Embed Size (px)

Citation preview

(Page 1 of 4)

J.D. Power Reports: Gen Z Has Arrived. Is Your Bank Ready? Overall Retail Banking Satisfaction is Up, Mobile and ATM Satisfaction Declines WESTLAKE VILLAGE, Calif.: 30 April 2015 — Gen Z,1 which comprises about one-fourth of the U.S. population, is entering adulthood and creating new challenges and opportunities for retail banks of all sizes to acquire them as customers, build their loyalty and capture a larger share of wallet as they age; however, banks will need to understand what drives satisfaction among this generational group. Additionally, while overall satisfaction has improved from 2014, satisfaction with mobile and ATM features has slightly declined raising a red flag about retail banks’ approach to technology, according to the J.D. Power 2015 U.S. Retail Banking Satisfaction StudySM released today. The 10th annual customer satisfaction study is the longest-running and most in-depth survey of the retail banking industry, with more than 80,000 consumers evaluating various aspects of their banking experience. The study measures satisfaction in six factors (listed in alphabetical order): account information; channel activities; facility; fees; problem resolution; and product offerings. Channel activities include six subfactors (listed in alphabetical order): ATM; branch; call center; IVR; mobile; and website. Banks are ranked based on overall customer satisfaction in each of the following regions: California, Florida, Mid-Atlantic, Midwest, New England, North Central, Northwest, South Central, Southeast, Southwest and Texas. Satisfaction is measured on a 1,000-point scale. Gen Z and Retail Banking:

Satisfaction among Gen Z customers (797) is higher than among Gen Y and Gen X customers (781 and 778, respectively.) Additionally, overall satisfaction among Gen Z customers of big banks2 (807) is higher than among Gen Z customers of regional banks (796) and midsize banks (769).

Among Gen Z customers, digital transactions are shifting from website to mobile. A higher percentage of Gen Z customers use mobile (38%) than the average use across all other generational groups (19%), and Gen Z uses mobile more often than other generations (48 times per year vs. 39 times).

Surprisingly, branch usage among Gen Z customers is on par with that of Gen X and Gen Y, as 76 percent of Gen Z customers have visited a branch in the past 12 months, compared with 72 percent of Gen Y customers and 74 percent of Gen X customers. Gen Z customers who visit a branch average 12 times per year, compared with Gen Y and Gen X who visit 11 times and 12 times, respectively.

1 J.D. Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y

(1977-1994); Gen Z (born after 1995). 2 Big banks are defined as the six largest financial institutions based on total deposits as reported by the FDIC, averaging $180

billion and above. Regional banks are defined as those with between $180 billion and $33 billion in deposits. Midsize banks are defined as those with between $33 billion and $2 billion in deposits.

Among Gen Z customers, overall satisfaction is highest with big banks, compared with regional and midsize banks, driven by satisfaction in the facility and product offering factors, and the ATM, branch, mobile and website subfactors.

Despite lower satisfaction, midsize and regional banks are capturing a greater share of Gen Z customers than they are with Gen X. Among midsize and larger banks, 18 percent of Gen Z customers indicate that their primary bank is a midsize bank, compared to 13 percent for Gen Y. More than one-fourth (28%) of Gen Z customers indicate their primary bank is regional bank, compared to 24 percent for Gen Y.

Satisfying Gen Z has a tremendous impact on advocacy. Highly satisfied Gen Z customers (satisfaction scores of 800 and higher) are five times more likely to say they “definitely will” recommend their bank than those with medium or low satisfaction (scores below 800), who say the same (68% vs. 12%, respectively).

“It is not surprising that Gen Z is satisfied with website and mobile at big banks, but they are also satisfied with the in-person experience at big banks,” said Jim Miller, senior director of banking at J.D. Power. “There is a common misconception that younger customers aren’t using the branch, but they use it about the same as Gen X and Y. Midsize and regional banks risk losing the Gen Z customers to big banks if they can’t meet their needs regarding digital and in-person interactions. There needs to be a seamless experience across all channels. The first step for retail banks is to understand what is important to Gen Z and what drives their satisfaction and loyalty.” Overall Satisfaction Up, Mobile and ATM Satisfaction Declines

Overall satisfaction with retail banks has improved to 790, an increase of 5 points from 2014. The increase is largely due to an increase in fee satisfaction and fewer customers experiencing a problem or having a complaint. Fee satisfaction has increased by 15 points to 684 from 669, with few customers indicating a change to their fees (9%) and only 14 percent of customers indicating they paid a monthly service charge during the past 12 months. In 2015, 14 percent of customers have experienced a problem or had a complaint, down from 16 percent in 2014 and 24 percent in 2010. Among customers who do experience a problem in 2015, problem resolution satisfaction has increased to 630, up by 10 points from 2014. Mobile satisfaction, which has increased each year since the sub-factor was included in the study in 2012, has declined by 3 points in 2015 to 837 from 840 in 2014. For big banks, this decline is largely due to a 6-point drop in mobile scores year over year (845 vs. 839, respectively), based on lower customer ratings in clarity of information and ease of navigating.

Despite increasing functionality offered in mobile, satisfaction has dropped as fewer customers indicate that they completely understand mobile (47% vs. 57% in 2014).

Among customers who completely understand mobile, 46 percent say they “definitely will not” switch banks, compared with the 34 percent of customers who partially understand mobile who say the same.

