Embed Size (px)

Citation preview

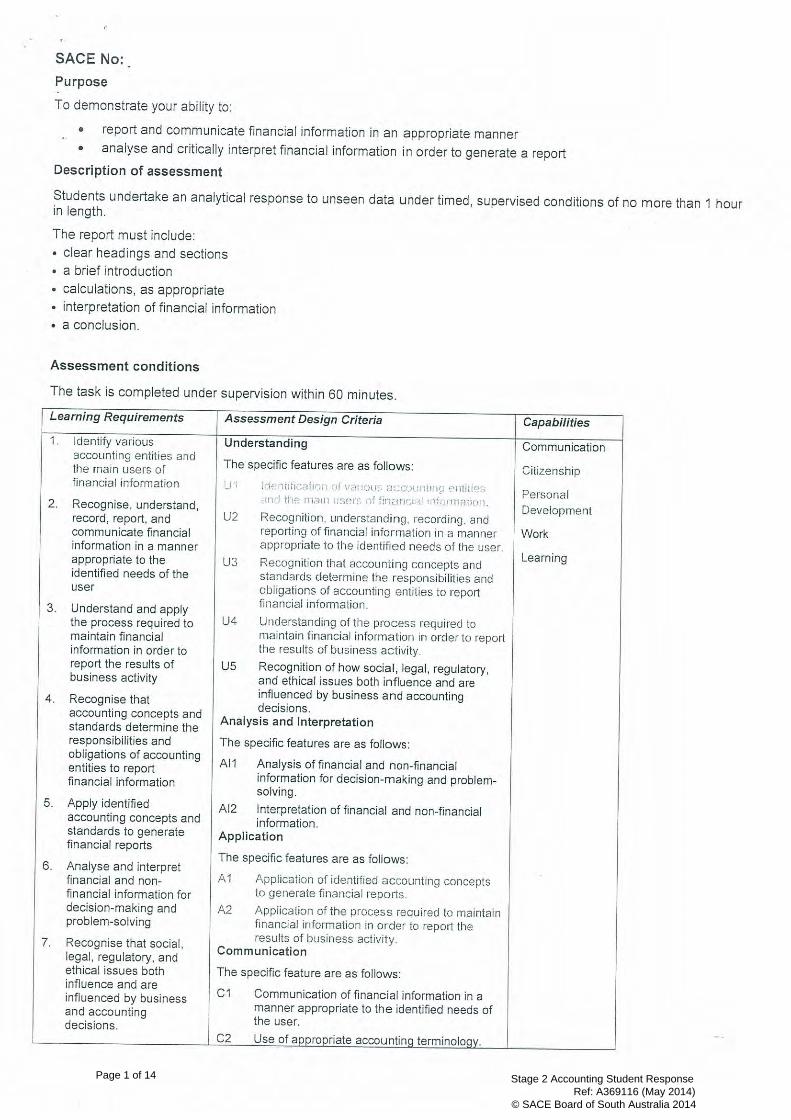

Page 1 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

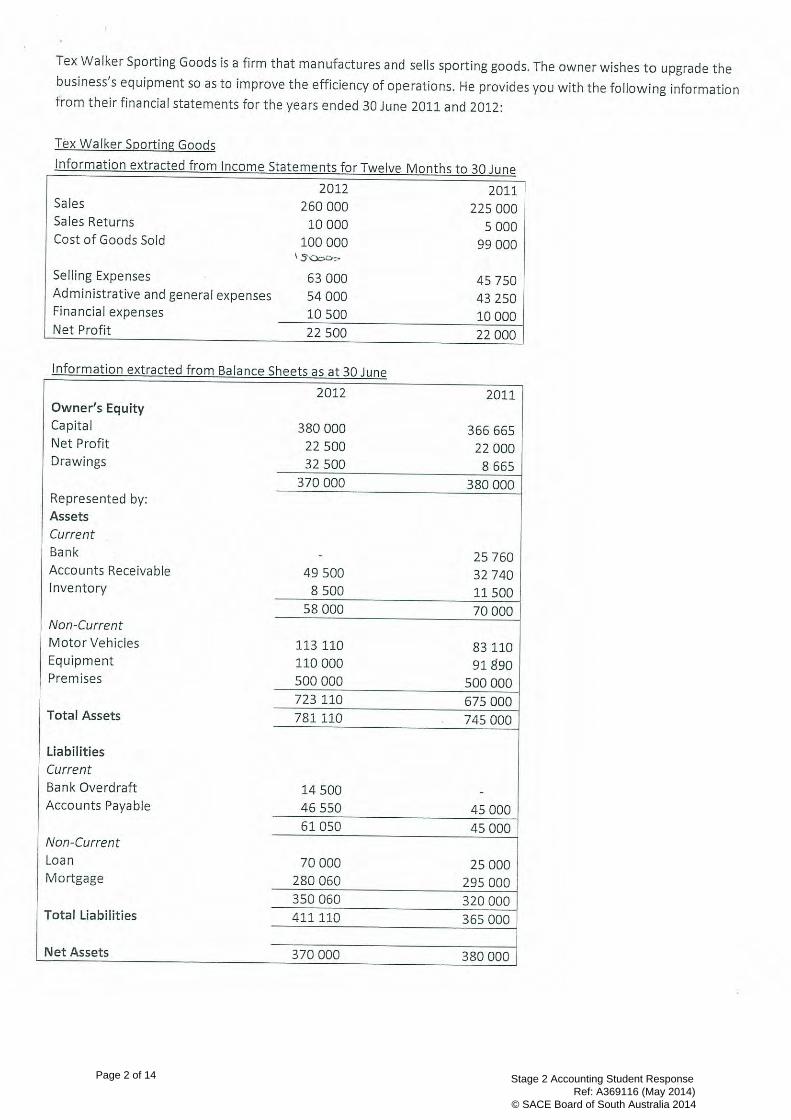

Page 2 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

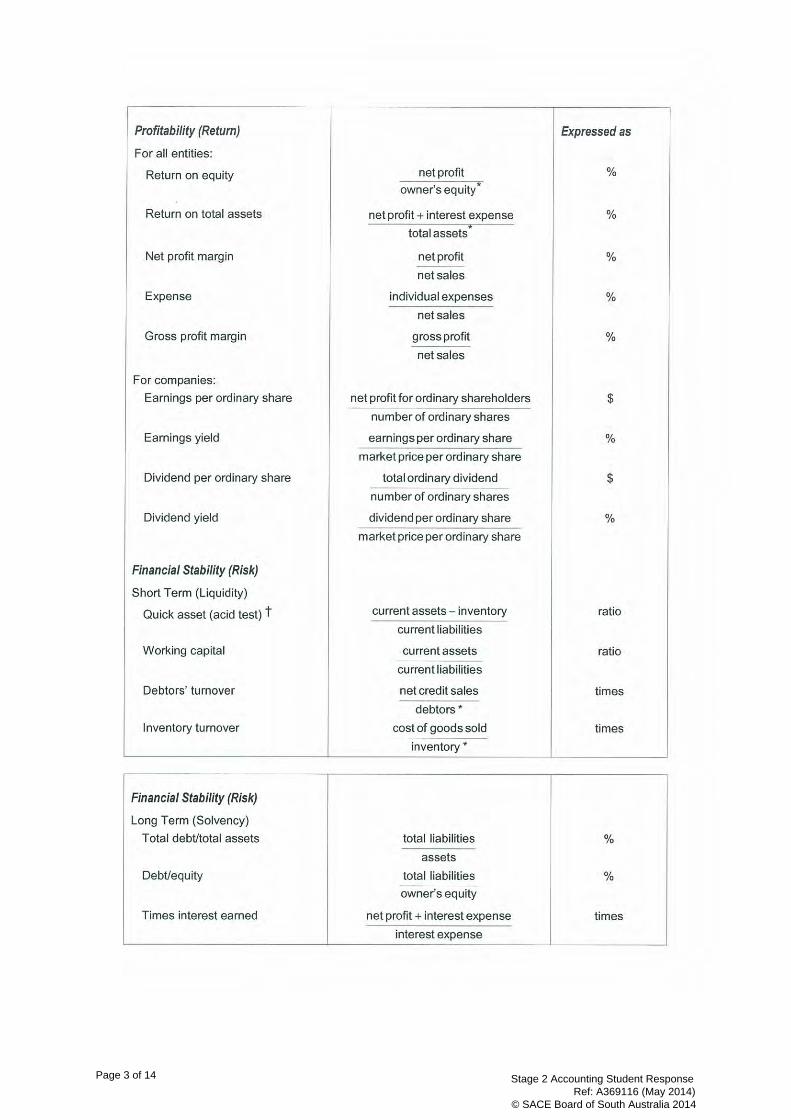

Page 3 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

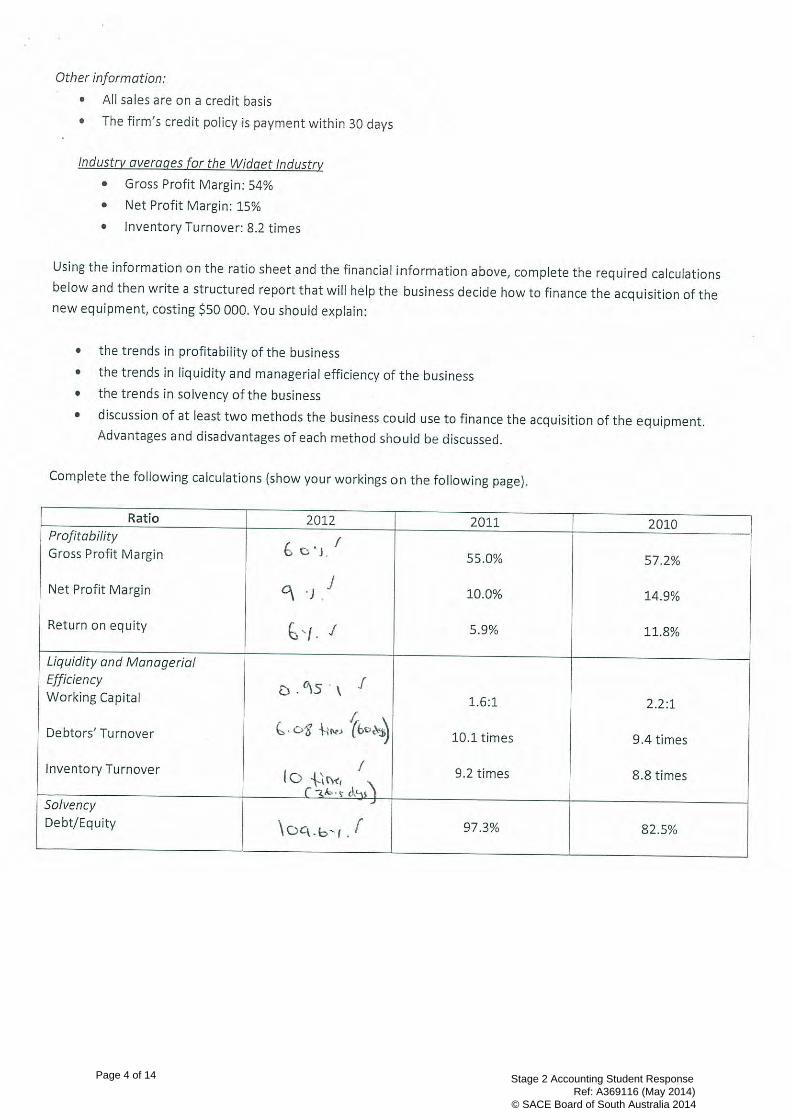

Page 4 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

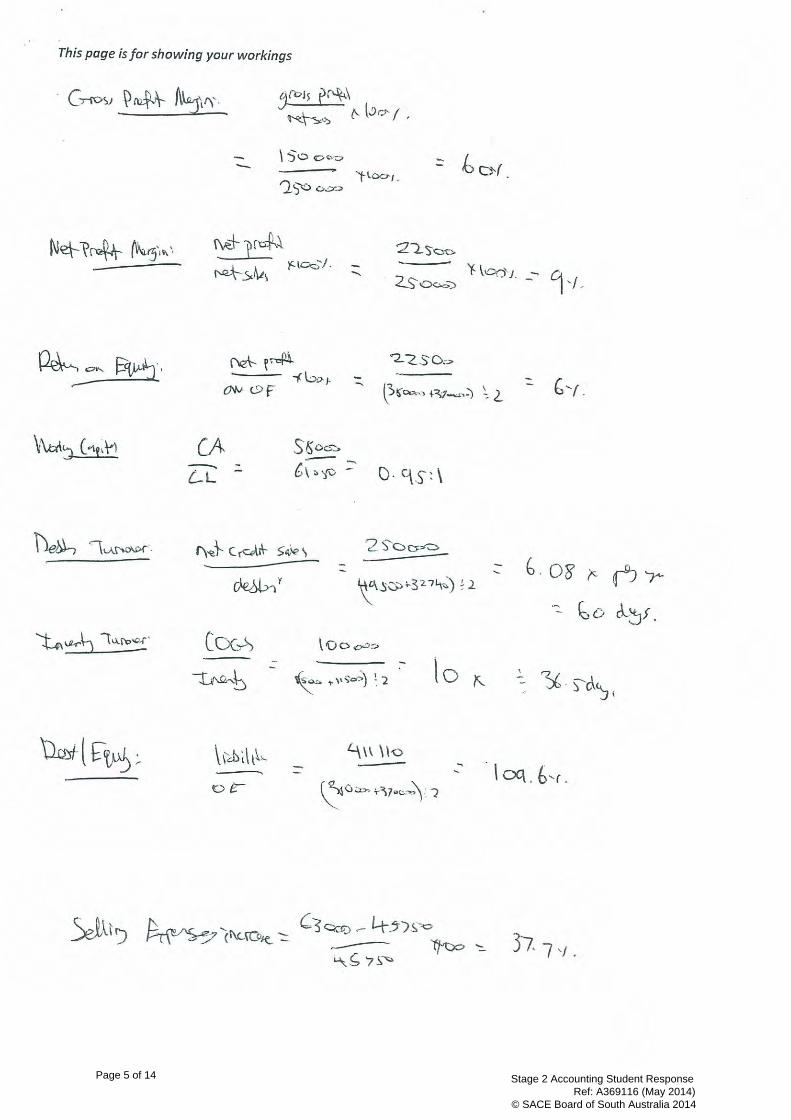

Page 5 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

Page 6 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

Page 7 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

