Embed Size (px)

Citation preview

1

Pass-Through EntitiesPass-Through Entities

Federation of Tax AdministratorsFederation of Tax Administrators2005 Annual Meeting2005 Annual Meeting

San Antonio, TexasSan Antonio, TexasJune 13, 2005June 13, 2005

The Audit ofThe Audit ofPass-Through EntitiesPass-Through Entities

Nonie ManionNonie ManionDirector of Tax AuditsDirector of Tax Audits

New York State Department ofTaxation and FinanceNew York State Department ofNew York State Department ofTaxation and FinanceTaxation and Finance

New York State Capitol BuildingAlbany, New York

2

Audit EvolutionAudit Evolution

Prior to current technology audit selectionPrior to current technology audit selectionconsisted of physically pulling and reviewingconsisted of physically pulling and reviewingreturns.returns.

As the program evolved specific issues wereAs the program evolved specific issues wereidentified enabling Audit to adjust the auditidentified enabling Audit to adjust the auditselection criteria.selection criteria.

Due to new technology and better dataDue to new technology and better dataidentifying non-compliant returns is easier.identifying non-compliant returns is easier.

Data WarehouseData Warehouse

State DataState Data

Federal DataFederal Data

Third Party DataThird Party Data

Query ToolsQuery Tools

3

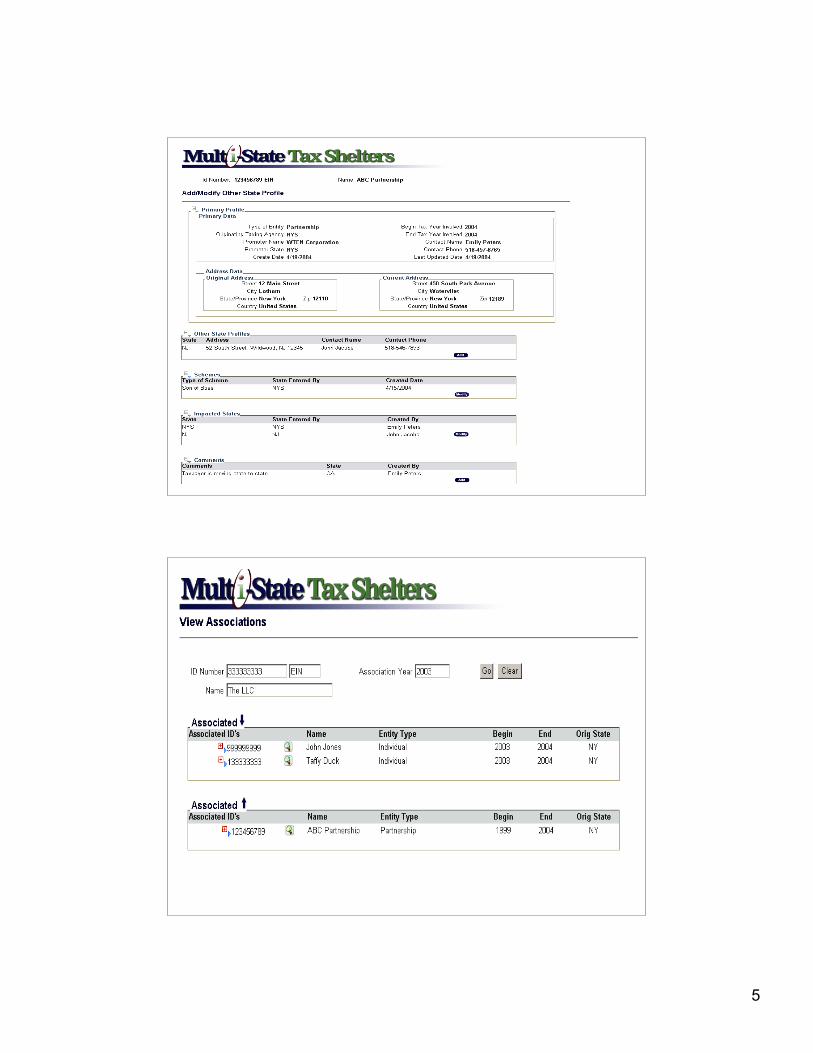

ACMS ScreeningACMS ScreeningApplicationApplication

Taxpayer ProfileTaxpayer Profile

Audit HistoryAudit History

Assessment HistoryAssessment History

Filing HistoryFiling History

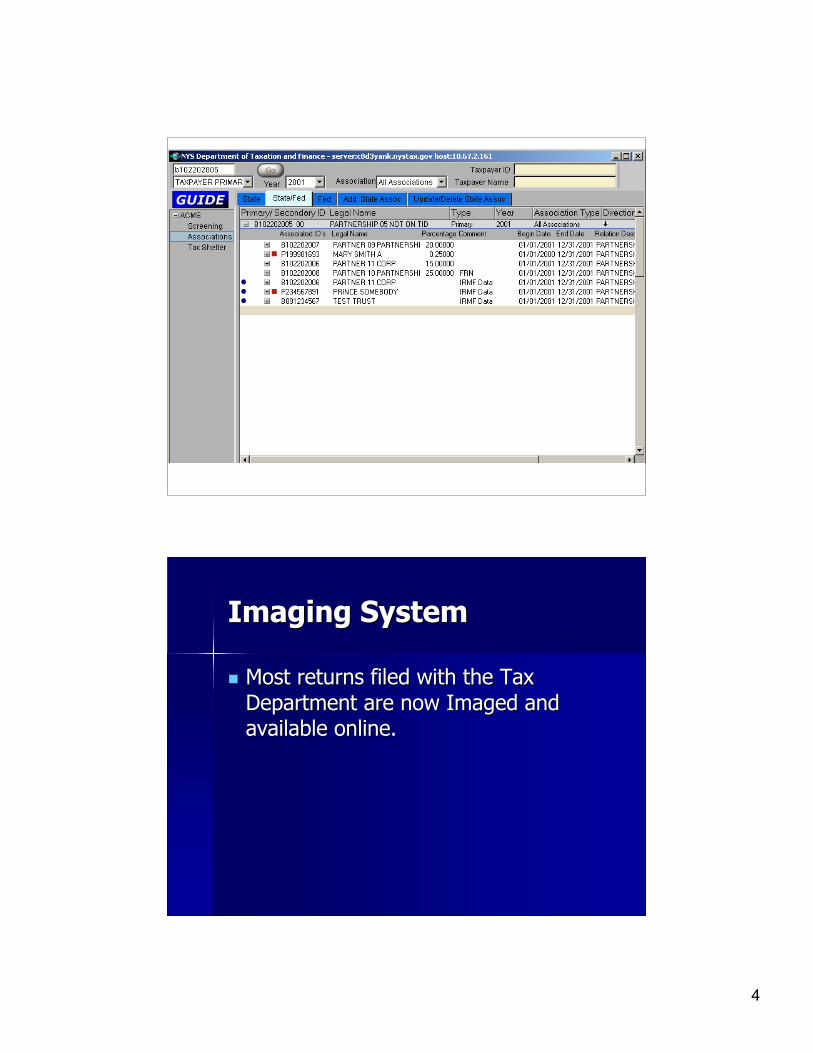

ACMS AssociationACMS AssociationApplicationApplication Illustrates the relationships between entitiesIllustrates the relationships between entities

and their owners.and their owners.

Identifies the responsible parties whoIdentifies the responsible parties whoshould be reporting the income from theseshould be reporting the income from theseflow through entities.flow through entities.

Includes state and federal associationIncludes state and federal associationinformation.information.

4

Imaging SystemImaging System

Most returns filed with the TaxMost returns filed with the TaxDepartment are now Imaged andDepartment are now Imaged andavailable online.available online.

5

6

Multi-State Pass-ThroughMulti-State Pass-ThroughEntity Database (MSPD)Entity Database (MSPD)

Modeled after the MSTS and ACMSModeled after the MSTS and ACMSAssociation applications.Association applications.

Allow states to share data relating toAllow states to share data relating toflow through entities.flow through entities.

Chainbridge, Inc.Chainbridge, Inc.

