Embed Size (px)

Citation preview

Part 4 Financial Statements Department of Health and Human Services

Statement of Comprehensive Income for the Year Ended 30 June 2012 210

Statement of Financial Position as at 30 June 2012 212

Statement of Cash Flows for the Year Ended 30 June 2012 213

Statement of Changes in Equity for the Year Ended 30 June 2012 215

Notes to and Forming Part of the Financial Statements for the Year Ended 30 June 2012 216

Independent Auditor’s Report 313

Statement of Certification 315

Tasmanian Ambulance Service

Statement of Comprehensive Income for the Year Ended 30 June 2012 317

Statement of Financial Position as at 30 June 2012 319

Statement of Changes in Equity for the Year Ended 30 June 2012 320

Notes to and Forming Part of the Financial Statements for the Year Ended 30 June 2012 320

Independent Auditor’s Report 351

Statement of Certification 353

DHHS Annual Report 2011-2012 – Part 4 – Financial Statements Page 209 of 355

Financial Statements Department of Health and Human Services

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 210 of 355

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Continuing Operations

Revenue and Other Income from Transactions

Revenue from Government

Appropriation revenue - recurrent 2.9(a) 1 488 161 1 530 234 1 522 158

Appropriation revenue - works and services 2.9(a) 480 9 768 1 336

Other revenue from Government 2.9(a) 0 0 2 995

Revenue from Special Capital Investment Funds 13 249 13 249 9 850

Grants 2.9(b), 8.1 65 000 63 600 59 742

Sales of goods and services 2.9(c), 8.2 175 942 185 868 168 958

Interest 2.9(d) 1 371 770 2 344

Contributions received 2.9(e), 8.3 0 0 90

Other revenue 2.9(f), 8.4 24 445 39 554 29 918

Total Revenue and Other Income from Transactions 1 768 648 1 843 043 1 797 391

Expenses from Transactions

Employee benefits 2.10(a), 9.1 964 094 1 002 020 971 688

Depreciation and amortisation 2.10(b), 9.2 51 857 61 044 59 467

Supplies and consumables 9.3 446 807 462 719 471 341

Grants and subsidies 2.10(c), 9.4 275 588 306 187 234 504

Borrowing costs 2.10(d), 9.5 9 623 9 626 9 913

Other expenses 2.10(f), 9.6 71 230 69 056 78 835

Total Expenses from Transactions 1 819 199 1 910 652 1 825 748

Net Result from Transactions (Net Operating Balance) ( 50 551) ( 67 609) ( 28 357)

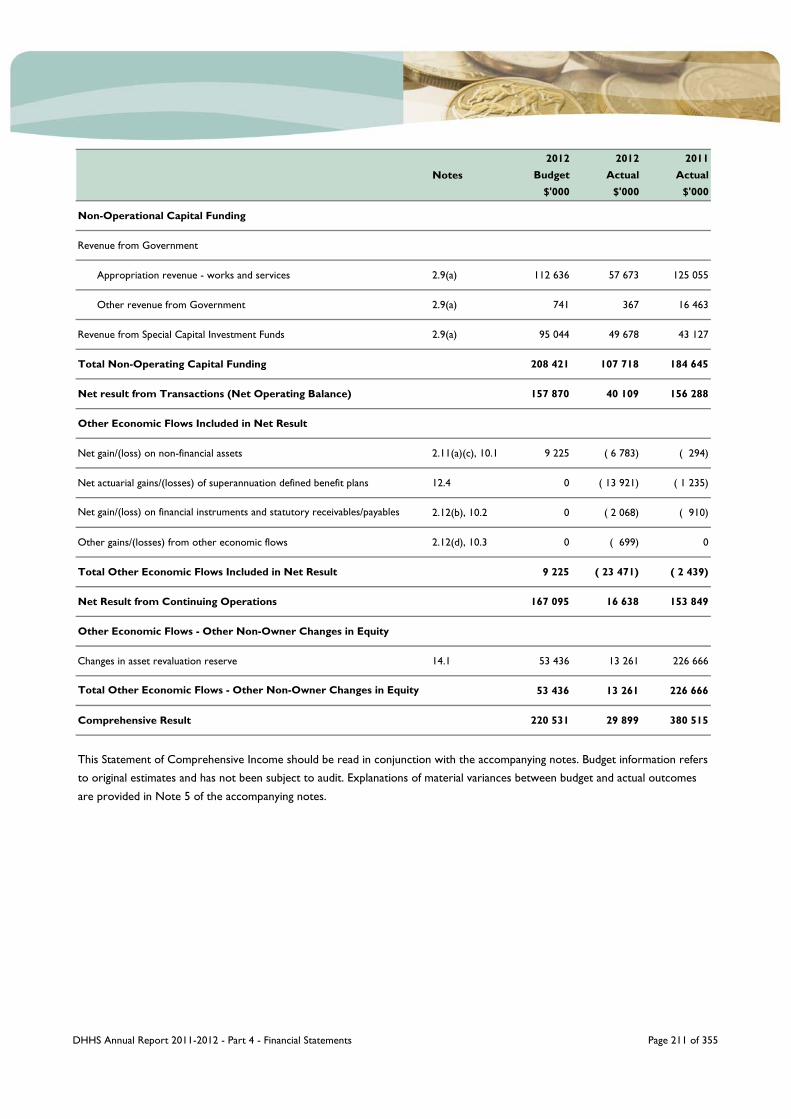

Department of Health and Human Services Statement of Comprehensive Income for the Year Ended 30 June 2012

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 211 of 355

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Non-Operational Capital Funding

Revenue from Government

Appropriation revenue - works and services 2.9(a) 112 636 57 673 125 055

Other revenue from Government 2.9(a) 741 367 16 463

Revenue from Special Capital Investment Funds 2.9(a) 95 044 49 678 43 127

Total Non-Operating Capital Funding 208 421 107 718 184 645

Net result from Transactions (Net Operating Balance) 157 870 40 109 156 288

Other Economic Flows Included in Net Result

Net gain/(loss) on non-financial assets 2.11(a)(c), 10.1 9 225 ( 6 783) ( 294)

Net actuarial gains/(losses) of superannuation defined benefit plans 12.4 0 ( 13 921) ( 1 235)

2.12(b), 10.2 0 ( 2 068) ( 910)

Other gains/(losses) from other economic flows 2.12(d), 10.3 0 ( 699) 0

Total Other Economic Flows Included in Net Result 9 225 ( 23 471) ( 2 439)

Net Result from Continuing Operations 167 095 16 638 153 849

Other Economic Flows - Other Non-Owner Changes in Equity

Changes in asset revaluation reserve 14.1 53 436 13 261 226 666

53 436 13 261 226 666

Comprehensive Result 220 531 29 899 380 515

This Statement of Comprehensive Income should be read in conjunction with the accompanying notes. Budget information refers

to original estimates and has not been subject to audit. Explanations of material variances between budget and actual outcomes

are provided in Note 5 of the accompanying notes.

Total Other Economic Flows - Other Non-Owner Changes in Equity

Net gain/(loss) on financial instruments and statutory receivables/payables

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 212 of 355

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Assets

Financial Assets

Cash and deposits 2.12(a), 15.1 56 169 85 650 61 035

Receivables 2.12(b), 11.1 23 663 22 783 21 457

Loan advances 2.12(c), 11.2 5 500 4 567 5 855

Equity investments 2.12(d), 11.3 4 059 4 623 3 152

Other financial assets 2.12(e), 11.4 10 095 6 720 10 015

Non-Financial Assets

Inventories 2.12(f), 11.5 13 062 13 832 11 265

Assets held for sale 2.12(g), 11.6 6 839 6 093 8 841

Property, plant and equipment 2.12(h), 11.7 2 991 396 2 898 600 2 867 035

Intangibles 2.12(i), 11.8 11 384 16 399 13 716

Other assets 2.12(j), 11.9 0 5 090 5 377

Total Assets 3 122 167 3 064 357 3 007 748

Liabilities

Payables 2.13(a), 12.1 27 823 38 760 40 431

Interest bearing liabilities 2.13(b), 12.2 209 808 209 808 216 620

Employee benefits 2.13(d), 12.3 217 330 208 492 183 930

Superannuation 2.13(e), 12.4 15 036 29 228 15 645

Other liabilities 2.13(f), 12.5 60 224 43 716 47 255

Total Liabilities 530 221 530 004 503 881

Net Assets 2 591 946 2 534 353 2 503 867

Equity

Contributed capital 6 094 6 094 6 094

Reserves 14.1 1 788 296 1 921 389 1 908 128

Accumulated funds 797 556 606 870 589 645

Total Equity 2 591 946 2 534 353 2 503 867

This Statement of Financial Position should be read in conjunction with the accompanying notes. Budget information refers to original

estimates and has not been subject to audit. Explanations of material variances between budget and actual outcomes are provided in

Note 5 of the accompanying notes.

Department of Health and Human Services Statement of Financial Position as at 30 June 2012

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 213 of 355

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Cash Flows from Operating ActivitiesInflows

(Outflows)

Inflows

(Outflows)

Inflows

(Outflows)

Cash Inflows

Appropriation receipts - recurrent 1 488 161 1 530 234 1 519 952

Appropriation receipts - works and services 480 6 980 3 542

13 249 13 249 9 850

Grants 65 000 63 666 60 113

Sales of goods and services 174 518 187 139 165 597

GST receipts 60 061 87 293 87 780

Interest received 1 371 701 2 071

Other cash receipts 28 075 41 306 38 315

Total Cash Inflows 1 830 915 1 930 568 1 887 220

Cash Outflows

Employee benefits ( 855 505) ( 883 839) ( 874 108)

Superannuation ( 86 172) ( 93 307) ( 91 705)

Borrowing costs ( 9 623) ( 9 626) ( 9 913)

GST payments ( 60 060) ( 85 912) ( 90 569)

Grants and transfer payments ( 275 588) ( 260 833) ( 233 987)

Supplies and consumables ( 447 032) ( 469 113) ( 480 365)

Other cash payments ( 70 650) ( 79 467) ( 79 053)

Total Cash Outflows (1 804 630) (1 882 097) (1 859 701)

Net Cash from (Used By) Operating Activities 15.2 26 285 48 471 27 519

Department of Health and Human Services Statement of Cash Flows for the Year Ended 30 June 2012

Receipts from Special Capital Investment Funds

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 214 of 355

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Cash Flows from Investing Activities

Cash Inflows

Proceeds from the disposal of non-financial assets 15 640 12 662 17 942

Receipts from non-operational capital funding - Works and services 112 636 60 945 125 472

95 044 50 222 42 583

Receipts from non-operational capital funding - Grants 0 0 0

Repayment of loans by other entities 0 1 167 1 186

Total Cash Inflows 223 320 124 996 187 183

Cash Outflows

Payment for acquisition of non-financial assets ( 238 463) ( 141 479) ( 229 485)

Payments for investments ( 3 400) ( 561) ( 747)

Total Cash Outflows ( 241 863) ( 142 040) ( 230 232)

Net Cash from (Used By) Investing Activities ( 18 543) ( 17 044) ( 43 049)

Cash Flows from Financing Activities

Cash Outflows

Repayment of borrowings ( 6 812) ( 6 812) ( 6 669)

Total Cash Outflows ( 6 812) ( 6 812) ( 6 669)

Net Cash from (Used By) Financing Activities ( 6 812) ( 6 812) ( 6 669)

Net Increase (Decrease) in Cash and Cash Equivalents Held 930 24 615 ( 22 197)

Cash and Deposits at the Beginning of the Reporting Period 55 239 61 035 83 232

Cash and Deposits at the End of the Reporting Period 15.1 56 169 85 650 61 035

Receipts from non-operational capital funding - Special Capital Investment Funds

This Statement of Cash Flows should be read in conjunction with the accompanying notes. Budget information refers to original

estimates and has not been subject to audit. Explanations of material variances between budget and actual outcomes are

provided in Note 5 of the accompanying notes.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 215 of 355

Contributed Capital

$'000

Reserves $'000

Accumulated

Funds $'000

Total Equity $'000

Balance as at 1 July 2011 6 094 1 908 128 589 645 2 503 867

Adjustment due to prior period error 1 0 0 587 587

Total comprehensive result 0 13 261 16 638 29 899

Balance as at 30 June 2012 6 094 1 921 389 606 870 2 534 353

Contributed Capital

$'000

Reserves $'000

Accumulated

Funds $'000

Total Equity $'000

Balance as at 1 July 2010 6 094 1 681 462 435 728 2 123 285

Adjustment due to prior period error 0 0 65 65

Total comprehensive result 0 226 666 153 852 380 515

Balance as at 30 June 2011 6 094 1 908 128 589 645 2 503 867

This Statement of Changes in Equity should be read in conjunction with the accompanying notes.

