will be constructed for a term of 99 years.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

17 (Continued)

The future aggregate minimum operating lease payments under the 2006 lease agreement are as follows. Additionally, the following includes the 2007 lease commitment:

Year ending June 30:2008 $ 1,114,420 2009 2,187,003 2010 2,401,519 2011 2,401,519 2012 2,401,519 Thereafter 59,323,807

$ 69,829,787

The future aggregate minimum lease receipts under both 99 year ground lease agreements are as follows:

Year ending June 30:2008 $ 81,275 2009 83,713 2010 86,219 2011 88,807 2012 91,466 Thereafter 24,261,490

$ 24,692,970

(13) Expenses by Function

Expenses by functional classification after allocating depreciation, operation and maintenance of plant, and interest are as follows for the year ended June 30, 2007:

Instruction $ 24,671,197 Research 577,167 Public service 208,314 Academic support 8,436,840 Clinics 3,355,548 Student services 7,041,802 Institutional support 8,798,715 Auxiliary 5,619,368

$ 58,708,951

(14) Postretirement Benefits Other Than Pensions

The University currently provides certain of its retired employees with health care benefits under a University sponsored defined benefit retiree health plan (the Plan). Effective June 1, 1997, the University amended the Plan such that employees hired after that date will not receive benefits under the Plan and prior eligible employees will receive a benefit capped at the fiscal 1997 premium cost, with the remainder

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

18 (Continued)

being paid by employees. Employees become eligible for these benefits as they retire from active employment. The Plan contains other cost sharing features such as coinsurance and is unfunded.

As discussed in note 2(q), effective June 30, 2007, the University adopted SFAS No. 158.

The following sets forth the plan’s status at the valuation date of June 30, 2007 and amounts recognized in the University’s statement of activities as of June 30, 2007:

Net periodic postretirement benefit cost:Service cost – benefits earned during year $ 27,467 Interest cost on accumulated postretirement benefits 42,404 Amortization of Plan change (32,360)

Net periodic postretirement benefit cost $ 37,511

Unfunded status and related statement of financial position amounts for the postretirement health care plan at June 30, 2007:

Accrued postretirement benefits:Retirees $ (33,501) Active Plan participants (673,239)

Accrued postretirement benefit cost $ (706,740)

The discount rate and health care cost trend rate used in determining the accumulated postretirement benefits at June 30, 2007 was 6% and 0%, respectively. The 0% associated with health care cost trend results from the premium cap.

The following lists postretirement benefit payments, which reflect expected future service. Payments expected to be paid over the next ten years are as follows:

2008 $ 88,560 2009 99,360 2010 101,520 2011 103,680 2012 108,000 2013-2017 494,640

$ 995,760

The University expects to contribute approximately $88,560 to the postretirement benefit plan in 2008.

(15) Funds Held in Trust by Others

Funds held in trust by others represent assets held and administered by trustees other than the University. The University as a beneficiary derives income or a residual interest from the assets of such funds after the passage of time or occurrence of specified events. When the University is notified that funds have been put

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

19 (Continued)

in a trust held by others and is designated as beneficiary, contribution income is recognized as an increase in temporarily or permanently restricted net assets, depending on the nature of restriction imposed by the donor, at the estimated present value of future cash flows to be received by the University.

The University has an irrevocable interest in seven trusts held by others that will be held in perpetuity with the University receiving income distributions annually. The fair value at June 30, 2007, was $18,453,822. In addition, there are three trusts held by others in life income annuities with a fair value of $890,138.

(16) Net Asset Borrowings

Net asset borrowings at June 30, 2007 represent temporarily unfunded transfers which will be eliminated principally through collections of accounts and pledges receivable, appropriation of other receipts, or charges to “operations”. University management believes that the University has the ability and intent to repay the net asset borrowings.

(17) Pension Plan

The University participates in a contributory defined contribution retirement plan covering substantially all full time personnel. Employee contributions to the plan are matched monthly by the University at the rate of up to 7% of the participating employees’ monthly compensation. Aggregate pension expense for the year ended June 30, 2007 was $1,629,947.

(18) Leases

(a) Operating Leases and Lease Commitments

The University leases office space for various instructional activities and certain equipment. Rental expense amounted to $846,104 for the year ended June 30, 2007.