Page 8 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

Page 9 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

Page 10 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

Page 11 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

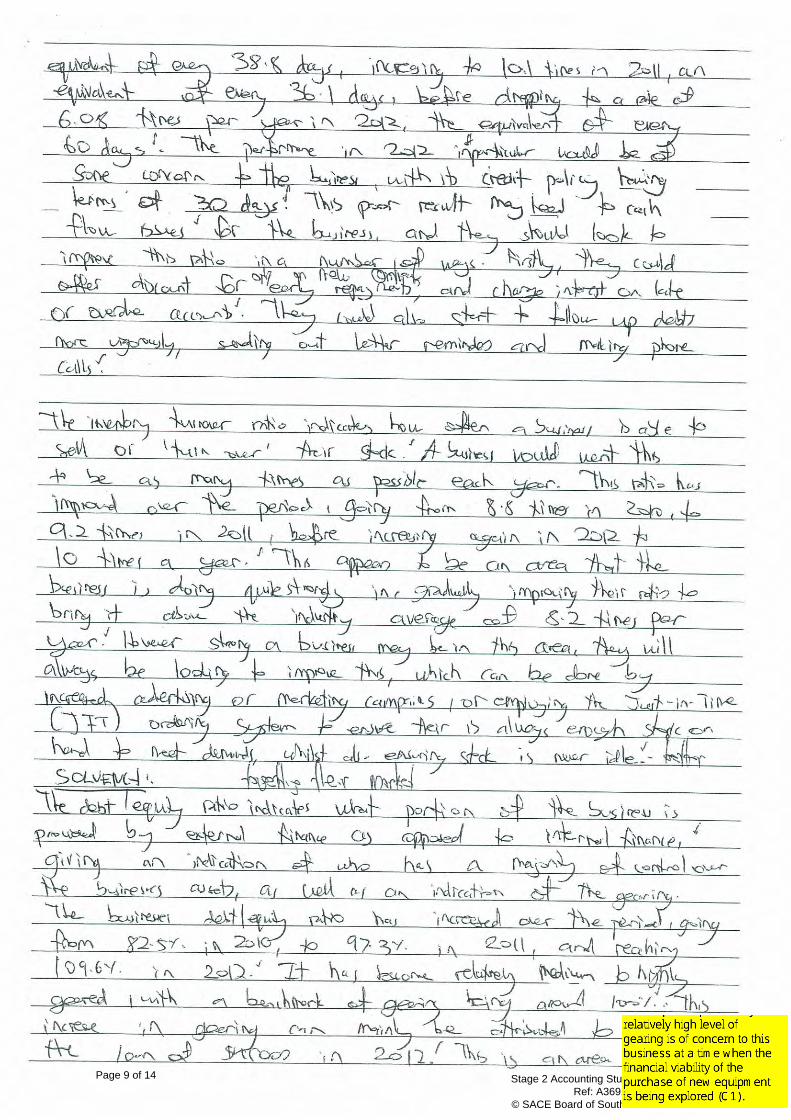

Assessment Comments Assessment Type 2: Report Grade: A+ This Task is an analytical response to unseen data, completed under timed conditions within 60 minutes. Understanding The Report shows ‘insightful and well-informed’ understanding of the business situation of the sporting goods firm for whom this Report is ostensibly written, and how the strategies to address the issue of the