Embed Size (px)

Citation preview

Restoring Confidence

2003 Annual Report

The Public Company Accounting Oversight Board isa private-sector, non-profit corporation, created by theSarbanes-Oxley Act of 2002, to oversee the auditors ofpublic companies in order to protect the interests ofinvestors and further the public interest in the prepara-tion of informative, fair, and independent audit reports.

Bill GradisonBoard Member

William J. McDonough Chairman

Kayla J. GillanBoard Member

Charles D. NiemeierBoard Member

Daniel L. GoelzerBoard Member

Public Company Accounting Oversight Board

PAGE 2 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

I am pleased to present the annual report of the PublicCompany Accounting Oversight Board, recounting theaccomplishments of the Board in the first year of operation of this remarkable organization.

What you will read in these pages is the story of the creationof an unparalleled regulatory body, charged by federal law tobuild a system of oversight that had never before existed, entail-ing the registration of public accounting firms, regular inspec-tions of those firms, and provisions for the investigation anddiscipline of accounting firms that betray the public trust intheir audits of publicly traded companies. This new body isrequired by federal law to set the standards that guide the auditsof publicly traded companies and to establish and implementthe funding structure that supports its activities.

The events that led Congress to take the radical step ofordering a new oversight regime for the accounting professionare well known: Beginning with the collapse of Enron in late2001, investors and the American public were beset by a seriesof corporate failures that undermined confidence in U.S. securi-ties markets and pointed to deep flaws in both corporate andregulatory governance.

The role of auditors in those corporate collapses caused theAmerican people and their representatives in Congress to ques-tion—and reject—the existing system for policing of account-ing firms, and the Public Company Accounting OversightBoard was conceived.

The PCAOB became reality on July 30, 2002, when PresidentGeorge W. Bush signed the Sarbanes-Oxley Act into law.

In addition to creating new oversight of auditors of publiccompanies, the Act prescribed specific steps to address specificfailures and codify the responsibilities of corporate executives,corporate directors, lawyers and accountants.

The merits, benefits, cost and wisdom of each of the prescrip-tions continue to fuel debate. But the context for the passage ofthe Sarbanes-Oxley Act, and the President’s signing it into law,cannot be ignored: Corporate leaders and advisors failed. Peoplelost their livelihoods and their life savings. The faith of Americaand the world in U.S. markets was shaken to the core.

To help restore faith in the audits of public companies, the Actfirst required the appointment of the Public Company AccountingOversight Board, comprising five members “who have a demon-strated commitment to the interests of investors and the public.”

I hope that this report on the first year of the PCAOB willleave you with the conviction that not just the Board members,but the entire staff of this new organization have indeed demon-strated their commitment to the interests of investors and thepublic. None of what is described in these pages could havebeen accomplished without the dedication and self-sacrifice of astaff that numbered a mere 25 people a year ago.

You may have noticed the lack of a salutation on my letter.We are a private-sector, nonprofit organization, so addressing“shareholders,” as you might see in the annual report of a publiccompany, would not be appropriate. The law, in fact, requiresthat we submit our annual report to the Securities andExchange Commission, which will then transmit a copy to thecommittees that created the PCAOB in the U.S. Congress.

I thank our colleagues at the SEC and the members ofCongress whose support undergirded our efforts. I believethey would join me in submitting the first annual report of thePCAOB to the people, in the United States and around theworld, who look to U.S. securities markets as a model for fair-ness and reliability. The people will ultimately judge how wellwe at the PCAOB have done our jobs. I humbly submit that wehave done our best to fulfill that awesome responsibility in thisfirst year and that we will continue to do nothing less in theyears to come.

William J. McDonoughChairman and Chief Executive OfficerPublic Company Accounting Oversight BoardWashington, D.C.

June 2004

Letter from the Chairman

PAGE 4 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

With President Bush’s signature on July 30, 2002, theSarbanes-Oxley Act became law, and an unprecedentedoversight organization was created.

The Act established an independent, nonprofit, non-governmental body to oversee the auditors of publiclytraded companies “in order to protect the interests ofinvestors and further the public interest in the preparationof informative, accurate, and independent audit reports.”

To accomplish this mission, the Act gave the new over-sight body four primary responsibilities:• Registration of accounting firms that audit public com-

panies trading in U.S. securities markets;• Inspection of registered accounting firms;• Establishment of standards for auditing, quality control,

ethics, and independence, as well as attestation, for regis-tered accounting firms; and

• Investigation and discipline of registered accountingfirms and their associated persons for violations of law orprofessional standards.The Act required the Securities and Exchange

Commission to select a Board made up of “individuals ofintegrity and reputation who have a demonstrated commit-ment to the interests of investors and the public…”

The Commission named the founding members of theBoard on October 25, 2002.

From then on, it was up to the Board to take all necessaryaction, “including hiring of staff, proposal of rules and adop-tion of initial and transitional auditing and other professionalstandards,” that would enable the SEC to determine that thePCAOB had the capacity to meet the requirements of the Act.

The Act set the deadline for the SEC’s determination atApril 25, 2003. The Act also gives the SEC oversightauthority over the Board. In addition to appointing orremoving members, the SEC, among other things, mustapprove the Board’s budget and rules, including auditingstandards, and may review appeals of adverse Board inspec-tion reports and disciplinary actions against registeredaccounting firms.

With the assistance of a handful of staff members,founding Board members Kayla J. Gillan, Daniel L. Goelzer,Bill Gradison and Charles D. Niemeier opened the doors

of the PCAOB’s first offices on January 6, 2003. The Boardheld its first public meeting on January 9, 2003, where themembers adopted bylaws for the organization and announcedan aggressive campaign to hire the staff that would enablethe Board to fulfill its mission.

At a series of public meetings in March and April, theBoard proposed its rules for the registration of accountingfirms, including non-U.S. firms, adopted interim auditingstandards and related standards for professional practice,proposed its ethics code, and submitted its Fiscal Year 2003budget to the Commission.

In March, the Board also proposed the establishment ofthe accounting support fees that would finance the PCAOB’soperations in future years. These fees, as provided in theAct, are to be paid by publicly traded companies andmutual funds—guaranteeing that the Board’s fundingwould be independent of the accounting profession as well as the federal government.

The Board organized its internal divisions and offices tomatch the responsibilities it was assigned by the Act. TheDivision of Registration and Inspections was charged withbuilding the registry of accounting firms and preparing forinspections of the firms. The Office of the Chief Auditorand Professional Standards was created to advise the Boardon standards-setting. The Division of Enforcement andInvestigations was formed to perform investigations of pos-sible violations of law or professional standards and to rec-ommend to the Board any disciplinary action.

To support the primary functions required by the Act, the Board created other key offices. The Office ofGeneral Counsel was established to provide legal adviceand assist the Board’s rulemaking functions. The Office ofAdministration was given responsibility for three areas that

There is established the Public CompanyAccounting Oversight Board…

Title I, Sec. 101(a), Sarbanes-Oxley Act of 2002

Creation

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 5

would be vital to the Board’s success: information technol-ogy, which developed the technology infrastructure to sup-port all of the Board’s programs, including the Web-basedregistration of accounting firms; human resources, taskedwith hiring the dozens of inspectors and other staff neededto carry out the PCAOB’s work; and the office of finance,which would administer the accounting support fees,among other things.

