Embed Size (px)

Citation preview

PAYE and foreign employment issues

Presented by: Karen van Wyk

Content of the session

Basics

Travel allowance

Subsistence allowance

Entertainment allowance

Fringe benefits

Link with VAT

Foreign employment exemptions

Basics

Allowances – Position of

inclusion

Gross income

Less: Exempt income

Less: Deductions

Less: Section 20 assessed loss

Less: Section 10(1)(k) fund contributions

Add: Taxable capital gain

Add: Section 8(1)(a) AllowancesLess: Section 18A donations

Taxable income

Allowances

Net amount should be included

Allowance / advance paid or granted

Less: Portion actually expended

Travel allowancesSection 8(1)(b)

Basics

Fixed travel allowance

Employee receives the same monthly amount, regardless of how many km’s he/she

travels for business purposes

Reimbursive travel allowance

Employee receives the allowance based on the actual distance travelled for business

Therefore, the employee first has to travel for business purposes and will then receive

the reimbursive allowance based on actual data

Fixed travel allowance

Portion that is expended for business purposes is effectively tax free

Can only be claimed if log book is kept

Therefore, the private part is taxable

If travel allowance is received in respect of a vehicle that is also a company car as

defined in paragraph 7 (i.e. It is one and the same vehicle)

Full travel allowance is included in taxable income

No deductions are allowed against the travel allowance

Travelling between home and work ≠ business travel

Deemed rate/km

Value of vehicle (including VAT, excluding finance charges)

Fixed cost (per annum)

Fuel cost (c/km)

Maintenance cost (c/km)

Does not exceed R80 000 26 675 82.4 30.8

R80 000- R160 000 47 644 92.0 38.6

R160 000 – R240 000 68 684 100.0 42.5

R240 000 – R320 000 87 223 107.5 46.4

R320 000 – R400 000 105 822 115.0 54.5

R400 000 – R480 000 125 303 132.0 64.0

R480 000 – R560 000 144 784 136.5 79.5

Exceeding R560 000 144 784 136.5 79.5

∑ = total deemed cost/km

Only if FULL cost borne by the employee

Deemed rate: Fixed cost

component

Total fixed cost .

Total km’s travelled

Total km’s travelled = All travel (i.e. Business and private)

Must be converted to cents (other components in table are quoted in cents)

Total fixed cost is a value per annum

Therefore, must be apportioned on a daily basis if travel allowance is received for less

than the full year

Represents total wear-and-tear / lease instalments, interest, licence and insurance for the

year of assessment

Actual rate/km

If accurate records are kept of actual expenses incurred, a taxpayer can also claim actual expenses against the

travel allowance received

How is the “cost” that can be deducted against the allowance calculated?

Leased vehicle (finance or operating lease) – Total lease expense is used and must be limited based on

the fixed cost in the table

Vehicles owned – Wear-and-tear must be determined over 7 years, cost of vehicle limited to R560 000

Actual costs also includes fuel, maintenance, insurance, finance charges, licence costs and toll fees

All actual cost is aggregated and divided by the total km’s travelled

Business km’s x actual rate/km = Actual cost which is then deducted from the travel allowance received

Example

Mr A owns a Polo Vivo that cost him R200 000 (including VAT, excluding finance charges).

He receives a R3 000 travel allowance per month from his employer. During the 2017 year

of assessment, he travelled 20 000 km in total of which 5 000 was travelled for business

purposes. He kept an accurate log book and record of actual costs incurred which

amounted to:

Fuel costs R10 000

Maintenance costs R5 000

Insurance R2 500

Finance costs R7 000

Licence cost R500

Solution – Deemed cost

Allowance received (R3 000 x 12) R36 000

Total km’s travelled 20 000

Less: Private km’s (15 000)

Business km’s 5 000

Deemed cost:

Fixed cost per tables(68 684 / 20 000 x 100) 343.4c

Fuel cost per table 100.0c

Maintenance cost per table 42.5c

Total cost per km 485.9c

Total deemed cost (485.9c x 5 000km) (24 295)

Taxable amount based on deemed cost 11 705

Solution – Actual cost

Allowance received (R3 000 x 12) R36 000

Less: Actual costs incurred

Wear-and-tear (R200 000 / 7) R28 571

Fuel costs R10 000

Maintenance costs R5 000

Insurance R2 500

Finance costs R7 000

Licence cost R500

Total actual costs R53 571

Actual cost deducted for business use (R13 393)

(R53 571 / 20 000km x 5 000km)

Taxable amount if actual costs are claimed R22 607

Therefore, taxpayer must claim deemed cost

Example

Mr A owns a Polo Vivo that cost him R200 000 (including VAT, excluding finance charges).

He received a R3 000 travel allowance per month from his employer for the last 6 months of

the 2017 year of assessment. During the last 6 months of the year of assessment, he

travelled 20 000 km in total of which 5 000 was travelled for business purposes. He kept an

accurate log book but did not keep record of expenses.

Solution – Deemed cost

Allowance received (R3 000 x 6) R18 000

Total km’s travelled 20 000

Less: Private km’s (15 000)

Business km’s 5 000

Total fixed cost per tables 68 684

Apportioned fixed cost for 6 months

68 684 x 181/365 34 060

Deemed cost:

Fixed cost per tables (34 060 / 20 000 x 100) 170.3c

Fuel cost per table 100.0c

Maintenance cost per table 42.5c

Total cost per km 312.8c

Total deemed cost (312.8c x 5 000km) (15 640)