Use of IRC Section 482to Combat

Corporate Tax Shelters

Eric CookExecutive Vice President

7

The ProblemThe Problem

Interstate and international companies canInterstate and international companies canmanipulate internal pricing (transfer pricing) tomanipulate internal pricing (transfer pricing) tominimize state corporate taxesminimize state corporate taxes

Transfer prices should be the same as if unrelatedTransfer prices should be the same as if unrelatedtaxpayers had engaged in the same transactiontaxpayers had engaged in the same transactionunder similar circumstancesunder similar circumstances

Variety of tax structures are used including bothVariety of tax structures are used including bothtraditional pass-throughs and new forms of pass-traditional pass-throughs and new forms of pass-throughsthroughs

Source of ProblemSource of Problem

Evolution of transfer pricing in accounting firmsEvolution of transfer pricing in accounting firms

Tax minimization schemes are heavily marketed toTax minimization schemes are heavily marketed tomajor corporationsmajor corporations

Accounting/consulting firms employ over 2,500Accounting/consulting firms employ over 2,500transfer pricing professionalstransfer pricing professionals

Consulting revenue for transfer pricing likely overConsulting revenue for transfer pricing likely over$500 million annually$500 million annually

8

Nature of ProblemNature of Problem

Delaware/Bermuda/Nevada holding companiesDelaware/Bermuda/Nevada holding companies

REITsREITs

Partnerships and Sub-SPartnerships and Sub-S

New forms of pass-throughs New forms of pass-throughs –– C corporations C corporations

Other methodsOther methods

Scope of ProblemScope of Problem

Corporate income taxes supplied 10.2Corporate income taxes supplied 10.2percent of state tax revenue in the statespercent of state tax revenue in the stateslevying them in 1979, but just 6.3 percent inlevying them in 1979, but just 6.3 percent in20002000

Total US loss of state corporate income taxTotal US loss of state corporate income taxrevenue attributable to tax planning wasrevenue attributable to tax planning was$10.353 billion for FY2001 (MTC estimate)$10.353 billion for FY2001 (MTC estimate)

Our research Our research –– state case study results 3 to state case study results 3 to4 times larger than MTC estimate4 times larger than MTC estimate

9

Tax Policy IssuesTax Policy IssuesLevel Playing FieldLevel Playing Field Large businesses must remain competitiveLarge businesses must remain competitive

Unequal reduction of tax payments by largeUnequal reduction of tax payments by largebusinesses versus small businessesbusinesses versus small businesses

Small businesses cannot compete by eliminatingSmall businesses cannot compete by eliminatingcorporate income taxes through multi-state taxcorporate income taxes through multi-state taxplanningplanning

Policy issues Policy issues –– eliminate corporate income tax or eliminate corporate income tax orlevel the playing fieldlevel the playing field

State Responses toState Responses toProblemProblem

Legislation Legislation –– unitary taxation unitary taxation Legislation Legislation –– royalty add-backs royalty add-backs Legislation Legislation –– alternative taxation methods alternative taxation methods Litigation Litigation –– involuntary combined filing involuntary combined filing Litigation Litigation –– ““economic nexuseconomic nexus”” Legislation and litigation Legislation and litigation –– application of IRC application of IRC

Section 482Section 482

10

What is IRC Section 482?What is IRC Section 482?

Allows the Secretary (of the Treasury) to adjust income, deductions,Allows the Secretary (of the Treasury) to adjust income, deductions,credits, etc. between or among two or more related parties in ordercredits, etc. between or among two or more related parties in orderto either prevent tax evasion or clearly reflect the income betweento either prevent tax evasion or clearly reflect the income betweenrelated partiesrelated parties

IRC regulations provide explicit methodologies for evaluating theIRC regulations provide explicit methodologies for evaluating thearmarm’’s length nature of intercompany pricess length nature of intercompany prices

Transfer prices must be the same as if unrelated taxpayers hadTransfer prices must be the same as if unrelated taxpayers hadengaged in the same transaction under similar circumstancesengaged in the same transaction under similar circumstances

If not, using 482 states have authority to adjust income, deductions,If not, using 482 states have authority to adjust income, deductions,credits, etc. between or among two or more related parties in ordercredits, etc. between or among two or more related parties in orderto either prevent tax evasion or clearly reflect the income betweento either prevent tax evasion or clearly reflect the income betweenrelated partiesrelated parties

Why Use IRC Section 482?Why Use IRC Section 482?