Notes:

1 This is a prior period error of $587 000 relating to a correction of Equity Investment recognition.

Department of Health and Human Services Statement of Changes in Equity for the Year Ended 30 June 2012

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 216 of 355

Notes Page No.

Note 1 Administered Financial Statements 219

1.1 Schedule of Administered Income and Expenses 219

1.2 Schedule of Administered Assets and Liabilities 220

1.3 Schedule of Administered Cash Flows 221

1.4 Schedule of Administered Changes in Equity 221

Note 2 Significant Accounting Policies 222

2.1 Objectives and Funding 222

2.2 Basis of Accounting 222

2.3 Reporting Entity 223

2.4 Functional and Presentation Currency 223

2.5 Changes in Accounting Policies 223

2.6 Administered Transactions and Balances 227

2.7 Activities Undertaken Under a Trustee or Agency Relationship 227

2.8 228

2.9 Income from Transactions 228

2.10 Expenses from Transactions 229

2.11 Other Economic Flows Included in Net Result 231

2.12 Assets 232

2.13 Liabilities 234

2.14 Leases 237

2.15 Judgements and Assumptions 237

2.16 Foreign Currency 238

2.17 Comparative Figures 238

2.18 Budget Information 238

2.19 Rounding 238

2.20 Departmental Taxation 238

2.21 Goods and Services Tax 238

Note 3 Agency Output Schedules 239

3.1 Output Group Information 239

3.2 240

3.3 250

3.4 Administered Output Schedule 251

3.5 252

3.6 252

Note 4 Expenditure under Australian Government Funding Arrangements 252

Reconciliation of Total Output Groups Comprehensive Result to Statement of Comprehensive

IncomeReconciliation of Total Output Groups Net Assets to Statement of Financial Position

Reconciliation of Total Administered Output Groups Comprehensive Result to Administered

Statement of Changes in EquityReconciliation of Total Administered Groups' Net Assets to Schedule of Administered Assets and

Liabilities

Notes to and Forming Part of the Financial Statements for the Year Ended 30 June 2012

Transactions by the Government as Owner – Restructuring of Administrative Arrangements

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 217 of 355

Notes Page No.

Note 5 Explanations of Material Variances between Budget and Actual Outcomes 253

5.1 Statement of Comprehensive Income 253

5.2 Statement of Financial Position 255

5.3 Statement of Cash Flows 256

Note 6 Events Occurring After Balance Date 257

Note 7 Underlying Net Operating Balance 259

Note 8 Income from Transactions 260

8.1 Grants 260

8.2 Sales of Goods and Services 261

8.3 Contributions Received 261

8.4 Other Revenue 262

Note 9 Expenses from Transactions 262

9.1 Employee Benefits 262

9.2 Depreciation and Amortisation 263

9.3 Supplies and Consumables 264

9.4 Grants and Subsidies 265

9.5 Borrowing Costs 266

9.6 Other Expenses 266

Note 10 Other Economic Flows Included in Net Result 266

10.1 Net Gain/(Loss) on Non-Financial Assets 266

10.2 Net Gain/(Loss) on Financial Instruments and Statutory Receivables/Payables 266

10.3 Other Gains/(Losses) from Other Economic Flows 267

Note 11 Assets 267

11.1 Receivables 267

11.2 Loan Advances 268

11.3 Equity Investments 268

11.4 Other Financial Assets 268

11.5 Inventories 269

11.6 Assets Held for Sale 269

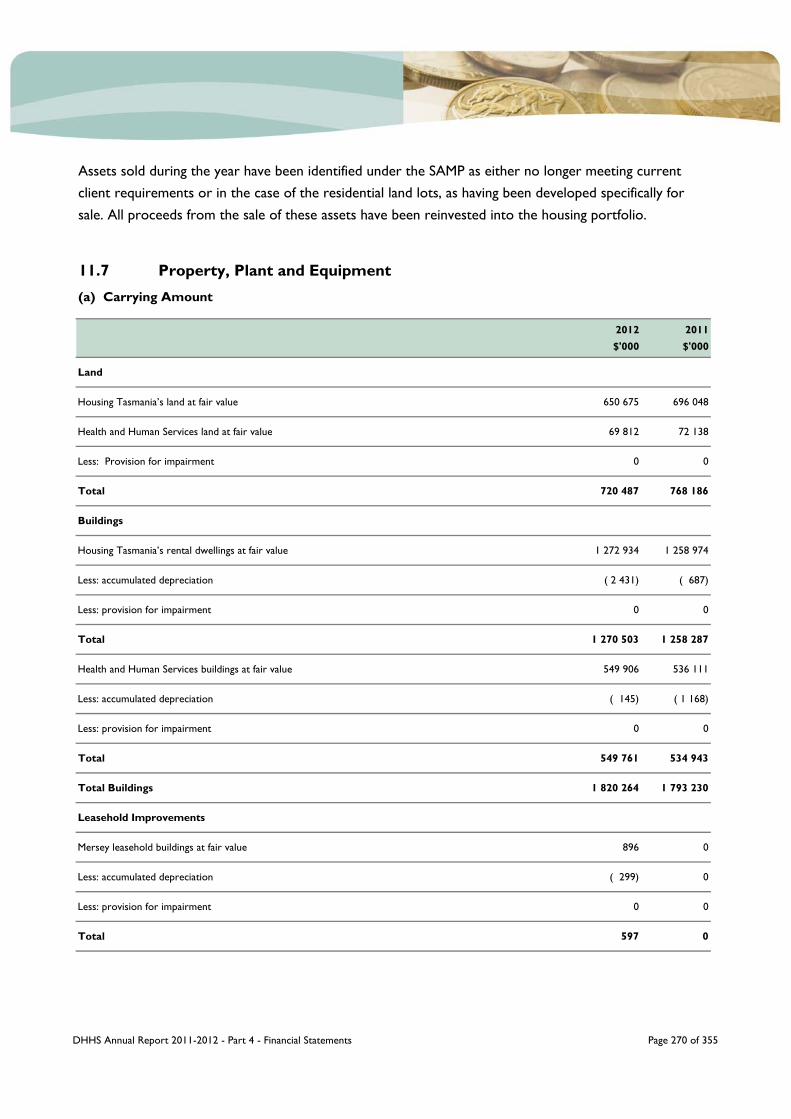

11.7 Property, Plant and Equipment 270

11.8 Intangibles 273

11.9 Other Assets 274

Note 12 Liabilities 274

12.1 Payables 274

12.2 Interest Bearing Liabilities 275

12.3 Employee Benefits 275

12.4 Superannuation 275

12.5 Other Liabilities 281

Note 13 Commitments and Contingencies 281

13.1 Schedule of Commitments 281

13.2 Contingent Assets and Liabilities 284

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 218 of 355

Notes Page No.