ATM satisfaction has declined by 6 points to 837 from 843 in 2014. ATM customer usage dropped to 65 percent from 70 percent in 2014 as use of cash has declined and the role of mobile as a banking tool has increased. Although customers indicate having more ATM features in 2015 than in 2014, they are less satisfied with the range of services the ATM can perform and with ease of use of ATMs.

“Satisfaction with mobile banking and ATMs is dropping as customer expectations are outpacing technology improvements,” said Miller. “Customers expect to be able to perform more functions on the same device this year than they did last year and that it will be easier to use. Success will not be driven by

just adding more bells and whistles, but by balancing functionality with ease of use and then clearly communicating features and benefits to customers.”

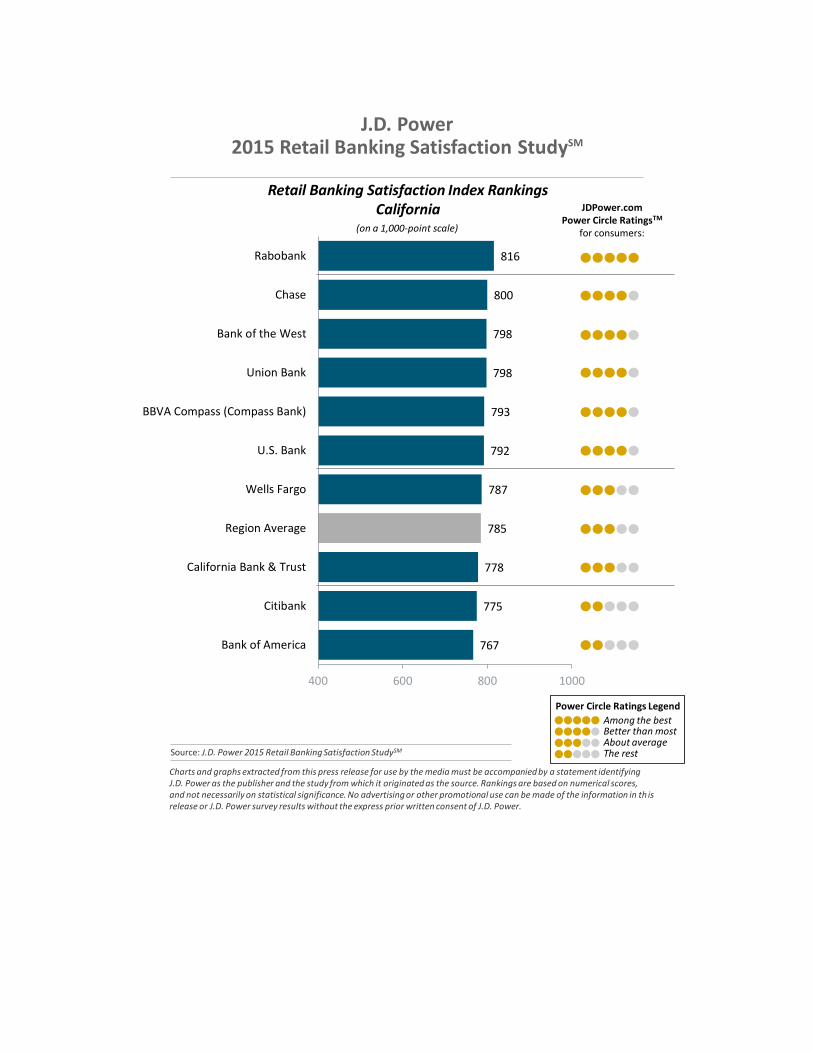

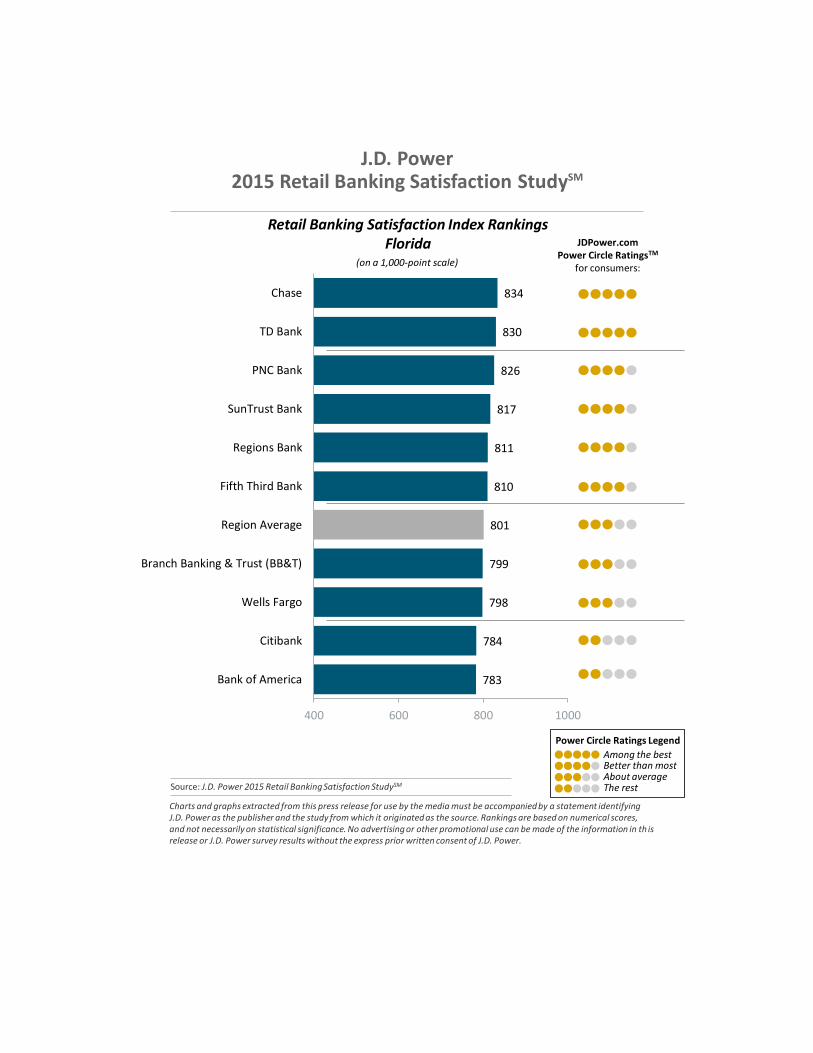

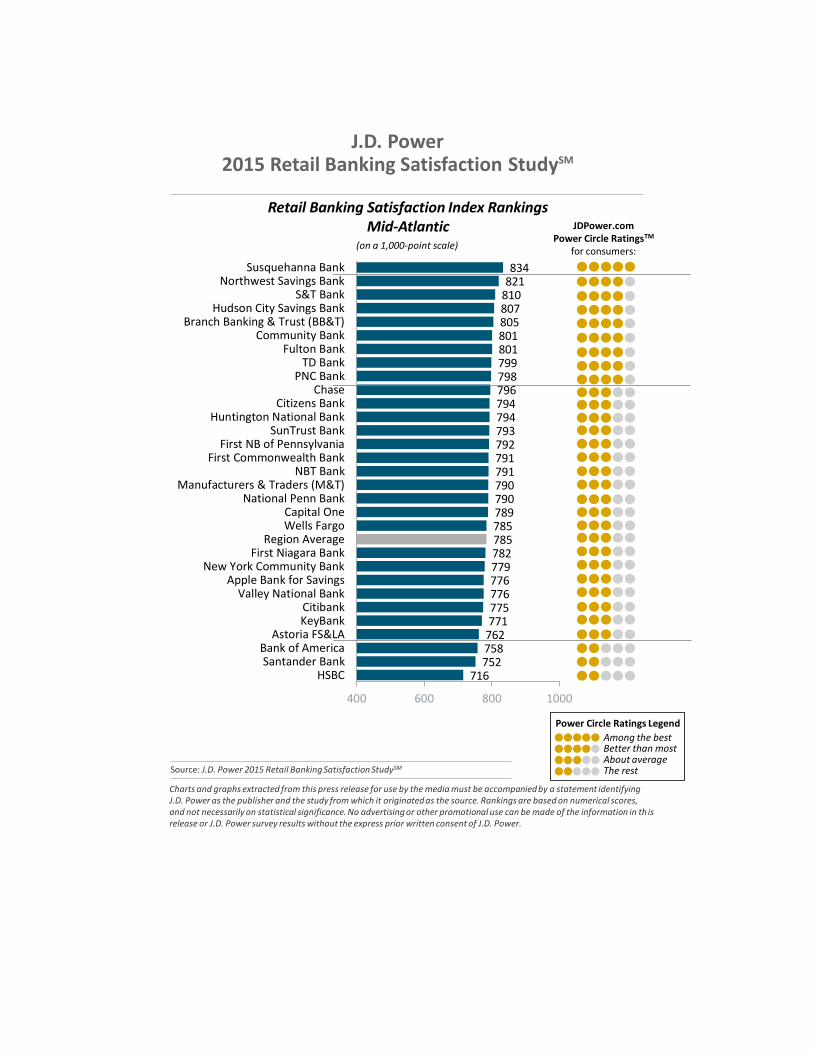

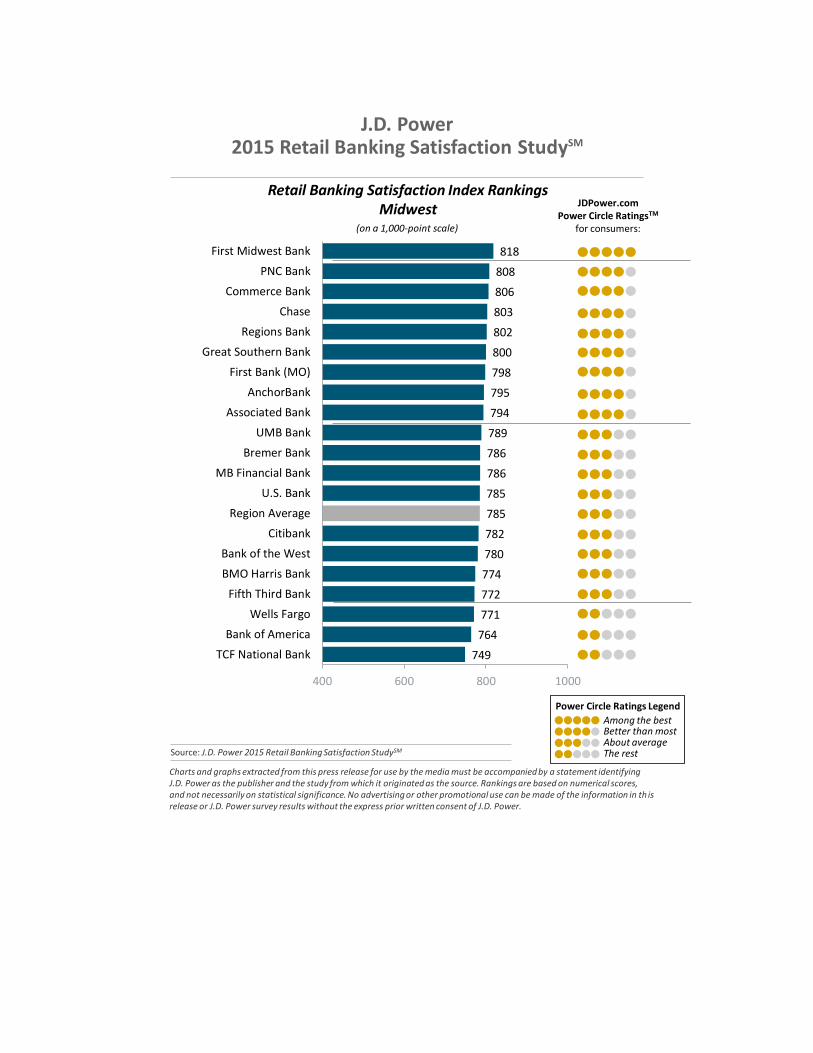

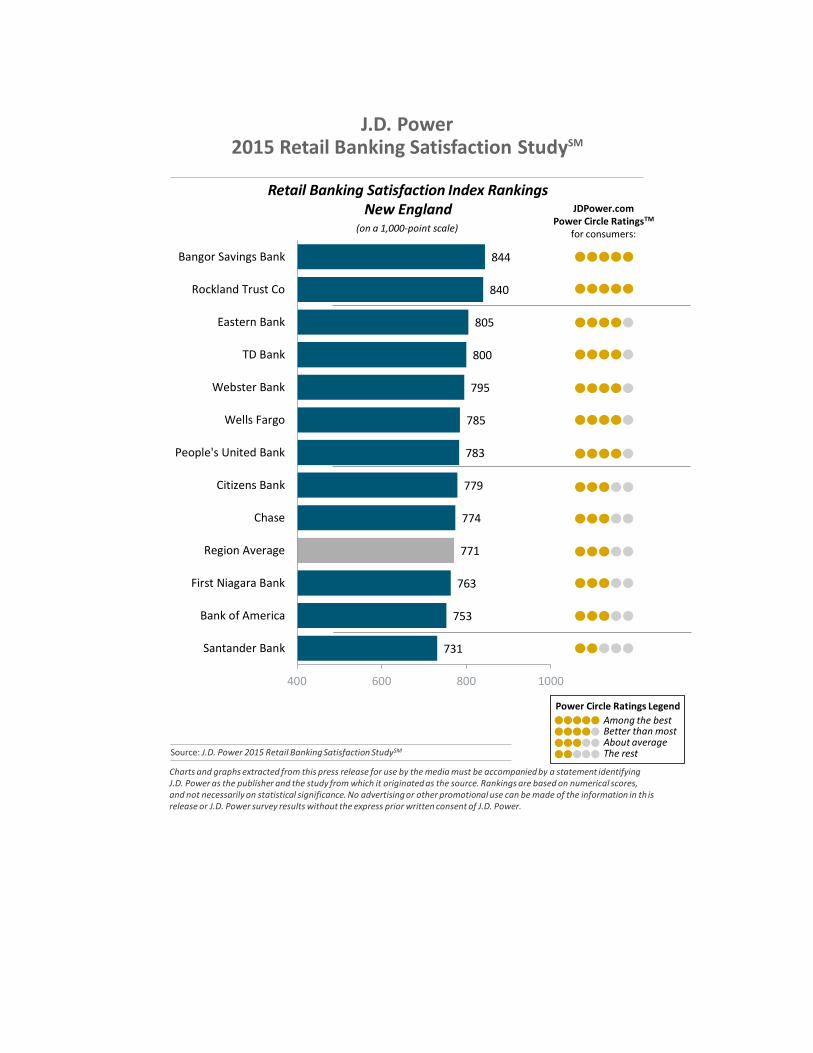

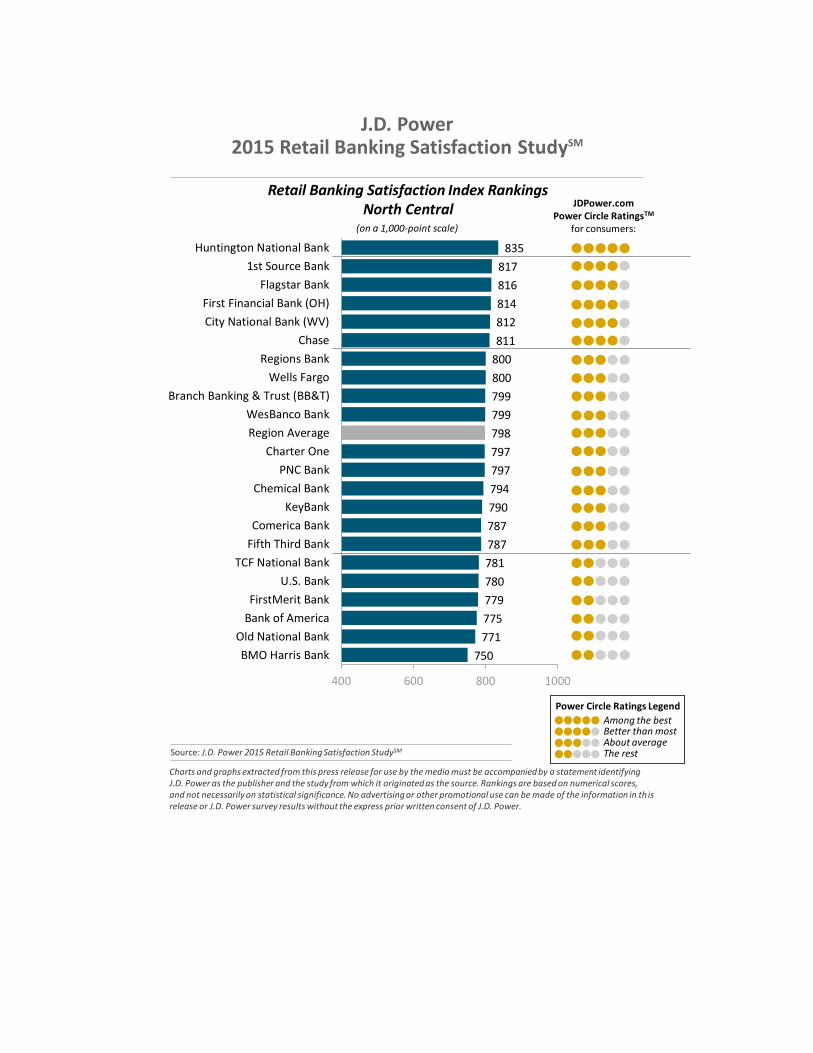

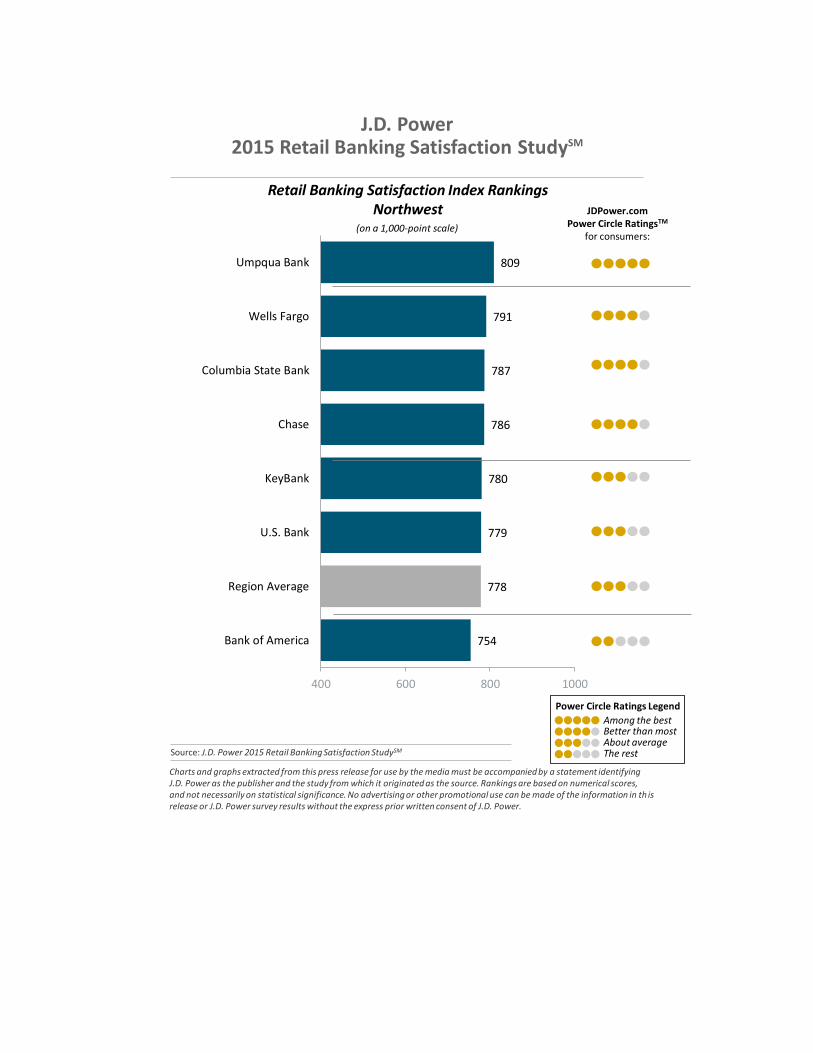

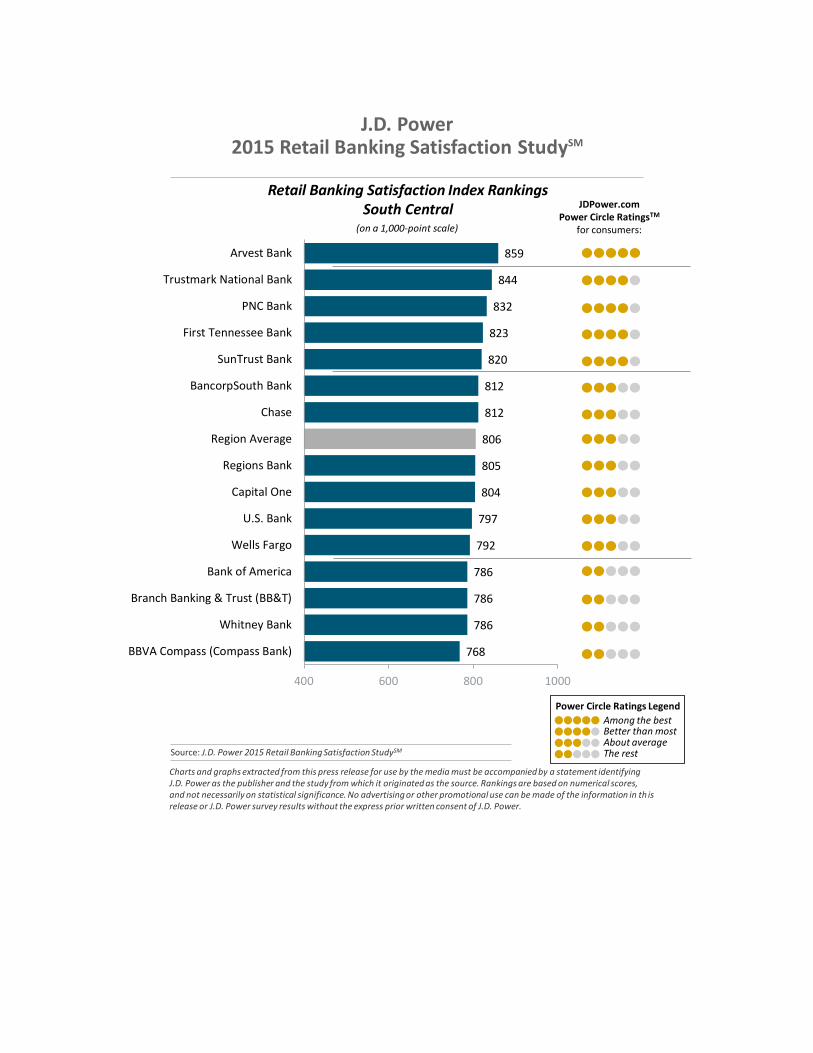

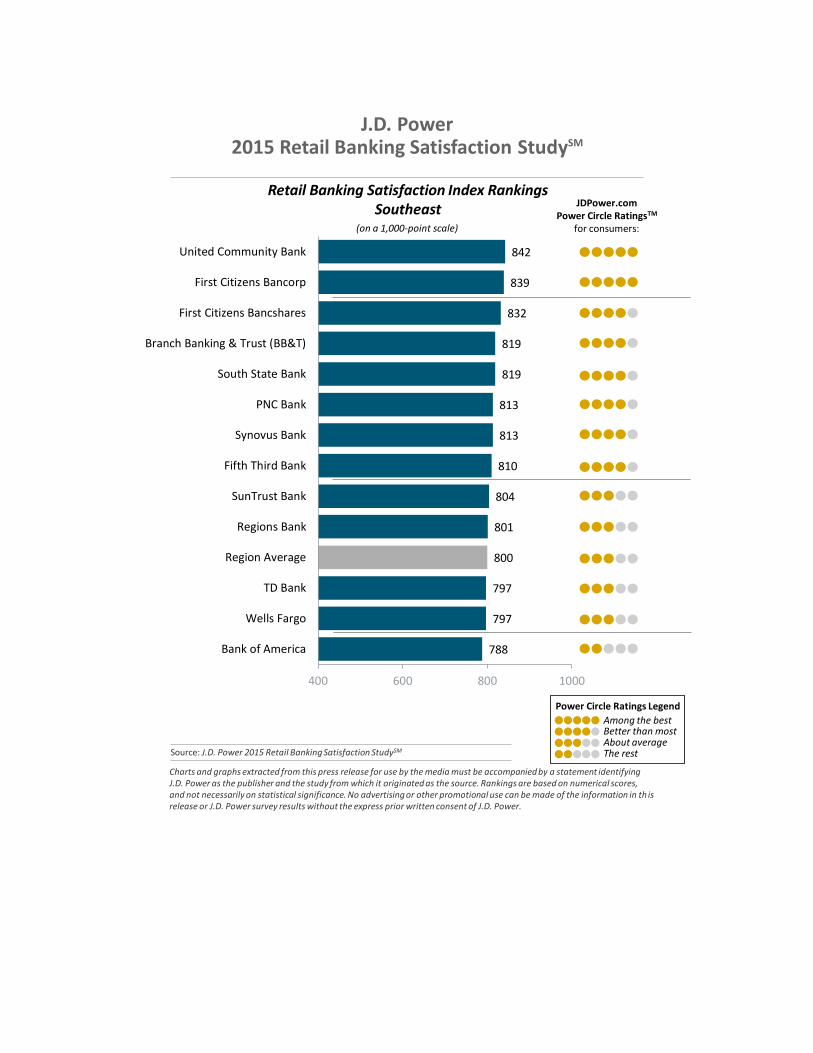

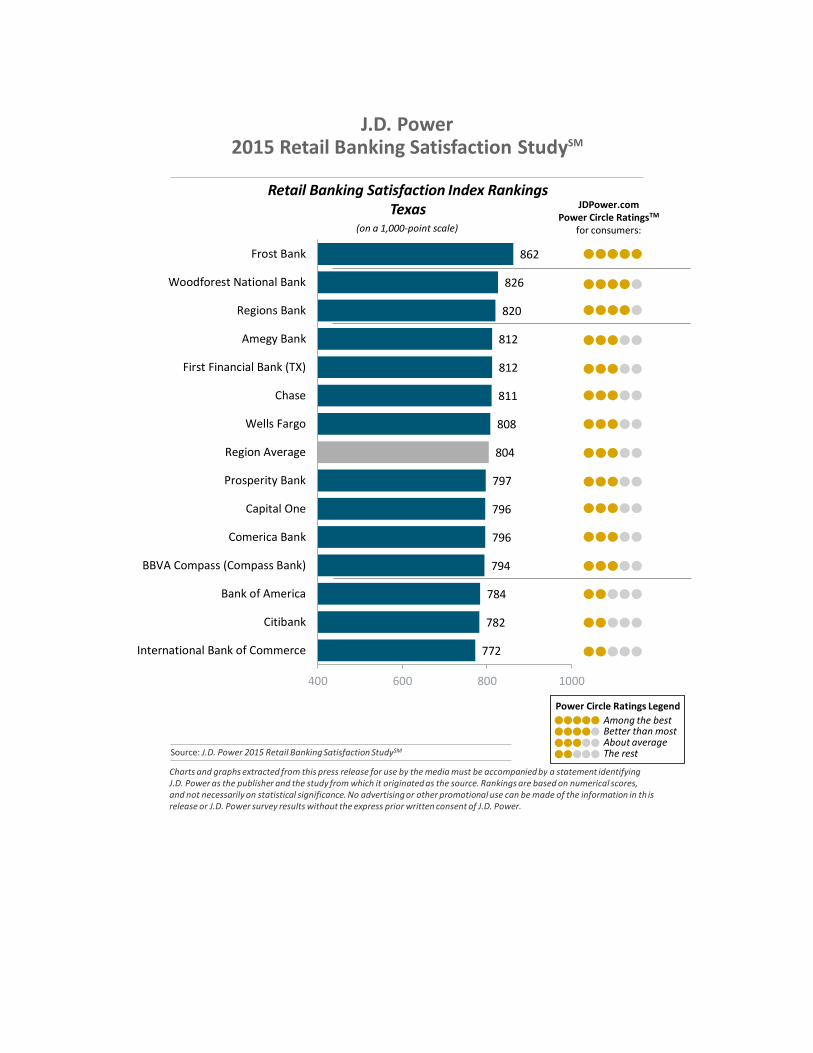

The study measures customer satisfaction with banks in 11 regions. Study results by region are: California Region: Rabobank ranks highest in the California region with a score of 816 and performs particularly well in the facility and channel activities factors. Following Rabobank in the rankings are Chase (800), and Bank of the West and Union Bank in a tie (798 each). Florida Region: Chase ranks highest