Embed Size (px)

Citation preview

Pakistan Power SectorNeed for Reforms

By Kalim A. Siddiqui

President-Petroleum MarketingByco Petroleum Paksitan Limited

3rd Pakistan Oil & Gas Conference 2011 – January 29, 2011

Outline

• Overview of Pakistan Energy Sector

• Reasons for Power Crisis

• Need for Reforms

• Roadmap towards reform

January 31, 20113rd Pakistan Oil & Gas Conference 2011, Islamabad

Pakistan Power SectorNeed for Reforms

Overview of Pakistan Energy Sector

January 31, 20113rd Pakistan Oil & Gas Conference 2011, Islamabad

Overview of Pakistan Energy SectorEnergy Mix

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Source: Economic Survey of Pakistan 2009-10

Energy Consumption of 37.4 Mn TOE in 2009-10Energy Consumption of 37.4 Mn TOE in 2009-10

Overview of Pakistan Energy SectorEnergy Mix - Comparison with global trend

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Source: Economic Survey of Pakistan 2009-10, EIA

World Pakistan

Overview of Pakistan Energy SectorA Profile

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Transmission System:NTDC : 5,177 km; 500kV

7,500 km; 220kVDISCOs: 31,000 km; 132kV

7,800 km; 66kV

Total KESC

Energy Generation 90 TWh 9 TWh

No. of Customers 20.7 Mn 2.0 Mn

T&D Losses 21% 34%

Source: Nepra

Overview of Pakistan Energy SectorPower Sources

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Source: Economic Survey of Pakistan , WAPDA

Total Installed Generation Capacity of 20, 190 MW in 2009-10 Total Installed Generation Capacity of 20, 190 MW in 2009-10

Overview of Pakistan Energy Sector Energy Consumption & Output

3rd Pakistan Oil & Gas Conference 2011, Islamabad

Average annual Consumption of electricity in the last 10 years has increased by nearly 5%, 73 Mn MWh of electricity being consumed in FY 2010 (-1.7% growth from FY 2009).

January 31, 2011

Source: Economic Survey of Pakistan 2009-10, Hydrocarbon Development Institute of Pakistan

Overview of Pakistan Energy SectorSupply and Demand Gap

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011Source: Websites of Wapda, Nepra

Pakistan Power SectorNeed for Reforms

Reasons for power crisis

January 31, 20113rd Pakistan Oil & Gas Conference 2011, Islamabad

Major Reasons for Power Crisis

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Lack of utilisation of alternative energy sources like coal, solar, wind, gas and nuclearLess emphasis and awareness regarding use of renewable sources of energy (wind, solar, waste to energy, etc)Availability and supply for natural gas for power generation

Lack of utilisation of alternative energy sources like coal, solar, wind, gas and nuclearLess emphasis and awareness regarding use of renewable sources of energy (wind, solar, waste to energy, etc)Availability and supply for natural gas for power generation

Alternate Energy

Alternate Energy

Lack of long term sustainable roadmap of power generationPlan to produce low cost power due to better mix of power generation sources Ineffective utilisation of installed power generation capacity

Lack of long term sustainable roadmap of power generationPlan to produce low cost power due to better mix of power generation sources Ineffective utilisation of installed power generation capacity

PlanningPlanning

Inefficiency due to ageing power generation equipment and old technologyWaste of energy due to line losses (technical and theft)Up -gradation of distribution network

Inefficiency due to ageing power generation equipment and old technologyWaste of energy due to line losses (technical and theft)Up -gradation of distribution network

Technical Losses

Technical Losses

Major Reasons for Power Crisis

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Uncertain law and order situationPolitical stability and continuity of government policies is vitalAlternate gas availability projects not materialized ( e.g. LNG, QP, IPI and TAPI) and need to expedite local exploration activities

Uncertain law and order situationPolitical stability and continuity of government policies is vitalAlternate gas availability projects not materialized ( e.g. LNG, QP, IPI and TAPI) and need to expedite local exploration activities

