Embed Size (px)

Citation preview

Partnership & SA Experience in the Development of BPO Sector

Mfanu Mfayela, BPeSA CEOGeneva, April 2007

Section I‘Background to Sector Development’

Business Process enabling SA

• National industry association representing the interests that aims to provide a national coordinated service & address key challenges incl. policy advocacy, etc.

– Aim to develop & grow industry to become a significant contributor to GDP, through attracting foreign direct investment & creating sustainable job creation.

– Aim to strengthen & improve sector, ensure and promote SA as a destination of choice investors.

Realising Opportunity

• BPeSA formed strategic partnership with dti and Business Trust designed to realise its objectives

– Has taken a non-traditional, development role as industry is being born

• Urgent focus on getting Government support to enable this development

• Need to achieve partnership with Government at national level, similar to successes already achieved at regional level

MOU with Regions

• Acknowledges value generated by BPeSA and its role as the national negotiator at Government and Private Sector level including Provinces and Local Municipalities through the regions

• Acknowledges BPeSA’s focus areas and its role in marketing, talent development, transformation, SME development, quality standards, knowledge base development, funding and BPeSA’s need to attract members of its own

• Positions BPeSA appropriately to negotiate with national Government on behalf of the industry as a whole.

Development Focus

Working with Government and Business

- 5 work streams underway:

1. Strategic Marketing

2. Institutional Development

3. Talent Development

4. Quality Assurance

5. Incentives

Requirements for Success of Workstreams

• BPeSA’s development initiatives on behalf of the industry will not achieve success unless all five workstreams are successful

• The industry can achieve some aspects alone but talent development, marketing and incentives require close partnership with Government at national level

• BPeSA needs to be given the kind of membership support that will position it appropriately for this powerful partnership

Section II‘South Africa – Alive with

Possibilities’

• A sophisticated and promising emerging market, providing an entrepreneurial and dynamic investment environment

• Rapidly becoming a premier alternative BPO destination

– Lower costs than near shore countries

– Better quality and value than traditional offshore destinations

• A well educated and functionally literate workforce, with world class tertiary education and internationally recognised professional bodies

• A western business culture combined with multi-lingual communities

Many players have already seized on SA’s outstanding

potential

Already in place

• World class captive and outsourced operations

• Across a diverse range of industries

• Sourcing both local and international firms

SA – alive with possibilities

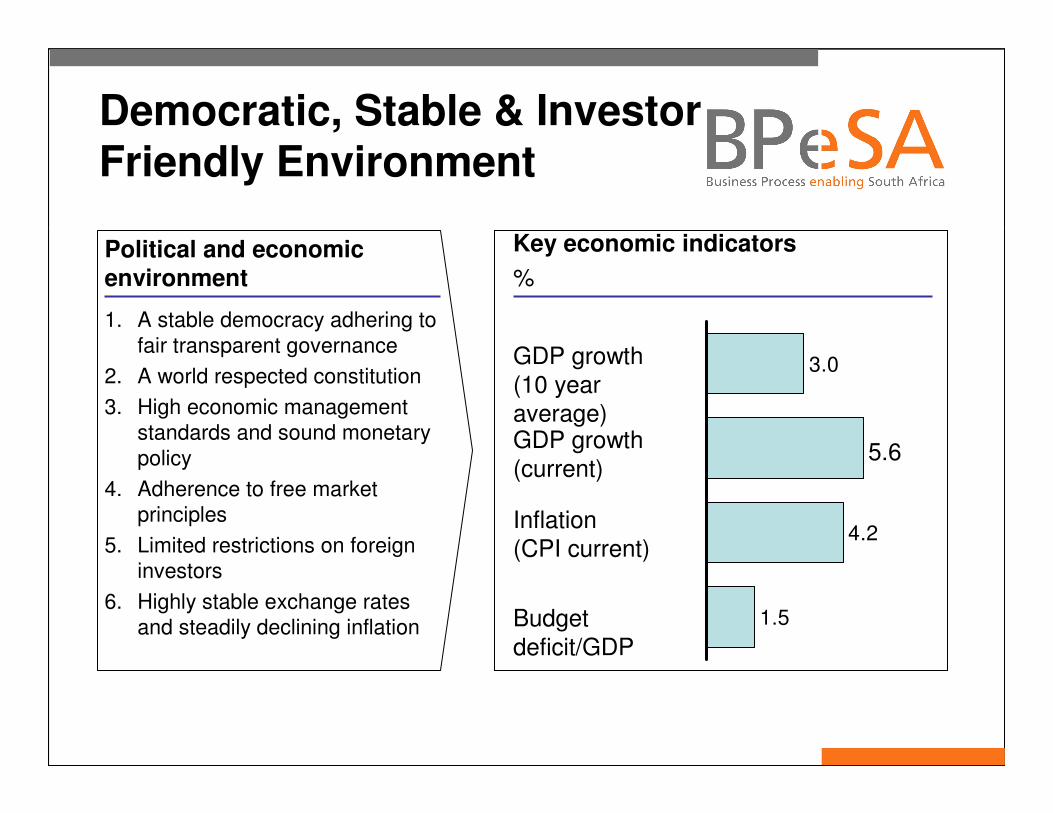

1.5

4.2

3.0

Democratic, Stable & Investor Friendly Environment

Political and economic environment

1. A stable democracy adhering to fair transparent governance

2. A world respected constitution

3. High economic management standards and sound monetary policy

4. Adherence to free market principles

5. Limited restrictions on foreign investors

6. Highly stable exchange rates and steadily declining inflation

Key economic indicators

%

GDP growth (10 year average)GDP growth (current)

Budget deficit/GDP

Inflation (CPI current)