Note 14 Reserves 286

14.1 Reserves 286

Note 15 Cash Flow Reconciliation 286

15.1 Cash and Deposits 286

15.2 Reconciliation of Net Result to Net Cash from Operating Activities 287

15.3 Acquittal of Capital Investment and Special Capital Investment Funds 288

15.4 Financing Facilities 291

Note 16 Financial Instruments 291

16.1 Risk Exposures 291

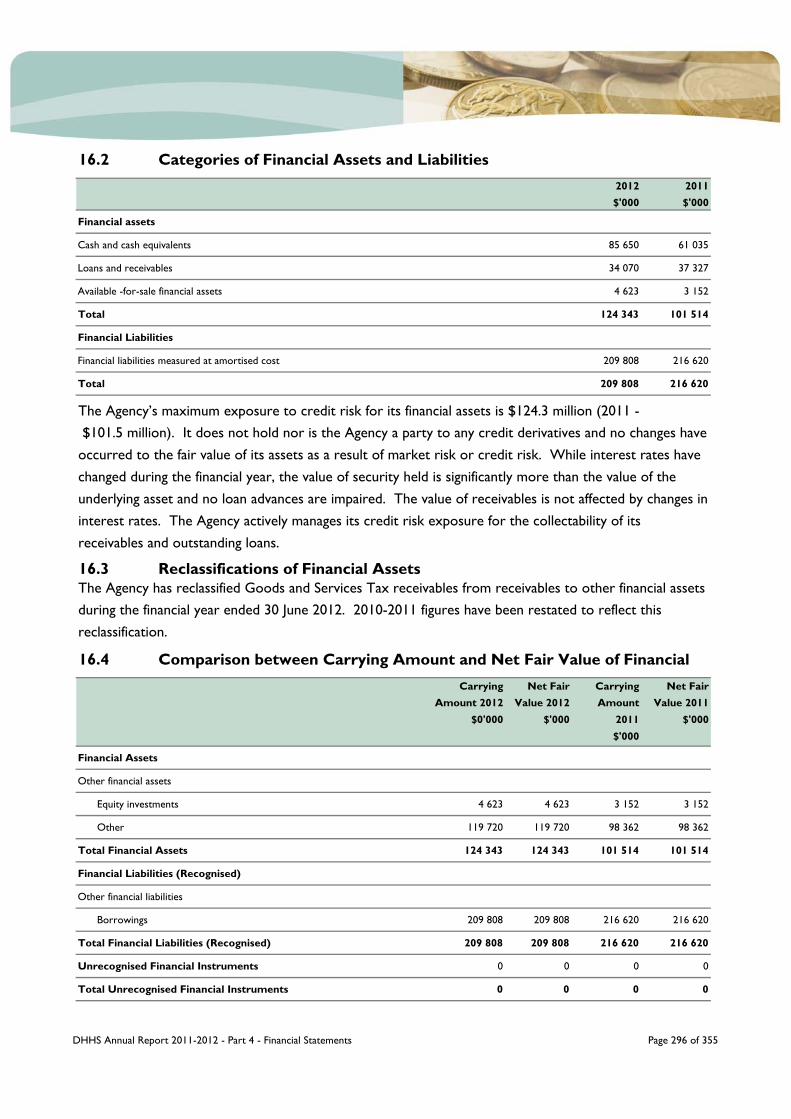

16.2 Categories of Financial Assets and Liabilities 296

16.3 Reclassifications of Financial Assets 296

16.4 296

16.5 Net Fair Values of Financial Assets and Liabilities 297

Note 17 Details of Consolidated Entities 298

17.1 List of Entities 299

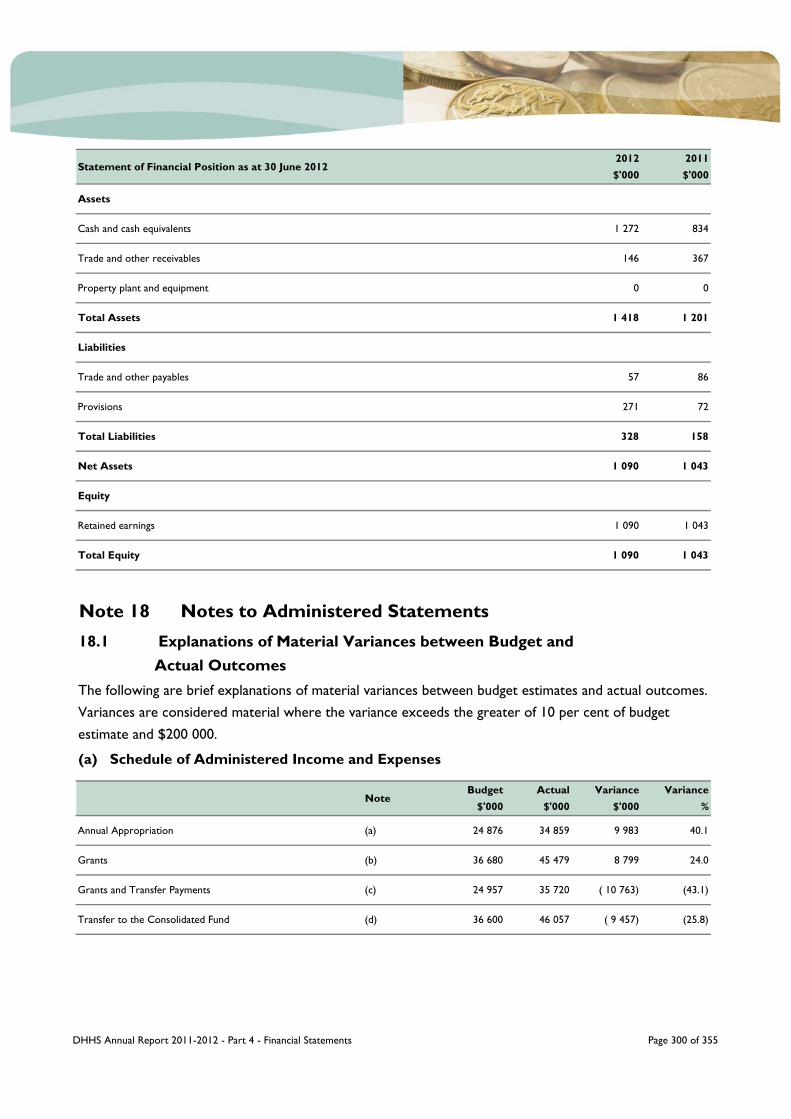

Note 18 Notes to Administered Statements 300

18.1 Explanations of Material Variances Between Budget and Actual Outcomes 300

18.2 Administered Underlying Net Operating Balance 302

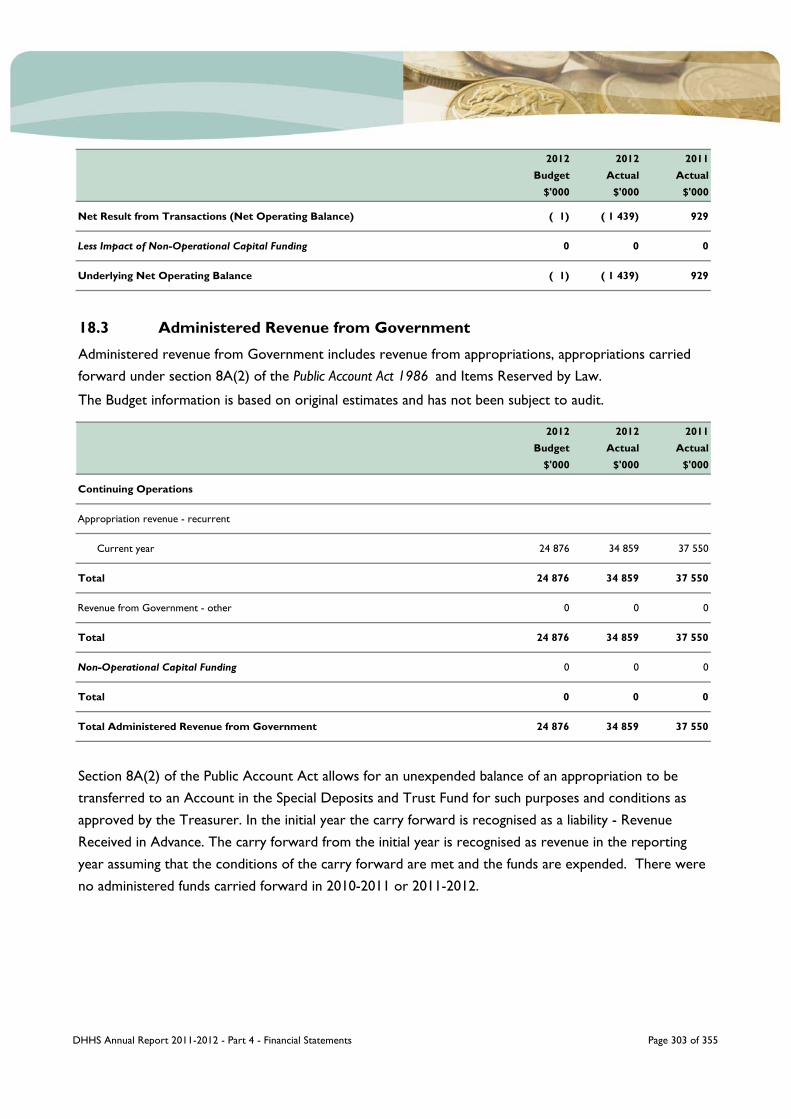

18.3 Administered Revenue from Government 303

18.4 Administered Grants 304

18.5 Administered Grants and Subsidies 304

18.6 Administered Receivables 305

18.7 Administered Payables 305

18.8 305

18.9 Financial Instruments (Administered) 306

18.10 Categories of Administered Financial Assets and Liabilities 309

18.11 Comparison Between Carrying Amount and Net Fair Value of Financial Assets and Liabilities 309

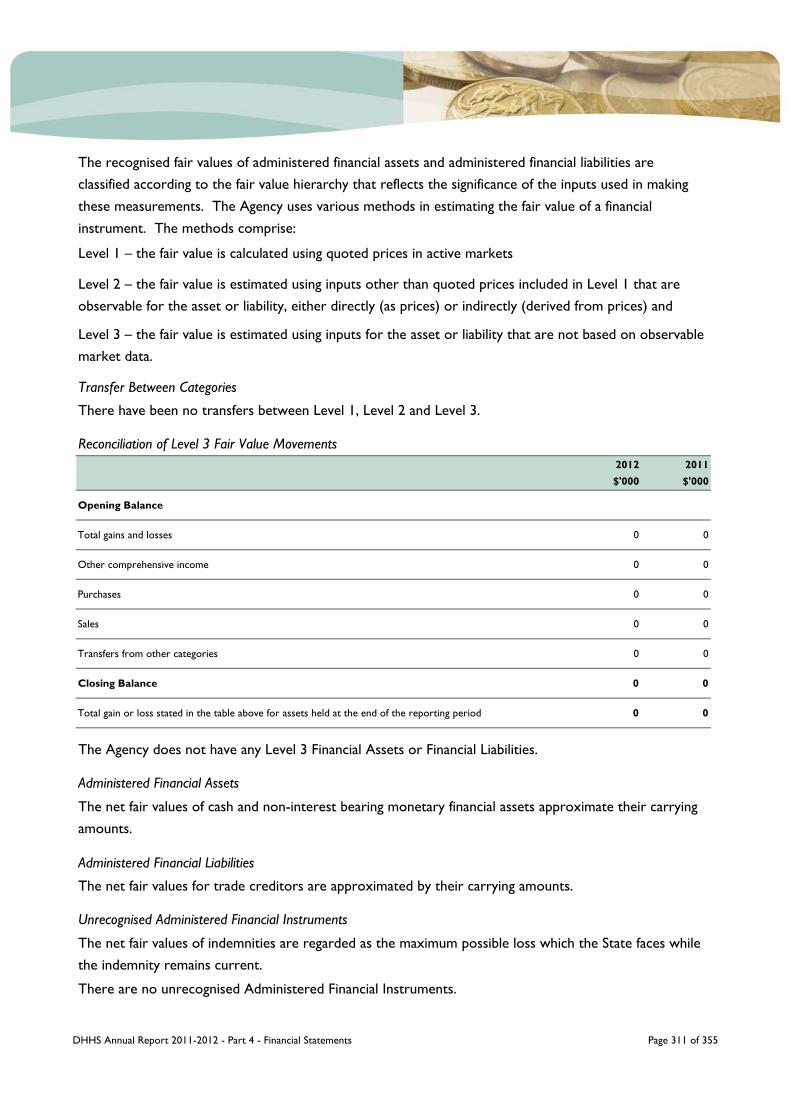

18.12 Net Fair Values of Administered Financial Assets and Liabilities 310

Note 19 Transactions and Balances Relating to a Trustee or Agency Arrangement 312

Reconciliation of Administered Net Result to Net Cash from Administered Operating Activities

Comparison Between Carrying Amount and Net Fair Value of Financial Assets and Liabilities

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 219 of 355

Note 1 Administered Financial Statements

1.1 Schedule of Administered Income and Expenses

· Highly Specialised Drugs

· Medical Specialist Outreach Program

· Transitional Care Program

· Extended Aged Care at Home and Community Aged Care Packages and

· Regional Health Services Program.

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Administered Revenue and Other Income from Transactions

Revenue from Government

Appropriation revenue - recurrent 2.9(a), 18.3 24 876 34 859 37 550

Grants 2.9(b), 18.4 36 680 45 479 46 133

61 556 80 338 83 683

Administered Expenses from Transactions

Grants and Transfer Payments 2.10(c), 18.5 24 957 35 720 38 734

Transfer to the Consolidated Fund 36 600 46 057 44 020

Total Administered Expenses from Transactions 61 557 81 777 82 754

Total Administered Revenue and Other Income from Transactions

The Agency administers Australian Government revenue collected on behalf of the Consolidated Fund in the form of Commonwealth Recurrent Grants and expenses in relation to Children Abused in Care and Aurora Energy Pensioner Concessions.