Taxable amount based on deemed cost 2 360

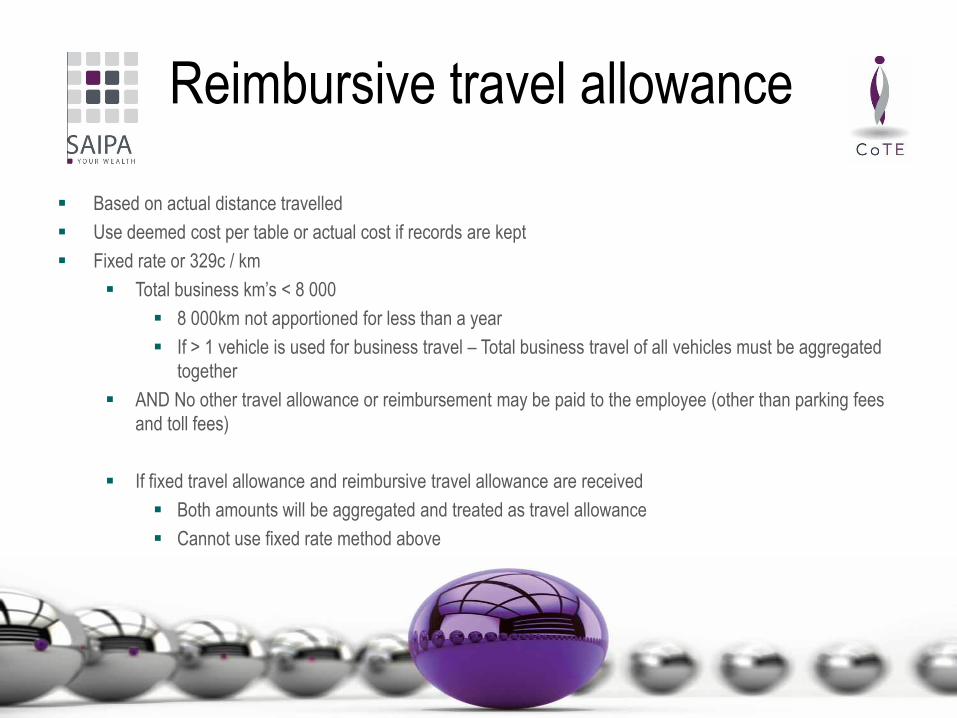

Reimbursive travel allowance

Based on actual distance travelled

Use deemed cost per table or actual cost if records are kept

Fixed rate or 329c / km

Total business km’s < 8 000

8 000km not apportioned for less than a year

If > 1 vehicle is used for business travel – Total business travel of all vehicles must be aggregated

together

AND No other travel allowance or reimbursement may be paid to the employee (other than parking fees

and toll fees)

If fixed travel allowance and reimbursive travel allowance are received

Both amounts will be aggregated and treated as travel allowance

Cannot use fixed rate method above

Example

Mr A owns a Polo Vivo that cost him R200 000 (including VAT, excluding finance charges).

He received a travel allowance of R3.00 per km travelled for business purposes. During the

year of assessment, he travelled 20 000 km in total. He kept an accurate log book but did

not keep record of expenses.

A) Assume he travelled 5 000 km for business purposes

B) Assume he travelled 10 000 km for business purposes

Solution A

Travel allowance received (R3.00 x 5 000 km) 15 000

Deemed fixed rate per km (329c x 5 000km) 16 450

Limited to travel allowance received (15 000)

Therefore, taxable amount 0

Solution B

Allowance received (R3.00 x 10 000km) 30 000

Total km’s travelled 20 000

Less: Private km’s (10 000)

Business km’s 10 000

Deemed cost:

Fixed cost per tables(68 684 / 20 000 x 100) 343.4c

Fuel cost per table 100.0c

Maintenance cost per table 42.5c

Total cost per km 485.9c

Total deemed cost (485.9c x 10 000km) 48 590

Limited to allowance (30 000)

Taxable amount based on deemed cost 0

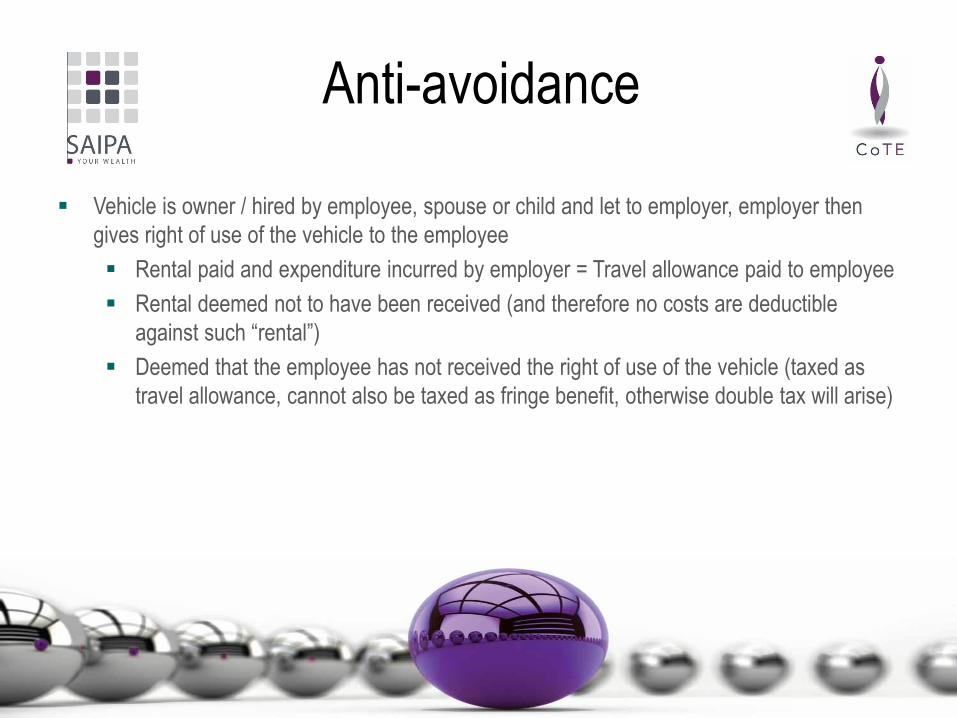

Anti-avoidance

Vehicle is owner / hired by employee, spouse or child and let to employer, employer then

gives right of use of the vehicle to the employee

Rental paid and expenditure incurred by employer = Travel allowance paid to employee

Rental deemed not to have been received (and therefore no costs are deductible

against such “rental”)

Deemed that the employee has not received the right of use of the vehicle (taxed as

travel allowance, cannot also be taxed as fringe benefit, otherwise double tax will arise)

Example

Mr B leases a Polo Vivo with a cost price of R200 000 (including VAT) for R3 000 per month. He then leases

the vehicle to his employer for R3 000 per month and is granted the right of use of the vehicle by his employer.