in the Florida region with a score of 834, performing particularly well in the channel activities, facility and account information factors. TD Bank (830) and PNC Bank (826) follow in the rankings. Mid-Atlantic Region: Susquehanna Bank ranks highest in the region with a score of 834 and performs particularly well in the channel activities, product offerings and account information factors. Northwest Savings Bank (821) and S&T Bank (810) follow in the rankings. Midwest Region: First Midwest Bank ranks highest in the region with a score of 818 and performs particularly well in the product offerings, account information and channel activities factors. Following First Midwest Bank in the rankings are PNC Bank (808) and Commerce Bank (806). New England Region: Bangor Savings Bank ranks highest in the region with a score of 844 and performs particularly well in the product offerings and fees factors. Rockland Trust Co. (840) and Eastern Bank (805) follow in the rankings. North Central Region: With a score of 835, Huntington National Bank ranks highest in the region, performing particularly well in the product offerings and fees factors. Following in the rankings are 1st Source Bank (817) and Flagstar Bank (816). Northwest Region: Umpqua Bank ranks highest in the region with a score of 809 and performs particularly well in the facility factor. Wells Fargo (791) and Columbia State Bank (787) follow in the rankings. South Central Region: Arvest Bank ranks highest in the region with a score of 859, performing particularly well in the channel activities, product offerings, facility, account information, fees factors. Following in the rankings are Trustmark National