No major water reservoirs/dams developed in over 3 decadesCoal reservoir not developed timelySlow development of Hydrocarbon projects Mismatch of economic progress and increasing power generation capacities

No major water reservoirs/dams developed in over 3 decadesCoal reservoir not developed timelySlow development of Hydrocarbon projects Mismatch of economic progress and increasing power generation capacities

Development issues

Development issues

Investment Crisis

Investment Crisis

High cost of furnace oil (price volatility)Circular DebtPoor mix of power generation sources linked to high cost

High cost of furnace oil (price volatility)Circular DebtPoor mix of power generation sources linked to high cost

Electricity price

Electricity price

Pakistan Power SectorNeed for Reforms

Need for Reforms

January 31, 20113rd Pakistan Oil & Gas Conference 2011, Islamabad

Need for ReformGlobal Trends Observed

3rd Pakistan Oil & Gas Conference 2011, Islamabad

• Ever increasing energy demands creating shortfalls in developed and emerging economies

• Increased competition between strategic players for energy

• Volatility/rise in furnace oil prices directing the development on alternative energy sources

• Increasing correlation between energy use and environmental impact such as carbon emissions, conservation and protection

January 31, 2011

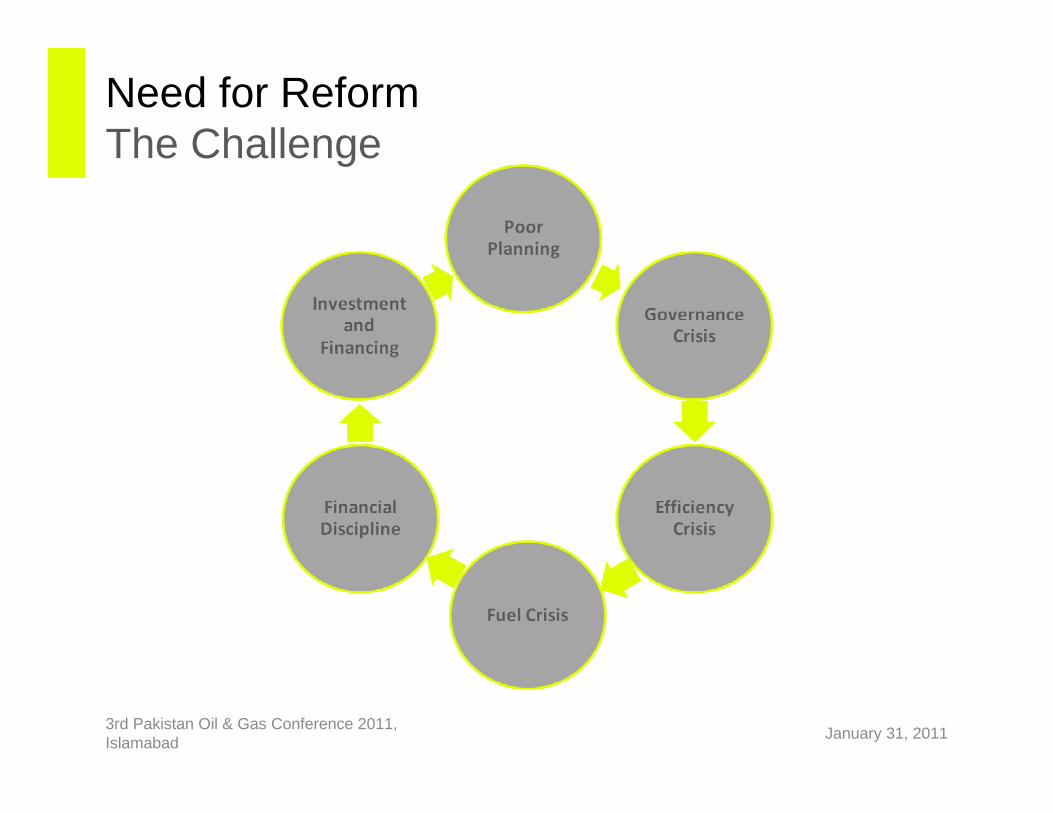

Need for ReformThe Challenge

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Need for ReformDrivers of Power Sector Reform