Mr X bears the full fuel cost and cost of maintenance of the vehicle. During the 2017 year of assessment Mr B

travelled a total 20 000 km of which 12 000 was travelled for business purposes

Solution

Rental income Not taxable

Rental expense Not deductible

Use of company car Not applicable

Travel allowance (R3 000 x 12) 36 000

Less: Deduction for business use (12 000km x 485.9c ) R58 308

Limited to travel allowance (36 000)

Taxable amount 0

Deemed cost:

Fixed cost per tables(68 684 / 20 000 x 100) 343.4c

Fuel cost per table 100.0c

Maintenance cost per table 42.5c

Total cost per km 485.9c

Link with employees’ tax

Normal rule: Include 80% of fixed travel allowance in remuneration for employees’ tax

purposes

If 80% or more of the vehicle is used for business purposes: Only 20% of fixed travel

allowance must be included in remuneration

Log book must be used to prove business use

Reimbursive travel allowance is not subject to employees’ tax

Regardless of what business km’s came to

Regardless of whether fixed rate was used or not

Unexpended portion will be subject to normal tax

Subsistence allowancesSection 8(1)(c)

Working

When an employee must spend at least one night away from usual residence for business purposes

Usual residence must be in SA

Not applicable for allowance received to move to a new place of residence (since no usual residence exists at

that point in time)

Can claim costs against allowance received

Actual accommodation, meals and other incidental costs (records must be kept)

OR

Deemed cost for each day or part of a day that a recipient is away from usual residence for business purposes

In SA:

Incidental costs only – R109 per day

Meals and incidental costs – R353

Outside SA: Tables (convert to Rand using average exchange rates)

Therefore, only ACTUAL costs allowed for accommodation (no deemed option)

Can only claim for ad hoc allowances, not applicable if salary is structured to include a fixed monthly subsistence

allowance

Can only claim if costs are incurred by employee (if incurred by employer, no deduction against allowance)

Example

Mr. C must spend one night away from his usual place of residence to visit a branch of the

employer that he is working for. He received an allowance of R5 000 in this regard.

(A) Mr. C travels to Limpopo and kept record of all expenses incurred by himself which

amounted to R2 800.

(B) Mr. C travels to Limpopo and does not keep record of expenses incurred by himself.

(C) Mr. C travels to Belgium. His employer pays for his accommodation and Mr. C pays for

meals and other incidental costs which amounted to R4 000 (but he has not kept accurate

record). The average exchange rate for the year of assessment is 1€ = R15.00

Solution

(A) Allowance received R5 000

Less: Actual expenditure incurred (R2 800)

Taxable amount R2 200

(B) Allowance received R5 000

Less: Deemed expenditure incurred (2 days x R353) (R706)

Taxable amount R4 294

(C) Allowance received R5 000

Less: Deemed expenditure incurred (2 days x €146 x R15) (R4 380)

Taxable amount R620

Link with Employees’ Tax

Subsistence allowances are excluded from the definition of remuneration for Employees’ Tax

purposes

Therefore, not subject to Employees’ Tax

If, by the end of the month following the payment of the subsistence allowance, the

employee has

Not spent at least one night away from usual place of residence; or

Paid back the allowance to the employer

THEN: Deemed to be paid for services rendered – Gross income paragraph (c)

Therefore, will then become subject to Employees’ Tax

Entertainment allowance

Working

Include amount awarded in taxable income

Can only claim a deduction against it if incurred in the production of income and the

requirements of section 11(a) have been met

General tax principles

Not of a capital nature

In the production of income (future income also allowed)

Fringe benefits

Basics

Calculate the cash equivalent per the Seventh Schedule if a benefit / advantage is given to

an employee by virtue of his/her employment

Needs employer/employee relationship

Still fringe benefit if employees are released from an obligation to repay an obligation to

the employer which arose prior to retirement

Directors and past employees who were the sole or controlling holders of shares are

specifically included in the definition of an employee

Benefits granted to a relative of an employee or another person by virtue of the employee’s

employment with the employer

Taxed in the hands of the employee

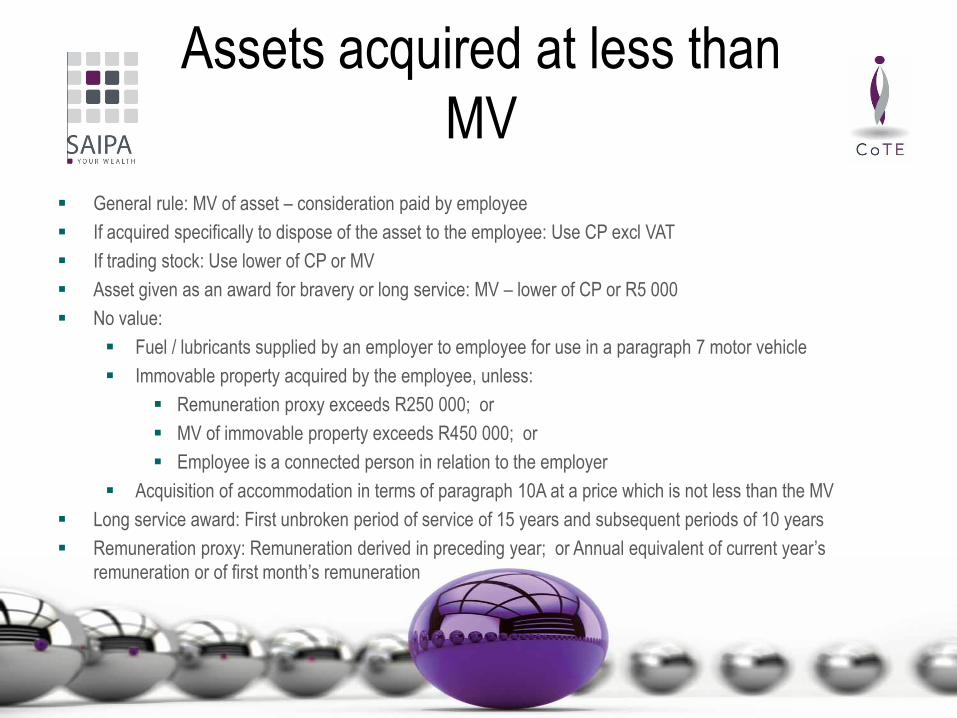

Assets acquired at less than

MV

General rule: MV of asset – consideration paid by employee

If acquired specifically to dispose of the asset to the employee: Use CP excl VAT