Bank (844) and PNC Bank (832). Southeast Region: United Community Bank ranks highest in the region with a score of 842 and performs particularly well in the product offerings and facility factors. Following United Community Bank in the rankings are First Citizens Bancorp (839) and First Citizens Bancshares (832). Southwest Region: With a score of 840, Arvest Bank ranks highest in the region, performing particularly well in the product offerings, facility, account information and fees factors. FirstBank (CO) (823) and Chase (813) follow in the rankings. Texas Region: Frost Bank ranks highest in the Texas region with a score of 862, and performs particularly well in the channel activities, product offerings, facility, account information and fees factors. Woodforest National Bank (826) and Regions Bank (820) follow in the rankings.

The 2015 U.S. Retail Banking Satisfaction Study is based on responses from more than 80,000 retail banking customers of more than 130 of the largest banks in the United States regarding their experiences with their retail bank. The study was fielded quarterly from April 2014 to February 2015: Wave 1: April 1, 2014 – April 30, 2014 Wave 2: July 1, 2014 – August 4, 2014 Wave 3: October 1, 2014 – November 4, 2014 Wave 4: January 5, 2015 – February 2, 2015 Media Relations Contacts Jeff Perlman; Brandware Public Relations; Woodland Hills, Calif.; 818-317-3070; [email protected] John Tews; J.D. Power; Troy, Mich.; 248-680-6218; [email protected] About J.D. Power and Advertising/Promotional Rules http://www.jdpower.com/about-us/press-release-info About McGraw Hill Financial www.mhfi.com

(Page 4 of 4) ###

Note: Eleven charts follow.