acquisition of new equipment need take into account legal, regulatory and financial issues (U5). The likely effects of the decision to fund the purchase of new equipment are considered in terms of the financial data generated through the initial calculations and the likely outcomes in terms of the solvency of the business. Analysis and Interpretation There is ‘astute analysis’ of financial information evident in the Report (AI1). All ratios are completed correctly. There is precise discussion of what each ratio means with comparison to industry averages as well as an interpretation of the data to show how the business can improve its situation. For example, discussion of the gross profit margin includes information about how the business might improve this ratio through an increase in net sales or a decrease in the cost of goods sold. This Report also identifies the ‘worrying’ trend of an increase in gross profit margin with a corresponding decrease in net profit margin, suggesting the need to investigate operating expenses (AI1 and 2). This pattern is followed in the discussion of each ratio indicating a ‘perceptive and critical’ understanding of the implications of the ratios, the capacity to make comparisons across financial report periods and with industry averages, the ability to identify trends and also point to areas of concern for the business. The Report also refers back to the balance sheet and income statement to support the argument (AI 1 and 2). Communication The Report is structured coherently under headings to enable the ‘astute communication of financial information’ in a manner ‘most appropriate’ in this case to the needs of the sporting goods firm (C1). The use of accounting terminology throughout the Report is ‘highly appropriate’ and the information is expressed in such a way that the meanings extracted from the financial data and their implications for the business are expressed clearly and professionally (C2). Overall Grade A+ This Report is very strong against all performance standards.