On April 25, 2003, six months after the foundingBoard had been named, the SEC issued the determinationrequired by the Sarbanes-Oxley Act. The members and staffof the PCAOB had demonstrated that they could fulfill theresponsibilities of the Sarbanes-Oxley Act.

On May 21, 2003, the SEC unanimously approved the appointment of William J. McDonough as Chairmanof the PCAOB.

The Board and the staff aggressively addressed the nextdeadline imposed by the Sarbanes-Oxley Act: the registrationof public accounting firms. Under the Act and the Board’srules, after October 22, 2003, only registered U.S. accountingfirms could audit or substantially participate in the audit of apublicly traded company. Through the summer of 2003, theBoard’s information technology team completed the construc-tion of the Web-based system for registration. The SECapproved the Board’s rules and form for registration onJuly 16, 2003. Registration applications were available on-line beginning July 17, and by October 22, the Board hadapproved the registration of 598 firms. Applications continuedto arrive after the October 22 deadline, and by December 31,the Board had approved the registration of 735 firms.

The Act requires a continuing program of inspections ofregistered public accounting firms that audit public compa-nies. In mid-2003, even though the largest firms were notyet registered, the Board launched limited inspections ofthose four firms in the belief that investors and the publicwould best be served by immediate inspections to helprestore investor confidence in public company auditing.After seeking and considering public comment, onOctober 7, 2003, the Board adopted the rules that wouldguide the inspections of all registered accounting firms—annual inspections for firms with more than 100 public

company clients and inspections no less frequently thanevery three years for other firms—as well as special inspec-tions. To accomplish the inspections, the Board opened anoffice in New York in September 2003 and began hiringstaff for additional offices near Atlanta, Dallas, and SanFrancisco. The Board paid close attention to hiring a cadreof experienced auditors to conduct the inspections, and byyear’s end, the PCAOB inspection staff had grown to 60.

While registration and limited inspections were underway, the Board, through its Office of the Chief Auditor andProfessional Standards, began addressing the momentoustask of developing standards for the audits of publiclytraded companies. The Board held two roundtable discus-sions with investors, issuers, and auditors to discuss stan-dards for audits of internal control and audit documentation,and it adopted rules for the establishment of a standingadvisory group to provide guidance on standards-setting.On October 7, 2003, the Board proposed the most com-plex standard required under the Sarbanes-Oxley Act: thestandard for auditors’ attestation to management’s assess-ment of internal control over financial reporting.

The proposal of the internal control standard was one ofalmost a dozen rulemaking actions taken by the Board inthe last half of 2003. The Board also proposed or adoptedrules for inspections of accounting firms, for investigationsand adjudication, and for oversight of non-U.S. accountingfirms that audit U.S. public companies.

During the year, the Board also established offices ofpublic affairs and government relations to assist the Boardin communications with the public, Congress, and thenews media. The Board also hired an international affairsstaff to advise the Board on international issues and facili-tate dialogue with foreign regulators regarding oversight ofregistered non-U.S. accounting firms. The Board also beganhiring the staff for investigations and enforcement.

Four Board members and a handful of staff membershad opened the doors to the organization’s first office onJanuary 6. By December 31, the organization was 118strong. The Public Company Accounting Oversight Boardwas well established and well on its way to fulfilling its statu-tory duties to investors and the public.

PAGE 6 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

Before the Sarbanes-Oxley Act of 2002, the accountingprofession largely operated outside the purview ofnational oversight. Individual accountants were subjectto the education and certification requirements of thestates in which they practiced, and accounting firmsvoluntarily participated in self-regulation through anational professional organization. Federal securities lawsset certain requirements for and limits on the work ofauditors of publicly traded companies, but none of thefederal or state regulations approached the regime ofoversight set out by the Sarbanes-Oxley Act.

The requirements of the Act compelled the PublicCompany Accounting Oversight Board to constructan unprecedented registry of domestic and non-U.S.accounting firms that audit, or play a substantial rolein the audits of, public companies and mutual funds.With registration, accounting firms become subject to the Board’s inspections, auditing standards andenforcement authority.

The Board proposed its rules for the registration ofpublic accounting firms on March 4, 2003—just twomonths after the Board began operations. The pro-posed rules sought the information required of suchfirms under the Sarbanes-Oxley Act, including:• The names of all issuers for which the firm prepared

or issued audit reports during the immediately pre-ceding calendar year, and for which the firm expectsto prepare or issue audit reports during the currentcalendar year.

• The annual fees received by the firm from eachissuer for audit services, other accounting servicesand non-audit services, respectively.

• A statement of the quality control policies of thefirm for its accounting and auditing practices.

• A list of all accountants associated with the firm whoparticipate in or contribute to the preparation ofaudit reports.

• Information relating to relevant criminal, civil, oradministrative actions or disciplinary proceedingspending against the firm or any associated person of the firm.

The Board, in its proposed rules, sought a limitedamount of supplemental information to assist it in mak-ing registration decisions. After considering the commentsit received, the Board adopted a final rule for registrationof accounting firms on April 23, 2003, and the rule wasapproved by the SEC on July 16, 2003.

The rules, in keeping with the Act, require the regis-tration of both U.S. and non-U.S. accounting firmsthat audit or play a substantial role in the audits ofcompanies trading in U.S. markets. The Board wassensitive to the special concerns of foreign accountingfirms and solicited a public roundtable discussion withnon-U.S. government representatives and other inter-ested persons on March 31, 2003. As a result, theBoard provided certain accommodations in the regis-tration process for foreign firms, including giving thosefirms additional time to register, ultimately setting thedeadline for July 19, 2004.

Building the Registration SystemBecause of the importance of registration to theBoard’s oversight responsibilities, the Board chose tobuild the registration system and not outsource theregistration function.

The Board recruited a team of experienced informa-tion-technology specialists who, working with the Board’sregistration and inspections staff, designed the Web-basedsystem that would capture the information requiredfrom registration applicants while both protecting theconfidentiality of the information and giving theBoard’s staff the ability to efficiently examine and analyze the information.

[I]t shall be unlawful for any person that is not a registered public accounting firm to prepare or issue,or to participate in the preparation or issuance of, any audit report with respect to any issuer.

—Title I, Sec. 102(a), Sarbanes-Oxley Act of 2002

Registration

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 7

Work on the system began early in 2003, and it wasready for launch the day after the SEC approved theBoard’s registration rules.

The Board began accepting applications and fees inearly August 2003 and made the names of applicantsavailable to the public through its Web site beginning

August 27. The Act and the Board’s rules give theBoard a 45-day period to review each application, afterwhich the Board is required to approve the application,provide the applicant with a notice of a hearing todetermine whether the application should be approvedor disapproved, or request more information from theapplicant, triggering another 45-day review period.

Evaluating ApplicationsIn early September, the Board began consideringapplications. The Board reviewed, among other things,legal and disciplinary proceedings against the applicantfirms, the firms’ descriptions of their quality-controlpolicies, the number and nature of audit clients,staffing levels, and any reported disagreements withclients. The decision on each applicant was based on asingle consideration: is registration of this accountingfirm consistent with the Board’s responsibilities toprotect investors and to further the public interest inthe preparation of informative, fair and independentaudit reports?

