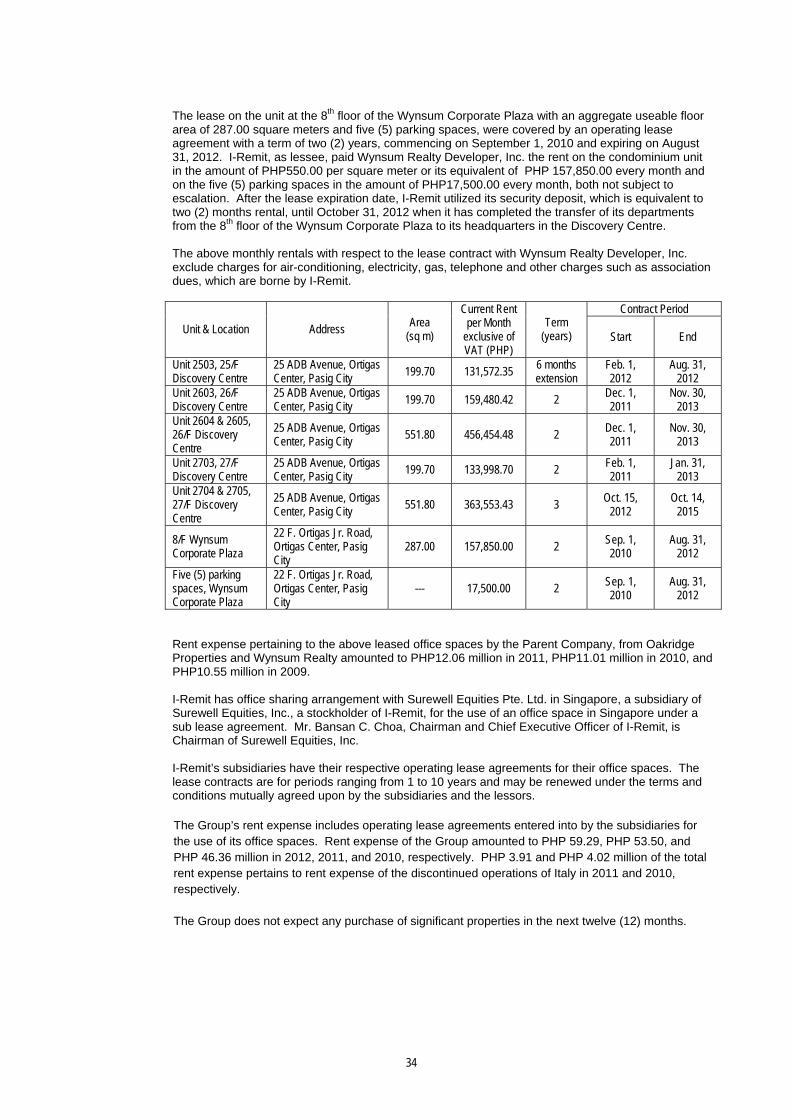

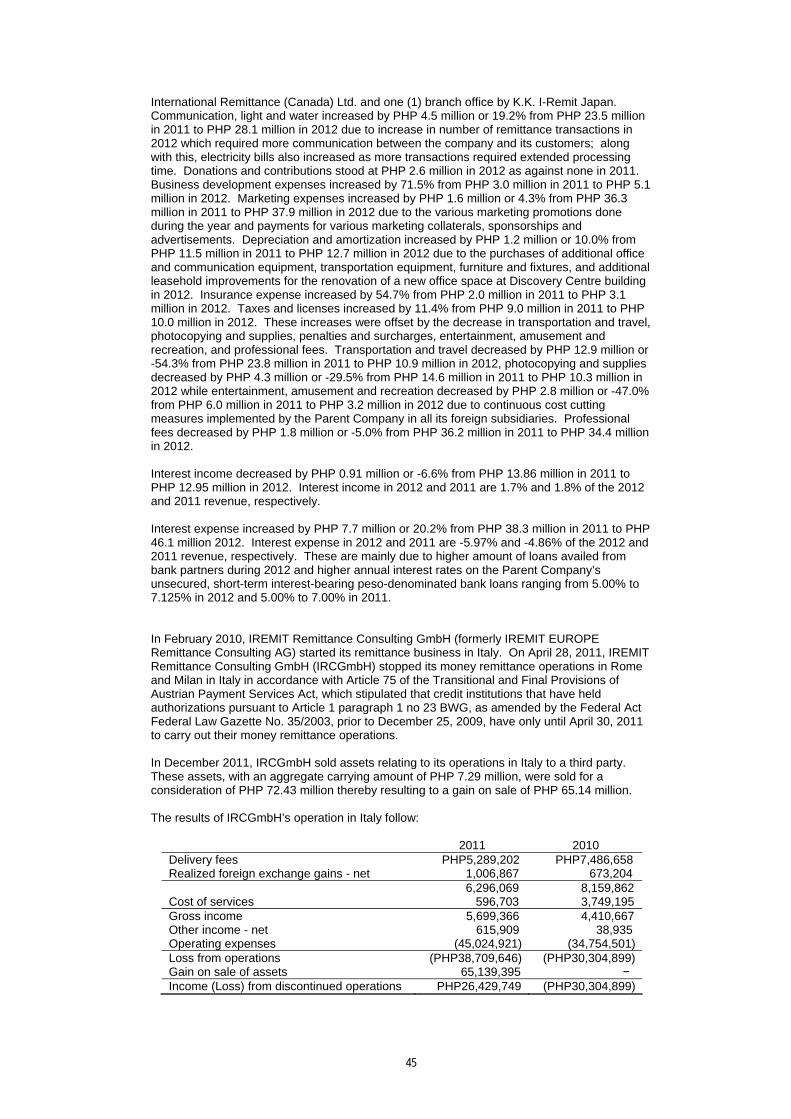

Embed Size (px)

Citation preview

1!I~!Jtlr www.myiremit.com

May 16, 2013

THE PHILIPPINE STOCK EXCHANGE, INC.3rd Floor, Philippine Stock Exchange PlazaAyala Triangle, Ayala AvenueMakati City, Metro Manila

Attention Ms. Janet A. EncarnacionHead, Disclosure Department

Gentlemen:

In accordance with the Securities Regulation Code, we are submitting herewith a copy ofSEC Form 17-A (Annual Report) of I-Remit, Inc. as at December 31,2012.

Thank you.

Very truly yours,

. JACILDOhief Operating Officer

I-Remit, Inc.26/F Discovery Centre, 25 ADB Avenue, Qrtigas Center, Pasig City 1605 PhilippinesTelephone: (632) 706-9999 and (632) 706-2737Facsimile: (632) 706-2767

COVER SHEET

A 2 0 0 1 0 1 6 3 1SEC Registration Number

I - R E M I T , I N C . A N D S U B S I D I A R I E S

(Company’s Full Name)

2 6 / F D i s c o v e r y C e n t r e , 2 5 A D B A v e

n u e , O r t i g a s C e n t e r , P a s i g C i t y

(Business Address: No. Street City/Town/Province)

Mr. HARRIS EDSEL D. JACILDO (02) 706 – 9999 Local 100/105/109 (Contact Person) (Company Telephone Number)

1 2 3 1 1 7 - A 0 7 Month Day (Form Type) Month Day

(Fiscal Year) (Annual Meeting)

(Secondary License Type, If Applicable)

Dept. Requiring this Doc. Amended Articles Number/Section

Total Amount of Borrowings

Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S Remarks: Please use BLACK ink for scanning purposes.

SEC Number A200101631 PSE Code File Number

I-REMIT, INC.

AND SUBSIDIARIES

(Company’s Full Name) 26/F Discovery Centre, 25 ADB Avenue,

Ortigas Center, Pasig City, 1605 Metro Manila

(Company’s Address) (02) 706 – 9999 Local 100 / 105 / 109 (Telephone Number) December 31 (Fiscal Year Ending)

(Month and Day)

SEC FORM 17-A Form Type Amendment Designation (if applicable) December 31, 2012 Period Ended Date (Secondary License Type and File Number)

SEC FORM 17-A

f'SECURITIES AND EXCHANGE COMMISSION A

D

ANNUAL REPORT PURSUANT TO SECTION 17OF THE SECURITIES REGULATION CODE AND SECTION 141

OF THE CORPORATION CODE OF THE PHILIPPINES

1. For the fiscal year ended December 31,2012

2. Commission Identification No. A200101631 3. BIR Tax Identification No. 210-407-466-000

4. Exact name of registrant as specified in its charter I-REMIT, INC.

5. _M::-=-=e..:.:tr,.=o....::.M:.::,a=::n=i1:=a:z...'P::...;H:..:.:..:IL=-:Ic::-P.::..P.:.:IN,.:..:E=::S=-:-:----:-_::--_6. _,. (SEC Use Only)Province, Country or other jurisdiction of Industry Classification Codeincorporation or organization

7. 26/F Discovery Centre, 25 ADB Avenue, Ortigas Center, Pasig City, Metro ManilaAddress of principal office

1605Postal code

8. (02) 706 - 9999 Local 100/105/109Issuer's telephone number, including area code

9. Not applicableFormer name, former address, and former fiscal year, if changed since last report

10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sec. 4 and 8 of the RSA

Title Number of Shares of Common StockOutstanding and Amount of Debt Outstanding

Common Stock 597,138,800 shares (as of December 31,2012)

II. Are any or all of these securities listed on a Stock Exchange?

Yes [,(] No [ ]

If yes, state the name of such stock exchange and the classes of securities listed therein:The Philippine Stock Exchange, Inc.