Page 12 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

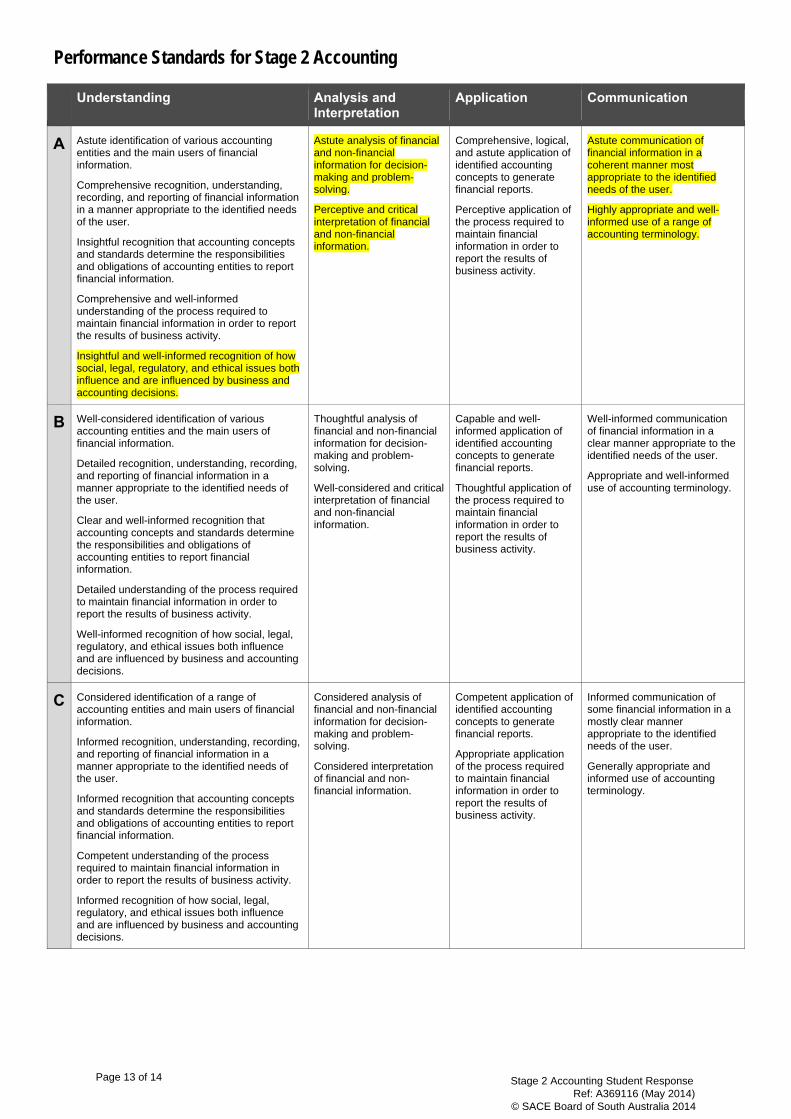

Performance Standards for Stage 2 Accounting

Understanding Analysis and Interpretation

Application Communication

A Astute identification of various accounting entities and the main users of financial information.

Comprehensive recognition, understanding, recording, and reporting of financial information in a manner appropriate to the identified needs of the user.

Insightful recognition that accounting concepts and standards determine the responsibilities and obligations of accounting entities to report financial information.

Comprehensive and well-informed understanding of the process required to maintain financial information in order to report the results of business activity.

Insightful and well-informed recognition of how social, legal, regulatory, and ethical issues both influence and are influenced by business and accounting decisions.

Astute analysis of financial and non-financial information for decision-making and problem-solving.

Perceptive and critical interpretation of financial and non-financial information.

Comprehensive, logical, and astute application of identified accounting concepts to generate financial reports.

Perceptive application of the process required to maintain financial information in order to report the results of business activity.

Astute communication of financial information in a coherent manner most appropriate to the identified needs of the user.

Highly appropriate and well-informed use of a range of accounting terminology.

B Well-considered identification of various accounting entities and the main users of financial information.

Detailed recognition, understanding, recording, and reporting of financial information in a manner appropriate to the identified needs of the user.

Clear and well-informed recognition that accounting concepts and standards determine the responsibilities and obligations of accounting entities to report financial information.

Detailed understanding of the process required to maintain financial information in order to report the results of business activity.

Well-informed recognition of how social, legal, regulatory, and ethical issues both influence and are influenced by business and accounting decisions.

Thoughtful analysis of financial and non-financial information for decision-making and problem-solving.

Well-considered and critical interpretation of financial and non-financial information.

Capable and well-informed application of identified accounting concepts to generate financial reports.

Thoughtful application of the process required to maintain financial information in order to report the results of business activity.

Well-informed communication of financial information in a clear manner appropriate to the identified needs of the user.

Appropriate and well-informed use of accounting terminology.

C Considered identification of a range of accounting entities and main users of financial information.

Informed recognition, understanding, recording, and reporting of financial information in a manner appropriate to the identified needs of the user.

Informed recognition that accounting concepts and standards determine the responsibilities and obligations of accounting entities to report financial information.

Competent understanding of the process required to maintain financial information in order to report the results of business activity.

Informed recognition of how social, legal, regulatory, and ethical issues both influence and are influenced by business and accounting decisions.

Considered analysis of financial and non-financial information for decision-making and problem-solving.

Considered interpretation of financial and non-financial information.

Competent application of identified accounting concepts to generate financial reports.

Appropriate application of the process required to maintain financial information in order to report the results of business activity.

Informed communication of some financial information in a mostly clear manner appropriate to the identified needs of the user.

Generally appropriate and informed use of accounting terminology.