Economic approach, not pure accounting approach Economic approach, not pure accounting approach –– not a not aforced combinationforced combination

State case law indicates that involuntary combination or add-State case law indicates that involuntary combination or add-back approach is a 50/50 chance in the face of Due Processback approach is a 50/50 chance in the face of Due Processand Commerce Clauseand Commerce Clause

Has been used successfully at the federal level for decadesHas been used successfully at the federal level for decades

Technically clean and economic principles are easy toTechnically clean and economic principles are easy tounderstandunderstand

11

State IssuesState Issues

Authority Authority –– explicit, language and broad explicit, language and broad

Case lawCase law

Combined, consolidated, separate and unitary filingCombined, consolidated, separate and unitary filingmattersmatters

Probabilities of payment and litigationProbabilities of payment and litigation

How States Are UsingHow States Are UsingIRC Section 482IRC Section 482 As part of the system that includes bothAs part of the system that includes both

monitoring and report generation functionsmonitoring and report generation functionsfor a state corporate auditing teamfor a state corporate auditing team

As a tool for generating analyses for specificAs a tool for generating analyses for specificstate tax court cases for a state legal teamstate tax court cases for a state legal team

As part of a system that is contemplated forAs part of a system that is contemplated fordelivery to a statedelivery to a state

12

JOBS for KentuckyJOBS for KentuckyTax ModernizationTax Modernization

Mark Treesh, CPA, CMA Mark Treesh, CPA, CMA –– Commissioner CommissionerKentucky Department of RevenueKentucky Department of Revenue

Finance and Administration CabinetFinance and Administration Cabinet

JOBS for KentuckyJOBS for KentuckyTax ModernizationTax Modernization

Signed by Governor Fletcher on March 18, 2005Signed by Governor Fletcher on March 18, 2005Effective for Corporation Income Tax PeriodsEffective for Corporation Income Tax Periods

Beginning On or After January 1, 2005Beginning On or After January 1, 2005

13

Goals ofGoals ofJOBS for KentuckyJOBS for Kentucky

Encourage rather than impede theEncourage rather than impede thesuccess of business;success of business;

Make changes that are revenueMake changes that are revenueneutral with elements that will spurneutral with elements that will spureconomic growth in the future; andeconomic growth in the future; and

Export some of the tax burden toExport some of the tax burden tononresidents.nonresidents.

ConclusionConclusion

The scope of state corporate tax sheltering isThe scope of state corporate tax sheltering issubstantialsubstantial

If the tax is on the books, as a matter of tax equityIf the tax is on the books, as a matter of tax equitylarge corporations should pay their sharelarge corporations should pay their share

The states have a great potential revenue gain byThe states have a great potential revenue gain bycollecting tax owed themcollecting tax owed them

14

Key Components ofKey Components ofthe JOBS Planthe JOBS Plan

Corporation Tax ChangesCorporation Tax Changes

Key Components ofKey Components ofthe JOBS Planthe JOBS Plan

Repeals Corporation License TaxRepeals Corporation License Tax Reduces Corporation Income Tax RateReduces Corporation Income Tax Rate

and Expands Bracketsand Expands Brackets Updates Internal Revenue CodeUpdates Internal Revenue Code

Reference Date with Some ExceptionsReference Date with Some Exceptions

15

Key Components ofKey Components ofthe JOBS Planthe JOBS Plan Closes Corporation Tax LoopholesCloses Corporation Tax Loopholes

Eliminates Carry Back Provisions of Eliminates Carry Back Provisions of NOLsNOLs Requires Nexus Consolidated FilingRequires Nexus Consolidated Filing Limits Yearly NOL Deduction to 50% onLimits Yearly NOL Deduction to 50% on

Nexus Consolidated ReturnNexus Consolidated Return Requires Disclosure and Establishes CriteriaRequires Disclosure and Establishes Criteria

for allowance of for allowance of ““Delaware Holding CompanyDelaware Holding Company””DeductionDeduction

Requires Three-Factor Apportionment for Requires Three-Factor Apportionment for LLCsLLCs and andPartnershipsPartnerships

