Embed Size (px)

Citation preview

PAKISTANWAVE REPORT

FII TRACKER SURVEYConducted September-October 2015

March 2016

PUTTING THE USER FRONT AND CENTER

PAKISTAN

The Financial Inclusion Insights (FII) program responds to the need identified by multiple stakeholders for

timely, demand-side data and practical insights into digital financial services (DFS), including mobile money,

and the potential for their expanded use among the poor.

The FII team conducts regular survey and qualitative research in Kenya, Tanzania, Uganda, Nigeria, India, Pakistan, Bangladesh and Indonesia to:

• Track access to and demand for financial services generally, and the uptake and use of DFS specifically;

• Measure adoption and use of DFS among key target groups (females, BOP, rural, unbanked, etc.);

• Identify drivers and barriers to further adoption of DFS;

• Evaluate the agent experience and the performance of mobile money agents; and

• Produce actionable, forward-looking insights to support product and service development and delivery, based on rigorous FII data.

The FII program is managed by InterMedia. Visit the FII Resource Center to learn more: www.finclusion.org.

2

CONTENTS

1. Executive Summary

2. Financial Inclusion

3. Pakistanis’ Financial Lives

4. Access to, Use of Mobile Phones

5. Financial Services Use

6. Banks

7. Mobile Money

8. Nonbank Financial Institutions

9. Methodology & Research Description

10. Glossary

PAKISTAN

3

4

13

19

30

39

45

52

66

70

73

EXECUTIVE SUMMARY

PAKISTAN

4

PAKISTAN

% of survey % of survey

Gender Age

Male 53% 15-24 28%

Female 47% 25-34 29%

Geography 35-44 17%

Urban 34% 45-54 15%

Rural 66% 55+ 11%

Income Aptitude

Above the $2.50/day

poverty line50% Basic literacy 65%

Below the $2.50/day

poverty line50% Basic numeracy 95%

Survey demographics

Figures are weighted to reflect national census data demographics.

5Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+) September-October 2015.

PAKISTAN

Country context

6

• As of June 2015, six banks and two microfinance banks were licensed to offer mobile financial services in Pakistan.

o Telenor Easypaisa remains the clear market leader.

• By the end of the second quarter of 2015, a total of 99.5 million transactions, valued at PKR 505.9 billion ($4.8 billion USD),

were conducted. This amounted to a 37 percent increase in transaction volume and a 43 percent increase in value over the

previous quarter.

o Customer transactions amounted to 94.3 million in volume and PKR 308.4 billion (2.95 billion USD) in value.

o Over-the-counter (OTC) transactions represented 70 percent of customer transactions in both volume and value; m-wallet

transactions amounted to approximately 30 percent each in volume and value.

o According to the State Bank of Pakistan, the rise in customer transactions can be attributed to the rise in cash deposits and

withdrawals, fund transfers, G2P transactions and mobile top-ups.

• According to the State Bank of Pakistan (SBP), there were 10.8 million registered mobile money accounts by the end of June

2015.

o Telenor Easypaisa accounted for 7.5 million of the registered accounts, followed by Omni with 1.8 million accounts, and Waseela

Microfinance at 1.2 million accounts.

o Between the first and second quarters of 2015, mobile money registration increased by 44 percent.

o As of the end of June 2015, an estimated 47,902 biometric identification devices were installed at agent locations to facilitate real-

time account opening. Thirty-six percent of agent locations across Pakistan had this capability as of June 2015.

o Between April and June 2015, Mobicash and Easypaisa opened 1.3 million customer accounts using the biometric verification

system, according to SBP data.

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+) September-October 2015.

• Financial inclusion remained at under 10 percent of adults.

o Financial inclusion increased from 7 to 9 percent between 2014 and 2015.

o Most demographic groups saw no more than a 1 percent change in financial inclusion. Financial inclusion grew

most for women, doubling from 3 percent in 2014 to 6 percent in 2015.

• Banks are still the major contributor to financial inclusion.

o Registered bank accounts remained steady; 7 percent of adults have bank accounts.

o Mobile money and NBFI accounts both grew from less than 1 percent of adults prior to 2015, to 1 percent of

adults in 2015.

PAKISTAN

Key findings: Financial inclusion

7

7%11%

3%

11%

6%10%

5%9% 11%

6%

12%

7%11%

6%

Totalpopulation

Men Women Urban Rural Abovepoverty

Belowpoverty

2014 2015

Financially included by demographic(Shown: Percentage of Pakistani adults within each demographic group, by year)

Source: InterMedia Pakistan FII Tracker surveys Wave 2 (N=6,000, 15+) September-December 2014; Wave 3 (N=6,000, 15+), September-October 2015.

• Access to financial accounts is driven by both mobile money and banks.

o More adults (9 percent) use mobile money than use banks (8 percent). However, the

majority of mobile money users are unregistered, using the service over the counter

(OTC).

o Eighty-six percent of mobile money users are using the services OTC through an

agent rather than registering for their own accounts.

• Non-digital access is the preferred route to bank account access.

o Nearly all bank account holders reported being able to access their accounts digitally,

but the preferred way to access an account is OTC at a bank branch (82 percent).

o The second choice was through ATMs, at 72 percent.

• Males are more than twice as likely as females to be active bank account holders.

o Ten percent of males were active bank account holders, compared with 4 percent of

females.

o Urban/rural and above/below poverty line divides were 10 percent vs. 6 percent, and

9 percent vs. 5 percent, respectively.

PAKISTAN

Key findings: Account access and ownership

8

1%

8%

9%

15%

0.2%

7%

8%

14%

N/A

9%

7%

14%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

Financial account access

(Shown: Percentage of Pakistani adults, by year)

2014 (N=6,000)

2015 (N=6,000)

2013 (N=6,000)

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

• Mobile money use, as a portion of awareness, remains steady at just over

one in 10.

o Seventy-two percent of Pakistanis were aware of at least one mobile money

provider, 13 percent of whom had used mobile money at least once. This

compares with 76 percent and 11 percent, respectively, in 2014.