By the statutory deadline of October 22, the Boardhad answered the question affirmatively for 598 publicaccounting firms, including the four largest U.S. firms.The Board made the names of the registered firmsavailable to the public through its Web site to enablepublic companies and mutual funds to confirm thattheir auditors were registered as required by law. Theapplications will be made public after requests for con-fidential treatment of certain information in the appli-cations are evaluated.

Registration applications continued to be filedafter October 22, and the Board and staff continuedthe process of reviewing and considering the applica-tions. By December 31, 735 firms were registeredwith the PCAOB.

The Board’s rules also provide for hearings on reg-istration applications. If the Board is unable to determinethat a public accounting firm’s application has met thestandard for approval, the Board may provide the firmwith a notice of a hearing, which the firm may electto treat as a written notice of disapproval that can be appealed directly to the Securities and ExchangeCommission. Alternatively, a firm may request a hearing by the Board.

The Board’s rules also set out procedures for firmsto withdraw from registration. Withdrawal is notautomatic. The Board may order that withdrawal bedelayed, for up to 18 months, while the Board carriesout a relevant inspection, investigation, or discipli-nary proceeding.

The Act compelled the Public CompanyAccounting Oversight Board to constructan unprecedented registry of domestic andnon-U.S. accounting firms that audit, orplay a substantial role in the audits of, public companies and mutual funds.

Registered Firms by Number of Clients

Number of Fee for Number of firmsissuer clients registration registered in 2003

0 . . . . . . . . . . . . . $ 250 . . . . . . . . . . . 1411–49 . . . . . . . . . $ 500 . . . . . . . . . . . 57950–100 . . . . . . . $ 3,000 . . . . . . . . . . . . . 7101–1,000 . . . . . $ 29,000 . . . . . . . . . . . . . 41,001+ . . . . . . . . $390,000 . . . . . . . . . . . . . 4

PAGE 8 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

The inspection of registered accounting firms carries thepotential for real-time improvement in the audits ofpublic companies and will require the largest commit-ment of the Board’s human and monetary resources.

This powerful tool gives the Board access to criti-cal information relating to audit quality, ranging fromcompetence and methodology to judgment and integrity.Inspections will provide insight into the registeredfirms’ audit practices to see how firms implementapplicable auditing and related professional practicestandards, how they comply with applica-ble laws and rules, where they are doingwell, and where improvements areneeded. The inspection process will allowthe Board to assess all of these thingsand, when necessary, to apply pressure toimprove a firm’s audit practices.

The Sarbanes-Oxley Act requires theBoard to conduct annual inspections ofregistered accounting firms that audit morethan 100 public companies. Eight suchfirms were registered with the PCAOB asof December 31. Other firms that audit, orplay a substantial role in the audit of, anypublic companies are required to beinspected at least once every three years.The Board also has the authority to con-duct special inspections as is necessary or appropriateto address issues that come to the Board’s attention.

At the end of each inspection, the Board will issuea report of its findings, including criticisms of, anddescriptions of potential defects in, the firm’s qualitycontrol systems. The Act requires the Board to keepnonpublic any criticisms and potential defects unlessthe firm fails to correct them within 12 months.

The Board proposed its rules for inspections at apublic meeting on July 28, 2003. After considering pub-lic comment, the Board adopted the inspection rules onOctober 7, 2003. The rules create a procedural frame-work for the conduct of the Board’s inspection program.

The Board also determined that conducting limitedinspections of the four largest firms would provide animportant foundation for the full-scale inspections tocome. Accordingly, the Board developed inspection pro-cedures and conducted initial limited inspections of thefour largest public accounting firms in the United Stateswith the firms’ consent.

These initial limited inspections focused on areas thathave not been the traditional focus of the auditing pro-fession’s own peer review process, including “tone at the

top” and partner evaluation, compensation, and promo-tion. The Board’s inspectors also looked at how thesefirms performed selected audit engagements. The lim-ited inspection procedures carved the path for theBoard’s comprehensive inspections program, which theBoard will fully launch in 2004.

The fieldwork for the 2004 inspections will be con-ducted from approximately May to November 2004. Inconnection with these inspections, the Board will focuson, among other things, efforts to detect fraud, the ade-quacy of documentation, the evaluation of firm riskassessments, and compliance with professional stan-dards. The Board also expects to continue its focus on

The Board shall conduct a continuing programof inspections to assess the degree of complianceof each registered public accounting firm andassociated persons of that firm with this Act, therules of the Board, the rules of the Commission,or professional standards, in connection with itsperformance of audits, issuance of audit reports,and related matters involving issuers.

—Title I, Sec. 104(a), Sarbanes-Oxley Act of 2002

Inspections

“tone at the top,” compensation practices, and otherbusiness practices that were the subject of limited proce-dures in 2003.

To help carry out its inspection program, the Boardopened an office in New York in September 2003 andbegan hiring staff for additional offices near Atlanta,Dallas, and San Francisco. The Board recruited a cadreof experienced public company auditors to conduct theinspections, and by year’s end, the PCAOB inspectionstaff had grown to 60. The Board expects to more thandouble its inspection staff by the end of 2004 in orderto carry out its statutory mandate.

The Board’s inspection teams are composed ofaccountants, who have an average of 12 years of audit-ing experience. Each team is led by an AssociateDirector or a Deputy Director of the Board’s Divisionof Registration and Inspections, who are generally for-mer partner-level employees of the major accountingfirms and have an average of 22 years of auditing expe-rience. The Board’s ability to implement meaningfuland robust inspections is a direct reflection of its inspec-tions teams’ high caliber, experience, and commitment.

The Board’s statutory responsibilities extend to non-U.S. accounting firms that perform audit services forU.S. public companies or for non-U.S. issuers who areregistered, and file reports, with the SEC. Accordingly,the Board’s inspection program will encompass firmsoutside of the United States. As a result of a dialoguewith its foreign counterparts and as part of a coopera-tive approach to the oversight of non-U.S. registered

firms, the Board proposed a rule that would permit theBoard to rely on the work of oversight systems in otherjurisdictions, to an appropriate degree, on a case-by-casebasis. In 2004, the Board will continue its dialogue withregulators in other countries in order to develop workprograms for the inspections of non-U.S. firms.

Initial limited inspections focused on areas that have not beenthe traditional focus of the auditing profession’s own peer reviewprocess, including “tone at the top” and partner evaluation,compensation, and promotion.

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 9

Number of Issuers per Registered Firm

Registered firms (2003) Issuer clients

8 . . . . . . . . . . . . . . . . . . . . . . . . . 100 or more5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51–10022 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26–5060. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11–2577. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6–10563 . . . . . . . . . . . . . . . . . . . . . . . . . 5 or fewer

PAGE 10 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

The Sarbanes-Oxley Act gives the Public CompanyAccounting Oversight Board considerable leeway in thedesign and adoption of standards for audits and profes-sional conduct by auditors. Among other things, itauthorizes, but does not require, the Board to designatea professional group of accountants to propose stan-dards to the Board.

Early in 2003, the Board determined that it couldbest fulfill its mandate for the protection of investors bydeveloping standards itself, with the assistance of a staffof highly qualified accountants recruited from acade-mia, professional practice, and government.

As a result of the Board’s decision, for the first time,the individuals developing auditing standards will haveaccess to robust empirical and anecdotal evidence fromthe Board’s inspections and enforcement activities—evidence that will cut through a cross-section of auditsand firms—to assist in setting priorities and developingnew standards.