The future aggregate minimum operating lease payments (including 2006 related party lease) are as follows:

Year ending June 30:2008 $ 1,954,868 2009 2,055,220 2010 1,662,279 2011 1,443,161 2012 1,352,379 Thereafter 26,134,160

$ 34,602,067

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

20 (Continued)

The future aggregate minimum lease payments on the 2007 related party lease commitment are as follows:

Year ending June 30:2008 $ — 2009 816,312 2010 971,532 2011 1,070,124 2012 1,131,912 Thereafter 33,359,976

$ 37,349,856

The University is leasing its bookstore to Barnes and Noble. Barnes and Noble is providing all bookstore services for the University under the terms of a lease agreement ending in November 2016. The University sold the bookstore inventory at cost to Barnes and Noble with the agreement that Barnes and Noble will sell the inventory back to the University at cost at the end of this lease agreement. During the term of the lease, Barnes and Noble will pay the University a percentage of bookstore sales for the use of the University’s property. The University received $87,323 in the current year.

(b) Capital Leases

The University has entered into two new capital lease agreements in the current year to acquire equipment totaling $270,027. The equipment was recorded at its present value at the inception of each lease. The total equipment purchase is included in the University’s assets under property, plant and equipment. It is also included in footnote 9 under cost of furniture and equipment.

The future minimum lease payments under the leases are as follows:

Year ending June 30:2008 $ 464,822 2009 461,042 2010 419,810 2011 311,613 2012 31,735 Thereafter —

Total minimum lease payment 1,689,022

Less amount representing interest (198,251) Present value of net minimum lease payment $ 1,490,771

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

21 (Continued)

(19) Liquidity

Summarized information regarding the classification of assets and liabilities of the University as of June 30, 2007 is as follows:

Total current assets $ 12,468,390 Total long-term assets 149,722,002

Total assets $ 162,190,392

Total current liabilities $ 12,095,674 Total long-term liabilities 58,725,460

Total liabilities 70,821,134

Net assets 91,369,258

Total liabilities andnet assets $ 162,190,392

(20) Commitments and Contingencies

The University receives and expends monies under federal grant programs and is subject to audits by cognizant governmental agencies. Management believes that any liabilities arising from such audits will not have a material affect on the University.

In 2006, the University entered into two construction contracts, which totaled $27,845,931 in contractor fees. As of June 30, 2007, the University had remaining commitments of $3,838,799 related to these two construction projects, which are in the process of completion.

In 2006, the University entered into a construction contract with Walsh Construction for the development and construction of the Berglund Studies Building. The contract was for approximately one and half years at an estimated cost of $9,456,600. As of June 30, 2007, the University has remaining commitments of $3,277,049 related to this construction project which is in the process of completion.

(21) Self-Insurance Consortium

The University has placed certain of its medical and dental insurance coverage with Pioneer Educators Health Trust (PEHT), formulated by seven similar western colleges and universities for the purpose of providing medical and dental insurance to higher education institutions. Under the agreement, member institutions are required to make contributions to the fund at such times and in an amount as determined by the Trustees for the various benefit programs sufficient to provide the benefits, pay the administrative expenses of the Plan which are not otherwise paid by the University directly, and to establish and maintain a minimum reserve as determined by the Trustees. In no event shall the total contributions paid by any college in any month to the fund be less than the amount of contributions to the cost of the benefit program that employees of such college have paid during the period.

PACIFIC UNIVERSITY

Notes to Financial Statements

June 30, 2007

22

In the event losses of PEHT exceed its capital and secondary coverages, the maximum contingent liability exposure to the University is approximately $295,000. This exposure will fluctuate based on factors including changes in actuarial assumptions, medical trend rates and reinsurance amounts. The level of reinsurance is not expected to fluctuate significantly in the future.

(22) Accounting for Conditional Asset Retirement Obligations

In March 2005, the Financial Accounting Standards Board (FASB) issued Interpretation No. 47 (FIN 47), Accounting for Conditional Asset Retirement Obligations, an interpretation of FASB Statement No. 143 (SFAS 143). Under FIN 47, costs related to legal obligations to perform certain activities in connection with the retirement, disposal, or abandonment of assets are required to be accrued. The University adopted FIN 47 as of July 1, 2005.

In 2006, the University identified asbestos abatement as a conditional asset retirement obligation. Asbestos abatement costs were estimated using a per square foot estimate. The University recorded site improvements of $387,445, accumulated depreciation of $277,512, an asset retirement obligation of $1,233,521, and a cumulative effect of change in accounting principle of $1,123,088. The estimated liability is determined annually on June 30 to reflect remediation efforts and updated costs for abatement. The estimated conditional asset retirement obligation is $1,264,793 at June 30, 2007.