• Regardless of which company someone has a SIM card with, Easypaisa is

the mobile money deployment they are most likely to be able to identify.

o The largest gap between customers’ awareness of their own mobile network

operators’ mobile money products and that of Telenor’s Easypaisa is seen

among Warid customers. Thirty-nine percent of Warid SIM-card holders

could identify Warid’s Mobile Paisa product, but 86 percent could identify

Easypaisa.

o Outside of Telenor SIM card holders, Mobilink customers were most likely

to be able to identify their company’s mobile money service. Sixty percent of

Mobilink customers knew about Mobilink Mobicash.

• Use of mobile money for advanced activities is increasingly common.

o In 2013, 42 percent of mobile money users only used the services for

depositing and withdrawing cash. Now, that number has dropped to 4

percent.

o Advanced use of mobile money services, such as bill pay and loans, has

moved from 28 percent of mobile money users in 2013 to 42 percent in

2015.

PAKISTAN

Key findings: Mobile money

9

42%

7%4%

68%

55%57%

28%

36%42%

2 0 1 3 ( N = 4 2 8 ) 2 0 1 4 ( N = 4 9 3 ) 2 0 1 5 ( N = 5 8 4 )

Basic activities only (CICO and account management)

Basic activities OR P2P only

At least one advanced activity (i.e., bill pay, loan activities)

Mobile money uses, by type(Shown: Percentage of all mobile money users)

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

• Many Pakistanis who do not have bank accounts lack the necessary information to make informed decisions about bank

account use.

o The top two reasons Pakistanis gave for not registering a bank account were they didn’t have enough money to do so or they didn’t

engage in financial activities that an account could facilitate.

o Among those who thought they did not have enough money, 71 percent admitted they did not know how much it costs to open an

account.

o Seventy-four percent of those who did not believe they could use a bank account for activities they engage in did not know that

bank accounts could be used to make retail purchases. Forty-five percent did not know that banks could be used to access credit.

• Low literacy and the inability to use a mobile phone remain significant barriers to adopting mobile-based financial services.

o Sixty-five percent of Pakistani adults are able to read and understand basic sentences in either Urdu or English.

o Seventy-six percent of adults can access a mobile phone, but just 40 percent had ever sent or received a text message. The technical

skills necessary for using mobile money are similar to those needed to send and receive text messages.

PAKISTAN

Key findings: Awareness, literacy and mobile competency

10

Estimate of cost of opening a bank account(Shown: Percentage of those who believe they don’t have

enough money to open an account, n=2,254)

I don't have enough moneyto open an account

71% Admit not knowing how much it costs to open

a bank account.

19% More than 1,000 PKR ($10 USD)

6% Less than 1,000 PKR ($10 USD)

4% Free

41%

Reason for not opening a bank account(Shown: Percentage of unbanked, n=5,518)

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+) September-October 2015.

PAKISTAN

At-a-glance: Bank accounts and mobile money continue to be the primary

means of financial account access

11

1%

7%

1%

9%

0.1%

7%

0.3%

7%

N/A

7%

0.4%

8%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

0.6%

7%

1%

8%

0.1%

6%

0.3%

6%

N/A

6%

0.4%

7%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

Financial account access Registered financial service users(Shown: Percentage of Pakistani adults for each year)

Active* account holders

2014 (N=6,000) 2015 (N=6,000)2013 (N=6,000)

Types of account ownership are not mutually exclusive. *Used the account in the last 90 days

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

1%

8%

9%

15%

0.2%

7%

8%

14%

N/A

9%

7%

14%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

PAKISTAN

Digital stored-value accounts: accounts in which a monetary value is represented in a digital electronic format and can be retrieved/transferred by the account

owner remotely. For this particular study, DSVAs include a bank account or NBFI account with digital access (a card, online access or a mobile phone

application) and a mobile money account.

12

Main FSP Indicator2014 2015

Base Definition% %

Base n Base n

Adults (15+) who have active digital stored-value accounts6% 8%

All adults6,000 6,000

Poor adults (15+) who have active digital stored-value accounts4% 5%

All poor3,102 3,074

Rural women (15+ ) who have active digital stored-value accounts 2% 3%

All rural females1,760 1,745

Adults (15+) who have active digital stored-value accounts and use them to access

other financial services (beyond basic wallet, P2P and bill pay)

4% 3%All adults

6,000 6,000

Poor adults (15+) who have active digital stored-value accounts and use them to

access other financial services (beyond basic wallet, P2P and bill pay)

3% 2%All poor

3,102 3,074

Rural women (15+) who have active digital stored-value accounts and use them to

access other financial services (beyond basic wallet, P2P and bill pay)

0.9% 0.7%All rural females

1,760 1,745

Active digital stored-value account ownership increased between 2014 and

2015, but use of these accounts for beyond-basic services did not change

Source: InterMedia Pakistan FII Tracker surveys Wave 2 (N=6,000, 15+), September-December 2014; Wave 3 (N=6,000, 15+), September-October 2015.

FINANCIAL INCLUSION

PAKISTAN

13

PAKISTAN

Understanding financial inclusion

What is financial inclusion?

FII’s definition of financial inclusion goes beyond

“having accessed” a financial service. This

comparatively conservative definition requires account

ownership with an institution that provides a full-suite of

financial services and comes under some form of

government regulation.

These services include savings, money transfers,

insurance or investment. Institutions that only offer

loans to consumers, such as some microfinance

institutions (MFIs), are not considered to be full-service

institutions. (Source: InterMedia FII Program)

How is it measured?

To determine financial inclusion, we look at the

percentage of adults who report having an account in

their name with at least one institution offering a full-

suite of financial services.

What is included in this?

Banks, nonbank financial institutions and mobile money

services are included in the financial inclusion measure.

In the case of Pakistan, nonbank financial institutions

include MFIs, committees, and post office banks. In all

countries, individuals must have an account in their own

name.

What isn’t included?

Excluded from the financial inclusion measure are

money guards, savings collectors, hawla/hundi

networks, and digital recharge cards that are not

attached to a bank or MFI account.

Additionally, individuals who have accessed formal

financial services but do not have their own account,

such as those using another family member’s account,

are not included.

14Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

Just under one-tenth of Pakistanis are financially included

9%Financially

included*

have a full-service NBFI account

have a full-service bank account**

have a mobile money account

7%

1%

1%

Individuals must have

accounts with institutions

offering a full suite of

financial services, including

savings facilities. Some

banks and many NBFIs

only offer credit services to

their customers; these are

not included.

*Overlap representing those who have multiple kinds of financial accounts is not shown.

15

**For the purposes of this study, bank account holders have accounts at full-service institutions, unless otherwise noted.

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

Incremental increases across mobile money and NBFIs grew financial

inclusion overall; product adoption by women drove progress

Overlap representing those who have multiple kinds of financial accounts is not shown.

16

7%9%

Financially included

2014 (N=6,000) 2015 (N=6,000)

Financially included(Shown: Percentage of Pakistani adults)

Source: InterMedia Pakistan FII Tracker surveys Wave 2 (N=6,000, 15+), September-December 2014; Wave 3 (N=6,000, 15+), September-October 2015.

0.3%

7%

0.1%1%

7%

1%

Mobile money Bank NBFI

7%11%

3%

9%11%

6%

Totalpopulation

Men Women

7%11%

6%9%

12%7%

Totalpopulation

Urban Rural

7%10%

5%9%

11%6%

Totalpopulation

Abovepoverty

Below poverty

Financially included by demographic(Shown: Percentage of Pakistani adults within each

demographic group, by year)

PAKISTAN

Financial inclusion corresponds to greater economic stability and financial

planning across poverty levels

17

15% 12%21%

25%

Financially includedabove poverty

(n=355)

Financially excludedabove poverty

(n=2,571)

Financially includedbelow poverty

(n=202)

Financially excludedbelow poverty

(n=2,872)

2015: Economically vulnerable(Shown: Percent of Pakistani adults by financial inclusion, poverty

levels)

2015: Have a financial plan for unexpected events(Shown: Percent of adults by financial inclusion, poverty levels)

62%57% 54% 51%

Financially includedabove poverty

(n=355)

Financially excludedabove poverty

(n=2,571)

Financially includedbelow poverty

(n=202)

Financially excludedbelow poverty

(n=2,872)

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

Few Pakistanis are digitally included; banks lead digital inclusion

8%Digitally

included*

have a digital NBFI account

have a digital bank account

have a mobile money account

7%

0.3%

1%

*Overlap representing those who have multiple kinds of financial accounts is not shown.

18

Digital access to an account means that an individual can access their account via any number of electronic platforms, including debit and credit cards,

electronic money transfers, or mobile phones.

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTANIS’ FINANCIAL LIVES

PAKISTAN

19

PAKISTAN

Most adults are at least occasionally able to pay their bills on time

20

*Question allowed for multiple responses.

Regularly experience economic

vulnerability (i.e., can’t afford

food, medical expenses)

Have a financial plan for

unexpected events

Able to pay bills on time

19%

54%

83%

2015: Financial responsibility, vulnerability(Shown: Percentage of Pakistani adults, N=6,000)

2015: Financially

included(n=557)

2015: Financially

excluded(n=5,443)

59% 54%

17% 19%

89% 82%

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

One in five experience economic vulnerability, most often having to pass on

medical help or family engagements

21

2015: Form of economic vulnerability (Shown: Percentage of vulnerable adults, n=1,148)

%

Gone without medical help 55%

Miss an important family event

(i.e., funeral, wedding, etc.)

40%

Gone without food to eat 23%

Gone without cooking fuel 21%

Gone without fertilizer for the farm 16%

Gone without help from a veterinarian 15%

Couldn’t pay school fees 10%

Had to close down business temporarily or completely 7%

19%regularly experience

some form of

economic vulnerability

2015: Economic vulnerability(Shown: Percentage of Pakistani adults, N=6,000)

2015: Profile of vulnerable adults (n=1,148)

53% Female

62% Rural

67% Live on less than $2.50 a day

14% Live on less than $1.25 a day

93% Numerate

46% Illiterate

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

13%

24%

18%

22%

11%

24%

17%

25%

34%

28%

31%

32%

26%

15%

22%

8%

10%

4%

7%

3%

6%

6%

6%

10%

Below poverty line

Above poverty line

Unbanked

Banked

We can buy

what we want

We can buy

some expensive

goods

Have enough

money for food &

clothes and can

save some

We have enough

money for food

but buying

clothes is hard

We don’t have

enough money

for food

Don’t know/

refused

2015: Perceptions of household purchasing power(Shown: Percentage of Pakistani adults, N=6,000)

22Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Unbanked and below-poverty-line households’ perceptions of their purchasing

power are far lower than the perceptions held by their counterparts

n=482

n=5,518

n=2,926

n=3,074

PAKISTAN

Close to half the population is gainfully employed

23

Housewife/student Gainfully employed Unemployed, seeking jobsRetired, disabled or other

2015: Employment(Shown: Percentage of Pakistani adults, N=6,000)

46% gainfully employed

51% housewife or student

2% unemployed, seeking jobs

2% retired, disabled or other

Due to rounding, percentages add to 101.

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

The vast majority of gainfully employed adults are males; working on or

owning a farm is the most common occupation

24

5%

5%

6%

12%

13%

27%

Driver, including rickshaws

Factory employee

Public or health serviceworker

Manual laborer

Shop owner

Farmer/ farm owner

2015: Most common primary occupation(Shown: Percentage of gainfully employed adults, n=2,857)

2015: Employment(Shown: Percentage of Pakistani adults, N=6,000)

%Gainfully employed

53% of the population is male; but males make

up 94% of the gainfully employed.

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

0.4%

0.5%

2%

7%

7%

13%

34%

89%

MFI

State Life Insurance Corporation ofPakistan

A money guard

With people in the community

Bank

Savings or lending group

Gold

Cash at home

PAKISTAN

Many Pakistanis save money, mostly through informal means

2015: Savings(Shown: Percentage of Pakistani adults, N=6,000)

25

currently have

savings

72%8%

of savers know the interest rate

they earn on their savings.

2015: Location of savings(Shown: Percentage of adults who save, n=4,291)

Emergencies (67%) and to make

ends meet (57%) are the top two

reasons people save money.