Australian Government Recurrent Grants reflect Commonwealth Own Purpose Expenditure (COPE) payments which are paid from the responsible Australian Government Agency to the relevant State Agency and receipted to the Consolidated Fund. Australian Government COPEs in 2011-2012 include:

The Children Abused in Care program is open to people who were abused in State care. The program was scheduled to be completed by 30 June 2011 but some claims remain to be processed.

The Agency provides funding to Aurora Energy for the purpose of providing a subsidy to eligible Tasmanian pensioners and Health Care Card holders on their electricity accounts. In 2010-2011 the Government provided funding of $7.9 million to provide eligible concession holders with a one-off payment of $100 as additional cost of living support for Tasmanian low income households.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 220 of 355

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

( 1) ( 1 439) 929

0 0 0

Administered Comprehensive Result ( 1) ( 1 439) 929

1.2 Schedule of Administered Assets and Liabilities

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Administered Assets

Administered financial assets

Receivables 2.12(b), 18.6 2 489 3 988 4 446

Total Administered Assets 2 489 3 988 4 446

Administered Liabilities

Payables 2.13(a), 18.7 6 036 8 041 7 059

Total Administered Liabilities 6 036 8 041 7 059

Administered Net Liabilities ( 3 547) ( 4 053) ( 2 614)

Administered Equity

Accumulated Funds ( 3 547) ( 4 053) ( 2 614)

Total Administered Equity ( 3 547) ( 4 053) ( 2 614)

Administered Net Result from Transactions Attributable to the State

Administered other Economic Flows in Administered Net Result

This Schedule of Administered Income and Expenses should be read in conjunction with the accompanying notes. Budget

information refers to original estimates and has not been subject to audit. Explanations of material variances between budget and

actual outcomes are provided in Note 18.1 of the accompanying notes.

This Schedule of Administered Assets and Liabilities should be read in conjunction with the accompanying notes. Budget

information refers to original estimates and has not been subject to audit. Explanations of material variances between budget and

actual outcomes are provided in Note 18.1 of the accompanying notes.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 221 of 355

1.3 Schedule of Administered Cash Flows

Notes2012

Budget$'000

2012Actual

$'000

2011Actual

$'000

Administered Cash Flows from Operating Activities

Administered Cash Inflows

Appropriation receipts - recurrent 24 876 34 859 37 550

Grants - Continuing operations 36 600 46 057 44 020

Total Administered Cash Inflows 61 476 80 916 81 570

Administered Cash Outflows

Grants and transfer payments ( 24 876) ( 34 859) ( 37 550)

Transfers to the Consolidated Fund ( 36 600) ( 46 057) ( 44 020)

Total Administered Cash Outflows ( 61 476) ( 80 916) ( 81 570)

Administered Net Cash from (Used By) Operating Activities 18.8 0 0 0

Net Increase (Decrease) in Administered Cash Held 0 0 0

0 0 0

0 0 0

1.4 Schedule of Administered Changes in Equity

Accumulated

Deficit $'000

Total Equity $'000

Balance as at 1 July 2011 ( 2 614) ( 2 614)

Total comprehensive result ( 1 439) ( 1 439)

Balance as at 30 June 2012 ( 4 053) ( 4 053)

Accumulated

Deficit$'000

Total Equity $'000

Balance as at 1 July 2010 ( 3 543) ( 3 543)

Total comprehensive result 929 929

Balance as at 30 June 2011 ( 2 614) ( 2 614)

Administered Cash and Deposits at the Beginning of the Reporting Period

Administered Cash and Deposits at the End of the Reporting Period

This Schedule of Administered Cash Flows should be read in conjunction with the accompanying notes. Budget information

refers to original estimates and has not been subject to audit. Explanations of material variances between budget and actual

outcomes are provided in Note 18.1 of the accompanying notes.

This Schedule of Administered Changes in Equity should be read in conjunction with the accompanying notes.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 222 of 355

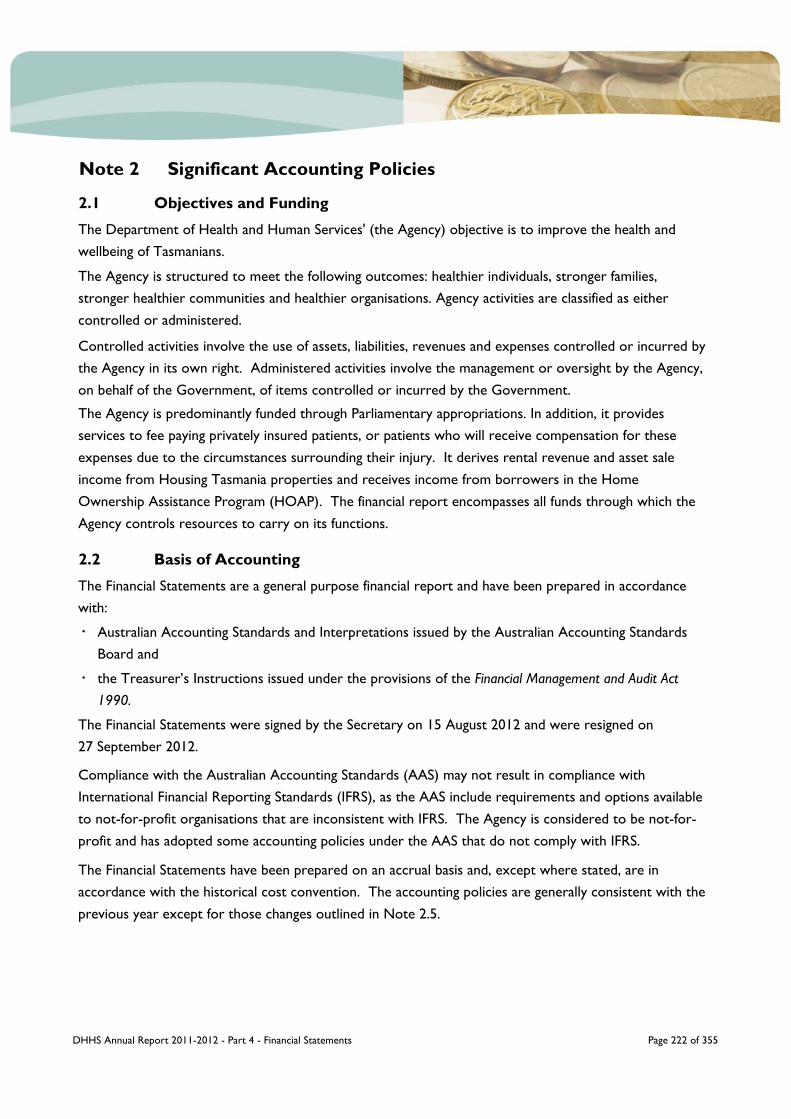

Note 2 Significant Accounting Policies

2.1 Objectives and Funding

2.2 Basis of Accounting

·

·

The Financial Statements have been prepared on an accrual basis and, except where stated, are in accordance with the historical cost convention. The accounting policies are generally consistent with the previous year except for those changes outlined in Note 2.5.

Compliance with the Australian Accounting Standards (AAS) may not result in compliance with International Financial Reporting Standards (IFRS), as the AAS include requirements and options available to not-for-profit organisations that are inconsistent with IFRS. The Agency is considered to be not-for-profit and has adopted some accounting policies under the AAS that do not comply with IFRS.

The Financial Statements were signed by the Secretary on 15 August 2012 and were resigned on 27 September 2012.

the Treasurer’s Instructions issued under the provisions of the Financial Management and Audit Act 1990.

The Financial Statements are a general purpose financial report and have been prepared in accordance with:

Australian Accounting Standards and Interpretations issued by the Australian Accounting Standards Board and

The Agency is structured to meet the following outcomes: healthier individuals, stronger families, stronger healthier communities and healthier organisations. Agency activities are classified as either controlled or administered.

Controlled activities involve the use of assets, liabilities, revenues and expenses controlled or incurred by the Agency in its own right. Administered activities involve the management or oversight by the Agency, on behalf of the Government, of items controlled or incurred by the Government.

The Agency is predominantly funded through Parliamentary appropriations. In addition, it provides services to fee paying privately insured patients, or patients who will receive compensation for these expenses due to the circumstances surrounding their injury. It derives rental revenue and asset sale income from Housing Tasmania properties and receives income from borrowers in the Home Ownership Assistance Program (HOAP). The financial report encompasses all funds through which the Agency controls resources to carry on its functions.

The Department of Health and Human Services' (the Agency) objective is to improve the health and wellbeing of Tasmanians.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 223 of 355

2.3 Reporting Entity

2.4 Functional and Presentation Currency

2.5 Changes in Accounting Policies

(a) Impact of New and Revised Accounting Standards

·

·

·

These Financial Statements are presented in Australian dollars, which is the Agency's functional currency.

The Financial Statements include all the controlled activities of the Agency, including Housing Tasmania and Ambulance Tasmania, with the exception of Tasmanian Affordable Housing Limited (TAHL). The Financial Statements consolidate material transactions and balances of the Agency and entities included in its output groups. Material transactions and balances between the Agency and such entities have been eliminated. Summary information relating to TAHL is disclosed in Note 17 - Details of Consolidated Entities.

The Financial Statements have been prepared as a going concern. The continued existence of the Agency, undertaking its current activities, is dependent on Government policy and on continuing appropriations by Parliament for the Agency’s administration and activities. National Health Reform was implemented in Tasmania from 1 July 2012 with the establishment of three Tasmanian Health Organisations (THOs) under the Tasmanian Health Organisations Act 2011 . The THOs replace the Area Health Services previously managed directly by the Agency. Please refer to Note 6 for further details.

AASB 2010-4 Further Amendments to Australian Accounting Standards arising from the Annual Improvements Project (AASBs 1, 7, 101, and 134 and Interpretation 13) – This Standard amends a range of Australian Accounting Standards and Interpretation as a consequence of the annual improvements project.

AASB 1054 Australian Additional Disclosures – This Standard in conjunction with AASB 2011-1 Amendments to AAS arising from the Trans Tasman Convergence Project, removes disclosure

requirements form other Standards and incorporates them in a single Standard to achieve convergence between Australian and New Zealand Accounting Standards. There is no financial impact.

AASB 2009-12 Amendments to Australian Accounting Standards (AASBs 5, 8, 108, 110, 112, 119, 133, 137, 139, 1023 and 1031 and Interpretations 2, 4, 16, 1039 and 1052) – This Standard makes editorial amendments to a range of Australian Accounting Standards and Interpretations. There is no financial impact.