If trading stock: Use lower of CP or MV

Asset given as an award for bravery or long service: MV – lower of CP or R5 000

No value:

Fuel / lubricants supplied by an employer to employee for use in a paragraph 7 motor vehicle

Immovable property acquired by the employee, unless:

Remuneration proxy exceeds R250 000; or

MV of immovable property exceeds R450 000; or

Employee is a connected person in relation to the employer

Acquisition of accommodation in terms of paragraph 10A at a price which is not less than the MV

Long service award: First unbroken period of service of 15 years and subsequent periods of 10 years

Remuneration proxy: Remuneration derived in preceding year; or Annual equivalent of current year’s

remuneration or of first month’s remuneration

Examples

A computer was acquired by XYZ Ltd at a cost of R10 000 (excluding VAT). The computer

was used for business purposes for 5 years and then sold to Employee A for R3 000

(excluding VAT) when the market value was R5 000.

A computer was acquired by XYZ Ltd at a cost of R10 000 (excluding VAT) with the specific

purpose of awarding it as a fringe benefit to Employee B when the market value thereof was

R12 000 (excluding VAT).

XYZ Ltd acquired a gold watch at a cost of R6 840 (including VAT) to award to Employee C

as a long-service award after completing 20 years of service. On the date that the watch

was awarded to Employee C, it had a market value including VAT of R7 500 (including VAT).

XYZ Ltd awarded a cash amount of R6 270 to Employee D after completing 20 years of

service.

Solution

Employee A:

Market value R5 000

Consideration (R3 000)

Cash equivalent R2 000

Employee B:

Cost price R10 000

Consideration R0

Cash equivalent R10 000

Employee C:

Cost price (R6 840 x 100/114) R6 000

Exempt (lower of R5 000 or R6 000) (R5 000)

Cash equivalent R1 000

Employee D:

Cash awarded R6 270

Private use of sundry assets

Other than right of use of motor car and residential accommodation

If rented:

Value of private use = rent paid by employer

If employee has sole right of use for useful life

Value of private use = cost price of asset

If asset is owned by employer

Value of private use = 15% x lower of CP/MV x period used/365

No value

Private use is incidental

Asset is amenity to by enjoyed at employee’s place of work or for recreational purposes at employee’s

place of work or at place of recreation provided by employer for the use of employees in general

Asset can be used by employees in general for short periods and value of private use does not exceed

amount determined in public notice of Commissioner

Telephone or computer which employer uses mainly for business purposes

Books, literature, recordings or work of art

Right of use of motor car

Determined value = Retail MV at the time when the employer acquired the vehicle

What is the retail MV?

Reduced by 15% diminishing value for every completed 12-month cycle that someone else had the right

of use or that the vehicle was used for a different purpose

Reduction is n.a. If the employee and the asset are transferred to an associated institution

Basic calculation

Operating lease: Actual cost of operating lease for the employer + cost of fuel

3.5% p.m. x Determined value less consideration given by employee

3.25% p.m. x Determined value if “maintenance plan” was automatically included in the CP of the motor

vehicle (“maintenance plan” = contract covering all maintenance costs for not < 3 years and a distance of

not < 60 000km) less consideration given by employee

Value of private use is apportioned on a daily basis

No reduction is made simply because the vehicle is for any reason temporarily not used by the employee

If an employee used > 1 vehicle primarily for business purposes – Value of private use is calculated as

3.5% or 3.25% on the vehicle with the highest determined value

Right of use of motor vehicle

Nil value

Vehicle is available to and used by employees in general and private use is infrequent

or merely incidental to business use and vehicle is not normally kept at or near the

employee’s residence when not in use outside of business hours

Employee is regularly required to use the vehicle for the performance of his duties

outside normal working hours and he is not permitted to use the vehicle for private

purposes other than to travel between work place and place of residence

Link with PAYE

Normal rule: 80% inclusion

If vehicle is used 80% or more for business purposes: 20% inclusion

Gross inclusion (i.e. Before adjusting for paragraph 7(7) and 7(8))

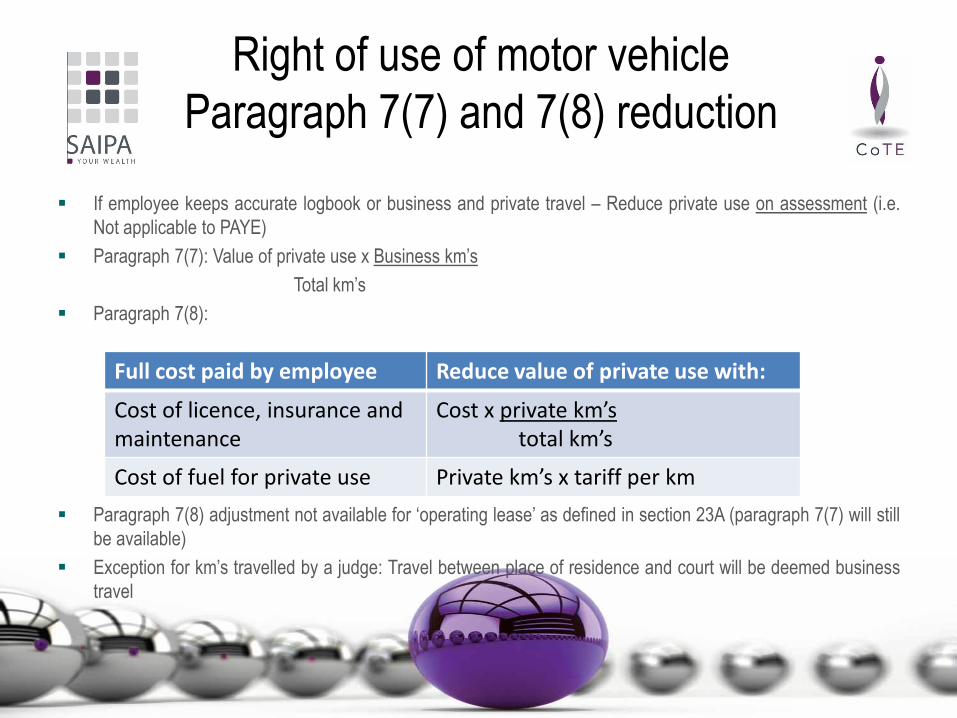

Right of use of motor vehicle

Paragraph 7(7) and 7(8) reduction

If employee keeps accurate logbook or business and private travel – Reduce private use on assessment (i.e.