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

2015: Borrowing(Shown: Percentage of Pakistani adults, N=6,000)

0.4%

2%

5%

6%

8%

85%

Other formal institution

Banks

MFI

A group that lends to others, withinterest

An informal moneylender

Family or friends

2015: Source of loans(Shown: Percentage of adults who borrow, n=1,123)

PAKISTAN

Few Pakistanis have borrowed money; family and friends are the primary

sources of loans

26

50% of borrowers know the

interest rates on their loans.

have borrowed

money

18%

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

0.4%

0.9%

2%

4%

18%

23%

72%

Unemployment

Retirement/pension

Property

Agriculture

Vehicle

Medical

Life

PAKISTAN

Few Pakistanis have insurance; most who do have life insurance

2015: Insurance(Shown: Percentage of Pakistani adults, N=6,000)

27

have

insurance

3%92% with life insurance bought it through

the State Life Insurance Corporation of

Pakistan; 6% acquired it through a private

insurance provider.

2015: Type of insurance(Shown: Percentage of adults with insurance, n=162)

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

28Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

2015: Primary reasons for not having insurance(Shown: Percentage of uninsured adults, n=5,838)

A lack of awareness and understanding is preventing insurance coverage

from becoming more commonplace

3% 97%

uninsured

3%

3%

5%

11%

22%

39%

Registration paperwork is too complicated

I don't own anything valuable

I don't know how to get it

No reason, never thought of it before

I don't know what it is

I don't need it

17%

17%

20%

22%

26%

32%

Loss of property due to theft or burglary

Loss of harvest or livestock

Bankruptcy

Loss of house due to a natural disaster

Death in the family

Major medical emergency

PAKISTAN

29

0.8% had health

insurance (n = 1,961)

0.1% had property

insurance (n = 1,004)

1% had life

insurance (n = 1,614)

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

2015: Unexpected expenses for which people have a financial plan(Shown: Percentage of Pakistani adults, N=6,000)

Insurance may be rare, but more do plan for medical expenses, death in the

family

ACCESS TO, USE OF MOBILE PHONES

PAKISTAN

30

72%

54%

76%

59%

PAKISTAN

31

Low mobile phone ownership and a lack of competency with a phone

continue to be barriers to DFS uptake

Have access to a mobile phone(Shown: Percentage of Pakistani adults, by year)

Own a mobile phone(Shown: Percentage of Pakistani adults, by year)

37%

sent/received

SMS

2014 (N=6,000) 2015 (N=6,000)

Basic mobile phone competency (has sent/received

text messages [SMS])(Shown: Percentage of Pakistani adults, by year)

2014

2015

40%

sent/received

SMS

In 2015, 62% sent

or received an SMS

Source: InterMedia Pakistan FII Tracker surveys Wave 2 (N=6,000, 15+), September-December 2014; Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

SIM-card access, ownership(Shown: Percentage of Pakistani men, women by year)

SIM-card access, ownership is largely static; few discarded a SIM as a result

of the verification initiative

32

77% 76%

29% 33%

7% 6%

29%

33%

2014 2015 2014 2015

WomenMen

Own a SIM card Can access but don’t

own a SIM

7%93%

Households affected by SIM-card verification initiative(Shown: Percentage of Pakistani adults, N=6,000)

A household member

discarded a SIM card due to

the verification initiative

The SIM-card verification initiative that was part of the new

biometric registration requirement caused some disruption,

with 7 percent of adults reporting their households were

affected by it. However, it did not appear to reduce

ownership or access to SIMs among either gender.

Source: InterMedia Pakistan FII Tracker surveys Wave 2 (N=6,000, 15+), September-December 2014; Wave 3 (N=6,000, 15+), September-October 2015.

11%

28%

72%

PAKISTAN

33

Basic phones – those that only allow calling, SMS and saving phone numbers

– are more common than smartphones or feature phones

Basic phone

Feature phone

Smartphone

2015: Type of mobile phone*(Shown: Percentage of mobile phone owners, n=3,547)

59%Own a mobile

phone

Basic phone: Only allows calling, text messaging (SMS) and saving phone numbers

Feature phone: Has a camera, radio, etc., but does not have email or mobile applications

Smartphone: Provides access to email accounts, mobile applications

*Question allowed for multiple responses, depending on the number of phones owned.

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

10%

18%

19%

31%

38%

Warid

Ufone

Zong

Mobilink

Telenor

PAKISTAN

34

Telenor has the greatest market share among mobile phone owners, and its

customers tend to have the highest rate of basic phone ownership

2015: SIM card providers(Shown: Percentage of mobile phone owners, n=3,547)

Basic Feature Smart

72% 28% 11%

69% 31% 14%

64% 37% 17%

66% 33% 16%

69% 31% 11%

2015: Mobile phone ownership type, by provider(Shown: Percentage of SIM-card owners, by MNO*)

*Mobile network provider

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

Male Female Above the poverty line Below the poverty lineUrban Rural

Mobile phone owners tend to be men, urban and above the poverty line;

women, rural, lower income individuals borrow phones if they have access at all

35

2015: Dynamics of mobile phone access(Shown: Percentage of mobile phone owners, by ownership type)

59%Own a mobile

phone

78%

65%66%

36%

55%51%

18%Can borrow a

mobile phone6%

20%

18%31%

17%18%

24%Have no access to

a mobile phone15% 15% 16%

33%28%

31%

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

0.5%

0.6%

3%

PAKISTAN

36

Consumers with greater mobile phone proficiency are more likely to have

mobile money accounts or be financially included

2015: Have ever sent a text message (SMS)(Shown: Percentage of Pakistani adults, N=6,000)

15%financially

included

40% 60%SMS incapableHave sent an SMS

(SMS capable)

2%

2%

14%Bank

Mobile money

NBFI

4%financially

included

Bank

Mobile money

NBFI

2015: Full-service account ownership

(financial inclusion)(Shown: Percentage of SMS capable, n=2,335)

2015: Full-service account ownership

(financial inclusion)(Shown: Percentage of SMS incapable, n=3,665)

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

15-24 year olds

(n=1,219)

25-34 year olds

(n=1,719)

35-44 year olds

(n=1,492)