5.6

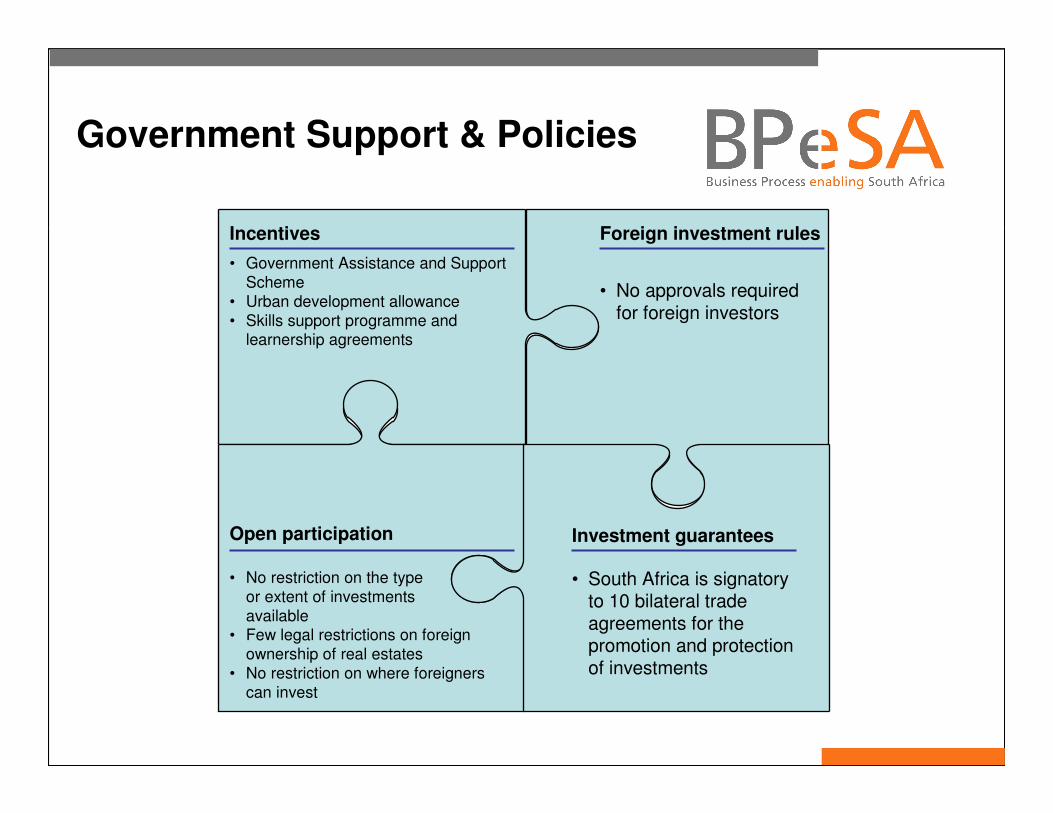

Government Support & Policies

Incentives

• Government Assistance and Support Scheme

• Urban development allowance• Skills support programme and

learnership agreements

Foreign investment rules

• No approvals required for foreign investors

Open participation

• No restriction on the type or extent of investments available

• Few legal restrictions on foreign ownership of real estates

• No restriction on where foreigners can invest

Investment guarantees

• South Africa is signatory to 10 bilateral trade agreements for the promotion and protection of investments

An Attractive Quality Lifestyle

Attractive lifestyle features

• Sophisticated cosmopolitan cities (e.g., Johannesburg, Port Elizabeth, Durban & Cape Town)