Not applicable to PAYE)

Paragraph 7(7): Value of private use x Business km’s

Total km’s

Paragraph 7(8):

Paragraph 7(8) adjustment not available for ‘operating lease’ as defined in section 23A (paragraph 7(7) will still

be available)

Exception for km’s travelled by a judge: Travel between place of residence and court will be deemed business

travel

Full cost paid by employee Reduce value of private use with:

Cost of licence, insurance and maintenance

Cost x private km’stotal km’s

Cost of fuel for private use Private km’s x tariff per km

Examples

Employee A was granted the right of use of a motor car owned by ABC (Pty) Ltd with effect from1 August 2016. ABC (Pty) Ltd originally acquired the vehicle on 1 February 2014 at a cost of R114 000(including VAT).

OLD rules for determined value

Original cost (including VAT) R114 000

Less: R114 000 x 15% (R17 100)

Subtotal R96 900

Less: R96 900 x 15% (R14 535)

Determined value R82 365

Cash equivalent: R82 365 x 3.5% x 7 R20 179

Employee B was granted the right of use of a motor car owned by ABC (Pty) Ltd with effect from1 August 2016. ABC (Pty) Ltd originally acquired the vehicle on 1 April 2015. Assume a retail market value ofR100 000.

NEW rules for determined value

Retail market value R100 000

Less: R100 000 x 15% (R15 000)

Determined value R85 000

Cash equivalent: R85 000 x 3.5% x 7 R20 825

Examples

Taxpayer K is granted the right of use of two motor vehicles which are owned by his

employer (no maintenance plan exists on these two vehicles). Vehicle 1 has a retail MV of

R136 800 and Vehicle 2 has a retail MV of R182 400. All costs are incurred by the employer

and Taxpayer K bears no cost.

(a) Assume Taxpayer K uses both vehicles primarily for business purposes and kept an

accurate logbook proving that 10 000km of the total distance travelled of 15 000km was

travelled for business purposes.

(b) Assume Taxpayer K uses both vehicles primarily for business purposes but kept no

accurate logbook. He applied for paragraph 7(6).

Solution (a)

Accurate logbook was kept

Therefore, paragraph 7(6) is not available

Paragraph 7(7) must be applied

Cash equivalent =

Vehicle 1: R136 800 x 3.5% R4 788

Vehicle 2: R182 400 x 3.5% R6 384

Total monthly cash equivalent R11 172

Taxable amount on assessment: R11 172 x 12 – (R11 172 x 12 x 10 000/15 000)

= R44 688

Solution (b)

Cash equivalent is based on vehicle with the highest determined value

Therefore, the monthly cash equivalent amounts to R182 400 x 3.5% = R6 384

Taxable amount for assessment purposes: R6 384 x 12 = R76 608

Example

DEF Ltd granted the right of use of a BMW X5 to its CEO from 1 March 2015. The vehicle

was acquired by DEF Ltd on 1 March 2015 and is subject to a maintenance contract. It has

a retail MV of R912 000. The CEO kept an accurate logbook of distance travelled. Total

travel during the 2016 year of assessment was 15 000km of which 10 000km was travelled

for business purposes. The CEO pays an amount of R5 000 for this right of use. He is

responsible for the total fuel expense and also paid R1 200 for the licence of the vehicle.

Solution

Value of private use (R912 000 x 3.25% x 12) R355 680

Consideration paid by CEO (R5 000 x 12) (R60 000)

Cash equivalent R295 680

Paragraph 7(7) adjustment (R355 680 x 10 000/15 000) (R237 120)

Paragraph 7(8) adjustment (R6 920)

Licence: R1 200 x 5 000/15 000 R400

Fuel: 5 000km x 130.4c = R6 520

Taxable income R51 640

Example

DEF Ltd granted the right of use of a BMW X5 to its CEO from 1 March 2016. The vehicle

was acquired by DEF Ltd on 1 March 2016 and is subject to a maintenance contract. It has

a retail MV of R912 000. The CEO kept an accurate logbook of distance travelled. Total

travel during the 2017 year of assessment was 15 000km. The CEO only uses the vehicle

to travel between his home and the office and uses it for private purposes over weekends

and family outings. The CEO pays an amount of R5 000 for this right of use. He is

responsible for the total fuel expense and also paid R1 200 for the licence of the vehicle.

Solution

Value of private use (R912 000 x 3.25% x 12) R355 680

Consideration paid by CEO (R5 000 x 12) (R60 000)

Cash equivalent R295 680

Paragraph 7(7) adjustment (not available – all travel is private)

Paragraph 7(8) adjustment (R21 675)

Licence: R1 200 x 15 000/15 000 R1 200

Fuel: 15 000km x 136.5c = R20 475

Taxable income R274 005

Example

DEF Ltd granted the right of use of a BMW X5 to its CEO from 1 March 2015. The vehicle

was leased by DEF Ltd from 1 March 2015 at a monthly rental of R20 000. It has a retail MV

of R912 000. The CEO kept an accurate logbook of distance travelled. Total travel during

the 2016 year of assessment was 15 000km of which 10 000km was travelled for business

purposes. DEF Ltd also pays R1 500 per month in respect of the fuel cost of the vehicle.