Key Components ofKey Components ofthe JOBS Planthe JOBS Plan Creates an Alternative Minimum CalculationCreates an Alternative Minimum Calculation

with taxpayer paying the maximum of;with taxpayer paying the maximum of;–– Regular Tax; orRegular Tax; or–– AMC Calculation (Lesser of A or B); orAMC Calculation (Lesser of A or B); or

A.A.$0.095 per $100 of gross receipts; or$0.095 per $100 of gross receipts; orB.B.$0.75 per $100 of Kentucky gross$0.75 per $100 of Kentucky gross

profits.profits.–– $175.00 Minimum Tax$175.00 Minimum Tax

16

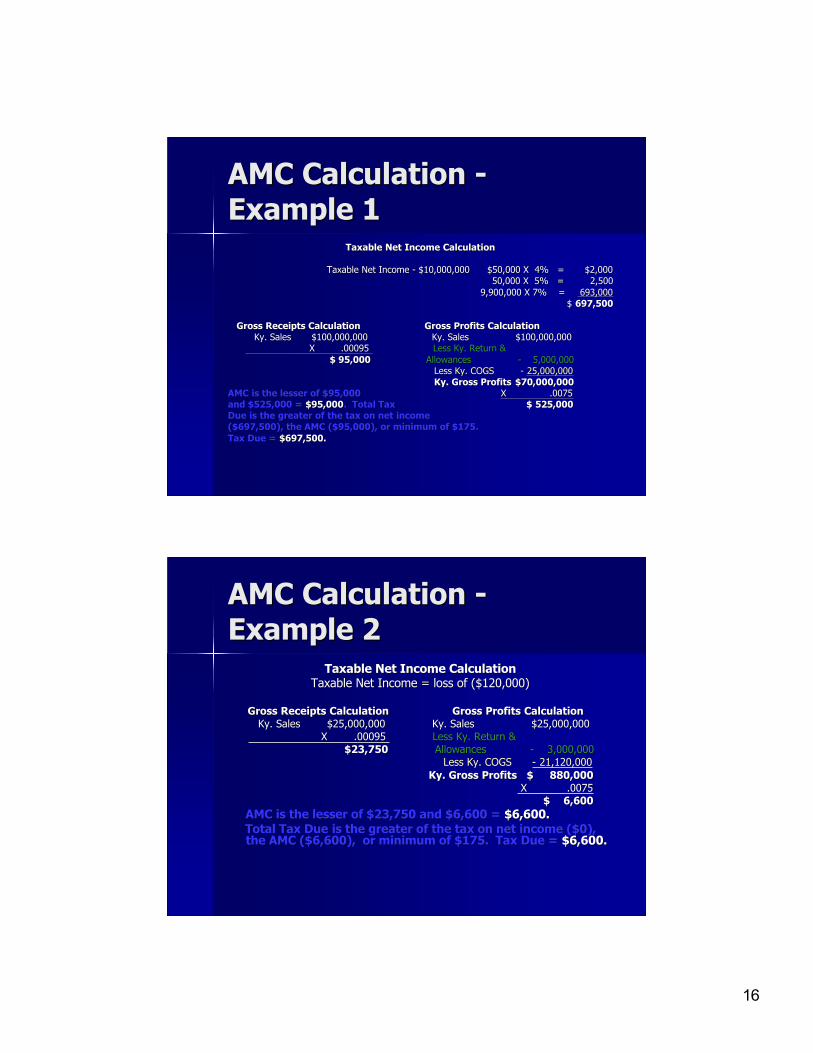

AMC Calculation -AMC Calculation -Example 1Example 1

Taxable Net Income CalculationTaxable Net Income Calculation

Taxable Net Income - $10,000,000 $50,000 X 4% = $2,000Taxable Net Income - $10,000,000 $50,000 X 4% = $2,000 50,000 X 5% = 2,50050,000 X 5% = 2,500

9,900,000 X 7% = 9,900,000 X 7% = 693,000 693,000 $ $ 697,500697,500

Gross Receipts Calculation Gross Receipts Calculation Gross Profits CalculationGross Profits Calculation Ky. Sales $100,000,000 Ky. Sales $100,000,000 Ky. Sales $100,000,000 Ky. Sales $100,000,000 X .00095 X .00095 Less Ky. Return &Less Ky. Return & $ 95,000$ 95,000 Allowances - 5,000,000Allowances - 5,000,000