• Excellent living standards and medical services

• English widely spoken

• International schools

• Diverse and abundant natural splendour and year-round temperate climate

• No restrictions on foreign ownership of residential properties

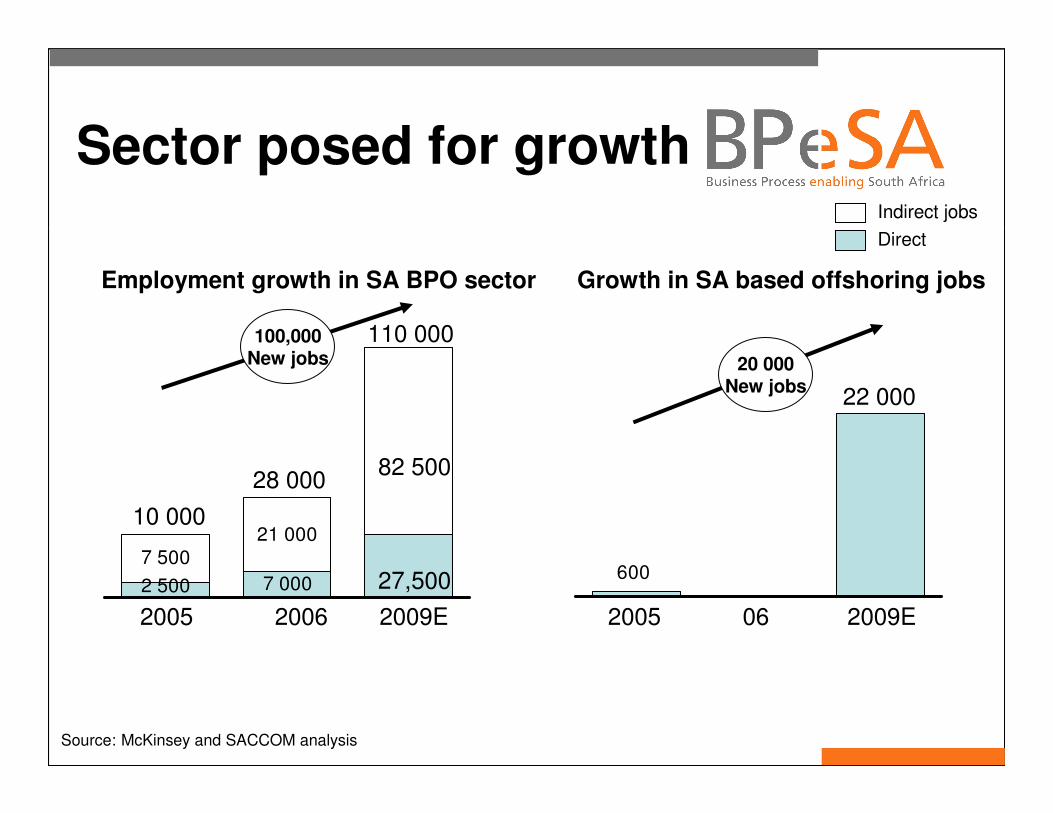

Sector posed for growthIndirect jobs

Direct

Employment growth in SA BPO sector

2 500 7 000

7 50021 000

27,500

82 500

100,000New jobs

110 000

28 000

10 000

2005 2006 2009E

Source: McKinsey and SACCOM analysis

Growth in SA based offshoring jobs

600

22 000

2005 06 2009E

20 000New jobs

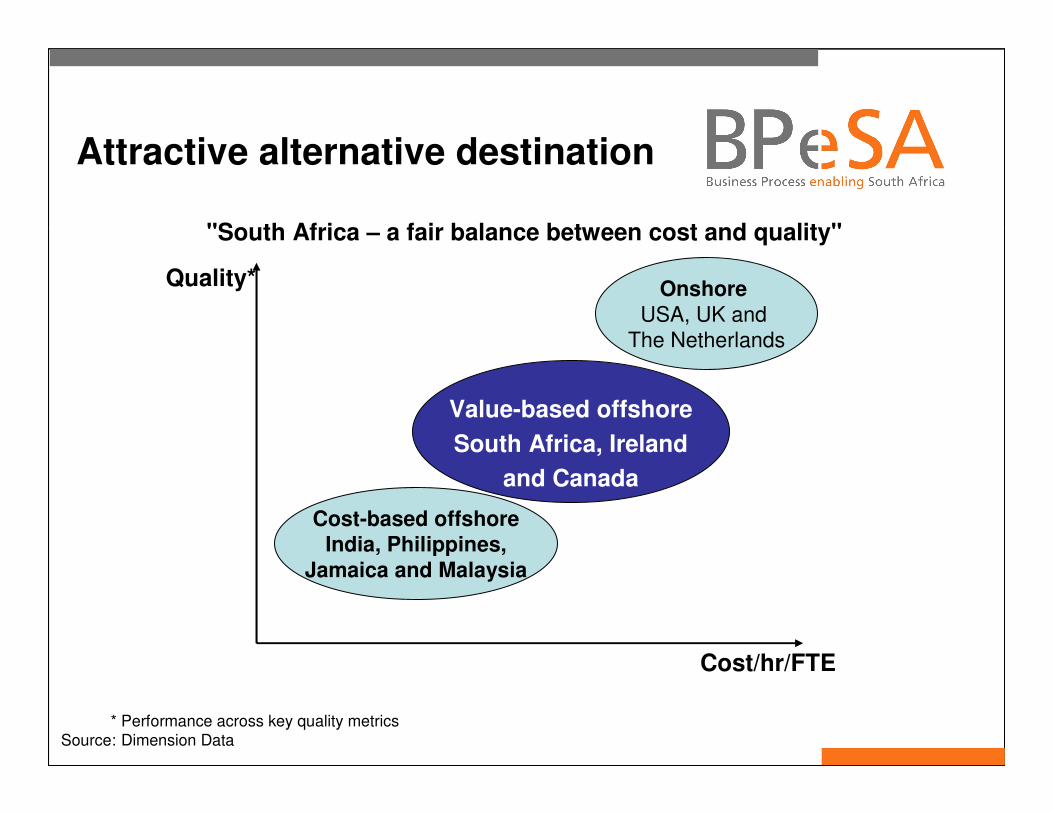

Attractive alternative destination

Quality*

Cost/hr/FTE

Onshore

USA, UK and The Netherlands

Value-based offshore

South Africa, Ireland

and Canada

Cost-based offshore India, Philippines,

Jamaica and Malaysia

"South Africa – a fair balance between cost and quality"

* Performance across key quality metricsSource: Dimension Data

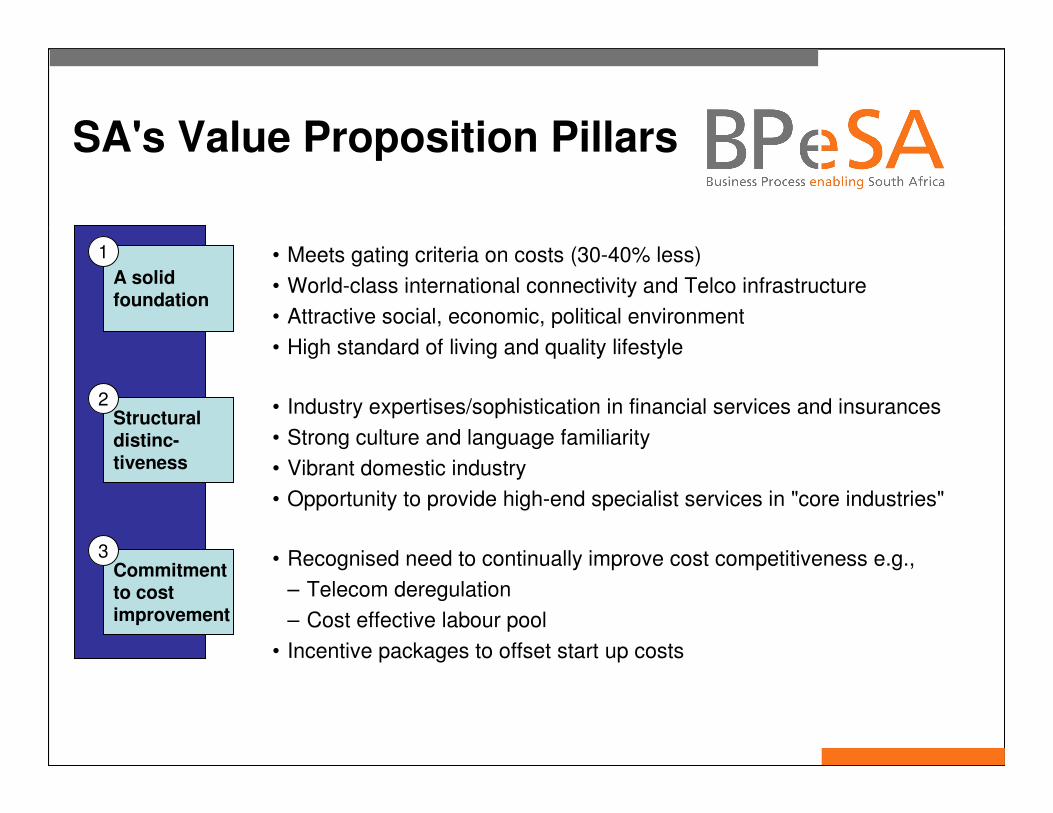

SA's Value Proposition Pillars

A solid foundation

1 • Meets gating criteria on costs (30-40% less)