45-54 year olds

(n=1,019)

55+

(n=551)

26% 20% 17% 11% 6%15-24

PAKISTAN

37

The greatest disparity in advanced phone use is by age, not by poverty or

gender

Male

(n=3,155)

Female

(n=2,845)

Urban

(n=2,030)

Rural

(n=3,970)

Above poverty

(n=2,926)

Below poverty

(n=3,074)

24% 12% 27% 14% 23% 14%

25-34 35-44 45-54 55+

2015: Advanced phone use by demographic(Shown: Percentage of subgroups)

18%

use a mobile

phone for advanced

functions

Greatest gap between

demographics

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Total populationN=6,000

PAKISTAN

38

Advanced users tend to take photos, browse the internet, download

multimedia or send/receive multimedia messages (MMS)

2015: Advanced phone use(Shown: Percentage of mobile phone users, n=4,605)

4%

4%

5%

7%

8%

10%

11%

11%

18%

Made a financial transaction

Navigation/ maps

Used "Call Tunes" or other on-demandaudio/video service

Downloaded any other mobile application

Used social media (i.e., WhatsApp,Facebook, etc.)

Sent/received MMS

Used/ browsed the internet

Downloaded music or video games

Took a color picture

use a mobile

phone for advanced

functions

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

15% use two or more

advanced functions

12% use three or more

Total populationN=6,000

18%

FINANCIAL SERVICES USE

PAKISTAN

39

PAKISTAN

At-a-glance: Mobile money access and use has grown vs. 2013

40

1%

7%

1%

9%

0.1%

7%

0.3%

7%

N/A

7%

0.4%

8%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

0.6%

7%

1%

8%

0.1%

6%

0.3%

6%

N/A

6%

0.4%

7%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

1%

8%

9%

15%

0.2%

7%

8%

14%

N/A

9%

7%

14%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

Financial account access Registered financial service users(Shown: Percentage of Pakistani adults for each year)

Active account holders

2014 (N=6,000) 2015 (N=6,000)2013 (N=6,000)

Types of account ownership are not mutually exclusive.

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

67%

96%

90%

97%

2014: Base (n) was too small to conduct analysis

87%

2013 and 2014: Bases (n) were too small to conduct analysis

87%

N/A

86%

87%

Nonbank financial institution

Bank

Mobile money

Any financial service

0.6%

7%

1%

8%

0.1%

6%

0.3%

6%

N/A

6%

0.4%

7%

Nonbank financial institution

Bank

Mobile money

Any financial service

PAKISTAN

Most account holders are active users of their financial services, bank

account holders are the most active

Active* financial account holders(Shown: Percentage of Pakistani adults)

41

Active* financial account holders(Shown: Percentage of registered users for each type of account, by year)

*A registered account used in the last 90 days. Types of accounts are not mutually exclusive.

2014 (N=6,000) 2015 (N=6,000)2013 (N=6,000) 2014 20152013

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

5%

6%

4%

7%

10%

10%

9%

1%

1%

0.1%

1%

2%

1%

1%

0.3%

0.2%

1%

0.6%

0.3%

2%

1%

6%

6%

5%

8%

11%

12%

11%

Below poverty line (n=3,074)

Rural (n=3,970)

Females (n=2,845)

Total population (N=6,000)

Males (n=3,155)

Urban (n=2,030)

Above poverty line (n=2,926)

PAKISTAN

2015: Active account usage by demographic(Shown: Percentage of each subgroup)

There are disparities in active use by poverty level, urban/rural and gender

42Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Types of accounts are not mutually exclusive.

Active mobile-money account holders Active NBFI account holdersActive bank account holders All financial account holders

42%

7%4%

68%

55%57%

28%

36%42%

2 0 1 3 ( N = 4 2 8 ) 2 0 1 4 ( N = 4 9 3 ) 2 0 1 5 ( N = 5 8 4 )

Basic activities only (CICO and account management)

Basic activities OR P2P only

At least one advanced activity (i.e., bill pay, loan activities)

PAKISTAN

Bank uses, by type(Shown: Percentage of active bank account holders)

43

Mobile money uses, by type(Shown: Percentage of all mobile money users)

37%27% 31%

39% 32% 38%

60%

67%

61%

2 0 1 3 ( N = 4 1 9 ) 2 0 1 4 ( N = 3 9 1 ) 2 0 1 5 ( N = 4 6 7 )

Basic activities only (CICO and account management)

Basic activities OR P2P only

At least one advanced activity (i.e., bill pay, loan activities)

Due to the changes in the questionnaire some data points may not be directly comparable across years.

More consumers are utilizing advanced mobile money services vs.

previous years

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

More adults know of a mobile money (MM) agent within 1 km of where they

live than they do of any banking point-of-service (POS)

PAKISTAN

2015: Proximity to points-of-service (POS) for financial institutions(Shown: Percentage of Pakistani adults N=6,000)

71%

47%

20%

46% 44%

32%

39%34%

10%5%

11% 13% 13% 13%18%

15%11%

8%

21%

15%18%

24%

32% 30%

7%

41%

48%

26% 25%

31%

12%

21%

Any POS ROSCA MFI Retail store with anMM agent

MM agent Retail store withbank deposit or

withdrawal

Bank branch ATM

52% know of any mobile

money agent within 1 km

of their home

44

44% know of any banking POS within

1 km of their home

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

1-5 kms from home More than 5 kms from homeLess than 1 km from home Don’t know

BANKS

PAKISTAN

45

PAKISTAN

At-a-glance: Bank account access and use is mostly static vs. 2013

46

1%

7%

1%

9%

0.1%

7%

0.3%

7%

N/A

7%

0.4%

8%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

0.6%

7%

1%

8%

0.1%

6%

0.3%

6%

N/A

6%

0.4%

7%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

Financial account access Registered financial service users(Shown: Percentage of Pakistani adults for each year)

Active account holders

2014 (N=6,000) 2015 (N=6,000)2013 (N=6,000)

Types of account ownership are not mutually exclusive.