In the current year, the Agency has adopted all of the new and revised Standards and Interpretations issued by the Australian Accounting Standards Board (AASB) that are relevant to its operations and effective for the current annual reporting period. These include:

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 224 of 355

·

·

·

·

·

·

(b) Impact of New and Revised Accounting Standards Yet to be Applied

·

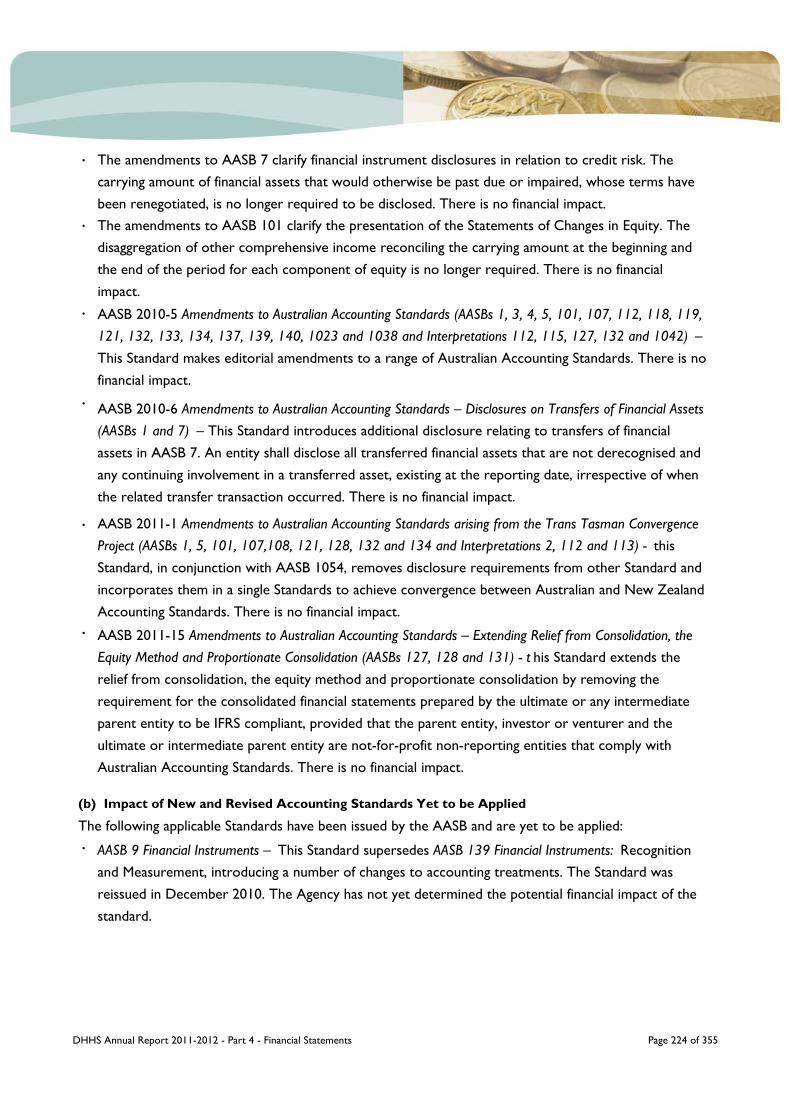

The amendments to AASB 101 clarify the presentation of the Statements of Changes in Equity. The disaggregation of other comprehensive income reconciling the carrying amount at the beginning and the end of the period for each component of equity is no longer required. There is no financial impact.

The amendments to AASB 7 clarify financial instrument disclosures in relation to credit risk. The carrying amount of financial assets that would otherwise be past due or impaired, whose terms have been renegotiated, is no longer required to be disclosed. There is no financial impact.

AASB 2010-5 Amendments to Australian Accounting Standards (AASBs 1, 3, 4, 5, 101, 107, 112, 118, 119, 121, 132, 133, 134, 137, 139, 140, 1023 and 1038 and Interpretations 112, 115, 127, 132 and 1042) – This Standard makes editorial amendments to a range of Australian Accounting Standards. There is no financial impact.

AASB 2010-6 Amendments to Australian Accounting Standards – Disclosures on Transfers of Financial Assets (AASBs 1 and 7) – This Standard introduces additional disclosure relating to transfers of financial assets in AASB 7. An entity shall disclose all transferred financial assets that are not derecognised and any continuing involvement in a transferred asset, existing at the reporting date, irrespective of when the related transfer transaction occurred. There is no financial impact.

AASB 2011-1 Amendments to Australian Accounting Standards arising from the Trans Tasman Convergence Project (AASBs 1, 5, 101, 107,108, 121, 128, 132 and 134 and Interpretations 2, 112 and 113) - this Standard, in conjunction with AASB 1054, removes disclosure requirements from other Standard and incorporates them in a single Standards to achieve convergence between Australian and New Zealand Accounting Standards. There is no financial impact.

AASB 2011-15 Amendments to Australian Accounting Standards – Extending Relief from Consolidation, the Equity Method and Proportionate Consolidation (AASBs 127, 128 and 131) - t his Standard extends the relief from consolidation, the equity method and proportionate consolidation by removing the requirement for the consolidated financial statements prepared by the ultimate or any intermediate parent entity to be IFRS compliant, provided that the parent entity, investor or venturer and the ultimate or intermediate parent entity are not-for-profit non-reporting entities that comply with Australian Accounting Standards. There is no financial impact.

AASB 9 Financial Instruments – This Standard supersedes AASB 139 Financial Instruments: Recognition and Measurement, introducing a number of changes to accounting treatments. The Standard was reissued in December 2010. The Agency has not yet determined the potential financial impact of the standard.

The following applicable Standards have been issued by the AASB and are yet to be applied:

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 225 of 355

·

·

·

·

·

·

·

·

·

AASB 11 Joint Arrangements – This Standard supersedes AASB 131 Interest in Joint Ventures, introducing a number of changes to accounting treatments. The Standard was issued in August 2011. The Agency has not yet determined the application or the potential impact of the Standard.

AASB 12 Disclosure of Interests in Other Entities - This Standard supersedes disclosure requirements under AASB 127 Consolidated and Separate Financial Statements and AASB 131 Interests in Joint Ventures. The Standard was issue in August 2011. The Agency has not yet determined the application or the potential impact of the Standard.

AASB 13 Fair Value Measurement – This Standard defines fair value, sets out a framework for measuring fair value and requires disclosures about fair value measurements. There is no financial impact.

AASB 119 Employee Benefits – This Standard supersedes AASB 119 Employee Benefits introducing a number of changes to accounting treatments. The Standard was issued in September 2011. The Agency has not yet determined the application or the potential impact of the Standard.

AASB 127 Separate Financial Statements – This standard supersedes requirements under AASB 127 Consolidated and Separate Financial Statements introducing a number of changes to accounting treatments. The Standard was issue in August 2011. The Agency has not yet determined the application or the potential impact of the Standard.

AASB 128 Investments in Associates and Joint Ventures – This Standard supersedes AASB 128 Investments in Associates and introduces a number of changes to accounting treatments. The Standard

was issued in August 2011. The Agency has not yet determined the application or the potential impact

of the Standard.

AASB 1053 Application of Tiers of Australian Accounting Standards – This Standard establishes a differential financial reporting framework consisting of two tiers of reporting requirements for preparing general purpose financial statements. The Standard does not have any financial impact on the Agency. However, it may affect disclosures if reduced disclosure requirements apply.

AASB 2010-2 Amendments to Australian Accounting Standards Arising from Reduced Disclosure Requirements (AASBs 1, 2, 3, 5, 7, 8, 101, 102, 107, 108, 110, 111, 112, 116, 117, 119, 121, 123, 124, 127, 128, 131, 133, 134, 136, 137, 138, 140, 141, 1050, and 1052 and Interpretations 2, 4, 5, 15, 17, 127, 129, and 1052) – This Standard makes amendments to Australian accounting Standards and

Interpretations to introduce reduced disclosure requirements for certain types of entities. There is no financial impact.

AASB 10 Consolidated Financial Statements – This Standard supersedes requirements under AASB 127 Consolidated and Separate Financial Statements and Interpretation 112 Consolidation – Special Purpose Entities , introducing a number of changes to accounting treatments. The standard was issued in August 2011. The Agency has not yet determined the application or the potential impact of the Standard.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 226 of 355

·

·

·

·

·

·

AASB 2011-8 Amendments to Australian Accounting Standards arising from AASB 13 [AASBs 1, 2, 3, 4, 5, 7, 9, 2009-11, 2010-7, 101, 102, 108, 110, 116, 117, 118, 119, 120, 121, 128, 131, 132, 133, 134, 136,

138, 139, 140, 141, 1004, 1023 and1038 and Interpretations 2, 4, 12, 13, 14, 17, 19, 131 and 132] – This Standard replaces the existing definition of fair value guidance in other Australian Accounting

Standards and Interpretations as the result of issuing AASB 13 in September 2011. There is no expected financial impact.

AASB 2011-9 Amendments to Australian Accounting Standards – Presentation of Items of Other Comprehensive Income [AASBs 1, 5, 7, 101, 112, 120, 121, 132, 133, 134, 1039 and 1049] – This Standard requires to group items presented in other comprehensive income on the basis of whether they are potentially reclassifiable to profit or loss subsequently (reclassification adjustments). It is not expected to have a financial impact.

AASB 2011-6 Amendments to Australian Accounting Standards – Extending Relief from Consolidation, the Equity Method and Proportionate Consolidation – Reduced Disclosure Requirements (AASBs 127, 128 and 131) – This Standard extends relief from consolidation, the equity method and proportionate consolidation by removing the requirement for the consolidated financial statements prepared by the ultimate or any intermediate parent entity to be IFRS compliant, provided that the parent entity, investor or venturer and the ultimate or intermediate parent entity comply with Australian Accounting Standards or Australian Accounting Standards – Reduced Disclosure Requirements. It is not expected to have a financial impact.

AASB 2011-7 Amendments to Australian Accounting Standards arising from the Consolidation and Joint Arrangements Standards (AASBs 1, 2, 3, 5, 7, 9, 2009 11, 101, 107, 112, 118, 121, 124, 132, 133, 136, 138, 139, 1023 and 1038 and Interpretations 5, 9, 16 and 17) – This Standard replaces the existing definition and fair value guidance in other Australian Accounting Standards and Interpretations as the result of issuing AASB 13 in September 2011. It is not expected to have a financial impact.

AASB 2010-7 Amendments to Australian Accounting Standards arising from AASB 9 (December 2010) (AASBs 1, 3, 4, 5, 7, 101, 102, 108, 112, 118, 120, 121, 127, 128, 131, 132, 136, 137, 139, 1023 and 1038 and Interpretations 2, 5, 10, 12, 19, and 127) – This Standard makes consequential amendments to other Australian Accounting Standards and Interpretations as a result of issuing AASB in December 2010. It is not anticipated that there will be any financial impact.

AASB 2011-2 Amendments to Australian Accounting Standards arising from the Trans Tasman Convergence Project – Reduced Disclosure Requirements (AASBs 101 and 1054) – This Standard makes amendments to

introduce reduced disclosure requirements for certain types of entities. There is no expected financial impact of applying these changes, as the Agency is a Tier 1 entity.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 227 of 355

·

·

(c) Voluntary Changes in Accounting Policy

2.6 Administered Transactions and Balances

2.7 Activities Undertaken Under a Trustee or Agency Relationship

AASB 2011-10 Amendments to Australian Accounting Standards arising from AASB 119 (September 2011) (AASBs 1, 8, 101, 124, 134, 1049 and 2011 8 and Interpretations 14) – This Standard makes amendments to other Australian Accounting Standards and Interpretation as a result of issuing AASB 119 Employee Benefits in September 2011. It is not expected to have a financial impact.

AASB 2011-12 Amendments to Australian Accounting Standards 119 (September 2011) arising from Reduced Disclosure Requirements – This Standard gives effect to Australian Accounting Standards – Reduced Disclosure Requirements for AASB 119 (September 2011). There is no financial impact.