The Act and the Board’s rules require registered publicaccounting firms to adhere to the Board’s auditing (andrelated attestation), quality control, and ethics standards,as well as its independence rules. Any registered account-ing firm that fails to adhere to applicable standards maybe subject to Board discipline.

New auditing standards will be established—andexisting standards will be changed—only by Board rule-making. While the Board will consider proposed new oramended auditing standards recommended to it by oth-ers, no such proposed rule will become a standard of theBoard unless adopted by the Board through rulemaking.

The Board will also rely on advice from a standingadvisory group to assist it in performing its standards-setting responsibilities. The Board also intends to solicitpublic comment, and, where appropriate, to convenehearings or roundtable meetings in order to obtain theviews of issuers, accountants, investors, and other inter-ested persons with respect to proposed auditing standards.In this regard, the Board welcomes input and advice fromestablished professional bodies and includes practicingaccountants among the members of its advisory groups.

Interim Auditing StandardsOn April 16, 2003, the Board adopted certain existingstandards as its interim auditing standards. Most of thesestandards were promulgated by the American Instituteof Certified Public Accountants and pre-date the Board’sformation. These interim standards are incorporatedinto the Board’s rules. Registered public accountingfirms are subject to the same obligation to comply withthe interim standards while they are in effect as with per-manent standards adopted by the Board.

Despite the need to adopt these existing standards inorder to assure continuity and certainty in the standardsthat govern audits of public companies, the Board hasnot determined whether it would be appropriate toinclude any of the interim auditing standards as perma-nent Board standards.

The Board will be mindful of the need to adoptnew auditing standards, especially in response toemerging issues and problems that arise in connectionwith audits of issuers.

The Board shall, by rule, establish…suchauditing and related attestation standards,such quality control standards, and suchethics standards to be used by registered pub-lic accounting firms in the preparation andissuance of audit reports, as required by thisAct or the rules of the Commission, or asmay be necessary or appropriate in the publicinterest or for the protection of investors.

—Title I, Sec. 103(a), Sarbanes-Oxley Act of 2002

Auditing Standards

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 11

Audits of Internal Control over Financial ReportingIn 2003, the Board also set out to fulfill other provi-sions of the Act that require the Board to adopt stan-dards in specific areas. The most complex of therequired auditing standards related to an auditor’sresponsibility in regard to a public company’s internalcontrol over financial reporting.

The Sarbanes-Oxley Act, in Section 404, requirescompany management to assess and report on thecompany’s internal control over financial reporting. Italso requires a company’s independent, outside audi-tors to issue an “attestation” to management’s assess-ment—in other words, to provide shareholders andthe public at large with an independent reason to relyon management’s description of the company’s inter-nal control over financial reporting.

The Board convened a public roundtable discus-sion on July 29, 2003, to discuss issues and hearviews related to reporting on internal control. Theparticipants included representatives from publiccompanies, accounting firms, investor groups, andregulatory organizations.

After considering comments made at the round-table, advice from the Board’s staff, and other input, the

Board developed and issued, on October 7, 2003, aproposed auditing standard titled “An Audit of InternalControl over Financial Reporting Performed inConjunction with an Audit of Financial Statements.”

The Board received 194 comment letters from avariety of interested parties, including auditors,investors, internal auditors, issuers, regulators, andothers on a broad array of topics.

The final standard for audits of internal control,adopted by the Board on March 9, 2004, incorpo-rated certain suggested changes and reflected certainbasic principles on which the Board members agreed:• Audit quality would be best improved by integrat-

ing the auditor’s examination of internal controlinto the audit of a company’s financial statements.

• The costs of an audit of internal control must be reasonable, particularly for small and medium-sized companies.

• Outside auditors may rely on the work of internalauditors and others, based on their competencyand objectivity.

• An assessment of the effectiveness of a company’saudit committee is a vital part of an audit of inter-nal control and consistent with existing standards.

Audit DocumentationThe Act directs the Board to adopt a standard requir-ing registered public accounting firms to prepare, andmaintain for a period of not less than seven years,audit work papers, and other information related toany audit report, in sufficient detail to support theconclusions reached in such report.

The Board sought expert advice on the standardfrom auditors, regulators, investors, and issuers duringa roundtable discussion on September 29, 2003, andproposed its standard for audit documentation onNovember 12, 2003.

The standard will be one of the fundamentalbuilding blocks on which both the integrity of auditsand the Board’s oversight will rest. The integrity ofthe audit depends in large part on the existence of a

For the first time, the individuals developing auditing standards will haveaccess to robust empirical and anecdotalevidence from the Board’s inspectionsand enforcement activities—evidencethat will cut through a cross-section ofaudits and firms—to assist in setting priorities and developing new standards.

PAGE 12 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

complete and understandable record of the work thatthe auditor performed, of the conclusions that theauditor reached, and of the evidence that supportsthose conclusions. Meaningful review by a secondpartner, or by the Board in the context of its inspec-tions, would be difficult or impossible without ade-quate documentation. Clear and comprehensive auditdocumentation is essential in order to enhance thequality of the audit and for the Board to fulfill itsmandate to inspect registered public accounting firms“to assess the degree of compliance” of those firmswith applicable standards and laws.

The standard would establish general requirementsfor documentation that the auditor should prepareand retain in connection with issuing an audit reporton the financial statements of a public company. The

standard would also set a new requirement that auditdocumentation must contain sufficient information toenable an experienced auditor, having no previousconnection with the engagement, to understand thework that was performed, who performed it, when itwas completed, and the conclusions reached.

Auditing Standard No. 1—References to PCAOB StandardsOn December 17, 2003, the Board adopted AuditingStandard No. 1, requiring registered public account-ing firms to include in their reports on the financialstatements of public companies a statement that theengagement was conducted in accordance with “the

standards of the Public Company AccountingOversight Board (United States).” The standardsupersedes previous standards that required referencesto “generally accepted auditing standards,” “U.S. gen-erally accepted auditing standards,” “auditing stan-dards generally accepted in the United States ofAmerica,” and “standards established by the AICPA.”The standard was approved by the Securities andExchange Commission on May 14, 2004, and becameeffective on May 24, 2004.

Advisory Groups and Task ForcesThe Act provides that the Board shall “convene, orauthorize its staff to convene, such expert advisorygroups as may be appropriate… to make recommen-dations concerning the content (including proposed

drafts) of auditing, quality control,ethics, independence, or otherstandards required to be estab-lished under this section.”

On June 30, 2003, the Boardadopted a rule describing its inten-tion to convene a standing advi-sory group to participate in thestandards-setting process. Theadvisory group will assist theBoard in reviewing existing audit-

ing standards, in formulating new or amended stan-dards, and in evaluating proposed standards suggestedby other persons. The Board may, based on the cir-cumstances of particular projects, form ad hoc taskforces composed of smaller groups of members of theadvisory group, of the Board’s staff, and other persons.

The Board began soliciting nominees for mem-bership in the standing advisory group in November2003 and received more than 170 nominations. TheBoard named the members of the standing advisorygroup in April 2004—30 individuals with a varietyof perspectives, including practicing auditors, pre-parers of financial statements, the investor commu-nity, academia, and others.

Auditing Standards(CONTINUED)

The standard for audit documentation will be one of the fundamental buildingblocks on which both the integrity of audits and the Board’s oversight will rest.