816

800

798

798

793

792

787

785

778

775

767

400 600 800 1000

Rabobank

Chase

Bank of the West

Union Bank

BBVA Compass (Compass Bank)

U.S. Bank

Wells Fargo

Region Average

California Bank & Trust

Citibank

Bank of America

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsCalifornia

(on a 1,000-point scale)

834

830

826

817

811

810

801

799

798

784

783

400 600 800 1000

Chase

TD Bank

PNC Bank

SunTrust Bank

Regions Bank

Fifth Third Bank

Region Average

Branch Banking & Trust (BB&T)

Wells Fargo

Citibank

Bank of America

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsFlorida

(on a 1,000-point scale)

834821

810807805801801799798796794794793792791791790790789785785782779776776775771

762758752

716

400 600 800 1000

Susquehanna BankNorthwest Savings Bank

S&T BankHudson City Savings Bank

Branch Banking & Trust (BB&T)Community Bank

Fulton BankTD Bank

PNC BankChase

Citizens BankHuntington National Bank

SunTrust BankFirst NB of Pennsylvania

First Commonwealth BankNBT Bank

Manufacturers & Traders (M&T)National Penn Bank

Capital OneWells Fargo

Region AverageFirst Niagara Bank

New York Community BankApple Bank for Savings

Valley National BankCitibankKeyBank

Astoria FS&LABank of AmericaSantander Bank

HSBC

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsMid-Atlantic

(on a 1,000-point scale)

818

808

806

803

802

800

798

795

794

789

786

786

785

785

782

780

774

772

771

764

749

400 600 800 1000

First Midwest Bank

PNC Bank

Commerce Bank

Chase

Regions Bank

Great Southern Bank

First Bank (MO)

AnchorBank

Associated Bank

UMB Bank

Bremer Bank

MB Financial Bank

U.S. Bank

Region Average

Citibank

Bank of the West

BMO Harris Bank

Fifth Third Bank

Wells Fargo

Bank of America

TCF National Bank

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsMidwest

(on a 1,000-point scale)

844

840

805

800

795

785

783

779

774

771

763

753

731

400 600 800 1000

Bangor Savings Bank

Rockland Trust Co

Eastern Bank

TD Bank

Webster Bank

Wells Fargo

People's United Bank

Citizens Bank

Chase

Region Average

First Niagara Bank

Bank of America

Santander Bank

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsNew England

(on a 1,000-point scale)

835

817

816

814

812

811

800

800

799

799

798

797

797

794

790

787

787

781

780

779

775

771

750

400 600 800 1000

Huntington National Bank

1st Source Bank

Flagstar Bank

First Financial Bank (OH)

City National Bank (WV)

Chase

Regions Bank

Wells Fargo

Branch Banking & Trust (BB&T)

WesBanco Bank

Region Average

Charter One

PNC Bank

Chemical Bank

KeyBank

Comerica Bank

Fifth Third Bank

TCF National Bank

U.S. Bank

FirstMerit Bank

Bank of America

Old National Bank

BMO Harris Bank

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsNorth Central

(on a 1,000-point scale)

809

791

787

786

780

779

778

754

400 600 800 1000

Umpqua Bank

Wells Fargo

Columbia State Bank

Chase

KeyBank

U.S. Bank

Region Average

Bank of America

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsNorthwest

(on a 1,000-point scale)

859

844

832

823

820

812

812

806

805

804

797

792

786

786

786

768

400 600 800 1000

Arvest Bank

Trustmark National Bank

PNC Bank

First Tennessee Bank

SunTrust Bank

BancorpSouth Bank

Chase

Region Average

Regions Bank

Capital One

U.S. Bank

Wells Fargo

Bank of America

Branch Banking & Trust (BB&T)

Whitney Bank

BBVA Compass (Compass Bank)

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsSouth Central

(on a 1,000-point scale)

842

839

832

819

819

813

813

810

804

801

800

797

797

788

400 600 800 1000

United Community Bank

First Citizens Bancorp

First Citizens Bancshares

Branch Banking & Trust (BB&T)

South State Bank

PNC Bank

Synovus Bank

Fifth Third Bank

SunTrust Bank

Regions Bank

Region Average

TD Bank

Wells Fargo

Bank of America

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsSoutheast

(on a 1,000-point scale)

840

823

813

806

804

798

795

795

785

777

776

769

762

400 600 800 1000

Arvest Bank

FirstBank (CO)

Chase

Bank of Oklahoma

BancFirst

Wells Fargo

Zions First National Bank

Region Average

U.S. Bank

Bank of the West

BBVA Compass (Compass Bank)

Bank of America

Nevada State Bank

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsSouthwest

(on a 1,000-point scale)

862

826

820

812

812

811

808

804

797

796

796

794

784

782

772

400 600 800 1000

Frost Bank

Woodforest National Bank

Regions Bank

Amegy Bank

First Financial Bank (TX)

Chase

Wells Fargo

Region Average

Prosperity Bank

Capital One

Comerica Bank

BBVA Compass (Compass Bank)

Bank of America

Citibank

International Bank of Commerce

Source: J.D. Power 2015 Retail Banking Satisfaction StudySM

Charts and graphs extracted from this press release for use by the media must be accompanied by a statement identifying J.D. Power as the publisher and the study from which it originated as the source. Rankings are based on numerical scores, and not necessarily on statistical significance. No advertising or other promotional use can be made of the information in th is release or J.D. Power survey results without the express prior written consent of J.D. Power.

J.D. Power2015 Retail Banking Satisfaction StudySM

JDPower.comPower Circle RatingsTM

for consumers:

Among the bestBetter than mostAbout averageThe rest

Power Circle Ratings Legend

Retail Banking Satisfaction Index RankingsTexas

(on a 1,000-point scale)