12. Check whether the issuer:

(a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder orSection 11 of the RSA and RSA Rule II(a)-1 thereunder, and Sections 26 and 141 of The CorporationCode of the Philippines during the preceding twelve (12) months (or for such shorter period that theregistrant was required to file such reports)

No [ ]

(b) has been subject to such filing requirements for the past 90 days

No [ ]

13. Aggregate market value of the voting stock held by non-affiliates of the registrant:PHP 1,666,017,252 (as of December 31, 2012, PHP 2.79 per share)

DOCUMENTS INCORPORATED BY REFERENCE

Documents incorporated by reference in any part of this report: 2012 Audited Parent Company and Consolidated Financial Statements of

I-Remit, Inc. and Subsidiaries (incorporated as reference for Items 1, 6, 7 and 8 of SEC Form 17-A)

TABLE OF CONTENTS

PART I BUSINESS AND GENERAL INFORMATION Item 1 Business 1 Item 2 Properties 33 Item 3 Legal Proceedings 35 Item 4 Submission of Matters to a Vote of Security Holders 35 PART II OPERATIONAL AND FINANCIAL INFORMATION Item 5 Market for Issuer’s Common Equity and Related Stockholder Matters 36 Item 6 Management’s Discussion and Analysis or Plan of Operation 41 Item 7 Financial Statements 59 Item 8 Changes in and Disagreements with Accountants on Accounting and Financial

Disclosure 59

PART III CONTROL AND COMPENSATION INFORMATION Item 9 Directors and Executive Officers of the Issuer 61 Item 10 Executive Compensation 72 Item 11 Security Ownership of Certain Beneficial Owners and Management 73 Item 12 Certain Relationships and Related Party Transactions 75 PART IV CORPORATE GOVERNANCE Item 13 Corporate Governance 78 PART V EXHIBITS AND SCHEDULES Item 14 a. Exhibit 79 b. Reports on SEC Form 17-C 79 SIGNATURES INDEX TO FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES INDEX TO EXHIBIT

1

PART I. BUSINESS AND GENERAL INFORMATION Item 1. Business (A) Description of Business (1) Business Development I-Remit, Inc. (“I-Remit”, “Parent Company”, or “Company”) is a company in the Philippines

engaged in the business of servicing the remittance needs of overseas Filipino workers (OFWs) and other migrant workers. The Parent Company was duly registered with the Securities and Exchange Commission (SEC) on March 5, 2001 with SEC Registration No. A200101631. It started commercial operations on November 11, 2001.

The Parent Company and its subsidiaries (“Group”) are primarily engaged in the business of

fund transfer and remittance services, from abroad into the Philippines or otherwise, of any form or kind of currencies or monies, either by electronic, telegraphic, wire or any other mode of transfer; as well as in undertaking the delivery of such funds or monies, both in the domestic and international market, by providing courier or freight forwarding services; and conducting foreign exchange transactions as may be provided by law and other allied activities relative thereto; provided that the foreign exchange transactions of the Parent Company shall be limited to ordinary money changing activity or “spot” foreign currency transaction; provided further that the Parent Company shall not engage in the business of being a commodity future broker or otherwise shall engage in financial derivatives activities such as foreign currency swaps, forwards, options or other similar instruments as defined under Bangko Sentral ng Pilipinas (BSP) Circular No. 102, Series of 1995.

The Parent Company is duly registered as a Remittance Agent with the Bangko Sentral ng

Pilipinas (BSP), with Certificate No. FX-2005-000364 issued on May 10, 2005, pursuant to BSP Circular 471 Series of 2005 dated January 24, 2005. It is subject to the applicable provisions of law and BSP rules and regulations, as well as the provisions of the Anti-Money Laundering Act of 2001 (Republic Act No. 9160 as amended by Republic Acts 9194, 10167, and 10365) and its revised implementing rules and regulations, and Republic Act 10168 or the Terrorism Financing Prevention and Suppression Act of 2012 and its implementing rules and regulations.

The Parent Company’s list of services also includes auxiliary services such as liaising and

coordinating with, and accepting and distributing membership contributions, loan amortization payments, and premium payments to various government and non-government entities such as the Social Security System (SSS), the Home Development Mutual Fund (HDMF or Pag-IBIG), the Philippine Retirement Authority (PRA) and the Philippine Health Insurance Corporation (PhilHealth), as well as various insurance, pre-need, and real estate companies.

The Parent Company is to exist for fifty (50) years from and after the date of incorporation. The registered office and principal place of business of the Parent Company is 26/F Discovery

Centre, ADB Avenue, Ortigas Center, Pasig City, 1605 Metro Manila, Philippines. The Company also operates in various countries through subsidiaries, associates, or affiliates,

and via tie-ups and strategic partnerships. Tie-up and partnership arrangements are utilized when the potential volume of remittances do not justify the investment of equity.

I-Remit currently operates in 25 countries and territories worldwide. Lucky Star Management Limited, the first international office of I-Remit, opened in Hong Kong

in May 2001. In the same year, I-Remit started its aggressive global expansion by forging alliances in other countries with high concentrations of overseas Filipino workers (OFWs) and Filipino migrants. In July 2001, I-Remit forged a tie-up with its Canadian partner International Remittance (Canada) Limited (IRCL), and established operations in three (3) major provinces of Canada: British Columbia, Alberta, and Ontario. In 2005, I-Remit acquired 65% ownership in the said company, and which was subsequently increased to 95% in 2006, and further consolidated to 100% by the end of June 2007. Also, in July 2001, I-Remit entered into its first European partnership in the United Kingdom (UK), and eventually started the operation of its subsidiary, IRemit Global Remittance Limited, in January 2003. It was sold by the Company in 2004 and was repurchased in June 2007. iRemit’s expansion in Europe is in pursuit of the authorization obtained from the Financial Services Authority of the United Kingdom by its wholly-owned subsidiary, IRemit Global Remittance Limited to operate as a payment institution in the European Economic Area (EEA). Under the European Payment Services Directive,

2

IRemit Global Remittance Limited may avail of its “passporting” rights and carry on its business activities in other EEA states by establishing branches, engaging agents, or providing cross-border services. I-Remit started its second Asian operation in Singapore through IRemit Singapore Pte Ltd, which commenced its commercial operations in October 2001. I-Remit acquired 49% ownership in the said company in June 2007. I-Remit further expanded in Asia through a tie-up in Taiwan, Hwa Kung Hong & Co., Ltd., which became operational in 2001. I-Remit acquired 49% ownership in the said tie-up in July 2009. I-Remit forged a tie-up in Australia that began its operations in September 2002. I-Remit Australia Pty Ltd (“IAPL”) was incorporated in December 2002 and in June 2007 ownership has been consolidated to 100%. Worldwide Exchange Pty Ltd (“WEPL”) in Australia started commercial operations in September 2003. The Company acquired 20% ownership of WEPL in June 2007 and additional 15% ownership in September 2007. On March 31, 2011, I-Remit acquired the 35% interest of minority shareholders in WEPL. With its 30% indirect voting interest through IAPL, I-Remit effectively owns 100.00% of WEPL. On July 25, 2007, the Financial Monetary Authority of Austria granted the remittance license of IREMIT EUROPE Remittance Consulting AG in which the Company has 74.9% equity interest. It started commercial operations on September 16, 2007. In November 2009, IREMIT EUROPE Remittance Consulting AG was registered by Banca D’Italia Eurosistema in the general list of financial intermediaries as a provider of money transfer services under Article 106 of the legislative decree 385/1993 of Italy’s Banking Law. On May 5, 2011, the Parent Company acquired the 25.10% ownership interest in IREMIT EUROPE Remittance Consulting AG from the noncontrolling stockholder. The acquisition increased the Parent Company’s ownership interest in IREMIT EUROPE Remittance Consulting AG to 100.0% from 74.9%. Consequently, on October 11, 2011, IREMIT EUROPE Remittance Consulting AG changed its legal name to IREMIT Remittance Consulting GmbH and changed its legal status from a stock company to a limited liability company. It also amended its Articles of Incorporation to include management consultancy in its business activities. I-Remit New Zealand Limited, a wholly-owned subsidiary was incorporated and its registration was approved by the New Zealand Ministry of Economic Development on September 11, 2007. It started commercial operations on February 13, 2008. On November 28, 2008, I-Remit’s Board of Directors (“Board”) ratified the acquisition of the 100.00% ownership interest in Power Star Asia Group Limited, a company based in Hong Kong which is engaged in foreign currency trading. On January 9, 2009, the Board of I-Remit authorized the acquisition of up to 49% of the outstanding capital stock of Hwa Kung Hong & Co., Ltd., a company engaged in the remittance business in Taiwan with offices in Taipei and Kaohsiung. The acquisition of the shares was completed on July 1, 2009. On June 10, 2011, K.K. I-Remit Japan was incorporated as a joint stock corporation in Tokyo, Japan with the primary purpose of providing money transfer and remittance services. On November 22, 2011, the company completed its registration with the Financial Services Agency (FSA) of Japan pursuant to the Payment Services Act of 2010. The company has offices in Tokyo and Nagoya.