Less Ky. COGS - Less Ky. COGS - 25,000,00025,000,000 Ky. Gross Profits Ky. Gross Profits $70,000,000$70,000,000

AMC is the lesser of $95,000AMC is the lesser of $95,000 X .0075X .0075and $525,000 = and $525,000 = $95,000$95,000. Total Tax. Total Tax $$ 525,000525,000DueDue is the greater of the tax on net incomeis the greater of the tax on net income($697,500), the AMC ($95,000), or minimum of $175.($697,500), the AMC ($95,000), or minimum of $175.Tax Due = Tax Due = $697,500.$697,500.

AMC Calculation -AMC Calculation -Example 2Example 2

Taxable Net Income CalculationTaxable Net Income CalculationTaxable Net Income = loss of ($120,000)Taxable Net Income = loss of ($120,000)

Gross Receipts Calculation Gross Receipts Calculation Gross Profits CalculationGross Profits Calculation Ky. Sales $25,000,000 Ky. Sales $25,000,000 Ky. Sales $25,000,000 Ky. Sales $25,000,000 X .00095 X .00095 Less Ky. Return &Less Ky. Return & $23,750$23,750 Allowances - 3,000,000Allowances - 3,000,000

Less Ky. COGS Less Ky. COGS - 21,120,000- 21,120,000 Ky. Gross Profits $ 880,000Ky. Gross Profits $ 880,000 X .0075 X .0075

$$ 6,6006,600 AMC is the lesser of $23,750 and $6,600 = AMC is the lesser of $23,750 and $6,600 = $6,600.$6,600. Total Tax Due Total Tax Due is the greater of the tax on net income ($0),is the greater of the tax on net income ($0),

the AMC ($6,600), or minimum of $175. Tax Due = the AMC ($6,600), or minimum of $175. Tax Due = $6,600.$6,600.