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 13

Each member of the advisory group has expertise inat least one of the following areas: public companyaccounting; public company auditing; public companyfinance; public company governance; investing in pub-lic companies; or other disciplines that the Board deemsto be relevant.

The members of the advisory group will serve in theirindividual capacities and may not delegate their duties asadvisory group members, including attendance at meet-ings. Advisory group members are also subject to certain

provisions of the Board’s Ethics Code, including provi-sions designed to protect nonpublic information andavoid conflicts of interest.

The European Commission recently proposed thatfinancial statement audits in the European Union shouldbe conducted in accordance with International Standardson Auditing, as developed by the International Auditingand Assurance Standards Board (the IAASB) and to theextent endorsed by the European Commission. In 2003,the Board accepted an invitation to observe, with speak-ing rights, the meetings of the IAASB. Similarly, theBoard invited the IAASB to participate as observers inthe standing advisory group. Although not an explicitobjective of the Board, the Board supports the develop-ment of high-quality international professional standards.

Future Standards-SettingWhile the Board has made significant strides its firstyear in crafting a process for setting standards in thepublic interest and in proposing and adopting certainof those standards, it still faces a challenging futureagenda. Among the issues that the Board, its staff, andthe standing advisory group expect to discuss in thecoming year are:• Reviews of existing, interim standards;• Revision to the hierarchy for generally accepted

auditing standards—to incorporate PCAOB audit-ing and related professional practice standards;

• Concurring or second partner review—to ensure allpublic company audits include a review by a secondpartner, and

• Communications and relations with audit commit-tees—to incorporate requirements mandated underthe Sarbanes-Oxley Act into the audit and relatedprofessional practice standards.In addition, the Board is considering projects related

to the quality control and independence standards,which Congress specifically addressed in the Sarbanes-Oxley Act.

The standing advisory group comprises 30 individuals with a variety of perspectives,including practicing auditors, preparers of financial statements, the investor community, academia, and others.

PAGE 14 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

The ability to impose disciplinary measures onerrant accounting firms and auditors is one of thestrongest tools given to the Board for the protectionof investors. The Board is empowered to imposepenalties as harsh as revocation of a firm’s registra-tion—effectively barring the firm from auditingpublicly traded companies—and monetary penal-ties of as much as $15 million per offense.

In September 2003, the Board laid the ground-work for its enforcement program by adoptingdetailed rules to govern its investigative and discipli-nary processes and to provide fair procedures for theconduct of investigations, the conduct of hearings,and the imposition and termination of sanctions. Therules were approved by the Securities and ExchangeCommission on May 14, 2004.

The overall objective of the Board’s enforcementprogram is to promote improvements in the qualityof public company auditing by taking remedial anddisciplinary measures with respect to—or, whereappropriate, barring—registered accounting firmsand associated persons that have failed to complywith the Sarbanes-Oxley Act, the rules of theBoard, and the rules of the Securities and ExchangeCommission relating to the preparation and issuanceof audit reports or professional standards.

When a violation of those rules or standards isconfirmed, the Board will impose sanctions intendedto prevent a repetition of the violation and to enhancethe quality and reliability of future audits.

The Board will implement its enforcement pro-gram with an emphasis on three important criteria: • Speed. The Board believes it is important that it

promptly and efficiently investigate significantinstances of apparent audit failure. Prompt inves-tigation will help shore up investor confidence.

• Fairness. The Board is committed to the principlethat persons charged with violations should have afull and fair opportunity to present relevant evi-dence and arguments in their defense before anyfinal determination is made.

• Thoroughness. Disciplinary proceedings should be based on a comprehensive assessment of the relevant facts.

The Act and the Board’s rules require registeredpublic accounting firms and their associated personsto cooperate with Board investigations. The Actand the Board’s rules also permit the Board to seekinformation from other persons, including clients ofregistered firms and, should those persons not com-ply, to seek issuance of a Securities and ExchangeCommission subpoena for the information.

As part of the cooperative approach to the over-sight of non-U.S. accounting firms, the Board hasproposed a rule that would allow the Board, undercertain circumstances, to rely on the investigation ora sanction of a non-U.S. oversight authority.

The Board shall establish…fair proceduresfor the investigation and disciplining ofregistered public accounting firms andassociated persons of such firms.

—Title I, Sec. 105(a), Sarbanes-Oxley Act of 2002

Enforcement & Investigations

The year 2003 was the initial operating year for thePublic Company Accounting Oversight Board. Thefinancial statements reflect significant investments intechnology and hiring necessary for the Board to imple-ment its mission to protect the interests of investors andfurther the public interest in the preparation of informa-tive, fair, and independent audit reports.

Each year, the PCAOB develops an operating budgetthat must be approved by the Securities and ExchangeCommission, as required by the Sarbanes-Oxley Act of2002. On April 23, 2003, the Board adopted a 2003budget of $68 million, which was approved by the SECon August 1, 2003.

The Board’s start-up expenses were covered byadvances from the Department of the Treasury, asauthorized by the Act. The advances, drawn over thefirst eight months of the year, totaled $20,342,000 andwere repaid in full on September 22, 2003, from theproceeds of the 2003 accounting support fees.

OPERATING REVENUEThe Act provides that the Board be funded by account-ing support fees assessed on issuers as defined in the Act.The Board adopted rules for the allocation, assessment,and collection of accounting support fees on April 16,2003, and the rules were approved by the SEC onAugust 1, 2003.

The accounting support fees or “fees from issuers,”as reflected in the financial statements, are equal to theBoard’s budget for the fiscal year in which they are set,less the amount of fees received from public accountingfirms to cover the cost of processing and reviewing regis-tration applications.

Under the Act and the Board’s rules, the annualaccounting support fees are based on the averagemonthly U.S. equity market capitalization of publiclytraded companies, investment companies, and otherequity issuers. However, issuers with average marketcapitalization of less than $25 million and investmentcompanies with net asset values of less than $250 mil-lion are exempt from the fees.

The Board issued invoices to approximately 8,500issuers beginning in early August 2003. The Board col-lected approximately $51 million in accounting sup-port fees. Approximately 62 percent of the issuersreceived invoices for $1,000 or less, and the largest1,000 issuers received invoices for about 87 percent of the total fees.

Combined, publicly traded companies contributedabout 95 percent of the total fees paid, while open-endmutual funds provided about 4.7 percent, and otherinvestment companies paid the remainder.

Another source of revenue is the registration of pub-lic accounting firms that audit public companies. Thisis reflected as “fees from registering accounting firms” inthe financial statements. These amounts are not used tofund the Board’s operations but to recover the costs ofprocessing and reviewing the registration applications.During 2003, the PCAOB registered 735 public account-ing firms. Each applicant paid a registration fee to theBoard based on the number of issuers the firm auditedin the preceding calendar year. The total amount col-lected from registration applicants in 2003 was approxi-mately $2 million.