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

1%

8%

9%

15%

0.2%

7%

8%

14%

N/A

9%

7%

14%

Nonbank financialinstitution

Bank

Mobile money

Any financial service

PAKISTAN

2015: Bank account ownership, by type(Shown: Percentage of Pakistani adults, N=6,000)

47

Credit-only bank accounts make up a small portion of consumer bank

accounts

Registered full-service

bank account

Do not have a

registered bank account

7%0.6%

91%

0.7%

Registered credit-only

bank account

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Registered neither credit-only

nor full-service bank account

PAKISTAN

2015: Preferred method of bank account access(Shown: Percentage of full-service bank account holders, n=482)

48

Bank account holders prefer to access their accounts over the counter at

a bank branch

1%

1%

6%

74%

82%

ATM

Over the counter at a

bank branch

Through a mobile app

Through the bank’s

website

Through a mobile wallet

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

PAKISTAN

2015: Top reasons for not registering for a bank account(Shown: Percentage of adults without a bank account, n=5,518)

49

The primary reasons Pakistanis do not register for bank accounts are a

perceived lack of money or the need for a bank account

2%

2%

2%

4%

6%

30%

40%I don’t have money

I don’t need one, I don’t

make transactions

I don’t have money to

make transactions

I don’t know what it is

I don’t know how to open

oneRegistration paperwork is

too complicated

93%of adults do not

have a bank

account registered

in their name

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

There is no bank close to

where I live

PAKISTAN

Estimate of cost of opening a bank

account(Shown: Percentage of those who believe they don’t

have enough money to open an account, n=2,254)

50

30%

40%

I don't need one, I don't maketransactions

I don't have money

71% Admit not knowing how

much it cost to open a

bank account

19% More than

1,000 PKR

6% Less than 1,000

PKR ($10 USD)

4% Free

Awareness of potential uses for

bank accounts(Shown: Percentage of those who believe

they don’t make transactions that warrant an

account, n=1,639)

26%

55%

70%

85%

88%

Retail shopping

Loans

Person-to-persontransfers

Cash withdrawal anddeposit

Savings

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

(Base: individuals who do not have a bank account, n=5,518)

The barriers to bank account ownership – the perceived lack of money or

need for an account -- are driven by low awareness of banking costs and uses

36%

24%

9%

8%

5%

4%

3%

2%

2%

PAKISTAN

Investment activity

Save/set aside money

Bill pay

Receive wages

Loan activity

Make bank2bank transfers

Receive G2P payments

Pay for large acquisitions

Pay for goods at a store

2015: Advanced bank account uses(Shown: Percentage of active bank account holders, n=467)

51

Active bank account holders utilize their accounts for an array of advanced

functions, including bill pay and receiving wages

61%of active registered

users have used at

least one

advanced function

through their

accounts

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Question allowed for multiple responses.

MOBILE MONEY

PAKISTAN

52

PAKISTAN

53

65%

aware

2013 (N=6,000)

Conversion from awareness of mobile money providers* to mobile money use(Shown: Percentage of Pakistani adults for each year)

2014 (N=6,000) 2015 (N=6,000)

MM OTC use, 7%

MM registered

users, 0.4%

MM OTC use, 8%

MM registered

users, 0.3%

MM OTC use, 8%

MM registered users, 1%

7% use

mobile

money

0.11

conversion

rate

8% use

mobile

money

0.11

conversion

rate

9% use

mobile

money

0.13

conversion

rate

Awareness of mobile money providers remains high; it has not yet

translated into widespread use

76%

aware72%

aware

*Awareness of at least one mobile money provider

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

0%

0%

1%

2%

5%

12%

20%

89%

MCB Mobile

Mobile Paisa

HBL Express

Zong Timepey

Ufone/Upayment

UBL Omni

Mobilink Mobicash

Telenor Easypaisa

PAKISTAN

Several providers have a presence in the market, with one-third using a

provider other than market leader Telenor

2015: Mobile money usage by provider(Shown: Percentage of mobile money users, n=584)

54

Don't use Telenor,

11%

Only use Telenor, 68%

Use Telenor & other MM

services, 21%

2015: Mobile money (MM) usage exclusivity(Shown: Percentage of mobile money users, n=584)

32% of mobile

money users

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Mobile money product awareness by SIM ownership(Shown: Percentage of SIM owners, by MNO)

Telenor(n=1,354)

Uphone(n=648)

Zong(n=672)

Warid(n=354)

Mobilink(n=1,109)

Telenor Easypaisa 85% 86% 77% 86% 81%

Ufone/Upayment 38% 47% 42% 45% 33%

Zong Timepay 38% 45% 47% 40% 28%

Warid Mobile Paisa 24% 25% 31% 39% 21%

Mobilink Mobicash 58% 58% 62% 65% 60%

PAKISTAN

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

With the exception of Telenor, only portions of an MNO’s customers know

that it offers mobile money

55

Easypaisa is the

most recognized

mobile money

product regardless

of which provider an

individual has a SIM

card with.

Mobile network operators

Mo

bile m

on

ey p

rovid

ers

PAKISTAN

7%

11%

3%

8%7%

9%

6%8%

12%

4%

10%

7%9%

7%9%

14%

4%

12%

8%

11%

8%

Total populationN=6,000

Male Female Urban Rural Above poverty line Below poverty line

Demographic trends for mobile money use (Shown: Percentage of adults to ever use mobile money who fall into each category)

Mobile money use increased across almost all demographics

56

2014 20152013

Source: InterMedia Pakistan FII Tracker surveys Wave 1 (N=6,000, 15+), November 2013-January 2014; Wave 2 (N=6,000, 15+), September-December 2014;

Wave 3 (N=6,000, 15+), September-October 2015.

*Categories are not mutually exclusive.

PAKISTAN

Most account holders registered for their accounts because of a

recommendation by a mobile money user

2015: Main reason for registering for a mobile

money account(Shown: Percentage of mobile money account holders, n=74)

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

32%

5%

3%

2%

0.9%

Bill pay

Loan activities

Make MM2MM transfers

Save/set aside money

Receive government payments

2015: Most common uses for mobile money account beyond

cash-in and cash-out transactions(Shown: Percentage of mobile money account holders, n=74)

57

51%Recommendation

from a current user

25%To send money to

someone

13%To receive money

from someone

11%Miscellaneous

Of those who only have a

mobile money account, the

majority do not use their

accounts for any activities.