The Company’s presence in various countries hosting overseas Filipino workers (OFWs) and

Filipino migrants and several strategic partnerships and tie-ups with various local and international banks, pawnshops, couriers, and telecommunications companies makes it the largest independent local remittance company.

The Company was also the first remittance company registered with the Board of Investments

(BOI) as a New Information Technology (IT) Service Firm in the Field of Information Technology Services (Remittance Infrastructure System) on a Non-Pioneer Status under the Omnibus Investments Code of 1987 which entitled the Company to Income Tax Holiday (ITH) Incentive for four (4) years and which was later extended to two (2) years and which expired on November 11, 2007.

I-Remit’s vision is to become the ultimate choice remittance service provider globally and to

capture a significant share of the huge annual inward remittances of OFWs around the world. It will achieve these by using the latest in information technology and communication technology through the Internet platform in delivering its products and services to its target customers.

3

The Company was initially incorporated with a capital stock of two hundred million pesos (PHP

200,000,000) divided into two million shares with a par value of one hundred pesos (PHP 100) per share.

The subscribers at incorporation are the following:

Name Nationality No. of Shares Subscribed

Amount of Capital Stock Subscribed

(PHP)

Amount Paid on Subscription (PHP)

iVantage Corporation Filipino 999,993 99,999,300.00 49,999,300.00 Ben C. Tiu Filipino 1 100.00 100.00 Wilson L. Sy Filipino 1 100.00 100.00 Willy N. Ocier Filipino 1 100.00 100.00 William L. Chua Filipino 1 100.00 100.00 Juan G. Chua Filipino 1 100.00 100.00 David R. de Leon Filipino 1 100.00 100.00 Randolph C. de Leon Filipino 1 100.00 100.00 TOTAL 1,000,000 100,000,000.00 50,000,000.00

On August 15, 2001, iVantage Corporation sold all its titles, rights, interests and obligations in

and to all its subscribed shares in the Company to the following:

Name Nationality No. of Shares Subscribed

Amount of Capital Stock Subscribed

(PHP)

Amount Paid on Subscription (PHP)

JTKC Equities, Inc. Filipino 650,000 65,000,000.00 32,500,000.00 Surewell Equities, Inc. Filipino 300,000 30,000,000.00 15,000,000.00 JPSA Global Services Co. Filipino 50,000 5,000,000.00 2,500,000.00 TOTAL 1,000,000 100,000,000.00 50,000,000.00

The new shareholders assumed pro rata the subscription payable to I-Remit, Inc. of iVantage

Corporation amounting to fifty million pesos (PHP 50,000,000). On February 8, 2005, JTKC Equities, Inc. assigned all of its rights, interests and obligations in

and to its entire subscription consisting of 650,000 shares in the Company unto Deighton Limited, a corporation organized and existing under the laws of Hong Kong.

On June 27, 2007, JTKC Equities, Inc. bought back the 650,000 shares in the Company from

Deighton Limited. On June 29, 2007, the Board and the stockholders of the Company approved the following

amendments to the Articles of Incorporation and By-Laws: On the Articles of Incorporation 1. Reduction of par value per share from PHP 100.00 to PHP 1.00 per share;

2. Increase in authorized capital stock from PHP 200 million to PHP 1.0 billion; 3. Denial of pre-emptive rights; 4. Authority of the Board of Directors to grant stock options, issue warrants or enter into

stock purchase or similar agreements; On the By-Laws 1. Period for closing of stock and transfer book or fixing of record date;

2. Period for notice of stockholders’ meeting; 3. Deadline for the submission / revocation of proxies; 4. Number, term of office, qualifications, and disqualifications; 5. Additional requirements for independent directors; 6. Election of directors; 7. Place of meeting of the Board of Directors; 8. Vacancies; 9. Constitution of a Nomination Committee; and

10. The addition of one or more Vice Chairmen to the list of officers of the Company.

4

On July 20, 2007, the Board approved a Special Stock Purchase Program (“SSPP”) for its

directors, the officers and employees of the Company who have been in service for at least one (1) calendar year as of June 30, 2007, and the Company’s resource persons and consultants. A total of fifteen million (15,000,000) shares of the Company, at a par value of one peso (PHP 1.00) per share, was allocated under the SSPP. The shares were allocated to those eligible to avail of the shares based on a formula developed by the Company’s SSPP Committee and approved by the Board of Directors.

The Board of Directors of the Company also declared stock dividends worth PHP

43,000,000.00 to its shareholders on July 20, 2007, which declaration was subsequently ratified and confirmed by the Company’s shareholders during their annual meeting held on the same day, immediately after the Board meeting. The Record Date was set on August 19, 2007, thirty (30) days from the date of approval of the Company’s shareholders.

On August 22, 2007, the Securities and Exchange Commission (“SEC”) approved the

Amended Articles of Incorporation and By-Laws of the Company. The shares subscribed and paid-up subsequent to the increase in capital stock were as

follows:

Name Nationality No. of Shares Subscribed

Amount of Capital Stock Subscribed

(PHP)

Amount Paid on Subscription (PHP)

Star Equities Inc. Filipino 158,418,225 158,418,225.00 158,418,225.00 Surewell Equities, Inc. Filipino 119,100,000 119,100,000.00 119,100,000.00 JTKC Equities, Inc. Filipino 99,631,775 99,631,775.00 99,631,775.00 JPSA Global Services Co. Filipino 19,850,000 19,850,000.00 19,850,000.00 TOTAL 397,000,000 397,000,000.00 397,000,000.00

On September 13, 2007, the SEC granted to the Company an exemption from registration of

the SSPP shares under Section 10.2 of the SRC. On September 20, 2007, the Company issued to the directors, officers and employees eligible to avail of the SSPP their respective shares under the program. Notwithstanding the aforesaid confirmation of the exempt status of the SSPP shares, the SEC nonetheless required the Corporation to include the SSPP shares among the shares of iRemit which were registered with the Commission prior to the conduct of its Initial Public Offering (IPO) in October 2007. The registration of the I-Remit shares, together with the SSPP shares, was rendered effective on October 5, 2007.

All 15,000,000 shares were subscribed. The shares subject of the SSPP were sold at par value or PHP 1.00 per share payable in full and in cash and subject to a lock-up period of two (2) years from date of issue which ended on September 19, 2009. The sale is further subject to the condition that should an officer or an employee resign from the Company prior to the expiration of the lock-up period, the shares purchased by such resigning employee or officer shall be purchased at cost by the Company’s Retirement Fund (“Retirement Fund”) for the benefit of retiring employees or officers. Total share purchases amounting to PHP11.74 million were paid in full while the difference amounting to PHP3.26 million were paid by way of salary loan. The shares acquired through the SSPP were subject to a lock-up period of two (2) years from the date of issue which ended on September 19, 2009.

On May 18, 2007, the Board of Directors of the Company approved the listing of its shares with

the Philippine Stock Exchange (“PSE”) in an initial public offering (IPO). The Board of Directors of the PSE, in its regular meeting on September 27, 2007, approved

the Company’s application to list its common shares with the PSE. On October 5, 2007, the Securities and Exchange Commission declared the Company’s Registration Statement in respect of the IPO effective and issued the Certificate of Permit to Offer Securities for Sale in respect of the offer shares.

The Company offered for subscription a total of 140,604,000 common shares each with par

value of PHP 1.00 per share consisting of (i) 107,417,000 new common shares issued and offered by the Company by way of a primary offer and (ii) a total of 33,187,000 existing shares offered by selling shareholders, JTKC Equities, Inc. (21,571,550 common shares issued), Surewell Equities (9,956,100 common shares offered), and JPSA Global Services Co. (1,659,350 common shares offered) pursuant to a secondary offer.

5

On October 17, 2007, the Company completed its IPO of 140,604,000 common shares,

representing slightly above 25% of the total outstanding capital stock of 562,367,000 (net of 50,000 treasury shares) at an offer price of PHP 4.68 per share for total gross proceeds of PHP 658,026,720.00.

The net proceeds from the primary offer of PHP 466,198,457.05, determined by deducting

from the gross proceeds of the primary offer the Company’s pro-rated share in the professional fees, underwriting and selling fees, listing and filing fees, taxes and other related fees and expenses, is intended to be used by the Company to finance, in part, its expansion in other countries and to partially retire some of the Company’s short term interest-bearing loans.

On August 16, 2008, the Board of the Company authorized the buy-back from the market of up

to 10 million shares, representing approximately 1.78% of I-Remit’s outstanding common shares. The program was adopted with the objective of preserving the value of the Company’s shares, which was grossly undervalued at that time. The program also sought to boost investor confidence in the Company. A total of 10,000,000 shares have been purchased and lodged as treasury shares. On September 16, 2011, the Board of the Company authorized the buy-back from the market of up to 10 million shares, representing approximately 1.64% of I-Remit’s outstanding common shares. The program was adopted with the objective of preserving the value of the Company’s shares, which was grossly undervalued at that time. The program also sought to boost investor confidence in the Company. A total of 10,000,000 shares have been purchased and lodged as treasury shares. On September 21, 2012, the Board of the Company authorized the buy-back from the market of up to 10 million shares, representing approximately 1.67% of I-Remit’s outstanding common shares. The program was adopted with the objective of preserving the value of the Company’s shares, which was grossly undervalued at that time. The program also sought to boost investor confidence in the Company. A total of 587,000 shares have been purchased and lodged as treasury shares.