Financial ReviewPublic Company Accounting Oversight Board

Year Ended December 31, 2003

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 15

Assessment of Accounting Support Fees for 2003Fee Number of issuers

$100–500 . . . . . . . . . . . . . . . . . . . . . . . . . . 4,244$501–1,000 . . . . . . . . . . . . . . . . . . . . . . . . . 1,094$1,001–5,000 . . . . . . . . . . . . . . . . . . . . . . . 1,911$5,001–10,000 . . . . . . . . . . . . . . . . . . . . . . . . 472$10,001–50,000. . . . . . . . . . . . . . . . . . . . . . . 536$50,001–100,000. . . . . . . . . . . . . . . . . . . . . . . 75$100,001–500,000. . . . . . . . . . . . . . . . . . . . . . 80$500,001–1,000,000 . . . . . . . . . . . . . . . . . . . . . 8$1,000,001+ . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Total. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,424

PAGE 16 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

STATEMENT OF FINANCIAL POSITIONThe PCAOB financial statements have been preparedin accordance with U.S. generally accepted accountingprinciples and are presented pursuant to Statement ofFinancial Accounting Standards No. 117, FinancialStatements of Not-for-Profit Organizations (SFAS No. 117). In accordance with SFAS No. 117, the netassets of the PCAOB are not subject to restrictionsand therefore all have been classified as unrestricted in the financial statements. The PCAOB’s unrestrictednet assets primarily consist of its investments in tech-nology and amounts to fund operations in the subse-quent year prior to collection of that year’s accountingsupport fees.

Cash and cash equivalents include demand depositswith financial institutions and short-term, highly liquidinvestments. The PCAOB utilizes a sweep service froma financial institution to invest daily in overnight repur-chase agreements, typically in U.S. Treasury or Agencyissues. Cash and cash equivalents also include approxi-mately $300,000 of cash collected on behalf of theFinancial Accounting Standards Board (FASB). A corre-sponding amount of approximately $300,000 is includedin accounts payable and other liabilities for amountsdue to the FASB. The Financial Accounting Foundation(FAF) designated the PCAOB as the collection agentfor invoicing and collection of the 2003 FASB account-ing support fees, as authorized by the Sarbanes-OxleyAct. In August 2003, the PCAOB issued invoices foraccounting support fees of approximately $25 millionon FASB’s behalf. The PCAOB earned and was paidapproximately $210,000 for acting as FASB’s collectionagent in 2003.

Accounts receivable of approximately $2.2 millionare almost entirely related to outstanding accountingsupport fees. As of year end, $567,000 of these fees

remained uncollected. Roughly $1.4 million of theaccounts receivable balance represents amounts duefrom approximately 430 issuers of American DepositaryReceipts that were assessed incorrect accounting supportfees due to errors in the market capitalization figuresused to calculate their fees. The PCAOB withdrew theinitial invoices on August 27, 2003, and issued newinvoices as part of the billing cycle for the 2004accounting support fee. Because the fees originallyassessed to the 430 issuers were higher than they shouldhave been, the errors effectively reduced the PCAOB’s2003 anticipated revenue by approximately $15.5 mil-lion and had the effect of reducing the share of theaccounting support fee billed to and collected from allother issuers subject to the fee by that amount.

During 2003, the PCAOB invested approximately$19.1 million in furniture and equipment, leaseholdimprovements, and information technology to build theinfrastructure of the organization. The PCAOB estab-lished its headquarters in Washington, D.C., a regionaloffice in New York City, and a Northern Virginia officefor its information technology group.

The investment in information technologyincluded the design, development, and implementa-tion of two proprietary software systems in 2003. ThePCAOB invested approximately $3.6 million todevelop a Web-based system for the registration ofpublic accounting firms. The PCAOB also investedapproximately $1.9 million to develop a system todetermine and calculate accounting support fees. Foreach proprietary system, the Board considered thecosts and benefits of making or buying the system, tak-ing into account the cost, technology, use, and security.In each instance, the Board found that the benefits ofbuilding the system in-house outweighed the benefitsof utilizing an existing system.

Financial Review (continued)Public Company Accounting Oversight Board

Year Ended December 31, 2003

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 17

OPERATING EXPENSESProgram ActivitiesThe Sarbanes-Oxley Act gives the PCAOB four pri-mary responsibilities to carry out its mission: registra-tion, inspections, standards-setting, and enforcement.These responsibilities represent the program activitiesfor the Board as reflected in the financial statements.Costs associated with these programs include salaries,benefits, and other direct operating expenses relatingto the specific activity.

Supporting ActivitiesSupporting activities made up a significant percentageof the PCAOB’s 2003 operating expenses as a result of the need to establish a corporate infrastructure to sup-port the Board’s program activities. The supportingactivities include the offices of the Board members andtheir staffs, the General Counsel’s Office, Public Affairs,Government Relations, Finance, Human Resources,and Administration. The majority of these offices wereoperational for the better part of the year. Also includedin supporting activities are costs relating to informationtechnology operating costs for system maintenance, net-work support, and depreciation of information technol-ogy equipment. At year end, the PCAOB had 118full-time employees.

Financial Review (continued)Public Company Accounting Oversight Board

Year Ended December 31, 2003

PAGE 18 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

AssetsCash and cash equivalents (Note 2) $14,984,233Accounts receivable, less allowance for doubtful accounts of $51,270 2,193,903Prepaid expenses and other assets 635,420Furniture and equipment, leasehold improvements and technology, net (Note 3) 16,430,878

Total Assets $34,244,434

Liabilities and Net Assets

LiabilitiesAccounts payable and other liabilities $ 5,417,498Deferred rent (Note 4) 3,028,134

Total Liabilities 8,445,632

Net AssetsUnrestricted 25,798,802

Total Net Assets 25,798,802

Total Liabilities and Net Assets $34,244,434

The accompanying notes are an integral part of these financial statements.