PAKISTAN

2015: Bank account ownership among registered mobile money

account holders(Shown: Percentage of mobile money account holders, n=74)

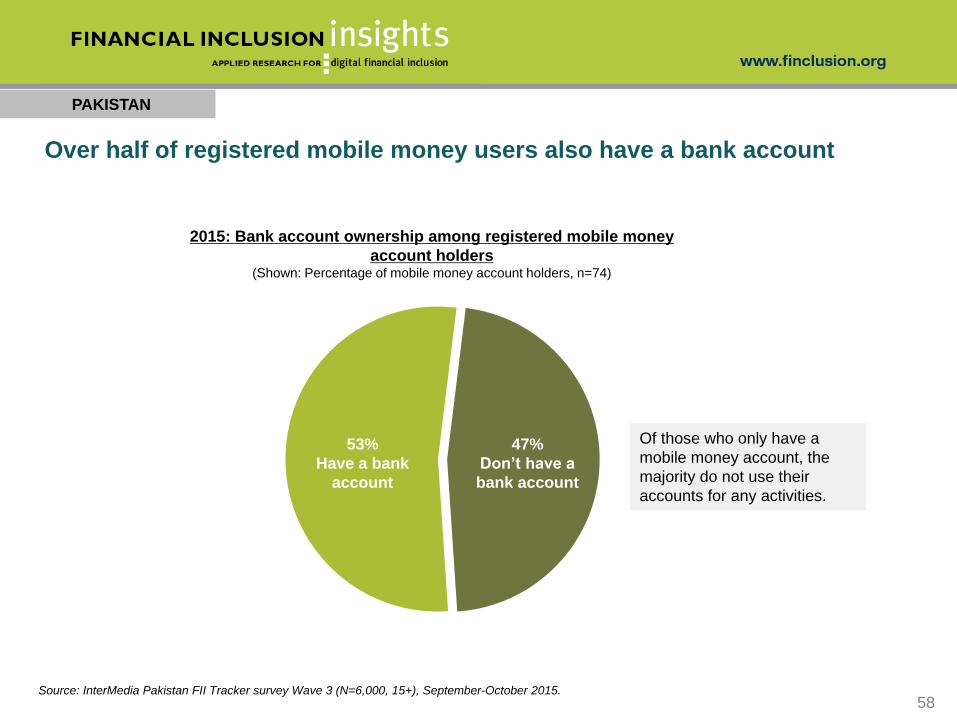

Over half of registered mobile money users also have a bank account

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.58

53%

Have a bank

account

47%

Don’t have a

bank account

20%

22%

60%

78%

90%

89%

21%

17%

21%

86%

70%

78%

Make retail payments

Get a loan

Save money

Send money

Keep money on the phone

Deposit and withdraw money

PAKISTAN

2015: Awareness of mobile money account functions(Shown: Percentage of registered and unregistered mobile money users)

59

Registered users are more likely than OTC users to realize they can save money

on mobile money accounts

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Question allowed for multiple responses.

Registered users

(n=74)

OTC

(n=510)

PAKISTAN

OTC mobile money users are much more likely than registered account

holders to live within 5 kilometers of a mobile money agent

60Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

55%

82%

52%

Nonusers(n=5,416)

OTC users(n=510)

Registered users(n=74)

2015: Five-kilometer proximity to a mobile money agent from home(Shown: Percentage of adults, by mobile money use type)

51%

59%

63%

71%

75%

95%

14%

28%

46%

33%

55%

88%

Internet

Call or SMS from mobilemoney provider

Family

Official mobile moneycompany materials

Friends

Mobile money agents

PAKISTAN

2015: Source of information on mobile money(Shown: Percentage of registered and unregistered mobile money users)

61

Mobile money users are learning about the services through multiple

avenues, including word-of-mouth and official company materials

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Question allowed for multiple responses.

Registered users

(n=74)

OTC

(n=510)

0.9%

2%

2%

6%

25%

65%

0.6%

0.7%

1%

24%

5%

69%

Friends

Customer service

Family

Mobile money transactionsnever go wrong

Resolve it oneself

Mobile money agents

PAKISTAN

2015: Preferred means of mobile money troubleshooting(Shown: Percentage of registered and unregistered mobile money users)

62

OTC mobile money users are much less likely to be able to resolve service

issues on their own

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

Registered users

(n=74)

OTC

(n=510)

PAKISTAN

86%

14%

Reason for not signing up for mobile money(Shown: Percentage of OTC users, n=510)

%

I don’t need to, I don’t make any transactions 27

I can have all the services I need through an agent 16

I never have money to make a transaction 13

Using an account is difficult 8

Fees for using such an account are too high 8

I don’t see any advantages to registration 7

I don’t understand the purpose of an account 6

OTC users continue to make up the majority of mobile money users;

perceived lack of need is an obstacle to registered use

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.

2015: Mobile money use: registered vs. OTC(Shown: Percentage of mobile money users, n=584)

63

Registered use Over-the-counter (OTC) use

PAKISTAN

2015: OTC users’ mobile money confidence(Shown: Percentage of OTC mobile money users, n=510)

2015: Reasons for not being able to operate a

mobile money account(Shown: Percentage of OTC mobile money users who can’t

perform transactions on their own, n=146)

12%

43%

52%

Won't know how to problem solve

Afraid of making a mistake

Don't understand it technically

OTC users who believe they can’t use mobile money on their own feel

hindered by a lack of technical skills

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.64

42%can perform

transactions on

their own 28%can’t perform

transactions on

their own

30%don’t know,

refused

PAKISTAN

Preferred location %

Near home 70

Food shops 54

Mobile phone shops 51

Transportation hubs 41

Near school/childcare 27

Near work 18

2015: OTC users’ preference for mobile

money agent locations(Shown: Percentage of OTC mobile money users, n=510)

Having a nearby mobile money agent is most important to OTC users; only

Easypaisa has agents within proximity of more than half of all OTC users

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.65

4%

5%

8%

12%

16%

34%

36%

86%

MCB Mobile

Warid Mobile Paisa

HBL Express

Zong Timepey

Ufone/ Upayment

UBL Omni

Mobilink Mobicash

Easypaisa

2015: OTC users’ view of which mobile

money agents are near their homes(Shown: Percentage of OTC mobile money users, n=510)

NONBANK FINANCIAL INSTITUTIONS

PAKISTAN

66

PAKISTAN

NBFIs do not play a significant role in the Pakistani financial inclusion

landscape

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.67

47%

only use

NBFIs

53%

have bank

or mobile

money

accounts

1%of adults have

used a nonbank

financial institution

This accounts

for 0.5% of the

total population.