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Capital ScarcityCapital Scarcity Economic Inefficiencies

Economic Inefficiencies

Industrial Development

Industrial Development Debts and DeficitsDebts and Deficits

•The power sector is a direct victim of lack of capital. Governments have been unable to spend on this sector over the years

•The challenge is reforming the power sector to attract the needed private investment

•The power sector is a direct victim of lack of capital. Governments have been unable to spend on this sector over the years

•The challenge is reforming the power sector to attract the needed private investment

•The power sector in Pakistan is saddled with large debts accumulated from years of not charging cost recovery tariffs, not collecting from all consumers, not disconnecting consumers who do not pay, and using the utility as a vehicle for subsidies and political patronage for jobs and other favors

•The power sector in Pakistan is saddled with large debts accumulated from years of not charging cost recovery tariffs, not collecting from all consumers, not disconnecting consumers who do not pay, and using the utility as a vehicle for subsidies and political patronage for jobs and other favors

•Lack of power generation has adversely affected industrial activity in Pakistan

•Lack of power generation has adversely affected industrial activity in Pakistan

•The power sector has been troubled by high technical losses, a lack of power generating cost recovery, poor maintenance, low equipment reliability, high staff levels, low productivity, corruption, a crippling non-payments problem, and mounting debt

•The power sector has been troubled by high technical losses, a lack of power generating cost recovery, poor maintenance, low equipment reliability, high staff levels, low productivity, corruption, a crippling non-payments problem, and mounting debt

Need for ReformEnergy Threats and Opportunity -Pakistan

Threats Opportunity

•Imported oil constitutes over 29% of energy consumption, at a very high cost due to import dependency.

• The depletion/decline of Pakistan’s natural gas reserves/production

• Energy prices are expected to increase over the next few years.

•To reduce poverty and increase prosperity – the energy consumption in Pakistan has to increase.

• The price and availability of natural gas and oil have grave impacts welfare and national security.

•India’s appetite for energy is escalating – natural gas pipelines from either Iran or Central Asia will have to pass through Pakistan.

•LNG for India is an option but at a much higher price.

•Develop energy corridor by partnering with China to provide energy to its western regions.

•Pipeline option can be attractive.

•Utilisation of Pakistan’s coal reserves could a big step towards solving Pakistan’s energy crisis.

Pakistan Power SectorNeed for Reforms

Roadmap Towards Reform

January 31, 20113rd Pakistan Oil & Gas Conference 2011, Islamabad

Roadmap Towards ReformMajor Potential Areas

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

InvestmentInvestment GovernanceGovernance Diversification

Diversification

Infrastructure

Infrastructure

• Fostering the environment to bring in foreign Investment in the power sector

• Fostering the environment to bring in foreign Investment in the power sector

• Improve existing infrastructure and upgrade it with latest technology for efficiency enhancement

• Improve existing infrastructure and upgrade it with latest technology for efficiency enhancement

• Developing sources of alternate Energy and encouraging diversification of energy mix

• Developing sources of alternate Energy and encouraging diversification of energy mix

• Resolve governance and organizational issues to streamline institutions and reduce flaws

• Stability in policy making and proper planning

• Resolve governance and organizational issues to streamline institutions and reduce flaws

• Stability in policy making and proper planning

EfficiencyEfficiency

• Reduction of inefficiencies

• Collection of dues

• Efficiency in transmission systems

• Reduction of inefficiencies

• Collection of dues

• Efficiency in transmission systems

R & DR & D

• Encourage research and development

• Spending on new technologies

• Encourage research and development

• Spending on new technologies

Vibrant economy with increasing

demand for power.

Vibrant economy with increasing

demand for power.