Cash equivalent: (R20 000 + R1 500) x 12 R258 000

Paragraph 7(7) adjustment (R258 000 x 10 000/15 000) (R172 000)

Taxable income R86 000

Meals, refreshments and

vouchers

Cost for employer less compensation paid by employee

Nil value

Meal or refreshment supplied in canteen, cafeteria or dining room operated by or on

behalf of the employer and patronised wholly or mainly by its employees

Meal or refreshment supplied by employer to employees on business premises

Meal or refreshment supplied by employer to employee during business hours or

extended working hours

Meal or refreshment supplied by employer to employee on a special occasion

Meal or refreshment enjoyed by an employee in the course of providing a meal or

refreshment to someone whom he is required to entertain on behalf of employer

Residential accommodation

Rental value less amount paid by employee for accommodation and household goods or power

Rental value = (A – B) x C/100 x D/12

A = Remuneration proxy

B = R75 000 (Rnil if employee or spouse controls the private company or they or their minor child have

the option to become the owner of the accommodation)

C = 17 (18 if four rooms and is either furnished or electricity is supplied; 19 if four rooms and furnished

and electricity is supplied)

D = number of FULL months that employee is entitled to accommodation

What is remuneration proxy?

Remuneration as defined in paragraph 1 of the Fourth Schedule

If employee was employed by the employer for the whole of the preceding year: full remuneration

If previous year’s remuneration is less than 365 days: remuneration must be grossed up for 365 days

If employee was not employed in previous year: remuneration of first month of employment must be

grossed up for 365 days

Residential accommodation

When will the formula be used?

Employer / associated institution owns the accommodation; or

Employee has an interest in the accommodation; or

Employer / associated institution does not own the accommodation; and

It is customary and necessary for the employer to provide free / subsidised accommodation

For proper performance of employee duties; or

As a result of frequent movement of employees; or

As a result of the lack of employer-owned accommodation; and

The benefit is solely for bona fide business purposes

When will an employee have an interest in the accommodation?

Accommodation is owned by employee / connected person; or

Any increase in the value of the accommodation accrues for the benefit of the employee / connected person; or

Employee / connected person has a right to acquire the accommodation from his/her employer

NEW PROVISION FROM 1 MARCH 2015 If employer or associated institution obtained the accommodation in an arm’slength transaction from a non-connected person and full ownership does not vest in the employer or associated institution:Use lower of

Formula value; or

Expenditure paid by employer / associated institution

If residential accommodation = 2 or more units situated at different places which the employee is entitled to occupy fromtime to time while performing duties: Highest rental value of the units

Residential accommodation

Nil value

Accommodation inside or outside SA supplied by an employer while the resident employee is away from

his/her usual place of residence in SA for work purposes

Not applicable if more than one residential accommodation is made available at different places

which the employee is entitled to occupy from time to time while performing his/her duties

Accommodation in SA supplied by employer to non-resident employee who is away from his/her usual

place of residence outside SA

For ≤ 2 years after date of arrival in SA: or

The employee is physically present in SA < 90 days in the y.o.a.

Rnil not applicable if employee was present in SA > 90 days during the y.o.a. Immediately

preceding the date of arrival of the employee in SA; or

Rnil not applicable to the extent that the cash equivalent of the value of the taxable benefit

exceeds R25 000 x number of months during which the employee was away

Examples

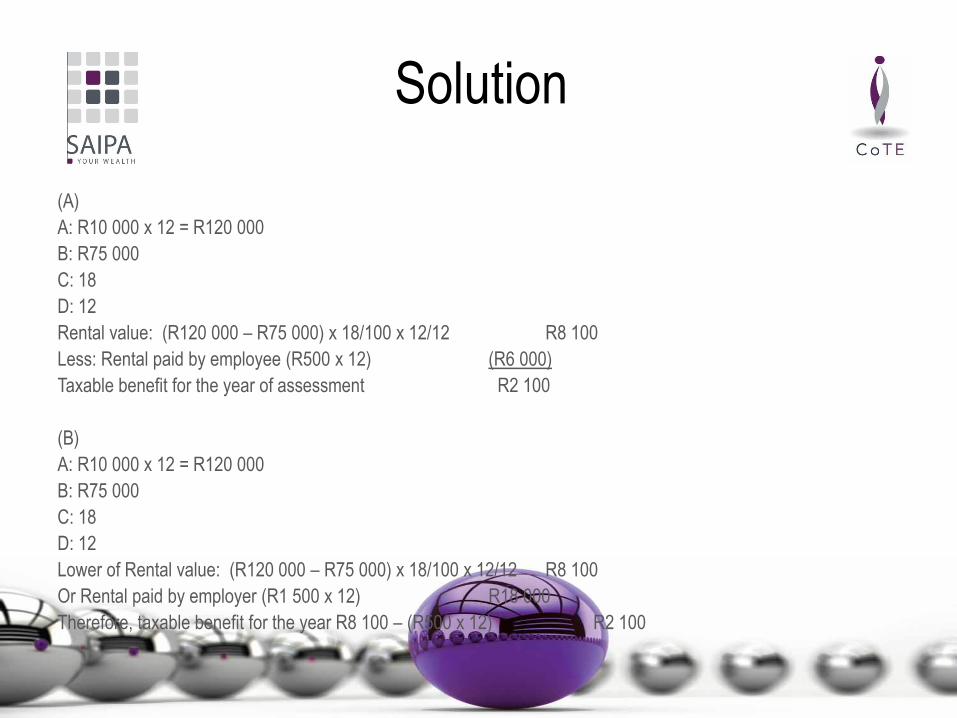

(a) Employee A was in the employ of KLM Ltd for the full previous year. His salary was

R10 000 per month. KLM Ltd owns accommodation and supplies Employee A with

unfurnished flat consisting of 3 bedrooms. Employee A uses the accommodation for the

full year and pays R500 rent per month. All other expenses are borne by the employer.

(b) Employee B was in the employ of KLM Ltd for the full previous year. His salary was

R10 000 per month. KLM Ltd rents a flat from an unconnected person in an arm’s length

transaction at a cost of R1 500 per month. Employee A uses the accommodation for the

full year and pays R500 rent per month.