• World-class international connectivity and Telco infrastructure

• Attractive social, economic, political environment

• High standard of living and quality lifestyle

Structural distinc-tiveness

2 • Industry expertises/sophistication in financial services and insurances

• Strong culture and language familiarity

• Vibrant domestic industry

• Opportunity to provide high-end specialist services in "core industries"

Commitment to cost improvement

3 • Recognised need to continually improve cost competitiveness e.g.,

– Telecom deregulation

– Cost effective labour pool

• Incentive packages to offset start up costs

Section III‘The South Africa BPO Sector’

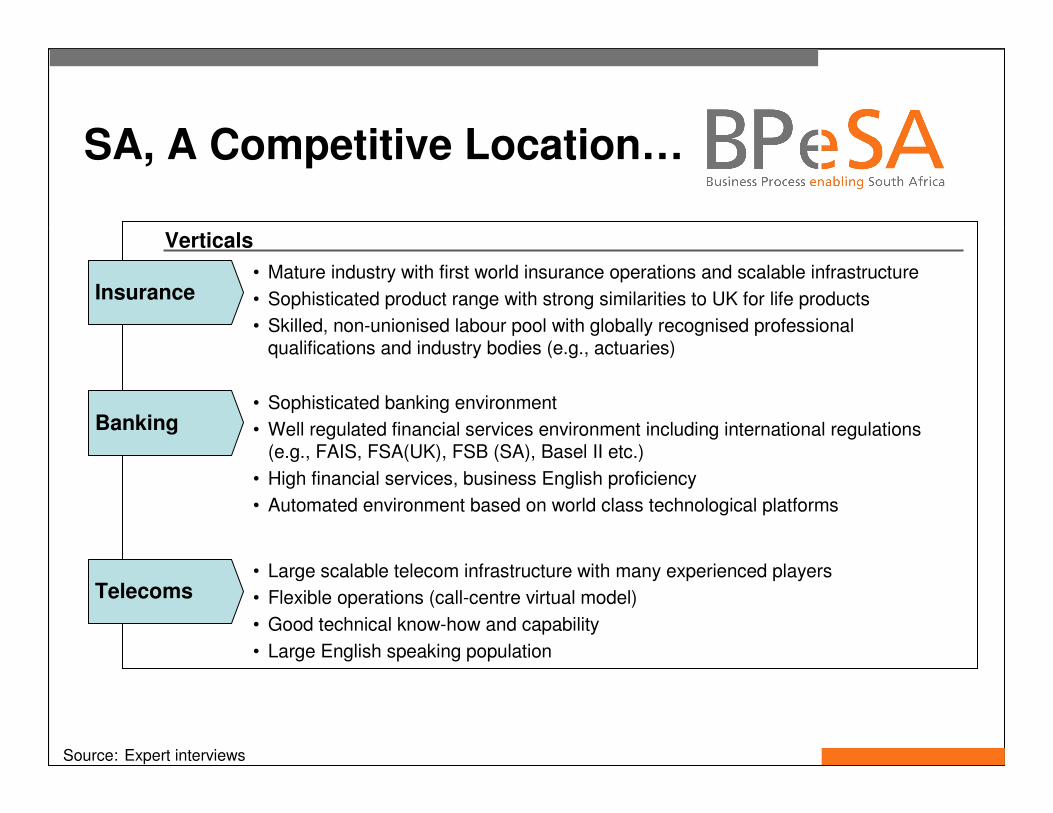

SA, A Competitive Location…

Verticals

• Mature industry with first world insurance operations and scalable infrastructure

• Sophisticated product range with strong similarities to UK for life products

• Skilled, non-unionised labour pool with globally recognised professional qualifications and industry bodies (e.g., actuaries)

Insurance

Banking• Sophisticated banking environment

• Well regulated financial services environment including international regulations (e.g., FAIS, FSA(UK), FSB (SA), Basel II etc.)

• High financial services, business English proficiency

• Automated environment based on world class technological platforms

Telecoms• Large scalable telecom infrastructure with many experienced players

• Flexible operations (call-centre virtual model)