As of March 31, 2013, the Company’s capital structure is as follows:

Name Nationality No. of Shares

Subscribed

Amount of Capital Stock Subscribed

(PHP)

% to Total Number of

Shares Star Equities Inc. Filipino 174,260,047 174,260,047.00 29.3342 Surewell Equities, Inc. Filipino 139,450,290 139,450,290.00 23.4745 JTKC Equities, Inc. Filipino 127,153,247 127,153,247.00 21.4044 JPSA Global Services Co. Filipino 19,510,000 19,510,000.00 3.2842 Public Various 133,677,216 133,677,216.00 22.5027 Total, March 31, 2013 594,050,800 594,050,800.00 100.0000

The Company’s general expansion plans in 2013 include the opening of new and/or additional

offices or the engagement of new tie-ups and partners in Ireland, Macau, Germany, the Netherlands, Saudi Arabia, Oman, Qatar and Kuwait.

6

(2) Business of Issuer (a) Description of Registrant The Parent Company and its subsidiaries are primarily engaged in the business of fund

transfer and remittance services of any form or kind of currencies or monies, either by electronic, telegraphic, wire or any other mode of transfer and undertakes the delivery of such funds or monies, both in the domestic and international market, by providing either courier or freight forwarding services; and conducts foreign exchange transactions as may be allowed by law and other allied activities relative thereto.

The Company’s subsidiaries are as follows: International Remittance (Canada) Ltd., a wholly-owned subsidiary, was incorporated

on July 16, 2001 pursuant to the Canada Business Corporations Act. It is registered with Industry Canada with registration number 392271-5. It is also registered as an extraprovincial company with the Registrar of Companies of the Province of British Columbia with certificate of registration number A-60718 dated December 3, 2003. Pursuant to the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, International Remittance (Canada) Ltd. is registered as a money service business (MSB) with the Financial Transactions and Reports Analysis Centre of Canada with registration number M081607706 valid until June 28, 2014 and subject to renewal every two (2) years. It started initially as a tie-up and partner of I-Remit, Inc, establishing its operations in three (3) major provinces in Canada, namely: British Columbia, Alberta, and Ontario. In 2005, I-Remit, Inc. acquired 65% ownership in the company that subsequently was increased to 95% in 2006 and eventually consolidated to 100% on June 29, 2007. It currently operates in nine (9) locations in Canada: Banff, Alberta; Bathurst Street, Toronto, Ontario; Pacific Mall, Calgary, Alberta; 7th Avenue, Calgary, Alberta; Edmonton, Alberta; Jamestown, Toronto, Ontario; Mississauga, Ontario; Richmond, British Columbia; and Winnipeg, Manitoba. The Filipino community is the third largest minority group in Canada. The Commission on Filipinos Overseas estimated that there were about 842,651 Filipinos in Canada as of December 2011.

I-Remit Australia Pty Ltd, a wholly-owned subsidiary, is a company incorporated on

December 10, 2002 in Victoria, Australia under the Australian Corporations Act 2001 and registered with the Australian Securities and Investments Commission with Australian Company Number (ACN) 103 107 982 and Australian Business Number (ABN) 22 103 107 982. As of June 29, 2007, the ownership of I-Remit, Inc. has been consolidated to 100%. Pursuant to subsection 75C(2) of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 of Australia, I-Remit Australia Pty Ltd is registered with the Australian Transaction Reports and Analysis Centre (AUSTRAC) as an affiliate of I-Remit, Inc. with remittance affiliate number AFF100314117-001 with effect from October 22, 2012 and valid for three (3) years thereafter. It has no regular employees and has not, since incorporation, engaged in any material activities other than those related to the maintenance of a bank account. Presently, it has a bank account with Westpac Banking Corporation where I-Remit’s agents deposit the remittances they receive for the purpose of eventually transferring the accumulated balances to I-Remit’s bank accounts in the Philippines.

IREMIT Remittance Consulting GmbH (formerly IREMIT EUROPE Remittance

Consulting AG) (100% owned) was incorporated on July 20, 2005 in Vienna, Austria. It started commercial operations on September 16, 2007. In November 2009, IREMIT EUROPE Remittance Consulting AG was registered by Banca D’Italia Eurosistema in the general list of financial intermediaries as a provider of money transfer services under Article 106 of legislative decree 385/1993, Italy’s banking law. It opened branches in Milan and Rome in Italy on April 18, 2010 and August 1, 2010, respectively. On April 28, 2011, it stopped its money remittance operations in accordance with Article 75 of the Transitional and Final Provisions of the Austrian Payment Services Act (Zahlungsdienstegesetz) which stipulated that credit institutions that have held authorizations pursuant to Article 1 paragraph 1 no. 23 of the Austrian Banking Act (Bankwesengesetz, BWG), as amended by the Federal Act, federal Law Gazette No. 35/2003, prior to December 25, 2009, had only until April 30, 2011 to carry out their money remittance operations. On May 5, 2011, the parent company, I-Remit, Inc., acquired the 25.1% ownership interest from a non-controlling stockholder of the company. The acquisition enabled I-Remit, Inc. to have 100% ownership of IREMIT EUROPE Remittance Consulting AG. Consequently, on October 11, 2011, it changed its legal name to IREMIT Remittance Consulting GmbH and changed its legal status

7

from a stock company to a limited liability company. It also amended its articles of incorporation to include management consultancy in its business activities. IREMIT Remittance Consulting GmbH was subsequently registered as an agent of IRemit Global Remittance Limited (United Kingdom) after the latter’s acquisition of passporting rights for establishment and offering of cross-border services in Austria. Pursuant to Article 12 para. 6 of the Austrian Payment Services Act (Zahlungsdienstegesetz), the Austrian law on the European Payment Services Directive (Directive 2007/64/EC), IREMIT Remittance Consulting GmbH provides money remittance services in Austria. It is registered in the Register of Payment Institutions of the Financial Services Authority of the United Kingdom with firm reference number 574797. The Commission on Filipinos Overseas estimated that there were 25,112 Filipinos in Austria as of December 31, 2011 who were mostly employed in the nursing field and other skilled and semi-skilled occupational groups.

IRemit Global Remittance Limited, a wholly-owned subsidiary, is a private limited

company in the United Kingdom and Wales that was incorporated on June 22, 2001. It is registered with the Companies House of the United Kingdom with company number 04239974 pursuant to the Companies Act 2006. It started commercial operations in July 2001. Initially, I-Remit, Inc. had a 96% equity interest in IRemit Global Remittance Limited until it was sold on January 18, 2004. I-Remit, Inc. reacquired the company on June 29, 2007 with 100% ownership interest. On April 15, 2011, it acquired authorization from the Financial Services Authority to carry on payment services activities, particularly, money remittance, pursuant to the Payment Services Regulations 2009 of the United Kingdom, the British law implementing the European Payment Services Directive (Directive 2007/64/EC). It was issued its FSA reference number 537568. On April 1, 2013, it was placed under the regulatory authority of the Financial Conduct Authority that replaced the Financial Services Authority. The company is registered with Her Majesty’s Customs and Excise with money laundering registration number 1213085 with certificate of registration issued on May 22, 2012 and expiring on June 1, 2013 subject to renewal. IRemit Global Remittance Limited has offices in London and Manchester in the United Kingdom, and in Milan and Rome in Italy. It has agents in the United Kingdom, Germany, and Austria. The Commission on Filipinos Overseas estimated that there were about 220,000 Filipinos in the United Kingdom who work mostly as nurses and caregivers in public and private nursing homes, medical professionals, and chambermaids.

I-Remit New Zealand Limited, a wholly-owned subsidiary, was incorporated on

September 11, 2007. It is registered with the Registrar of Companies of the Ministry of Economic Development with certificate number 1984331. The company is registered in the Financial Service Providers (FSP) Register of the Companies House of New Zealand with FSP number 45263. It is also a participant in Financial Services Complaints Limited, a dispute resolution organization. It has an office in North Park, Manukau. The company started operating commercially on February 13, 2008. The Commission on Filipinos Overseas estimated that there were 35,175 Filipinos in New Zealand as of December 2011.

Lucky Star Management Limited, a wholly-owned subsidiary, was incorporated on

March 16, 2001 as a limited liability under the Companies Ordinance (Cap 32) of Hong Kong. It is registered in the Companies Registry with company number 750525. It is licensed as a money service operator pursuant to Section 30 of the Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Cap 615) with license no. 12-07-00326 from July 9, 2012 to August 8, 2014. It has offices in World Wide Plaza, Central; United Center, Admiralty; and Lik Sang Plaza, Tsuen Wan. The Commission on Filipinos Overseas estimated that there were 174,851 Filipinos in Hong Kong as of December 2011.

Power Star Asia Group Limited, a wholly-owned subsidiary, was incorporated on April

28, 2008 under the Companies Ordinance (Cap 32) of Hong Kong. It is registered with the Companies Registry with company number 1232132. It was acquired by I-Remit, Inc. on November 12, 2008. Power Star Asia Group Limited is engaged in foreign exchange trading activities.