Page 13 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014

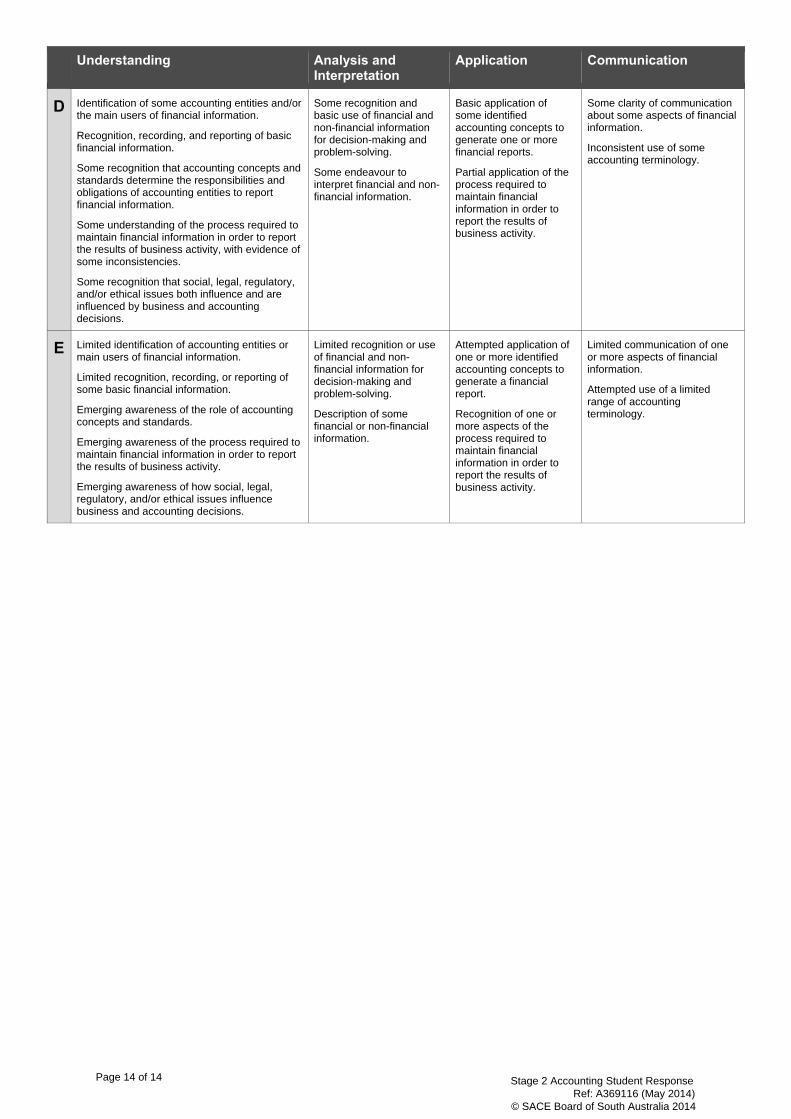

Understanding Analysis and Interpretation

Application Communication

D Identification of some accounting entities and/or the main users of financial information.

Recognition, recording, and reporting of basic financial information.

Some recognition that accounting concepts and standards determine the responsibilities and obligations of accounting entities to report financial information.

Some understanding of the process required to maintain financial information in order to report the results of business activity, with evidence of some inconsistencies.

Some recognition that social, legal, regulatory, and/or ethical issues both influence and are influenced by business and accounting decisions.

Some recognition and basic use of financial and non-financial information for decision-making and problem-solving.

Some endeavour to interpret financial and non-financial information.

Basic application of some identified accounting concepts to generate one or more financial reports.

Partial application of the process required to maintain financial information in order to report the results of business activity.

Some clarity of communication about some aspects of financial information.

Inconsistent use of some accounting terminology.

E Limited identification of accounting entities or main users of financial information.

Limited recognition, recording, or reporting of some basic financial information.

Emerging awareness of the role of accounting concepts and standards.

Emerging awareness of the process required to maintain financial information in order to report the results of business activity.

Emerging awareness of how social, legal, regulatory, and/or ethical issues influence business and accounting decisions.

Limited recognition or use of financial and non-financial information for decision-making and problem-solving.

Description of some financial or non-financial information.

Attempted application of one or more identified accounting concepts to generate a financial report.

Recognition of one or more aspects of the process required to maintain financial information in order to report the results of business activity.

Limited communication of one or more aspects of financial information.

Attempted use of a limited range of accounting terminology.

Page 14 of 14 Stage 2 Accounting Student Response Ref: A369116 (May 2014) © SACE Board of South Australia 2014