• Good technical know-how and capability

• Large English speaking population

Source: Expert interviews

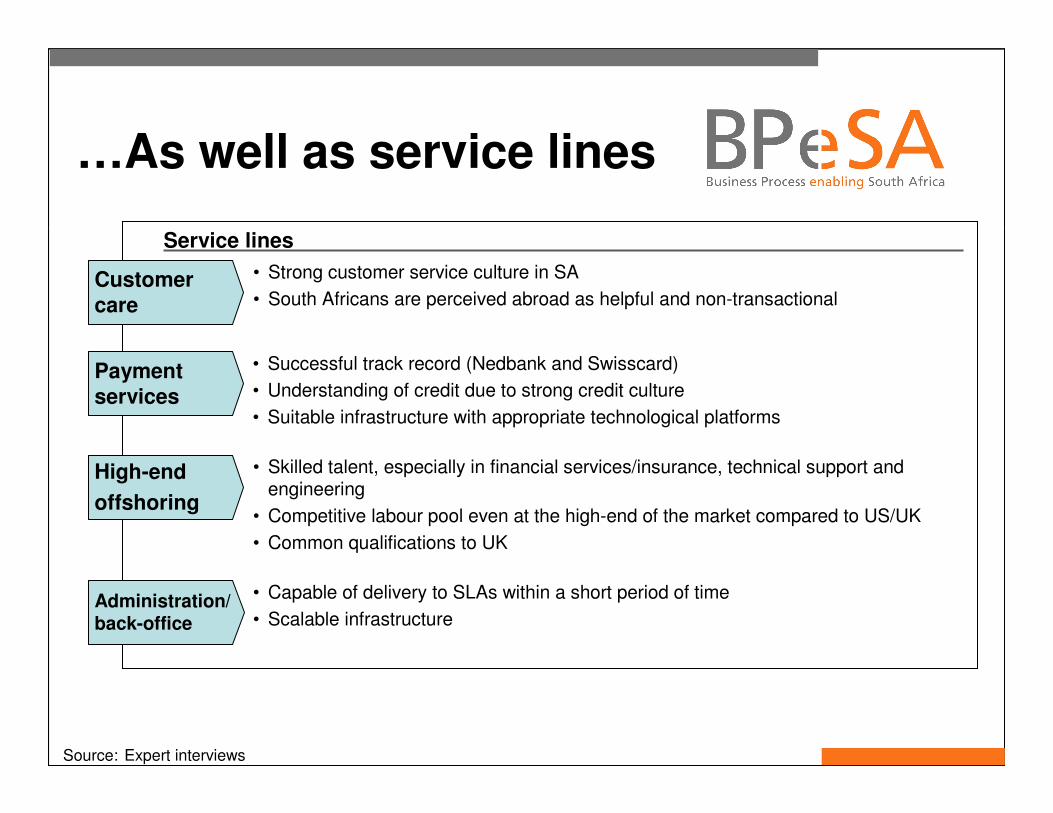

…As well as service lines

Service lines

• Strong customer service culture in SA

• South Africans are perceived abroad as helpful and non-transactionalCustomer care

Payment services

• Successful track record (Nedbank and Swisscard)

• Understanding of credit due to strong credit culture

• Suitable infrastructure with appropriate technological platforms

High-end

offshoring

• Skilled talent, especially in financial services/insurance, technical support and engineering