Worldwide Exchange Pty Ltd, a wholly-owned subsidiary (through a direct equity

interest of 70% and indirect equity interest through I-Remit Australia Pty Ltd of 30%), is a company that was incorporated on September 29, 2003 in Queensland, Australia under the Australian Corporations Act 2001 and registered with the Australian Securities and Investments Commission with Australian Company Number (ACN) 106 493 047 and Australian Business Number (ABN) 35 106 493 047. Pursuant to

8

subsection 75C(2) of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 of Australia, Worldwide Exchange Pty Ltd is registered with the Australian Transaction Reports and Analysis Centre (AUSTRAC) as an affiliate of I-Remit, Inc. with remittance affiliate number AFF100309950-001 with effect from September 28, 2012 and valid for three (3) years thereafter. It has offices in Blacktown, New South Wales and in Perth, Western Australia. It started commercial operations in September 2002. The Commission on Filipinos Overseas estimated that there were 384,637 Filipinos in Australia as of December 2011.

K.K. I-Remit Japan is a joint stock corporation (“Kabushiki Kaisha”) that was

incorporated and registered on June 10, 2011 in Tokyo, Japan with the primary purpose of providing money transfer and remittance services. Its company number is 0100-01-140611. On October 14, 2011, it became a member of the Japan Payment Service Association (JPSA), the designated dispute resolving organization for payment service providers, including money transfer companies. On November 22, 2011, the company completed its registration with the Financial Services Agency (FSA) of Japan pursuant to the Payment Services Act of 2010 with Registration No. KLFB00019. The company has offices in Tokyo and Nagoya. It started commercial operations in Tokyo on May 14, 2012 and in Nagoya on September 1, 2012. The Commission on Filipinos Overseas estimated that there were 220,882 Filipinos in Japan as of December 31, 2011.

The Company’s associates are as follows: IRemit Singapore Pte Ltd (49% owned) is a private limited company that was

incorporated on May 11, 2001 and is registered in the Registry of Companies and Businesses of the Accounting and Corporate Regulatory Authority with company number 200103087H. It is licensed by the Monetary Authority of Singapore to carry on the remittance business pursuant to Section 8(3) of the Money-changing and Remittance Businesses Act (Cap 187) with RA No. 01038 valid until December 31, 2013 and renewable every year. It started commercial operations in October 2001. The Commission on Filipinos Overseas estimated that there were 180,000 Filipinos in Singapore as of December 2011.

Hwa Kung Hong & Co. Ltd. (49% owned) is registered with the Department of Foreign

Exchange, the Central Bank of China with Issued Document No. Taipei Central No. 0980000061. It has offices in Taipei and Kaohsiung. The Commission on Filipinos Overseas estimated that there were 93,896 Filipinos in Taiwan as of December 2011.

Principal Products and Services Through the years, I-Remit has developed products and services that cater specifically

to the various remittance needs of OFWs and other migrant workers as follows: Bank-to-Bank A facility for “same-day” online crediting to bank

account in the Philippines. A remittance transaction received before 12:00 noon Manila time may be withdrawn by the designated beneficiary from the bank branch or any BancNet, MegaLink, or ExpressNet automated teller machine (ATM) on the same day of the remittance transaction. As of December 31, 2012, there were 9,472 bank branches and 12,285 ATMs in the Philippines.

Door-to-Door Delivery of cash remittances to designated

beneficiaries through third party couriers. I-Remit has the widest delivery reach nationwide, capable of delivering cash remittances within the day for beneficiaries in Metro Manila and the province of Rizal. Next-day deliveries may be made in the following cities and provinces: Batangas, Bulacan, Cavite, Cebu, Davao, Laguna, La Union, Pampanga, Pangasinan, Tacloban, and Tarlac. Deliveries in other remote areas may be made in two (2) to three (3) days or more depending on the actual location of the beneficiary. I-Remit can deliver in 17 regions, 79 provinces, and 136 cities and municipalities in the country.

9

Notify-to-Pay Allows a beneficiary in the Philippines to pick-up a

remittance in any of I-Remit’s 9,559 pay-out stations within 24 hours. These designated pay-out stations number 2,843 in Metro Manila; 2,952 in the rest of Luzon; 2,319 in the Visayas; and 1,445 in Mindanao. I-Remit has tied-up with the following commercial banks, thrift banks, rural banks, pawnshops and remittance agents which branches serve as pay-out stations for cash pick-up: Allied Banking Corporation; Bank of the Philippine Islands; BDO Unibank; Cebuana Lhuillier Pera Padala; China Banking Corporation; CIS Bayad Centers; Development Bank of the Philippines; Eight Under Par, Inc. (Palawan Pawnshops); Enterprise Bank, Inc.; ExpressPay, Inc.; First Consolidated Bank; Global Pinoy Remittance and Services; HJP Pawnshop; KwartaGram Corporation; Maybank Philippines, Inc.; ML Kwarta Padala; One Network Bank, Inc.; Philippine National Bank; Philippine Savings Bank; Philippine Veterans Bank; Prime Asia Pawn and Jewelry Shop, Inc.; Rural Bank of Malinao, Inc.; Security Bank Corporation; Security Bank Savings (formerly Premiere Development Bank); Sterling Bank of Asia (A Savings Bank); Tambunting Pawnshop Philippines; Union Bank of the Philippines; UCPB Savings Bank; United Coconut Planters Bank.

Visa Card I-Remit Visa Card is a “debit and ATM card in one”

through which remitters can send money to their beneficiaries almost instantaneously. Cardholders may withdraw cash from more than 10,000 BancNet, MegaLink, or ExpressNet ATMs in the Philippines and any Visa ATM worldwide. As a debit card, cardholders may use the I-Remit Visa Card to pay for their purchases from any of the 12 million Visa-affiliated merchant establishments in over 170 countries worldwide. The I-Remit Visa Card is issued in partnership with Chinatrust (Philippines) Commercial Bank Corporation while the Visa Electron Card is issued in partnership with the Standard Chartered Bank Philippines. In 2008, I-Remit also introduced the I-Remit Shop ‘N’ Pay Card in partnership with Sterling Bank of Asia (A Savings Bank). The I-Remit Shop ‘N’ Pay Card utilizes the EMV (Europay, MasterCard, Visa) technology, the standard for the interoperation of IC cards (“chip cards”) and IC capable POS terminals and ATMs, for authenticating credit and debit card payments.

10

Auxiliary Services I-Remit is authorized to accept payments,

contributions, premiums, or donations from Filipinos abroad for the following government agencies, private companies, and organizations: Social Security System (SSS); Overseas Workers Welfare Administration (OWWA); Home Development Mutual Fund (HDMF or Pag-IBIG); Philippine Health Insurance Corporation (PhilHealth); AMA Communities, Inc.; AMA Land, Inc.; CDC Holdings, Inc.; Century Properties Group, Inc.; CHMI Land, Inc.; C&P Properties International, Inc.; Citihomes Builders and Development, Inc.; Confed Properties, Inc.; DMCI Homes, Inc.; Duraville Realty and Development Corporation; Durawood Lumber and Construction Supply; Dynamic Realty and Resources Corporation; Earth and Style Corporation; Earth Aspire Corporation; Earth Prosper Corporation; Extraordinary Development Corporation; Eton Properties Phils., Inc.; Fiesta Communities, Inc.; Hausland Development Corporation; Homeowners Development Corporation; Ledesco Development Corporation; LLSP Development Corporation; Major Homes, Inc.; Major Properties, Inc.; Malate Construction and Development Corporation; Megaworld Corporation; Northpine Land, Inc.; Phinma Property Holdings Corporation; PICAR Development, Inc.; Pioneer Life, Inc.; Pueblo de Oro Development Corporation; RJ Lhinet Development Corporation; Robinson’s Homes, Inc.; SM Development Corporation; SM Synergy Property Holdings, Inc.; Surewell Equities, Inc.; Vistaland International Marketing; CBN Asia, Inc.; Insular Life Assurance Co., Ltd.; Jollibee Foods Corporation; Nestle Philippines; Savers Appliance Depot (Sentine Development Corporation); Suntrust Home Developers, Inc.; Zalora Philippines (BF Jade E-Services Phils., Inc.).

SMS (Short Message

Service) via Globe G-Cash and Smart Padala

Beneficiaries may encash remittances in more than 5,000 Globe G-Cash and Smart Padala encashment centers and ATMs nationwide once received on their mobile phones. Beneficiaries may also use the facility for “cashless shopping” in G-Cash and Smart affiliated business establishments.

iRemit Direct Online

Remittance System (iDOL)

iDOL is I-Remit’s Internet-based remittance service that offers convenient and secure remittance services online. It is currently available to Filipinos in Canada and the United Kingdom. It will also be made available in Australia, Hong Kong, Italy, Japan, New Zealand, and Taiwan.

11

I-Remit derives its income from remittance transactions in the form of: (i) service fees,

and (ii) on the spread on the applicable foreign exchange rate for each conversion of any remittance to the Philippines. Service fees cover all logistical and operational expenses of the Company and its partner or tie-up company for each remittance transaction. These fees vary per country of operation depending on competition and the current foreign exchange situation. The timing of a remittance is also a consideration in applying a foreign exchange factor.

Percentage of Sales or Revenues Contributed by Foreign Sales I-Remit operates in various countries through its subsidiaries and associates or through

tie-ups. The former allows the Company to own up to 100% equity while the latter is through agent-partner agreements. Partnership arrangements are utilized when the volume of remittances do not justify incorporating new companies.