The Agency has not adopted any new accounting policies during the financial year ended 30 June 2012.

The Agency administers, but does not control, certain resources on behalf of the Government as a whole. It is accountable for the transactions involving such administered resources, but does not have the discretion to deploy resources for the achievement of the Agency’s objectives.

Administered assets, liabilities, expenses and revenues are disclosed in Note 1 to the Financial

Transactions relating to activities undertaken by the Agency in a trust or fiduciary (agency) capacity do not form part of the Agency’s activities. Trustee and agency arrangements, and transactions/balances relating to those activities, are neither controlled nor administered.

Fees, commissions earned and expenses incurred in the course of rendering services as a trustee or through an agency arrangement are recognised as controlled transactions.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 228 of 355

2.9 Income from Transactions

(a) Revenue from Government

(b) Grants

(c) Sales of Goods and Services

(d) Interest

Interest on funds invested is recognised as it accrues using the effective interest rate method.

Amounts earned in exchange for the provision of goods are recognised when the significant risks and rewards of ownership have been transferred to the buyer. Revenue from the provision of services is recognised in proportion to the stage of completion of the transaction at the reporting date. The stage of completion is assessed by reference to surveys of work performed.

Non-reciprocal grants are recognised as revenue when the grant is received or receivable. Conditional grants may be reciprocal or non-reciprocal depending on the terms of the grant.

Grants payable by the Australian Government are recognised as revenue when the Agency gains control of the underlying assets. Where grants are reciprocal, revenue is recognised as performance occurs under the grant.

Appropriations, whether recurrent or capital, are recognised as revenues in the period in which the Agency gains control of the appropriated funds. Except for any amounts identified as carried forward in Note 18.3, control arises in the period of appropriation.

Income is recognised in the Statement of Comprehensive Income when an increase in future economic benefits related to an increase in an asset or a decrease of a liability has arisen that can be measured reliably.

Net assets received under a restructuring of administrative arrangements are designated as contributions by owners and adjusted directly against equity. Net assets relinquished are designated as distributions to owners. Net assets transferred are initially recognised at the amounts at which they were recognised by the transferring agency immediately prior to the transfer. There were no assets received or relinquished during the year.

2.8 Transactions by the Government as Owner – Restructuring of Administrative Arrangements

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 229 of 355

(e) Contributions Received

(f) Other Revenue

2.10 Expenses from Transactions

(a) Employee Benefits

(b) Depreciation and Amortisation

Vehicles 5 years

Plant and equipment 2-20 years

Medical equipment 4-20 years

Buildings 40-50 years

Employee benefits include, where applicable, entitlements to wages and salaries, annual leave, sick leave, long service leave, superannuation and any other post-employment benefits.

Expenses are recognised in the Statement of Comprehensive Income when a decrease in future economic benefits related to a decrease in an asset or an increase of a liability has arisen that can be measured reliably.

Other revenue is primarily the recovery of costs incurred and is recognised when an increase in future economic benefits relating to an increase in an asset or a decrease of a liability has arisen that can be reliably measured.

Contributions of assets at no cost of acquisition or for nominal consideration are recognised at their fair value when the Agency obtains control of the asset, it is probable that future economic benefits comprising the contribution will flow to the Agency and the amount can be measured reliably. However, where the contribution received is from another government agency as a consequence of restructuring of administrative arrangements, where they are recognised as contributions by owners directly within equity. In these circumstances, book values from the transferor agency have been used.

Services received free of charge by the Agency, are recognised as income when a fair value can be reliably determined and at the time the services would have been purchased if they had not been donated. Use of those resources is recognised as an expense.

All applicable non-financial assets having a limited useful life are systematically depreciated over their useful lives in a manner which reflects the consumption of their service potential. Land, being an asset with an unlimited useful life, is not depreciated.

Depreciation is provided for on a straight line basis, using rates which are reviewed annually. Major depreciation periods are:

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 230 of 355

Software 3-5 years

Long-Term Community Housing Program Grant 11 years

(c) Grants and Subsidies

·

·

(d) Borrowing Costs

·

·

·

·

·

(e) Contributions Provided

(f) Other Expenses

Borrowing costs include:

interest on bank overdrafts and short-term and long-term borrowings

unwinding of discounting provisions

Other expenses are recognised when a decrease in future economic benefits related to a decrease in an asset or an increase of a liability has arisen that can be reliably measured.

amortisation of discounts or premiums related to borrowings

amortisation of ancillary costs incurred in connection with the arrangement of borrowings and

finance lease charges.

Contributions provided free of charge by the Agency, to another entity, are recognised as an expense when fair value can be reliably determined. No contributions were provided free of charge during 2011-2012.

Depreciation of Housing Tasmania’s rental dwellings and community rental stock is based on a useful life of 50 years in accordance with the State Housing Authority’s Accounting Policies and Reporting Framework (March 1995). All other buildings are depreciated over their remaining useful life.

All intangible assets having a limited useful life are systematically amortised over their useful lives reflecting the pattern in which the asset’s future economic benefits are expected to be consumed by the Agency.Major amortisation periods are:

Grant and Subsidies expenditure is recognised to the extent that:

the services required to be performed by the grantee have been performed or

the grant eligibility criteria have been satisfied.

A liability is recorded when the Agency has a binding agreement to make the grants but services have not been performed or criteria satisfied. Where grant monies are paid in advance of performance or eligibility, a prepayment is recognised.

All borrowing costs are expensed as incurred using the effective interest method.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 231 of 355

2.11 Other Economic Flows Included in Net Result

(a) Gain/(Loss) on Sale of Non-Financial Assets

(b) Impairment – Financial Assets

(c) Impairment – Non-Financial Assets

All impairment losses are recognised in the Statement of Comprehensive Income.

In respect of other assets, impairment losses recognised in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extend that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

Other economic flows measure the change in volume or value of assets or liabilities that do not result from transactions.

Gains or losses from the sale of non-financial assets are recognised when control of the assets has passed to the buyer.

Financial assets are assessed at each reporting date to determine whether there is any objective evidence that there are any financial assets that are impaired. A financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset.

An impairment loss, in respect of a financial asset measured at amortised cost, is calculated as the difference between its carrying amount, and the present value of the estimated future cash flows discounted at the original effective interest rate.

All impairment losses are recognised in the Statement of Comprehensive Income.

An impairment loss is reversed if the reversal can be related objectively to an event occurring after the impairment loss was recognised. For financial assets measured at amortised cost the reversal is recognised in the Statement of Comprehensive Income.

All non-financial assets are assessed to determine whether any impairment exists. Impairment exists when the recoverable amount of an asset is less than its carrying amount. Recoverable amount is the

higher of fair value less costs to sell and value in use. The Agency’s assets are not used for the purpose

of generating cash flows; therefore value in use is based on depreciated replacement cost where the asset would be replaced if deprived of it.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 232 of 355

(d) Other Gains/(Losses) From Other Economic Flows

2.12 Assets

(a) Cash and Deposits

(b) Receivables

(c) Loan Advances

(d) Equity Investments

(e) Other Financial Assets

(f) Inventories

Other gains/(losses) from other economic flows includes gains or losses from reclassifications of amounts from reserves and/or accumulated surplus to net result, and from the revaluation of the present values of

the long service leave liability due to changes in the bond interest rate.

Assets are recognised in the Statement of Financial Position when it is probable that the future economic benefits will flow to the Agency and the asset has a cost or value that can be measured reliably.

Cash means notes, coins, any deposits held at call with a bank or financial institution, as well as funds held in the Special Deposits and Trust Fund, being short-term of three months or less and highly liquid. Deposits are recognised at amortised cost, being their face value.

Receivables are recognised at amortised cost, less any impairment losses, however, due to the short settlement period, receivables are not discounted back to their present value.

Loan advances are borrowings provided to clients for the purchase of homes and are recognised at the balance of the outstanding principal less any impairment losses.

Equity investments are recorded at fair value with any changes in the fair value being recorded as income or expenses in the Statement of Comprehensive Income. Equity investments are not depreciated.

Other financial assets are recorded at fair value.

Inventories held for distribution are valued at cost adjusted, when applicable, for any loss of service potential. Inventories acquired for no cost or nominal consideration are valued at current replacement cost. Inventories held for resale are valued at cost.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 233 of 355

(g) Assets Held for Sale

(h) Property, Plant, Equipment and Infrastructure

The cost of replacing part of an item of property, plant and equipment is recognised in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Agency and its costs can be measured reliably. The carrying amount of the replaced part is derecognised. The costs of day-to-day servicing of property, plant and equipment are recognised in the Statement of Comprehensive Income as incurred.

(iii) Asset Recognition Threshold

The asset capitalisation threshold for tangible assets adopted by the Agency is $10 000. Assets valued at less than $10 000 (or $50 000 for intangible assets) are charged to the Statement of Comprehensive Income in the year of purchase (other than where they form part of a group of similar items which are material in total).

Cost includes expenditure that is directly attributable to the acquisition of the asset. The costs of self‑constructed assets includes the cost of materials and direct labour, any other costs directly attributable to bringing the asset to a working condition for its intended use, and the costs of dismantling and removing the items and restoring the site on which they are located. Purchased software that is integral to the functionality of the related equipment is capitalised as part of that equipment.

When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment.

(ii) Subsequent Costs

Assets held for sale (or disposal groups comprising assets and liabilities) that are expected to be recovered primarily through sale rather than continuing use are classified as held for sale. Immediately before classification as held for sale, the assets (or components of a disposal group) are remeasured in accordance with the Agency’s accounting policies. Thereafter the assets (or disposal group) are measured at the lower of carrying amount and fair value less costs to sell.

(i) Valuation Basis

Land, buildings, infrastructure, heritage and cultural assets and other long-lived assets are recorded at fair value less accumulated depreciation. All other non-current physical assets, including work in progress, are recorded at historic cost less accumulated depreciation and accumulated impairment losses.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 234 of 355

(i) Intangibles

·

·

(j) Other Assets

Other assets are recorded at fair value and include prepayments.

2.13 Liabilities

(a) Payables

Intangible assets held by the Agency are valued at fair value less any subsequent accumulated amortisation and any subsequent accumulated impairment losses where an active market exists. Where no active market exists, intangible assets held by the Agency are valued at cost less any subsequent accumulated amortisation and any subsequent accumulated impairment losses. The asset capitalisation threshold for intangible assets adopted by the Agency is $50 000.

it is probable that an expected future benefit attributable to the asset will flow to the Agency and

the cost of the asset can be reliably measured.