• Competitive labour pool even at the high-end of the market compared to US/UK

• Common qualifications to UK

Source: Expert interviews

Administration/back-office

• Capable of delivery to SLAs within a short period of time

• Scalable infrastructure

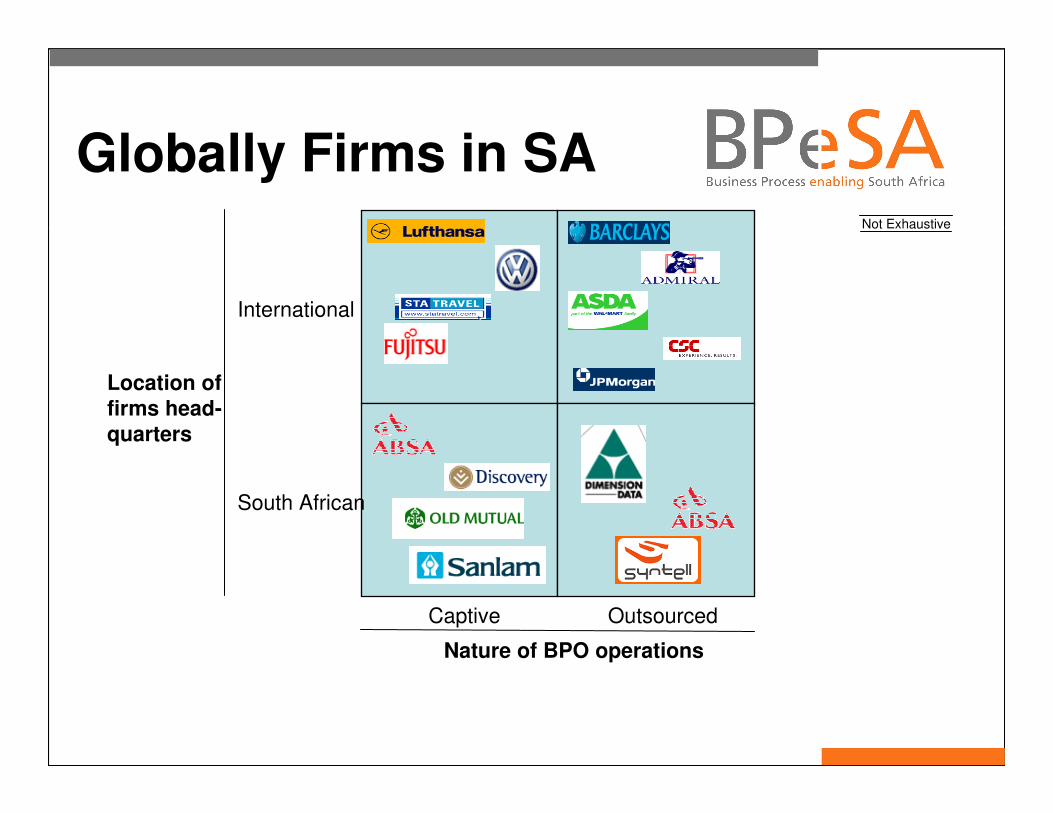

Globally Firms in SA

International

South African

Location of firms head-

quarters

Captive Outsourced

Nature of BPO operations

Not Exhaustive

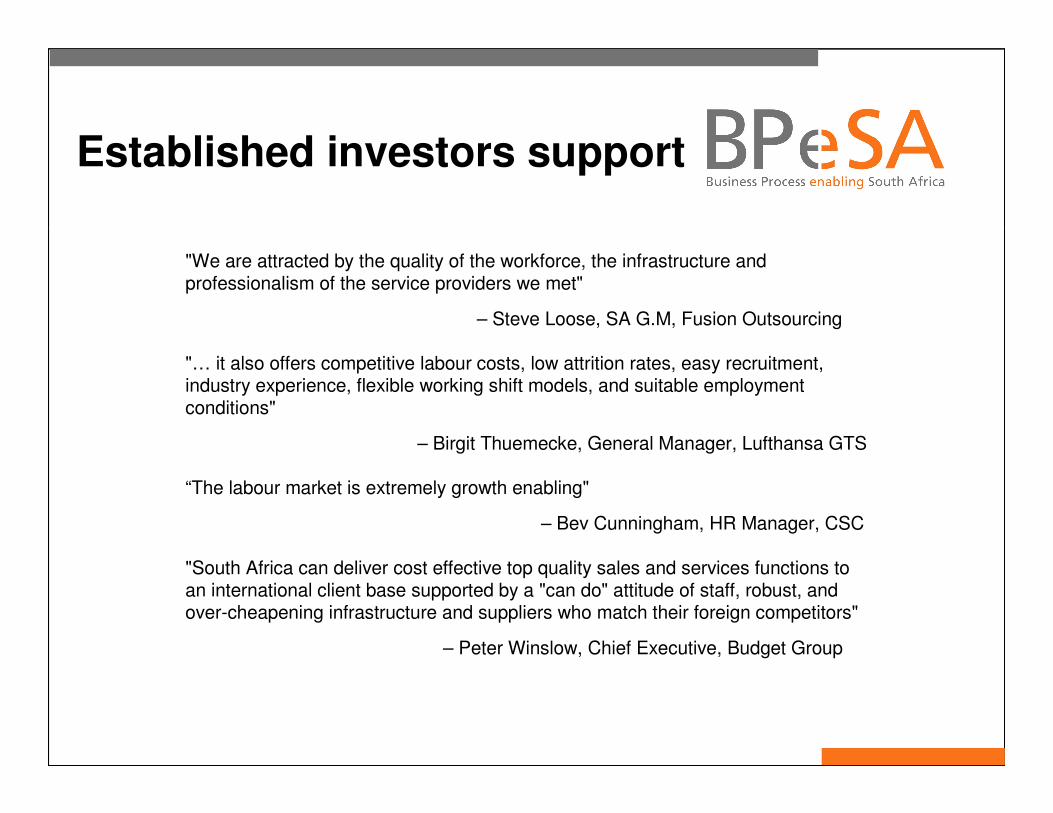

Established investors support

"We are attracted by the quality of the workforce, the infrastructure and professionalism of the service providers we met"

– Steve Loose, SA G.M, Fusion Outsourcing

"… it also offers competitive labour costs, low attrition rates, easy recruitment, industry experience, flexible working shift models, and suitable employment conditions"

– Birgit Thuemecke, General Manager, Lufthansa GTS

“The labour market is extremely growth enabling"

– Bev Cunningham, HR Manager, CSC

"South Africa can deliver cost effective top quality sales and services functions to an international client base supported by a "can do" attitude of staff, robust, and over-cheapening infrastructure and suppliers who match their foreign competitors"

– Peter Winslow, Chief Executive, Budget Group

Section IV “Case studies, challenges,

and learnings"

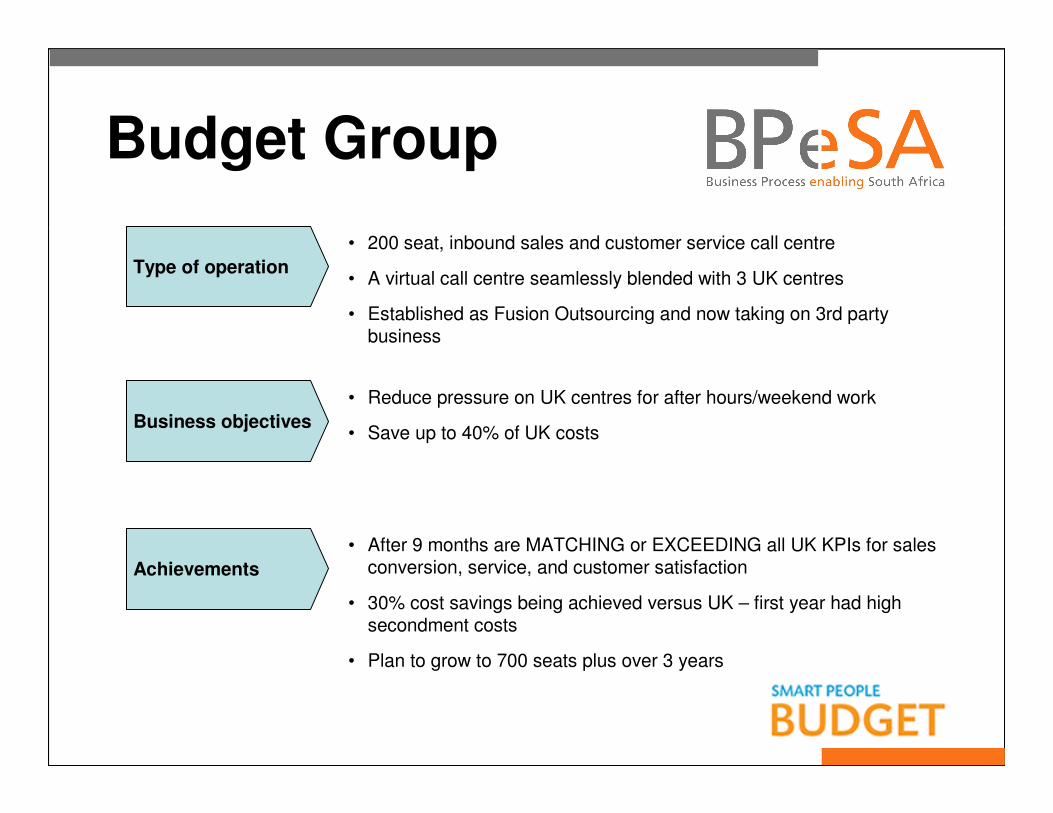

Budget Group

• 200 seat, inbound sales and customer service call centre

• A virtual call centre seamlessly blended with 3 UK centres

• Established as Fusion Outsourcing and now taking on 3rd party business

• After 9 months are MATCHING or EXCEEDING all UK KPIs for sales conversion, service, and customer satisfaction

• 30% cost savings being achieved versus UK – first year had high secondment costs