Solution

(A)

A: R10 000 x 12 = R120 000

B: R75 000

C: 18

D: 12

Rental value: (R120 000 – R75 000) x 18/100 x 12/12 R8 100

Less: Rental paid by employee (R500 x 12) (R6 000)

Taxable benefit for the year of assessment R2 100

(B)

A: R10 000 x 12 = R120 000

B: R75 000

C: 18

D: 12

Lower of Rental value: (R120 000 – R75 000) x 18/100 x 12/12 R8 100

Or Rental paid by employer (R1 500 x 12) R18 000

Therefore, taxable benefit for the year R8 100 – (R500 x 12) R2 100

Holiday accommodation

Prevailing rate per day less consideration paid by employee

If employer is not the owner and rents accommodation for the employee from a person other than an

associated institution: Costs incurred by employer for rental, meals, refreshments and other services

Example

ABC Ltd makes free holiday accommodation available to Employee E, his wife and three children

at its cottage in Hermanus for ten days

(A) What is the cash equivalent of the taxable benefit if the cottage is normally let for R2 000

per day?

10 days x R2 000 = R20 000

(B) What is the cash equivalent of the taxable benefit if the cottage is normally let for R500

per person per night?

9 nights x R500 x 5 = R22 500

Low-interest rate loans

If loan granted relates to services rendered – Fringe benefits

Not applicable if loan is granted to enable employees to buy qualifying shares

If loan granted relates to holding of shares – Deemed dividend

Calculation: Interest on outstanding capital based on official interest rate less actual interest paid by employee

What is the official interest rate?

When does this cash equivalent accrue to the employee?

Nil value

Debt ≤ R3 000 at any point in time; or

Debt enables the employee to further his/her own studies

Deemed loan: Residential accommodation is deemed a low-interest rate loan if

Employee lives in employer-owned house; and

Employee, his spouse or minor child is entitled or obliged to acquire the house from the employer at a

future date at a price stated in an agreement; and

Employee is required to pay for use of accommodation a rental based wholly or partly as a % of future

purchase price stated in the agreement

THEN: Loan granted = future purchase price

THEN: Employee’s payment for use = deemed interest paid

Examples

DEF Ltd has awarded the following loans to employees during the 29 February 2016 year of

assessment:

(a) On 1 June 2015 R2 000 was awarded to Employee D to enable him to pay unexpected medical bills.

Employee D repaid the R2 000 on 31 July 2015.

(b) On 1 July 2015 R10 000 was awarded to Employee E to enable him to pay for his study fees.

Employee E is taking management and basic accounting courses.

(c) On 1 August 2015 R5 000 was awarded to Employee F. The amount was repaid on 30 September

2015.

(d) On 1 November 2015 R100 000 was awarded to Employee G to enable him to renovate his family

home. An amount of R10 000 was repaid on 31 January 2016. The loan bears interest at 5%.

Assume an official interest rate of 5.75% until 31 August 2015 and 6% since 1 September 2015.

Solution

(a) R2 000 loan < R3 000. Therefore, Rnil value

(b) R10 000 loan to further studies. Rnil value

(c) (R5 000 x 5.75% x 1/12) + (R5 000 x 6% x 1/12) = R48.96

(d) Until 31 January 2016 ((R100 000 x (6% - 5%) x 3/12)) = R250

1 Feb – 28 Feb 2016 ((R90 000 x (6% - 5%) x 1/12)) = R75

Therefore, total cash equivalent = R325

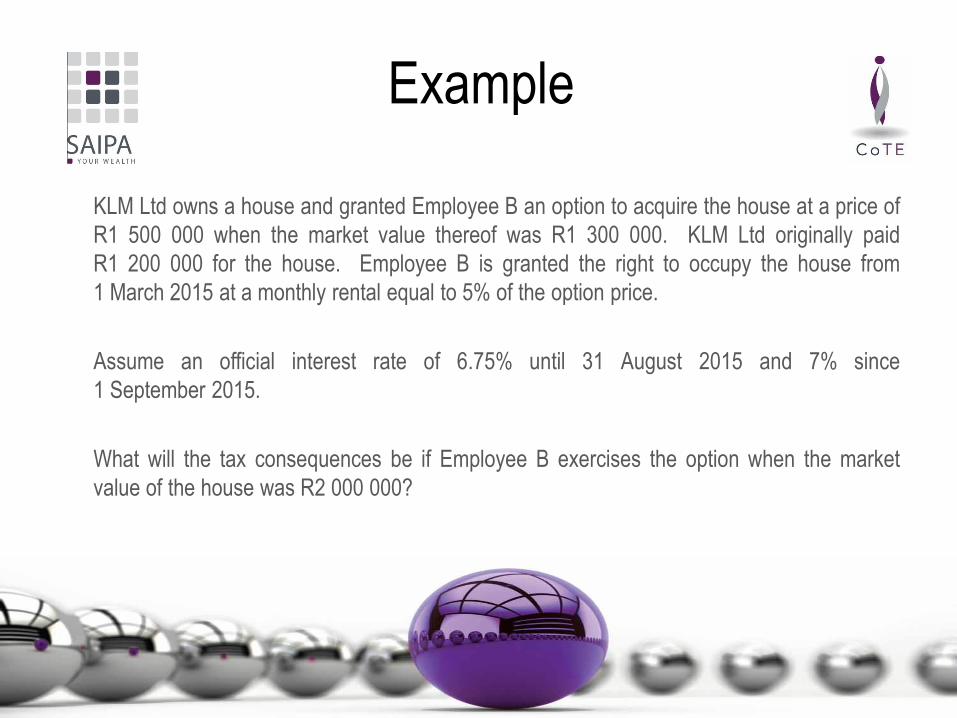

Example

KLM Ltd owns a house and granted Employee B an option to acquire the house at a price of

R1 500 000 when the market value thereof was R1 300 000. KLM Ltd originally paid

R1 200 000 for the house. Employee B is granted the right to occupy the house from

1 March 2015 at a monthly rental equal to 5% of the option price.

Assume an official interest rate of 6.75% until 31 August 2015 and 7% since

1 September 2015.

What will the tax consequences be if Employee B exercises the option when the market

value of the house was R2 000 000?