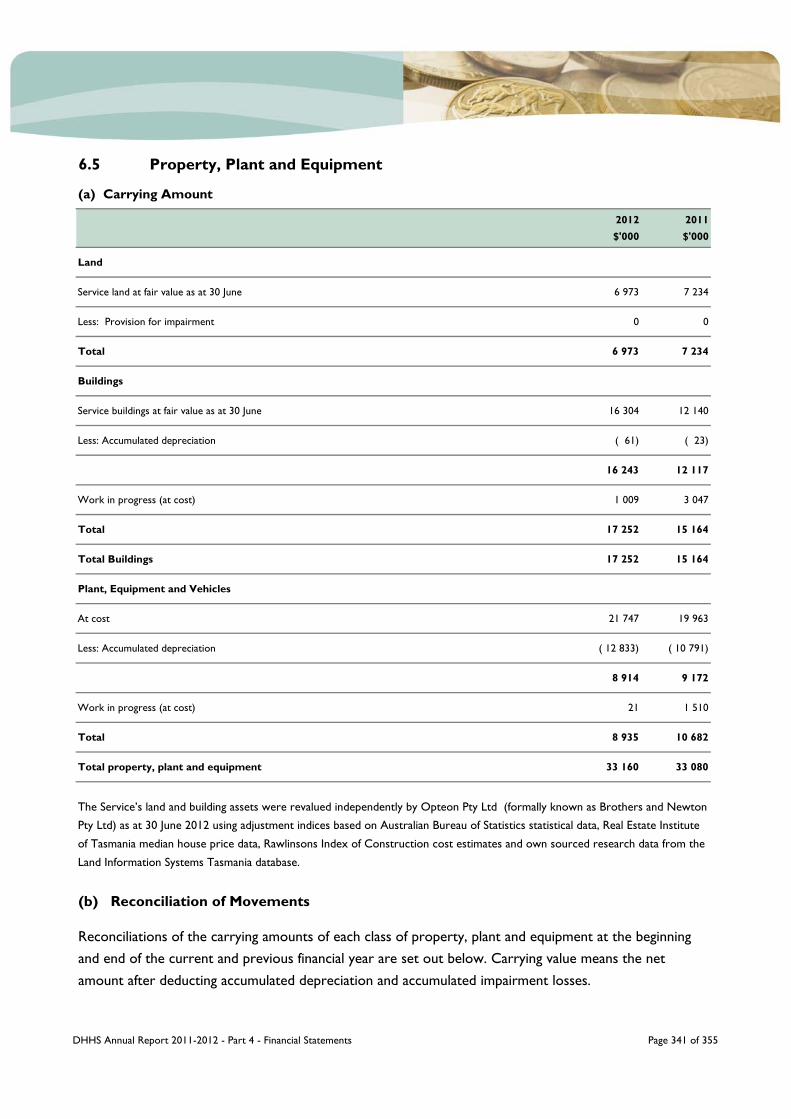

(iv) Revaluations

The Agency’s land and building assets (excluding Housing Tasmania’s rental properties) were revalued independently by Opteon Pty Ltd (formally known as Brothers and Newton Pty Ltd) as at 30 June 2012 using adjustment indices based on Australian Bureau of Statistics statistical data, Real Estate Institute of Tasmania median house price data, Rawlinsons Index of Construction cost estimates and own sourced research data from the Land Information Systems Tasmania database. Housing Tasmania land and

building assets are revalued annually as at 31 October using a mix of onsite revaluations and suburb based indices adjustments. These annual revaluations are provided by the Valuer-General of Tasmania.

An intangible asset is recognised where:

Liabilities are recognised in the Statement of Financial Position when it is probable that an outflow of resources embodying economic benefits will result from the settlement of a present obligation and the amount at which the settlement will take place can be measured reliably.

Payables, including goods received and services incurred but not yet invoiced, are recognised at amortised cost, which due to the short settlement period, equates to face value, when the Agency becomes obliged to make future payments as a result of a purchase of assets or services.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 235 of 355

(b) Interest Bearing Liabilities

(c) Provisions

(d) Employee Benefits

(e) Superannuation

A defined contribution plan is a post-employment benefit plan under which an entity pays fixed contributions into a separate entity and will have no legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution plans are recognised as an expense when they fall due.

Bank loans and other loans are initially measured at fair value, net of transaction costs. Bank loans and other loans are subsequently measured at amortised cost using the effective interest rate method, with interest expense recognised on an effective yield basis.

Liabilities for wages and salaries and annual leave are recognised when an employee becomes entitled to receive a benefit. Those liabilities expected to be realised within 12 months are measured at the amount expected to be paid. Other employee entitlements are measured as the present value of the benefit at 30 June 2012, where the impact of discounting is material, and at the amount expected to be paid if discounting is not material.

A liability for long service leave is recognised, and is measured as the present value of expected future payments to be made in respect of services provided by employees up to the reporting date.

(i) Defined Contribution Plans

The effective interest rate method is a method of calculating the amortised cost of a financial liability and allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments through the expected life of the financial liability, or where appropriate, a shorter period.

A provision arises if, as a result of a past event, the Agency has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a rate that reflects current market assessments of the time value of money and the risks specific to the liability. Any right to reimbursement relating to some or all of the provision is recognised as an asset when it is virtually certain that the reimbursement will be received.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 236 of 355

(f) Other Liabilities

(ii) Defined Benefit PlansA defined benefit plan is a post‑employment benefit plan other than a defined contribution plan.

The Agency makes contributions in respect of certain employees of Ambulance Tasmania to the Tasmanian Ambulance Service Superannuation Scheme being a defined benefit scheme where members receive lump sum benefits on resignation, retirement, death or invalidity. The scheme is closed to new

members. The Agency’s superannuation obligations in respect of this scheme are recognised at the latest actuarial assessment of the member’s entitlements, net of scheme assets. Actuarial gains and losses in respect of this scheme are recognised in the Statement of Comprehensive Income.

With the exception noted below, the Director of Housing does not recognise a liability for the accruing superannuation benefits of Service employees. This liability is held centrally and is recognised within the Finance‑General Division of the Department of Treasury and Finance.

The Director of Housing’s superannuation obligations, in respect of the contributory service of current and past government employees, are recognised at the latest actuarial assessment of the members’

entitlements, net of scheme assets. The valuation is determined by discounting to present value, the gross

benefit payments at a current, market-determined, risk-adjusted discount rate appropriate to the respective plan.

Actuarial gains or losses arising from the actuarial revaluation of superannuation liabilities are recognised in the Statement of Comprehensive Income.

Other liabilities and other financial liabilities are recognised in the Statement of Financial Position when it is probable that an outflow of resources embodying economic benefits will result from the settlement of

a present obligation and the amount at which the settlement will take place can be measured reliably. Other liabilities include revenue received in advance and on costs associated with employee benefits. As

a consequence of the Treasurer's decision to cease levying payroll tax on agencies from 1 October 2012, other liabilities no longer includes a component relating to a provision for payroll tax associated with

employee leave entitlement provisions. Revenue received in advance is measured at amortised cost. On-costs associated with employee benefits expected to be realised within 12 months are measured at the amount expected to be paid. Other on-costs associated with employee benefits are measured at the present value of the cost at 30 June 2012, where the impact of discounting is material, and at the amount expected to be paid if discounting is not material.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 237 of 355

2.14 Leases

2.15 Judgements and Assumptions

Judgements made by the Agency that have significant effects on the Financial Statements are disclosed in the relevant notes to the Financial Statements. In particular, information about significant areas of estimation, uncertainty and critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the financial statements are described in the following notes:

· 2.12(h) and 11.7(a) Property, Plant Equipment and Infrastructure and

· 2.10(b) Depreciation and Amortisation

· 2.13(e) and 12.4 Superannuation.

These judgements relate to adoption of the recommendations by the valuer, Opteon Pty Ltd, in respect of land and building valuations and the Valuer-General for valuation of the Housing Tasmania rental properties and the recommendations of the State Actuary in respect of the Superannuation liabilities.

The Treasurer has announced the policy decision to cease levying payroll tax on agencies from 1 October 2012. This decision has been factored into the calculation of employee entitlement provisions and the associated on cost liabilities as at 30 June have been stated, exclusive of payroll tax.

The Agency has entered into a number of operating lease agreements for property, plant and equipment, where the lessors effectively retain all the risks and benefits incidental to ownership of the items leased. Equal instalments of lease payments are charged to the Statement of Comprehensive Income over the lease term, as this is representative of the pattern of benefits to be derived from the leased property.

The Agency is prohibited by Treasurer’s Instruction 502 Leases from holding finance leases.

In the application of Australian Accounting Standards, the Agency is required to make judgements, estimates and assumptions about carrying values of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making the judgements. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

The Agency has made no other judgements or assumptions that may cause a material adjustment to the carrying amounts of assets and liabilities.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 238 of 355

2.16 Foreign Currency

2.17 Comparative Figures

2.18 Budget Information

2.19 Rounding

2.20 Departmental Taxation

2.21 Goods and Services Tax

Budget information refers to original estimates as disclosed in the 2011-2012 Budget Papers and is not subject to audit.

All amounts in the Financial Statements have been rounded to the nearest thousand dollars, unless otherwise stated. Where the result of expressing amounts to the nearest thousand dollars would result in an amount of zero, the financial statement will contain a note expressing the amount to the nearest whole dollar.

The Agency is exempt from all forms of taxation except Fringe Benefits Tax, Payroll Tax and the Goods and Services Tax (GST).

Revenue, expenses and assets are recognised net of the amount of GST, except where the GST incurred is not recoverable from the Australian Taxation Office (ATO). Receivables and payables are stated inclusive of GST. The net amount recoverable, or payable, to the ATO is recognised as an asset or liability within the Statement of Financial Position.

In the Statement of Cash Flows, the GST component of cash flows arising from operating, investing or financing activities which is recoverable from, or payable to, the Australian Taxation Office is, in accordance with the Australian Accounting Standards, classified as operating cash flows.

Transactions denominated in a foreign currency are converted at the exchange rate at the date of the transaction. Foreign currency receivables and payables are translated at the exchange rates current as at balance date.

Comparative figures have been adjusted to reflect any changes in accounting policy or the adoption of new standards. Details of the impact of changes in accounting policy on comparative figures and amendments to comparative figures arising from correction of an error are disclosed at Note 2.5.

Where amounts have been reclassified within the Financial Statements, the comparative statements have been restated.

Restructures of Outputs within the Agency (internal restructures) that do not affect the results shown on the face of the Financial Statements are reflected in the comparatives in the Output Schedule at Notes 3.1 and 3.2.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 239 of 355

Note 3 Agency Output Schedules3.1 Output Group Information

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Continuing Operations

Revenue and Other Income from Transactions

Revenue from appropriation 784 186 819 092 814 634

Grants 65 000 63 600 59 742

Sales of goods and services 75 189 89 564 77 338

Interest income 758 533 935

Contributions received 0 0 90

Other revenue 18 903 23 483 20 087

Total Revenue and Other Income from Transactions 944 036 996 272 972 826

Expenses from Transactions

Employee entitlements

Salaries and wages 564 398 583 355 561 663

Other employee related expenses 12 624 12 184 14 682

Superannuation expenses 53 057 70 501 59 866

Depreciation and amortisation 24 269 26 557 25 710

Supplies and consumables

Consultants 1 750 1 030 1 886

Maintenance and property services 30 491 27 499 28 956

Communications 3 584 4 925 4 491

Information technology 11 100 8 827 10 428

Travel and transport 7 808 10 178 9 537

Medical, surgical and pharmacy supplies 158 151 162 034 164 343

Advertising and promotion 102 118 145

Output Group 1 – Acute Health Services

Budget information refers to original estimates and has not been subject to audit.

Comparative information has not been restated for external administrative restructures.