17

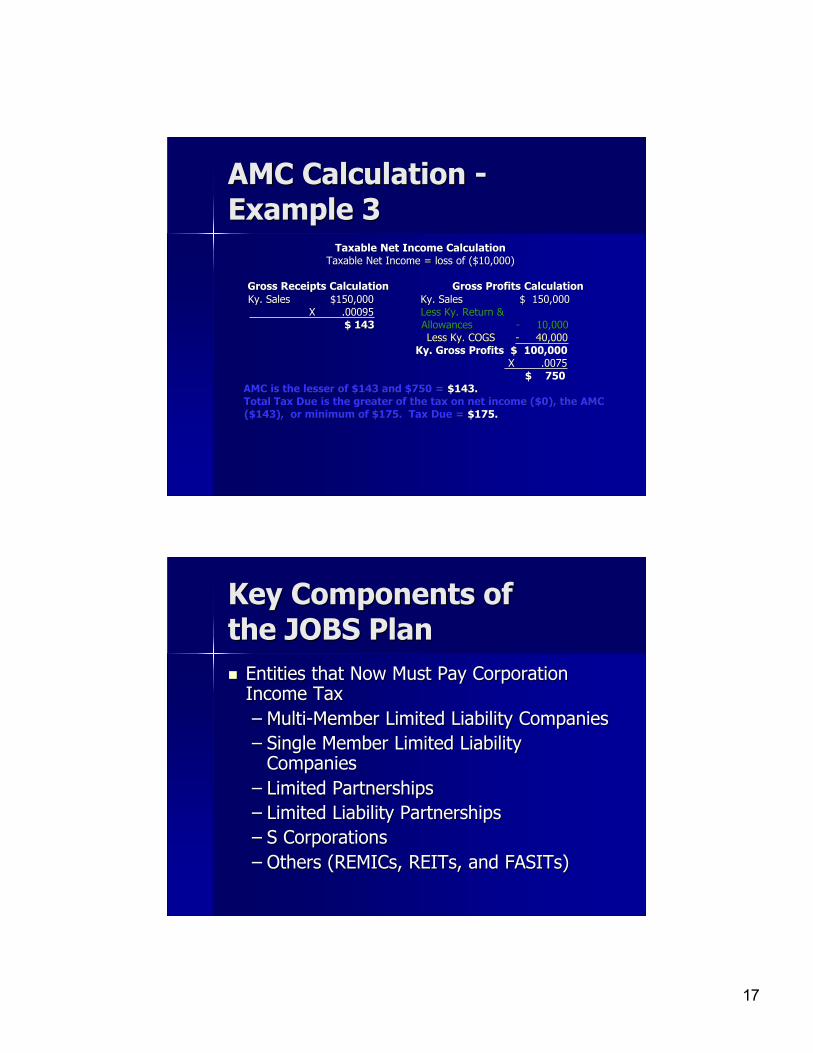

AMC Calculation -AMC Calculation -Example 3Example 3

Taxable Net Income CalculationTaxable Net Income CalculationTaxable Net Income = loss of ($10,000)Taxable Net Income = loss of ($10,000)

Gross Receipts Calculation Gross Receipts Calculation Gross Profits CalculationGross Profits Calculation Ky. Sales $150,000 Ky. Sales $ 150,000 Ky. Sales $150,000 Ky. Sales $ 150,000

X .00095 X .00095 Less Ky. Return &Less Ky. Return & $ 143$ 143 Allowances - 10,000Allowances - 10,000

Less Ky. COGS Less Ky. COGS - 40,000- 40,000 Ky. Gross Profits $ 100,000Ky. Gross Profits $ 100,000 X .0075 X .0075

$$ 750750 AMC is the lesser of $143 and $750 = AMC is the lesser of $143 and $750 = $143.$143. Total Tax Due Total Tax Due is the greater of the tax on net income ($0), the AMCis the greater of the tax on net income ($0), the AMC ($143), or minimum of $175. Tax Due = ($143), or minimum of $175. Tax Due = $175.$175.

Key Components ofKey Components ofthe JOBS Planthe JOBS Plan Entities that Now Must Pay CorporationEntities that Now Must Pay Corporation

Income TaxIncome Tax–– Multi-Member Limited Liability CompaniesMulti-Member Limited Liability Companies–– Single Member Limited LiabilitySingle Member Limited Liability

CompaniesCompanies–– Limited PartnershipsLimited Partnerships–– Limited Liability PartnershipsLimited Liability Partnerships–– S CorporationsS Corporations–– Others (REMICs, REITs, and FASITs)Others (REMICs, REITs, and FASITs)

18

Key Components ofKey Components ofthe JOBS Planthe JOBS PlanTreatment of Individual OwnersTreatment of Individual Owners

–– Individual partners, members or shareholders ofIndividual partners, members or shareholders ofpass through entities will receive a credit for thepass through entities will receive a credit for thetax paid on net income at the entity level basedtax paid on net income at the entity level basedon their distributive share ratio.on their distributive share ratio.

–– In addition, a refundable credit is provided forIn addition, a refundable credit is provided forindividual owners for tax periods ending afterindividual owners for tax periods ending afterJanuary 1, 2005 and before January 1, 2007.January 1, 2005 and before January 1, 2007.The credit is based on the 1% differenceThe credit is based on the 1% differencebetween the top corporate rate and the topbetween the top corporate rate and the topindividual rate.individual rate.

IssuesIssues

Forms Forms –– Partnership or Corporation Rules on Partnership or Corporation Rules onForms?Forms?

Credit For Tax Paid to Kentucky - How WillCredit For Tax Paid to Kentucky - How WillOthers States Treat KentuckyOthers States Treat Kentucky’’s Entitys EntityTaxation on Partners, Shareholders andTaxation on Partners, Shareholders andMembers Individual Income Tax Returns?Members Individual Income Tax Returns?

Non-Refundable Credit Non-Refundable Credit –– How Many How ManyIndividual Taxpayers Will Not Be Able ToIndividual Taxpayers Will Not Be Able ToFully Utilize the Entity Tax Credit on TheirFully Utilize the Entity Tax Credit on TheirKentucky Individual Income Tax Returns?Kentucky Individual Income Tax Returns?

19

ContactsContacts

Nonie Manion 518-457-2750Nonie Manion 518-457-2750Eric CookEric Cook 703-359-8211703-359-8211Mark Treesh 502-564-3226Mark Treesh 502-564-3226