Statement of Financial PositionPublic Company Accounting Oversight Board

December 31, 2003

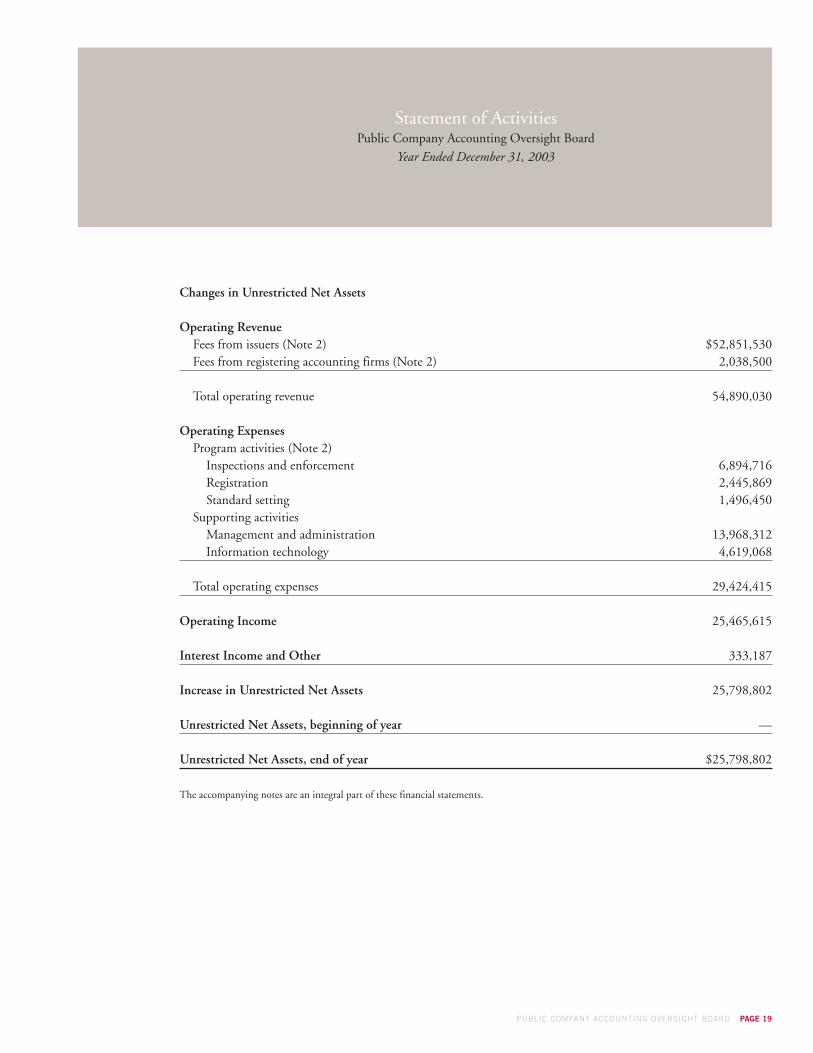

Changes in Unrestricted Net Assets

Operating RevenueFees from issuers (Note 2) $52,851,530Fees from registering accounting firms (Note 2) 2,038,500

Total operating revenue 54,890,030

Operating ExpensesProgram activities (Note 2)

Inspections and enforcement 6,894,716Registration 2,445,869Standard setting 1,496,450

Supporting activitiesManagement and administration 13,968,312Information technology 4,619,068

Total operating expenses 29,424,415

Operating Income 25,465,615

Interest Income and Other 333,187

Increase in Unrestricted Net Assets 25,798,802

Unrestricted Net Assets, beginning of year —

Unrestricted Net Assets, end of year $25,798,802

The accompanying notes are an integral part of these financial statements.

Statement of ActivitiesPublic Company Accounting Oversight Board

Year Ended December 31, 2003

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 19

PAGE 20 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

Cash Flows from Operating ActivitiesCash received from issuers $ 50,895,673Cash received from registering accounting firms 2,032,250Interest income and other 333,187Cash paid to suppliers and employees (19,177,792)

Net cash provided by operating activities 34,083,318

Cash Flows from Investing ActivitiesPurchases of furniture and equipment, leasehold improvements and technology (19,099,085)

Cash Flows from Financing ActivitiesAdvances 20,342,000Repayment of advances (20,342,000)

Net cash provided by (used in) financing activities —

Net Increase in Cash 14,984,233

Cash and Cash Equivalents, beginning of year —

Cash and Cash Equivalents, end of year $ 14,984,233

Reconciliation of Net Income to Net Cash Provided by Operating Activities:

Increase in Unrestricted Net Assets $ 25,798,802Reconciliation Adjustments

Depreciation and amortization 2,668,207Provision for losses on accounts receivable 51,270Increase in receivables from issuers and registering accounting firms (2,245,173)Increase in prepaid expenses (635,420)Increase in accounts payable, accrued expenses and employee benefit accruals 5,417,498Increase in deferred rent 3,028,134

Net Cash Provided by Operating Activities $ 34,083,318

The accompanying notes are an integral part of these financial statements.

Statement of Cash FlowsPublic Company Accounting Oversight Board

Year Ended December 31, 2003

Notes to the Financial StatementsPublic Company Accounting Oversight Board

Year Ended December 31, 2003

NOTE 1. NATURE OF ACTIVITIESThe Public Company Accounting Oversight Board(the “PCAOB”) was established by the Sarbanes-OxleyAct of 2002 (the “Act”) to oversee the auditors of pub-lic companies in order to protect the interests ofinvestors and further the public interest in the prepara-tion of informative, fair, and independent auditreports. The Act established the PCAOB as a private,nonprofit corporation.

The U.S. Securities and Exchange Commission(the “SEC”) has oversight authority over the PCAOB.Among other things, the SEC has the capacity toappoint or remove, for cause, members of the PCAOB’sBoard, approve the PCAOB’s budget and rules, andreview appeals of aspects of adverse PCAOB inspectionreports and disciplinary actions. In its oversight role, theSEC determined on April 25, 2003, that the PCAOBhad the capacity to discharge its responsibilities andenforce compliance with the Act. The PCAOB’s initialyear of activity primarily focused on the recruitment ofqualified professionals, registration of public accountingfirms, initial limited inspections of the four largest pub-lic accounting firms, the establishment of standards forthe auditing profession, and the development of infra-structure to support its ongoing activities. The accompa-nying financial statements present the activities fromJanuary 1, 2003.

NOTE 2. SUMMARY OF SIGNIFICANTACCOUNTING POLICIESPresentation. The financial statements have been pre-pared in accordance with U.S. generally acceptedaccounting principles and are presented pursuant toStatement of Financial Accounting Standards No. 117,Financial Statements of Not-for-Profit Organizations(“SFAS No. 117”). Under SFAS No. 117, the PCAOBis required to report information regarding its finan-cial position and activities according to three classes

of net assets: unrestricted net assets, temporarilyrestricted net assets, and permanently restricted netassets. The net assets of the PCAOB are not subject to restrictions and therefore all have been classified as unrestricted in the accompanying statements. ThePCAOB’s unrestricted net assets primarily consist ofits investments in technology and amounts to fundoperations in the subsequent year prior to collection of that year’s funding. Inspections and enforcement,registration, and standard setting are the programactivities for the PCAOB. Costs associated with these program activities include salaries, benefits, and other direct operating expenses relating to theabove activities. Indirect costs, such as occupancy, are not allocated to program activities, but areincluded in management and administration under supporting activities.

Program Activities of the PCAOB• Inspections and Enforcement. The PCAOB con-

ducts a continuing program of inspections of registered public accounting firms to assess theircompliance with the Act, the rules of the PCAOBand the rules of the SEC and professional standards,in connection with the firms’ performance of audits,issuance of audit reports, and related matters involv-ing issuers, as defined in the Act. The Act grants thePCAOB broad investigative and disciplinary author-ity over registered public accounting firms and per-sons associated with such firms.

• Registration. In accordance with the Act, the PCAOBreviews registration applications and annual reportsfor public accounting firms that choose to registerwith the PCAOB. Under the Act and PCAOB rules,an accounting firm that is not registered with thePCAOB may not prepare or issue, or play a substan-tial role in the preparation or issuance of, any auditreport with respect to any issuer.

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 21

PAGE 22 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

• Standard Setting.The PCAOB establishes auditing,related attestation, quality control, independence,and ethics standards to be used by registered publicaccounting firms in the preparation and issuance ofaudit reports.

Use of Estimates. The preparation of financial state-ments in accordance with U.S generally accepted account-ing principles requires management to make estimatesand assumptions that may affect the reported amounts ofassets, liabilities, revenues, and expenses, and the disclo-sure of contingent assets and liabilities. Accordingly, actualresults could differ from these estimates.

Fees from Issuers. Fees from issuers, which arereferred to as Accounting Support Fees in the Act, areamounts invoiced to certain issuers whose shares arepublicly traded and to certain investment companiesto fund the operating budget of the PCAOB for thatyear. Such fees are recognized as revenue in the budgetyear to which they relate. The amount of fees invoicedto individual entities is determined as prescribed inthe Act and the Rules of the PCAOB. The PCAOBreports all fees from issuers as an increase in unre-stricted net assets.