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 240 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Other supplies and consumables 60 662 49 797 54 923

Grants and subsidies 1 465 2 995 934

Borrowing costs 0 2 0

Other expenses 40 785 43 995 49 093

Total Expenses from Transactions 970 246 1 003 997 986 657

Net Result from Transactions (Net Operating Balance) ( 26 210) ( 7 725) ( 13 831)

Other Economic Flows Included in Net Result

Net gain/(loss) on sale of non financial assets 40 47 85

0 ( 1 137) ( 72)

Net actuarial gains/(losses) of superannuation defined benefit plans 0 ( 8 902) ( 2 505)

Total Other Economic Flows Included in Net Result 40 ( 9 992) ( 2 492)

Net Result from Continuing Operations ( 26 170) ( 17 717) ( 16 323)

Other Economic Flows - Other Non-Owner Changes in Equity

Changes in physical asset revaluation reserve 620 13 056 17 752

Total Other Economic Flows - Other Non-Owner Changes in Equity 620 13 056 17 752

Comprehensive Result ( 25 550) ( 4 661) 1 429

Expense by Output

1.1 Clinical Support Services 45 871 46 180 44 685

1.2 Medical Services 381 003 391 352 379 892

1.3 Surgical Services 238 311 245 598 252 067

1.4 Women's and Children's Services 109 454 113 858 112 240

1.5 Diagnostic and Pharmacy Services 135 483 144 947 141 169

1.6 Ambulance Services 57 770 59 651 54 423

1.7 Forensic Medicine Services 2 354 2 411 2 180

Total 970 246 1 003 997 986 656

Net Assets

Total assets deployed for Acute Health Services 690 499 579 977

Total liabilities incurred for Acute Health Services ( 202 746) ( 179 965)

Net Assets Deployed for Acute Health Services 487 753 400 012

Net gain/(loss) on financial instruments and statutory receivables/payables

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 241 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Continuing Operations

Revenue and Other Income from Transactions

Revenue from appropriation 381 098 374 899 365 798

Grants 0 0 0

Sales of goods and services 14 572 18 159 17 492

Interest income 6 0 6

Contributions received 0 0 0

Other revenue 4 080 5 411 4 625

Total Revenue and Other Income from Transactions 399 756 398 469 387 921

Expenses from Transactions

Employee entitlements

Salaries and wages 226 113 219 810 214 635

Other employee related expenses 4 773 3 665 5 858

Superannuation expenses 24 838 27 314 24 049

Depreciation and amortisation 4 656 6 286 6 174

Supplies and consumables

Consultants 671 615 788

Maintenance and property services 15 481 14 878 16 444

Communications 2 293 2 282 2 489

Information technology 3 317 3 902 4 125

Travel and transport 6 202 6 327 6 909

Medical, surgical pharmacy supplies 18 807 16 876 17 470

Advertising and promotion 193 224 251

Other supplies and consumables 21 123 17 914 19 977

Grants and subsidies 58 392 61 885 50 166

Other expenses 19 758 17 757 19 921

Total Expenses from Transactions 406 617 399 735 389 256

Net Result from Transactions (Net Operating Balance) ( 6 861) ( 1 266) ( 1 335)

Output Group 2 – Community Health Services

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 242 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Other Economic Flows Included in Net Result

Net gain/(loss) on sale of non financial assets 0 ( 2 376) 17

0 ( 121) ( 58)

Total Other Economic Flows Included in Net Results 0 ( 2 497) ( 41)

Net Result from Continuing Operations ( 6 861) ( 3 763) ( 1 376)

Other Economic Flows - Other Non-Owner Changes in Equity

Changes in physical asset revaluation reserve 30 919 3 568 6 140

Total Other Economic Flows - Other Non-Owner Changes in Equity 30 919 3 568 6 140

Comprehensive Result 24 058 ( 195) 4 764

Expense by Output

2.1 Primary Health Services 191 260 191 378 179 511

2.2 Oral Health Services 26 317 27 555 26 674

2.3 Population Health Services 39 600 36 820 37 023

2.4 Mental Health Services 149 440 143 982 146 048

Total 406 617 399 735 389 256

Net Assets

Total assets deployed for Community Health Services 244 559 235 531

Total liabilities incurred for Community Health Services ( 67 073) ( 62 919)

Net Assets Deployed for Community Health Services 177 486 172 612

Net gain/(loss) on financial instruments and statutory receivables/payables

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 243 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Continuing Operations

Revenue and Other Income from Transactions

Revenue from appropriation 322 124 335 442 340 974

Grants 0 0 0

Sales of goods and services 82 287 78 038 73 797

Interest income 607 237 1 403

Other revenue ( 2 239) 1 682 2 898

Total Revenue and Other Income from Transactions 402 779 415 399 419 072

Expenses from Transactions

Employee entitlements

Salaries and wages 67 353 70 929 77 289

Other employee related expenses 1 982 552 613

Superannuation expenses 8 129 9 877 9 541

Depreciation and amortisation 22 932 27 991 27 347

Supplies and consumables

Consultants 1 022 568 590

Maintenance and property services 67 642 73 282 71 819

Communications 1 594 1 370 1 554

Information technology 1 945 1 885 1 988

Travel and transport 3 028 2 696 3 487

Medical, surgical pharmacy supplies 318 74 71

Advertising and promotion 622 769 725

Other supplies and consumables 25 997 44 930 41 773

Grants and subsidies 204 517 237 198 178 845

Borrowing costs 9 623 9 624 9 913

Other expenses 8 762 7 041 9 593

Total Expenses from Transactions 425 466 488 786 435 148

Net Result from Transactions (Net Operating Balance) ( 22 687) ( 73 387) ( 16 077)

Output Group 3 – Human Services

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 244 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Other Economic Flows Included in Net Result

Net gain/(loss) on sale of non financial assets ( 15 415) ( 16 726) ( 27 396)

0 ( 810) ( 780)

Net actuarial gains/(losses) of superannuation defined benefit plans 0 ( 5 019) 1 270

Other gains/(losses) from other economic flows 0 1 134 0

Total Other Economic Flows Included in Net Results ( 15 415) ( 21 421) ( 26 906)

Net Result from Continuing Operations ( 38 102) ( 94 808) ( 42 983)

Other Economic Flows - Other Non-Owner Changes in Equity

Changes in physical asset revaluation reserve 21 897 ( 3 363) 202 774

Total Other Economic Flows - Other Non-Owner Changes in Equity 21 897 ( 3 363) 202 774

Comprehensive Result ( 16 205) ( 98 171) 159 791

Expense by Output

3.1 Child and Family Service 96 075 107 330 115 820

3.2 Youth Justice Services 14 762 15 184 14 970

3.3 Disability Services 163 152 164 628 148 205

3.4 Housing Services 151 477 201 644 156 153

Total 425 466 488 786 435 148

Net Assets

Total assets deployed for Human Services 2 129 258 2 192 179

Total liabilities incurred for Human Services ( 260 065) ( 260 867)

Net Assets Deployed for Human Services 1 869 193 1 931 312

Net gain/(loss) on financial instruments and statutory receivables/payables

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 245 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Continuing Operations

Revenue and Other Income from Transactions

Revenue from Appropriation 753 802 752

Sales of Goods and Services 3 15 16

Other Revenue 1 0 0

Total Revenue and Other Income from Transactions 757 817 768

Expenses from Transactions

Employee entitlements

Salaries and wages 522 491 473

Other employee related expenses 10 4 19

Superannuation expenses 56 60 51

Depreciation and amortisation 0 1 1

Supplies and consumables

Consultants 2 30 35

Maintenance and property services 57 64 60

Communications 10 16 15

Information technology 6 6 9

Travel and transport 29 23 42

Medical, surgical pharmacy supplies 1 0 0

Advertising and promotion 1 0 1

Other supplies and consumables 32 71 35

Grants and subsidies 1 0 0

Other expenses 37 37 41

Total Expenses from Transactions 764 803 782

Net Result from Transactions (Net Operating Balance) ( 7) 14 ( 14)

Output Group 4 – Independent Children’s Review

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 246 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Other Economic Flows Included in Net Result

Net gain/(loss) on sale of non financial assets 0 0 0

0 0 0

Total other Economic Flows Included in Net Results 0 0 0

Net result from Continuing Operations ( 7) 14 ( 14)

Other Economic Flows - Other Non-Owner Changes in Equity

Changes in physical asset revaluation reserve 0 0 0

Total Other Economic Flows - Other Non-Owner Changes in Equity 0 0 0

Comprehensive Result ( 7) 14 ( 14)

Expense by Output

4.1 Office of the Commissioner for Children 764 803 784

Total 764 803 784

Net Liabilities

Total assets deployed for Independent Children’s Review 41 61

Total liabilities incurred for Independent Children’s Review ( 120) ( 130)

Net Liabilities Deployed for Independent Children’s Review ( 79) ( 69)

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Continuing Operations

Revenue and Other Income from Transactions

Revenue from appropriation 113 857 67 807 145 849

Sales of goods and services 3 891 30 270

Other revenue 3 700 8 975 2 306

Total Revenue and Other Income from Transactions 121 448 76 812 148 425

Output Group – Capital Investment Program

Net gain/(loss) on financial instruments and statutory receivables/payables

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 247 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Expenses from Transactions

Employee entitlements

Salaries and wages 230 568 1 121

Other employee related expenses 0 8 11

Superannuation expenses 9 68 91

Supplies and consumables

Consultants 0 63 409

Maintenance and property services 0 486 177

Communications 0 99 15

Information technology 0 171 27

Travel and transport 0 24 36

Medical, surgical pharmacy supplies 0 18 9

Advertising and promotion 0 20 2

Other supplies and consumables 730 1 685 1 625

Grants and subsidies 0 1 862 800

Other expenses 1 888 51 56

Total Expenses from Transactions 2 857 5 123 4 379

Net Result from Transactions (Net Operating Balance) 118 591 71 689 144 047

Other Economic Flows Included in Net Result

Net gain/(loss) on sale of non financial assets 24 600 12 277 27 000

Other gains/(losses) from other economic flows 0 ( 1 833) 0

Total Other Economic Flows Included in Net Results 24 600 10 444 27 000

Net Result from Continuing Operations 143 191 82 133 171 047

Other Economic Flows - Other Non-Owner Changes in Equity

Changes in physical asset revaluation reserve 0 0 0

Total Other Economic Flows - Other Non-Owner Changes in Equity 0 0 0

Comprehensive Result 143 191 82 133 171 047

DHHS Annual Report 2011-2012 - Part 4 - Financial Statements Page 248 of 355

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Expense by Output

Capital Investment Program 2 857 5 123 4 379

Total 2 857 5 123 4 379

Net Assets

Total assets deployed for Capital Investment Program 0 0

Total liabilities incurred for Capital Investment Program 0 0

Net Assets Deployed for Output Capital Investment Program 0 0

2012Budget

$'000

2012Actual

$'000

2011Actual

$'000

Continuing Operations

Revenue and Other Income from Transactions

Revenue from Special Capital Investment Funds 108 293 62 927 52 977

Sales of goods and services 0 62 45

Other revenue 0 3 2

Total Revenue and Other Income from Transactions 108 293 62 992 53 024

Expenses from Transactions