• Plan to grow to 700 seats plus over 3 years

• Reduce pressure on UK centres for after hours/weekend work

• Save up to 40% of UK costs

Type of operation

Business objectives

Achievements

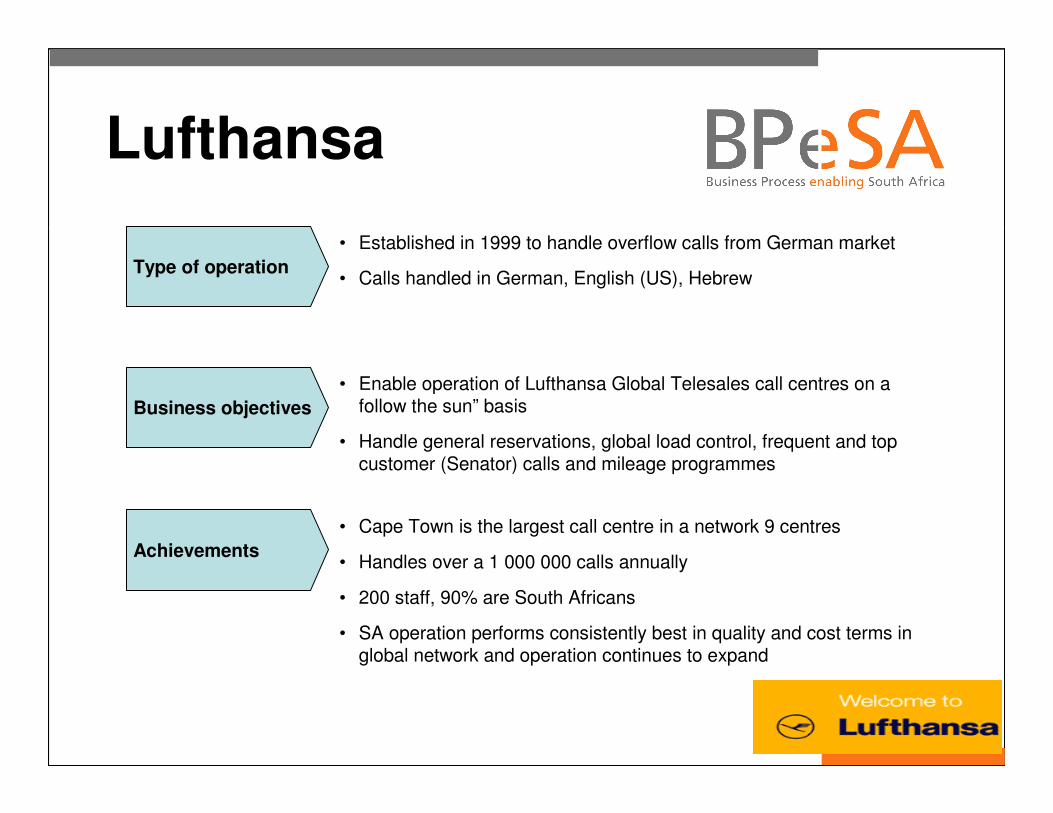

Lufthansa

• Established in 1999 to handle overflow calls from German market

• Calls handled in German, English (US), Hebrew

• Enable operation of Lufthansa Global Telesales call centres on afollow the sun” basis

• Handle general reservations, global load control, frequent and top customer (Senator) calls and mileage programmes

• Cape Town is the largest call centre in a network 9 centres

• Handles over a 1 000 000 calls annually

• 200 staff, 90% are South Africans

• SA operation performs consistently best in quality and cost terms in global network and operation continues to expand

Type of operation

Business objectives

Achievements

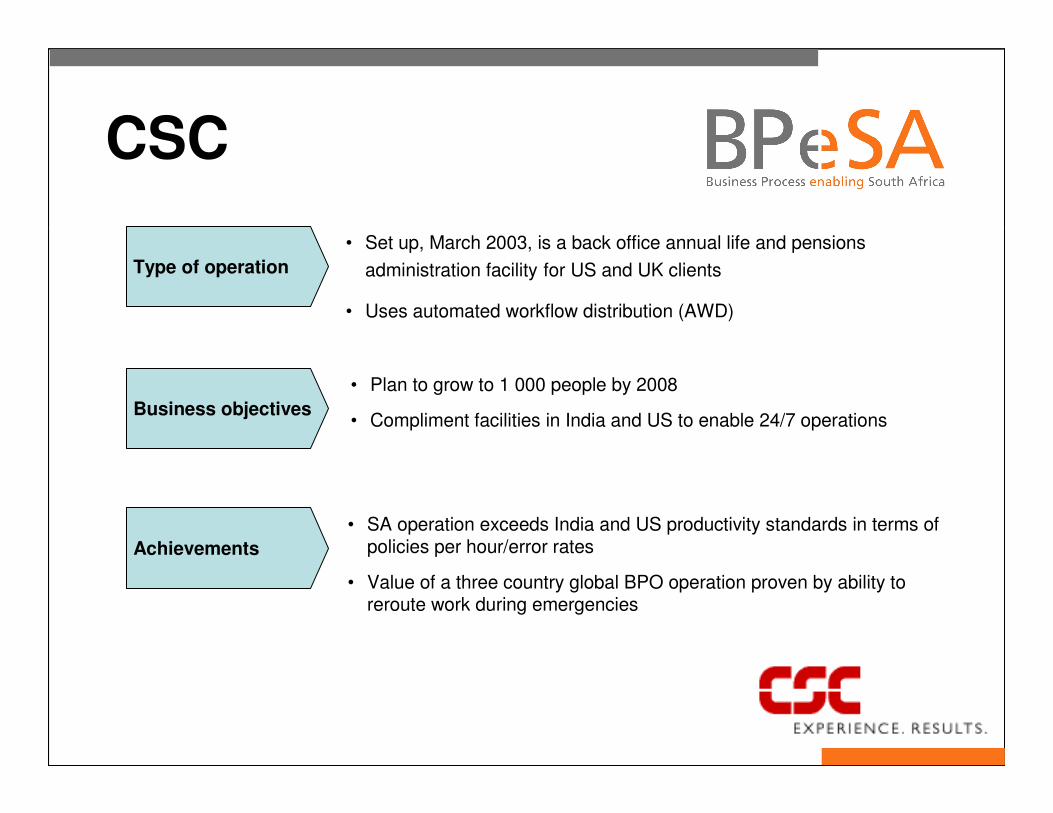

CSC

• Set up, March 2003, is a back office annual life and pensions

administration facility for US and UK clients

• Uses automated workflow distribution (AWD)

• Plan to grow to 1 000 people by 2008

• Compliment facilities in India and US to enable 24/7 operations

• SA operation exceeds India and US productivity standards in terms of policies per hour/error rates

• Value of a three country global BPO operation proven by ability to reroute work during emergencies