Fees from Registering Accounting Firms. Fees fromregistering accounting firms are amounts collected fromeach public accounting firm that applies for registrationwith the PCAOB to recover the costs of processing andreviewing registration applications. The PCAOB reportsall fees from registering accounting firms as an increasein unrestricted net assets and are recognized as revenuein the budget year to which they relate.

Cash Held for Others under Agency Agreement. Onbehalf of the Financial Accounting Standards Board(the “FASB”), the Financial Accounting Foundation (the“FAF”) designated the PCAOB as the collection agent

for invoicing and collection of the 2003 FASB account-ing support fees. The PCAOB earned and was paid$209,400 from FAF for acting as the collection agent in2003, which is included in interest income and other inthe accompanying statement of activities. Otherwise, thePCAOB recognizes no revenue or expense related to thisrelationship and maintains a separate bank account forall fees collected on behalf of the FASB. As of December31, 2003, the PCAOB had $304,131 included in cashand cash equivalents related to the FASB. A correspon-ding $304,131 was included in accounts payable andother liabilities for amounts due to the FASB.

Cash and Cash Equivalents. The term cash and cashequivalents, as used in the accompanying financialstatements, includes currency on hand, demanddeposits with financial institutions, and short-term,highly liquid investments purchased with a maturity ofthree months or less. At times, the PCAOB’s demanddeposits with financial institutions exceed federallyinsured limits. However, the PCAOB has not experi-enced any losses in such accounts, and managementbelieves the PCAOB is not exposed to any significantcredit risk on these accounts.

Depreciation and Amortization. Furniture andequipment, leasehold improvements, and technologyare stated at cost, less accumulated depreciation andamortization computed under the straight-line methodover their useful lives. Furniture and equipment andtechnology are depreciated over their estimated usefullives of 3 to 5 years. Leasehold improvements are amor-tized over the shorter of their estimated useful lives orthe remaining term of the current office leases.

Income Taxes. The PCAOB is exempt from incometaxes under Section 501(c)(3) of the Internal RevenueCode. Therefore the accompanying financial statementsinclude no provision for income taxes.

Notes to the Financial Statements (continued)Public Company Accounting Oversight Board

Year Ended December 31, 2003

NOTE 3. FURNITURE AND EQUIPMENT,LEASEHOLD IMPROVEMENTS, ANDTECHNOLOGYThese assets consist of the following at December 31, 2003:

Furniture and equipment $ 2,570,573Leasehold improvements 2,598,037Technology 13,930,475Total 19,099,085Accumulated depreciation and amortization (2,668,207)

$16,430,878

NOTE 4. LEASE COMMITMENTSIn 2003, the PCAOB occupied office space inWashington, DC, New York City, and Sterling,Virginia, on leases that expire from 2006 to 2013. Theleases include provisions for scheduled rent increasesover the respective terms.

Rent is being charged to expense using the straight-line method over the respective lease terms. Rent underthis method was $2,342,617 in 2003. Deferred rentexpense amounted to approximately $3,028,134 as ofDecember 31, 2003. Deferred rent is being amortizedover the remaining lives of the operating leases.

Minimum rental commitments under the operatingleases for the office space as of December 31 are as follows:

Year ending December 31,2004 $ 2,769,0232005 2,812,3852006 2,756,4642007 2,300,8212008 2,346,838Thereafter 11,364,699

$24,350,230

NOTE 5. RETIREMENT BENEFIT PLANThe PCAOB has a defined contribution retirementplan which covers active employees. The PCAOBmatches contributions in an amount equal to 100%up to 6% of the eligible compensation. The PCAOB’scontributions become fully vested immediately. ThePCAOB’s contributions to the employees’ accountswere $412,152 for 2003.

NOTE 6. 2003 ADVANCES FROM THEDEPARTMENT OF THE TREASURYIn accordance with the Act, the PCAOB was advancedfunds to cover its start-up expenses from The Departmentof the Treasury totaling $20,342,000 during 2003. Theseadvances were repaid on September 22, 2003.

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD PAGE 23

Notes to the Financial Statements (continued)Public Company Accounting Oversight Board

Year Ended December 31, 2003

PAGE 24 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

To the Board of the Public Company Accounting Oversight BoardWashington, DC

We have audited the accompanying statement of financial position of the Public Company AccountingOversight Board (the PCAOB) as of December 31, 2003, and the related statements of activities and cashflows for the year then ended. These financial statements are the responsibility of the PCAOB’s manage-ment. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with U.S. generally accepted auditing standards. Those standardsrequire that we plan and perform the audit to obtain reasonable assurance about whether the financial state-ments are free of material misstatement. An audit includes examining, on a test basis, evidence supportingthe amounts and disclosures in the financial statements. An audit also includes assessing the accountingprinciples used and significant estimates made by management, as well as evaluating the overall financialstatement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, thefinancial position of the Public Company Accounting Oversight Board as of December 31, 2003, and thechanges in its net assets and its cash flows for the year then ended in conformity with U.S. generallyaccepted accounting principles.

Washington, DCMarch 18, 2004

Independent Auditors’ ReportPublic Company Accounting Oversight Board

Chief of StaffSamantha E. Ross

Counsel and Advisors to the BoardRon BosterPhoebe W. BrownJoanne O'Rourke HindmanDonald R. MarlaisMary M. SjoquistMarilyn H. Weimer

Office of the Chief AuditorDouglas R. Carmichael, Chief AuditorThomas Ray, Deputy Chief Auditor

Division of Enforcement and InvestigationsClaudius Modesti, Director

Office of Internal Oversight and Performance AssurancePeter Schleck, DirectorFred Doggett, Deputy Director

Office of Public AffairsChristi Harlan, Director

Office of Government RelationsMary Moore Hamrick, DirectorHelene Rayder, Deputy Director

Office of General CounselLewis H. Ferguson III, General CounselJ. Gordon Seymour, Deputy General Counsel

International AffairsTravis Gilmer, Special AdvisorRhonda Schnare, Special Counsel

Division of Registration and InspectionsGeorge Diacont, DirectorChris D. Mandaleris, Deputy Director—InspectionPatricia Thompson, Deputy Director—RegistrationPhil Wedemeyer, Deputy Director—Inspection

Office of OperationsPaul Schneider, Chief Administrative OfficerThomas C. Hohman, Chief Financial OfficerSara Simko Bridwell, Human Resources DirectorAlbert R. (Ray) Schmidt, Chief Information Officer

© 2

004

Pub

lic C

omp

any

Acc

ount

ing

Ove

rsig

ht B

oard

Des

ign:

Fin

anci

al C

omm

unic

atio

ns In

c.B

ethe

sda,

MD

ww

w.fc

icre

ativ

e.co

m

New York Office1251 Avenue of the Americas35th FloorNew York, NY 10020

Atlanta Office3455 Peachtree RoadSuite 500Atlanta, GA 30326

Dallas Office5215 N. O’Connor Blvd.Suite 1860Irving, TX 75039

San Francisco Office1001 Bayhill Drive2nd FloorSan Bruno, CA 94066

Washington Office 1666 K Street, NW Washington, DC 20006-2803 Phone: (202) 207-9100 www.pcaobus.org

PAGE 26 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

Washington Office 1666 K Street, NW Washington, DC 20006-2803 Phone: (202) 207-9100 www.pcaobus.org