Due to the nature of its business, a substantial portion of the Company’s sales or

revenues are from foreign sales. The percentage shares of the Company’s major markets in terms of total value of

inward remittances (in US dollar amounts) is as follows: Share in Value (in USD) of Remittances Region 2012 2011 2010 Asia-Pacific 32% 32% 34% Europe 11% 11% 11% Middle East 17% 18% 19% North America 12% 14% 15% Others 28% 25% 21% Total 100% 100% 100% The percentage shares of the Company’s major markets in terms of the volume

(number of transactions) of inward remittance transactions is as follows: Share in Volume (in No. of Transactions) of Remittances Region 2012 2011 2010 Asia-Pacific 42% 43% 43% Europe 12% 11% 10% Middle East 30% 29% 29% North America 13% 14% 15% Others 3% 3% 3% Total 100% 100% 100%

12

Distribution Methods of the Products or Services I-Remit operates globally through a combined network of branches and tie-ups

worldwide offering its products and services to overseas Filipino workers (OFWs). Currently, I-Remit is present in the following 25 countries and territories:

Asia Pacific Europe Middle East North America Australia Austria Bahrain Canada Brunei Germany Israel Hong Kong Greece Jordan Indonesia Ireland Lebanon Japan Italy Qatar Malaysia Spain United Arab Emirates New Zealand The Netherlands People’s Republic of China United Kingdom Singapore Taiwan The Company’s general expansion plans in 2013 include the opening of new and/or

additional offices or the engagement of new tie-ups and partners in Ireland, Macau, Germany, the Netherlands, Saudi Arabia, Oman, Qatar and Kuwait.

The distribution methods in the Philippines of the Company’s products or services are

as described under “Principal Products and Services.” Remittances may be credited to any bank account in the Philippines and the funds may

be withdrawn from the branch of account or from automated teller machines (ATMs). As of December 31, 2012, there were 9,472 bank branches and 12,285 ATMs in the Philippines.

I-Remit has the widest coverage in door-to-door delivery nationwide and is capable of

delivering cash remittances within the day for beneficiaries in Metro Manila and the province of Rizal. Next-day deliveries may be made in the following cities and provinces: Batangas, Bulacan, Cavite, Cebu, Davao, Laguna, La Union, Pampanga, Pangasinan, Tacloban, and Tarlac. Deliveries in other remote areas may be made in two (2) to three (3) days or 10 – 12 days depending on the specific location of the beneficiary. I-Remit can deliver in 17 regions, 81 provinces, and 136 cities and municipalities in the country.

Under the Company’s “Notify-to-Pay” services, remittances may be picked up by

beneficiaries in any of I-Remit’s 9,559 designated pay-out stations nationwide. Beneficiaries may also encash remittances in more than 5,000 Smart Padala and Globe

G-Cash encashment centers nationwide once notified by “text” on their mobile phones.

New Products or Services iDOL, the Company’s Internet-based remittance service that offers convenient and

secure remittance services online was made available to Filipinos in Canada and the United Kingdom in 2012. It will also be made available in Australia, Hong Kong, Italy, Japan, New Zealand, and Taiwan.

There are other services planned for launching in 2013. These products and services

are intended to improve product delivery and enhance I-Remit’s competitiveness in the OFW remittance market. Among these are various payment and collection services. The Company also intends to offer its remittance services to other nationalities through partnerships with banks or remittance companies of countries that have large populations of overseas workers. There are no publicly-announced new products or services which completion of development would require a material amount of the resources of I-Remit. New products or services will be developed using internal resources.

13

Competition Players In its publication “Migration and Development Brief 20” (April 19, 2013), the World Bank

estimated that officially recorded remittances to developing countries reached USD 401 billion in 2012 growing by 5.3 percent compared with 2011. The money transfer or remittance industry has numerous players that are classified into two (2) major categories: the formal and informal channels.

Formal Channels Formal funds transfer or remittance channels may be defined as composed of

institutions that transfer value or funds from one geographic location to another and are operating within the regulated financial sector. These institutions are regulated and supervised by government agencies and by laws and regulations that determine their establishment and scope of operations. Based on the standards set by the Financial Action Task Force (IX Special Recommendations) and the Basel Committee on Banking Supervision, aside from licensing and registration, formal remittance institutions must have in place mechanisms for customer due diligence and monitoring of transactions. The formal channels may include banks, money transfer operators, credit unions, and postal services.

Banks. The Philippine remittance industry is dominated today by the country’s five

largest universal banks that lay claim to 85 percent of the total remittances flowing through the formal channels. There are over 20 commercial and thrift banks that are active players in the Philippine overseas remittance industry. Many remittance centers operating abroad are either subsidiaries or affiliates of domestic banks and are incorporated under the laws of their host countries. Some local banks have also established tie-up arrangements with banks and money transfer operators abroad. The major commercial banks in the Philippines involved in the remittance industry such as Banco de Oro Unibank, Philippine National Bank, Metropolitan Bank and Trust Company, Bank of the Philippine Islands, and the Rizal Commercial Banking Corporation. These banks also subscribe to the SWIFT system for bank-to-bank transfers and have a combined international network of correspondent banks, overseas branches, and international remittance centers.

International Money Transfer Operators. International money transfer operators consist

of companies whose subsidiaries or affiliates are licensed or registered with regulatory agencies. These operate under laws and regulations that are specific to money transfer operators or payment service providers. Among these companies are Western Union, MoneyGram, Trans-Fast, Xpress Money, and Ria Money Transfer.

Domestic Money Transfer Companies. The major domestic players include I-Remit,

LBC Express, Lucky Money, 2GO, M. Lhuillier, and Cebuana Lhuillier. Most of the companies classified under this category are local logistics service providers, courier companies, or pawnshops that have branched out into the remittance business.

Telecommunications Companies. The continuing advances in information and

telecommunications technologies allowed companies such as Smart Communications, Inc. and Globe Telecom, Inc. to offer innovative modes of sending and receiving remittances such as through short messaging system (SMS) or “text” or through e-money. Smart introduced Smart Padala in August 2004 while Globe introduced GCash in October 2004. International money transfer companies are also starting to utilize mobile phones for their money transfer businesses. In 2006, Internet payments innovator started its mobile SMS-based transfer system called PayPal Mobile. It has also developed applications for popular smart phones Blackberry, iPhone, and Android. In 2009, Twitter launched TwitPay, which interfaces with PayPal’s platform and uses the sender’s mobile-enabled Twitter account as a platform to send money to other Twitter users. The company TextPayMe was acquired in 2010 by Amazon.com which also offers Internet-based transfers through its Amazon Payments service. Through Amazon.com’s TextPayMe, users with an Amazon Payments account can send money to another person by sending an SMS text message with their mobile phone, or using their mobile phone’s Internet browser or one of several special applications designed for smartphone users. MasterCard also launched its MoneySend service in the United States which allows senders to make payments via SMS text message of their phone’s Internet browser.

14

Technology-Based Companies. The emerging new players in the industry are

composed mostly of technology-based companies that utilize the Internet in offering remittance services. Their services may be availed of through traditional browers or via Web-enabled mobile phones. The online money transfer companies tapping the Philippine market are composed of Remit2Home, Xoom, and PayPal. Many remittance companies are also expanding their operations through the Internet. Western Union and MoneyGram currently offer customers the option of sending money online, as do banks such as Wells Fargo and Citibank.

Informal Channels Informal channels refer to institutions that engage in the remittance business outside of

the regulated financial sector. Cash may be sent through the recruitment agency or through the local office of the employer, through friends, relatives, or fellow workers traveling back to the Philippines. Alternatively, OFWs can bring the cash themselves upon their return to the Philippines.

“Padala” System. The literal meaning of the local word “padala” is to send something

through the courtesy of another person. In this practice, it is assumed that the person asked to bring the money to the Philippines is reliable and trustworthy, and the practice repeats as trust and confidence builds between the parties with each completed delivery.

“Kaliwaan” System. The system, despite its lack of popularity, operates through a well-

tested network of currency exchanges. It involves the use of agents in the source and destination countries who operate outside of regulatory restrictions as they arrange currency transfers. The method has been the subject of congressional inquiries because of its use in laundering monetary proceeds from illegal activities such as “jueteng.”

Hand-carry System. This method refers to the practice of overseas Filipinos in bringing

home cash themselves when they return to the Philippines for vacation or after the expiration of their work contracts.

OFW remittances continue to fuel the Philippine economy. The continuing upward

trends in inward remittance flows are expected to be sustained by the increased deployment of OFWs. Likewise, there is an observed overall shift from the utilization of unregulated, informal channels to the more formal structured channels for remittances that emphasizes the growing need for reliability, efficiency and convenience.

As competition among industry players intensifies, banks, money transfer agents, and

other similar service providers are expected to become more aggressive in their marketing and promotional activities to lure potential clients and capture larger shares of the market.

Advances in information and communications technology have allowed new players to

roll-out a growing variety of products and services catering to the evolving needs and requirements of OFWs. Such innovative approaches are expected to fuel further industry growth, help reduce transaction costs, and improve service delivery. Due to rising competition from non-traditional players, banks and money transfer agents need to upgrade their technology, expand network coverage, and enhance their distribution structures.

Industry players, particularly banks and remittance agents, will always be on the look-

out and competing for new tie-up arrangements with overseas partners, particularly in untapped geographic markets. Banks and other financial institutions will continue to seek partnership opportunities with correspondent banks, money transfer agents, and other types of partners overseas to expand their coverage while also planning to establish their own offshore units in key overseas markets like the Middle East, Canada, and the United States, that have a growing concentration of OFWs and Filipino immigrants. While the industry remains highly-competitive, industry players often link-up and have overlapping or complementary offerings with other service providers under revenue-sharing schemes.