Attractive and competitive return

on investment

Attractive and competitive return

on investment

Roadmap Towards ReformIncentives to invest in Pakistan Power Sector

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

One‐window facility provided by Private Power Infrastructure Board for PrivateProjects

One‐window facility provided by Private Power Infrastructure Board for PrivateProjects

Balanced risk profile for

investors, lenders and government

agencies

Balanced risk profile for

investors, lenders and government

agencies

Independent regulator to

balance interest of consumers and

power sector companies

Independent regulator to

balance interest of consumers and

power sector companies

Track record of successful private

sector participation (5599 MW ;US$ 6 billion)

Track record of successful private

sector participation (5599 MW ;US$ 6 billion)

Identified hydropower

potential of over 54,000 MW

Identified hydropower

potential of over 54,000 MW

Confirmed wind energy potential of more than 346,000 MW and solar power potentialof over 2.9 million MW

Confirmed wind energy potential of more than 346,000 MW and solar power potentialof over 2.9 million MW

Proven coal reserves of 175 billion tons in Thar generating a potential of 100,000 MWs @ 536 million tons per year

Proven coal reserves of 175 billion tons in Thar generating a potential of 100,000 MWs @ 536 million tons per year

Source: PPIB Website

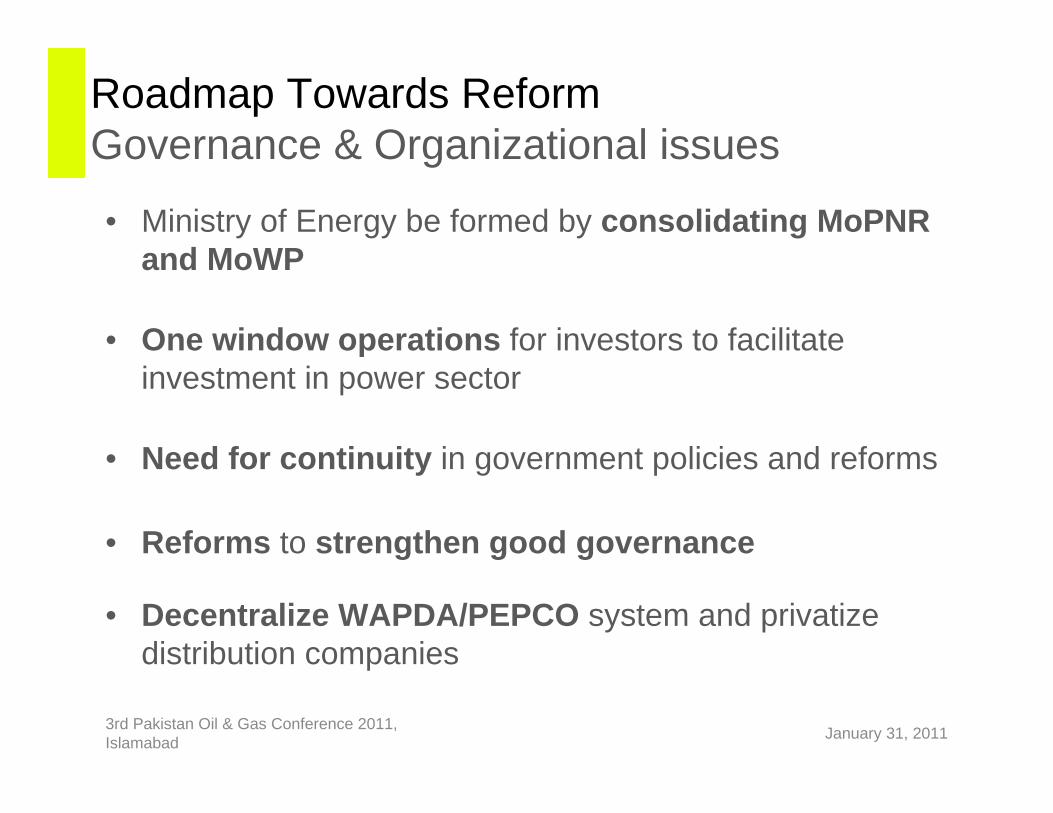

Roadmap Towards ReformGovernance & Organizational issues

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• Ministry of Energy be formed by consolidating MoPNR and MoWP

• One window operations for investors to facilitate investment in power sector

• Need for continuity in government policies and reforms

• Reforms to strengthen good governance

• Decentralize WAPDA/PEPCO system and privatize distribution companies

Roadmap Towards ReformAlternate Energy

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• Availability of low cost power generation mix