2015: NBFI use(Shown: Percentage of Pakistani adults, N=6,000)

2015: NBFI users’ use of other financial services(Shown: Percentage of NBFI users, n=67)

PAKISTAN

0.5%

12%

90%

State Life Insurance Corporation

Microfinance institutions

ROSCA/committees

2015: Use of NBFIs, including non-full-service institutions*(Shown: Percentage of NBFI users, n=715)

2015: The gender divide in ROSCA use(Shown: Percentage of ROSCA users, n=646)

ROSCAs are the most widely used form of NBFI; women are much more

likely to be ROSCA users than are men

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.68

73%

Female

27%

Male

*All numbers shown in this slide are based on access to any kind of NBFI, including credit-only and those that are neither credit-only nor full-service institutions.

PAKISTAN

2015: Negative experiences with ROSCA use(Shown: Percentage of ROSCA users, n=646)

Money/cash not available immediately 74%

Disagreement among the group 67%

Loss of membership 64%

Poor leadership 62%

Lost money through bad investments 61%

Fraud by a ROSCA member 61%

Default by members 61%

Fraud by an outsider 59%

Most ROSCA members have had at least one negative experience; lack of

available cash is the most common

Source: InterMedia Pakistan FII Tracker survey Wave 3 (N=6,000, 15+), September-October 2015.69

METHODOLOGY & RESEARCH DESCRIPTION

PAKISTAN

70

Survey Summary

• Annual, nationally representative survey (N=6,000) of Pakistani adults aged 15+

• Face-to-face interviews lasting, on average, 44 minutes

• Third survey (wave 3) conducted from 9/03/2015 to 10/30/2015

• Tracks trends and market developments in DFS based on the information gathered in the first survey,

conducted in 2013, and second survey conducted in 2014

Data Collection

• Basic demographics and poverty measurement (Grameen Progress Out of Poverty Index)

• Access/use of mobile devices

• Access/use of mobile money

• Access/use of formal financial services (e.g., bank accounts)

• Access/use of semi-formal and informal financial services (e.g., MFIs, cooperatives, village savings groups)

• Financial literacy and preparedness

• General financial behaviors

PAKISTAN

FII Pakistan Tracker Survey details

71

Sampling Frame • A nationally representative sample of adults (defined as those aged 15 or above) was developed using 2011-12 national population

projections based on 1998 Census Data.

• The total sample was distributed proportionally to the size of the population within urban and rural strata in each of Pakistan’s four

provinces – excluding the federally administered tribal areas.

• The total population was further administratively divided into 5,000 census-defined urban circles and 48,000 rural mouzas.

Primary Sampling Units (PSUs)

•Within urban strata, census circles and within rural strata, mouzas were selected proportionally to their population size.

•Ten interviews were conducted in each selected urban circle and mouza primary sampling unit.

•For security reasons, PSUs were divided randomly between male and female interviewing teams.

Sampling Start-Points, Households and Respondents

• The census circles and villages to which sampling points were assigned were mapped into blocks and a block was randomly selected. The

household within the selected block from which interviewing commenced was selected by generating a random number between one and 10,

and skipping that number of households from the first household that interviewers encountered when entering the block.

•After completing an interview at the randomly selected first household, subsequent households were selected using the right-hand rule (every

fifth household in urban areas and every third household in rural areas).

• One respondent from each household was selected using the Kish grid method, and relevant consent for eligible respondents under 18 years

of age was obtained.

PAKISTAN

SAMPLING METHODOLOGY

72

GLOSSARY

PAKISTAN

73

GLOSSARY

74

• Access – Access to a bank account or mobile money account means a respondent can use bank/mobile money services either via their own

account or via an account of another person.

• Active account holder – An individual who has a registered financial account and has used it in the last 90 days.

• Active user – An individual who has used any financial account for any type of transaction in the past 90 days via his/her own account or

somebody else’s account.

• Adults with DFS access – Adults who either own a DFS account or have access to someone else’s account.

• Below the poverty line – In this particular study, adults living on less than $2.50 per day, as classified by the Grameen PPI.

• Credit-only financial institutions – Financial institutions that only offer loan disbursement services to their customers.

• Digital financial services (DFS) – Financial services provided through an electronic platform (mobile phones, electronic cards, the internet,

etc.). For this particular study, digital financial services include bank services and mobile money services.

• Mobile money (MM) – A service in which a mobile phone is used to access financial services.

• Mobile-money value-added services –Individually branded service products offered by mobile money providers in addition to or along

with their basic mobile money services.

• Registered active user – A person with a registered DFS account that has used it in the last 90 days.

• ROSCA/committee – An informal rotating savings and credit association (ROSCA) whose members are a group of individuals who agree

to meet for a defined time period to save and borrow together, a form of combined peer-to-peer banking and peer-to-peer lending.

• Services beyond basic wallet – DFS transactions that go beyond simple deposits, withdrawals or money transfers.

• Urban/rural – Urban and rural persons are defined according to their residence in urban or rural areas as prescribed by the national bureau

of statistics.

• Grameen Progress out of Poverty Index (PPI) – A poverty measurement tool from the Grameen Foundation wherein a set of

country-specific questions are used to compute the likelihood that a household is living below the poverty line.

• Financially included – Individuals who have registered for a financial service account with a full-service financial institution.

• Full-service institutions – A financial institution that offers customers at least one of the following services: savings, money transfers,

insurance or investments.

For more information, contact:

Nat Kretchun, FII Asia Lead

Imran Khan, FII Pakistan [email protected]

Caldwell Bishop, Research Manager