I-Remit expects to encounter direct and indirect competition from domestic and foreign

companies offering money remittance services locally and internationally.

15

The Company competes mainly in terms of pricing and service efficiency against the

domestic commercial banks, Philippine-based money transfer agencies, international money transfer agencies, and telecommunications firms.

I-Remit is able to compete effectively against the major players in the industry because

of its network of branches and tie-ups abroad, its local tie-ups with local and foreign banks, its flexibility to expand in other markets, its relatively faster decision-making process, and its marketing strategies that are customized for the Filipino populations in each country that it operates in.

The Company believes that its customer-centric model, complemented by its flexible

and dynamic structure, will allow it to compete actively in the local and international markets by capitalizing on its strengths in its core business while offering value-added services to OFWs around the world. The Company similarly believes that with its relentless drive for innovation, its streamlined organization, and efficient cost structure in its local and foreign operations, it will be able to compete effectively in the global marketplace through the continuous establishment of foreign offices in strategic locations characterized by high-densities of OFW populations that will allow it to tap a broader market, and consequently, deliver potentially high-yield profits.

Sources and Availability of Raw Materials and Names of Principal Suppliers The Company has a broad base of suppliers, both local and foreign. The Company is

not dependent on one or a few suppliers in conducting its business.

Dependence Upon a Single Customer or a Few Customers The Company serves a wide spectrum of overseas Filipino workers (OFWs) and

Filipino immigrants of different occupational groups in 25 countries and territories around the world. It is not dependent on a single customer or a few customers. Neither is there a single customer that accounts for, or will account for 20% or more of the Company’s sales. The International Organization for Migration (IOM)'s report on ''Health in the Post-2015 Development Agenda'' cited that there are approximately 215 million international migrants as of 2011. About 5% of this number or 10.46 million are overseas Filipinos in about 217 countries and territories. In 2011, the permanent migrants (47% or 4.86 million) comprise the largest category of overseas Filipinos, followed closely by temporary migrants (43% or 4.51 million). The irregular migrants (10% or 1.07 million) constitute the smallest category. Compared with 2010 data, the number of permanent, temporary, and irregular migrants increased by 10%, 4.36% and 52%, respectively. Irregular migrants could be found mainly in the United States, Malaysia, and Singapore. The large increase of irregular migrants in 2011 can mainly be traced to Malaysia’s 124% increase of irregular migrants from 200,000 in 2010 to 447,590 in 2011; and United States’ 67% increase from 156,000 in 2010 to 260,000 in 2011. The Philippine Overseas Employment Administration (POEA) also reported an increase in the number of workers deployed which in 2012 grew by 6.7 percent at 1,800,465 against the 1,687,831 in 2011. In its Migration and Development Brief 20 dated April 19, 2013, the World Bank estimated that officially recorded remittances to developing countries are expected to have reached USD 401 billion in 2012, up by 6.5% from USD 381 billion in 2011. The top recipients of remittances in 2012 are: India (USD 70 billion); China (USD 66 billion); the Philippines (USD 24 billion); Mexico (USD 24 billion); and Nigeria (USD 21 billion). The Bangko Sentral ng Pilipinas (BSP) reported that the 2012 full-year personal remittances of overseas Filipinos to the Philippines reached USD 23.8 billion, higher by 6.4% compared to the inflows recorded in 2011. The growth in remittances was driven by higher personal transfers from land-based overseas Filipino workers with work contracts of one year or more (by 13.3%), as well as sea-based workers and land-based workers with short-term contracts (by 11.6%).

16

Cash remittances from overseas Filipinos coursed through banks reached USD21.4 billion for the full year 2012, posting an annual growth of 6.3% and exceeding the BSP’s full-year growth projection of 5%. In particular, remittances from both sea-based (USD4.8 billion) and land-based workers (USD16.6 billion) grew by 11.4% and 4.9% respectively. The resilience of overseas Filipino remittances continues to support the country’s economic growth and development. In 2012, cash remittances from overseas Filipinos coursed through banks represent about 6.5% of the country’s Gross National Income (GNI) and 8.5% of Gross Domestic Product (GDP). Remittances continue to draw strength from the increasing demand for a wider range of skilled Filipino workers abroad, mostly in the Middle East. In particular, preliminary reports by the POEA indicated that a total of 29,533 approved job orders for January and February 2013 were mostly for service, production, professional, technical and related workers to meet the manpower requirements in Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, and Taiwan.

Transactions and/or Dependence on Related Parties The Company has transactions with its subsidiaries and associates abroad, i.e., the

remittance centers that accept transactions from its customers, mostly OFWs, in Australia, Austria, Canada, Hong Kong, New Zealand, Singapore, the United Kingdom, and Japan. These transactions primarily consist of delivery services for a fee.

Pursuant to the Company’s usual course of business, it also advances funds to its

subsidiaries, associates and affiliates. These are accounts receivable from subsidiaries, associates and affiliates pertaining to remittance transactions. It also consists of advances made to subsidiaries, associates, and affiliates for working capital to maintain cash balances in bank accounts and other financial and operating requirements. The account receivables are usually settled on the next banking day. On the other hand, advances for financial and operating requirements are due on demand.

The Company leases office space from Oakridge Properties, a related party. The Company has office sharing arrangement with Surewell Equities Pte. Ltd. in

Singapore, a related party. The Company maintains peso deposit accounts with Sterling Bank of Asia, Inc. (A

Savings Bank), a related party. The Company’s retirement benefit fund is maintained with Sterling Bank of Asia, Inc. (A Savings Bank), an affiliate due to common stockholders, as trustee. The said bank’s majority shareholders are: JTKC Equities, Inc., Surewell Equities, Inc. and Star Equities Inc. which are also the shareholders of the Company. Please see also Item 12. Certain Relationships and Related Party Transactions.

Significant Agreements and/or Commitments The Company conducts its remittance and collection business internationally by

organizing wholly-owned corporations, entering into joint ventures, and signing Memoranda of Agreements (MOAs) with remittance or money transfer operators that are authorized or licensed in their respective countries and territories including Australia, Austria, Bahrain, Brunei, Canada, China, Germany, Greece, Hong Kong SAR, Indonesia, Ireland, Israel, Italy, Japan, Jordan, Lebanon, Malaysia, the Netherlands, New Zealand, Qatar, Spain, Taiwan, United Kingdom, and the United Arab Emirates.

The Memoranda of Agreement entered into with individuals and corporations in various

countries and territories follow a general format with minor variations. Generally, the MOAs entered into on or after 2004 provide that I-Remit retain exclusive proprietary rights over its I-Remit Foreign Remittance System which the foreign parties will use to implement the remittance arrangement. MOAs entered into on or before 2003 do not contain this provision. All MOAs, however, are aimed at limiting I-Remit’s exposure by specifying that: (i) the foreign parties are not agents but independent contractors; (ii) the foreign parties shall be shall be responsible for compliance with all applicable laws in

17

their respective countries and territories; and (iii) funds must first be deposited to an I-Remit bank account before the Company shall release the same to the intended beneficiaries in the Philippines. Contracts executed on or after 2004 also stipulate amicable settlement or arbitration as the mode of settlement of disputes and provides for the exclusive jurisdiction of the Philippine courts. New contracts with tie-ups require bond or advanced payment cover in order to fulfill the delivery of any transaction. The bond or “advanced payment cover” is deposited to an I-Remit-designated bank account that serves as collateral.

The bulk of the MOAs executed in the Philippines cover the arrangement between the

Company and various companies and institutions, such as commercial banks, thrift banks, and pawnshops for the appointment of the latter to provide pay-out stations through their branches for the Company’s notify-to-pay services.

Certain MOAs also involve the appointment of the Company as a collection agent for

the remittance of amortization payments, loan payments, premiums, and contributions for government financial institutions and agencies consisting of the Social Security System (SSS), Overseas Workers Welfare Administration (OWWA), Home Development Mutual Fund (HDMF or Pag-IBIG Fund), Philippine Retirement Authority (PRA) and the Philippine Health Insurance Corporation (PhilHealth), and various pre-need and real estate development companies.

Principal Terms and Expiration Dates of All Patents, Trademarks, Copyrights, Licenses, Concessions, and Royalty Agreements Held

I-Remit, Inc. is duly registered as a Remittance Agent with the Bangko Sentral ng

Pilipinas (BSP), with Certificate No. FX-2005-000364 issued on May 10, 2005, pursuant to BSP Circular 471, Series of 2005, dated January 24, 2005. It is subject to the applicable provisions of laws and BSP rules and regulations, as well as the provisions of the Anti-Money Laundering Act of 2001 (Republic Act No. 9160 as amended by Republic Acts 9194, 10167, and 10365) and its revised implementing rules and regulations, and Republic Act No. 10168 or the Terrorism Financing Prevention and Suppression Act of 2012 and its implementing rules and regulations.