• Increase share of nuclear, hydel and coal based power projects in the country’s energy mix

• Encourage and facilitate private sector participation

• Foster development of renewable energy sources such as Wind, Solar, Ocean Waves, etc

• Policies to establish alternate energy sources so that market potential is clearly visible to MNCs and International investors

• Develop Global alliances for energy security

Roadmap Towards ReformAlternate Energy - Examples

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• Initial development alone could bring in investment of USD 12 Billion

• Entire Thar Coal Reserves can be used to generate 100,000 MW of electricity for over 200 years with cost and environmental benefits

Thar Desert contains the world’s 7th largest coal reserves:

175 Billion Ton = 50 Billion TOE = 2000 TCFTotal Thar Coal Reserve More than Saudi Arabia 68 times higher than

& Iranian Oil Reserves Pakistan’s total gas reserves

Source: Thar Coal Mining & Power Generation Project – Engro Powergen

1% = 25%Pakistan’s Power Generation Capacity in 2010

Thar Coal Reserve

Roadmap Towards ReformAlternate Energy - Examples

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

•Total Area of Sindh suitable for wind farms = 9,749 km2

•Gross wind power potential of Sind Coast is 43 kMW

• Exploitable electric power generation potential of this area is 11 kMW

•Total Area of Sindh suitable for wind farms = 9,749 km2

•Gross wind power potential of Sind Coast is 43 kMW

• Exploitable electric power generation potential of this area is 11 kMWLandhi Bio Gas Project

Landhi Cattle Colony (spread over an area of 18,500 hectares) is expected to produce 15-20 MW of renewable energy for KESCFrom 3,000 MT of manure (daily being discharged into the Sea).

Pakistan is the 6th luckiest country in the world where sun-availability is up to 16 hours on average

Pakistan is the 6th luckiest country in the world where sun-availability is up to 16 hours on average

Pakistan has about 1000 km long coastline of with complex network of creeks showing relevance of strong wave energy, which could be harness for the generation of electric power for rapidly developing coastal cities

Sources: KESC, Pakistan Meteorological Dept, Other media sources

Roadmap Towards ReformAlternate Energy

January 31, 2011

Nuclear Energy Sites

Roadmap Towards ReformInfrastructure

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• Effective and efficient utilization of existing power generation infrastructure

• Capacity Additions through thermal and hydro power projects

• Expedite projects such as power projects (nuclear, coal, solar, wind, etc) pipelines (Qatar, IPI and TAPI) and large as well as small and medium sized dams

Roadmap Towards ReformInfrastructure

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

Proposed Dams in the country

Roadmap Towards ReformInfrastructure

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• Transmission Projects need to be developed for evacuation of power from hydro projects in the north and from thermal projects in south

• Distribution system needs to be modernized by use of smart metering systems

Roadmap Towards ReformInfrastructure – Example of Power Parks

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• To facilitate investment on fast track basis, there is a need to establish Power Parks

• These will be located at 4-5 strategic locations near river or canal head for availability of water, and near main highway or rail link for transportation of fuel in addition to the availability of utilities

• These Parks will house 4000-5000 MW capacity plants which serve as ‘base load plants’

• These will be based on coal and gas, local or imported

Source: Nepra

Roadmap Towards ReformEfficiency

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• Transmission and distribution losses to be curtailed to reduce cost of generation

• Reducing illegal use and theft as well as encourage efficiency in usage and savings

• Improving efficiencies through latest technologies and better governance

• Recovery of billed amounts and financial discipline

Roadmap Towards ReformResearch & Development

3rd Pakistan Oil & Gas Conference 2011, Islamabad January 31, 2011

• Integrated energy plan for the country

• Roadmap for progression

• Develop R&D mechanisms in the country

• Synergy between nuclear, hydel and coal/gas energy and environment policies

• Foster niche markets for early commercialization of new technologies and development of alternative energies such as Wind, Solar, Ocean Waves, Bio-technology, etc

Thank You