Type of operation

Business objectives

Achievements

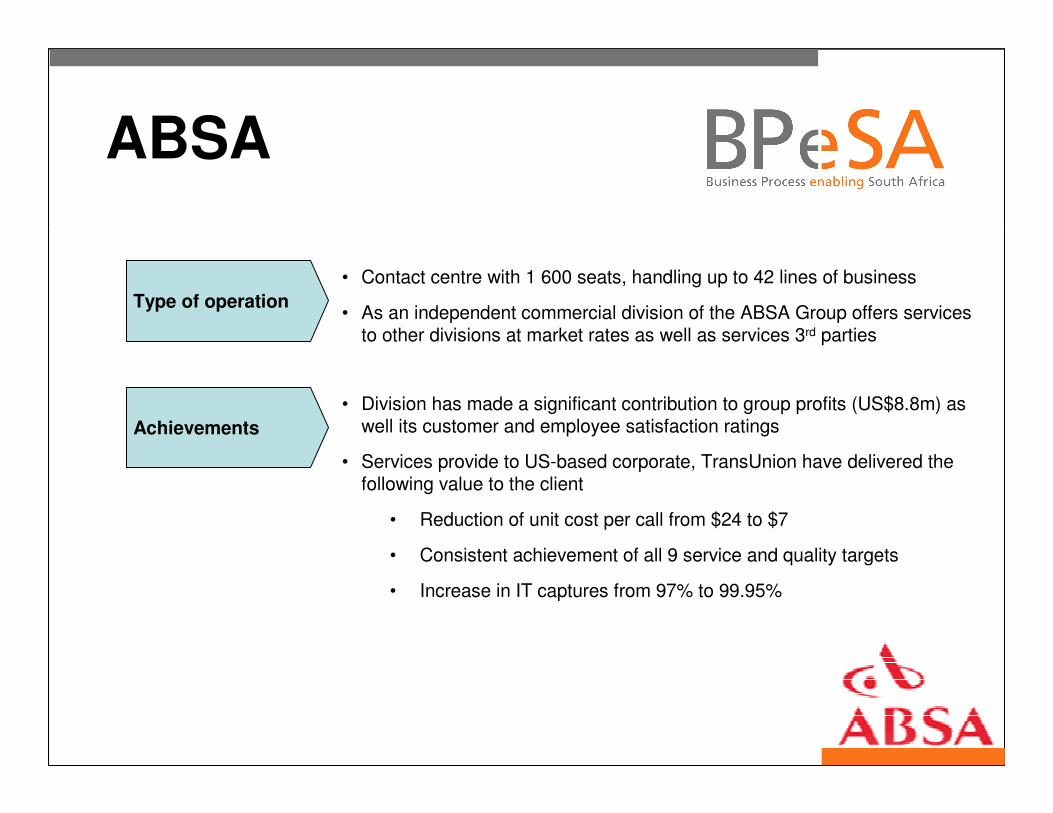

ABSA

• Contact centre with 1 600 seats, handling up to 42 lines of business

• As an independent commercial division of the ABSA Group offers services to other divisions at market rates as well as services 3rd parties

• Division has made a significant contribution to group profits (US$8.8m) as well its customer and employee satisfaction ratings

• Services provide to US-based corporate, TransUnion have delivered the following value to the client

• Reduction of unit cost per call from $24 to $7

• Consistent achievement of all 9 service and quality targets

• Increase in IT captures from 97% to 99.95%

Type of operation

Achievements

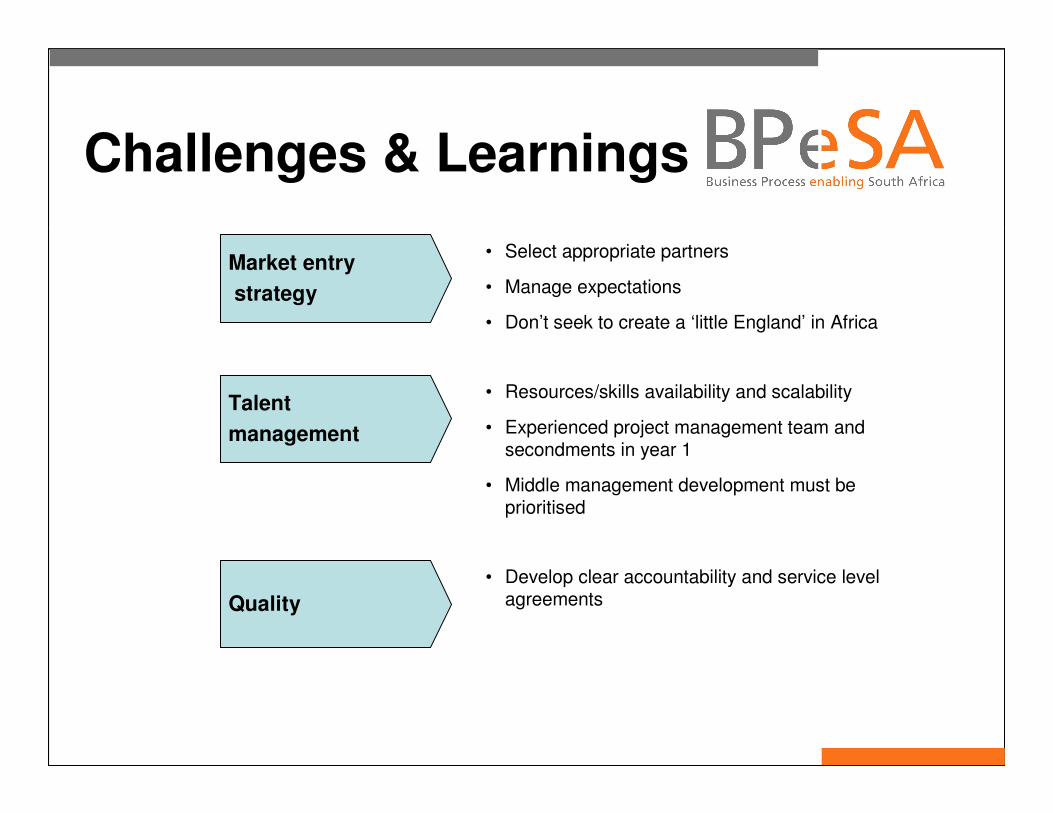

Challenges & Learnings

• Select appropriate partners

• Manage expectations

• Don’t seek to create a ‘little England’ in Africa

• Resources/skills availability and scalability

• Experienced project management team and secondments in year 1

• Middle management development must be prioritised

• Develop clear accountability and service level agreements

Market entry

strategy

Talent

management

Quality