Solution

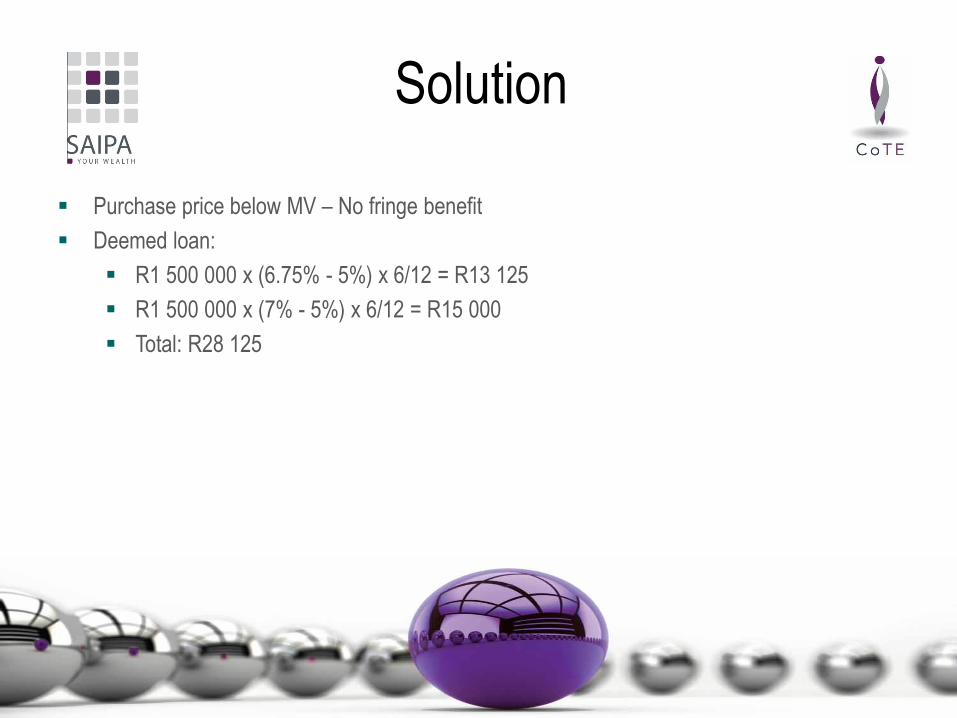

Purchase price below MV – No fringe benefit

Deemed loan:

R1 500 000 x (6.75% - 5%) x 6/12 = R13 125

R1 500 000 x (7% - 5%) x 6/12 = R15 000

Total: R28 125

Discharge of debt

Debt owing to employer or debt owing to a 3rd party

Includes a person who retired from the employ of the employer due to ill health, age or other infirmity

prior to 1 March 1992 and after retirement is released from an obligation that arose before retirement

Exclusions:

Contributions by employer to medical aid

Costs in respect of medical services paid by employer

Calculation: Value of discharge

Deemed discharge if debt prescribes (3 years after becoming payable or claimable) and employer could

have recovered the debt or could have interrupted the running of the discharge

Rnil values

Subscription to professional body that is a requirement of the employment contract

Insurance paid by employer indemnifying employee from negligent acts

Obligation to 1st employer related to bursary or study loan which is settled by the 2nd employer (provided

that the employee has undertaken to work for the 2nd employer for a minimum of the unexpired period

related to the service of the 1st employer)

Contributions to medical

schemes

Value of benefit = value of contribution paid

If contributions are made as lump sums and cannot be specifically attributed to an employee and his/her

dependants: Total contributions .

Total number of employees

Nil value

Person who has retired due to age, ill health or other infirmity

Dependants of deceased employee who was in the employ of the employer at the date of death

Dependants of former employee after his death (provided that the employee retired from the employ due

to age, ill health or other infirmity)

Contributions to retirement

funds

NEW!!! Effective 1 March 2016

Value of fringe benefit

Fund consisting only of defined contribution components: Total contributions paid to pension, provident

and RAF funds

Fund also consisting of other components: X = (A x B) – C

A = fund member category factor of the employee

B = retirement funding income of the employee

C = contributions by the employee (excluding voluntary and buy-back contributions)

Contribution certificate must be provided by the fund to the employer with the abovementioned

calculation

Nil value:

Benefit is for a retired member of the fund; or

Benefit is in respect of dependants or nominees of a deceased member of the fund

Link with VAT

Fringe benefits

Time of supply

Time when the benefit becomes subject to employees tax

Value of supply

Fringe benefit value, except right of use of a motor vehicle

What happens if the fringe benefit has a Rnil value in terms of the Seventh Schedule?

Remember exempt supplies

Examples

Cash allowances?

Long service awards – cash?

Long service awards – assets?

Holiday accommodation?

Low interest rate loan?

Share incentive scheme?

Bursary scheme?

Supply of a motor vehicle at less than market value?

Use of motor vehicle

Determined value is ALWAYS excluding VAT, even if input VAT was denied

15% diminishing value

If input tax deduction was denied

0,3%

If input tax was not denied

0,6%

Employee bears FULL maintenance costs

Deduct cost incurred, limited to R85 per month

MONTHLY!!!

TAX FRACTION!!!

Apportion for taxable use

Example

ABC Ltd is a registered VAT vendor. The CEO of ABC Ltd, Mr. Smith felt that he deservedto drive a luxury vehicle after his recent promotion as CEO. Therefore, ABC Ltd decided tobuy a BMW 325 for Mr. Smith. ABC Ltd bought the BMW from Alberante BMW and paidR399 000 for the vehicle. Mr. Smith will be responsible for all costs relating to themaintenance and repair of the vehicle.

Solution

Determined value = R399 000 x 100/114

= R350 000

“Motor vehicle” as defined Therefore, input tax deduction was denied

Therefore, 0,3%

R350 000 x 0,3% = R1 050

Deduction of R85 p.m.

= R1 050 – R85

= R965

x 2 months (assumption) = R1 930

x 14/114 = R237.02 output VAT (during that VAT period)

x % taxable supplies

Foreign employment exemption

Section 10(1)(o)(ii)

Remuneration received by employee for services rendered outside SA will be exempt, if:

Employee was outside SA > 183 full days during 12 month period; and

Period outside SA includes a continuous period of absence of > 60 full days during the 12 month period; and

Services were rendered during the period of absence from SA; and

Services were rendered for or on behalf of an employer (situated inside or outside SA)

Which remuneration?

What are “days”?

What about a person being in transit through SA?

Applies only to normal tax

QUESTIONS?