I-Remit, Inc. is duly registered with the Australian Transaction Reports and Analysis Centre (AUSTRAC) as a Remittance Network Provider, with registered remittance network provider number RNP100035640-001, pursuant to subsection 75C(2) of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) of Australia with effect from April 13, 2012 and valid for three (3) years thereafter. The Company’s subsidiaries and affiliates, and their branches are registered with or licensed by the relevant government regulatory bodies in their host countries in Australia, Austria, Canada, Hong Kong SAR, Italy, Japan, New Zealand, Singapore, Taiwan, and the United Kingdom. The said licenses and registrations have been granted subject to compliance with the applicable laws governing the operation of remittance companies or money transfer businesses and anti-money laundering and counter-terrorism financing. I-Remit Australia Pty Ltd is registered with the Australian Securities and Investments Commission (ASIC) as an Australian proprietary company, limited by shares with ACN 103 107 982 and ABN 22 103 107 982 with registration date December 10, 2002 and next review date December 10, 2013. Pursuant to subsection 75C(2) of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) of Australia, I-Remit Australia Pty Ltd is registered with AUSTRAC as an affiliate of I-Remit, Inc., with remittance affiliate number AFF100314117-001, with effect from October 22, 2012 and valid for three (3) years thereafter. Worldwide Exchange Pty Ltd is registered with the Australian Securities and Investments Commission (ASIC) as an Australian proprietary company, limited by shares with ACN 106 493 047 and ABN 35 106 493 047 with registration date September 29, 2003 and next review date September 29, 2013. Pursuant to subsection 75C(2) of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act) of Australia, Worldwide Exchange Pty Ltd is registered with AUSTRAC as an affiliate of I-Remit, Inc., with remittance affiliate number AFF100309950-001, with effect from September 28, 2012 and valid for three (3) years thereafter.

18

International Remittance (Canada) Ltd. is registered with Industry Canada, with registration number 392271-5, pursuant to the Canada Business Corporations Act with date of incorporation July 16, 2001. International Remittance (Canada) Ltd. is registered as an extraprovincial company with the Registrar of Companies of the Province of British Columbia with certificate of registration number A-60718 dated December 3, 2003. Pursuant to the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, International Remittance (Canada) Ltd. is registered as a money services business (MSB) with the Financial Transactions and Reports Analysis Centre of Canada with registration number M081607706 valid until June 28, 2014. Lucky Star Management Limited (trading as “IRemit Hong Kong”) is registered as a limited liability company in the Companies Registry of Hong Kong pursuant to the Companies Ordinance (Cap 32). Lucky Star Management Limited (trading as “IRemit Hong Kong”) is a licensed money service operator pursuant to Section 30 of the Anti-Money Laundering and Counter-Terrorist Financing (Financial Institutions) Ordinance (Cap 615) with License No. 12-07-00326 from July 9, 2012 to August 8, 2014. K.K. I-Remit Japan is registered as a “Kabushiki Kaisha” (joint stock corporation) with the Legal Affairs Bureau of the Ministry of Justice of Japan with company number 0100-01-140611. Pursuant to the Payment Services Act of 2010, K.K. I-Remit Japan is registered with the Kanto Local Finance Bureau with Registration No. KLFB00019. K.K. I-Remit Japan is a member of the Japan Payment Services Association, a dispute resolution body, with membership number 00390. I-Remit New Zealand Limited is registered with the Registrar of Companies of the Ministry of Economic Development with certificate number 1984331 effective September 11, 2007. I-Remit New Zealand Limited is registered in the Financial Service Providers Register of the Companies House of New Zealand with FSP number 45263. I-Remit New Zealand Limited is a participant to the Financial Services Complaints Limited, a dispute resolution organization. IRemit Singapore Pte Ltd is registered in the Registry of Companies and Businesses of the Accounting and Corporate Regulatory Authority with company registration number 200103087H. IRemit Singapore Pte Ltd is licensed by the Monetary Authority of Singapore to carry on the remittance business pursuant to Section 8(3) of the Money-changing and Remittance Businesses Act (Cap 187) with RA No. 01132 valid until December 31, 2013 and renewable every year. IRemit Global Remittance Limited is registered with the Companies House of the United Kingdom with company number 04239974 pursuant to the Companies Act 2006. IRemit Global Remittance Limited has been granted authorization by the Financial Conduct Authority (FCA) to carry on payment services (money remittance) with Firm Reference Number 537568 effective April 15, 2011 pursuant to the Payment Services Regulations 2009. IRemit Global Remittance Limited is registered with Her Majesty’s Customs and Excise with money laundering registration number 1213085 with certificate of registration issued on May 22, 2012 and expiring on June 1, 2013 subject to renewal. The branches of IRemit Global Remittance Limited in Rome and Milan, Italy are registered in Albo of art. 114 septies TUB (Albo degli Istituti di Pagamento) under supervision of Banca D’Italia with identification code 36023.0. pursuant to Art. 1 Paragraph 1(b) of Legislative Decree 11/2010 of Italy with effect from July 7, 2011. IREMIT Remittance Consulting GmbH is registered as an agent of IRemit Global Remittance Limited pursuant to Article 12 para. 6 of the Austrian Payment Services Act (Zahlungsdienstegesetz). IREMIT Remittance Consulting GmbH is registered in the Register of Payment Institutions of the Financial Conduct Authority of the United Kingdom with firm reference number 574797. Hwa Kung Hong & Co. Ltd. is registered with the Department of Foreign Exchange, the Central Bank of China with Issued Document No. Taipei Central No. 0980000061.

I-Remit, Inc. and its subsidiaries, associates, and affiliates offer their products and services through the “I-Remit” trademark, salesmark, and/or trade name.

19

I-Remit has registered the following patents, trademarks and/or trade names: Name/Trademark Date Filed Date Registered I-Remit Name and Logo January 20, 2004

Application No. 4-2004-0000529

December 11, 2006 Registration No. 4-2004-000529 Registered for a term of 10 years from date of registration

I-Load June 16, 2004 Application No. 4-2004-0005251

January 21, 2006 Registration No. 4-2004-0005251 Registered for a term of 10 years from date of registration

I-Travel June 16, 2004 Application No. 4-2004-0005252

October 1, 2005 Registration No. 4-2004-0005252 Registered for a term of 10 years from date of registration

I-Pay June 16, 2004 Application No. 4-2004-0005253

October 1, 2005 Registration No. 4-2004-0005253 Registered for a term of 10 years from date of registration

iDol July 8, 2004 Application No. 4-2004-0006066

July 30, 2006 Registration No. 4-2004-006066 Registered for a term of 10 years from date of registration

I-Serve February 14, 2008 Application No. 4-2008-001818

December 15, 2008 Registration No. 4-2008-001818 Registered for a term of 10 years from date of registration

I-Value February 14, 2008 Application No. 4-2008-001819

September 8, 2008 Registration No. 4-2008-001819 Registered for a term of 10 years from date of registration

I-Reward February 14, 2008 Application No. 4-2008-001816

December 1, 2008 Registration No. 4-2008-001819 Registered for a term of 10 years from date of registration

I-Care February 14, 2008 Application No. 4-2008-001817

September 8, 2008 Registration No. 4-2008-001819 Registered for a term of 10 years from date of registration

I-Remit Trademark

June 23, 2006 e-Filing No. 125586

June 23, 2006 Trademark No. T06/12356G Registry of Trademarks, Property Office of Singapore

I-Remit Trademark

November 1, 2007 New Zealand Trademark Registration No. 778760 Registered for a term of 10 years from date of registration

I-Remit Trademark

September 18, 2009 Application No. 145s2333

Registration pending; for publication in Trademarks Journal (Canada)

20

I-Remit has licenses to the following information technology software and systems used

in its operations: Software / System,

Version Purpose Acquisition and

Effectivity License / Renewal of Maintenance Service

Enterprise Resource Information and Control (ERIC) Financial Suite (General Ledger & Accounts Payable) Version 5.2, Jupiter Systems, Inc.

The General Ledger module serves as the central financial data repository that allows for convenient and accurate preparation of the Company’s financial statements. The Accounts Payable module manages supplier payables and disbursements.

Version 3.2 acquired in 2002; upgraded to version 5.2 in 2006; perpetual license

Support agreement is renewed every year

Enterprise Resource Information and Control (ERIC) Payroll, Human Resource Management, Timecard, Version 5.2, Jupiter Systems, Inc.

The Payroll module is used for employees’ pay computation, payroll processing, and statutory reporting. The Human Resource Management module is used for capturing 201-file information and record-keeping. The Timecard module is used in recording and processing employee working hours.

Acquired in 2007; perpetual license

Support agreement is renewed every year

Microsoft SQL Server 2000 (Standard Edition), Microsoft Corporation

A relational data base management system used for the “back-end” data base of I-Remit’s remittance system

Version 2000, acquired on October 31, 2005; Version 2008, acquired on February 27, 2009; perpetual license

Software assurance ended on February 28, 2011

Microsoft SQL Server – Enterprise Edition

A relational data base management system used for the “back-end” data base of I-Remit’s remittance system

Version 2008, acquired on February 27, 2009; perpetual license

Software assurance ended on February 28, 2011

Microsoft Exchange Server, 2003 and 2007 – Enterprise Edition

A messaging and collaborative software used for the electronic mail system of I-Remit, Inc.

Version 2003, acquired on August 11, 2006; additional licenses acquired on September 27, 2007; perpetual license

Internet Service Accelerator 2004

Used as an internal firewall Acquired on August 11, 2006

Microsoft Office – Small Business

Software used in creating documents, files and reports

Version 2003, acquired on October 31, 2005; version 2007, acquired on November 20, 2008; perpetual license

21

Software / System,

Version Purpose Acquisition and

Effectivity License / Renewal of Maintenance Service

Microsoft Windows Server – Enterprise and Standard Edition

Operating system used in servers